Abstract

This study aims to present Paweł Ciompa’s (1867–1913) econometric theory of bookkeeping, associated with the banking sector and vocational education in Galicia, a territory seized by Austria as a result of the partition of Poland. Ciompa presented his theory of bookkeeping in Polish in the work Zarys ekonometryi i teorya buchalterii [An outline of econometrics and the theory of bookkeeping] and in German in Grundrisse einer Oeconometrie und die auf Nationalökonomie aufgebaute Natürliche Theorie der Buchhaltung [An outline of econometrics and the development of a natural theory of bookkeeping based on economics]. Both were published in Lviv in 1910. The concept presented in these works constitutes an original econometric and geometric approach to the description of economic phenomena. It has a didactic value despite the fact that it has not found many followers, and accounting historians find it difficult to place it unambiguously in the research trends of the turn of the nineteenth and twentieth centuries.

Introduction

The purpose of this study is to discuss the significance of the work of Paweł Ciompa (1867–1913), a banker, teacher and social activist living at the turn of the nineteenth and twentieth centuries, and in particular his econometric theory of bookkeeping. Ciompa lived in Poland which at the time did not exist on the political maps of Europe because of three partitions (the first in 1772, the second in 1793, and the third in 1795); which had divided Polish territory between Russia, Prussia and Austria. It was only after World War I, in which these three powers fought against each other, that Poland regained independence after 123 years, in November 1918. During the partitions, Poland attempted to regain independence in unsuccessful national uprisings: the November Uprising in 1830, and the January Uprising in 1863. After the defeat of the January Uprising the age of positivism began in literature and in social and economic activity of organic work protecting the nation against complete denationalization by the partitioners.

Ciompa lived in the territory of the Austrian partition, so called Galicia, which was a common name for the Austrian crown land of the Kingdom of Galicia and Lodomeria formed after the First Partition in 1772 and abolished at the end of World War I in 1918. It encompassed southern Lesser Poland, eastern Roztocze, eastern Podkarpacie and the Podolian Uplands (for more details see Davies, 2010: 418–463).

The development of science and vocational education took place during the partitions of Poland under strict control of the invaders, and every textbook published in Polish required the approval of the Censor. For this reason, the overall number of textbooks on accounting by Polish authors is not very high. 1 In the bibliography covering the four centuries from the sixteenth to the nineteenth, one can point to only 112 textbooks on merchant, industrial and agricultural accounting by 65 Polish authors and authors writing in Polish. In the nineteenth century alone, there were 68 publications (Szychta, 1989, 1995, 2020: 316). The first Polish textbook which may be regarded as an attempt to scientifically approach double-entry bookkeeping was written by Stanisław Budny in 1826 in Vilnius, which was under the Russian partition. The book was only 65 pages long and entitled Buchalteria ułatwiona, czyli sposób utrzymywania ksiąg kupieckich pojedynczego i podwójnego rachunku podług metody Edmunda Degrange [Easy bookkeeping, that is, the method of keeping single and double account books according to Edmund Degrange’s method]. In this publication, Budny (1826: 8, 43–44) explained the functioning of bookkeeping accounts according to the principle of personification, and before drawing up the balance sheet he proposed to prepare a statement of turnover and balances, which he referred to as a facilitated balance sheet – hence the term “easy bookkeeping” in the title of his booklet (see also Sojak and Kowalska, 2014).

Between 1833 and 1835 Antoni Barciński published a three-volume handbook under the title O rachunkowości kupieckiej [On merchant accounting], devoted entirely to double-entry bookkeeping. While Budny's textbook was most probably the translation of a French book, Barciński’s was entirely his own. The first volume (1833) dealt with commercial arithmetic, the second (1834) with commercial and bank accounting, and the third (1835) with factory and farm accounting. 2

An analysis of cost accounting textbooks, mainly from the second half of the nineteenth century, that is, from the period of the aforementioned organic work, was conducted by Chojnacka (1969) and Szychta (2014, 2020). Most of these publications are handbooks also discussing the theoretical foundations of cost measurement and double-entry bookkeeping. They include, among others: Szumlański (1865), Nowicki (1876), Pietrzycki (1886), Danilewicz (1887) and Krakowski (1887).

Ciompa’s theory is known only to a narrow circle of accounting historians in Poland, whereas it is almost unknown to the international community of scholars. This article thus aims to present this theory and its reception as well as juxtapose it with well-known bookkeeping theories.

The article contains a short professional biography of Paweł Ciompa and the specification of his publishing output, which includes only a dozen or so textbooks mainly prepared for students at economic vocational schools. The main part of the article is devoted to the presentation of the theoretical concept of accounting proposed by Ciompa. This part explains the basic concepts used by the author, the econometric and geometric concept of value, the relationship between property and capital, the econometric quadrigon, which Ciompa used to explain all economic events, and the principles of functioning of bookkeeping accounts. He presented it in two publications: in Polish (Ciompa, 1910b) and in German (Ciompa, 1910a), both of which will be referred to in the text. This is followed by an attempt to classify Ciompa’s theory within the research trends in bookkeeping theory of the day and its reception by other authors. The paper concludes by explaining to whom the authorship of the new word ‘econometrics’ is due – Ciompa, who first used it in 1910, or Frisch, who used it in 1926.

Biography of Paweł Ciompa

Paweł Ciompa was born on 2 January 1867 in Toszonovice Górne (now the Czech Republic) near Těšín. He died at the age of 46 on 18 June 1913 in Lviv. It is known that he attended a real school (from German: Realshule) in Cieszyn and that he graduated from the Trade Academy in Vienna. However, it has not been established when, how long and what he studied at the Trade Academy in Vienna. The existing biographies of Ciompa do not provide any details on the subject, simply stating that he was an economist, lawyer and banker (Encyclopedia of Krakow, 2000: 115; Brzezin and Knop, 2007: 29). Only Józef Golec and Stefania Bojda in Biographical Dictionary of the Cieszyn Land (1995: 39) and Zenon Jasiński and Bogdan Cimała in Lexicon of Poles in the Czech and Slovak Republics (2015: 54–55) point to his legal education. This is also confirmed by Władysław Sosna (2013: 12) who, when recalling Ciompa on the 100th anniversary of his death, refers to him as a ‘counsellor’ and a banking lawyer. It is certain, however, that in 1892 he began working as a bank clerk. This fact is recorded in the annual register of Galician officials, the so-called Szematyzm Królestwa Galicyi i Lodomeryi z Wielkiem Księstwem Krakowskiem [The Schedule of the Kingdom of Galicia and Lodomeria with the Grand Duchy of Krakow] for the year 1892, on page 573. 3

For his entire life Ciompa was professionally active in the banking sector of Galicia (he started his work in Krakow and ended it in Lviv). From 1892 to 1900, he worked as an ordinary clerk, and from 1901 to 1907 as an auditor of the Krakow branch of the Austro-Hungarian Bank. From 1899 to 1906 he worked as a teacher for the Commercial Course at the four-class female St Scholastica School. At the same time, in the years 1900–1906, he taught commercial calculus and bookkeeping at the Higher School of Commerce in Krakow. 4

In the years 1906–1907 he was the Secretary, and from 1908 to 1911 a member of the Supervisory Board of the Folk School Society in Krakow (Encyclopedia of Krakow, 2000: 115; Brzezin and Knop, 2007: 31). From 1908 until his death, he was also a member of the board of the Commercial School Society in Lviv. In 1908, he began working at the National Bank of the Kingdom of Galicia and Lodomeria with the Grand Duchy of Krakow, 5 first as an adjunct, 6 and in 1911–1913 as Director of the Accountancy Department and Proxy. In 1910, he was appointed to the post of deputy auditor (member of the auditing commission) in the newly established Industrial Bank for the Kingdom of Galicia and Lodomeria within the Grand Duchy of Krakow in Lviv. It should be noted that Ciompa usually indicated the functions he held on the title pages of his books. Thus, in the books published between 1903 and 1906 Ciompa appears as an auditor of the Krakow branch of the Austro-Hungarian Bank, teacher at the Commercial Academy in Krakow, and in the period from 1909 to 1913 as the Director of Accounts of the National Bank. Between 1907 and 1908, Ciompa did not publish. As a social activist, he gave legal and commercial advice in Evangelical churches in Krakow and Lviv. He was also an ordinary member of the “Macierz Szkolna dla Księstwa Cieszyńskiego” Society.

Ciompa was therefore primarily a practitioner and only then a schoolteacher and activist 7 As Ciompa was not a university employee (there was the Jagiellonian University in Krakow, founded in 1364, and the Jan Kazimierz University in Lviv, founded in 1661), he did not obtain academic titles and his publications, at first in the form of handbooks, were mainly the result of his concern for vocational education. 8

Bibliography of Paweł Ciompa

Ciompa’s writing includes the following publications listed chronologically in Table 1.

A chronological list of Ciompa's works.

I have retained the original spelling and content given on the title pages of studies deviating from the currently used bibliographic description.

Source: Bibliografia Polska 1901–1939, ed. by Janina Wilgat (1998), vol. 4, editors of the volume: Bożena Dobrzyńska, Irena Olszewska, Biblioteka Narodowa, Warszawa 1998, pp. 490–491.

Between 1772 and 1867 German was the official language in Galicia, and in the second half of the nineteenth century, when Poland gradually regained autonomy, Polish was introduced into schools and offices, but German was still the language of commerce. Hence, Ciompa wrote in both German and Polish. The first six publications in this list are of a guidebook nature and stem from Ciompa’s socially-oriented stance. Alongside his assistance in the aforementioned court cases, they are part of the “organic work” typical of the age of positivism. 9 The next four are scholarly works.

Paweł Ciompa's econometric theory of bookkeeping

The year 1910 was an important date in Polish accounting history. 10 This is when three of Ciompa’s most important works were published. First, the article Majątek i kapitał w buchalteryi [Assets and capital in bookkeeping], in the XIX Rocznik Asekuracyjno-Ekonomiczny for 1910 [XIX Yearbook of Safety and Economics for 1910]. 11 Afterwards, the same article was reprinted by the publishers of the Commercial School Society in Lviv with the added title Zarys ekonometryi i teorya buchalteryi [Outline of econometrics and bookkeeping theory] (Ciompa 1910b: 47). 12 Finally, also in Lviv, Grundrisse einer Oeconometrie und die auf Nationalökonomie aufgebaute natürliche Theorie der Buchhaltung (…) 13 was published. The book has 200 pages of main text numbered in Arabic numerals, and 16 pages of introduction and table of contents numbered in Roman numerals. The main text comprises three parts. Part I is entitled Oekonometrische primäre Gleichungen und oekonometrische Verhältnisse [Econometric primal equations and econometric relations] (pp. 1–71), Part II − Oekonometrische sekundäre und tertiäre Gleichungen [Econometric dual and tertial equations] (pp. 72–133) and Part III − Bewertung des Kapitalvermögens in der Bilanz [Valuation of assets and capital in the balance sheet] (pp. 134–200). It is worth noting that the book is cited in publications on the history of accounting of the German- and English-speaking area (Dean and Clarke, 1989: 3; Mattessich and Küpper, 2003: 106–137; Mattessich 2008: 42, 45). 14

The fundamental issues in all theoretical concepts of accounting are primarily concerned with the measurement of economic values, the relationship between assets and capital, the functioning of bookkeeping accounts and the double entry principle. These were also the issues that Ciompa grappled with in developing his theory.

The relationship between wealth and capital in bookkeeping can be explained by econometrics, which according to Ciompa was a new science. Ciompa explains the title of his work and the relationship between accounting and econometrics as follows (Ciompa, 1910b: 8): In theory, economics seeks to explain all phenomena of value, while in practice, mathematics and bookkeeping account for the values of goods. Bookkeeping thus stands in a very close relationship to economics. The theory of bookkeeping must be based on economics, and the rules of bookkeeping must be justified by economics. Just as physics represents mechanical, acoustic, dynamic, etc. phenomena, so too should economic phenomena be represented by the science we call econometrics. Econometrics is based on economics, mathematics and geometry, and is part of economics, just as trigonometry is part of geometry. Bookkeeping is then only an application of econometrics, just as mathematics applies the laws of algebra.

15

According to Ciompa, econometrics is intended to help accounting measure, describe and report changes in economic values. Ciompa does not create new economic concepts and does not seek ways to solve economic problems (Israel, 2016: 3; Lulek, 1922: 43).

Econometric and geometric value of a good

Ciompa begins the presentation of his theory by explaining the concept of a good and its value. Goods serve people to satisfy their needs, they can be tangible and intangible (services) and are exchangeable. There are also free goods (objects that have no exchange value and are not subject to exchange, for example, air, water) (Ciompa, 1910a: 1–2, 1910b: 5). Accordingly, accounting deals only with those economic goods that are subject to market exchange. Every good (excluding free goods) must have a value, and a distinction can be made between a use value and an exchange value. Both values can be viewed as subjective and objective. The first view is subjective, the second is objective. Thus, the price is an objective convertible value expressed in money, shaped by the subjective values of the seller and the buyer during negotiations (see Table 2).

Value of goods.

Source: Own elaboration based on Ciompa (1910b: 6–7).

Thus, according to Ciompa the value of a good is not bound to it in a permanent way, but depends on the current needs, individual inclinations, and the economic and social situation of an individual. Therefore, it is subject to constant change, and the only way to reliably obtain information about the value of a good is through exchange. A completed transaction reveals the objective value of a good. Thus, a price signifies the value of one good (commodity) by means of the value of another good, which is money. Money, like other goods, does not have a fixed value (purchasing power), but Ciompa does not deal with the causes of changes in the value of money – this is the domain of economics, not accounting (Ciompa, 1910b: 12). This is obviously not Ciompa’s original conception, and although in presenting the above concepts in the Polish version of Theory… (Ciompa 1910b) Ciompa does not point to the literature, and in the German version (Ciompa, 1910a) he mainly cites accounting literature [that is, Richard Reisch and Klemens J. Kreibig (1907), Robert Stern (1902) and Herman V. Simon (1899)], it is likely that these concepts were also familiar to him from Carl Menger's Principles of Economics published in 1871 16 (similar views are expressed by Israel 2016: 5), 17 or from Charles Gide's Principes d'économie politique [Principles of Political Economy] of 1883, translated into Polish in 1893 (Gide, 1983: 42–91, 124–139).

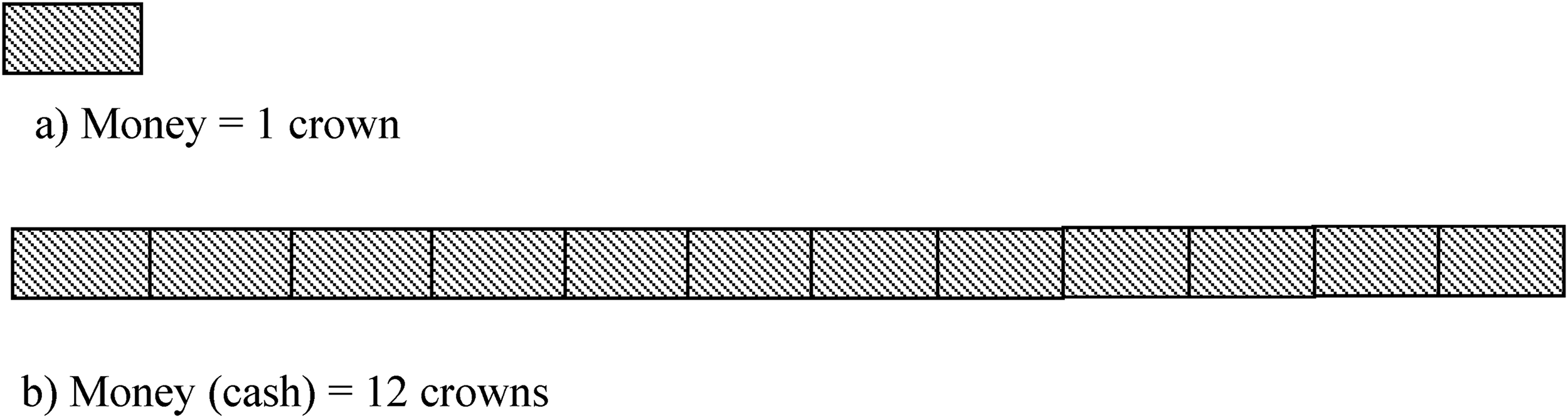

Econometrically, the value of a good is the product of the quantity of the good and its unit price. Geometrically, this product is the area of a rectangle, one side of which has a length equal to the quantity of the good and the other to the unit price of the good (Ciompa, 1910b:10). Ciompa calls this rectangle the field (plane) of the value of the commodity. The fields of the rectangles of two different commodities can be the same but their sides may be different, which is explained by Ciompa graphically in Figure 1. The value of the commodities is thus the same (12 crowns 18 ), but graphically (geometrically) it is not, because it is shaped by the different sides of the rectangle, that is, by the quantity and unit price of the commodity, which he calls the factors of the commodity value field (Ciompa, 1910b: 13–14). The difference between these values will only become apparent when we do not buy one of them because of the high price, in which case the use-value of the good is less than the replacement value for us and for this reason we refrain from buying. In fact, the use-value of money (which we have) is higher for us than the use-value of the commodity we want to buy (Ciompa, 1910b: 9).

Value and factors of the commodity value field.

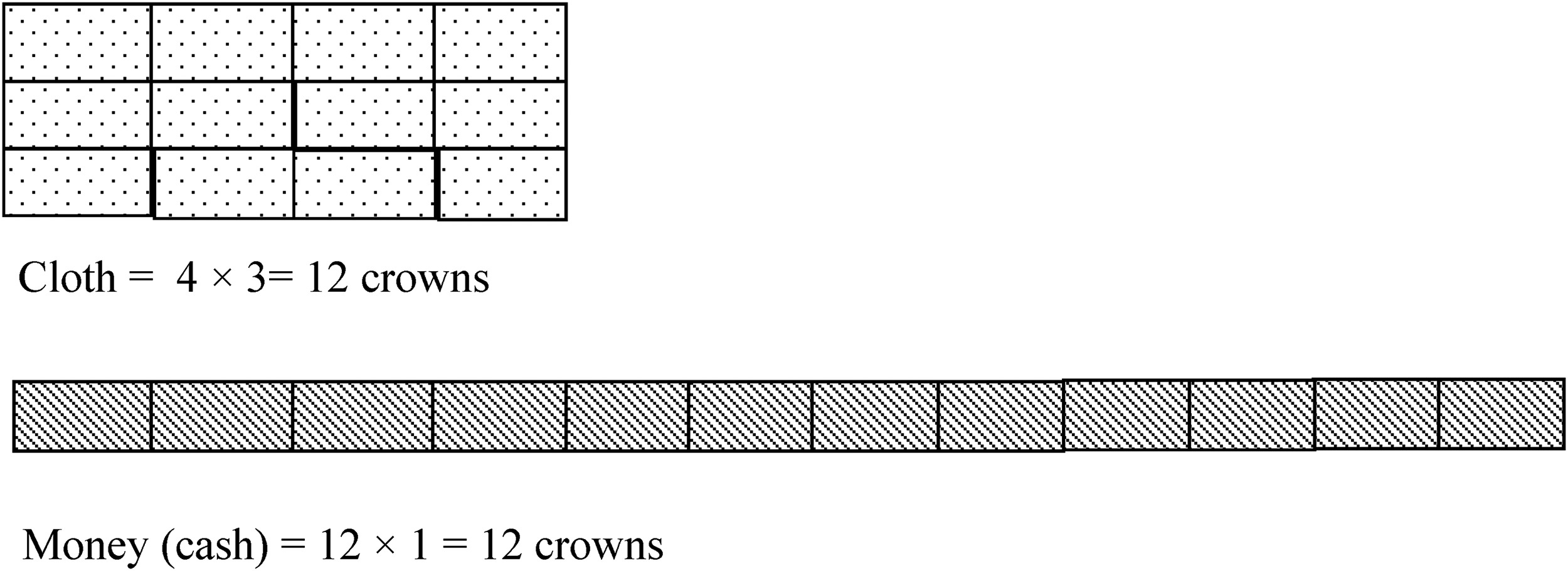

The value of a monetary unit in econometrics is also represented by the plane of a rectangle (Figure 2a). With this presentation of one crown, the value of 12 crowns in the plane will consist of 12 monetary units (Figure 2b).

Value of a monetary unit (a) and 12 crowns (b).

If we exchange our own good (money) for another (e.g. cloth), we are dealing with a purchase, while if we exchange the cloth for money, we are dealing with a sale. As a result of this transaction the two planes of value (cloth and money – see Figure 3) are equalized.

Sale and purchase transaction.

Relationship between assets and capital

The basis of every enterprise is property, which must be productive and whose representative is capital. Capital is the result of labour and productive property. There can be assets without ‘capital power’, but it is impossible to imagine capital without assets. Thus, sugar in the shop represents capital, but bought by the customer it ‘loses the power of capital’ because it has lost its purpose, which was the ability to sell (in the shop). For the customer, sugar has not lost this ability to sell, although it was bought for a different purpose. Sugar in the shop and bought by the customer is therefore an asset. Capital owes its existence only to its productive property and is the cause of the creation of new goods (Ciompa, 1910b:13).

Productive wealth is thus, as Ciompa notes, the cause, or action of capital, which in turn is the effect, or reaction of wealth. These relations cannot be represented by an algebraic equation:

The econometric equation.

Assets are something real, that is. positive ( + ), while capital is only its creative force (‘econometric activity of assets’), that is, something negative (−). Investing cash into an enterprise one would say: ‘10000 crowns in cash is represented in the enterprise’s capital by 10000 crowns’ (Ciompa, 1910a: 12, 1910b: 14), which would be written down as follows:

Given the positive value of assets and the negative value of capital, the econometric equation will have positive quantities on the left and negative quantities on the right.

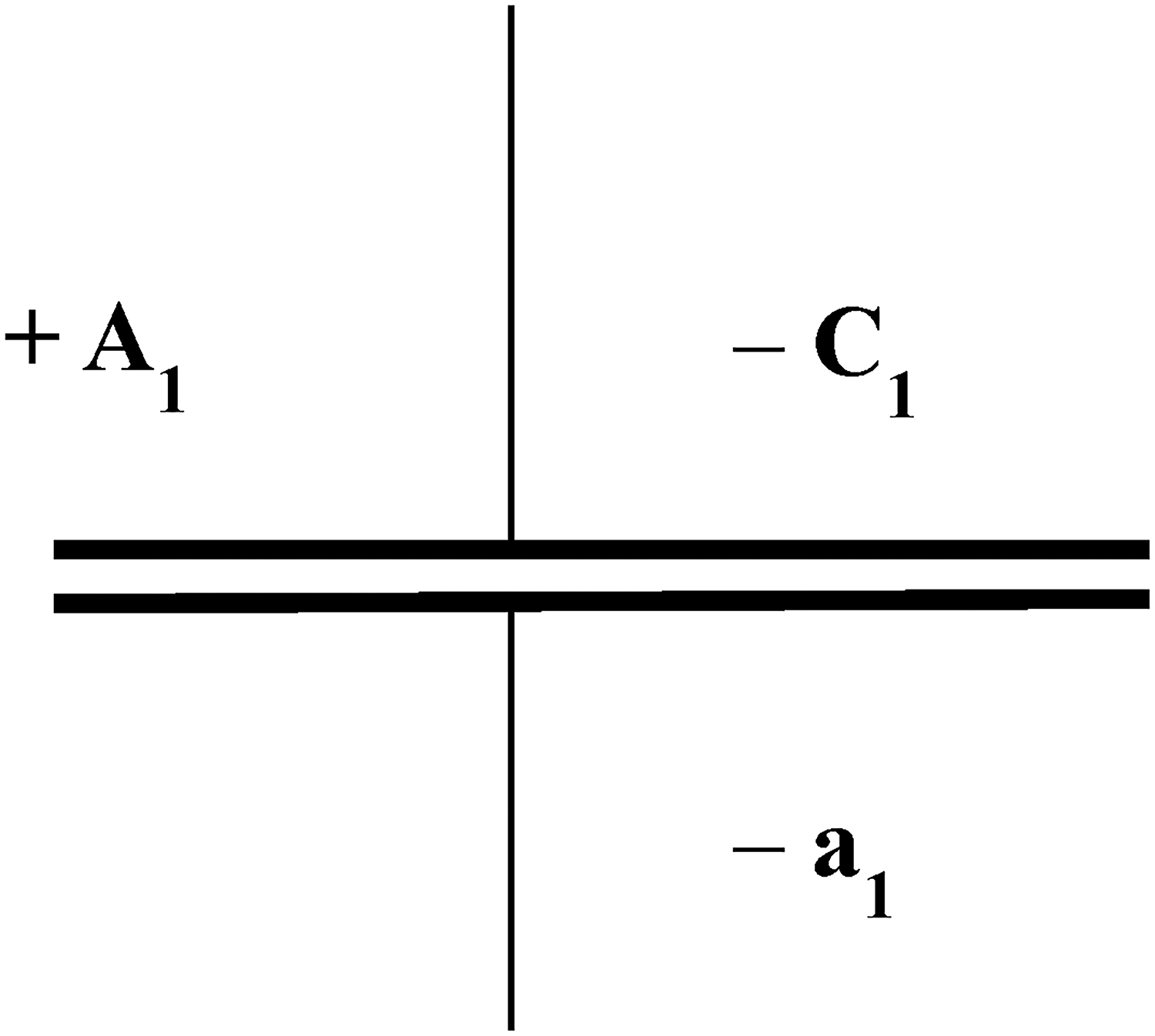

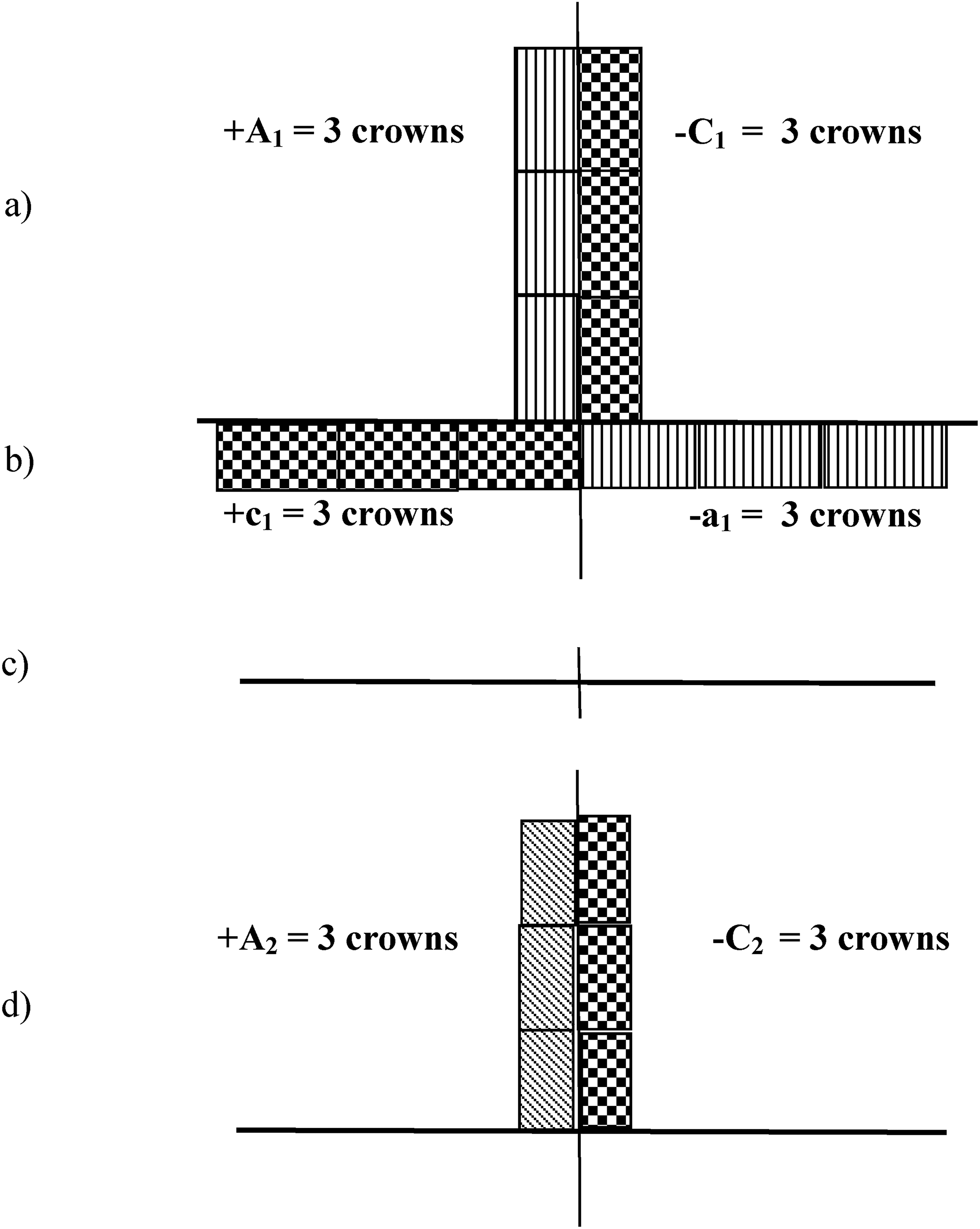

A good (A1) that has lost its productive power (−a1) reduces its value to A2 (or A1 − a1). For this reason, the loss of wealth must be placed on the right-hand side of the vertical line of the econometric equation. However, since (A1 − a1) is not an econometric equation because these values are not equal, the size of a1 to distinguish it from capital must be placed in the square below the horizontal line of equality on the right side of the vertical line (Figure 5).

Loss of productive power of assets (balance sheet imbalance).

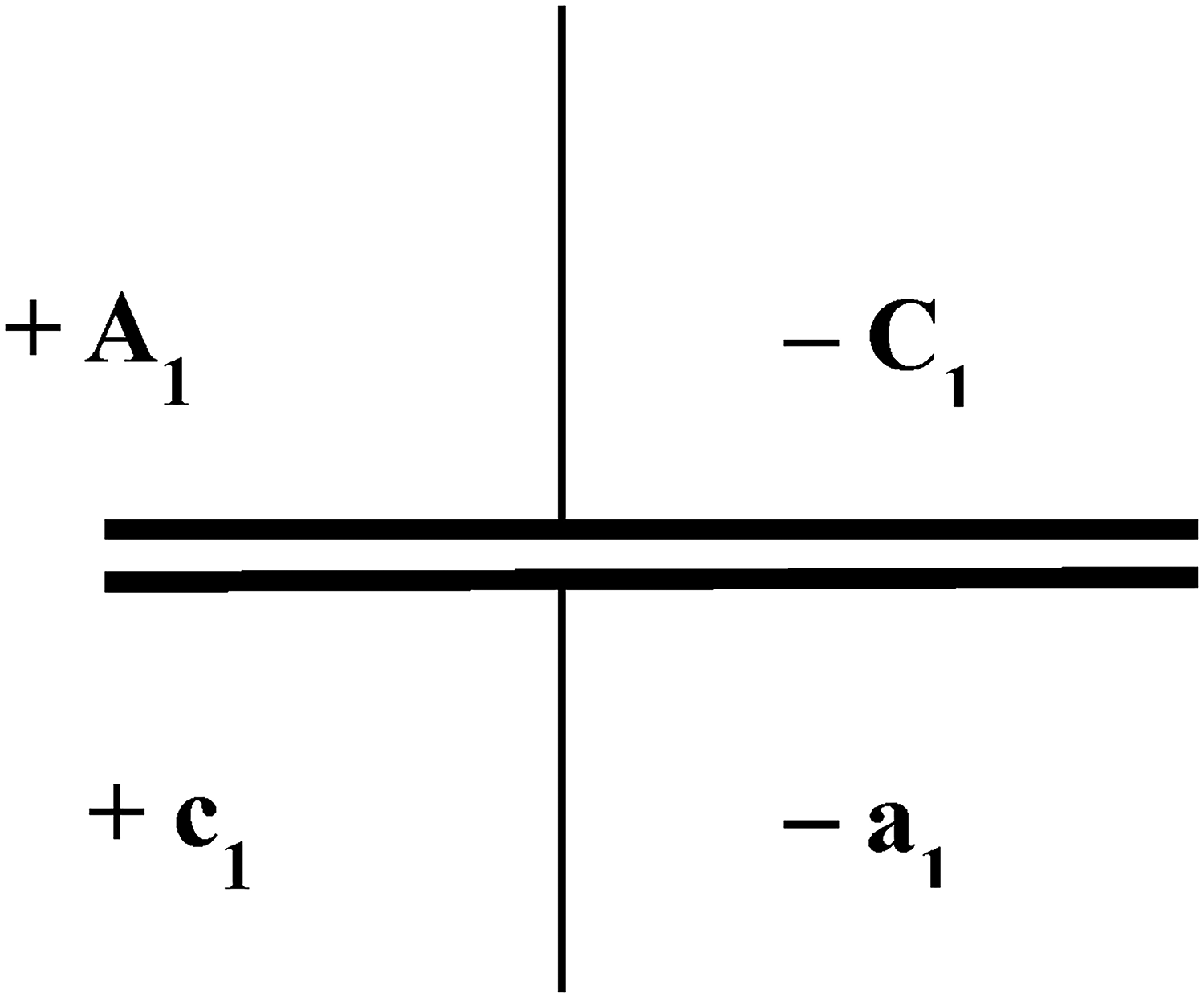

The lost asset power (− a1) ‘no longer has a representative in capital’, and so the reaction to the loss of asset power must be a reduction in capital, for otherwise there would not be an equilibrium in the geometrical figure above. It is obtained by representing the loss of capital ( + c1), to the left of the vertical line and below the horizontal line of the econometric equation (see Figure 6).

Loss of productive power of assets and loss of capital (balance sheet equilibrium).

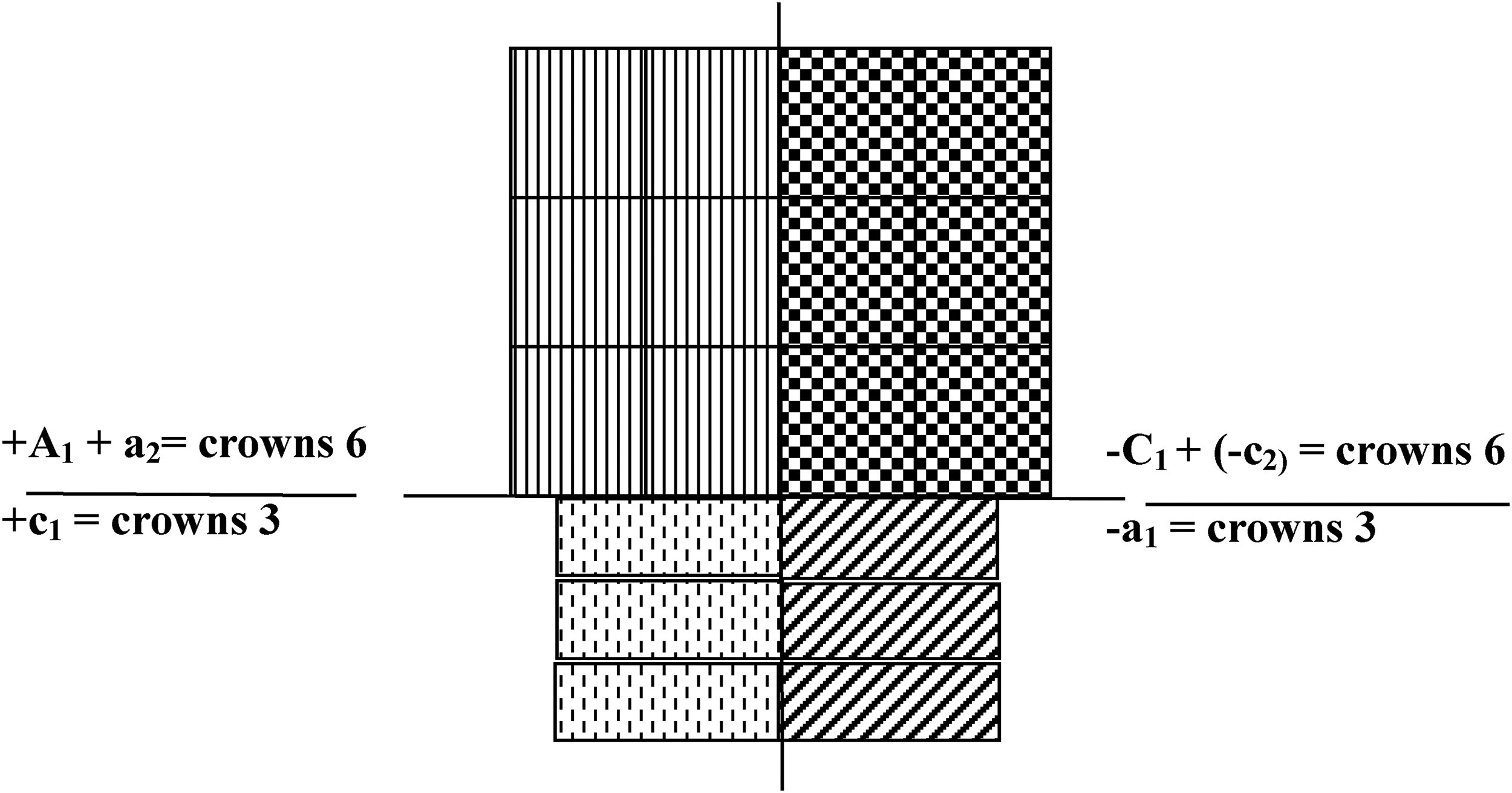

Consequently, there are entries and fields that increase assets and capital above the horizontal line and decrease them below. Using the fields of property and capital values, Ciompa called this equation in a geometric form a quadrigon (see Figure 7). It consists of four elements that form inverse econometric equations, resulting from the double entry used in accounting. The upper left plane records the initial wealth A1 = 6 crowns, the upper right plane balances this wealth with capital -C1 = 6 crowns. This is represented by value fields of equal size, differentiated only by a different shade of the gradient. In the course of economic activity, the part of the initial wealth -a1 = −3 crowns (lower right quadrant plane) and capital c1 = −3 crowns (lower left quadrant plane) is reduced.

Ciompa's geometric quadrigon (I).

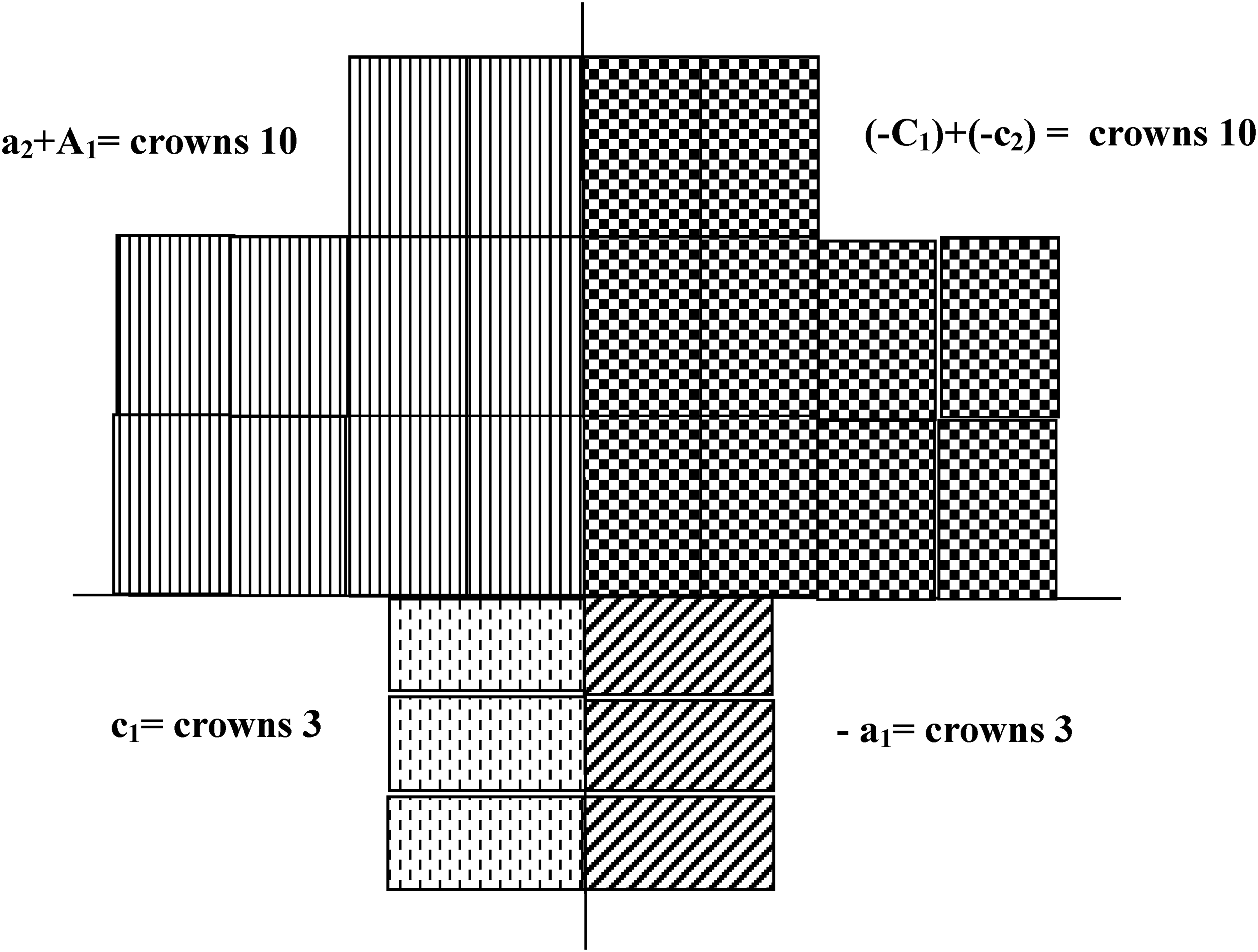

Figure 7 shows the loss of wealth and consequently capital. For a complete picture of the changes in wealth Ciompa also shows its increase by a2 = 4 crowns (new four rectangles in the upper left plane). This simultaneously means an increase in capital of -c2 = 4 crowns (the new four rectangles in the upper right plane (Figure 8).

Ciompa's geometric quadrigon (II).

It is worth noting that the fields of values above the line of equality are set vertically and below horizontally (Ciompa, 1910b: 15). This quadrigon is the basis of all the fundamental rules of bookkeeping (Ciompa, 1910b: 19): asset increase and capital decrease are always recorded on the left-hand side, while capital increase and asset increase are always recorded on the right-hand side of the equation or the econometric equation.

Note that Ciompa ‘runs’ each change in wealth (assets: increase, decrease) through capital. Hence, the sale for cash will consist of four actions:

Sale of goods: a) initial state, b) goods released to the recipient, c) state after sale, d) receipt of cash.

In practice, the third element of this transaction is invisible and only signifies the moment when we no longer have the goods (and capital), and we do not yet have cash (A2) and new capital (-C2). With a deferred sale in the fourth element of the transaction we will have receivables instead of cash (‘hope to receive cash’ – Ciompa, 1910b: 32). In the case of a sale at a profit of one crown the activities (b) and (d) would have four fields in this econometric account, which would mean an increase in wealth and capital. This gain will only be ‘visible’ when the account is closed (balance sheet drawn up). Any gain is therefore a gain in assets and capital. Similarly, we will present a loss, i.e. a situation in which the objective value of goods determined at the time of sale will be lower than its book value, which means there will be a simultaneous decrease in assets and capital. When, on the other hand, the price is equal to the cost of production of the good, it will have a so-called normal value, and wealth and capital will not change (Ciompa, 1910b: 7). An analogous interpretation is the purchase of goods with deferred payment. At the moment the goods are accepted, there is an increase in assets and liabilities arise, which means an increase in capital, except that it is foreign capital. Since our debt to the creditor is an asset, for us debt is capital, and therefore must be shown on the capital side. However, from the point of view of the company, ‘debt is completely the same capital as entrepreneurial capital (equity). Foreign capital only determines the legal relationship to the entrepreneur’ (Ciompa, 1910b: 33). The above examples indicate that Ciompa’s objective is to graphically (econometrically) illustrate and calculate the results (gains, losses) achieved from the assets (and capital). 19

Assets and capital are subject to changes as a result of the so-called economic activities (accounting operations). According to Ciompa, they can be of positive or negative nature. He assigned the digit ( + 1) to positive actions and the digit (−1) to negative ones.

Uniform rules for the operation of accounts

Ciompa believed that bookkeeping accounts of assets and liabilities should function on a uniform basis, that is, the Debit side of accounts serves for entries that should be interpreted as positive ( + ), the Credit side − as negative (−).

20

He consistently divided economic activities into positive and negative ones. He assigned the digit + 1 to positive actions and −1 to negative actions. An increase (gain) of assets or capital is the result of a positive action, while a decrease (loss) of assets or capital is the result of a negative action. Therefore, using the property of multiplication of positive and negative numbers, the following equations can be used: increase in assets ( + 1) × ( + a2) = + a2 (entry on the Debit side)

decrease in assets (−1) × ( + a1) = − a1 (entry on the Credit side)

increase in capital ( + 1) × (−c2) = − c2 (entry on the Credit side)

decrease in capital (−1) × (−c1) = + c1 (entry on the Debit side)

Thus, the positive result of actions and values should be written on the positive side (Debit), as an action, and the negative result of actions and values on the negative side (Credit) as a reaction, which is confirmed by the following examples (Ciompa, 1910a: 21, 1910b: 23): Assets (A):

Beginning balance ( + A) + crowns 10000 (action)

Decrease (−1) × ( + a1) −

= + crowns 6000

(A− a1 + a2) = + crowns 8000

Capital (C):

Beginning balance (−C) − crowns 10000 (reaction)

Decrease (−1) × (−c1)

= − crowns 6000

(−C) − (−c1) + (−c

The signs ‘ + ’ and ‘−’ disappear if the above values are recorded in bookkeeping on the Debit and Credit of a given account because the place of recording itself determines their meaning (Ciompa, 1910a: 21, 1910b: 23−24):

Characters in brackets are omitted in practice. The above also proves that each account is given a name. Generalizing, the entries in an account will be as follows:

A negative interpretation of the entries on the Credit side of the capital account does not raise any objections in the case of foreign capital, which is treated as debt (debt in everyday language is something negative, and therefore negative). It is more difficult to explain equity as a negative quantity. However, it is possible to treat equity as a liability (debt) in an enterprise, a legally separate entity, to its owner.

The entries in the accounts according to the above equations are a consequence of the econometric rules of economic processes (see Table 3).

Econometric rules of economic process.

Source: (Ciompa, 1910a: 20–21; Ciompa, 1910b: 22).

Before closing the accounts and drawing up the balance sheet, it is necessary to carry out a so-called trial balance, that is, to check whether the principle of double entry in accordance with the econometric rules of action and reaction has been observed, which in fact boils down to entry on opposite sides of the bookkeeping accounts. An error in such an entry will show an imbalance of the Debit and Credit sides. A trial balance is not an account but a control of entries on all accounts. It is not a bookkeeping equation, but a purely mathematical operation (Ciompa, 1910b: 20).

Ciompa's theory in the light of bookkeeping theories

Every scholar attempting to explain for didactic purposes their own conception of the theoretical foundations of accounting tries to place it in a particular research context, even if this conception is original or draws on the achievements of other scholars (Szymański, 1984: 71). Although Ciompa does not explicitly indicate this, one may attempt to situate his theory in a larger theoretical framework. Bookkeeping theories known up to the beginning of the twentieth century, that is, up to the moment when Ciompa introduced his ideas, can be divided into two basic groups, namely personalistic (personalized, legal) and materialistic (economic) (Brzezin, 1980; 74–113; Gmytrasiewicz, 1977: 52–78; Mattessich, 2008: 23–30, 43–46; Szymański, 1984, pp. 71–85). The personalistic theory is known in the literature starting with Pacioli’s 1494 treatise on double entry accounting (Pacioli, 2007) and was widely used in textbooks in Europe almost until the end of the nineteenth century. It treats each bookkeeping account as independent ‘persons’ between whom there are legal debtor-creditor relationships. Personalistic bookkeeping theories were divided into one-order and two-order account theories. In the one-order theory Brzezin (1980: 84) states: the characteristic feature of economic events is that two entities are involved, the dual nature of these events being that the entity receiving a certain value is the debtor and the one transferring the value is the creditor. This results in the uniform character of all accounts, since in each account the “receipt” of a given value causes us to treat the account as a debtor (personification), and the account on which we registered the transfer of a given value will be treated as a creditor.

Remnants of the one-order personification theory can be seen in the Polish language in the naming of the sides of accounts: Winien (Debit) and Ma (Credit). These theories were based on the following equation (Mattessich, 2008: 44):

Personalistic theories fulfilled their role especially in didactic processes to explain the principle of double entry, but at the end of the nineteenth century they were displaced by new theories, referred to as materialistic. At the same time, this term did not derive from any empirical-theoretical basis but served mainly to distinguish them from personalistic theories (Mattessich, 2008: 44). Their basis was no longer the ‘subject’ but the object of record, which in the one-order theories was each bookkeeping account.

The interpretation of one order of accounts in both personalistic and materialistic theories is specific in that all asset and liability accounts function equally, that is, the left side records positive values and the right-side records negative values. One-order theories are not suitable for teaching purposes, as it is difficult to explain economic events using them by means of a minimum number of accounts (a recording model). In two-order theories such minimum correspondences are definable.

Materialistic theories with two rows of accounts represented an important advance in accounting in terms of explaining the subject of records. They had many variants, with the owners of such assets – shareholders and creditors – playing an important role in them. The basic balance sheet equation in this approach is as follows:

Gustav Sykora (1949, as cited in Brzezin, 1980: 81) classifies Ciompa’s econometric theory as one of the personalistic account theories, without indicating a more detailed classification. 22 Lulek (1922: 43) also classifies Ciompa’s theory in a similar way, suggesting that it belongs alone to the econometric bookkeeping theories. For this reason, no one has taken over from him the graphical explanation of values (value fields). My experience as a lecturer confirms the usefulness of this concept for explaining the relationship between wealth and capital. In particular, the quadrigon (Figure 8) is suitable for explaining all possible events that increase and decrease wealth and capital. It is true that it is not practical, but the divisibility of the bookkeeping accounts makes it easier to move from the quadrigon to the balance sheet and the determination of income (capital growth). However, Ciompa did not try to convince anyone to apply geometrical figures (fields of value) to the accounts – what mattered here were the numerical equivalents. These figures served him first to explain the differences in the value of property (goods), and only then to explain the changes of property and capital in the quadrigon and, as a consequence, to explain the addition and subtraction in the bookkeeping (balance sheet) equations of intrinsically non-additive quantities (cloth and sugar).

Reception of Paweł Ciompa's theory

Ciompa’s theory did not have many followers. According to Lulek (1922: 73, 92) it was taken over by Eugen Schigut (1912) in his Introduction to Accounting for Lawyers (Einfűhrung in die Buchfűhrung fűr Juristen, and Heirich Nicklisch (1912) in Allgemeine kaufmännische Betriebslehre with the latter called by Lulek ‘a poacher’ because he did not cite the original source (Lulek 1922: 73). His later concept of the two orders of unitary bookkeeping theory is clearly modelled on Ciompa’s concept (Gmytrasiewicz, 1977: 65). The same applies to the theory proposed by J. F. Schär (Brzezin, 1980: 97–109).

Paweł Ciompa’s theory was generally overlooked by Polish scholars in the inter-war period. Neither Witold Byszewski (1912) in his A Brief Overview of the History of Accounting, nor Cezary Łagiewski (1934) in The History of Accounting in Poland, or Marceli Scheffs (1939) in The History of Accounting. 23 It is possible that this was influenced by very critical remarks of Tomasz Lulek, who repeatedly refers to Ciompa’s work. 24 It should be noted that no one else at the time analysed accounting theory from the German-speaking area in such detail, and in this sense his voice was significant. 25

According to Lulek, Ciompa’s views on the connections between merchant accounting and geometry were incomprehensible and unjustified. The objects of accountancy are not abstract geometrical figures (and their dimensions or mutual relations) but concrete things such as money, goods, bills of exchange. His malice towards Ciompa’s theory resounds in the following statement (Lulek, 1922: 43): Apart from the fact that an enterprise may produce or trade lines, triangles, verticals, measuring instruments, etc., and in so doing show them in its accounts, it is impossible to imagine any affinity between accounting and geometry.

From the combination of geometric figures (quadrilaterals) denoting economic concepts such as wealth, capital, value, Ciompa derives ‘a new name for accounting – econometrics’ (Lulek, 1922: 43). According to Lulek, neither econometric equations nor geometric figures (personification pictures) are scientific. For Ciompa, the only task of accounting is to measure economic values with monetary units, while Lulek (1922: 43) believes that accounting should be a science of bookkeeping, its methods and systems.

In balance sheet theory, the interpretation of the right-hand side of the accounting balance sheet causes much trouble. Ciompa’s explanation that it means the origin of capital (both own and foreign) is too vague, since the left side of the balance sheet also contains the ‘capital’ of the enterprise (Lulek, 1922: 84). It has not been sufficiently clarified whether the right side of the balance sheet (passive state) contains real quantities or only ideal, abstract ones.

Ciompa believed that the terms ‘assets’ and ‘capital’ were two different expressions for the same thing. The passive state for own and foreign capital should be interpreted in such a way that the enterprise is indebted for all the capital entrusted to it to those who provided it, although this debt should be interpreted differently from the own capital, which brings us back to the personalistic theory of the account.

Paweł Ciompa and Ragnar Frisch

Finally, it should be noted that Ciompa’s name is associated not only with accounting but also with econometrics. For a long time, many economists mistakenly believed that the author of the term ‘econometrics’ was the Norwegian economist and statistician Ragnar Frisch, the 1969 Nobel Prize winner, who used this name in Frisch (1926) in a French-language article entitled Sur un problème d'économie pure (in the Norsk Matematisk Forenings Skrifter Series 1(16): 1–40). Meanwhile, as the bibliography presented here testifies, the word was first used by Ciompa in 1910, though admittedly in a slightly different sense because it was used only in the context of using algebra and geometric figures for accounting purposes (Knop, 2004: 19). It must also be admitted that Lulek, so critical of Ciompa’s theory, nevertheless claimed Ciompa’s ‘paternity’ for the term econometrics attributed to Frisch. Indeed, he sent a letter to the editors of the journal Economerica on this matter, to which Frisch replied (1936: 95), suggesting that he regarded the term econometrics as the simultaneous use of economic theory, statistics and mathematics, while Ciompa’s term emphasized the descriptive side of econometrics. 26 A digressive mention of Ciompa in the context of the definition of econometrics did not appear until 1981 in Maciej Iłowiecki’s History of Polish Science (1981: 225). This authorship is no longer disputed by scholars today (Bochenek, 2014: 30–31; Maciejewski, 2002: 118; Rutkowski, 1978: 16–18; Wiśniewski, 2009: 7; Wiśniewski, 2016: IX). It is also mentioned in encyclopaedias and lexicons in the West (Jaruga and Szychta, 1996: 466; Jaruga et al., 2008: 265–266).

It is not my purpose to analyse Ragnar Frisch’s concept of econometrics - there is already an extensive literature on this subject. I will only limit myself to the already cited noteworthy article by Karl-Fridrich Israel (2016) comparing two concepts of econometrics by Paweł Ciompa and Ragnar Frisch. In the conclusion of the article, the author observes (Israel, 2016: 29): Ragnar Frisch was convinced that econometrics is in fact a set of tools for solving social and economic problems as it provides the guidelines for economic planning. Having Paweł Ciompa’s vision of econometrics and economographics, as a descriptive economics (…) it should rather be seen as a set of tools for identifying and describing the empirical manifestations of social and economic problems, nothing more and nothing less.

There is no doubt that the long overlooked econometric theory of bookkeeping is Ciompa’s original authorial concept noticed in the academic circles at the beginning of the twenty-first century, that is almost 100 years after its creation. It deserves a place not only in the history of Polish, but also world accounting. Even if Ciompa was, as Lulek (1922: 43) suggests, the only representative of the geometric direction of accounting.

Conclusions

The main purpose of this article was to present the econometric theory of bookkeeping developed 110 years ago in Lviv by Paweł Ciompa, a banker, teacher, social activist, and the first Polish accounting theorist Ciompa wrote, among other publications, bookkeeping handbooks and textbooks for students at economic schools. His most important work is the econometric theory of bookkeeping presented in this article. In this publication, Ciompa attempted to explain the practical aspects of accounting within a theoretical framework, which he called econometrics, although he also used the term economography, which would perhaps be more appropriate in this case. At the heart of his theory is the relationship between the value of assets and capital. In econometric terms, the value of an asset is the product of the quantity of a good and its unit price. In geometric terms, this product is the area of a rectangle. The basis of any enterprise is productive assets, whose creative force (‘econometric asset activity’) is capital. Using the property and value fields of capital, the equilibrium equation was referred to by Ciompa in geometric terms as the quadrigon. This quadrigon is the basis of all basic accounting principles. Ciompa also believed that asset and liability accounts should operate on a uniform basis, that is, the debit side is used for positive entries and the credit side for negative entries. Ciompa’s theory eludes some accounting scholars in terms of its classification. Some classify it as one of personalistic theories, others claim it belongs to materialistic theories, and still others believe a separate class must be reserved for Ciompa, namely, a geometric bookkeeping theory. Ciompa himself would like to be classified as a representative of econometric theory of bookkeeping.

Footnotes

Acknowledgements

I would like to thank the two anonymous reviewers for their insightful comments pointing out the shortcomings of the original version of the article. I have tried to include their comments in the published version. It’s also possible that some of the comments would require clarification in new, separate articles.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.