Abstract

Studies of Britain's accounting history date from the second half of the nineteenth century. Up to 1970 contributions to what became labelled the ‘traditional’ accounting history literature came from authors with diverse backgrounds – for example, archivists, civil servants, economists, (non-accounting) historians, lawyers, librarians, government employees and accounting practitioners. Accounting remained on the periphery of academe, through to the 1960s, thereby explaining the lack of historiographical contributions from accounting faculty. The theoretical underpinning of historical studies was increasingly recognised, post-1970, with investigations explicitly grounded in economics by the so-called neoclassicists. The second half of the 1980s, in Britain, saw a methodological revolution in the study of accounting's past accelerate through a movement christened ‘The new accounting history’. Key venues for the circulation and publication of studies informed by theories taken from numerous other disciplines included the Interdisciplinary Perspectives on Accounting Conference, first held in Manchester in 1985, and support provided by Accounting, Organizations and Society and other high-ranking academic journals for the publication of historical studies into the behavioural, organisational and sociological positioning of accounting. Participation in accounting history research by academics from other sectors of academe has featured prominently in the growth in interdisciplinarity.

Introduction

This paper reveals discernible patterns in British accounting historiography despite the absence of, say, any equivalent to the heavy focus of Italian scholars (certainly until quite recently) on a single topic - double-entry bookkeeping - and the ‘holistic’ economia aziendale as the philosophical and theoretical foundation for the study of accounting and its history (Maran and Leoni 2019: 10). The British traditions and contributions recounted here comprise a range of events, institutional initiatives and publications which have contributed to the elevation of accounting history as a discipline for scholarly pursuit.

It is also acknowledged that this paper cannot aspire to be comprehensive in coverage due to limitations on the space available for individual contributions to this special issue of Accounting History. Its more limited purpose is to describe and explain important events, themes and philosophies which have shaped the study of accounting history in Britain. Most if not all types of research covered by this study are by no stretch of the imagination exclusively British. For example, the ideas of the French philosopher Michel Foucault have inspired the study of accounting's history in many countries, but it is the role of British authors and institutions in bringing the ideas of Foucault, and others, before the accounting community which is focused upon here. Nor is it feasible to identify all the key players, much less the full range of relevant publications as that would occupy most of the pages of this special issue. This, alone, demonstrates how far the study of accounting history has travelled since Robert H. (Bob) Parker published his bibliography of prior historical studies in 1969.

The remainder of the paper is structured as follows. First, key features of British accounting history publications up to 1970 are identified. The section entitled “Critical accounting” recognises the increasing specification, by researchers, of the theoretical basis for their historical studies post-1970; a movement which became more explicit with the onset of critical accounting and the provision of new interdisciplinary perspectives through which to view and interpret accounting's past. “More on accounting and capitalism” then illustrates how the study of accounting history has thereby been transformed using accounting and capitalism as an exemplar. The role of selected institutional initiatives in underpinning accounting history as an academic discipline in Britain is then made explicit and concluding remarks are presented.

Profiling accounting history publications pre-1970

1970 is a landmark year in the history of research into accounting history. The first World Congress of Accounting Historians, initiated by Ernest Stevelinck, was held in Brussels in October of that year. 1970 also witnessed publication of the American Accounting Association's (1970: 53) report of its Committee on Accounting History chaired by Professor Steve Zeff which, among other things, offered a widely cited definition of accounting history. It is possible to gain an insight into the scope and limitations of accounting history research in Britain prior to 1970 by drawing on two sources: the bibliography assembled by Bob Parker (Parker, 1969) and the columns of Accounting Research published between 1948 and 1958. 2

Parker (1969) listed and briefly described English-language publications he had succeeded in tracing up to the time of writing. The earliest identified accounting history resource is Benjamin Foster's The Origin and Progress of Book-keeping (Foster, 1852), described by Napier (2020: 36) as ‘an annotated list of mainly British and American books on accounting published before 1850’. Within his own inventory, Parker's (1969: 89–99) list of publications on ‘Early English and Scottish accounting’ helps to paint a picture of early accounting history research, in Britain, by identifying the topics that received attention and the workspaces which their authors occupied. There are 27 items listed under the sub-heading ‘Manorial, household and parochial accounts’, none of whose authors would be classified as accounting historians, per se. Publications traverse the period 1890–1964 and the following sample provides a fair indication of their authors’ occupations: J.C. Cox (Cox, 1913), cleric and local historian; Noel Denholm-Young (Denholm-Young, 1937), fellow and archivist of Magdalen College, Oxford; John Summers Drew (Drew, 1947), Hampshire local historian; George Herbert Fowler (Fowler, 1940), English zoologist, historian and archivist; Strickland Gibson (Gibson, 1909), librarian, bibliographer and archivist; Peter Heath (Heath, 1964), lecturer in medieval history at Hull University; Elizabeth Lamond (Lamond, 1890), Cambridge history graduate and librarian; and the Liverpool University-based medieval historian, Dorothea Oschinsky (Oschinsky, 1947). 3

Early English and Scottish accounting publications listed in Parker (1969: 92–97) under the sub-heading ‘Mercantile accounts’ are also notable for the absence of accountants, though 10 of the 28 items are the work of the economist and ‘pioneer of historical accounting research’ in Britain, Basil S. Yamey (Napier, 2021: 332). The third and final sub-section entitled ‘Government accounts’ (Parker, 1969: 97–99) contains contributions, mainly from archivists, historians and local and central government employees, for example, the Edinburgh City Archivist, Helen Armet (Armet, 1956), the Newcastle upon Tyne Archivist, Elizabeth M Halcrow (Halcrow, 1956), a civil servant working in the Public Record Office, Hubert Hall (Hall, 1891), a lecturer in diplomatics at Oxford University, Reginald Lane Poole (Poole, 1912) and a reader in medieval history at the University of Exeter, Bertram Wolffe (Wolffe, 1956). Most of the papers in Parker's bibliography fail to state their purpose or their contribution to the study of accounting history and are often entirely descriptive in content.

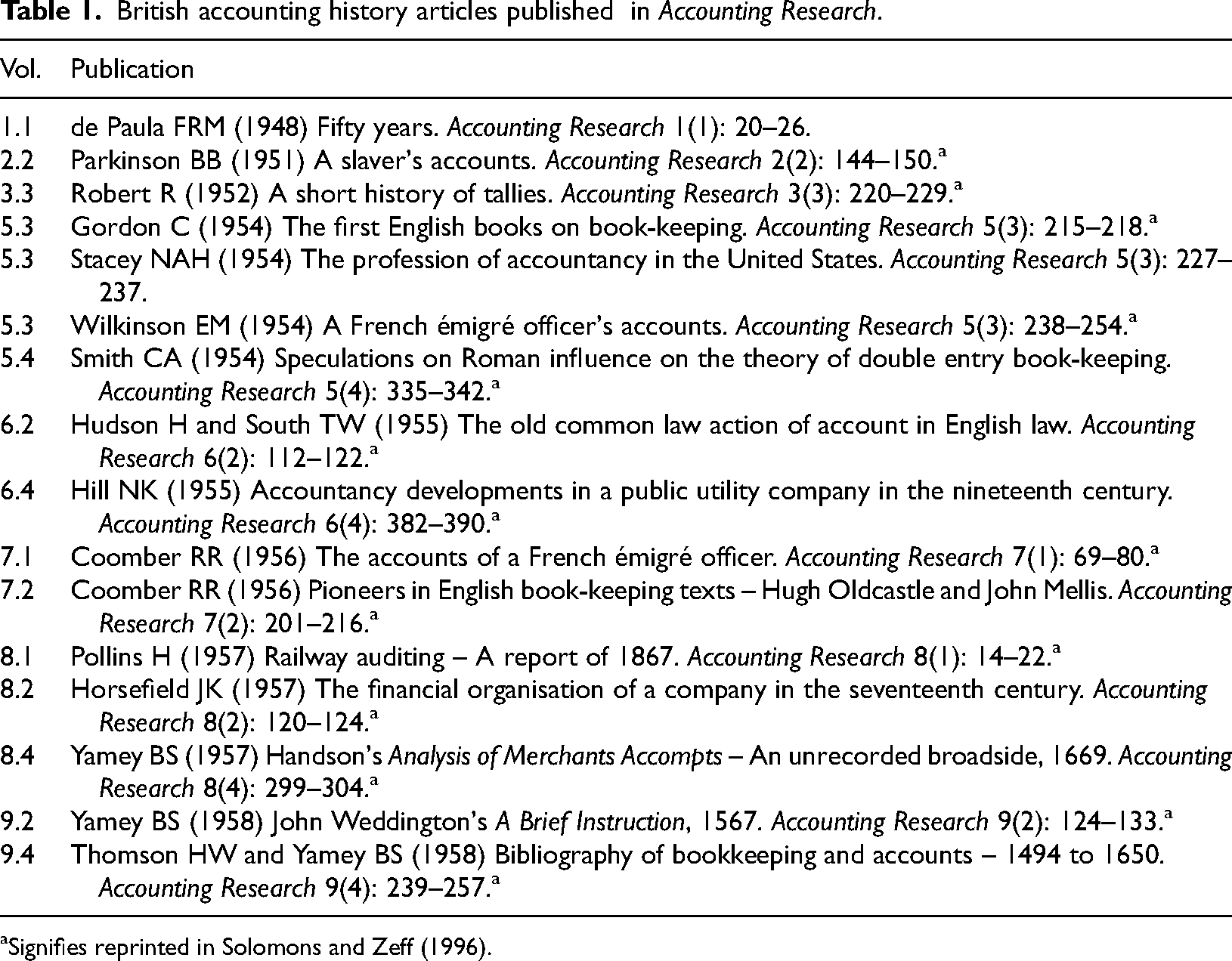

British outlets for accounting history articles, within the accounting literature, were, through to 1948, mainly confined to The Accountant and The Accountant's Magazine. However, each of these publications primarily targeted a readership comprising accountants in business and professional practice. 1948 saw the launch of Accounting Research compiled by the Incorporated Accountants Research Committee. The journal was jointly edited by: Frank Sewell Bray – senior partner of Tansley Witt & Co. – who gives his academic affiliation as the Department of Applied Economics, University of Cambridge; and Leo T. Little, University College of the South West of England (today Exeter University). The first issue of Accounting Research appeared in print in November 1948 and the last of its 36 numbers in October 1958. The journal remains substantially hidden from history despite the reprint of 14 of 16 items on British accounting history (see Table 1) in Solomons and Zeff (1996). For example, I have found no citation of Parkinson's article (Parkinson, 1951) in the ‘critical’ slavery literature that has emerged in recent decades.

British accounting history articles published in Accounting Research.

Signifies reprinted in Solomons and Zeff (1996).

A variety of author affiliations includes a former librarian of the ICAEW (Cosmo Gordon), an accountant working in business (Rudolph Robert) and one in professional practice (Robert Ronald Coomber). Most of the remainder were academics, at least for part of their career, possibly reflecting the status of the publication outlet as an academic journal. John Keith Horsefield lectured at the London School of Economics (LSE) though, by the time he was published in Accounting Research, he was pursuing a highly successful career in the civil service. de Paula occupied a chair part-time at the LSE while Bradbury Parkinson lectured at the University of Liverpool. Harold Pollins was a labour and economic historian who taught at Ruskin College, Oxford.

Books on accounting history published prior to 1970 focused principally on accounting institutions. A History of the Chartered Accountants of Scotland was published in 1954 as was that of the Association of Certified and Corporate Accountants. Three years later the History of the Society of Incorporated Accountants, 1885–1957 was compiled by its long-time secretary (Garrett, 1961) and, in the following decade, The History of The Institute of Chartered Accountants in England and Wales 1880–1965 was authored by the ICAEW's past president, Sir Harold Howitt (Howitt, 1966). Stacey's (1954) English Accountancy: A Study in Social and Economic History, 1800–1954 is welcomed by Parker (1969: 106) as ‘A critical survey by a non-accountant’. Broader-based studies of accounting's history, though with a significant focus on the accounting profession, were scripted by Beresford Worthington (1895), journalist and author, Richard Brown (1905), Secretary of the Society of Accountants in Edinburgh whose book is described as ‘The most important of the early British works’ (Parker, 1969: 76), Arthur H Woolf (1912), barrister-at-law and the Scottish lawyer, David Murray (1930). A start was also made by leading accountants wishing to place the history of their firm in the public domain, including the joint senior partner of Cooper Brothers (Benson, 1954) and the senior partner of Deloitte, Plender, Griffiths & Co. (Kettle, 1957). 4

Controversies: accounting and capitalism

The single major debate that featured in the British accounting history literature through to the 1960s concerned the relationship between double-entry bookkeeping (DEB) and the rise of capitalism.

The role of accounting in economic development attracted the attention of German economic and social theorists in the early decades of the twentieth century. Werner Sombart and Max Weber argued that the development, and adoption, of DEB supplied an ensemble of accounting calculations that gave rise to a ‘calculative mentality’ (Bryer, 2000a) which enabled management to conduct business affairs more efficiently and profitably. These ideas, unquestioned for many years, were the subject of critical analysis by Yamey, beginning in 1949 (Yamey, 1949), based on his study of both early British accounting records and books on DEB published between 1494 (Pacioli's Summa) and the end of the eighteenth century. His major reservations concerning the significance of DEB for business efficiency received strong support from the prominent economic historian Sidney Pollard (1965: 248) whose study of business records caused him to conclude: ‘The practice of using accounts as direct aids to management was not one of the achievements of the British industrial revolution; in a sense, it does not even belong to the later nineteenth century, but to the twentieth’.

It is a debate which, we shall see, featured prominently in the traditional and critical accounting history literature post-1970.

Critical accounting

Accounting history, as an academic discipline in Britain, began to blossom in the latter part of the 1970s, partly as the result of support for this area of study provided by Bob Parker who became editor of Accounting and Business Research (ABR) in 1975. Parker also helped raise the profile of accounting history in Britain as the joint-coordinator for the Third International Congress of Accounting Historians held in London, August 16–18, 1980, and by arranging for the publication of a special issue of ABR (vol. 10, supp. 1, 1980) devoted to historical studies. Much of the growing literature continued to make little attempt to specify the theory on which studies were based. In common with Yamey, researchers grounded their studies in neo-classical economics and, at a time when that theoretical paradigm remained dominant, it was often assumed that nothing more needed to be said (Napier, 2021: 334). 5

All this was to change with the creation of new ways of studying the role of accounting in organisations and society, beginning in the 1970s. It was a decade which saw, in the United States, the movement (referred to as a ‘revolution’ by Beaver, 1989) towards empirical accounting research, which had begun in the previous decade, gain pace with the initiation of the positivists’ agency-information research programme. Academics in Britain, in contrast, began to devise diametrically different ways of studying accounting in both the present and the past. Laughlin (2014: 766, 769) recounts the role of Ernest Anthony (Tony) Lowe and a group of like-minded scholars (including the likes of Wai Fong Chua, David Cooper, Trevor Hopper, Richard Laughlin, David Otley, Tony Puxty and Tony Tinker) – referred to as the ‘Sheffield School’ – in what he described, much later, as ‘the now global Interdisciplinary and Critical Perspectives on Accounting [ICPA] Project’. 6

The 1970s also saw Anthony G. (Tony) Hopwood begin to make his mark, from 1976 as editor of Accounting, Organizations and Society (AOS). AOS became, in due course, a celebrated outlet for ‘socio-historical accounting research’ 7 focusing on how accounting impacts on individuals, organisations and society in general (Napier, 2020: 40; Roslender and Dillard, 2003). Lowe and Hopwood, who worked briefly together at the Manchester Business School in the late 1960s, have been identified as ‘key, if not the key, founders of the ICPA Project’ (Laughlin, 2014: 768). It soon became clear that the Project envisioned radical new ways of studying accounting's history.

Hopwood's inaugural editorial in AOS lamented the fact that ‘all too often accounting has been seen as a rather static and purely technical phenomenon’ but continues: ‘Nothing could be further from the truth’ (Hopwood, 1976: 1). The potential for accounting history to contribute to a dialogue which might help in ‘putting accounting where accounting was not’ (Hopwood, 1987: 214) is made clear in a later editorial which, as Napier (2006: 446) points out, ‘was couched in terms that would later be labelled as “traditional”. Certainly, when Hopwood (1977: 277) refers to the ‘evolutionary perspective’ that historical study might provide, the conveyed image is not so radically different from the definition of accounting history, compiled by the American Accounting Association in 1970, which became the subject of criticism, if not ridicule, from new accounting historians who judged it to seriously delimit the appropriate area for potential study.

The first nine volumes of AOS include just 11 papers on accounting history of which two can be placed squarely within the traditional neo-classical economics framework (Napier, 2006: 447). Hopwood (1985) contains observations which, with hindsight, signal his aspirations for AOS in terms of its contribution to the study of accounting history. Dissatisfaction was expressed with ‘not only the present state of knowledge in the area but also the current directions of historical research’, and this was because, in his view, there had been ‘a tendency for technical histories of accounting to be written in isolation of their social, economic and institutional contexts’ (Hopwood, 1985: 365). The critique of prior historical research continued in the same uncompromising manner when berating ‘the partial, uncritical, atheoretical and intellectually isolated nature of much historical work in the accounting area’ (Hopwood, 1985: 365). The very next issue of AOS contained a prime example of the better type of study that Hopwood had in mind (i.e., Burchell et al., 1985).

Further impetus for the critical study of accounting history was provided by special issues of AOS dedicated entirely (1991, vol. 16, no 5/6) or substantially (1993, vol. 18, no. 7/8) to historical papers.

8

The first of these contains an introductory piece authored by Peter Miller of the LSE, Trevor Hopper of the University of Manchester and Richard Laughlin of the University of Sheffield. There they celebrate a proliferation of methodologies, a questioning of received notions such as progress and evolution, a widening of scope, a new attentiveness to the language and rationales that give significance to accounting practices, and a shift of focus away from invariant characters such as the bookkeeper and the decision-maker towards a concern with broader transformations in accounting knowledge. New ways of posing questions about the past of accounting have become possible as a result. (Miller et al., 1991: 395)

Miller et al. (1991) christened what was judged to be radical new ways of doing historical research as ‘The new accounting history’ which, as explained below, transformed the study of accounting history in Britain and, in due course, in many other parts of the world.

Napier (2006: 447) reviews the contribution of AOS to the study of accounting history over the first 30 years of its existence and concludes that, during the second half of the 1980s, ‘historical research came into its own’ in the pages of AOS. His study reveals the wide range of theoretical lenses employed by researchers into accounting's past and, in the limited space available, I focus principally on the illumination provided for British researchers by the ideas and theories of the French philosopher, Michel Foucault, the German philosopher, Karl Marx, and the Italian-born sociologist, Magali Sarfatti Larson.

Foucault

According to Cooper and Tinker (1994: 1) Foucault's theories ‘have had a profound affect on social science, and accounting thought in particular’. Writing in the same year, Armstrong (1994: 26) correctly predicted that Foucauldian theories would continue to provide inspiration for much academic research. British authors were at the forefront in employing a Foucauldian framework to help understand how accounting, as a disciplinary technique which renders the actions of workers visible and calculable, succeeds in changing employees’ behaviour to better achieve managerial objectives. More specifically, Power (2011: 43) believes that Burchell et al. (1985) and Miller and O’Leary (1987) ‘are emblematic of what came to be called the Foucauldian turn in accounting research’.

Burchell et al. (1985: 399–400) present a study of accounting, founded on power and knowledge, to analyse and understand ‘the specific social space within which value added [accounting] appeared and developed’ in the 1980s. The power-knowledge dimension became more explicit in four papers published in AOS over the next three years. Hoskin and Macve were responsible for two of these contributions, in 1986 and 1988; the former to better understand the invention and much later diffusion of double-entry bookkeeping; the latter to uncover the role of West Point graduates in developing a “grammatocentric” and “panoptic” system for human accountability’ at the Springfield Armory, Massachusetts, beginning in 1817 (Hoskin and Macve, 1988: 37). In the intervening year, Hopwood (1987: 207) famously observed: ‘relatively little is known of the preconditions for such [accounting] change, the process of change or its organisational consequences’, and ‘The archaeology of accounting systems’ explored how Foucault's ideas could help to shine a light on such issues.

Loft's (1986) study – published in the same issue of AOS 9 as Hoskin and Macve (1986) – was stimulated by a concern that, within prior research, management accounting was ‘viewed as an objective form of knowledge untainted by social values and ideology; the practitioners as technically skilled professionals whose political and social allegiances have no bearing on their practices’ (Loft, 1986: 137). Loft's oeuvre, designed to embrace ‘wider accounting-society relationships’, is inspired by the work of Foucault generally and, ‘in particular the history, described as “genealogical” in form, [in] Discipline and Punish (1977)’ (Loft, 1986: 138–139).

Turning to the second of Power's ‘emblematic’ papers, Miller and O’Leary (1987) locate the creation of the governable worker, in Britain, as part of the scientific management movement, often referred to as Taylorism. Miller and O’Leary (1987: 241) reveal how standard costing, as part of the quest for scientific management that gained momentum during the first three decades of the twentieth century, took cost accounting to a new level by rendering visible the level of efficiency of individuals within an enterprise.

Authors, both in Britain and elsewhere, have built significantly on this cluster of pioneering publications – the two by Hoskin and Macve (1986, 1988), together with those of Burchell et al. (1985), Loft (1986), and Miller and O’Leary (1987) – which are ranked as five of the nine ‘most influential’ research papers for the study period 1990–1999 (Carmona, 2006: 257). Naturally, of course, these authors’ ideas have also been the source of comment and criticism. For example, Boyns and Edwards take a broader view of what counts as management accounting and, therefore, are unconvinced that the history of cost and management accounting should be viewed through an American centric lens. Some aspects of their differences, and their common ground, feature in a 2000 issue of The Accounting Historians Journal (Boyns and Edwards, 2000; Hoskin and Macve, 2000). 10

Further, the idea that the history of, say, cost and management accounting is marked by key discontinuities – for example, at the Springfield Armory in the early nineteenth century (Hoskin and Macve, 1988) – has not remained unchallenged. One might not deny the possibility of someone such as Josiah Wedgwood ‘putting accounting where accounting was not’ (Hopwood, 1987: 214), or that the First World War, through the work of accountants at the Ministry of Munitions, may have had a dramatic and positive effect on companies’ costing procedures (Loft, 1986). However, Boyns and Edwards, based on their own research and that of others, argue that accounting practices which appear new, at first sight, might take on a less revolutionary guise when researchers dig deeper into accounting's past. They therefore categorise accounting's history as more likely exhibiting ‘continuity with change’ than discontinuity (Boyns and Edwards, 2013; see also Edwards, 2019).

Marx

British researchers have also been at the forefront when drawing on the work of Karl Marx to reveal how accounting, as a social phenomenon, can be employed to control and exploit the labour force. In Tinker's estimation, ‘Marxist oriented critical accounting research – “as we know it” – began to emerge in the UK in the mid-1970s’ (Tinker, 2005: 106). Napier (2020: 39) identifies Tinker, together with Neimark, writing towards the end of the following decade (Tinker and Neimark, 1987, 1988), as ‘early advocates for a Marxist accounting history’ based on social conflict between the capitalist and labouring classes.

A Marxist influence is evident, early on, in the work of Armstrong (1985, 1987; see also Hopper and Armstrong, 1991) who draws on labour process theory to investigate the social consequences of accounting. More specifically, to reveal how cost accounting and budgeting-based control systems may be ‘viewed as mechanisms for controlling labour, and financial reporting is theorised as a process for allocating surplus value among different “fractions of capital”' (Napier, 2020: 40). As Napier (2020: 40) further points out, the Marxist approach is most explicit in the prolific literature authored by Bryer (e.g., 2005, 2006) ‘who has suggested that changing “modes of production”, most particularly the transition from feudalism through mercantilism to capitalism as exemplified by the British Industrial Revolution, can be associated with changes in modes of accounting’.

Larson

We have seen that the history of the accounting profession featured prominently in articles and books written by traditional accounting historians pre-1970. Such works continued to feature in the literature and include two first class studies of the history of accounting firms authored by the business historian, Jones (1981, 1995). As the title of the first of these indicates, the histories of Ernst & Whinney and of Price Waterhouse are entwined with that of the British economy and are squarely located within a neo-classical economics framework. Between the date of Jones’ two books the academic literature, as discussed above, had begun to display a ‘critical’ dimension which questioned the previously accepted idea that there was some kind of common pathway to professional status whose achievement was perfectly natural and desirable. As Poullaos and Ramirez put it (2020: 281): '“Critical” scholars analysed professions as the outcome of a hard-fought struggle by status and rent-seeking aspirants whose right to professional status was sometimes far from obvious’.

The change of direction was substantially founded on the Weberian concept of closure 11 through the pursuit of a ‘professional project’ designed to enable those on the inside to access enhanced social and economic rewards (Larson, 1977). 12 These ideas were applied to the history of the accounting profession, early on, by the sociologist Macdonald (1984, 1995) and the management and organisational studies expert, Willmott (1986). The latter publication, which came into the light in the columns of AOS during the transformative period for accounting history research, has been described as ‘a marker for the introduction of the aforementioned sociological insights to the study of the accountancy profession’ (Poullaos and Ramirez, 2020: 281). These works have been built upon by numerous British accounting historians, among whom the most prominent is Stephen Walker whose sociologically-informed studies of the history of the accounting profession stretch from 1988, which saw the publication of his PhD thesis (Walker, 1988), through to the present day. Major contributions to this literature have also been made by British authors such as Ken Shackleton (often in conjunction with Walker) and Tom Lee.

It is important to note, however, that not everyone is convinced that the ‘new accounting history’ better explains the historical trajectory of the accounting craft in Britain with Matthews (2006: 501) insisting that ‘technological determinism offers a more powerful [explanatory] model’. The continued publication of such ideas may be seen as a further example – see also capitalism and the history of costing discussed above – of the ‘British’ liberal tradition of controversy within the accounting history arena.

More on accounting and capitalism

It was noted earlier that Yamey's criticism of the Sombart-Weber thesis was based principally on his study of accounting records created and bookkeeping texts published in the seventeenth and eighteenth centuries. Further, and more extensive, studies of the archives have made Yamey's, and Pollard's, conclusions the subject of serious questioning. Edwards and Newell (1991: 35), drawing partly on an extensive study of Welsh business records conducted by Jones (1985), conclude: there is sufficient evidence that businessmen were cost-conscious and utilised costing data for planning, control and decision-making purposes from the sixteenth century to challenge the established view of lack of progress in these forms of accounting before the late nineteenth century.

13

Further work by Edwards, Boyns, David Oldroyd, and many other authors, based on the study of British business archives, have since reinforced these conclusions (Boyns and Edwards, 2013, chs 5 and 6).

The debate about the relationship between accounting, capitalism and economic development thus remains ‘ongoing’ (Arnold and McCartney, 2008: 1186) and has attracted attention from critical historians. Most prominently, Bryer (e.g., 2000a, 2000b, 2005) is judged to have ‘moved the discussion forward by focussing on “accounting calculations rather than recording methods”, above all the calculation of the rate of return on capital, and linking this to the concept of “calculative mentality”' (Arnold and McCartney, 2008: 1186). Bryer detects evidence of this ‘calculative mentality’ during Britain's agricultural revolution and more explicitly during the industrial revolution. Toms (2010) does not dispute the broad thrust of Bryer's arguments but finds little or no evidence of return on investment calculations during the industrial revolution, considering them to be late nineteenth-century innovations.

A study conducted by Edwards et al. (2009) has parallels with that of Bryer in that it re-examines the Sombart–Weber thesis, and Yamey's critique of that thesis, through the lens provided by DEB texts published in Britain during the seventeenth and eighteenth centuries. These were found to contain incontrovertible written evidence explicitly testifying to recognition of the potential usefulness of DEB for purposes of performance assessment and decision making.

The debate on the relationship between capitalism and economic development featured prominently in ‘A brief history of double entry bookkeeping’ aired on BBC Radio 4 in 10 episodes between 8 and 19 March 2010. The series was compiled by Jolyon Jenkins based on a series of interviews he conducted with, amongst others, Boyns, David Cooper, Edwards, Macve, Walker and Yamey. Jenkins was inspired to create this series by his reading of The Routledge Companion to Accounting History (Edwards and Walker, 2009).

Institutional initiatives

We have seen that the Accounting Research journal was a creation of the Incorporated Accountants Research Committee. There have occurred, in Britain, other institutional initiatives that have furthered the study of accounting history within and beyond Britain. Some of these are summarised below in roughly chronological order.

In 1970 Bob Parker, then at the University of Dundee, encouraged the Institute of Chartered Accountants of Scotland to set up the Scottish Committee on Accounting History comprising academics, practitioners and archivists. Parker was the first convenor of the Committee, followed by two other leading students of accounting history – Tom Lee and Stephen Walker.

14

Walker (2020: 18) sums up the Committee's contributions as follows: The Committee performed valuable work in bibliographical compilation, locating and preserving archives, managing the antiquarian book collection of its sponsoring institute, and supporting research projects and publication, primarily on Scottish subjects including biographical and institutional studies on the history of the accountancy profession.

South of Hadrian's Wall, the Accounting History Committee for England and Wales, renamed the Accounting History Society in 1974, was formed in 1972 ‘to promote the study of accounting history’ (Boys and Freear, 1992: ix). The journal Accounting History, launched by the Society in 1976, was initially edited by John Freear of the University of Kent. Eight volumes were published over the next 10 years. The Editorial (Boys, 1986: 1) 15 to the last issue reported: ‘The journal flourished in its early years, but … Now, unfortunately, so few articles have been submitted for consideration that it is no longer feasible to continue publication’. Clearly, researchers preferred to target other journals; the US-based Accounting Historians Journal was launched in 1974 and generalist research journals were, in the main, open to historical studies. It may be that the somewhat homespun appearance of the journal – articles typed double-spaced and photocopied – did not meet the professional image desired by prospective authors. During its short life, the journal published many quality research articles of which 26 are reproduced in Boys and Freear (1992).

Although not confined to accounting history, there is no doubt that the Interdisciplinary Perspectives on Accounting Conference, first held in Manchester in 1985, 16 has been an important factor in the blossoming of its research agenda. The conferences, which sought to advance the ‘IPA project’ which, ‘At its simplest, … entails viewing accounting through the lens of another discipline’ (Roslender and Dillard, 2003: 327), was organised by David Cooper and Trevor Hopper. 17 Historical studies presented at the 1985 conference formed the basis for the following publications cited in this paper: Armstrong (1987), Loft (1986), Hoskin and Macve (1986, 1988) and Puxty et al. (1987). Growing recognition of ‘accounting as a social and institutional practice’, as well as a technical activity, was marked by publication of a collection of almost exclusively British-authored studies under that title in 1994 (Hopwood and Miller, 1994).

1988 saw the second IPA conference, held in Manchester, and the creation of the Business History Research Unit (from 2007 the Accounting & Business History Research Unit) at the Cardiff Business School. To signal the latter's existence, a conference entitled ‘Accounting and business decision making in companies, 1844–1939’ was held in September 1989. The conference took place annually, thereafter, through to 2011, attracting papers and delegates from all over the world. The ‘Cardiff conference’ – a term designed to signal its connection with its former home and with the ideology underpinning the event – was revived in 2019 though then held at Edge Hill University and organised by Cheryl McWatters and Alasdair Dobie.

In 1989, the Accounting, Business & Financial History journal was launched and edited by Edwards and Boyns of the Cardiff Business School's Business History Research Unit. As the name of the journal indicates, similarly with the annual conference, the aim was to encourage interdisciplinarity by connecting accounting historians with business and finance historians who made use of accounting information in their research. Boyns (2020) draws attention to the fact that the editors of ABFH also sought to expand the geographical boundaries of historical research in accounting, business and financial history. To help achieve that goal, they successfully implemented a policy of commissioning geographical-based issues of the journal guest-edited by academics with specialist knowledge of the selected country's accounting history. Carnegie and Potter's (2000: 188) study of publishing patterns in the three specialist English-language accounting history journals, in the late 1990s, revealed that ‘the extent of subject countries or regions under examination was found to be the largest for ABFH with contributions on 16 countries or regions’. One geographical-based special issue was published during Carnegie and Potter's study period, but eight more – China, France (twice), Germany, Ireland, Italy, Japan and the United States – appeared in the noughties.

A final institutional initiative designed to further stimulate accounting history research and teaching saw the creation of the Accounting History Special Interest Group of the British Accounting and Finance Association in 2018.

Concluding remarks

The section entitled “Profiling accounting history publications pre-1970” revealed a significant British literature on accounting history prior to 1970. However, up until 1939, according to Parker and Yamey (1994: 3), it did not ‘include studies that could compare with the best works of Continental scholars’. Nor did any British author attempt ‘an ambitious history of accounting’ such as that penned by America's AC Littleton (1933) (Parker and Yamey 1994: 4). Nevertheless, British contributions were judged ‘quite impressive’ (Parker and Yamey, 1994: 3) and their scope, content and public profile increased over the next 30 years due to support for historical studies provided by Accounting Research, the publication of institutional histories, and the academic leadership of Basil Yamey which included publication of the widely-cited Studies in the History of Accounting in collaboration with AC Littleton.

Up to 1970, in Britain, probably more articles studied the content of early (pre-1800) accounting records than any other topic; for books, the development of the profession featured most prominently. Most accounting history publications were descriptive and chronicled past events with little further comment. Amongst published authors, librarians/archivists, practitioners, local historians and non-accounting academics were most populous. These ‘traditional’ type authors are seen, by advocates of the ‘new accounting history’, to be preoccupied with treating history as one of continuous evolution, technical elaboration and constant improvement towards its present state (Loft, 1995: 25). The sole, major, critical study of accounting's past, pre-1970, was authored by an economist. In Napier's estimation, Yamey's ‘work was crucial in turning accounting history (at least among Anglophone scholars) from a hobby into a serious research field … Today's historians of accounting stand on the shoulders of Basil Yamey’ (Napier, 2021: 334). The ‘traditional’ approach to the study of accounting's past was increasingly given a more explicit grounding in economics, in the 1970s and 1980s, by researchers that Loft (1995: 25) has labelled neoclassicists.

Arrival of the ‘new accounting history’ saw a vigorous and productive debate between accounting historians, of different theoretical persuasions, concerning the best way of doing accounting history (Fleischman and Radcliffe, 2003). Proponents of the new accounting history were ‘suspicious of theorisations of accounting's past based on neo-classical economics’ with, as Napier (2021: 334) points out, Yamey being ‘squarely’ within that theoretical tradition. In contrast: Much of the ‘new’ accounting history emerging in the late 1980s and early 1990s showed the clear influence of theorists such as Marx, Weber, Foucault, Habermas, Derrida, Latour and Giddens, as well as sociological ideas such as institutional theory, feminist/gender theory and social constructivism. (Napier, 2020: 34)

Central to this blossoming of the research agenda was the focus on interdisciplinarity (Baskerville et al., 2017), perhaps especially in Britain, under the initial impetus provided by the Interdisciplinary Perspectives on Accounting Conference, first held in Manchester in 1985, and, from round about the same date, the willingness of AOS to publish historical studies on ‘the behavioural, organizational and social positioning and importance of accounting’ (Hopwood, 2009: 887).

As the theorisation of accounting's past gained pace, the character of the accounting history community changed dramatically. Increasingly, authors were located within academe, though not necessarily accounting faculty. The involvement of academics from cognate and more far-flung departments also became more common as interdisciplinary research became, for many, a priority. For example, sociologists (e.g., Keith Macdonald), economists (e.g., Trevor Boyns), management scientists (e.g., Peter Armstrong and Hugh Willmott) and educationalists (e.g., Keith Hoskin), and many others possessing expert knowledge, have helped and should continue to help expand the territories occupied by studies of accounting history.

Footnotes

Acknowledgments

This study has received the benefit of invited comments and criticisms from Trevor Boyns and Stephen Walker and inputs from two anonymous referees.

Funding

The author received no financial support for the research, authorship and/or publication of this article.