Abstract

In this introduction, we observe that the study of social structures and social relationships constitutes a common theme among the articles and commentaries contained within this special issue on Theories of Family Enterprise. Individuals and organizations are embedded in complex networks of social organization and exchange. Within business enterprises, familial relationships engender unique goals, governance structures, resources, and outcomes. We discuss these relationships, potential research directions, and the contributions made by the articles and commentaries. In so doing, we expand the literature on how social structures and social relationships affect the behavior and performance of family firms.

This article, and the special issue it introduces, continues a series of special issues on family business that began in 2003. 1 In this special issue, the articles and commentaries deal with the social structures and social relationships that exist in family firms. Our purpose is to introduce that topic, identify relevant directions for future research, and review the articles and commentaries that follow. In this respect, we extend the contributions of previous special issues in this series (e.g., Steier, Chua, & Chrisman, 2009).

Social relationships among members of an organization as well as their boundary spanning activities affect the resources and performance of all organizations (Eisenhardt & Schoonhoven, 1990; Penrose, 1959; Uzzi, 1997). The influence of social relationships on family firms is likely to be different, however, because of the controlling family’s structural, cognitive, and relational embeddedness in the firm (Bird & Zellweger, 2018). For example, relationships within family firms typically differ from those of nonfamily firms in terms of conditions of membership, communication principles, norms of justice, and time horizons (Zellweger, 2017). The embeddedness, and the legitimacy and power that the family may exercise as a result of the property rights secured through controlling ownership allows the family to pursue family-oriented nonfinancial goals that generate socioemotional wealth (SEW), which are rarely present and would be considered illegitimate in nonfamily firms.

These social relationships may be categorized as: (a) intra-family relationships that exist among family members; (b) extra-family relationships that exist between family members not directly involved in the family firm and nonfamily individuals and groups; (c) intra-firm relationships that exist among family and nonfamily members of the firm; and (d) extra-firm relationships that exist between the firm or its members (family or nonfamily) and external stakeholders. In the typical family firm, these relationships will interact with each other. For example, sibling rivalry within the family can affect relationships between family and nonfamily workers in the firm. Likewise, a non-involved family member’s relationship with someone outside the family and the firm may lead to an expansion of the firm’s network (cf. Steier, 2007). Globally, these behaviors are further influenced by contextual factors such as the formal or informal institutions in a region or nation (Steier, 2009). In other words, while social relationships matter, so does the social structure within which they are embedded (Burt, 1992; Granovetter, 1985).

In turn, a family firm’s pursuance of financial and nonfinancial goals requires ability—both in terms of the decision-making control and the resources needed to act—and the willingness to use that ability to behave in a particularistic fashion (Carney, 2005; Chrisman, Sharma, Steier, & Chua, 2013; De Massis, Kotlar, Chua, & Chrisman, 2014). Social relationships can enhance ability by strengthening the capacity of a family firm’s dominant coalition to govern and by providing access to valuable resources (Pearson, Carr, & Shaw, 2008). Social relationships may also affect the willingness of the dominant family coalition to pursue particularistic financial and nonfinancial goals.

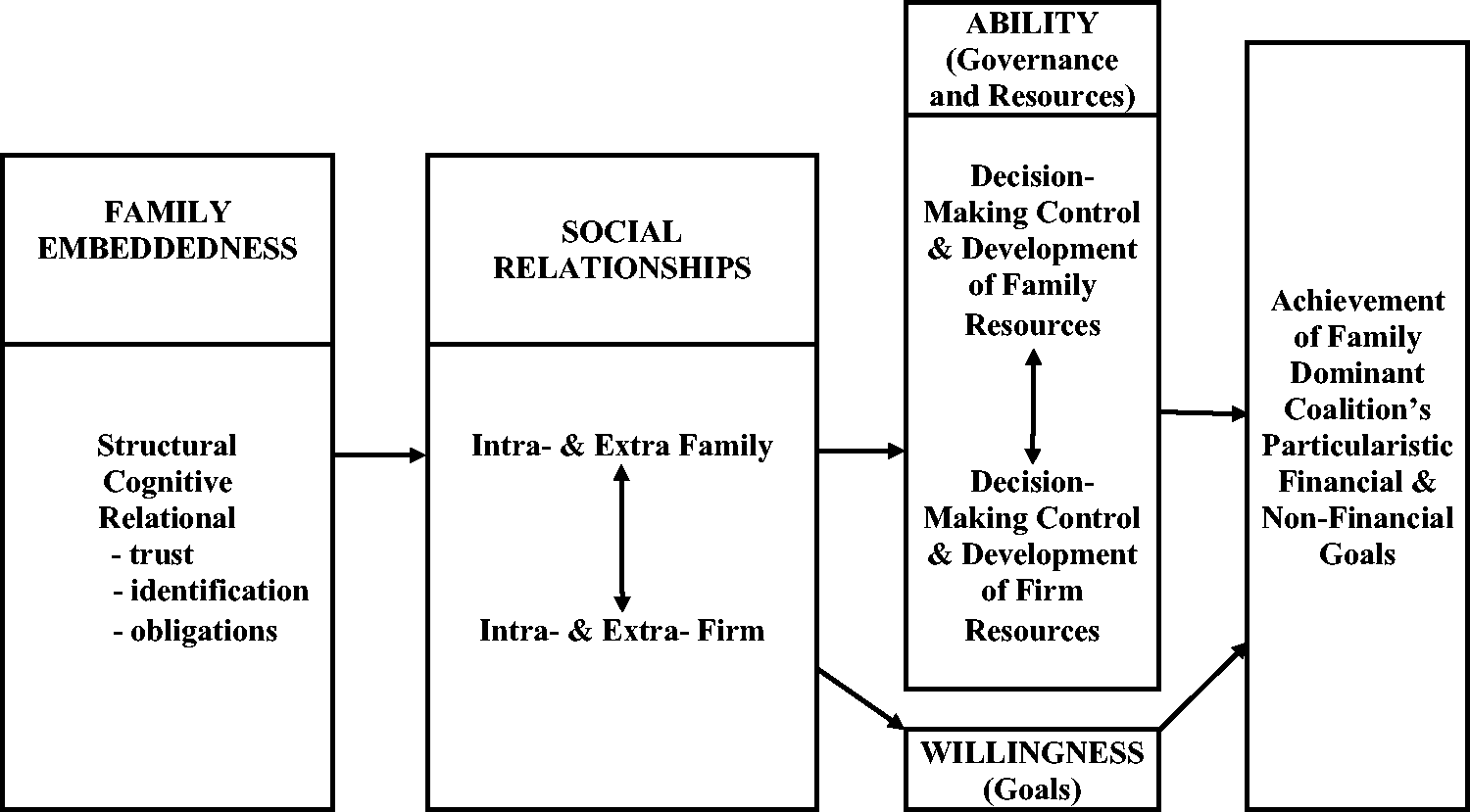

The model in Figure 1 depicts the effects of family embeddedness and social relationships on a family firm. As the model shows, the family’s structural, cognitive, and relational embeddedness affects the four interactive categories of social relationships. These social relationships help the family maintain decision-making control of the firm and develop both family- and firm-level resources, which interact with one another (as shown by the double-headed arrow). Social relationships also influence the willingness for particularistic behavior. Together, ability and willingness influence the achievement of financial and nonfinancial goals.

Model of social relationships in family firms.

Potential Research Directions

Researchers have explored in quite some detail the structural embeddedness of firms, such as the size, openness, centrality, and spatial distribution of their networks (e.g., Bruderl & Preisendorfer, 1998; Jack & Anderson, 2002; Sorenson & Stuart, 2001). This research has explored how social networks (Batjargal, 2010; Brass, Galaskiewicz, Greve, & Tsai, 2004; Stam & Elfring, 2008) and interorganizational alliances (Davidsson, Achtenhagen, & Naldi, 2010; Stuart, 2000) contribute to firm performance. Furthermore, Arregle, Hitt, Sirmon, and Very (2007) discuss how family social capital is formed and spills over to form organizational social capital and Chua, Chrisman, Kellermanns, and Wu (2011) study situations where family firms borrow family social capital. Nevertheless, we still do not know much about how relational embeddedness—the quality of the relationships between members of a group, in terms of levels of trust, identification, and mutual obligations (Blatt, 2009; Moran, 2005)—impact economic action and success (Bird & Zellweger, 2018). The dearth of research is perceptible not only among members of top management teams (TMTs), but also between TMTs and other stakeholders, both inside and outside family firms.

Keeping in mind the complexities associated with family and nonfamily relationships inside family firms, these deliberations about structural and relational embeddedness suggest that the time is ripe to revisit what we mean when we say that a family is embedded in the firm because family embeddedness so far has been studied primarily in the context of newly founded firms (Aldrich & Cliff, 2003). This line of research suggests that an entrepreneur’s embeddedness in a family can facilitate the startup process by providing resources and emotional support (e.g., Chua et al., 2011). Alternatively, family relationships may undermine entrepreneurial intentions and activities (Kellermanns, Eddleston, & Zellweger, 2012). For example, family ties primarily generate bonding social capital rather than bridging social capital and consequently hold only a limited amount of novel information. This may depress innovativeness (Ruef, 2002, 2010). In certain cases, network closure may inhibit the ability of family firms to capitalize on the strength of weak ties available in the broader social system (Granovetter, 1973). Furthermore, financial and nonfinancial obligations embedded in familial relationships can have negative performance implications and threaten the family system (Arregle et al., 2015; Sieger & Minola, 2017).

However, families can be embedded in established firms as well. A contribution of this special issue is to revisit and unpack the concept of family embeddedness in terms of social structures and social relationships (Bird & Zellweger, 2018; Jennings, Eddleston, Jennings, & Sarathy, 2015; Le Breton-Miller, Miller, & Lester, 2011). In combination with the insights gained from the articles and commentaries in this issue, we see family embeddedness in terms of a firm’s exposure to familial relationships that either support or constrain the firm’s development. With this definition, we draw attention to features that seem decisive for a more in-depth understanding of family embeddedness in business activity.

Foremost, we need to expand our understanding of family embeddedness beyond the founding context to the entire lifecycle of the firm (Van de Ven & Poole, 1995). In the founding context, the family may be a critical resource contributor to an entrepreneurial venture even if other family members are not directly involved (Steier, 2007). In contrast, in established firms, the resource flows between family and business may change direction over time so that the family may become a net recipient of resources from the firm (cf. Sharma, 2008). In fact, this is the dominant concern of the well-developed principal–principal agency literature.

It also seems important to take into account the life course of key decision makers, which shape their views and behaviors (Aldrich & Kim, 2007; Elder, Johnson, & Crosnoe, 2003). As part of a family embeddedness perspective, critical life course events come in the form of the birth of children, marriage, divorce, or death, to mention just a few decisive life course events. At this point, we can only speculate about the ways in which these events spill over onto a firm, such as when they alter owners’ risk aversion, dividend demands, propensity to engage in mergers and acquisitions, and eventually even decisions for a firm’s sale or closure.

Moreover, we have to be more specific about whether we speak about the structural, cognitive, or relational embeddedness of decision makers and firms (Dacin, Beal, & Ventresca, 1999; Leana & Van Buren, 1999; Nahapiet & Ghoshal, 1998; Pearson et al., 2008; Tsai & Ghoshal, 1998). For instance, it appears important to move beyond a monolithic view of family to take into account structural, relational, and cognitive embeddedness differences among various types of families and their firms (Bird & Zellweger, 2018; Parsons, 1949; Zellweger, 2017). In fact, the need to differentiate the types of families in control of a firm is well-known in the family business literature, which, for example, distinguishes between owner–manager, sibling partnership, and cousin consortium constellations (Gersick, Lansberg, Desjardins, & Dunn, 1999). Exploring the structural, cognitive, and relational embeddedness of different types of family firms holds wide theoretical and practical promise.

Moving beyond the mere presence or absence of certain types of social relationships, researchers and practitioners alike would benefit tremendously from further insights into how family firms manage these relationships. The formation of social capital in family firms has been explored at the conceptual level (e.g., Arregle et al., 2007; Pearson et al., 2008). However, we lack adequate insights into how social relationships with stakeholders such as employees and clients are maintained by family firms across time and even generations. We also know relatively little about the stability of these relationships, and what types of behaviors support or undermine them. In this regard, family business researchers have started to build upon the transaction cost economics literature to better understand problems of asset specificity, holdup, bounded rationality, and bounded reliability, which may drive a wedge between family and nonfamily members of an organization (Chrisman et al., 2014; Gedajlovic & Carney, 2010; Verbeke & Greidanus, 2009; Verbeke & Kano, 2012). In light of the importance of nonfinancial goals for family firms (Chrisman, Chua, Pearson, & Barnett, 2012; Gomez-Mejia, Haynes, Nunez-Nickel, Jacobson, & Moyano-Fuentes, 2007; Zellweger, Nason, Nordqvist, & Brush, 2013), we also need studies that investigate how goals influence the development and maintenance of relationships, and through what processes family firms generate and appropriate the financial and nonfinancial value that is tied to these relationships. In sum, we call for further research on the formation, maintenance, stability, and instrumentality of social relationships in family firms.

Any in-depth discussion of family embeddedness will have to deal with cross-level and multilevel phenomena (Rousseau, 1985), in particular, individuals, families, and firms. The interactions among these levels are intricate since they exist along various governance domains, such as ownership, the board of directors, and the TMT. In working toward unpacking cross-level and multilevel effects of family and business, it seems promising to build on the rich work in the human resource literature that deals with such effects (e.g., Glisson & James, 2002; Takeuchi, Chen, & Lepak, 2009).

Finally, work on family embeddedness needs to take into account the linkages between the family and firm on the one hand, and the broader societal context in which the firm is embedded on the other. This discussion will have to move beyond observations about whether families are good at navigating environments with weak market and legal institutions (Banalieva, Eddleston, & Zellweger, 2015; Khanna & Palepu, 2000), or whether family firms fill or exploit institutional voids (Luo & Chung, 2013). For instance, family membership and who is a legitimate claimant to a firm’s assets has been found to vary greatly depending on societal context (Khavul, Bruton, & Wood, 2009; Smith, 2009). Furthermore, we know relatively little about the impact of laws and regulations on the transgenerational preservation of family assets (Carney, Gedajlovic, & Strike, 2014; Ellul, Pagano, & Panunzi, 2010).

Contributions of the Articles and Commentaries

The articles and commentaries in this special issue contribute toward an understanding of social relationships in family firms in multiple ways. We group them according to whether they explore (a) intra-family social relationships, (b) intra-firm social relationships, or (c) extra-firm social relationships. However, none of the studies in the special issue investigate extra-family social relationships, which suggests an avenue that future research needs to explore.

Intra-Family Social Relationships

The article by Garcia, Sharma, De Massis, Wright, and Scholes (2019) explores how parental support and psychological control alter the self-efficacy and commitment of next-generation family members. Garcia et al. argue that parental support (i.e., instrumental assistance, career-related modeling, verbal encouragement, and emotional support) has a positive effect on perceived self-efficacy and both the affective and normative commitment of next-generation family members to engage in a family firm. In contrast, psychological control (i.e., excessive control, manipulation, and constraining interactions by a domineering parent) weakens next-generation family members’ self-efficacy and affective commitment while strengthening their normative and continuance commitment. As such, their article complements prior work by McMullen and Warnick (2015) who explain how parent-founders can promote affective commitment in successors and that of Parker (2016) who proposes that investment in intangible capital and high parental effort can help solve the willing successor problem.

In her commentary, Reay (2019) further unpacks the black box of within-family relationships and draws attention to family routines, such as family celebrations, family traditions, and family interactions, which she sees as mechanisms through which norms, values, and beliefs are communicated between generations. Such family routines have been found to foster identity and increase support among group members, which may be particularly valuable in times of crisis. Building on recent advancements in the routines literature (Howard-Grenville & Rerup, 2016) and by pointing to the family therapy literature, Reay assigns important roles to agency, change, and intervention, thereby moving the discussion of parenting styles in the context of family business succession from a static and passive perspective toward a more dynamic and active perspective.

In conjunction with prior literature, the work of Garcia and colleagues (2019) and Reay (2019) suggest multiple avenues for future research. For instance, researchers could test the impact of instrumental assistance, career-related modeling, verbal encouragement, and emotional support on the commitment of next generation family members (Turner & Lapan, 2002). Furthermore, while the supportive and altruistic role of parents is discussed in many studies of family firms (e.g., Eddleston & Kellermanns, 2007; Schulze, Lubatkin, Dino, & Buchholtz, 2001; Zellweger, Richards, Sieger, & Patel, 2016), the constraining, domineering, and even manipulative behavior of parents has received less attention (e.g., Criaco, Sieger, Wennberg, Chirico, & Minola, 2017). The article by Garcia and colleagues and the commentary by Reay thus represent important work on which future researchers can build to explore both the bright and dark sides of family relationships (Kellermanns et al., 2012). There is a particular opportunity to study problematic behaviors that sometimes occur during family business succession and the strategies that might reduce their chance of occurrence (cf. Le Breton-Miller & Miller, 2018). The flip side of problematic parental behavior is the reactions of the next generation, which may include social comparisons, feelings of inferiority and entrapment, perceived restrictions to autonomy, and so forth (Criaco et al., 2017; Sieger & Minola, 2017). These reactions may vary in different kinds of families. For example, in tightly knit families, parents’ supportive or controlling behaviors could have outsized positive or negative effects.

The above studies primarily focus on how support can foster commitment and willingness to join a family firm. However, neither parental support nor an offspring’s willingness necessarily reflects his or her managerial capability, which is often lower than that of professional CEOs, who are selected from among the very best of a much larger talent pool (Bennedsen, Nielsen, Perez-Gonzalez, & Wolfenzon, 2007; Perez-Gonzalez, 2006). Therefore, the relationship between the willingness and capability to lead a family firm deserves more scrutiny, as does how parents and other family owner-managers can develop the latter along with the former. Just as the motivational triggers underlying willingness and commitment may differ substantially (Sharma & Irving, 2005), capability is somewhat context specific and has both innate and developmental components that need to be better understood.

Intra-Firm Social Relationships

A second stream of articles deal with social relationships within family firms. Kotlar and Sieger (2019) explore the entrepreneurial behavior of family and nonfamily managers. They draw from transaction cost economics to argue that in comparison to family managers, nonfamily managers face greater bounded rationality problems in terms of understanding the goals, strategic alternatives, and entrepreneurial opportunities of family firms. They further suggest that nonfamily managers are more likely to reduce their commitment to the family firm over time, creating a bounded reliability problem. Both of these problems are expected to limit the entrepreneurial behavior of nonfamily managers in family firms. Indeed, in their study of 296 family firms, Kotlar and Sieger find that nonfamily managers exhibit lower levels of entrepreneurial behavior than family managers. However, the entrepreneurial behavior of nonfamily managers is higher when a founder is involved in the firm.

Looking at the mechanisms for increasing the entrepreneurial behavior of nonfamily managers, Kotlar and Sieger (2019) find monitoring, distributive justice, participation in the TMT, and perceived control to be effective. These findings cast further doubt on the predictions of stewardship theory, which suggests that the interests of owners and managers should naturally align. In fact, Kotlar and Sieger find that managerial controls are necessary since owners cannot count on managers to automatically defer to owners on the goals of the company, especially in family firms that pursue nonfinancial as well as financial goals.

Interestingly, though, Kotlar and Sieger find that some of the classical agency-based remedies for managerial opportunism such as shareholding and performance-based pay are unable to increase the entrepreneurial behavior of nonfamily managers. The non-finding for shareholding perhaps conceals a more fundamental problem about the actual control that the family is willing to cede. For example, little incentive is likely to be provided if a nonfamily manager is given a minority share in the firm only to realize that while he is indeed an owner on paper, his actual influence and remuneration remains low. Such problems may be especially severe in family firms that pay out very low dividends and pursue nonfinancial as well as financial goals (Le Breton-Miller et al., 2011; Neckebrouck, Schulze, & Zellweger, 2018). Similarly, the non-finding for performance-based pay may be an indication that such practices are more show than substance in many family firms, that the incentives offered are simply not sufficient to elicit more effort, or the system is not sensitive enough to the performance of the individual manager (Chua, Chrisman, & Bergiel, 2009). All in all, a major conclusion from Kotlar and Sieger’s study is that the assumptions of both agency and stewardship theory regarding the types and use of governance mechanisms may need to be revisited and reconciled in light of the problems of bounded rationality and bounded reliability.

In their commentary, Soleimanof, Singh, and Holt (2019) switch the focus to the family to explore how family institutions, such as family structures, parenting styles, and communication patterns impact the entrepreneurial attitudes and mindsets of family members. They suggest that family institutions shape family members’ cognitions as well as their interactions and relationships. For example, Soleimanof et al. argue that rigid family structures, authoritarian parenting styles, and conformity in communication patterns tend to stifle entrepreneurial behaviors whereas greater flexibility in these dimensions can enhance entrepreneurial behaviors. They also note that cultures, particularly those based on hierarchical authority, collectivism, and ethnicity can have a major role in shaping family institutions. Thus, Soleimanof et al.’s commentary complements the article by Kotlar and Sieger, as well as that of Garcia et al. (2019), and suggests that research on how family institutions and culture influence the entrepreneurial behavior of both family members and nonfamily members would be useful.

The second article on relationships within family firms by Cruz, Justo, Larraza-Kintana, and Garces-Galdeano (2019) explores how female members of boards of directors impact family firms’ corporate social performance (CSP). They suggest that while female directors are more likely to favor actions that enhance CSP, not all have the power and/or perceived legitimacy to influence board decision making. Probing a sample of Fortune 1000 firms over the period from 2008 to 2012, Cruz et al. find that increases in CSP associated with women on the boards of family firms are due mainly to the presence of two types of women directors: (a) nonfamily, outside directors, and (b) family inside directors. However, family outsiders, women directors who are family members but do not work in the firm, and nonfamily insiders, women directors who work in the firm but are not part of the family, do not seem to influence CSP.

The article by Cruz et al. (2019) raises some interesting questions. Conceptually, the article draws attention to role identities and gender stereotypes in family firms, a topic that has received increasing, but still insufficient attention (e.g., Amore, Garofalo, & Minichilli, 2014; Martinez-Jimenez, 2009; Rodríguez-Ariza, Cuadrado-Ballesteros, Martínez-Ferrero, & García-Sánchez, 2017). Since only 13.6% of the board members of the companies Cruz et al. studied are females, and only about 1/6 of these are female family members, women are obviously underrepresented. However, regarding their influence on board decisions, it is possible that some female directors may not be advocates for CSP or may have simply been outvoted rather than marginalized. It is also likely that some female board members share the mindsets of their male counterparts (for or against CSP), while others have different perspectives. Thus, a direct comparison with male directors is needed to fully understand the influence and status of female directors. Such a comparison would need to account for variations in family and firm status, as well as the perceptions of board members on issues such as CSP. In sum, the article by Cruz et al. indicates the need for more research into the micro-processes in family firm boardrooms. Moreover, it seems highly topical as the possibility of the appointment of a first-born daughter as successor rather, than the appointment of a first-born son as successor, is increasing.

In the third article dealing with social relationships within family firms, McLarty, Vardaman, and Barnett (2019) argue that pursuit of family and firm-related goals in family firms creates dissonance for employees about how to channel their efforts on behalf of the organization. Drawing on social exchange theory, they propose that congruence between supervisors’ familial status and the importance they place on SEW aids in resolving this dissonance and signals to employees that the supervisor is a genuine and trustworthy exchange partner. McLarty et al. suggest that congruence also removes uncertainty about where to direct effort by signaling what activities are valued, allowing committed employees to achieve higher task and citizenship performance. In contrast, supervisors with incongruent behavior may be seen as obsequious and weak, thereby creating confusion among employees about how they should prioritize their efforts.

The empirical findings by McLarty et al. (2019) support their theoretical arguments and have direct practical relevance, pointing to an understudied aspect of leadership in family firms. The consistency between the status and the goals of a supervisor seems to help turn high commitment into high task and citizenship performance. Thus, firm leaders need to be aware of the importance of behaving predictably and reliably: a certain role identity (e.g., family versus nonfamily status) creates expectations about goal priorities (e.g., emphasis on SEW versus financial performance). Congruence has a supportive effect for employees with high levels of commitment who seem to appreciate guidance from a leader they perceive as legitimate, whether that leader is a member of the owning family or not.

On the other hand, incongruence may not be a problem for those employees who are less committed. In fact, an intriguing and apparently unanticipated insight of their study is that when supervisors behave inconsistently (family supervisors with low SEW concerns, or, nonfamily supervisors with high SEW concerns), employees with low commitment reach higher levels of task performance, higher even than employees with high commitment when supervisors display consistent behavior. These findings suggest that commitment per se is no guarantee of the highest levels of task performance. Taken to the extreme, highly committed employees may also be those that are less competent and require the guidance of a legitimate leader to reach high levels of task performance. However, as is the case for the Garcia et al. (2019) article, the article by McLarty et al. (2019) does not take individual capabilities into account. In family firms, employees with lower commitment may be those with higher capabilities who are only there until more promising job prospects in nonfamily firms come along. But if such employees see supervisor incongruity as a sign of weak or ineffectual leadership they may perceive an opportunity for their own advancement and increase their efforts. In any event, future studies should more closely scrutinize the (managerial, technological, general) capabilities of family and nonfamily employees in family firms as well as their commitment (cf. Chrisman, Devaraj, & Patel, 2017).

In their commentary, Campopiano and Rondi (2019) take the idea of incongruence one step further and suggest that in line with leader-follower congruence arguments, employee commitment is also influenced by hierarchical dyadic congruence (Zhang, Wang, & Shi, 2012). Hierarchical dyadic congruence exists when the supervisor and the supervisee both have the same familial status and SEW concerns. Campopiano and Rondi argue that while hierarchical dyadic congruence always strengthens the supervisee commitment-performance relationship, hierarchical dyadic incongruence does not always weaken the supervisee commitment-performance relationship. Taken together, the article by McLarty et al. (2019) and the commentary by Campopiano and Rondi add to knowledge on micro organizational behaviors in family firms (Gagné, Sharma, & De Massis, 2014).

Extra-Firm Social Relationships

The final set of articles investigates the intersection of societal contexts and family firms. Mani and Durand (2019) take a refreshing look at the business group affiliation of family firms. They find that family firms in India are less likely to be part of business groups, to exhibit cross group ties, and to be embedded in intercorporate ownership networks, findings that seem to be in conflict with institutional void arguments (Luo & Chung, 2013). On the other hand, Mani and Durand find that firms with greater involvement in trading communities are more likely to be part of business groups, to exhibit cross group ties, and to be embedded in intercorporate ownership networks. These trading communities are distinguished by commonalities among members in terms of characteristics such as religion, language, region, and caste. Thus, they are roughly analogous to ethnic groups; but their shared characteristics also make them similar to family firms, when family is defined very broadly.

Indeed, prior work is suggestive of the similarities between community enterprises and family firms in that there is a relational component that can be more important than merit in their governance systems (Peredo & Chrisman, 2006). The fact that trading communities such as these seem to possess characteristics that one might normally associate with family firms suggests that they deserve more research attention. Indeed, it would be useful to understand the extent to which social relationships and other characteristics of trading communities or community enterprises are similar or different from family firms, business families (Steier, Chrisman, & Chua, 2015), multifamily firms (Pieper, Smith, Kudlats, & Astrachan, 2015), and business groups (Morck & Yeung, 2003) and how those differences are shaped by institutional contexts (Steier, 2009).

The commentary by Hsueh and Gomez-Solorzano (2019) adds further value by discussing heterogeneity in the social ties of family firm and community leaders. As those authors suggest, besides varying in strength, ties can: (a) be neutral or negative as well as positive; (b) be based on affective or instrumental logics; (c) have symmetric or asymmetric content for the parties in the relationship; and (d) change their characteristics over time. Hsueh and Gomez-Solorzano point out that each of these characteristics can influence the network strategies selected by individuals or firms. Likewise, these network strategies can vary in their efficiency and effectiveness depending on the characteristics of the ties on which they are based. Given the importance of social relationships and social capital to family firms (Arregle et al., 2007; Pearson et al., 2008), Hsueh and Gomez-Solorzano provide useful insights on how the strong and weak ties of family firms can be conceptualized and measured. One particularly interesting research question derived from their work is how the addition or deletion of ties with different characteristics might affect family firms. With regard to addition of ties, the list of circumstances would include events such as marriage, adoption, and the inclusion of nonfamily members in the TMT or ownership group. Mehrotra, Morck, Shim, and Wiwattanakantang’s (2013) study of arranged marriages might be an instructive starting point for such an investigation.

In the second article in this group, Baù, Chirico, Pittino, Backman, and Klaesson (2019) explore the structural embeddedness of family firms in rural and urban contexts using a matched sample of 7,829 family firms and 7,829 nonfamily firms in Sweden. They hypothesize that family firms will grow slower than nonfamily firms but local embeddedness, especially in rural areas, will have a larger positive impact on family firm growth than nonfamily firm growth. However, family firms are found to grow faster than nonfamily firms in general, a finding that is unexpected, particularly given prior research (e.g., Bird & Zellweger, 2018). Nevertheless, their study confirms that family firms benefit most from local embeddedness and that the impact of local embeddedness on family firm growth is greatest in rural settings. The authors suggest that the reason for these findings is that the dual financial and nonfinancial goals of family firms provide them with incentives to cultivate their embeddedness in the local community, making them more likely to use social capital as an integral part of their strategy.

Interestingly, local embeddedness may decrease the growth of nonfamily firms. Baù et al. (2019) attribute this to potentially lower quality, antagonistic relationships that some nonfamily firms develop in the community. However, since they do not measure the quality of the extra-firm social relationships of family or nonfamily firms directly, more work on the positive and negative aspects of local embeddedness is needed. Similarly, work on how family firms recognize, build, and exploit relationships in their communities, and which relationships are key to growth, profitability, and SEW would be especially useful.

Finally, Lude and Prügl (2019) investigate how 418 nonprofessional investors perceive family firms using an experimental study based on the precepts of prospect theory (Kahneman & Tversky, 1979). Lude and Prügl find that owing to a reputation for trustworthiness and longevity, family firms are able to benefit from a cognitive embeddedness advantage among investors, which the authors label “family firm bias.” Here, we should note that reputation is similar to social capital in that it is based on prior dealings that enable a firm to have access to certain resources that are necessary for it to achieve its objectives (cf. Luoma-aho, 2013). Furthermore, like social capital, if handled properly, reputation grows stronger with use.

Lude and Prügl (2019) find that nonprofessional investors disproportionately prefer to invest in family firms in comparison to nonfamily firms, even when the former represent riskier investments. This finding holds regardless of whether investors operate in the domain of gains or losses. Indeed, the effect is most pronounced in the gain context where investors are presumed to be more risk averse. Interestingly, results indicate that the family firm investment option does not affect risk awareness of nonprofessional investors, only their willingness to assume risk.

Of particular importance is Lude and Prügl’s effort to investigate the editing process where investors evaluate the information at their disposal for subsequent decision making, as this is a first step toward determining cause and effect relationships. They find that trust and longevity underlie the family firm bias that lead individuals to prefer risky family firm investments over less risky, nonfamily ones. Unexpectedly, family firms’ reputation for longevity trumps trust as a cognitive motivator. This is notable as it suggests that the practical and well as theoretical utility of the transgenerational sustainability goal associated with family firms has not been fully appreciated in the literature (cf. Chua, Chrisman, & Sharma, 1999; Zellweger, Kellermanns, Chrisman, & Chua, 2012). Put differently, the implication that the transgenerational sustainability of family firms is a resource that has value to external stakeholders as well as family stakeholders, suggests a promising new line of research. Additionally, their experimental approach might be usefully applied to confirming or denying the idea that SEW leads to risk aversion in the gains domain and risk seeking in the loss domain (Chrisman & Patel, 2012), as well as to sorting out the influence of its components (Berrone, Cruz, & Gomez-Mejia, 2012).

In their commentary, Fang, Siau, Memili, and Dou (2019) discuss four cognitive factors in prospect theory (Kahneman & Tversky, 1979) that may also create bias in assessing risky decisions and might also help explain some of the underlying mechanisms associated with the family firm bias of investors identified by Lude and Prügl (2019). These include anchoring (a mental starting point), representativeness (assessment based on the similarity of a situation with other situations), stereotype heuristic (assessment based on prevailing or socially dominant beliefs), and information availability (assessment based on partial information). To our knowledge, no one has applied these to a family business setting even though they may yield useful insights, separately, and in combination. Furthermore, aside from helping to understand risky decisions, these cognitive factors might also help to understand social relationships in family firms, particularly those involving new participants such as nonfamily managers and in-laws.

Conclusion

In this introductory article, we argue that it is important to further understand how family firm behavior is affected by social structures and social relationships emanating from a family’s embeddedness in a firm. We also describe how the articles and commentaries in this special issue contribute to this understanding. Significantly, we identify four categories of social relationships: intra-family, intra-firm, extra-family, and extra-firm. Unfortunately, extra-family relationships are not represented among the studies in this special issue, which may indicate a topic area that is ripe for investigation. However, the other categories are well-represented.

We argue that future research endeavors would benefit from taking into account the whole lifecycle of the firm, life course events of key decision makers, and the structural, cognitive, and relational embeddedness of decision makers and firms. We also call for further empirical work on the formation, maintenance, stability, and instrumentality of social relationships in a family firm context, and advocate closer attention to cross-level and multilevel phenomena, in particular between the family and firm levels.

Overall, there are many opportunities for research on the societal and institutional contexts in which firms are embedded, taking into particular account cognitive and regulatory institutions that impact family firm behavior. The articles and commentaries in this special issue, combined with work on family sociology (Jaskiewicz, Combs, Shanine, & Kacmar, 2017), economic sociology (Dacin et al., 1999; Portes & Sensenbrenner, 1993; Uzzi, 1997), and economics (Ellul et al., 2010; Williamson, 1985), should provide insights that will facilitate such investigations.

Footnotes

Acknowledgments

The guest editors acknowledge the Swiss Research Institute of Small Business and Entrepreneurship and Center for Family Business at St. Gallen University, the Centre for Entrepreneurship and Family Enterprise at the University of Alberta, the Center of Family Enterprise Research at Mississippi State University, and an anonymous donor for providing financial support for the conference where the articles and commentaries contained in this special issue were originally presented. We also thank Marlies Graemiger of the University of St. Gallen for her assistance in managing the local arrangements. We are grateful to the following individuals for sharing their time and expertise to help develop this special issue of Entrepreneurship Theory and Practice on Theories of Family Enterprise by reviewing the articles and commentaries submitted.

Tim Blumentritt, Kennesaw State University

Isabel Botero, Stetson University

Gabriella Cacciotti, University of Warwick (United Kingdom)

Erick Chang, Arkansas State University

Danielle Cooper, University of North Texas

Josh Daspit, Texas State University

Alexandria Dawson, Concordia University (Canada)

Bart Debicki, Towson University

Federico Frattini, Polytecnico di Milano (Italy)

Rich Gentry, University of Mississippi

Danny Holt, Mississippi State University

Liena Kano, University of Calgary

Ambra Mazzelli, Asia School of Business (Malaysia)

Aaron McKenny, University of Central Florida

Onnolee Nordstrom, North Dakota State University

Pankaj Patel, Villanova University

Whitney Peake, Western Kentucky University

Torsten Pieper, University of North Carolina, Charlotte

Kirk Ring, Louisiana Tech University

Matthew Rutherford, Oklahoma State University

Savatore Sciascia, IULM University (Italy)

Wenlong Yuan, University of Manitoba (Canada)

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.