Abstract

Humor is a key indicator of the health of work groups, including during times of crisis. Moreover, studies of newly formed groups show that the type of humor used can change as members of a group get to know one another and form bonds. Yet in the context of a relatively established work group, can the nature of the group’s humor evolve in response to a crisis? We address this question in the context of the Federal Open Market Committee (FOMC), examining whether the FOMC was able to pivot its use of humor following the 2007 financial crash. As hypothesized, we find a post-crash increase in “affiliative” humor in general, and “playful banter” specifically, indicating effective group dynamics among members (which bodes well for the global economy). The FOMC thus offers evidence that established work groups can use humor as a dynamic mechanism for adapting to new circumstances.

A wide variety of work groups face challenges of elevated stress that demand effective action from the group, be it a school board, a city council, or a corporate board of directors. Such times of crisis may result from a budget shortfall, a scandal, or any other number of other problems. In these tough times, work groups must respond effectively, or the group’s future—and in many cases outcomes for other members of the public—will be in peril. It is well documented that crises can threaten a group’s functionality (Driskell et al., 1999; McGrath, 1997; T’Hart et al., 1997). Work groups thus need to use every available tool to maintain the group’s health and effectiveness during times of stress.

One such tool is humor, which has been documented to help groups navigate crises (Beck et al., 2012; Firestien, 1990; Francis, 1994; Vivona, 2014). In the context of stressful decisions, humor can provide group members with emotional space “to figure out what to do next” (Keyton & Beck, 2010, p. 386; see also Weingart & Todorova, 2010). Studies also show that some types of humor are more conducive to productivity and group cohesion than others (Bolman & Deal, 2017; Plester & Sayers, 2007; Scheel & Gockel, 2017; J. W. Smith & Khojasteh, 2014). Further, Terrion and Ashforth (2002) show that a newly-formed work group can evolve its use of humor over time. Yet to date, no study has examined whether established work groups are capable of changing the type of humor they use in response to a crisis. This gap in our understanding includes how the type of humor a group uses shifts from before to after the onset of a major crisis event that uniformly changes how they are to operate.

The purpose of this study is to examine the degree to which a work group changes its use of humor before and after a crisis event, and in what ways. We study this question in the context of the Federal Open Market Committee (FOMC)—the main governing body of the U.S. Federal Reserve. Described as “the world’s most influential central bank” (Mui, 2018, para. 4), the FOMC is one of the most powerful work groups in the world, operating within the larger Federal Reserve organization. Studies point to the significant effects of FOMC policy decisions (i.e., interest rates) on the stock market (e.g., Bomfim, 2003; Nikkinen & Sahlström, 2004). “The Fed’s decisions can ripple through the economy, making mortgages more expensive, causing mining companies to reduce investment in new machinery and preventing retail stores from hiring new workers” (Vinik, 2017, para. 2). The 12 voting members of the FOMC, along with seven non-voting members, make these policy decisions during their meetings, regularly scheduled (at least) eight times a year.

For this paper, we use quantitative text analysis tools, as well as qualitative analysis, to examine the role that humor plays in FOMC meetings before and after a major financial crisis hit in 2007. The question of whether a work group can shift to using more cohesion-fostering types of humor during crisis is an important one, as crises can threaten the group’s functionality (Choi, 2002; Street & Anthony, 1997; T’Hart et al., 1997). If an established and seemingly healthy work group is not capable of pivoting from less-helpful to more-helpful types of humor in times of crisis, this would position humor as a non-flexible mechanism of group dynamics, only useful when the type of humor a group uses happens to be useful for the particular circumstances of the moment. Yet if an established and healthy work group is capable of shifting its use of humor in response to a crisis, while successfully managing that crisis, this would position humor as an especially powerful potential tool for helping groups navigate times of crisis.

Essentially, this study seeks to contribute to the literature on humor in groups and within meeting processes in several ways. We theorize and state two hypotheses comparing FOMC meeting transcripts before the 2007 financial crisis hit (i.e., pre-crash) to those after the crisis hit (i.e., post-crash). We expect that the FOMC as a work group will change their prevailing humor use after the crisis to be more affiliative in nature (H1), including an increase in playful banter (H2). We also believe that these changes after the crisis began served as social lubricants, helping facilitate small group decision making. We further discuss the implications of these contributions and the limitations associated with the current study methodology.

Humor in Work Groups

Humor has been shown to be a key indicator, as well as a driver, of the health of various work groups (e.g., Ziv, 2010), from military settings (Fisher, 2021) to the German Parliament (Müller, 2011). As Vivona (2014) puts it, humor serves as a “barometer of the [team members’] negotiation of the emotional burdens” of their work (p. 127). Part of the explanation for the power of humor in work groups comes from research on the collective mood states of individuals working in groups, which indicates that, when working together, individuals begin to share the same affective experience, whether positive or negative (K. K. Smith & Crandell, 1984)—a phenomenon referred to as emotional contagion (Hatfield et al., 1994). Reus and Liu (2004) argue that in the context of “. . .groups of organizational members that face knowledge-intensive tasks” (p. 246), such emotional contagion is particularly salient because of the intensity of the social interactions. In an extensive study of 70 four-to-eight-member work groups, Bartel and Saavedra (2000) found significant positive correlations between instances of observed laughter and individual group members’ self-reported individual and group moods. In other words, groups in which laughter was observed were perceived as more pleasant at the group level and elicited more positive self-reported moods in individual members.

Research has begun to clarify the mechanism through which laughter and humor are associated with positive group dynamics and mood, as well as the varied forms humor may take in achieving positive group outcomes. When laughter is present in a group context, group members rate the group’s overall affective state more positively—even in those cases where their rating of the group’s affective state was not the same as their own individual affective state (Kelly & Jones, 2012). Hence, emotional contagion impacts group members’ perceptions of the group as a whole. When humor events elicit positive emotional displays (e.g., laughter), it leads to emotional contagion that creates shared positive affect, which further encourages the occurrence of additional humor events, thereby creating a humor-friendly climate that fosters a positive cycle of humor (Lehmann-Willenbrock et al., 2011; Robert & Wilbanks, 2012). As Lehmann-Willenbrock et al. (2011) put it, “humor manifests in cycles of humor/laughter/humor sequences” (p. 644). Further, this positive impact of humor on group dynamics is not necessarily dependent on the positive or negative form of humor, but on the group’s perception of the humor (Martineau, 1972). In other words, even disparaging humor can positively shape a group by solidifying it (but with important caveats we discuss below).

Given that humor can impact and reflect group processes, it is important to consider the benefit of humor in reducing or managing stressful situations. At an individual level, exposure to humor can mitigate threat-induced anxiety (Lang & Lee, 2010; Yovetich et al., 1990) and improve task performance (R. E. Smith et al., 1971). By making a joke about a stressful situation, one may develop a sense of dominance or control over the situation (Henman, 2001). In the context of work groups, humor can serve not only to ease individual-level anxiety but also to keep the group connected and effective. Even jokes “in poor taste” can provide groups “an opportunity for a cognitive/affective shift or restructuring of the situation so that it is less stressful” (Vivona, 2014, p. 128).

Humor can also help establish the set of social rules that brings a group closer together. Specifically, humor can promote positive feelings among group members by fostering stronger interpersonal bonds (Francis, 1994). Joking relationships can be used as an index reflecting the existence of power and changes in power (Dwyer, 1991; Kahn, 1989). Put simply, “successful collective humor serves to reaffirm group identity in terms of ‘who we are, what we are doing, and how we do things’” (E. Romero & Pescosolido, 2008, p. 399). In this way, beyond the objects and targets of the humor used within a group, the mere use of humor itself can construct the group identity by creating a collective understanding of who they are and how they operate.

Of course, humor can also result in negative outcomes (e.g., Pollio, 1995; J. W. Smith & Khojasteh, 2014). The use of humor to belittle or disparage others can have negative effects on the group dynamics (E. J. Romero & Cruthirds, 2006). Regardless of the intention or the target of a piece of humor, humor can be perceived as offensive, especially when it is at the expense of an individual or a demographic group (e.g., women; Plester & Sayers, 2007). Thus, while humor can strengthen group cohesion, it can also harm the group through “negative functions such as derision and social isolation” (Scheel & Gockel, 2017, p. 21). Romero and Pescosolido (2008) capture the duality of humor’s role in groups when they say “we cannot stress enough that a distinction needs to be made between the positive and negative uses of humor” (p. 411).

Types of Humor

Whether humor has a positive or negative influence on a work group depends in large part on the type of humor being employed. Arguably the most comprehensive (and most referenced, with more than 2,600 Google scholar citations to date) typology of humor comes from R. A. Martin et al. (2003), who divide humor types in groups into four broad categories: two that enhance the self and two that enhance the group. Within each pair, one humor type is more positive and the other more negative. Humor that enhances the self can be used in a way that is “tolerant and non-detrimental to others (self-enhancing humor)” or in a way that comes “at the expense and detriment of one’s relationships with others (aggressive humor).” Correspondingly, humor that enhances relationship with others and thus the group as a whole can be used in a way that is “relatively benign and self-accepting (affiliative humor)” or used “at the expense and detriment of the self (self-defeating humor)” (R. A. Martin et al., 2003, p. 52).

Although each of these four main humor types can result in either positive or negative group outcomes, in general, documented instances of humor that damages relationships and the group as a whole fall into the aggressive category, whereas instances of humor that most strongly benefit the group are in the affiliative category (Plester & Sayers, 2007; Scheel & Gockel, 2017; J. W. Smith & Khojasteh, 2014). For example, Terrion and Ashforth (2002) conducted a 6-week study of a group of 27 recruits in a Canadian police training center, observing changes in the group’s humor over time. They documented a shift in the use of humor away from individualized self-deprecation (i.e., self-defeating humor) and toward collective putdowns of the group as a whole (i.e., affiliative humor) as the recruits bonded (Terrion & Ashforth, 2002). This shift in humor served to “. . .test, signal, and reinforce the growing trust and solidarity of the classmates” (Terrion & Ashforth, 2002, p. 80). Importantly, nearly all the instances of humor Terrion and Ashforth documented in their study of cohesion building fell within the two humor categories that enhance the group: affiliative and self-defeating.

Humor in Work Groups During Times of Crisis

Scholars have documented how humor types can shift over time among populations experiencing or witnessing a crisis, such as shifts in humor among members of local communities in Sierra Leone during the West African Ebola crisis of 2013 to 2016 (L. S. Martin, 2022), among Canadian patients with anxiety or depression throughout the COVID-19 pandemic (Rothermich et al., 2021), and on Twitter throughout the 2009 H1N1 “swine flu” outbreak (Chew & Eysenbach, 2010) and Hurricane Sandy in 2012 (McGraw et al., 2014), but none of these populations are work groups. Terrion and Ashforth’s (2002) study is one of the few scholarly works to examine how a work group’s use of humor evolves over time, although the group was a newly formed recruit group, rather than an established or ongoing group. Thus, to date, no studies explicitly examine whether and how an established, ongoing work group’s use of humor might change in response to crisis or stress.

Our study addresses a gap in the literature by investigating the use of humor within an established work group, the FOMC. Given that affiliative humor is the type of humor found to be most associated with strong group cohesion, with studies showing that adaptability and flexibility are key hallmarks of productive work groups (e.g., Schippers et al., 2014; Wiedow & Konradt, 2011), we hypothesize the following: Hypothesis 1: After the 2007 economic crash, there is an increase in the proportion of affiliative instances of humor used during FOMC meetings.

In particular within the affiliative category, playful banter forms of humor “are an essential source of invention and group spirit” (Bolman & Deal, 1992, p. 41). In her examination of the role of humor in a small, family-run corporation, Vinton (1989) calls playful banter “the great leveler” because it can be used “to deflate the importance of status”; if differences in status “were overemphasized in such a small and highly interactive group,” she writes, “it could be very difficult to get the work done. Consequently, bantering puts everyone on (more or less) the same plane and makes the job more enjoyable in such close quarters” (p. 161). As Plester and Sayers (2007) note, because playful banter can facilitate “synergy and functioning work groups,” it “both helps to forge culture and is a manifestation of that culture” (p. 159). In short, the presence of affiliative forms of humor generally, but also playful banter specifically, are generally indicative of and help propel positive group dynamics.

We therefore anticipate that after the crisis, the FOMC shifted its humor toward a specific type of affiliative humor, namely playful banter. There is not enough supporting literature to help speculate at length about the health of the FOMC in terms of workplace dynamics. Still, having weathered the 2007 financial crisis with their reputation relatively intact, the FOMC is generally deemed a healthy work group (Adolph, 2013). Given the documented role of playful banter in healthy work groups (Plester & Sayers, 2007), it is likely that the FOMC increased their use of this behavior during as the crisis unfolded. We thus propose the following: Hypothesis 2: After the 2007 economic crash, there is an increase in the proportion of “playful banter” instances of humor during FOMC meetings.

Methods

Context: The FOMC as a Work Group

We focus here on the U.S. Federal Open Market Committee (FOMC) as an important “work group.” According to Guzzo and Dickson (1996), a work group is defined as a group: made up of individuals who see themselves and who are seen by others as a social entity, who are interdependent because of the tasks they perform as members of a group, who are embedded in one or more larger social systems (e.g., community, organization), and who perform tasks that affect others (such as customers or coworkers). (pp. 308–309)

Formed by the Banking Act of 1933, the FOMC is the arm of the U.S. Federal Reserve charged with the crucial task of safeguarding the nation’s market operations by controlling interest rates and the monetary supply. As FOMC member William Poole said during a committee meeting in 2006, “The economy is not fragile, and our job, of course, is to keep it that way” (Mr. Poole, May 10, 2006). The FOMC’s tasks and decisions have far-reaching effects on others, including all those involved in the U.S. economy and beyond; thus, in line with Guzzo and Dickson’s (1996) definition, we classify it as a work group.

The FOMC is comprised of 19 people (12 voting and seven non-voting members), and FOMC meetings are also attended by “the Manager and Special Manager of the System Account, and those few staff members whose presence is essential to the work of the Committee” (Broida, 1974). The result can add up to a sizable number of people in the room, but with the focus squarely on interactions among the 19 board members themselves. Although at 19 people the FOMC does not fit Hackman’s (2004) “ideal team” size of fewer than 10 people, the committee’s level of frequent interactions and inter-personal comradery meets Bales (1953) definition of a small group (see also Pincus & Guastello, 2005 as an example of treating groups above 10 people as small groups): any number of persons engaged in interaction with one another in a single face-to-face meeting or a series of such meetings, in which each member receives some impression or perception of each other member distinct enough so that he can. . . give some reaction to each of the others as an individual person, even though it be only to recall that the other was present. (Bales, 1953, p. 30).

Thus, regardless of whether we classify the FOMC as small or medium in size, our study has implications for small groups since the group dynamics within the FOMC mirror those of a small group.

Although the high-powered individuals who comprise the FOMC are often of many minds on fiscal policy, the group has strong incentives to be a well-functioning, cohesive body. As Adolph (2013) writes, “the central bank as a whole benefits from the appearance of unanimity and confidence it inspires on the part of market observers” (p. 129). In line with its culture of cohesiveness, the FOMC tends to experience very little turnover, since the members have long term limits or no term limits depending on their specific role (see Appendix for more details on the FOMC membership, meeting agendas, etc.). Thus, we can imagine that the group dynamics of the FOMC are relatively consistent over time. For example, in 2014, Janet Yellen took over from Ben Bernanke as the Chair of Federal Reserve (and, thus, the FOMC), but Yellen had already been an on-again, off-again member of the FOMC for the previous 20 years. What changes, we will argue, is how the group responds to the economic context at hand.

FOMC Transcript Data

By law, the FOMC must meet at least four times each year. In practice, the FOMC tends to have eight regularly scheduled meetings per year, with more meetings during troubled economic periods. For example, in 2008 they met 14 times (eight times in person, and six times by conference call) as the financial crisis unfolded. Meeting transcripts are created by the FOMC Secretariat after each meeting, based on internal audio recordings (thus ensuring a high level of accuracy). Committee members are given the opportunity to review each transcript for accuracy but not for content. Each meeting therefore results in a transcript that contains many pre-scripted remarks or presentations, but also considerable back and forth among a small set of board members. The written transcripts are made public after a period of 5 years, but not the audio on which they are based.

We quantitatively analyzed all FOMC meeting transcripts from 2005 to 2008, for instances of laughter. We chose the 2005 to 2008 time period because we are interested in the period directly before and after the onset of the global financial crisis of that decade, which we identify as beginning on August 9, 2007 (Elliott, 2012). While the exact beginning of the crisis is hard to pinpoint, and many events contributed to it, such as the sudden downturn of the stock market in October 2007 and the bankruptcy of Lehman Brothers in September 2008, the first major event in the spiral of economic crisis occurred on August 9, 2007, when BNP Paribas blocked withdrawals from three hedge funds, citing evaporation of liquidity (Elliott, 2012). In total, the FOMC met 41 times between 2005 and 2008: 32 times in person and nine times by conference call. We obtained the meeting transcripts, in PDF format, from the Federal Reserve’s website, and converted them to plain text (extracting speaker identities, dates, etc.) using a pipeline we built for this study.

Because the transcripts are based on audio recordings of the meetings, they are detailed enough to include false starts of sentences as speakers find their wording, interruptions, and—of key interest to us here—laughter (annotated in the transcripts as “[Laughter]”). Because the recordings themselves are not available, we cannot differentiate between laughter amongst a few people and laughter amongst the entire group. Still, knowing which points in discussion prompted moments of laughter can reveal a great deal about the dynamics of the FOMC. In total, there were 977 instances of laugher, indicating 977 instances where something “humorous” was said. Of course, not all items that evoke laughter are necessarily funny, and not all jokes evoke laughter. Nevertheless, the presence of laughter signals a communal response to the item just uttered.

Each speaking turn in the transcripts is annotated with the identity of the speaker. We further divided each speaking turn into our main unit of analysis: the sentence, using the sentence splitter in the Stanford CoreNLP toolkit—one of the most accurate sentence splitters available (Dyomkin, 2020). We used the sentence, rather than the speaking turn, as our unit of analysis for three reasons. First, laughter tags are interspersed within speaking turns. For example, “The next item on the agenda is the selection of a Federal Reserve Bank to execute transactions for the System Open Market Account. My notes indicate to me, and I quote, ‘New York is the odds-on favorite.’ [Laughter] In that event, not wishing to go against the odds, I will entertain any motion which is restricted to nominating the Federal Reserve Bank of New York!” (Mr. Greenspan, January 31, 2006). Second, there may be multiple laughter tags in a single speaking turn. Third, speaking turns can be very long (i.e., many sentences). The meetings in our data set varied considerably in length, from the shortest meeting (a conference call) of 217 sentences immediately following the onset of the crisis (August 10, 2007) to the longest meeting (a 2-day in-person meeting) of 4,191 sentences (December 15–16, 2008).

Analysis Strategy

We utilized two types of analyses. First, we used automated content analysis to affirm the face validity of using annotated laughter as a gage for work group dynamics. We started by automatically counting the instances of laughter (raw count by date, as a proportion of all sentences by date, and overall count by committee member) in the meeting transcripts. We then conducted word-list-based sentiment analysis developed by Loughran and McDonald (2011) to examine the tone of the discussion, which involved identifying positive and negative words that captured the sentiment of financial texts. For example, “encouraging,” “favorable,” and “strong” are all counted as positive words, whereas “collapse,” “poor,” and “shutdown” are all counted as negative words (see Appendix for more details). If instances of laughter are indeed capturing the positive mood of the group, they should correlate positively over time with positive words, and negatively with negative words. They should also correlate positively with market conditions, which we measured using the S&P Real Index.

Second, we conducted manual quantitative content analysis to test our hypotheses and to further explore the work group dynamics revealed by moments of laughter. Specifically, we coded the sentence preceding each instance of laughter according to a codebook of humor types developed inductively by the authors for this study through a two-step process (see Stemler, 2000). In Step 1, keeping in mind R. A. Martin et al.’s (2003) broad categorization of humor, which focused on two types of self-focused humor (self-enhancing humor and aggressive humor) and two types of group-focused humor (affiliative humor and self-defeating humor), we read a random sample of the transcript sentences prompting “[Laughter]” and noted the different types of humor at play. We identified six main types of humor: individual self-deprecation, collective self-deprecation, process-oriented humor, economic conditions/policy humor, out-group humor, and finally playful banter. The economic conditions/policy humor type included instances of gallows humor, which we decided to code as a particularly interesting sub-category of economic conditions/policy humor given our interest in the FOMC’s use of humor before versus after the financial crash; we discuss the gallows humor findings briefly below. We created an other category for cases that did not fit into any of the six categories but also did not warrant a distinct category. This other category mostly includes sentences where even in context there was not enough substance to interpret the nature of the humor, except to determine that it does not belong to any of the other identified humor types.

In Step 2, in order to contextualize our data in the literature on work group humor (and directly address our Hypothesis 1 about affiliative humor), we compared the six types of humor to R. A. Martin et al.’s (2003) self-focused and group-focused categories. Only one type of humor used in FOMC meetings focused on the self: process-oriented humor. These instances included poking fun at the processes surrounding the meeting structure and schedule and joking derisions by one member (often the Chair) about the rest of the group’s tendencies for tardiness, lengthy discussion patterns, etc. When nested in R. A. Martin et al.’s (2003) scheme, these humor instances are not self-aggrandizing. Rather, they tend to jokingly criticize aspects of the process itself in a way that casts the speaker in a positive light as someone who has mastered the meticulousness of the FOMC’s processes enough to ridicule them (or the rest of the committee for not following them), putting this type of humor in the self-enhancing category. It is thus of note that our inductive examination of the transcripts did not reveal any instances of the aggressive form of self-focused humor that tends to be detrimental to a group. The other five types of humor we identified fall into R. A. Martin et al.’s (2003) group-focused humor. Two of them, individual self-deprecation and collective self-deprecation, fall within the self-defeating category, while two others, out-group humor and economic conditions/policy, are nested within the affiliative category (relevant to Hypothesis 1). The last type, playful banter (relevant to Hypothesis 2).

Table 1 shows examples of the six, plus other, humor types, each incorporated within R. A. Martin et al.’s (2003) broader categories. Many of these examples might not seem funny to the reader (or to us), but they were considered humorous enough to elicit laughter in the FOMC meetings. Recall that humor is subjective, that as specialists in the financial realm members of the FOMC are not “average bears,” and that like any co-workers they may share their own insider jokes.

Types of Humor Tracked in Quantitative Content Analysis of FOMC Transcripts, 2005 to 2008.

This excerpt is an example of regional rivalry between fifth district of Richmond, VA, represented by the speaker, Mr. Lacker, versus others in the northeast.

Two trained coders worked together to code all 977 instances of humor using the six types of humor (plus other). Using independent codings of 40 random items, the two coders demonstrated inter-coder agreement at 83% (Cohen’s Kappa = .769; Krippendorff’s Alpha = .771). Although this level of inter-coder reliability satisfies established benchmarks (Krippendorff, 2018), in order to assure the quality of our data we employed both coders to code all the instances of humor. For all cases of disagreement, the coders met with the lead author to decide on a final code, ensuring that the final dataset reflects 100% inter-coder agreement.

Results

Over the course of the 41 FOMC meetings between 2005 and 2008, 90 unique individuals spoke, but only 34 spoke extensively, uttering at least 500 sentences each. As noted above, FOMC meetings frequently involve the presence of various staff members, who may occasionally speak but do not contribute to the primary back-and-forth discourse between members that constitutes the main component of each meeting. For example, at the November 1, 2005 meeting, 18 FOMC board members spoke, along with 21 staff members (most of whom only spoke once). On average, the top 10 speakers in a meeting account for 69% of all the sentences in the meeting, and the top 19 speakers account for 94% of the sentences.

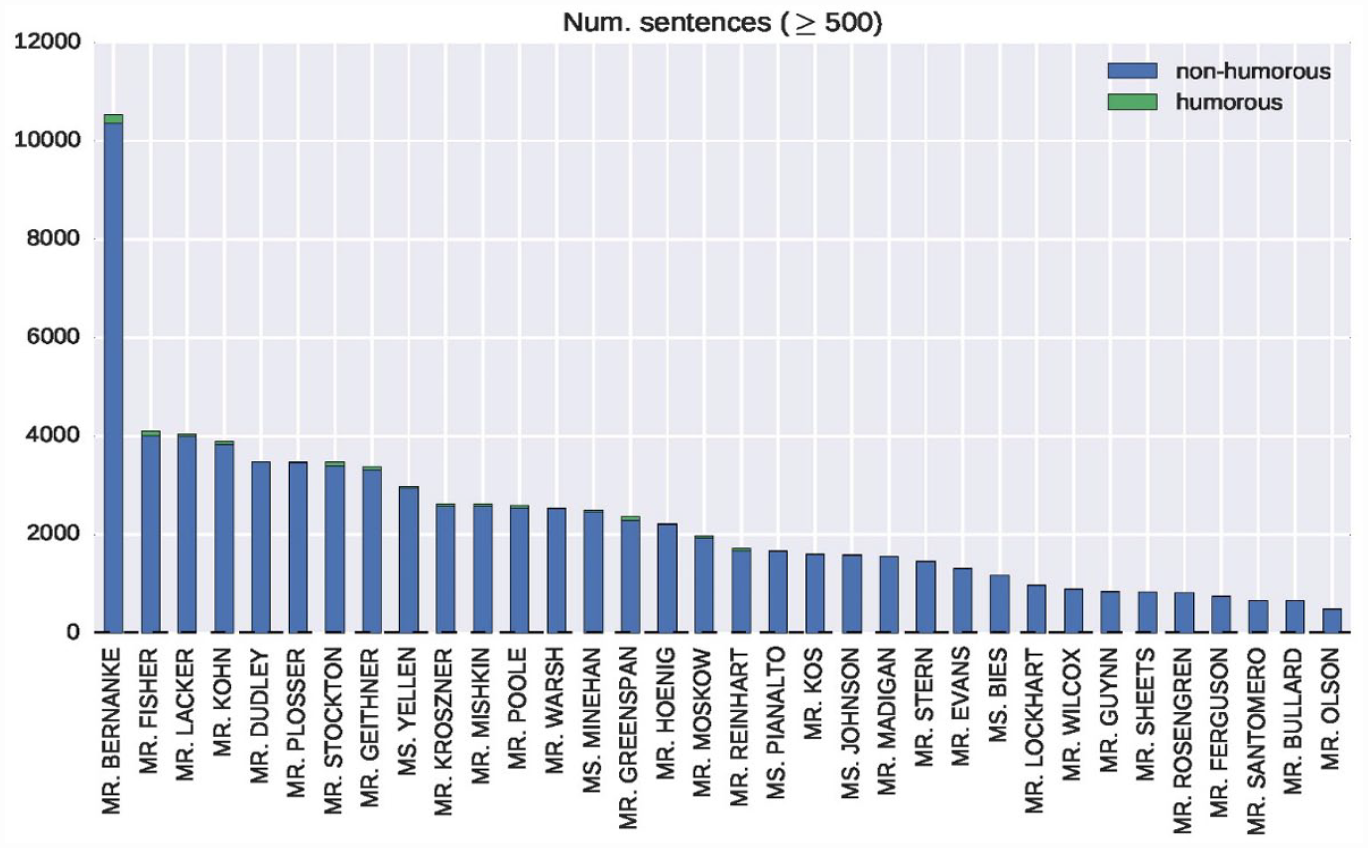

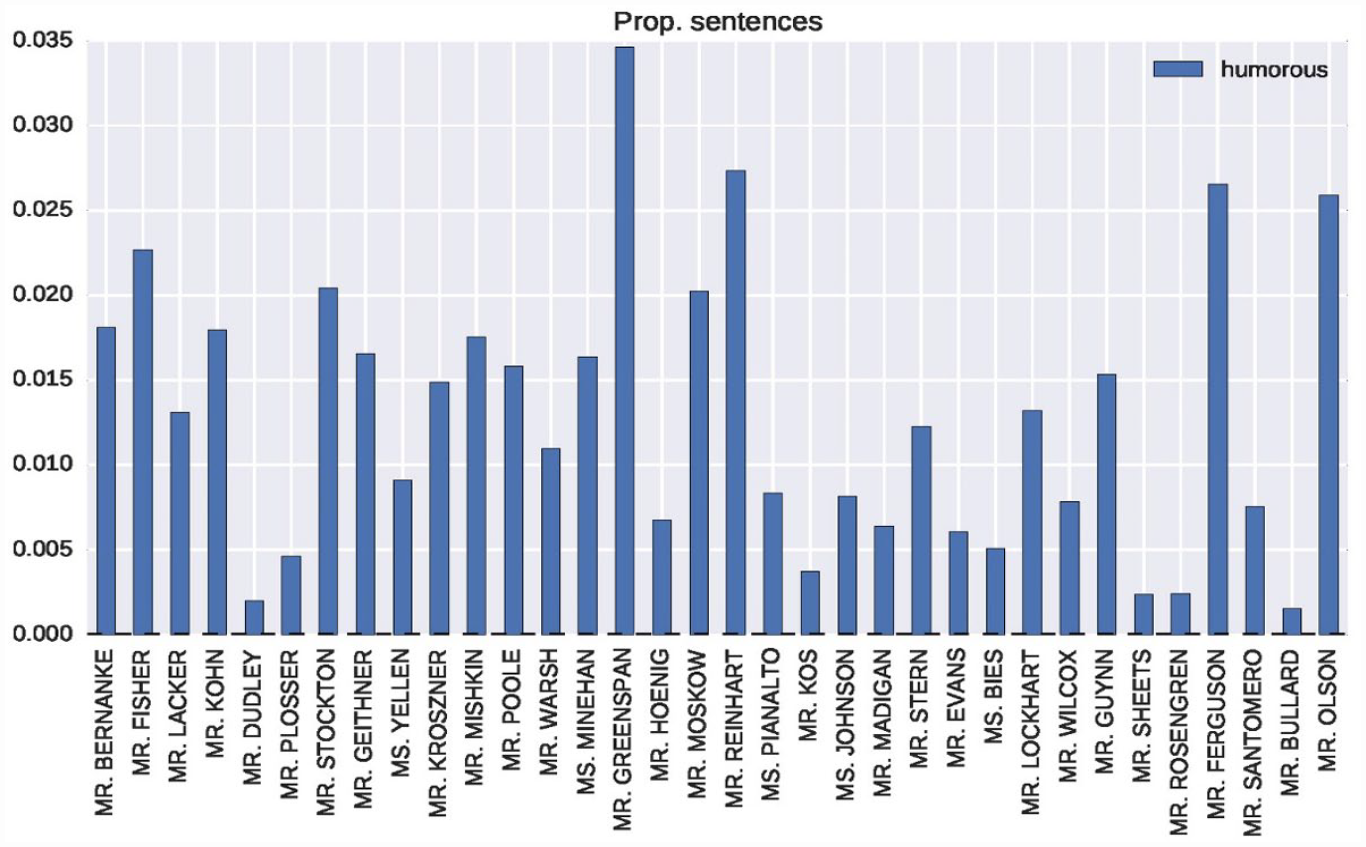

To get a sense of the role of humor in interpersonal dynamics at play in these meetings, Figure 1 shows the number of sentences spoken by each of the individuals who spoke at least 500 sentences, broken down by non-humorous and (barely visible) humorous sentences, sorted by speaker in decreasing order of the total number of sentences spoken across all transcripts. Mr. Bernanke delivered the highest number of sentences, while Mr. Olson spoke the least. Mr. Greenspan’s speaking frequency falls somewhere in the middle; his role as Chair of the FOMC ended in January 2006, which was only 1 year into our dataset. Figure 2 shows the same data as Figure 1, in the same order, but instead displays the proportion of each speaker’s sentences that were humorous (again, for speakers with a total of 500 or more sentences). Figure 2 shows that some speakers are quite humorous, others less so. Mr. Olson, for example, talked the least but had one of the highest proportions of laughter-inducing sentences. Mr. Greenspan had the highest proportion of laughter-inducing sentences, although it is possible that a different trend may have emerged if we had analyzed earlier FOMC transcripts. The year we focused on (2005) was a favorable one for the economy, and it is plausible that Mr. Greenspan’s humorous statements were particularly effective in inducing laughter due to the contrast between his seniority and his levity. Mr. Dudley, by contrast, spoke a great deal (3,482 sentences), yet hardly ever provoked laughter (seven humorous sentences total), although we cannot know whether Mr. Dudley rarely jokes or whether his jokes just fall flat. Overall, Figure 2 illustrates that humor in the FOMC is hardly restricted to one or two class clowns. Many members of the group use humor when they speak; specifically, 19 members induce laughter with 1% or more of their sentences.

Number of sentences spoken by each FOMC member who, in total, spoke at least 500 sentences, 2005 to 2008.

Proportion of sentences that induced laughter (i.e., were humorous) by each FOMC member who spoke at least 500 sentences, 2005 to 2008.

Checking the Face Validity of the Data

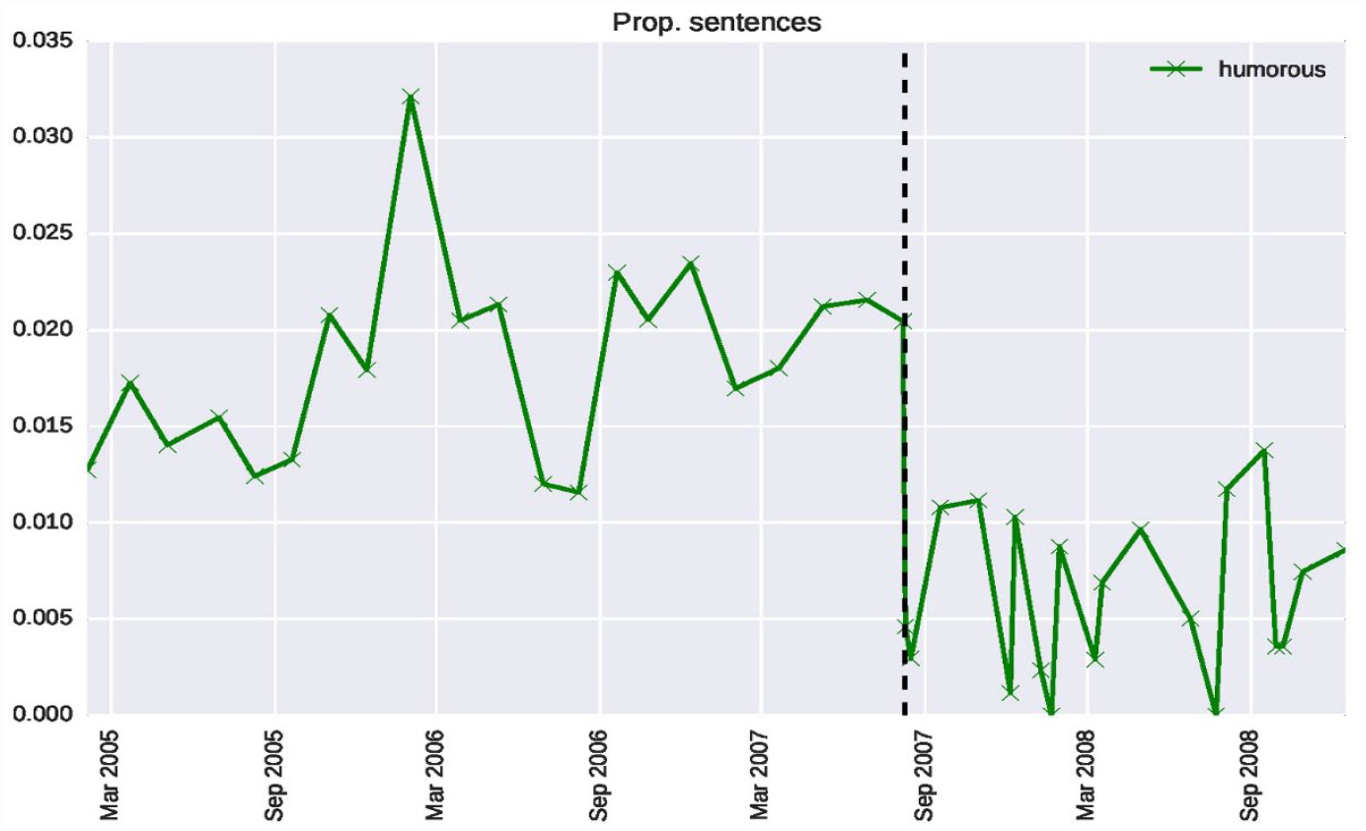

We took two measures to examine the face validity of using laughter annotations in the transcript data to gage the mood of the FOMC. First, as shown in Figure 3, we examined the proportion of humorous sentences over time (see Appendix Figure A3 for the number of humorous sentences per meeting). As we would expect, the financial crisis dramatically lowered the relative amount of humor used in FOMC meetings. In this vein, we examined the correlation between the proportion of humorous sentences and the Real S&P Index (available at a monthly level), a standard benchmark for capturing stock market performance. We collapsed the proportion of humorous sentences per month by computing the mean values for months that featured more than one FOMC meeting. We conducted correlation analysis between the monthly proportion of humorous sentences in FOMC meetings and the Real S&P Index monthly values. As we would expect, the correlation is strong and positive (r = .38), indicating the use of humor in FOMC meetings rises and falls largely in tandem with marketplace conditions, including an immediate drop with the financial crash of 2007.

Proportion of humorous sentences, by FOMC meeting, 2005 to 2008.

Second, we examined the correlation between the proportion of laughter occurring in each FOMC meeting (number of laughter-inducing sentences out of total number of sentences) and the proportions of positive and negative words used in each meeting (see Appendix for details). Although the units of measurement are not identical (i.e., sentence for laughter-inducing variable and word for sentiment variable), by calculating an overall proportion per meeting, we can determine whether uses of humor and positive versus negative sentiment tend to vary (directly or inversely) in tandem (See Appendix Figures A1 and A2, which show that the proportion of positive and negative words changed exactly as we would expect following the financial crash). Results of our analysis showed humorous sentences are positive correlated with positive words (r = .55) and negatively correlated with negative words (r = −.46), providing further support for the validity of our data.

Hypothesis Testing

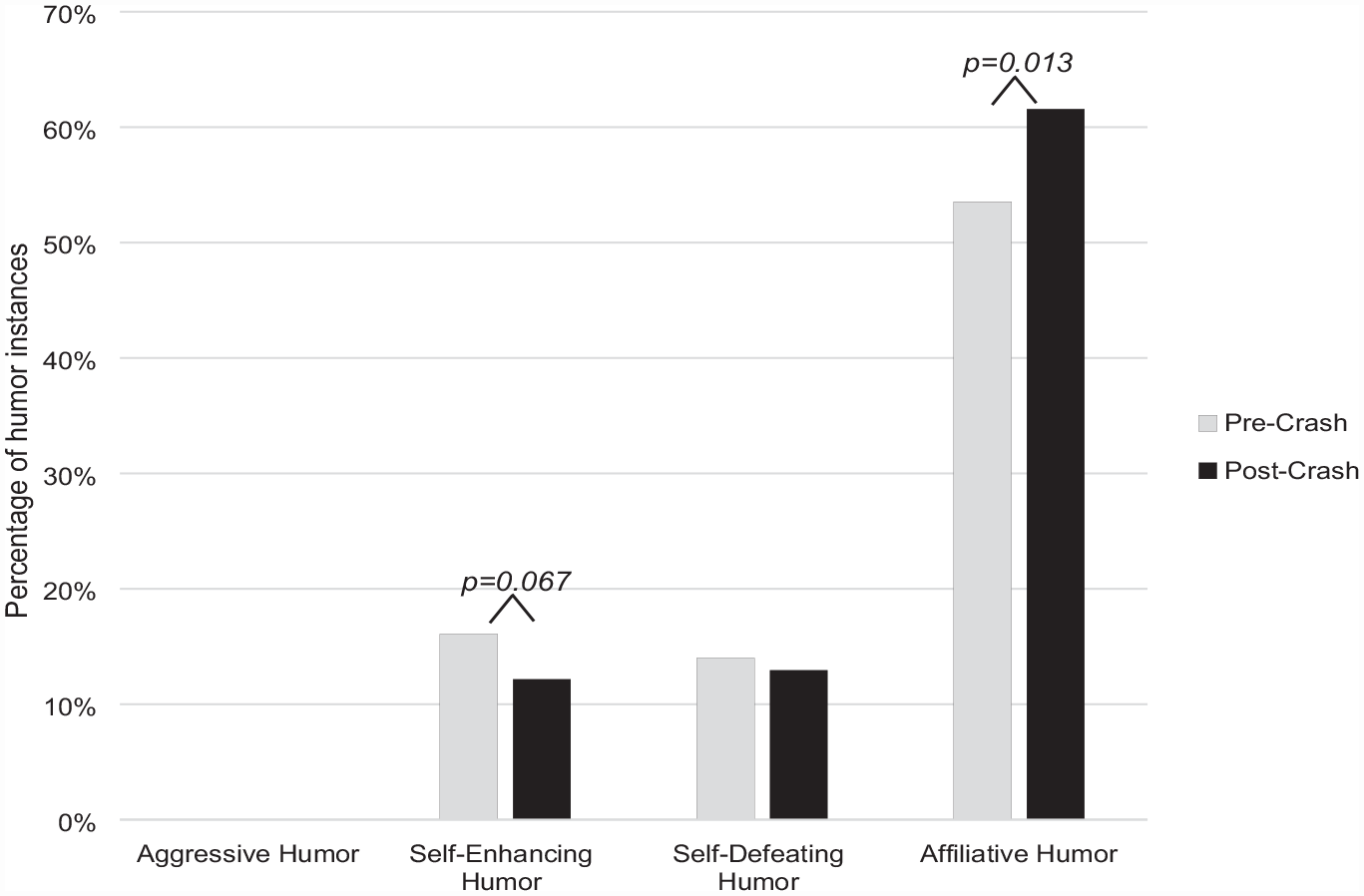

We hypothesized that after the 2007 economic crash, there was an increase in the proportion of affiliative instances of humor (Hypothesis 1), and more specifically, use of playful banter (Hypothesis 2) during FOMC meetings. Figure 4 shows the difference in the use of R. A. Martin et al.’s (2003) broad categories of humor types between the 12 pre-crash meetings versus 13 post-crash meetings. (Again, note the absence of any aggressive humor instances in the FOMC meetings.) The use of self-enhancing humor declined, and in a statistically significant way (p = .067, using t-tests and considering results significant at a 90% or higher confidence interval). By contrast, supporting Hypothesis 1, the relative use of affiliative humor increased significantly (p = .013), from 54% pre-crash, which was already high, to 62% post-crash.

Humor instances by broad categories of humor (R. A. Martin et al., 2003): pre- versus post-economic crash (August 2007).

One example of affiliative humor in action took place in the August 10, 2007 meeting: an emergency conference call convened as the markets were in free-fall. At this very brief meeting, only one statement induced laughter, which was an economic conditions/policy item (specifically in the form of gallows humor): “I think markets are working fine. The quantities just happen to be zero right now in some of them, [laughter] and things are going to hell in a handbasket” (Mr. Lacker).

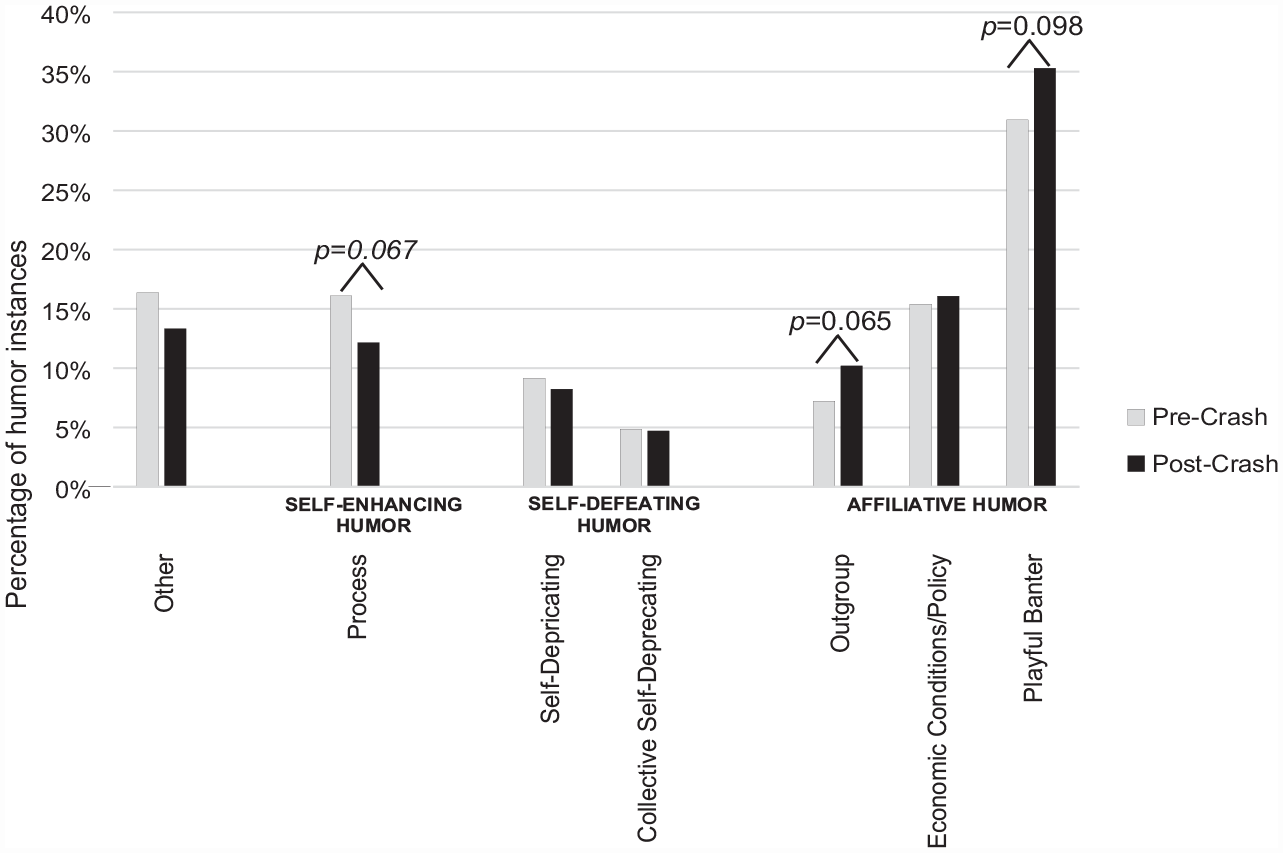

Figure 5 shows the six more fine-grained humor categories (plus other) we identified in the FOMC data, clustered according to R. A. Martin et al.’s (2003) broader categories. The increase in affiliative humor after the 2007 economic crash is reflected in all three types of humor that fall within the affiliative category: outgroup humor, economic conditions/policy humor, and playful banter humor. In support of Hypothesis 2, there is a statistically significant increase in the relative use of playful banter, from 31% to 35% (p = .098). Note that outgroup humor also demonstrates a statistically significant increase (p = .065). Although the economic conditions/policy humor type overall does not show a significant increase (p = .395), its sub-category, gallows humor, does (p = .006), more than doubling from 2% before the crash to over 5% post-crash (see Appendix Figure A4). These results show that, in the face of the crisis, although members of the committee joked and laughed less frequently overall (Figure 3), they increased their relative use of playful banter. For context, as the crisis was unfolding, the Fed took unprecedented actions in cutting rates steeply month after month. Not all members were in agreement as the committee made drastic changes to the federal interest rates throughout 2008. But the members seemed to use playful banter directed at one another as a social lubricant to ease stress in the room, come to compromise, and strengthen the bonds between members. In the transcripts, playful banter appears most often in the form of lighthearted exchanges with ribbing and insult (people’s age, regional rivalries, etc.) and playful compliments (such as how kind or brilliant another member is).

Humor instances by specific types of humor: pre- versus post-economic crash (August 2007).

As an example of how playful banter served as a social lubricant during the crisis, consider the April 30, 2008 FOMC meeting. The tension and disagreement in this meeting are evident even in the transcript, indicating a high level of stress. However, the transcript also makes clear that the group used levity to navigate the crisis. Not only were there isolated instances of playful banter, but there was also a running thread of playful banter comments that built on one another. This banter seemed to create a more relaxed atmosphere, helping to facilitate productive discussions around the complex issues at hand. Ultimately, the group was able to reach an agreement on how to move forward. Early on in the meeting, Frederic Mishkin describes being torn between two policy options being discussed, “alternative B” and “alternative C”: “I’m in a very uncomfortable position because I’m actually sitting exactly on the fence between alternative B and alternative C. As you know, sitting on the fence and having a fence right in that anatomically uncomfortable position is not a good place to be. [Laughter].” [Long discussion of options] “I tend to look at financial markets as being the canary in the coal mine. Though being a New Yorker, I actually have been in a coal mine [laughter] at the Museum of Science and Industry in Chicago. It’s really cool. All of you should go there someday when you go visit Charlie.”

Randall Kroszner replies immediately: “But he has never seen a canary. [Laughter].” To which Mishkin says: “I have seen a canary. But the key is that the canary has not keeled over. In fact, if you look at what’s going on in the financial markets, the concerns in terms of inflation compensation have dissipated somewhat. . ..” After another long statement, Mishkin concludes: So I’m quite comfortable with the language of alternative B. I’m willing to support B. It looks as though that is the consensus, and my view today is that I’m going to go with whatever the consensus is. Thank you very much.

Geithner replies: “Thank you, Mr. Chairman. The transcript says, Mishkin says canary wheezing but hasn’t keeled over. I support alternative B. I think you could frame this as a modest recalibration of policy with a hawkish soft pause.” Bernanke chimes in: “And a wheezing canary. [Laughter].” Although we cannot definitely say that the Committee would not have converged around “alternative B” as quickly or smoothly without humor, it is reasonable to think that the use of playful banter helped ease the tension in the room, allowing the work group to build a sense of affiliation among members, allowing them to operate effectively in response to the crisis.

In summary, results of our analyses supported Hypotheses 1 and 2, indicating that the work group exhibited flexibility in their use of humor, adapting it to the context of the situation. Specifically, they used affiliative humor in general, and playful banter specifically, as a social lubricant to ease tensions and foster comradery during the crisis.

Supplemental Analyses: Examining Potential Factors at Play

The increase in the use of affiliative humor, specifically playful banter, after the financial crash suggests that the FOMC may have evolved its use of humor in response to the crisis. The transcript data from this group are rich enough to allow additional insights into the various factors underpinning the group’s ability to change its use of humor in a more processual manner. We conducted qualitative analysis of the transcripts to explore (1) what role leadership (i.e., the FOMC Chair) might play in fostering the group’s humor culture; (2) whether membership matters (i.e., whether members seem less comfortable uttering humorous sentences depending on their specific role, their time on the committee, and/or when there has recently been turnover in membership); (3) exactly what role self-enhancing humor (specifically process-oriented humor) played before the crisis and how it gave way to affiliative humor after the crisis; and (4) what role the meeting format (in-person vs. conference call) might play.

Leadership That Fosters a Culture of Individual-Targeted Humor

Results of our qualitative analysis reveal that the FOMC Chair—first Greenspan and then Bernanke—not only infused the committee meetings with humor but did so in a way that knitted the group together. Both Chairs relied strongly on playful banter, with 32% of Greenspan’s and 43% of Bernanke’s humorous sentences coded as playful banter. They also seemed to be deliberate in directing their humor toward individual members of the group, and importantly, this banter transcended job titles and hierarchy levels. For example, in the August 7, 2007 meeting (right before the crash), Bernanke opens the meeting with a humorous remark that utilized playful banter: “Good morning, everybody. We start off today with some welcomes and farewells. I would first like to welcome Eric Rosengren, the new President of the Federal Reserve Bank of Boston. MR. ROSENGREN. Thank you. CHAIRMAN BERNANKE. I have known Eric for about twenty years. We used to be squash partners. I won’t say who won. We know who wins now. [Laughter]”

As another example, in the first in-person meeting following the crash (9/18/07), Bernanke used process-oriented humor, but directed it toward another member of the group: “Let’s put president Poole between us and the coffee break. President Poole. [Laughter]”

Although we cannot definitely say whether the Chairs’ (a) frequent use of playful banter and (b) practice of directing their humor (across humor types) toward specific individuals were strategic attempts to foster a culture of humor or simply products of their personalities, their use of humor seems to have helped foster a close-knit work group.

Stability and Inclusivity Across Roles, Seniority, and Changes in Membership

We carefully analyzed all the transcripts, looking for any evidence that a member’s role on the committee (i.e., public Senate-confirmed appointees vs. private Bank Presidents; see Appendix), their tenure on the committee, and/or recent turnover on the committee could predict the use of humor. This type of analysis could also include examining factors such as members’ backgrounds, levels of expertise, and history of prior work with other members. In the case of the FOMC, however, investigating these factors was deemed unnecessary, as all 19 members have exemplary resumes, expertise in fiscal policy, and a history of working with one another (even before joining the FOMC).

Results of our analysis showed that there was no relationship between role, seniority, or membership turnover and the use of humor. Although some members are generally more humorous (e.g., Mr. Olson) than others (e.g., Mr. Dudley), there were no differences in the committee members’ use of humor based on their role or seniority. The Chair’s use of individually-directed humor, as well as the members’ extensive history of working together even before joining the FOMC, likely helps explain why members across roles and seniority levels feel comfortable engaging in humor. We even found several cases where members used humor in their first meeting on the committee. For instance, in the September 20, 2006 meeting, Bernanke welcomes Frederic Mishkin by saying: “We’d like to welcome new Governor Rick Mishkin. Welcome, Rick. Rick attended FOMC meetings from 94 to 97 when he was on the New York Fed staff, but this is the first time he has gotten to sit at the big table. [Laughter]”

Despite it being his first time at the “big table,” Mishkin appears to feel welcome to join in the fun, saying: “I wanted to sit right back there, but they wouldn’t let me. [Laughter]” And finally, we found no evidence that changes in membership affected the members’ humor proclivities. One possible explanation for our finding is that, although 90 unique individuals spoke at least once across the course of these 41 meetings, the core group of participants remains remarkably stable, with very little turnover. Consider, for example, the September 18, 2007 meeting—the first in-person meeting following the financial crash. Of the 23 people who spoke during this meeting, 19 (83%) had been participating in FOMC meetings for at least a year, and 14 (61%) for at least 2 years. This consistency in membership may be a contributing factor to the Chair’s ability to foster a culture of humor and inclusivity that enables even newcomers to feel comfortable adding levity.

Flexibility in Letting Go of Old Humor Types

Results of our main analysis showed that the proportion of affiliative humor in general and playful banter specifically increased following the financial crisis, thus indicating a shift toward these types of humor and away from other types. Specifically, Figures 4 and 5 show a sharp decline in self-enhancing (specifically process-oriented) humor. Our qualitative analysis suggests that the growing concern for the global financial situation may have led members to refrain from making self-enhancing jokes about the intricacies of their jobs. Members may have considered making jokes about their responsibilities inappropriate when they were charged with keeping the financial boat afloat during a difficult time, especially given the high profile and public nature of the FOMC meetings. It is also possible that members understood that process-related humor would not help them build the kind of intragroup social capital they needed to work effectively together in the aftermath of the crisis. To further explore the role process-oriented humor played in the FOMC both before and after the financial crash, we conducted a quantitative analysis of process-oriented references (both with and without laughter) over time.

Our qualitative analysis had revealed that process-oriented conversations most often concerned the wording of the Fed’s statement (see Appendix for an example), and so we identified a series of keywords, including statement, wording, language, paragraph, alternative A, alternative B, alternative C, alternative D. Using the same method employed in our main analyses, we calculated the proportion of sentences in each FOMC meeting that included at least one of these statement-related words. To produce a graph of these proportions over time, we averaged the percentages by month. Results showed that the proportion of humorous sentences that included these keywords plummeted post-crash. Specifically, sentences containing paragraphs and alternatives A-D decreased post-crash (see Appendix Figure A5).

One possible explanation for our findings is that, when marketplace conditions were strong, the committee had the luxury of fixating on minor issues such as discussing the wording of the Fed’s statement. As the FOMC maintained a consistent approach of raising rates by 0.25 at each meeting between 2004 and 2006 (before the crash), it is possible that their attention focused on the public presentation of these numbers, rather than substantive conversations about what they ought to do with the rates. Once global financial indicators began turning down, however, the committee was dealing with larger, graver concerns, such as cutting the rate (starting in September 2007). Thus, although discussions about the Fed’s statement were still important, the committee had to prioritize the careful selection of words (e.g., “materially” vs. “appreciably” vs. “significantly” in a debate on how much financial risks had increased), as they were likely overshadowed by more substantive concerns about the rate cuts.

In short, our findings suggests that process-oriented humor—and process-oriented discussion more broadly—served the FOMC well during favorable economic conditions before the financial crisis, but less so post-crisis. Crucially, after the crash, the committee members quickly shifted toward affiliative forms of humor and away from process-oriented humor.

The Value of In-Person Meetings

Finally, results of our exploratory analyses reveal that the nine conference call meetings had lower proportions of laughter compared to in-person meetings. All nine conference call meetings in the data were held after the financial crash, although they were interspersed with in-person (and more humor-filled) meetings. Of particular note, the two meetings that immediately followed the financial crash were conducted via conference call. As noted above, the first of these meetings (August 10, 2007) had only one instance of laugher, prompted by Mr. Lacker’s gallows humor (“I think markets are working fine. The quantities just happen to be zero right now in some of them, [laughter] and things are going to hell in a handbasket”). This single instance of humor accounted for 0.5% of the sentences in that short meeting. The second conference call meeting (August 16, 2007) had two instances of laughter, both prompted by Mr. Kohn, and that together accounted for 0.3% of the sentences in the meeting. However, the subsequent two meetings (September 18 and October 31—both in person), each boasted a 1.1% humor rate. Just as importantly, each of those two meetings showcased multiple members volleying humor, with 65% and 71% of the participants, respectively, saying at least one thing that prompted laughter. Our findings align with prior research indicating that in-person meetings are generally better than conference calls in terms of participation, engagement, and satisfaction (Reed & Allen, 2021, 2022).

In sum, our exploratory qualitative analyses yielded four interrelated findings: (1) the Chair’s use of humor was extremely important for setting the tenor and tone of the group’s use of humor; (2) roles, seniority, or turnover had no effect on the use of humor; (3) although process-oriented humor served the FOMC well in the good times before the financial crisis, the group was able to shift away from this humor type after the crash; and (4) laughter is less likely to occur in conference calls than in person. Together, our findings suggest that, in order for a powerful work group to have the capacity to evolve its use of humor in response to a crisis, they must have leadership that sets a strong culture of humor even across changes in leadership, a stable culture of inclusion and group confidence, and yet the agility needed not only to adopt a new type of humor (e.g., playful banter) but also to let go of the main type of humor on which they previously relied (e.g., process-oriented humor). Further, as many individuals who have experienced Zoom fatigue can attest, in-person meetings tend to be more conducive to humor and laughter than conference calls.

Discussion

The forgoing results demonstrate that humor behaviors in established work groups can change in response to a crisis, which in turn can impact group processes such as leadership and collaboration. In the case of the FOMC, humor behaviors became more affiliative and more supportive of group dynamics after the 2007 financial crisis. Our findings have important theoretical and practical implications.

Theoretical Implications

Our study offers a new lens through which to view humor in work groups. Specifically, this study contributed to the literature by documenting the capacity of the FOMC as an important and high-stakes work group to use humor to foster healthy group dynamics under normal circumstances, as well as its ability to adapt its use of humor in times of crisis. This finding amplifies the importance of humor as a flexible and dynamic tool that healthy work groups can use to strengthen group cohesion in good times and in bad. Studying the FOMC has value in and of itself because this group’s decisions affect the national and global economy. The FOMC is widely regarded as one of the most important work groups in the world, and our study showcases its capacity to maintain highly functional interpersonal dynamics, even during difficult periods.

Second, our findings suggest that a group that, by definition, is on the outside edge of being a small group, can still experience small group dynamics as they pertain to humor. Specifically, the types of humor identified and the way in which they are deployed by members of the FOMC are consistent with previous research on smaller groups (Lehmann-Willenbrock & Allen, 2014). Further, given the nature of the FOMC’s internal dynamics (as discussed in our supplementary analyses section above) and the tasks for which they are responsible, the FOMC serves as a suitable example of a small work group. Thus, our findings have implications for future research on the use of humor in small-to-medium-sized work groups.

Third, our findings indicate that crisis events that intersect with group tasks can impact group member interaction. Although our study is of a specific group and crisis, it demonstrates the kind of equilibrium shift that many work groups experienced due to the COVID-19 pandemic. Specifically, the financial crisis of 2007 was a significant equilibrium shift for the FOMC, which led to changes in its role in the economic affairs of the United States and beyond, as well as changes in the ways members interacted with each other, as demonstrated by the use of humor in our study. With COVID-19, an even larger equilibrium shift, many groups experienced a monumental shift in how their members interact with one another (Reed & Allen, 2021), including a transition from physical face-to-face meetings to more virtual interaction. The implication of our study is that, when major crises occur, groups (at least healthy groups) adapt and change how they operate, rather than disbanding.

Practical Implications

Our results have meaningful practical implications for leaders and followers in groups, particular when responding to major crises that impact their operations. First, group leaders should utilize humor, as it fosters positive interaction between group members under the right conditions. Specifically, leaders should deploy positive, affiliative humor, rather than put-down humor. As evidenced in our supplementary analyses, if a leader can foster a culture of affiliative humor through personally-directed banter, it can help stabilize the group’s dynamics during changes in membership as well as in times of major crises. Second, followers in groups should not wait for the leader to initiate a joke that can foster positive feelings or trust. Instead, they should take the initiative and engage in affiliative humor themselves. In other words, leaders and followers can both benefit from the proper use of humor, which facilitates effective team interaction.

Third, group leaders should be mindful of their group’s response to crises. It is likely that not all groups will respond to crises in the same way, and our findings represent just one potential pattern that could emerge following a crisis. When a leader realizes they are in the midst of a crisis, they should closely monitor how group members are interacting with one another, such as any positive or negative behaviors that appear to be on the rise. Our recommendation is to engage in positive humor, although leaders may also want to seek out additional research and practical advice on how to manage the group through the crisis with regard to other behaviors beyond humor.

Limitations

Our study has limitations. First, the FOMC is likely not representative of all small-to-medium-sized work groups, as it is a highly professionalized group comprised of especially elite and powerful individuals (and 19 in number). Compare the FOMC, for example, to the work group of city leaders in Fargo, North Dakota in the study by Beck et al. (2012), where they examined how the leaders’ naïve theories influenced their response to the record flood of 2009, yielding varying degrees of effectiveness. While the FOMC is able to pivot in its use of humor during times of crisis, this does not necessarily imply that all work groups are able to do so. Yet based on past studies of the use of positive and negative forms of humor, we expect work groups (especially small ones) to be able to shift toward affiliative humor during times of crisis.

Second, the financial crisis that sets the stage for our analysis here may not be representative of the typical crises that work groups face. However, previous research on healthy work groups in crisis fields such as crime scene investigations (Vivona, 2014) and nursing (Schippers et al., 2014), we expect that most healthy work groups are able to shift in the type of humor employed in times of crisis, leaning away from the type of humor that served them well in the pre-crisis period and toward a more appropriate form of humor (likely “affiliative”) that better serves them in new conditions.

Third, the smooth transitions in leadership observed within the FOMC may not necessarily apply to other small work groups, specifically when a new leader has no prior experience with the group. The shift in FOMC Chair from Bernanke to Yellen in 2014 does not seem to have been disruptive, likely because Yellen had been on the FOMC Board for many years. Similarly, when President Trump nominated Jerome Powell to succeed Yellen as Chair in 2018, Powell had already served on the Board for 5 years (nominated to the FOMC by President Obama in 2012), and the transition from Yellen to Powell seems to have gone relatively smoothly as well. Thus, given the context-specific nature of our findings, they may not necessarily generalize to other situations or groups.

Future Directions and Conclusion

As the world faces complex problems that require collaboration between experts and across domains, effective communication in work groups becomes increasingly crucial. Our study points to humor as an important and dynamic tool in the small work group’s communication toolbox. We hope that our findings can serve as a foundation for further research on how humor can be used in various domains, such as economics, health, politics, and science, to enhance the productivity, good will, and cohesiveness of work groups. We envision many potential avenues of future study building from our work, but two in particular stand out.

First, future research could extend our approach to other small-to-medium sized work groups of similar member turnover rate and influence, but in different domains, such as Congressional committees, city councils, and boards of trustees. This line of research would help identify the precise ways in which—and conditions under which—humor can fuel healthy collaborative experiences that maximize group efficiency to benefit society. Ideally such studies would utilize video recordings of group interactions rather than relying solely on written transcripts as we did in this study. This approach would enable researchers to observe non-verbal cues of and in responses to humor. Additionally, such studies could explore the importance of leadership in establishing a culture of positive humor. For example, it would be valuable to investigate work groups facing crises that resemble the FOMC case we examined, but with leaders who deter rather than foster humor. Such research could help determine whether work groups are less resilient in handling crises without the use of humor. Further investigation is also needed to explore the potential harm to group function that might result from a shift toward more negative emotional behaviors following a crisis.

Second, future work could use experimental methods to identify the specific effects, both positive and negative, of different types of humor used in varying scenarios. Based on our findings, we anticipate some types of humor (e.g., process oriented) do not land as well as others (e.g., gallows humor) during times of crisis. Experimental evidence would help inform work groups about specific strategies for utilizing humor as a tool for navigating crises effectively.

Footnotes

Appendix

Acknowledgements

We are grateful to Stephanie Bonham, Joseph Broad, Shayla Griffin, Jeremy Kirshner, Lei Otsuka, and especially Summer Mielke and Hannah Dillman Murnane for exceptional research assistance. We also thank Bret Bradley and anonymous reviewers for expert feedback on earlier drafts, and Lyn van Swol and Chen-Ting (Tammy) Chang for expert editing. Finally, we are indebted to John Wilkerson, Anne Washington, and the larger Text as Data community for inspiring this project.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.