Abstract

CEO power seems to be a double-edged sword: Agency-theoretic research views CEO power as ultimately detrimental to the firm, whereas the strategic leadership literature highlights the instrumental role of CEO power in getting things done. These competing perspectives motivate a lively debate in the organizational literature on the performance consequences of CEO power. To extend this line of inquiry, we examine the CEO power–firm performance relation during industry turmoil and delve into the role of three critical situational exigencies—managerial discretion, market competitiveness, and technological innovativeness. Predictions are tested on publicly traded Standard & Poor’s (S&P) 1500 firms in the United States using archival data over 20 years. Implications for further research and practice are discussed.

Power gives leaders the capacity to translate dreams into reality and sustain it. Power tends to corrupt, and absolute power corrupts absolutely.

Introduction

The topic of CEO power—defined as the concentration of decision-making authority in the chief executive (Finkelstein, 1992)—is of tremendous interest to organizational scholars and manager practitioners (Abernethy, Kuang, & Qin, 2015; Krause, Priem, & Love, 2015). It is widely accepted that powerful CEOs influence firm performance, but the nature and strength of the power–performance relation continues to be an enigma in both the academic literature and the popular media. Confusion about the performance consequences of CEO power stems from divergent perspectives that can be found in academic and popular discourse. Consistent with the first quote above, the strategic leadership literature considers power as a useful tool for the CEO to get things done (Cannella & Monroe, 1997), whereas, and in accordance with the second quote above, agency theory views CEO power as something that potentially needs to be limited and controlled (Jensen, 1993). The seemingly puzzling link between CEO power and firm performance becomes more muddled when firms are confronted with unpredictable events so that empirical research and anecdotal evidence can be marshaled in favor of and against the need for powerful CEOs in such situations (Boyd, 1995; Eisenhardt & Bourgeois, 1988). A clearer understanding of the anticipated effects of CEO power may therefore require consideration of critical exigencies pertaining to the fit between CEO power and other constructs of interest.

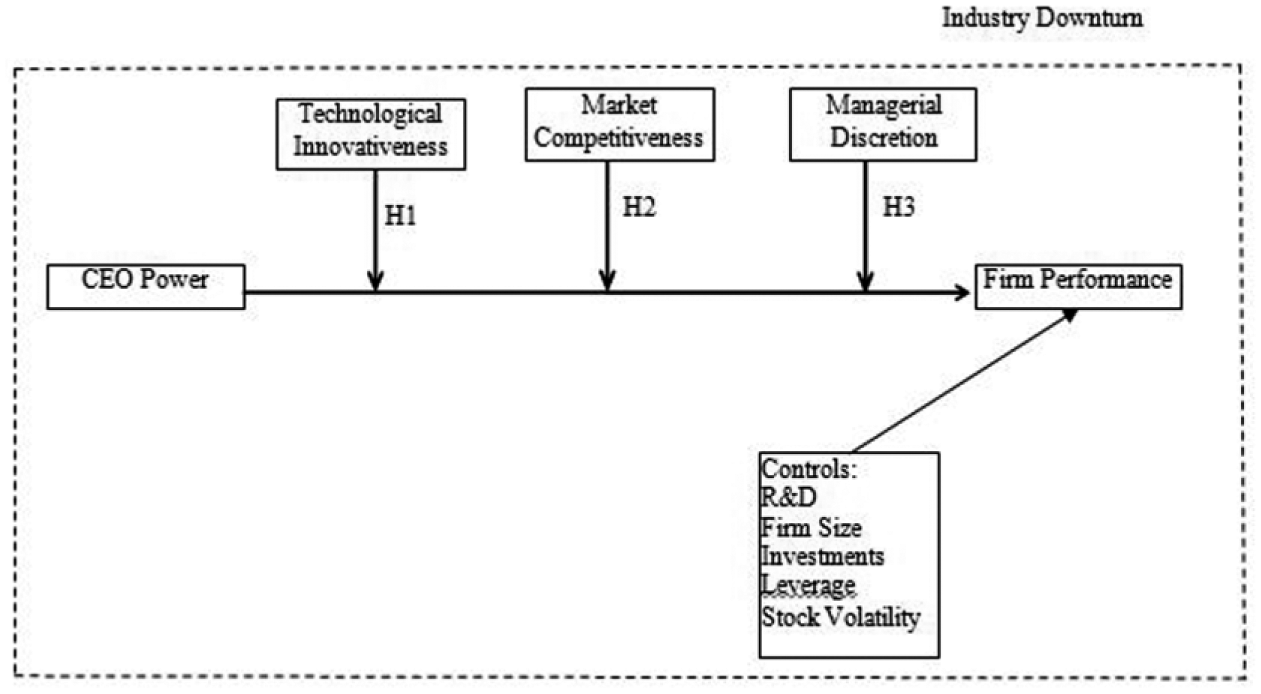

One of the major functions of top executives is to manage the organization’s interface with its environment (Hambrick, 1989). It is thus important to explore how the context in which CEOs operate interacts with executive power to affect organizational outcomes. Indeed, several researchers argue that executive power needs to be properly aligned with situational exigencies to reap its full potential (Haynes & Hillman, 2010). Based on upper echelon research (Finkelstein, Hambrick, & Cannella, 2009), we examine the role of three contingencies—technological innovativeness, market competition, and managerial discretion—to provide a better understanding of the anticipated performance consequences of CEO power during times of industry turmoil. Figure 1 presents our research model.

Research model.

In addressing this research model, we seek to make four specific contributions to the literature. First, as a major theoretical contribution, we advance research on the power–performance relation by integrating three theoretically meaningful contingencies in the executive power nomological net (Adams, Almeida, & Ferreira, 2005). We argue theoretically and validate empirically the circumstances under which executive power can have favorable or adverse impact on firm performance. As knowledge around CEO power has expanded, there has been a growing interest in the interplay between CEO power and other organizational and industrial characteristics (Short, Payne, & Ketchen, 2008). Thus, we provide much-needed insights into the orchestrating themes and integrative mechanisms that impinge on executive power.

Our second contribution lies in the use of exogenous industry “shocks,” defined as significant industry-wide downturns, to investigate the performance impact of CEO power. Industry downturns are outside the immediate control of any one firm or CEO and combining these with firm-fixed effects allows us to draw richer inferences related to the impact of CEO power on firm performance. We thus contribute novel insights into the ongoing debate about the performance implications of CEO power (Adams et al., 2005; Daily & Johnson, 1997).

Our third contribution lies in our focus on how organizations cope with turbulent events that create high levels of uncertainty for top management and are also potential threats to the viability of the organization. Prior research suggests that top management effectiveness differs under varying circumstances (Patel & Cooper, 2014). Yet, upper echelon researchers have typically concentrated on the normal course of a firm’s business and not given adequate attention to firms in crisis situations (Mellahi & Wilkinson, 2004). This is surprising because, sooner or later, crisis situations are going to confront almost every firm. Thus, it is essential to develop a more in-depth understanding of firms operating in difficult situations, as we do in this study.

The fourth contribution relates to the external validity—that is, generalizability—of the power–performance relation. Prior work usually focuses on one or two industries, which limits generalizability and can lead to conflicting results based on the firms or time frame chosen. For example, several studies focus on computer-related industries and find conflicting results (e.g., Dowell, Shackell, & Stuart, 2011; Eisenhardt & Bourgeois, 1988; Haleblian & Finkelstein, 1993). Notably, we examine more than 2,000 firms and identify 30 industries experiencing a total of 60 downturns over almost a 20-year period, which we believe strengthens confidence in the external validity of the findings we report.

Theory and Hypotheses

There is intense fascination with CEOs in modern society. They are prominently featured in the press, with many achieving celebrity status (Ketchen, Adams, & Shook, 2008). Researchers from myriad theoretical backgrounds attribute fortunes and trajectories of firms to the actions (or inactions) of their CEO (Finkelstein et al., 2009). The general consensus is that CEOs—for good or for bad—greatly influence what happens to their firms, in part because of the unique position they occupy at the apex of the organization (Hambrick, 2007).

Originating in the upper echelon literature, CEO power is a multifaceted construct at the core of which is the “idea of overcoming resistance” in making decisions and taking strategic actions (Pfeffer, 1997, p. 138). As Adams et al. (2005) note, CEO power can be defined as the ability of the top executive to consistently influence key decisions in their firms, despite potential opposition from others inside and outside the firm. Powerful CEOs are able to make unilateral rapid decisions without the need to build consensus and get buy-in from middle managers or rank-and-file employees (Harris & Helfat, 1998). CEOs may also be internally motivated to lead their organizations in genuinely transformational ways. Thus, superior value is likely to be created for the organization when the CEO exercises appropriate authority with unambiguous and unchallenged decision-making responsibility (Donaldson & Davis, 1991). Accordingly, there is some evidence to show that CEO power has a positive influence on firm performance (Finkelstein & D’Aveni, 1994).

However, some studies raise doubts about the potential benefits of CEO power. Researchers caution that powerful CEOs may not receive candid advice from directors and senior executives (Greve & Mitsuhashi, 2007) and may also be less willing to accept suggestions and inputs from others because of exaggerated self-opinion (Magee, Gruenfeld, Keltner, & Galinsky, 2005). Agency theory, with its emphasis on the divergent interests of management and owners, suggests that too much power allows the CEO to pursue an agenda that may be against the best interests of shareholders (Dalton, Daily, Ellstrand, & Johnson, 1998; Finkelstein & D’Aveni, 1994). The contention that CEO power may not translate into positive performance benefits is an unnerving one for managers who prefer greater power and justify it on the grounds that they are good stewards of corporate assets (Davis, Schoorman, & Donaldson, 1997).

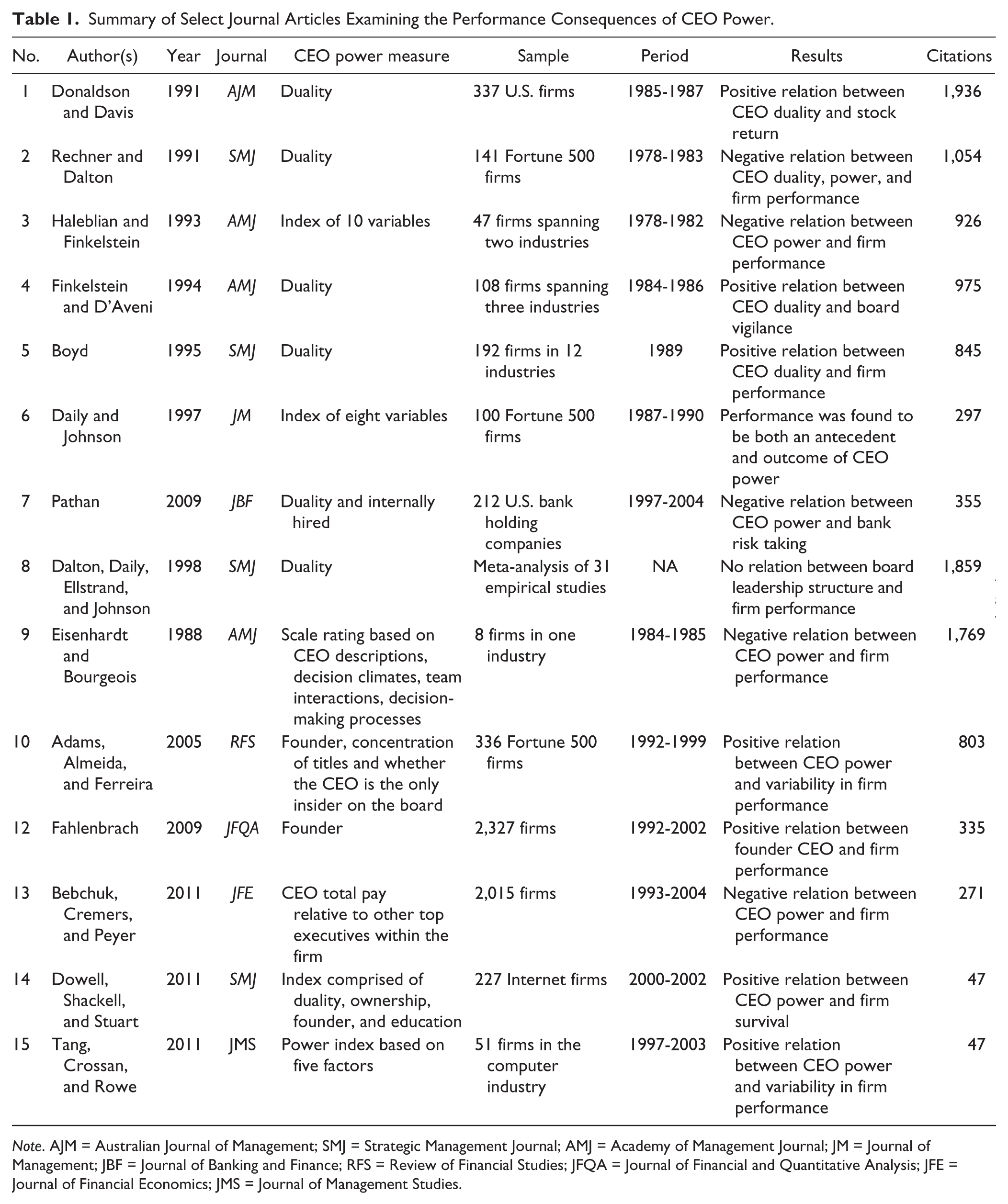

Table 1 presents summary information on selected journal articles examining the performance consequences of CEO power. There seems to be conflicting evidence regarding the impact of CEO power on firm performance with several articles finding a positive impact, some finding a negative impact, and yet others finding no impact. Such disparate findings may result from articles covering a relatively small number of firms or industries, or a relatively short time period, or a relatively narrow definition of CEO power. Consequently, further more in-depth efforts are needed to gain a solid grasp on the factors and processes that translate CEO power into superior (or weaker) firm performance.

Summary of Select Journal Articles Examining the Performance Consequences of CEO Power.

Note. AJM = Australian Journal of Management; SMJ = Strategic Management Journal; AMJ = Academy of Management Journal; JM = Journal of Management; JBF = Journal of Banking and Finance; RFS = Review of Financial Studies; JFQA = Journal of Financial and Quantitative Analysis; JFE = Journal of Financial Economics; JMS = Journal of Management Studies.

We posit that although the costs of having a powerful CEO may be counterbalanced by the associated benefits during the normal course of business, having a powerful CEO could be especially detrimental for firms in crisis situations. Ever since Max Weber famously discussed that crises create an increased opportunity for totalitarian leaders to establish themselves, several researchers have recognized that crisis situations provide fertile grounds for all-powerful leadership (Bligh, Kohles, & Meindl, 2004). Nominally referred to as the “centralization thesis” (Pfeffer, 1978), this stream of research suggests that under conditions of crisis, leadership tends to become concentrated. Centralization of decision making in powerful leaders during crisis occurs for various reasons, such as communicating the legitimacy of managerial control to key stakeholders, enabling quick and decisive decision making, and to delink lower level members from responsibility or action in case adaptive strategies fail (Dutton, 1986).

Yet, navigating crises requires thoughtful consideration of various alternatives, which is facilitated by sharing power among senior executives, rather than being vested in one top executive (Haleblian & Finkelstein, 1993). Prior research suggests that when power is distributed unevenly, fewer solutions and alternatives are generated to the problems at hand (Dewett, 2004). Pitcher and Smith (2001) contend that centralization of power in the CEO reduces heterogeneity of ideas during executive meetings, which leads to poor strategic choices. Powerful CEOs are more likely to engage in uninformed or excessive risk taking, grandiose initiatives, and intimidating acts targeted toward other stakeholders (Hayward & Hambrick, 1997), which can encourage extreme decisions. Organizations in crises need a steadying influence at the helm, which is more likely to come from egalitarian CEOs who exchange ideas and thoughts equitably with other executives (Peterson, Smith, Martorana, & Owens, 2003). Moreover, to the extent that information is more uncertain and noisy during crisis situations, a more decentralized decision-making process tends to produce better outcomes (Sah & Stiglitz, 1986). For these reasons, it is possible that the impact of powerful CEOs may be most adverse during times of crisis such as when there is industry turmoil. Industry downturns are turbulent events for any organization as they are outside the immediate control of any one firm or executive. CEOs who are able to motivate various organizational stakeholders to work together toward common goals and contribute to the well-being of the firm during such industry-wide crisis situations are likely to be rewarded and facilitated by shareholders and other stakeholder groups (Dalton et al., 1998).

Although the above logic points to a contingent association between CEO power and firm performance (CEO power will have a more negative effect on performance during industry downturns), greater insights into the power–performance relation will be gained by considering appropriate “fit” among multiple factors (Delery & Doty, 1996). Accordingly, we posit that in certain situations, the adverse effects of CEO power on firm performance will be alleviated (or exacerbated) during industry downturns. Our approach enables us to investigate the integrative mechanisms that ensure complementarity among various aspects of the situation and provides simultaneous, joint consideration of multiple situational characteristics.

Specifically, we posit that during industry downturns, the impact of a CEO’s power is likely influenced by organizational innovativeness, market competition, and the discretion afforded to the CEO. Thus, we focus on three specific settings in which we expect the quality of a CEO’s decisions to be more consequential for firms experiencing industry downturns. The first is when the firm’s strategy is innovation-driven, the second is when the market is competitive, and the third is when the industry is characterized by managerial discretion. In these contexts, given the burden of an industry downturn, we expect the quality of the CEO’s decision making to be critical and the impact of CEO power on firm performance to be greater. We elaborate on these contingencies below.

Firm Innovativeness, Competitive Markets, and Managerial Discretion

We posit that the actions of CEOs are especially likely to affect firm outcomes in innovative firms. CEOs generally have rich unparalleled firm-specific knowledge, which may be particularly important for innovative firms because of their sensitive information base (Brickley, Linck, & Coles, 1999). Specific information is detailed information that is costly to transfer, and the literature suggests innovative firms have more specific information unknown to outsiders (Graham & Harvey, 2001). In addition, CEOs of innovative firms often fail to see reasonable threats in their competitive environments until too late, isolating themselves from the advice of others and becoming myopic in their views (Ranft & O’Neill, 2001). Christensen (1997) argues that innovative firms are unable to sustain their superior performance because they are occupied with meeting the needs and wants of their customers. We believe that this effect is potentially compounded when the CEO has greater power. For innovative firms facing an industry-wide downturn, the benefits of a dispersed power base may become vital. Outside directors may be able to provide expertise and experience that complements the CEO’s knowledge of the firm, which can be especially important during downturns. This leads to the following prediction:

Several studies have shown that conversion of top management attributes into superior firm performance is embedded in the market environment. We believe the extent to which a market is concentrated or competitive will influence the effect of CEO power on firm performance. This is because the CEO’s ability to flaunt power may change with the number of players in the market. In concentrated markets, only a few firms hold a majority of the market share, whereas fragmented (i.e., competitive) markets have a large number of players (Hirschman, 1964). Aldrich (1979) proposes that strategic decisions are made more frequently in competitive environments relative to ones that are more concentrated. Although CEO power enables quicker decisions, it does not necessarily follow that CEO power enables better quality decisions. In competitive markets, the consequences of managerial decisions are more severe than in concentrated markets as there is less room for error when rivals are in constant struggle for customers and profits. For example, product differentiation or barriers to entry insulate a firm in concentrated industries relative to competitive industries, enabling firms to be somewhat shielded from poor decisions. To the extent that decision making is sub-optimal in such situations, we offer the following prediction:

Upper echelon researchers generally assume that top executives greatly affect what takes place in their firms (Hambrick, 1989), a position challenged by those (e.g., population ecologists or neo-institutionalists) who argue that management is severely constrained by external forces (Hannan & Freeman, 1977). To reconcile these conflicting perspectives, researchers have identified an important moderator, namely, managerial discretion, defined as a manager’s latitude of action, which may account for why top executives matter more in some situations than in others (Hambrick, 2007). When top executives have greater discretion, their impact on firm decisions and outcomes is stronger (Finkelstein et al., 2009). Managerial discretion might then be an important moderator of the relation between CEO power and firm value.

Discretion exists when there is less constraint and more means-ends ambiguity (Hambrick, 2007). Hambrick and Finkelstein (1987) posit that discretion varies by industry such that CEOs have more “degrees of freedom” in some industries, but not in others. CEOs operating in high-discretion industries face fewer restrictions, and so the range of options CEOs can choose from is significantly enhanced (Finkelstein et al., 2009). A consequence of discretionary variations across industries is that CEOs are expected to follow established routines when discretion is low and limit untested and potentially risky actions and behaviors to the bare minimum. Low-discretion industries embody many taken-for-granted cause-and-effect understandings and have more ossified communication patterns, presenting more impediments to CEOs’ explorations into unchartered waters. Conversely, when managerial discretion is high, powerful CEOs’ biases about their own problem-solving capabilities (Camerer & Lovallo, 1999), the resources required and organizational resource endowments they have access to (Shane & Stuart, 2002) and the problems and issues confronting the firm (Kahneman & Lovallo, 1993) will become more salient and have a stronger impact on firm outcomes. Based on this logic, we predict the following:

Having presented three specific predictions grounded in prior research, we now turn toward the methodology used to obtain data for providing rigorous empirical examination of our conceptual logic.

Method

Data and Sample

To create our sample, we start with the Standard & Poor’s Execucomp database, which provides information on large publicly traded firms. Such firms are particularly appropriate for examining questions about top management as they are most subject to public scrutiny and serve as precursors for strategic practices and procedures for smaller firms. The firms in Execucomp span approximately the 1,500 largest listed firms in any given year and account for the majority share of business activity in the United States. Following prior research (e.g., Bertrand & Schoar, 2003), we eliminate financial institutions and utilities from the sample as firm characteristics such as leverage and the market-to-book ratio (M/B) in regulated industries can be extreme, difficult to interpret, and not representative of firms in general. For example, banks (unlike firms in other industries) have minimum capital requirements imposed by government, which directly affects leverage and the M/B.

We merge the sample of Execucomp firms from 1992 (the year Execucomp data begin) to 2009 with the Compustat database for financial information, Center for Research in Security Prices (CRSP) for stock price information, and the Investor Responsibility Research Center (IRRC) and RiskMetrics databases for information pertaining to the board of directors. Our final sample consists of 3,724 CEOs in 2,097 unique firms during 1992 to 2009, covering a total of 17,604 firm-years. In all, 58 two-digit and 348 four-digit Standard Industry Classification (SIC) codes are represented in our sample. Of particular importance, no four-digit SIC code accounts for more than 3% of the total sample, and no two-digit SIC code accounts for more than 10%. Our sample is therefore broad enough to guard against potential industry effects and lends generalizability across major business sectors, thus enabling us to test hypothesized relations in a conservative fashion.

Independent Variables—CEO Power and Industry Shock

CEO power

We measure CEO Power using a well-regarded measure developed by Finkelstein (1992) and modified by Tang, Crossan, and Rowe (2011). Specifically, we construct a measure of CEO power based on seven variables: CEO Pay Slice (CPS), Duality, Triality, Tenure, Ownership, Non-Independent Directors, and Founder. Of these, CPS, Duality, Triality, and Non-Independent Directors are used to measure structural power; Ownership and Founder to measure ownership power; and Tenure to measure expert power. We now describe each of these variables more fully below.

CPS: CPS is measured as the CEO’s total compensation as a fraction of the total compensation of the firm’s top five executives (Bebchuk, Cremers, & Peyer, 2011). Total compensation includes salary, bonuses, restricted stock grants, stock options, long-term incentive compensation, non-equity incentive compensation, deferred compensation, and “other” compensation as reported in Execucomp. CPS reflects the relative importance of the CEO as well as the extent to which the CEO is able to extract rents (Bebchuk et al., 2011). Greater values of CPS indicate greater CEO power.

Duality: A large body of research uses concentration of titles vested in the CEO as a measure of CEO power (see Adams et al., 2005; Morse, Nanda, & Seru, 2011; Pathan, 2009; among others). We create two indicator variables to reflect the concentration of titles. The first is Duality, an indicator variable that takes the value one if the CEO is also Chair of the company’s board of directors.

Triality: The second indicator variable we create to reflect the concentration of titles is Triality, an indicator variable that takes the value one if in addition to the CEO serving as Chair, the CEO also has the title of President of the firm.

Tenure: CEO tenure increases the CEO’s influence over the board and thus increases CEO power (Finkelstein, 1992).

Ownership: Greater CEO stock ownership reduces the influence of the board and enables the CEO to exercise more discretion in making decisions, thus increasing CEO power (Finkelstein, 1992). We use Execucomp to determine each CEO’s stock ownership.

Founder: CEOs who are also founders are likely to be more powerful (see Adams et al., 2005; Morse et al., 2011). We construct an indicator variable, Founder, which takes the value one if the CEO is also the founder. We consider a CEO as founder of the company if the CEO is the founder, a descendant of the founder, or served as CEO from inception. Defining founder more strictly by not including descendants does not materially affect our results.

Non-Independent Directors: The higher the proportion of non-independent directors on the board, the more likely the CEO can exert influence over the board (Morse et al., 2011). We thus construct a variable that represents the proportion of non-independent directors for the firm. We use the IRRC database from 1996 to 2006 and the RiskMetrics database from 2007 to 2009 to construct this variable. As is common when using these databases, in years not covered by either database, we backfill the data using the closest year following the missing observation (Gompers, Ishii, & Metrick, 2003).

We create a continuous CEO power measure by standardizing the four continuous components (CPS, Ownership, Non-Independent Director, and Tenure), summing these along with the remaining indicators (Duality, Triality, and Founder).

Industry shock

We define an industry downturn or “shock” as a 5% or greater decrease in aggregate industry sales (we discuss later that variations in cutoffs do not materially change our results). Our definition of an industry shock is similar to that of Mitchell and Mulherin (1996) in that industry downturns are based on industry sales activity (measures based upon industry stock market returns and industry excess market returns, that is, adjusted for the overall stock market, yield similar results as we also discuss later). Using each firm’s primary four-digit SIC code, we assign sample firms to one of 49 Fama and French’s (1997) industry classifications, which sorts four-digit SIC codes into industry groups that are more likely to share common risk characteristics (Bhojraj, Lee, & Oler, 2003). This classification scheme, widely used in the financial economics literature (Chan, Lakonishok, & Swaminathan, 2007), was originally developed to address some of the problems with SIC codes caused by changes in the variety and growth of products and services, shifts in technology, and the makeup of businesses. Using the 5% cutoff, we identify a total of 60 industry shock years distributed across 30 industries over the sample period.

Moderating Variables

Innovativeness

Innovativeness is measured as the number of patents a firm registers in a given year (Patents). As is common in the literature, if Patents is missing, we set Patents to zero and set a Patents Missing dummy to one. We obtain data on patents and citations from the National Bureau of Economic Research (NBER) patent project through Bronwyn Hall’s website (http://eml.berkeley.edu//~bhhall/patents.html/). Following the literature utilizing the patent database, we adjust patent counts using “weight factors” computed from the application-grant empirical distribution and adjust citation counts (used as an alternative measure of innovation) by estimating the shape of the citation-lag distribution. These are necessary to address truncation issues inherent in the NBER patent database.

Market competitiveness

We measure the intensity of market concentration using the Herfindahl Index, defined as the sum of the squared market shares for all firms in an industry group. The Herfindahl Index ranges from 0 to 1, where a score approaching 0 reflects high fragmentation in the market and a score approaching 1 reflects a concentrated industry.

Managerial discretion

We use Hambrick and Abrahamson’s (1995) industry discretion ratings to classify industries into high- and low-discretion categories. To increase the matches with our data, we follow Adams et al. (2005) in averaging Hambrick and Abrahamson’s measure by two-digit SIC code.

Dependent Variable

Our measure of firm performance in a given time period is the value added or destroyed during that time period. The M/B is a common valuation metric used in the literature (see, for example, Bebchuk et al., 2011; Crossland & Hambrick, 2011; Gompers et al., 2003). Thus, we measure firm performance as the change in the Market-to-Book ratio, ΔM/B, where the M/B is defined as the market value of common equity plus the book value of assets minus the book value of common equity, all divided by the book value of assets. We compute the yearly change in the M/B, ΔM/B, as M/B t − M/Bt − 1 where M/B t is the M/B in year t.

Control Variables

Based on prior research, we control for the following firm-specific variables for their potential influence on firm performance. Firm Size is the log of the firm’s market capitalization (share price times shares outstanding). Investments is the ratio of firm investments (capital expenditures plus R&D) to total assets. Leverage is the ratio of long-term debt to total assets. Stock Volatility is the standard deviation of a firm’s daily stock returns over the previous year. We also include year dummies to control for temporal conditions and firm dummies to control for time-invariant firm heterogeneity.

Estimation

We have a panel data set, and because unobservable firm characteristics are likely to affect firm value, we estimate firm fixed-effect models using each firm’s change in M/B as the dependent variable. Fixed-effect models are an unbiased method of controlling for omitted variables in panel data sets. We use industry shocks to investigate the impact of CEO power on firm performance. Moreover, change in M/B can be more directly related to the shock as absolute measures of post-shock value likely reflect enduring performance effects carried over from the pre-shock period (Datta & Rajagopalan, 1998). As we discuss later, our results are robust to using industry-adjusted measures and to various econometric techniques.

Results

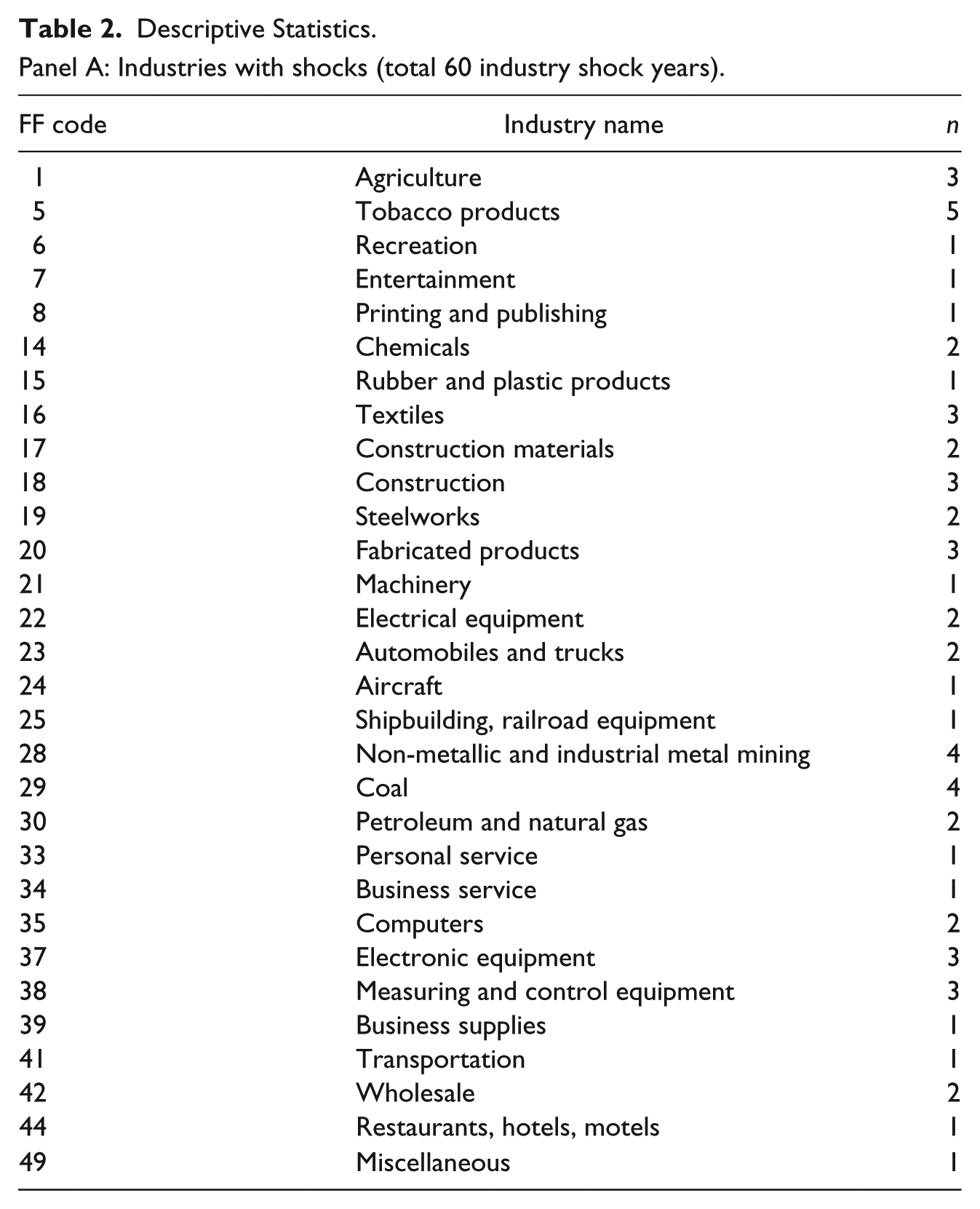

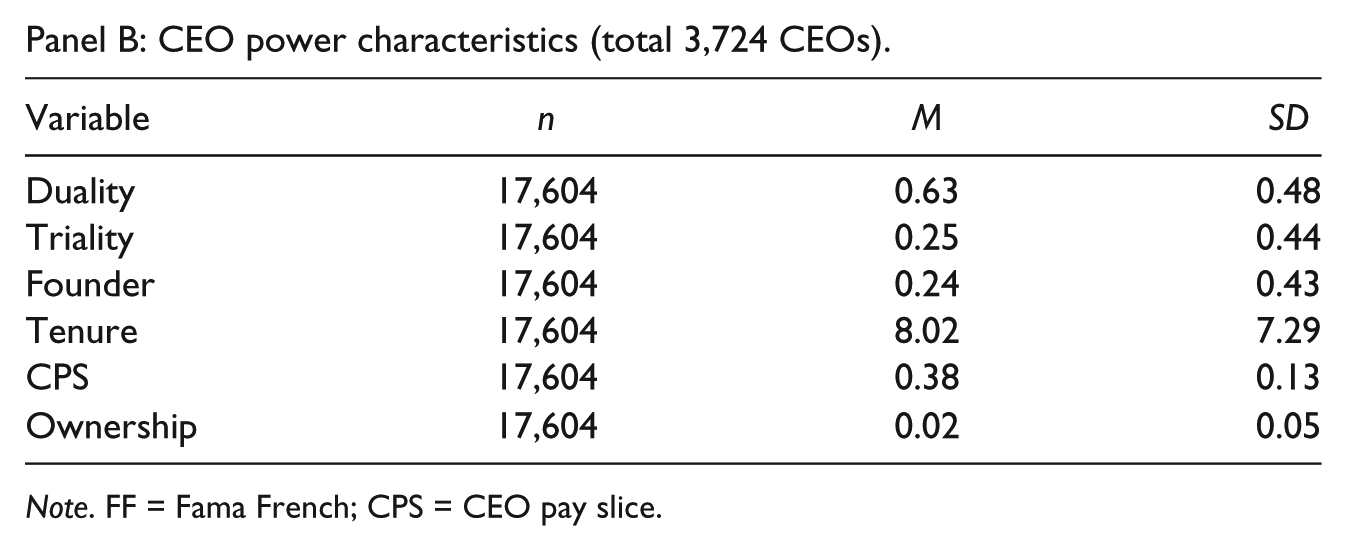

Table 2 presents frequency of shocks per industry (Panel A) and descriptive statistics for the individual components of our CEO power metric (Panel B). As previously noted, there are a total of 60 industry shock years distributed across 30 industries over the sample period. The CEO is the chairman 63% of the time and founder 24% of the time, has an average tenure of 8 years, and owns 8% of the firm (median ownership is 0.4%). The 38% average CPS we report is similar to that reported in Bebchuk et al. (2011).

Descriptive Statistics.

Panel A: Industries with shocks (total 60 industry shock years).

Panel B: CEO power characteristics (total 3,724 CEOs).

Note. FF = Fama French; CPS = CEO pay slice.

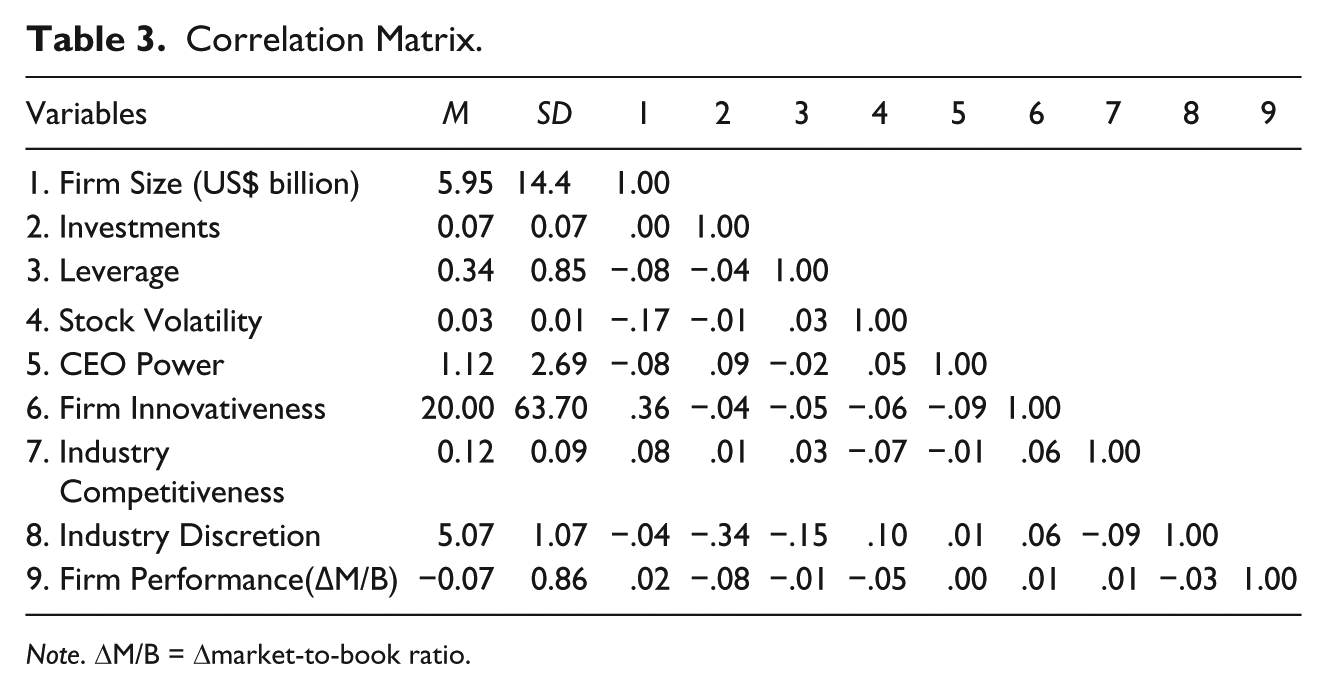

Table 3 presents descriptive statistics and correlations for our independent variables. The average firm size is almost US$6 billion (median US$1.4 billion), which is consistent with Execucomp’s emphasis on the largest 1,500 listed companies. On an annual basis, firms in our sample spend on average 7% of total assets on investments (sum of capital expenditures and R&D). The average number of patents in a firm-year is 20. We find that among the independent variables, most of the correlations are less than 20% in absolute terms. Thus, multicollinearity does not appear to present a significant problem for our analysis. In untabulated results (available from the authors), we find the correlations among the individual components that comprise our CEO power index are relatively small, with the majority of the correlations being less than 20% in absolute terms. Overall, it appears the individual power components detect different aspects of CEO power.

Correlation Matrix.

Note. ΔM/B = Δmarket-to-book ratio.

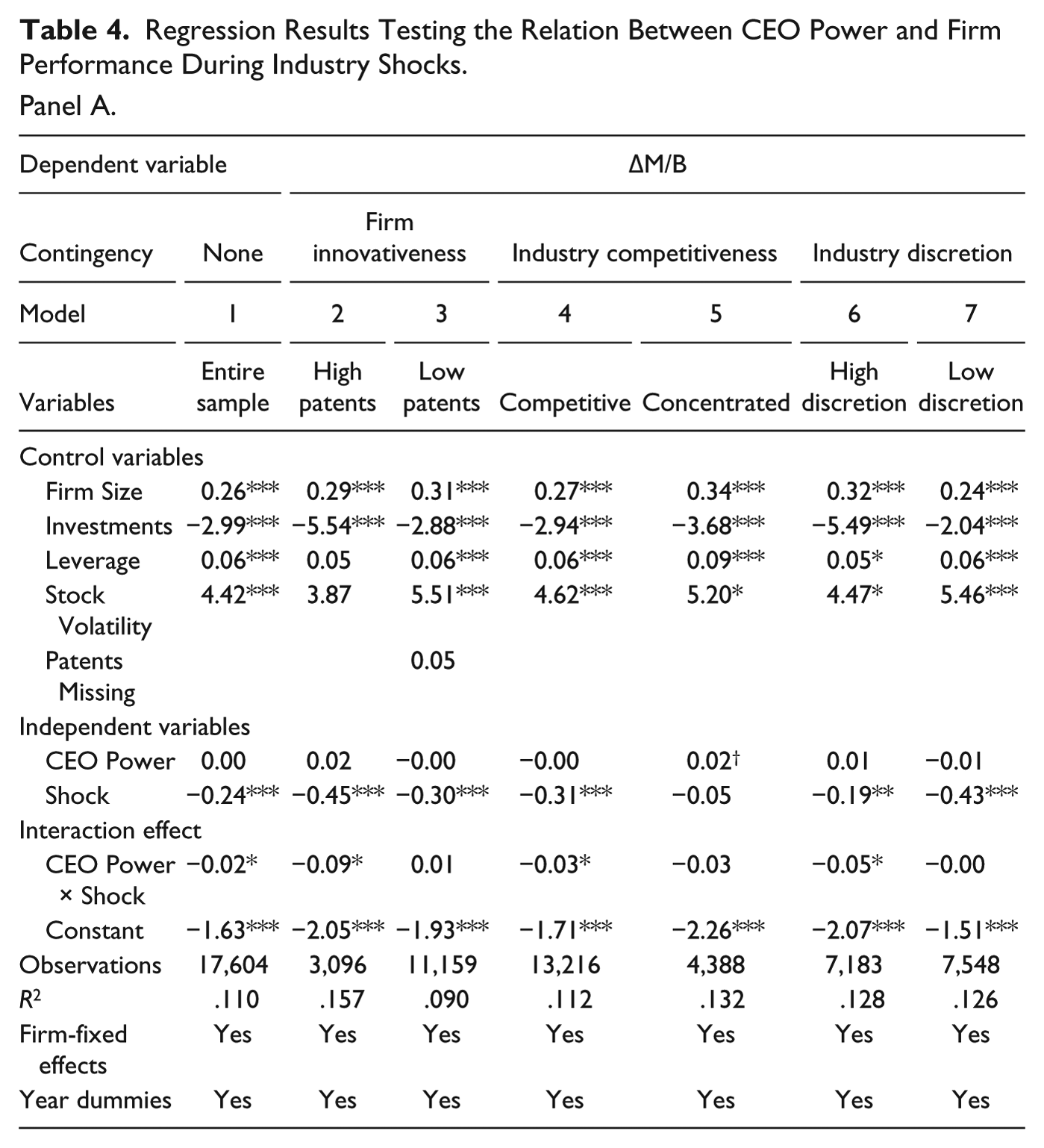

Table 4 presents regression results. Panel A provides results from subgroup analyses, and Panel B provides results from using three-way interactions. Model 1 of Panel A contains the results incorporating the control variables and the direct effect of CEO Power and Shock along with the interaction of CEO Power and Shock. Not surprisingly, the coefficient on the Shock variable is significantly negative. Although the coefficient on CEO power measure is negative, it is not significant. However, the coefficient on the interaction term of CEO Power and Shock is negative and significant (β = −.02, p < .05).

Regression Results Testing the Relation Between CEO Power and Firm Performance During Industry Shocks.

Panel A.

Panel B.

Note. ΔM/B = Δmarket-to-book ratio.

p < .10. *p < .05. **p < .01. ***p < .001.

Hypothesis 1 predicts that CEO power will have a negative effect on firm value for innovative firms during industry downturns. To test this hypothesis, we split the sample into two subsamples based on whether the firm’s innovativeness is above (Panel A, Model 2) or below (Panel A, Model 3) the sample median. The coefficient of the Shock and CEO Power interaction term is negative and significant (β= −.09, p < .05) for the subsample where innovativeness is above the sample median. The coefficient of this interaction term is not significant in Model 3 where innovativeness is below the sample median. These results support Hypothesis 1.

Hypothesis 2 predicts the net effect of CEO power on firm value during industry downturns is more pronounced in competitive industries. To test this hypothesis, we use the Herfindahl Index as our measure of competition and define an industry as competitive when the Herfindahl Index is below the sample median (Panel A, Model 4) and define an industry as concentrated when the Herfindahl Index is above the sample median (Panel A, Model 5). The coefficient of the Shock and CEO Power interaction term is negative and significant (β= −.03, p < .05) for the competitive subsample, but the coefficient of this interaction term is not significant for concentrated markets. These results support Hypothesis 2.

Hypothesis 3 predicts that CEO power will have a more pronounced negative effect on firm value for high-discretion settings (i.e., where managerial decision making faces fewer constraints) during industry downturns. To test this hypothesis, we split the sample into two subsamples based on whether managerial discretion is above (Panel A, Model 6) or below (Panel A, Model 7) the sample median. The coefficient of the Shock and CEO Power interaction term is negative and significant (β= −.05, p < .05) for the high-discretion subsample, but the coefficient of this interaction term is not significant for the low-discretion setting. These results support Hypothesis 3.

As an alternative approach to the subgroup analysis of Panel A, in Panel B we test each hypothesis via a three-way interaction. In particular, we test Hypothesis 1 by interacting CEO Power, Shock, and Patents (Model 1); Hypothesis 2 by interacting CEO Power, Shock, and Competition (Model 2); and Hypothesis 3 by interacting CEO Power, Shock, and Discretion (Model 3). In each case, we find that the coefficient on the three-way interaction term is significantly negative. Thus, once again, we find support for each of our hypotheses.

We note from Table 4 that, although not predicted by theory, the level of CEO Power is generally not significant outside of downturns. Thus, it appears that the costs associated with having a powerful CEO are counterbalanced to some extent by the associated benefits during non-downturn periods. Moreover, in supplementary tests, we investigated the impact of CEO power on firm value during positive shock years and found that powerful CEOs generally have little incremental effect on firm performance relative to less powerful CEOs during such years. Based on these exploratory findings, we encourage deeper probing on the impact of CEO power on firm performance during non-downturn periods.

We also undertook additional analyses to substantiate the robustness of our findings. We reanalyze the data using an alternative measure of innovativeness: number of independent citations (i.e., excluding self-citations) a firm’s patents receive in subsequent years. This measure captures the impact of innovativeness. Our findings remain largely the same. We use the market share captured by the largest four firms in a market as a measure of concentration, so that the smaller the overall share, the less concentrated the market. Again, our findings remain largely the same. We redefine an industry downturn in three alternative ways—a 10% or greater decrease in aggregate industry sales, a negative industry stock return, and a negative industry market-adjusted return—and find similar results. We also create a CEO power measure based upon the first principal component of our individual proxies. Again, our inferences are largely unaffected. Finally, when we use an industry fixed-effect specification, CEO Power again has no discernable effect on firm value outside of shock years, suggesting our results are not the outcome of CEO power mirroring greater CEO risk-taking behavior.

Overall, our results are both statistically and economically significant. Using the results from the subgroup analysis, we find that for innovative firms, a one standard deviation increase in CEO Power is associated with a 10% decrease in the firm’s M/B during shock years. A one standard deviation increase in CEO Power for firms in competitive industries is associated with a 4% decrease in the firm’s M/B during shock years. Finally, a one standard deviation increase in CEO Power for firms in high-discretion industries is associated with a 5% decrease in the firm’s M/B during shock years.

Discussion

A key debate among practitioners as well as academics revolves around how much power should be vested in the top executive. Our purpose in the present inquiry is to provide a new vantage point for understanding the dilemma about powerful CEOs. Specifically, following upper echelon research (Finkelstein et al., 2009), we posit that organizational innovativeness, market competition, and industrial discretion represent theoretically meaningful boundary conditions on the power–performance relation during times of turmoil. We find that for innovative firms with powerful CEOs, a shock to the industry results in a notable decrease in the firm’s M/B relative to a less powerful CEO. Similarly, for firms with powerful CEOs in competitive industries and also for firms with powerful CEOs in high-discretion industries, a shock to the industry results in a decrease in firm value. Thus, our results highlight the benefits that accrue to firms from having a more dispersed decision-making structure (e.g., receiving independent advice from the board or an independent chairman), especially during industry-wide downturns. Our results also highlight the types of firms that may have the most to gain from organizational structures that enhance the channels of information flow to top management. Given the difficulty in altering a CEO’s power once it is obtained, our results are instructive for regulators pushing for firms to have a more dispersed power base.

Our finding that powerful CEOs ultimately undermine firm performance during turbulent times is doubly informative for recent debates about the usefulness of agency theory. First, critics have charged that agency concerns are overblown as managers are generally good stewards of corporate resources and assets (Davis et al., 1997). Although claims of efficient stewardship on the part of top managers at large corporations are appealing, our research clearly points to a significant loss in firm value when power is concentrated in the CEO, which is consistent with agency-theoretic logic. Second, it has been argued that agency concerns are relevant only within a very narrow range of conditions not usually found in the business world (Wiseman, Cuevas-Rodriguez, & Gomez-Mejia, 2012). Our results show that agency concerns are real and pervasive as powerful CEOs have a serious adverse impact on firm performance, with this negative influence worsening under the right alignment of contextual conditions. Although we broadly agree with the position that the agency literature paints a pessimistic picture of managerial behavior, based on our results we caution against attempts to jettison agency theory in favor of more heroic and positive conceptions as they are likely to come at the expense of firm success.

The present inquiry focuses on the impact of CEO power on firm performance during industry downturns. As such, we do not delve into the literature pertaining to situations outside of industrial downturns. It may be the case that the benefits of having a powerful CEO counterbalance or outweigh the associated costs during non-downturn periods. Consequently, the effect(s) of CEO power on firm performance during non-downturns is a matter of theoretical and empirical inquiry beyond the scope of this study. Although our research allows us to briefly explore the empirical aspect of the CEO power and firm performance relation during non-downturn periods, much deeper probing is needed to truly understand how CEO power affects firm performance during such periods.

Theory-based empirical research on firms that find themselves in crisis and turbulence is very rare (Withers, Corley, & Hillman, 2012). This is somewhat surprising as firms are often in crisis situations that can create severe threats to the viability of the firm. When firms are unable to effectively navigate through crisis, it can lead to untimely demise, as happened with Circuit City and Steve & Barry’s during the recent Great Recession. The limited empirical research available on firms facing crisis typically involves laboratory experiments, qualitative case studies, and retrospective field investigations (Sommer, Howell, & Hadley, 2016). Because it is difficult to find studies conducted on firms weathering serious economic upheavals, our research should be a valuable addition to understanding the manifestation of specific strategic constructs and organizational behaviors during such difficult times.

Departing from much of previous corporate governance research, we focus on fit across CEO power and situational characteristics. In doing so, we respond to calls for researchers to pay attention to the patterned variations in corporate governance contingent on achieving alignment between various crucial factors. Based on our findings, we believe future scholarship will benefit from considering complex combinations of relations involving CEO power across different types of situations, rather than attempting to uncover simplistic relations that hold across all organizations and environments (Short et al., 2008).

Limitations and Avenues for Further Research

Like other studies, several limitations of our research offer opportunities for potentially valuable and exciting research going forward. Studies using archival measures have played a substantive role in knowledge development in organizational and managerial research (Boyd, Haynes, Hitt, Bergh, & Ketchen, 2012). At the same time, it must be noted that archival proxies are at best a partial approximation of the underlying construct (Ketchen, Ireland, & Baker, 2013). To illustrate, patent statistics are often used to assess innovativeness as we do in this study, yet innovative activity is only partially reflected in patent counts. Indeed, it is commonly known among innovation researchers that not all innovations are patented and not all patents reflect true innovations. Thus, future research should consider validating our predictions using alternative measures for the constructs comprising the nomological net in this study. More broadly, for organizational research to continuously advance the knowledge it creates for practitioners and academics, replications with similar as well as novel measures of the same constructs would be invaluable (Boyd, Bergh, Ireland, & Ketchen, 2013).

Second, as is common in organizational research, our study findings are derived from a particular sampling procedure. In our case, the sample was large, well-established publicly traded companies in the United States. Our approach has the advantage of holding constant extraneous factors unrelated to the research question at hand. Whether the study’s results also hold for smaller and younger firms (mostly, privately held) as well as in other countries with institutional environments different from the United States is a matter of empirical validation. Because external validity is best viewed as a characteristic of a stream of research and not a single study, we encourage future research to examine the generalizability of our results to other samples.

A third limitation may lie in our measurement approach toward CEO power. Specifically, we follow prior research (e.g., Tang et al., 2011), in assessing CEO power as a composite construct. Future research might examine how various elements of the executive power construct (structural, ownership, expert, and prestige) interact differently with the exigencies considered here. Furthermore, our assessment of CEO power is unable to tease out the effects stemming from the kinds of people who ascend to CEO positions in the first place. Our reading of the relevant literature suggests that the inability to measure CEO power in a way that separates the role of qualities that facilitate the rise to CEO positions has been a sustained weakness in the literature (Daily & Johnson, 1997). We hope researchers will consider this critical issue in future inquiries about CEO power.

Finally, our research focuses on the performance impact of CEO power during industry downturns. Whether CEO power will have similar or different performance consequences during non-downturn periods remains for future research to examine. Such research will be most useful when researchers distinguish among different types of periods such as normal times, upswings, and downturns, clearly articulating when their conceptual arguments are expected to hold most strongly. Distinguishing among periods that a firm may confront in its life will not only be responsive to calls for scholarship that mirrors organizational realities (Alvesson & Gabriel, 2013) but also can bring more accuracy and validity to inferences about the role and value of governance practices that shape CEO power.

Conclusion

The role of CEOs in organizational success (or failure) has been of long-standing interest to organizational scholars. Because CEOs may not be able to effectively shape their organizations in all cases and circumstances, we sought to cast light on the conditions under which they appear to matter significantly for firm performance. The results of our research support the idea that vesting considerable power in the CEO does not create value for the firm during industry downturns. Our results also indicate that firms with powerful CEOs are worse off under conditions of innovativeness, greater competition in the industry, and industries characterized by high discretion. Thus, our research shines new light on the contextual factors affecting the relation between CEO power and firm performance during times of industry turmoil.

Footnotes

Acknowledgements

We thank Associate Editor Orlando Richard and the anonymous reviewers for their insightful comments and suggestions throughout the review process. Of course, all errors and omissions remain our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Associate Editor: Orlando Richard