Abstract

Dismissal (or involuntary exit) of the chief executive officer (CEO) is a significant milestone with substantial implications for organizations and their members. The growing occurrence of CEO dismissals, and increased academic interest in this area, motivates our comprehensive multidisciplinary synthesis of the extant literature. Our analysis is organized around understanding the antecedents and outcomes of CEO dismissal, and the relevant moderators that play a contingent role in the nomological network. Based on our synthesis of the extant cross-disciplinary literature, we offer a multilevel organizing framework articulating the current state of research on CEO dismissal. In doing so, we catalog and analyze the concepts, theories, and constructs prevalent in the CEO dismissal literature. We also offer an in-depth discussion for the field going forward and identify a constructive agenda for future research on CEO dismissal.

Chief executive officer (CEO) dismissal is widely considered important to organizational theory (Fredrickson, Hambrick, & Baumrin, 1988) as it offers a unique “window into the heart of executive accountability” (Crossland & Chen, 2013, p. 79). The decision to dismiss the CEO rests with the board of directors of the firm (Boeker, 1992) and serves as the ultimate tool for disciplining the CEO (Beck & Wiersema, 2011; Crossland & Chen, 2013). Not surprisingly, when CEOs are dismissed, it often causes significant upheaval (Friedman & Saul, 1991; Tao & Zhao, 2019; Wiersema, 2002) and attracts considerable media attention (Cordeiro & Shaw, 2010). CEOs influence their firms in a variety of ways, including setting strategy and guiding performance (Adams, Keloharju, & Knüpfer, 2018; Liu, Fisher, & Chen, 2018; Wowak, Gomez-Mejia, & Steinbach, 2017). Indeed, substantial agreement exists among researchers and practitioners that CEOs are central figures in their organizations (Hambrick & Quigley, 2014). Thus, CEO dismissal is “one of the most theoretically interesting topics” for organizational researchers (Li & Lu, 2012, p. 1007).

Substantial previous research has focused on the general process of CEO turnover (Berns & Klarner, 2017; Giambatista, Rowe, & Riaz, 2005; Ma, Seidl, & Guérard, 2015). While voluntary departure has historically been the most common form of CEO exit in modern corporations (Parrino, 1997), the incidence of dismissal has been on the rise (Fuhrmans & Feintzeig, 2019). 1 The increasing trend of CEO dismissal may arise from “greater scrutiny of CEO behavior, a greater desire for swift justice and action, and a smaller margin of error” (Karlsson, Aguirre, & Rivera, 2017, p. 3). Unfortunately, it is often difficult to distinguish between voluntary and involuntary departures as the precise reason for the separation of the CEO from the firm is rarely accurately disclosed (e.g., Parrino, 1997; Pitcher, Chreim, & Kisfalvi, 2000; Shen & Canella, 2002a), indicating that the occurrence of CEO dismissal may be underestimated (Hilger, Mankel, & Richter, 2013). Yet, the increasing incidence and focus on CEO dismissal suggests that many opportunities remain to enhance our understanding of this area (Louca, Petrou, & Procopiou, 2020).

For consistency and clarity, we view CEO dismissal as a specific subset of CEO turnover that refers to situations “in which the CEO’s departure is ad hoc (e.g., not part of a mandatory retirement policy) and against their will” (Fredrickson et al., 1988, p. 255). Consequently, a key feature of dismissal (involuntary turnover) that distinguishes it from voluntary turnover is dissatisfaction with the CEO that motivates a change in leadership (Hutzschenreuter, Kleindienst, & Greger, 2012; Schepker, Kim, Patel, Thatcher, & Campion, 2017). Dismissing the CEO, which is the responsibility of the board of directors, provides the board an opportunity to select a new, preferred leader (Cao, Maruping, & Takeuchi, 2006). The decision to dismiss CEOs may seem straightforward—when firms experience poor performance (or other indications of questionable leadership competence), boards move to dismiss CEOs. Yet, CEOs, wishing to retain their position, often push back. This situation creates opposing interests: the board wanting to dismiss the CEO, but the CEO not willing to be dismissed. A number of factors influence the incidence of CEO dismissal (as we discuss later in this review), either making it easier to dismiss the CEO or making it more difficult for the CEO to be dismissed. As a result, dismissal causes significant disruption for the firm as a whole and profoundly impacts various stakeholders (Friedman & Saul, 1991; Tao & Zhao, 2019).

We organize our analysis around examining the antecedents and outcomes of CEO dismissal, as well as relevant moderators in the nomological network. We examine these factors at four key levels: CEO, board, firm, and external. In doing so, we add value to the field by developing an organizing framework that categorizes previous research and offers clarification on the critical constructs and underlying theories relevant to CEO dismissal. Through this organizing framework, we identify fruitful research avenues to pursue going forward.

Our study proceeds as follows. First, after discussing the parameters of our literature search, we delve into the process and timing of CEO dismissal. In doing so, we offer a clearer understanding of the tension between the two main parties in this process: the CEO and the board. Second, we explore the state of the field by discussing theories and constructs used to examine CEO dismissal. For ease of interpretation and integration, we organize this review around antecedents, moderators of antecedents, outcomes, and moderators of outcomes at four key levels: CEO, board, firm, and external. From this analysis, we are able to ascertain what we know about CEO dismissal and where future research opportunities still exist. We then offer specific and actionable future directions, motivated by our literature review and important for the field to gain a more complete understanding of CEO dismissal.

CEO Dismissal in the Literature: Where Are We?

Search Terms Paired with Chief Executive Officer.

Note. We also searched derivations of each keyword.

In the interest of thoroughness, we further expanded our search beyond journals listed by O’Brien et al. (2010),

2

which yielded 63 additional articles. Thus, our final sample includes 179 articles published between 1985 and 2020. Figure 1 charts the increasing trend in research regarding CEO dismissal across this 35-year period. Scholars in fields other than management, particularly finance and accounting, are leading the way in research on CEO dismissal. Table 2 offers a sampling of exemplary scholarship on CEO dismissal, including the main theoretical theme(s), primary method(s), samples, and relevant findings. A full table including all 179 articles can be found in our online appendix (Supplementary Table). Count of chief executive officer dismissal articles by year. Sampling of Exemplar Research on Chief Executive Officer Dismissal. aJournal: AMJ = Academy of Management Journal; AR = Accounting Review; CGIR = Corporate Governance: An International Review; FM = Financial Management; HRM = Human Resource Management; JAE = Journal of Accounting and Economics; JBFA = Journal of Business Finance & Accounting; JBR = Journal of Business Research; JCF = Journal of Corporate Finance; JOF = Journal of Finance; JFE = Journal of Financial Economics; PAR = Pacific Accounting Review; RFS = Review of Financial Studies; SMJ = Strategic Management Journal; CEO = chief executive officer. bIndividual models/subsamples may differ. Note. OLE = ordinary least squares; GEE = generalized estimating equation.

Processes and Timing of CEO Dismissal

Central to CEO dismissal is the interaction between the board and CEO. Specifically, two opposing factors underlie the process and timing of CEO dismissal: (1) the board’s desire to change the leadership of the firm as boards are tasked with hiring and firing the CEO (Boeker, 1992) and (2) the CEO’s desire to retain leadership over the firm. Once hired, CEOs are tasked with setting strategy and guiding performance (Adams et al., 2018; Liu et al., 2018; Wowak et al., 2017) as well as maintaining organizational culture, values, and controls (Hambrick, 2007; Schnatterly, Gangloff, & Tuschke, 2018). As time passes, various stakeholders (e.g., the board, investors, and analysts) update their expectations and assessment of the CEO (Conger, Finegold, & Lawler, 1998; Wiersema & Zhang, 2011). When firms falter in one or more of these areas, such as poor firm performance (Dou, Sahgal, & Zhang, 2015; Engel, Hayes, & Wang, 2003), failed acquisitions (Alexandridis, Doukas, & Mavis, 2019; Lehn & Zhao, 2006), or fraud (Khanna, Kim, & Lu, 2015; Persons, 2006), the failure is often attributed to the CEO, who is viewed as not meeting expectations as leader of the firm (Calder, 1977; Vinkenburg, Jansen, Dries, & Pepermans, 2014; Weber & Wiersema, 2017).

The board’s assessment of the CEO is particularly important in the decision to dismiss a CEO since the board of directors is tasked with overseeing the CEO on behalf of stakeholders and taking corrective action (i.e., dismissing the CEO) if necessary (Boeker, 1992; Graffin, Boivie, & Carpenter, 2013). Once the CEO is hired, the board has the opportunity to directly observe CEO quality and fit with the firm (Jacobsen, 2014). He and Fang (2016, p. 25) explain that as “managerial talent is revealed over time, the board will update its prior knowledge on CEO quality and make dismissal or retention decisions accordingly.” Thus, the board’s desire to change the company’s leadership is contingent on its recognition of the needs of the firm under existing circumstances (including the nature of the reasons to consider dismissal) (Sebora & Kesner, 1996), informed by information available to boards (Cornelli, Kominek, & Ljungqvist, 2013).

The timing of CEO dismissal speaks to the question of when the process is enacted. On the one hand, frictions between the CEO and board may build up over time, with dismissal only occurring following lengthy discussion and debate by the board (Cornelli et al., 2013; Koskinen, 2018). Declining performance (Dou et al., 2015; Ertugrul & Krishnan, 2011), in particular, is often cited as the reason for a CEO gradually losing the confidence of the board. For example, Carly Fiorina was dismissed as CEO of Hewlett-Packard after a significant period of performance declines and protracted disagreements within the board about the direction of the company (Tam, 2005). On the other hand, when unforeseen major negative events or crises unexpectedly arise, the board may abruptly seek CEO change (Berns & Klarner, 2017; Ertugrul & Krishnan, 2011). Possible crisis situations examined in prior research include accounting restatements (Beneish, Marshall, & Yang, 2017), earnings manipulations (Hazarika, Karpoff, & Nahata, 2012), and personal indiscretions (Cline, Walking, & Yore, 2018). For example, Steve Easterbrook was abruptly dismissed as CEO of McDonald’s following revelations about an inappropriate romantic relationship with a subordinate in violation of the company’s personal conduct policy (Haddon & Vranica, 2019). Thus, the timing of CEO dismissal—after lengthy consideration or suddenly—reflects the board’s perceived urgency regarding the need for leadership change (Weber & Wiersema, 2017).

Complicating the dismissal decision and its timing is the board’s ability to enact their decision versus the CEO’s preference to remain in charge. Even if the board would like to dismiss the CEO, the CEO may have considerable power (by being the chair of the board or having a nontrivial ownership stake in the firm, for example). Under these circumstances, the board’s collective preference for dismissing the CEO might not prevail. Similarly, if the board has greater power than the CEO, the CEO’s position becomes somewhat more precarious. In such conditions, CEOs may want to remain at the helm, but boards will be able to dismiss them if and when they feel it is necessary.

Another complication with regard to the timing of CEO dismissal concerns the ramifications for the firm from dismissing the chief executive. CEO dismissal may leave the firm leaderless or with a temporary CEO for an extended period of time, leading to firm disruption (Wiersema, 2002) and instability (Intintoli, 2013). Furthermore, significant financial and time costs are associated with the search for a new CEO (Mooney, Semadeni, & Kesner, 2017; Taylor, 2010).

Bringing together these concerns about the timing of CEO dismissal highlights the question of whether the dismissal was “too late” (reactive dismissal) long after poor performance was obvious or “too soon” (proactive dismissal) before a CEO’s strategic changes have had time to yield benefits. Some scholars (e.g., Ertugrul & Krishnan, 2011; Martin & Combs, 2011) have recently discussed the possibility that CEO dismissals can be “too proactive” or “too reactive.” The ramifications of dismissal timing are significant as more proactive dismissals may not allow a CEO to rectify problems in the firm, while more reactive dismissals can exacerbate the negative consequences for the firm (Ertugul & Krishnan, 2011; Hazarika et al., 2012). Yet, determining whether the board acted too hastily or slowly in dismissing a CEO is difficult given the speculative nature of CEO dismissal. Thus, until we can accurately ascertain whether a board dismissed a CEO prematurely or only after it was well overdue, our understanding of the “ultimate effectiveness” of such an action will remain unclear (Cools & van Praag, 2007, p. 739).

Prevailing Theories and Constructs Explaining CEO Dismissal

Several theories offer explanatory power for understanding CEO dismissal. The most prominent theory in the literature on CEO dismissal, accounting for approximately 50% of CEO dismissal studies, is agency theory (Jensen & Meckling, 1976). Focused on the monitoring relationship between agents and principals, agency theory speaks to the power struggle that emerges between the board, who monitors the firm on behalf of shareholders, and the CEO when dismissal is considered. Several other theoretical lenses (e.g., signaling (Akerlof, 1970), network theory (Burt, 1984), and attribution theory (Calder, 1977)) are also used to understand CEO dismissal. We intersperse the theories used and constructs examined throughout our review of the literature.

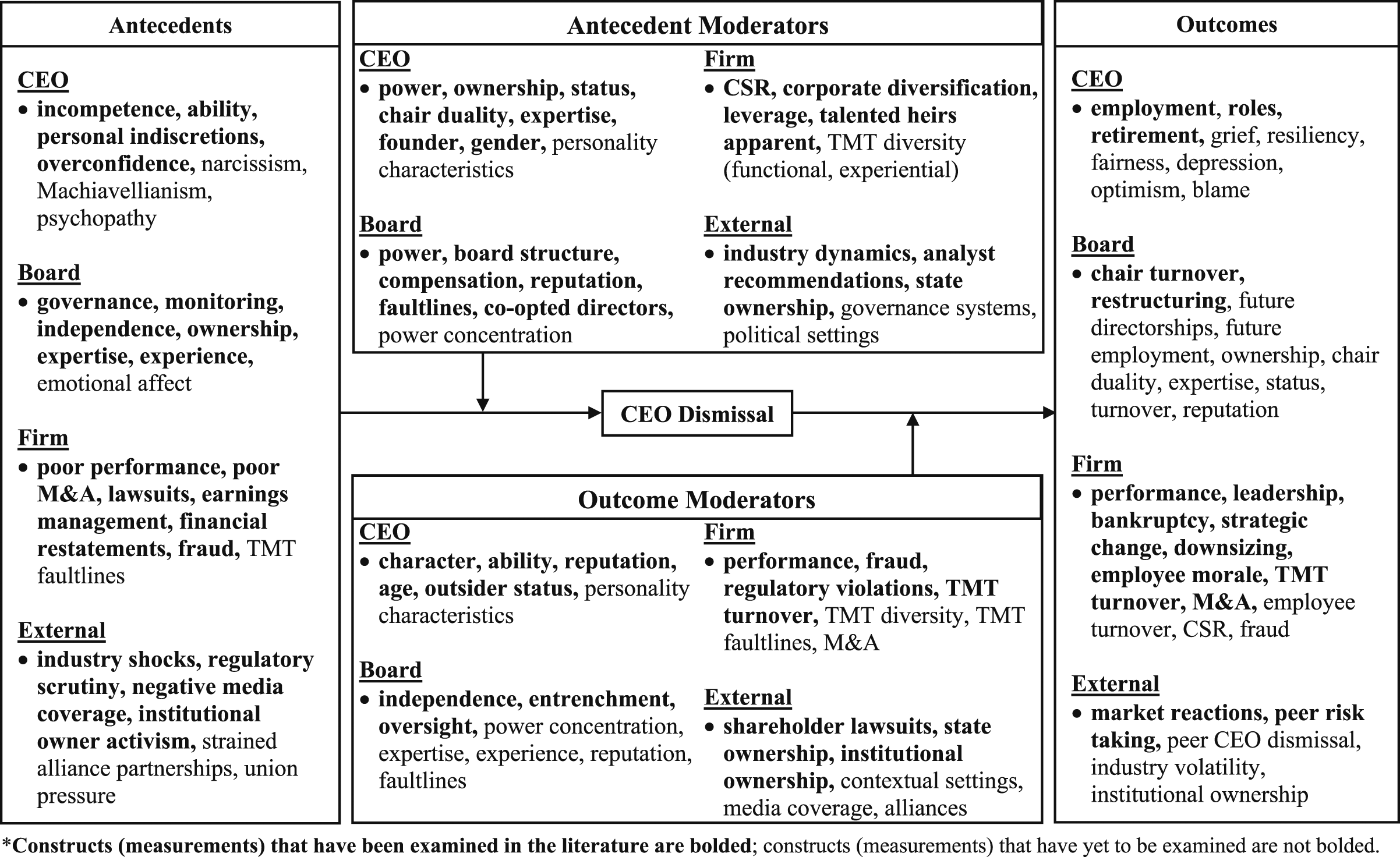

Four key levels of analysis emerged from our review of extant CEO dismissal literature: CEO, board, firm, and external. Within each level, constructs can be antecedents, outcomes, or moderators of either antecedents or outcomes. Below, we explore these constructs at each level by discussing theories utilized and constructs examined. Figure 2 presents an organizing framework highlighting a sampling of the areas that have been explored at each level and areas where opportunities for future research remain. In Figure 2, areas that have already been examined in the literature appear in bolded font, while those yet to be explored appear in regular font. Our framework provides a structured visual synthesis of what we know as well as opportunities that exist for future researchers. Key gaps that we identified are elaborated in the section on future directions. Noticeably, for each level, previous work has largely focused on antecedents surrounding CEO dismissal, with much less attention paid to the outcomes. Among other contributions, we hope our analysis draws attention to this imbalance in the CEO dismissal literature. Organizing framework of chief executive officer dismissal. Note. Constructs (measurements) that have been examined in the literature are bolded; constructs (measurements) that have yet to be examined are not bolded.

Antecedents of CEO Dismissal

CEO

Several CEO attributes have been found to be antecedents to CEO dismissal. CEO characteristics, or perceptions and interpretations of them, offer signals regarding the quality and fit of the CEO (Chemmanur & Fedaseyeu, 2018). For example, perceptions of CEO capabilities, including a lack of perceived ability (Bruton, Fried, & Hisrich, 2000) and perceived incompetence (Cornelli et al., 2013), are positively related to CEO dismissal. Furthermore, personality characteristics, such as overconfidence (Kim, 2013), are positively related to CEO dismissal. The perceived character of the CEO also impacts CEO dismissal. Consequently, when CEOs commit personal indiscretions, they are often dismissed (Cline et al., 2018; Haddon & Vranica, 2019). Thus, the perceptions of signals (e.g., ability, incompetence, and personal indiscretions) can undermine CEO credibility, motivate calls for leadership change, and drive boards’ decisions to dismiss CEOs.

Board

We find a number of studies use agency theory to examine boards, their monitoring (or lack thereof) of the CEO, and the decision to dismiss the CEO (e.g., Boeker, 1992; Conyon & He, 2011; Dou et al., 2015). In line with agency logic, boards that are more effective monitor and dismiss the CEO more readily. For example, boards with greater independence (Boeker, 1992; Conyon & He, 2011) offer greater monitoring capacity and thus are more apt to dismiss the CEO. Relatedly, characteristics of board structure such as director ownership (Alam, Chen, Ciccotello, & Ryan, 2014; Ertugrul & Krishnan, 2011) and meeting frequency (Alam et al., 2014; Khanna et al., 2015) also encourage greater monitoring and are positively related to CEO dismissal. Furthermore, directors bring certain resources to the board that impact the dismissal decision. For example, boards with more expert directors (Francis, Hasan, & Wu, 2015; Wang, Xie, & Zhu, 2015) and experienced directors (Cai & Nguyen, 2018; Dou et al., 2015) dismiss CEOs more often.

Firm

Firm performance is the most studied antecedent of CEO dismissal, examined in over 50% of the studies in our sample (e.g., Ahn & Shrestha, 2013; Banerjee & Homroy, 2018; Cannella & Lubatkin, 1993). Attribution theory (Calder, 1977) offers that firm outcomes (e.g., performance) will be ascribed to the CEO by the board and other stakeholders (e.g., shareholders and analysts). While the relationship between poor firm performance and CEO dismissal is expected, performance is only part of the CEO dismissal picture. Failures in other areas, both strategic and operational, also lead to CEO dismissal. As an example of a strategy failure, poor or failed merger and acquisition deals have been found to precede CEO dismissal (Alexandridis et al., 2019; Lehn & Zhao, 2006; Roosenboom, Schlingemann, & Vasconcelos, 2013). Similarly, corporate scandals, such as earnings management and subsequent restatements (Beneish et al., 2017; Gomulya, Wong, Ormiston, & Boeker, 2017; Hazarika et al., 2012), fraud (Khanna et al., 2015), and tax avoidance (Chyz & Gaertner, 2018), represent operational failure on the CEO’s part, leading to dismissal of the CEO.

External

External to the firm, environmental conditions and stakeholder attitudes impact CEO dismissal. Indeed, adversity spurs challenges to CEO power (Ocasio, 1994), facilitating calls for dismissal. Consequently, dismissal is more commonplace following industry shocks (Eisfeldt & Kuhnen, 2013; Gomulya & Boeker, 2016) and with increased regulatory scrutiny (Guo & Masulis, 2015). The potential threat of takeover has also been found to motivate CEO dismissal (Burkart & Raff, 2015). Additionally, some stakeholders have the power to exert influence over the board and facilitate CEO dismissal. Using an agency lens, researchers have examined stakeholders (e.g., analysts, media, and shareholders) who monitor the CEO and use their legitimacy to exert influence on CEO dismissal. For example, scrutiny from the media (Bednar, 2012) and institutional owners (Helwege, Intintoli, & Zhang, 2012; Wu, 2004) are positively related to CEO dismissal.

Moderators of the Antecedents of CEO Dismissal

CEO

CEOs do not want to be dismissed. Thus, much of the work in this area focuses on how CEOs facing dismissal protect themselves. The managerial entrenchment literature (Walsh & Seward, 1990) speaks to the difficulty of CEO dismissal as CEOs often wield significant power (Adams, Almeida, & Ferreira, 2005; Finkelstein, 1992) and are able to insulate themselves from accountability and repercussions (Florou & Pope, 2008; Fredrickson et al., 1988). CEO power can come from various sources: structural/positional (e.g., duality), ownership, expertise (e.g., knowledge and tenure), and prestige (e.g., social status and celebrity) (Finkelstein, 1992). Bringing unique qualities to the firm is one way that CEOs increase their power and insulate themselves from dismissal. Being the founder (Beneish et al., 2017; Guo & Masulis, 2015) and having greater firm-specific knowledge (Oehmichen, Schult, & Wolff, 2017; Wang, Zhao, & Chen, 2017) insulate CEOs from dismissal as these CEOs bring valuable resources to the firm. Similarly, CEOs with greater ownership (Boeker, 1992; Gao, Harford, & Li, 2012) and those who are also the chair of the board (Gomulya & Boeker, 2016; Guo & Masulis, 2015) are more insulated as they are able to overcome or avoid board attempts at dismissal via their votes (ownership) or their ability to control board meetings and activities via their role as chair. Networking theory has also been used to understand how the CEO’s network of connections (e.g., prestigious and political) can insulate them from calls for dismissal. For instance, being a high-status CEO (Flickinger, Wrage, Tuschke, & Bresser, 2016; Park, Kim, & Sung, 2014) and being connected to high-status individuals (e.g., politicians) (Cao, Pan, Qian, & Tian, 2017; Khanna et al., 2015) enable CEOs to resist calls for dismissal. Furthermore, recent research suggests that male CEOs may have a lower likelihood of dismissal than their female counterparts (Gupta, Mortal, Silveri, Sun, & Turban, 2020).

Board

Some boards are able to dismiss the CEO with little resistance, while others struggle to do so. Indeed, researchers have found that reputed boards (those with more prestigious directors) are more empowered and thus more capable of dismissing CEOs (Masulis & Mobbs, 2014). Similarly, network theory (Burt, 1984) has also been used to examine how the social capital (external ties and prestigious connections) of board directors can positively influence the board’s ability to dismiss CEOs (Flickinger et al., 2016; Harris & Helfat, 2007). However, some board characteristics weaken the board, making it harder to dismiss the CEO. Boards with more co-opted (or beholden) directors (Dou et al., 2015; Khanna et al., 2015) and directors belonging to the same social network as the CEO (Nguyen, 2012) are closer to the CEO and, consequently, less likely to call for dismissal. Similarly, interlocked directors (Devos, Prevost, & Puthenpurackal, 2009) and better paid directors (Chen, Goergen, Leung, & Song, 2019) are less likely to dismiss the CEO as interlocks facilitate reciprocal relationships. Further, board structural characteristics such as classified boards (Ahn & Shrestha, 2013) decrease board monitoring intensity and make dismissal less likely. Interestingly, dysfunction within the board may also deter monitoring and insulate the CEO from dismissal. Indeed, Van Peteghem, Bruynseels, and Gaeremynck (2018) found that fault lines within the board decrease dismissal likelihood. In short, when boards are more powerful than the CEO, they are better positioned to dismiss the CEO when they choose; when boards are relatively weaker, dismissing the CEO becomes much more difficult (Buchholtz, Young, & Powell, 1998; Pearce & Zahra, 1991).

Firm

While poor firm performance is positively related to CEO dismissal, other firm characteristics may affect the performance-dismissal relationship. Positive firm signals (e.g., engagement in corporate social responsibility) are attributed to the quality of leadership provided by CEOs and can insulate them from dismissal (Chen, Zhou, & Zhu, 2019; Chiu & Sharfman, 2018; Hubbard, Christensen, & Graffin, 2017). In contrast, negative firm signals (e.g., high leverage) weaken the CEO’s ability to resist calls for dismissal (Marshall, McCann, & McColgan, 2014). Furthermore, top management team (TMT) characteristics also impact the dismissal process. For example, having an internal talented heir apparent increases the likelihood of CEO dismissal (Mobbs, 2013; Mooney et al., 2017). Thus, if the perceived path of leadership transition is already planned, the disruption from dismissing a CEO may be minimized, so boards are more likely to push for change.

External

The likelihood of CEO dismissal is also dependent on industry dynamics (Eisfeldt & Kuhnen, 2013). CEO dismissal is more common in industries that are competitive (Dasgupta, Li, & Wang, 2018; DeFond & Park, 1999), poorly performing (Peters & Wagner, 2014), and volatile (Peters & Wagner, 2014). However, external factors can also empower CEOs, enabling them to resist calls for dismissal. For example, when powerful stakeholders offer support to CEOs, they can better weather calls for dismissal and limit the board’s ability to enact desired change. For firms that are at least partly state-owned, state-backing empowers the CEO, allowing for entrenchment, making CEO dismissal less likely (Shen & Lin, 2009). Similarly, positive evaluations by external stakeholders, such as favorable recommendations from analysts (Wang et al., 2017; Wiersema & Zhang, 2011), who act as monitors, decrease the likelihood of CEO dismissal.

Outcomes of CEO Dismissal

CEO

Dismissed CEOs seem to be at a disadvantage in the subsequent labor market. Not surprisingly, after dismissal—a salient signal of leadership failure—CEO careers suffer (Fee, Hadlock, & Pierce, 2018). Dismissed CEOs experience diminished opportunities for subsequent employment positions and roles (Ertugrul & Krishnan, 2011; Fee et al., 2018; Humphery-Jenner, 2012; Ward, Sonnenfeld, & Kimberly, 1995), and this effect is similar for other top executives below the CEO (Fee & Hadlock, 2004; Tao & Zhao, 2019). Thus, the dismissal of the CEO sends a clear negative signal that appears to stigmatize them and reduces future career opportunities.

Board

Board-level consequences of CEO dismissal have rarely been addressed in the literature. A notable exception is Florou (2005), who found that after dismissing a CEO, the board chair is often replaced and the board restructured. This finding suggests that, as the board is tasked with overseeing the CEO, the board is penalized for its association with a failed CEO. Board-level outcomes of CEO dismissal are an area where rich research opportunities remain.

Firm

CEO dismissal signals dysfunction within the firm (Dedman & Lin, 2002), which encourages calls to hire an outside successor to reinvigorate the firm and break from established norms (Farrell & Whidbee, 2003). Accordingly, outside successors are often hired after a CEO is dismissed (Cannella & Lubatkin, 1993; Farrell & Whidbee, 2003; Marshall et al., 2014). Following CEO dismissal, subsequent financial performance for the firm frequently improves (Ertugrul & Krishnan, 2011; Gao et al., 2012). However, CEO dismissal also creates volatility and significant disruptions to the firm (Friedman & Saul, 1991; Tao & Zhao, 2019). Firms that dismiss the CEO are prone to subsequent downsizing (Fee, Hadlock, & Pierce, 2013), capital restructuring (Hornstein, 2013), firm delisting (Ertugrul & Krishnan, 2011), and even bankruptcy (Ertugrul & Krishnan, 2011). Furthermore, CEO dismissal signals a failure in leadership and monitoring at other levels within the firm, often resulting in the dismissal of other TMT members (Fee & Hadlock, 2004). Together, these disruptions lead to low employee morale throughout the firm (Friedman & Saul, 1991). Thus, the consequences for CEO dismissal are often poor for the firm.

External

A substantive area where CEO dismissal outcomes have been examined is investor reactions. A positive reaction following CEO dismissal has been observed as CEO change is often welcomed by investors (Cools & van Praag, 2007; Friedman & Singh, 1989; Kim, 2013; Marshall et al., 2014). However, succession problems (e.g., lack of replacement) following dismissal are not well received by investors (Dedman & Lin, 2002). Nor is dismissal well received by investors when it is viewed as premature (proactive or “too soon”), before the CEO has had a chance to enact change (Ertugrul & Krishnan, 2011). Furthermore, Connelly, Li, Shi, and Lee, (2020) found the dismissal of a CEO impacted the risk taking of other CEOs within their industry, demonstrating that the dismissal of one CEO can have ramifications for other firms as well as for the industry as a whole.

Moderators of the Outcomes of CEO Dismissal

CEO

CEO factors can also indirectly impact outcomes of their dismissal. Perceptions about CEO character and ability that may have led to dismissal impact their future career trajectories by signaling capabilities (or lack thereof) to effectively lead a firm in the future. For example, dismissal because of serious indiscretions (e.g., personal scandals) decreases the likelihood of the CEO finding employment after dismissal (Schepker & Barker, 2018; Ward et al., 1995). Yet, it seems some CEOs are able to weather dismissal better than others. From a network theory perspective (Burt, 1984), having social and reputational capital aids dismissed CEOs in finding subsequent employment (Nguyen, 2012; Schepker & Barker, 2018). Other CEO characteristics, such as demographic attributes, also impact their careers post-dismissal. For example, older CEOs who are dismissed are less likely to find executive employment (Ertugrul & Krishnan, 2011; Ward et al., 1995) but more likely to attain advisory roles (Ward et al., 1995).

Board

Many outcomes of CEO dismissal are also contingent on board-level factors. As noted earlier, board chairs are likely to be replaced, particularly when they oversaw the selection of the dismissed CEO (Florou, 2005). The replacement of the board chair seems to be an indictment of their monitoring and leadership abilities and, consequently, a “settling up” for their failure. Board characteristics also play a role in selecting the next successor to lead the firm. Following the dismissal of a CEO, boards with more outside directors are more likely to hire an external successor (Borokhovich, Parrino, & Trapani, 1996), while boards with more inside directors are more likely to hire an internal successor (Shen & Cannella, 2002b). These findings speak to entrenchment due to lack of independence within the board. Furthermore, board characteristics exert influence on subsequent firm performance. For instance, board independence strengthens the ability of newly appointed CEOs to enact strategic change as they are better able to work with the board, but only when the incoming CEO is an outsider (Schepker et al., 2017).

Firm

Firm factors also exert influence on the outcomes of CEO dismissal. For the CEO, poor firm performance prior to dismissal (Ward et al., 1995) and dismissal following negative events (e.g., fraud and violations) signal poor leadership and decrease subsequent employment opportunities (Desai, Hogan, & Wilkins, 2006). Firm factors pre-dismissal also moderate firm outcomes post-dismissal. Firm performance prior to dismissal impacts the trajectory of the firm post-dismissal as poorly performing firms are more likely to hire an outside successor (Cannella & Lubatkin, 1993; Huson, Parrino, & Starks, 2001; Schwartz & Menon, 1985) and experience subsequent improvements in performance (Shen & Lin, 2009). However, firms performing well prior to dismissal experience a decline in performance post-dismissal (Shen & Lin, 2009). Furthermore, TMT turnover following dismissal further weakens subsequent performance, but only when an outside successor is appointed as the new CEO (Shen & Cannella, 2002a).

External

External factors can also moderate the relationship between dismissal and outcomes. Shareholder lawsuits curtail the dismissed CEO’s ability to attain subsequent board and executive positions (Humphery-Jenner, 2012). Firm outcomes are also impacted by external factors. For example, state ownership signals confidence and buoys firm performance, following CEO dismissal (Shen & Lin, 2009). Furthermore, declining institutional ownership prior to CEO dismissal is positively related to hiring an outside successor (Parrino, Sias, & Starks, 2003), presumably because it signals discontent with firm leadership and a desire for change.

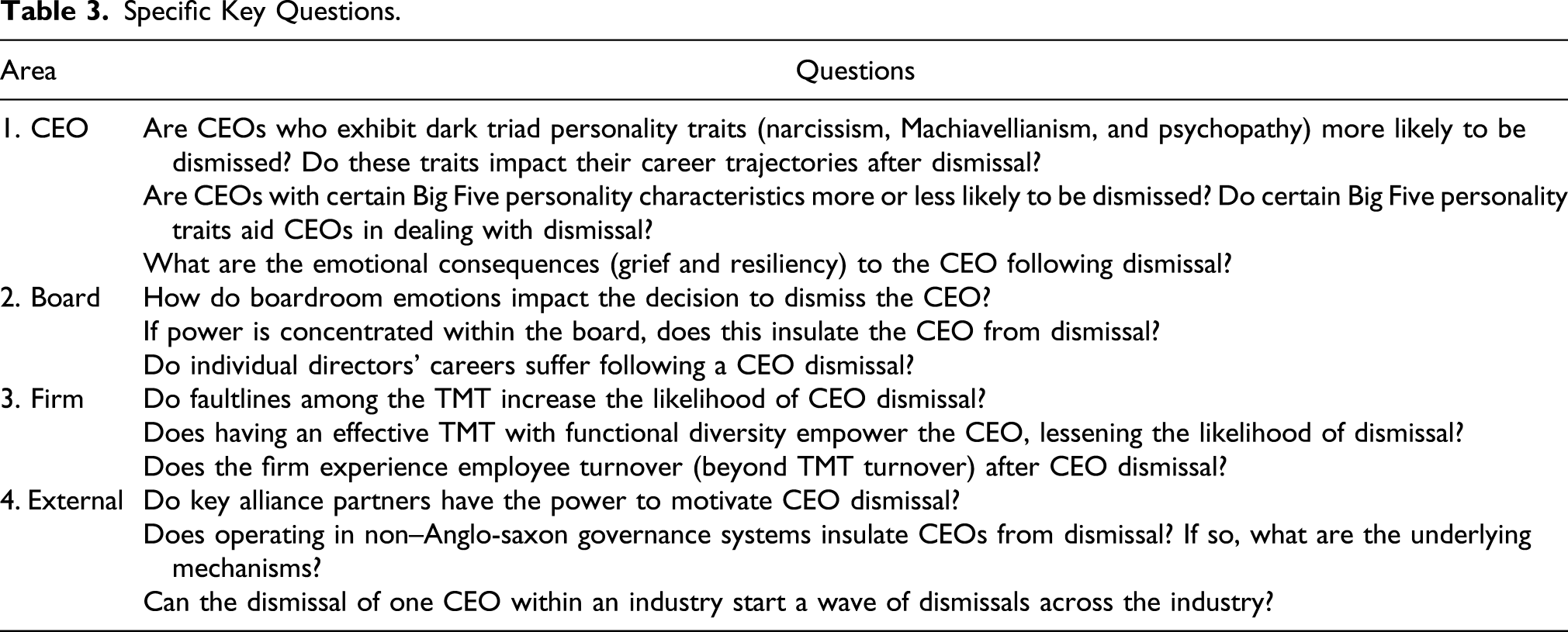

The Future of CEO Dismissal: Where Do We Go?

Specific Key Questions.

CEO

Microlevel theoretical lenses have been employed to understand how CEO attributes such as optimism (Campbell, Gallmeyer, Johnson, Rutherford, & Stanley, 2011) and role congruity (Gupta et al., 2020) are positively associated with CEO dismissal. Yet, similar research grounded in microlevel theory on personality characteristics facilitating CEO dismissal is limited, leaving ample opportunities for future scholars. Specifically, individuals with personality traits such as narcissism, Machiavellianism, and psychopathy (i.e., the dark triad) are associated with disagreeableness (Paulhus & Williams, 2002). While these traits are also associated with poor job performance and counterproductive work behavior, being in an authority position (e.g., CEO) may moderate these relationships (Forsyth, Banks, & McDaniel, 2012). Given the interesting dynamic between the dark triad and leadership, research is warranted to ascertain whether the dark triad is indeed facilitative of CEO dismissal and whether these characteristics impact the subsequent careers of dismissed CEOs.

Furthermore, our review did not uncover any studies that delved into the Big Five personality characteristics (Barrick & Mount, 1991; Goldberg, 1990) of CEOs and dismissal. This is surprising as the Big Five personality traits have been widely studied and seem particularly important in shaping how people lead (Judge & Bono, 2000; Judge, Heller, & Mount, 2002). On the one hand, high levels of certain Big Five personality characteristics, such as openness to experience and conscientiousness, would seem to be beneficial for CEOs facing calls for dismissal. On the other hand, high levels of other Big Five personality characteristics, such as neuroticism, would seem to be detrimental to the CEO and hasten CEO dismissal. Thus, future research should unpack if and how the Big Five personality dimensions facilitate or insulate CEOs from dismissal and how these traits impact how dismissed CEOs deal with dismissal.

Given the ongoing “affective revolution” in organizational literature (Ashkanasy & Dorris, 2017; Grandey, 2008), it is surprising that the emotional consequences of CEO dismissal have gone largely unnoticed in the literature. While the dismissal of the CEO is certainly disruptive for the firm (Friedman & Saul, 1991; Tao & Zhao, 2019), the effects on the CEO have received little attention. To date, we have only found a handful of studies that examine CEO outcomes, all of which focus on subsequent career opportunities (e.g., Ertugrul & Krishnan, 2011; Fee et al., 2018; Humphery-Jenner, 2012; Ward et al., 1995). Yet, this career focus ignores the potential mental toll that dismissal has on the CEO. Thus, scholars need to examine the effects of dismissal on emotions (e.g., shame or grief), perspectives (e.g., fairness), and behavior (e.g., resiliency). Many dismissed CEOs probably want to helm another firm, so factors affecting their future leadership ability and potential seem worthy of future study.

Board

Details of how boards dismiss CEOs are often difficult to ascertain (Leblanc & Schwartz, 2007). Thus, opportunities remain in disentangling board discussions preceding dismissal, specifically, the emotional tone of these discussions. The emotional tone, or the degree to which conversations elicit positive or negative affect (Ashkanasy, Humphrey, & Huy, 2017; Kelly & Barsade, 2001), offers information on the emotional state and changes in the direction of discussion as emotions change (see emotional contagion; Barsade, 2002). The emotional state in which the board finds itself when discussing the fate of the CEO, and if and how it changes, is of importance to understanding their ultimate decision. Yet, we found no studies exploring the emotional dynamics within the boardroom preceding CEO dismissal. This omission is surprising given the extent of the literature on emotions within groups and considering the pressure that exists as the board tries to make a decision as significant as dismissing a CEO.

Several studies identify board power as a key facilitator of CEO dismissal (e.g., Alam et al., 2014; Boeker, 1992; Conyon & He, 2011; Ertugrul & Krishnan, 2011), but we did not find any research that examined the concentration of that power within the board. One way the power can be concentrated within the board is by a few select directors dominating committee appointments, since much of the work of the board takes place in committees (Bilimoria & Piderit, 1994; Jiraporn, Singh, & Lee, 2009; Kesner, 1988). If power is concentrated among a few corporate elite (or in-group) directors, the CEO may be insulated from dismissal. Social identity theory suggests that dominant in-group members will exert control over out-group members (Tajfel, Billig, Bundy, & Flament, 1971; Tajfel & Turner, 1986). Thus, future researchers need to assess whether concentrated power among in-group board members impacts CEO dismissal.

Finally, opportunities remain to examine the subsequent career impact of the board’s decision to dismiss the CEO on the individual directors. Notably, Florou (2005) found that the chair of the board as well as other board members are likely to leave the board following CEO dismissal, which is consistent with Fee and Hadlock (2004)’s finding that other TMT members leave following CEO dismissal, subsequently detrimentally impacting their careers. However, opportunities remain to study the subsequent career impact on directors associated with dismissed CEOs. One would expect that board members, who are tasked with monitoring the CEO, particularly the members of the nominating committee, may be substantively impacted following CEO dismissal. Given that the dismissal of a CEO may be seen as an acknowledgment of failure to adequately oversee the CEO, calling into question their ability to effectively monitor, the board members involved may suffer similar career setbacks (e.g., fewer and less prestigious directorships), which seem a fertile area for future inquiry.

Firm

Our review revealed little about the relationship between dismissal and the dynamics of the TMT—a key firm-level factor. 3 This absence is surprising as, next to the CEO, the TMT is critical to organizational functioning. Indeed, group dynamics between the TMT and the CEO are integral to firm performance (Peterson, Smith, Martorana, & Owens, 2003). For example, faultlines—attribute-based group divisions (Lau & Murnighan, 1998)—within the TMT could create dysfunction within the leadership of the firm. While faultlines within the board have been found to reduce effectiveness and decrease the likelihood of CEO dismissal (Van Peteghem et al., 2018), the relationship between CEO dismissal and faultlines within the TMT has yet to be examined. Indeed, faultlines among the TMT would seem to have the opposite effect: facilitating dismissal by increasing dysfunction within the upper echelons of the firm. Given the growing attention to TMT faultlines in the broader literature (Bunderson & Van der Vegt, 2018), attending to this area within the CEO dismissal literature seems warranted.

Another key characteristic of firms is the functional diversity of the TMT. While prior literature has found that CEOs with diverse functional expertise relevant to the firm are less likely to be dismissed as they have made themselves integral to the firm (Oehmichen et al., 2017), opportunities remain in exploring the relationship between TMT functional diversity and CEO dismissal. The relationship between the CEO and TMT is integral to firm functioning (Peterson et al., 2003). Collaborative, well-functioning TMTs with diverse functional backgrounds improve firm performance (Boone & Hendriks, 2009; Cannella, Park, & Lee, 2008), but this improvement is contingent on the relationship with the CEO (Buyl, Boone, Hendriks, & Matthyssens, 2011). Therefore, if CEOs are surrounded by suitable or appropriate TMTs, they are better positioned for success. We encourage future scholars to explore whether CEOs who have collaborative, functionally diverse, and adept TMTs better weather calls for dismissal.

CEO dismissal causes significant upheaval within firms (Friedman & Saul, 1991; Tao & Zhao, 2019). Indeed, restructuring (Hornstein, 2013) and downsizing (Fee et al., 2013) have been observed following CEO dismissal. Consequently, CEO dismissal has been observed to diminish employee morale arising from the sudden instability employees face (Friedman & Saul, 1991), and low morale motivates employee turnover (Staw, 1980). While previous research has noted that TMT turnover follows CEO dismissal (Fee & Hadlock, 2004), whether the broader workforce of the firm turns over disproportionately following CEO dismissal remains to be seen. This question is vital as employees form the backbone of any organization (Liu, Combs, Ketchen, & Ireland, 2007), and employee turnover would further exacerbate disruption within the organization (Shaw, 2011).

External

While several key external stakeholders, such as institutional owners (Helwege et al., 2012; Wu, 2004), analysts (Wiersema & Zhang, 2011), and the media (Bednar, 2012), have been examined in the CEO dismissal literature, exploring other key stakeholders presents an opportunity for future scholars. For example, alliance partners form key relationships for firms, allowing for resource complementarity and performance benefits (Lunnan & Haugland, 2008; Robson, Katsikeas, Schlegelmilch, & Pramböck, 2019). Our review revealed an opportunity for researchers to explore how relationships with alliance partners impact CEO dismissal. Since alliance partners are key stakeholders, we encourage future researchers to examine whether the presence of alliance partners, particularly powerful ones, can facilitate CEO dismissal when they voice concerns about the CEO (similar to shareholders, analysts, and the media).

Academic understanding of CEO dismissal is derived largely from Anglo-Saxon systems of corporate governance (Hilger et al., 2013). However, in non–Anglo-Saxon contexts, banks and governments (rather than shareholders) are often prominent stakeholders, which concentrate ownership and lend greater emphasis to long-term performance (Weimer & Pape, 1999). In examining a non–Anglo-Saxon setting (namely, China), Shen and Lin (2009) found the performance-dismissal relationship to be less sensitive than in Anglo-Saxon contexts, suggesting a fundamentally different view from most research in the area. Thus, the institutional environment in which the firm operates may insulate the CEO from dismissal pressure, but future research needs to further flesh out how specific differences (e.g., state vs. bank vs. family vs. employee-dominated stakeholder systems) impact CEO dismissal.

Finally, opportunities remain in examining the external implications of CEO dismissal. Morgeson, Mitchell, and Liu (2015) proposed event system theory to understand the spillover (and potentially interactive) effects of critical episodes at different levels (environment, organization, team, and individual) of the firm. Dismissing the CEO would certainly constitute an impactful event capable of having such spillover effects. In this vein, Connelly et al. (2020) recently found that CEO dismissal at one firm induces heightened fears of job insecurity among CEOs at competing firms. Yet, whether the dismissal of a CEO at one firm actually leads to a wave of dismissals at other firms remains to be investigated. If this scenario is indeed the case, the competitive landscape of industries could drastically change with the dismissal of just one CEO, creating a possible domino effect. Thus, future research needs to continue to examine how the dismissal of one CEO impacts the broader environment and the stakeholders therein.

Conclusion

CEOs are at the helm of the organizational hierarchy of their firms. Consequently, CEO dismissals are pivotal events with significant effects for organizations and individuals. The rate of CEO dismissal has grown substantially in recent years as has the literature exploring CEO dismissal. Yet, within this burgeoning literature, many theoretical and empirical opportunities remain. In this critical synthesis, we seek to add value to the field by summarizing, organizing, and analyzing what is currently known about CEO dismissal across four key levels (CEO, board, firm, and external), forming the basis for our identification of fertile research opportunities for future inquiry.

Supplemental Material

sj-pdf-1-gom-10.1177_1059601120987452 – Supplemental Material for Chief Executive Officer Dismissal: A Multidisciplinary Integration and Critical Analysis

Supplemental Material, sj-pdf-1-gom-10.1177_1059601120987452 for Chief Executive Officer Dismissal: A Multidisciplinary Integration and Critical Analysis by John P. Berns, Vishal K. Gupta, Karen A. Schnatterly and Clarissa R. Steele in Group & Organization Management

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Associate editor: Lucy Gilson.

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.