Abstract

Prior empirical research investigating the relationship between chief executive officer (CEO) tenure and firms’ financial performance has shown inconclusive results. Based on arguments of agency and behavioral agency theories, we suggest that this relationship is nuanced and may vary depending on CEO pay and board monitoring. In response to these arguments, we meta-analytically test 385 studies (n = 1,029,602). We find that CEO tenure is positively related to firms’ financial performance. This positive relationship is enhanced when CEOs receive higher cash compensation or hold more stock ownership. On the other hand, the above positive relationship becomes weaker when CEOs receive higher long-term incentives or when the firm has more independent board directors. These findings suggest that CEO pay and board monitoring, or agency mechanisms in general, can offer new research avenues to help explore boundary conditions of the CEO tenure and firms’ financial performance relationship.

Keywords

According to agency theory, the lack of interest alignment between chief executive officers (CEOs) and shareholders results in agency problems, such as shirking (e.g., Biggerstaff, Cicero, & Puckett, 2017), entrenchment (e.g., Finkelstein & D’aveni, 1994), risk aversion (e.g., Stroh, Brett, Baumann, & Reilly, 1996), or other managerial opportunistic behaviors that deteriorate firms’ financial performance (Eisenhardt, 1989; Jensen & Meckling, 1976; Nyberg, Fulmer, Gerhart, & Carpenter, 2010). This interest misalignment is likely to occur when the goals of CEOs and shareholders diverge (e.g., CEOs and shareholders hold conflicting goals), when shareholders are unable to adequately monitor CEOs’ actions (e.g., information asymmetry exists between CEOs and shareholders), or when CEOs’ actions entail risks (e.g., CEOs forgo risky but potentially profitable investments) (Eisenhardt, 1989; Jensen & Meckling, 1976; Stroh et al., 1996). A specific consideration of agency theory is the career length of a CEO (Eisenhardt, 1989). CEO tenure, which refers to the length of time an individual has occupied the CEO position, strongly affects CEOs’ interest alignment with those of shareholders and their firms’ financial performance (Eisenhardt, 1989; Finkelstein & Hambrick, 1990; Hambrick, 2007; Hambrick & Mason, 1984; Jensen & Meckling, 1976; Wiseman & Gomez-Mejia, 1998). It is thus not surprising that many studies have devoted much attention to understanding how a CEO’s time in office affects his/her firms’ financial performance (e.g., Hambrick & Fukutomi, 1991; Henderson, Miller, & Hambrick, 2006; Leonard-Barton, 1992; McClelland, Barker, & Oh, 2012; Miller, 1991; Miller & Shamsie, 2001; Simsek, 2007; Wang, Holmes, Oh, & Zhu, 2016). However, prior studies have presented conflicting insights and inconclusive findings.

On the one hand, some studies have suggested that the relationship between CEOs and shareholders becomes more efficient as CEOs remain in their position for longer periods (Eisenhardt, 1989). This is because CEOs and shareholders learn about each other during their long-term relationship (Eisenhardt, 1989). Over time, shareholders gain more information about CEOs’ actions to assess their behaviors more readily, and CEOs are less likely to hold conflicting goals with shareholders (Eisenhardt, 1989). In addition, long-tenured CEOs have more experience than their short-tenured counterparts in dealing with strategic risks and are better at selecting, assessing, and executing the strategic risk-taking process (Simsek, 2007). Thus, they would be more willing and ready to become involved in situations that require necessary strategic risk-taking (Simsek, 2007). Therefore, proponents of long-tenured CEOs propose a positive relationship between such tenure and firms’ financial performance (e.g., Brockmann & Anthony, 2002; Simsek, 2007; Simsek, Veiga, Lubatkin, & Dino, 2005; Zhang, 2008). For example, examining a sample of 495 firms and their CEOs, Simsek (2007) finds that CEO tenure has a positive effect on the top management team’s risk-taking propensity and thus increases firms’ financial performance. Observing a sample of 104 acquisitions over 5 years, Bergh (2001) shows that longer-tenured top executives are associated with more successful acquisition outcomes, and that there is no evidence of negative effects of longer tenure such as strategic status quo and rigidity.

On the other hand, some studies have expressed concerns that the interest misalignment between CEOs and shareholders is more likely to occur if CEOs stay longer in their position as they can have more power and exert over the board of directors for their own interests (Hill & Phan, 1991; Miller, 1991). For example, long-tenured CEOs may resist important requests from stakeholders (Miller, 1991), nominate favored board members (Westphal, 1999) to minimize dissent (Acharya & Pollock, 2013; Zajac & Westphal, 1996), or exert power to accommodate a weaker link between firms’ performance and their own pay (Buchholtz, Young, & Powell, 1998; Hill & Phan, 1991). Therefore, even though shareholders learn more about CEOs in a long-term relationship (Eisenhardt, 1989), long-tenured CEOs may have more opportunities to misinform shareholders and pursue conflicting goals, as they gain more power. In addition, some studies have pointed out that long-tenured CEOs are more inclined to forgo risky but potentially profitable investments to protect their existing legacies (Matta & Beamish, 2008; Miller, 1991). Therefore, opponents of long-tenured CEOs have argued that the relationship between such tenure and firms’ financial performance is negative (e.g., Henderson et al., 2006; Leonard-Barton, 1992; McClelland et al., 2012). For example, in a sample of 104 firms and their CEOs, Hill and Phan (1991) report that CEOs’ tenure weakens the relationship between CEO pay and firms’ stock return because CEOs’ board influence increases with tenure. In another study, utilizing a sample of 95 firms, Miller (1991) finds that long-tenured CEOs are worse at matching their firms’ strategy and structure to the challenges posed by the environment, which resulted in their firms’ lower financial performance.

One possible explanation for these conflicting findings may be that the effect of CEO tenure on firms’ financial performance is conditional on other factors that increase or decrease the interest alignment between CEOs and shareholders. We propose that agency and behavioral agency theories provide vital directions in searching for such contingent factors. To mitigate agency problems, agency theory suggests using stock-based incentives to align the interests of CEOs with those of shareholders and board monitoring to mitigate CEOs’ opportunistic behaviors (Beatty & Zajac, 1994; Eisenhardt, 1989; Jensen & Meckling, 1976). More specifically, it is suggested that stock-based incentives help mitigate agency problems by tying CEOs’ managerial compensation and personal wealth to firms’ financial performance (Eisenhardt, 1989; Jensen & Meckling, 1976). The theory also suggests that board monitoring ensures that CEOs act in shareholders’ best interests, and that an independent board (e.g., more independent board directors) is more vigilant in monitoring CEOs’ actions (Eisenhardt, 1989; Jensen & Meckling, 1976; Westphal, 1998).

Drawing from prospect theory, behavioral agency theory further elaborates on the agency-based views of executive risk-taking (Kahneman & Tversky, 1979; Wiseman & Gomez-Mejia, 1998). According to behavioral agency theory, when decision makers are exposed to greater downside risks, they exhibit a stronger preference for risk aversion (Kahneman & Tversky, 1979; Wiseman & Gomez-Mejia, 1998). Alternatively, when decision makers have nothing to lose but something to gain, they exhibit a stronger preference for risk-seeking (Kahneman & Tversky, 1979; Wiseman & Gomez-Mejia, 1998). In this sense, CEOs are not simply risk-averse as assumed by traditional agency theory, but rather loss-averse (Wiseman & Gomez-Mejia, 1998). When making a decision, they tend to pay greater attention to downside risks rather than the upside potential and may even prefer riskier options if these options help them avoid losses (Wiseman & Gomez-Mejia, 1998). As such, behavioral agency theory argues that stock-based incentives and board monitoring may have more nuanced implications on agency problems than what traditional agency theory suggests (Dalton, Daily, Ellstrand, & Johnson, 1998; Lim & McCann, 2013; Sanders, 2001; Sanders & Hambrick 2007; Wiseman & Gomez-Mejia, 1998). For example, Sanders (2001) reports that CEOs with more stock ownership are exposed to greater downside risks if the stock price declines, while those who hold more stock options have minimal downside risks. Likewise, intense board monitoring can increase CEOs’ perceived downside risks and make them more risk-averse. CEOs facing intense board monitoring may intentionally avoid risky investments if they believe that making such investments increase the likelihood of negative outcomes, such as dismissal (Goranova, Priem, Ndofor, & Trahms, 2017). It then follows that stock-based incentives and board monitoring may not always help mitigate agency problems, especially when CEOs are exposed to greater downside risks and have something to lose.

In this article, we conduct a meta-analysis on the relationship between CEO tenure and firms’ financial performance based on agency theory. We also utilize the elaborated agency-based views of behavioral agency theory to investigate three types of CEO pay (i.e., cash compensation, long-term incentives, and stock ownership) and board monitoring (i.e., the board’s independent director ratio). We consider the abovementioned factors to be potential moderators of the relationship between CEO tenure and firms’ financial performance. We specifically chose these three types of CEO pay because they broadly represent the forms of CEO compensation and are substitutions of one another (Matta & McGuire, 2008). Since these three types of CEO pay expose CEOs to different levels of downside risks, they may exhibit different incentive effects and moderate the effect of CEO tenure on firms’ financial performance differently. In addition, we study the board’s independent director ratio as a moderator because it is a gauge of board independence and reflects the intensity of board monitoring (Eisenhardt, 1989; Jensen & Meckling, 1976; Westphal, 1998). Although board independence increases the vigilance of board monitoring (Eisenhardt, 1989; Jensen & Meckling, 1976; Westphal, 1998), recent studies have suggested that intense board monitoring can be costly since it weakens CEOs’ perceived board support and exposes them to greater downside risks (e.g., Matta & McGuire, 2008). An investigation of the board’s independent director ratio allows us to understand the moderating effect of intense board monitoring on the relationship between CEO tenure and firms’ financial performance.

We believe a meta-analysis is needed to advance the conversation on the impact of CEO tenure on financial performance. First, as detailed previously, extant studies have presented conflicting insights and inconclusive findings of this relationship. Since meta-analytic techniques provide more precise estimates of population characteristics (Hunter & Schmidt, 1990), a meta-analysis can help generalize findings and reduce concerns about sampling errors (Combs, Ketchen, Crook, & Roth, 2011; Homberg & Bui, 2013). Second, extant studies have not thoroughly examined agency mechanisms as contingent factors that moderate the relationship between CEO tenure and firms’ financial performance. A meta-analysis can help reassess and extend existing theories (Combs et al., 2011). Third, the impact of CEO tenure could change due to the nuances of study design. Previous studies have often relied on accounting performance (e.g., return on assets [ROA]) or market performance (e.g., Tobin’s Q); however, the relationship between CEO tenure and firms’ financial performance may vary depending on the use of different performance measures. A meta-analysis can systematically investigate these nuances and provide more comprehensive findings (Jeong & Harrison, 2017). In particular, we examine a total of 385 studies (n = 1,029,602) that report the correlation between CEO tenure and firms’ financial performance and find that CEO tenure is positively related to firms’ financial performance. We further find that this positive relationship is enhanced when CEOs receive higher cash compensation or hold more stock ownership, and that this relationship is weakened when CEOs receive higher long-term incentives or when the board has more independent board directors.

Theory and Hypotheses Development

Agency and Behavioral Agency Theories

Agency theory suggests that agency problems may arise when principals delegate authority to agents who perform tasks on behalf of the principals in a contractual relationship (Jensen & Meckling, 1976). Since a firm is based on complex contracts, management researchers use agency theory to examine the relationship between agents (in our study, CEOs) and principals (in our study, shareholders) within the organization (Eisenhardt, 1989). More specifically, two agency problems exist that may hurt shareholders’ interests in firms.

One agency problem arises when agents and principals have divergent interests, and shareholders have imperfect information about agents’ actions (Eisenhardt, 1989; Jensen & Meckling, 1976). For example, CEOs may spend firm resources for their own leisure activities even though it can undermine firms’ profitability (Biggerstaff et al., 2017; Jensen & Meckling, 1976). The other agency problem arises when agents and principals have different preferences for risk-taking. Principals are risk-neutral because they can diversify risks by investing in multiple options, while agents are risk-averse because they may not be able to diversify risks associated with their employment (Jensen & Meckling, 1976). As such, agents may make suboptimal decisions at the expense of principals’ interests (Eisenhardt, 1989; Jensen & Meckling, 1976). For example, CEOs may forgo risky but potentially profitable projects (Stroh et al., 1996). To mitigate these agency problems, management researchers have suggested using stock-based incentives and board monitoring to align agents’ interests with those of principals (Beatty & Zajac, 1994; Eisenhardt, 1989; Jensen & Meckling, 1976). Agents could have an incentive to maximize principals’ returns when their compensation is outcome based, and when the board of directors can effectively monitor their actions (Eisenhardt, 1989; Jensen & Meckling, 1976).

Behavioral agency theory further suggests that stock-based incentives and board monitoring may not always align agents’ interests with those of principals, especially when agency mechanisms create a perceived loss for agents (Dalton et al., 1998; Lim & McCann, 2013; Sanders, 2001; Sanders & Hambrick, 2007; Wiseman & Gomez-Mejia, 1998). Specifically, behavioral agency theory extends traditional agency theory by integrating elements of prospect theory and elaborating on the agency-based views of executive risk-taking (Wiseman & Gomez-Mejia, 1998). It argues that agents compare anticipated outcomes from available options against a reference point when making decisions (Kahneman & Tversky, 1979; Lant, 1992; Wiseman & Gomez-Mejia, 1998). Agents care more about downside risks that may result in a loss of wealth rather than upside potentials that may lead to an increase in wealth (Kahneman & Tversky, 1979; Wiseman & Gomez-Mejia, 1998). In this sense, they are not simply risk-averse, as suggested by traditional agency theory, but rather loss-averse (Wiseman & Gomez-Mejia, 1998). For example, when making strategic decisions, CEOs usually create subjective reference points using their compensation plan to examine whether they are in a loss or gain context (Pepper & Gore, 2015). As such, the efficacy of stock-based incentives and board monitoring then largely depends on agents’ perception of losses resulting from these agency mechanisms.

To conclude, agency theory provides a theoretical foundation for understanding the relationship between CEO tenure and firms’ financial performance since it fundamentally explains agency problems that may arise during the length of CEO tenure (Eisenhardt, 1989). Behavioral agency theory further extends agency theory by elaborating on the agency-based views of executive risk-taking (Wiseman & Gomez-Mejia, 1998). It allows for more nuanced interpretations of CEO pay and board monitoring as contingencies of the relationship between CEO tenure and firms’ financial performance.

CEO Tenure and Firm Financial Performance

Prior studies on the relationship between CEO tenure and firms’ financial performance have shown conflicting insights and inconclusive findings. On the one hand, proponents of long-tenured CEOs suggest a positive relationship between CEO tenure and firms’ financial performance (e.g., Brockmann & Anthony, 2002; Gulati & Westphal, 1999; Simsek, 2007; Simsek et al., 2005; Zhang, 2008). First, it has been suggested that the relationship between CEOs and shareholders becomes more efficient as CEOs remain in their positions longer because the length of the relationship increases their interest alignment (Eisenhardt, 1989). When shareholders learn more about CEOs over a long-term relationship, they can assess their actions more readily (Eisenhardt, 1989) and develop an accurate picture of the CEOs’ ability (Tosi, Katz, & Gomez-Mejia, 1997). Long-tenured CEOs also become better at understanding and interpreting shareholders’ interests (Hendry, 2002). Thus, the information asymmetry between long-tenured CEOs and shareholders is likely to be smaller, and long-tenured CEOs and shareholders are less likely to hold conflicting goals (Eisenhardt, 1989). The firms’ financial performance will, in turn, be much higher. For example, Zhang (2008) reports that short-tenured CEOs are associated with a much higher dismissal rate than long-tenured CEOs because of greater information asymmetry between these short-tenured CEOs and shareholders. The dismissals result in organizational disruption and substantially lower firms’ financial performance (Zhang, 2008). Gulati and Westphal (1999) state that a long-term relationship between CEOs and shareholders enhances cooperation, thereby increasing firms’ performance. Second, it is also suggested that long-tenured CEOs are better at selecting, assessing, and executing the strategic risk-taking process than their short-tenured counterparts (Simsek, 2007). A long-term relationship also reduces CEOs’ perceived risks because shareholders have more experience with CEOs and can differentiate between mismanagement and factors outside their control (Tosi et al., 1997). As such, long-tenured CEOs are more willing and ready to take necessary strategic risks, increasing the interest alignment with shareholders and firms’ financial performance. For example, Simsek (2007) finds that long-tenured CEOs increase the top management team’s risk-taking propensity and firms’ financial performance. As he explains, firms can benefit in the long run from risky investment through exploration and exploitation. Barker and Mueller (2002) report that long-tenured CEOs have a greater ability to shape research and development (R&D) spending, which increases firms’ long-term performance. Bergh (2001) also finds that long-tenured CEOs are associated with better acquisition outcomes and firms’ financial performance because of a more intimate understanding of their own firms, as well as the risk and uncertainties involved in the corporate acquisition process.

On the other hand, opponents of long-tenured CEOs suggest that the relationship between CEO tenure and firms’ financial performance is negative (e.g., Henderson et al., 2006; Leonard-Barton, 1992; McClelland et al., 2012). First, it has been suggested that the longer the CEOs’ tenure, the more power they can exert to advance personal interests over the board (Hill & Phan, 1991; Miller, 1991). Although CEOs and shareholders learn more about each other in a long-term relationship (Eisenhardt, 1989), long-tenured CEOs simultaneously gain more power to behave opportunistically and deteriorate firms’ financial performance. Such opportunistic behaviors include, but are not limited to, resisting important requests from stakeholders (Miller, 1991), nominating favored board members (Westphal, 1999) to minimize dissent (Acharya & Pollock, 2013; Zajac & Westphal, 1996), and exerting power to accommodate a weaker link between firms’ performance and CEO pay (Buchholtz et al., 1998; Hill & Phan, 1991). For example, Hill and Phan (1991) suggest that CEOs’ board influence substantially increases with their tenure, and long-tenured CEOs tend to withhold relevant information, which allows them to blame the board for poor firm performance. Biggerstaff et al. (2017) find that some CEOs shirk their responsibilities, causing lower firm performance. Even more interestingly, the study finds that long-tenured CEOs who shirk duties often avoid discipline, but short-tenured CEOs who do so are more likely to be replaced by the board (Biggerstaff et al., 2017). Second, it is also suggested that long-tenured CEOs often refuse to take necessary strategic risks because such risks may jeopardize their existing legacies (Matta & Bearish, 2008; Miller, 1991). Such CEOs are overprotective about their existing paradigm (Wang et al., 2016) and require a higher risk premium to effectively align their interests with those of shareholders (Hou, Priem, & Goranova, 2017). Therefore, long-tenured CEOs are likely to forgo risky but potentially profitable investments that harm firms’ financial performance in the long run. For example, Miller (1991) reports that long-tenured CEOs are less likely to match their firms’ strategy and structure with challenges posed by the environment, and this lack of alignment can have a negative impact on firms’ financial performance. Such resistance against necessary risk-taking is particularly harmful in a more dynamic environment since long-tenured CEOs become wedded to their existing paradigm that may suddenly become obsolete (Hambrick & Fukutomi, 1991). Hill and Phan (1991) comment that long-tenured CEOs are more inclined to invest in projects that increase the size and scope of their firms, while less willing to risk their careers in risky investments. These risk-averse actions will lead to an increase in firm size but a decrease in shareholders’ return. With these conflicting rationales in mind, we suggest the following competing hypotheses.

CEO Pay

We examine the moderating effects of three types of CEO pay: cash compensation, long-term incentives, and stock ownership. 1 Among these three types of CEO pay, long-term incentives and stock ownership are outcome based. They are designed to tie CEOs’ personal wealth to firms’ financial performance and thus increase the interest alignment between CEOs and shareholders (Eisenhardt, 1989; Jensen & Meckling, 1976). Many studies have documented the extensive use of outcome-based pay and its increasing substitutions as cash compensation (e.g., Matta & McGuire, 2008). However, behavioral agency theory points out that different types of CEO pay expose CEOs to different levels of downside risks and thus may exhibit heterogeneous incentive effects (Wiseman & Gomez-Mejia, 1998). Even stock options and stock ownership, which are commonly viewed as having congruent incentive effects, may affect CEOs’ actions differently because of asymmetric risk characteristics (Sanders, 2001).

We define CEO cash compensation as the CEO’s annual base salary plus any cash bonus. We argue that CEO cash compensation helps align interests of CEOs with those of shareholders, and thus positively moderates the relationship between CEO tenure and firms’ financial performance. First, CEOs that receive higher cash compensation (i.e., a higher proportion of cash compensation relative to CEOs’ total compensation) exhibit stronger preferences of necessary strategic risk-taking. The rationale for such preferences is that cash compensation is relatively consistent over time, and there is no evidence showing that CEO cash compensation is more sensitive to firms’ poorer financial performance than to better performance (Larraza-Kintana, Wiseman, Gomez-Mejia, &, Welbourne, 2007; Shaw & Zhang, 2010). Thus, CEOs, whose primary pay is in cash form, tend to perceive lower downside risks when making a decision and less likely to be risk-averse. Several studies have made similar arguments. For example, Guay (1999) finds that CEOs with higher cash compensation are less risk-averse and help improve their firms’ financial performance by investing more outside the firm. Bloom and Milkovich (1998) report that managers’ risk-averse behaviors can be mitigated by increasing managers’ annual base salary and that firms achieve better financial performance when CEOs receive more cash compensation. Knight, Durham, and Locke (2001) also suggest that when decision makers’ pay is not contingent upon goal attainment, they are more likely to take necessary strategic risks to achieve higher firms’ performance. Second, the level of information asymmetry between CEOs and shareholders is lower when CEOs receive higher cash compensation. Since performance volatility may not threaten CEOs’ current wealth, they are less likely to withhold vital information from shareholders, which increases information flow between the two parties (Shaw & Zhang, 2010). For example, Fong (2010) suggests that CEO pay can influence CEOs’ opportunistic behaviors, particularly regarding R&D spending. The study suggests that firms can use more cash compensation to reduce the information asymmetry regarding R&D activities, which improve the alignment of interests between CEOs and shareholders (Fong, 2010). Balkin, Markman, and Gomez-Mejia (2000) also point out that firms should increase the use of cash compensation to align the interests of CEOs with those of shareholders and reduce the information asymmetry.

Taken together, CEOs whose primary pay is in cash form are exposed to lower downside risks and thus tend to exhibit a stronger preference to take necessary strategic risks. They are also less likely to withhold vital information from shareholders, and therefore, the information asymmetry between CEOs and shareholders is lower. As such, CEO cash compensation tends to positively moderate the relationship between CEO tenure and firms’ financial performance. If the direct relationship between CEO tenure and firms’ financial performance is positive as specified in H1a, it follows that with higher CEO cash compensation, the relationship between CEO tenure and firm’s financial performance will be more positive than the relationship with lower CEO cash compensation. Alternatively, if the direct relationship between CEO tenure and firm’s financial performance is negative as specified in H1b, it follows that with higher CEO cash compensation, the relationship between CEO tenure and firm’s financial performance will be less negative than the relationship with lower CEO cash compensation. We thereby suggest the following hypothesis.

We define CEOs’ long-term incentives as the proportion of total compensation in long-term incentive forms, such as stock options. 2 We argue that CEOs’ long-term incentives help align the interests of CEOs with those of shareholders, and thus positively moderates the relationship between CEO tenure and firms’ financial performance. CEOs who receive higher long-term incentives are exposed to lower downside risks and willing to take more necessary strategic risks. Specifically, stock options are a major component of long-term incentives (McGuire, Dow, & Argheyd, 2003). When granted, stock options have no marketable value, and no one would exercise their stock options if the price is at or below the option price (Sanders, 2001). Therefore, CEOs whose pay is primarily in long-term incentives gain benefits along with shareholders if stock prices increase but have no actual financial losses if stock prices decline (Sanders, 2001). Since these CEOs can obtain an unlimited upside potential while avoiding a downside outcome, they are less risk-averse or even prefer to take more necessary strategic risks to enlarge the upside potential (Sanders, 2001; Sanders & Hambrick, 2007). For example, Sanders (2001) finds that CEOs with higher stock options are motivated to pursue potentially larger gains and more likely to make bets on acquisition deals even if the acquisition involves more risks. Sanders and Hambrick (2007) comment that long-term incentives, such as stock options, can stimulate CEOs to make large strategic investments, such as investing in the development of radically new products rather than extending product lines and thereby taking higher levels of risks. Despite the fact that risk-taking may lead to high-variant outcomes, it reduces opportunity costs for risk-neutral shareholders who prefer to maximize their return and promote the interest alignment between CEOs and shareholders.

To conclude, CEOs whose primary pay is in long-term incentives are more willing to take necessary strategic risks. Since these CEOs can obtain an unlimited upside potential if stock prices increase, they might be more motivated to communicate with the board of directors for strategic advice. Therefore, the information asymmetry between CEOs and shareholders is also likely to be lower. As such, CEO long-term incentives tend to positively moderate the relationship between CEO tenure and firms’ financial performance. If the direct relationship between CEO tenure and firms’ financial performance is positive as specified in H1a, it follows that with higher CEO long-term incentives, the relationship between CEO tenure and firm’s financial performance will be more positive than the relationship with lower CEO long-term incentives. Alternatively, if the direct relationship between CEO tenure and firm’s financial performance is negative as specified in H1b, it follows that with higher CEO long-term incentives, the relationship between CEO tenure and firm’s financial performance will be less negative than the relationship with lower CEO long-term incentives. We thereby suggest the following hypothesis.

We define CEOs’ stock ownership as the percentage of their firm ownership stake. We argue that CEOs who own higher stock ownership are likely to be more risk-averse due to higher downside risks, and CEO stock ownership thus negatively moderates the relationship between CEO tenure and firms’ financial performance. When granted, unlike stock options, stock ownership has real and immediate marketable value (Sanders, 2001). CEOs who own stock ownership can experience significant wealth reduction if stock prices decline and thus become exposed to greater downside risks (Sanders, 2001). When CEOs are afraid of losing something, they tend to exhibit a stronger preference for risk aversion and behave in a more risk-averse manner (Kahneman & Tversky, 1979; Wiseman & Gomez-Mejia, 1998). They may forgo risky but potentially profitable investments, leading to lower firms’ financial performance. For example, Wright, Kroll, Lado, and Van Ness (2002) find that CEOs with more stock ownership tend to avoid risky and potentially profitable acquisitions because their personal wealth concentration induces them to take risk-reducing strategies. Likewise, Kim and Lu (2011) report that higher levels of CEO stock ownership reduce firms’ R&D, which is associated with growth opportunities as well as risks.

To conclude, CEOs who hold more stock ownership are more likely to be risk-averse. When CEOs behave in a more risk-averse manner, their goal conflicts with risk-neutral shareholders are also likely to be higher, and thus they are less likely to maintain effective communication with shareholders. As such, CEO stock ownership tends to negatively moderate the relationship between CEO tenure and firms’ financial performance. If the direct relationship between CEO tenure and firms’ financial performance is positive as specified in H1a, it follows that with higher CEO stock ownership, the relationship between CEO tenure and firm’s financial performance will be less positive than the relationship with lower CEO stock ownership. Alternatively, if the direct relationship between CEO tenure and firm’s financial performance is negative as specified in H1b, it follows that with higher CEO stock ownership, the relationship between CEO tenure and firm’s financial performance will be more negative than the relationship with lower CEO stock ownership. We thereby suggest the following hypothesis.

Board Monitoring

We examine the moderating effects of board monitoring using the board’s independent director ratio (Dalton et al., 1998; Westphal & Zajac, 1994; Wiseman & Gomez-Mejia, 1998). Since independent directors are not affiliated with the top management team, they are likely to monitor CEOs’ actions vigilantly (Goranova et al., 2017). Thus, prior studies often use the board’s independent director ratio to gauge board independence and the intensity of board monitoring. Although such monitoring can mitigate opportunistic managerial behaviors to some extent (Beatty & Zajac, 1994; Eisenhardt, 1989), recent studies have suggested that it comes with greater managerial myopia, which negatively influences the interest alignment between CEOs and shareholders (Faleye, Hoitash, & Hoitash, 2011). First, intense board monitoring increases CEOs’ perceived downside risks and pushes them away from necessary strategic risk-taking, as CEOs tend to have growing concerns about board support due to the inherent ambiguity of evaluation criteria and the difficulty of reaching consensus over such criteria (Wiseman & Gomez-Mejia, 1998). Thus, CEOs tend to become more hesitant to invest in risky but value-enhancing projects (Faleye et al., 2011). For example, Goranova et al. (2017) suggest that tight board monitoring that focuses on an oversight role of the board could lower CEOs’ risk-taking and constrain big gains in merger and acquisition activities. Further, Faleye et al. (2011) illustrate that firms with intense board monitoring exhibit worse acquisition performance and reduced corporate innovation. Second, intense board monitoring increases the information asymmetry between CEOs and shareholders. When monitored intensively by a board, CEOs are concerned that the board will interfere with the decision-making process and thus are less likely to share firm-specific information with board members (Adams & Ferreira, 2007). Excessive board monitoring will also divert managers’ attention to symbolic actions to please the board and disengage from substantive tasks (Garg, 2013).

Taken together, intense board monitoring increases CEOs’ risk aversion and weakens the communication between CEOs and shareholders. As such, the board’s independent director ratio tends to negatively moderate the relationship between CEO tenure and firms’ financial performance. If the direct relationship between CEO tenure and firms’ financial performance is positive as specified in H1a, with a higher board’s independent director ratio, the relationship between CEO tenure and firm’s financial performance will be less positive than a lower board’s independent director ratio. Alternatively, if the direct relationship between CEO tenure and firm’s financial performance is negative as specified in H1b, with a higher board’s independent director ratio, the relationship between CEO tenure and firm’s financial performance will be more negative than a lower board’s independent director ratio. We thereby suggest the following hypothesis.

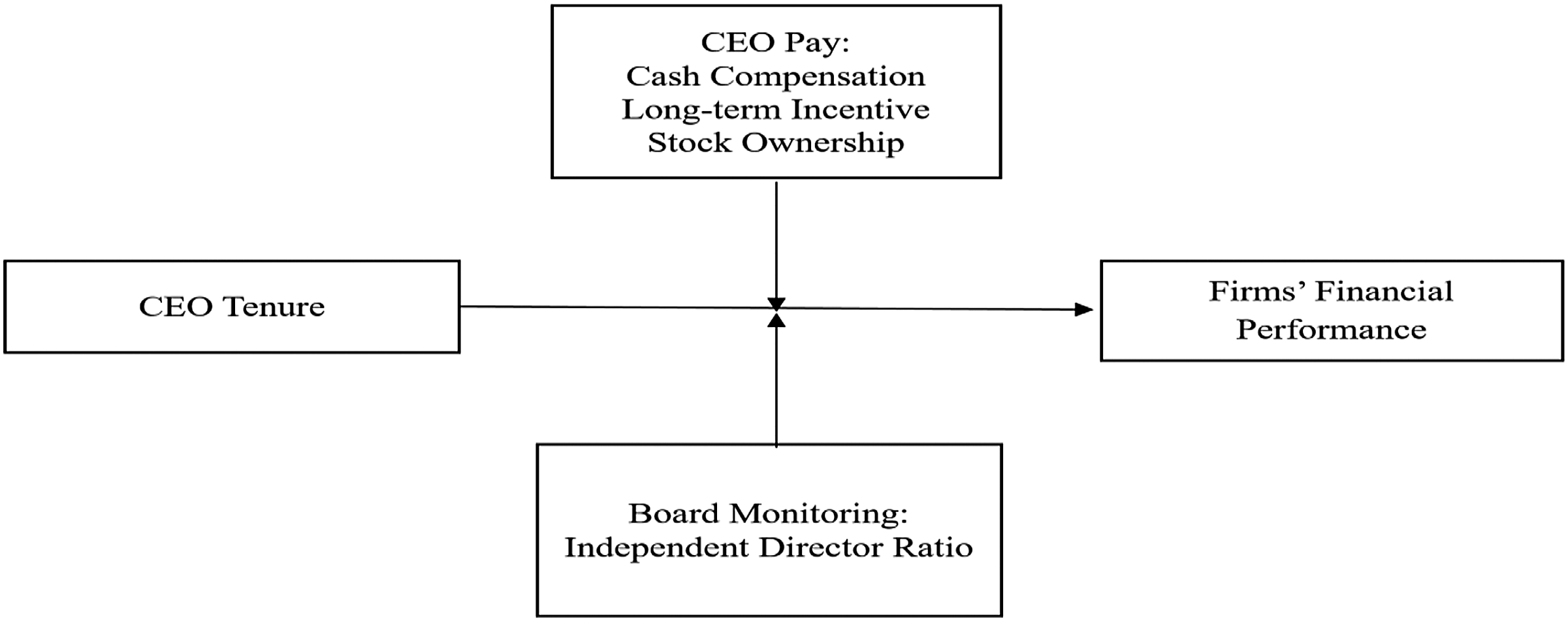

Figure 1 presents our proposed conceptual model. Proposed conceptual model. Note. We examine the moderating effects of CEO pay and board monitoring on the relationship between CEO tenure and firms’ financial performance.

Method

Sample

We used several search techniques to identify relevant studies related to CEO tenure and firms’ financial performance that were available online as of 2019. First, we conducted a full text keyword search of the following bibliographic databases: Business Source Premier, Proquest ABI/INFORM Global (including dissertations and theses), PsycINFO, and Scopus based on the following keyword combinations: “CEO tenure,” “CEO job tenure,” “CEO position tenure,” “CEO organizational tenure,” “CEO organization tenure,” “CEO time in role,” “CEO time in position,” and “CEO time in an organization.” Then, we reviewed identified studies by the title and abstract of each result. We only included studies that empirically reported the correlation between CEO tenure and firms’ financial performance. Then, we evaluated these studies’ eligibility for a meta-analysis. Specifically, it was not necessary that the CEO tenure and firms’ financial performance relationship be the focus of a study. When a correlation between these variables was provided, we included it in the study. We also examined the reference lists of candidate studies for identifying further suitable studies. Noticeably, some of these empirical studies include more than one sample by using a variety of financial performance indicators (e.g., market performance and accounting performance). As Dalton et al. (1998) suggest, multiple samples from a single study can only be combined when they reflect similar study characteristics (e.g., the same operationalization of different financial performance indicators); otherwise, these samples from a single study should be counted as usable samples separately (Dalton et al., 1998). We followed Dalton et al. (1998), and our final sample includes 385 empirical studies with a total number of 1,029,602 observations.

Meta-Analytical Procedures

A meta-analysis is a quantitative approach, often used in management research (e.g., O’Boyle, Patel, & Gonzalez-Mulé, 2016) that synthesizes prior empirical findings with two major objectives (Smith & Glass, 1977). First, it aims at providing an accurate estimate of the true relationship between two variables in the population (Hunter & Schmidt, 1990; Lipsey & Wilson, 2001). Second, it investigates the effect of contingent factors that causes inconsistencies between study findings (Hunter & Schmidt, 1990; Lipsey & Wilson, 2001).

We conducted a meta-analysis following the guidelines of Hunter and Schmidt (1990) that correct for various statistical artifacts using a random effects model. A random effects model assumes the population effect sizes vary randomly from study to study (Hunter & Schmidt, 1990). It is particularly favorable for the current study, given that CEO tenure is temporal in nature and there is no single true correlation being estimated (Overton, 1998). Further, in almost all situations, a random effects model is more appropriate because it yields a more conservative test result (Aguinis, Gottfredson, & Wright, 2011; Overton, 1998). Specifically, this approach requires that each observed correlation be weighted by the sample size to obtain the mean weighted correlation. By further correcting the reliability of the included studies, we can calculate the corrected estimates of the SD of the mean corrected effect size, the SE, credibility, and confidence intervals (Hunter & Schmidt, 1990; Whitener, 1990). When there is no reliability information provided in the studies, we used a conservative .8 reliability estimate instead (Dalton et al., 1998; Hunter & Schmidt, 1990). There is a true relationship between the variables of interest if the 95% confidence interval around the corrected mean does not include zero.

We also tested outliers from the sample using the sample-adjusted meta-analytic deviancy statistics, and outliers were defined as individual correlations four SDs above or below the mean of the correlations in the sample (Huffcutt & Arthur, 1995). In our sample, there are two observations (correlations = −.59 and .50, respectively, for the relationship between CEO tenure and firms’ financial performance), which could be considered as outliers. However, an analysis without these two studies did not change the results. Therefore, we report the results based on the complete sample.

Although meta-regression is a better approach to investigate the explanatory power of relevant moderators simultaneously, it needs a relatively large number of subjects per moderator to make the analysis meaningful (Borenstein, Hedges, Higgins, & Rothstein, 2011; Pigott, 2012). Since the moderator information of the included studies is dispersed (i.e., only a few studies include all relevant moderators), we will lose a substantial number of studies using a meta-regression. Thus, we conducted moderator analyses by separating the samples into relevant subgroups using the mean value of the moderators as our main analysis. We validated the results by using the median value of the moderators and found the results to be consistent. This approach has been used in previous meta-analyses (e.g., Dalton et al., 1998; Wang, Oh, Courtright, & Colbert, 2011). We also used multiple imputation and weighted least square (WLS) multiple regression to supplement the results of subgroup comparison. The results of WLS multiple regression are reported in Appendix B.

We separated the sample into relevant subgroups and examined the potential existence of moderating variables following two guidelines. First, if 95% credibility interval is wide or includes zero, then it suggests that moderators are operating in the relationship (Koslowsky & Sagie, 1993; Whitener, 1990). Second, for the subgroup analyses, a critical ratio, essentially a Z-score, is provided to evaluate whether the moderator pairs of samples are statistically significant (Dalton et al., 1998, Dalton, Daily, Johnson, & Ellstrand, 1999; Quiñones, Ford, & Teachout, 1995).

Results

CEO Tenure and Financial Performance

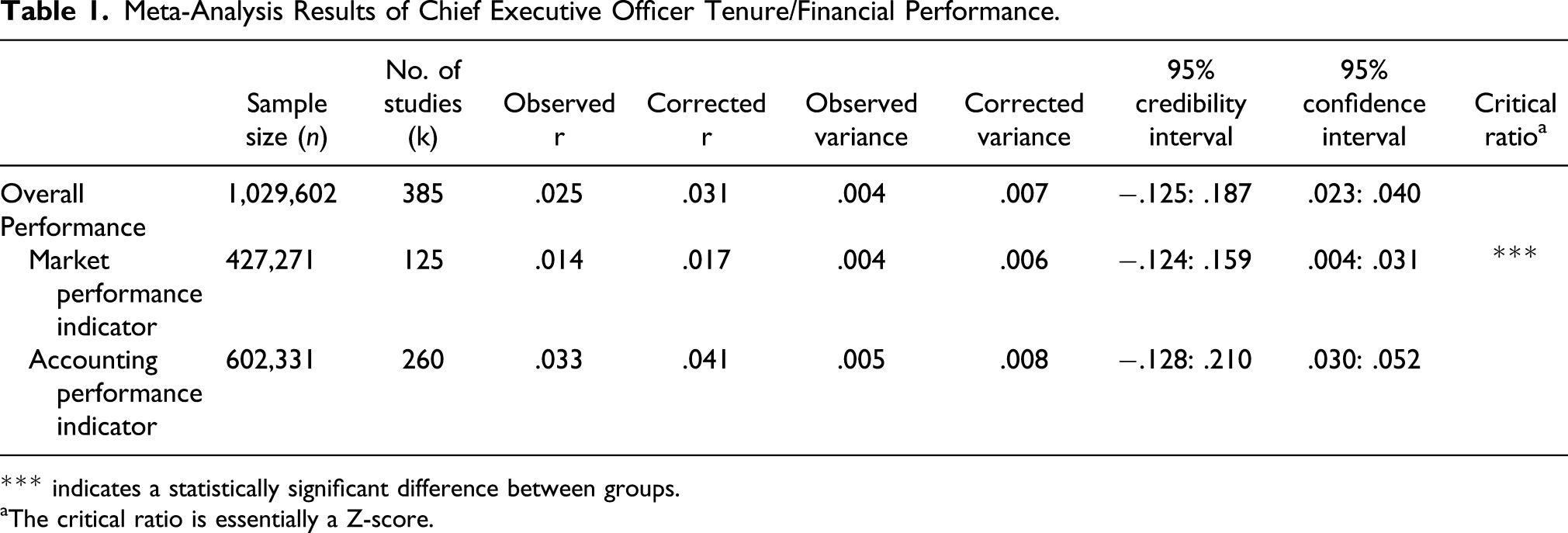

Meta-Analysis Results of Chief Executive Officer Tenure/Financial Performance.

*** indicates a statistically significant difference between groups.

aThe critical ratio is essentially a Z-score.

We further analyzed whether the above findings differ using market versus accounting performance indicators. Market performance indicators are based on market returns, such as Jensen’s alpha or cumulative abnormal return, etc. CEOs and top management teams have relatively less control over these market-based indicators (Dalton et al., 1999; Hambrick & Finkelstein, 1987). Accounting performance indicators are more achievable for management teams, and they usually include ROA, return on investment, or return on equity (Dalton et al., 1999). As can be seen in Table 1, the corrected mean correlation estimate for market performance indicator is .017 (125 studies, n = 427,271). The 95% confidence interval does not include zero (.004–.031), suggesting the true population correlation between CEO tenure and market financial performance is nonzero. The 95% credibility interval is wide and includes zero (−.124–.159), suggesting the presence of moderators. The corrected mean correlation estimate for accounting performance indicator is .041 (260 studies, n = 602,331). The nonzero 95% confidence interval (.030–.052) indicates that the relationship between CEO tenure and firms’ accounting performance is positive. The 95% credibility interval includes zero (−.128–.210), suggesting the presence of moderators. The significant critical ratio illustrates that the population correlation estimate for market performance indicators is statistically lower than that for the accounting performance indicators. These findings confirm that CEO tenure is positively related to a firm’s performance (i.e., H1a), especially accounting performance. These findings also confirm the presence of moderating effects.

Moderating Effects of CEO Pay and Board Monitoring

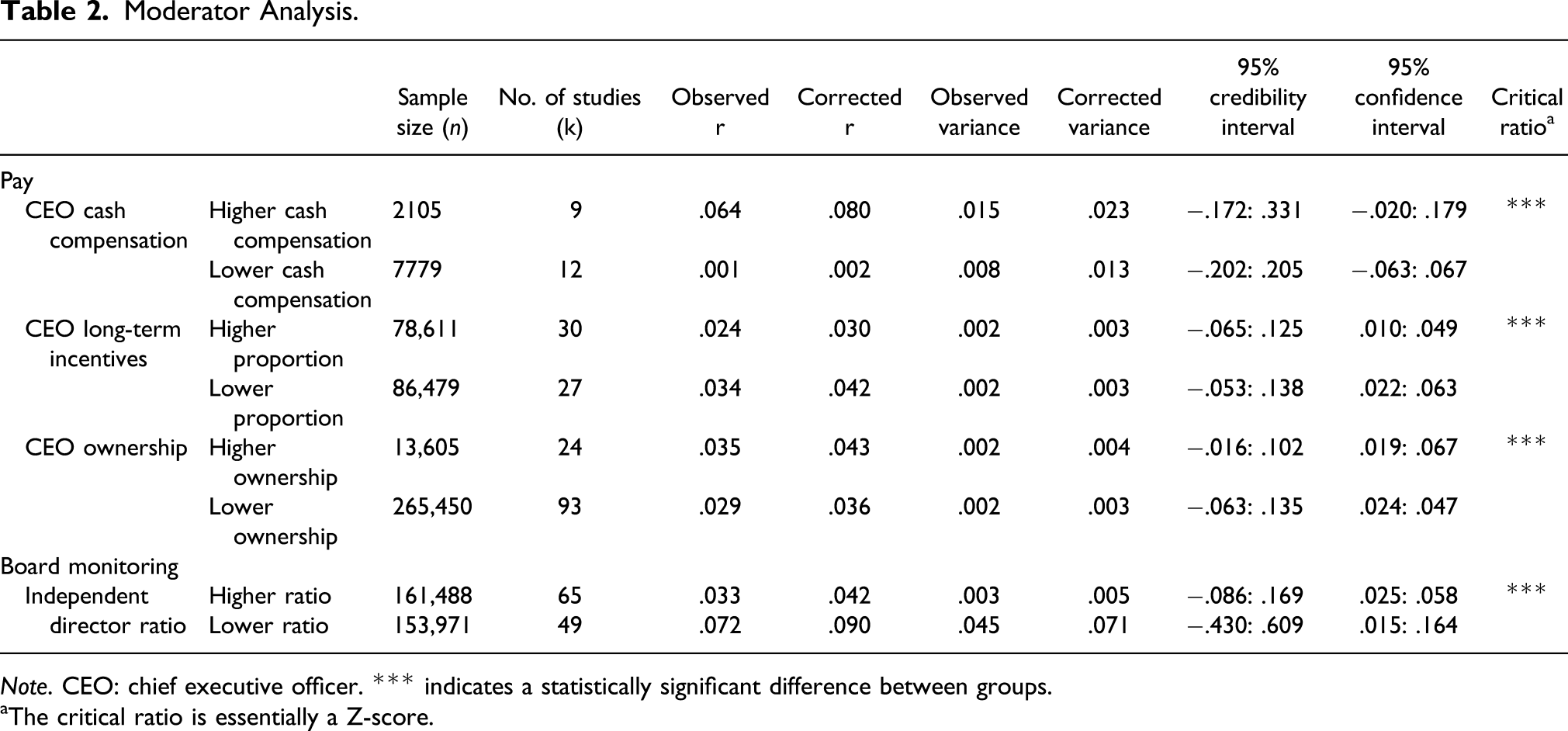

Moderator Analysis.

Note. CEO: chief executive officer. *** indicates a statistically significant difference between groups.

aThe critical ratio is essentially a Z-score.

Our hypothesis 3 suggests that CEO long-term incentives positively moderate the relationship between CEO tenure and firms’ financial performance. However, the results show that the corrected mean correlation between CEO tenure and firms’ financial performance is significantly lower when CEOs receive higher long-term incentives (corrected mean correlation = .030) versus when CEOs receive lower long-term incentives (corrected mean correlation = .042). The 95% credibility intervals for these subgroups are wide and include zero (−.065–.125 for higher long-term incentives group and −.053–.138 for lower long-term incentives group), confirming the presence of moderating effects. The 95% confidence intervals of these two subgroups do not include zero (.010–.049 for higher long-term incentives group and .022–.063 for lower long-term incentives group), indicating the true relationships between CEO tenure and firms’ financial performance for the subgroups are positive. The above findings suggest that long-term incentives negatively moderate the relationship between CEO tenure and firms’ financial performance, which is opposite to our hypothesis 3. Thus, hypothesis 3 is not supported.

Our hypothesis 4 suggests that CEO stock ownership negatively moderates the relationship between CEO tenure and firms’ financial performance. However, the results show that the corrected mean correlation between CEO tenure and firms’ financial performance is significantly higher when CEOs hold more stock ownership (corrected mean correlation = .043) versus when CEOs hold lower stock ownership (corrected mean correlation = .036). The 95% credibility intervals for these subgroups are wide and include zero (−.016–.102 for higher stock ownership group and −.063–.135 for lower stock ownership group), confirming the presence of moderating effects. The 95% confidence intervals of these two subgroups do not include zero (.019–.067 for higher stock ownership group and .024–.047 for lower stock ownership group), indicating the true relationships between CEO tenure and firms’ financial performance for the subgroups are positive. The above findings suggest that stock ownership positively moderates the relationship between CEO tenure and firms’ financial performance, which is opposite to our hypothesis 4. Thus, hypothesis 4 is not supported.

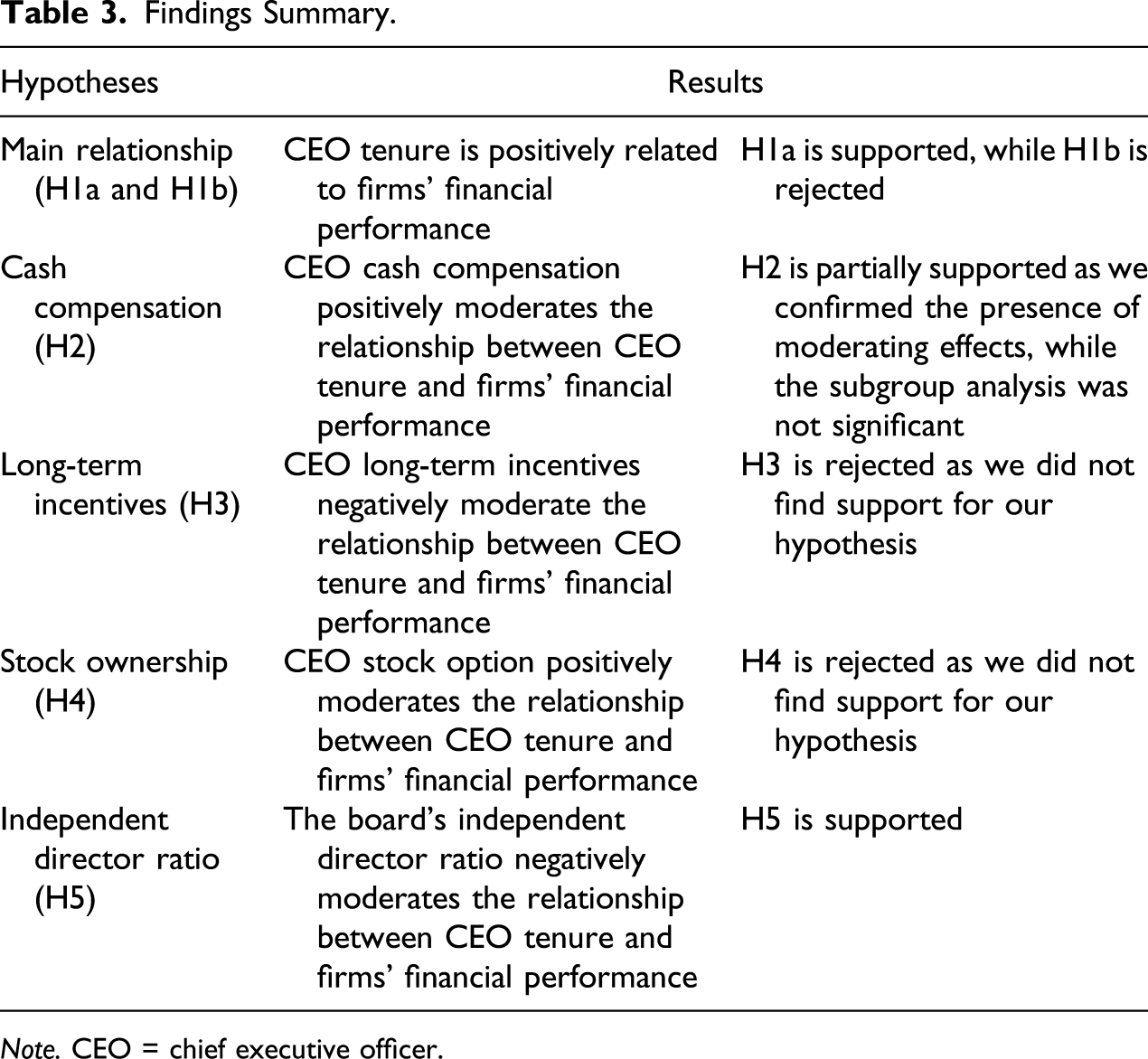

Findings Summary.

Note. CEO = chief executive officer.

Discussion

Based on the theoretical arguments of agency and behavioral agency theories, this study meta-analytically examines the relationship between CEO tenure and firms’ financial performance as well as the moderating effects of CEO pay and board monitoring. Our study provides several intriguing findings and implications. First, the results suggest that CEO tenure is positively related to firms’ financial performance, especially accounting performance. Our findings support the arguments that the relationship between CEOs and shareholders becomes more efficient in a long-term relationship (Eisenhardt, 1989). This study also adds to the debate over “how does a CEO’s time in office affect a firm’s financial performance?” by suggesting that the relationship between CEO tenure and firms’ financial performance may change depending on the use of performance indicators. Since CEOs and the top management teams have relatively less control over market performance than accounting performance (Dalton et al., 1999; Hambrick & Finkelstein, 1987), the mixed insights of prior studies may be attributed to different performance indicators. The above findings also suggest that accounting performance might be a more accurate performance indicator than market performance when evaluating long-tenured CEOs’ discretion regarding firms’ strategic decisions. Second, we deduce from the elaborated agency-based views of behavioral agency theory and argue that CEO pay and board monitoring may moderate the relationship between CEO tenure and firms’ financial performance. We find that the relationship between CEO tenure and firms’ financial performance is more positive when CEOs receive higher cash compensation. However, inconsistent with our prediction, the effect of CEO tenure on firms’ financial performance becomes less positive when CEOs receive higher long-term incentives. One possible explanation could be that CEOs’ downside risks can increase dramatically if their pay is primarily in long-term incentives (Sanders, 2001), especially when the awarded stock options are positively valued (Larraza-Kintana et al., 2007). If the awarded stock options are positively valued, CEOs tend to incorporate the positive value into the calculation of their current wealth and may behave opportunistically to avoid any potential wealth reduction (Wiseman & Gomez-Mejia, 1998). Thus, even though long-term incentives, such as stock options, might be able to help with the interest alignment between long-tenured CEOs and shareholders, firms’ financial performance would still decrease as these CEOs’ may perceive increased downside risks. In addition, we find that the relationship between CEO tenure and firms’ financial performance is more positive when CEOs hold more stock ownership. One possible explanation could be that the effect of CEO stock ownership on firm performance depends on other employees’ stock ownership (Welbourne & Cyr, 1999). Or CEOs who own more stock are financially and psychologically attached to their firms (Garg, 2013). Even though these CEOs are exposed to higher downside risks, they are less willing to do something that might harm the firm in the long run. Third, we suggest that intense board monitoring (i.e., more independent directors) may increase the information asymmetry between CEOs and shareholders and push CEOs away from taking necessary strategic risks. Consistent with our arguments, the effect of CEO tenure on firms’ financial performance is less positive when there are more independent directors on the board.

The above findings confirm that CEO pay and board monitoring moderate the relationship between CEO tenure and firms’ financial performance. These findings show that while CEO cash compensation can increase the interest alignment between long-tenured CEOs and shareholders, the use of CEO long-term incentives and stock ownership should be planned more carefully. For example, long-tenured CEOs who receive higher long-term incentives might still behave opportunistically if their pay is primarily in long-term incentive forms, or the current value of stock options is too high. On the other hand, even though long-tenured CEOs who own more stock are exposed to higher downside risks, their interests might be well aligned with those of shareholders if they envision a long-term future benefit. These findings also show that intense board monitoring may not always help align the interests of long-tenured CEOs and shareholders. Indeed, since independent directors usually are constrained by information asymmetries relative to firms’ insiders (Goranova et al., 2017), they may not even possess the ability to exert control over long-tenured CEOs.

It is worth pointing out that the effect of CEO tenure on firms’ financial performance might be nonlinear (e.g., Hambrick & Fukutomi, 1991; Miller & Shamsie, 2001). We followed suggestions by Sturman (2003) to test this possibility but did not find support for it. Miller (1991) also similarly tested a U-shaped relationship between CEO tenure and firms’ financial performance and found the relationship to be nonsignificant. It is possible that CEO tenure may influence firms’ financial performance in a more nuanced manner in different contexts, yet our systematic review suggests that longer CEO tenure, in general, leads to higher financial performance for the firm. In addition, it is possible that firms’ financial performance affects CEO tenure. The causality of the relationship between CEO tenure and firms’ financial performance is clearer if a study uses a longitudinal sample. In our article, around 56% of sampled studies use longitudinal sample, while the rest of them uses a cross-sectional sample. We conducted a supplementary analysis to examine whether our conclusion changes across different types of sample design. The results are consistent and show that longer CEO tenure leads to higher firms’ financial performance. One interesting future direction along the line of our study is to provide more insight into the causality of CEO tenure and firms’ financial performance. Furthermore, there are other factors that may influence the relationship between CEO tenure and firms’ financial performance, such as environmental conditions (Gupta, Han, Nanda, & Silveri, 2018), performance feedback (Lim & McCann, 2013), and CEOs’ gender (Wang, Holmes, Devine, & Bishoff, 2018) among others. We chose agency mechanisms as moderators since they can be adjusted depending upon a firm’s policy and provide greater managerial implications. Additionally, it is also possible that CEOs who have exercised their stock options may behave differently from CEOs who have not exercised their stock options (e.g., Sanders, 2001; Sanders & Hambrick, 2007). In this article, we were unable to control for the exercise, or lack thereof, of CEO stock options. Last, employee ownership can play a role in the relationship between CEO tenure and firms’ financial performance (Kim & Patel, 2020; O’Boyle et al., 2016; Ren, Xiao, Yang, & Liu, 2019). Employee ownership can reduce agency problems associated with employees and increase their risk bearing (Kim & Patel, 2020; O’Boyle et al., 2016; Ren et al., 2019), which can affect CEOs’ decision-making and firms’ performance. Unfortunately, we were not able to control it due to limited data availability. However, these limitations may serve as an invitation for future research that further elaborates, along with all the nuances mentioned above, on the effect of CEO tenure on firms’ financial performance. Taken together, our findings highlight the potential of CEO pay and board monitoring as new research avenues in enhancing the understanding of the relationship between CEO tenure and firms’ financial performance.

Conclusion

We draw on arguments of agency and behavioral agency theories to examine the relationship between CEO tenure and firms’ financial performance and the moderating effects of CEO pay and board monitoring. We meta-analytically test samples from 385 studies (n = 1,029,602) and find that CEO tenure is positively related to firms’ financial performance. The results also show that different types of CEO pay and board monitoring influence the impact of CEO tenure on the firm’s financial performance differently. Our findings add to the debate over CEO tenure and suggest CEO pay and board monitoring, or in general agency mechanisms, as new research avenues to help further understand the relationship between CEO tenure and firms’ financial performance.

Footnotes

Appendix A

Note. We define CEOs’ long-term incentives as the proportion of long-term incentives in total compensation.

Select included studies

Definition of long-term incentives

He and Wang (2009)

Bonuses, long-term incentives payments, and stock options

Li and Qian (2011)

Option and stock granted

Wowak, Hambrick, and Henderson (2011)

Stock and options

Hill (2010)

Stock options, restricted stock grants, and long-term incentive plan

Berrone and Gomez-Mejia (2009)

Stock options, restricted stock, and other long-term compensation

Ghosh and Sirmans (2003)

Stock and options

Henderson and Fredrickson (1996)

All long-term, contingent pay in the form of stock options, performance unit or share plans, restricted stock, and long-term management incentive plans

Finkelstein and Boyd (1998)

Deferred income

Sanders and Carpenter (1998)

Long-term forms (e.g., stock options, restricted stock, and long-term incentive plan)

Westphal (1999)

Long-term incentive grants

Sanders (2001)

Stock options

Van der Laan (2010)

The value of portfolios of options and shares previously granted to the CEO

Gomez-Mejia, Larraza-Kintana and Makri (2003)

The value of stock options as the number of options granted to a CEO multiplied by 25% of the exercise price

Appendix B

Since most studies in the sample did not simultaneously report the means of CEO pay (e.g., cash compensation, long-term incentives, and stock ownership) and board monitoring (e.g., independent director ratio), we used multiple imputation and WLS multiple regression to supplement the results of subgroup analyses. Multiple imputation is widely used in many contexts of missing data, including meta-analysis (Pigott, 2012). For a detailed discussion of multiple imputation and WLS multiple regression in a meta-analysis, please refer to Pigott (2012). We report the multiply imputed estimates below. As shown, the moderating effects of CEO pay are not significant, and the board’s independent director ratio negatively moderates the effect of CEO tenure on firms’ financial performance (b = −.080, p < .001). However, as mentioned above, the results here should be interpreted with caution since they are based on multiple imputation using a relatively small number of studies with moderators. *p < .05, ** p < .01, *** p < .001. Note. Imputation = 5 times and n = 385

Model 1

Model 2

p.a

s.e

p.a

s.e

Intercept

.057

.079

.085**

.025

Cash compensation

−.024

.029

Long-term incentive

.550

.576

Stock ownership

−.357

.492

Independent director ratio

−.080***

.044

R-square

.018

.003

Adjusted R-square

.016

.003

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Associate Editor: Devaki Rau