Abstract

In this review, we provide a framework for understanding both the predictors and approaches of CPA that firms undertake to achieve their objectives. We identify the predictors of CPA and classify them into two distinct categories: internal and external. In addition, we suggest that CPA approaches will vary depending on the firm’s goal to either manage or mitigate regulation and legislation as compared to attempting to pass new bills into law. We conclude by suggesting several future CPA research directions for management scholars.

Introduction

Research in strategic management has traditionally centered on market strategies at the corporate and business levels to attain competitive advantage. In recent years, there has been increasing realization that market strategies alone may not be enough for a firm to survive and succeed (Doh et al., 2015; Mellahi et al., 2016; Dorobantu, Kaul, & Zelner, 2017). Market strategies are more likely to be successful when they are complemented with appropriate nonmarket strategies as well (Mellahi, Frynas, Sun & Siege, 2016). Nonmarket strategies cover a wide spectrum of activities such as corporate social responsibility (CSR) initiatives, corporate political activities (CPA), and other stakeholder management efforts.

Among nonmarket strategies, CPA occupies a singularly important place, as evidenced by the increasing resources that firms spend on it both domestically and internationally (Brown, Yaşar & Rasheed, 2018). CPA is defined as “Corporate political activities, or corporate attempts to shape government policy in ways favorable to the firm (Hillman, Keim, & Schuler, 2004, p. 837).” CPA is an umbrella term encompassing a wide variety of activities such as campaign contributions, lobbying, co-optation of politicians and government officials into company boards, formation of political action committees, and bribing. CPA research has mostly focused on lobbying and campaign contributions. Prior literature has tried to categorize CPA activities (Hillman & Hitt, 1999; Lawton, McGuire, & Rajwani, 2013), identify their antecedents (Hillman et al., 2004) and evaluate their outcomes (Hillman et al., 2004; Lux et al., 2011; Hadani, Bonardi, & Dahan, 2017). In addition, increasing research interest on various aspects of CPA is evidenced by the proliferation of studies on CPA in recent years. Benefiting from the availability of more fine-grained data, recent research has been able to examine a variety of new predictors of CPA than was possible earlier. Similarly, researchers have begun to acknowledge the heterogeneous nature of CPA. However, despite the insights gained from these attempts, we still have only limited understanding of the factors that motivate a firm to engage in CPA as well as the variety of approaches firms take to engage in CPA.

The political activities of firms have attracted the attention of researchers from a wide variety of academic disciplines such as strategic management (Hadani & Schuler, 2013), entrepreneurship (Pinkse & Groot, 2015), marketing (Ormrod & Henneberg, 2010), business law (Bagley, 2010), political science (Hansen & Mitchell, 2000), sociology (Walker & Rea, 2014), and other academic domains. This multidisciplinary breadth of CPA research provides us with a variety of perspectives and insights on the political activities of firms. However, this disciplinary fragmentation also makes it difficult to integrate the findings from diverse disciplines and build cumulative knowledge. This lack of integration is further compounded by the fact that CPA itself is highly heterogeneous in nature. For example, a firm can choose from a variety of CPA categories or choose a portfolio of political activities. Most studies tend to treat CPA as a “black box” and measure it in terms of the dollar amount spent by a firm in a particular year. Unfortunately, the problem with such aggregate measures of CPA is that it fails to capture the variety and richness of political strategies available to firms. Nor does it recognize the differential effectiveness of varied political strategies in specific contexts.

The increasing recognition of the importance of nonmarket activities by firms has led to a substantial increase in the number of academic studies on CPA in the last two decades. The accumulation of empirical studies has led to attempts to discern generalizable relationships among CPA, its antecedents, and outcomes (Hillman, Keim, & Schuler, 2004; Lux, Crook & Woehr, 2011; Lawton, McGuire & Rajwani, 2013; Hadani, Bonardi, & Dahan, 2017). This effort has followed two complementary approaches to aggregate the results of CPA research and draw valid generalizations from them. First, researchers have undertaken meta-analyses to extract conclusions from the accumulated body of empirical evidence (Lux et al., 2011; Hadani, Munshi, & Clark, 2017). Second, there have also been efforts to aggregate and organize this growing body of research through review papers (Hillman et al., 2004; Lawton, McGuire, & Rajwani, 2013). For example, the focus of Lawton, Rajwani and Doh (2013) review was on the different conceptual lenses researchers have used in studying CPA. They identified three primary theoretical lenses prior research has used and highlighted the need for greater theoretical integration among the three lenses. Hillman et al.’s (2004) seminal review mapped the domain of CPA studies in a systematic and comprehensive fashion. In the nearly two decades since this study was published, a substantial number of empirical studies of increasing sophistication have accumulated. These studies reflect an increasing acknowledgment that CPA can take a variety of forms. However, what has been missing is an effort to systematically classify different types of political strategies and explain why a firm would choose one political strategy, or a combination of strategies, over another.

Our review provides a systematic classification of different approaches to CPA as new insights and ways of engaging in CPA have been identified since the seminal review by Hillman and colleagues (2004). Our objective is to examine extant research on CPA using an integrative organizing framework that incorporates the complexity of the CPA phenomenon in terms of its multiple antecedents and the variety of activities that constitute CPA. We start with a general discussion of the motivations and objectives of CPA by firms. We then examine the internal and external predictors of CPA. CPA represents an important strategic choice for firms that must first decide whether or not they will engage in CPA, and if so, they must determine which types of CPA they will engage in. A firm’s choices in this regard are driven by a complex mix of individual, top management team, firm, industry, and institutional factors. This is followed by a review of the different activities that are generally considered as CPA, thereby highlighting the highly heterogeneous nature of CPA. We conclude with a number of suggestions for advancing research on CPA by firms.

Political considerations are recognized as an important component in strategic management (Keim, 1981). In the early 1980s, the concept of CPA was defined by Baysinger (1984) as corporate engagement in external political activity in an attempt to shape policies in ways that are advantageous to the firm. Since then, a growing number of subsequent definitions of CPA have arisen, and each addresses the attempts of firms to influence government policy in ways that align with the strategic interests of organizations (Hillman & Hitt 1999; Hillman et al. 2004; Tian & Deng 2007). Corporate political activity refers to “corporate attempts to manage political institutions and/or influence political actors in ways favorable to the firm” (Mellahi et al., 2016, p. 144). Because laws, regulations, and a host of policy issues influence organizations, firms need to engage with governmental bodies and need to interact with political institutions, government, and local authorities (Rival & Major, 2018; Hadani, Bonardi, & Dahan, 2017; Gao et al., 2018).

Corporate political activity (CPA) is a nonmarket activity aimed at managing an organization’s societal context. While market strategy deals with “suppliers, customers, and competitors,” nonmarket strategy addresses the “social, political, legal, and cultural arrangements that constrain or facilitate firm activity” (Doh et al., 2012, p. 23). Nonmarket strategy researchers consider a political strategy to be a key aspect of a firm’s overall business strategy across industries because it affects a firm’s behavior and performance (Keim & Hillman, 2008; Hillman et al., 2004; Hillman & Hitt, 1999; Getz, 1997). Corporate political strategy is intentional and encompasses “the strategy that enterprises employ to influence the formulation and implementation process of government policy and regulation to create a favorable external environment for their business activities” (Deng, Tian, & Abrar, 2010, p. 372).

Schuler, Rehbein, and Cramer (2002) identify the goal of any engagement in political activities as the pursuit of strategic advantage. Scholars also point to the wide variety of regulations and public policies enacted by regional and national governments and by international treaties that create substantial complexity and costs for firms (Puck et al., 2018). Consequently, firms use CPA to help them understand and engage with the environment (e.g., Lawton et al. 2013a, b). Additionally, the political environment in international markets can create significant threats for firms and negatively influence the strategic options available to firms as a result of regulatory or legal pressures (De Villam, Rajwani, & Lawton, 2015). Hence, CPA is seen as increasingly important for firms to incorporate in their strategic decision-making.

In the remainder of the paper, we will (1) discuss CPA’s role within strategic management, (2) provide an organizing framework for understanding and categorizing the current CPA literature, (3) review the CPA literature within the context of our organizing framework, and (4) examine implications for future research providing a roadmap for scholars to advance CPA research in the coming years.

CPA Research: An Organizing Framework

Firms engage in corporate political activity (CPA) in an effort to have their voice heard in the policy conversation and to gain long-run strategic advantage. The firms that engage in CPA believe that their interaction and engagement with the government is worth the cost and time they spend to have some say in the regulatory “rules of the game.” Firms also engage in CPA to gain various favors from governments, given that governments play a significant role in the economic activities within a country through regulation, procurement, approvals, and sanctions. Governments also play a role in international trade and investment through trade treaties, free trade agreements, taxation of foreign entities, and rules governing foreign direct investment. The breadth, intensity, and scope of CPA have continued to grow regardless of which political party is in power.

As CPA grows in importance, with firms spending more and more resources every year on CPA, there has been significant growth in research on CPA. In order to conduct a systematic review of prior research on CPA and synthesize their results, it is helpful to first develop an organizing framework. As Ginsberg and Venkatraman (1985, p. 422) noted, “an analytic review scheme is necessary for systematically discerning patterns from a widely differing set of studies and evaluating the contributions of a given body of research.”

The first part of our organizing framework involves the variety of factors that influence a firm’s decision to engage in CPA and the choice of the specific type of CPA. We call these factors CPA predictors because the presence of these factors increases the likelihood that the firm may undertake CPA. We classify these predictors into two categories: internal and external to the firm. Internal predictors examined in prior research include CEO characteristics (Rudy & Johnson, 2019; Johnson, 2019), top management teams (Ozer, 2010), board characteristics (Johnson, 2019), ownership structure (Hadani, 2007, 2012; Dahan, Hadani, & Schuler, 2013; Hadani, Dahan, & Doh, 2015) and CEO ideology (Chin, Hambrick, & Treviño, 2013). Prior research has also identified a number of external predictors of firm CPA. These include industry-level (Hadani and Schuler, 2013) and country-level factors (Brown et al., 2018), and the social (Hadani, Doh, & Schneider, 2018; Hadani, Doh, and Schneider, 2019) and political environment (Werner, 2017) in which the firm operates.

We then examine the variety of CPA approaches that are available to firms. We classify CPA approaches by what outcome they seek, either mitigating or taking advantage of government policies and regulation as it is implemented, or proactively influencing the creation of new policies and regulations. The types of CPA approaches that a firm engages in include activities such as administrative and legislative lobbying, political action committee (PAC) contributions (Brown, De Leon, & Rasheed, 2019), CEO political activism (Chatterji & Toffel, 2019), hiring internal and external lobbyists (Tyllström & Muarry, 2021), and co-opting or bribing of those in power. We seek to understand why and when a firm would use a specific strategy. While CPA has been studied in the literature, especially lobbying and PAC contributions, the complexity of these activities has not been fully recognized. Our organizing framework is presented in Figure 1. CPA predictors and approaches.

Method

Our review builds on the work of Hillman et al., (2004) and reviews the research on both what influences CPA and the variety of approaches that firms use to engage in CPA. In order to identify relevant prior research for our review, we followed a systematic process. Due to the multi discipline domain of CPA, we used search terms rather than a journal list to locate applicable research. Searching EBSCO Host, Jstor, Lexis-Nexis, and Google Scholar, we aggregated all studies that included the following keywords “Corporate political,” “firm-government,” “business-government,” “political strategies,” “political action committee(s),” “PAC,” “political donations,” “lobbying,” “politically tied/ties,” and “regulation.” Our final sample of relevant work included 62 papers.

Predictors of CPA

Internal Predictors

There is considerable divergence across firms regarding the resources they spend on corporate political activity (CPA) and the types of CPA activities they undertake. While researchers have examined antecedents of CPA (Hillman et al., 2004), these were often looked at as firm, industry, or broader environmental factors that influenced firm’s willingness and motivation to engage in the political process with much less attention on factors internal to the firm. Researchers have tried to identify firm-specific factors that can explain the observed variance in the CPA activities of firms. A number of internal factors have been examined in recent years as potential antecedents of CPA. The management-related and governance-related factors discussed in prior literature include chief executive officer (CEO) characteristics (Rudy & Johnson, 2019; Johnson, 2019), CEO ideology (Chin, Hambrick, & Treviño, 2013), top management team characteristics (Ozer, 2010), board characteristics (Johnson, 2019), and ownership structure (Hadani, 2007, 2012; Dahan, Hadani, & Schuler, 2013; Hadani, Dahan & Doh, 2015). We review the extant empirical research on each of these antecedents below.

CEO and Board Characteristics

Given that the decision to engage in CPA is a strategic choice made by the firm and its top management, recent work has begun to examine the individual actors in firms and their influence on CPA, namely, the CEO and board of directors. Hadani, Dahan, and Doh (2015) found that the CEO was vital in the effectiveness of firm CPA. By examining competing hypotheses, they found that CEO discretion decreases CPA effectiveness, possibly due to the lack of oversight from the board when CEO discretion is high. Using upper echelons theory, Rudy and Johnson (2019) found that CEO’s age, tenure, functional, and educational backgrounds influenced whether and how firms engaged in CPA. Sun, Hu, and Hillman (2016) found that political capital on boards could come with downsides. Using a sample of Chinese firms, they found that political capital on boards was positively associated with increased rent appropriation by blockholders. Finally, Kim (2008) found that highly paid CEOs at firms with declining sales trends increase their lobbying, but not campaign contributions.

CEO Political Activism

A relatively recent stream of research has started focusing on the political and ideological leanings of the CEO. Instead of examining CEO political giving as CPA, this stream of research has viewed the nature of that giving as a proxy for political ideology. Looking at various measures of political bents in campaign contributions, scholars have created indexes of conservatism and liberalism. CEO ideology has been found to influence the way the CEO leads the firm. For example, CEO political ideology influenced a firm’s corporate social responsibility (CSR) profile (Chin, Hambrick, & Treviño, 2013). In addition, Semadeni, Chin, and Krause (2021) find that the political ideology of the CEO can influence a firm’s threat response. When CEOs’ political ideology diverges from the national political climate, they interpreted this as a threat. In response, firms lower their R&D spending and increase retained earnings.

The implications of CEO ideology are not limited to firm-level decision-making. Brown, Manegold, and Marquardt (2020) suggest that the political ideology of the CEO can lead to misfit for employees with an opposing political view. They posit that this misfit will lead to negative firm-level outcomes, including increased turnover intentions, when the CEO engages in political activism. Empirical research suggests that CEO liberalism increases the likelihood that their employees will engage in activism by creating socially focused employee groups that correspond to the CEO’s ideology (Briscoe, Chin, & Hambrick, 2014). CEO activism has also influenced public opinions about government policies and consumer attitudes about the company (Chatterji & Toffel, 2019).

Finally, in an effort to better understand political ideology’s influence on firm behavior, researchers have suggested separating out social ideologies from economic ideologies (Chin, Zhang, Afshar Jahanshahi, & Nadkarni, 2021). For example, Chin et al. (2021) find that social conservatism will increase corporate entrepreneurship while economic conservatism negatively influences corporate entrepreneurship by impairing decision-making. While researchers studying political ideology have differentiated the literature from that of CPA, the majority of this work (exceptions include Chin et al., 2021; Chatterji, & Toffel, 2019) is still using political contribution data to create these political ideology scales. Given that the CEO and the firm are virtually indistinguishable in the public mind, political contributions by CEOs should be viewed as more than an individual expressing his or her political sympathies. To the extent that these are political statements, they can be viewed as strong signals that might influence the actions of decision-makers in the political realm. In addition, they are also powerful signals to the general public about the firm’s ideological position. One problem, however, in using a CEO’s political contributions as a proxy for the firm is that it is difficult to distinguish between purely ideological contributions and those that constitute instrumental actions by self-interested CEOs on behalf of their firm, or whether they are a mix of both. One of the few papers investigating political ideology as CPA found that firms that avoid extreme ideologies in their CPA were more effective and that their political expenditures were positively associated with firm performance (Greiner & Lee, 2020).

Firm Experience and Opportunity

Another predictor of firm CPA is the unique experiences of the firm and the current situation of the firm. Different firm experiences and opportunities will influence the firm’s willingness to engage in CPA. For example, in some industries that rely heavily on government contracts, CPA can become a self-sustaining spending approach. Hadani, Munshi, and Clark (2017) found that the more firms spend on political activities, the more the value of political contacts would increase. This suggests that prior CPA might influence current CPA due to the positive feedback loop, as firms who invest heavily in CPA can expect to receive more back in direct government contracts. Lux (2016) suggests that strategic fit determines whether or not firms will engage in CPA. In other words, firms will engage in CPA if they believe that it “fits” for the firm and will improve firm performance. But unlike many strategic decisions, incremental CPA is rarely effective. That is, either a firm spends heavily on CPA or chooses to free ride. This is because CPA functions as an auction market and the gains from CPA gravitate to the biggest spenders. For legislation to be passed or regulatory implementation to be changed, CPA must reach a critical mass, or the CPA is insufficient to make a difference. On the other hand, the free riders assume that since government policies are rarely targeted at a specific firm, the gains from the leader’s CPA spending will trickle down to them as well.

Lux (2016) found that the free-riding strategy was negatively related to firm performance in the US coal industry. Brown, De Leon, and Rasheed (2019) also found that during times of economic uncertainty, such as the 2008 financial crisis, politically active firms could better appropriate direct gains in the form of Troubled Asset Relief Program (TARP) funding than politically inactive firms. Thus, they avoided free riding. In looking at CPA from a business history approach, Perchard and MacKenzie (2020) found that path dependence can play a role in firm CPA. Prolonged business–government relationships can have a lock-in effect on the firm in their CPA. A firm’s future plans might influence its engagement in CPA. For firms who plan to engage in an IPO in the future, engaging in CPA might be a profit-maximizing approach as increased CPA prior to initial public offering (IPO) has been found to help IPO performance (Rudy & Cavich, 2020). Aggarwal et al. (2012) suggest that the firm’s strategy and financial position influence CPA. They found that firms with large amounts of free cash flow and lower R&D and investment spending use those excess funds on increased CPA. Finally, Meznar and Johnson (2005) suggest that firms differ in their strategy and structure for engaging in business–government relations. They measure the firm’s attempt at buffering or bridging in political markets. Buffering is an attempt to insulate from political risks, and bridging is adapting operations to comply with political stakeholders. They measured the structure of business–government relations by examining the formal procedures for political affairs employees within an organization. Using survey data of political affairs employees, Meznar and Johnson (2005) found that in isolation strategy was more important than structure in influencing firm performance. That being said, the firm’s ability to align its strategy and structure did lead to increased performance of the firm’s business–government relations.

External Predictors

In addition to internal predictors of CPA, the external environment has also been shown to shape firm CPA. These external forces can come in a variety of levels, including the country level and industry level. In addition, the social and political environments have been found to influence firm CPA (Brown, Manegold, & Marquardt, 2020). Some studies of country-level influences are multi-country studies that attempt to compare the CPA activities of firms based on some country-level characteristics (Brown et al., 2018; Liou et al., 2021). Other studies use single country samples, which do not allow comparison across countries but still provide insights about the unique characteristics of a country and how it influences CPA activities of firms within that country (e.g., Mbalyohere & Lawton, 2018).

Country-Level Predictors

Several studies have examined the influence of country-level characteristics on CPA in the US by foreign firms. In a study of foreign firms engaged in business in the US, Brown, Yaşar, and Rasheed (2018) found that a firm’s willingness to engage in CPA was influenced by the cultural cognitive (individualism and uncertainty avoidance), normative (corruption), and regulative (administrative distance) institutional characteristics of their home countries. For foreign firms invested heavily in the US market, Liou, Brown, and Hasija, (2021) found that foreign firms who had engaged in M&A with US firms used both market strategies of acquiring less of an ownership stake in combination with increased lobbying efforts when the firm faced legitimacy issues due to country-level political animosity. This relationship was stronger for firms cross-listed in the US. In a study of foreign defense contracts, Kim (2019) examined how firms overcome the liability of foreignness by lobbying. They found that greater lobbying spending and longer relationships with lobbyists lead to more defense contracts.

In two studies of 105 foreign firms in India, Shirodkar and Mohr (2015a) found that when foreign firms depend on local intangible resources, they will use information-based political strategies instead of financial strategies, that is, political spending. But the inverse was found to be the case for firms that depend on local tangible resources. Firms that use both tangible and intangible resources use a constituency-building strategy. In addition, they find that firm strategy influences their political strategy in India. Ties to local businesses make subsidiaries less likely to engage in transactional CPA (Shirodkar & Mohr, 2015b).

Studies on CPA in African countries provide valuable insights on how CPA addresses institutional voids. Most countries in Africa lack political institutions that can guarantee transparency in decision-making, continuity in economic policies, and uniformity in applying existing rules and regulations. Such contexts highlight the importance of political contacts and relational CPA. In examining pro-market reform, Mbalyohere and Lawton (2018) find that MNEs engaged in proactive and reactive CPA during Uganda’s pro-market reform of electricity generation, with the host government remaining the most important political stakeholder. But local engagement and a multi-stakeholder approach were found to be necessary later in the reform process. In a qualitative study of 13 banks in Nigeria, Liedong, Aghanya, and Rajwani (2020) found that firms use four CPA strategies: affective, financial, pseudo-attribution, and kinship strategies. The authors argue that these strategies can be context-fitting but ethically suspect at times. In Ghana, a survey of 28 directors found that political strategies included relationships with politicians, giving to politicians, and logistical connections to political actors (Liedong, 2021).

Europe represents the polar opposite of the African context in terms of established legal conventions, mature institutions, and a relatively low level of corruption and administrative arbitrariness. The center of gravity of European lobbying is Brussels, where the European Union is headquartered. Given that European Union (EU) officials write most regulations, multinational firms maintain a presence there to influence the economic policies of the EU. In a comparative case study of CPA by Toyota and Hyundai, Barron, Pereda, and Stacey (2017) found that decentralized and coordinated subsidiaries were more influential than centralized and loosely coordinated subsidiaries.

In a study of subsidiaries of multinational corporation (MNC) competing in Australia, Banerjee and Venaik (2018) found that in addition to firm strategy, regulation and global integration lead to greater CPA. Interestingly, they found that while CPA leads to increased legitimacy, it did not lead to increased firm performance. On the other hand, for foreign MNC subsidiaries in Australia, mimetic CPA approaches outperform constituency building, financial, and relational approaches to CPA. In a study of six New Zealand MNEs engaged in foreign market entry, Elsahn and Benson-Rea (2018) found that both manager and firm experience and country institutional development all influenced firm CPA strategy.

As can be seen from the review above, we now have an accumulation of studies of CPA in many national contexts. However, our ability to draw generalizations from these studies is limited by the fact that the variance in these studies is at the firm level rather than the country level. Political activity is highly context-dependent in the sense that they are highly tailored to the unique political context of each country. There are also limitations on what types of data researchers have access to in each country. While political connections of a firm may be relatively easy to measure, money spent on lobbying or political contributions may be opaque in the absence of stringent disclosure requirements in many countries. Therefore, we suggest that both academics and business leaders understand the best practices within the political contexts in which the firms are competing.

Regulation and Regulatory Uncertainty

While research has long recognized that there is a positive relationship between regulation and CPA, recent research has found that regulatory uncertainty also influences a firm’s decision to engage in CPA. Regulatory uncertainty is conceptually distinct from regulation. Industries with a heavy but stable regulatory burden have predictable regulatory environments. On the other hand, industries with high regulatory change and uncertainty year over year require firms to continually adjust and adapt to the new and evolving regulatory environment. Brown, Goll, Rasheed, and Crawford (2020) found that firms respond to both high regulatory uncertainty and high levels of regulation with increased nonmarket activities, both CPA and CSR. In addition, they also recognize the tradeoffs between CPA and CSR when determining where to allocate their nonmarket spending. Kingsley, Vanden Bergh, and Bonardi (2012) suggest that firms engage in three different dimensions of nonmarket strategy to manage regulatory uncertainty, profile level (high or low profile nonmarket strategies), coalition breadth, and pivotal target. Hadani and Schuler (2013) did not find a significant relationship between CPA and firm performance except for firms in highly regulated industries. The strong conclusion that emerges from these studies is that firms experiencing regulatory intensity and regulatory uncertainty tend to engage in political processes to manage the regulatory environment.

Social Attention and Customers

Firms engaged in CPA must consider the political markets in which they are competing and the firm’s customers, and even the broad social attention that CPA can attract. Social attention can arise from a variety of scenarios. After the Supreme Court case of Citizen’s United, V. FEC, in which FEC limitations on corporate political giving were effectively removed, firms could spend unlimited amounts on political contributions. However, the financial markets reacted negatively to what was perceived as excessive political spending by firms, especially when CEOs had control through duality (Skaife & Werner, 2020), possibly because shareholders expect that this combination of unlimited freedom to spend and unrestrained CEO power could result in excessive CPA that might exacerbate principal–agent problems. Although the goal of CPA is to maximize profits by gaining the favor of political actors, the downside to either excessive or highly visible CPA is that it might lead to possible backlash from the social attention that their political activities can create because consumer preferences are influenced by party attachments (Panagopoulos, Green, Krasno, Schwam-Baird, & Endres, 2020).

The impact of nonmarket strategies cannot be fully understood in isolation. Instead, their influence is often determined in conjunction with other nonmarket strategies. For example, firms can influence the social environment by combining CPA and CSR. Hadani, Doh, & Schneider (2018) found that CPA could sway SEC decision-making in their favor when the firm also engaged in CSR activism. Firms have also found that CPA can act as an insurance-like mechanism to make firms less subject to social pressures. Prior research suggests that firms who engage heavily in CPA have decreased willingness to negotiate with socially oriented shareholder proposals and are more likely to challenge those proposals (Hadani, Doh, & Schneider, 2019).

The benefits from CPA are found in issues that are opaque to the general public, but in areas that firms can obtain economic rents (Bebchuk & Jackson, 2012). For example, government contracting is generally opaque to the general public, but highly profitable for successful firms. For this reason, research suggests that media attention can be a negative influence on CPA. This is true even when that attention is positive because even positive media attention reduces political opacity. For this reason, both general media attention and even positive media reputation have a negative effect on the association between CPA and contract awards (Hadani, Aksu & Coombes, 2021).

Political Environment

The political environment in which the firm operates can influence its engagement in CPA. In a study on the influence of covert CPA through dark money, which is donations with undisclosed donor information, Werner (2017) found that on average, investors positively reacted when it was revealed that firms were making these political investments. This was especially true when the firm previously engaged in CPA or they were in heavily regulated industries, but it was viewed negatively if the firm had been previously asked by shareholder resolution to reveal all of its political investments. In an extension of this work, Minefee, McDonnell, and Werner (2021) found that when firms’ dark money investments were targeted toward controversial sociopolitical issues, investor reactions were negative. Firms’ participation in CSR mitigated this relationship.

The relationship between CPA and investor reactions is bidirectional. That is, while the magnitude and type of CPA can influence investor reactions, investor reactions can also influence a firm’s CPA. Heavy foreign institutional investment can lead to increased political and regulatory scrutiny. Shi, Gao, and Aguilera (2021) find that firms with heavy foreign institutional investment manage and mitigate these risks by investing in CPA.

The external environment has been shown to influence and modify the effectiveness and return on CPA. Blau et al. (2013) found that if a bank had political connections, they were more likely to receive TARP funding and they received more of that funding earlier than non-politically engaged banks. Firms are constantly scanning the political environments in which they operate to identify potential opportunities and threats. Bonardi et al. (2005) found that the political environment the firm was in, including the attractiveness of the political market and rivalry among politicians and interest groups, as well as the firm’s political capabilities can influence how much a firm spends. Favorable internal and external characteristics will decrease a firm’s political transaction costs. While the environment might influence how firms engage in CPA (Brown, Manegold, & Marquardt, 2020), government risks have been found to be especially important in influencing firm CPA (Abdurakhmonov et al., 2021). When government risks are perceived to be high, through public political risk and home government relations, firms will attempt to evade risk with the host government (De Villa, Rajwani, Lawton & Mellahi, 2019). This is accomplished by trying to evade government attention, rapid compliance with government regulations, reconfiguring the firm, and anticipating future public policy. Another example of how changes in the political environment influence the way firms engage in that political environment can be found by looking at firms’ political activity before and after the Citizens United case. The Supreme Court case of Citizens United removed limits on political donations for firms. In response, lobbying and PAC activity of firms increased in both the amount they invested as well as the frequency of investments (Coates, 2012). Firms respond to incentives and opportunities. This has been understood when examining market competition, but these findings suggest that firms also respond to nonmarket characteristics in a similar manner.

The Variety of CPA Approaches

Prior research on corporate political activity (CPA) has primarily focused on lobbying and campaign contributions. These political spending variables are especially common in the case of studies using US samples. This may be primarily due to the fact that US laws require that firms disclose their lobbying expenses and campaign contributions. In this section, we will outline how researchers can contribute to our knowledge of the approaches to CPA. We will examine how firms attempt to both influence new policy and manage and mitigate policy implementation by the government.

Firms engaged in CPA pursue a variety of political tactics. Financial strategies are strategies in which firms provide financial support and incentives to politicians and access the political process in return (Hillman & Hitt, 1999). Financial contribution strategies are usually identified with the US context because organizations can contribute through Political Action Committees (PACs). The Federal Election Commission (FEC) made PAC summary data available (Fremeth et al., 2016; Milyo, Primo & Groseclose, 2000) to the public from the early 1980s. This enabled researchers to analyze campaign contributions by firms. Campaign contributions are payments from individuals or PACs. Both individuals and PAC giving can be tied back to the corporations they originated from (Fremeth et al., 2016).

Another form of CPA strategy is relational strategies which have been extensively studied in the literature. There are various ways that organizations attempt to build relationships and develop networks with policy-makers (Chung & Ding, 2010; Faccio et al., 2006). One tactic to develop a network with policy-makers is to appoint a former politician to be a member of the corporate board (Gray, Harymawan, & Nowland, 2016; Dahan, Hadani, & Schuler, 2013; Goldman, Rocholl, & So, 2009; Faccio et al., 2006; Hillman, 2005; Fisman, 2001). A second approach is to engage in lobbying. Hillman and Hitt (1999) describe the aims of lobbying are “to affect public policy by providing policy-makers specific information about preferences for policy or policy positions and may involve providing information on the costs and benefits of different issue outcomes” (p. 834). In comparison to campaign contributions, there is far less detail on lobbying activity at the federal level in the United States (De Figueiredo & Richter, 2014). There is some research that evaluates different forms of lobbying. Grassroots lobbying describes attempts to reach policy-makers indirectly via constituents (Thomson & John, 2007). In these cases, lobbyists try to “influence public policy by gaining support of individual voters and citizens, who, in turn, express their policy preferences to political decision makers” (Hillman & Hitt, 1999, p. 834). Sectors with high public visibility such as health care, arts and entertainment, and energy tend to see higher levels of grassroots activities (Walker, 2012). Some research suggests that grassroots is one of the most effective forms of lobbying (Lord, 2000; Nownes, 2006).

The third type of political strategy is generally referred to as informational strategy. Firms provide specific information to the government agencies about their preferred policies (Hillman & Hitt, 1999). This type of CPA can be viewed as a part of the firm’s communication strategy for developing trust between the firm and policymakers (Liedong, Ghobadian, Rajwani, & O’Regan, 2015). While these approaches to CPA have been studied, what is less common is investigating how firms engage in these CPA efforts. We examine in the following section how these approaches differ depending on whether a firm is attempting to manage or mitigate regulations or legislation, or they are trying to influence government policy.

“Manage and Mitigate” Policies

CPA researchers have identified two primary ways in which CPA can be beneficial to firms. First, CPA helps firms to influence the creation of new and favorable legislation. This can be viewed as the proactive approach to CPA. Firms can also reactively use CPA to manage and mitigate unfavorable policy or legislation. Although both these goals of CPA have been acknowledged in prior literature, empirical studies have seldom evaluated whether performance outcomes of CPA vary depending on which of these two separate sets of goals the firm is attempting to accomplish. In this section, we examine research that goes beyond firm lobbying dollars spend and instead investigate how firms are using their political spending and how they are engaging in CPA to mitigate harmful regulation and legislation.

Administrative Lobbying

In the political science literature, lobbying has been broadly bifurcated into two types of lobbying activities: administrative and legislative lobbying. Legislative lobbying is targeted at legislators in an effort to create new laws, while administrative lobbying is targeted at government agencies. These government agencies are tasked with implementing the laws and policies of the government. Administrative lobbying is a prime example of managing and mitigating the implementation of government legislation. Research has found that high levels of legislation and yearly increasing regulation increased CPA as a firm response (Brown, Goll, Rasheed, & Crawford, 2020), suggesting that firms respond to increased regulation through CPA to mitigate the effects of the new and changing regulatory environment. At the state level, lobbying of the heads of state agencies increases the influence that firms have over the decisions made by those agencies over time (Kelleher & Yackee, 2006). In addition, these interactions lead to increased contracting between the agency and the organization, although this is moderated by the agency’s proclivity to contract out public service deliveries (Kelleher & Yackee, 2009). At the federal level, McKay and Yackee (2007) examine what happens when two or more interests are lobbying on opposing sides of a potential policy. They find that the “squeaky wheel gets the grease,” and they suggest that the more a firm lobbies a particular agency, the more likely an agency will change the content of their final rules in favor of the group most actively lobbying. This is especially important for firms as these agency rule changes exhibit a “bias towards business” in that business lobbyists have influence over the content of the final agency rules, but nonbusiness lobbyists do not (Yackee & Yackee, 2006). Future research should continue to directly examine how firms are spending their lobbying dollars (Rivera & Patnaik, 2017) and what the outcomes of those lobbying dollars are.

Internal and External Lobbyists

In their lobbying efforts, firms employ two types of lobbyists, internal lobbyists, and external lobbyists. Internal lobbyists are generally legal counsel employed by the firm representing the firm as a lobbyist and meet the requirements to file under the lobbying disclosure act. On the other hand, external lobbyists are not employed by the firm but rather are external actors hired as intermediaries between the firm and government officials. In the US, firm lobbying spending data can be obtained from the Opensecrets.org company aggregation of lobbying disclosure reports filed to the Federal Election Commission (FEC). Prior CPA research has rarely differentiated between these two types of lobbyists in terms of their effectiveness or suitability for specific lobbying goals. In one of the few papers examining external lobbyists specifically, Tyllström and Muarry’s (2021) qualitative study of external lobbyists found that there can be agency issues between the firm and the lobbyists that they hire. This can be a potential risk for the firm because they also find that intermediaries can shape their client’s agendas. More recently, Nalick et al. (2022) finds that when a CEOs ideology diverges from the ideological bents of those in power, internal lobbying decreases more when compared to external lobbying. Future research should continue to further investigate the differences between internal and external lobbyists. Comparative evaluation of the effectiveness of internal and external lobbyists is an area where there is little research available. Also, at this point, we do not have much understanding of the contextual factors that influence a firm’s decision to choose internal or external lobbyists, or a combination of the two.

Lobbying Breadth/Lobbying Strategy

Prior CPA research has focused on the firms that spend their resources on lobbying. Prior research has paid very little attention to lobbying firms themselves, although they are the key actors in this arena. Lobbying firms differ in terms of their revenues, number of lobbyists employed, the type of lobbying they do, and the strategies that they pursue. The lack of research on lobbying firms may be partly due to the fact that lobbying firms are privately held and are not required to disclose much information about their activities. However, lobbying firms must disclose what agencies they lobby and the issues they are attempting to influence. At this point, it appears that researchers have not taken full advantage of this publicly available data, although there are some notable exceptions. Abdurakhmonov et al., (2021), for example, investigated where firms target their lobbying expenditures. They found that broadly lobbying across various lobbying agencies and legislative acts can mitigate political risks. Firms with increased risk will increase the breadth of lobbying. In contrast, other risk mitigation variables, such as slack, will decrease the relationship between risk and lobbying breadth. Lobbying breadth has also been found to influence the performance of the firm measured both in economic performance and awards of government contracts (Ridge, Ingram, & Hill, 2017). In general, increased lobbying breadth across a variety of issues and agencies improves performance. Ridge et al. (2017) found diminishing returns at the very highest levels of lobbying breadth.

Appointment of Politicians on Boards

The appointment of politicians on boards has increased over time (Korn/Ferry International, 2000). Hillman (2005) found that these politician appointments are much more frequent in highly regulated firms. Further, the appointment of politicians on boards was found to lead to better performance based on market-based measures regardless of whether or not they were in a highly regulated industry. Yoshikawa, Rasheed, and Del Brio (2018) examined the impact of performance decline on firms’ likelihood to either appoint directors who are politically connected or to engage in downsizing. By examining more than 1,000 firms across 11 countries in Europe, they found that in heavily regulated industries, firms were more likely to hire politically connected directors while firms in industries with lower regulation would instead choose to downsize. On the other hand, Lester et al., (2008) examined how firms evaluate the social and human capital of former politicians when examining whether firms will hire a former politician as a director. They find that both breadth and depth of human capital are positively associated with being appointed as a director of a firm. Also, politicians are much more likely to be appointed as soon as they leave office, and the likelihood sharply decreases over time. Surprisingly, political party affiliation in power did not influence appointment.

Political Connections

In addition to appointing politicians to a firm’s board, firms can take advantage of political connections that do not necessitate a board appointment. These connections can be passive, such as firm-government connections through political voting districts, to active forms such as lobbying or PAC contributions (Duchin & Sosyura, 2012). These connections were found to influence firm TARP funding, but they were also associated with underperformance as compared with firms that were not politically connected (Duchin & Sosyura, 2012). In studying political connections, Faccio et al. (2006) found that if a top officer of a firm was previously a head of state, a government minister, or a member of national parliament, their firm was subsequently more likely to be bailed out, and this bailout frequency increased when the International Monetary Fund or the World Bank provides financial assistance to the home government of the firm. Direct connections do not always equate to financial returns for the firm. It appears that there is some context specificity involved. For example, personal ties to Richard Cheney through board linkages did not provide any financial value to the connected firm when measured by market reactions (Fisman et al., 2012). On the other hand, looking at partisan connections, Goldman, Rocholl, and So (2009) examine board members of S&P 500 companies and their ties to either the Republican or Democratic Party. Nomination announcements for a candidate politically connected to a board member resulted in increased abnormal stock returns for the firm. In addition, in the year 2000, firms connected to the Republican Party increased in value while firms connected to the Democratic Party decreased in value. Similar results were found when examining the House and Senate elections of 1994 with firms politically connected to the winning party increasing procurement contracts after the election while connections to the losing party results in a decrease in procurement contracts after the election (Goldman, Rocholl, & So, 2013). In addition to these direct benefits, politically connected firms might also be using their connections in an attempt to mitigate firm risks. Politically connected firms were found to have higher leverage and higher volatility in their stock price. These higher leveraged firms actually increased their leverage during the housing bubble prior to the 2008 financial crisis (Kostovetsky, 2015).

Proactive Influence of Policy and Government Support

In addition to mitigating the effects of legislation and enacted policy, firms are also active in promoting legislation helpful to the firm or fighting potential legislation that is harmful to the firm. Currently, management research in CPA has done little to investigate this side of the firm’s government interactions. This section will lay out several promising areas of future research and highlight the few papers that have shed some light on this process.

Legislative Lobbying

As mentioned previously, firms lobby the administrative agencies to influence the implementation of legislation and government policy. Equally important, firms also proactively attempt to influence the legislative process. This is seen most clearly in firms engaged in lobbying congress to pass or reject specific bills they are voting on. On their lobbying disclosure reports, lobbyists will indicate exactly which bill they are lobbying and on behalf of which firm in their descriptions of services rendered. At this point, CPA researchers do not seem to have taken full advantage of this publicly available information to examine either the process or effectiveness of legislative lobbying empirically. Hall and Deardorff (2006) examined the hiring of lobbyists as a legislative subsidy providing “policy information, political intelligence, and legislative labor to the enterprises of strategically selected legislators.” (p. 69). They suggest that firms are less able to change politicians’ minds, but rather find mutually beneficial situations in which the legislator and the organization have concurrent objectives.

PAC Contributions

Most empirical studies operationalize CPA as donations to political action committees (PACs) and lobbying expenditures. However, there has been very little effort to either theoretically examine PAC contributions as the proactive attempts to influence policy or to evaluate their effectiveness in terms of change in the content of legislation or passage or failure of legislation. Before the Lobbying Disclosure Act of 1995, and the subsequent lobbying data availability beginning in 1998, scholars primarily relied on PAC data in CPA research. Now, it is more common to see scholars simply examine lobbying data (Brown et al., 2018) or combine lobbying and PAC data as one single CPA measure (Brown, Manegold, & Marquardt, 2020). Because PAC contributions fund individual political campaigns, these funds target lawmakers in congress responsible for passing or rejecting future legislation. But with the turnover of political actors, it has been difficult to determine the profitability of investing in PAC spending (Hersch, Netter, & Pope, 2008), and when they are successful it appears to be in relatively narrow contexts (Wright, 2004). Future research should look at how firms engage in PAC contributions independently of other CPA activities such as lobbying. Specifically, scholars should see if PAC funding is primarily driven by an attempt to engage in proactive legislative influence in government more so than lobbying since lobbying could be targeted at both the legislative and administrative state. Theoretically, PAC giving, in the aggregate, should be a proactive CPA approach, but empirical work has yet to fully examine this approach. In our framework, PAC contributions and legislative lobbying are more similar to each other than legislative and administrative lobbying. PAC contributions are typically used to fund political campaigns. In this way, both PAC contributions and legislative lobbying will target lawmakers in congress.

On the other hand, administrative lobbying targets the administrative agencies that implement the law. Firms have to make choices in terms of relative allocation of resources between administrative and legislative lobbying. At this point, we have only a very limited understanding of how firms make these choices. More research is needed on firm CPA portfolios and how firms engage in proactive strategies to influence legislation and reactive CPA to mitigate harmful government actions.

Implications for Future Research

Our review of prior research on corporate political activity (CPA) clearly demonstrates that considerable progress has been made in recent years in understanding the CPA phenomenon. The review also suggests that progress has been somewhat uneven, with some research areas attracting multiple studies while other equally important research questions have received little attention. In this section, our goal is to highlight some of these research gaps and identify fruitful approaches for future research.

Need for a “Meso” Approach

Although it is widely acknowledged that both internal and external factors influence a firm’s willingness to engage in CPA, most studies have examined these predictors in isolation rather than in conjunction. A firm’s CPA approach is the joint outcome of both internal and external predictors. Simultaneous consideration of both sets of predictors is likely to provide a richer understanding than examining them in isolation. From a theoretical perspective, we suggest that we engage in a “meso” approach that incorporates the role and influence of institutions, specifically that of “normative institutions” in shaping CPA behaviors. For example, research is needed to determine how institutional logics shape decisions about “whether” and “how” to engage in CPA. At the same time, these factors influence CPA alongside more micro firm-level variables and macro-level external variables. Examining how these variables interact and influence each other, rather than examining them in isolation, will be key for advancing future research.

Alignment of Predictors with CPA Approaches

Our review shows that most studies focus on one specific type of CPA. Lobbying and PAC contributions still dominate the literature, although these are only two of the variety of activities that constitute CPA. While various CPA approaches have been acknowledged in the literature, rarely has research examined why a firm would engage in one approach over another. It is also possible that firms would choose a portfolio of CPA approaches, either to attain the same goals or different goals. The key unanswered research question involves the alignment of predictors with CPA approaches. That is, does the main predictor or combination of predictors of CPA determine the choice of specific CPA approaches? Understanding this relationship will help us gain more meaningful insights into the choice of CPA approaches by firms.

Collective Action

Prior CPA research has, in general, focused on CPA by individual firms (Hillman et al., 2004). Other disciplines, such as economics, have a long history in collective action research in lobbying (Olson, 1965). Firms are likely to engage in collective action when an industry is threatened by proposed regulation, import competition, or highly adverse environmental developments. Similarly, in highly fragmented industries, individual firms may be too small to have the resources to engage in effective individual CPA. Industries with strong industry associations may also be able to engage in collective CPA. A promising direction for future research is the predictors of collective action. Further, collective action requires considerable coordination among firms. The processes by which such coordination is achieved will help us understand why there is variance across industries regarding collective engagement in CPA.

CEO Political Activism

Currently, the literature on CEO political activism is focused on monetary contributions to politicians or political causes. But these are not the only way CEO political activism manifests. CEO activism is generally defined as corporate leaders taking public stands on social and environmental policy issues that are not directly related to their core business (Chatterji & Toffel, 2018). A variant of CEO activism is CEO political activism. Mike Lindell, founder, and CEO of My Pillow Inc., for example, has been an ardent supporter of former President Trump and the Koch brothers who run Koch Industries have been big supporters of right-wing causes. Such activism may lead to a backlash from certain stakeholder groups and increased loyalty from others. Sandikci and Ekici (2009) found evidence for consumer backlash based on political positions of firms. In a more recent study of investment professionals in the private equity industry, Bermiss and McDonald (2018) found that ideological misfit leads to employee departure and that those who leave join organizations that fit their ideology better. These studies have significant implications because firms are often identified with their CEOs in the public mind and strong political positions by CEOs may have unintended consequences, especially when the CEOs’ political positions are misaligned with their employees (Brown, Manegold, & Marquardt, 2020) or the current political ideologies of those in power (Nalick et al., 2022). The implications of CEO political activism in terms of reactions by financial markets, customer groups, and employees are yet to be researched.

Lobbying Approach

Lobbying firms are the key players in lobbying efforts, but they have so far remained black boxes in CPA research. Although clustered mostly in the same location, lobbying firms vary widely in terms of the number of lobbyists, backgrounds of the lobbyists, and their specializations. Some lobbying firms are specialists focusing on a small number of industries or issues. Others tend to be generalists providing services in a number of areas and issues. An important research question is how firms decide to hire a specific lobbyist. Second, it will be interesting to examine whether specialists or generalists are more successful in lobbying for a specific issue or cause. Similarly, if multiple lobbying firms are working on the same issue on behalf of multiple firms, it would be important to examine if there is any formal or informal coordination among them, considering that there are tight networks of connections among individual lobbyists.

Firm Performance

It is widely documented that firms are expending ever-increasing resources to CPA, and there is no sign that this trend is likely to slow down in the future (Evers-Hillstrom, 2020). A survey by The Conference Board (2022) reveals the environment for corporate political activity shows no signs of calming in 2022. Surprisingly, researchers have not been able to find a clear positive relationship between CPA and firm performance. Although our review did not focus on the performance implications of CPA, the framework we proposed could be of considerable value in future investigations of the CPA–performance relationship. A better understanding of what is driving firm CPA and why firms are engaging in CPA and why they use the CPA approach that they do could help understand the CPA–performance relationship with greater granularity. Second, it may be more meaningful to examine intermediate outcomes that are more proximal than firm performance. The problem with using contemporaneous accounting measures to assess the effectiveness of CPA is that performance could be affected by a multitude of other factors that make it impossible to isolate the effects of CPA. Second, the effects of CPA may be felt over several years and not immediately. At least in some cases, such as hiring a lobbying firm to lobby for or against import tariffs can be evaluated in terms of whether the goal was achieved or not. Similarly, the effectiveness of campaign contributions to a candidate can be assessed in terms of the legislator’s voting record in issues that are salient to the firm.

Exploration of Nonlinear Relationships

Despite the accumulation of a large number of studies on nonmarket strategies, including studies focused on CPA, researchers have found it difficult to draw meaningful generalizations about the antecedents and outcomes of CPA (Hadani, Bonardi & Dahan, 2017). Part of the reason may be the context specificity of these relationships. A more likely reason for conflicting findings may be the assumption of linearity in these relationships. For example, the relationship between CPA and performance may be nonmonotonic. Once CPA reaches a certain level, returns from additional CPA expenditures may at best be marginal due to diminishing returns. It is even possible that CPA may cause a negative backlash beyond a certain level because politicians do not want to appear as “bought” by corporations. Stakeholder groups may turn against a firm and withdraw support if a firm is perceived as attempting “state capture.” Therefore, we suggest that future researchers attempt to theorize nonlinear relationships and test them with appropriate statistical models.

Is CPA Activity Strategic or Is It an Agency Problem?

CPA research has typically considered CPA as an attempt to improve firm performance or achieve objectives of the executives (Fremeth et al., 2016). CPA has been viewed as an attempt to be strategic in that its ultimate goal is to improve firm performance, and meta-analytic research supports this view (Lux, Crook, & Woehr, 2011). Research has also found that the campaign contributions of corporate executives can be tied to strategic motivations. For example, executives with more incentive-laden compensation schemes are more likely to contribute to political candidates (Gordon, Hafer, & Landa, 2007), and executives target those politicians who have the most influence on the policies and issues most salient to their firms (Ovtchinnikov & Pantaleoni, 2012).

There is also evidence suggesting that campaign contributions represent an agency problem within the firm. For example, Hadani and Schuler (2013) suggest that the principal–agent problem might be one reason that the CPA and firm performance relationship has been difficult to support empirically, and in some cases, why the relationship is negative. Others have identified firms whose PACs contribute more in aggregate suffer financially and engage in other activities that are consistent with agency problems (Aggrawal, Mescke, & Wang, 2012). Fremeth and colleagues point out that research has not systematically tied PAC transactions to the preferences of executives, despite the growing interest in an agency explanation for CPA (Fremeth, Richter, & Schaufele, 2016). The evidence that CPA, at least in some cases, may be a manifestation of agency problems suggests the need to examine the antecedents and contextual characteristics of strategic engagement in CPA versus CPA as an agency problem. Even in the absence of agency issues, it is difficult to say if a firm’s CPA is necessarily strategic. It is entirely possible that some of it is due to isomorphic forces and that firms engage in CPA because other firms within the industry are doing so. Banerjee and Venaik (2018), in their study of Australian subsidiaries of MNCs, for example, found that their CPA activities were mostly mimetic in nature.

Covert CPA

While firms engage in CPA using a variety of different modes and for a host of potential outcomes, one aspect of CPA that is often ignored is how firms might conceal CPA to some stakeholders to avoid any of the negative consequences of CPA. Firms potentially engage in these false representations (Hewlin, 2003) due to their perceived vulnerability in terms of who they associate with in political markets. This can lead to unwelcome inquiry by societal stakeholders (Baumgartner et al., 2009; Jia, 2018; Kim, 2019). Brown, Manegold, and Marquardt (2020) found that firms will increase their CSR as they begin to increase CPA in response to increased regulation. They suggest that firms do this as part of their effort to manage general public stakeholders while still influencing the content and intensity of regulation by the government via CPA. We also have some evidence of stakeholder response to covert CPA after the revelation of dark money contributions of firms (Werner, 2017; Minefee, McDonnell, & Werner, 2021). One of the problems of doing research on covert CPA is that by definition, firms are attempting to conceal these actions, and therefore, information may not be easily available in the public domain. More research into this phenomenon would help scholars to not only understand the benefits of CPA on firms’ outcomes but also better understand the negative consequences that firms must consider when engaging with government.

Intra-firm Drivers of CPA

One often missing level of analysis in CPA research is the importance of intra-firm drivers on firm CPA decisions (Sun et al., 2021). Liedong et al. (2015) point out that in the context of CPA and CSR, inter-and intra-firm trust can be an important variable in firm performance. Shaffer and Hillman (2000) suggest that three types of intra-firm conflicts exist when developing business–government relations. These include proactive policy positions, compliance modes, and representational conflict. Future research should investigate how internal stakeholders (e.g., employees and shareholders) shape CPA. In addition, while some research on CEO political activism has examined turnover intentions (Brown, Manegold, & Marquardt, 2020), actual employee departure (Bermiss & McDonald, 2018), and consumer backlash (Sandikci & Ekici, 2009), more research is needed to understand how CPA more broadly shapes perceptions of the firm to internal stakeholders.

Application of Novel Methodological Approaches

One of the ways of advancing CPA research is by applying novel methodological approaches that can provide new insights. One of the most promising approaches is fuzzy set analysis. This is most applicable when many factors influence a dependent variable and evaluating them in isolation from one another may not be meaningful. Instead, they can be examined in “bundles,” or combinations, that may mutually enhance the ability of each to achieve important organizational outcomes (Fiss, Cambre, & Marx, 2013). Configurational perspectives allow for the study of “multi-dimensional constellations of conceptually distinct characteristics that commonly occur together” (Fiss, 2007, p. 1180). Employing a configurational approach enables examinations into how multiple factors can combine together along different paths to achieve similar outcomes (Aguilera, Filatotchev, Gospel, & Jackson, 2008; Hoskisson, Castleton & Withers, 2009; Ward, Brown, & Rodriguez, 2009). We suggest that configurational approaches may be particularly suitable for CPA research. For example, a firm may be pursuing a number of nonmarket strategies at the same time, such as CSR, campaign contributions, and lobbying. Some of these activities may be complementary, whereas others may be substitutes for each other. The configurational approach may also be appropriate for examining different bundles of market and nonmarket strategies as well. The development of methodological tools such as fuzzy set analysis (Fiss, 2007) makes it possible for researchers to examine how different combinations of nonmarket strategies could work together in dissimilar ways to produce similar levels of performance as the principle of equifinality (Katz & Kahn, 1966) suggests that a variety of paths can lead to the same outcome.

Management research has used social network analysis to provide insight into many relevant research questions (Burt, Kilduff, & Tasselli, 2013). Borgatti and Foster (2003) suggest that relationship networks are useful for understanding board interlocks, information flows, social contagion, joint ventures, and group processes (Borgatti & Foster, 2003). Lobbying relationships between both firms and lobbyists and also firms and politicians fit nicely into a network structure for future analysis. Different firms hire overlapping lobbyists or lobbying firms. This provides bipartite network relationships that have, to this point, been unstudied. Scholars should investigate what drives nonmarket networks. This type of network research could also shed light on whether firm-level concerns override industry or country-level concerns when constructing lobbying networks. In addition to examining which lobbyists were hired by firms, future research should analyze lobbying networks by firms lobbying on similar issues, the same agencies, or overlapping bills.

Finally, it may be of considerable value to apply qualitative methodologies to study CPA by firms to develop richer theory. Currently, we capture CPA activity mostly by dollar expenditures, but we have little knowledge of the complex decision processes that result in these expenditures. Nor do we have much knowledge about the activities of the lobbyists themselves. Qualitative research including in-depth interviews with company executives and lobbyists, as well as detailed examination of the trail of paper and money can hopefully take us beyond the black box approach wherein we look at the input (expenditures) and output (performance) without examining the underlying processes.

Theoretical Synthesis

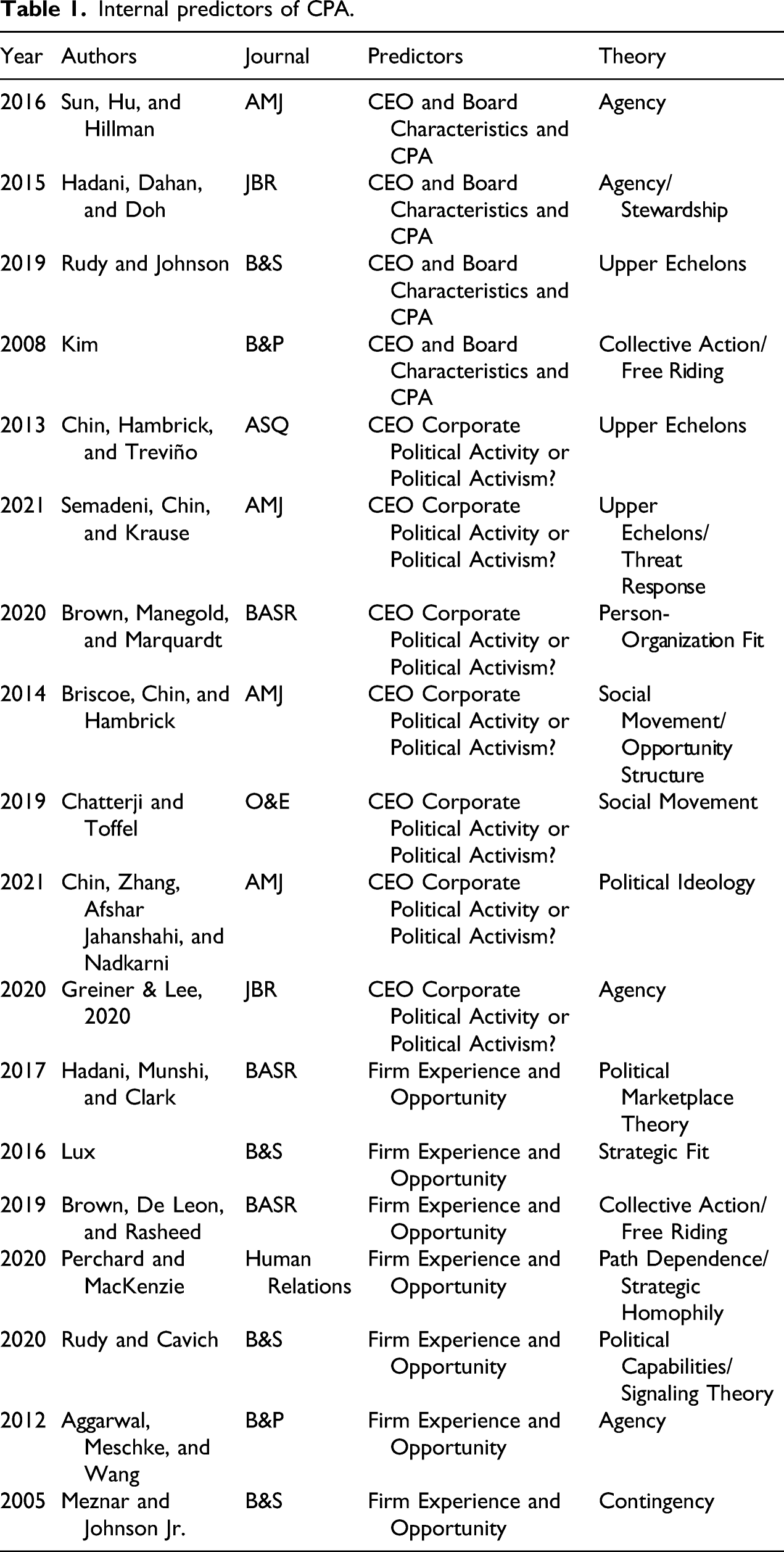

Internal predictors of CPA.

External predictors of CPA.

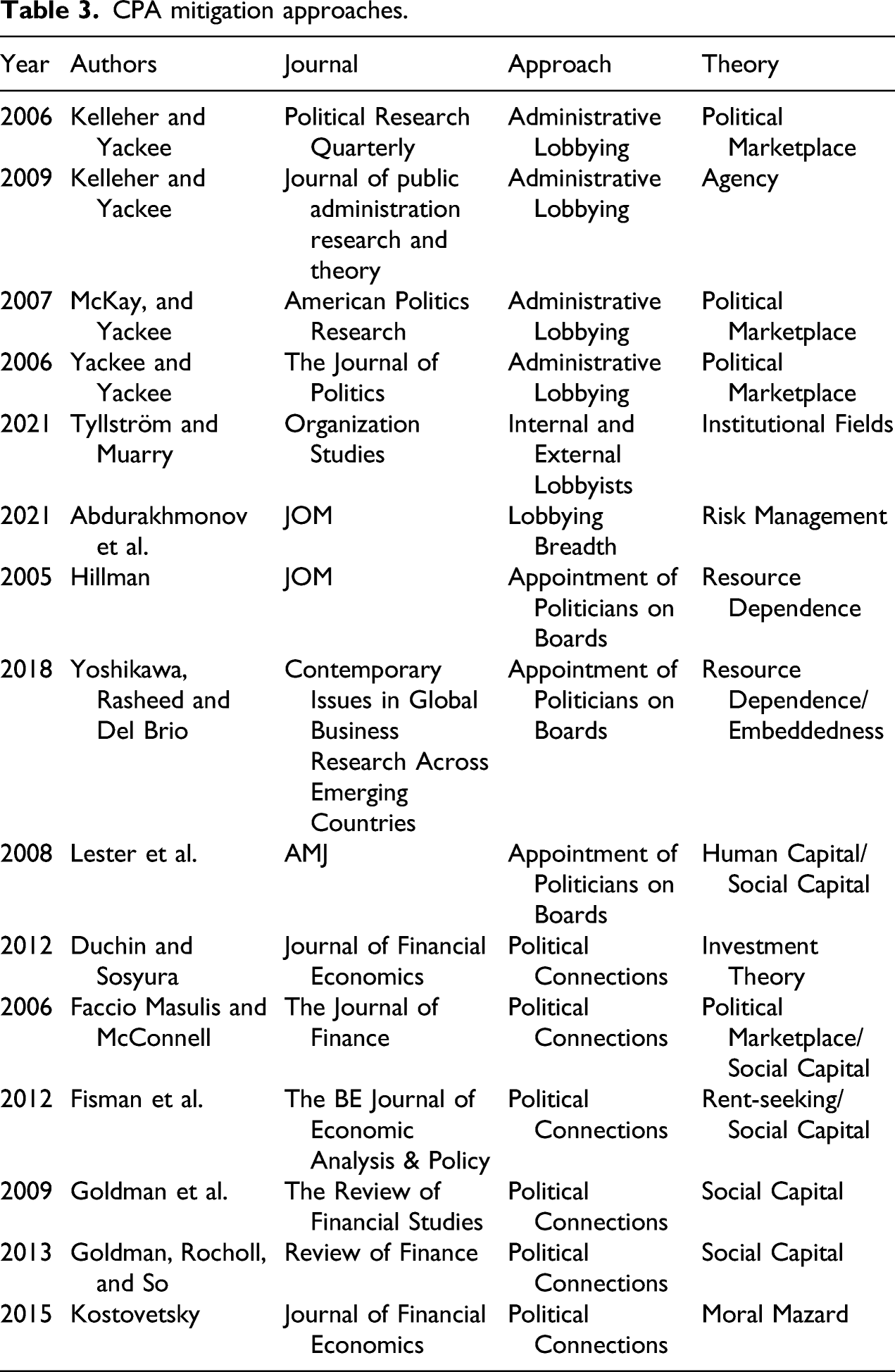

CPA mitigation approaches.

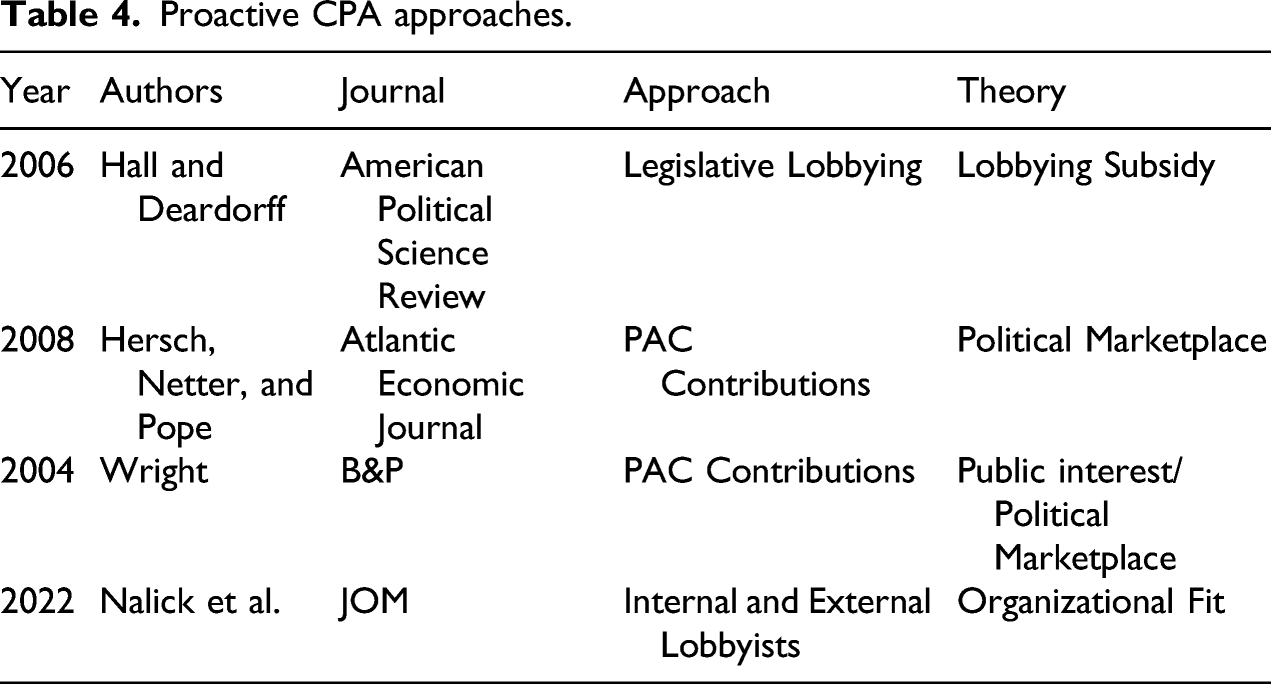

Proactive CPA approaches.

Conclusion

Organizations are increasingly recognizing that they must complement their market strategies with nonmarket strategies to survive and succeed (Doh et al., 2015; Mellahi et al., 2016; Dorobantu et al., 2017). Our review focused on an important type of nonmarket strategy—CPA. This is primarily due to the attention it has received from researchers across a wide variety of academic disciplines. The accumulation of empirical studies has led to attempts to discern generalizable relationships among CPA, its antecedents, and outcomes. Our review examines extant research on CPA using an integrative organizing framework that incorporates the complexity of the CPA phenomenon in terms of its multiple predictors and the variety of activities that constitute CPA. Our review systematically classifies different types of political strategies and explains why a firm would choose one political strategy, or a combination of strategies, over another. We highlight the complex factors that drive the firm’s CPA decision-making process and then shed light on the variety of CPA approaches that firms use to mitigate or proactively influence regulation and legislation. Lastly, we have offered suggestions for advancing research on the CPA of firms. While much has been learned about CPA over the last few decades, our framework highlights many areas in which scholars should aim for future investigation to shed light on the myriad of ways that firms engage in CPA and the variety of reasons that influence that decision.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.