Abstract

Do economic performance and economic news coverage influence public perceptions of the economy? Efforts to assess the effects are hampered by the interrelationships among the variables. In this paper, we bring to bear a more careful accounting of available economic variables than previous studies have used. We find that both media tone and economic attitudes are strongly related to actual economic performance. Moreover, after taking into account the economy itself, a substantial relationship between media tone and economic attitudes persists. Given that economic attitudes influence a wide variety of political outcomes, this finding carries important normative and political significance.

Economic performance influences important political phenomena such as presidential approval and election outcomes (e.g., Hibbs 2000; Kramer 1971; Lewis-Beck 1988; MacKuen, Erikson, and Stimson 1992; Tufte 1975). Incumbent presidents and their parties are rewarded in good economic times and punished in bad ones. But how, exactly, do citizens assess the economy in the first place? The simplest explanation is that citizens’ economic well-being causes their economic assessments, which in turn influence their political opinions and behaviors. A second explanation is that news coverage of the economy, rather than the economy itself, drives citizens’ economic perceptions. And a third possibility is that both economic news coverage and real economic performance shape public perceptions of the economy.

Determining whether the media plays a role in the process is important because there is no reason to expect that media coverage will perfectly mirror actual economic performance. In fact, a substantial body of empirical evidence argues that news coverage of the economy does not always track economic performance (e.g., Blood and Phillips 1995; Doms and Morin 2004; Goidel and Langley 1995). Sometimes news coverage will be more positive than economic performance warrants, and often, it will be more negative (Soroka 2006). If citizens’ economic assessments respond to news coverage (either instead of or in addition to responding to actual economic performance), the political rewards and punishments they confer on politicians and parties may be biased. This, of course, was George H. W. Bush’s concern in his bid for reelection in 1992, when he claimed the economy was performing at a notably higher level than the media was giving him credit for (Hetherington 1996).

Despite the importance of distinguishing the effects of actual economic performance and news coverage of the economy, doing so is difficult. Published research demonstrates that news coverage of the economy predicts economic attitudes (Casey and Owen 2013; De Boef and Kellstedt 2004; Doms and Morin 2004; Fan and Cook 2003; Goidel and Langley 1995; Goidel et al. 2010; Hollanders and Vliegenthart 2011; Nadeau et al. 1999; Soroka 2006; Soroka, Stecula, and Wlezien 2015). But there are reasons to question whether the evidence reflects a causal relationship. As observed by Soroka, Stecula, and Wlezien (2015): The fact that media variables are statistically significant predictors of public perceptions need not mean that news coverage actually causes those perceptions. It may be that media measures just do a very good job of capturing the economy itself, better even than particular economic indicators. (Soroka, Stecula, and Wlezien 2015, 471)

This article attempts to estimate the effect of economic news on economic attitudes to assess whether media coverage has a distinct effect on economic attitudes above and beyond the role played by actual economic performance. To do this, we employ a new measure of media tone developed by applying supervised machine learning (SML) methods to thousands of newspaper articles in four national newspapers and validated by human coding. We make new contributions on the questions of how economic performance and media tone affect collective economic attitudes by estimating models of media tone and economic attitudes that are “saturated” with economic indicators and then analyzing the relationship between the residuals from these two models. The approach allows us to determine whether the portion of economic news coverage that cannot be explained by economic fundamentals has a significant relationship to the portion of citizens’ economic attitudes that also cannot be explained by economic fundamentals. The evidence we present suggests that it is not merely the case that media tone and mass economic attitudes move together. We find that a substantial relationship between media tone and public opinion persists even after taking into account actual economic performance.

The Case for and Against the Influence of Economic News on Economic Perceptions

At the outset, it is useful to clarify what we mean—and what is generally meant—by the term economic performance. We are interested in the overall, aggregate performance of the U.S. economy as measured by a large number of economic indicators, many of which are produced by the government. For example, the economy is stronger when unemployment is lower and growth is higher. Collectively, the range of available economic indicators provides a good proxy for the reality of economic performance.

A second initial issue to consider relates to the effect that economic news coverage may have on economic attitudes, specifically consumer confidence (which we measure with the Index of Consumer Sentiment [ICS]). News coverage of the economy surely reflects some of what is happening with the economy “on the ground.” This first portion of news coverage includes reports and discussion of jobs reports, stock market trends, economic growth, and so on. At the same time, there may be other aspects of economic news coverage that are out of sync with economic performance—what we will call extra-economic news coverage, defined as that portion of economic news coverage that are not explained by economic fundamentals. 1 Some of this extra-economic media coverage might not reflect economic “realities.” For instance, some extra-economic coverage might be due to journalists letting their personal perspectives color their reporting. Yet some extra-economic media coverage may contain valid economic cues that our measures of economic fundamentals fail to capture. The economy is, after all, more than the sum of government statistics. It is important to determine whether this extra-economic media coverage is related to citizens’ perceptions. Thus, an important question to consider is whether extra-economic news coverage of the economy influences public opinion about economic performance. Several conceptual and empirical issues make answering this question difficult.

Conceptual Issues

Let us consider the reasons we might expect—and might not expect—economic news coverage to influence consumer sentiment. We begin with the observation that public perceptions of economic performance are clearly related through some causal chain to economic performance. 2 When times are good, people are more positive in their assessments than when times are not so good. Evidence of this relationship is abundant. Summarizing the empirical research, De Boef and Kellstedt (2004, 647) write that “we have long known that economic conditions influence consumer sentiment.”

It may be the case that the positive correlation between economic performance and economic assessments reflects a direct causal link, with no media influence. Unlike some social and political phenomena that most people experience exclusively through the media (e.g., foreign conflicts), members of the mass public routinely experience the economy, which may shape their perceptions of economic performance. People get and lose jobs. Their earnings increase and decrease. The prices they pay for goods and services change from month to month. Relatedly, through social interaction, people may learn about the experiences of friends, family, colleagues, neighbors, and others. Collectively, all of these experiences could produce aggregate public opinion about the economy that reflects overall national economic performance. When times are good, more people get and keep jobs, earn more money, buy more goods and services, and so on. These experiences in turn produce more positive assessments of the economy. When times are bad, the reverse takes place. In short, collective economic experiences may directly lead to collective economic opinion. No direct, intervening, or any other effect of the media is necessary. 3 Indeed, it may be that “economic issues are precisely the type least likely to be influenced by mass media, presumably because of the immediacy and accessibility of personal experiences” (Mutz 1992, 484).

Yet the tone of news coverage of the economy may also influence collective economic opinion (Kiewiet 1983; Nadeau et al. 1999; Soroka 2006; Soroka, Stecula, and Wlezien 2015). Content analyses of news coverage (television and newspapers) routinely reveal that the economy receives a substantial amount of coverage, both in absolute terms and relative to other issues (Boydstun 2013; Harrington 1989). News coverage of the economy may provide citizens with context for understanding their own economic experiences and, thus, judging economic performance. And people are likely exposed to at least some of the news coverage of the economy. The exposure might be direct or indirect, and it might be intentional or unintentional. In any case, the sizable amount of news coverage of the economy in combination with many citizens’ regular exposure to it suggest the plausibility of the proposition that mass economic attitudes are influenced by news coverage of the economy.

Importantly, some portion of the economic news coverage that may be influencing collective perceptions of economic performance may be biased, in the sense that it is overly optimistic or pessimistic than economic performance warrants. In other words, a part of news coverage about the economy may be “extra-economic,” meaning simply that it strays from economic realities. There are at least four reasons that a portion of news coverage may be extra-economic in nature. First, journalistic incentives might create a negativity bias in reporting (Soroka 2006). Second, journalists may unintentionally bring their subjective (and inaccurate) perceptions of the economy to bear on their reporting. Third, the information available to news outlets at the time of reporting might not be accurate. For example, during the presidential campaign period between January and October of 1992, the government’s initial reports of economic performance indicated an average monthly increase of twenty-five thousand jobs, a 1.5 percent increase in personal income, a 2.3 percent growth in consumer expenditures, and a GDP growth rate of 2.0 percent. Over time, those estimates have been revised upward considerably and suggest that economic performance was indeed much better. The jobs, income, consumer expenditure, and GDP data now indicate increases of eighty-two thousand jobs, 2.7 percent, 4.8 percent, and 4.4 percent, respectively. In short, the revised estimates show that the economy in 1992 was performing two to four times better than initially reported. If the media faithfully and accurately reported the available economic information at the time, the tone would have been more negative than justified by economic reality, which only became apparent in official government reports afterward. From this perspective, Bush’s complaints about being blamed for a poor economy were legitimate (Hetherington 1996). Fourth and finally, the resource and agenda limitations of the media, along with the complexity of the economy, make it possible that even the most able and well-intentioned members of the media might present a picture of the economy that does not perfectly reflect economic reality.

A related consideration is that, just as economic assessments may be caused by economic performance, so, too, might news coverage of the economy. Amid their myriad goals, members of the media are motivated by accuracy in reporting (Cook 1998; Graber and Dunaway 2014). Existing empirical evidence substantiates the proposition that economic performance and the tone of news coverage move together (e.g., Casey and Owen 2013; Fogarty 2005; Goidel and Langley 1995; Hollanders and Vliegenthart 2011; Nadeau et al. 1999; Soroka 2006, 2012; Soroka, Stecula, and Wlezien 2015; Wu et al. 2002). One would expect a positive correlation (perhaps a very strong one) between the tone of news coverage of the economy and mass economic assessments, even if there is no causal relationship between the two because both are caused, at least in part, by economic reality.

Taking all of these considerations into account, we expect that economic performance directly influences media tone and economic attitudes. We also expect that the part of economic news coverage not driven by economic performance may have a significant influence on how citizens view the economy. In other words, we expect that just as actual economic performance directly influences economic attitudes, so too does media tone have an independent and direct effect.

If public perceptions of the economy are shaped by economic news coverage, either in lieu of or in addition to the influence of economic performance, the implications are significant. In a world in which economic news coverage perfectly reflects economic fundamentals, it does not matter politically (or normatively) whether economic attitudes respond to news coverage. In this case, news coverage provides the same information as the economy itself. This would not deny a causal influence on citizen perceptions; it could be that citizen responses to changing economic performance occur only because citizens hear about them through media coverage. Such a situation would not be of normative concern. Our concerns should begin at the point at which there are deviations between economic performance and economic news coverage. It is important to assess whether this extra-economic aspect of economic news coverage influences citizens’ economic assessments because we want to know whether news outlets have sway over citizens’ perceptions of the world.

These conceptual issues also pose an analytical problem. Since we have good reasons to think that economic performance influences both citizens’ economic perceptions and economic news coverage, and since we also have good reasons to think that economic news coverage might shape economic perceptions, how are we to disentangle empirically the relationships?

Empirical Challenges in Modeling Consumer Sentiment

The conceptual issues highlighted above present a central problem for assessing the relationships among economic performance, economic attitudes, and media tone: whether or not media tone causes economic attitudes, we expect the two variables to be positively correlated. One solution to this problem is to include economic performance measures along with a measure of media tone in models of economic attitudes. The logic behind this approach is that if the public responds to both (or only directly to media), then a relationship between media tone and economic attitudes will be evident even with economic performance in the model. For this approach to work, however, we must do an exhaustive job of capturing “economic performance” by including all relevant economic indicators that are correlated with economic media tone. Otherwise the estimated effects of media tone will be biased.

Although previous research makes important contributions, most studies include a relatively modest set of economic indicators and a limited lag structure. The result may be that media coverage measures serve as proxies for economic performance and pick up its effects in addition to any media effects. For example, Soroka, Stecula, and Wlezien (2015) control for current changes and one lag of the leading economic indicator index in their effort to determine the influence of media sentiment on consumer sentiment. 4 MacKuen, Erikson, and Stimson (1992) model sentiment as a function of current values of change in unemployment, inflation, and quarterly annualized growth in the leading economic indicator index, along with survey measures of attention to economic news. Goidel and Langley (1995) include the current unemployment rate, percentage change in the CPI over the last month, percentage change in the unemployment rate over the last twelve months, and percentage change in GDP over the last quarter—all at time t—along with counts of positive and negative news stories. De Boef and Kellstedt (2004) model sentiment as a function of a more extensive set of economic variables, including the lagging economic indicator index, the coincident economic indicator index, inflation, unemployment, and the federal funds rate—all at time t—along with a variety of political variables. Doms and Morin (2004) include the most comprehensive set of economic indicators in their effort to isolate the effect of news stories mentioning recession. They include percentage change in year over year change in the Standard & Poor (S&P), lags of monthly changes in the CPI, lags of the monthly unemployment rate, change in payroll employment, and current change in gas prices in their models of consumer sentiment. Their study is perhaps the strongest test of the influence of media coverage to date. They find that counts of the words “recession” and “economic slowdown” have an additional effect on consumer sentiment, beyond economic performance. As we will show below, even these more extensive sets of economic indicators are not enough to capture the full effect of economic performance. As such, much of the previous research reporting an effect of media on economic attitudes is prone to omitted variable bias and is, therefore, potentially misleading. If stock market performance, for example, is important to consumers’ evaluations of the economy, omitting market prices and their changes from models of consumer sentiment means those effects—because they are covered in the media—will be attributed to the media, rather than economic performance, where they properly belong.

We advance efforts to isolate the effects of economic performance and economic media tone on economic attitudes by fitting models of both media tone and economic attitudes as a function of a large array of economic indicators (including many lags and different period growth rates of each) in an effort to purge both measures of the variance that is explained by economic performance. Then, we examine the relationship between the residuals in these models for evidence of a direct relationship between media tone and perceptions of the economy. We also estimate a single model of economic perceptions including all our economic indicators and media tone. Throughout our analyses, we focus on the period from January of 1980 through December of 2014, using the month as our temporal unit of analysis.

A Strategy for Isolating the Effects of Economic Performance and Media Tone on Attitudes

For our analysis, we begin by adopting a strategy used by De Boef and Kellstedt (2004) and utilize many economic indicators and measures to tap economic performance. Specifically, to isolate the portion of consumer sentiment due to economic performance from that due to other factors, we estimate a saturated model of consumer sentiment that includes a large number of lags of a number of highly collinear economic time series and excludes media measures and lagged consumer sentiment, thereby maximizing the potential for the economy to explain variation in sentiment. The result, as De Boef and Kellstedt (2004, 6) note, provides “an excellent ex ante forecast of economic sentiment based solely on economic conditions.” The residuals from this model—what they refer to as irrational exuberance and pessimism, and what we call extra-economic attitudes—are thus purged, to the best of our ability, of the influence of economic performance.

In addition to estimating a saturated model of consumer sentiment, we also estimate a saturated model of the tone of economic news coverage. Our purpose in estimating this model is the same: to isolate the portion of the tone of economic news coverage due to economic performance from that extra-economic portion that is due to other factors, thereby purging media tone from its roots in economic performance. If we have effectively purged the consumer sentiment and media tone measures of their economic causes, then we have eliminated the possibility that economic performance confounds the relationship between media tone and economic sentiment in our analysis.

After purging both measures, we examine the relationship between the residuals from the two models and ask how the extra-economic portion of the tone of news coverage about the economy relates to the extra-economic portion of citizen evaluations of the economy. As an alternative approach to the same test, we also estimate a single equation that accomplishes this same task by regressing raw consumer sentiment on raw media tone, controlling for all the measures of economic fundamentals that we used to purge consumer sentiment and media tone above. To summarize our findings, we find that media tone has a significant relationship with economic attitudes above and beyond the influence of economic fundamentals, providing the best evidence to date that the tone of economic news coverage has an independent, direct connection with economic attitudes.

Measures of Economic Performance

Our chief goal is to purge both consumer sentiment and media tone of their respective economic causes. This means we need to be comprehensive in our selection of economic indicators. We include seven sets of measures of economic performance designed to capture the many dimensions of economic performance. The first four are identical to those used in De Boef and Kellstedt (2004): monthly and quarterly growth rates in the consumer price index (all urban consumers, all items, known as CPIAUCSL) as calculated by the Bureau of Labor Statistics (BLS) and downloaded from the database of economic data maintained by the Federal Reserve Bank of St. Louis – the Federal Reserve Economic Data (FRED); monthly and quarterly growth rates in the Conference Board’s Index of Lagging Economic Indicators 5 ; monthly and quarterly growth rates in the Conference Board’s Index of Coincident Indicators 6 ; and the monthly (civilian) unemployment rate (UNRATE) as calculated by the BLS and downloaded from FRED. 7 They capture quantities of central concern to families—prices and the job market—and, via the Conference Board indices, the “cyclical turning points” in the economy as measured by statistics that tap manufacturing activity, the labor market, financial conditions, and incomes. 8 And they capture short (monthly and quarterly) rates of change in aggregate economic performance. In addition, we include annualized changes in these same measures and unemployment twelve months prior to capture longer-term trends in economic performance. We also include three other sets of measures that tap economic performance: monthly, quarterly, and annualized growth rates in the number of jobs added (BLS); the monthly, quarterly, and annualized growth rate in real disposable per capita income (A229RX0, chained 2009 dollars, seasonally adjusted annual rate), downloaded from FRED; and monthly, quarterly, and annualized growth rates in the average daily closing stock prices in the S&P composite index, in 2016 dollars as reported by Shiller (2015) and downloaded from his website. 9 These measure trends in job growth, average incomes, and financial market performance. In total, we include fifty-seven right-hand-side economic variables, after accounting for the full set of lags and complement of growth rates. 10 We believe this comprehensive set of measures taps into the full range of economic activity as it may be perceived by consumers making judgments about economic performance.

Measuring the Tone of Economic News Coverage

Scholars have assessed media coverage of the economy using a variety of strategies. The usual approach is to identify stories about the economy, typically in the New York Times, and apply some coding rules or a dictionary to the text to create a measure of the tone of news coverage. Some have counted the frequency of use of the term recession as an indicator of negative tone (Blood and Phillips 1995; Doms and Morin 2004), or broader set of terms (Hopkins and King 2010). Others have applied sentiment dictionaries developed to capture the positive versus negative tone of discussion across any policy issue (and thus not specific to the economy) (Soroka, Stecula, and Wlezien 2015). Still others have generated and applied dictionaries in the specific context of the research question (De Boef and Kellstedt 2004). These different measures have significantly expanded our understanding of the causes and effects of media coverage of the economy.

Here, we borrow Barberá et al.’s (2016) dataset of economic media coverage, which builds on recent innovations in treating “text as data.” Barberá et al. measure the tone of economic news (i.e., positive, negative, or neutral) using supervised machine learning (SML) techniques (Gareth et al. 2013; Grimmer and Stewart 2013; Klebanov, Diermeier, and Beigman 2008; Lowe 2008; Monroe, Colaresi, and Quinn 2008; Monroe and Schrodt 2008; Van Atteveldt, Kleinnijenhuis, and Ruigrok 2008). Briefly, SML involves three steps. First, human coders label the tone of a sample set of texts. Second, the features of the labeled text (words and phrases) are used to predict the tone assigned by the humans in the sample. “In this way the classifier learns the relevant features of the dataset and the weight assigned to each” (Barberá et al. 2016, 10). The results are evaluated using cross-validation, in which the accuracy of predicted tone is compared with (out of sample) subsets of the human-coded data. The results from multiple classification methods are compared before the best classifier is applied to the full set of available texts in the final step. Monthly measures of media tone can then be created by computing the average predicted probability that the tone of an article is positive across all articles in a given month.

Barberá et al. (2016) develop and validate their measure of tone of the U.S. economy as presented in the New York Times from 1948 to 2014. 11 In what follows, we rely on a measure of tone generated by Barberá et al. (2016) using an expanded universe of media comprising the four national newspapers with the highest circulation in the United States: New York Times, Washington Post, Wall Street Journal, and USA Today. Although newspapers, and these newspapers in particular, do not capture the full extent of the media environment, they continue to originate the majority of policy-based content that is then circulated and filtered through the rest of the media system (Althaus, Edy, and Phalen 2001; Golan 2006; Haider-Markel and Cagle 2004; McCombs and Funk 2011).

Briefly, the measure was developed as follows: A sample of stories from each of the four newspapers over the period they are available electronically was selected using an extended keyword search. 12 A subset of four thousand articles from each newspaper was then randomly selected and human-coded using CrowdFlower. In the next step, the human-coded data were used to train a classifier on each individual newspaper. 13 The result is a predicted tone for each article in each newspaper. A monthly measure of tone was calculated for each paper by averaging across the predicted tone of the full set of articles in a given month. In the final step, the results for each newspaper were averaged to create a measure of the weighted average sentiment across the newspapers. The weights were based on the number of relevant articles in each paper in each month. For the analysis presented here, we focus on the time period from January of 1980 through December of 2014.

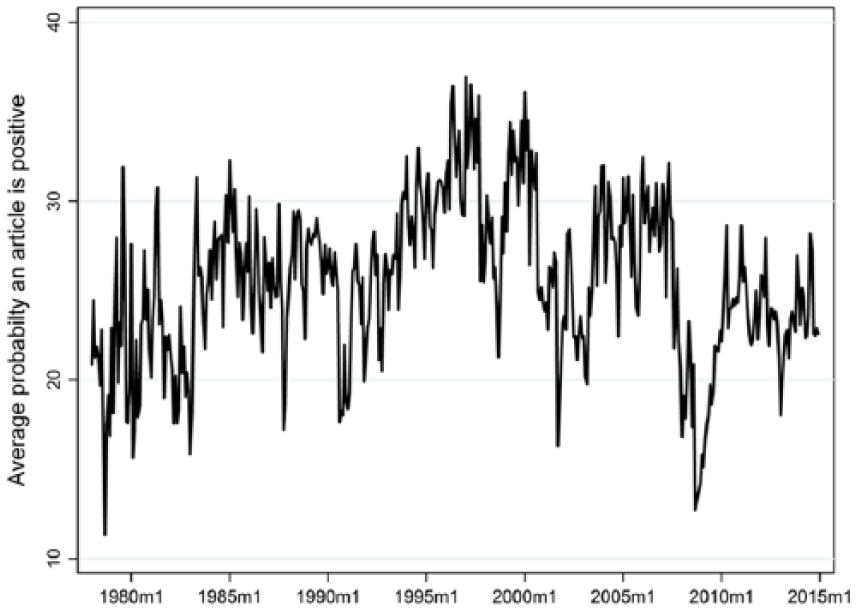

The measure of media tone is presented in Figure 1. The series has a mean of 27.5 percent positive and a standard deviation just under 4.4 percentage points over this time period. It ranges from approximately 13 percent positive to 37 percent positive, confirming the tendency for the media to focus on the negative (Soroka 2006). The series moves as we would expect given our knowledge of economic history. It is relatively low in the early 1980s and early 1990s, grows more positive over much of the Clinton years, and declines again in the early 2000s before rebounding and then bottoming out in the 2008 recession, after which it climbs slowly upward (but still remains consistently well below the long-run mean) to the end of the series. Notably, the series is fairly choppy. Given that the media is primed to cover new information, this is not surprising, but undoubtedly some of the noise is due to measurement error.

Tone of economic news coverage by month, 1980–2014.

Results

The first step in our effort to purge the effects of economic performance from both the tone of economic news coverage and perceptions of economic performance is to model each (tone and consumer sentiment) as a function of the set of economic indicators described above. To do so, we make two specification decisions. First, we omit lagged dependent variables from the models, which allow the economic variables to account for as much of the variation in these two variables as possible. 14 Second, we adopt a lag structure that includes contemporaneous lag 1 and lag 2 values of each variable in the set of economic indicators described above. 15 We employ this lag structure for two reasons. First, we are agnostic with respect to the correct lag structure but have theoretical reason to expect that any effects play out over time. This approach requires the inclusion of some number of lags. Second, most of our indicators are included in the model as growth rates measured with reference to the previous month, quarter, and year. We thus capture a variety of potential temporal effects, meaning that we need not include a large number of lags of any single one. These specification decisions mean that individual estimates from the model are inefficient and some coefficients may be incorrectly signed or statistically insignificant. They will, however, remain unbiased and asymptotically consistent. Given that our interest is not in ascertaining the precise nature of the influence of economic performance on consumer sentiment, but in allowing economic indicators to have their maximal influence on media tone and consumer sentiment, the potential inefficiency of the estimates is not of concern.

Table 1 reports the results. Block F-tests on each set of economic variables test for the joint significance of each set of variables. We present the p-values associated with the F-tests in Table 1 in the equation for ICS (column 1) and media tone (column 2). (See Online Appendix Table A1 for descriptive statistics.)

The Economic Causes of Consumer Sentiment (ICS) and Media Tone, January 1980 to April 2014.

Cell entries are block F-tests for the joint significance of excluding lags 0, 1, and 2 (and in the case on unemployment lag 12) from the saturated equation for ICS and Media Tone. The p-value represents the probability that the block of variables does not help explain Consumer Sentiment (column 1) or Media Tone (column 2). ICS = Index of Consumer Sentiment.

We find that variation in both consumer sentiment and media tone is significantly predicted by a broad array of economic indicators measured over a number of lags, confirming our expectations that both are influenced by economic performance. In particular, both equations account for a large proportion of the variance, nearly 85 percent of consumer sentiment and 68 percent of economic media tone, notably higher proportions than reported in previous studies based on less complete sets of economic indicators and lags. (And, recall that the models do not include lagged values of the dependent variables.) Both consumer sentiment and media tone follow economic fundamentals quite closely, as shown in Online Appendix Figures A1 and A2. Furthermore, with the exception of the lagging economic indicator index, each set of economic indicators accounts for significant variation in the ICS. Media tone, on the other hand, responds to all but real disposable income growth per capita (p = .379) and perhaps the number of jobs added (p = .088). That so many of the block F-tests show a significant influence on consumer sentiment suggests that previous studies containing fewer economic controls and with a less robust lag structure likely suffer from omitted variable bias.

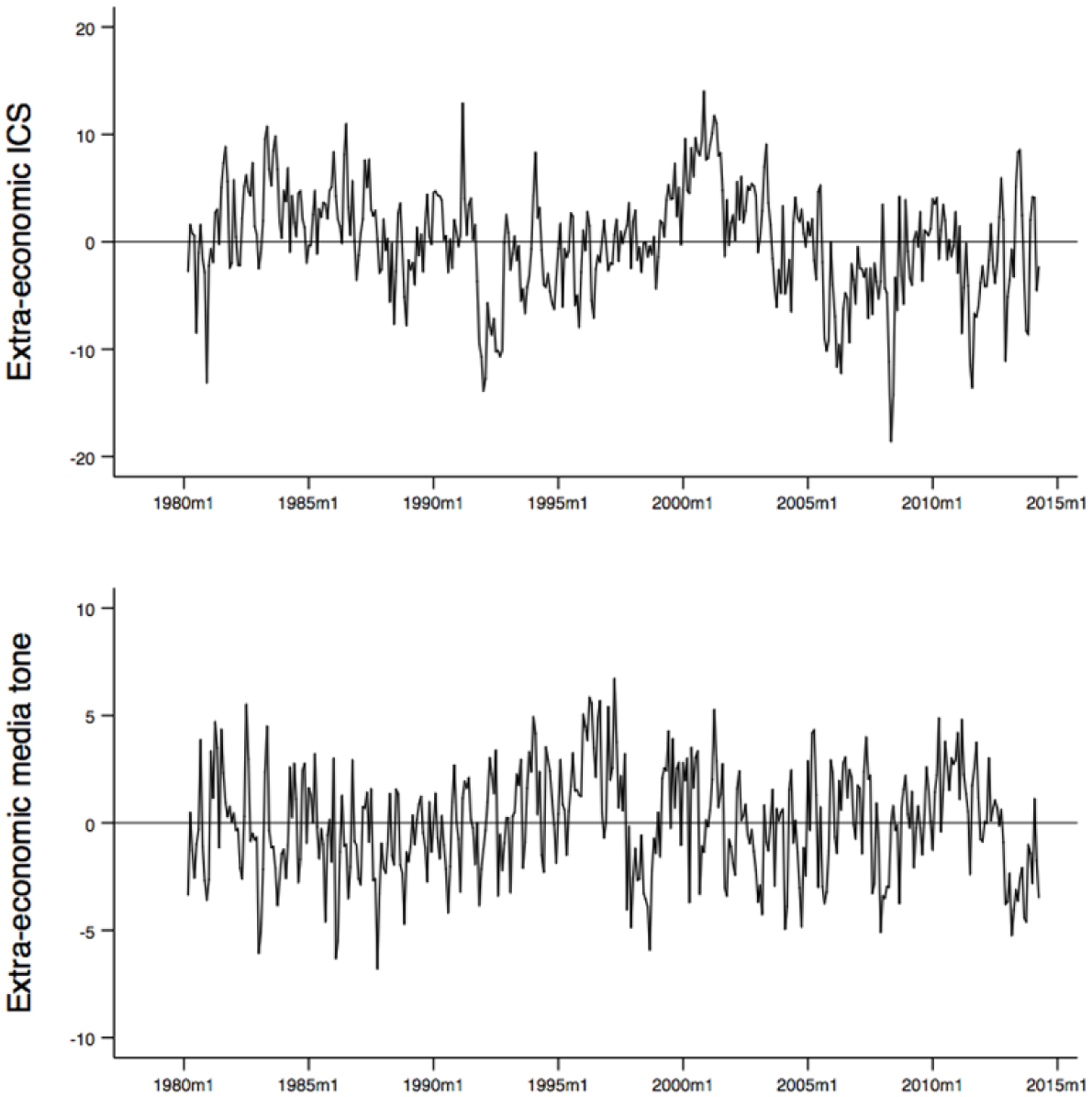

The residuals from these two models represent the variation in media tone and economic sentiment that remains unexplained by economic fundamentals and are shown in Figure 2. Two observations are readily apparent. First, even after controlling for a number of economic indicators, there appears to be systematic variation in both consumer sentiment and the tone of economic news coverage. For example, we see periods (early 1980s and 2000s) when consumer sentiment is overly optimistic (given economic performance as reported by the government) for extended periods of time and others when it is more negative than economic performance measures warrant (namely the early 1990s and from 2005 to the end of our analysis in December of 2014). Media tone appears to exhibit less systematic variation after accounting for economic performance, but it, too, is overly positive in the early 1980s, Clinton’s second term, and again from 2010 to 2012. It is overly negative during much of the 1980s and early 1990s (as then-President Bush suggested), and through the end of 2014.

“Extra-economic” consumer sentiment (ICS) and “extra-economic” tone of news coverage.

A second observation evident in the two series is that they often move together. For example, both trend upward following the 2008 recession up until 2012, and then both trend downward from 2012 to the end of the series. These results suggest the extra-economic portion of media tone may, in turn, influence exuberance or pessimism on the part of the public that is out of step with economic performance as the government can measure it. 16 We examine the evidence on this score next.

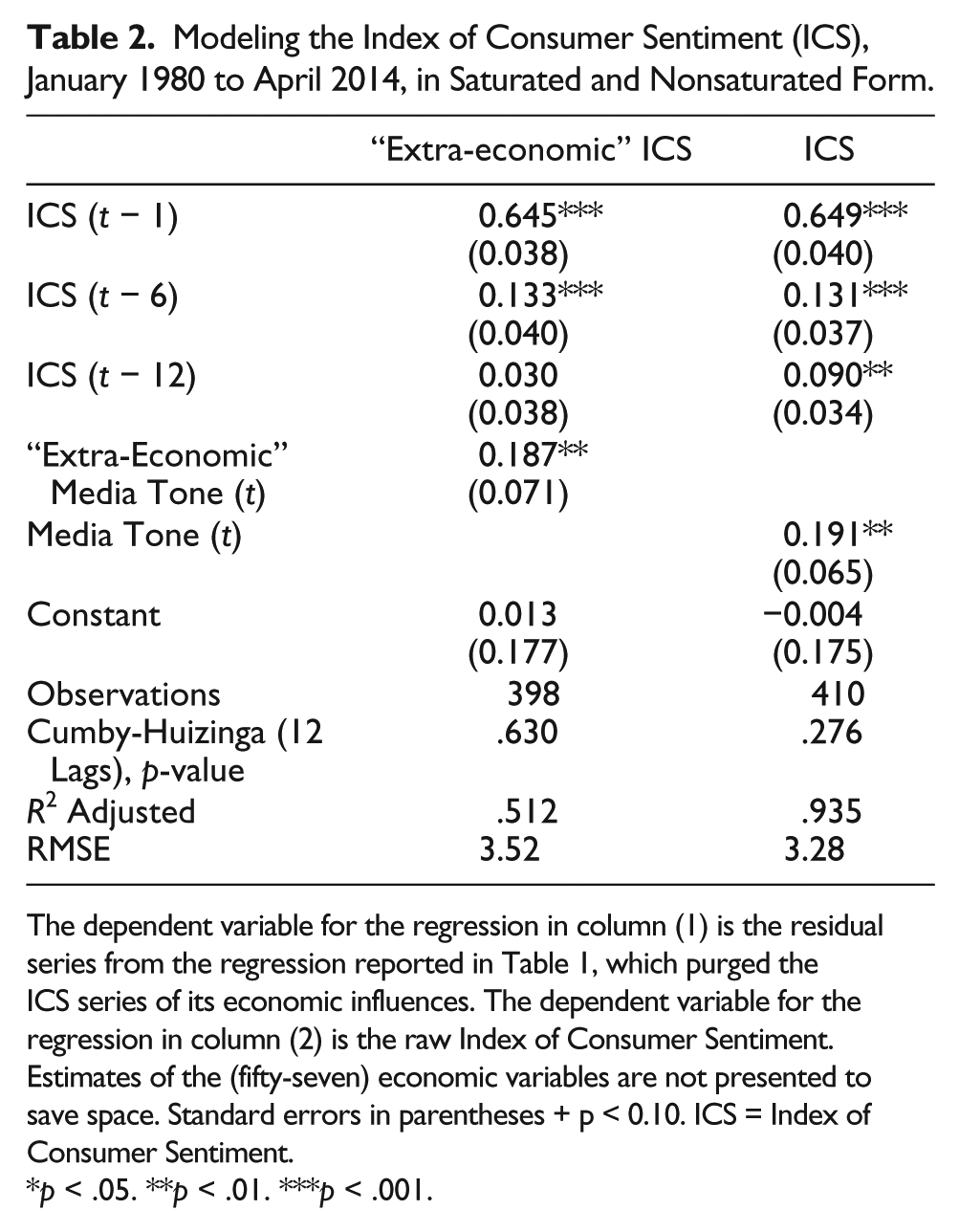

The first column of Table 2 displays the results from regressing extra-economic consumer sentiment (i.e., consumer sentiment purged of economic causes) on contemporaneous extra-economic media tone (i.e., media tone purged of economic causes), controlling for lagged values of purged consumer sentiment. The Cumby-Huizinga p-value indicates that the model is well behaved, with white noise residuals. The results suggest that extra-economic consumer sentiment is moderately persistent; current sentiment this month is a function of the previous month’s sentiment, even after controlling for economic indicators. We also see a semiannual and annual seasonality in purged sentiment, reflecting the intuition that sentiment depends on the month we are in. We are more (or less) optimistic in December than in January, for example, and sentiment this January (February, etc.) is related to the previous January (February, etc.). Overall, the model accounts for about 51 percent of the variation in purged sentiment. 17

Modeling the Index of Consumer Sentiment (ICS), January 1980 to April 2014, in Saturated and Nonsaturated Form.

The dependent variable for the regression in column (1) is the residual series from the regression reported in Table 1, which purged the ICS series of its economic influences. The dependent variable for the regression in column (2) is the raw Index of Consumer Sentiment. Estimates of the (fifty-seven) economic variables are not presented to save space. Standard errors in parentheses + p < 0.10. ICS = Index of Consumer Sentiment.

p < .05. **p < .01. ***p < .001.

Of particular interest is the estimated effect of extra-economic media tone on extra-economic consumer sentiment. The parameter estimate is moderate in size and highly significant (p < .01). When purged tone becomes 1 point more positive, consumer sentiment becomes more positive by 0.187 points in the short run. To estimate the long-run multiplier (De Boef and Keele 2008; Enders 2015), we divide the coefficient for purged tone by one minus the coefficients of the lags of purged sentiment (0.187 / (1 − (0.645 + 0.133 + 0.030)) = 0.97). Thus, the long-run multiplier of the same 1-point increase in purged tone is just less than 1 point. A standard deviation increase in extra-economic tone (2.5 points) leads to an expected increase in extra-economic sentiment of nearly 0.5 in the short term and roughly 2.5 points in the long run—approximately equal to half a standard deviation in purged sentiment. To determine whether these effects are large effects or small, consider that the purged consumer sentiment retains the same unit of measurement as the raw sentiment series. Thus, when we calculate that a standard deviation increase in extra-economic media tone yields roughly 2.5 points of long-run movement in extra-economic sentiment, this also means that the raw sentiment measure moves roughly 2.5 points. Given that the standard deviation of the raw sentiment measure is about 13 points, this effect appears as both large and politically meaningful. These results suggest consumer sentiment responds to media cues above and beyond the economic factors that drive them both.

As an alternative and nearly equivalent strategy, Table 2 also shows a single equation model of consumer sentiment (column two) where each of the economic indicators and each of the lags identified above are included on the right-hand side of the equation, along with our original media tone series and lagged values of the dependent variable to capture the inertia in consumer attitudes. The estimated effect of media tone using this single equation model is nearly identical (0.191 compared with 0.187 in the first model) to that using the multistage process.

Discussion

We have two central findings, each with important implications. First, the mass public’s collective economic attitudes appear to be tethered to economic reality to an extent greater than reported in previous research. The lion’s share of consumer sentiment is explained by economic fundamentals; recall that the saturated model accounted for 85 percent of the variance in the ICS. In other words, there is a high degree of correspondence between what people perceive and the economic reality that (normatively) should be producing it. Our finding in this regard stands in contrast to previous research. As noted by Achen and Bartels (2016), existing research typically reports more modest relationships between economic performance and economic attitudes, which implies that mass opinion about the economy is “subject to considerable vagaries” (Achen and Bartels 2016, 107). Instead, we have shown that economic attitudes are strongly related to what actual economic performance is. Likewise, the saturated model also accounted for a substantial amount of the variation in the tone of media coverage of the economy. That economic performance accounts for so much of the variance in economic media tone is reassuring to those who see the proper role of the media as providing information about the “true” state of the economy and to those concerned that consumer evaluations should reflect economic performance.

Second, we have provided evidence suggesting that economic attitudes may be caused by the portion of media coverage that deviates from economic performance, or what we have termed extra-economic media coverage. 18 Economic evaluations are not fully accounted for by economic performance. And when evaluations stray from the economic fundamentals, we can trace their movement to media coverage that is more or less positive than economic performance measures would predict.

The fact that extra-economic media tone is related to economic evaluations, even after taking into account a comprehensive range of economic indicators, may in some cases be the result of news outlets performing a public service by accurately conveying aspects of real economic conditions that the government’s measures simply fail to capture. In other cases, news outlets may be (unintentionally) leading the public astray, for example, by giving disproportionate attention to dips in the economy, especially when those dips can be described in sensational terms that will draw in readers. Thus, a key task for future research is an empirical assessment of the systematic causes of this extra-economic media coverage.

Whatever their sources, how and how much do extra-economic signals in the tone of media coverage matter? Empirically, our evidence suggests they can move consumer sentiment a substantial amount. But the significance of this effect also depends on the consequences of economic evaluations for economic and political outcomes. We speculate that a causal role for the tone of media coverage on economic evaluations above and beyond economic performance may be of concern for at least two reasons. First, any distortions in coverage (extra-economic media tone that does not capture economic reality) could lead voters to reward and punish candidates and incumbents not merely for how the economy actually performs but for perceptions of the economic performance that are non-economic in their origins. Second, there may be significant downstream consequences of that portion of extra-economic media tone that strays from economic realities for consumer behavior. If economic evaluations drive behavior in the marketplace, the consequences of that portion of economic media coverage that is extra-economic may lead to a mutually reinforcing cycle in which consumer behavior becomes detached from economic reality. For instance, if economic attitudes become overly pessimistic, consumer spending may drop, economic performance may weaken, news coverage may become more negative, and consumers may become still more pessimistic. This sequence of events—coupled with a negativity bias in the news—could make it much harder for the economy to recover from recessions and more prone to them in the first place. Clearly, significant normative and political implications hang in the balance.

Supplemental Material

Appendix_online_supp – Supplemental material for Assessing the Relationship between Economic News Coverage and Mass Economic Attitudes

Supplemental material, Appendix_online_supp for Assessing the Relationship between Economic News Coverage and Mass Economic Attitudes by Amber E. Boydstun, Benjamin Highton, and Suzanna Linn in Political Research Quarterly

Footnotes

Acknowledgements

We thank Jamie Monogan, Markus Prior, and Walt Stone for helpful comments on previous drafts. We are also immensely grateful to Pablo Barberá, Ryan McMahon, Jonathan Nagler, Stuart Soroka, Dominik Stecula, and Christopher Wlezien for their general support and insights on the relationship between economic conditions, media coverage, and mass attitudes.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.