Abstract

Financial well-being—the evaluation of current personal finances and expectations for the financial future—has gained attention in research, practice, and policy. Yet, there is no consensus on its conceptualization or its operationalization. The authors contribute to this area of research by proposing a conceptual framework and reassessing a measure used in data on subjective financial well-being from 16 countries. The findings highlight methodological concerns in international marketing studies and show not only financial well-being but also its measures to be context dependent. Furthermore, although many studies use unidimensional financial well-being measures, some conceptualizations have at least two components: a current and a future element. The authors analyze the effects of individual and contextual factors on current and future financial well-being and explore their possible interaction. They observe income to be a significant predictor of both components of financial well-being, while institutional settings are correlated with current financial well-being and national culture with future financial well-being. They conclude that initiatives aimed at increasing financial well-being need to clearly target either its current or its future component as their antecedents differ.

Keywords

Financial well-being—the evaluation of current personal finances and expectations for the financial future—has a significant role in our lives. Yet, there is no consensus on what financial well-being means and how it should be measured. Some researchers consider it to be an objective measure (Greninger et al. 1996), perhaps even a synonym for wealth. Others argue that it is a subjective measure (Strömbäck et al. 2017), the perceived ability to maintain current living standards and to reach a desired lifestyle in the future (Brüggen et al. 2017). The third school of thought takes a medial position, suggesting a combination of both objective and subjective measures for assessing financial well-being (Kempson, Finney, and Poppe 2017; Organisation for Economic Co-operation and Development [OECD] 2019).

In recent years, several conceptualizations and frameworks of financial well-being have been developed (Brüggen et al. 2017; Kempson and Poppe 2018; Netemeyer et al. 2018). In addition, a multitude of similar constructs (e.g., financial health, financial wellness, financial resilience, financial vulnerability) have been designed and tested. The development of a wide range of closely related constructs is not helpful for developing a universal understanding of financial well-being, for making valid international comparisons, or for deepening the knowledge of its antecedents.

Most studies use a unidimensional financial well-being score when studying its antecedents and outcomes (Barrafrem, Västfjäll, and Tinghög 2020b; Lee, Lee, and Kim 2020), although some studies indicate that financial well-being has several components (Netemeyer et al. 2018; Salignac et al. 2020). This approach does not enable sufficient analysis of the factors affecting each of the components. Furthermore, the focus has been so far mostly on individual factors, such as socioeconomic status, personality traits, or financial knowledge (Barrafrem, Västfjäll, and Tinghög 2020b; Comolli, Bernardi, and Voorpostel 2021; García-Mata, Zerón-Félix, and Briano 2022; Lind et al. 2020), without deeper analysis of the contextual factors or of the interaction between individual and contextual factors affecting the components of financial well-being.

In this study, we make five contributions to the international marketing and financial well-being literature. First, we extend the literature on conceptualization and operationalization of financial well-being by developing its conceptual framework. Second, we reassess an existing financial well-being measure and show its weaknesses for international consumer research. Third, we analyze and compare the current and future components of financial well-being in 16 countries around the world because the majority of financial well-being studies have been conducted in the context of single countries or using single financial well-being scores. Fourth, we shed light on the links between the two components of financial well-being, on the one hand, and individual, institutional, and cultural factors, on the other. We also explore the interaction between individual and contextual factors and their effects on the components of financial well-being. Fifth, we highlight that the marketing and educational initiatives aimed at increasing financial well-being need to explicitly target either reducing current money management stress (CMMS) or improving expected future financial security (EFFS). As the antecedents of these two components of financial well-being differ, the design of interventions also needs to differ in order to have a significant effect on either of them.

Theoretical Background

What Is Financial Well-Being?

As noted in the introduction, there is no common agreement on what the term “financial well-being” stands for and how it should be measured. Our first aim is to contribute to that definition by developing a conceptual model of financial well-being. We adhere to the subjective approach to financial well-being and distinguish its two components: evaluation of current personal finances and expectations for the financial future.

Objective or subjective financial well-being?

The supporters of objective measures use mainly ratios and indexes for evaluating financial well-being. For example, Greninger et al. (1996) suggest the use of ratios in the areas of liquidity, savings, asset allocation, inflation protection, tax burden, housing expenses, and credit. These figures are clearly comparable, yet they may not sufficiently reflect personal situations. As a result, in recent years, subjective or combined measures have gained more support. Some of the definitions are given as examples in Table 1.

Selected Definitions of Subjective Financial Well-Being.

Often, financial well-being is confused with financial behaviors and capabilities. For example, indicators of financial health in the United States are “spending less than income” and “paying bills on time” (Financial Health Network 2019). These are prudent behaviors that lead to improved financial well-being but are not financial well-being as such. We consider financial well-being to be an evaluation of current personal finances and an expectation for the financial future, that is, the perceived ability to keep one’s current lifestyle and to reach or maintain the desired living standard in the future. Financial well-being is not a particular behavior or set of behaviors, although these constructs do correlate.

Another common misinterpretation is considering financial well-being as a synonym for wealth, an objective figure. Although income and assets do affect financial well-being and the size of assets can increase financial security, financial well-being involves more than wealth alone. We agree with Brüggen et al. (2017, p. 230), who state that “individuals may experience high or low financial well-being regardless of their objective financial position.” Therefore, we recommend measuring subjective financial well-being.

As with any conceptualization in the social sciences, the assessment of subjective financial well-being has both advantages and limitations. The main benefit is the reflection of individual perceptions and context (e.g., social norms, income inequality) that objective ratios miss. It also reflects the values and lifestyle choices of individuals. Materialistic values decrease the perception of financial well-being (Garðarsdóttir and Dittmar 2012); the inverse can be true as well, as the rise of minimalism and postmaterialism may make such objective measures meaningless for assessing financial well-being. If one prioritizes self-expression or ecological sustainability over economic security, measuring current assets will not gauge the satisfaction with living standards. Without understanding individual values, the interpretation of objective ratios is insufficient. Furthermore, in the world of the gig economy (Constantino 2018) and blended families, an objective assessment of household income is already a challenge in itself. Thus, these developments pose challenges in the assessment of objective financial well-being.

The main disadvantages of the subjective approach are that the assessment can be influenced by the timing of the measurement (e.g., less money management stress right after a payday, more stress a few days before a payday) and that it can be manipulated (e.g., populists declaring the retirement system to be utterly flawed).

Terminological creativity and confusion

Although many authors have done extensive reviews of existing analyses and suggested their own conceptualizations of financial well-being, the terminological discussion has not yet reached a consensus. Furthermore, several terms are used for studying similar concepts. For example, “financial health” is defined as “a state in which an individual can meet current needs, absorb financial shocks, and pursue financial goals” (Singh et al. 2021, p. 14). That is rather similar to financial well-being. In fact, these two terms are starting to be used as synonyms (UNSGSA 2021, p. 4): “Financial health or wellbeing is the extent to which a person or family can smoothly manage their current financial obligations and have confidence in their financial future.” Abrantes-Braga and Veludo-de-Oliveira (2019, p. 1028) propose an assessment of “financial preparedness for emergency,” which they define as “an individual's state of being financially prepared to cope with a financial shock that could prevent him/her to conduct their regular activities.” De Bruijn and Antonides (2020) analyze “financial worry” and “rumination,” defining “financial worry as repeated and negative thinking about the uncertainty of one's (future) financial situation while financial rumination refers to repetitive, passive, and pessimistic thinking about the possible causes and consequences of one's financial concerns.” O’Connor et al. (2019, p. 422) study “financial vulnerability,” which they define as “the likelihood that an individual will experience financial hardship.” This is similar to the “financial preparedness” concept of Abrantes-Braga and Veludo-de-Oliveira (2019).

Other related terms are “financial wellness,” “financial satisfaction,” “financial resilience,” and “financial comfort” (Nibud 2018; OECD 2019; Schmidtke et al. 2020; Sorgente and Lanz 2017). Some even go as far as diagnosing “financial illnesses”—low financial security and high financial anxiety (Helander 2020). In our understanding, all these concepts evaluate some aspect of financial well-being from different angles and with varying scope. Comparisons of these findings mean the comparison of dissimilar things, although many authors do that without warning of the different conceptualizations.

Unidimensional measure or a construct with several components?

Scholars also differ in how they operationalize these concepts. Some use ten or more items (e.g., Barrafrem, Västfjäll, and Tinghög 2020b; Kempson and Poppe 2018; Netemeyer et al. 2018; Strömbäck et al. 2020), whereas others apply shorter measures. For example, Xiao and Porto (2017) ask respondents to rate, on a one-item scale, how satisfied they are with their finances. Ruggeri et al. (2020) stress the advantages of using multidimensional measurements of well-being components and warn of the deficiencies that single-item instruments have.

Some analyze two components of financial well-being separately; others use a single score. Netemeyer et al. (2018) distinguish two components of financial well-being: current money management stress (CMMS) and expected future financial security (EFFS). They explain that CMMS encompasses “feelings of being stressed/worried about one's current financial situation, and being unable to manage money effectively today to meet financial obligations and to live the life one wants to live,” whereas EFFS includes “perceptions of having a financially secure future and meeting future financial goals” (Netemeyer et al. 2018, p. 71).

Others calculate a single financial well-being score (e.g., Barrafrem, Västfjäll, and Tinghög 2020b; Strömbäck et al. 2020), but we see the two-component approach as more informative. It is possible that one has high money management stress/financial anxiety in the present but also perceives a financially secure future. In such a case, the sum (the financial well-being score) would be similar to that of people who rate both constructs to be around the average. Looking at the two components separately allows to analyze a greater variety of perceptions of both parts of financial well-being. Therefore, we analyze subjective financial well-being—the evaluation of current personal finances and expectations for financial future—and assess its current and future components (CMMS and EFFS) within and across 16 countries.

The Netemeyer et al. (2018) CMMS and EFFS statements have so far been validated in single countries (the United States and Brazil; Netemeyer et al. 2018; Ponchio, Cordeiro, and Gonçalves 2019); our study is the first to assess them in international data. Our second research objective is to assess whether CMMS and EFFS are valid measures for comparing financial well-being across countries.

Antecedents and Outcomes of Financial Well-Being

Financial well-being has an effect on mental health, life satisfaction, social relations, and overall well-being (Brüggen et al. 2017; Netemeyer et al. 2018; Shim et al. 2009). Therefore, its importance goes far beyond financial matters. The vast majority of research studies examine the effects of various factors on a single financial well-being score as the dependent variable, even if they distinguish several components of financial well-being in their definition of it. In addition, the latest reviews of the financial well-being literature summarize the effects of various indicators on a unidimensional financial well-being construct, without distinguishing its components (Kaur, Singh, and Singh 2021; Nanda and Banerjee 2021; Warmath 2021; Wilmarth 2021). Very few papers use the components of financial well-being as separate dependent variables and analyze their antecedents (Netemeyer et al. 2018; Ponchio, Cordeiro, and Gonçalves 2019). Thus little is known about whether and how the effects of individual and contextual factors differ across the components of financial well-being, especially across several countries.

Fu (2020) compared financial well-being in emerging and developed economies. Apart from individual differences in socioeconomic factors, structural and institutional differences (such as information, choice among providers, and semiformal borrowing) explain the levels of financial well-being in their study. However, they did not assess the two parts of financial well-being that are the focus of this paper. Instead, they used a composite financial well-being score that they calculated on the basis of ten questions from the OECD adult financial literacy competencies survey (Fu 2020; OECD 2016). These questions were designed to assess financial literacy, not financial well-being, although some of the statements overlap.

Salignac et al. (2020, p. 1585) emphasize the role of life stages and structural conditions “such as global financial markets, the national economy, government policy, labour markets, social inequalities, community services, social relationships and family dynamics” in financial well-being. Barrafrem, Västfjäll, and Tinghög (2020b) showed that contextual factors have a significant influence on financial well-being by analyzing the “better-than- average effect” in the United Kingdom and Sweden related to the COVID-19 crisis.

In the current study, we build on the two financial well-being components developed by Netemeyer et al. (2018). They showed that the drivers of the first component, CMMS, are late payments, materialism, and lack of self-control. For the second component, EFFS, they found the drivers to be perceived financial self-efficacy, positive financial behaviors, willingness to take investment risks, and planning for the long term. Both of these components influence overall well-being, but when they are included in the analysis simultaneously, the effect of CMMS on well-being is mediated by income. Netemeyer et al. (2018) conclude that it is only for low-income groups that CMMS has an impact on overall well-being. However, their findings are based on data from the United States and Amazon Mechanical Turk (MTurk) alone. Ponchio, Cordeiro, and Gonçalves (2019) used the same CMMS and EFFS measures to analyze the effects of personal factors on subjective financial well-being in data from Brazil and found CMMS and EFFS to be predicted by consumer spending self-control, materialism, and time perspective.

Neither of these studies focused on the effects of socioeconomic factors on these two components. Instead, the first study included income as a mediator between CMMS and well-being; the latter study used age, gender, education, and income as control variables. The relation of these socioeconomic variables with a unidimensional financial well-being score has been studied the most, but with data from single countries. In the current study, we focus on the effects of age, gender, education, and income on CMMS and EFFS in data from 16 countries. One might assume that in data collected using the same methodology, age, gender, income, and education would have similar relations to both components of financial well-being in all countries; only the effect sizes and their significance may differ. Thus, our third objective is to analyze that assumption in our data, and we formulate the first hypothesis:

Financial well-being seems to increase with age (Collins and Urban 2020; Kaur, Singh, and Singh 2021) and seems to be higher in older cohorts (De Bruijn and Antonides 2020; Fu 2020), but it may have a U-shaped relationship with lower financial well-being in middle age groups (Riitsalu and Murakas 2019; Xiao and Porto 2017). In Mexico, older individuals have lower financial well-being (García-Mata, Zerón-Félix, and Briano 2022). However, not all studies find a significant relation between age and financial well-being (Strömbäck et al. 2020). Note that these analyses use a single financial well-being score. These findings suggest that CMMS might decrease and EFFS increase with age. We study this assumption and formulate the following hypotheses:

The relation between gender and financial well-being seems to be more complicated. Some researchers find men to have higher financial well-being (Fu 2020; Lind et al. 2020; Riitsalu and Murakas 2019; Strömbäck et al. 2020); others find the relation between gender and financial well-being to be insignificant (de Bruijn and Antonides 2020). A recent literature review focusing on the gender differences in financial well-being (Gonçalves, Ponchio, and Basílio 2021, p. 839) finds women to have “reduced financial well-being” due to several disadvantages, such as lower financial knowledge, the gender pay gap, and primary caregiver status. In addition, women’s financial well-being depends more on family and work trajectories than men’s (Comolli, Bernardi, and Voorpostel 2021). Therefore, we hypothesize that women have higher CMMS and lower EFFS:

The only factor most researchers find to be significantly and positively correlated with financial well-being is income (Collins and Urban 2020; Fu 2020; Kaur, Singh, and Singh 2021; Kempson 2018). Netemeyer et al. (2018) showed in data from the United States that higher-income groups have significantly lower CMMS and higher EFFS. We study whether a similar relation exists in all 16 countries and formulate these hypotheses:

Higher-education groups have been found to have higher financial well-being in some studies (Fu 2020; Riitsalu and Murakas 2019), but not all studies find a significant correlation between education and financial well-being (De Bruijn and Antonides 2020; Lind et al. 2020). It appears that education is a significant antecedent of financial well-being in less developed countries, such as India (Chatterjee, Kumar, and Dayma 2019) and Mexico (García-Mata, Zerón-Félix, and Briano 2022). To explore the relation between education level and the two components of financial well-being in 16 countries, we formulate the following hypotheses:

Contextual Factors: National Culture and Institutional Setting

Our fourth objective is to explore the relationship between national culture, institutional setting, and the two components of financial well-being across countries.

The perception of financial well-being is affected by contextual factors (Barrafrem, Västfjäll, and Tinghög 2020b; Brüggen et al. 2017), including culture. Consumer culture and its globalization (or localization) have been in the focus of international marketing research (Solberg 2018; Steenkamp 2019; Steenkamp and de Jong 2010). Individuals may no longer be comparing themselves to their neighbors (“keeping up with the Joneses”) but aspire to reach the living standard of someone on the other side of the globe. Furthermore, the younger generation may have more in common with the same generation in another country than with the older generation in their home country, a phenomenon that has been called the rise of the “global consumer” (Solberg 2018, p. 48). We investigate the effects of contextual factors by measuring the two components of financial well-being and comparing both across age groups and countries.

Global consumer culture promotes immediate gratification rather than prudent long-term behavior. Humans tend to be present-biased and prefer well-being today over an abstract and intangible or even unimaginable well-being in the distant future (Barrafrem, Västfjäll, and Tinghög 2020a; Greenberg and Hershfield 2019). Pressure from peers and marketers can tempt individuals to sacrifice the well-being of the future self for the status of the present self (Hershfield et al. 2009). However, the rise of sustainable consumption may have positive effects in the context of financial well-being as well. Once the pressure to have the newest smartphone or wear the latest fashion is eased by the rise of reusing and consuming for longer, consumers can start saving (more) for securing their financial future. In that context, the global consumer culture can shift from prioritizing immediate gratification to promoting sustainable choices for well-being in the future. In addition, the rise of the FIRE (financial independence, retire early) movement promotes frugality, avoiding debt, and investing for the future (Taylor and Davies 2021).

Several approaches to operationalizing national culture are available. Probably the best known (but also most criticized; Shenkar 2001) are the Hofstede cultural dimensions: individualism, power distance, uncertainty avoidance, masculinity, long-term orientation, and indulgence (Hofstede Insights 2020). In individualistic cultures, individuals prioritize their own well-being, whereas in collectivistic cultures the focus is on harmony in the family and community. Power distance stands for “the extent to which less powerful members of a society accept and expect that power is distributed unequally” (De Mooij and Hofstede 2011, p. 182). Uncertainty avoidance reflects ambiguity tolerance: cultures that have high levels of uncertainty avoidance prefer more formal rules and structure. Masculine cultures are oriented toward success and achievement, and feminine cultures value caring and quality of life (De Mooij and Hofstede 2011). Long-term orientation refers to the extent to which long-term goals and well-being are prioritized over the past and present, and invested for. Indulgence indicates the preference for well-being in the present rather than controlling “human desires related to enjoying life” (Hofstede 2011).

One might assume that consumers from more individualistic, masculine, and long-term-oriented cultures have higher level of financial well-being, or at least are more concerned about their financial future. In more collectivistic and feminine countries, people can rely more on support from family and peers; therefore, they do not need to prioritize individual financial well-being as much. Similarly, in cultures that score lower on long-term orientation and higher in indulgence, securing one’s financial future might gain less attention. However, to date, there is no empirical evidence of the correlation between the Hofstede cultural dimensions and perceived financial well-being components in international data. Instead, Nanda and Banerjee (2021, p. 762) call for future financial well-being research to study “the cross-cultural differences using Hofstede's cultural dimensions.” To contribute to that, we study the relation between the Hofstede dimensions and the two components of financial well-being and formulate the following hypotheses:

The alternative approach is to use Inglehart's values (traditional vs. secular-rational, survival vs. self-expression) operationalized in the World Values Survey. Steenkamp (2019, p. 11) finds these to be the most reliable in international marketing research: “Inglehart's framework is most useful for cultural attitudes at the country level, from both a conceptual and a statistical perspective.” We also look at the possible relation between this framework and financial well-being.

Besides cultural context, institutional setting influences financial well-being (Brüggen et al. 2017; Gonçalves, Ponchio, and Basílio 2021; Nanda and Banerjee 2021). Studies have shown that trust in government increases financial well-being (Barrafrem, Tinghög, and Västfjäll 2021) and that universally accessible formal financial services (high financial inclusion) have a positive effect on financial well-being (Nandru, Chendragiri, and Velayutham 2021). However, these studies have used a single financial well-being score. We contribute to this discussion by studying the relation between institutional setting and the two components of financial well-being. We assume that in a favorable institutional setting—high financial inclusion, low income inequality, and high trust in government—CMMS is lower and EFFS is higher. However, as we have data from 16 countries and for a few of them no reliable comparable macro-level data are available, we cannot analyze the directions of these relations sufficiently. Yet, we formulate the last two hypotheses:

Conceptual Model

From the findings discussed previously, we propose a conceptual model of financial well-being (Figure 1). We highlight the broad scope of factors influencing and influenced by financial well-being. However, we do not test the full scope in the current study. Instead, we focus on a few of the factors in data from 16 countries. On individual level, we look at the effects of socioeconomic status, operationalized by age, gender, income, and education variables (H2a–H5b). On contextual level, we analyze the correlation of financial well-being with indicators of national culture (Hofstede dimensions; H6a and H6b) and institutional setting (financial inclusion, income inequality, and trust in government; H7a and H7b).

Conceptual model of the antecedents and outcomes of financial well-being.

The constructs that have been found to influence financial well-being in previous research but are not included in the empirical analysis in the current study are personality, life stages and changes, attitudes and values, and financial competence. We use “financial competence” to avoid the terminological confusion of defining “financial literacy” and “financial capability” (Riitsalu and Põder 2016) and to be more in line with the recent developments in policy that prioritize financial competence (European Commission 2021). In our understanding, financial competence includes financial knowledge and skills, attitudes and behaviors, motivation, and confidence needed for increasing financial well-being (Aarna, Riitsalu, and Venesaar 2021).

The lack of motivation to manage personal finances relates to financial ignorance (Barrafrem, Västfjäll, and Tinghög 2020a). Financial knowledge and skills do not necessarily make one make plans for securing the financial future. Financial decisions may be perceived as overly complicated, tedious, and boring—things to be avoided or postponed (Ariely and Kreisler 2017; Greenberg and Hershfield 2019; Sunstein 2014). Barrafrem, Västfjäll, and Tinghög (2020a, p. 16) wittily label this behavior as “Financial Homo Ignorans,” or “tendencies to ignore relevant aspects of decision-making.” Instead of finding motivation to make informed and considered financial choices, it may simply be more tempting to ignore the need. Unfortunately, this ignorance has negative consequences for financial well-being, as recently evidenced by Barrafrem, Västfjäll, and Tinghög (2020a, b).

Financial well-being has been found to affect subjective well-being, including mental health, life satisfaction, and relationship quality (Brüggen et al. 2017; Netemeyer et al. 2018; Shim et al. 2009). We include these outcomes in our conceptual model to illustrate them but do not test these relations in the current study.

Methodology

Survey Description and Sample

On our request, the measurements of CMMS and EFFS were added into the ING International Survey on savings. This online survey is carried out for ING Bank every year. The data for our study were collected by the market research agency Ipsos in autumn 2019. The questionnaire was translated into local languages by Ipsos under the supervision of experts from local ING branches.

Respondents from 16 countries were asked to choose a response ranging from 1 = “Does not describe me at all” to 5 = “Describes me completely” to the following statements (Netemeyer et al. 2018):

1. Because of my money situation, I feel I will never have the things I want in life. 2. I am behind with my finances. 3. My finances control my life. 4. Whenever I feel in control of my finances, something happens that sets me back. 5. I am unable to enjoy life because I obsess too much about money.

1. I am becoming financially secure. 4. I am securing my financial future. 2. I will achieve the financial goals that I have set for myself. 3. I have saved (or will be able to save) enough money to last me to the end of my life. 4. I will be financially secure until the end of my life.

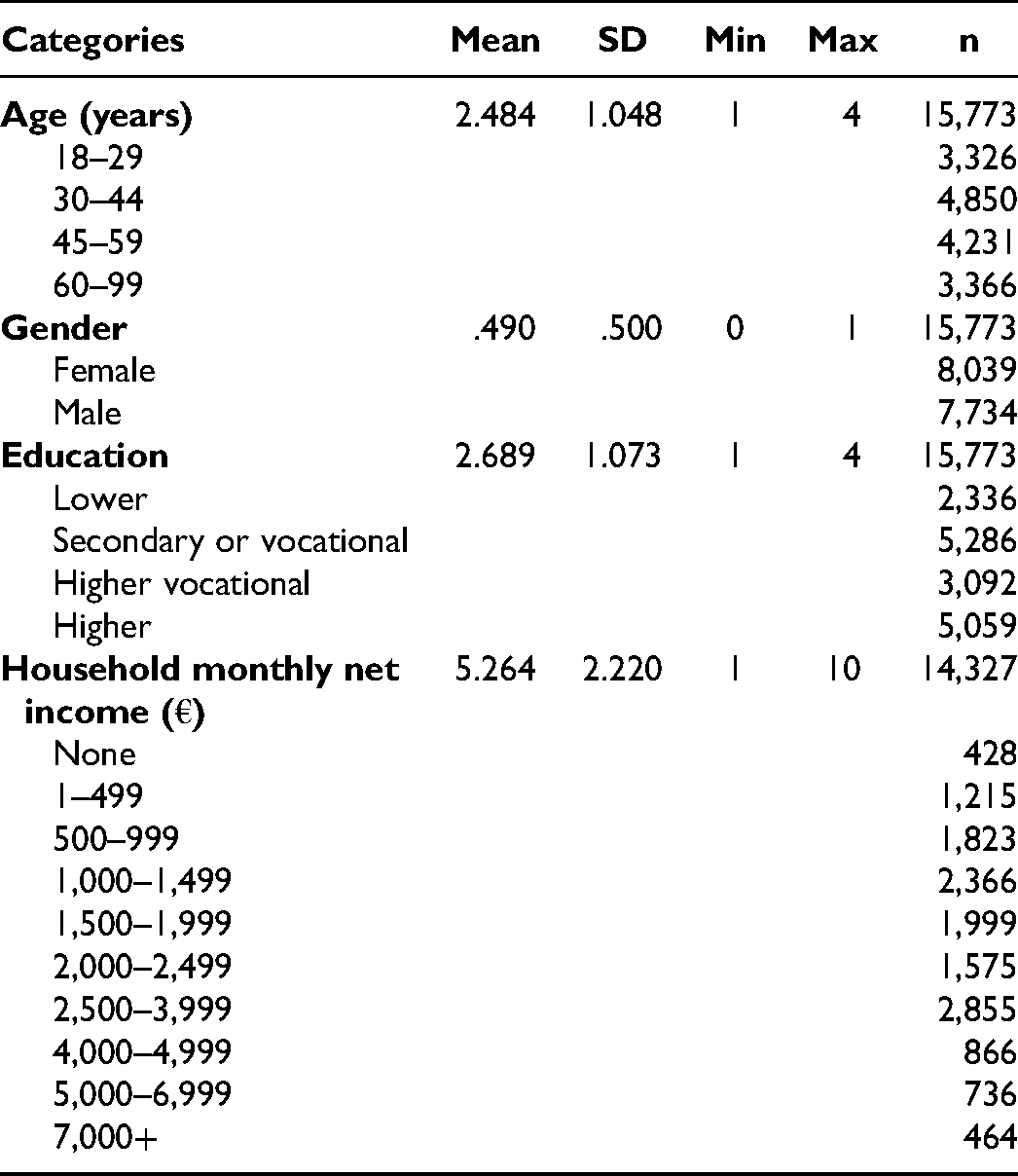

The sample included 15,773 individuals aged 18–99 years (M = 44.67 years, SD = 15.93), 51% female and 49% male. No observations were lost for either of the constructs. The sample size and mean age for each of the countries can be found in Appendix A, and the socioeconomic background of the full sample is presented in Table 2.

Summary Statistics of the Full Sample.

In three of the countries—Romania, the Philippines, and Turkey—the sample is representative of the online population. Ipsos added a quota for education and working status in Turkey and for education in Romania. In the Philippines, the sample is representative for the online population, gender, and age within the group 18–45 years. Therefore, data from these three countries must be interpreted as valid for the online population and not for the entire population. In the other 13 countries, the sample is representative of the population based on age, gender, and region.

Reliability of the Scales

First, we calculated Cronbach’s alpha as a reliability measure of the constructs. We found evidence of good reliability in measuring both components of financial well-being (CMMS α = .87, EFFS α = .90).

Next, we conducted principal component analysis (PCA; rotated factor loadings, principal component method, varimax) to test if the scales measure the two components (CMMS and EFFS) of financial well-being in all 16 countries. We see that a second component of EFFS was observed in Austria and Germany (see Appendix B, Table B1). Presumably, the translation into German added an extra meaning to the EFFS scales. In all other countries, no such problems occurred.

Measurement Invariance

International marketing studies need to be wary of common method variance (CMV; Baumgartner and Weijters 2021). When using a measure developed and tested in one country (in our case, the CMMS and EFFS scales in the United States) for assessing and comparing a consumer research issue across countries, the main methodological concern is whether these constructs are cross-nationally invariant (Steenkamp and Baumgartner 1998). That is, do we measure and compare the same constructs, despite the possible differences in samples, translations, and response styles? In the worst-case scenario, we could be comparing mean scores mistakenly if there were systematic biases in the way individuals respond in some or many of the countries. Baumgartner and Steenkamp (2001, p. 143) found “systematic effects of response styles on scale scores” using representative samples from 11 European Union countries. Response styles such as always choosing the middle point or responding in a socially desirable way may reduce the validity of the findings. To avoid such biases and contamination of data, we assess the measurement invariance of both CMMS and EFFS using multisample structural equation modeling (SEM; Baumgartner and Weijters 2021; Steenkamp and Baumgartner 2000).

Ideally, potential method effects could be assessed before the international study is conducted. In most cases, however, these threats to the validity of the findings need to be diagnosed after the collection of the data and before the results are reported, which is also the case in our study. Because we could add only a limited number of questions into the ING savings survey, we could not add items such as the social desirability scale (Steenkamp, De Jong, and Baumgartner 2010) to assess the method effects. However, we did use balanced scales, randomization of the order of statements, and placement of the financial well-being items in the beginning of the survey to avoid the effects of respondent fatigue in the selection of options. Furthermore, the CMMS statements were worded in the negative and EFFS statements in the positive frame, meaning that a higher rating in the first meant a negative rating in the second—a positive assessment. Thus, one could not just mindlessly click the same response through all ten statements.

However, we do need to control for method effects post hoc (Baumgartner and Weijters 2021). One way would be to choose items from the survey that are not related to financial well-being and analyze the response to them in comparison with the responses to CMMS and EFFS scales to diagnose the possible response styles. Unfortunately, all questions in the ING survey are in one way or another related to financial well-being or financial situation and behavior in a broader sense. Therefore, we follow the methodological guidelines for international marketing research by Baumgartner and Weijters (2021) and start, as they suggest, by calculating the multisample structural equation models with no invariance constraints imposed across countries, that is, without considering method effects. Measurement models showed the five-statement latent variables to have a poor fit. Because SEM revealed large covariances between a few of the statements, we decided to use four observed variables instead of the original five for both latent variables. The path diagrams of the baseline models are presented in Figure 2. These models have a better fit, as Table 3 shows.

Path diagrams of the two latent variables in the full sample.

Measurement Models with No Invariance Constraints in the Full Sample (n = 15,773).

Notes: In these models, the first item is fixed to 1 and the mean of the latent variable is set to 0.

Next, we conducted multisample SEM to assess the group-level goodness of fit of the measurement models with four statements in each of the countries (see Appendix C, Tables C1 and C2). We found varying fit for both measurement models. Especially troublesome was the fit of the EFFS model in Austria and Germany, as already indicated by the PCA results. However, we decided not to exclude these countries from our analysis.

As our intention was to compare the mean scores across countries, we needed to assess scalar invariance (Steenkamp and Baumgartner 1998). To do this, we calculated models with inferred response scale factors as suggested by Baumgartner and Weijters (2021). We estimated the 16-group structural equation models for both latent variables separately (Models 1–3 for CMMS, Models 4–6 for EFFS). In all of these models, we fixed the first item to 1 and set the mean of the latent variable to 0. The goodness-of-fit statistics are presented in Table 4.

Measurement Models in the Multisample SEM Analysis.

An acceptable fit would be if the comparative fit index (CFI) and the Tucker–Lewis index (TLI) are less than .95, the root mean square error of approximation (RMSEA) is less than .06, and the standardized root mean square residual (SRMR) is less than .08 (Baumgartner and Weijters 2021). Only Model 1 meets these criteria, as none of the other models shows acceptable fit. The changes in TLI and CFI should not exceed .01, and the change in RMSEA should be less than or equal to .015 (Cheung and Rensvold 2002), which does not hold in our results. Thus the models do not support measurement invariance, either metric or scalar.

Cleveland, Laroche, and Papadopoulos (2009) say in their eight-country study that measurement invariance is something to aspire to but cannot fully be met in large multisample international studies. In our case, the 16 countries with a total of 15,773 respondents make it even harder to achieve. Yet, we must refrain from comparing the mean financial well-being scores across countries. Although we calculated Cronbach’s alpha and conducted PCA to test the reliability of the scales, multisample structural equation models across countries revealed the weaknesses of the financial well-being measure. This is a clear illustration of the arguments of Baumgartner and Weijters (2021), who warn of the methodological problems with conducting international comparisons in consumer studies.

Individual and Contextual Indicators

As explained previously, the four individual factors we decided to focus on in this research were age, gender, income, and education. The first was a binary variable (1 = male, 0 = female); the remaining three were categorical variables. We calculated structural equation models to study the effects of these on the two components of financial well-being both in the full sample and in each country’s data (H1–H5). In these, the latent constructs were CMMS and EFFS.

We used cultural and institutional factors as contextual indicators; see Appendix D, Table D1, for the details. To select the cultural indicators to be used in the models, we first ran linear regressions with all six Hofstede dimensions and three Inglehart–Welzel indexes as independent variables and CMMS or EFFS as the dependent variable. From the results, we selected the most promising indicators to test hypotheses H6a and H6b in linear regression models.

The institutional indicators are based on the literature reviewed previously and were operationalized using the latest OECD or World Bank data available. Financial inclusion is operationalized as the proportion of individuals age 15 or older who own an account at a financial institution (World Bank 2017), income inequality is measured by the Gini coefficient with values between 0 and 1 (1 = totally unequal; World Bank 2021), and trust in government is expressed as the share of individuals who report having confidence in the national government (OECD 2021b). These institutional indicators were used as independent variables in linear regressions with CMMS or EFFS as the dependent variable to test hypotheses H7a and H7b. To summarize the study design and to clarify its relation to the conceptual model proposed in Figure 1, we present a model of our study in Figure 3.

Study design.

Analysis and Results

Effects of Socioeconomic Status on Financial Well-Being

To test H1 and assess the relation between the components of financial well-being and socioeconomic status (H2a–H5b), we calculated structural equation models first in the full sample (Figure 4) and then for each of the countries (Table 5).

Effects of the socioeconomic status on financial well-being in the full sample (n = 14,327).

Relation Between Socioeconomic Status and Financial Well-Being in Each of the Country Samples.

*p < .05.

**p < .01.

***p < .001.

As the PCA showed, in German-speaking countries a second component of EFFS was observed (see Table B1 in Appendix B), causing the poor fit of the models in Austria and Germany.

Notes: Standardized structural equation models, latent variables with 4 + 4 observed CMMS or EFFS variables as shown in Figure 2. Observed socioeconomic status variables: age from 18 to 99 years, gender (1 = male and 0 = female), income in ten categories, and education in four categories; see the details of these categories in Table 2. A substantial number of observations were lost in all countries because of missing values for income.

For the full standardized model (measurement and structural) in the full sample (n = 14,327 because of missing values in some of the socioeconomic status variables, mostly in income) the goodness-of-fit statistics are χ2 = 2,400.503 with d.f. = 43; p = .000; RMSEA = .062 (90% confidence interval [.060, .064]); CFI = .958; TLI = .942; SRMR = .040; and CD = .174.

Interestingly, the best model fit is for Romania and the Philippines—countries where the sample was representative of the online population—and in the United States, where the original scales were developed.

Age and income have a significant effect on both components of financial well-being in the full sample (Figure 4) and in almost all the countries in our sample (Table 5). Older individuals have less money management stress (significant effect in 12 countries out of 16) but also perceive their future as financially less secure (significant effect in 15 countries out of 16); the effect of age on CMMS is the largest in the United States, and the effect on EFFS is largest in Luxembourg. Therefore, we find evidence to support H2a but not H2b as the effect is in the opposite direction from what we assumed.

Income has a clear relation to financial well-being: those with higher income have lower CMMS and higher EFFS in the full sample, and the effects are significant in almost all of the countries (except for EFFS in Austria, Czechia, and Luxembourg). These effects are also quite large; for example, in France the effect of income (standardized coefficient) is −.34 on CMMS and .21 on EFFS, and in Turkey, these effects are −.38 and .35, respectively. Thus we find evidence to support both H4a and H4b.

We find that gender has no effect on CMMS and little effect (.06) on EFFS in the full sample. Looking into the results by country, we see significant effects in a few of the countries. In Romania women and in Turkey men have slightly higher CMMS (effect size around .1 in both), but in the remaining 14 countries, gender does not have a significant effect on CMMS. In 7 countries out of 16, men have higher EFFS (Austria, Belgium, Czechia, France, Poland, Spain and the United States; effect size around .1), and, interestingly, women have higher EFFS in Luxembourg. Therefore, we do not find evidence to support H3a or H3b.

Education has a significant effect on both components in the expected direction (H5a and H5b) in the full sample, but the relation between education and financial well-being is more diverse across countries. In four countries (Austria, Belgium, Czechia, and Germany), higher education decreases CMMS, but in the United States, interestingly, it increases CMMS instead. In 12 out of 16 countries, higher education increases EFFS. The effect size is the largest in the United States (.25). In some countries (the Netherlands and Turkey), education has no effect on either component of financial well-being. Thus H5a and H5b are only partially supported.

From this analysis, we see that H1 is only partially supported: only income has a significant effect on financial well-being in all 16 countries, and the effects of age, gender, and education on CMMS and EFFS differ between countries.

We also find that CMMS has a large effect on EFFS, ranging from .14 in the Philippines to −.49 in Belgium. In the full sample, CMMS mediates a small proportion of the effects of socioeconomic status on EFFS: 15% of the total effects of education and 26% of the effects of income are indirect. However, 46% of the total effects of age on EFFS are mediated by CMMS.

Financial Well-Being Across Age Groups and Countries

We see that the mean scores of both components of financial well-being differ significantly across age groups (Table 6): individuals 18–44 years old have higher CMMS than older cohorts, and EFFS is highest in the youngest (18–29) age group.

Means of the Latent Variables by Age Groups.

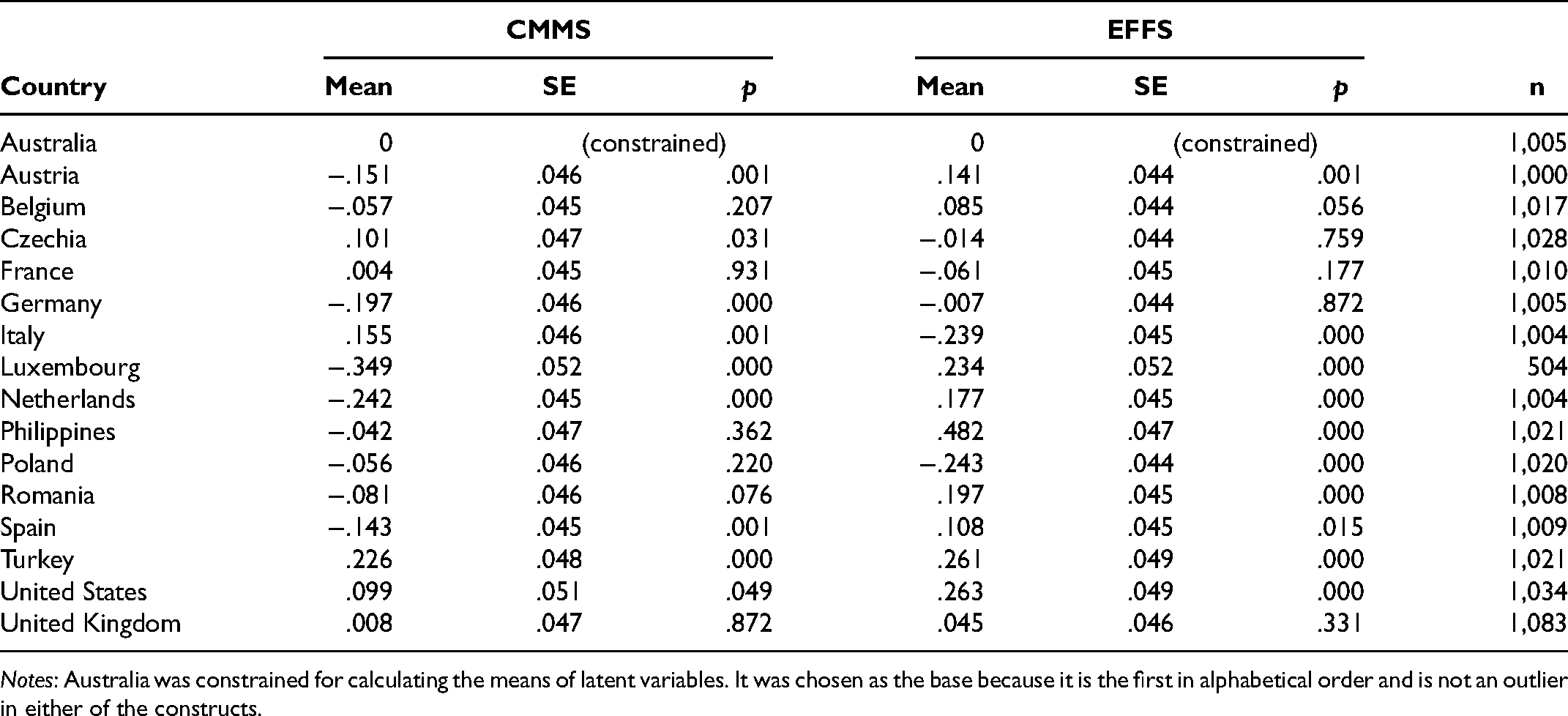

The country comparison is more complex (Table 7). In seven countries CMMS and in nine countries EFFS differs significantly (p ˂ .01) from the corresponding level in the base country (Australia). The largest difference is, expectedly, in Luxembourg, where CMMS is substantially lower and EFFS higher. The most surprising result is that EFFS is the highest in the Philippines, the only developing country in our sample. Because we have problems with measurement invariance, we cannot be fully certain when comparing the mean scores in these 16 countries. However, the significant differences across age groups indicate that financial well-being components may differ across age groups even more than they do across countries.

Means of the Latent Variables CMMS and EFFS by Country.

Notes: Australia was constrained for calculating the means of latent variables. It was chosen as the base because it is the first in alphabetical order and is not an outlier in either of the constructs.

Relation Between National Culture, Institutional Setting, and Financial Well-Being

Although the sample of 16 countries is not large enough to diagnose the relation between cultural and institutional setting on the one hand and the components of financial well-being on the other, we do shed some light on this matter.

Ideally, we would have observed clear groups of countries in our results by their economic development, institutional setting, or national culture. Surprisingly, in the only developing country in our sample—the Philippines—EFFS is the highest. An explanation might be in the culture, as this country also scores the highest on collectivism in the Hofstede cultural dimensions (Hofstede Insights 2020) in our sample. However, the second-highest EFFS score was measured in the most individualistic country of our sample: the United States.

The objective macroeconomic conditions seem to have a clear relation to financial well-being only in the exceptionally wealthy country in our sample: Luxembourg. This finding is not sufficient to claim causation between country wealth and subjective financial well-being, especially in light of research warning against overemphasizing the role of GDP in subjective well-being (Ruggeri 2019, p. 223), and given that income inequality may be a more important predictor of financial well-being than GDP is (CCPC 2018; Kempson 2018). The finding of the highest EFFS in the Philippines undermines the assumption of correlation between country wealth and financial well-being.

We see that in English-speaking countries (Australia, United States, and the United Kingdom), the CMMS level does not differ, but for EFFS, the United States has a significantly higher mean score. One might assume that the neighboring countries Belgium and the Netherlands have similar financial well-being, but this does not hold in our data. In the Netherlands, CMMS is lower and EFFS higher than in Belgium.

One might also assume that the Southern European countries Spain and Italy have similar financial well-being as they are on a similar level, according to the World Bank data on GDP per capita and income inequality (Gini coefficient), but we observe CMMS to be higher and EFFS lower in Italy. This finding might relate to the cultural clusters as well.

In the Inglehart–Welzel values framework (Inglehart and Welzel 2005), most of our sample countries rank higher in secular than in traditional values and higher in self-expression than in survival values in the World Values Survey wave 7 (2017–2020) data. The two countries leaning more toward survival values are the Philippines and Turkey, both of which scored higher in EFFS. It would be appealing to say that those focusing on survival do not spend their scarce resources on thinking about their financial future (Shah, Shafir, and Mullainathan 2015), but the country with the second highest EFFS score—the United States—prioritizes self-expression values. Therefore, that assumption does not hold in our data either.

In short, no clear clusters of countries emerged on the basis of either cultural or economic indicators. As our fourth objective was to analyze the possible relations between cultural and institutional factors and financial well-being components, we calculated linear regression models where the dependent variable is the mean of the latent CMMS or EFFS per country and the independent variables are the cultural and institutional indicators. We observed that the selected cultural indicators—individualism and indulgence—seem to correlate with EFFS (Figure 5), but not with CMMS, and the third indicator—long-term orientation—does not have a significant correlation with either of the components.

Correlation between national culture and financial well-being (n = 13).

The statistically significant correlations (p ˂ .01) between EFFS and selected cultural indicators had high beta coefficients: β = −.84 for individualism and β = .84 for indulgence. The first negative correlation is expected. Those from more individualistic cultures perceive their financial future as less secure, while in more collectivistic cultures people can rely on support from family and community, not only on their own savings and investments. The positive correlation observed between indulgence—“the extent to which people try to control their desires and impulses” (Hofstede Insights 2020)—and EFFS is surprising. One might assume that those who indulge in life in the present do not save or plan much for their financial future. This finding might refer to being overly optimistic about the future, or it might relate to either the myopia or financial ignorance discussed previously.

Testing H7a and H7b showed that two institutional factors—financial inclusion and trust in government—appear to have a significant relation with CMMS (Figure 6), but not with EFFS, and the third indicator, income inequality, does not have a significant correlation with either of the components in our data.

Correlation between institutional setting and financial well-being (n = 15).

The standardized beta coefficients are large for the statistically significant (p ˂ .001) correlations between CMMS and selected institutional indicators: β = −.65 for financial inclusion, and β = −.63 for trust in government. Where financial inclusion and trust in government are high, individuals are less stressed about managing their finances in the present. One might assume that these indicators also affect EFFS, but we do not find evidence of it in our data.

Thus we found evidence to support H6b and H7a and did not find evidence to support H6a or H7b. However, these results should be treated with caution, as the sample size is small (n = 15 and n = 13 respectively) and the issues with measurement invariance limit our ability to compare the mean scores across countries. Appendix D provides the values of the cultural and institutional indicators per country.

Additional Analysis of the Contextual Factors

We conducted additional exploratory analysis of the interaction between individual and contextual factors and its effects on the two components of financial well-being. However, we must refrain from comparing the effect sizes. First, as we merged individual- and country-level data, we contradict our criticism of defining culture solely by national borders. For an in-depth analysis of the moderating role of culture on the effects of socioeconomic status on financial well-being, future studies should include items that measure values of the respondents and also ask about their ethnicity and religion. Second, to analyze the components of financial well-being as latent variables and the interaction effects of individual and cultural indicators, we needed to use general SEM (gsem package in Stata), which does not enable standardization of the estimates. Third, we lost numerous observations in some of the models because of missing data on some of the indicators. Therefore, these results need to be interpreted with caution and serve as a mere indication of possible moderating effects of the contextual factors on financial well-being.

We calculated four general structural equation models and found the individual and contextual factors to have significant effects on the components of financial well-being in our previous analysis. We studied the moderating effects of institutional setting (financial inclusion and trust in government) on the relation between socioeconomic indicators (age or income) and CMMS, and the moderating effects of cultural dimensions (individualism and indulgence) on EFFS. We found that financial inclusion affects CMMS and moderates the effects of age on CMMS in the younger (30–44 years old) and oldest groups (Table 8). Trust has an effect on CMMS but does not moderate the effects of age. When income, financial inclusion, and trust in government are included simultaneously, trust has no significant effect on CMMS, nor does it moderate the effects of income on CMMS, except for the lowest-income group (household net income €1–€499). Financial inclusion moderates the effects of income on CMMS in middle income groups (€2,000–€3,999).

Interaction Between Socioeconomic Status and Contextual Indicators, and Their Effect on the Latent Financial Well-Being Component in the Full Sample.

*p < .05.

**p < .01.

***p < .001.

Notes: This table presents coefficients with SEs in parentheses. The general structural equation model command in Stata, gsem, does not enable standardized estimates. FI = financial inclusion. Coefficients for the four contextual factors have been omitted from the table for brevity. Base categories of the individual factors are age 18–29 and zero household net income. The details of the categories can be seen in Table 2. Sample sizes for gsem models are as follows: (1) CMMS, age, financial inclusion, and trust in government, n = 13,744; (2) CMMS, income, financial inclusion, and trust in government, n = 12,469; (3) EFFS, age, indulgence, and individualism, n = 15,773; and (4) EFFS, income, indulgence, and individualism, n = 14,327.

Analyzing the interaction between age and cultural indicators, we see that indulgence moderates the effects of age on EFFS in younger to middle age groups (age 30–59), but not for the older cohort (60+). Individualism has a significant effect on EFFS but does not moderate the effects of age. When income and cultural indicators are included in the model simultaneously, indulgence has no significant effect on EFFS. Individualism moderates the effect of income on EFFS in the lower- (up to €1,999) and highest- (more than €7,000) income groups.

To conclude, we find evidence to suggest that the moderating effects of the country context exist for certain socioeconomic groups (e.g., young people, low-income households) but are not universal across populations.

Discussion and Conclusions

We proposed a conceptual model building on financial well-being research and reassessed an existing financial well-being measure. We tested 13 hypotheses on the effects of individual and contextual factors on the two components of financial well-being and found sufficient evidence to support five of them. We also shed light on the possible interaction between the individual and contextual indicators affecting financial well-being.

Although the reliability of the CMMS and EFFS statements was satisfactory for the full sample of 15,773 individuals, SEM measurement models revealed problems with measurement invariance for comparing the mean scores of 16 countries. This is a clear illustration of the arguments of Van Raaij (1978) and Baumgartner and Weijters (2021) on the methodological restrictions in international marketing research. Although the Cronbach’s alpha and PCA results allowed us to assume the suitability of the measures, SEM multisample analysis revealed the lack of measurement invariance that would have allowed reliable cross-country comparisons. Therefore, we found the CMMS and EFFS scales to have weaknesses for international consumer research.

Interestingly, the full structural model with two latent variables (CMMS and EFFS) and four socioeconomic status variables had a better fit in countries where the sample was representative of the online population (Romania and the Philippines). As the original CMMS and EFFS measures were tested online in MTurk, our results may indicate that these measures are better to be used for analyzing online populations, but some other measures may be better suited for assessing financial well-being in a representative sample of the entire population. For that purpose, new instruments could be developed, or the existing ones (such as the financial well-being measures of Strömbäck et al. 2020 or Kempson and Poppe 2018) should be tested in large international samples.

As financial well-being is context dependent, so can be the scales for assessing it. For understanding the meaning of financial well-being in various countries and cultures, qualitative studies such as the one conducted in Australia by Salignac et al. (2020) should be done as a prerequisite for designing the scales for internationally comparable results. Note that all existing financial well-being measures were developed in Western countries, many of them in English-speaking countries. The CMMS and EFFS scales were developed in the United States (Netemeyer et al. 2018). As Van Raaij (1978, p. 693) warned, consumer research “made in the USA” may introduce ethnocentrism in the type of questions addressed in international marketing research. These arguments are supported by the good fit of the full SEM model in the U.S. sample.

Many factors affect financial well-being on both individual and contextual levels, as summarized in our conceptual model (Figure 1). We find evidence on both levels that the antecedents of the two components of financial well-being differ. Previous studies using the CMMS and EFFS scales have found these differences only at the individual level and in single countries (Netemeyer et al. 2018; Ponchio, Cordeiro, and Gonçalves 2019).

On the individual level, we focused on the effects of socioeconomic status and showed that these effects differ by country and component, except for income, which has a straightforward and universal relation to financial well-being. The latter finding is consistent with previous research (Fu 2020; Kempson 2018). Higher education is related to CMMS in some countries, but in others it is related to EFFS. Gender differences were observed in only a few countries.

We found that age has a clear effect on both components of financial well-being, but the relation of financial well-being to national culture and institutional setting is more complex. The reason may be that the globalizing world makes evaluations of financial situation universal, despite cultural or institutional context. Instead of comparing one’s lifestyle to that of local peers, social media allows people to immediately see a wider range of lifestyles and compare themselves with members of aspirational and associative reference groups around the world. Therefore, the reference point may have shifted from local to global consumers.

We conducted an exploratory analysis of the interaction between individual and contextual factors and found that financial inclusion moderates the effects of age on CMMS in the younger (30–44 years old) and oldest groups, and it moderates the effects of income in the middle-income group. In countries with higher financial inclusion, middle-income individuals have less stress about managing their finances. Trust in government did not have a significant interaction with age or income, except in the lowest-income group. We found individualism to moderate the effects of income on EFFS in lower-income groups (€1–€1,999). These findings must be interpreted with caution because of the data limitations explained previously.

On the country level, we observed that financial inclusion and trust in government have a significant correlation with CMMS. The first of those observations is consistent with the financial well-being literature (Latif et al. 2015), whereas the latter relation has been explored less. In a recent study conducted in Sweden, trust in government was found to have a significant effect on financial security (a construct similar to EFFS) on the individual level (Barrafrem, Tinghög, and Västfjäll 2021). This contrasting finding might be related to the slightly different approaches to measuring financial well-being, and to the differences between individual- and country-level analyses. In our data, the Scandinavian countries were not included, and thus we cannot compare the findings. Furthermore, our data were collected before the outbreak of the COVID-19 pandemic, the effects of which are in the focus of the Swedish study.

We found indications that national culture correlates with EFFS, whereas institutional setting has a relation with CMMS. To our knowledge, this distinction has not been described before. That has important implications for practice. Instead of aiming at increasing financial well-being, public and private sector initiatives should target either CMMS or EFFS, the present or future component of financial well-being.

Managerial Implications

Initiatives for increasing financial well-being are often designed and implemented by multiple stakeholders from the public and private sectors. A recent policy report refers to such partnerships as “financial health ecosystems” and calls for their development worldwide (UNSGSA Financial Health Working Group 2021). Thus, we provide recommendations without drawing a strict line between practice and policy. Tools for increasing financial well-being can include financial education, nudges, policy interventions (such as pension reforms or national strategies for financial education), and the design and marketing of financial services.

Financial well-being is seen as the ultimate outcome of financial education (OECD 2020b). Simply put, financial education is the process of developing financial competence. In its narrowest approach, it is seen as teaching financial knowledge through formal education, whereas in the broader meaning it includes any initiatives designed to help individuals to make informed financial choices for increasing their financial well-being (OECD 2005; Riitsalu 2018). For example, these initiatives can include consumer education portals, promotional campaigns such as the annual Global Money Week (OECD 2021a), or apps designed by banks or fintech companies for managing personal finances. Promoters of financial education initiatives should clearly decide which component of financial well-being they aim to improve and design their interventions accordingly.

Marketers of financial services and promoters of financial education need to decide which component of financial well-being they wish to address, as these are influenced by various individual and contextual factors. If the goal is to reduce CMMS, younger individuals and lower-income groups should be targeted. Policy makers can take steps to improve financial inclusion for everyone to have access to formal financial services. However, the COVID-19 pandemic has accelerated the development of digital financial services that are seen as the cure for financial exclusion (Morgan 2021; OECD 2020a); thus, rapid improvements in financial inclusion have already occurred.

If the goal is to increase EFFS, middle-aged and older individuals should be supported and encouraged in taking steps to secure their financial future, although reminding younger audiences of their possible myopia in long-term finances would do no harm. As with CMMS, lower-income groups should be targeted. Perhaps instead of financial education or persuasion, their financial well-being would benefit from changes in social policy. In more individualistic cultures, the future seems less secure, and therefore the development of supportive communities can have a positive impact on expectations for the financial future in these countries.

Alternatively, interventions for improving financial well-being can employ nudges. Nudges are behaviorally designed elements of choice architecture that make sound options (such as saving) easier and less beneficial choices (such as impulsive spending) more difficult but not impossible to choose (Thaler and Sunstein 2009). They can be employed in the design of financial services, advice, and education, but also in marketing and policy making. For example, sending a simple weekly statement of automatic micro-investments accompanied by a gamified option to increase these contributions had a positive effect on the amounts invested (Riitsalu and Uusberg 2021). Such tools enable people to secure their financial future.

Because of the diversity of consumers within and across countries, global messages may not be efficient for increasing financial well-being. Instead, personalized communication that takes into account not only the cultural context and financial situation of the consumer but also the consumer’s life stage (Salignac et al. 2020), personality, and lifestyle should be preferred by policy makers and marketers. Although most retail banks are part of large international brands and tend to have globalized marketing communications (Wright 2002), the digitalization of financial services, advice, and financial education (Morgan 2021) enables greater personalization and customization to align with customers’ needs and behaviors. Thus, their communications can be globalized and narrowly customized at the same time. The first steps could include assessment of the current and future financial well-being components in their target groups and markets; segmentation that builds on the assessment findings and the analysis of their customers’ values, lifestyles, and financial behavior; and tailoring of the tools to increase financial well-being accordingly.

Limitations and Further Research

We contribute to the emerging stream of research on the conceptualization of financial well-being. We did not intend to conduct an in-depth investigation of the full range of its antecedents and outcomes; instead, our research lays the groundwork for internationally comparable, detailed investigations of financial well-being.

However, we did endeavor to map possible paths for further research by comparing scores and conducting regression analysis with cultural and institutional indicators. The main limitations of these findings are related to the data. As discussed in detail, the CMMS and EFFS data lacked measurement invariance. Although 16 countries are represented in the sample, even more should be involved for more detailed analysis of the individual and contextual differences across countries. Furthermore, in three of the countries, the sample was representative of the online population only, and data on cultural and institutional indicators were missing for a few countries. Because of the limitations of the data, we focused on four socioeconomic indicators. Future studies could include a broader range of such factors, for example, to analyze how the roles and responsibilities in managing current and future financial affairs within a household affect the components of financial well-being.

In our analysis of the relation between culture and financial well-being, we used indicators of the national culture. Cleveland, Laroche, and Papadopoulos (2009) emphasize that most countries are multicultural; Van Raaij (1997) adds that regional differences in culture should not be ignored. Thus, it is naive to group individuals into different cultures on the basis of country borders. Instead, individual values could be assessed. However, we did find an indication that national culture might correlate with EFFS. Further research is needed to examine the relation between indulgence and EFFS, preferably together with individual psychological characteristics, such as impulsiveness, conscientiousness, and financial ignorance. Research into the effects of national culture on financial well-being could be studied further in data from a larger group of countries.

We suggest conducting internationally comparable studies on the individual and contextual factors affecting CMMS and EFFS, and analyzing how these factors interact. We shed some light on the possible interaction between individual and cultural factors, but further studies are needed. These studies could include measures of financial competence, personality, and values, and they could assess cultural differences in subjective financial well-being. They could also ask about the respondent’s ethnicity and religion, and include objective measures, such as individual income, size of the savings buffer, and the value of the assets held, to determine whether people have a valid and realistic idea of their present and future financial situation. Ideally, the whole range of factors presented in our conceptual model could be included in a large-scale, longitudinal international financial well-being assessment, and common method variance (Baumgartner and Weijters 2021) would be dealt with prior to data collection.

Footnotes

Appendices

Acknowledgments

The authors are grateful to Kai Ruggeri, Andero Uusberg, Rein Murakas, and Andu Rämmer for their feedback and advice and to the participants of the financial well-being session of the IAREP-SABE 2021 virtual conference, especially Leonhard Lades, Agata Gąsiorowska, Thomas Post, and Gustav Tinghög, for their suggestions. We would also like to thank the Think Forward Initiative for supporting our study.

Associate Editor

Amir Grinstein

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The data were collected as part of a short-term research project funded by the Think Forward Initiative.