Abstract

After substantial global investments into biofuel production from 2005 to 2008, challenges to a sustainable and robust biofuel industry have become more apparent than many proponents have anticipated. Across country and development contexts, conflicts arose as plans to scale up production clashed with local preferences or national policies, and Southern Africa has been no exception. This article analyzes recent difficulties with biofuels projects in Tanzania before the background of the more successful experiences of Brazil and South Africa. We identify areas of incompatibility between local expectations, government policy, and investor incentives. An assessment of different biofuels business models shows that some—such as contract farming—may not be appropriate for Tanzania’s situation and that policies are necessary that can address the needs of both local and regional stakeholders and provide adequate incentives for investors to pursue sustainable biofuels production.

Biofuel Retrenchment in Southern Africa

Although ambitious biofuels initiatives attracted substantial global attention and investment between 2005 and 2008, it has become clear that developing a sustainable and robust biofuel industry will be more challenging than was at first envisioned. Across both country and development contexts, conflicts arose as plans to scale up production clashed with local preferences or national policies. For example, U.S. corn ethanol raised extensive questions on environmental efficacy (Borras, McMichael, & Scoones, 2010), expansion of palm oil plantations in Southeast Asia raised questions about land use and deforestation (McMichaels, 2010), continued growth in Brazil’s ethanol sector provoked criticisms that it displaces rural peoples (Fernandes, Welch, & Concalves, 2010), and India’s development of jatropha led to questions about whether poor farmers could benefit from growing energy crops (Ariza-Montobbio, Lele, Kallis, & Martinez-Alier, 2010).

Southern African countries underwent similar expansions that raised concerns as well. In an initial period of enthusiasm, biofuel production was advocated as a development solution in several Southern African countries, but most of them had no specific biofuels policies in place to direct investment or ensure sustainable outcomes (Jumbe, Msiska, & Madjera, 2009). Early investors came to government officials with proposals to establish sugarcane, jatropha, and palm oil plantations which prompted extensive discussion about the potential for each of these crops (Amigun, Sigamoney, & von Blottnitz, 2008). Yet in addition to the now-familiar problems of scale-up, displacement of food production, and environmental impact, many projects in Southern Africa also encountered new problems mostly with a number of companies failing to secure new capital during the global financial crisis of 2008-2009, which at times led to failures in their initial investments. To date, two of the first biofuels companies in Tanzania have sold their properties to new investors, and one has apparently abandoned its properties and employees.

This article evaluates some of the past obstacles encountered by biofuel projects in Tanzania and compares elements of that experience to others in Brazil, India, and several African countries. We review the recent history of biofuel production in Tanzania and assess the relevant parallels to biofuels programs throughout the wider region. We identify the major problems that have arisen in recent projects and then discuss other approaches that will be potentially more successful. Finally, we evaluate Tanzania’s new biofuels policy in light of these results, and make recommendations about how to better incorporate alternative approaches into future policy decisions.

Tanzania as a Locus of Biofuel Development Initiatives

Biofuels in the Southern African and Global Context

The early evolution of biofuels production in Southern Africa was characterized by a proliferation of alternate feedstocks and processes. Until quite recently, there were few systematic comparisons of the potential of different types of biofuels and feedstocks in Tanzania. Stakeholders—including national and regional officials as well as development advocates—therefore have had a difficult time in isolating the fuels and feedstocks best suited to national and local circumstances. Complicating the early analysis was the large diversity of approaches taken by other biofuel producer countries that were seen as potential models. India, for example, cultivates mainly jatropha for biodiesel, whereas the Southeast Asian biodiesel industries almost exclusively grow oil palm (Peters & Thielmann, 2008; Pye, 2010)—Indonesia in particular has more than doubled oil palm production since 2000 and continues to increase their output (McCarthy, 2010). Brazil famously relies on sugarcane ethanol, and the United States equally so on maize ethanol (Fernandes et al., 2010; Gillon, 2010). Europe increasingly relies on imports from places like Southern Africa and Southeast Asia, but it also produces biodiesel domestically, mainly from rapeseed (Jumbe et al., 2009; Pye, 2010).

Other Sub-Saharan African countries provided disparate and diffuse examples for Tanzania, confounding easy identification and application of “best practices.” Ethanol from sugarcane and sugar molasses both have a large presence in the region, including operations in Kenya, Zimbabwe, Uganda, South Africa, Malawi, and Tanzania (Jumbe et al., 2009). Well over a dozen Sub-Saharan African countries also have substantial biodiesel operations (Amigun et al., 2008). Tanzania relies primarily on jatropha or oil palm as biodiesel feedstocks; but soya bean, coconut, sunflower, cassava, cashew, and others that can produce biofuels are all under cultivation in various parts of the country for food production (Jumbe et al., 2009; Mulugetta, 2009). This vast diversity of approaches to biofuels production offers mixed lessons at best, and no one strategy has emerged as a perfect solution. Furthermore, even the most successful operations elsewhere have encountered pitfalls that Tanzania would do well to avoid, for example, from an environmental point of view, crop selection matters significantly. High-yield crops such as sugarcane for ethanol and oil palm for biodiesel produce more per acre than most competing feedstocks (Maltsoglou & Khwaja, 2010; Mulugetta, 2009), although these are not feasible in all environments. A country that instead opts for a feedstock such as jatropha must trade-off possible benefits against poor yield, possible invasiveness (IUCN, 2008, 2009) and other forms of environmental degradation and pollution. In addition, jatropha is not edible by people or most wild animals and has roots that make it difficult to remove. Also, several biofuel feedstocks, such as sugarcane, demand regular water. If irrigated, these too could strain water resources in semiarid or water-limited environments.

The motivations behind biofuel expansion in Tanzania and other Southern African countries also remain diverse and sometimes contested. Although arguments for biofuels development in Africa include rural development and availability of resources such as land and labor (Amigun et al., 2008), scholars continue to disagree about the relationship between biofuels and development. Biofuel production does offer countries an opportunity to reduce dependence on foreign fuels, especially oil, and to partially insulate domestic growth from rising oil prices (Amigun et al., 2008; Mulugetta, 2009). Biofuels may especially help the economic development of rural areas by making rural electrification more feasible and cost-effective and by providing sources of fuel other than traditional biomass (Martin, Mwakaje, & Eklund, 2009). Yet the overall benefits of biofuels to economic development will depend on a wide variety of factors, including the cost of feedstocks, fuel production costs, and the price of fossil fuels (Amigun et al., 2008; Mulugetta, 2009). If implemented well, biofuels can compete in a stable market, encourage development (Romijn & Caniels, 2011), and provide employment benefits. New jobs are most likely to be primary sector jobs (farm labor, manufacturing, etc.) but would also support secondary types of employment in the service and support sectors.

However, biofuel expansion can create hazards as well. Production of biofuels has, in some cases, displaced food production (McMichaels, 2010); moreover, by reducing the amount of land available for growing food and grazing livestock, it can also decrease overall food security (Martin et al., 2009; Mulugetta, 2009), by which we mean the security associated with having a steady and reliable stream of food that is domestically produced and consumed. Indeed the food security implications of biofuels have raised questions about the allocation of grain crops to biofuels rather than nutrition. For this reason, even supporters of biofuels caution that potential producer countries must account for “a collision with food crops” and urge biofuel expansion to avoid high-value farmland (Jumbe et al., 2009). Biofuel production can increase pressure on natural resources by creating incentives to clear land, threatening the environment and biodiversity and (depending on the feedstock) diverting water resources (Jumbe et al., 2009; Martin et al., 2009; Mulugetta, 2009). This is particularly true of large-scale operations that are designed for high output (Martin et al., 2009). In addition, farmers or local populations are sometimes denied equal participation in decisions about biofuel development and other “environmental” initiatives (Bozmoski & Hultman, 2010; Fernandes et al., 2010; McMichaels, 2010), sometimes because they have difficulty in negotiating with developers and investors (Mlingwa, 2009; Romijn & Caniels, 2011; Vermeulen & Cotula, 2010). Large corporate growing operations may displace or disenfranchise small farmers as well by taking away their power to negotiate prices, as well as their decision of what to grow (Fernandes et al., 2010; White & Dasgupta, 2010). Cumulatively, such circumstances can impair the local population’s ability to produce competitively priced food and sustain livelihoods through traditional—or even modernized—methods of agriculture.

Drivers: Energy, Agriculture, and Biofuels in Tanzania

Climate change mitigation, rural development, and energy self-sufficiency have all been highlighted as the driving forces behind biofuel development in Tanzania (Sulle & Nelson, 2009). However, the potential destruction of forests and wildlife migratory corridors, as well as threats to rural livelihoods and land rights, were identified as some of the critical challenges in establishing a biofuel industry in the country (Kamanga, 2008; Songela & Maclean, 2008; Sulle & Nelson, 2009). In Tanzania, 90% of the energy consumed both in rural and urban areas is derived from biomass. Electricity is only accessible to about 10% of the country’s estimated 42 million people. The rate of deforestation, largely driven by demand for biomass, stands between 100,000 and 125,000 ha annually (Peter & Sander, 2009). Agriculture is the dominant economic activity in Tanzania; more than 80% of the population engages in some form of agriculture. In 2010, the agricultural sector accounted for 28% of gross domestic product (GDP; World Bank, 2011). Food crops account for 85% of this sector. A similar percentage of all food producers engage in subsistence agriculture. In fact, only 22% of Tanzanian agriculture is for commercial purposes (Maltsoglou & Khwaja, 2010). Altogether, subsistence farmers cultivate about 85% of the arable land in the country (Sulle & Nelson, 2009; Sulle, 2010 in Lorenzo & Rebecca, 2010).

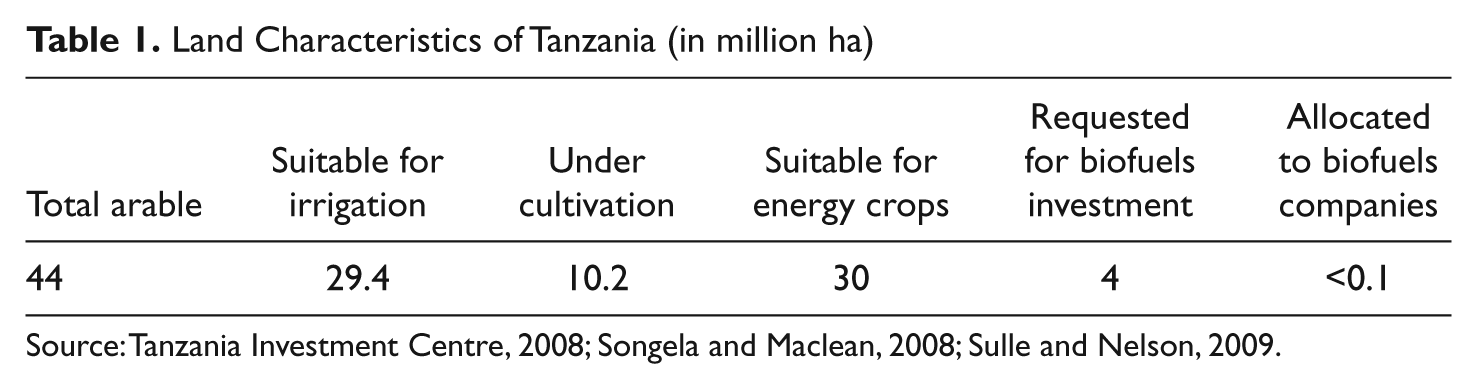

From a purely technical standpoint, Tanzania appears to have sufficient resources to produce biofuels both for its own consumption and for export, without competing for land with current food production (Table 1). In total, the country has 94.5 million ha of land of which 44 million ha is arable and 29.4 million is suitable for agriculture; only 10.2 million ha are currently under cultivation (Tanzania Investment Centre, 2008). Moreover, Tanzania’s environment could potentially support several different biofuels feedstocks at varying levels of productivity, including sugarcane, coconut, oil palm, sunflower, cassava, cashew nuts, sweet sorghum, and jatropha (Songela & Maclean, 2008; Sulle & Nelson, 2009). Sugarcane is currently grown by both large- and small-scale operations, whereas most of the others, including sunflower and palm oil, are grown predominantly by small farmers. Maize, wheat, rice, and sweet sorghum are all basic food crops in Tanzania; if producers divert them from the food supply to biofuel production, this could create real or perceived problems with food prices (Jumbe et al., 2009).

Land Characteristics of Tanzania (in million ha)

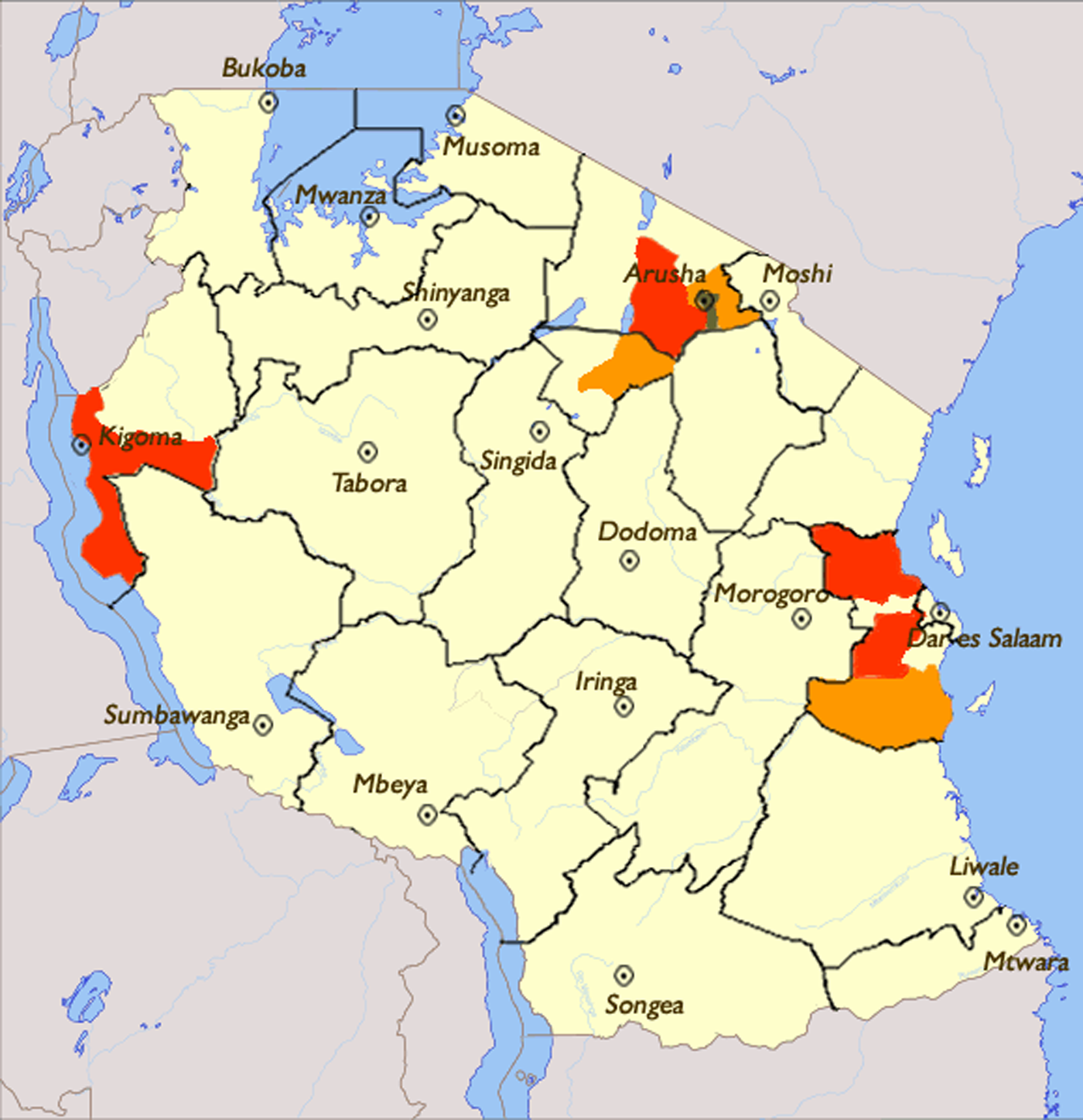

It has been estimated that between 2007 and 2008, Southern Africa experienced an influx of more than US$3 billion in biofuels investments; Tanzania alone received commitments of about US$1 billion to be spread over 20 years (Sulle & Nelson, 2009; Richardson, 2010), which is an large relative to Tanzania’s 2010 GDP which was estimated at US$23.057 billion (World Bank, 2011). About US$20 million was invested in a jatropha plantation in the Kisarawe district (van Eijck & Romijn, 2008); a large number of other private companies also established processing facilities and initiated land acquisition processes (Songela & Maclean, 2008; Sulle & Nelson, 2009). Currently, major biofuels companies in Tanzania have invested in jatropha (e.g., Sun Biofuels, Ltd.—a branch of the U.K.-based BioShape Ltd., Bioshape Tanzania Ltd.—a subsidiary of the Netherlands BV Holdings, Diligent Tanzania Ltd., and PROKON Tanzania Ltd.), sugarcane (SEKAB BioEnergy Tanzania Ltd.), and palm oil (FELISA Company Ltd. and InfEnergy Tanzania Ltd.). A number of these companies have their offices in Dar es Salaam (Figure 1), whereas a few have offices in regions such as Kigoma (FELISA) and Arusha (Dillegent). These companies have chosen these crops for diverse reasons, including geographical location, crop suitability, and the structure of their business model. Two companies have large-scale jatropha farms. Two more have contracts with small-scale farmers for jatropha and supply their produce to biodiesel processing companies. Other companies are interested in developing sugarcane plantations with outgrowers to produce ethanol or palm oil plantations to produce biodiesel (ActionAid, 2009; Kamata, 2009; Mwamila et al., 2009; Songela & Maclean, 2008; Sulle & Nelson, 2009).

Locations of major biofuels production areas in Tanzania

The Tanzanian Ministry of Agriculture, Food Security, and Cooperatives (MAFSC) and the United Nations Food and Agriculture Organization (UN FAO) recently assessed the biofuels potential of different regions by crop. This has helped to fill the considerable knowledge gap regarding ideal biofuels and feedstocks for Tanzania. According to the MAFSC and UN FAO, Tanzania has a total of about 26 million ha suitable for growing sweet sorghum with a maximum total output 346 million tons of juice (Maltsoglou & Khwaja, 2010). This report also found that Tanzania has 882,921 ha suitable for producing sugarcane; if fully cultivated this resource could produce 7 million tons of sugar per year (Maltsoglou & Khwaja, 2010), but to date there are only 5 sugar mills operating in the country, using less than 60,000 ha. Proponents of biofuels development in Tanzania argue that the small current cultivation implies an enormous potential resource is being underused.

The MAFSC and UN FAO study also concluded that cassava is perhaps the most promising biofuel feedstock for Tanzania in terms of technical potential (Maltsoglou & Khwaja, 2010). However, it is somewhat difficult to judge such claims due to a lack of actual experience. In contrast to these other crops, Tanzania has a long history with palm oil. The country has cultivated it since roughly 1920, and palm oil is a major source of food in the western regions of Tanzania, as well as for the manufacturing of soaps and refined edible oils. UN FAO estimated that there are 887,950 ha suitable for palm oil cultivation in Tanzania (Maltsoglou & Khwaja, 2010). Currently, however, Tanzania does not produce enough palm oil even to satisfy local demand. Reports from the Kigoma Farmers Association indicate that they collect an annual total of about 150,000 liters of palm oil, most of which goes to edible oil refineries and soap producers in Dar es Salaam (Sulle & Nelson, 2009). Although MAFSC/UN FAO study has addressed a number of salient questions, it has not ended the conversation. Even setting aside possible questions of data reliability, each of these feedstocks presents considerable challenges to Tanzania. Producing biofuels from sorghum or cassava would affect food production as both are staple food crops. Sugar and oil palm have presented considerable problems for other countries, not the least of which is the capital intensity required to grow them.

Challenges to Tanzanian Biofuels Implementation

Tanzania was one of the first African countries that attracted biofuels investments. However, despite the country’s potential, early biofuels investments did not succeed very well. Like many other African nations, Tanzania underwent an expansion of biofuels production before defining or implementing any policy strategy for the development and regulation of this industry. The reasons for problems vary widely, but derive inter alia from ineffective policy formulation processes, lack of financing, and governance problems such as contradictory policies, inconsistent enforcement, and poor management by central and local authorities (Songela & Maclean, 2008; Sulle & Nelson, 2009). Another major challenge was that the Tanzanian government was unable to handle investors’ requests to establish biofuels plantations and businesses properly because, at the time, it did not have appropriate policies or legal frameworks in place. Local and international NGOs opposed the new biofuel operations in the absence of defined policy and legal frameworks, pointing out the potential threats they might pose to both the environment and rural livelihoods. These organizations were then able to force the government to halt land allocations to biofuels companies, mostly through research publications that they actively disseminated to the public (Kamanga, 2008; Songela & Maclean, 2008). The government promised to allow further land allocation once it developed appropriate biofuels policies as well as legal and institutional frameworks to govern such investment and development (Sulle & Nelson, 2009).

Current Tanzanian investment procedures require companies to present their case to the Tanzania Investments Centre (TIC) before negotiating for land, and then to work with district officials during the land acquisition phase to ensure that deals are fair to villagers. However, some biofuels companies appear to have negotiated land deals with villagers after getting introductory letters from the TIC with little involvement from district officials. Sometimes, district-level authorities facilitated land acquisition processes (Sulle & Nelson, 2009); in other cases, villagers ceded land to investors in exchange for sometimes unreliable promises of schools, health facilities, or jobs.

Financial and credit problems also plagued some biofuels projects. Some companies were affected by the financial crisis of 2008-2009. For instance, one company was not able to pay its permanent employees in Tanzania for several months because of what company officials describe as financial difficulties faced by the mother company in the Netherlands, BioShape Holding B.V. Another company that was also forced to close down its operations in 2009 because of financial difficulties was SEKAB Tanzania Ltd.

Other projects were affected by controversy or difficulties with governance of land and land aquisitions. Less than 20% of Tanzania’s 44 million ha of arable land is under cultivation or used for grazing (Shekighenda, 2010), but even gaining access to unused land in Tanzania is difficult for indigenous and foreign investors alike. Although safeguards to access land were designed to help protect the rights of rural communities, often these goals are not met, still some village lands have been transferred to the general land without proper procedures being followed (Songela & Maclean, 2008). At the same time, these policies create uncertainty for investment. Sun Biofuels and SEKAB BT are among the few companies that have attempted to navigate these cumbersome procedures. Sun acquired 8,211 ha in Kisarawe to develop jatropha plantations. SEKAB managed to lease 22,000 ha but failed to secure other lands in the Bagamoyo and Rufiji districts for sugarcane plantations. SEKAB representatives spent two years looking for land in Tanzania before the company’s finances were affected by the global financial crisis, which, perhaps in conjunction with other issues, convinced it to withdraw.

Other times, questions have arisen as to how well the existing regulations are serving larger policy goals. Bioshape Tanzania, a Dutch biofuels company, signed a deal to acquire 34,000 ha of Miombo woodland (tropical forests) with the stated intention of developing a jatropha plantation for biodiesel production. Bioshape was then able to acquire this land from the Ministry of Land and Housing Development, bypassing the legal custodian of foreign investments and land deals in Tanzania, the Tanzania Investment Corporation. Bioshape Tanzania Ltd is also the largest wood producer in East Africa, raising questions of appropriateness of this regulatory procedure as well as about the need for monitoring of activities on the lands that were purported to be for biofuels development (Lawson, Lukumbuzya, & Wambura, 2009).

In a third example, a company’s search for land yielded an unexpected surprise due to a lack of planning on their part, and poor communication on the part of the government. InfEnergy, a British company, was one of the early investors interested in palm oil development in Tanzania. Unfortunately, for InfEnergy, it secured land in a region that had previously been designated as a food production region by the central government. Because of this designation, the regional authorities would not allow for the company to grow palm oil for biodiesel on the land it had acquired. The company had to alter its business plan to cultivate rice instead to avoid a complete loss on their investment (Songela & Maclean, 2008; Sulle & Nelson, 2009).

Recordkeeping and monitoring—two basic requirements for ensuring compliance and informing future policy improvements—have also been inconsistent. To date, the national government has made no effort to determine how much ethanol and biodiesel is being produced in the country. At least two international companies have been harvesting jatropha seeds and processing them into biodiesel in Tanzania for years, yet the government has little information about how or where these products are consumed. In addition, rather than conduct an independent assessment, the government of Tanzania simply adopted a report produced by an unaccountable organization—the Land Rights Research and Resource Institute (LARRI)—as its reference on biofuels investment statistics in the country (Kamanga, 2008; Sulle & Nelson, 2009). While it is of course possible that LARRI conducted perfectly sound research, deferring to outside entities for essential information can potentially undermine confidence in the data as well as reducing the possibility for implementing changes to the reporting procedures.

Establishing Better Biofuels Development Models

The development of the Tanzanian biofuel industry has been beset by mismanagement and a poor implementation of policies, leading to business failures and negative consequences for some stakeholder groups. While the failure of some individual projects may not be widely mourned, the possibility remains to learn from recent experience and perhaps improve on existing models to achieve a moderate amount of the potential that has been so widely touted. A well-conceived regulatory and investment model might be able to encourage a healthy growth in biofuels production that provides wide and equitable social benefits while also providing a reasonable return on investments.

The rest of this section identifies the potential components of such a framework through two models. First, it examines potential policies by comparison with Brazil, which arguably operates the most economically viable biofuels operation in the world (Xavier, 2007), and South Africa, which is similar to Tanzania geographically, but has had much more success in the biofuels industry. Second, it outlines several alternative models for Tanzania.

Learning From Previous Biofuels Transitions

Brazil has long been an economic leader in biofuel production and currently produces the second most ethanol worldwide, behind the United States. By taking advantage of its large amounts of arable land, Brazil has further maximized this edge by developing advanced bioenergy technologies, better ethanol processing facilities and flex-fuel vehicles (Goldemberg, 1998). In the early stages, the government used economic benefits and energy security to justify biofuels expansion, but recently the motivations have been expanded to include a reduction in greenhouse gas emissions (Borras et al., 2010). Xavier (2007) observes that “even in Brazil, where climate and labor market conditions favor ethanol production, ethanol is cost-competitive with gasoline only during periods when oil prices are high. (p.4)” Biofuel production remains volatile as demand tends to rise during growing seasons and fall during harvesting seasons. This is partially because ethanol production from sugarcane happens only during the harvest season, as sugarcane cannot be stored. This makes it challenging to ensure sufficient supply year-round, particularly right before the harvest (Mlingwa, 2009).Because of its unique situation, with a large preexisting sugar industry and a history of strong government involvement in the early stages of biofuels expansion, the Brazilian experience is in many ways a poor analogue for new biofuel initiatives.

However, one element that does provide a possible insight is the importance of domestic demand and locally useful technologies. Ethanol use in Brazil’s vehicles had declined precipitously in Brazil in the 1990s and early 2000s, due to low oil prices and the loss of government ethanol support. The introduction of “flex-fuel” cars, which can operate on both gasoline and ethanol, or any mixture of the two, stopped this decline and led to a resurgence of ethanol use. This technological improvement enabled the product to be sold widely in the domestic market, which led to broader marketability and domestic support for the technology. This issue has proven to be an important component in the South African context.

South Africa has drier, less fertile land than many other countries in Southern Africa, including Tanzania, which makes it less ideal for biofuels. But despite this, South Africa remains the region’s biofuels leader in terms of production capacity. The country has encouraged local entrepreneurship in biofuels, and there are currently 200 small-scale biodiesel producers in South Africa (Republic of South Africa, 2007). South Africa has also leveraged domestic experts on biofuels in ways that other countries have not. The country has more research universities than any other in Southern African, and several of these perform significant biofuels research and development work. For example, the University of Cape Town and Stellenbosch University both operate several domestic biofuels projects. Such programs can help countries become a more attractive location for outside investors, as they create a source of domestic technical capacity.

Also mirroring Brazil’s early experience, the South African government has also been very involved in promoting the development of feedstocks it considers beneficial to the country and opposing those it feels are less promising. The government has banned the growing of jatropha in the country, choosing to develop sugarcane and other feedstocks, such as sunflower, instead. One can argue with these judgments, but the weight of this policy intervention has been strong. South Africa, because of food security issues, has also shown little support for maize and soy, to the surprise of investors (Lourens, 2009). These policies do sometimes have negative economic consequences for South Africa, at least in the short term. For example, because of the government’s lack of support, Ethanol Africa Ltd. has suspended construction of several planned maize-to-fuels plants in the country (Lourens, 2009). Investors in South Africa, however, have criticized the government for being slow in setting policies, establishing a legal and institutional framework, and only too late pressing their preferences for specific feedstock.

Biofuels Models for Tanzania

Combining an understanding of what has not worked well in Tanzania with what has succeeded in similar contexts allows some synthesis of potentially promising approaches for Tanzania. It appears that much of the potential innovation in this area is not in the more technical dimensions of feedstock and production, but rather in the institutional frameworks that are being deployed often in incongruous contexts. Unfortunately, relatively little investment-oriented research exists on this institutional dimension—most research on African biofuels industries has focused instead on the costs and benefits of increasing biofuel production in developing countries (Gordon-Maclean et al., 2008; Kamanga, 2008; Songela & Maclean, 2008). However, Sulle and Nelson briefly described a hybrid business model as one possibility for biofuels investments in Tanzania (Sulle & Nelson, 2009). Mlingwa has argued that block farming is an ideal model for cultivation of communal village lands for energy crops in Tanzania (Mlingwa, 2009).

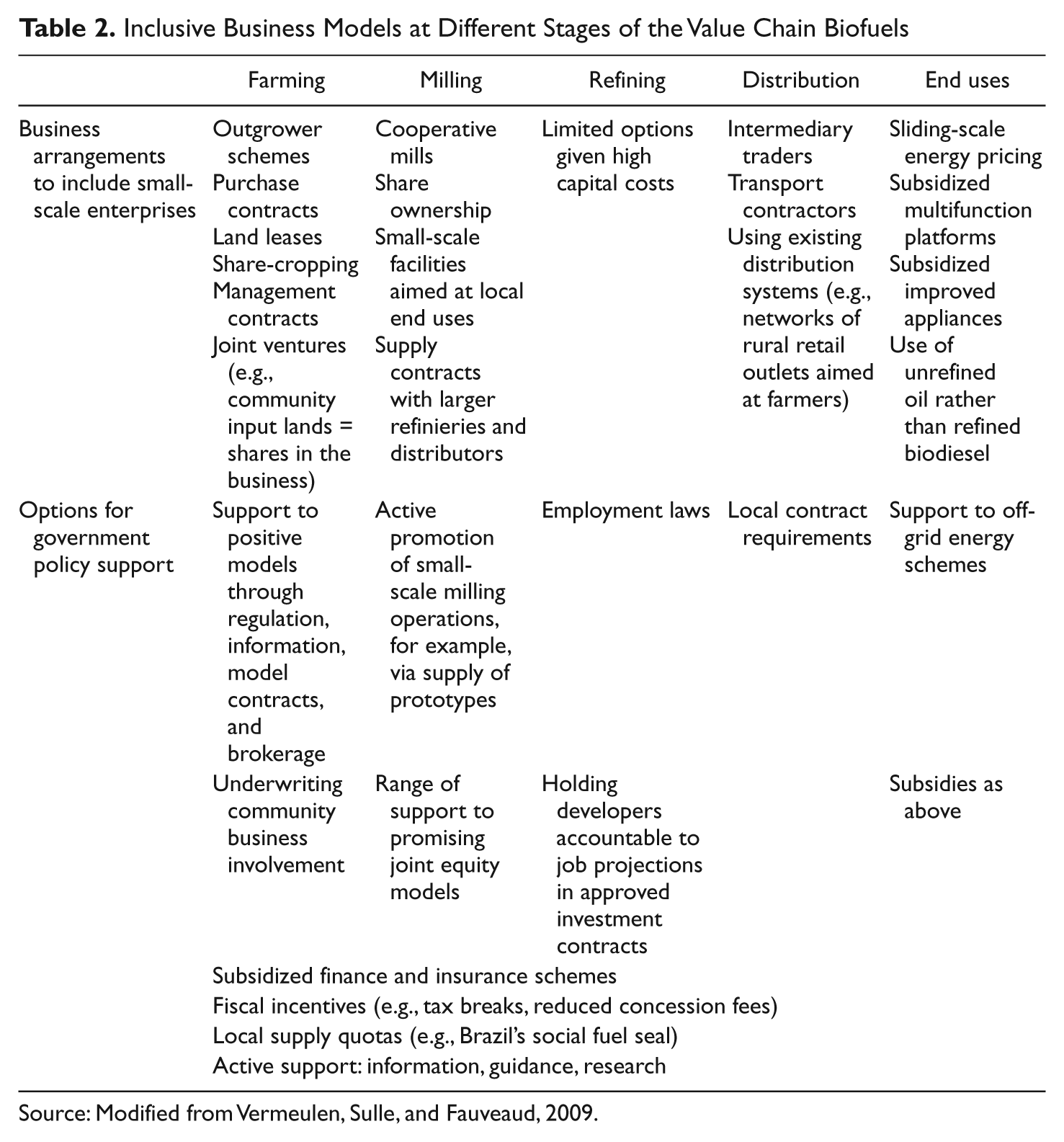

A number of international and aid organizations have investigated the benefits of alternate business models They include the UN FAO, the International Institute for Environment and Development (IIED), International Fund for Agriculture Development (IFAD), and the World Business Council for Sustainable Development—Netherlands Development Organization (WBCSD-SNV). 1 Table 2 lists a number of the suggested options, including small-scale farming, plantations, contract farming, and hybrid models. Both WBCSD-SNV and IIED suggest “inclusive business models” which include a variety of small-scale producers and enterprises (Vermeulen & Cotula, 2010). Sulle and Nelson (2009) suggested hybrid and contract business models as potentially appropriate production models in Tanzania (Sulle, 2010 in Lorenzo & Rebecca, 2010).

Inclusive Business Models at Different Stages of the Value Chain Biofuels

Source: Modified from Vermeulen, Sulle, and Fauveaud, 2009.

Plantation models involve centralized ownership and production of crops and control of the biofuels process. These systems can work well for capital-intensive crops such as sugarcane, or oil palm, and are often used in Brazil for sugarcane production. However, because about 70% of Tanzanian land is under village ownership, the Tanzanian land acquisition process presents a major difficulty to this approach. For investors to purchase or lease this land, it must be transferred from village land to general land. The process may take up to 2 years because the land for investment needs to be surveyed and villages must be given certificates of land use plans (United Republic of Tanzania, 1999).

Contract farming involves a centralized processing plant that negotiates contracts for crop delivery and is one of the major models used in the Brazilian ethanol industry. The UN FAO has vast literature on contract farming ventures (Miyata, Minot, & Hu, 2007) but in general, projects that used a contract farming model were relatively successful in the first phase of the biofuels investments in Tanzania. Contract farming has proven less successful in other places, however, underscoring a few potential deficits in this approach. The first is that it has been relatively unsuccessful at improving local farmers’ participation in multiple stages of the value chain (from distribution to the sale of final product; Rachman, Savitri, & Shohibuddin, 2009). Second, under many such arrangements, farmers are forced to adopt monoculture planting as part of the contract, limiting systemic and individual flexibility. Finally, because the prices of these crops are determined by the world market, farmers lose the ability to determine the price for which they sell their output. This can essentially reduce a land-owning farmer to a laborer, a phenomenon observed among biofuel farmers in Indonesia over the past two decades (White & Dasgupta, 2010). Third, larger and better financed companies, which can be better equipped to undertake initial investments, have been averse to contract farming when there is no proper legal framework that protects both and investors and farmers. Finally, individual farmers negotiate their contracts with companies, an often unequal bargaining situation.

A hybrid model refers not to a mix of plantation and outgrower models, but rather to a combination of large- and small-scale farming methods, offsetting some disadvantages of both systems. Resource ownership is flexible between the farmers and companies participating in the business because the different parties are not a single entity, watchdog groups and institutions can advise the partners in different ways. It retains the need for large amounts of initial capital to purchase equipment and machinery. Participants can receive both government and private financial support either individually or as part of the partnership. The hybrid model lends itself perhaps better to public–private partnerships (PPPs), because operations are heterogeneous and can be supported or operated by different entities. Through PPPs, public entities can invest in the biofuels sector, support farmers, operate mills or processing facilities, and so forth. (Sulle & Nelson, 2009). Medium-sized sugar companies that combine plantations, mills, and outgrower farming schemes have already set the benchmark for a better model of sugarcane production in Tanzania. Currently, 1,500 sugarcane outgrowers supply the 4 sugar mills in Tanzania. After sale of the final product (sugar), the outgrowers receive between 53% and 55% of the proceeds (Sulle, 2010). 2 This model has some weaknesses as well. For instance, Mwamila et al. (2009) documented complaints from outgrowers in the Kagera about the lack of transparency regarding payments and the weighing of their produce by the nucleus company. Moreover, in January 2011, outgrowers in the Morogoro region complained to their Member of Parliament (MP) about delays to their proceeds from the central operation (Balaigwa, 2011).

Weighing Alternate Business Models

Investors, local communities, and governments may all have preferences for different models. Governments may enact policies to encourage certain ones, but regulatory procedures should be flexible enough to accommodate the range of possible approaches within their territory. The choice of production model is affected by several factors. These include the number of farmers participating in the production of a particular feedstock, the land area required to produce an economical yield, the milling or processing technology required, and the capital needed to start the business. For example, some feedstocks (e.g., sugar) have large initial capital requirements, whereas others (e.g. sunflower) do not. Therefore, these two crops will require different agricultural approaches to reach maximum production efficiency: Sunflower can be produced by outgrowers, whereas sugarcane works better in a plantation model or a combination of both plantations and outgrowers.

Beyond economic efficiency, there are also social considerations for each model. Tanzanians, and other people with a memory of unreliable land tenure, may resist the plantation model because it has historically led to evictions in different parts of the country (Kamata, 2009). Inclusive business models (such as those described earlier) could be seen as more reliable protectors of farmers’ production assets. They also have the potential to give farmers more of a voice in deciding how to share the rewards and risks of biofuel production (Vermeulen, Sulle, & Fauveaud, 2009). Because of the importance and dynamism of these myriad factors, there will likely be no single model that works best for Tanzania. However, a flexible but carefully implemented policy framework could encourage biofuel investment in Tanzania that is mutually beneficial to all parties.

Policy for the Tanzanian Biofuels Industry

New Biofuels Guidelines in Tanzania

As a result of early problems encountered with biofuels investments, the National Biofuel Task Force (NBTF) was formed in 2006 and tasked with formulating a set of coherent policy guidelines for biofuels. The initial biofuels policy formulation process in Tanzania was criticized as having had inadequate participation from stakeholders such as NGOs and representatives from rural areas (Sulle & Nelson, 2009). After this process, the Ministry of Energy released the country’s official guidelines for sustainable liquid biofuels development in Tanzania in November 2010. These reforms established new institutional arrangements and requirements for investment in biofuels and the purchase of land for biofuel production.

Under the new guidelines, coordination, approval, and monitoring of biofuel investments all must be routed through and approved by the TIC. To receive approval for a project, investors must submit a complete business plan, obtain several agricultural, natural resource use, and industrial permits, and conduct both a feasibility study and an Environmental and Social Impact Assessment for the proposal. Investors must consult local, regional, and national stakeholders during the feasibility study and project planning phases and must also develop a memorandum of understanding with the relevant village authorities. Once approved, all projects receive 5-year probationary leases. If the project adequately demonstrates “investment seriousness,” the lease is extended to 25 years. Land must be used only for the purpose stated in the investor’s application and total land acquisition is capped at 20,000 ha per developer/investor. The guidelines state that biofuels investments should not cause the displacement of people, threaten food production and food security, or adversely affect the environment and biodiversity. Investments are expected to document positive contributions to the local economy, as well as the social well-being of their employees and the local population. Furthermore, the guidelines direct investors to give employment priority to local residents, and they are strongly encouraged to adopt outgrower or hybrid models of production. Finally, the guidelines require that all biofuels processing from these operations must occur within Tanzania; the guidelines lay out safety provisions for biofuel processing, transportation, and distribution, as well as provisions for waste management (see United Republic of Tanzania, 2010, for further details on these guidelines).

Although many of the principles in the new guidelines are sound, major challenges to the implementation of these regulations and to coordination between government institutions remain (Table 3). At times, the government has mentioned insufficient local funding, a lack of expertise in renewable energy and inadequate exposure as major constraints that delay implementation of the guidelines. As biofuel investments require large amounts of land, property may be transferred from village lands to general lands, placing them under control of the TIC. The TIC then gives production rights to the investor for a maximum of 25 years. Without legal clarification of who will own the land after the biofuels investor has returned it to the TIC, it is possible that villagers will lose their ownership of land. Another significant challenge is that these guidelines only address the production of liquid biofuels hence excluding solid and gaseous biofuels. Although gaseous biofuels (such as methane from biogas digesters) are not yet in place, solid biofuels currently constitute over 90% of the rural energy in Tanzania (Peter & Sander, 2009). With these guidelines in mind as a positive basis for future development, we can suggest the following enhancements to biofuels policy:

Support the existing regulatory framework: Several biofuels business models, especially contract farming, require a strong legal framework to mitigate contract risks for both investors and growers. Insufficient oversight and legal protections deny farmers their right to make informed decisions when negotiating contracts with investors. For example, Diligent Tanzania’s facilities in Arusha procure jatropha from both contracted and noncontracted farmers; however, these farmers receive little assistance from the district legal offices. In other places, farmers and companies are engaging in completely informal negotiations and agreements. The government’s legal support will be crucial to ensuring that these contracts are upheld and fulfilled, and that the rights of farmers are protected.

Situate biofuels policy in an overall energy and agricultural policy: Although there is now better guidance on biofuels specifically, Tanzania currently does not have an overarching energy policy or policy on renewable or clean energy technologies. While not a direct obstacle to development of these technologies, this may provide incentives for investors to look elsewhere until any outstanding legal questions are resolved. The managing director of Katani, who recently formed a PPP with the Tanzania Sisal Authority, explained it well, noting that “countries leading in utilization of biogas technology, such as China and Germany moved quickly and surely, because their governments push through legislation” (Sembony, 2010). This is another example of how the Tanzanian government has lagged behind the renewable energy and biofuels industries. By contrast, Mali worked with international NGOs to help local communities generate their own energy. The Tanzania Rural Electrification Agency (REA) can likewise work with local communities ready to initiate generation projects, although it has not yet pursued such partnerships.

Expand research and development: Part of the successful experience in both Brazil and South Africa derived from the creation of a domestic technical capacity through an active R&D program. During the past year, the Tanzanian government has set a goal of devoting at least 1% of GDP for research activities by public and private institutions as well as individuals (Sulle, 2010). However, the contribution of local universities to biofuels R&D remains low due to the lack of resources for both funding and personnel, and there is little prospect that this will change soon. The Ministry of Energy and Minerals has stated that this lack of R&D is a problem, which needs to be addressed for the country to reach its desired goals in energy industry (United Republic of Tanzania, 2003). For example, there is still insufficient data to indicate which models of business or production are suitable in the country. The government, through the permanent Secretary for the Ministry of Agriculture, announced plans to survey areas suitable for biofuels investments in the country, which should help to fill this knowledge gap (Philemon, 2010). However, this needs to be paired with empirical studies of different biofuels business models to determine ideal combinations for Tanzania. Embedding innovation and research in Tanzania’s economic agenda could help it tap into evolving multilateral initiatives on climate and development finance that are targeted to sustainable energy.

Embed biofuels policy into a wider economic agenda: One dimension of Brazil’s success was its ability to generate a domestic capacity to supply technology, expertise, and capital. The current economic growth rate in Tanzania has been achieved largely by foreign direct investment in the country. In the past, there have traditionally been poor linkages between the local and central economies; most recently, debates on this topic have emerged in the mining and tourism sectors. The same activities that have propelled Tanzania as a tourist destination have also spurred ever-increasing evictions, resulting in conflicts around the country (Igoe & Croucher, 2007). Curtis and Lissu (2008) indicated that Tanzania is losing investment benefits from large mining multinational corporations while at the same time evicting communities in rural areas. These experiences make communities suspicious of foreign investment in the country and inhibit the development of support for potentially useful projects. However, reframing biofuels as a locally driven economic initiative could help domestic actors retain both the initiative and potential financial development benefits.

Focused and strategic crop identification: Other biofuels transitions show that human and technical capacity increase in cases where there is a focused technology system based on an appropriate feedstock. While the government may wish to avoid “picking winners,” it may help the government to ensure that farmers are able to grow crops suitable for their region. Currently, regions that receive significant rainfall year-round continue to grow jatropha, even though they could be earning a substantially higher income from high-yield energy crops such as palm oil, sugarcane, or sunflower. Partially because the pace of zoning decisions has been so slow, farmers are growing less productive feedstock crops that are not cost-effective when compared with their other options. On the consumer side, food security could become a major concern with biofuels development. Therefore, the merits of each feedstock in specific contexts will require careful evaluation from a technical standpoint as well as a conversation with local communities about appropriateness. This is a role that the government can facilitate.

Weigh export markets against building domestic demand: Questions often arise as to how much production to steer toward domestic uses, but past experience does not provide definitive guidance. Brazil, for example, based its entire biofuels expansion on domestic demand, but occasionally at great cost to the central government. There some trade-off, moreover, between energy security and export revenue: by exporting more biofuels, Tanzania can increase its foreign exchange holdings beyond its current reserves of US$3.8 billion (United Republic of Tanzania, 2011), most of which are currently lost in the purchase of petroleum products. In 2009, because Tanzania does not produce any oil itself, the country was importing roughly 34.00 thousand barrels (bbl) per day (US Energy Information Administration, 2010) or roughly 12 million bbl per year. Without a clear plan for cultivation of domestic research and technical capacity, a goal of simply increasing biofuel production is less likely to lead to the long-term viability of an export-oriented biofuels industry.

Targeting National Biofuels Policies to Common Problems

Note: TIC = Tanzania Investments Centre; GDP = gross domestic product.

Conclusion

The experience with biofuels production in Tanzania so far is mixed at best, and the Tanzanian governments’ current biofuels’ guidelines do not sufficiently address key challenges highlighted in the present analysis. Nevertheless, a moderate development of biofuels’ capacity could contribute to Tanzania’s economic well-being, energy security, and sustainable energy trajectory. This is suggested by the more positive experiences of other countries within the region and in other parts of the world. Yet with a shaky policy foundation, developing the biofuels’ industry in Tanzania will be a challenging task. To make a positive outcome more likely, the government must build on its existing policy guidelines and establish a stronger legal framework, embedded in a more comprehensive energy and agricultural policy. It must also attempt to more systematically leverage international funding for research and development into biofuels.

The choice of feedstock and business model used for producing biofuels will have a significant effect on the ultimate success of any given project. Careful assessment of geographic characteristics, land availability, and labor migration patterns will be a helpful contributor to public and stakeholder engagement. Significant R&D beyond what the government has already devoted to biofuels could enhance the domestic capacity and create a self-sustaining technical infrastructure. Research should also focus on standard agricultural issues such as feedstock performance and should also gather better data on overall biofuel operations within the country to help identify possible places for new investment.

Regulations for zoning and irrigation schemes can ensure that water is distributed sustainably and with appropriate allocations to different stakeholders. Zoning and permitting procedures could address concerns about low-yield biofuel crops displacing food crops on highly productive land. Finally, for the biofuels sector to function fairly and equitably, investors and communities will need a strong legal framework for contracts to function properly and for citizens’ rights to be protected throughout the production process. For example, the best business models respond to the challenges of resource ownership, ensuring equitable input from all partners, and the distribution of project risks and benefits. For this to happen, local communities will also need to develop bylaws or other locally accepted procedures for evaluating and processing contracts and land deals to protect themselves.

However, these recommendations alone are not enough. For negotiations to take place in good faith, farmers and rural communities must also develop the capacity to understand the legal frameworks that have been developed and be able to understand of their legal needs and opportunities. On this front, a simple exhortation toward “education” does not ensure that the recipients of information will actually benefit. Further research can examine specifically how local governments can work with citizens to achieve the goal of more equitable negotiations between locals and investment corporations. Possible solutions include the development of informational literature, media campaigns, and technical workshops organized for local stakeholders looking to become involved in the biofuel industry. Building a sustainable industry will require contextualizing the biofuels policy as a component of a wider energy policy, support of domestic technical capacity, and an institutional and legal framework that can resolve disputes over business approaches and potential trade challenges in this growing industry.

Footnotes

Acknowledgements

The authors are grateful to Rebecca Gasper and Dylan Rebois for comments on earlier drafts, to Volha Roshchanka, and to five anonymous reviewers for helpful comments.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.