Abstract

We examine the influence of property tax delinquency on the sale price of nearby homes from 2002 to 2013 using more than 46,000 residential property sales in a representative midwestern central city—Milwaukee, Wisconsin. After controlling for a number of property and neighborhood characteristics including nearby foreclosures, we find property tax delinquency has a significant influence on nearby home sales. The relationship is negative; one additional tax delinquent property within 250 m of a home sale is associated with a discounted sale price of 0.79% or approximately $1,085 on average. In addition, the influence of tax delinquent properties on home sale prices diminishes with distance, suggesting blight is the source of the discount. Based on these findings, the negative influence of tax delinquency is likely to be exacerbated in central cities where housing density is greater and delinquency is higher and more persistent than the surrounding suburbs, which has the potential to lead to fiscal distress as property taxes are the primary revenue source for cities. As such, we suggest a two-tiered approach for cities to mitigate the negative consequences of tax delinquency: a combination of policies to eliminate delinquency and also to help homeowners become financially stable.

Introduction

Recent studies of the housing market have focused much attention on foreclosures. At the heart of this research is the effect of foreclosed properties on the value or sale price of neighboring homes. There are two possible mechanisms at work with regard to foreclosures. Most visibly, completed foreclosures can lead to vacant or abandoned properties that have negative impacts on neighborhoods. To the extent that a foreclosure-induced vacancy leads to a lowering of neighborhood quality, one would expect surrounding house prices to decline. Alternatively, being in the process of foreclosure may signal homeowner financial distress, in which case homeowners may choose to stop maintaining their homes, as they believe losing their homes to be inevitable. Such decline in the outward appearance of occupied homes in a neighborhood can also contribute to neighborhood decline and lower surrounding home prices. The policy implications of this research are apparent given the recent housing crisis.

However, along with Alm et al. (2016) and Whitaker and Fitzpatrick (2013), we believe that neighborhood decline and depressed market values of homes can occur separate from the foreclosure process. No less important, but significantly less studied, is the influence of property tax delinquent properties. The expected influence of these types of properties on surrounding home sales is similar to that of foreclosed properties. Due to occupancy, property tax delinquency may not be visible from the street, and homeowners in the neighborhood or prospective buyers are unlikely to devote the time to ascertain the tax delinquency status of nearby properties. But, tax delinquent homeowners are also likely to be unable or unwilling to maintain the outward appearance of their homes for the same reasons as those associated with foreclosures. Tax delinquency may signal homeowner financial distress or, regardless of the homeowner’s financial status, the probability of seizure may be high. Both can lead to property blight and lower neighborhood quality. 1 However, we argue these effects are distinguishable from those of bank-initiated foreclosures and can occur before the tax foreclosure process begins. As such, the purpose of this study is to examine the influence of tax delinquent properties on nearby residential sale prices. There is a significant gap in the literature regarding these types of properties and their impact on housing values. Currently, we know of only two other studies that examined this correlation (Alm et al. 2016; Whitaker and Fitzpatrick 2013).

As a legacy of the urban crisis of the 1960s, property tax delinquency presents a persistent and pervasive problem for central cities. For many years, the blight associated with tax delinquency and other forms of distressed properties plagued central cities and presented an impediment to neighborhood revitalization. We examine this phenomenon using housing sale price data merged with the master property file for the City of Milwaukee, Wisconsin, from 2002 to 2013; we are able to estimate the correlation between residential sale prices and nearby tax delinquent properties, while controlling for nearby foreclosed properties. In addition, we estimate the influence of tax delinquent properties at various distances from the property sale, allowing us to determine whether proximity is an important factor. As we hypothesize, our results reveal negative correlations with coefficient magnitudes within range of existing literature on foreclosures. Similar to the foreclosure literature, the strength of the relationship between delinquency and sale price is a function of distance. The closer the tax delinquent property is to the sale property, the larger the magnitude of the sale price discount.

This article proceeds as follows. In the next two sections, we examine the previous empirical literature pertaining to the neighborhood effects of foreclosures and other types of residential disinvestment. Then we provide an overview of the data and present our econometric model, followed by our results, and finally, we conclude and discuss policy implications.

Previous Research on Distressed Properties

The vast majority of the empirical literature examining the relationship between nearby distressed properties and housing prices focuses on bank-initiated foreclosures. Although these studies are not exactly relevant to our research question, they do provide a theoretical basis for how nearby distressed properties may influence house prices. Overall, these studies (discussed below) conclude that nearby properties in bank-initiated foreclosures reduce sale prices; however, the physical proximity of a home to a foreclosed property that is required to reduce the sale price varies across the studies.

Theoretically, there are three potential mechanisms by which foreclosed properties could influence the sale price of surrounding properties (Lee 2008). First, and the most common justification, is the potential blight from foreclosed properties. Homeowners in any stage of the foreclosure process are likely to be in some form of financial distress, potentially leading to a lack of upkeep on their home. This outward degradation of the home can lead to declining neighborhood quality and depress surrounding values. After foreclosure, homes are typically abandoned and may attract further blight through crime or vandalism (Ellen, Lacoe, and Sharygin 2013) as the broken windows theory would predict. Second, foreclosed homes typically sell at a discount (Campbell, Giglio, and Pathak 2011) and residential properties are typically valued on the basis of neighborhood comparables. The presence of below market value comparables may get capitalized into surrounding properties and depress their values (Whitaker and Fitzpatrick 2013). Finally, the presence of a large number of foreclosures in a market may increase the supply of housing. This increase in housing supply can depress sale prices in the market when demand is currently being met (Lee 2008).

Although the theoretical underpinnings are rather straightforward, empirical analysis of the influence of foreclosed properties on nearby home sales is quite disparate in its use of data and methods. In general, these analyses examine the number of foreclosures over a given time period (six months to multiple years) within a certain distance band from the property (250-3,000 ft.) with varying empirical methods. The general consensus in the literature is the presence of an additional nearby foreclosed property leads to approximately a 1% to 2% discount in the sale price (Harding, Rosenblatt, and Yao 2009; Immergluck and Smith 2006; Leonard and Murdoch 2009; Rogers and Winter 2009; Schuetz, Been, and Ellen 2008). However, there is variation in effect sizes across the literature. A few studies find discounts of less than 1% (Groves and Rogers 2011; Wassmer 2011), and additional studies find effect sizes of greater than a 1% to 2% discount. Using recent data on Chicago housing prices, Lin, Rosenblatt, and Yao (2009) found the impact of foreclosures within 0.9 km (approximately 2,700 ft.) on house prices is approximately an 8.7% discount. This effect dissipates over time, declining to between a 1.7% and 4.7% discount when the foreclosure is liquidated within five years. Very recently, a study using quantile regression suggests the influence of foreclosures is largest among low-priced homes (0.25 quantile) located within 250 ft. of the foreclosed property and within 12 months of foreclosure (Zhang and Leonard 2014). Although the approach is new, the results reinforce the findings from the previous literature discussed above.

To our knowledge, only two academic studies have directly examined the influence of property tax delinquency on surrounding house prices, and two additional studies include property tax delinquency as a control variable; three use Cleveland, Ohio, as the study area, and one uses Chicago, Illinois. Examining 12,100 single-family and duplex home sales from 1992 to 1994, Simons, Quercia, and Levin (1998, p. 154) defined property tax delinquency as “the percentage of housing property within 1-2 blocks over 15% delinquent on property taxes.” They found a 1% increase in their tax delinquency variable leads to a $788 decrease in the sale price of a nearby home. In a similar study, Ding, Simons, and Baku (2000) examined the same variable for 7,751 single-family home sales in 1996 and 1997. They found a smaller effect than Simons, Quercia, and Levin (1998), with a 1% rise in tax delinquency leading to a $162 to $198 sale price discount. However, property tax delinquency is not the main focus of these two studies. Examining Chicago, Alm et al. (2016) found an additional tax delinquent property with a tax lien (sold or unsold) within the Census block of a property sale to be associated with a 2.7% to 2.8% decrease in the sale price. This is equivalent to a $6,600 discount on the sale of the average home in their data. Alm et al. (2016) also found the influence of foreclosed properties within the Census block of a property sale to be much larger than tax delinquency: approximately, a 20% decrease in the sale price for every 1% increase in the foreclosure rate. 2

Whitaker and Fitzpatrick (2013) examined the interactive effect of tax delinquency, foreclosure, and property vacancy in Cleveland for property sales in 2010 and 2011. This analysis is unique among the foreclosure literature by examining the interactive effects of tax delinquency, foreclosure, and property vacancy. To our knowledge, no other analysis has taken this approach. For each measure, they examined the count of delinquent properties within 500 ft. of the sale. They found that an additional tax delinquent property within 500 ft. is associated with a 1.5% decrease in the sale price. This is slightly lower in high-poverty areas (0.8%) and higher in low-poverty areas (2.5%). This is compared with a 4.7% discount for foreclosed properties. The influence of foreclosed properties is not statistically significant in high-poverty areas and is larger (7.4%) in low-poverty areas. In the full sample, the total interactive correlation (Delinquent × Foreclosed × Vacant) is not statistically significant. In high-poverty neighborhoods (greater than 20% poverty rate), the total interactive influence is approximately a 25% decrease in the neighboring sale price.

Are Tax Delinquency and Foreclosures Different?

We aim to contribute to the distressed properties literature in a particular way. We focus specifically on the correlation between property tax delinquency and home sales. Property tax delinquency is an indication of homeowner financial distress (insofar as the delinquency is not strategic) and thus shares some commonality with the mortgage foreclosure literature referenced above. However, as Whitaker and Fitzpatrick (2013) noted, property tax delinquency must be understood separately from bank-initiated foreclosures, because the processes are different in that foreclosures rarely go into tax delinquency. Lenders and mortgage service providers typically continue to pay property taxes for mortgaged homes in default to prevent a municipality from placing a lien on the home that supersedes the mortgage to protect their asset (Whitaker and Fitzpatrick 2013). So, yes, the practical influence of property tax delinquency and bank-initiated foreclosures is expected to be different.

Theoretically, however, the two situations share a common broken windows narrative. The homeowner who is delinquent on his or her property tax liability is likely to be in some form of financial distress. This reason for the inability to pay his or her property tax bill is also likely to prevent the homeowner from affording the maintenance required to keep the outward appearance of the home in proper order. Similarly, if the homeowner perceives the probability of exiting from delinquency to be low, he or she may forgo maintenance until the home is seized by the bank or taxing jurisdiction. Regardless of the motivation, this outward projection of the homeowner’s financial distress leads to blight that may reduce home values in the surrounding area. The density of the surrounding area will dictate how many homes will be affected by a blighted property. In urban areas where housing density is at its highest, a great number of properties are likely to be affected by a single blighted property.

Depressed sale prices of tax delinquent properties may also drive down the price of surrounding home sales through capitalization. Two possibilities can occur. First, the tax delinquent property is seized by the taxing jurisdiction in which it is delinquent. The jurisdiction sells the property at auction with little regard for capturing the full market value of the property, only the value required to pay the outstanding taxes and accrued interest. This reduces the sale price and may be capitalized into the real estate market through comparables as previously discussed. Second, the value of the tax delinquency itself is likely to be capitalized into the value of the home. Property tax delinquency follows the property rather than the owner. If the property is sold to a new owner, the new owner will likely demand a lower price to be compensated for having to pay outstanding taxes and accrued interest to remove the delinquency status on the property. This will lower the sale price and may lower neighborhood sale prices, again through comparables valuation. The latter is the likely mechanism for our sample of home sales because both the city and county of Milwaukee use the “in rem” foreclosure process by which they sell the tax foreclosed property at full market value rather than the value of the tax delinquency. 3

Although theoretically similar, the practical implications of property tax delinquency are distinct from bank-initiated foreclosures (Whitaker and Fitzpatrick 2013). Yet, very few studies have analyzed this subset of distressed properties empirically to determine such influence. Therefore, we contribute to the broader literature of the effects of neighborhood quality and homeowner financial distress on nearby home sales by focusing on the influence of nearby delinquency rather than mortgage foreclosure. Next, we define “nearby” and discuss the data and variables used for analysis.

Data and Method

As is typical in these analyses, we specify a log-linear hedonic pricing regression model (Rosen 1974) where the natural log of sale price is regressed on a vector of characteristics of the home and its location, including nearby property tax delinquency and likely foreclosures. 4 We estimate the following model:

where lnP is the natural log of the home sale price, X is a vector of individual home characteristics identified from the literature along with a series of n − 1 dichotomous variables indicating the sale month, D is a count variable identifying the number of tax delinquent properties at various distances from the home sale, F is a count variable identifying the number of likely foreclosed properties at various distances from the home sale, η is zip code–level fixed effects to control for characteristics of the neighborhood within which the sale property is located, γ is year fixed effects to control for the influence of the housing market crash and Great Recession, and ϵ is the usual error term. Complete descriptions of all variables are provided in Table 1.

Variable Descriptions.

We are particularly interested in the sign and magnitude of the δ in equation 1. Consistent with previous literature, we hypothesize δ to be negative, indicating an inverse correlation between home sale price and the number of nearby tax delinquent properties. We make no prediction for the magnitude of correlation between tax delinquent properties and sale prices. However, consistent with previous research, we do expect that the magnitude of the sale discount will decline with increasing distance of tax delinquent properties. An important consideration in this model is capturing the relative influence of tax delinquency separate from bank-initiated foreclosure. To do so, we include the number of nearby likely foreclosed properties, as well as an interaction between the number of delinquent and likely foreclosed properties, all at the same distance bands surrounding the sale property. In keeping with the previous literature, we hypothesize θ and ρ to be negative.

Data

All data come from the City of Milwaukee, Wisconsin, and are publicly available from the City’s website (city.milwaukee.gov). The first data source reports the date and price of all residential property sales that occurred citywide from 2002 to 2013, along with limited information about the property characteristics and neighborhood location. A unique taxkey number identifies each property parcel. The second data source is the City of Milwaukee Master Property File, which is an annual inventory of all property parcels in the city dating back to 1975. Each property parcel in this database is also identified by the same unique taxkey number used in the property sales data, which we used for merging relevant data from both sources. This second database, however, provides significantly more information on property assessments, property characteristics, and neighborhood location. We use this second data source for three primary purposes: (1) to add variables measuring the home characteristics of sale properties to the first dataset, (2) to measure tax delinquency near the sale properties, and (3) to measure likely bank-initiated foreclosures near the sale property.

Using geographic information system software, we draw a circle around each home sale at various radii. For this analysis, we use four different distances: 250, 355.55, 500, and 707.11 m from the home sale. 5 We then count the number of tax delinquent, likely foreclosed, and both tax delinquent and likely foreclosed parcels inside each circle. This strategy allows for a number of possibilities in terms of estimation. At the most basic level, it allows us to estimate the influence of nearby tax delinquency on property sales at various distances. Second, it allows us to follow the trend in the literature and calculate distance bands around the sale of a property (Harding, Rosenblatt, and Yao 2009; Immergluck and Smith 2006). We expect the influence of a tax delinquent property on the sale price of a home to vary inversely with its distance from the sale home. Specifically, we expect the negative influence of tax delinquent properties to be the strongest when the distance from the sale home is the smallest. And, as the distance from the sale home increases, we expect the magnitude of the negative correlation to decline.

Similar to other urban areas, property tax delinquency is not an uncommon phenomenon in Milwaukee. The property tax delinquency rate was 6.5% in 2011. 6 Between 2005 and 2009, the average property tax delinquency rate for Wisconsin cities was 2.5% (Waldhart and Reschovsky 2012). Among peer cities identified by the City of Milwaukee Comptroller, 7 the average property tax delinquency rate was 11.84% in 2011 and the median delinquency rate was 7.87%. By comparison, the City of Detroit, Michigan, had an estimated property tax delinquency rate of 47% in 2011 (MacDonald and Wilkinson 2013). Tax delinquent parcels are identified by the City of Milwaukee. Under Wisconsin state law, property tax bills must be mailed by the third Monday of December for the next tax year (Olin 2013). Assuming the taxing jurisdiction does not have multiple installment payments, taxes must be paid by January 31 or in two installments due before January 31 and July 31. Property taxes become delinquent if the tax payment is not received within the five-day grace period established under state law. In the case of Milwaukee, property taxes are either due in full before January 31 or in 10 equal installments due before the end of each month, January through October. A taxpayer may have one late payment without forfeiting the installment option. A second late payment will trigger a delinquency with the entire tax bill due on the first of the month after the missed payment. Under Wisconsin state law, delinquent taxes accrue interest at 1% per month, and if taxes are unpaid for two years or more, the property can be sold at auction to recover the lost taxes and accrued interest.

Identification of likely foreclosed properties follows the recent literature by utilizing property ownership records (Ellen, Madar, and Weselcouch 2014; Immergluck 2012; Immergluck and Law 2013). First, all parcels are classified by their ownership into lenders (banks and other financial institutions as well as government-sponsored entities) and nonlenders (private individuals and corporate entities). 8 Second, changes in ownership records are recorded. A likely foreclosed property is identified when the ownership of a parcel changes from the name of an individual to a bank- or government-sponsored enterprise. A parcel is no longer considered foreclosed if the ownership record reverts back to a nonlender. 9 A property that is both tax delinquent and likely foreclosed is recorded by comparing tax delinquency records with likely foreclosure data.

Methodology

Our dependent variable is the natural log of the sale price of each individual property. Although these data are reported over a 12-year time period (2002–2013), the data are not considered a panel because properties only appear in the database when they are sold, which are most frequently only once. Our data are a pooled cross-section, so we are not able to apply panel data methods for analysis even though our observations occur over time. As such, we use ordinary least squares (OLS) regression, but all estimations include year fixed effects and Huber–White sandwich standard errors. All of the housing and neighborhood characteristics are measured in the same months and/or years of the property sales as appropriate. The variables measuring nearby delinquency and likely foreclosure are measured according to assessment year, which occurs in the year before (t − 1) the year of sale. 10 We are particularly interested in whether the prevalence of tax delinquent parcels in the area surrounding a home sale is associated with a discounted sale price. The one-year lag of tax delinquency suggests that parcels identified as delinquent last year might influence the sale price of proximate residential properties this year. The lagged structure of our data also helps to eliminate the potential simultaneity bias between home prices and tax delinquency (Harding, Rosenblatt, and Yao 2009).

Results

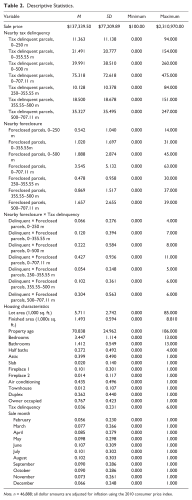

Table 2 provides descriptive statistics for our variables. As shown in Table 2, the average selling price of a residential property in the City of Milwaukee during 2002 to 2013 was $137,339.50. The sale prices ranged significantly from a minimum of $100 for vacant land classified as residential, to upward of $2.3 million for a home overlooking Lake Michigan. With a standard deviation of $77,209.89, however, sales of multimillion dollar homes were certainly the exception. Most of the residential property sales that occurred throughout the city consisted of single-family homes at prices accessible to middle- and upper-middle-class homebuyers. Further evidence of the types of homes sold is found in the descriptive statistics for the remaining housing characteristics. On average, most sales consisted of detached single-family homes with three or four bedrooms, 1.5 to 2 bathrooms, which often had amenities like attic spaces, full or partial basements, fireplaces, and air conditioning. Most of these homes were occupied by their owners and had very low rates of tax delinquency. Unsurprisingly, these home sales were most likely to occur in the late spring and summer months. In addition, the data in Table 2 reflect the well-established housing stock of an older rustbelt city like Milwaukee, with the average homes sold having been built around 1940.

Descriptive Statistics.

Note. n = 46,888; all dollar amounts are adjusted for inflation using the 2010 consumer price index.

Table 2 also provides information pertaining to the prevalence of tax delinquency in the area surrounding the sale properties. On average, we observe approximately 11 tax delinquent properties within a 250-m radius of a home sale, an additional 19 tax delinquent properties 250 to 355.55 m away from the sale, an additional 18 properties 355.55 to 500 m away from the sale, and an additional 35 tax delinquent properties 500 to 707.11 m away from the sale on average. However, these statistics vary a good deal with some home sales having virtually no exposure to nearby tax delinquent properties, while other sales occurring in areas heavily saturated with tax delinquency. Spatially, this can be seen in Figure 1. Each point in Figure 1 indicates a tax delinquent parcel at any time over our 2002 to 2013 time period. In areas to the north and south on the map, tax delinquency is only a sporadic phenomenon. However, as one moves toward the center of the map (closer to downtown and the poorer inner city neighborhoods), the level of tax delinquency noticeably rises.

Tax delinquent parcels, City of Milwaukee, 2002 to 2013.

Foreclosures are a rare occurrence in our data with the average sale experiencing less than one like foreclosure within 250 m of the property. However, there is significant variation in the prevalence of likely foreclosures with some sales experiencing zero foreclosures nearby and others seeing as many as 63 likely foreclosed properties within 707.11 m of the sale. Properties that are both tax delinquent and likely foreclosed are even rarer with the average sale experiencing virtually no such properties. However, the spatial variation in such properties is high with some sales seeing as many as 11 tax delinquent and likely foreclosed properties nearby.

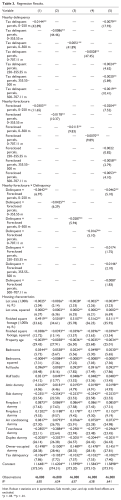

Table 3 provides a series of regression results. Again, all of the models shown in Table 3 were estimated using OLS regression with Huber–White robust standard errors and month, year, and zip code fixed effects. The dependent variable for each regression model is the natural log of sale price in 2010 constant dollars. 11 Model 1 includes only the number of tax delinquent, likely foreclosed, and both delinquent and likely foreclosed parcels within 250 m from the home sale. Models 2, 3, and 4 increase the distances from the home sales over which tax delinquent parcels are observed. These distances are 355.55, 500, and 707.11 m, respectively. Model 5 presents the full estimation, with distance bands of 0 to 250 m, 250 to 355.55 m, 355.55 to 500 m, and 500 to 707.11 m. Although we believe the results from Model 5 are most appropriate, we offer the other models for comparison purposes and robustness checks. Model 5 is statistically significant overall (F = 927.18) at the 99% confidence level and explains 64.1% of the variation in residential sales prices in Milwaukee during 2002 to 2013. We report these statistics; however, it should be noted that our analysis is of the entire population of residential home sales in Milwaukee during the time period, and does not constitute a sample.

Regression Results.

Note. Robust t statistics are in parentheses; Sale month, year, and zip code fixed effects are excluded.

p < .05. **p < .01.

The results pertaining to housing characteristics conform to expectations in all models. According to the results in Table 3, older properties, having a slab as opposed to a full or partial basement, shared housing in the form of townhouses and duplexes as opposed to detached single-family homes, and tax delinquency of the seller are all associated with lower sale prices. In terms of magnitude, the lacking of a full or partial basement and the style of attached/shared housing have the largest negative correlations with sale prices, while older homes exert the least negative influences.

However, more full and half bathrooms, along with amenities like attic spaces, fireplaces, and air conditioning all contribute to higher sales prices of homes as expected. Housing sales during the summer and early fall months also elicit higher sales prices. Finally, as expected, owner-occupied housing is associated with higher sales prices and elicits the greatest correlation in terms of magnitude among these variables. Finally, when it comes to a home sale, the old adage of “size matters” certainly applies here, although bigger is not necessarily better. Property size is generally considered nonlinear, because its relationship to market value is highly dependent on the demand for housing stock at the time of a home sale (Carroll 2008). So, we include variables measuring a sale home’s lot area, finished square footage, and number of bedrooms along with squared terms of each to account for the nonlinear nature of these variables when it comes to sale prices. All of these variables display results as expected. The lot area and finished square footage variables show demand for smaller properties and houses, which is commensurate with the age of the housing stock in Milwaukee and that of property sales in our sample. In addition, the results indicate that houses with more bedrooms sell for higher prices, but only up to some optimal point at which having too many bedrooms in a house works against market demand and leads to lower sale prices.

Turning to the primary focus of this analysis, Model 5 in Table 3 shows the full results pertaining to nearby tax delinquency, likely foreclosures, and the interaction of these two variables. The results are consistent with our hypothesis of a negative correlation between nearby tax delinquency and residential sales price. According to the results, one additional tax delinquent parcel within 250 m of a home sale is associated with a sale price that is 0.79% lower on average. In real terms, these findings suggest that if a single homeowner on a city block becomes delinquent on his or her real estate taxes owed for last year, when another homeowner on the same block puts his or her house on the market, it will sell for $1,085 less on average. Our results suggest that greater distances between home sales and tax delinquent properties have diminishing influences on discounting the sale prices of homes. For properties within the range of 250 to 355.55 m of tax delinquent parcels, one additional property tax delinquency is associated with a 0.24% or $330 lower sale price on average. An increase in one delinquent property between 355.55 and 500 m from a home sale is correlated with a 0.20% decrease in sale price, leading to a decline of $275. Last, an increase in one delinquent property between 500 and 707.11 m from the home is associated with a decrease in sale price of 0.19% or $261 on average.

Because the variables are measured exactly the same, the results for tax delinquency can also be directly compared with those of likely foreclosed properties. On average, a single likely foreclosure increase within 250 m of a sale leads to a 2.04% decrease in sale price or roughly a two and a half times larger size effect than tax delinquency within the same distance. In dollar terms, an additional likely foreclosed property within 250 m is associated with approximately a $2,800 decline in sale price. This result is smaller but consistent with Whitaker and Fitzpatrick’s (2013) findings; however, it is somewhat larger than previous results examining only foreclosures, suggesting that excluding tax delinquent properties is a source of omitted variable bias in these analyses. Similar to tax delinquent properties and the foreclosure literature, broadly, the influence of likely foreclosed properties declines with distance, but maintains approximately a two to two and a half times larger size effect than tax delinquency. Finally, the most distressed case in our data, tax delinquent and likely foreclosed, has the largest size effect with a one-parcel increase within 250 m of a sale being associated with a 4.62% decrease in sale price. This size effect is much larger than that found by Whitaker and Fitzpatrick (2013).

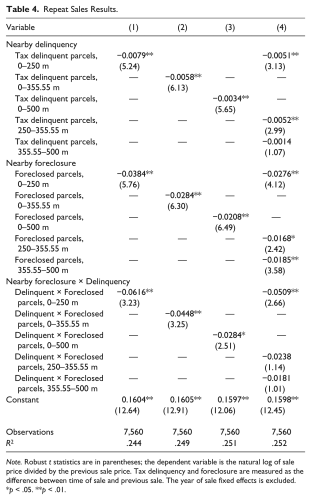

As a robustness check, a repeat sales model is specified using the data outlined above. We estimate the model as follows:

This specification is similar to that of Alm et al. (2016) where the log ratio of the most recent price (Pt) to the previous price (Pt−1) is a function of the difference in delinquency (D), foreclosures (F), and foreclose and delinquent (D × F) properties over the same time period. In addition, year fixed effects are included. This method can be viewed as superior to the OLS specification above because it more effectively controls for time invariant factors.

In our preferred specification (Model 4 in Table 4), the point estimate for tax delinquent parcels within 250 m is negative but smaller than that found in Table 3. In addition, the effect diminishes faster as distance increases with no statistically significant effect after 355 m. The results for likely foreclosed properties are similar to those in Table 3. The results for the most distressed case, delinquent and foreclosed, are somewhat larger than the OLS results and diminish much faster with distance. Overall, the repeat sales results reinforce the previous findings of a negative and spatially declining influence of property tax delinquency from the hedonic model specific above.

Repeat Sales Results.

Note. Robust t statistics are in parentheses; the dependent variable is the natural log of sale price divided by the previous sale price. Tax delinquency and foreclosure are measured as the difference between time of sale and previous sale. The year of sale fixed effects is excluded.

p < .05. **p < .01.

Conclusions and Policy Implications

The purpose of this research was to examine the influence of nearby tax delinquent properties on the sales prices of homes in the City of Milwaukee, Wisconsin. Our findings suggest that this influence is negative, discounting the sale price of a home by 0.19% to 0.79% or an average of $261 to $1,085 with the addition of one tax delinquent property depending on its distance to the sale property. It is important to note that this effect is the result of only a single nearby homeowner becoming tax delinquent, so the total aggregate influence of nearby tax delinquency could potentially be much greater for homeowners trying to sell. As the total level of nearby tax delinquency rises, so too does the cumulative negative effect on nearby home sales prices. Furthermore, urban housing densities tend to make the total impact of tax delinquency quite high for homes in high-delinquency neighborhoods. Our findings of a decline in the negative influence of tax delinquency on a home sale price as distance between the two increases suggests that visible blight is the primary mechanism at work, which is similar to that of foreclosed properties and in line with the broken windows theory.

This research presents a number of unique contributions to the distressed property literature. First, our long time period for analysis is uncommon in the literature. In our assessment of the literature, only one study (Campbell, Giglio, and Pathak 2011) utilizes data over a time period longer than two years. This long time period allows us to observe multiple market conditions and decreases the likelihood that our findings are the result of a particular real estate market condition (primarily the housing crash associated with the Great Recession). Second, our focus on property tax delinquency, a similar yet unique form of financial distress from mortgage foreclosure, expands the literature on distressed property owners. In our data, bank-initiated foreclosures ebb and flow with the business cycle. Yet, similar to what others have observed about central cities, the level of property tax delinquency is higher and more persistent (i.e., stable over time) than its suburban counterparts. 12 Our results suggest that while the marginal effect of tax delinquency is smaller than foreclosure, the total effect may be much higher given the relatively higher prevalence of tax delinquency and present a unique problem for central cities.

From a practical standpoint, our results imply that tax delinquency poses a problem for city governments. The first-order problem of tax delinquency is a problem of timing. Nearly 100% of current or delinquent property taxes are collected in the long run, but delinquency sometimes requires the long process of foreclosure and resale to recoup owed taxes. Each step in this process takes time and can lower annual property tax collections substantially. Our analysis also suggests a second-order problem whereby tax delinquent properties lower the market values of nearby homes. And, this negative influence occurs separate from the impact of foreclosures on home sales, which is the point at which nearly all of the academic research has been focused to date. If assessed values are determined on the basis of market value or some fraction of market value, as is the case in most cities, the discount of home sale prices resulting from tax delinquency further erodes the local property tax base. In the extreme, this outcome can lead to a financial crisis similar to what Detroit, Michigan recently experienced. However, even moderate levels of tax delinquency like that experienced by Milwaukee and many other central cities, through the two mechanisms identified above, combined with urban housing densities that exacerbate the second-order effects have the potential to erode the property tax base to a point of triggering a fiscal crisis. To our knowledge, the possibility of such a delinquency-induced fiscal crisis is a gap in the literature on urban fiscal health and should be explored in future research.

As Whitaker and Fitzpatrick (2013) note, it is easy for researchers to magically will away tax delinquency as doing so will likely improve neighborhood conditions. In reality, the problem is much more complex as programs designed to help homeowners prevent delinquency (installment plans) or become current (payment plans) do not necessarily solve the underlying financial distress that is at the root of delinquency. The sources of blight can still exist even if the homeowner has become current on their tax bill. Increased code enforcement in areas with high tax delinquency could help eliminate blight; however, social equity issues are likely as many neighborhoods with high tax delinquency are densely populated, low-income, and/or minority neighborhoods. Policies designed to help homeowners, particularly low-income homeowners, become both current on their tax bills and alleviate the underlying financial distress are likely to be the most successful in neighborhood revitalization. Therefore, we suggest a combination of policies would be necessary to eliminate the delinquency and help the homeowner become financially stable. To this end, the City of Milwaukee began the Strong Neighborhoods Plan (SNP) 13 in 2014 to attempt to alleviate these issues. The four-part plan, among other things, helps homeowners become current on their tax bills and provides partially forgivable loans to homeowners to make emergency repairs to blighted properties. Such that SNP is successful at eliminating both tax delinquency and the associated blight, our analysis suggests that nearby home prices should rise providing additional tax revenue to the city and equity to homeowners.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.