Abstract

An increasing number of municipalities cooperates in the field of economic development. In this article, we focus on a specific instrument in this field, namely the development of joint business parks. We apply a hazard model to data from West German municipalities between 2000 and 2015. We find interlocal business parks to be more frequent among small municipalities and in urban clusters and other constellations where suitable land is scarce. Our main focus rests on the role of intraregional competition. An analogy building on the literature on international tax coordination supports the hypothesis that interlocal business parks are more likely in regions where intraregional competition is intense. We measure the intensity of competition using local tax rates and find the evidence to be affirmative: The likelihood of interlocal business park formation increases in the intensity of intraregional (tax) competition.

Introduction

Local firms provide jobs for local residents and generate local tax revenues. Therefore, building and maintaining an attractive environment for business activities is an important objective of local governments (e.g., Büttner and Schwerin 2016; Peddle 1990). One essential element of such an environment is attractive land for business settlements (e.g., Taylor 1992). In many countries, land for business settlement is provided in so-called business parks. These encompass a large entity of land specifically dedicated to commercial and/or industrial activities of several firms (Peddle 1990). 1 When developing business parks, local governments face a trade-off. On one hand, they can benefit substantially from developing business parks jointly with neighboring jurisdictions. This cooperation allows them to exploit economies of scale, pool the risk associated with underutilization and internalize spillovers (e.g., Oates and Schwab 1988). On the other hand, these neighboring jurisdictions are competitors. Offering a business park that is better than the one in the neighborhood or finalizing it earlier may attract substantial amounts of capital—also from these neighboring jurisdictions (e.g., Taylor 1992). Developing business parks jointly means waiving the potential benefits of this intraregional competition. Our article takes this trade-off as its starting point.

The main course of argumentation in this article proceeds in three steps. First, building on the economic theory of cartels (e.g., Levenstein and Suslow 2006) and international tax coordination (e.g., Keen and Konrad 2013), we argue that joint business parks creates a platform that allows municipalities to coordinate behavior and reduce the intensity of intraregional competition. Second, we argue that the incentives to form joint business parks depend—among other things—on the intensity of intraregional competition. The more intense the intraregional competition is, the larger the incentives for local governments to develop business land jointly with others. Third, we test this conjecture using data on interlocal business parks in Germany developed between 2000 and 2015. We focus on municipal tax-setting behavior as a crucial dimension of intraregional competition. We are aware of the fact that intraregional competition is multidimensional and contains more than competition in local tax rates (e.g., Overton 2017; Taylor 1992). On the contrary, tax competition is a well-understood and important dimension of this competition. Its main advantage is the availability of clear-cut indicators that allow us to measure the intensity of intraregional (tax) competition. To the best of our knowledge, the question as to whether intraregional competition fosters intermunicipal cooperation (IMC) has not been raised in the literature, nor has it been tested. Thus, our article breaks new grounds.

German municipalities are a highly suitable testing ground. First, they have the competence to decide how much land to provide for business settlements. Unlike in some other countries like the United States, German municipalities not only regulate land usage but usually develop it before it is sold to firms (e.g., Hirt 2012). Hence, public financing is common. Second and more importantly, German municipalities collect revenues from local business and land taxes and they are entitled to set the tax rates for both taxes (e.g., Bischoff and Krabel 2017). 2 Economic theory (Wellisch 2006) predicts that regions with intense competition for mobile firms apply low tax rates to mobile tax bases like business profits while simultaneously applying high tax rates to less mobile bases like land and real estate. Thus, the institutional settings in Germany allow for a very direct way to measure the intensity of intraregional (tax) competition and test the above hypothesis.

To test this hypothesis, we apply a hazard model to a panel of more than 6,000 West German municipalities between 2000 and 2015. The results strongly support our hypothesis: We find interlocal business parks to be more likely to emerge among municipalities that—other things equal—have low business tax rates and high land tax rates. This result remains stable over a wide range of econometric specifications. We control for many other factors that have the potential to drive the emergence of joint business parks. In line with the previous literature on IMC, we find joint business parks to be more frequent among small municipalities and among municipalities that are similar in composition of their population. We also find evidence supporting the notion that interlocal business parks serve as an instrument to solve the problem of land scarcity.

We continue by reviewing the existing literature before developing our main hypothesis. Then, we introduce the institutional framework and describe our data before presenting the method and results. Subsequently, we discuss our findings and end with concluding remarks.

Review of Literature

Interlocal Competition

Economic theory takes it that local governments compete for mobile businesses and firms (e.g., Boyne 1996; Oates and Schwab 1988). Classical location theory stresses the relevance of access to markets, transportation, and/or raw materials (e.g., Dawkins 2003) while new economic geography emphasizes the importance of existing agglomerations in attracting new capital (e.g., Borck and Pflüger 2006). From the perspective of a single municipality trying to attract firms, most of these factors are difficult to change. However, there are a number of factors such as education and especially tax policies that are controlled by local governments and thus may serve as instruments in the competition for firms (e.g., Blair and Premus 1987; Oates and Schwab 1988; Wolkoff 1992).

Interlocal competition shapes local policy decisions in many fields and the complex multidimensional game is still not well-understood (e.g., Overton 2017). At the same time, the rich literature on tax competition can serve as a starting point to identify important mechanisms at work. The seminal paper by Zodrow and Mieszkowski (1986) and a large number of theoretical papers building on them show that the mobility of capital forces governments to set low tax rates for mobile factors—especially capital. 3 The largest bulk of the empirical studies on tax-setting behavior show that local business tax rates are spatially correlated—thus supporting the notion of tax mimicking among local governments (e.g., Allers and Elhorst 2005; Revelli 2001). 4 To finance local amenities, they have to rely on other, less mobile tax bases. Next to taxes on labor income, land and local real estate taxes are commonly used for this purpose (e.g., Wellisch 2006; Wilson 1999).

Taylor (1992) turns to another dimension of interlocal competition, namely infrastructure investments. He argues that time is the main strategic variable: Municipalities can increase the chance of attracting firms if they are faster in providing the necessary infrastructure than their competitors. Jayet and Paty (2006) build a two-stage model of interlocal competition. In stage 1, the municipalities build infrastructure before they compete using tax rates in stage 2. Their model explains why we often see an overprovision of land devoted to business purposes (see also Dembour and Wauthy 2009). After setting up a theoretical model, Büttner (2006) uses data from Germany to analyze the relationship between tax competition and amount of land that municipalities dedicate for commercial purposes. Exploiting institutional characteristics of the fiscal redistribution system, he finds that municipalities which are exposed to more intense tax competition provide a higher amount of commercial land.

IMC

The second strand of literature deals with IMC. IMC is widespread in many industrialized countries and covers a wide spectrum of municipal activities (Hulst et al. 2009; LeRoux, Brandenburger, and Pandey 2010). Over the last 20 years, scholars mostly from public administration have compiled a large body of empirical studies on the emergence of IMC (see Bel and Warner 2016 for an excellent review). Some studies focus on municipal characteristics and how they shape the expected gains from IMC—showing that especially small and fiscally weak municipalities are more likely to cooperate (e.g., Bel, Fageda, and Mur 2013; Schoute, Budding, and Gradus 2018; Warner and Hefetz 2002).

Pioneered by Richard Feiock and co-authors, the Institutional Collective Action (ICA) framework illustrates that negotiating, implementing, and controlling IMC contracts entails substantial transaction costs (e.g., Feiock and Scholz 2009). Under the ICA framework, these transaction costs are considered the main obstacle for interlocal cooperation. Accordingly, transaction costs are lower and thus IMC is more likely the more similar municipalities are (e.g., Feiock, Steinacker, and Park 2009). This argument is known as the homophily argument (e.g., Bel, Fageda, and Mur 2013). Furthermore, preexisting political networks are found to matter because they create a platform for exchange among administrative staff and political decision makers (e.g., LeRoux, Brandenburger, and Pandey 2010). Embeddedness in these platforms lowers transaction costs and thus fosters IMC (Feiock 2013). The empirical relevance of both homophily and embeddedness is supported in numerous empirical studies (e.g., Bel, Fageda, and Mur 2013; Feiock 2013; Schoute, Budding, and Gradus 2018; Warner and Hefetz 2002)—including a number of papers that investigate cooperation aiming specifically at fostering economic development (e.g., Feiock, Lee, and Park 2012; Feiock, Steinacker, and Park 2009; Hawkins 2010, 2017). Using data from a survey among development officials in U.S. cities, Feiock, Steinacker, and Park (2009) also show that economic development joint ventures are more likely to emerge in cities where economic development is considered critical.

Few studies have investigated the emergence of IMC in Germany. Bergholz (2018) focuses on IMC in tourism marketing while Bischoff and Wolfschütz (2019) analyze IMC in administrative services. Using the same survey among German municipalities, they both find IMC to be more likely among small municipalities. Bischoff and Wolfschütz (2019) also find population decline to be an important driver of IMC arrangements while IMC agreements are less frequent in election years. Wuschansky and König (2006) conducted a survey among German municipalities involved in interlocal business parks: The respondents state that interlocal business parks are most frequently motivated by the particular suitability of land situated at the municipal border. Other factors include strategic development goals, financial straits, or the shortage of land.

Coordinated Behavior Among Competitors

Let us now turn to the intersecting set of the studies on interlocal competition and on IMC. Di Liddo and Giuranno (2016) provide a theoretical model showing that local governments can impair interlocal competition through IMC. They argue that governments interested in extracting rents make use of IMC because this increases the amount of extractable rents without reducing the probability of reelection. While rent extraction is unlikely to play a major role in business parks, the main logic of Di Liddo and Giuranno (2016) clearly applies to business parks: Interlocal business parks may serve as a means to take the bite out of intraregional competition for mobile capital.

In the literature on international tax competition, one focus rests on the obstacles to tax coordination (e.g., Keen and Konrad 2013). Very generally, the existing studies point at limits in the enforceability of tax agreements and at the fact that tax rates are just one among many instruments in the competition for mobile capital. The literature also shows that coordination is more difficult among heterogeneous jurisdictions. For instance, the outsider position is found to be particularly interesting for small jurisdictions with large neighbors (e.g., Keen and Konrad 2013). Drawing analogies from the literature on cartels (e.g., Levenstein and Suslow 2006), the likelihood of successful coordination can be increased if jurisdictions are organized in associations because these facilitate surveillance and side-payments and provide a platform to punish defectors (see Feuerstein 2005).

Only very few papers relate IMC to tax-setting behavior. Breuillé, Duran-Vigneron, and Samson (2018) analyze the impact of IMC on local taxation. They show that the membership in the French “Establishments for IMC” increases municipal tax rates. Büttner and Schwerin (2016) explore the fact that a strikingly large number of German municipalities apply exactly the same tax rate. They argue that this tax bunching is an indication of partial tax coordination, though they do not provide any empirical evidence to back this hypothesis. Blesse and Martin (2015) analyze the tax-setting behavior of municipalities in the German state North Rhine-Westphalia and find more intense tax interactions among municipalities located in the same county or administrative district (Regierungsbezirk) or covered by the same local newspaper. While these studies indicate that tax coordination takes place where there are networks or organizations of interlocal interaction, they do not test for the role of tax competition in the establishment of these networks or organizations. This is where our article comes in.

Main Hypothesis

Consider the government in a certain municipality m. Assume that it wants to maximize expected business tax revenues net of business-related expenditures. The government may share this objective with the local electorate if tax competition is too intense (e.g., Zodrow and Mieszkowski 1986). And even if this condition does not apply, it is in the interest of the local governments to reduce the intensity of tax competition, because this increases their propensity to generate tax revenues and increase expenditures without burdening the local median voter (e.g., Aidt, Veiga, and Veiga 2011). To achieve its aim, the government can either change the tax rate or take measures to broaden the tax base. The latter can be achieved by improving the quality of the existing land or by developing new land for business activities. New business land can either be developed individually or jointly with neighboring municipalities. Our main argument is that forming a joint business park has the potential to achieve both aims—broaden the tax base and allow for an increase in tax rates.

This argument builds on the literature on tax coordination and collusion sketched above. It shows that preexisting organizational structures and institutional platforms facilitate effective coordination. By establishing an interlocal business park, municipalities create such an institutional platform that facilitates interlocal coordination in the future. This effect cannot be reached by improving the infrastructure in existing business parks or by establishing a business park without municipal partners. 5 Furthermore, municipalities that agree on a joint business park automatically also agree on a common quality of infrastructure and timing of land development. Thereby, they commit themselves not to circumvent a possible agreement on tax coordination by shifting the competition to the field of infrastructure quality or the time of finalizing it.

Municipalities face different costs and benefits when developing business land—jointly or individually. As business parks are long-term investments, comparing the jointly and individually developed business parks requires a comparison of present value. Taking the option “no new business park” as a benchmark case, the total present value (PVb) of the other two options—b = ind(idvidual), joint—is given by the following expressions:

with τ tb = business tax rate in period t (t = 0, . . ., T); ΔBtb = change in tax base compared with the benchmark case in t; Ctb = costs of establishing a business park in t; TCt = (additional) transaction costs associated with negotiating, implementing and running the business park jointly in t; rt = interest rate in t; T = time horizon of the investment. Forming a joint business park is beneficial if PVjoint > PVind and PVjoint > 0.

For reasons of simplicity, let us start by assuming that the additional tax base ΔBt as well as the discount rate rt do not depend on whether the additional business land attributed to municipality m is produced jointly or individually. In this case, the difference in present values can be expressed as follows:

The first sum captures the benefits from economies of scale and scope while the second sum captures the additional transaction costs associated with cooperation. Other things equal, joint business parks are more profitable, the larger the economies of scale and scope and the lower the transaction costs. According to the ICA framework (see section “IMC”), it is the second term that poses the major obstacle to the formation of joint business parks. The main new argument proposed in this article is expressed in the third sum. It captures the additional tax revenues that municipality m can generate because cooperation creates a platform for tax coordination that can be used to apply higher tax rates. Other things equal, joint business parks are more profitable, the more power municipalities have to raise taxes when they cooperate.

A positive relationship between the intensity of interlocal competition faced by a municipality and the expression

A more convincing argument emerges if we take into account evidence on the political economy of IMC provided by Bergholz and Bischoff (2018). They analyze data from a survey among local politicians in the German state of Hesse. Their results show that politicians associate cooperation with a loss in political power that reduces their utility from holding office. It seems reasonable to assume that the loss in power from interlocal cooperation is less severe in municipalities operating under intense tax competition because politicians have less discretionary power in the first place. The more intense the intraregional competition is, the less discretionary power is lost and thus the more inclined politicians are to cooperate—other things equal. This notion is supported by a side-result of Bergholz and Bischoff (2018)—showing that politicians in municipalities suffering from high debt per capita and a high ratio of running expenditures to own revenues are more likely to support IMC.

It is important to note that the potential benefits are likely to be regionally limited in scope. In other words, interlocal business parks may help to reduce intraregional competition but are unlikely to have any effect on interregional competition. This also implies that the incentives to form an interlocal business park are driven by the intensity of intraregional competition. This leads to our main hypothesis:

Institutional Background

We use data on West German municipalities between 2000 and 2015 to test the above hypothesis. East Germany is excluded because it went through fundamental regional reforms that prevent the use of long panel data sets. German municipalities provide important public services like local roads, business parks, cultural infrastructure, and preschool childcare. They account for approximately 20% of overall government expenditures (Zimmermann 2009). While having to fulfill minimum standards set by upper-tier governments, German municipalities have considerable leeway when choosing quality and quantity of many important public services. More than 50% of municipal revenues come from state grants and vertical tax sharing. The largest part of state grants are unconditional grants distributed through a formula-based fiscal equalization system. It gives more grants per capita to fiscally weak municipalities without fully eliminating differences in fiscal capacity (e.g., Büttner 2006).

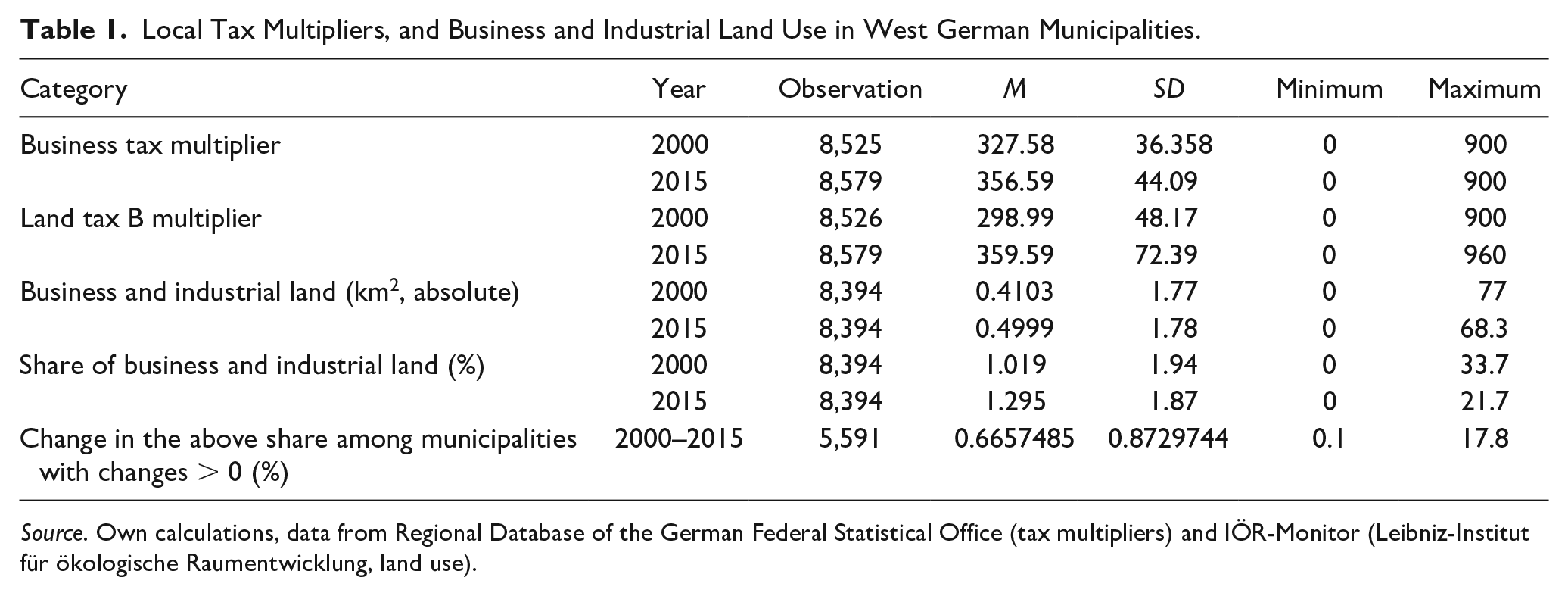

The local business tax is the most important endogenous source of municipal revenues accounting for more than 15% of revenues in West Germany in 2015. Municipalities decide about the effective rate on profits of local business establishments. Specifically, they set a so-called tax multiplier that is applied to a unified tax base. A multiplier of 400 is equivalent to a tax rate of 14%. Similarly, they determine the tax multipliers and thus rates and receive the revenues from local land taxes (e.g., Bischoff and Krabel 2017). The so-called land tax A is imposed on agricultural and forested land while land tax B burdens developed real estate and buildable ground. In 2015, both sum up to 7.1% of average municipal revenues (West Germany). Around 86% of the land tax revenues stem from land tax B. Table 1 provides descriptive statistics for the tax multipliers in West German municipalities for business and land tax B. There is substantial variation across space and time. On average, both multipliers increase in the period of observation.

Local Tax Multipliers, and Business and Industrial Land Use in West German Municipalities.

Source. Own calculations, data from Regional Database of the German Federal Statistical Office (tax multipliers) and IÖR-Monitor (Leibniz-Institut für ökologische Raumentwicklung, land use).

German local governments have the power to regulate the use of land within its borders. The German land-use regulation system rests on the principle of functional zoning and—in its basic mechanism—resembles other systems such as land zoning in the United States (e.g., Hirt 2012). The municipalities develop plans of land usage in which they legally dedicate land to specific purposes (Hirt 2012). Changes in the plans for land usage must pass the municipal council and need approval by an upper-tier administration. The main categories of land usage are residential, agricultural, commercial/industrial purposes, and natural reserves. Firms are only allowed to operate on land which is dedicated to business activities. This creates a direct link between the provision of commercial land and tax revenues on the local level (Büttner 2006). Table 1 shows that most municipalities (5,591 out of 8,394) have increased the share of land dedicated to business purposes between 2000 and 2015 (on average by 0.67% age points).

The provision of commercial land is an (if not the most) important instrument for promoting local economic development for German municipalities (Lehmann-Grube and Pfähler 1998). Unlike in some other countries where the development of commercial land tends to be carried out by private-sector companies, German municipalities actively develop business land. They acquire suitable land from its owners (if not already owned by the municipality), develop it, conduct marketing and sale activities, and take over ongoing management and/or maintenance tasks. 6 This makes the development of business land an expensive endeavor with inherent risks for the municipality. If business parks fail to attract firms, municipalities must still bear the costs.

In an increasing number of cases, business parks are developed jointly by two or more municipalities. The municipalities participating in these interlocal business parks generally settle their agreements in a formal contract. This contract settles the land allocation as well as fiscal aspects: Municipalities agree on the division of both development costs and local tax revenues from the joint business park. Often, costs and revenues are divided between the participants accordingly, for example, a municipality that bears 20% of the costs also receives 20% of the tax revenues.

Data

There is no official data on interlocal business parks in Germany. We collect data on joint business parks from various sources. Data were extracted (1) from an extensive study on German joint business parks by Wuschansky and König (2006), (2) from official data on municipality owned enterprises, (3) from official data on administrative unions, (4) from federal commercial estate databases, and (5) from supplementary Internet searches using keywords—to identify outliers. 7 Given the comprehensive approach of our data collection, we are confident to have constructed a complete data set of joint business parks in Germany. 8 For every joint business park, we know which municipalities participate in it and we know the year in which the contractual agreement between the participants was signed. Finally, we gather information about which of the cooperating municipalities provide land for the business park (so-called situs municipalities).

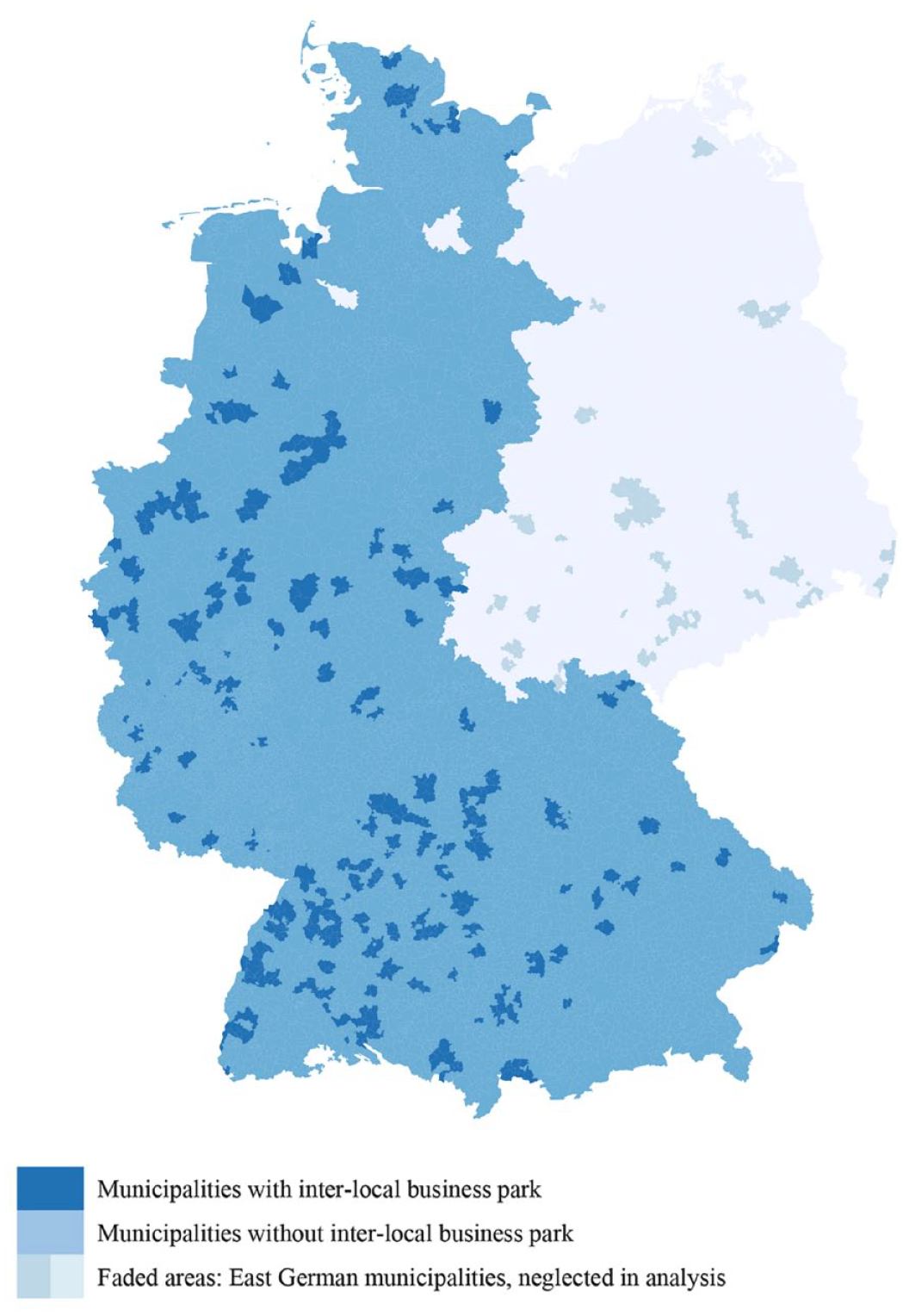

In total, we have identified 180 joint business parks as of December 2017 involving 570 participating municipalities (approximately 6.5% of West German municipalities). There has been a general increase in joint business parks which intensified during the 1990s. Figure 1 depicts how many municipalities have started a joint business park between 1970 and 2015. Figure 2 maps the involved municipalities across Germany. It becomes clear that joint business parks are not spread equally across Germany. Most notably, there is much more cooperation in western and southwestern regions.

Number of West German municipalities starting an interlocal business park from 1970 to 2015.

German municipalities with interlocal business parks in 2015.

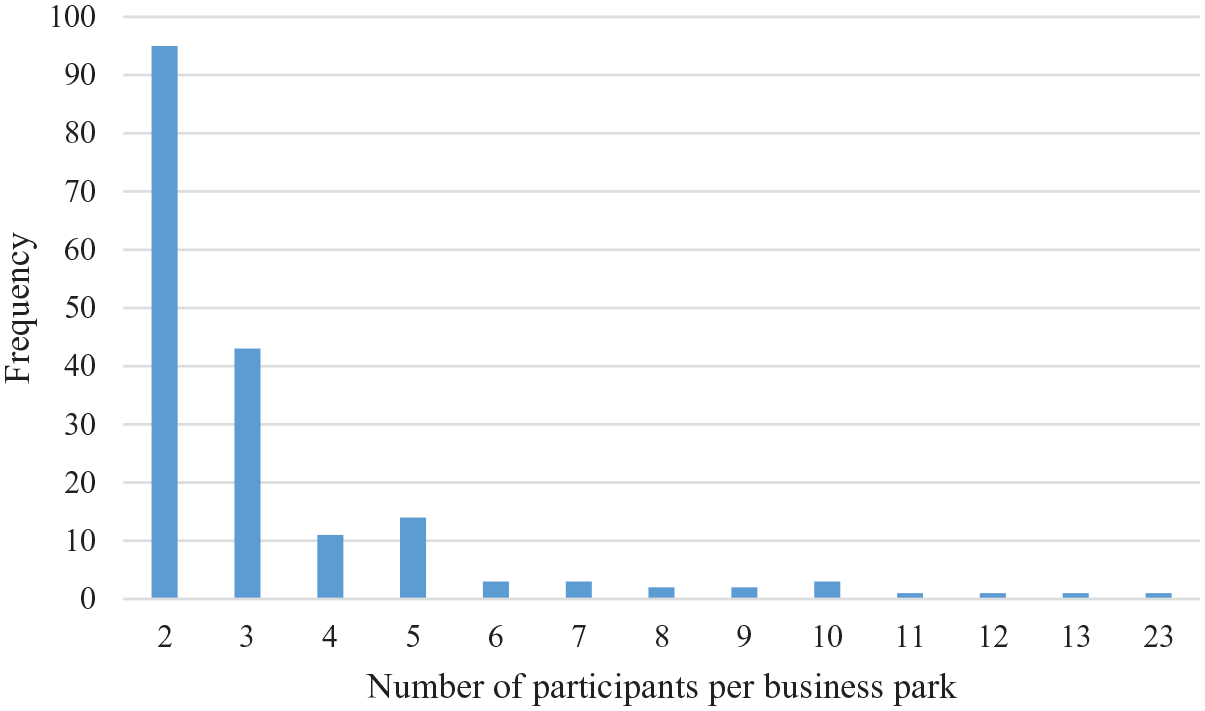

Most interlocal business parks encompass two cooperating municipalities (95 cases; 53%). In 43 cases, three municipalities are involved. Business parks with four or more partners are rare (see Figure 3). Slightly more than half of the interlocal business parks are cross-boundary in nature (at least two municipalities contribute land) while intraboundary interlocal business parks (only one land donor) comprise about 44% of the cases.

Number of participating municipalities.

Our main hypothesis states that the intensity of intraregional competition drives the emergence of joint business parks. Two decisions have to be made when developing a measure for intraregional (tax) competition. First, we have to decide which measure best captures the intensity of intraregional competition. In this article, we use measures that build on the local tax rates. Clearly, interlocal competition is multidimensional with tax competition being only one dimension (e.g., Overton 2017). At the same time, tax rates capture an essential part of this competition and it is very unlikely that intense competition does not also manifest in the tax rates. Moreover, their main advantage is that they provide a clear quantitative measure that is readily available. Following the basic logic of the tax competition literature (see section “Interlocal Competition”), we use the multiplier of the local business tax as well as the multiplier of the local land tax B. Economic theory predicts that municipalities facing intense competition for mobile capital will impose low taxes on capital. To fund necessary expenditures, these municipalities have to tax immobile land and real estate at a higher rate - other things equal (e.g., Wilson 1999). Building on this logic, we use these two tax multipliers as proxies for the intensity of tax competition: The intensity of tax competition is high if the business tax multiplier is low and the land tax multiplier is high. Consequently, our main hypothesis translates as follows: Joint business parks are more likely to emerge in local clusters with low business and high land tax multipliers. Second, we have to decide about the boundaries of the relevant intraregional market on which municipality m is competing with other municipalities for firm settlements. Following the studies on spatial interaction in local tax-setting behavior (e.g., Bischoff and Krabel 2017), we will use the cluster of municipality m and its direct neighbors, that is, municipalities that share a common border with m. In other words, we measure the intensity of tax competition that a certain municipality faces by the multipliers this municipality sets and by the tax multipliers its direct neighbors set.

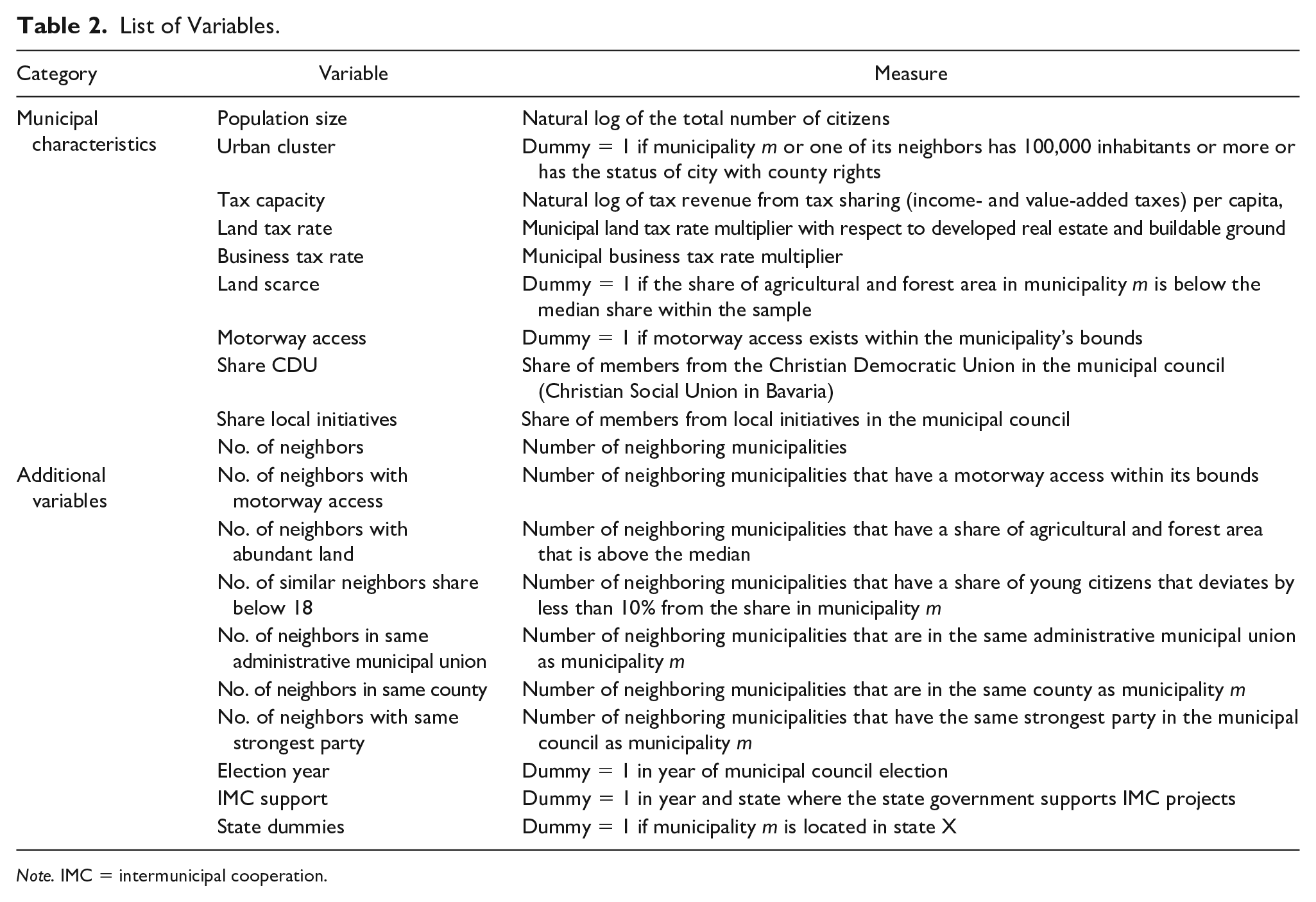

We introduce numerous other explanatory variables to account for other factors that may drive the emergence of joint business parks (see Table 2 and 3). The selection of variables primarily builds on the literature on IMC. In addition, we introduce a number of variables related to the specific context of developing business land. First, we account for the fact that municipalities may be limited in the availability of suitable land and thus the ability to develop new business parks. In these municipalities, the incentives to join an interlocal business park are high (e.g., Wuschansky and König 2006). Other things equal, the scarcer suitable land is in municipality m, the more likely it is to develop a business park jointly with other municipalities. In addition, the availability of land among the potential cooperation partners is likely to have a moderating effect on the probability of a municipality with land scarcity to develop a business park jointly with other municipalities. In particular, joint business parks may be more likely to emerge in constellations where municipality m and its neighboring municipalities differ in the availability of suitable land—other things equal. Thus, we first introduce the dummy variable “land_scarce.” It takes on the value 1 if the share of land available for development (captured by land currently used in farming and forestry) in m is below the median of all municipalities (0 else). Second, we introduce the number of neighboring municipalities for which the corresponding share is larger than the median. Finally, we interact the latter variable with the dummy variable “land_scarce.”

List of Variables.

Note. IMC = intermunicipal cooperation.

Descriptive Statistics of Selected Variables for the Year 2000; Differentiated Between Municipalities with (w) and Without (w/o) Interlocal Business Park.

We also control for the availability of a good transport connection in municipality m and its neighbors. Transport connectivity is regarded as a major location factor (e.g., Meinel, Reichert, and Killisch 2007; Möller and Zierer 2018) and hence an essential factor determining the quality of business parks. We capture the availability of a transport connection in municipality m using a dummy variable that takes on the value 1 if there is a motorway junction within the jurisdictional borders of m (0 else). To account for the transport connections in municipality m’s neighbors, we introduce the number of neighboring municipalities with a motorway junction on their territory.

Next, we control for variables that have been found to drive IMC in earlier studies. These studies suggest that municipality’s m inclination to start IMC is driven by its fiscal situation and size (Di Porto et al. 2016; Ferris and Graddy 1988; Garrone and Marzano 2015). The impact of municipal size is captured by the logarithm of the total number of citizens. We measure fiscal capacity by per capita tax revenues from vertical tax sharing generated by the observed municipality. The tax revenues from business and land taxes are excluded to avoid endogeneity issues. To account for the situation in municipality m’s neighbors, we also include the spatial lags, more precisely the median value for logarithmic population size and fiscal capacity among municipality m’s neighbors. A dummy variable marks urban clusters. It takes on the value 1 in all cases where municipality m or one of its neighboring municipalities has more than 100,000 inhabitants (0 else) or has the status of a city with county rights. Urban clusters generally offer the benefits of agglomeration (see section “Interlocal Competition”). In addition, they often host institutions of higher education that are of particular importance for start-ups and innovation networks (e.g., Audretsch, Lehmann, and Warning 2005). At the same time, land tends to be scarcer in urban clusters.

To accommodate the ICA approach, we introduce a number of variables. Two variables are introduced to control for the homophily argument according to which similarities in citizens’ tastes between municipality m and its potential partners foster IMC. First, we use the number of neighboring municipalities that are similar to municipality m in their age composition; a neighbor is considered similar if the share of inhabitants younger than 18 years deviates by less than 10% from that in municipality m. On average, slightly more than half of the neighboring municipalities qualify as similar in this respect. Second, we control for the number of neighboring municipalities that have the same strongest party in the local council as municipality m (e.g., Bel and Warner 2016; Bergholz 2018; Feiock 2007; LeRoux and Carr 2007). This variable also serves as a proxy for the expected political transaction costs associated with IMC. The higher the number of neighbors with ideologically similar municipal councils, the lower the expected transaction costs (e.g., Bergholz 2018; Bischoff and Wolfschütz 2019). On average, slightly more than 40% of the neighboring municipalities qualify as similar in this respect.

Next, we introduce two variables that capture the embeddedness of municipality m in preexisting local networks that reduce IMC-related transaction costs. The first network is the county. Especially the mayors within a county are firmly organized in the so-called “Bürgermeister-Kreisversammlung”—a committee consisting of all mayors within one county. This committee meets regularly to discuss political and administrative questions of all kinds. Except for the cities with county rights, all municipalities are member of one of these committees. The second formal network we account for are the so-called “Verbandsgemeinden,” “Samtgemeinden,” or “Ämter” (hereafter covered by the generic term administrative municipal union). These are jurisdictions formed to support a group of small municipalities in a number of government tasks, especially back-office activities. These jurisdictions have been formed in a top-down process by the state governments to increase efficiency. These special jurisdictions only exist in Rhineland-Palatine, Lower Saxony, and Schleswig-Holstein, and their scope differs across states. While these jurisdictions do not have the right to decide about tax multipliers, they—just like the “Bürgermeister-Kreisversammlung”—provide a network for exchange among neighboring municipalities. In the regressions below, we will calculate the level of embeddedness between municipality m and its direct neighbors by calculating the number of neighboring municipalities belonging to the same county and special jurisdiction, respectively. A high level of embeddedness reduces the transaction costs of collective action. However, this does not automatically mean that joint business parks are more likely among well-embedded municipalities. In fact, even the opposite may be true because the administrative municipal unions and “Bürgermeister-Kreisversammlung” may themselves be a platform to coordinate tax policies. In this case, they serve as substitutes for IMC.

We control for the role of ideologically motivated differences in the attitude toward IMC among both citizens and local politicians. To this end, we include the share of seats in municipality m’s council held by “local initiatives” (mainly free voters associations) and by the Christian democrats (CDU). To control for possible timing effects of IMC agreements in the election cycle, we introduce a dummy variable for election years (e.g., Bischoff and Wolfschütz 2019). Some state governments support municipalities that engage in IMC through subsidies for new consortia granted upon application. We control for the influence of this state policy by introducing a dummy variable that is 1 for all state-year-combinations with an active IMC-promotion policy (0 else).

Our sample consists of all municipalities in West Germany and covers the time period 2000–2015. Because of missing values in explanatory variables, we are left with 84,293 observations from an initial number of 6,061 municipalities in the sample, 277 of which start to cooperate during our observation period. Table 3 presents descriptive statistics for those municipalities included in the analysis. It differentiates between those 277 municipalities that form a joint business park at some point in time between 2000 and 2015 and the other 5,784 municipalities that do not.

Table 3 shows that the tax multipliers on both business profits and land are slightly larger on average in those municipalities that cooperate eventually. At the same time, the maximum tax multipliers are higher in the municipalities that do not form a joint business park in our period of observation. Univariate tests show that the difference in tax multipliers is significant (t test, p = .05). There is, however, a noticeable difference in population size: Cooperating municipalities are substantially larger and have larger neighbors on average. This also goes along with a larger number of neighbors, higher tax revenues per capita from tax sharing (due to rules in the fiscal equalization schemes), and a higher share of municipalities with motorway junctions, more land scarcity, and fewer neighbors with abundant land and lower scores on embeddedness in an administrative municipal union. Apart from that, the two groups of municipalities do not differ much.

Empirical Analysis

Empirical Strategy

Previous studies on IMC in Germany show that IMC agreements—once reached—are very rarely resolved (e.g., Rosenfeld et al. 2016). When it comes to joint business parks, it is even more costly to resolve the cooperation than, for example, in the field of construction yards or administrative services. Within our sample, only one municipality decided to exit a joint business park arrangement. Thus, the incident that requires explanation is the decision to install a joint business park.

An adequate empirical method to analyze the emergence of such an incident is a hazard model (cf. Bergholz 2018; Bischoff and Wolfschütz 2019; Chen, Feiock, and Hsieh 2016). Municipalities that start cooperating in t are dropped from the analysis in t + 1. This draws a clear line between starting cooperation and continuing cooperation after t. Following Allison (1982), the discrete-time hazard rate is defined as the conditional probability of municipality m cooperating in time t given that it did not cooperate before.

Solving the corresponding discrete-time hazard function provides the complementary log-log function (Allison 1982):

Here,

Results

We use a hazard model as described in expression (2) to identify factors driving the fact that a certain municipality m forms a joint business park in period t (year of signing the intermunicipal contract). State dummies are used to control for all time-invariant institutional differences, for example, in the degree of decentralization and in the fiscal equalization system. Except for the political measures and geographical variables, all independent variables are lagged by one year to avoid a simultaneity bias.

Table 4 reports the results of different specifications using different measures for our central variables. It is important to note that we report odds ratios rather than regression coefficients. Odds ratios tell us by what (multiplicative) factor the probability that municipality m starts cooperating in t increases when the corresponding explanatory variable increases. Odds ratios lower than 1 indicate that a factor retards the formation of a joint business park while odds ratios above 1 indicate that a factor accelerates it. Standard errors are clustered at the municipal level.

Results from the Hazard Model on the Emergence of Joint Business Parks (Odds Ratios).

Note. All models include state and year dummies. Robust SE given in parentheses. IMC = intermunicipal cooperation.

p < 1. **p < .05. ***p < .01.

The baseline specification includes all variables described above. The tax multiplier for the business tax in municipality m does not have a significant effect on the likelihood that this municipality cooperates in the development of business land while the tax multiplier for the land tax has a positive effect. Turning to the spatial lags, we find municipality m’s likelihood of cooperating to decrease in the median business tax multiplier among m’s neighbors and increase in the median land tax multiplier. These results are largely in line with our main hypothesis.

Municipality m is more likely to enter a joint business park if land is scarce and/or it has a motorway access on its territory. A negative effect is observed for the interaction of Land Scarcity × Abundant Land Among Neighbors. The larger the number of neighbors being part of the same administrative municipal union as municipality m, the less likely the latter is to form a joint business park. The same negative relationship is reported for the number of neighboring municipalities with the same strongest party in the city council while the opposite is true for the number of neighbors with a similar age composition of the population. The likelihood of cooperation decreases in the population size of a municipality and in the median population size of its neighbors. Election years see fewer agreements while state policies supporting IMC increase the likelihood that joint business parks emerge. The probability to form a joint business park increases in the share of seats in the municipal council held by free voter associations or Christian democrats. All other variables are insignificant.

In model 2, we replace the multipliers for land and business tax as well as the corresponding spatial lags by joint measures covering the tax multipliers in the cluster of municipality m and its neighbors. Specifically, we calculate the median tax multiplier applied in the cluster. The rationale behind using these joint measures is that the intensity of intraregional tax competition applies to the entire cluster. Thus, it is expected to affect the tax-setting behavior in municipality m in the same way it affects the tax-setting behavior of its neighbors. This translates into a substantial degree of collinearity between the tax multipliers in municipality m and its neighbors. The joint measures help reduce collinearity while the logic behind our main hypothesis applies alike. Both joint tax multipliers perform as predicted. The size of municipality m and the number of neighbors embedded in the same administrative municipal union seize to be significant, Apart from that, all other variables perform like they do in the baseline model.

In model 3 and 4, we use yet another set of measures to test our main hypothesis. In model 3, we introduce the ratio of business tax multiplier and land tax multiplier for municipality m and its neighbors. In model 4, we calculate the corresponding ratio for the median value in the cluster of municipality m and its neighbors. The higher these ratios, the lower is the intensity of intraregional tax competition. As predicted in our main hypothesis, they have a significantly negative impact on the probability of municipality m cooperating in the development of business land. Compared with model 1, the population size of municipality m and the number of neighbors belonging to the same administrative municipal union becomes insignificant. All other variables perform like they do in model 1.

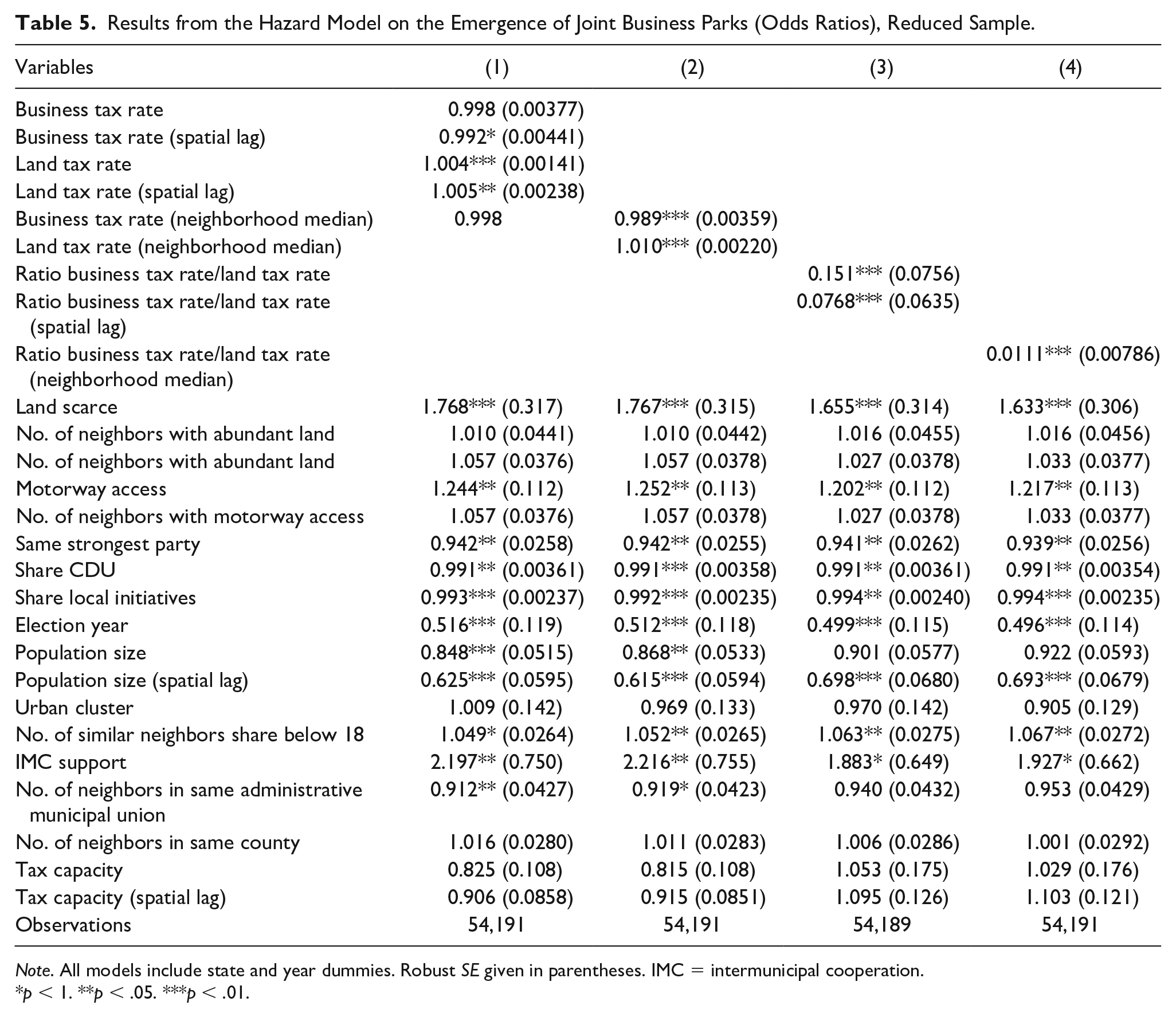

We learned that not all municipalities developed additional land during the period of observation. The fact that some municipalities did not devote additional land to business purposes may have two reasons: First, there may have been no demand for additional business land. Second, there may have been demand yet the development of business land was not possible because a stand-alone business park was unfeasible or too expensive or the municipalities were unable to find suitable partners. Thus, it is not clear ex ante whether the municipalities that did not develop additional land between 2000 and 2015 should be part of the population that we apply our regression model to. To test the robustness of our results, we rerun the models in Table 4 with a reduced starting population consisting only of those municipalities that actually develop additional business land in the period 2000–2015 (see Table 5). Expect for a minor difference in the performance of the spatial lag of the business tax multiplier in model 1, the performance of the main variables of interest is equivalent to the one in Table 4. Again, they strongly support our main hypothesis. The performance of all other exogenous variables is qualitatively unchanged.

Results from the Hazard Model on the Emergence of Joint Business Parks (Odds Ratios), Reduced Sample.

Note. All models include state and year dummies. Robust SE given in parentheses. IMC = intermunicipal cooperation.

p < 1. **p < .05. ***p < .01.

The size of the odds ratios for significant variables informs us about the magnitude of their impact on municipality m’s probability to form a joint business park. It is important to note that the overall probability of establishing a joint business park in our sample is low. Among the 6,061 municipalities in our baseline sample, 277 eventually establish a joint business park. This amounts to 4.6%. Odds ratios inform us about the degree to which this average probability is scaled up or down. The odds ratio of 2.06 for urban clusters informs us that municipalities in urban clusters have a probability of forming a joint business park that is by 106% higher than those of municipalities outside the clusters—other things equal. The value of 1.90 for the dummy variable indicating land scarcity means that municipalities with less available land for business development than the median municipality are by 90% more likely to cooperate than municipalities with a share of available land above the median. A very strong effect emerges for the election year and state policies supporting IMC: In election years, the probability to sign an agreement on a joint business park drops by almost 50% while the state policies increase the probability by 110%. Having access to the motorway reduces this probability by about 25%. Let us now turn to the main variables of interest: The impact of a change of one standard deviation in the median tax multiplier on business profits in the cluster of m and its neighbors amounts to more than 30%. For the land tax multiplier, the change by one standard deviation in the tax multiplier is equivalent to an increase in the probability of cooperation by 38%. In sum, the effects are sizeable.

We run a large number of additional models to test the robustness of the results. Among other things, we include other fiscal indicators and additional control variables (e.g. population dynamics or topographic characteristics). This does not change the performance of the main variables of interest (results are available upon request).

Discussion

We use a hazard model to analyze the factors that drive the establishment of joint business parks in West Germany between 2000 and 2015. In line with the previous literature, we find cooperation to be more frequent among small municipalities. Our results also indicate that joint business parks are used as a means by which municipalities cope with land scarcity. Interestingly, agreements for local business parks are less likely in election years.

The main focus of this article rests on the role of intraregional competition in fostering the establishment of joint business parks: We hypothesized that joint business parks are more likely to emerge the more intense intraregional competition is. In cases of intense competition, joint business parks serve as a platform to coordinate tax policies and thereby reduce the intensity of competition. Joint business parks are a highly suitable means for this purpose because they set high incentives or even force municipalities to agree on the business tax multiplier as well as the quality of infrastructure provided and the timing of providing the additional land for business purposes. Our results strongly support this hypothesis: Interlocal business parks are more likely when municipalities (and their neighbors) apply low tax multipliers on business profits and high tax multipliers on land.

At first sight, our results seem at odds with parts of the ICA framework. While we find support for the homophily argument in all our models, the number of municipalities with the same strongest party in the municipal council is negatively correlated with the formation of joint business parks. In two specifications, the same holds for the number of neighbors in the same administrative municipal union—one of our measures for embeddedness. However, the contradiction is less severe once we acknowledge that these variables point at the existence of other platforms that can be used to coordinate activities and thereby reduce the bite of intraregional competition. These platforms may serve as a substitute for joint business parks. If interpreted this way, our results no longer contradict the ICA approach.

Our analysis is not without shortcomings. Unfortunately, we cannot observe the degree of capacity utilization of the municipalities’ existing business parks. Thus, we lack information on the individual municipalities’ need to develop new business land. We account for this shortcoming through the sample reduction in Table 4. However, it cannot fully account for differences in demand for additional business land. Second, the national account data are only available at county level. Thus, we cannot control for the local industry structure and possible differences in their specific demand for business land.

Second, we measure the intensity of intraregional competition for mobile capital solely based on data on tax multipliers. Other dimensions of competition between municipalities (e.g., Overton 2017) are ignored. Consequently, we do not fully capture the phenomenon. However, the taxation-based measures we use are widely accepted to be one of the most important parameters of interlocal competition. Thus, we confidently claim that low business tax multipliers—together with high tax multipliers on land and real estate—provide a strong indication that there is intense competition for mobile capital. What is more, we are convinced that tax multipliers provide the only reliable measure for intraregional competition that is available on a larger scale.

Conclusion

We provide an empirical study on the role of interlocal competition in fostering IMC. To the best of our knowledge, it is the first study on this issue. Neither has there been a large-scale empirical analysis on the emergence of interlocal business parks nor has the specific role of interlocal competition been emphasized before. Based on the literature on collusive behavior and international tax coordination, we argue that interlocal business parks can be seen as a cartel of municipalities aimed at coordinating policies—among them business tax multipliers. Thus, we hypothesized that interlocal business parks are more likely to emerge among municipalities suffering from intense competition.

We test this hypothesis applying a hazard model to a large panel of more than 6,500 West German municipalities spanning over a time period of more than 15 years (2000–2015). The intensity of interlocal competition is measured using the local tax multipliers set by a municipality and its direct neighbors. Intense competition implies low business and high land tax multipliers—other things equal. Our results strongly support our main hypothesis. Joint business parks are more frequent in clusters of municipalities that apply low business tax multipliers and high tax multipliers on land. This result is stable and the effect size is economically meaningful. Thus, interlocal competition is identified to be one important driver of joint business park formation.

The question that immediately follows from our article is the following: Do joint business parks reduce intraregional tax competition? Except for the paper by Breuillé, Duran-Vigneron, and Samson (2018), the economics literature has not addressed this question so far. If we compare the recent multipliers set by West German municipalities in 2015, we find that the average business tax multiplier and the average land tax multiplier are higher in those with a joint business park. The ratios of business to land tax multipliers used as explanatory variables above are on average slightly below 1.0 for these municipalities, while they are above 1.02 for those municipalities that do not form a joint business park. At first sight, this seems to support the notion that joint business parks reduce intraregional competition. However, this comparison is by no means compelling. Neither are the differences statistically significant nor does this naïve and univariate comparison control for covariates, and so on. Clearly, a thorough analysis of this question goes far beyond the scope of this article and must be left to further research.

Footnotes

Acknowledgements

We would like to thank the editors and reviewers for their constructive suggestions and comments. Furthermore, we are grateful to Martin Rosenfeld, Peter Haug, Christian Bergholz, and the participants of the 15th PEARL Workshop in Zermatt for their valuable input.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.