Abstract

An analysis of how the organic dairy commodity chain in the Northeast United States is structured uncovers significant power asymmetries and conflicting tendencies regarding the treadmill of production in organic dairy farming, distribution, and marketing, thus calling into the question the capacity of the state to simultaneously promote markets and transform agriculture in the direction of ecological sustainability. While organic certification has contributed to highly centralized business structures and more advanced processing technology at the distribution and marketing levels, it has also fostered significant changes in farming practices that represent a shift away from intensification and industrialization of agriculture. The standards governing organic dairy production require a slowing down of bovine metabolism and an overall reduction in material throughput, even as the economic system flowing from this regulatory regime has led to changes in milk processing, distribution, and economic control that constitute an acceleration of the treadmill of production.

Keywords

In contrast to conventional agriculture’s reliance on nonrenewable and polluting petrochemical inputs, organic farming seeks to minimize use of purchased inputs, and avoid application of synthetic fertilizers and pesticides to crops, and use of antibiotics or synthetic hormones with livestock production. In concert with these prohibitions, organic farming seeks to close the nutrient cycle and avoid the need for external inputs through cultural practices such as cover cropping, crop rotation, application of manure or compost, and polyculture. These cultural practices are meant to increase soil fertility, reduce soil erosion, and minimize pest control problems. The limits on antibiotics and hormones are meant to create healthier animals and livestock products (Lampkin, 2000). The question is whether these agronomic and animal husbandry principles, embodied in the Organic Foods Production Act, are sufficient, absent changes in the social and economic infrastructure undergirding the production and marketing of organic food, to induce the broad-scale changes in agricultural practices called for by critics of the industrial food system (Buck, Getz, & Guthman, 1997; Guthman, 2004; Jaffe & Howard, 2010).

As the organic food industry has grown into a significant economic sector with tens of billions of dollars in sales (Fromartz, 2006), sympathetic critics assert that its transformative potential is being subordinated to its profit-making capacity, and its socioeconomic and ecological character increasingly mimics the larger industrial food system (Buck et al., 1997; Guthman, 2004; Jaffee & Howard, 2010). Informal and decentralized organic food markets have given way to highly structured and centralized organic food distribution systems as the industry has grown.

An early focus on niche, local markets and an orientation toward high-quality, unprocessed food in the organic sector is giving way to mass-produced organic food sold through mainstream channels. In Guthman’s (2004) analysis of the California organic sector, organic farming is a latter day stage in the historical process of agricultural intensification, which has reached a particularly high level in California in comparison to the rest of the United States. Organic farming becomes another iteration of the agricultural treadmill of production in which farmers are forced to increase their productivity to keep up with their competitors, while in the long run productivity gains are dissipated through higher land values or lower prices (Cochrane, 1993). In the organic milk sector organic dairy firms largely control the commodity chain through centralized supply and distribution networks in which farmers usually receive a lower share of the consumer dollar than in comparable nonorganic milk commodity chains.

The marketing-intensive character of the chain puts pressure on price premiums, leads to geographically dispersed yet economically centralized production and marketing networks, and even influences processing technology and the taste of the product, in what some would say an inferior direction. However, at the same time farmers are reducing overall throughput and moving away from reliance on purchased inputs. The central question to be explored in this article is how and why the organic dairy industry is developing the way it is, and the implications of these seemingly contradictory developments for organic certification as a tool for environmental regulation, and for treadmill theory as a framework for understanding the dual role of the state as economic expansion catalyst and environmental regulator (Novek, 2003; Schnaiberg & Gould, 1994).

The focus of the study is on the Northeast United States, with considerable reference to general patterns manifest throughout the country. This emergent industry’s development is framed as a unique example of the complex ways in which the treadmill of production manifests itself, using commodity chain analysis to break down the industry into key constituent parts or nodes, and how such nodes separately and together constitute the treadmill of production. The empirical analysis starts with an analysis of the role firms play in the organic milk commodity chain and the geographic scale of production, and moves on to discuss the relationship between geographic and economic scales of production, including how linkages between farmers and firms are influenced by firm structure. Analyzing the industry’s structure shows how the treadmill of production operates at different speeds at different nodes of the chain, and informs discussion of how market-oriented environmental regulation has unintended, if not self-defeating consequences flowing from the state’s entanglement with the treadmill of production.

Treadmill Dynamics and Commodity Chain Analysis

The very same forces of globalization, economic concentration, and relentless technological “improvement” that spawned the development of organic dairy farming as a way to slow down the relentless march of the agricultural treadmill insinuate themselves into various stages of organic food commodity chains, albeit in different ways than with conventional agricultural production.

The agricultural treadmill, as laid out by Willard Cochrane (1993), addresses the tendency within American agriculture toward greater adoption of technology and increasing productivity, leading to concentration in land ownership. Agricultural innovations pursued in the interests of greater productivity are negated by declining prices or higher land prices. Farmers adopt innovations in the hopes of increasing profitability, yet the gains from such innovations are largely dissipated through lower prices brought on increased supply or higher land prices when prices are propped up by subsidies. The state aids this process with extension services and research oriented around increasing productivity, but Cochrane does not believe the basic dynamic can be altered.

The general concept of the treadmill of production refers to the tendency within late capitalist society of firms to invest in increasingly capital-intensive systems of production, putting pressure on the underlying natural and social bases of production to extract greater profits. As the treadmill produces economic dislocation and environmental damage, policy makers, corporate leaders, and even unions push for more capital-intensive investment as a way to ameliorate social and ecological dislocation wrought by the treadmill, only serving to accelerate the process (K. A. Gould, Pellow, & Schnaiberg, 2008; Schnaiberg, 1980; Schnaiberg & Gould, 1994; Weinberg, Pellow, & Schnaiberg, 2000). Organic agriculture can be seen as a counterweight to the treadmill of production by shifting to a less capital-intensive system of production that reduces natural resource withdrawals and pollution, or additions in treadmill parlance. Such an approach has the potential to significantly reduce the environmental and social damage wrought by agricultural production (Obach, 2007). One key difference between Cochrane’s conceptualization of the agricultural treadmill and the treadmill of production theorists is that treadmill of production theory says the treadmill can be resisted through state action or mobilization by citizen-workers (K. A. Gould, Schnaiberg, & Weinberg, 1996; Schnaiberg, 1980), while the agricultural treadmill is seen as fundamentally unstoppable (Cochrane, 1993). The former clearly applies to the organic certification regime as various environmental and agricultural groups have mobilized to pass organic legislation, expand regulation, and enforce regulation, all the while battling economic interests that seek to weaken the standards in the interests of expanding the organic market, which they argue would increase the overall environmental benefit flowing from the standards (Obach, 2007).

In laying out how the organic milk commodity chain is structured, especially in regards to the role of firms vis-à-vis their farm suppliers, this article explains how treadmill dynamics manifest themselves within the chain. Showing how the treadmill of production simultaneously speeds up or slows down at different points along the commodity chain demonstrates how the state intervention that is the organic dairy certification regime produces contradictory effects because of the state’s dual role as growth promoter and agent of social consensus (K. A. Gould et al., 1996; Novek, 2003). The organic certification regime simultaneously aims to create new opportunities for capital accumulation through the marketing of a new, differentiated product, while also mobilizing market forces to effect environmental improvement as consumers stimulate new forms of farm-level production based on lower input usage, lower milk production, and eschewal of harmful synthetic fertilizers and pesticides.

Using organic certification to both create new market opportunities and reduce the environmental impact of agriculture sets up a fundamental conflict; profit runs up against strict standards, yet overly restrictive standards would presumably reduce the potential of the organic certification regime to transform agricultural practices. Furthermore, the interests of many organic farmers and organic food processors and marketers appear to be at odds with each other as far as standards setting and enforcement; farmers want to maintain high standards, restrict new entrants, and maintain premium farm gate prices, while processors and marketers would like to see a plentiful supply of organic food commodities to lower their input costs; if that means the standards are not quite as strict then so be it.

In organic dairying, the returns to farmers can increase as the treadmill of production is slowed down. Rather than investing in labor saving and yield enhancing technologies to increase profits, organic dairy farmers in the Northeast employ less productive technology and more labor to meet organic standards, and earn higher prices for their milk. This slowing down of the treadmill observed at the farm level in the Northeast (Guptill, 2009) coexists with changes in the distribution and marketing nodes of the commodity chain that seem to contradict the farm-level tendencies. The presence of geographically dispersed distribution chains, widespread use of pasteurization technology that makes the milk less perishable, and economically concentrated marketing networks point to a more technified, less competitive distribution and marketing node that fosters power imbalances within the commodity chain. While certainly not unique to the organic dairy sector, the two broad sets of activities—farming/primary food production on the one hand, and distribution/marketing on the other hand—are in such fundamental conflict that the stated purposes of the organic certification regime are jeopardized.

The mass marketing of organically certified food products exemplifies how treadmill logic can even take over in sectors of economic activity that are presumably oriented toward slowing down the treadmill (K. A. Gould, Pellow, & Schnaiberg, 2003). Activities fostered at the distribution stage to increase profits—such as special processing to create a longer shelf life, buying from larger farms, and shipping milk and milk products long distances—are in tension with the activities that farmers need to engage in to sustain petty commodity production, let alone accumulate capital at the farm level. The economically centralized, geographically dispersed character of this marketing-intensive commodity chain leads to highly asymmetric relationships between organic dairy farmers and their buyers. While hardly unusual in agribusiness writ large, this asymmetry is particularly significant in this case as the economic pressures faced by organic dairy farmers make it hard for them to comply with organic standards, including purchasing expensive organic feed, pasturing animals, and not using antibiotics; following all of these strictures threaten to drive up costs of production per unit of milk produced even as their capacity to pass on such costs to buyers and eventually consumers is severely constrained.

This apparently simultaneous speeding up of the treadmill in one part of the chain and slowing down at another part of the chain demonstrates that treadmill dynamics need not be uniform or coordinated across the vertical dimension of a particular commodity chain—moving from farming to processing to marketing, but it is unclear how long such severe tension as exists in this case can endure before the arrangement collapses under the weight of its internal contradictions. While other treadmill studies have examined conflicts between treadmill actors and citizens wanting to prioritize use values that would impede the treadmill (K. A. Gould et al., 1996; Novek, 2003; Weinberg et al., 2000), what makes this case unique is how the two forces that are seemingly working at cross purposes are inextricably linked to each other within a single commodity chain, depending on each other for their existence even as they struggle with one another. In doing so they vividly operationalize the difficulties of making environmental sustainability dependent on expanding economic production, which is responsible for the unsustainability of production in the first place because of the ever-expanding resource withdrawals and pollution required to support it.

Commodity chain analysis is used as an analytical frame to focus attention on the relationships between different actors (Gereffi, Kornzeniewicz, & Kornzieniwicz, 1994; Sturgeon, 2009) within the organic dairy industry, how power infuses itself within these relationships, and how territoriality and the spatial concentration or dispersion of production mediate these relationships and in turn impact treadmill dynamics. Commodity chain analysis is particularly useful as a technique for making more transparent the dynamics and relationships operating within an industry such as the organic dairy sector that is so laden with symbolism and ethical values or motivations. The organic label is fraught with contradictions and veilings as it seeks to tell consumers how their food was produced (Allen & Kovatch, 2000). Making commodity chain dynamics more transparent sheds additional light on the complex, and seemingly contradictory manner in which the treadmill of production manifests.

As laid out initially by Allan Schnaiberg (1980), the treadmill of production is most prevalent in large, highly capitalized sectors of the economy in which a few firms dominate. Such firms pursue a strategy of high capital investment to increase labor productivity and hence profits. Such capital investments incur additional withdrawals of resources from the environment and additions to the environment in the form of pollution. The relative lack of competition means such firms are more able to maintain high prices to customers, but the high profits engendered by such a strategy lead to capital-intensive investments, which only lead to a repetition of the cycle as such investments need ever higher levels of production to be paid back and earn a profit.

However, at the same time these large, capital-intensive firms are controlling prices and displacing labor with machines, they are able to exercise strong bargaining over suppliers, moving toward monopsony. In the case of food and agriculture the general trend is one of highly asymmetric relationships between a highly competitive farming sector, where individual producers have practically no ability to set prices nor control prices of inputs (Hendrickson, Heffernan, Lind, & Barham, 2008), and a highly concentrated food processing sector, whose members exercise a great deal of control over price setting vis-à-vis their suppliers, that is, farmers.

Using commodity chain analysis in combination with treadmill of production theory helps to focus attention on these tensions between different nodes within the chain, and how the level of competition between actors within each node of the commodity chain influences the ability of each node to bargain with other nodes. Commodity chain analysis allows us to see how the treadmill of production can in fact be slowed down at the farm level, even as it continues to accelerate at the processing and marketing levels, where less competition is extant than in the agricultural sector. Commodity chain analysis enriches treadmill of production theory in two ways. One, it highlights how different nodes within the chain are able to influence the direction or speed of the treadmill of production through technology adoption and relationships with buyers/suppliers. Two, it focuses attention on how asymmetric relationships between two nodes within a chain can influence the overall direction of the treadmill, either toward more capital investment, environmental withdrawals and additions, and high labor productivity, or more toward production methods that minimize resource use and pollution, inhibit economic concentration, and employ less capital-intensive technologies. This results in a richer understanding of how the state’s dual role as development promoter and environmental regulator manifests, and is constantly subject to pressures from different economic interests and political constituencies.

Data and Method

Primary data informing this study were drawn from interviews with marketing, government relations, milk procurement, and business development executives with organic milk firms, as well as semistructured interviews with 40 organic dairy farmers in Vermont, Maine, New York, and Pennsylvania, organic certifiers, and trade industry representatives conducted from 2003 to 2005. The key informants from the milk firms were selected through review of newspaper and other written accounts of key executives at the respective firms, and referrals from other key informants and farmer suppliers.

These primary data were complemented and updated via review of journalistic accounts, industry sources, including the ODAIRY listserv, NODPA News, the newsletter of the Northeast Organic Dairy Producers Alliance, government data, and company annual reports.

A key methodological innovation was the use of the Interstate Milk Shipper license numbers printed on all milk cartons to calculate distance from processing plant to market, and hence relative concentration or dispersion of organic in comparison to conventional milk distribution chains. Readings were taken from 23 stores in New York, New Jersey, Pennsylvania, Vermont, and Massachusetts from organic and conventional milk cartons. Distance to market from processing plant was calculated by looking up the Interstate Milk Shipper license numbers on the Food and Drug Administration website and finding the corresponding plant locations, and then using Mapquest to determine the distances from processing plants to retail outlets.

Organic Certification as Resistance to the Treadmill of Production

Generally, commercial farmers in advanced industrialized countries face a cost-price squeeze in which powerful input suppliers and processors capture the lion’s share of value added (Goodman & Redclift, 1991; Mooney, 1988), pressuring farmers to adopt more and more “efficient” technologies to lower their cost of production. However, this drive for efficiency produces significant environmental externalities and reduces the overall number of farmers as a positive feedback loop manifests as higher productivity only increases the pressure on surviving farmers to maintain and increase their productivity (Cochrane, 1993). Organic certification runs counter to this impulse as it seeks to valorize more ecologically sustainable production methods that often are less “efficient” in terms of yield per acre or person hour of farm labor (Guthman, 2009).

The agricultural treadmill has accelerated quite rapidly in the dairy industry over the past four decades, with the number of dairy farms declining by more than 90%, from 1.13 million in 1964 (Blayney, 2002) to 69,000 in 2007 (National Agricultural Statistics Service, 2009). Consolidation at the farm level has been accompanied by, and perhaps accelerated by a parallel concentration in milk processing that has led to a dramatic reduction in the number of milk-processing plants—from fluid milk to cheese and butter, from New York, to Wisconsin and California (Lyson & Geisler, 1992; Lyson & Gillespie, 1995). From 1971 to 2001 the number of milk-processing plants in the United States declined by 73%, from 4,278 to 1,173 (LaDue, Gloy, & Cuykendall, 2003).

Role of Marketing Firms as Commodity Chain Drivers in the Organic Dairy Industry

Organic dairying is a new form of production that slows down the treadmill of production at the farm level even as the treadmill of production continues to operate at a fast rate—or even increases in speed—at the distribution and marketing levels. The price premium afforded to organic dairy farmers, which represents a combination of rents and unavoidable higher costs of production, is vulnerable to downward pressure when farmers have an asymmetric relationship with their milk buyers.

Organic dairy companies manage commodity chains from farm to lips. They contract with farmers to raise cows and produce milk, with processors to bottle the milk, and with distributors or trucking companies to deliver milk to retail outlets. Completing the chain, the two main firms have national sales forces that support and develop existing accounts with retailers, and are continually reaching out to new retail outlets, be they natural food chains, supermarket chains, warehouse stores like Costco, or independent grocery and natural food stores. They own very little in the way of processing facilities for bottling milk or making cheese and other dairy products, choosing to contract out these functions for the most part. Organic Valley only owns one butter plant, and contracts out all other production with more than 40 plants around the country (Stevenson, 2009); Horizon works with 45 plants to process and package its products. A vice-president with QAI, one of the biggest certifiers of organic food manufacturers, commented on this lack of infrastructure investment: You know . . . My favorite question to people is what do organic manufacturers manufacture? And the answer is . . . labels, because many organic manufacturers don’t manufacture. They subcontract it to other places that run it for them, and put their . . . focus on brokering, marketing and distribution.”

In part, this lack of ownership of manufacturing facilities by organic food companies is an artifact of scale. As they are essentially bit players in the $1 trillion+ U.S. food business, they simply cannot manufacture on the scale necessary to justify owning dedicated manufacturing facilities. However, scale alone fails to explain this dynamic as growth in the organic industry has if anything led to more contracting out of production. This same QAI representative described this process as follows: . . . The trend seems to be the reverse. When Hain bought Walnut Acres, Walnut Acres had their own manufacturing facility. That was scrapped. It’s all made in New Jersey now.

In organic food marketing the money lies in control of the label, not manufacturing. There is little to be gained through ownership of facilities, while potential losses are greater when precious capital is tied up in fixed infrastructure. In this manner firms avoid the problem of sunk costs (Clark & Wrigley, 1997) by avoiding investment in fixed capital. Contracting out production provides firms more flexibility to respond to fast changing markets.

If there are super profits to be made in the organic food sector, it is in the ability of firms to extract economic rent from consumers through shrewd use of the organic label. Each firm constructs its own story in connection with the general attributes of organic to attract consumers. A marketing representative from CROPP/Organic Valley (2009) described this process as follows: we are a public relations driven company, and that’s how I’d describe our outreach to the consumer. . . . One of the things that we do a lot of is we press out stories of our farmers, we press out our commitment and our story about being a life-line to farmers in rural America.

While the logistics behind the scenes are key to making the marketing effective, it is the marketing that is driving the chain. Farmers sometimes try to get involved with the marketing side, by working with neighboring farmers to jointly process and market their milk together, knowing that this is where a large proportion of value is generated. However, this strategy is difficult to implement given the stiff competition faced by local processors from the national firms and the time constraints faced by farmers who have more than enough challenges just handling farm management, let alone the complexities of aggregation, processing, and marketing of milk. One New York farmer, who used to sell to a small organic cheese cooperative, and then switched to CROPP/Organic Valley after the cooperative failed to pay even conventional milk prices because of difficulties in marketing the cheese, reflected on his experience—it’s all in the marketing. But the problem is farming is a full-time job.

The power of firms revolves around their de facto ability to restrict access to this coveted label, which functions as a barrier to entry (Guthman, 2009). Firms, informed by projections of market demand and evaluations of logistical convenience, have a great deal of influence over whether a particular farmer can get on the milk truck and thus gain access to this lucrative market. Beyond serving as gatekeepers and product marketers, the firms also determine how much producers are paid, the stability of farmer pay prices, how and where it is processed, and the extent of the distribution network. The firms thus direct the design and trajectory of the commodity chain, contributing to an overall acceleration of the chain even as the standards dictate a slowing down of the farm-level treadmill.

Milk-Marketing Firms Contract With Farmers to Feed the Marketing Treadmill

The two main firms contract with more than 1,700 farms (Horizon, 506; Organic Valley, 1,200+) accounting for more than 75% of organic dairy farms in the country, 1 who in turn work with dozens of certifiers around the country who operate as gatekeepers under the supervision of the U.S. Department of Agriculture’s (USDA) National Organic Program. As managers of the entire chain the organic milk firms exercise a great deal of power over myriad actors and institutions, with considerable leverage over individual farmers, or even groups of farmers. Firms can cut off farmers with 90 days notice if they are concerned about quality. This relationship between organic milk firms and their farm suppliers is an example of what Silvia Sacchetti and Roger Sugden (2003) call a directed network, in which a large firm has disproportionate power to direct the activities of a multitude of subcontractors. The leaders of organic dairy supply networks are well positioned to respond quickly to crises as they see fit, which can have dramatic unplanned consequences for their farm suppliers.

Power Dynamics Within Commodity Chains Influence Response to Economic Slowdown

When the recession hit in 2008 the organic milk market faced a sudden slackening of demand, with absolute declines in some months leading to milk surpluses. Milk buyers had previously projected increased demand for this period and had brought on new producers as well as encouraged existing producers to increase supply to meet this projected increase in demand. The 3-year lead time for organic certification of land and 1-year lead time for certification of organic livestock requires milk buyers to anticipate their milk needs far into the future. However, even the best long-range planning cannot predict exactly when financial crises will occur, or determine their impact on market demand once they occur. In response to the milk surplus, milk buyers instituted quotas, dropped producers that were too far from processing plants or had low-quality milk, and lowered milk prices in an effort to reduce supply and bring it more in line with demand (Maltby, 2010). The need to institute such measures was accentuated by the centralized nature of the organic milk commodity chain. The two firms with national distribution and sourcing networks had to respond rapidly to milk surpluses. This supply/demand imbalance, while directly caused by the economic downturn, would not have been as severe if the organic milk supply network was not simultaneously highly dispersed spatially and economically centralized. Regional surpluses were primarily in the Western United States, but the sociogeographic character of the organic dairy commodity chain amplified the impact of surpluses, making them more national in scope. Treadmill dynamics operative at the aggregation, processing, and marketing levels shaped the spatial extent of the commodity chain, which served to send local or regional ripples or disruptions much farther and faster than would have been the case in more geographically circumscribed production networks, showing yet again the vulnerable position of those actors—organic dairy farmers—most responsible for implementing the organic standards, which serve as a partial break on the treadmill.

Horizon, Organic Valley, and H.P. Hood—based in New England and marketing milk under the Stonyfield label in the Eastern United States—had been competing with each other for producers and customers based on demand projections that proved erroneous. H.P. Hood was very aggressive in giving high pay prices to steal existing producers from other companies as well as signing up producers in remote areas of Eastern Maine, far from processing plants; it has now exited the organic dairy industry completely and handed over its 270 contracts to Organic Valley (Maltby, 2010). Horizon was securing a significant portion of its supply from a few, very large organic dairy farms in the West and Southwest, including a company-owned farm in Idaho. Additionally, Aurora Organic, an integrated organic dairy/processor brought into production several multithousand-cow operations starting in the mid-2000s that contributed to regional milk surpluses (Fantle, 2008).

Intense competition for suppliers combined with concentration at the firm level and geographic dispersion at the farm level made for a highly unstable situation that was vulnerable to these external shocks of weakening demand and increased supply concentrated in particular regions. The dominance of the distribution and marketing nodes of the chain, largely derivative of the buyer-led nature of the commodity chain in which the marketing component reigns supreme (Gereffi et al., 1994), has made the farm-level sector more vulnerable to sudden changes in the entire sector, wherever they may occur. This joining of agricultural production within geographically dispersed production networks exemplifies how the treadmill of production is accelerated; organic milk marketing transcends the limits of place in pursuit of profit, facilitated by advances in transportation and communication technology and subsidized energy (Weinberg et al., 2000), thus acting in opposition to the general pattern of deceleration of the treadmill at the farm level.

Food Miles, Power, and Locality in the Organic Milk Commodity Chain

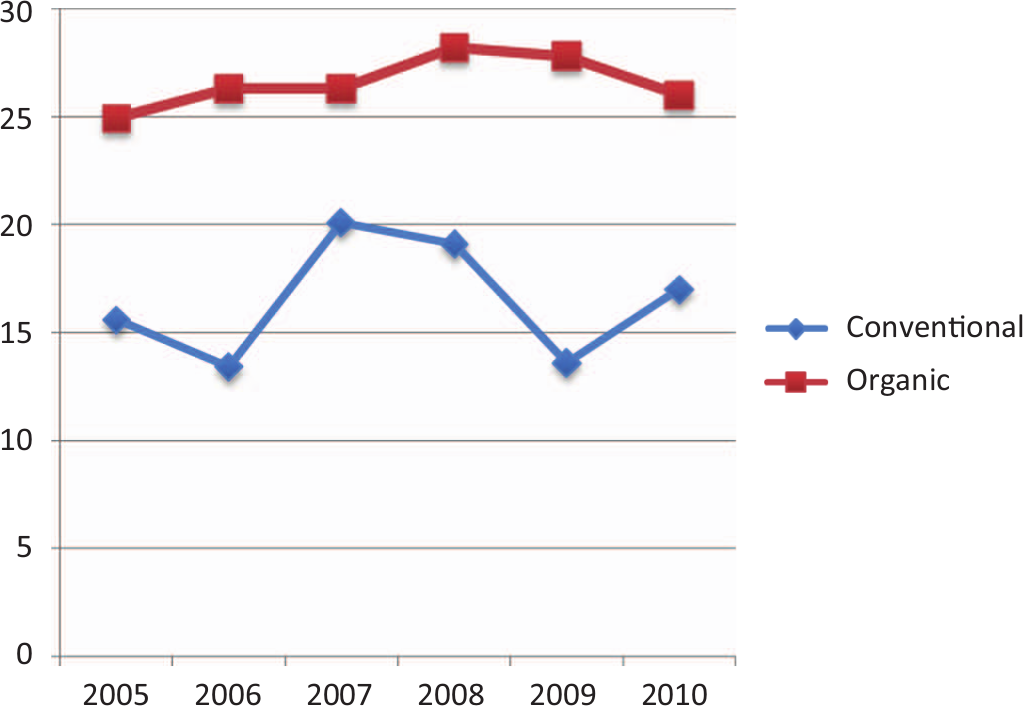

In general, organic dairy farmers receive substantial premiums for their milk over what conventional dairy farmers receive (Figure 1). As Figure 1 shows, this premium varies considerably as the price of conventional milk fluctuates dramatically from year to year, while the price of organic milk has been fairly steady, and on a slight upward trajectory during most of this time period. This chart is for only one region, but charts for other regions would show a very similar pattern both in terms of premiums and the juxtaposition of price volatility and price stability for conventional and organic dairy, respectively. This steady pay price for organic milk has been of tremendous benefit to organic dairy farmers, allowing them to better predict their cash flow from month to month and year to year. One Maine farmer emphasized how price stability more than compensates for lower production and makes organic dairying a better business proposition, albeit with some stresses: We have a herd average of 16,000 lbs. now, had been around 21-22,000 lbs before went to grazing but it was putting us out of business. With the conventional market you never knew what the price would be; with organic it’s a stable price, but it’s been flat for last 4 years, which is essentially a decline factoring in inflation. . . . CROPP is very conservative with utilization, meaning they don’t want to take on new producers unless they know they have a secure market for it. . . . Organic stabilizes the market, basically it’s a quota system that controls supply and price.

New England: Farm gate prices for organic and conventional milk, 2005-2010 ($/100 lb).

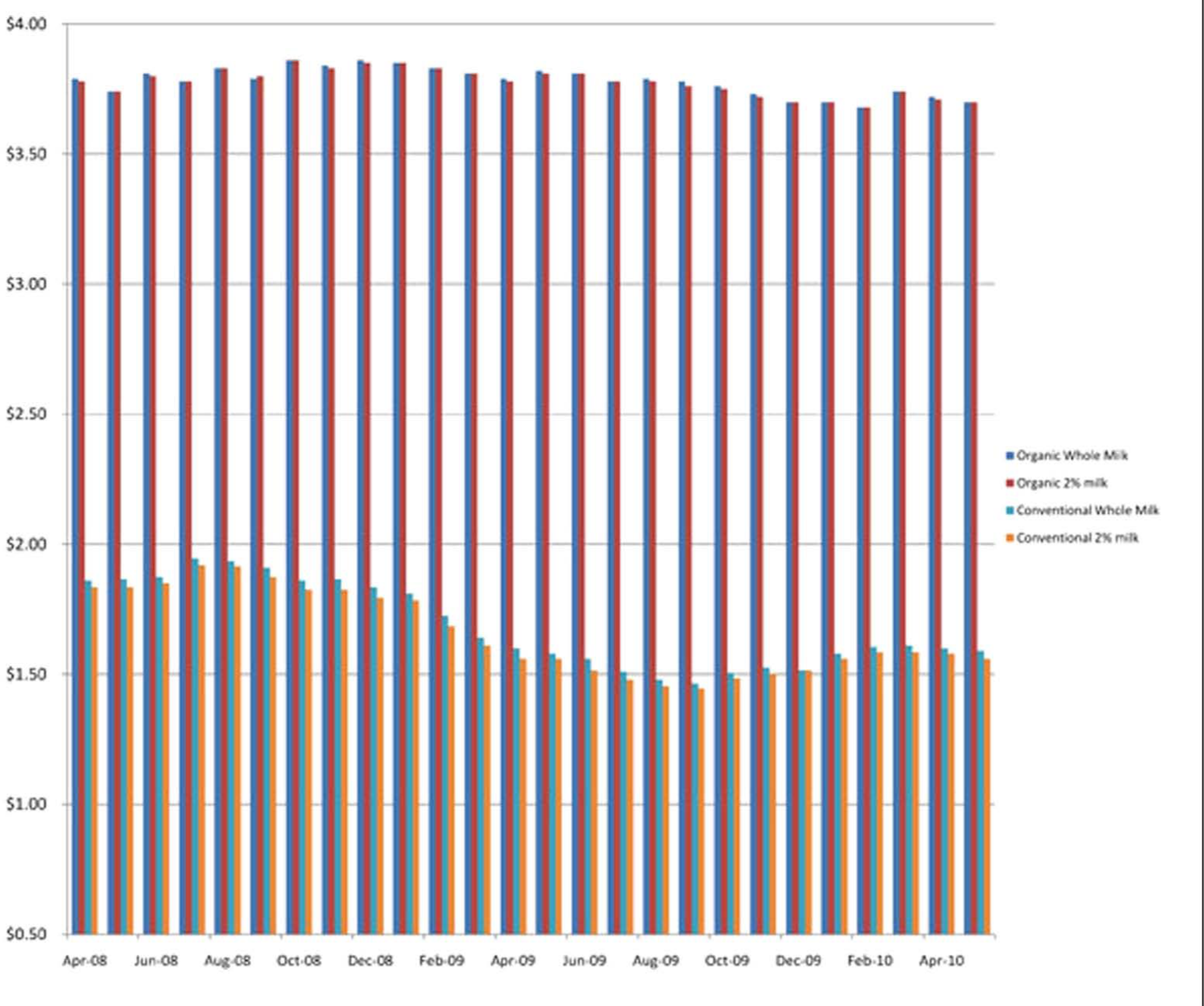

Greater price stability is one manifestation of how the organic certification regime has slowed down the dairy treadmill of production whereby highly variable prices in concert with secular price declines have put pressure on dairy farmers to invest in more efficient milking technologies, feed more grain to cows to increase milk production per cow, and increase herd size to spread equipment costs over a larger production base. However, even with these higher and more stable prices for organic milk, organic dairy farmers and organizations have repeatedly called for higher prices to cover the dramatically higher cost of organic feed (Maltby, 2006, 2012; Richardson, 2008) which can be twice as expensive as conventional feed. The premium at the farm gate is significantly lower than the premium at the retail level, as shown by comparing Figures 1 and 2. While organic milk retail prices were consistently more than twice those for conventional milk, farm gate prices for the former range from just more than 25% to 100% higher than the latter.

Comparison between organic and conventional retail milk price.

On average, the distribution, marketing, and retail components of the organic milk commodity chain account for a greater share of retail milk prices than with conventional milk. In part, this derives from the geographically dispersed character of organic milk distribution chains, and their attendant higher transportation costs. One way to measure geographic dispersion of milk distribution networks is to calculate average distance from milk bottling plants to retail outlets. Based on the Interstate Milk Shippers License numbers printed on all cartons of milk, which indicate point of packaging, the average distance for 35 cartons of organic milk from 17 stores in New York, Pennsylvania, New Jersey, and Massachusetts was 262 miles, while for nonorganic “conventional” milk, the average distance for 37 cartons from 15 stores in those same states was 108 miles. The median distance showed more divergence, 250 and 56 miles for organic and conventional, respectively. The niche character of the organic market requires larger distribution sheds for any given processing plant in comparison with conventional milk.

These added food miles add considerably to transportation costs for the milk-marketing firms. Comparing the median distances for organic and conventional milk from processing plant to store, the added cost is approximately $873 per milk tanker load (30,000 lb), using cost estimates for 2008 used in a study of the Mideast Milk Marketing Order, which includes parts of New York and Pennsylvania (Newton, 2011). For a 100-cow dairy with a 15,000 pound herd average this would amount to an additional milk-hauling cost of $43,650 per annum, which could make the difference between being in the red and turning a modest profit for farms of this size (Parsons & McCrory, 2011). Officially the milk hauler pays most of these hauling charges, but in reality the pay price to farmers is reduced as milk buyers have to pay for significantly higher milk-hauling expenses. Also, organic milk usually travels farther from farm to processing plant because organic dairy farms are sprinkled amidst a sea of conventional dairy farms, requiring the milk trucks to travel longer distances between farms to pick up a full load to drop off at the bottling plant, to say nothing of the fact that organic farms are smaller on average than conventional farms, requiring more stops to fill up a milk tanker truck with 30,000 lb of milk. Organic standards restrict the scale of farm operations, but not the scale of milk supply networks. In fact, it seems that the niche character of the organic market encourages larger scale supply networks, due to the smaller size of individual farms as well as their relative scarcity amidst the dairy landscape. The capacity of markets to transform agriculture is inhibited by the treadmill dynamics unleashed by this new regulatory regime.

Processing Technology as Tool for Changing Spatial Extent of Treadmill

One technology that has accelerated both the geographic extent of distribution chains and the concentration at the firm level is UHT or ultra-high-temperature pasteurization. Instead of using traditional HTST or high-temperature short-time pasteurization, which has a 17-day shelf life, organic dairy firms have used UHT pasteurization extensively as a method to extend shelf life and thus the distribution chain. UHT milk, heated to 280°F and injected with steam to prevent scalding, has up to a 70-day shelf life.

While conventional dairy companies pioneered the use of the technology, it has been more widely adopted by the organic dairy industry as a technique to extend shelf life, allowing milk to sit longer, either in a warehouse or on the retail shelf. In particular, the longer sell-by dates played a crucial role in initial retail acceptance as dairy case managers did not have to worry about rotating the organic section every few days. A marketing representative from Horizon described the rational for UHT as follows: when it was starting out, gosh it’s been a long time now, but several years ago, organic milk didn’t turn as quickly. . . . So in the ultra-pasteurized technique you’re able to get a little more code date, a little more shelf life, and that gave our customers, our retail customers, the opportunity to sell through the product before it would spoil. . . . So that was originally the reason that we started offering ultra-pasteurized. Really as a company that’s growing we were looking for all different ways that we could offer milk to our customers.

Beyond the obvious point that the different processing technology gives more shelf life, the subtext is that employment of a technology that changes the organoleptic character of the product

2

is done in the interests of retail customers, not end consumers. The marketing and sales dimension of organic is laid bare as not necessarily responding to consumer desires. Rather, the product is reconfigured to ameliorate retail stores’ concerns that this new product will not turn over fast enough in the dairy case before it goes bad. And, even when this reason is stripped away, retail customers’ preferences carry the day: It’s really very much a customer decision. Uhhm . . . we offer both . . . and we really work with customers to make sure that they have the milk that works best for them and their store. And a lot of the stores today could sell through HTST milk just as well as UP, but they’ve been carrying UP for the past five years and they continue to carry it.

One conclusion to be drawn from this statement is that retailers have tremendous power to shape both production decisions made upstream and consumer decisions made downstream. One representative of CROPP/Organic Valley was quite forthcoming about UHT processing and the contradiction this represents for the organic milk industry: Yeah. . . . It’s a controversial thing. UHT sterilization doesn’t make a lot of sense for organic. Organic by definition is minimally processed.

3

The exigencies of meeting market demand overrode concerns about integrity of the product. There is a push–pull relationship between UHT processing and dispersed distribution patterns. The use of UHT processing has accelerated the expansion of the organic milk commodity chain by increasing shelf life, while in turn its use has been fostered by the geographically dispersed character of the distribution network already in place when it was introduced, which is itself an artifact of the niche character of organic products (Watts, Ilbery, & Maye, 2005). When UHT was introduced, Horizon and CROPP/Organic Valley were already building national brands, and the distribution networks to support them. Adoption of UHT technology greatly facilitated this process. We see here a recursive process of market structure influencing technology, and technological innovation influencing market structure. Horizon introduced UHT in 1999, and their sales have rapidly expanded from $49 million in 1998 to $433 million in 2008 (Horizon Organic Dairy Company, 2001). 4 Likewise, CROPP/Organic Valley introduced UHT milk in 1998, and their sales have similarly exploded, going from $28 million in 1997 to $532 million in 2009 (CROPP/Organic Valley, 2009).

An industrial process is used to mitigate variability resulting from biological processes (Goodman, Sorj, & Wilkinson, 1987), in this case the tendency for milk to turn sour in 7 to 10 days as bacteria feed on the lactose, the sugar in milk, if not pasteurized. Perishability has long been one of the main difficulties in marketing milk (DuPuis, 2002), and ultrapasteurization partially eliminates this obstacle to efficient, wide-scale marketing and sales. It seems that UHT processing has also contributed to firm concentration; there are fewer plants with UHT capacity, and it enhances the market power of national companies by facilitating the creation of geographically dispersed yet economically concentrated distribution chains. With fewer plants having UHT capacity, smaller companies with a more limited geographical reach are less likely to have access to one. With less concern about perishability as they ship product long distances to stores and warehouses, the national firms are well positioned to edge out regional firms. This interplay between market dynamics, technology, and distribution patterns leads to relatively few competitors in the organic milk distribution industry. The relative lack of competition contributes to an acceleration of the treadmill as this noncompetitive sector invests in more capital-intensive strategies to increase production, and profits. However, this highly concentrated distribution node of the chain asymmetrically articulates with thousands of organic milk suppliers who operate in a highly competitive environment, and whose survival largely depends on slowing down the treadmill of production at the farm level.

Organic standards have led to higher production costs and prices, which in turn have led to more dispersed distribution patterns in comparison to conventional milk. Unlike the conventional milk market, whose pricing system leads to clustering of producers near processing plants and population centers, the organic milk pricing system encourages a more dispersed system of production and distribution. Whereas in the conventional milk market farm gate prices vary with distance from primary cities to reflect shipping charges to the plant and distance to market (Bailey, 1997), organic milk farm gate milk prices do not vary according to proximity to market, only by region to adjust for regional differences in cost of production.

Thus, the structure of the commodity chain, which is influenced to a large degree by state issued standards, manifests treadmill dynamics that work against each other internally, as farmers endure a cost-price squeeze while marketing firms operate spatially dispersed yet economically concentrated supply chains. Within the commodity chain the conflicting goals of government play out. As Schnaiberg and Gould (1994, Chap. 3) characterize it: government actors want to have their cake and eat it too; they want economic expansion, but they also genuinely want to protect the environment for themselves and their constituents . . . the government is either ambivalent or a broker between environmental pressure groups and treadmill defenders.

This complicated position of government actors can exacerbate tensions between commodity chain actors and lead to contradictory outcomes as the vulnerability of farmers within the chain as well as the fossil fuel–intensive supply and distribution networks undercuts assertions that this new system of food production is a model of social and ecological sustainability.

Firm Concentration and Branding in a Buyer-Driven Commodity Chain

While on an absolute level the dominant organic milk companies are bit players in comparison to their conventional counterparts, with Horizon’s $433 million in annual sales for 2008 (42% market share) dwarfed by those of its parent company—Dean Foods, with sales of $9 billion (Investopedia, 2009), Horizon has a greater market share of the organic dairy market than Dean does of the conventional dairy market. The two largest firms—Horizon and CROPP/Organic Valley controlled 75% of the organic milk market in 2007 (Zhuang, Dmitri, & Jaenicke, 2009). In the conventional dairy industry the two largest firms controlled approximately 19% of the total dairy market in the United States in 2008 (B. W. Gould 2010), and the four largest firms in fluid milk processing controlled 42% of the market in 2002, right after the merger of the two biggest processors—Dean Foods and Suiza in 2001 (Shields, 2010), and even then there is no national brand of conventional milk as it has become a generic “commoditized” food item.

Increasingly, milk in supermarkets is sold under store brands, with regional brands of milk such as Lehigh Dairy or Garelick Farms, which often comes from the exact same processing plant and thus the same milk pool, selling for 10 cents more a half gallon. Dean Foods owns dozens of processing plants around the country and the regional brands associated with them, but because of the limited premium for milk with a non–store brand label there is no sense in trying to sell Lehigh Dairy milk in California. With organic, the branding process has evolved such that the label “organic” with the “USDA Organic” seal has created sufficient symbolic capital to justify the expense of national marketing campaigns. The brand recognition produced by these campaigns allows the national firms to charge higher prices than more regional or local organic dairy firms (King et al., 2010), further accelerating the dichotomous treadmill paths at the farm and marketing/distribution levels, respectively.

The entire regime of organic certification and the resulting market segmentation, in which organic food companies carve out specialized niche markets appealing to particular subpopulations, encourages, if not necessitates high levels of concentration at the firm level. While it is certainly possible for more regional companies to succeed in this market, certain market exigencies have contributed to a scale bias toward large firms with extended distribution and marketing reach in the organic dairy sector.

The small niche character of this industry has led to extended distribution, which in turn supports market concentration. If 2% of the U.S. fluid milk market is organic it takes a population base 50 times greater to absorb the same amount of production. Whereas a conventional dairy farm with 100 cows and a 20,000 lb herd average (8.6 lb/gallon) needs a consumer milk shed of 3,262 people to absorb its production, assuming per capita dairy product consumption of 25 ounces daily (International Dairy Foods Association, 2002), an organic dairy farm with 100 cows and a 15,000 lb herd average would require a consumer milk shed of 122,325 people to absorb the same level of production.

It is necessary to dramatically extend the geographic extent of the distribution chain to capitalize on the branding process and build the company beyond the level of a small business. Some scholars of alternative agrifood chains argue that the very need to label the origin of one’s product is itself indicative of the inability of such production to be absorbed in its regions of production (Watts et al., 2005). The standards partially limit farm size in the dairy belts of the Northeast and the Midwest even as they contribute to concentration of economic activity at the firm or marketing level.

Organic Standards and Slowing the Treadmill on the Farm

While organic standards have no mention of scale or of any social criteria whatsoever, field research in the Northeast indicates that there is an implicit scale bias in the standards, even before the pasture standard was tightened up in 2010 to deal with complaints of an uneven playing field and uneven enforcement of the “access to pasture” provision of the National Organic Rule. If organic dairy farmers are required by their certifiers to pasture their animals it is very difficult to have an organic herd bigger than 500 to 600 cows, especially so in the Northeast where it is much harder to find large amounts of contiguous, high-quality pasture land. Farmers and key informants repeatedly articulated how difficult it is to pasture intensively large numbers of cows for three reasons: lack of contiguous pasture land, too much time spent taking cows to pasture and back, and too much energy spent by cows walking to and from the pasture. The pasture requirement seems to place a de facto upper limit on herd size amongst organic producers.

This scale bias of intensive pasturing slows down consolidation at the farm level, and slows down the treadmill of production; pasture-based dairying systems require less machinery as field crop acreage is reduced or eliminated, and they have lower milk production per cow as animals spend more time ingesting a given level of caloric intake on a pasture-based diet compared to a grain diet, limiting their energy intake and their milk production, while reducing stress on their bodies as their metabolism slows down. One farmer explained this process by saying, I’m a grass farmer. I let the cows do the work. I haven’t trimmed a cow’s hoof in 10 years. Cows are healthier and live longer on pasture.

For the study sample, herd average went down considerably from peak production prior to organic certification to the time of the interviews, as did grain feeding. While the data were incomplete due to farmers not having ready recall of production data from years past, for the 24 farms for which data were collected the average herd milk production per cow declined by 19% and grain feeding declined 43% for the 40 farmers reporting. These figures certainly overstate the impact of organic certification as the interim step of moving away from a confinement system with heavy grain feeding toward a pasture-based system was a major contributor to reduced milk yields. However, the shift to organic production reinforces this deceleration of the treadmill of production; the high price of organic grain makes heavy grain feeding uneconomical and risky because high per cow milk production increases the risk of mastitis, a common infection of the cow udder which is traditionally treated with antibiotics. Because organic standards completely prohibit antibiotic use on cows if their milk is ever to be marketed as organic, farmers aim to minimize mastitis by reducing overall throughput in their cows’ metabolic systems. The energy input for the cows is reduced, as is the product output; higher per unit prices are supposed to compensate for this reduction in bovine productivity.

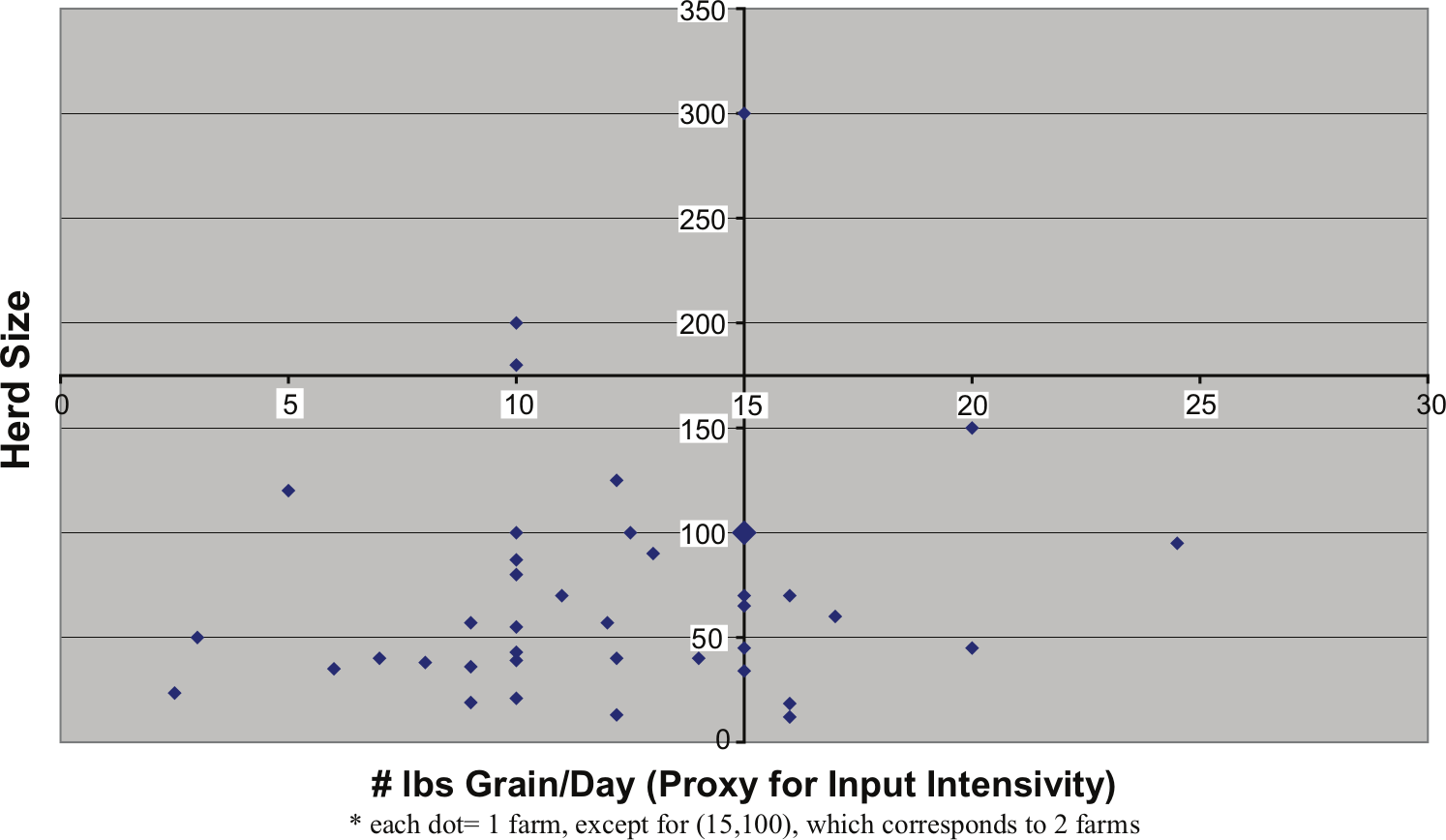

Complementing this shift in bovine metabolism, dairy production under an organic regime appears to slightly favor smaller farmers, and serves to valorize a more craft style of production over larger scale, higher input industrial production (Harper, 2000). The sample of organic farms was less polarized than the universe of conventional farms in the same states, with herds with 100+ milking animals constituting 25% of the farms in the study and 50% of all the milk cows for the farms in the study, compared with 18% and 52% for herds and milk cows, respectively, for the dairy sector as a whole in the four states in 2002 (National Agricultural Statistics Service, 2004). A scatter plot of the farms (Figure 3) shows that, of the 40 farms visited, 60% can be classified as small-herd/low-input farms, and 17.5% can be classified as high-input/small-herd farms. No farms fall in the large-herd/high-input quadrant. Within dairying generally, concentration of farms combined with higher production per cow are the two primary indicators of an accelerating treadmill of production, and with organic production the trend is clearly away from larger herds and higher input use.

Variation in organic diary farm practice.

However, this slowing down of the treadmill of production on the farm in the Northeast is paralleled by and exists in tension with the acceleration of the treadmill of production downstream from the farm in the processing and distribution nodes of the commodity chain. Guptill’s (2009) study of the organic dairy industry in New York state supports these findings, with organic dairy farmers replacing purchased feed with on-farm sources, experimenting with cow genetics to optimize grazing, and developing local sources of feed grain. On the distribution side, large national milk firms dominate the market, and contribute to a cost-price squeeze for farmers (Guptill, 2009).

The creation of national brands of organic milk highlighting more “natural” production processes has contributed to the development of economically centralized and geographically dispersed distribution and marketing networks. These two factors in turn have put organic dairy farms in a vulnerable position. High marketing and distribution costs put pressure on farm gate milk prices, while high organic grain prices raise production costs. This cost-price squeeze has reached the point that a recent study indicated declining profitability for Vermont organic dairy farms from 2006-2010 (Parsons & McCrory, 2011). In some cases financial pressures have caused organic dairy producers to either exit farming or abandon organic certification (Maltby, 2012). Nonetheless, organic certification has contributed to dramatic changes in production practices away for maximum production, high stress on bovine metabolic systems, and dependence on purchased inputs. How organic dairy firms respond to the cost-price squeeze facing their farm suppliers will have significant implications for the financial success of their suppliers, how they run their farms and the efficacy of organic certification as a tool for environmental change.

Conclusions

In the organic dairy commodity chain, processing technology, markets, and standards interact so as to produce geographically dispersed yet economically concentrated distribution chains, in which marketing-driven intermediary companies exercise dominance over primary producers. This buyer-driven commodity chain (Gereffi et al., 1994) structurally is weighted against the interests of the actors who are most at risk financially, and who must bear the additional costs incurred by compliance with organic standards.

However this acceleration of the treadmill off the farm is paralleled by a deceleration of the farm-level treadmill of production, which suggests that market-oriented regulations such as organic certification have contradictory effects. While certainly the increased fuel use to ship organic milk long distances is not in line with the goals of organic agriculture, this could be seen as a necessary step toward advancing more sustainable systems of dairying.

If national firms—with their emphasis on branding, marketing, and sales—continue to dominate the commodity chain, the industry’s capacity to provide farmers with a more stable economic base is vulnerable to changing market conditions. Furthermore, if in fact the negative environmental effects of intensive dairy farming, including shortened animal life spans, and pollution of water bodies with pesticides and fertilizer runoff, are largely stimulated by the drive to increase efficiency and productivity, the cost-price squeeze that confronts organic dairy farmers may limit the ability of organic standards to produce the ecological goals outlined in the preamble to the National Organic Program. 5 Producers may be compelled to cut corners and follow the letter, but not the spirit of the law to increase profits, or producers and/or firms may agitate for weakening the standards so as to reduce costs of compliance.

An alternative scenario is that new, decentralized, and more farmer-controlled marketing channels will emerge that will reduce the cost-price squeeze on farmers and provide them greater breathing room with which to run their operations in a financially and ecologically sustainable manner. Ironically, the growth of the dairy sector under the leadership of the national firms may make it easier for smaller, more regional, or local organic dairy firms to carve out profitable niches as the overall market share for organic dairy has grown, expanding business opportunities within a given geographic space.

Either way, the trajectory of the organic dairy treadmill of production stands as a powerful demonstration of how environmental regulations always have socioeconomic implications, which can either undermine or advance the environmental goals of said regulation. While the organic regulations seek to slow down the treadmill with respect to ecological damage, largely by reducing additions by prohibiting use of synthetic fertilizer and pesticides that can pollute soil and water, they are silent regarding labor, social standards, or scale of operations. In attempting to leverage consumer demand to effect environmental change without consideration of related social/economic issues the standards are at risk of being self-defeating. The treadmill of production operates in two parallel realms—the ecosystem and the economic system. Addressing one without the other may be possible in the short term, but in the long run the continuing treadmill in the economic sphere may counterbalance the slowing of the treadmill in the ecosystem (Obach, 2007).

While being technically scale neutral, organic standards foster the articulation of a highly competitive farm node with an intermediary node that is relatively uncompetitive. The organic dairy certification regime is meant to reduce the environmental impact of farming and thus slow down the treadmill, but it is always working against the same dynamics that produced industrial dairying in the first place and its attendant environmental problems. Furthermore, creating a niche market, with a label based on third-party certification that earns a price premium for producers, may actually accelerate the treadmill of production beyond that extent in conventional dairying as aggregation, distribution, and marketing intermediaries gain in importance.

By intervening in food markets and agricultural production to advance the twin goals of environmental enhancement and market development, the state is positing that the very forces of technological innovation and productivity enhancement that have produced environmental damage can be marshaled to reverse such damage (Obach, 2007). The evidence suggests a much more complicated and messy picture as the goals of the regulatory state to minimize damage from production conflict with the imperative of the state in capitalist society to foster greater production and capital accumulation. While it may be possible to channel profit-seeking behavior toward public purposes through market-oriented environmental regulation, the divergent treadmill tendencies in the case of the organic dairy commodity chain highlight the challenges and contradictions of such an endeavor.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research for this article was supported by the National Science Foundation (Grant No. BCS-0326876).