Abstract

The objective of this article is to explore how decision makers in small- and medium-sized enterprises explain their lack of commitment to sustainability through various justifications. These justifications are intended to rationalize and legitimize, through socially acceptable arguments, the absence of substantial actions in this area. A case study based on 33 interviews in nine Canadian small- and medium-sized enterprises showed that managers rationalize their lack of commitment to sustainability in several different ways. These can be grouped into three main types of justifications: prioritization of economic survival, looking for a scapegoat, and denial and minimization (denial of negative impacts, minimization of sustainability issues, self-proclaimed sustainability). The study contributes to bridge the gap between the literatures on neutralization theory, resistance to institutional pressures, and corporate unsustainability. It also sheds further light on the reasons underlying the lack of commitment to sustainable development and how managers justify this to themselves and others.

Keywords

An increasing number of organizations must respond to social pressures on sustainability issues, which are often perceived by managers to be incompatible with their economic objectives and business-as-usual practices (De Clercq & Voronov, 2011; Pache & Santos, 2010). This situation is particularly prominent in the case of small- and medium-sized enterprises (SMEs), whose managers are often reluctant to implement changes and become involved in sustainable development (Perrini, 2006). Corporate sustainable development (SD) “involves corporations’ taking into consideration their environmental and social impacts in concert with their economic objectives” (Strand, 2014, p. 688). SD initiatives are often considered by SMEs to be a source of costs rather than benefits, and their managers often appear as rather “laggard” (Collins, Roper, & Lawrence, 2010; Revell & Rutherfoord, 2003; Tilley, 1999). However, recent empirical studies suggest that increasing numbers of SMEs are becoming involved in sustainability initiatives (Battisti & Perry, 2011; Revell, Stokes, & Chen, 2010), and their contributions in this area might even be underestimated (Battisti & Perry, 2011; Baumann-Pauly, Wickert, Spence, & Scherer, 2013; Besser, 2012).

Overall, corporate commitment to sustainability could be explained by institutional pressures exerted on managers. In fact, the increasing media coverage of SD issues and their increasing importance to society in general (Holt & Barkemeyer, 2012; Perrini, 2006) may have raised owner-managers’ awareness of the environmental impacts of their activities (Revell et al., 2010; Williams & Schaefer, 2013) and led them to implement measures to mitigate them (Brammer, Hoejmose, & Marchant, 2012; Revell et al., 2010). However, this outlook does not explain the behavior of numerous SMEs that are less active in the field of SD (Revell & Rutherfoord, 2003; Tilley, 1999). The general management literature has shown the complexity and diversity of corporate responses to institutional pressures (e.g., Greenwood, Raynard, Kodeih, Micelotta, & Lounsbury, 2011; Oliver, 1991; Pache & Santos, 2010, 2013). According to Oliver (1991), these responses can be classified into two main categories: accommodation and resistance. If organizations’ SD accommodations, motivated by institutional pressures, have been thoroughly studied (e.g., Bansal, 2005; Delmas & Toffel, 2004), both the resistance to these pressures and managers’ justifications to legitimate their lack of commitment have been overlooked in the literature. The objective of this article is to explore how managers of SMEs justify their lack of commitment to sustainability through various justifications, intended to rationalize and legitimize, through socially acceptable arguments, the absence of substantial actions in this area. These justifications tend to improve the social acceptability of organizations and to respond to institutional pressures for the integration of SD.

The justifications for a lack of commitment to sustainability and responses to institutional pressures in this area can be illustrated by the techniques of neutralization used by managers. Techniques of neutralization can be defined as the justifications used by individuals to legitimize, through various types of rationalizations, their nonlegitimate, inappropriate, or reprehensible behaviors (Lim, 2002; Sykes & Matza, 1957). Neutralization techniques are “universal modes of response to inconsistency” (Hazani, 1991, p. 135), as they can be “applied to any situation where there are inconsistencies between one’s actions and one’s beliefs” (Maruna & Copes, 2005, p. 223).

Drawing on interviews with 33 decision makers from nine SMEs, this study explores the techniques of neutralization used by managers to legitimize their lack of commitment to sustainability. More specifically, this article addresses the following two complementary and interdependent questions:

How do managers of SMEs who are not committed to SD perceive sustainability issues?

How do managers of SMEs justify their limited commitment to SD?

This study contributes to the debate on the extent to which SMEs take SD into account and addresses two gaps in the existing literature.

First, most studies of corporate sustainability focus on large companies (Baumann-Pauly et al., 2013; Williams & Schaefer, 2013), even though the economic importance of SMEs suggests that they have a significant role to play (Gadenne, Kennedy, & McKeiver, 2009; Revell & Blackburn, 2007). SMEs account for about 95% of private companies in industrialized countries (Organisation for Economic Co-Operation and Development, 2005; Wymenga, Spanikova, Barker, Konings, & Canton, 2012), with the percentage varying according to the definition of SMEs. Moreover, the studies that do focus on SMEs are often based on companies that are active and exemplary in the field of SD (e.g., Jenkins, 2009; Williams & Schaefer, 2013). They therefore fail to fully describe all SMEs (Kusyk & Lozano, 2007). By focusing on the perceptions of sustainability in passive SMEs, this study illuminates a type of organization that remains understudied in the literature.

Second, this research responds to the need for empirical studies of how business managers deal with competing institutional logics (Greenwood et al., 2011; Pache & Santos, 2013). The techniques of neutralization observed in this study elucidate the strategies of institutional resistance and managers’ justifications in addressing, or failing to address, sustainability issues.

The remainder of the article is organized as follows. First, the major debates surrounding SMEs and sustainability are presented in a literature review. Second, the conceptual framework used to analyze the results, based on moral justifications and techniques of neutralization, is presented and its relevance discussed. Third, the methodology is described. Fourth and finally, the results that emerged from the research are presented and analyzed.

SMEs and Sustainability: From External Pressures to Responsible Behavior

Even though the pressures to adopt sustainability practices have grown, how SMEs respond to them remains a controversial topic in the literature. Some empirical studies have shown that SMEs are increasingly aware of the impacts of their activities (Revell et al., 2010; Williams & Schaefer, 2013). As a result, SMEs appear to be taking more concrete steps to minimize the negative consequences of their operations and to fulfill their social and environmental responsibilities (Brammer et al., 2012; Cassels & Lewis, 2011; Revell et al., 2010). The reasons managers provide to defend this commitment are essentially ethical, strategic, and commercial in character. At the ethical level, the owner-managers’ own values, level of commitment, and roles prove to be important in determining an SME’s commitment to sustainability (Hemingway & Maclagan, 2004). In fact, causal links have been established between proactive SMEs and the personal commitment or altruistic concerns of owner-managers (Fuller & Tian, 2006; Jamali, Zanhour, & Keshishian, 2009). At the strategic and commercial levels, it is primarily the financial benefits of SD that have been emphasized. From this point of view, SMEs implement sustainability practices for business opportunities, competitive advantages (Simpson, Taylor, & Barker, 2004; Torugsa, O’Donohue, & Hecker, 2012), and financial gains or cost reduction (Hamman, Habisch, & Pechlanern, 2009).

Conversely, several studies have shown that SMEs are unaware of the impacts of their activities (Collins et al., 2010; Revell & Rutherfoord, 2003; Tilley, 1999) and are reluctant to implement improvements. Many explanations have been offered and these often focus on the fact that SMEs have a more limited room to maneuver. In fact, SMEs often lack time and resources (e.g., Revell & Blackburn, 2007; Rutherfoord, Blackburn, & Spence, 2000), as well as information on and expertise in SD (Revell et al., 2010; Santos, 2011). Moreover, the fact that the impact of each SME taken individually is relatively limited (Masurel, 2007; Simpson et al., 2004) does not encourage their owner-managers to implement modifications, which they often perceive as expensive (Revell & Blackburn, 2007; Simpson et al., 2004). SMEs may therefore be encouraged to make compromises on or to limit their commitment to SD.

These mixed results on SMEs’ commitment to SD can be explained by various factors, including the diversity of attitudes toward sustainability and the difficulty of measuring commitment to this issue. According to Revell et al. (2010), the level of SMEs’ commitment to sustainability also depends on the time at which the empirical studies were conducted: In older studies, a more passive attitude toward sustainability was generally observed among SMEs. Differences in results could in fact be explained by a positive trend toward SD, fueled by the dissemination of information on the subject (Battisti & Perry, 2011; Revell et al., 2010). This evolution can, however, also be explained by the optimistic rhetoric surrounding sustainability issues and organizations’ search for social legitimacy. From this point of view, increasing sustainability pressures do not necessarily result in more substantial actions to ensure sustainability; they could rather lead organizations, including SMEs, to adopt SD only symbolically (Boiral, 2007; Christmann & Taylor, 2006; Jiang & Bansal, 2003) or to use resistance strategies such as avoidance, defiance, and manipulation of institutional requirements (Oliver, 1991). These pressures could also increase the social desirability bias associated with this type of study (Roxas & Lindsay, 2012) and thus artificially inflate perceptions that SMEs are increasingly committed to sustainability. Whatever the resistance strategy adopted, the increase in institutional pressures for sustainability strengthens the need among passive or unsustainable organizations to explain and legitimize their lack of commitment.

Legitimizing Resistance to Sustainability Issues Through Techniques of Neutralization

In the context of increasing pressures for sustainability, SMEs with low involvement may seem to be disconnected from dominant social norms and expectations, which can lead to a questioning of their legitimacy. The concept of legitimacy has been widely used in various disciplines and encompasses different meanings in different contexts (e.g., Kostova & Zaheer, 1999; Suchman, 1995). According to Suchman (1995), legitimacy can be defined as “a generalized perception or assumption that the actions of an entity are desirable, proper or appropriate within some socially constructed system of norms, values, beliefs and definitions” (p. 574). In the area of management, the search for legitimacy is generally associated with an organization’s social acceptability and social license to operate (Boiral, 2007; Oliver, 1991; Parsons, Lacey, & Moffat, 2014). The rationale underlying organizations’ adaptation to external pressures is generally explained through neoinstitutional theories. Neoinstitutional theory assumes that organizations adopt new practices and structures not necessarily for the associated economic benefits or to promote internal efficiency, but in order to respond to institutional pressures and to increase the legitimacy of the firm (DiMaggio & Powell, 1983; Meyer & Rowan, 1977). According to the neoinstitutional perspective, organizations are called on to justify their behavior to stakeholders to ensure that they are understood and perceived as acceptable (Scott & Meyer, 1991).

Various empirical studies have shown the relevance of this neoinstitutional approach to explaining organizations’ positions on sustainability issues and their official statements on SD (e.g., Bansal, 2005; Boiral, 2007; Cho, Roberts, & Patten, 2010). From this point of view, the official organizational commitment to sustainability is mostly intended to increase the consistency of the organization’s image with social expectations.

Nevertheless, corporate responses to institutional pressures are not necessarily monolithic and corporations may make use of various strategies, including institutional resistance (Greenwood et al., 2011; Oliver, 1991; Pache & Santos, 2010; Westermann-Behaylo, Berman, & Van Buren III, 2014). According to Oliver (1991), organizational responses are influenced by the nature and context of institutional pressures, which she describes as the five Cs: cause, constituents, content, control, and context. These responses appear on a continuum ranging from passive conformity to active resistance. The greater the consistency between organizational objectives and institutional demands, the greater the organization’s conformity. Conversely, when businesses are confronted with multiple demands and conflicting institutional logics that challenge their values and objectives, they are more likely to actively resist institutional expectations (De Clercq & Voronov, 2011; Oliver, 1991; Pache & Santos, 2010; Westermann-Behaylo et al., 2014) and to justify their actions and the rationales underlying them (Oliver, 1991; Scott, 1991). It follows that it is very important to consider these justifications and rationales to understand how organizations accommodate expectations that may be contradictory. Recently, some scholars have become interested in the strategies organizations mobilize when confronted with such situations (e.g., Greenwood et al., 2011; Quirke, 2013), but few studies have explored this question through the day-to-day preoccupations of the company or the management’s explanations (Pache & Santos, 2013; Smets & Jarzabkowski, 2013). This issue appears to be particularly important for small businesses, which are often in precarious economic situations and must accommodate various institutional pressures—including sustainability issues—perceived to be a threat to their profitability or even survival (De Clercq & Voronov, 2011; Pache & Santos, 2010). Indeed, SD entails a broadening of potentially major responsibilities and investments (Jenkins, 2004). Managers of SMEs may then be brought to explain themselves in order to legitimize their lack of commitment to sustainability. Because of its emphasis on proactive SMEs and exemplary managers (e.g., Jenkins, 2009; Williams & Schaefer, 2013), the literature on corporate greening has overlooked these justifications for corporate unsustainability. Such research is important to better understand the reasons underlying the passivity of many managers of SMEs regarding SD as well as how passive managers perceive sustainability issues.

The literature on techniques of neutralization can contribute to develop a relevant conceptual framework to explore SME managers’ justifications of passive behaviors. The concept of techniques of neutralization was originally developed by Sykes and Matza (1957) to conceptualize justifications and rationalizations of noncompliance. Techniques of neutralization can be considered as a form of impression management that focuses on the rationalization and legitimization of misbehavior, that is, behaviors which are considered to be socially inappropriate or not in line with dominant norms (Christensen, 2010; Sykes & Matza, 1957). Nevertheless, techniques of neutralization are not only a rationalization of misbehavior used to influence the perceptions of others. They also reflect the degree to which certain social norms are internalized by individuals (Maruna & Copes, 2005; Maruna & Mann, 2006). While misbehavior appears to be dissonant with dominant social norms, socially acceptable justifications can also be used to give an appearance of legitimacy to deviance. Given this fact, neutralization theory, like some of the research based on cognitive dissonance theory, attempts to shed light on the “conflict between one’s self-concept as a moral person and one’s morally questionable behavior” (Maruna & Copes, 2005, p. 225).

Although the literature on techniques of neutralization was originally based on the study of delinquency at an individual level (for a review of this literature, see Maruna & Copes, 2005), a growing body of research applies this approach to organizational activities, including the management of ethical issues (Lim, 2002). Most applications of neutralization theory to managerial behavior have essentially focused on the arguments used by organizations, managers, or consumers (e.g., Chiou, Wu, & Chou, 2012; Harris & Dumas, 2009) to legitimize unethical behavior. For example, the concept of techniques of neutralization has been used to explain organizations’ defensive reactions to “stockholder-initiated proxy resolutions” (McCormick & Zampa, 1990), to describe the unethical behaviors of marketing practitioners (Vitell & Grove, 1987), to analyze consumers’ perceptions of a double ethical standard in individual as opposed to corporate practices (Vitell, Keith, & Mathur, 2011), to examine how companies legitimize products that pose severe risks for customers (Fooks, Gilmore, Collin, Holden, & Lee, 2013; Stuart & Worosz, 2012), or to explain the justifications of environmental impacts used in sustainability reporting (Boiral, 2014; Talbot & Boiral, 2015). Several studies have also focused on delinquency in the workplace, such as theft and fraud (e.g., Dabney, 1995; Piquero, Tibbetts, & Blankenship, 2005) and white-collar crimes (e.g., Benson, 1985; Klenowski, Copes, Christopher, & Mullins, 2011).

This literature has made it possible to explore various techniques of neutralization and to substantially expand the scope and applications of the model initially proposed by Sykes and Matza (1957). Although this study does not aim to analyze the manifestation of these predefined techniques of neutralization inside passive SMEs, they are here used to shed light on the rationalizations used by managers to justify their lack of commitment. Because techniques of neutralization were initially developed in a very different context—essentially the study of delinquency at an individual level of analysis—they are not necessarily all appropriate or applicable to a managerial context. Nevertheless, some of these techniques may be relevant to understand how corporate unsustainability and conflicting institutional logics can be rationalized by managers. Empirical investigations are necessary to delve deeper into this unexplored issue.

Method

The objective of this article is to explore how managers of SMEs legitimize their lack of commitment to sustainability through the use of various justifications intended to rationalize their passivity in this area and to provide a socially acceptable explanation for it. To research this issue, an analysis of owner-managers’ perceptions and interpretations was necessary. To this end, a qualitative methodology appeared to be the most appropriate, as it can produce more accurate information and highlight, in an inductive manner, the various positions and perceptions of owner-managers (Spence, 2007).

In this inductive perspective, theories and models are not predefined but emerge from the data and their analysis (Strauss & Corbin, 1990). Therefore, even though the techniques of neutralization described in literature seem to be relevant to understand the justifications of SMEs inactive in the field of SD, the interviews and data analysis were not aimed at verifying the existence of those techniques. In line with the grounded theory approach, the relevance of the techniques of neutralization emerged afterward, throughout the data analysis process and in the search for a theory that could successfully fit our observations. Nevertheless, for practical reasons and as suggested by Suddaby (2006, p. 637), “we suspend this interpretive reporting hallmark [grounded theory] for the sake of advance clarity, and employ the more traditional presentational strategy of providing a theoretical overview first, to preview the major findings and resulting model.”

The case method (Yin, 1984) was chosen for this investigation for several reasons. Case study design is appropriate when the study concerns contemporary events (Yin, 2009), the investigation involves explanations of complex causal relationships (Eisenhardt, 1989) or the existing theoretical frameworks produce many interpretations of the topic under study (Eisenhardt, 1989; Yin, 2009). This is the case for the implementation of SD in SMEs. Although case studies are not suited to develop a representative sample of the population of organizations, the focus on multiple cases encourages more in-depth observations than those that can be obtained from just one case (Yin, 2009). Multiple cases tend also to reduce some bias and increase the validity of results (Kumar, Stern, & Anderson, 1993). In order to focus our research on decision makers, who are generally considered to be accountable for sustainability and therefore have to justify their action or inaction in this area, the research was conducted among owner-managers and other managers working with them, such as executives and associates. The fact that a close relationship exists between these people in SMEs suggests that they share certain values and objectives for the company (Burns, 2001), in particular, their readiness to develop sustainable and responsible practices (Jenkins, 2009; Torugsa et al., 2012). All in all, nine SMEs were visited to conduct in-depth, semistructured interviews coupled with in situ observations. Relevant documents were also studied to obtain information on the issues discussed.

Case Selection

SMEs were selected on the basis of three criteria: sector of activity, lack of commitment to sustainability, and size. First, the manufacturing sector was chosen because of its impacts on sustainability issues. Indeed, the sector uses, transforms, and consumes large quantities of raw materials and energy, generating a significant amount of waste (Millar & Russell, 2011). It also has an impact on noise levels as well as emissions, which are caused by operations and the transportation of products (Holland & Gibbon, 1997). According to the International Energy Association (2007), manufacturing businesses use almost a third of the world’s energy and are responsible for 36% of CO2 emissions.

Second, the study focuses on SMEs that are passive toward sustainability issues. The selection of passive organizations is challenging because of the social desirability bias and the lack of reliable information on sustainability performance (e.g., Devinney, 2009; Springett, 2003). Generally speaking, SMEs tend to provide very little information about their sustainability practices and may even implement measures in certain areas of SD without being aware of the meaning or significance of the concept (Ciliberti, de Hahn, de Groot, & Pontrandolfo, 2011; Fassin, 2008).

To overcome these challenges, contacts were made with regional business development centers with which SMEs work closely, notably because these groups offer expertise and financial support. Those people responsible for SMEs identified a number of them openly recognized as reticent to implement sustainability initiatives. Contacts at the regional business development center then contacted the business director to explain the research project and request their participation. Once permission was obtained (some declined), the primary researcher for the project made a first contact by telephone to provide further details, to confirm the level of commitment to SD by asking certain questions on the business’ activities, and to make an appointment to conduct interviews in the company. To qualify, the SMEs could not display significant SD activity. To identify passive SMEs, several methods were used: information gathered on the Internet, interaction with contacts and business groups, and preliminary telephone interviews with the owner-managers. Surprisingly enough, during the preliminary telephone interviews, most managers of the selected SMEs recognized quite openly and explicitly that their company was not significantly involved in SD. In all cases studied, this information on low involvement in SD was subsequently confirmed by more detailed interviews conducted in each company. Third, in compliance with the characteristics defined by the European Union (2005), the companies had to be independent (not more than 25% owned by a larger company), running profit-oriented activities, and employ no more than 250 people. These criteria are widely used in academic research on this type of business (e.g., Simpson et al., 2004; Wickert, 2014).

Data Collection

Data from SMEs were collected in 2010 and 2011. In each case studied, the research objectives were specified in detail. To begin the interview, the meaning of SD, which can be defined as a “development that meets the needs of the present generation without compromising the ability of future generations to meet their own needs” (World Commission on Environment and Development, 1987, p. 43), was explained to ensure that the interviewees understood the implications of the concept and the issues being studied. The three main dimensions of sustainability—economic, social, and environmental—were also explained to respondents through examples of sustainability initiatives. The confidentiality of the data collected was explained at this stage, which proved to be an important factor in ensuring the collaboration of participants. In line with qualitative and grounded theory approaches, an iterative process was used to determine the sample size (Glaser & Strauss, 1967; Thomson, 2011; Wasserman, Clair, & Wilson, 2009). New cases were analyzed until no new and significant data were found, that is, until theoretical saturation (Strauss & Corbin, 1998).

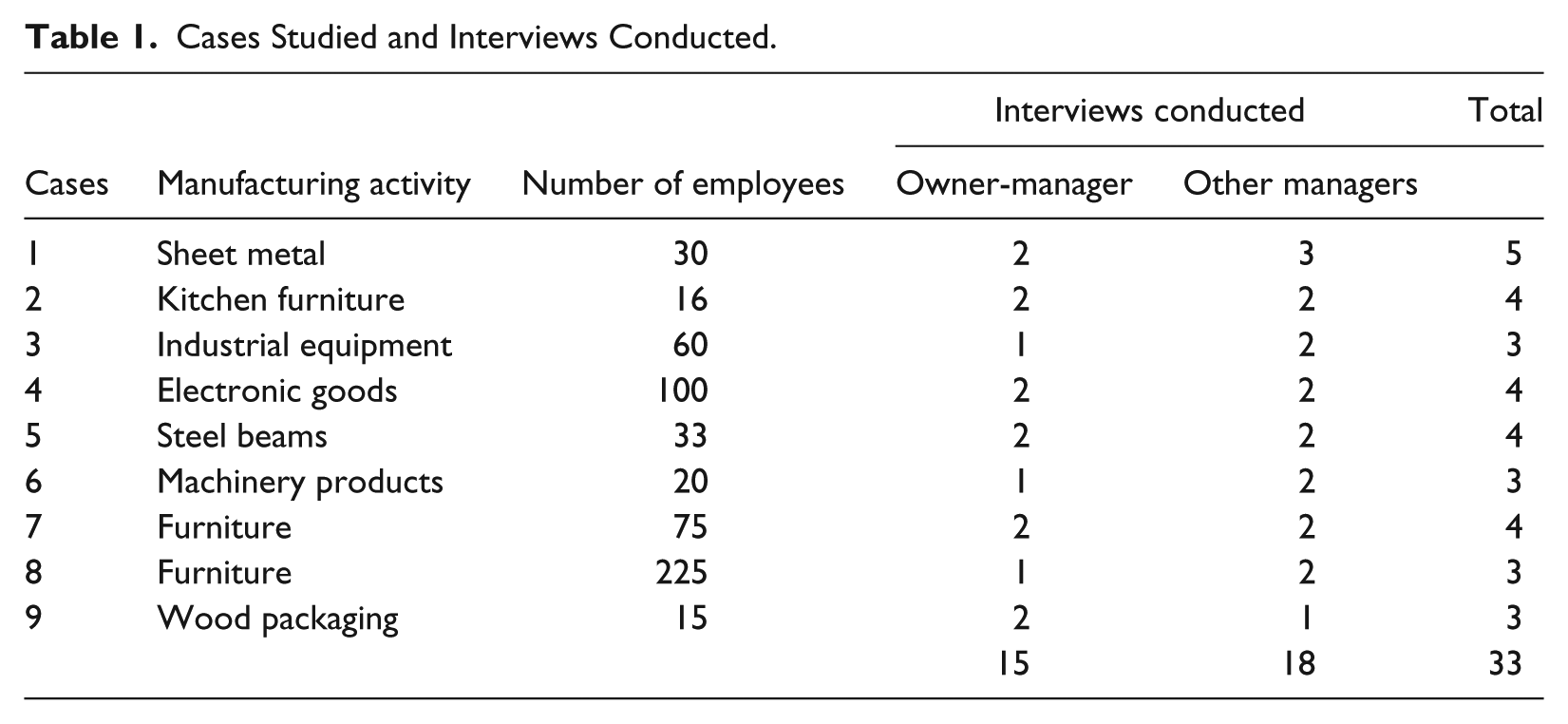

For all SMEs, interviews were conducted on-site with the owner-managers and at least two other persons in positions of responsibility in the company. Those most appropriate to answer the study’s questions were selected by the owner-managers themselves, as is recommended for such an approach (Huber & Power, 1985; Wagner, Rau, & Lindemann, 2010). Additional information was also collected from corporate documents and observations made during meetings and, in some cases, factory visits. Finally, another researcher involved in the project contributed by conducting a second interview with the managers who agreed to it. This second interview, conducted with six managers, made it possible to clarify and complete the information previously collected. A total of 33 interviews (7 with women and 26 with men) were conducted in nine SMEs (see Table 1).

Cases Studied and Interviews Conducted.

Data Analysis

Data analysis was based on an inductive process. Data were categorized based on the methodology proposed by grounded theory (Glaser & Strauss, 1967; Strauss & Corbin, 1990; Suddaby, 2006).

All interviews were recorded and transcribed. To facilitate data analysis, QDA Miner qualitative analysis software was used. The initial coding was performed based on the themes of the interview questionnaire, designed on the basis of invariants determined in the literature. Subsequently, coding was developed based on the data that emerged from the analysis of the transcripts. As suggested by Strauss and Corbin (1998), the analysis of data began during the interview process, and continued throughout transcription and categorization. This inductive approach facilitated the preparation of later interviews and development of concepts grounded in data rather than based on preestablished hypotheses. Interviews were transcribed immediately after meetings with respondents, which facilitated data analysis and enabled the adaptation of later interviews to the relevant issues that emerged from the field. To improve consistency in data processing, the complete coding of all interviews was conducted by the principal researcher. For the same reason, a second researcher and encoder was involved from the outset.

At the end of the categorization process, more than 2,600 passages were grouped into 50 categories and eight main themes. These main themes were the following: perceptions of SD, environmental impacts, main environmental issues, motivations and obstacles, social and environmental initiatives, employee involvement, governance and regulation, and leadership and values. In line with the grounded theory approach, most of the categories and related main themes emerged from the categorization process and therefore reflect the study’s findings rather than the interview questionnaire. After the data were coded, other subthemes were developed to interpret the data and meet the specific objectives of this study.

Due to the large amount of information collected and diversity of issues that emerged from the interviews, the data analysis was not focused on all of the 50 categories that resulted from the categorization process. For the purpose of this case study, data analysis was rather focused on the categories most relevant to how SMEs managers intended to rationalize and legitimize their lack of commitment to SD. More specifically, data analysis focused on the following categories:

Accounting for the impact of company activities

Owner-managers’ values and perceptions in the area of commitment to sustainability

Economic implications of SD initiatives

External factors that may affect commitment to sustainability

Justifications used to legitimize company behavior

The following section presents the main findings that emerged from the study. To better illustrate the significance of the data, several representative passages of the participants’ comments are presented. Due to its qualitative focus, this study is not intended to provide quantitative results. Nevertheless, when possible and relevant, the proportion of cases affected by certain findings was specified to contextualize the main results and provide more information on the tendencies observed.

Techniques of Neutralization Used to Justify a Lack of Commitment to Sustainability

All managers interviewed used techniques of neutralization to rationalize their lack of commitment to SD. The main neutralization techniques observed (in terms of frequency of use) were the following: economic priorities, transfer of responsibility, “small is beautiful,” denial of negative impacts, minimization of sustainability issues, risk control, condemnation of the condemners, and self-proclaimed sustainability (see Table 2). It is worth noting that these techniques are not mutually exclusive. For example, the rationalization of SMEs’ lack of commitment can be based on both “small is beautiful” and the denial of negative impacts. Moreover, all managers interviewed used several of these techniques to explain their lack of commitment. The techniques used to justify SMEs’ unsustainability can be grouped into three main kinds of rationalizations:

Prioritization of economic survival (economic priorities, risk control)

Looking for a scapegoat (transfer of responsibilities, “small is beautiful,” condemnation of the condemners)

Denial and minimization (denial of negative impacts, minimization of sustainability issues, self-proclaimed sustainability)

Most Common Techniques of Neutralization and Representative Examples.

Note. SD = sustainable development.

Prioritization of Economic Survival

In all cases studied, the main rationalization for the unsustainability of SMEs was economic survival. This justification does not necessarily reject the importance of environmental issues and corporate responsibilities in this area. Nevertheless, the managers interviewed claimed that they must assume more important responsibilities related to the future of their company that are not necessarily compatible with a substantial commitment to SD. Therefore, in the eyes of these managers, the legitimacy or moral justification for a lack of commitment to SD lies in its possible consequences: layoffs, plant closures, and risk of bankruptcy, among others. This rationalization is backed by two complementary techniques of neutralization: economic priorities and risk control (see Table 2).

First, financial and economic arguments were omnipresent in all interviews conducted. The decision to take or not to take action on SD appears to be based on economic rationales. Those interviewed seemed little worried about the environmental impacts of their operations. Only when complying with the legal requirements they are subject to, or when introducing changes bringing them tangible financial gains in the short term, do these companies implement actions to minimize environmental impacts. They downplay the actual or potential negative effects of their activities in their discourse because they perceive the smooth running of their business and the financial performance of the company to be most important. Only three respondents explicitly expressed some guilt (Cases 1, 3, and 9). The following example illustrates well the kind of spontaneous thinking evidenced in the interviews. It also demonstrates the process associated with techniques of neutralization: admission of guilt, recognition of dominant values, and neutralization.

We can obviously feel pressure to engage in SD, but is it enough to act on? It depends a lot on priorities. Sometimes, we get the impression that we feel guilty about not doing enough. Even if we’re aware of it deep down, in real life, there are other priorities. There is a little green light that’s on—the environmental light—and there’s a big spotlight next to it that says: “You have to achieve this goal.” So then we don’t see the green light anymore. What we have to do is so important. We need to reach our goals to carry through on our plan to the financiers and ensure long-term viability from an economic point of view. Everything we do is aimed at achieving that goal. (Owner-manager, Case 3)

Without clearly expressing guilt for not actively responding to pressures to engage in SD, the vast majority of respondents admitted to no longer operating as they used to and to having developed an awareness of SD. However, economic priorities were highlighted in all cases. Other arguments cited in support of this business logic involved the importance of making a profit, achieving a short-term payback, market requirements, competition, the law of the lowest price, and concern for the growth of the company (often associated with the “sustainable development” of the company by respondents).

Second, the risks associated with a commitment to sustainability were invoked in six out of nine SMEs. These risks are essentially related to economic uncertainties. According to the managers interviewed, environmental improvements often require changes in procedures and processes. This necessitates investments, trial and error, and time to adjust. In more than half of the SMEs studied, managers admitted that they preferred to wait for others to conduct the experiments and introduce the innovations that sustainability initiatives require. Companies justify this “wait-and-see” attitude through the need to limit the risks of making changes that may not correspond to market needs or the company’s financial possibilities. Managers therefore prefer to follow rather than lead and to maintain business-as-usual, even if such a position is not quite compatible with the concept of SD. This perspective is reflected in the statement:

For sure, if the market comes along, we will get on it. We’ll all get on board. At present, it would be too big of a step. Nobody wants to venture first and have a higher price and say that we’re sure it will sell because we can offer consumers a green product. (Purchasing manager, Case 7)

Looking for a Scapegoat

The second type of rationalization is related to looking for a scapegoat. This was observed in all SMEs studied. Like legitimation through economic survival, this rationalization does not necessarily deny the importance of sustainability issues. Nevertheless, managers who use this form of justification do not recognize their sustainability responsibilities and tend to condemn other actors, notably the supply chain, large organizations, and the government. This rationalization is associated with three techniques of neutralization: transfer of responsibilities, “small is beautiful,” and condemnation of the condemners (see Table 2).

First, most managers interviewed underlined the fact that their margin of maneuver is limited and that they depend on the supply chain, especially suppliers and customers. Concerning products they use, especially those that are not environmentally friendly, the SMEs studied deny any responsibility by saying that they are dependent on the products and technologies available. Companies say they have to follow the suppliers, as they are not important enough in the market to force changes themselves. The responsibility for sustainability initiatives is therefore transferred to suppliers.

Honestly, that’s what we do: we follow the supply. We are somewhat dependent on what is supplied to us. On the whole, in the world and in the business, we are a small fish. It is not us who are inventing things. (Owner-manager, Case 8)

All of the representatives interviewed stated that their customers apply little pressure for them to improve the impact of their products. At the request of customers, some SMEs must comply with environmental requirements, but no real compliance follow-up exists. As in the case of suppliers, clients can implement sustainability initiative if, for example, there is a clear demand for green products. From this point of view, SMEs appear to merely follow the market, which is the main driver of change. The responsibility for introducing sustainability initiatives is therefore diluted; if an SME is not committed to SD, they claim it to be the market’s fault.

Second, most managers stated that large organizations bear a greater responsibility for the implementation of sustainability initiatives because they have a greater impact on the environment and possess the internal competence to manage this issue. In this perspective, commitment to sustainability depends on the organization’s size. As a result, it may seem legitimate for SMEs to remain passive or, in the best case scenario, to act as followers. Such arguments tend to overlook the aggregate effect of SMEs, especially on environmental issues. Nevertheless, most managers interviewed consider that, unlike large organizations, they do not have the financial resources necessary to be more proactive in this area. One manager summarized it thus:

In SMEs, we have fewer resources, and it is also harder to allocate a specific resource. In a larger company, it is easier to assign a person to a specific dossier, the environment for example, and really work on it, which we cannot do in SMEs. Allocating partial resources works, but when we are a little overstrained, it’s the first thing to go because it is less urgent, less important for the company. (Co-owner and production VP, Case 1)

Third, nearly half of all managers interviewed also blame the government and public agencies for their inadequate policies on sustainability issues. The main criticisms are related to the failure to adapt existing regulations to business realities, the administrative constraints of environmental issues, the lack of financial assistance to support the sustainability initiatives of SMEs, and the inability of government agencies to set an example in sustainability. The following statement is quite representative of these criticisms:

The government is more controlling or mistrustful. We really have a heavy system: we are overtaxed, we over-contribute. And then we are asked to implement sustainable development. (Owner-manager, Case 1)

Denial and Minimization

The last type of rationalization used by SMEs to legitimize their lack of commitment to sustainability is based on the denial or minimization of the importance of this issue. This rationalization may be based on rejecting the supposed negative impacts associated with the activities of SMEs, minimizing sustainability issues themselves, or the self-proclaimed sustainability of the organization (see Table 2).

The most frequent kind of denial consists in questioning the existence of critical sustainability issues related to organizational activities. This argument can be related to the aforementioned “small is beautiful” technique of neutralization, but also to the denial of the injury or harm caused by the organization. Although all companies studied are involved in the manufacturing sector and may have significant environmental impacts, none of the managers interviewed clearly admitted that such impacts represent a real problem. One manager summarized it thus:

I can’t say that with the size of my company, I feel that I have a major effect. But I sort of have the feeling that I can’t do much about it. Even if I felt concerned, my resources are limited and so is my volume of greenhouse gas emissions. We have a truck to make deliveries and two small vehicles for installers to go on site. Sure there’s an impact, but it’s minor. (Owner-manager, Case 2)

More important, in more than half of the cases (1, 3, 5, 6, and 8), the managers interviewed claimed that their organization was doing enough for sustainability in general, although they could not provide convincing information, evidence, or examples of their commitment. This self-proclaimed sustainability was not necessarily intended to present the organization as a model to emulate in this area. Rather, it appeared as a legitimate justification for not doing more and for avoiding stringent regulations or controls. This justification tends to put emphasis on the need to have confidence in the social responsibility of managers and their freedom of action:

Standards and laws have to exist, but at some point I think we have to leave some space to common sense, to management rights. You know, at some point, a manager has the right to make the decisions he wants. Sustainable development might be something that we decide we want to do. (Owner-manager, Case 5)

The last kind of denial challenges the very existence of sustainability issues, including global warming, which the media and society in general tend to consider critical. All respondents were interviewed about information conveyed by the media on SD and climate change. It was in fact the subject used as an introduction when interviewers presented the background of the study. The managers of the vast majority of SMEs (seven out of nine) questioned the scientific data and sometimes even derided the need for action. They often criticized the attitude of the media, which they accused mainly of conveying highly biased, alarmist, and incorrect information on environmental issues, or of disseminating contradictory messages. From this point of view, a company’s lack of commitment seems legitimate because the merits and justifications for external pressures on the issue are contested. The respondents acknowledged that the issue is increasingly present in the media and in society in general, but they were not necessarily concerned and felt no need to express guilt, even if they felt the need to justify this stance.

For sure, we see climate change a little bit like a fad. It’s important, but at the same time, there’s a lot of people who make ads out of it, and it’s too publicized. (Owner-manager, Case 2)

Discussion and Conclusions

The objective of this article was to explore the justifications used by the managers of SMEs to legitimize their lack of commitment to sustainability. The case studies conducted demonstrate that SD issues are to a great extent subordinate to economic concerns, which are generally used to justify the passivity of SMEs.

When faced with SD issues, SMEs are incentivized to legitimize behaviors deemed questionable by society through moral justifications, in order to make these behaviors appear more socially acceptable (Sykes & Matza, 1957). All respondents used techniques of neutralization to provide a moral justification for their passive or harmful behavior.

The importance granted to economic aspects illustrates that SD represents a conflicting logic for the SME managers interviewed. The techniques of neutralization managers articulated illustrate the difficulty of internalizing institutional pressures when these pressures appear—rightly or wrongly—as incompatible with more prominent organizational objectives (Boiral, 2014; De Clercq & Voronov, 2011; Oliver, 1991; Pache & Santos, 2010; Westermann-Behaylo et al., 2014). They thus also support an alternative logic that finds echoes in the business world (Campbell, 2007; De Clercq & Voronov, 2011), which confers their own legitimacy (Bitektine, 2011; Suchman, 1995). Thus, the dominance of institutional pressures favoring the mimetic adoption of SD is not necessarily recognized by managers of SMEs (Quirke, 2013; Scott, 2008). The testimonies of interviewees illustrate paradoxical tensions which lead them to resist but also to justify themselves when questioned on this topic (Oliver, 1991; Scott, 1991).

This study’s findings reveal that the techniques of neutralization employed to justify corporate unsustainability are mostly based on debatable opinions rather than facts. The ambiguity and imprecise definition of SD (Gray, 2010; Springett, 2003) may also have contributed to erroneous interpretations of this concept, to minimize its importance, and to fuel beliefs that managers have done enough in this area. Certain techniques of neutralization observed (e.g., small is beautiful, condemnation of the condemners, denial of negative impacts, minimization of sustainability issues) may reflect managers’ lack of understanding of an elusive concept that is perceived as either irrelevant or as not adapted to the priorities of SMEs.

Nevertheless, these techniques of neutralization are not necessarily cast in stone and managers’ opinions may evolve through open discussion, even if this angle has been overlooked in the institutional literature (Greenwood et al., 2011). In fact, such an evolution was unexpectedly observed in some organizations (notably Cases 1, 2, and 9) over the course of this study: After interviews with some managers who were initially reluctant to commit to sustainability, these managers implemented certain SD initiatives in the organization. For example, two businesses set up a system for recyclable materials after our interviews (Cases 2 and 9). Two businesses also asked the team’s researchers to provide them with simple tools to put SD initiatives into place (Cases 1 and 9). This allows us to confirm that organizations and their leaders are not passive actors in their institutional environments and that they may evolve with time (Hoffman, 1999; Oliver, 1991).

Contributions

This article contributes to the literature in several ways. First, the article proposes a relevant conceptual framework to analyze the justification of SME managers’ lack of commitment to sustainability and to illustrate the competing institutional logics that underpin them. As stressed by many researchers (e.g., Colquitt & Zapata-Phelan, 2007; Gioia & Pitre, 1990; Zahra & Newey, 2009), the transfer or adaptation of theories between fields and disciplines is one of the main avenues for theory building and tends to foster the development of new perspectives to analyze field data. Although the objective of this study was not to mechanically apply techniques of neutralization to the specific context of unsustainable SMEs, the main findings made it possible to explore the relevance of these techniques to managers’ justifications of corporate unsustainability. The legitimizing rhetoric of managers and its frequent disconnection from sustainability practices has been largely criticized in the literature (e.g., Cho et al., 2010; Jiang & Bansal, 2003). Nevertheless, this criticism has essentially remained general and unspecific. As a result, the specific arguments used to justify the lack of commitment have been largely overlooked. This study therefore contributes to bridge the gap between the literature on neutralization theory, which focuses mostly on the field of criminology and the research on corporate sustainability, which tends to ignore the legitimizing rhetoric used to justify inaction. Neutralization theory provides a new perspective to enable a better understanding of the nature and scope of this rhetoric.

Second, the study contributes to the literature on conflicting institutional pressures and the kinds of active resistance that organizations may use to confront them (Oliver, 1991). It has been demonstrated that SMEs’ resistance can be explained as much by organizational factors (i.e., limits and incapacities) as institutional ones (i.e., market functioning and consumer preferences), which confirms the heterogeneity of institutional logics and leaves greater latitude for organizational resistance (De Clercq & Voronov 2011; Oliver, 1991; Pache & Santos, 2010; Westermann-Behaylo et al., 2014). These results empirically illustrate organizational resistance in a specific context and the justification of managers reacting passively to institutional pressures for the integration of SD, two subjects which have been very little studied in the literature (Campbell, 2007; Kusyk & Lozano, 2007).

Managerial Implications

This study has implications for managers and stakeholders concerned with sustainability issues.

First, the focus on passive SMEs may help managers better understand conflicting logics and the main difficulties associated with sustainability in other organizations and encourage them to share their own experiences with these difficulties. The dominant optimistic rhetoric on corporate greening and the focus on proactive organizations may create guilt for many managers; however, interviewees appeared surprisingly frank and open in explaining their lack of commitment to sustainability. By shedding light on corporate unsustainability, this study may facilitate more open and frank exchanges with the many managers who are not significantly committed to SD. To this end, business associations concerned with sustainability issues could organize discussion groups to explain the lack of commitment in this area and its possible justifications. The techniques of neutralization identified in this article could help structure discussions in such groups and compare the different views expressed on this issue. For example, the findings of this study suggest that looking for a scapegoat and the condemnation of condemners, notably governmental agencies, occur quite frequently among SME managers. In order to facilitate managers’ involvement, encourage open debate, and prevent the possible feelings of guilt related to the lack of commitment to sustainability, these discussion groups could involve a small number of participants from passive SMEs. They could subsequently include managers from proactive organizations and stakeholders interested in sharing their views. This sharing could help managers better clarify, substantiate, and possibly question the legitimacy of their justifications for unsustainability by allowing them to compare their arguments with those expressed by other managers or stakeholders.

Second, assuming that some interconnectedness between ex post excuses and ex ante motivations of unsustainable behavior exists, this study may help stakeholders identify the reasons underlying the managers’ lack of commitment and the inherent tensions in adopting SD. Generally speaking, understanding the techniques of neutralization used contributes to develop a better understanding of individuals’ cognitive skills and their internalization of certain social norms (Peretti-Watel, 2003). The findings of this study can facilitate the development of initiatives that are better suited to these norms and that reflect the constitutive rules and specific context of SMEs. For example, governmental agencies and environmental associations could use these techniques to implement information programs for SMEs. In particular, the denial or minimization of certain sustainability issues such as global warming, which was observed in this study, could be addressed through information and awareness programs designed for managers of SMEs. Since techniques of neutralization are based on the use of various justifications to convince others and ourselves that misbehaviors are legitimate or excusable, one can assume that the development of environmental competences will contribute to reduce the perceived legitimacy of excuses for inaction. However, given the complexity and uncertainty associated with many sustainability issues, such as that of global warming, providing more information and knowledge in this area could have a perverse effect, causing certain passive managers to justify the status quo with new arguments based on partial and incomplete information. The same remark applies to discussion groups on this issue. Nevertheless, this type of perverse effect remains hypothetical and it should not discourage initiatives for promoting information, training, and group discussion.

Limitations and Avenues for Future Research

The study also has certain limitations, which call for further research in this area. The applicability of the results of this study is restricted because of the methodology used and the limitations of the sample in terms of size and the choice of companies with low SD commitment. This limitation is related to the case study method, which does not allow for the generalization of results, as it aims instead to understand complex phenomena (Eisenhardt, 1989). The results are thus specific and cannot be generalized to other geographic areas, countries, or cultures. Moreover, qualitative approaches are not suited to measurements and statistics (Gephart, 2004). As a result, it was not possible to measure the level of integration of the different components of sustainability inside organizations or the relationships between the techniques of neutralization observed and the specific context of each case studied (e.g., sector of activity, size, degree of environmental impact, and external pressures). Likewise, it was not possible to analyze the role of specific individual characteristics (e.g., the manager’s age, gender, or education level) in the emergence of neutralization techniques. Although all organizations studied belonged to the manufacturing sector, were established in the same Canadian province, and were exposed to similar institutional pressures, it is possible that contextual variables influenced the emergence of different neutralization techniques. For example, one can assume that the external pressures around specific issues, such as the major spillage of harmful substances, would give rise to new neutralization techniques. The size of the organization could also have an impact on the legitimation of corporate unsustainability, although this was not observed in this study. Nevertheless, the verification of such an assumption would require quantitative studies based on a larger and more diversified sample. These studies could also shed more light on the reasons for the occurrence and frequency of different techniques of neutralization: economic situation, sector of activity, size, and environmental issues, among others.

Nevertheless, no matter what issues future research on the techniques of neutralization and corporate (un)sustainability focuses on, the collection of data may be challenging because of the social desirability bias and social pressures associated with environmental and ethical issues. These biases and pressures certainly explain the emphasis in the mainstream literature on legitimacy theories, which are more in line with the current dominant social paradigm. The concept of techniques of neutralization illuminates hidden and controversial aspects that, while difficult to explore, are probably more relevant to explain how sustainability issues are really perceived and managed inside a large number of organizations.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.