Abstract

Although the literature has shown the benefits of corporate environmental reputation, little is known about how this reputation develops. Based on impression management theory, we examine how a firm’s environmental practices create its environmental reputation. We undertake a fine-grained analysis by distinguishing between high and low environmental external visibility practices and examining the effect of decoupling environmental practices (i.e., using only practices that are highly visible) on environmental reputation. We also propose that corporate environmental disclosure moderates these relationships. The hypotheses are tested on a sample of 241 U.S. firms included in Newsweek’s Green Rankings. Our results suggest that managers should avoid decoupling because such practices heavily jeopardize environmental reputation. In contrast, developing a balanced set of both high and low environmental external visibility practices, enhanced through environmental disclosure, pays for environmental reputation.

Keywords

Introduction

Over the past two decades, the natural environment and environmental sustainability have become significant social issues (Hart & Dowell, 2011; Norheim-Hansen, 2015). Environmental regulations are increasingly stringent (Rugman & Verbeke, 1998), and firms’ constituents demand more environmentally responsible behaviors. Firms are aware of the relevance of environmental concerns (Henriques & Sadorsky, 1996) and the possible risks of not improving their environmental footprints (Buysse & Verbeke, 2003). Because firms search for behaviors that are rewarded by their constituents (Dowell, Sastry, Hart, & Bernicke, 1997), firms have progressively incorporated the natural environment into their strategic decision making (Judge & Douglas, 1998; Sharma & Vredenburg, 1998). The inclusion of the natural environment in corporate strategies represents the firms’ efforts to generate value regarding the natural environment for their constituents (Buysse & Verbeke, 2003). When constituents interpret that a firm creates value in the environmental dimension, the firm gains in corporate environmental reputation (Philippe & Durand, 2011).

Empirical scholarship has recognized the benefits of a firm’s environmental reputation. For example, a firm that is well known for being environmentally committed increases its ability to attract talented employees (Reinhardt, 1999) and investors (Delmas & Blass, 2010). Consumers prefer to buy products and acquire services from companies with a favorable environmental reputation (Biloslavo & Trnavčevič, 2009). Such a reputation can also help promote alliance formation (Norheim-Hansen, 2015). Moreover, evidence shows that environmental reputation is positively associated with a firm’s general reputation (Tang, Lai, & Cheng, 2012).

Although the literature has demonstrated the benefits of corporate environmental reputation, little is known about its development to date. Previous research on the formation of environmental reputation has focused mainly on the role of corporate environmental disclosure. These studies have drawn attention to qualitative aspects of the statements disclosed, such as quality and level of detail (Toms, 2002), content of environmental disclosures, and level of procedural commitment (Philippe & Durand, 2011). However, the effect of other firms’ environmental practices on environmental reputation remains unexplored.

Based on impression management theory, we examine how a firm’s environmental practices create an environmental reputation. We undertake a fine-grained analysis by distinguishing between environmental practices with low and high external visibility. Visibility is “the extent to which phenomena can be seen or noticed” (Bowen, 2000, p. 93) and “the extent to which a particular firm task is easily observable or attracts the attention of the public” (Jiang & Bansal, 2003, p. 1058). We consider high environmental external visibility practices as those easily noticed by external constituents of the firm. For example, certifications of environmental management systems (EMS) such as ISO 14001 are highly visible externally, since they are easy for firms to display and for the public to confirm. Jiang and Bansal (2003) argue that firms adopt this EMS because it is highly visible to firm’s constituents. Other examples of environmental practices with high external visibility include participation in voluntary government programs (such as the Environmental Protection Agency’s WasteWise program), environmentally oriented board committees, environmental trademarks, and environmental pay policies (Berrone, Gelabert, & Fosfuri, 2009). In contrast, we define low environmental external visibility practices as actions that are difficult for external constituents such as nongovernmental organizations, consumers, investors, and the general public to see.

We also analyze the effect of decoupling environmental practices on environmental reputation. Environmental decoupling occurs when firms develop only environmental practices that are highly visible externally, ignoring practices with low external visibility (usually proactive environmental production practices that improve environmental performance) creating a false image among their constituents. This definition follows previous definitions of decoupling (e.g., Ansari, Fiss, & Zajac, 2010; Crilly, Zollo, & Hansen, 2012; Westphal & Zajac, 2001), although many terms (e.g., hypocrisy, greenwashing, etc.) have been used to designate the concept. We propose that corporate environmental disclosure acts as a moderator of the relationship between environmental practices and environmental reputation, and predicts moderating effects of disclosure for high and low external visibility environmental practices. We also consider the role of the firm’s environmental disclosure in the relationship between environmental decoupling and environmental reputation.

We tested the hypotheses on a sample of 241 U.S. firms included in Newsweek’s Green Rankings (Newsweek Staff, 2010), and the results make important contributions to the extant literature. First, research on impression management theory and organizations has been limited (Bolino Kacmar, Turnley, & Gilstrap, 2008), and we extend application of impression management theory at the organizational level of analysis to a new context, that of environmental issues. Second, we contribute to identification of the determinants of environmental reputation by identifying environmental practices as determinants of environmental reputation that shape the perceptions of the firm’s constituents. Third, we contribute to research on environmental disclosure. Previous studies have focused mainly on the direct effect of corporate environmental disclosure on environmental reputation (e.g., Cho, Guidry, Hageman, & Patten, 2012; Philippe & Durand, 2011). We extend this prior work by demonstrating that environmental disclosure can also moderate the relationship between a firm’s environmental practices and its environmental reputation.

Theoretical Background

Organizational Impression Management Theory and Corporate Environmental Reputation

Although impression management has traditionally been used in psychology to describe self-promotional behavior at the individual level (Talbot & Boiral, 2015), impression management also occurs at the organizational level (Bolino et al., 2008). As social actors, firms pursue self-promotion and self-presentation (Highhouse, Brooks, & Gregarus, 2009) based on their desire to garner respectability and impressiveness from their constituents (Highhouse et al., 2009). Organizational impression management then consists of “any action that is intentionally designed and developed to influence an audience’s perceptions of the organization” (Bolino et al., 2008, p. 1095).

The firm’s actions act as cues that signal corporate images in the minds of their constituents (Highhouse et al., 2009), such as the image of being a socially responsible firm or good employer (Highhouse et al., 2009). Constituents use these cues to form individual impressions of the firm. Individual impressions aggregated with other people’s impressions over time constitute corporate reputation (Highhouse et al., 2009). Corporate reputation refers to “the perceptions by a firm’s audience about the firm’s ability to provide value compared with its peers and rivals” (Philippe & Durand, 2011, p. 971). Firms can create value along financial and nonfinancial dimensions (Rindova & Fombrun, 1999; Rindova, Pollock, & Hayward, 2006), and we will refer to assessment along the environmental dimension as corporate environmental reputation (Philippe & Durand, 2011).

Audiences’ perceptions of the firm are at the heart of formation of corporate reputation. To shape audiences’ perceptions, firms undertake the actions expected to make the most desirable impression (Gardner & Martinko, 1988). The success of these actions depends on the extent to which the firm’s performance is perceived as congruent with constituents’ definition of a situation (Gardner & Martinko, 1988). When the level of congruence is high, the firm is more likely to create a positive impression among its constituents and achieve a favorable response. Behavior perceived as inappropriate is more likely to generate negative impressions and reactions (Gardner & Martinko, 1988).

Society’s increasing concerns about the natural environment are placing environmental management a prominent issue on the corporate agenda (Bansal, 2005; Henriques & Sadorsky, 1999; Kramer & Porter, 2011). Firms adopt a variety of environmental practices with low and high visibility in an effort to conform to constituents’ environmental expectations, obtain legitimacy, and create and preserve environmentally friendly images (Bansal & Clelland, 2004; Hart, 1995), which ultimately influence their environmental reputation. For example, firms can implement externally low visible actions to reduce their greenhouse gas emissions or high externally visible actions, such as the signature of an international commitment to enhance their reputation. Problems may arise, however, when firms attempt to create an image that does not correspond to their actual practice or implementations. This is the case of decoupling environmental practices that consist of adopting highly visible environmental practices without implementing low external visibility actions, that usually require significant changes in core practices (Berrone & Gomez-Mejia, 2009; Christmann & Taylor, 2001).

In this article, we analyze how low and high environmental external visibility practices and decoupling environmental practices contribute to the formation of environmental reputation. We also examine the moderating role of corporate environmental disclosure in the relationships between environmental practices and environmental reputation. Previous studies have tested the direct effect of environmental disclosure as a highly visible practice on environmental reputation (e.g., Cho et al., 2012; Philippe & Durand, 2011). We consider corporate disclosure as a powerful tool that not only enhances the effect of both low- and high-visibility environmental practices on environmental reputation but also affects the relationship between environmental decoupling and environmental reputation.

Hypotheses

Environmental Practices and Corporate Environmental Reputation

Firms face increasing pressures to engage in sustainable behaviors (Henriques & Sadorsky, 1999). Environmental claims to protect the natural environment emerge from a variety of a firm’s constituents, including government, communities (nonprofit organizations, local groups of neighbors, and social activists), shareholders, customers, and employees (Henriques & Sadorsky, 1996, 1999). To shape audiences’ perceptions of their environmental images, firms adopt a variety of environmental practices that differ in their degree of external visibility. Visibility refers to “the extent to which phenomena can be seen or noticed” (Bowen, 2000, p. 93) and to “the extent to which a particular firm task is easily observable or attracts the attention of the public” (Jiang & Bansal, 2003, p. 1058). Some examples of environmental practices that are easily visible externally include certified EMS or the participation in voluntary government programs. Through highly visible practices, firms attempt to project the impression that they have a truly proactive commitment to the natural environment (Bansal & Clelland, 2004; Berrone et al., 2009). Constituents will get the firm’s information that they can perceived easily, the firm’s actions that are externally highly visible. Since reputation is about the aggregation of individual impressions (Highhouse et al., 2009), we state that a firm’s environmental practices with high external visibility will positively contribute to corporate environmental reputation. The more people view the firm in high regard for its visible environmental commitment, the better its environmental image and, ultimately, its environmental reputation.

Low environmental external visibility practices, in contrast, usually require significant changes in core practices, entail some risks, and are difficult for external constituents such as nongovernmental organizations, consumers, or investors to see. They include pollution prevention strategies and environmental innovation in internal processes (Berrone & Gomez-Mejia, 2009; Christmann & Taylor, 2001). We might expect low environmental external visibility practices to have limited or no effect on a firm’s reputation, as it is very difficult for constituents to develop a positive impression of a firm if they cannot perceive its proactive environmental behavior. However, we argue, that their contribution to reputation depends on the type of constituent, the constituent’s relationship to the firm, and the amount of information the constituent proactively collects about the firm. For example, investors closely look at the firm’s environmental practices because poor environmental behavior affects their investment. Previous research has shown that companies with a larger stock of environmental resources may experience a smaller loss in the case of an eco-harmful event because they are better insured against such events (Flammer, 2013). Constituents that invest time and effort in collecting information on the firm’s environmental behavior may thus identify not only highly visible practices but also those that are more difficult to see externally.

Just as each environmental practice (high-/low-visibility) addresses a different environmental issue, each group of constituents may make different environmental demands based on its relationship with the company. Consumers may pay more attention to the environmental footprints of the products they consume, whereas employees familiar with the firm’s operations may be concerned about whether the firm uses recycled materials. A firm that adopts a diverse set of environmental practices is thus more likely to satisfy the environmental demands of a wider range of constituents. Basdeo, Smith, Grimm, Rindova, and Derfus (2006) found that the number of market signals was positively associated with corporate reputation because it provided constituents with more information about the firm’s market strategy. Since adopting a broad set of practices gives the firm’s constituents more information about the firm’s environmental commitment, firms that adopt both high- and low-visibility environmental practices will develop a favorable environmental reputation by meeting the expectations of a wider audience.

Based on this reasoning, we suggest the following hypotheses:

The Moderating Effect of Environmental Disclosure on the Relationship Between Environmental Practices and Corporate Environmental Reputation

Although adopting a set of environmental practices can earn the firm a favorable environmental reputation, some constituents have difficulty obtaining and analyzing the environmental information to develop their perceptions. Corporate environmental disclosure is a powerful tool to enhance the effect of both low and high external visibility environmental practices on environmental reputation.

Disclosure of environmental information on its products and processes (Bansal & Clelland, 2004) can change constituents’ perceptions of the firm’s commitment to the natural environment, as the firm gives constituents valuable information with which to evaluate its environmental commitment (Philippe & Durand, 2011). Firms can choose among different socially acceptable modes of disclosure, including annual reports, sustainability reports, and websites (Philippe & Durand, 2011). Sustainability reporting, for example, has become widespread among large companies; nearly 95% of the world’s 250 largest companies publish sustainability reports (Talbot & Boiral, 2015). Firms that disclose information on their environmental behavior attempt to align with their constituents’ demands, emphasizing the congruence between the firm’s values and actions and those deemed appropriate by society (Deephouse, 1996; Suchman, 1995) to enhance the positive effect of these practices on their environmental reputation.

Disclosure can intensify the prominence of visible environmental practices in the eyes of constituents, since developing a favorable reputation depends on constituents’ awareness of corporate activities (Du, Bhattacharya, & Sen, 2010). Research on the direct impact of environmental disclosure on environmental reputation showed its positive influence on audience perceptions of the firm’s environmental commitment and thus its environmental reputation (Philippe & Durand, 2011; Toms, 2002). The positive effect of highly visible practices on a firm’s environmental reputation will thus be augmented by corporate environmental disclosure.

Disclosure can also increase the visibility of practices that are more difficult for constituents to see. Firms build reputations not just by words but—perhaps even more important—by actions (Deephouse, 2000). Since constituents prefer actions that represent true commitment to environmental issues (Berrone et al., 2009), firms that meet minimal standards to gain social approval are likely to continue such action to become the most admired (Staw & Epstein, 2000). Disclosure of environmental information can increase the positive effect of implementation low external visibility practices by strengthening credibility of the firm’s environmental commitment. Credibility is at the core of building a favorable environmental reputation (e.g., Connelly, Certo, Ireland, & Reutzel, 2011; Hart, 1995). In fact, building a positive reputation without the trust of a firm’s stakeholders is very difficult (Robertson, 2008). We thus expect environmental practices with low and high external visibility to have a positive effect on development of environmental reputation. Based on this reasoning, we propose the following hypotheses:

Decoupling Environmental Practices and Environmental Reputation

Firms can show an alignment between their organizational values and societal values by adopting practices that are consonant with societal expectations and demands (Meyer & Rowan, 1977; Oliver, 1991). If conforming to constituents’ environmental expectations gains firm’s legitimacy and reputation (Bansal & Clelland, 2004; Hart, 1995), the easiest way to achieve such gains is by “adopting certain visible and salient practices that are consistent with social expectations while leaving the essential machinery of the organization intact” (Ashforth & Gibbs, 1990, p. 181). We consider that decoupling happens when the environmental practices developed by the firm are composed solely of environmental practices with high external visibility while ignoring completely practices with low visibility. Decoupling aims to manipulate societal perceptions by using highly visual actions to obtain legitimacy or acceptance (Ashforth & Gibbs, 1990; Bansal & Clelland, 2004; Jiang & Bansal, 2003; Meyer & Rowan, 1977), thereby enhancing a firm’s environmental reputation. When a firm deceives their constituents and the general public by implementing decoupling environmental practices, it creates a false environmental image.

Firms may apply decoupling practices, if they do not perceive adverse consequences (e.g., Christmann & Taylor, 2006), in response to certain internal and external factors (e.g., Weaver, Treviño, & Cochran, 1999). However, a company needs to combine high-visibility practices with practices that are less visible (Bowen & Aragon-Correa, 2014), which usually require substantive changes in core practices and imply risks (e.g., Berrone et al., 2009; Ferrón-Vílchez, 2016) to achieve legitimacy and enhance performance. Ferrón-Vílchez (2016) found that companies adopt ISO 14001 certification for legitimizing their environmental behavior, henceforth, as a cue to enhance their environmental image; however, this author concluded that only firms that implement additionally environmental practices with low visibility show improvements in both environmental and business performances. Thus, it seems that firms’ actions need to be congruent with their audience’s idea of what constitutes ideal behavior.

When a company lacks such congruence, constituents can penalize it. The audience perceives the organization as hypocritical, resulting in loss of credibility (Wagner, Lutz, & Weitz, 2009) and damage to its image. Philippe and Durand (2011) found that congruence and balance between low- and high external visibility practices are necessary to shape environmental reputation in environmentally sensitive industries. Companies that adopt decoupling environmental practices may fail to enhance their environmental reputations (Darnall & Edwards, 2006). Pursuing legitimacy or audience ideal is thus a double-edged sword (Ashforth & Gibbs, 1990).

Recent studies suggest that decoupling environmental practices do not pay off the effort. Walker and Wan (2012) found that decoupling practices (discrepancy between green talk and green walk) had a negative effect on financial performance in firms operating in dirty industrial sectors. Wu and Shen (2013) did not discover any relationship between decoupling practices and financial performance in nonpolluting sectors such as banking. Consumer behavior literature also sheds light on decoupling. For example, Aji and Sutikno (2015) demonstrated that the use of marketing practices (public relations, advertising, or marketing), to create the deceptive perception that a product or service is “green,” was positively associated with green consumers’ skepticism and loss of trust. This research suggests that the public may tire of being deceived and penalize companies that are not congruent.

Nowadays, access to environmental performance information is greater and better than ever, and the general public—especially external constituents, such as nongovernmental organizations or media—often accesses a company’s real environmental performance. For example, firms’ emissions and pollution data are published in the United States’s Toxics Release Inventory and similar programs in other countries, enabling the public and other constituents to determine how significant a firm’s practices are in reducing pollution. Furthermore, environmental consciousness is increasing in the United States and other developed countries, as the demand for information about sustainability actions (Eagan, Wiese, & Liebl, 2001). Higher demand can pressure media to be more vigilant and to publish more such news, particularly about very visible firms, as very large or publicly owned firms are subject to more scrutiny. Bansal and Roth (2000) concluded that more visible firms are prone to comply with norms due to greater social pressure. Similarly, Kim and Lyon (2011) observed that companies reduce decoupling strategies (greenwashing and brownwashing 1 ) when scrutiny is higher. More generally, Rindova et al. (2006) argued that a firm’s visibility may determine the extent to which audiences perceive the firm’s image.

We argue that large firms (e.g., the 500 largest publicly traded U.S. companies) are more visible and subject to more scrutiny, as they receive more attention from external constituents such as media and nonorganizational groups. Such scrutiny can expose their environmental actions and behaviors. In this scenario, decoupling practices are far less effective, as these firms have a greater chance of being caught. Firms that develop an environmental strategy based on decoupling practices may thus suffer a loss of environmental reputation.

The Moderating Effect of Environmental Disclosure on the Relationship Between Decoupling Practices and Corporate Environmental Reputation

The negative effect of decoupling on a firm’s environmental reputation may be amplified through disclosure of these practices. Firms recognize their constituencies’ increasing demand for sustainable information (Eagan et al., 2001) and seek to increase transparency (Aras & Crowther, 2009). In its 2015 survey, the consultancy KPMG (2015) indicated that 73% of the largest companies per country and 92% of the Global 250 companies have issued some type of corporate social responsibility (CSR) report, indicating that the main driver of CSR reporting is legislative and affirming “a growing trend of regulations requiring companies to publish nonfinancial information” (p. 30). Furthermore, Cho, Michelon, Patten, and Roberts (2015) argued that firms can increase CSR disclosure to seek better CSR ratings and augment likelihood of membership in social responsibility investment funds or social indexes, since all the causes mentioned can promote improved stakeholder relationships.

Some studies argued that firms with greater environmental disclosure have better environmental performance (e.g., Clarkson, Li, Richardson, & Vasvari, 2011; Mallin, Michelon, & Raggi, 2013) because good performers want their stakeholders to know about their performance. A company with a higher degree of disclosure will ensure that its constituents are more informed of and become familiar with the firm’s environmental efforts, and constituents will appreciate the firm’s environmental commitment (Alon & Vidovic, 2015). What happens, however, if the company develops decoupling practices and discloses them?

Prior research on the role of disclosure in the relationship between environmental and organizational performance found that firms with no reporting and poor environmental performance scores achieve higher market value (Mervelskemper & Streit, 2017). This finding may suggest that when the content of environmental disclose is not good, it might be better to hide it. Nevertheless, companies may need to disclose information in order to enhance their reputations, as reputation is a valuable resource (Petrick, Scherer, Brodzinski, Quinn, & Ainina, 1999; Roberts & Dowling, 2002).

Since reputation is built over time, in a continuous and relentless process (Fombrun & Shanley, 1990), companies must be persistent and consistent in their signals. Firms that reveal and update progress regularly to achieve a stable image cannot simply stop disclosing if they wish to continue to build their reputation. According to Lyon and Montgomery (2015, p. 228), “a failure to disclose information will be interpreted as an admission of poor performance (Milgrom, 1981) and attempts to hide information will fail [ . . . ], then a failure to disclose may simply indicate that the firm itself is not fully informed (Krishna & Morgan, 2001).” Lack of self-disclosure can, then, damage a firm’s image. Firms’ constituents increasingly require disclosure as a cue shaping the firm’s image (Delmas & Burbano, 2011). Self-disclosure of environmental information is necessary to achieve acceptance and legitimacy (Pollock & Rindova, 2003), to avoid damage to the firm’s credibility (Lokuwaduge & Heenetigala, 2017), and just to continue to build its image. According to Lyon and Maxwell (2011), some constituencies “increasingly interpret nondisclosure as withheld negative information rather than as true uncertainty on the part of the manager” (p. 27).

As result, companies can be compelled to disclose their environmental information even when this information is not positive or is limited to decoupling environmental practices. Some studies outline possible negative outcomes of environmental disclosure. For instance, Cormier and Magnan (2015) concluded that a discrepancy between disclosure and performance can severely damage the company’s credibility among financial analysts and legitimacy in the community at large. If the firm that develops decoupling environmental practices thinks that these practices can positively affect its reputation, this firm can also believe that reporting and disclosing these practices will amplify the positive effect on its reputation. However, disclosure of such decoupling can undermine the firm’s reputation deeply because the company is publicizing actions that its constituencies view not as achievements but as deception.

Methodology

Sample

Our sample was derived from the list of companies included in Newsweek’s Green Rankings 2010. This ranking provides data about environmental reputation for the 500 largest publicly traded U.S. companies measured by revenue, market capitalization, and number of employees. We used this sample because our measure of environmental reputation was based on this ranking. As the result of financial and environmental data availability, our final sample consisted of 241 U.S. firms (48.2% of the initial sample). The industry composition of the sample was the following: 6.22% mining (SIC10-14); 0.04% construction (SIC15-17); 50.62% manufacturing (SIC20-39); 5.81% transportation and communications (SIC40-48); 11.20% utilities (SIC 49); 10.79% wholesale and retail trade (SIC50-59); 7.88% finance, insurance, and real estate (SIC60-67); and 7.05% services (SIC70-89).

Variables

Environmental Reputation

We used the environmental reputation score reported by Newsweek to measure environmental reputation. This measure is consistent with previous studies that have examined the formation of environmental reputation (e.g., Cho et al., 2012; Tang et al., 2012). The environmental reputation score was obtained through a survey that captured the opinions of CSR professionals, academics, and other environmental experts. The CEOs of the 500 U.S. companies listed in Newsweek were also invited to participate in the survey.

Some prior studies of environmental reputation have been based on Fortune’s scores, obtained from the “community and environmental friendliness” dimension published in the Fortune Most Admired Companies Annual Report (e.g., Philippe & Durand, 2011; Toms, 2002). However, limitations of Fortune’s reputation measures have been widely described in previous studies (e.g., Brown & Perry, 1994). Furthermore, we find at least two main strengths of using Newsweek’s environmental reputation scores instead of Fortune’s. First, Newsweek’s survey captures the opinions of a broader range of constituents, including CSR professionals, academics, and other environmental experts and CEOs, whereas Fortune’s ratings are restricted to the responses of company executives, directors, and financial analysts. Second, the environmental reputation scores from Newsweek provide a more precise measure of environmental reputation because respondents were asked to assess opinions on environmental performance only, not on other social issues related to the community as a whole.

Environmental Practices

Data on firms’ environmental practices were drawn from KLD STATS (KLD Research & Analytics, 2008). The KLD database, used extensively in the management literature (e.g., Graves & Waddock, 1994; Hillman & Keim, 2001; Johnson & Greening, 1999; Turban & Greening, 1997), provides ratings for companies on corporate social behavior regarding community, diversity, employee relations, natural environment, human rights, products, and corporate governance. Each of these categories rates a set of “strengths” and “concerns” using a binary measure. Previous studies have identified concerns as a measure of corporate irresponsibility and strengths as a measure of corporate responsibility (Strike, Gao, & Bansal, 2006). As we are interested in positive environmental practices, we focused on strengths included in the environmental category available in 2009: development of beneficial products and services, pollution prevention programs, recycling, clean energy, management systems, and other practices that demonstrate a commitment to the natural environment.

Based on the concept of visibility in Bowen (2000), which refers to “the extent to which phenomena can be seen or noticed” (p. 93), we classified the items beneficial products and services, pollution prevention, recycling, and clean energy as low environmental external visibility practices. These practices are difficult for external constituents to see and usually require significant changes in a firm’s core practices to improve its environmental performance. We classified the items management systems and other strengths (including management systems and commitment to other environmental programs) as high environmental external visibility practices because these practices can be easily observed by the firm’s constituents. Although adoption of an EMS is an act internal to the firm, the ISO 14001 certification is a highly visible public signal (Barla, 2007). Moreover, adoption of an EMS indicates commitment but may or may be not fully implemented. Environmental management programs such as ISO 14001 have also been described as cosmetic practices oriented to external constituents that seek merely to create facade when not adopted with high-quality commitment to the requirements (e.g., Ashforth & Gibbs, 1990; Barla, 2007; Darnall & Kim, 2012; van Halderen, Bhatt, Berens, Brown, & van Riel, 2016).

Environmental Disclosure

This variable measures the extent of a company’s Environmental, Social, and Governance disclosure. It is based on the environmental disclosure score included in the Bloomberg database, a financial services system that provides current and historical financial, economic, and government information on all market sectors worldwide. This variable ranges from 0.1 for firms that disclose a minimum of environmental data to 100 for firms that disclose all of the environmental data collected by Bloomberg. Each data item is weighted in terms of importance. For example, data on greenhouse gas emissions carry greater weight than other environmental disclosures. Furthermore, since the disclosure score is tailored to different industry sectors, each company is only evaluated in terms of the data relevant to its industry sector. Companies not covered by the Environmental, Social, and Governance group will have no score, and companies that do not disclose information are excluded.

Decoupling Environmental Practices

We consider a firm to develop decoupling environmental practices when its environmental practices are composed solely of high environmental visibility practices and ignore low environmental visibility practices. To create the decoupling environmental practices variable, we first restricted the initial sample (241 firms) to firms that adopted any type of environmental practice, a total of 120 firms. Of these 120 firms, 24.2% did not develop any low-visibility practice but did adopt at least one high-visibility practice. The decoupling environmental practices variable takes the value of 1 when the firm only develops high-visibility environmental practices but does not adopt any low-visibility environmental action, and the value of 0 otherwise. Through this variable, we attempt to capture whether or not a firm adopts decoupling environmental practices.

Control Variables

Financial Performance

Previous studies have shown that financial performance may be positively related to reputation because superior financial performance may influence constituents to evaluate a firm more favorably (e.g., Deephouse, 1996; Deephouse & Carter, 2005; Fombrun & Shanley, 1990). We use return on assets in 2009 as a proxy of previous financial performance. Data on financial performance were collected from the Compustat North America database.

Size

A firm’s size may be positively related to its reputation (Deephouse, 1996; Deephouse & Carter, 2005). Size also influences a firm’s visibility and the relationships with its environment (Deephouse, 1996). We used the Napierian logarithm of total assets in 2009 in thousands of dollars to control for size. Data on total assets were extracted from the Compustat North America database.

Sensitive Industry

We included industry dummies to control for sensitive industries. This variable takes the value of 1 if a firm operates in an environmentally sensitive industry and 0 otherwise. Following Villiers, Naiker, and van Staden (2011), sensitive industries include the following SIC codes: 800-899 (forestry), 1000-1099 (metal mining), 1200-1399 (coal mining and oil and gas exploration), 2600-2699 (paper and pulp mills), 2800-3099 (chemicals, pharmaceuticals, and plastics manufacturing), 3300-3399 (iron and steel manufacturing), and 4900-4999 (electricity, gas, and waste water).

Capital Intensity

Firms that undertake capital-intensive activities are likely to generate more pollution (Bansal, 2005) and attract the attention of constituents. We measured capital intensity as the value of the plant’s property and equipment divided by sales in 2009 (Bansal, 2005; Sharma & Kesner, 1996).

Results

We tested our hypotheses using a moderated regression model. Table 1 reports descriptive statistics and correlations for the study variables. In the moderation regressions, we centered the independent variables to reduce potential problems of multicollinearity. After each regression, we also calculated the variance inflation factor. None of the variance inflation factors exceeded 1.4, values well below the conservative limit of 2.5 (Allison, 1999), indicating that multicollinearity was not a problem.

Means, Standard Deviations, and Correlations. a

Note. Table contains Pearson’s correlation coefficient.

n = 241. bMean, SD, and correlation for this variable are based on n = 120.

Significant at †p = .10. *Significant at p = .05 **Significant at p = .01. ***Significant at p = .001.

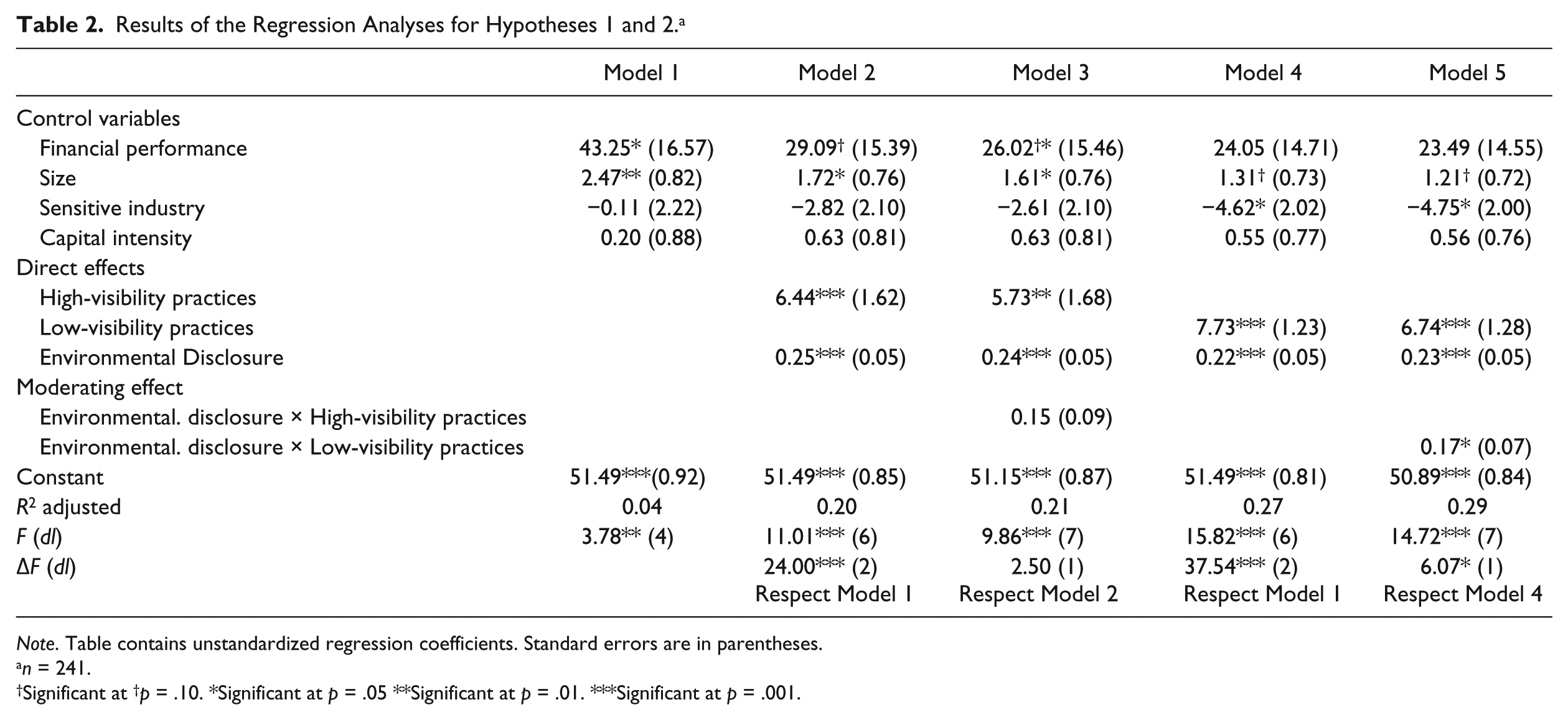

Table 2 provides the results of the regression analyses for Hypotheses 1 and 2. Model 1 shows the results for the control variables. Financial performance and firm size are statistically significant and have a positive impact on environmental reputation. We used the F test in every model to measure the improvement from one model to another as a result of incorporating variables in each step.

Results of the Regression Analyses for Hypotheses 1 and 2. a

Note. Table contains unstandardized regression coefficients. Standard errors are in parentheses.

n = 241.

Significant at †p = .10. *Significant at p = .05 **Significant at p = .01. ***Significant at p = .001.

Hypotheses 1a and 1b propose that a firm’s environmental practices with high and low external visibility contribute positively to corporate environmental reputation. Models 2 and 4 show that the direct effect of both types of environmental practices on corporate environmental reputation is positive and statistically significant, supporting Hypotheses 1a and 1b.

Models 3 and 5 include the moderating effect of environmental disclosure on the relationship between high and low environmental external visibility practices and corporate environmental reputation. Model 3 tested the moderating effects for highly visible practices. The results show that the moderating effect of environmental disclosure is not statistically significant. Comparison of Model 3 (moderation effect of disclosure on relationship between highly visible practices and environmental reputation) with Model 2 (direct relationship without any moderating effect) shows that the F test is not significant (ΔF =2.50 | p = .116). Thus, our data do not support Hypothesis 2a.

In Model 5, we tested the moderating effect of disclosure for low environmental visibility practices. The moderation coefficient is statistically significant. In addition, when we compare Model 5 with Model 4, the F test indicates that the improvement significant (ΔF = 6.07 | p = .014). Figure 1 shows that the effect of low environmental visibility practices on environmental reputation is more intense with high environmental disclosure than with low. Model 3 improved due to incorporation of the moderation effect, but Model 5 did not. The positive moderating effect of environmental disclosure on the relationship between environmental practices and environmental reputation is thus supported for low environmental external visibility practices but is not statistically significant for highly externally visible practices, supporting Hypothesis 2b.

The moderating effect of environmental disclosure on the relationship between low environmental external visibility practices and corporate environmental reputation.

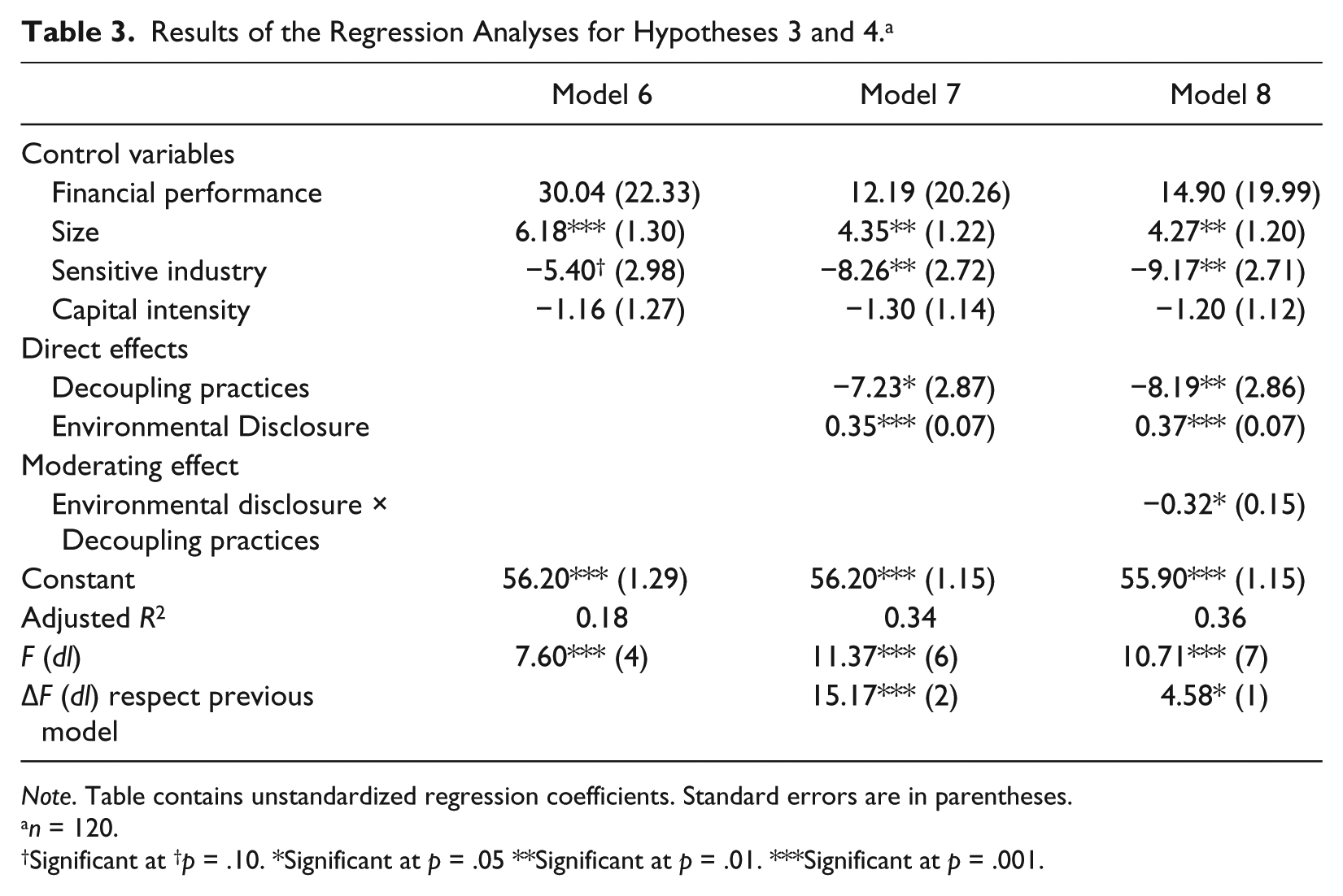

Finally, Table 3 reports the results of Models 6, 7, and 8 to test Hypotheses 3 and 4. Model 6 is the baseline model with the control variables. Model 7 shows that the direct effect of decoupling environmental practices on corporate environmental reputation is negative and statistically significant, supporting Hypothesis 3. Model 8 includes the results for the moderating effect of environmental disclosure on the relationship between decoupling environmental practices and environmental reputation. The moderation term is statistically significant. Additionally, the F test comparing Model 8 to Model 7 indicates that the improvement of the model is significant (ΔF = 4.58| p = .035).

Results of the Regression Analyses for Hypotheses 3 and 4. a

Note. Table contains unstandardized regression coefficients. Standard errors are in parentheses.

n = 120.

Significant at †p = .10. *Significant at p = .05 **Significant at p = .01. ***Significant at p = .001.

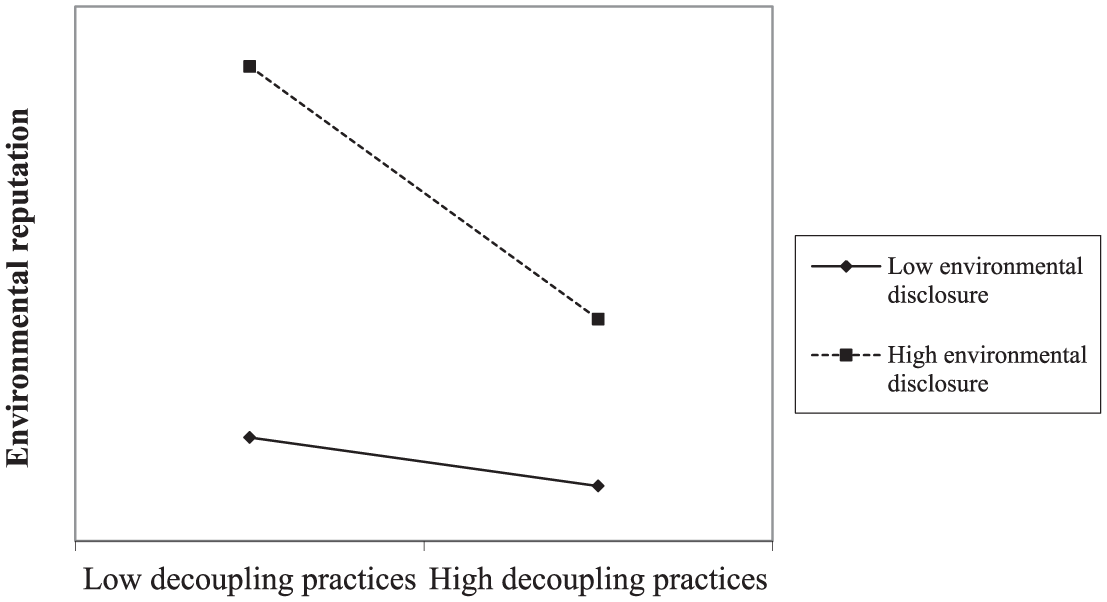

Figure 2 shows that decoupling practices have an important negative effect on firms with high levels of environmental disclosure, but the effect of decoupling practices on environmental reputation is less intense when the level of environmental disclosure is low. Therefore, Hypothesis 4 is also supported.

The moderating effect of environmental disclosure on the relationship between decoupling practices and corporate environmental reputation.

Discussion

This study aims to explain the effect of environmental practices on corporate environmental reputation. We distinguished between low and high environmental external visibility practices and tested their effects on corporate environmental reputation. To examine whether firms can build their environmental reputation based solely on high-visibility practices, we explored the impact of decoupling environmental practices on this reputation. Our findings reveal that a firm’s environmental practices (low visibility, high visibility, and decoupling) contribute to the formation of corporate environmental reputation. In addition, environmental disclosure plays a significant role in moderating the relationships between environmental practices and environmental reputation. This study has important research and managerial implications, which we now discuss.

Contributions and Implications for Research

First, this research extends existing work on organizational impression management theory. Research on impression management theory at the organizational level of analysis has been limited (Bolino et al., 2008), and most of this organizational literature has focused on impression management as a way firms can legitimize their behaviors (e.g., Bansal & Clelland, 2004; Bansal & Kistruck, 2006; Talbot & Boiral, 2015). For example, Talbot and Boiral (2015) analyzed 10 case studies of large Canadian industrial emitters and their practices to manage impressions and legitimize their impact on climate change. Application of this theory to explain other organizational outcomes, such as reputation, has been even more limited, with a few exceptions (e.g., Highhouse et al., 2009). In this study, we contribute to extend the application of impression management theory to organizations in the context of environmental issues.

Second, this article makes an important contribution by identifying some determinants of corporate environmental reputation. We found that corporate environmental practices with high and low external visibility can positively affect constituents’ perceptions about firms’ environmental commitment. Previous empirical studies have found that environmental disclosure (Cho et al., 2012; Dowell et al., 1997; Philippe & Durand, 2011; Toms, 2002), holding a membership in the Dow Jones Sustainability Index (Cho et al., 2012), and environmental governance (Tang et al., 2012) are some precursors of environmental reputation. Our work extends this research by showing that high and low environmental external visibility practices, such as the development of beneficial products and services, pollution prevention programs, recycling, clean energy, and management systems, can contribute to building a favorable environmental reputation. Our findings derived from Hypotheses 1a and 1b are also consonant with prior research on the formation of general reputation. For example, Basdeo et al. (2006) found that the total amount of market actions positively influenced a firm’s reputation. Our work also provides evidence of the impact of a firm’s low- and high-visibility actions on the development of its environmental reputation.

In addition, we investigated how a firm’s environmental disclosure can influence the relationship between environmental practices and environmental reputation. Our results support the positive moderating effect of environmental disclosure on the relationship between low environmental external visibility practices and corporate environmental reputation (Hypothesis 2b), but this effect is not statistically significant for externally highly visible practices (Hypothesis 2a).

Previous studies have found that disclosure is positively associated with formation of environmental reputation (Cho et al., 2012; Dowell et al., 1997; Philippe & Durand, 2011; Toms, 2002). Based on a sample of 92 U.S. firms from the basic materials, oil, and gas and utility industries, Cho et al. (2012) found that the extent of environmental disclosure in annual financial reports and stand-alone CSR reports improved perceptions of environmental reputation. Examining a sample of 215 U.K. firms, Toms (2002) found that the quality of environmental disclosure included in annual reports enhanced environmental reputation. Our results extend this research by showing that environmental disclosure can amplify the positive effect of environmental practices that are not easily visible on environmental reputation. This finding suggests that, besides adopting environmental practices that are not visible, firms can engage in high levels of disclosure to obtain the highest reputation gains. We did not find a moderating effect of environmental disclosure on the relationship between high environmental visibility practices and environmental reputation. The explanation for this result may be that constituents will obtain easily perceived firm information, as this information is highly visible. In this case, corporate disclosure may be not as essential mechanism to increase corporate environmental reputation.

Our study also demonstrates that the adoption of decoupling practices negatively affects environmental reputation, particularly in large and very visible firms like those in our sample (Hypothesis 3). Our results are consistent with the need for congruency indicated by other studies (e.g., Berrone & Gomez-Mejia, 2009; van Halderen et al., 2016). This finding suggests that managers should not base their environmental practices solely on highly visible practices if they aim to increase or create a positive environmental reputation. Cañón-de-Francia and Garcés-Ayerbe (2009) found that ISO 14001 certification had a negative effect on the market value of less-polluting and less-internationalized firms. While an ISO 14001 certification may seem purely ceremonial, constituents see this practice as a waste of resources that could be used more efficiently on other projects. Christmann and Taylor (2006) concluded that exploiting a shortcoming by strategically choosing high-visible practices to avoid the higher costs of low-visibility practices has adverse consequences. Our results are consistent with these studies.

Finally, we examined the role of firms’ environmental disclosure in the relationship between decoupling environmental practices and environmental reputation (Hypothesis 4). Our results show that a high level of corporate environmental disclosure amplifies the negative effect of decoupling practices on environmental reputation. This result confirms that environmental disclosure is not always a good idea and should be accompanied by low environmental visibility practices. Our results also highlight that today’s managers may be forced to disclose environmental information and will be penalized for some hypocrisy by loss of environmental reputation.

Limitations and Direction for Future Research

Our study has several limitations. First, our sample was drawn from the 500 largest publicly traded U.S. companies, measured by revenue, market capitalization, and number of employees. This drives two main caveats: First, the results may be limited to U.S. corporations. Audiences in other countries could interpret a company’s environmental cues very differently. Cultural values, environmental consciousness, economic development, and regulations—which differ between countries and geographical regions—can play a role in the relationships studied, as some works on related topics have suggested (e.g., Marquis, Toffel, & Zhou, 2016; Roulet & Touboul, 2015). Interesting future research could address the role of different geographical peculiarities or characteristics from a variety of regions/countries in the relationships studied.

Second, the firms in our sample are very visible, just by their size. As we argued, visibility can key to scrutiny (Delmas & Montes-Sancho, 2010) and thus to reputation; in smaller companies, the outcomes may differ. Future research could contrast the role of a firm’s size or visibility. Measures of a firm visibility in the media must be included to determine whether the media are an influential constituent affecting the impression of other audiences (e.g., Carter, 2006).

Third, this is a cross-sectional study. Our results may be limited to the years 2009 and 2010. It would be very interesting to perform a longitudinal analysis to observe changes in firms’ environmental practices and reputation in new studies. Moreover, the years that we consider fall in the middle of a global economic crisis, although we do not have any indication that this fact affected the phenomena studied. Future research may contrast whether the results differ in years or time periods of economic expansion.

Fourth, corporate disclosure could be considered as another high-visibility practice. Some previous studies have used disclosure as the prime high-visibility practice (e.g., Crilly, Hansen, & Zollo, 2016; Philippe & Durand, 2011). We were not interested, however, in evaluating disclosure as a ceremonial practice, but in evaluating a firm’s environmental quality and quantity of transparency. In our measure, therefore, each datum is weighted in terms of importance (e.g., data on greenhouse gas emissions carry greater weight than other environmental disclosures), and the disclosure score is tailored to different industry sectors. This measure of disclosure is similar to the weighted disclosure ratio that Marquis et al. (2016) used to obtain the selective disclosure magnitude. According to these authors, the weighted disclosure ratio represents degree of transparency/opacity, which “measures the proportion of a company’s relevant environmental indicators that it publicly discloses in a given year, incorporating the materiality of these disclosures by factoring in financial estimates of the environmental harm associated with each environmental indicator” (Marquis et al., 2016, appendix B, p. 3). We thus consider that our measure of firm disclosure includes the quality and quantity of the environmental information disclosed by the firm. Since different types of disclosure may moderate the relationship studied differently, it would be interesting for future research to explore how different types of self-disclosure (e.g., selective vs. substantive disclosure) affect and alter these relationships.

Fifth, we measured environmental (high and low visibility), and decoupling practices based on a sum of dichotomous environmental actions according to KLD. Binary metrics may be limited in capturing all nuances of every practice. Alternative measures, such as questionnaires, could be used. Future studies could explore the extent to which our results apply using alternate measures of environmental practices.

Moreover, due to data availability, we analyzed a small number of high- and low-visibility environmental practices. Future research could examine the effect of other highly visible practices, such as an environmental pay policy, environmental trademarks, or an environmental committee on the board (Berrone et al., 2009), on corporate environmental reputation.

Implications for Managers

Corporate reputation is a valuable intangible asset for the firm (Barney, 1991; Hall, 1992; Hart, 1995; Rindova, Williamson, Petkova, & Sever, 2005; Roberts & Dowling, 2002; Russo & Fouts, 1997). Favorable environmental reputation generates multiple benefits, such as attracting talented employees (Reinhardt, 1999) and investors (Delmas & Blass, 2010) or promoting alliance formation (Norheim-Hansen, 2015). As evidence exists that environmental reputation is positively associated with a firm’s general reputation (Tang et al., 2012), managers should make an effort to build a favorable environmental reputation because it also enhances corporate reputation.

Our research has at least three main implications for managers in building the firm’s reputation. First, managers should develop low environmental external visibility practices to the same extent that they adopt high-visibility practices. Constituents that invest time and attention in collecting information about the firm will be aware of these less visible environmental practices and collectively contribute to developing a positive environmental impression of the firm that will result in a favorable reputation.

Second, managers should disclose especially low-visibility environmental practices to influence the firm’s reputation positively. Third, managers should avoid adopting environmental decoupling practices, as such actions heavily jeopardize environmental reputation. In the era of information and social media, constituents can access firms’ environmental information easily, and decoupling is harmful even if the firm does not disclose its deceptive practices. In contrast, development and implementation of low environmental visibility practices coupled with high-visibility actions enhanced through environmental disclosure can contribute to a favorable environmental reputation. Firms should thus both be and seem environmentally respectful, instead of just seeming respectful, as this practice pays for environmental reputation.

Footnotes

Acknowledgements

The authors would like to thank the editor and the two anonymous reviewers for their helpful and constructive comments that greatly contributed to improve the final version of this paper.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research has been partially funded by grants from the Spanish Ministry of Education and Science: ECO2016-75909-P and ECO2013-47009-P.