Abstract

We investigate the possibility of using a percentage tax on crude oil and imported refined oil products consumed in the United States to fund the nation’s transportation infrastructure. This tax on oil could replace existing gasoline and diesel taxes and, potentially, other transportation taxes, such as taxes on airline tickets. The revenues from this tax could be used to fully fund federal infrastructure expenditures on highways, public transit, and aviation. The goal of this article is to raise the key issues associated with using an oil tax to fund U.S. transportation infrastructure, identify decisions Congress would need to make in designing such a tax, and outline some of the likely implications of adopting such a tax.

Introduction

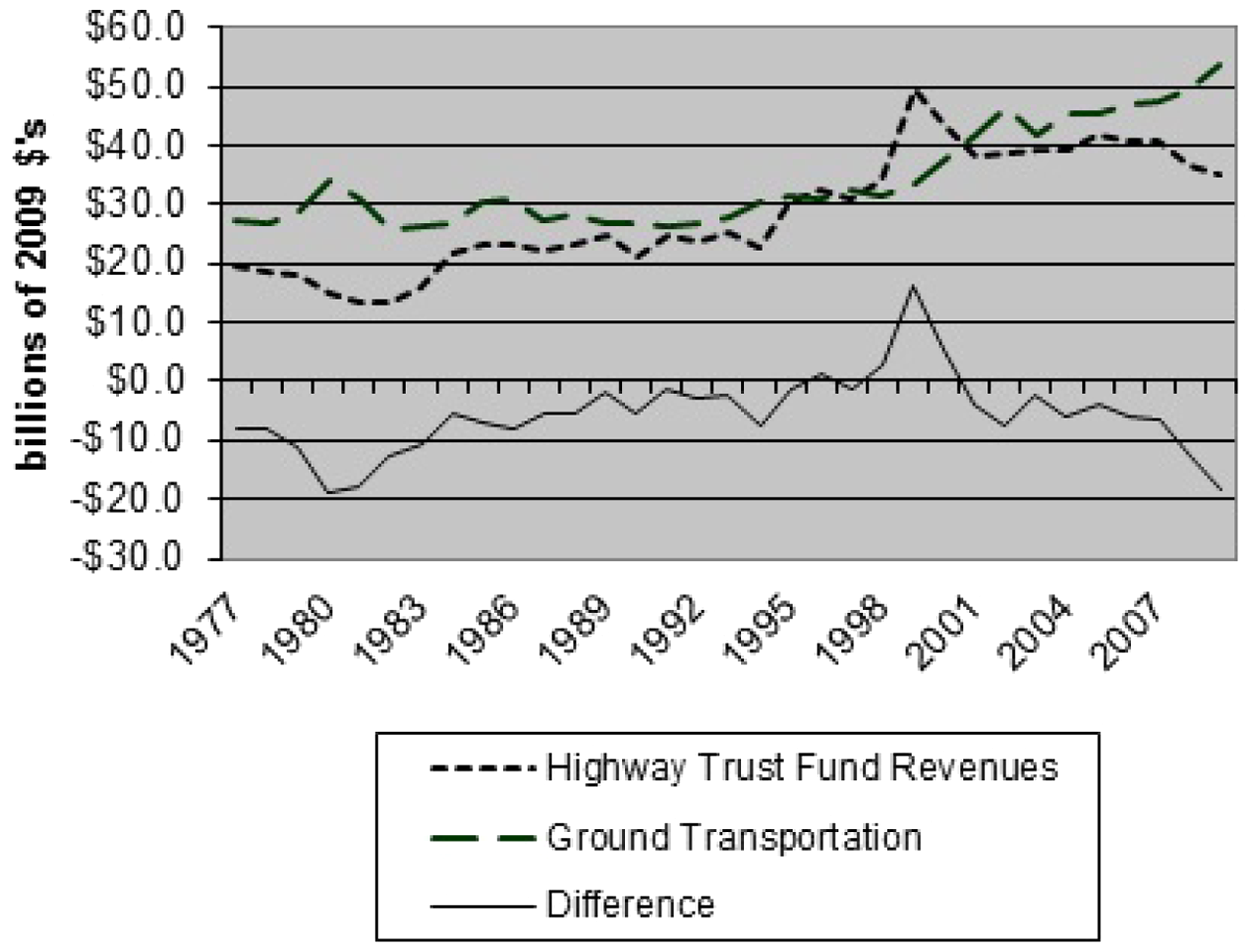

The need for highway expenditures in the United States is increasing while revenues from traditional funding sources, taxes on gasoline and diesel, are declining (Figure 1). As Americans continue to drive, but motor vehicles become more fuel efficient, this funding gap will continue to widen, presenting Congress with the challenge of finding a new way to reliably fund transportation infrastructure.

Highway trust fund revenues and U.S. federal government expenditures on surface transportation in constant 2009 dollars (1977-2009)

Each year, U.S. citizens incur a number of real, if unseen, costs associated with the consumption of gasoline and diesel and, by extension, oil. These range from environmental pollution stemming from the consumption of gasoline and diesel fuel to macroeconomic instability from oil price shocks to national security costs related to oil production by unfriendly regimes. Because these costs are external to consumers, the price of gasoline, diesel, and other oil-based products does not accurately reflect the true cost of oil consumption. An oil tax—imposed on petroleum and petroleum products consumed in the United States—is one way to simultaneously provide a reliable source of funding for U.S. transportation infrastructure and ensure that the price of oil more accurately reflects its true costs.

In this article, we present one option for a federal oil tax and estimate potential revenue streams that might be generated by such a tax. We then discuss the benefits and challenges associated with implementing an oil tax. Specifically, we identify and describe—quantitatively where feasible—the external costs associated with oil consumption that are not currently paid by consumers of oil. An oil tax is an effective mechanism through which to shift these costs from the public at large to those who impose these costs on society. The oil tax we propose is a percentage tax applied to domestic oil, imported oil, and imported oil products that would be periodically adjusted to reflect changes in the price of oil so that sufficient revenues are generated to cover government expenditures and external costs. 1 It would be designed to rise with inflation and to increase to cover increased costs of federally funded roads and surface transportation, while not overly burdening consumers when oil prices rise. We also discuss potential distributional implications for the tax, including how the burden would be shared between consumers and producers, how much of the tax foreign producers might bear, and which income and geographic groups would be likely to pay the tax.

The article is organized as follows: The next section, “Why Tax Oil?” introduces the concept of an oil tax as a mechanism to fund federal spending on transportation. It discusses a design for such a tax. The third section, “How Much Might Oil Be Taxed?” explores the potential types of expenditures an oil tax would fund and describes the external costs associated with oil consumption. In the last section, “Who Would Pay the Tax?” we discuss who would pay for an oil tax, focusing on income and distributional effects, and implications for federal transportation funding.

Why Tax Oil?

Gasoline and Diesel Taxes Are Insufficient to Pay for Roads

The U.S. federal government and the states’ finance meets expenditures on roads and some on public transportation by taxing gasoline and diesel fuel. Revenues from federal taxes flow into the federal Highway Trust Fund (HTF), which includes a transit account. Federal transportation appropriations are paid to the states through disbursements from the trust fund.

Federal taxes on gasoline and diesel fuel are US$0.184 and US$0.244 per gallon, respectively. Gasoline taxes have not been raised since 1993 and diesel fuel taxes were last increased in 1997 (Energy Information Administration, 2010a). Since the federal gasoline tax was last increased, the purchasing power of the dollar, as measured by the consumer price index, has fallen by one-third. In addition to the effects of inflation, as cars and trucks have become more fuel efficient, they travel farther on a gallon of gasoline or diesel fuel. Federal HTF revenues per mile driven have fallen dramatically as better fuel economy translates into fewer gallons of fuel purchased. As a consequence of the effects of inflation and improved fuel economy, federal fuel taxes are no longer sufficient to cover the costs of federal highway programs. In 2008, HTF revenues ran US$36.4 billion; expenditures ran US$49.2 billion. In 2009, revenues fell as expenditures rose: Inflation-adjusted HTF revenues from taxes on gasoline and diesel fuel fell to 30% below their 1999 peak.

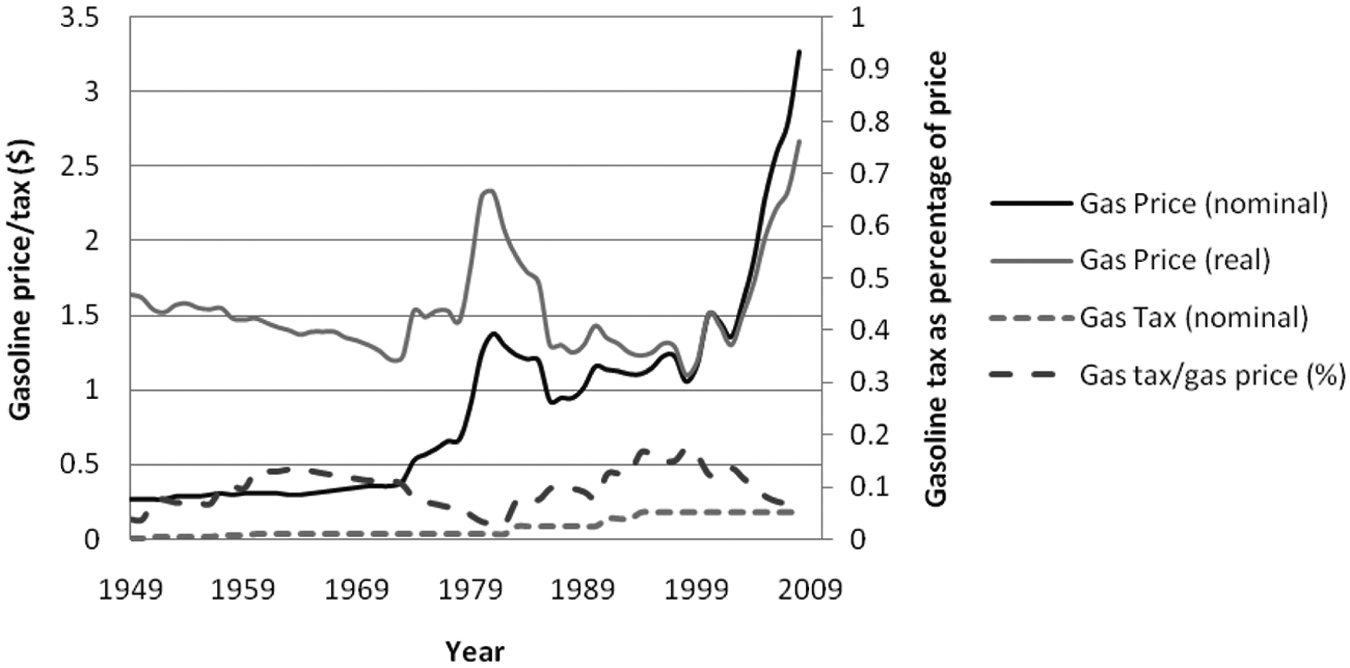

Figure 2 shows prices of gasoline and federal gasoline taxes over time. In 2008, the federal tax constituted 5.5% of the cost of a gallon of regular gasoline, substantially less (40%) than the average share of federal taxes in the price of gasoline in the 1990s (13.9%) (more detail is provided in the Appendix).

Gasoline prices and taxes: 1949-2008

Revenues from gasoline and diesel taxes will continue to decline once adjusted for inflation. The U.S. federal government has mandated further improvements in the fuel economy of cars and light trucks under Corporate Average Fuel Economy (CAFE) standards. By 2016, manufacturers will be required to achieve average corporate fuel economy of 37.8 miles per gallon (mpg) for cars and 28.8 mpg for light duty trucks, up from 27.5 mpg for cars and 23.5 mpg for light trucks in 2010. Between 2010 and 2016, improvements in fuel efficiency will lead to annual average declines of 5.2% and 3.3% in average fuel consumption per mile for new cars and light trucks, respectively. Between 1993 and 2007, the last prerecession year, the number of vehicle miles traveled (VMT) in the United States rose at an average annual rate of 1.6%. Even if increases in VMT return to prerecession rates, improvements in fuel economy are likely to result in declines in the consumption of gasoline and diesel fuel and hence revenues from fuel taxes. Efforts to introduce plug-in hybrids or to use biofuels, which presently are untaxed, could result in even lower revenues.

While revenues from fuel taxes have fallen, costs of building and repairing roads have risen. Limited HTF revenues have, by necessity, been channeled into road repair rather than new capacity. As a consequence, over the past three decades, the United States has added very little capacity to its road network, while VMT rose 95% between 1980 and 2008. During this same period, congestion has increased markedly. At least some of this congestion could be reduced by investments in roads and public transportation. Fuel taxes and other charges could also directly affect congestion by causing driver behavior to change.

Legislators Have Been Unwilling to Raise Motor Fuel Tax Rates

Antitax sentiment has made legislators reluctant to raise the per-gallon tax on motor fuels, especially when the price of gasoline is high. The federal government and some states have responded by turning to general revenues, levying other dedicated taxes, or issuing bonds to finance roads.

The shift to general revenues is contrary to traditional practice. For decades, taxpayers have considered gasoline and diesel taxes to be “user fees” for roads and transportation. Through these taxes, those who use the roads bear their costs. When roads and public transportation are funded out of general revenues, they compete for funding against schools, police, and parks at the state level, and against defense, health care, and other expenditures at the federal level.

A shift away from the practice of “user pays” is likely to lead to more use of roads and less investment. Current transportation taxes and fees are insufficient to ensure that drivers pay the full costs of using roads. By decoupling road use from taxes, fuel is cheaper for drivers and truckers than it otherwise would be. This reduces incentives to restrain driving and contributes to more congestion. Moreover, general revenue support for transportation infrastructure might be less reliable than dedicated funds, leading to insufficient funding for roads and other transportation infrastructure.

Design and Benefits of a Tax on Oil

A tax on oil would encounter some of the same antitax concerns that have made Congress unwilling to raise federal gasoline and diesel taxes. However, the public might be more willing to support a tax on oil in lieu of raising motor fuel taxes or as a substitute for these taxes. The American public has long been concerned about national security risks associated with oil consumption; this concern has engendered support in some quarters for measures designed to reduce dependence on oil—especially imported oil. However, because a tax on oil would necessarily affect a large number of interest groups, including groups that have active and effective lobbying power, the political challenges facing a proposed oil tax are likely to be significant. 2

In light of opposition to raising federal gasoline taxes, one option for covering increased costs of maintaining and improving our roads and transportation infrastructure would be to replace fixed-rate per gallon taxes on gasoline and diesel fuel with a percentage tax on each barrel of oil consumed in the United States. We argue that the percentage rate levied under this tax should be flexible: It should be set so as to ensure adequate revenues for surface transportation and other expenditures deemed to be tied to U.S. oil consumption. This percentage should be adjusted on an annual or quarterly basis to ensure that sufficient revenues are available but that consumers are not penalized during periods when prices spike. Accordingly, when oil prices rise, the tax rate would fall so that consumers and businesses are not doubly penalized by both higher oil prices and higher taxes. Conversely, when oil prices fall, the tax rate would rise, ensuring that sufficient revenues are available to cover the cost of roads.

The tax would probably best be collected at the refinery. To ensure that the domestic refining industry faces a level international playing field, imports of refined petroleum products would incur a tax equivalent to that on oil. 3 To preserve their competitiveness, exporters of refined petroleum products would receive a tax rebate equivalent to the tax on the crude oil used to produce the exported products.

There are multiple advantages to employing an adjustable percentage tax on oil as opposed to fixed per-gallon taxes on gasoline and diesel. First, one of the greatest problems with the current tax is that it is not adjusted for inflation. Road construction costs rise over time, but the tax does not. Revenues from an adjustable percentage tax would increase as oil prices rise, and the percentage rate could be automatically adjusted to ensure that a sufficient level of revenue for transportation funding is available if prices drop.

Second, the tax could replace multiple other taxes, potentially simplifying the tax system. If the proposed tax were adopted, excise taxes on gasoline, diesel fuel, and aviation fuel all could be eliminated, reducing the number of transportation taxes collected.

Third, an oil tax could be designed to internalize various external costs associated with the production and consumption of petroleum products. As so vividly demonstrated by the recent oil spill in the Gulf of Mexico, producing oil imposes environmental costs. Consuming oil also imposes environmental and human health costs. An oil tax that incorporates the costs of damage to the environment would allow consumers and producers to make decisions based on prices that reflect the full environmental costs of their activities. On the other hand, to the extent that different transportation modes impose different external costs (as discussed in the third section, “How Much Might Oil Be Taxed?”), a single tax would be less effective than differentiated taxes in providing proper signals to consumers of gasoline and diesel concerning the real costs of their behavior.

In addition to environmental costs, imported oil from unstable or unfriendly states imposes national security costs on the United States. Abrupt cutoffs in the global supply of oil, no matter the source, would trigger a sharp rise in world oil prices, potentially harming the U.S. economy. By imposing a tax on oil, the U.S. government would tap into a stream of revenues that would defray some of the costs of preserving economic stability in the event of a surge in oil prices. For example, the tax could be designed to cover the cost of stocking and maintaining the Strategic Petroleum Reserve.

Since the presidency of Jimmy Carter, U.S. armed forces have been tasked with defending sources of oil and the transportation routes along which oil is shipped. 4 The cost of this mission is significant. In line with sound economic principles, the cost of this service could be incorporated into the price of oil through a tax yielding an offsetting amount of revenue.

An oil tax would be more broadly based than taxes on specific transportation fuels. An oil tax, as opposed to taxes on just gasoline and diesel, would spread the burden of environmental and national security costs across all consumers of petroleum products, home heating oil, and petroleum coke. A tax imposed on all oil products ensures that tax policies do not distort the development of new technologies by encouraging the substitution of other refined oil products for diesel and gasoline.

How Much Might Oil Be Taxed?

A key challenge to implementing a percentage tax on petroleum is setting appropriate tax rates. In any one period, the rate needs to be set so that it generates sufficient revenues to fund appropriated levels of federal spending on transportation. We argue that rates should also be set so that they address the external costs associated with oil consumption. In this section, we discuss the tax rates needed to generate revenues sufficient to fund current proposals for spending on surface transportation and describe the various external costs the tax might also be used to cover.

Revenue Needs

In 2009, federal spending on surface transportation ran US$53.6 billion, while federal HTF revenues were US$34.96 billion (Office of Management and Budget, 2011a). The difference between these expenditures and HTF revenues was financed by federal borrowing. The U.S. House of Representatives Committee on Transportation and Infrastructure in 2010 considered but was unable to pass a bill to appropriate US$450 billion over the next 6 years for surface transportation and an additional US$50 billion for high-speed rail for an annual expenditure of US$83 billion. Assuming that U.S. consumption of gasoline and diesel fuel remains at about 2009 levels, to fund this level of expenditure, existing taxes on gasoline and diesel would have to be increased by US$0.28 per gallon, increasing the gasoline tax from US$0.184 to US$0.46 per gallon and that on diesel from US$0.244 to US$0.52 per gallon.

In 2009, the United States consumed 6,865,650,000 barrels of oil or oil-equivalent fuel products, purchased at an average price of about US$59.04 per barrel of oil for a total expenditure of US$405 billion. If all federal taxes on gasoline and diesel were eliminated and replaced with a percentage tax on oil, in 2009, a 9% tax on the value of a barrel of oil would have generated the same amount of revenue for the federal HTF as current taxes do on gasoline and diesel fuel. Assuming that U.S. oil consumption remains flat and oil prices average US$72 per barrel, roughly the price of oil at midsummer, sufficient revenues (US$83 billion) could be raised to fund federal surface-transportation programs with a percentage tax of approximately 17%. In the long run, oil demand would respond to higher prices from an oil tax, and higher tax rates would likely be needed to achieve revenue targets. We address this point further in the fourth section, “Who Would Pay the Tax?”

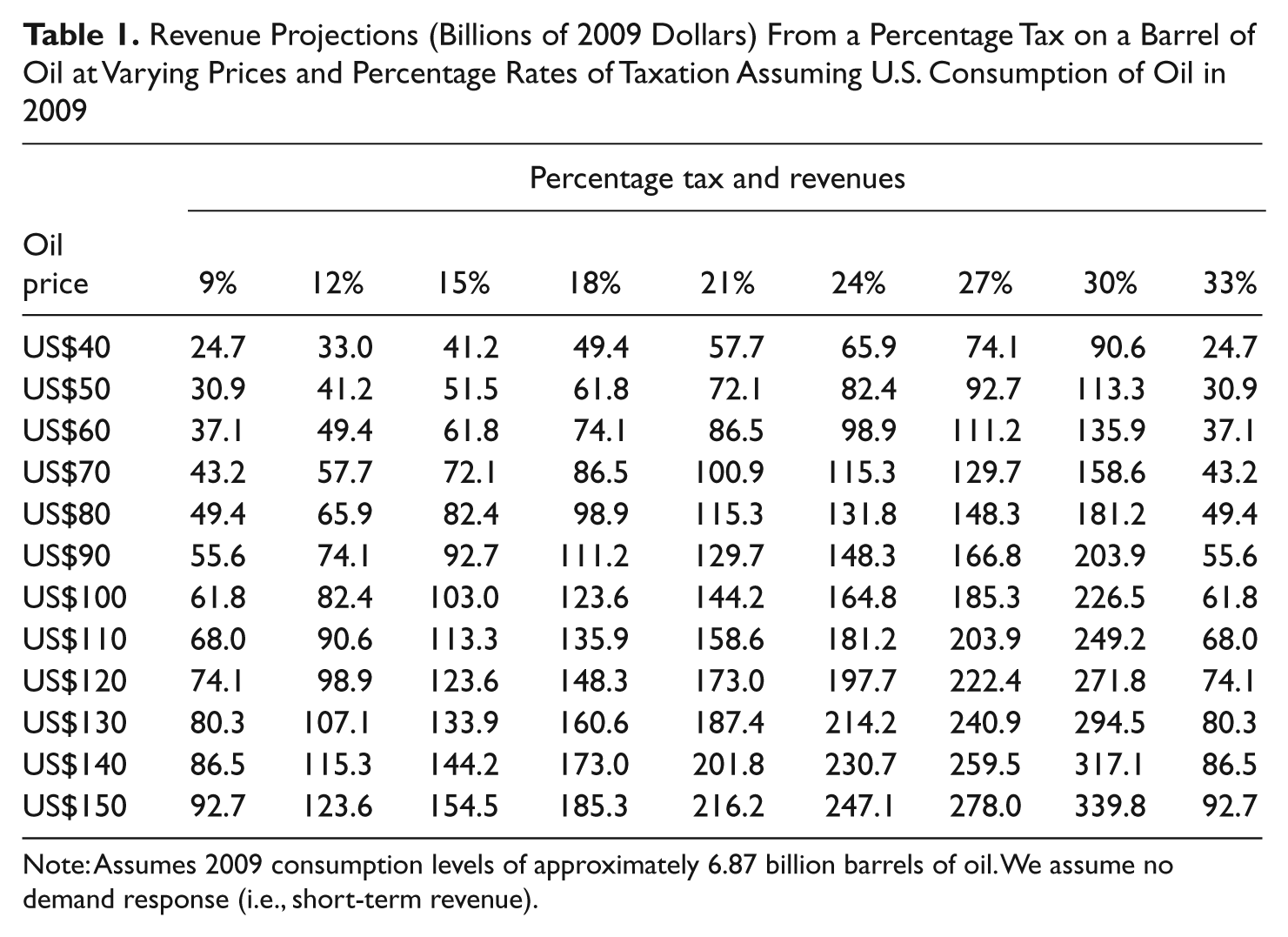

Different percentage taxes and various oil prices would generate a wide range of revenues. Table 1 illustrates potential revenue streams for a variety of price points and levels of taxation assuming 2009 oil-consumption levels.

Revenue Projections (Billions of 2009 Dollars) From a Percentage Tax on a Barrel of Oil at Varying Prices and Percentage Rates of Taxation Assuming U.S. Consumption of Oil in 2009

Note: Assumes 2009 consumption levels of approximately 6.87 billion barrels of oil. We assume no demand response (i.e., short-term revenue).

For example, a tax on oil could be set at a level to cover federal spending on air transportation as well as on surface transportation. U.S. revenues from taxes on air travel were US$10.6 billion in 2009. If a tax on oil were to be substituted for these taxes, it would have to be set at 19% at a price of US$72 per barrel to cover all expenditures on transportation, 2 percentage points more than a tax set just to cover federal expenditures on surface transportation.

As we discuss in more detail in the fourth section, “Who Would Pay the Tax?” higher oil prices would lead to a drop in the amount of oil demanded in the long run. As a result, the tax rates presented in Table 1 might not reflect the long-run revenue potential for an oil tax since the total oil consumed would fall, reducing the total tax revenue generated. In Table 2, we present revenue numbers based on how consumers might respond to higher oil prices. The “long-run” revenues reflect reduced demand for oil—based on a –0.3 elasticity—from higher prices. For any given oil price and tax rate combination, the long-run revenues are smaller than the short-run revenues; for example, a tax of approximately 19% would be needed to generate US$83 billion in revenue, the amount needed to fund near-term transportation expenditures. Although the long-run revenue potential is important to consider, we focus in the remainder of the article on short-run revenue generation since we are motivated by near-term appropriations for highway transportation.

Revenue Projections (Billions of 2009 Dollars) From a Percentage Tax on a Barrel of Oil at Varying Prices and Percentage Rates of Taxation Assuming 2009 U.S. Oil Consumption Levels With Demand Response From Consumers

Note: Assumes 2009 consumption levels of approximately 6.87 billion barrels of oil and demand response based on a long-term elasticity of –0.3. Demand response is independent of initial oil prices, which we acknowledge is a potentially unrealistic assumption; thus, total oil consumption is constant across rows.

Externalities

In addition to generating revenue for federal government expenditures on transportation, a tax on oil could help to ensure that markets more efficiently allocate goods by taxing oil for the unpaid or external costs that oil production and consumption impose on society. External costs, in the case of oil and other goods, are real costs but are typically not incorporated into market prices, leading to greater consumption or production than would be warranted if consumers or producers had to pay the full costs of the product.

In this section, we review costs stemming from environmental damage; where available, we provide quantitative estimates of these costs. We also include costs associated with macroeconomic disruptions and costs pertaining to national security associated with oil. We do not wish to suggest that an oil tax that would generate offsetting revenues for all these costs would be optimal: Calculating a socially optimal tax—a Pigovian tax that accurately reflects all external costs—is beyond the scope of this article and the data available. 5 Rather, the discussion illustrates—numerically, when feasible—some of the costs associated with oil production and consumption that an oil tax could help reduce.

Damage to the Environment

Extracting oil from the ground and using it to power vehicles, pave roads, and heat homes generates adverse side effects that harm human health and environmental quality. These additional costs are external to the person making the decision to consume oil—they are borne by society. Markets allocate goods and services more efficiently and more equitably when these external costs are internalized—that is, they are shifted to the individuals who are responsible for these costs: producers of oil and consumers of oil products. Here, we review the major environmental externalities associated with petroleum products and, where possible, provide estimates of their economic costs.

Oil consumption

Refined petroleum products, including gasoline, diesel fuel, aviation fuel, and heating oil, when combusted, produce a variety of airborne pollutants. These include sulfur oxides (SOx), nitrogen oxides (NOx), particulate matter (PM), hydrocarbons, carbon monoxide (CO), and carbon dioxide (CO2); some pollutants combine to form other air pollution, such as tropospheric ozone. Most of these pollutants have adverse health effects, some of which (e.g., PM and ozone) are especially harmful to at-risk populations, including children and the elderly. Others, such as sulfur dioxide (SO2), damage crops and have other adverse economic effects.

The use of refined oil products indirectly generates external costs associated with transportation, including congestion and vehicular crashes. Most research on fossil-fuel externalities focuses on roadway congestion and crashes associated with gasoline consumption (e.g., Parry & Small, 2005), but these externalities also apply to transportation-related diesel fuel use and air travel. Congestion imposes significant time costs on all drivers (or aircraft operators) in the congested area, not just the individual driver. In addition, some costs associated with roadway crashes are not borne by the driver and are not taken into account when drivers decide how much to drive—and thus how much oil to consume.

A great deal of research has focused on the external costs of oil or gasoline consumption by passenger vehicles. A recent review paper calculated the external costs associated with gasoline consumption at approximately US$2.30 (US$2009) per gallon (Parry, Walls, & Harrington, 2007). This equates to approximately US$44.85 per barrel of oil at current levels of gasoline consumption. However, many of these external costs are associated with the marginal mile driven rather than barrel of oil consumed. An oil tax is unlikely to be the most-efficient way to account for these indirect costs, although, as with gasoline taxes, an oil tax could be a second-best alternative to other more direct taxes, such as congestion surcharges. Policy instruments directly focused on reducing congestion or accidents are likely to be more effective than a tax on oil for addressing these externalities. For example, a congestion tax is a more efficient way to internalize the costs that each driver imposes on others during congested periods. Emissions that damage the environment can be reduced through policies that improve fuel economy or directly reduce pollution per gallon of gasoline combusted. Consequently, under a scenario in which distance-based costs are internalized through alternative policies, we exclude the indirect costs associated with the consumption of oil through passenger travel from our estimates of total external costs.

We know less about the external costs of freight transport, whether by heavy trucks or rail. Like passenger vehicles, these transport modes produce local air pollution, CO2, noise, congestion, and crashes. In the case of truck travel, there is also the cost of wear and tear on public infrastructure, which might not be internalized by current policies (such as weight restrictions).

There are few estimates of the external costs associated with burning aviation fuel. As with freight travel, much of the pollution produced by airplanes has little effect on human health because it takes place far from population centers. Another significant pollutant produced by aviation, CO2, is relatively straightforward to internalize through appropriate greenhouse gas charges. Noise, as with automobile transport, is a significant external cost of air transport. But, like road congestion, noise is a function of aircraft characteristics and flight flows and paths, and is highly localized. An oil tax is not the most-efficient way to address these associated costs.

The remaining external costs from oil combustion are those associated with other economic activities for which we consume oil, including home heating, road paving, and finished goods for which petroleum is an input (such as plastics). There are few, if any, estimates of these costs, even though there are cases, such as emissions from asphalt paving, in which costs exist.

Oil production

The process of exploring for, extracting, and transporting petroleum generates external costs. These range from environmental damage and pollution resulting from oil spills caused by drilling for and extracting oil—as with the Macondo oil spill off the coast of Louisiana—or during transport, such as the oil spill from the Exxon Valdez oil tanker. The key issue is the extent to which these costs are borne by oil producers. Some states, such as Alaska, impose surcharges on oil production that are designed to be “environmental taxes,” though these are not universal and are relatively low. Oil companies are also liable for the costs of oil spills, although the liability to private parties (noncleanup costs) was capped at US$75 million per spill, an amount that would not cover the cost of a major spill. These types of measures help to internalize the external costs of oil production, but, if they are limited or incomplete, they will not fully account for these costs.

Until recently, the literature on the external costs of oil spills focused on spills associated with intra- and international shipping. Spills associated with, for example, offshore drilling, were not typically included in calculations of total costs (see, for example, Delucchi, 2004). Consequently, existing estimates do not take into account the costs of oil spills from blowouts, such as the spill in the Gulf of Mexico.

Estimating the externalities associated with producing the “marginal” barrel of oil is challenging. Existing policies, such as the Oil Pollution Act of 1990 (Oil Pollution Act of 1990, Pub. L. No. 101-380), make it difficult to use historical data on production risks because these policies internalize some external costs and make it difficult to model the relationship between fuel use and oil spills. Nevertheless, our best estimate of the environmental externalities associated with production is about US$0.15 (in 2009 dollars) per barrel (Delucchi, 2000) although we acknowledge that this estimate is out of date. Moreover, Delucchi focuses on tanker-based spills and not, for example, spills associated with deepwater drilling; consequently, this estimate could be considered a lower bound.

Climate change

A rough estimate of the external costs associated with emissions of CO2 from burning refined oil products is approximately US$5.45 per ton of CO2 or US$2.37 (in 2009 dollars) per barrel (Nordhaus, 2007; Parry et al., 2007). However, potential damage to the environment from climate change caused by emissions of CO2 and other greenhouse gases is more difficult to estimate than environmental damage from localized sources.

Economists have estimated charges (taxes) on CO2 emissions necessary to substantially reduce emissions in a cost-effective manner. Reductions need to be deep enough and come quickly enough to cause concentrations of greenhouse gases in the atmosphere to stabilize before climate change becomes catastrophic. However, if charges are too high, they might impose substantial economic costs, for example, scrapping parts of the existing capital stock before they are fully depreciated. This approach differs from calculating the costs of global warming associated with oil consumption, as these estimates focus on inducing changes in technologies and behavior, not estimating discounted economic costs of climate change.

A US$30-per-ton tax on CO2 has been discussed in connection with climate change legislation as a point at which a number of generating technologies (nuclear, wind, biomass, geothermal) might become competitive with coal-fired electricity, the cheapest source of base-load electricity in the United States. Coal-fired power plants are also the largest source of greenhouse gas emissions in the United States. One barrel of oil generates 0.432 metric tons of CO2. Consequently, imposing a US$30-per-ton charge on emissions of CO2 would be equivalent to a US$13 tax per barrel of oil. At a price of US$72 per barrel, this would be equivalent to an 18% tax on a barrel of oil.

Total environmental costs

To calculate total external costs associated with oil consumption and production, one would ideally combine estimates of each cost component for which there are credible estimates (e.g., air pollution, oil spills, climate change). However, there are a number of external costs for which no credible estimate exists; therefore, our estimate of total environmental costs is likely to be on the low side.

From this analysis, we find that one could argue for a tax on oil of as much as US$58.00 (high estimates, including local pollution) per barrel or as low as US$2.52 per barrel (low estimates, excluding local pollution). The high number incorporates “indirect” costs associated with oil consumption—for which other policy instruments are preferable and an oil tax would be second best. The low estimate excludes these costs.

Macroeconomic Disruptions and National Security

Consuming oil creates or exacerbates economic and political threats to U.S. national security. In addition, there are costs related to maintaining military forces to reduce these risks to U.S. security.

Consumption of oil creates two major economic risks to the United States. One, an abrupt fall in the global supply of oil would result in a surge in the world market price. Because refined oil products are an important input to economic activity in the United States and a sharp price increase disrupts U.S. economic activity, several economists argue that past price surges precipitated economic recessions (Brown & Huntington, 2010). A surge in oil prices triggered by instability among oil exporters or an embargo would threaten U.S. security through the economic disruption it would entail.

Two, because the United States is a net importer of oil, large increases in U.S. consumers’ oil payments associated with shifts in oil prices—or because of deliberate reductions in supply by major exporters—result in a shift in the terms of trade, reducing the value of U.S. income and assets. Although economic in nature, a large shift in payments reduces resources within the United States to pay for the Department of Defense, the Office of the Director of National Intelligence, and other efforts to make the United States secure.

Oil consumption, especially of imported oil, has been linked with multiple political threats to U.S. national security. These include the following:

the potential of major oil exporters to manipulate exports to influence other countries in ways inimical to U.S. interests;

the potential for competition for oil supplies to exacerbate international tensions or disrupt international oil markets;

the effect of higher revenues from oil exports on the ability of “rogue” oil exporters, such as Venezuela and Iran, to thwart U.S. policy goals; and

the potential role that oil export revenues can play in supporting terrorist groups.

Among these linkages, embargoes on exports of oil (and natural gas) have been unsuccessful in changing policies of nations that were targeted by an embargo (Crane et al., 2009). As long as oil is a globally traded commodity, oil-exporting nations cannot successfully target specific countries because importers can purchase alternative supplies on the global market.

Crane et al. (2009) found that higher oil export revenues have enhanced the ability of certain states, such as Iran and Venezuela, to pursue policies contrary to U.S. interests. However, the importance of donations from individuals and charities in oil-rich Middle Eastern states for financing al Qaeda and its affiliates has declined as terrorist groups have increasingly turned to crime to finance their attacks. Moreover, the costs of perpetrating a terrorist attack are so small (US$15,000 to US$500,000) that even a substantial fall in Middle Eastern oil revenues would not affect al Qaeda’s ability to raise sufficient funds to finance its operations.

Some scholars have attempted to calculate these national security costs. Brown and Huntington (2010) estimate the additional costs associated with importing oil from unstable states at US$2.35 per barrel on domestic oil and US$4.60 per barrel on imported oil (both in 2009 dollars). If we assume that these estimates are accurate, then a US$2.35 oil tax on all oil consumption combined with an additional tariff of US$2.25 (US$4.60 – US$2.35) would internalize the external economic costs associated with oil consumption.

Costs of Defending Foreign Sources of Oil and Transit

Beginning with President Carter, ensuring the security of oil supplies and global transit of oil has been officially declared as a vital interest of the United States. It is a prominent element in U.S. force planning. If this mission were to disappear, the United States would almost certainly reduce some of its active-duty forces although not all the forces engaged or earmarked for operations to protect oil supplies would be dropped from the force structure. Some of the forces included in planning for this mission are included in plans for defending U.S. interests through other missions.

Crane et al. (2009) estimate how much might be saved from the Department of Defense budget if the mission to protect the supply and transit of oil were to be eliminated. Crane et al. put together two estimates of these potential savings. The first analyzed savings from the post–Cold War drawdown, once the mission to defend Europe from the Soviet Union disappeared. Crane et al. used this analogy to estimate potential savings in forces that have been assigned to U.S. Central Command (CENTCOM), if the oil mission were to disappear. Using this approach, Crane et al. estimate total potential savings of US$75.5 billion per year in 2009 dollars.

They also use a top-down approach to generate a second estimate of this cost. They estimate the share of effort in each combatant command dedicated to defending the supply and transit of oil. After dividing defense spending into core (fixed) and noncore expenditures, Crane et al. (2009) estimate potential savings in force structure and costs if this mission were to disappear. They find that US$91 billion could be saved annually. The bottom-up and top-down estimates represent 12% and 15% of the 2009 U.S. defense budget, respectively.

These estimates are perforce approximations. Nevertheless, they serve to help bound these costs. They suggest that the cost of forces associated with protecting oil resources is neither US$29 billion annually (a lower bound estimate from Delucchi & Murphy, 2008) nor US$143 billion per year (Copulos, 2007)—two numbers that have appeared in the debate.

Monopsony Premium

The United States is responsible for approximately 22% of total world oil consumption; consequently, if the United States were to reduce oil consumption, it could affect the world price for oil. Monopsony premium is the term used by economists to describe the potential effect on world market oil price—and hence the average cost per barrel U.S. consumers pay—that the United States might have by reducing its consumption of oil (Brown & Huntington, 2010; Parry & Darmstadter, 2003). Leiby, Jones, Randall Curlee, and Russell Lee (1997) find that the optimal tariff associated with the monopsony premium is between US$3.30 and US$11 (in 2009 dollars) per barrel. Tariffs at this level improve aggregate U.S. welfare by pushing down world market prices through declines in U.S. demand. Although such a tariff could improve U.S. welfare, it is not optimal from a global perspective, and we do not consider it in our calculations.

A Potential Tax Rate for Oil

In the preceding discussion, we identified government expenditures linked to oil that might best be covered by a tax on oil. We also listed costs on society imposed by the production and consumption of oil. In Tables 3 and 4, we show the amounts of revenue and tax rates at various oil prices that would be needed to cover these costs. Table 3 shows tax rates and revenues needed to cover total federal transportation-related expenditures. We estimate the total transportation expenditures at US$564.9 billion over 6 years or US$94.15 billion per year.

Percentage Tax Rates Necessary to Cover Expenditures on Transportation

Note: All calculations are based on total 2009 U.S. consumption of 6,865,650,000 barrels of oil or oil equivalent. The numbers below each per-barrel oil price indicate the percentage of the price of a barrel of oil that each expenditure category would constitute.

Indicates the total expenditures divided by total consumption in 2009.

Percentage Tax Rates Necessary to Cover Externalities and Other Associated Costs

Note: All calculations are based on total U.S. 2009 consumption of 6,865,650,000 barrels of oil or oil equivalent. The numbers below each per-barrel oil price indicate the percentage of the price of a barrel of oil that each expenditure category would constitute.

Calculated by multiplying 2009 oil consumption by the average internal and external costs of consuming oil given in Brown and Huntington (2010).

Indicates the total expenditures divided by total consumption in 2009.

Table 4 provides our low-end estimate of total external costs. We include climate change costs in Table 4 based on the marginal cost estimates of climate change outlined above. We do not include other consumption externalities, as we assume that those costs will be internalized through other, more direct policies. Finally, for national security costs, we assume an average of costs associated with domestic and imported oil. These costs are levied on all oil consumption, roughly equivalent to the current fraction of imported oil.

In general, these costs are not new. They are either currently being incurred by society with no offsetting revenues from oil or they are being paid through other taxes. Thus the illustrative tax rates in Table 4 would not impose additional costs on taxpayers, since society is bearing these costs, even if not explicitly. The tax on oil would substitute for existing taxes or reduce deficit financing used to pay for these expenditures.

In Table 4, defense spending associated with security and protecting oil resources constitutes US$83 billion, or two thirds of the total external and associated costs. Because this cost is not strictly an externality, the external costs associated with oil production and consumption total US$41.15 billion. Recall that this is a lower bound on these costs.

Who Would Pay the Tax?

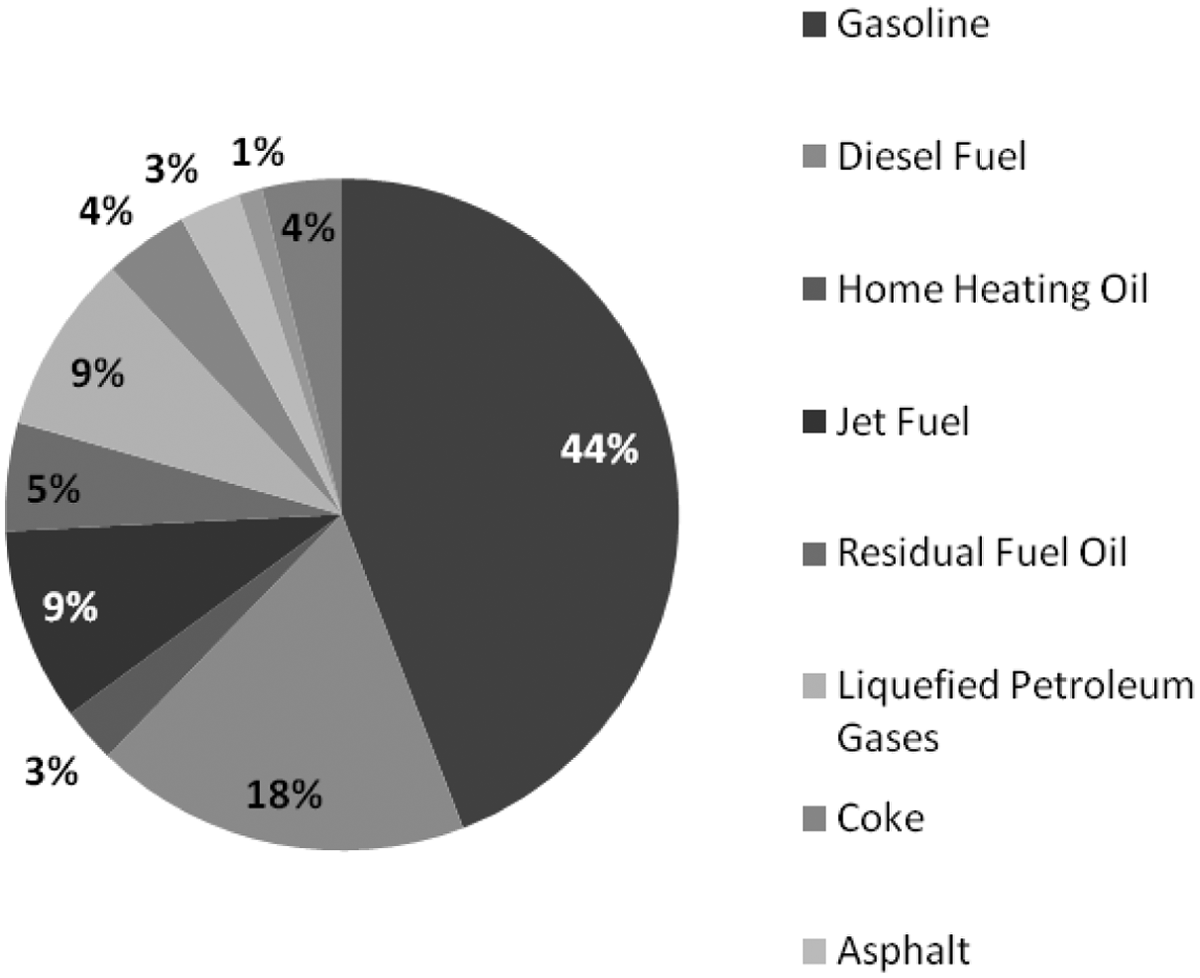

The most cost-effective place to collect a per-barrel tax on domestically refined oil would be at the refinery. For imports of refined oil products, the collection point would be at the port of entry. Both refiners and terminal operators would attempt to pass the cost of the tax along by raising prices for products produced from the oil, the most important of which are gasoline, diesel fuel, home heating oil, jet fuel, liquid petroleum gases, and residual fuel oil (bunker fuel; see Figure 3). An oil tax would raise the price consumers pay for petroleum-based products. At the same time, some of the tax would be borne by producers, both domestic and foreign. In this section, we review the economic incidence of an oil tax and assess its distributional effects on consumers. We conclude the section by discussing how the oil tax could affect federal transportation appropriations and key implementation issues.

Composition of a barrel of oil in terms of refined oil products

Distribution of the Tax Among Consumers, Refiners, and Domestic and Foreign Producers

In the third section, “How Much Might Oil Be Taxed?” we note that a tax of 17% on oil priced at US$72 per barrel, the price as of July 2010, would yield US$11.52 per barrel in federal revenue and would be sufficient to cover the costs of proposed federal expenditures on surface transportation. Such a tax would replace current federal highway taxes on gasoline and diesel fuel. If a tax of this size were passed through to consumers—and if refiners passed the tax through uniformly across all refined oil products—the tax on oil would be equivalent to a tax of US$0.261 per gallon of gasoline, US$0.077 per gallon more than the current gasoline tax.

In the face of higher prices, consumers would reduce the quantity of these products they demand. How much they reduce demand depends on how badly consumers need these products or, in economic parlance, the elasticity of demand. In the short run, the demand for gasoline and diesel tends to be relatively inelastic; in other words, motorists and truckers have a hard time finding ways of reducing their consumption of these products. However, over time, demand is considerably more elastic, as motorists purchase more fuel-efficient vehicles or, in some instances, change commuting patterns or even move closer to their places of employment. In the short run (typically 1 year), estimates indicate that, if gasoline prices rise 10%, demand for gasoline falls only 1% or less (Goodwin, Dargay, & Hanly, 2004). However, in the longer run (typically 5 to 10 years or more), a 10% increase in price could result in a 3% reduction in demand. 6

The demand for jet fuel and residual fuel oil (bunker fuel) is likely to be more elastic than demand for gasoline and diesel fuel (see, for example, Dargay & Gately, 2010). A substantial amount of airline travel is discretionary, that is, for pleasure. Increased costs of air travel stemming from increased prices for jet fuel is likely to result in a sharper decline in demand for jet fuel than for diesel fuel, which is used for commerce, or gasoline, since motorists find it necessary to make many trips. Residual fuel oil competes in some instances with coal or natural gas for industrial purposes. Its price is determined in great part by the prices of those substitutes because refiners have to price this residual product to sell. Refiners find it difficult to increase the price of this product.

Consequently, refiners do not mark up refined oil products uniformly: At any one time, margins on refined oil products are dictated in part by differences in the elasticity of demand. Because of these differences in demand, refiners might pass along more of the cost of a tax on oil on products for which demand is less elastic than on products for which demand is more elastic. Thus, in the short run, gasoline and diesel fuel might bear most of the burden of an increase in the price of a barrel of oil because demand for these products is more inelastic. If refiners passed through a US$12-per-barrel charge exclusively on gasoline, diesel fuel, and home heating fuel, the prices of these fuels might rise by US$0.401 per gallon. As before, the net effect would be smaller if gasoline and diesel taxes were eliminated. However, passing costs through exclusively to a subset of fuels would be unlikely because jet fuel, lubricants, and other products would also bear some of the increased cost. In the long-run the relative elasticities of fuels could change, affecting the way an oil tax burden would be distributed over consumers.

Higher prices would lead to a drop in the quantity of oil demanded. Although the short-term demand for oil is inelastic, so is the supply. Because most of the cost of extracting oil is incurred when drilling wells and building pipelines, once those investments are made, the variable cost of producing oil is modest. Consequently, producers do not cut back production when prices fall, as they continue to more than cover their extraction costs; especially domestically, there is limited strategic production shut-in. Because the supply of oil is inelastic, at least in the short run, small reductions in demand might result in larger falls in prices. This occurred in the first quarter of 2009. In the long run, however, oil supply is more elastic, and we would expect oil producers to respond to changes in the price of oil by adjusting production quantities.

The United States is a major consumer of oil, accounting for an estimated 22% of global consumption in 2009. The decline in U.S. consumption caused by an oil tax would lead to a fall in global demand, pushing down world market prices of oil. As noted earlier, imposing a 17% tax on oil priced at US$72 per barrel is enough to cover projected federal ground-transportation expenditures. Such a tax would raise oil prices in the United States by US$11.52 per barrel. However, if the tax replaces current taxes on gasoline and diesel, the net effect for consumers would be roughly equivalent to an increase in oil prices of US$6.67 per barrel, a 9.3% increase in the price of oil because the increase in gasoline and diesel prices caused by the oil tax would be offset by the elimination of these taxes. Assuming a long-run price elasticity of demand of –0.3, over the long run, a sustained increase in oil prices of this magnitude might induce a decline in the amount of oil demanded in the United States by about 3%, or 535,000 barrels of oil per day. This decline in consumption would put some downward pressure on international oil prices. Using a model developed by Camm, Bartis, and Bushman (2008), we estimate that a decline in U.S. consumption of this size would push down world market oil prices by about 1.2%, or US$0.83, when oil is priced at US$72 per barrel. Under these assumptions, oil producers would pay 7.2% of the tax. The United States imported 54% of the oil and refined oil products it consumed in 2009. If that proportion were to continue, 4% of the tax would be paid by foreign producers of oil.

Refining and retail margins have been very tight in recent years because of excess capacity. Although margins widened in 2007 and 2008, the recent recession reduced margins again. Consequently, neither refiners nor retailers would be likely to pay a substantial share of the tax. Thus, according to the preceding analysis, U.S. consumers would pay about 93% of the tax.

Distributional Effects of an Oil Tax

The cost of an oil tax to consumers comes in two forms: direct and indirect. Direct costs include higher prices for gasoline or diesel paid for directly by purchasers. Indirect costs arise because of the increased cost of goods and services for which refined oil products are an input, such as plastics, or the increased costs of consumer goods sold in stores stemming from higher transportation costs.

Not all consumers will face the same burden from an oil tax. Households, whether categorized by income or geography, differ in terms of expenditures on oil-related products. For example, households that consume few oil-intensive goods, use public transit, and heat with electricity would see their energy costs rise less under an oil tax than households whose members drive to work and heat their homes with heating oil. Households in geographic regions where oil is used as a home heating fuel would face greater increases in energy costs than households whose energy come from nonpetroleum sources.

The same holds true of businesses. Firms that use more refined oil products—such as shipping companies, for which petroleum-derived products constitute a larger share of costs—would be disproportionately affected by an oil tax relative to businesses that consume fewer refined oil products.

Based on the data in Figure 3, if an oil tax were evenly spread across all refined oil products, most of the tax would fall on motorists (44.1% of the tax) and truckers (18.2%). People who heat their homes with fuel oil would pay 2.7% of the tax; airlines and the U.S. Air Force and Navy, 9.3%; and road-paving companies, 2.9%, although this would be passed on to government road-repair and construction budgets.

Energy costs are typically thought to be regressive, insofar as lower income households spend a higher share of their income on energy products. Gasoline taxes have been shown to be at least weakly regressive based on gasoline expenditures as a share of total income (Poterba, 1991). Metcalf (1999) finds that energy taxes (e.g., carbon taxes or energy taxes, such as the British thermal unit (Btu) tax proposed by the Clinton administration) are regressive, though their indirect effects might be less regressive, especially on a lifetime income basis (Bull, Hassett, & Metcalf, 1994). Households in different parts of the country are also affected differently by energy taxes. For example, in the case of a Btu tax, the burden of direct costs would be higher in the Northeast, but the indirect costs would be lower for households in the Northeast, with the combined effect being less total variation in incidence across regions (Bull et al., 1994).

An oil tax could be designed to reduce the burden on households by rebating tax revenue through reductions in other taxes that distort other markets. The potential benefits of this “revenue recycling” have been demonstrated in the context of energy or environmental taxes. The regressive effects of an oil tax could be counterbalanced by reducing other taxes that are also considered regressive, such as payroll taxes. However, any revenue recycling would necessarily reduce the funding available for transportation and other uses because oil tax revenue would be offset by revenue losses from other taxes. Consequently, the total oil tax amount will need to take into account several competing uses.

Implications of the Proposed Tax for Transportation Appropriations

Assuming that the proposed tax per barrel on crude oil would be passed on to and indirectly paid by the consumers of the various refined oil final products, Congress would have to consider how the revenues might be apportioned across a variety of federal programs and geographic areas—and implicitly population groups. While it is difficult to predict the outcome of a debate, it is possible to envision several alternative possibilities.

Even though some of the petroleum products that result from each barrel of oil are not ultimately used as transportation fuels or as asphalt, Congress may wish to use the proceeds of such a tax to bolster the existing Federal Highway Trust Fund. It could direct some or all of the proceeds into the trust fund to augment or possibly replace entirely the revenues that are produced by motor fuel taxes. Important complications could arise from following this approach, and further study would be needed to develop a complete understanding of the implications. A major component of trust fund appropriations policy has been the “equity bonus” program, which insures that each state receives in funding a substantial proportion, currently about 92.5%, of the amount contributed to the trust fund by taxpayers in that state. A new funding source might require extensive restructuring of those provisions. On the other hand, Congress has not raised the motor fuel tax rate in nearly 20 years and has already been augmenting trust fund balances using general fund revenues. In part for this reason, many have advocated that the trust fund be abolished or that it be replenished by one or more alternative mechanisms (Schank & Rudnick, 2011). A thorough analysis of a variety of possible trust fund arrangements is beyond the scope of this article. However, it is clear that because other consumers of oil products would be paying part of the tax, the Federal Highway Trust Fund could no longer be considered as being financed only by user fees, which are discussed further in the next section.

If the trust fund were to be retained and existing user fees discontinued, it would seem to many to be appropriate that that proportion of the tax revenue that approximates the portion of petroleum consumption that eventually becomes gasoline and diesel fuel be designated for deposit into the trust fund. Similarly, the proportion of each barrel of petroleum that becomes aviation fuel could be designated for use in the federal air transportation program. The remainder of the revenue could then be contributed to the general fund. This approach would adhere to the concept of user fees, but would be more complex to administer because it is difficult to precisely estimate the future proportions of the outcomes of the refining of petroleum which, to some extent can be fine-tuned to market conditions. It would also be more difficult to determine a geographic basis for apportionment of the funds than under the current program.

Implementation

Setting the Tax

The most important failure of current gasoline and diesel taxes is that revenues have not kept pace with the cost of building and maintaining federally funded highways, nor have they covered the external costs associated with oil. For an oil tax to be an effective means of raising needed revenues for transportation, it will have to be structured in such a way that revenues keep pace with costs. We also argue that such a tax could usefully tax producers and consumers of oil for external costs imposed on society by this product.

One way to rectify these problems is to set the percentage rate each year at a level that would cover appropriated expenditures and an estimate of external costs. Congress would appropriate funds for transportation; the percentage tax rate would be set so that the tax would be projected to generate sufficient funds to cover these expenditures and to cover external costs. For example, if the price of oil were US$80 per barrel, a rate of approximately 40% would cover desired transportation expenditures (17%) and externalities (23%), under a hypothetical scenario in which these costs are additive.

Because oil prices fluctuate, the percentage rate would need to be adjusted so as to ensure that sufficient revenues are raised while cushioning taxpayers when prices spike. One way to achieve this goal would be to adjust the percentage rate quarterly, based on the average price of oil in the first two months of the previous quarter. For example, drawing on the example above, if the percentage rate had been fixed at 40% because oil prices had averaged US$80 per barrel, and oil prices surged to US$100 per barrel, the percentage rate would be cut to 32% in subsequent quarters because this rate would maintain revenues at the projected level.

Phasing in the Tax

In the previous section, we discussed potential shifts in prices on refined oil products and world market oil prices following the imposition of a tax. How these shifts will actually play out will depend on a wide range of market forces. Because of these uncertainties, Congress might choose to phase in an oil tax while reducing existing taxes on gasoline and diesel fuel. Such an approach would give policy makers time to determine how the tax affects refined oil product prices and therefore how the tax is being distributed across producers, domestic and foreign, refiners, and consumers. Using this analysis, Congress could make adjustments in terms of either expenditures or percentage rates.

Conclusion

There are compelling reasons to consider alternatives to existing motor fuel taxes in the United States. Current federal gasoline and diesel taxes—the largest contributors to U.S. federal transportation funding—are not indexed to inflation, and have not been raised to produce sufficient revenue to cover federal transportation infrastructure costs. An alternative, explored in this article, is to replace existing fuel taxes with a single tax on oil and imported refined oil products. An oil tax would have appealing features: It is likely to be relatively easy to administer because it would be collected at the refinery or ports; 7 it would spread the cost of transportation funding across a larger pool of users than current taxes do; it could account for the external costs associated with oil production and consumption; and it could be designed in ways to provide consistent funding for transportation infrastructure and other spending priorities. By tying tax rates to appropriated monies for transportation spending, and adjusting those rates to changes in world market oil prices, the tax would ensure that future revenues keep pace with transportation expenditures.

At the same time, imposing and implementing a percentage tax on crude oil would be challenging, and an oil tax is not without its limitations. Antitax sentiment is a major reason that existing federal fuel taxes have not been raised since 1994. Similar antitax political pressure could stall an oil tax proposal, although national security concerns might lend support to a tax on oil that other taxes lack. Phasing in might also help garner public acceptance for an oil tax. Ensuring that the transition away from motor fuel taxes toward a unified oil tax is gradual could make the tax more politically feasible. Setting the right rate for the tax is a key challenge, especially if one goal of the tax is to address the external costs of oil consumption. We have provided estimates of some of environmental, macroeconomic, and national security costs, but more detailed analysis would be needed to fully justify both a particular external cost estimate and the appropriate balance between revenue goals and reducing externalities. Finally, just as gasoline tax revenues fall as cars become more fuel efficient, an oil tax would be subject to the same revenue limitations. 8 Consequently, an oil tax would likely be one part of a more complete transportation funding approach, which could include policy instruments like VMT taxes to account for fuel efficiency and local externalities.

We also acknowledge that existing fuel taxes could be adjusted to take advantage of some of the features we have proposed for an oil tax. In particular, the gasoline and diesel taxes could be converted to an adjustable, percentage based system. In this way, revised versions of existing fuel taxes could adjust automatically for inflation and/or be adjusted periodically to provide sufficient revenue for transportation expenditure. It is difficult to assess whether changing the existing tax structure would be more or less political feasible than implanting a new tax although it is possible that it would be easier to create an optimal tax “from scratch” than trying to adjust an existing tax. Nevertheless, an oil tax would be a broader based tax, it could more effectively account for externalities associated with petroleum consumption, and it would go further in reducing oil consumption in our economy.

Footnotes

Appendix

Gasoline Price and Federal Tax History (1949-2007)

| Unleaded regular | Federal gasoline tax | |||

|---|---|---|---|---|

| Year | Price (nom.) US$ | Price (real) US$ | Nominal (in US$) | Tax/price % |

| 1949 | 0.27 | 1.64 | 0.01 | 4 |

| 1950 | 0.27 | 1.62 | 0.01 | 4 |

| 1951 | 0.27 | 1.54 | 0.02 | 7 |

| 1952 | 0.27 | 1.52 | 0.02 | 7 |

| 1953 | 0.29 | 1.57 | 0.02 | 7 |

| 1954 | 0.29 | 1.58 | 0.02 | 7 |

| 1955 | 0.29 | 1.55 | 0.02 | 7 |

| 1956 | 0.30 | 1.54 | 0.02 | 7 |

| 1957 | 0.31 | 1.55 | 0.03 | 10 |

| 1958 | 0.30 | 1.48 | 0.03 | 10 |

| 1959 | 0.31 | 1.47 | 0.03 | 10 |

| 1960 | 0.31 | 1.48 | 0.04 | 13 |

| 1961 | 0.31 | 1.45 | 0.04 | 13 |

| 1962 | 0.31 | 1.42 | 0.04 | 13 |

| 1963 | 0.30 | 1.40 | 0.04 | 13 |

| 1964 | 0.30 | 1.37 | 0.04 | 13 |

| 1965 | 0.31 | 1.39 | 0.04 | 13 |

| 1966 | 0.32 | 1.39 | 0.04 | 13 |

| 1967 | 0.33 | 1.39 | 0.04 | 12 |

| 1968 | 0.34 | 1.35 | 0.04 | 12 |

| 1969 | 0.35 | 1.33 | 0.04 | 11 |

| 1970 | 0.36 | 1.30 | 0.04 | 11 |

| 1971 | 0.36 | 1.26 | 0.04 | 11 |

| 1972 | 0.36 | 1.20 | 0.04 | 11 |

| 1973 | 0.39 | 1.22 | 0.04 | 10 |

| 1974 | 0.53 | 1.53 | 0.04 | 8 |

| 1975 | 0.57 | 1.49 | 0.04 | 7 |

| 1976 | 0.61 | 1.53 | 0.04 | 7 |

| 1977 | 0.66 | 1.53 | 0.04 | 6 |

| 1978 | 0.67 | 1.46 | 0.04 | 6 |

| 1979 | 0.90 | 1.82 | 0.04 | 4 |

| 1980 | 1.25 | 2.30 | 0.04 | 3 |

| 1981 | 1.38 | 2.33 | 0.04 | 3 |

| 1982 | 1.30 | 2.07 | 0.04 | 3 |

| 1983 | 1.24 | 1.90 | 0.09 | 7 |

| 1984 | 1.21 | 1.79 | 0.09 | 7 |

| 1985 | 1.20 | 1.72 | 0.09 | 8 |

| 1986 | 0.93 | 1.30 | 0.09 | 10 |

| 1987 | 0.95 | 1.30 | 0.09 | 10 |

| 1988 | 0.95 | 1.25 | 0.09 | 10 |

| 1989 | 1.02 | 1.30 | 0.09 | 9 |

| 1990 | 1.16 | 1.43 | 0.09 | 8 |

| 1991 | 1.14 | 1.35 | 0.14 | 12 |

| 1992 | 1.13 | 1.31 | 0.14 | 12 |

| 1993 | 1.11 | 1.25 | 0.14 | 13 |

| 1994 | 1.11 | 1.23 | 0.18 | 17 |

| 1995 | 1.15 | 1.25 | 0.18 | 16 |

| 1996 | 1.23 | 1.31 | 0.18 | 15 |

| 1997 | 1.23 | 1.29 | 0.18 | 15 |

| 1998 | 1.06 | 1.10 | 0.18 | 17 |

| 1999 | 1.17 | 1.19 | 0.18 | 16 |

| 2000 | 1.51 | 1.51 | 0.18 | 12 |

| 2001 | 1.46 | 1.43 | 0.18 | 13 |

| 2002 | 1.36 | 1.30 | 0.18 | 14 |

| 2003 | 1.59 | 1.50 | 0.18 | 12 |

| 2004 | 1.88 | 1.72 | 0.18 | 10 |

| 2005 | 2.30 | 2.03 | 0.18 | 8 |

| 2006 | 2.59 | 2.22 | 0.18 | 7 |

| 2007 | 2.80 | 2.34 | 0.18 | 7 |

| 2008 | 3.27 | 2.67 | 0.18 | 6 |

Source: Gas tax information retrieved from http://www.fhwa.dot.gov/infrastructure/gastax.cfm; Price data retrieved from http://www.eia.gov/emeu/aer/txt/ptb0524.html.

Acknowledgements

The authors thank Frank Camm, David Ortiz, Steven Popper, Constantine Samaras, and the staff at the office of U.S. Representative John Garamendi for valuable feedback. They also recognize the contributions and recommendations from two reviewers, Kenneth Small and Johanna Zmud, and three anonymous reviewers. All errors and omissions remain their own.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research and/or authorship of this article: The RAND Corporation.