Abstract

Asset recycling (AR) has gained attention in the United States as a way of improving life cycle asset maintenance and realizing maximum value from existing public infrastructure. In an AR program, proceeds from leases or sales of mature, underutilized public assets are reinvested in much-needed infrastructure improvements. Although the benefits of AR are often noted in both academic and policy circles, the academic literature on AR has not yet explored AR’s application to social infrastructure. To address this gap, we explore the concept of AR and its relevance for U.S. social infrastructure. We first examine the steps and conceptual features of a “fix-it-first” AR approach to social infrastructure. We then use Infrastructure Ontario’s Capital Planning Program as a case study to highlight the potential viability of such programs. Finally, we conclude by discussing the benefits and challenges of adopting AR policies in the United States.

Introduction

America’s networks of physical infrastructure are vast. They include roads, bridges, tunnels, seaports, airports, dams, levies, drinking water systems, wastewater treatment systems, electricity systems, postal systems, communications systems, sidewalks, and streetlights, as well as stand-alone social infrastructure such as schools, prisons, courthouses, and hospitals. That infrastructure provides critical public services, including transportation, communications, clean water, heating, lighting, and criminal justice.

Although some developing countries have completed such networks only recently, the United States and most developed countries have enjoyed basic infrastructure services for decades. Much of that infrastructure now suffers from serious, endemic problems that hinder its performance. Those include deferred maintenance, underinvestment in mature systems, and slow rates of technological adoption, among others. The incentives of asset owners often favor investing in new infrastructure projects while discounting proper life cycle asset maintenance (Surowiecki, 2016). Systemic underinvestment has created a significant infrastructure gap, defined as the difference between current investment rates and that required to maintain a state of good repair. Woetzel et al. (2016) estimate the annual global infrastructure gap at US$350 billion annually while other experts believe it to be as large as US$1.5 trillion by 2025 (McBride, 2018). 1

Engineering assessments confirm the deleterious effects of deferred maintenance. In its 2017 quadrennial Report Card, the American Society of Civil Engineers assigned low grades to much of the U.S. infrastructure stock. Examples include a “D” for roads, a “D” for dams, and a “D” for drinking water systems, with an overall grade of “D+” for American infrastructure. The Society summarized with, “the nation is failing to maintain even the current substandard conditions, a dangerous trend that is affecting highway safety and the health of the economy.”

Casady et al. (2018, 2019) also point to a variety of institutional barriers affecting U.S. infrastructure investment. Casady et al. (2018) specifically note that America’s unique, tax-exempt municipal bond market and election cycles accentuate misalignments in federal, state, and local investment priorities. Politicians routinely favor launching new infrastructure projects while discounting the costs of life cycle asset maintenance (Surowiecki, 2016). It is also politically contentious for public agencies to ignore the cost-of-capital advantages associated with the multi-trillion-dollar, tax-exempt municipal bond market. 2 Taken together, these institutional barriers tend to tilt the playing field in favor of traditional project delivery, an approach which suffers from poor project selection, 3 100% government-backed financing, and systemic underinvestment in asset operations and maintenance (Bennon et al., 2017). 4 In total, U.S. public-sector owners often have little to no incentives to view infrastructure as a set of valuable, but stranded, assets. There are often weak incentives to adopt techniques to enhance and capture the value of those mature assets.

The challenges facing America’s infrastructure today are unlike those of earlier decades. The United States no longer lacks connectivity between cities or between farms and markets, as was the case in the early 20th century. The main challenge is not designing, funding, and constructing nationally significant infrastructure such as the Interstate Highway Program, Clean Water Program, or Urban Mass Transportation Agency’s (UMTA) 5 transit program. Instead, America faces the combined challenges of deferred maintenance, underinvestment, and legislative inaction that inhibits the flow of funds into infrastructure (Davis, 2019; Spackman, 2013). Congressional legislators have even considered reinstituting the discredited earmark process to address those concerns (Kane, 2019). 6

To address such concerns, U.S. policymakers are exploring alternative infrastructure policy approaches that prioritize effective management, operation, and value creation from existing, mature systems. In the last few years, asset recycling (AR) has become an increasingly attractive policy for facilitating such improvements (Niquette, 2017; Poole, 2018; Varn & Kline, 2017), especially in “democratic societies [which] are systematically prone to spend far too little on normal civic infrastructure” (Fallows, 2015). AR programs are designed to “incentivize jurisdictions to recycle capital from existing mature public infrastructure assets toward new productive investments” (Infrastructure Australia, 2016, p. 90). In a country like the United States where there is little appetite for big spending measures and a growing infrastructure gap (see, Oxford Economics, 2017), AR is appealing because it offers a viable, catch-up infrastructure funding mechanism (Infrastructure Australia, 2016). In addition, public owners stand to benefit from unlocking of the substantial latent value embedded in American infrastructure that has accumulated over decades and remains dormant today. 7 Other potential benefits ascribed to AR include

The monetization of underutilized assets to fund infrastructure maintenance needs,

The relief of pressure on state budgets,

The transfer of operations and maintenance costs and risks to private firms, and

The use of sale/lease proceeds to fund new urban infrastructure or pay for infrastructure upgrades in rural areas (see, for example, Niquette, 2017; Poole, 2018; Varn & Kline, 2017).

Despite the prevalence of these oft-cited benefits, AR remains understudied in both academic and policy circles. The extant academic literature is particularly sparse, despite AR’s apparent potential for wide-ranging applications in the U.S. context and abroad. This article attempts to clearly conceptualize AR and explore its relevance for social infrastructure in the United States. We begin by defining AR, enumerating its five basic steps, and documenting a handful of AR examples in the United States. We next outline a “fix-it-first” approach to AR and its relevance for social infrastructure. This approach includes the creation of a permanent fund to preserve investment proceeds for investment in deferred maintenance and social infrastructure. Turning to a case study, we then review the Capital Planning Program of Infrastructure Ontario (IO), which contains elements of a social infrastructure AR program. We conclude by discussing the potential benefits and existing challenges of adopting “fix-it-first” AR policies in the United States.

AR: An Overview

What Is AR?

AR originated in Australia as part of the government’s 2014 Asset Recycling Initiative (ARI) (“How America Can Copy Australia’s Asset Recycling Scheme,” 2017). The Aus$3.3 billion ARI program incentivized state governments throughout Australia to sell or lease underutilized public assets to private firms to reinvest the lease or sale proceeds into new infrastructure projects (Varn & Kline, 2017). Each asset sold or leased by Australian states and territories received an additional 15% of the original transaction value in federal dollars (see Figure 1).

An overview of Australia’s asset recycling initiative.

In total, the program generated roughly Aus$23 billion in infrastructure investment (Chalmers et al., 2018).

Since the inception of AR in 2014, there have been a handful of reflections on the Australian experience. For some, AR seems to be more of a language game than a novel infrastructure funding approach (Hodge & Greve, 2010, 2019; Linder, 1999). Strong critics of AR state that “asset recycling may look new and exciting” but claim it is really “the last gasp of a failed model” (Quiggin, 2017). Other detractors of privatization and public–private partnerships (PPPs) see AR as simply “old wine in a new bottle.” This comes at a time when reviews of the international literature suggest “that PPPs are on average more costly and provide approximately similar [Value for Money] VfM as conventional procurement” (Petersen, 2019, p. 227). 8

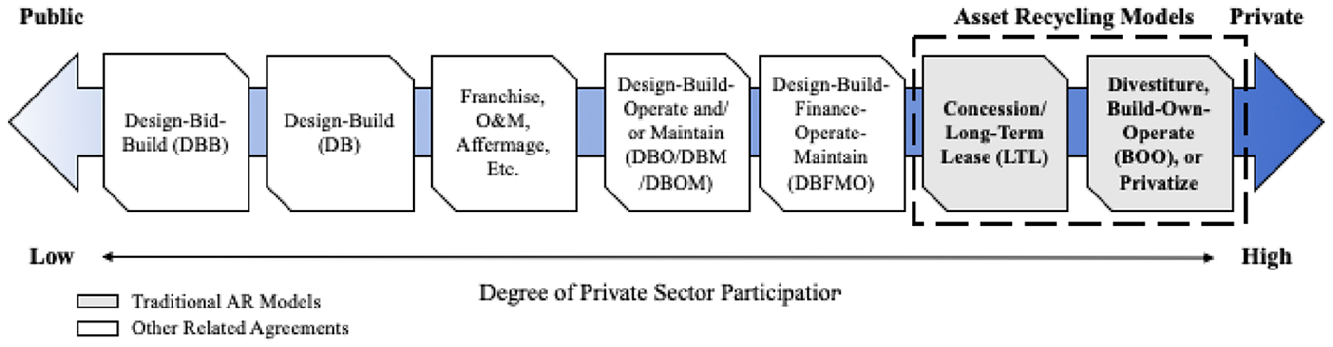

Taken together, these critiques are understandable because existing conceptualizations of AR routinely associate the model with privatization (see Figure 2).

Traditional AR conceptualizations.

For example, Poole (2016) defines AR as follows: [A] state government leases (for 50 to 99 years) existing infrastructure assets (airports, seaports, toll roads, electric utilities, transmission grids, etc.) to investment funds and pension funds-and uses the proceeds for new, greenfield infrastructure. Thus, the asset value that is liberated from existing infrastructure is recycled into much-needed new infrastructure. The assets that are leased are ones with healthy user-fee revenue streams, while the projects into which the proceeds are invested are ones without such revenues: transit systems, schools, other public buildings, etc.

Although such conceptualizations of AR resemble some of the earliest calls for privatization and raise questions about the appropriate management of “public” versus “private” value (see, for example, Alford et al., 2017), “[t]raditional 20th century debates between public ownership and privatization are increasingly irrelevant to the real choices confronting governments that face mounting public debt and undiminished expectations from citizens” (Fenn, 2014, p. 4). The economic effects (i.e., cost savings) of contracting out have also historically been twice as large in Anglo-Saxon countries (Petersen et al., 2018). 9 AR thus remains attractive in the United States because of its ability to unlock substantial amounts of stranded capital and balance sheet capacity for jurisdictions looking for funds to invest in much-needed infrastructure projects (Infrastructure Australia, 2016). In this light, AR offers a broader portfolio approach to public infrastructure asset management, one that consists of five key steps aimed at maximizing public-sector value. We describe those five steps below.

Steps of AR

Naturally, the first step of any AR program is determining the best use of newly raised funds. This is the origin of the term “asset recycling.” One common suggestion is to allocate these funds from revenue-generating infrastructure into non-revenue generating infrastructure. An alternative strategy for utilizing AR revenue would be adopting a “fix-it-first” approach. This approach would create a permanent fund that uses newly raised funds to generate investment income devoted to supporting social infrastructure (see, for example, Fenn, 2014). In either scenario, a careful accounting of who will benefit and who will pay is required before a program can be set up.

The second step in AR is to inventory all infrastructure assets owned by a particular jurisdiction. Owners must know exactly what assets they control. Although this may seem obvious, many infrastructure owners are not fully aware of exactly what they own. In one example, after completing a thorough audit, New York City discovered it owned 1,131 vacant lots, worth untold millions if not billions of dollars (New York City Comptroller, 2016). 10 Naturally, other jurisdictions stand to reap similar informational benefits from a comprehensive infrastructure audit. Although knowing what the public sector owns and its financial dollar value is not necessarily unique to AR, 11 this remains the first critical step of any portfolio approach to public infrastructure asset management.

The third step of AR is to assess the approximate market value of the inventoried assets. This will require enlisting the help of experts in the valuation of land, office buildings, parking lots and garages, and other types of infrastructure. This step is particularly significant because the market value of many infrastructure assets is inherently challenging to assess. Transactions of infrastructure assets are rare and values can change drastically over time. Such market information will thus not only help guide owners’ decisions about proper management but may also give them stronger incentives to undertake proper operation and maintenance of those assets. Even if owners have firm estimates of infrastructure asset values, an external audit has substantial market value.

The fourth step is to use asset valuation information along with new management techniques to conduct a fresh, thorough analysis of the best way to utilize infrastructure assets under a jurisdiction’s control. In this portfolio analysis, all options are at play. In typical AR conceptualizations, the long-term lease/no-lease PPP-based decision is a primary consideration (Poole, 2016). However, other options may include asset sales (e.g., sales of underutilized parking lots, garages, office buildings, or other real estates), short-term leases/concessions, in-kind asset transfers, and value capture, among other novel approaches. The best option may also be to do nothing, implying that those assets are managed as efficiently as possible under current approaches.

Finally, the last step is to execute those key operational and managerial changes, realize value from all transactions undertaken, and reinvest the proceeds into new assets. This step may require extensive objective, outside advice regarding the best mix of options to use in various circumstances. 12 The set of optimal choices is also likely to vary across jurisdictions depending on the type of infrastructure, the infrastructure’s age, and a variety of other considerations. Although there is no “one-size-fits-all” solution, this process is likely to generate considerable revenue. However, institutional inertia will almost certainly guarantee this process does not happen quickly. Because the public sector often fears making big, costly mistakes (see, for example, Chicago’s parking concession), AR programs will not be adopted without proof. Carefully designed and monitored pilot projects and/or programs will thus be needed to build a case for AR.

Fortunately, a handful of cases already exist in the United States which lend credibility to AR. Concessions like the Chicago Skyway, Puerto Rico’s Toll Road and Airport, Maryland’s Seagirt Marine Terminal, and Ohio State University’s parking offer notable examples of the AR concept in practice (see, for example, Poole, 2018). However, none of these deals are as illustrative as the Indiana Toll Road (ITR).

Back in 2005, then-Governor Mitch Daniels leased the ITR to the Indiana Toll Road Concession Company. Indiana received US$3.85 billion for the 75-year concession, which required the consortium to implement electronic tolling, invest in upgrading/widening sections of the toll road, and maintain specified levels of service in designated rural and urban areas. In return, the consortium received revenues from the road’s tolls.

This stand-alone “asset recycling” deal proved to be extremely beneficial for Indiana’s 10-year surface transportation plan called “Major Moves.” Since 2006, the Indiana Department of Transportation (INDOT) used the proceeds generated from the ITR concession to leverage US$10.8 billion in additional investment through 2015 (Fernandez, 2017). These transportation upgrades across the state included almost 500 miles of new highway, 6,400 miles of rehabilitated or replaced highway, and 60 new or reconstructed interchanges, and 1,400 rehabilitated or replaced bridges—that is, ~25% of the state’s inventory (INDOT, 2020). In addition, Poole (2018) notes that this deal allowed the state to repay “$200 million in outstanding ITR debt and [invest] $500 million into a ‘Next Generation Trust Fund’, which was designed to provide stable, long-term maintenance funding for the new transportation infrastructure” (p. 23). According to Gilroy and Aloyts (2013), this fund generated roughly US$755.5 million in interest income as of April 2011, thereby turning “a [once] revenue-losing asset into an asset that is funding billions in transportation investment now and generating hundreds of millions of dollars for the state’s long-term transportation infrastructure needs.”

Although this transaction was ultimately not called “asset recycling,” ITR serves as a clear-cut example of the AR process. Moreover, ITR offers the clearest workable hypothesis for tying AR to social infrastructure using a “fix-it-first” approach—that is, one that creates a permanent fund that uses newly raised funds to generate investment income devoted to supporting social infrastructure. In the next section, we describe this “fix-it-first” model in more detail.

AR for Social Infrastructure: A Conceptual “Fix-It-First” Model

A “fix-it-first” AR approach uses program proceeds to address critical deferred-maintenance problems. It then uses any remaining funds generated to capitalize a permanent fund. A permanent fund is one type of public trust fund. Permanent funds are currently utilized in Alaska, Texas, Norway, Canada, and other parts of the world. Traditionally used to preserve natural resource wealth, permanent funds are also attractive for AR programs because “[f]unds from major asset sales could be deposited in a public trust that invests in community or social infrastructure” (Fenn, 2014, p. 36). The fund would also be insulated from a jurisdiction’s general budget and political spending pressures. The Alaska Permanent Fund (APF) offers an illustrative model of these benefits.

The APF was implemented in response to wasteful government spending that followed the discovery of large oil deposits on the North Slope in Alaska in 1968. As one commentator described, In 1968, nine years after statehood, Atlantic Richfield pumped the first oil from Prudhoe Bay, beginning a new boom cycle. The following year the state held an auction for oil leases, and in a single day collected $900 million, at a time when the state budget itself was barely over $100 million. This shower of riches sent Alaska into a frenzy of public spending, particularly on capital projects. From 1961 to 1981 state general fund expenditures grew at an average annual rate of 22 percent, from $45 million to over $3 billion.

Created in response to this “frenzy of public spending,” the APF was designed to help preserve the value inherent in Alaskan natural resources in perpetuity. The Alaskan constitution requires that at least 25% of the revenue from oil and gas sales or royalties be placed into the Fund. Investment income generated by the Fund is then used to pay an annual dividend to all Alaskan taxpayers. The Fund had a market value of US$65.5 billion as of March 31, 2019, 13 and its 2019 dividend was US$1,606.

An AR permanent fund would function in a similar fashion to the APF. However, rather than distributing investment income as dividends to shareholders, an AR permanent fund would utilize income generated by the trust to support social infrastructure.

This is an advantageous model for social infrastructure for several reasons. First, social infrastructure represents stand-alone structures such as schools, prisons, courthouses, and hospitals. Such infrastructure does not cover its costs via user-fee revenue. It thus requires subsidies. Those subsidies could be covered in perpetuity via permanent fund investment income. Second, AR occurs within a political environment, and there is clear political appeal to supporting and improving social infrastructure without raising taxes. 14 These considerations may help generate the political support needed to adopt an AR program. Third, an AR program focused on social infrastructure ensures that proceeds stay in the infrastructure space and are less likely to be diverted to short-term, non-infrastructure purposes. Although no social infrastructure AR program currently exists using this model, IO’s Capital Planning Program contains elements of such an AR scheme. We next discuss the steps IO has taken to develop such an asset-management process.

Building a Social Infrastructure AR Program: Lessons From IO

AR for social infrastructure has not been examined extensively. As noted, social infrastructure is often thought of as stand-alone facilities such as schools, prisons, hospitals, police stations, office buildings, and courthouses. Unlike airports, toll roads, railways, and other network infrastructure, those assets typically do not have dedicated revenue streams, which makes them more difficult to monetize in AR schemes. However, evidence from IO suggests AR may be viable for social infrastructure if the program is appropriately designed and executed. We next explore the elements of IO’s Capital Planning Program and their potential for translation into a social infrastructure AR program.

IO’s Capital Planning Program: An Overview

Established by the Ontario Infrastructure and Lands Corporation Act 2011 (OILC Act), IO serves as “a Crown agency of the Province of Ontario that supports the Ontario government’s initiatives to modernize and maximize the value of public infrastructure and real estate” (IO, 2019a). The organization consists of four major business lines:

Major Projects—serves as the procurement and commercial lead for all major provincial infrastructure projects (including PPPs);

Real Estate—provides asset planning, facilities contract management, and real estate advisory services for the modernization and enhancement of the government’s real estate portfolio;

Commercial Projects—advises and supports negotiations for the government and public-sector partners in commercial transactions, including major land developments; and

Infrastructure Lending—supports public-sector infrastructure renewal via low-cost and low-risk loans to eligible clients.

Within IO’s Real Estate business line, the Capital Planning Division manages and maintains the Ontario Government’s largest real estate portfolio, known as the General Real Estate Portfolio (GREP) and Provincial Secondary Land Use Program. This portfolio is the primary responsibility of the Ministry of Infrastructure (MOI) but also contains government real estate assets in use by ministries such as the Ministry of the Attorney General (MAG), the Ministry of the Solicitor General (SolGen), the Ministry of Transportation (MTO), and the Ministry of Natural Resources and Forestry (MNRF; IO, 2017). As a result, the portfolio itself is large, old, valuable, and diverse. The average age of assets in GREP is approximately 51 years and properties range from courthouses, offices, and prisons to laboratories, heritage buildings, and land banks. As of March 2019, GREP contained 5,057 buildings and structures (4,370 owned, 28 PPPs, and 659 leased), totaling roughly 45.1 million rentable square feet, with a Can$12.3 billion replacement value (IO, 2019b).

Managing Ontario’s Social Infrastructure Assets

To manage the GREP portfolio, IO Capital Planning Division maintains an asset-management program that assesses public buildings, develops and updates maintenance plans, and implements rehabilitation contracts. 15 Used primarily for provincial buildings as well as those owned by local governments and other public agencies, this program supports the long-term, strategic, and evidence-based planning and investment principles outlined in the Infrastructure for Jobs and Prosperity Act of 2015. IO leads the province’s long-term infrastructure development plans. It does so by

Inventorying the province’s social infrastructure assets;

Measuring the condition of its assets; and

Identifying the anticipated infrastructure requirements, including improvements.

IO uses standardized templates to capture inventory and assessment data from on-site inspections of their properties. Those data are stored in VFA, a cloud-enabled asset-management software. As a web-enabled platform, VFA’s information is accessible in real-time from any location. It also allows different levels of data aggregation (i.e., by asset category, building type, component type, or region) and facilitates simple or complex “What if?” analysis for strategic decision-making (IO, 2019b).

Data in the software are used to create a multi-year listing of prioritized life cycle reinvestment project requirements based on building systems and component classifications (e.g., Uniformat II), industry standard unit costs for repair and renewal (e.g., RSMeans), and life cycle measures (e.g., BOMA [or Whitestone] Useful Life Spans). This multi-dimensional priority-ranking enables IO to develop strategic and defendable implementation plans for the GREP portfolio based on data-driven insights. The ability to simulate the impact of various funding scenarios on condition metrics also allows IO to substantiate its annual budget development/submission (IO, 2019b).

The Importance of an Asset Inventory

The foundation of IO’s asset-management program is its comprehensive asset inventory. IO maintains a database on all assets it manages. According to IO (2019b), this database includes

Unique identifiers—for land parcels and individual buildings;

Asset types—by original construction use (courthouse, laboratory, office, etc.);

Location data—both municipal addresses and geo-position (latitude/longitude);

Characteristics—including size, ownership, year of original construction, heritage designation;

Valuation data—that is, Net Book Value and Current Replacement Value;

Condition metrics—for example, age, Facility Condition Index (FCI), deferred maintenance;

Management responsibilities—for both capital renewal and operations and maintenance;

Ongoing costs—to manage and maintain; and

Relationship to government program use—that is, asset categorization, based on anticipated longevity of government use.

For any potential AR program to be successful, “[a]n organization must [first] know what assets it owns and manages, their locations, their condition, their management responsibilities, their ongoing costs to manage and maintain, and their relationship to government program use” (IO, 2019, p. 17). Without a comprehensive inventory, governments cannot possibly explore or effectively execute an AR scheme. IO is thus well positioned to utilize its comprehensive asset inventory for a future social infrastructure AR program.

Asset Categorization

As stated above, IO’s Capital Planning Division uses evidence-based decision-making processes to identify reinvestment project requirements. IO draws upon industry best practices as well as standardized asset inventory, condition assessment, and life cycle estimation methodologies. It groups project requirements into three categories:

Major Repairs—that is, maintaining the pre-determined service potential of components/assets for their given useful life;

Life Cycle Renewals—that is, rebuilding or replacing existing components/assets to extend their useful life; and

Functional Deficiencies—that is, the inability of components/assets to serve their intended function based on design standards.

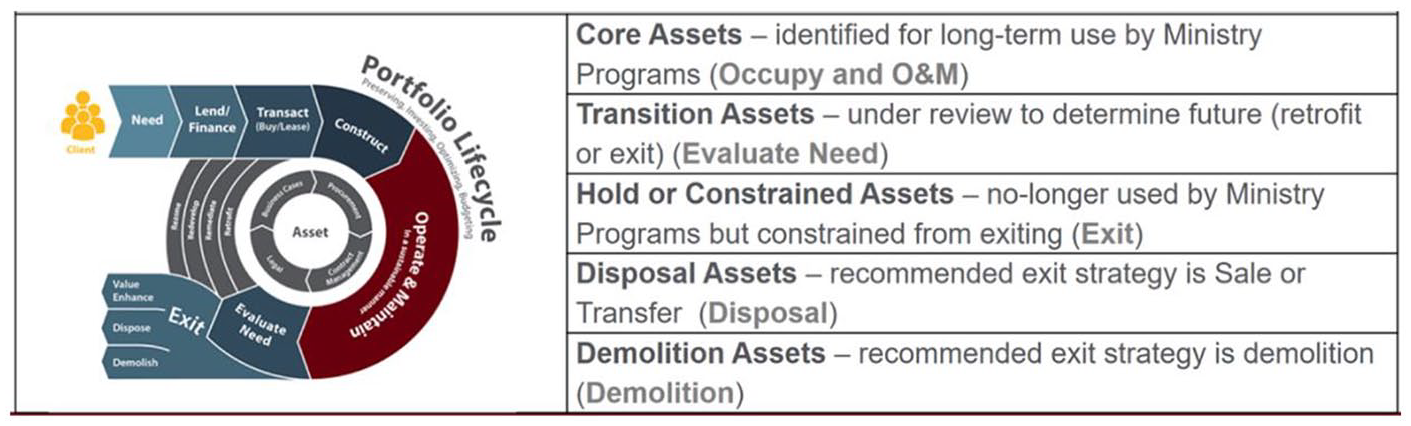

Applying this approach across GREP, IO feeds these project requirements from a snapshot of their rolling 10-Year Plan of Need through two filters within the VFA software. The first is pair-wise prioritization ranking analysis based on dimensions such as asset category, priority, status (e.g., on hold, planned, draft, deferred, etc.), and FCI, among others. The second filter includes an analysis of individual project business cases. Once those analyses are complete, 3-Year Tactical Delivery Plans are developed. Any deferred maintenance is also tracked overall and by asset category. 16 Within the tactical plans, assets are also categorized into different life cycle stages (see Figure 3) for the purposes of “identify[ing] appropriate levels of service, opportunities for value enhancement, [and] recommended best use options” that “maximize the value of the asset and the value to the portfolio” (IO, 2019b, p. 19).

Asset categorization in relation to realty life cycle (IO, 2019b).

These categorizations determine many aspects of an asset’s management, including the required capital repairs and maintenance/inspection needs as well as potential leasing, sale, or demolition strategies.

IO’s Opportunity for AR

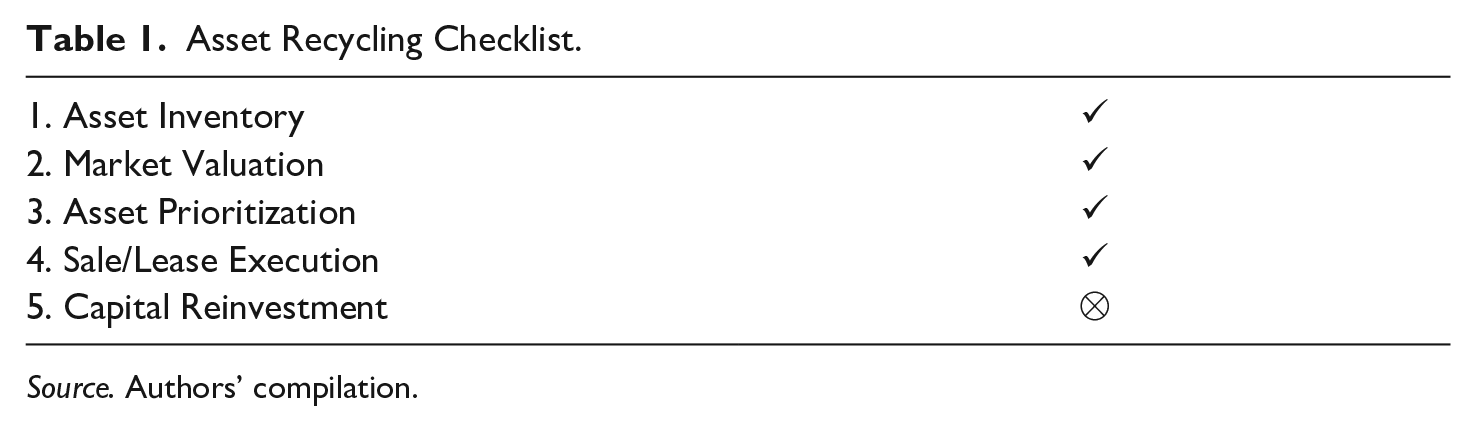

Overall, “IO has established itself as a hub for real estate knowledge, capacity and expertise” (IO, 2017, p. 9). Because of its industry best practices, IO now has an opportunity to explore the use of AR in its Capital Planning Program. Table 1 illustrates where IO currently stands in the process of setting up and executing a social infrastructure AR program.

Asset Recycling Checklist.

Source. Authors’ compilation.

IO has sold many surplus assets in the past. The organization hopes to sell a large number of buildings in its portfolio in the coming fiscal years. However, one of the lingering challenges IO faces is securing the rights to the capital raised from any asset sales. Currently, all proceeds from divestitures are allocated to the government’s general fund. The completion of an IO AR program is thus predicated on the establishment of a new, dedicated fund or trust that will preserve the proceeds of IO’s planned (and future) asset sales for reinvestment in future capital improvements across the province. However, “[c]ommitting to a policy of asset recycling would mark a sea change in fiscal policy for Ontario. As with most major policy reforms, it would involve disruption, controversy, teething problems, and plenty of criticism, both general and specific” (Fenn, 2014, p. 20).

Conclusion: A Way Forward for Social Infrastructure AR Programs in the United States

Evidence from IO suggests that AR may be a viable strategy for directing new capital into social infrastructure. If jurisdictions across the United States were to implement similar capital management practices to IO and develop social infrastructure AR programs, the amount of new funding that could be generated would be substantial (International Monetary Fund, 2015). However, state governments across the United States still “are not even sure which assets they have, tend not to report what they hold in one place, fail to assess their intangible assets and rarely have coordinated conversations across departments about how to manage or integrate assets” (Fenn, 2014, p. 32). In addition, because the delineation between local, state, and federal infrastructure assets is complex, executing asset inventories and valuations might be particularly challenging, especially when public appetite for broad private ownership of infrastructure assets is poor due to past privatization blunders like Chicago’s 2008 PPP parking deal—a US$1.15 billion, 75-year concession that has garnered significant public backlash, undergone a handful of renegotiations, and may, in the end, earn investors a US$9.58 billion profit before interest, taxes, and depreciation (Kling, 2019; Preston, 2010). In light of those challenges, Fenn (2014) notes, [t]he most effective way of enlisting public support for an asset recycling strategy is to establish a dedicated fund or trust, either to underwrite new capital projects or to defray the actuarial impact of future obligations, like pensions. In the meantime, such funds or trusts can accumulate profits by investing the proceeds of asset dispositions, while awaiting the call for their specific use. Several sovereign wealth funds are designed in this way.

17

(p. 23)

In a “fix-it-first” approach to AR, preserving new funding in perpetuity through state-level permanent funds for ongoing social infrastructure needs would allow owners to better understand their public asset portfolios, obtain more-accurate valuations, and improve the sophistication and objectivity of capital allocation to future infrastructure projects (Psychogios & Fischer, 2014). However, “[o]nly through engagement and consensus across multiple stakeholders will it be possible to undertake the transformation necessary to unlock the value of public assets, to protect the public interest and to reinvest in new assets” (Fenn, 2014, p. 38). Future research on AR is thus needed to explore its application and implications, both in the United States and abroad.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.