Abstract

This article investigates the impact of state-level tax and expenditure limits (TELs) on state government revenues and aid to local governments. Using an instrumental variable approach to control for endogeneity, the authors find that the general fund TELs (i.e., revenue and expenditure limits) have led to substantial increases in tax and nontax revenues. States with procedural limits (i.e., those with voter approval and/or legislative supermajority requirements votes) have significantly lower tax revenues. For states with these procedural limits, their ability to impose new or higher taxes is limited by the rules for passing such legislation. This study also finds that states with general fund TELs have higher levels of aid to local governments, while those with procedural TELs have lower levels of aid. Local government property tax limits do not have any impact on taxing authority of states and have only marginal impacts on the state-aid programs.

Keywords

The effect of tax and expenditure limitations (TELs) on government spending has been theoretically debated and empirically tested since the early adoption of TELs. This study contributes to this literature by making three contributions. First, whereas prior studies have focused on the TEL’s base (revenue limit or expenditure limit), method of approval (voter initiative, referendum, or a legislative vote), institutional codification (constitutional or statutory), or the fiscal growth factor (personal income or population growth plus inflation), or some combination of the above, this study highlights the importance of understanding how these limits are executed. The relevant construct, and the one we advance in this article, distinguishes between limits on the general fund (i.e., revenue or expenditure limits) and procedural limits on taxing authority (i.e., legislative supermajority or voter approval requirements for new or higher taxes; Kioko 2011; Stark 2001). We find tax and nontax revenues are higher in states with general fund limits, while tax revenues are significantly lower in states with procedural limits. This suggests that imposing new or higher taxes is more difficult in states with procedural limits. We also find aggregating general fund and procedural limits into a single measure, or excluding either of these institutions, could lead to omitted variable bias.

Second, we find that the question of endogeneity of these institutions has been largely overlooked. In this study, we attempt to improve upon prior estimates through an instrumental variable approach. A crucial instrument and a critical component of the tax revolt movement are the voter initiative provisions. Robustness tests reveal these to be weak and our examination of the literature suggests these instruments would be relevant explanatory variables. In our alternative instrumental variable specification, we consider the structure of the voter initiative provisions while maintaining the institutions presence as a relevant explanatory variable.

Third, while most studies examine the impact of local-level TELs on local government revenues or expenditures, we examine the impact of state-level TELs on aid to local governments. Given the presence of state-level tax limits, our expectation was that aid to local governments would likely decline as governments attempt to preserve their own spending powers. We however found higher levels of aid to local governments in states with general fund limits. States with procedural TELs, which we earlier found had lower levels of tax revenues, had significantly lower levels of aid to local governments.

The article proceeds as follows. We begin with a brief discussion on TELs as well as a review of the literature. We continue with a description of our empirical approach and report the results of the fixed effects model as well as the first instrumental variable approach. We propose alternative instruments and report these results in the Alternative Instrumental Variable section. We provide a discussion on the impact of state-level TELs on aid to local government as well as the potential for omitted variable bias if both the general fund TELs and the procedural TELs are not correctly specified. Concluding remarks follow in the Discussion and Conclusion section.

Background and Literature Review

Although New Jersey’s TEL dates to 1976, the modern movement to restrict government fiscal behavior is often attributed to California’s 1978 Proposition 13. A number of states followed suit, imposing limits on their taxing and spending authority in the late 1970s through the mid-1980s. A second wave of TELs swept the nation in the mid-1990s and again in the early 2000s.

TELs are constitutional and/or statutory restrictions on a government’s spending or revenue collection activities intended to supplant the decision-making process, thereby diminishing the politicians’ discretion and undermining the government’s ability to respond to legitimate demands (Johnson and Kriz 2005; Briffault 2008; Rubin 1998).

Traditionally, TELs have been classified as revenue limits, expenditure limits, appropriation limits, or a combination of the aforementioned. Much of the extant literature draws this distinction. Yet, apart from the state’s choice of a starting point—which is fundamental to determining the cap—revenue limits, expenditure limits, and limits on appropriations are fundamentally equivalent restrictions on a government’s appropriation/spending authority (Kioko 2011). To determine the limit, states are required to establish their base year general fund revenues or expenditures subject to the limit and adjust these base year revenues or expenditures with a factor of growth that is equal to growth in personal income or population growth plus inflation. States can only exceed this cap if they exercise their override provision. Funds in excess of the limitation are refunded to taxpayers, deposited in a rainy day fund, or used for purposes as provided by law.

Following Stark (2001), we reconceptualize the classification of TELs into two broad categories: general fund limits, that is, limits that affect tax-related revenues, expenditures, or appropriations, 1 and procedural limits, that is, rules that restrict the taxing authority of government. Unlike the general fund limits, procedural limits are not part of the annual budgeting process. Even so, procedural limits present a real constraint on a government’s ability to amend its tax code through either a voter approval requirement or legislative supermajority vote requirement. 2 Knight (2000) captures the difference in how the limitations restrain the public sector: “Traditional limitations place an external restraint in the form of a binding tax or expenditure cap on the legislature, while supermajority requirements place internal restrictions on the legislature by modifying the rules for passing legislation” (p. 45, emphasis added). Thus, the general fund caps and procedural limitations are likely to have different effects on fiscal policy.

Initial studies on the impact of TELs generally concluded that they were ineffective constraints on state government spending (Abrams and Dougan 1986; Cox and Lowery 1990). Empirical work since then has provided mixed results. For example, King-Meadows and Lowery (1996), extending the initial work of Cox and Lowery (1990), concluded that while the share of government spending typically declined in the presence of a TEL, these differences were quite small and in some instances were not significantly different from zero. Elder (1992) found that tax burdens were significantly reduced in states with ‘expenditure’ limits but that there was no reduction in tax burdens in states with ‘revenue’ limits. Poulson and Kaplan (1994) found TELs significantly reduced the rate of growth in spending in the short run; however, the growth in spending recovered in the long run, suggesting that TELs quickly lose their impact. Their findings are consistent with Dougan (1988), who argued that these limits reflected voter preferences at the time they were approved; however, these limits “do not deflect public sector spending from the long-run path it would have followed in the absence of limits” (Dougan 1988, 3).

Shadbegian (1996) later found that TELs significantly decreased growth in government spending; however, the impact was limited to states with low income growth. In their examination of fiscal discipline mechanisms, Bails and Tieslau (2000) found state and local government spending was significantly lower in states with expenditure limits, balanced budget requirements (if TELs were present), and supermajority balanced budget requirements. New (2001) found that states with limits requiring the government to refund excess revenues or limits based on inflation plus population growth to be more effective in constraining expenditures; statutory TELs, in contrast, actually cause per-capita expenditures to increase. Studies have also shown that the limits did not have a substantial impact on the absolute size of the state and local public sector (Joyce and Mullins 1991; Mullins and Joyce 1996; Skidmore 1999). The actual effect of the TELs was to shift expenditure and revenue decisions away from local governments, as they filled the void created by the imposition of local government TELs.

Much of the aforementioned literature fails to control for endogeneity. As a result, the estimates of the impact of TELs are unreliable. As Knight and Levinson (2000) and Poterba and Rueben (2001) point out, differences across the states may reflect voter preferences, not institutional outcomes. Therefore, a positive or negative correlation between TELs and spending is not necessarily indicative of any causal relationship (Rueben 1997). A simple comparison of states with TELs to those without shows that those with TELs have lower tax increases; however, this result may be explained by states’ underlying aversion to tax increases rather than the effect of the TEL itself (Knight and Levinson 1998). States that experience tax increases over long periods may respond by enacting TELs. In this case, one could find that TELs have a positive impact on state spending, even if the causal relationship is not apparent.

There are exceptions: Rueben (1997), Knight (2000), and Kousser, McCubbins, and Moule (2008). Using direct legislation provisions as instruments for TELs, Rueben (1997) found general expenditures as a percentage of personal income were two percentage points lower in states with binding limits—this effect was however partially offset by higher local spending. 3 Using a similar approach to Rueben (1997), Knight (2000) concluded that the procedural limits were more effective in reducing tax rates at the state level, especially when compared to the general fund limits. Using a difference-in-difference approach, Kousser, McCubbins, and Moule (2008) found the limits were not effective—except in Colorado, for which they concluded that Colorado’s Taxpayers Bill of Rights (TABOR) was effective because it limited all revenues and required voter approval for any tax increases or changes to the limitation. They further argue the political climate in Colorado boded well for the initiative’s effectiveness (Kousser, McCubbins, and Moule 2008, 352).

The construct we advance in this article distinguishes limits on the general fund (i.e., revenue or expenditure limits) from the procedural limits on taxing authority (i.e., legislative supermajority or voter approval requirements for new or higher taxes). Scholars have often specified revenue limits and/or expenditure limits but excluded the procedural limits. In some instances, revenue limits have been treated as a procedural limits on the taxing authority of the legislature (Poterba and Rueben 2001, 549) and subsequently thought to limit a state’s ability to raise revenue or service debt (Johnson and Kriz 2005, 97). In another instance, the procedural limits were considered an essential component of the TELs (Resnick 2004; Kousser, McCubbins, and Moule 2008). For example, in their discussion of Colorado’s TABOR, Kousser, McCubbins, and Moule (2008) note the TABOR was effective because it limited all revenues and required voter approval for any tax increases or changes to the limitation (p. 352). We argue the limit on all tax revenues is the general fund limit while the voter approval requirement for any tax increases is the procedural limit. Moreover, differences in taxing levels are likely to be observed when we examine differences in policy implementation. Procedural limits rely on a consensus building process that is fundamental to amending the state’s tax code. General fund limits simply restrict the appropriation authority by placing a cap on appropriations, for which, in most instances, the limit is set too high to constrain the government’s spending authority (Kioko 2011). Moreover, both the general fund limits and the procedural limits should be specified, as exclusions could lead to omitted variable bias (Knight 2000).

Our examination of this literature also finds that scholars have often examined the impact of these policy instruments on either state government revenues or expenditures or an aggregate measure of state and local governments’ revenues or expenditures. Given our explicit focus on state-level institutions, we believe the most appropriate unit of observation for this study is the state government. An extensive literature already examines the impact of property tax limits on local government revenue and spending. We therefore contribute to this broad set of literature by examining the levels of aid to local governments in the advent of state-level TELs.

Empirical Model and Results

To demonstrate bias if endogeneity is not addressed, we begin by reporting the results of a fixed effects model. We briefly describe instruments used in this literature and report the results of an instrumental variable model. Robustness checks reveal these instruments to be weak, and our review of the literature suggests these instruments are theoretically invalid (i.e., relevant explanatory variables). In the next section, we propose and report results using an alternative set of instruments. We also discuss the impact of state-level TELs on local government spending and the potential for omitted variable bias, given alternative specifications of both general fund and procedural limits.

Fixed Effects Model

We specify our fixed effects model as follows:

Table 1 was used to determine the presence of a state-level TEL in state i at time t. We included two indicator variables if state i at time t has a general fund limit (TEL it ) and/or a procedural limit (TEL_VOTE it ), where the former represents a constraint on a government’s annual spending authority while the latter represents a procedural constraint on a government’s taxing authority.

General Fund Limits and Procedural Limits by State

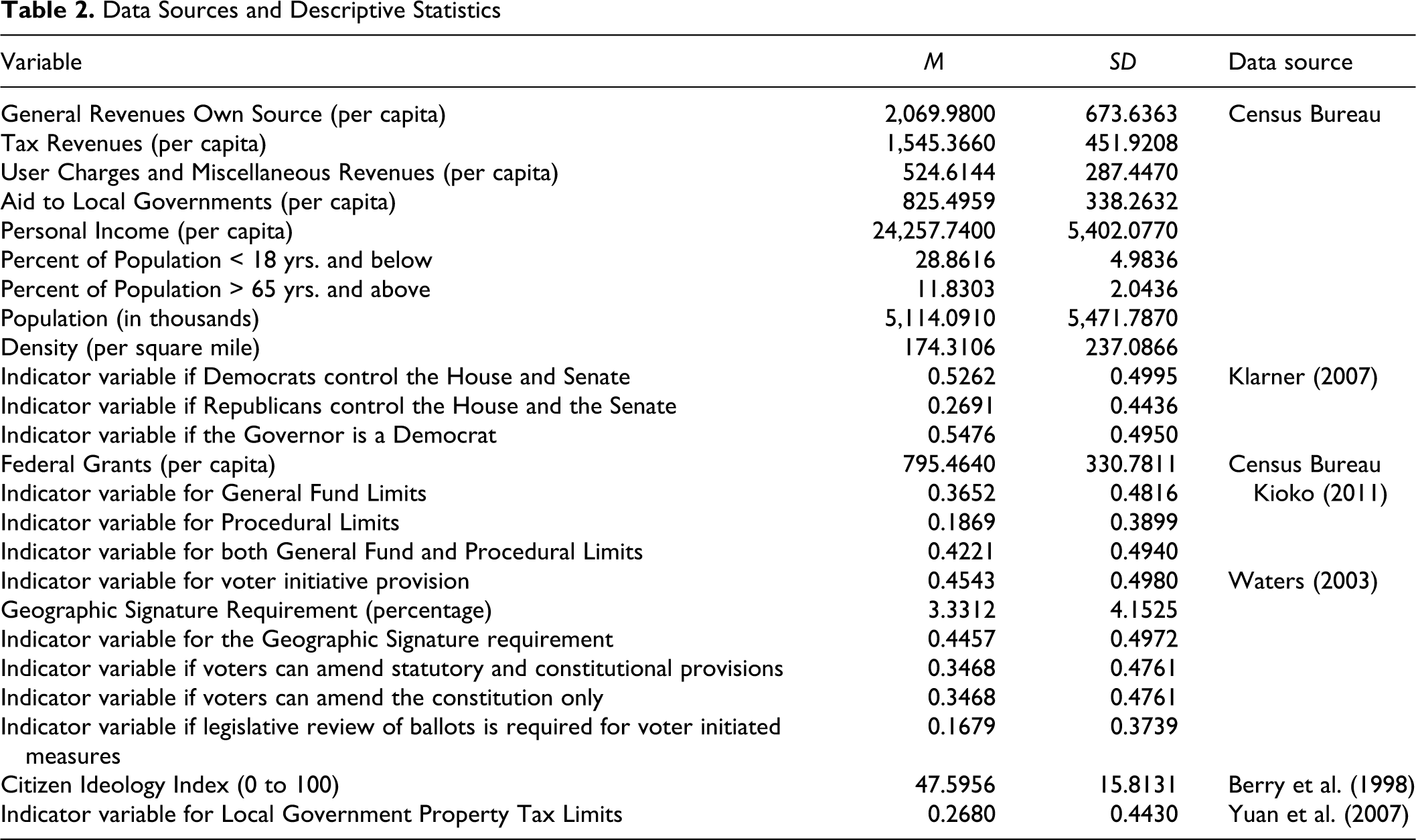

This study uses three different measures for our dependent variable—general revenues, tax revenues, and user charges and miscellaneous revenues. 5 We use revenue data because the expenditure data reported by the Census Bureau does not disaggregate spending by funding source. It therefore includes federal funds, proceeds from borrowing, and prior year-end fund balances. Since the TEL laws explicitly exclude all federal funds and debt proceeds, we believe the revenue-type variables are appropriate dependent variables (Kioko 2011). We also want to examine the impact of TELs on both tax and nontax revenues. Evidence at the local level suggests local governments are increasingly reliant on nontax revenues sources, given restrictions on their property-taxing authority (McCubbins and Moule 2010; Hoene 2004; Shadbegian 1999; Skidmore 1999). Current data show states have also made a smilar shift, with nontax revenues making up more than 29 percent of own source revenues and up from 19 percent in 1970. What is more, these nontax sources are not subject to the TEL. We therefore expect the coefficients for the policy measures to be positive in the nontax revenue regressions, an indicator that the states substitute lost tax revenues with nontax sources of revenue.

Xit includes personal income (per capita), population (in thousands), percent of population below the age of eighteen and above the age of sixty-five, density (per square mile), an indicator variable if Democrats control both the house and the senate, an indicator variable if Republicans control both the house and the senate, an indicator variable if the governor is a Democrat, and federal funds (per capita). We expect a higher personal income would lead to greater demand for public services. We anticipate opportunities for economies of scale in densely populated states. Population below the age of eighteen will lead to an increased demand for government spending. The population above the age of sixty-five will also exert additional spending pressures specifically toward health and welfare programs. We further control for demand for public services using our population variable. We also include federal funding per capita and expect additional intergovernmental funds would lead to higher state spending.

Given the prospending proclivity of Democrats, our expectation is that if the leadership in the house and the senate is Democrat and/or if the governor is a Democrat, the coefficients for these two variables would be positive. If the leadership in the house and the senate is Republican, we expect lower revenues. Table 2 reports our descriptive statistics and data sources.

Data Sources and Descriptive Statistics

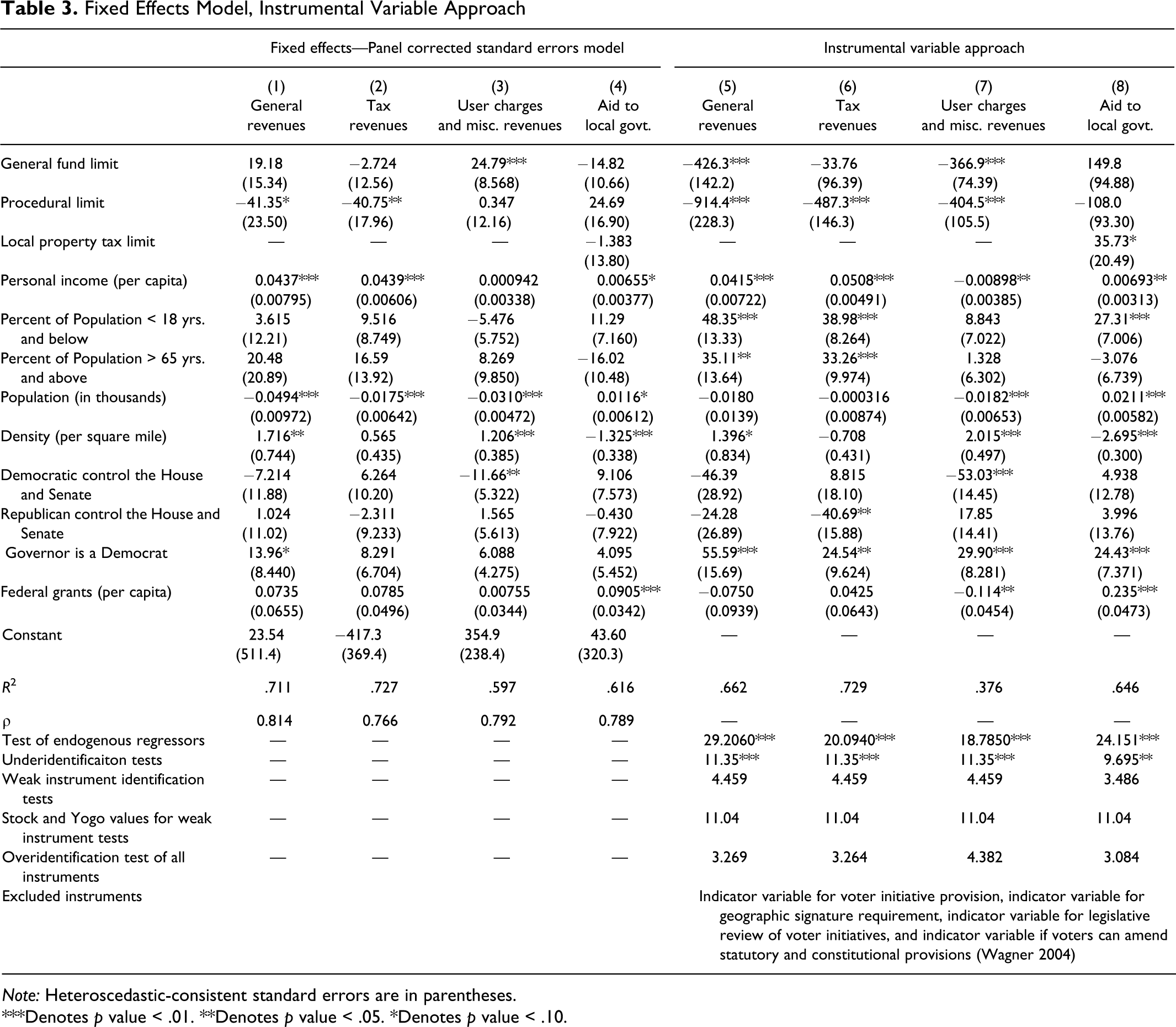

Since panel data exhibit serial correlation, cross-sectional correlation, and groupwise heteroscedasticity, we estimate a panel corrected standard errors model and report these results in columns 1 through 3 of table 3 (Beck and Katz 1995; Kittel and Winner 2002).

Fixed Effects Model, Instrumental Variable Approach

Note: Heteroscedastic-consistent standard errors are in parentheses.

***Denotes p value < .01. **Denotes p value < .05. *Denotes p value < .10.

Prior to addressing the effect of TELs on state government tax and nontax sources, let us review the control variables briefly. Most of the control variables have the expected sign; however, they are not significantly different from zero. Income has the expected positive effect on general revenues and tax revenues. As expected, populations below the age of eighteen and above the age of sixty-five will exert additional taxing and spending pressures—though our coefficients are not significantly different from zero. Larger states experience economies of scale—our population coefficient is negative and statistically significant. The coefficient for the density variable in the user charges and miscellaneous revenues regression is positive and statistically significant. This finding suggests governments rely on user charges and fees to meet service-related expenditures in densely populated areas. The coefficient is not significant in the tax revenue regression, although it is positive in the general revenue regression, in part due to the construction of the general revenue measure. Although we expected states with Democrats controlling the house and the senate and those with a Democrat governor to have higher tax revenue levels and states with Republicans controlling the house and the senate to have lower tax revenue levels, our coefficients for the most part are not significantly different from zero. The federal grants per capita coefficient is positive but is also not significantly different from zero.

When TELs are treated exogenously, the general fund limit variable is positive and significantly different from zero but only in the user charges and miscellaneous revenues regression (column 3). This suggests states with a TEL will subsidize spending with nontax sources that are not subject to the limit. The coefficient in the tax revenue regression is negative, but not significantly different from zero. The coefficient for the procedural limit indicator variable is negative and statistically significant in the general revenue and tax revenue regressions (columns 1 and 2). These restrictions do impose an additional constraint on the government’s ability to amend the tax code. However, these governments do not substitute lost tax-revenue capacity with nontax sources—the coefficient for procedural limit in the user charges and miscellaneous revenue regression is not significant.

These results should be however be treated with caution. In failing to control for endogeneity, one could underestimate the impact of both policy instruments as our unobserved effect (∊ it ) is correlated with our variable of interest (TEL it and TEL_VOTE it ).

Instrumental Variable Approach

Instrumental variable (IV) is a standard approach to such problems. The basic idea is to find a set of valid instruments that account for the presence of the endogenous variables (TEL it and TEL_VOTE it ), and use these instruments to generate values for the instrumented variable (TEL it* and TEL_VOTE it*). Rueben (1997) uses direct legislation and recall provisions as instruments for the existing tax and expenditure laws. The direct legislation provisions enable voters to directly or indirectly amend their state constitution and statutes. 6 Oftentimes, these measures are put on the ballot with significant support from interest groups (Boehmke 2005; Smith 2004; Waters 2003).

Knight (2000), Shadbegian (1999), and Wagner (2004) use the voter initiative provisions as instruments for TEL provisions. In addition to an indicator variable for the presence of initiative processes, Knight (2000) uses the number of sessions required to initiate a legislative amendment to the constitution and the legislative vote required in both chambers to pass a legislative amendment to the state’s constitution. Shadbegian (1999) uses an indicator variable for voter initiative procedures as well as the approval rate of ballot measures as instruments for local government property tax limits. Wagner’s (2004) instruments include an indicator variable if citizens may propose both statutory and constitutional initiatives, an indicator variable if citizens must satisfy the geographic signature requirement, and an indicator variable if the state permits legislative review of proposed initiatives.

We specify our IV model as follows:

Following Rueben (1997), Knight (2000), and Wagner (2004), we include the following instruments: (1) an indicator variable if the voter initiatives are present in state i at time t, (2) an indicator variable if citizens may propose both statutory and constitutional initiatives, (3) an indicator variable if citizens must satisfy the geographic signature requirement, and (4) an indicator variable if the state permits legislative review of proposed initiatives, that is, the indirect initiative provision (columns 5 through 7 of table 3). 7

Again, our control variables have the expected sign and for the most part are significantly different from zero. Income has the expected positive effect on general revenues and tax revenues and a negative effect on user charges and miscellaneous revenues. Populations below the age of eighteen and above the age of sixty-five exert taxing pressures. The population variable is again negative, though not significantly different from zero except in the user charges and miscellaneous revenues regression. Our density variable is positive and significant in our user charges and miscellaneous revenues regression. States with Democrats controlling the house and the senate do not levy higher taxes. These states do however have significantly lower user charges and miscellaneous revenues. As hypothesized, if Republicans control the house and senate, tax revenues are significantly lower. If the governor of the state is a Democrat, tax revenues and user charges were higher. The federal grants per capita coefficient is positive, though not significant when we consider general revenues or tax revenues. The coefficient in the user charges and miscellaneous revenues regression is negative and significantly different from zero, suggesting a substitution effect—that is, for every additional dollar in federal revenues, user charges are 11 cents lower.

The coefficient for the general fund limit is now negative in all three regressions and significantly different from zero in our general revenue and user charges and miscellaneous revenue regressions. Our estimates for the procedural limit are significantly larger. For states with a procedural limit, their tax revenues are $487 per capita lower compared to states without these instruments, while their user charges and fees were $405 per capita lower as well. These results differ substantially from our fixed effects estimates as well as other estimates in this literature. To ensure our results are reliable, we performed several robustness checks.

Results of the underidentification test (11.35, p value < .01) reveal the excluded instruments are appropriate predictors of TELs. However, to explore the strength of the relationship, we report the results of a weak instrument test. Our null hypothesis is that our instruments are weak and subject to bias that we find unacceptably large. The weak instrument statistic estimates the correlation between the endogenous regressors and the excluded instrument. If the F statistic (4.459) is below the Stock and Yogo (2005) critical value (11.04), which it is in this case, the excluded instruments are weakly correlated with the endogenous variable and therefore are not the best predictors of TELs. In instances of weak instruments, results from an IV model could yield misleading results of statistical significance (Murray 2006). Given this finding and results reported in table 3, we believe a new set of instruments should be identified. What is more, even though results from an overidentification test suggest our instruments are not correlated with the error term, one concern is that theoretically, our instruments are correlated with the dependent variable of interest, and therefore invalid.

Alternative Instrumental Variable Specification

The instruments used in the previous section were derived from the voter initiative provisions. We therefore begin by examining the robustness of this variable as an instrument. We know the initiatives were vital to the tax revolt era. Rueben’s (1997) work has argued that these direct legislation provisions affected state revenues or expenditures indirectly through these tax limits (Rueben 1997, 28). However, in an extensive survey of the provisions, Waters (2003) finds they have been used to change administration of government, reform programs, and alter the direction of state and local government policies. 8 Piper’s (2000) survey of initiatives found 131, or 15 percent of all measures proposed between 1978 through 2000 were tax related. Of these, 87 were antitax—and of those, 35 were TEL specific. Finally, Matsusaka’s (1995, 2004) extensive research in this particular area has also found lower taxing and spending levels in states with voter initiative provisions.

We therefore argue that if voter initiative provisions have been used to propose changes to the state’s policies including taxing and spending policies independent of the TEL laws, the initiative provisions are an important explanatory variable that should be used to explain the presence of the limit, but more importantly have an independent effect on taxing and spending levels. In our alternative specification, both voter initiative provisions and its corresponding geographic signature requirement are included as relevant explanatory variables. We already know these institutions to be important predictors of both TEL it and Yit , and believe this to be a more appropriate specification. We further assume the initiative to be an exogenous policy variable (Marschall and Ruhil 2005). 9

We now need to identify an alternative set of instruments that are correlated with the endogenous variable and not correlated with the error term. We find we cannot divorce ourselves from the initiative as an instrument and consider provisions within the initiative, rather than its mere presence. We include (1) whether voters can initiate an amendment to the state’s constitution directly without legislative review and (2) whether voters must submit ballot measures for legislative review. The former allows voters to place a measure on the ballot directly. The provision empowers voters more than any other initiative provision does, as the legislature cannot intervene on such a measure and the constitution can only be amended via referendum. The legislative review of ballot measures gives the legislature the opportunity to amend and/or adopt any measure either as a statutory measure (via simple majority vote) or a constitutional amendment (via a legislative referendum). In this instance, voters have significantly less control over the measure that is actually adopted by the legislature. We include a third instrument—the citizen ideology index. This index is often used as a proxy measure for the unobservable preferences of voters that is a source of potential endogeneity (Wagner 2004). We believe voters who prefer a conservative taxing and spending policy will support tax limit measures while those who prefer a more liberal taxing and spending policy would not support TEL measures.

We include as an additional explanatory variable an indicator variable for local government property tax limits and rely on Yuan et al. (2009) in developing the variable. These limits are independent of the state-level TELs, but impose a real constraint on the taxing and spending authority of local governments (Preston and Ichniowski 1991; Shadbegian 1999; McCubbins and Moule 2010). As such, local governments are increasingly reliant on nontax sources of revenue including state aid to meet current service demands. Consequently, the taxing and spending burden for state governments is even greater.

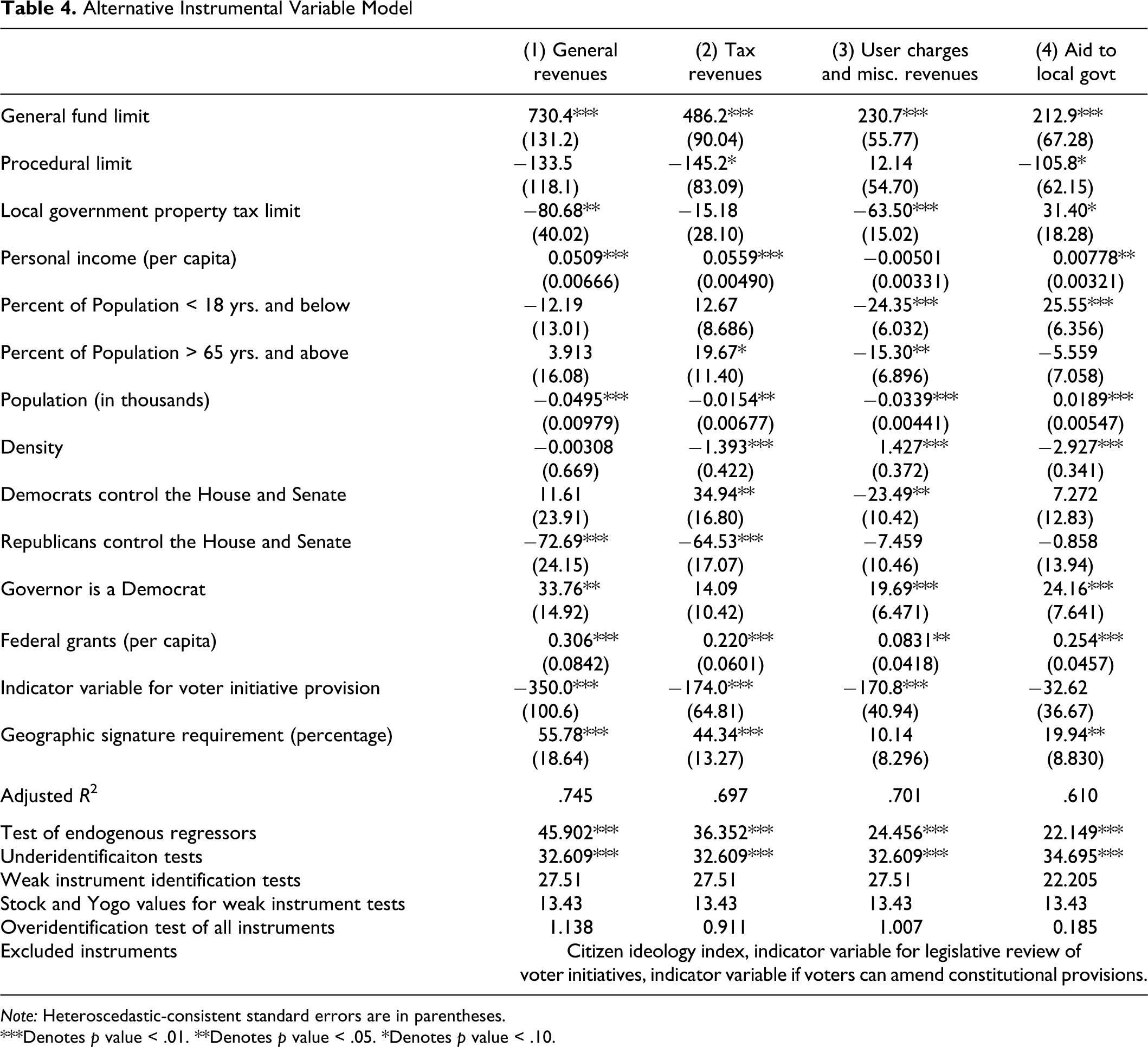

Our results given the preceding specification are reported in table 4 (columns 1 through 3). Note that coefficients for the general fund limit are now all positive and significantly different from zero in all three regressions. States with general fund limits raise an additional $730 in own source revenues; of which $486 is from tax revenue and $231 is from user charges and miscellaneous revenues. Our coefficient for the procedural limits is negative, but is only statistically significant in our tax revenue regression (−$145, p value < .10). This suggests the procedural limits constrain taxing authority of governments. These states do not substitute their lost taxing authority with nontax sources of revenue.

Alternative Instrumental Variable Model

Note: Heteroscedastic-consistent standard errors are in parentheses.

***Denotes p value < .01. **Denotes p value < .05. *Denotes p value < .10.

This regression includes three additional variables—an indicator variable for the voter initiative provision, the geographic signature requirement (as a percentage), and an indicator variable for presence of a local government property tax limit. Our findings for the voter initiative and geographic signature requirement are consistent with Matsusaka’s (1995, 2004) work. States with voter initiative provisions have significantly less revenues. It also becomes more difficult for voters to initiate measures to block any additional taxing and spending programs if the geographic signature requirement is higher. The coefficient for the local government tax limit is also negative. We found states did not increase their taxing authority, but rather reduce their nontaxing revenues by approximately $64 per capita. 10

Our results are robust. Our weak identification statistic (27.51) is now greater than the Stock and Yogo (2005) critical value (13.43). This suggests our instrument set is more appropriate. The p values for the overidentification tests are now far from rejection, giving us greater confidence that our instrument set is valid. 11

Impact of TELs on State Aid to Local Governments

Mullins and Joyce (1996) and Skidmore (1999) found the enactment of local TELs was associated with increased centralization. We examine the impact of state-level TELs on aid to local governments. As we noted earlier, a second wave to state-level TELs swept the nation in the mid-1990s and again in the early 2000, effects of which are not captured in the existing literature. We also find evidence of the impact of state-level TELs on aid to local government is limited, as scholars often examine the impact of local government TELs on local government revenues and spending, often with the local government as the unit of analysis.

Our dependent variable (Yit ) is state aid to local governments. We include control variables, time dummies, and state fixed effects as specified in equation (1). We include an indicator variable for local government TELs, that is, whether the state has imposed a limit on assessments, general or specific property tax rates, property tax revenues, or local government revenues or expenditures (Yuan et al. 2009). We did not include states with a full disclosure or truth in taxation requirement.

Note that in estimates reported in table 3 (columns 4 and 8), neither the general fund limit nor the procedural limit had a statistically significant impact on aid to local governments. Once we specify voter initiative as an explanatory variable and develop alternative instruments, the general fund limit coefficient is now positive and statistically significant (table 4—column 4). 12 States with a general fund limits transfer $213 more per capita to their local governments. These states have greater discretion over state aid to local governments as the general fund limits do not impose any real constraint on their taxing or spending levels (Kioko 2011). We also previously estimated that states with procedural limits have lower tax revenues ($145 per capita). In these states, their aid to local governments is also lower—$106 per capita. We also found aid to local governments in states with local TELs was slightly higher ($31 per capita).

Omitted Variable Bias of Institutional Variable

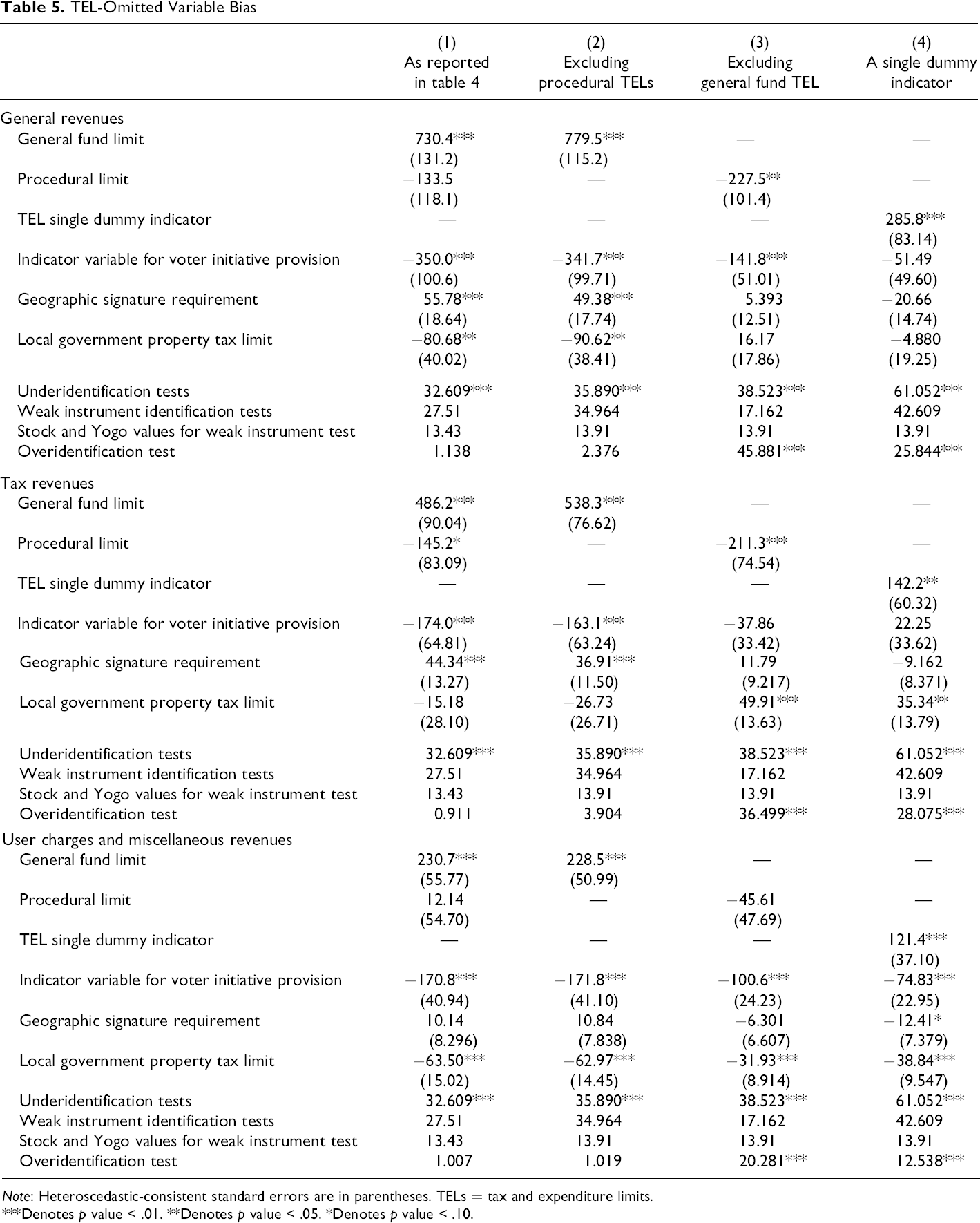

To be consistent with the literature, we compare the results from table 4 (repeated in column 1 of table 5) to those of three alternative specifications of the TELs. Each of these three alternative specifications are reported for general own source revenue, tax revenue, and user charges and miscellaneous revenue. As detailed in table 1, of the thirty-four TEL states, eighteen states only have a general fund limit, thirteen states have both a general fund limit and a procedural limit, and three states only have a procedural limit.

TEL-Omitted Variable Bias

Note: Heteroscedastic-consistent standard errors are in parentheses. TELs = tax and expenditure limits.

***Denotes p value < .01. **Denotes p value < .05. *Denotes p value < .10.

Our first regression estimates the impact the general fund limits on general revenues but excludes the indicator variable for the procedural limit (i.e., estimates for the thirty-one states with a general fund limit). Our survey of the public finance literature finds the general fund limits are often specified, but the procedural limits are generally not. As column 2 shows, the coefficients are slightly larger (by $49 and $52 per capita). There are also marginal changes to the voter initiative as well as the geographic signature requirement. The indicator variable for the local government TEL was also included in the regressions. In both the general revenue and tax revenue regression, the coefficient is slightly larger but consistent with what we reported in table 4. Also note there were only slight changes in the user charges and miscellaneous revenue regressions. Overall, the weak identification F statistic is sufficiently greater than the critical value, and we are also far from rejection in our overidentification tests.

In column 3, we exclude the general fund TEL indicator variable and specify only the procedural TEL variable which includes sixteen states, thirteen of which also have the general fund limit. Although this specification is rare in the literature, our objective here is to demonstrate the potential bias in results if the general fund TEL is omitted. Our coefficient for the procedural TELs remains negative in the general revenue and tax revenue regressions and is now not significant in the user charges regression. If the procedural TELs were substitutes for the general fund TEL, we would expect this coefficient to pick up on the effects of the general fund limit and become positive. The coefficient for the voter initiative provision is also significantly smaller in all three regressions. This suggests that the voter initiative dummy indicator is picking up the effects of the omitted variable—general fund TELs. Note that seventeen states have both the general fund TEL and the voter initiative provisions. For the general revenue regression, our coefficient for the local government TEL is now positive. Although it is not significant in the general revenue regression, it is positive and significant in the tax revenue regression. Robustness checks for all three regressions reveal troublesome results. We fail to reject the null in the overidentification tests, suggesting our instruments are correlated with the error term.

Finally, we aggregate the measure of TELs into a single dummy variable and present the results in column 4. This specification is very common in the literature. The variable includes the thirty-four states with any of the TELs in place. Our coefficient for the aggregated TEL measure is positive, statistically significant and nearly a third of the first two specifications. Our voter initiative and local government TEL measure are no longer significant. Also in the tax revenue regression, the coefficient for the local government TEL is now positive and statistically significant. Based on the overidentification test, we are not confident in these results. Rather, they affirm that using a single TEL indicator variable fails to get at the nuances of how TEL design impacts fiscal policy.

Discussion and Conclusion

In conclusion, this research contributes to the literature by identifying both general fund and procedural limits as important forms of TELs, controlling for endogeneity through an IV approach—improving upon previous specifications, and examining the impact of state-level TELs on state aid to local governments. The results of this study show that general fund limits do not constrain taxing and spending authority of governments. Conversely, procedural limits do diminish the taxing authority of states. Therefore, while general fund limits are not effective at controlling the public purse, procedural limits are. While in much of the research on TELs, the general fund limits and the procedural limits were thought to be comparable institutions, our findings suggests these institutions are operationally distinct tools. Our study finds the supermajority or voter approval requirement effectively constrain the government’s ability to impose new or higher taxes.

Our models of the impact of state TELs on aid to local governments also show that the limits on general fund authority do not decrease intergovernmental aid, but that procedural limits do. Surprisingly, local government property tax limits do not significantly affect intergovernmental aid. While previous studies show local governments counterbalance local property tax limits by increasing user fees and charges and income tax revenue, the local TELs are not the cause of change in state aid.

Finally, a growing literature tells us why these limits do not have a significant impact at the state level. For example, Bails (1990), Howard (1989), and Kioko (2011) found that there are a number of exempt expenditure categories in the general fund that may render the limit ineffective. A number of states, for example, exempt intergovernmental transfers and aid to local governments, property tax relief, or K–12-related spending. In a survey of the constitutional and statutory language of TELs across the states, Kioko (2011) finds the statutory and constitutional provisions have undermined the limits effectiveness, with the caps being set too high to be effective. Others have shown that states and local governments may use debt to meet capital-related expenditure needs as debt related expenditures are not subject to the TEL restrictions or rely on nontax sources of revenue (Bennett and DiLorenzo 1982; Clingermayer and Wood 1995).

Footnotes

Acknowledgments

The authors would like to thank the editor James Alm. The authors are also grateful for the valuable comments they received from John Yinger, William Duncombe, and the two anonymous reviewers. Remaining errors are the sole responsibility of the authors.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.