Abstract

Empirical studies suggest that the effects of tax audits are not only in terms of recovered unpaid tax (direct effect) but there are also indirect effects in terms of future better compliance that tend to outweigh the direct effect. However, current policy decisions on the allocation of investigation resources across different groups of taxpayers generally neglect the indirect effects, generating a potential resource misallocation issue. With the aim to clarify a possible mechanism through which the indirect effects work, the authors model tax compliance as a social norm and show that taxpayers’ interdependencies introduce a multiplier effect to an increase in the audit rate.

This article focuses on the indirect effects of auditing taxpayers. When a tax audit takes place, two main effects can be expected: (1) a direct effect, consisting of the amount of recovered unpaid tax and any fines applied to the noncompliant taxpayers, and (2) indirect effects, consisting of changes to future compliance behavior. These indirect effects take two forms: (1) changed behavior by audited taxpayers and (2) spillover effects to nonaudited taxpayers.

According to the empirical evidence on the impact of audits on taxpayers’ compliance, the indirect effects substantially outweigh the direct effect. Dubin, Graetz, and Wilde (1990) estimate a ratio between indirect and direct effects of six to one, that is, the indirect effects of audits produce six of every seven dollars of additional revenue. 1 A recent extension of this study by Dubin (2007) includes factors that measure the criminal investigation activity of the Internal Revenue Service (IRS) and considers the period from 1988 to 2001. Results from a simulation on doubling the audit rate suggest a ratio between indirect and direct effects of fifteen to one. Plumley (1996) presents an econometric analysis on the determinants of voluntary compliance, using a very rich data set by state and year, from 1982 through 1991. Controlling for tax policy measures (e.g., filing threshold, allowed exemptions), burden/opportunity variables (e.g., hours needed to complete a tax return, type of income), IRS enforcement measures (audit rate at the start of the period, information return matching program, nonfiler notices, refund offsets, and criminal tax convictions), IRS responsiveness (telephone assistance, return preparation services), and taxpayers’ demographic and economic characteristics, the author obtains an estimate for the ratio between indirect effects and direct effects in a similar way to Dubin, Graetz, and Wilde (1990) and gets a value of eleven to one.

The fact that taxpayers may be affected by the audits even if not directly involved in the assessment seems to be confirmed by surveys and laboratory experiments on taxpayers’ attitudes toward noncompliance. Several studies show that individuals’ (self-reported) compliance is correlated with their estimate of other individuals’ compliance (e.g., Bosco and Mittone 1997; De Juan, Lasheras, and Rafaela 1994; Webley, Henry, and Morris 1988). Torgler (2002) reviews experimental findings on tax compliance, which suggest that there are some interdependencies in individuals’ decision of whether or not to evade and their perceptions of other taxpayers’ evasion.

However, current policy decisions on the allocation of investigation resources across different groups of taxpayers typically neglect the indirect effects. Actual targets and resources for audits across different groups of taxpayers are set on the direct yield:cost ratio, at least in the United Kingdom and United States, as this is currently the only available measure of the effects of an audit. If the ratio between the indirect and direct effects were constant across different groups of taxpayers, then neglecting the indirect effects would not pose a problem of misallocation of resources. But, if the ratio were to vary, the resulting decision would be suboptimal, as it would not take into account the full marginal benefit of an increase in the audit rate. In order to assess the potential misallocation issue, we need a better understanding of the determinants of the indirect effects. Although the indirect effects have been estimated in empirical studies, the theoretical models on tax evasion do not seem to pay attention to the distinction between the direct and indirect effects of audits. In the standard portfolio models, 2 the tax parameters are fixed, chosen independently from taxpayers’ behavior. Later contributions have analyzed, by the use of game theoretical models, the interaction between taxpayers and the tax authority. The assumption made in those models is that the choice of the tax parameters depends on the extent of evasion, in that taxpayers’ decisions have an impact on the tax revenues raised by the government. 3 However, these models consider the overall response of taxpayers to the audit policy, without distinguishing between direct and indirect effects.

In this article, we model a possible mechanism through which the indirect effects may work. We consider the role of social interactions in a community of taxpayers in explaining the existence of indirect effects. Similar to Myles and Naylor (1996), these social interactions work through a conformity payoff: in case of evasion an individual incurs a psychic cost, which (positively) depends on the proportion of honest taxpayers. However, in our model, this psychic cost is suffered only in case of detection, as a loss in reputation for being discovered cheating the tax authority. Unlike in Myles and Naylor (1996), it is not a personal moral cost incurred for hiding one's income, irrespective of being subject to an audit. We not only show that an increase in the probability of audit has the expected deterrence effect, consisting of an increase in the expected fine, but we also identify a multiplier effect of audits which acts through the reputational cost.

The remainder of this article is organized as follows: The second section sets out our model. We first consider individual behavior and then extend the analysis to a community of taxpayers. In the third section, we consider the effects of an increase in the audit probability on a possible interior equilibrium and distinguish the normal deterrent effect of inquiries from a multiplier effect due to the existence of the reputational cost of being caught. The fourth section presents our conclusions.

The Role of a Social Psychic Cost of Being Investigated

Social interactions across taxpayers have been considered by some theoretical developments of the standard model of tax evasion. The assumption made in these models is that individuals attach a moral content to tax compliance and hence suffer a psychic cost when cheating the tax authority. Gordon (1989) considers the case of a social stigma attached to the act of evading taxes, which depends on the proportion of the population who are believed to consider tax evasion as morally wrong and is suffered irrespective of being detected. Myles and Naylor (1996) capture the influence of social interactions in the taxpayers’ decision whether or not to evade in the framework of the social custom and conformity approach. In their model, a social custom utility is derived when taxes are paid honestly. Individuals also get an extra utility from conforming with the standard pattern of social behavior. Hence, the utility from nonevasion includes two extra arguments neglected in the standard portfolio model: a fixed gain from following the social custom and an extra gain from conforming to the other honest taxpayers, which depends on the number of honest taxpayers. Like in Gordon (1989), Myles and Naylor assume that there is a moral dimension in the act of behaving honestly.

In our model, we adopt a different approach than Gordon (1989) and Myles and Naylor (1996). In line with the rather uncompelling results of empirical studies on how morals actually translate into taxpayers’ behavior, 4 we adopt a less strong moral connotation attached to tax compliance. We assume that individuals suffer a psychic cost for evading only in case of detection, such as a loss in reputation. This loss in reputation is not linked to the act of evading, but rather to the fact of being audited and caught. There is not necessarily any personal conviction that paying taxes honestly is morally right, that is, there is no personal moral cost of evading. In line with the empirical evidence mentioned previously, we assume that this psychic cost is decreasing with the perceived number of tax cheaters in the community. Kim (2003) also considers a model where taxpayers suffer a stigma for being audited and exposed as cheaters. The author is interested in the analysis of the existence and characterization of the equilibria emerging when taxpayers’ behavior is affected by this social stigma and in the analysis on the impact of income distribution on the existence of multiple equilibria. The aim of our model is to analyze the taxpayers’ response to an increase in the audit probability when social interactions act through a reputational nonmonetary cost. The previous models on social interactions did not consider this issue, their main focus being the explanation of why taxpayers tend to be more honest than expected by the standard portfolio model.

In the next section, we present our model. We first consider the decision of a single individual and then we extend the analysis to a group or community of taxpayers.

Individual Behavior

In the analysis that follows, we consider the taxpayer decision as a two-step decision: the taxpayer first decides whether or not to evade, by comparing the utility of nonevasion with the expected utility of evasion, and then chooses the optimal amount of evasion. We focus on the decision whether or not to engage in tax evasion. In order to keep notation simple and to concentrate on the effects of social interactions, we make the assumption of risk neutrality. Our results are not qualitatively affected by this assumption. In fact, the degree of risk aversion does not affect the decision whether or not to evade: tax evasion will be chosen whenever the probability of being detected is below a certain threshold, determined by the value of the fine and tax rate. 5 The degree of risk aversion affects instead the decision how much to evade. Another assumption we make is that once an individual is investigated, tax evasion is fully detected, as in the standard portfolio model.

Let us define the utility from nonevading for an individual i, with income normalized to 1 and facing a tax rate t, as follows:

The utility from evading is as follows:

We shall assume that from a monetary point of view, evasion is always worth it, that is,

The Community of Taxpayers

In our model, opportunities to evade are exogenous, in that they are not affected by the tax parameters and the psychic cost. Given that we assume

Let

We now check what types of equilibria there might exist:

Zero evasion equilibrium: It can be easily seen that an equilibrium with zero-evasion will not be possible as follows: if

Full evasion equilibrium: if

Interior equilibria: As

with

All we can say about the sign of equation (7) is that if

In conclusion, the existence of multiple equilibria depends on the shape of the psychic cost function and on the distribution of the importance attached to the psychological cost of being audited.

In what follows, we shall assume the existence of a unique interior equilibrium and consider the comparative statics for a change in the audit rate. We make the assumption that

Effects of an Increase in the Probability of Detection on the Proportion of Evaders

We now consider the effect of an increase in the probability of being audited on the number of evaders. In equilibrium, equation (6) holds and

The first term on the left-hand side of equation (9) represents the normal deterrence effect of audits: an increase in the probability of detection makes the entry condition for evasion more restrictive and hence lowers the critical level of importance of the psychic cost (

In order to assess the magnitude of this additional effect due to taxpayers’ interactions relative to the normal deterrence effect, we run a simulation. We assume

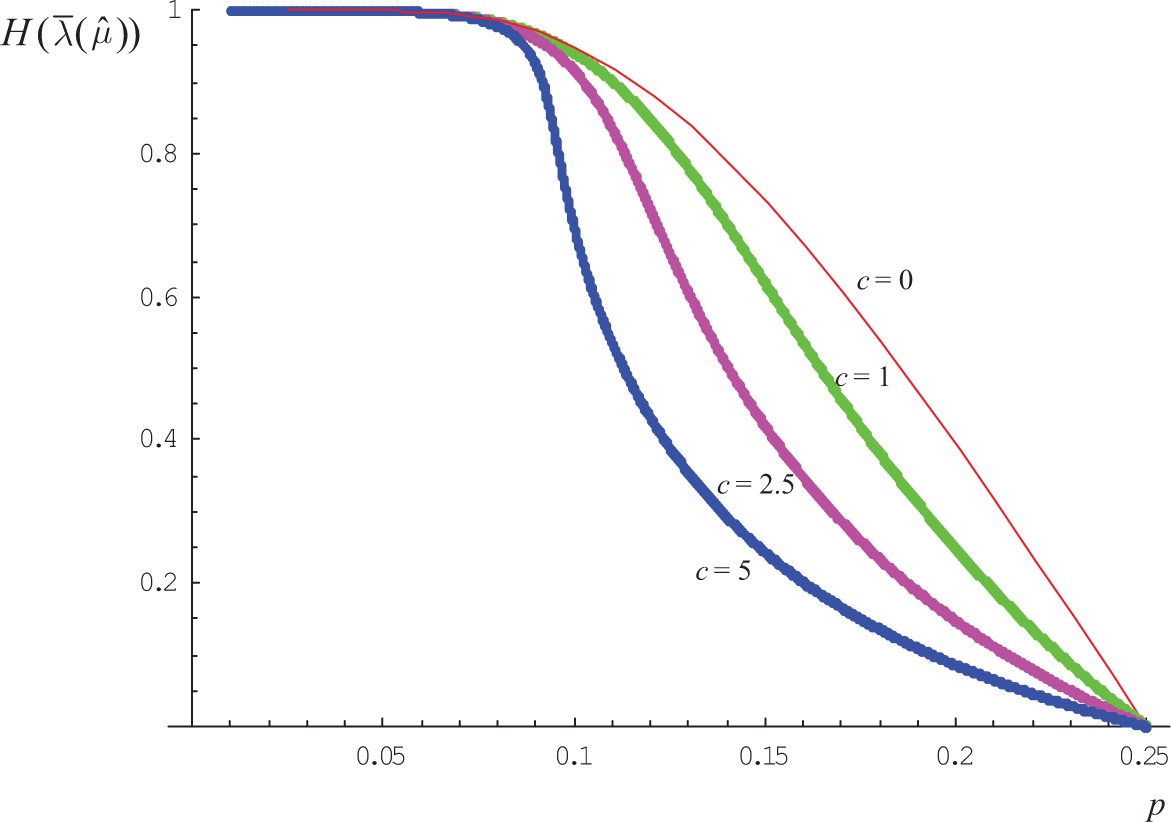

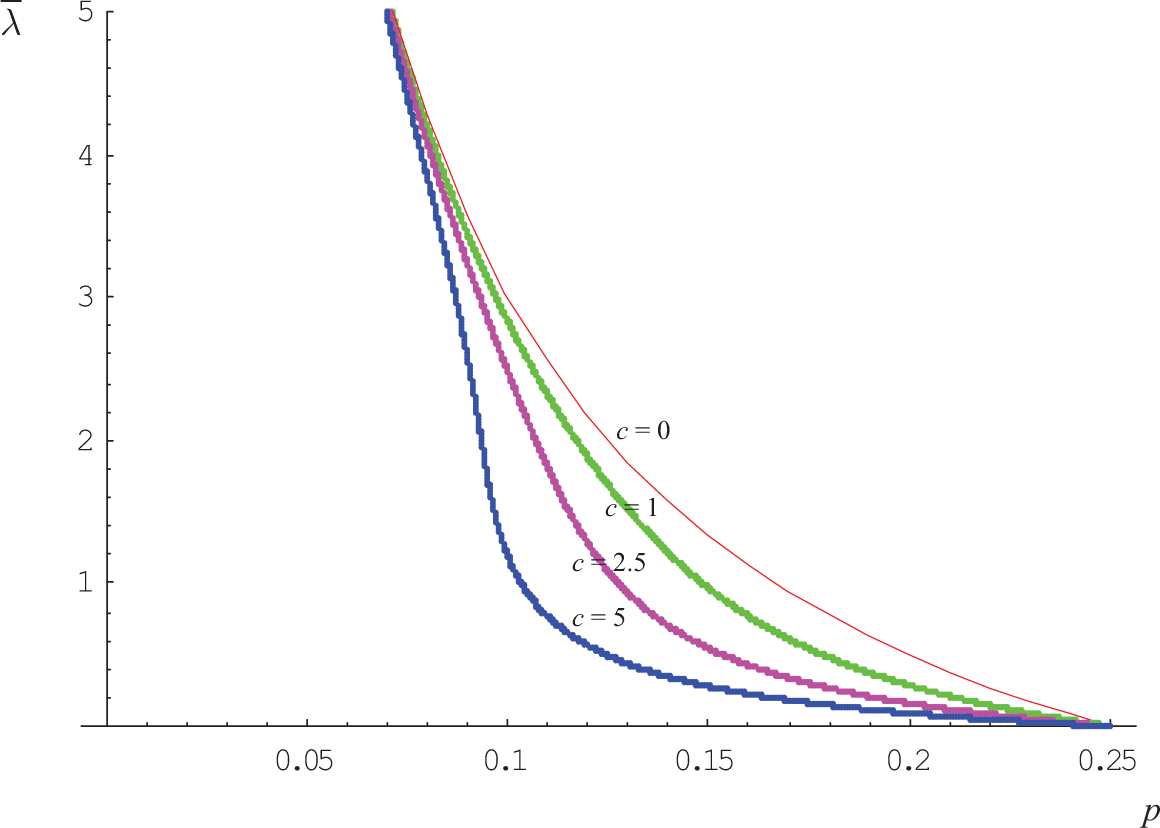

We then consider how a change in the probability of being detected affects taxpayers’ behavior at the margin. In figure 2, we show how the equilibrium upper limit of the distribution of evaders, as defined in equation (8), changes with the probability of detection, for different values of the marginal psychic cost of being caught.

Equilibrium proportion of evaders for different values of the probability of being detected.

Equilibrium upper limit of the distribution of evaders for different values of the probability of being detected.

The standard deterrence effect of an increase in the probability of detection is illustrated on the curve for c = 0. The additional effect due to taxpayers’ interactions is represented by the difference in the slope of the curve for c = 0 and the slope of any curve for c > 0, for each value of p.

Figure 2 shows that, for low values of the probability of detection, the slope of the curve for c = 5 is greater than the slope of the other curves. This implies that for low values of the probability of detection, the greater the marginal cost of losing one’s reputation in case of detection, the greater the additional effect on the equilibrium proportion of evaders relative to the normal deterrence effect. As the probability of being detected increases, the additional effect of taxpayers’ interactions becomes less and less important relative to the normal deterrence effect. With the chosen parameters, for values of p > .11, the curve for c = 5 becomes flatter than the other curves. As we approach p = .25 hardly anybody evades and the slope of any of the curves for c > 0 is less than the slope of the curve for c = 0. The intuition is that the greater the number of compliant taxpayers, the more negligible the additional effect of social interactions, driven by a switch from evasion to non evasion. Hence, an increase in the probability of an audit is most effective when the probability of detection is very low and the marginal psychic cost is very high.

In conclusion, in the presence of a nonpecuniary cost of being investigated which depends on the proportion of evaders, an increase in the probability of detection will cause the fraction of the population who evades to fall, and this will give an extra reason for people to stop evading over and above the normal deterrence effect. Moreover, for sufficiently low values of the probability of detection, the greater the marginal psychic cost, the greater will be the fall in the proportion of evaders. 9 Note that these results rely on the assumption that the psychic cost of being audited increases with the number of other honest taxpayers. Similar results could be obtained in Myles and Naylor (1996). Although the authors do not consider this issue, it can be shown that an increase in the probability of detection causes the marginal individuals to stop evading; this lowers the proportion who evades, which in turns reduces evasion, as the extra gain from conforming with the honest taxpayers increases—and so on. However, in their model, results may not be so clear-cut. In fact, their approach is based on the assumption that tax compliance has a moral connotation. According to some authors, 10 the intrinsic motivation to comply with the tax duties, based on morals, may be crowded out by an external intervention of the tax authority, such as an increase in the audit rate. In their view, an increase in the audit rate would be perceived by taxpayers as a controlling activity—that is, not giving any recognition to civic virtue. This would change their utility function, by making the extra utility gain from conforming with the honest taxpayers less important. Hence, there would be two opposing effects of an increase in the audit rate: an increase in the payoff from conforming to the honest taxpayers—due to a decrease in the proportion of evaders—and a decrease in the importance attached to that same payoff—due to the crowding-out effect—,possibly leaving the final effect undetermined.

Conclusion

In this article, we consider how taxpayers’ interdependencies may amplify the normal deterrence effect of audits. We extend the standard portfolio model by introducing a nonmonetary cost of being audited, which increases with the number of honest taxpayers in the community. We show that an increase in the probability of audit causes the marginal individuals to stop evading. This is the normal deterrent effect of investigations pointed out in the standard portfolio model. However, there is an additional effect. Given that less people than before are evading, the magnitude of the psychic cost increases and this discourages even more people to continue evading and so on, giving rise to a multiplier effect. This prediction gives some support to the results of empirical studies suggesting the overwhelming role of indirect effects of investigations over the direct effects. Although we cannot claim the multiplier effect to be greater than the direct deterrence effect as a general result, our simulation shows that for sufficiently low values of the probability of detection, the multiplier effect can be greater than the direct deterrence effect. We should also note that in our analysis, we only considered one group of taxpayers (subject to the same tax parameters). In the presence of different groups of taxpayers, there will be spillover effects across different groups, which will make the indirect effects even more important and hence more likely to be greater than the direct effects.

Our results also make it clear that the indirect effects depend on the magnitude of the reputational cost of being audited and on the importance attached to this cost, which are very likely to vary across taxpayers. Hence, we should not expect the ratio indirect/direct effect to be constant, even across taxpayers belonging to the same group (subject to the same tax parameters). This implies that if audit resources are allocated by only considering the direct effects, there are important misallocations issues. A better understanding of how interdependencies across taxpayers actually occur is then crucial for any policy intervention. This calls for the identification of a possible reference group, which may differ across different taxpayers and could be based, for example, on occupation, or on neighborhoods or on the use of the same tax agent.

An important policy implication of our results is that the announcement of the investigation results can have a substantial role in reenforcing the multiplier effect of audits if reputational effects are at work. This raises the question of what kind of announcements the tax authority could make to deter noncompliant behavior. However, the answer to this question hinges on the type of social interactions that may be at work. As pointed out by Manski (2000), in order to analyze social interactions, it is crucial to distinguish between preference interactions—one person may imitate another because the former prefers to act like the latter—from the expectation interactions, generated by observational learning—one person may imitate another because he or she believes that the other person has superior information. These different explanations of social interactions have different policy implications in that “Interventions that provide new information may alter the nature of expectations interactions or even cause them to disappear, but should have no effect on preference interactions.” 11

In this article, we consider preference interactions, and indeed the policy implication is that the greater the publicity of the number of people convicted and stopping to evade, the greater the impact of the social psychic cost. However, social interactions among taxpayers could also be explained as expectation interactions. For example, if taxpayers do not know the actual probability of being detected, they could use the information about the proportion of detected cheaters to update their perceptions of the audit rule. But, in line with what suggested by Manski (2000), in this case, an announcement by the tax authority about the audit results may have detrimental effects, especially if individuals tend to overestimate the probability of detection. Hence, more research needs to be undertaken on the updating process of audit perceptions in order to have more conclusive policy implications of the tax authority’s announcements about the results of an audit.

Footnotes

Acknowledgments

We are very grateful to Thibaud Vergé for his helpful suggestions. For helpful comments on earlier versions of this paper, we would also like to thank two referees and the editor of Public Finance Review. This article benefited from the contributions of participants at the IFS Public Economics Working Group (Warwick, 2004), at the International Conference on Public Economic Theory PET04 (Beijing), at the Royal Economic Society annual conference 2005 (Nottingham), at the Macroeconomic and Policy Implications of Underground Economy and Tax Evasion Conference (Bocconi University 2009), and at seminars at CMPO (Bristol University), Paris 1 Pantheon-Sorbonne and Paris-Dauphine. All remaining errors are the authors.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.