Abstract

This article investigates whether reputation-building strategies may guide US governors’ state cigarette tax choices and whether the federal cigarette tax influences such behavior. Using 1975–2000 data, we find evidence indicating that governors are prone to engage in reputation building, in particular in states with relatively important agricultural tobacco production. Moreover, lame ducks are more prone to raise the state cigarette tax the lower the federal tax.

Keywords

Tobacco use is the leading preventable cause of death in the United States. A direct contributor to this massive health burden is the effectiveness of the tobacco industry’s activities, including campaign contributions. —D. A. Luke and M. Krauss (2002, 363)

The literature studying political reputation-building behavior by politicians has recently documented how state fiscal and environmental policies are used to attract certain voter groups to governors’ platforms (Besley and Case 2003; List and Sturm 2006). List and Sturm (2006) present a two-policy model where a politician sets both primary policies (e.g., government spending or the extent of wealth redistribution) and secondary policies (e.g., environmental policy or trade policy). Their model predicts that if the secondary policy is some voters’ main priority, politicians may distort the secondary policy to attract such “single-issue voters.” The state cigarette tax is (in our view) an example of a secondary policy, and this is the policy focus in the current article.

Taxation of tobacco products is a relatively important issue in the United States. For example, in 1997 US tobacco farmers sold tobacco leaf valued at $2.9bn, US consumers spent $52.6bn on tobacco products (out of which $5.7bn was federal taxes and $7.8bn was state and local taxes), and 1 to 2 million jobs are supported by the tobacco industry (farming, manufacturing, wholesale, and retailing), according to Gale, Foreman, and Capehart (2000). Uri and Boyd (1997) find that a $1 per pack equivalent increase in the excise tax on tobacco products could cause a fall in the consumption of all goods and services in the United States by approximately 0.49 percent, a fall in tobacco consumption by more than 12 percent, a decline in total utility by almost 0.5 percent, and a net increase in government revenue by more than 1.7 percent. 1 Various voter and interest groups have intense preferences over state cigarette taxes. These groups include not only cigarette smokers but also factor owner lobby groups and workers in agricultural tobacco production and in the cigarette (tobacco products) manufacturing industry. These groups all favor lower cigarette taxes. 2 On the other hand, antismoking groups favor higher cigarette taxes.

Politicians value financial contributions from special interest groups (Grossman and Helpman 1994; Kroszner and Stratmann 1998), and this is also true in the area of cigarette taxation. For example, Glantz and Begay (1994), Goldstein and Bearman (1996), Morley et al. (2002), Luke and Krauss (2002), and Esteller-Moré, Galmarini, and Rizzo (2012), all argue that lobbying is an important influence on policy in the area of state cigarette taxation. 3 In this article, we rely mainly on the theoretical framework developed by Kroszner and Stratmann (1998), who argue that politicians build a reputation with various lobby groups. Kroszner and Stratmann (1998) argue that over time, as a politician’s credibility rises as a champion of a particular group’s interest, the politician will be supported with larger amounts of campaign contributions by groups close in ideology. Kroszner and Stratmann (1998) suggest that as the probability rises that the politician leaves office, the level of contributions will decline. Kroszner and Stratmann (1998) find evidence that political action committee (PAC) contributions dried up almost completely for US House Banking Committee members who announced their retirement. Apollonio and La Raja (2006) also report that term-limited state legislators receive fewer campaign contributions. Since a lame duck governor has a probability equal to unity of leaving office, it follows that contributions given to such governors should decline sharply. In the area of tobacco, lobbying is carried out by tobacco farmers, the tobacco manufacturing industry, and by antismoking groups. 4 Our first objective in this article is to study whether US governors use cigarette taxes to (1) build reputation among voters with a strong interest in the tax rate and/or (2) build reputation among agricultural and manufacturing lobby groups with a large stake in cigarette taxation.

Anecdotal evidence indeed indicates that governors use cigarette taxes to build reputation and gain re-election, and then raise this tax during the lame duck term. For example, in his lame duck term, Gov. Parris N. Glendening (D) of Maryland pushed through a 30 cents/pack state cigarette tax (to 66 cents per pack, effective July 1, 1999). His predecessor Gov. William D. Schaefer (D) had then already raised this tax twice in 1991 and 1992, while in lame duck status. 5

In our analysis of reputation building, we also contribute by incorporating insights from the literature on fiscal federalism: policies set by one level of government have been found to influence the policies set by the government at another level. We therefore believe the results from the literature on vertical tax interactions should be taken into consideration in empirical studies of state cigarette taxation. This literature establishes that states set taxes (e.g., cigarette, gasoline, income, and corporate taxes) conditional on the federal cigarette tax rate (see, e.g., Besley and Rosen 1998; Esteller - Moré and Solé - Ollé 2001, 2002; Rork 2003; Devereux, Lockwood, and Redoano 2007; Fredriksson and Mamun 2008). This suggests that governors may take the federal tax rate into consideration also when engaging in reputation-building activities. Our second objective is to investigate whether building in the area of cigarette taxation is conditional on the federal cigarette tax rate.

In 2000, seventeen states had positive amounts of agricultural tobacco production, while eighteen states had cigarette manufacturing located within their borders. This makes cigarette taxation a suitable policy to study reputation building, as state politicians may be expected to be especially likely to build relationships and reputation among tobacco (agricultural and manufacturing) lobby groups in states with tobacco-related economic activity. The share of smokers in the population may also matter for governors’ propensity to engage in reputation building (List and Sturm 2006).

Our empirical results appear to partially confirm that reputation building occurs. Utilizing state-level panel data for 1975–2000, we find that governors engage in reputation building as indicated by a temporal difference in tax rates when they reach lame duck status. In particular, such reputation building is conditional on the amount of agricultural tobacco production in the state (indicating agricultural tobacco sector lobbying; see Potters and Sloof 1996). The amount of cigarette manufacturing and the share of smokers in the state do not appear to generally affect reputation building, however. A lame duck governor raises the state cigarette tax, in particular if the state has a high concentration of agricultural tobacco production. Thus, not only do voters hold governors accountable as shown by List and Sturm (2006), but reputation building is also related to lobby group activity, as suggested by Kroszner and Stratmann (1998). Moreover, the policy effects of these reputation-building activities are conditional on the federal cigarette tax. Lame duck governors raise the state cigarette tax by more, the lower the federal cigarette tax. We believe our empirical results complement existing findings in the literature.

The article is organized as follows: the second section further outlines the theoretical predictions provided by the literature and gives a brief overview of the existing empirical results. The third section discusses the empirical model and data. The fourth section presents the results and is followed by the conclusion.

Theoretical and Empirical Background

Theoretical Predictions

Kroszner and Stratmann (1998) argue that politicians seek to build up a favorable reputation with lobby groups through repeated interactions over time. 6 As time passes, a politician’s credibility rises with a particular interest group due, for example, to a consistent voting record and high effort level on behalf of the group(s) (e.g., by drafting bills, negotiating with legislators, giving media interviews, or by meeting and persuading voters). This reduces uncertainty for the lobby groups regarding policy outcomes (see also Gilligan and Krehbiel 1989). As time progresses, the politician increasingly receives support only from groups close in ideology and policy preferences. The amounts of campaign contributions received increase due to the reputation-building activities. However, these funds disappear when the politician faces a certain eviction from office. Consistent with the empirical findings by, for example, Kroszner and Stratmann (1998) and Apollonio and La Raja (2006), we assume that a lame duck governor receives lower amounts of campaign contributions by the agricultural tobacco and cigarette manufacturing lobbies. Thus, the term-limited politician has a lower incentive to set a cigarette tax that deviates from his or her most-preferred policy.

List and Sturm (2006) present a two-policy model where a politician sets both a frontline policy and a secondary policy. Voters have heterogeneous preferences over policies. While most voters have no preferences over the secondary policy, for some voters the secondary policy is of greater importance than the frontline policy. There is uncertainty regarding the politician’s preferences over the secondary policy. The model predicts that if the secondary policy is some voters’ main priority, politicians may distort the secondary policy to attract “single-issue voters.” An increase in the number of voters that can be attracted by distorting the secondary policy raises the probability that incumbent governors engage in reputation building activities. 7 In equilibrium, even politicians with views opposite to the single-issue voters may seek to placate this voter group by distorting their policy choice in order to win reelection. However, when politicians face a binding term limit, they set their preferred policies rather than strategically distorting policies, since gaining votes and reelection are no longer considerations (consistent with, e.g., Alesina 1988). This view is supported empirically by Besley and Case (1995) who report that lame duck governors do not appear to care for either their own or their party’s reputation, as evidenced by the finding that only reelectable governors respond to natural disasters by raising expenditures. Thus, we expect reelectable governors to attract smokers to their platform by lowering the cigarette tax but to raise this tax as they gain lame duck status.

Besley and Case (1995) provide a model where voters with imperfect information reelect a governor with a higher probability, the greater the incumbent’s “effort” (which yields more “successful” policies and high voter utility) and reputation (see also Barro 1973; Banks and Sundaram 1998). In the governor’s final term, she finds herself a lame duck without reelection prospects, with no payoff from building reputation. Thus, she puts in less effort and her policy choices differ from earlier periods, consistent with List and Sturm (2006). 8

The theoretical literature on vertical tax interactions identifies a multitude of opposing and ambiguous effects of a federal tax on state commodity taxes. The impact of the federal tax rate depends on the price elasticity of demand, revenue effects, the extent of cross-border shopping, and on the degree of horizontal tax competition (see, e.g., Besley and Rosen 1998; Keen 1998; Devereux, Lockwood, and Redoano 2007). 9 It follows that governors are likely to take the federal tax rate into account when building reputation, as the cost of acquiring a reputation (and distorting state tax policy) will depend on the federal tax. Moreover, it appears probable that state legislatures’ willingness to change state taxes (or not) is conditional on the corresponding federal tax, as the marginal effect of, for example, a state tax increase is influenced by existing taxes levied by other levels of government.

Vertical yardstick competition may also play a role for reputation building by governors (see Salmon 1987; Bodenstein and Ursprung 2005). If voters compare the performance of the federal and state governments, governors eligible for reelection will take the federal tax into consideration in their reputation building. This will, in turn, affect their behavior as lame ducks.

Empirical Literature

The related empirical literatures contain a multitude of results. Kroszner and Stratmann (1998) find that older US House representatives and those who announce their retirement (from the Banking Committee) face declining PAC contributions, as they can no longer benefit from the reputation they have built with lobby groups. The empirical literature on the impact of reputation building on tax policy includes the important contribution by Besley and Case (1995), who find that Democratic lame duck governors set significantly higher per capita total state taxes and state expenditures than other governors. Millimet, Sturm, and List (2004) report that Republican lame ducks raise taxes and spending per capita more than do Democratic lame ducks. 10 List and Sturm (2006) establish that governors’ environmental policy (the secondary policy) choices change notably once they obtain lame duck status, and the change is conditional on the environmental preferences of the electorate. Lee (2002), Erler (2007), and Escaleras and Calcagno (2009) report that term limits lead to higher levels of spending. Chirinko and Wilson (2010) find that lobbying affects the level of horizontal tax interdependence. Fredriksson, Wang, and Mamun (2011) find that Democratic and Republican governors set similar environmental policies while eligible for reelection, but significantly different policies when facing binding term limits.

Besley and Rosen (1998; using 1975–89 data) and Devereux, Lockwood, and Redoano (2007; using 1977–97 data), for example, find some positive effects on US state cigarette and gasoline taxes of an increase in the corresponding federal excise tax. On the other hand, Fredriksson and Mamun (2008) report a negative vertical cigarette tax externality for the shorter time span, 1982–2001, while Esteller-Moré and Rizzo (2011) report an insignificant effect for the 1975–2006 period. This literature has not previously been incorporated in studies of reputation building and has not discussed such issues in the area of agricultural sector policy making.

Empirical Analysis

The Empirical Model

Drawing on the existing theories and empirical results discussed above, we distill three empirically testable implications. First, in states with more active agricultural tobacco and cigarette manufacturing lobby groups (with more at stake, as discussed by, e.g., Potters and Sloof 1996) and thus more intense reputation building by governors, we should see a sharper temporal difference in the state cigarette tax as governors reach lame duck status. Second, the temporal difference in the cigarette tax when a governor is reelectable versus a lame duck should depend on the fraction of voters with a relatively intense interest in the cigarette tax rate, reflected by the share of voters classified as smokers. The larger is this set of voters, the greater is the incentive of governors to build reputation with the help of cigarette taxes, by moving away from her bliss-point policy. Finally, if state cigarette taxes are set conditional on the federal cigarette tax, reputation-building behavior should also be conditional on the federal cigarette tax. Thus, we evaluate whether the temporal difference in the cigarette tax set by a re-electable and a lame duck governor may be conditional on the federal cigarette tax. The following empirical model is estimated:

where

Data and Hypothesis Specification

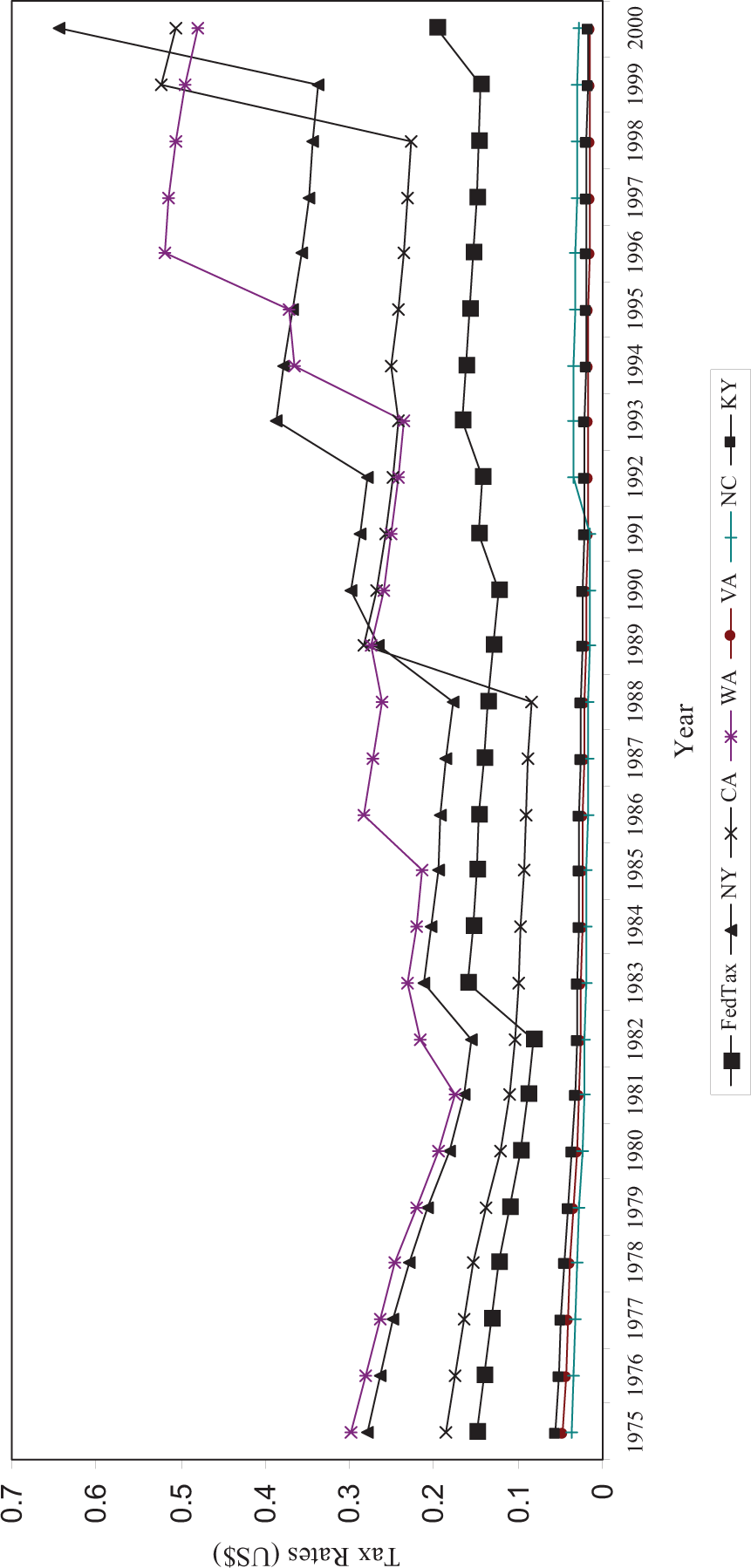

Our 1975–2000 panel data covers the 48 contiguous US states. All sources, variable definitions, and summary statistics are reported in table 1. The state and federal cigarette excise tax rates (per pack of 20 cigarettes) come from Orzechowski and Walker (2003) and are deflated to 1983 constant prices. The state tax rates (STATETAX) vary considerably across states and time. For example, during 1975–2000, the average real state cigarette tax was $0.025 in Virginia, while it was $0.38 in Washington. The nominal state cigarette tax rate increased in most states during this time period, although not in every state. The federal tax rate (FEDTAX) is (of course) identical for all states in any given year. The nominal federal tax rate was 8 cents per pack from year 1952 to 1982, but after several tax hikes it had increased to 34 cents by year 2000. Figure 1 presents the pattern of real cigarette tax rates over the sample period for (1) the three states with greatest real increases (CA, NY, and WA); (2) the three states with the greatest real declines (KY, NC, and VA); and the real federal tax rate.

Real federal cigarette tax rates and state cigarette tax rates. Note. Figure includes the three states with the greatest increases (CA, NY, and WA) and the three states with the largest declines (KY, NC, and VA).

Summary Statistics.

Note: GSP = gross state product; USDA = US Department of Agriculture.

Data on gubernatorial term limits come from List and Sturm (2006). LAMEDUCK takes a value equal to one in years where the incumbent governor is facing a binding term limit and zero otherwise. In many US states, governors face term limits after two terms in office. However, one term, three terms, and no term limits also existed during our sample period.

Data on the share of the population who are smokers come from the State Tobacco Activities Tracking and Evaluation (STATE) System of the Centers for Disease Control and Prevention (various years). Since the relative size of the smoking population across years is highly correlated within states, we use an average of smokers across years 1975–2000 to create the dummy variable SMOKER STATE, which takes a value of unity in states heavily populated by smokers and zero otherwise. While an average of 23.8 percent of the population in the United States are classified as smokers during the sample period, 31 percent of the inhabitants of Kentucky are smokers (highest frequency). While we do not have data on the number of antismoking proponents with preferences sufficiently intense to take them into account at the voting booth, we believe they are relatively few. 11

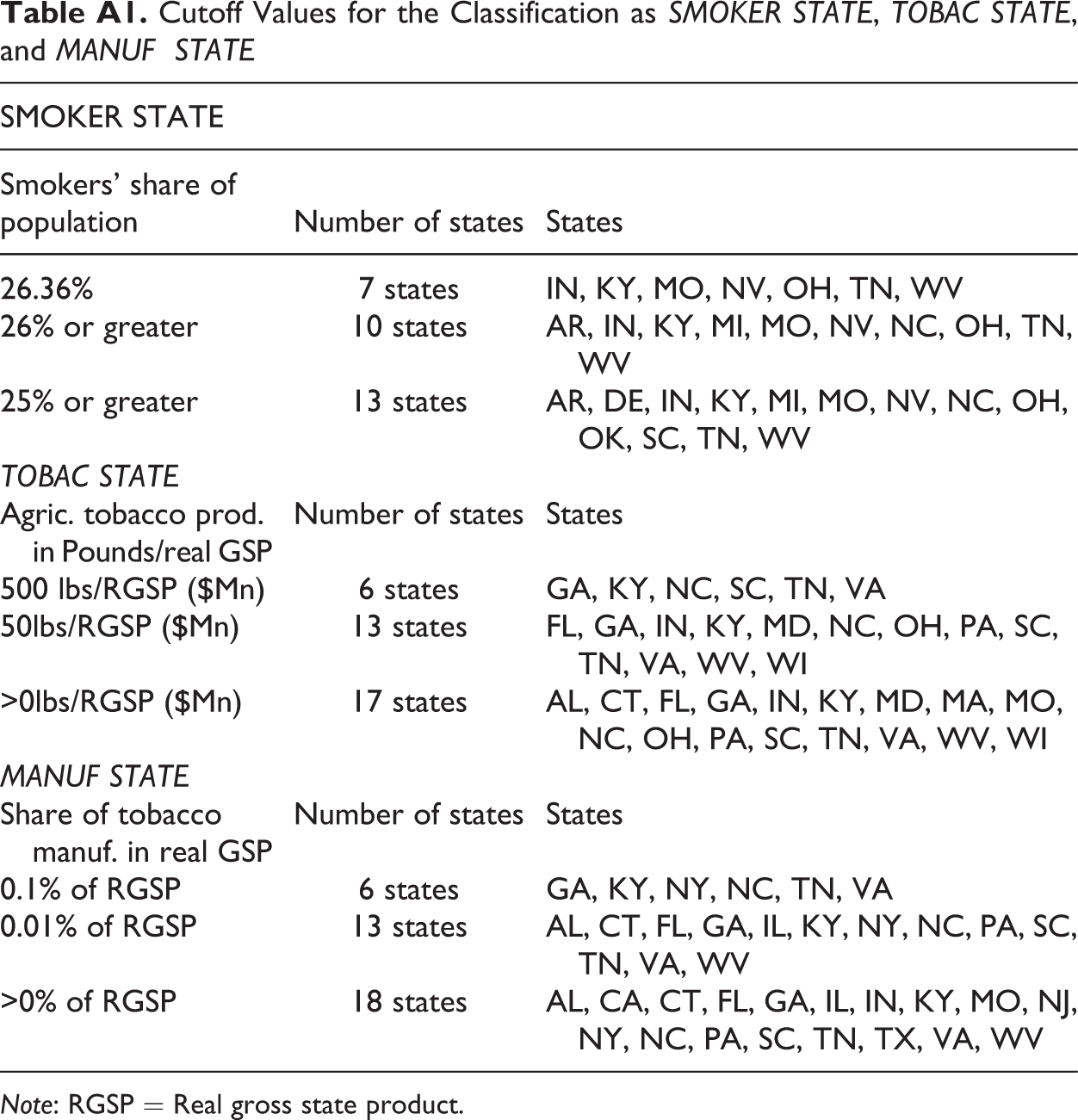

We also create dummy variables based on the average state agricultural tobacco production in pounds per $ million real gross state product (GSP; TOBAC STATE), and the average percentage of real GSP coming from the tobacco (cigarettes and other tobacco products) manufacturing sector (MANUF STATE; both variables are averages for years 1975–2000). These variables represent the lobbying impact of the agricultural tobacco lobby and the tobacco manufacturing industry lobby, respectively. With local production activity, lobbying influence is likely to be stronger, since more is at stake for the industry in such states (see, e.g., Potters and Sloof 1996). According to Jacobson, Wasserman, and Anderson (1997), the tobacco industry wields its strongest influence at the state level. See table A1 in the appendix for information about exact cutoff values and states. Data on agricultural tobacco production come from US Department of Agriculture (USDA various years), and data on tobacco/cigarette manufacturing come from the Bureau of Economic Analysis (US Department of Commerce various years).

All models (except in the robustness analysis, where noted) include NEIGHBORTAX, which controls for horizontal tax interactions (see Brueckner 2003; Devereux, Lockwood, and Redoano 2007). We utilize the population-weighted tax set by neighboring states, instrumented by the population-weighted state unemployment rate, the percentage of children and old in the population, and the proportion of democrats in the state house, following Rork (2003; see also Devereux, Lockwood, and Redoano 2007). Moreover, all models (except where noted) also include a lagged-dependent variable, STATETAXt −1, which is likely to be appropriate if state taxes exhibit strong serial correlation (Devereux, Lockwood, and Redoano 2007). STATETAX t −1 is instrumented by the second lag of the dependent variable. 12

We utilize similar control variables as Besley and Rosen (1998). In order to control for political party dominance, we use (1) a dummy variable equal to one if the state governor is a democrat (DEMOGOV), (2) the proportion of democrats in the state senate (DEMOSENATE), and (3) the proportion of democrats in the state house (DEMOHOUSE). Note that Nebraska has a nonpartisan, unicameral legislature due to the unicameral system of the state legislature. We therefore drop Nebraska completely from our data set, following, for example, Reed (2006). The state governor data come from the National Governors Association (2005), while the proportions of democrats in the senate and the house come from various editions of the Statistical Abstracts of the United States (US Census Bureau various years).

National real gross domestic product (GDP, NatlGDP) and the national unemployment rate (NatlUNEMPLOY) capture fluctuations in the national economic climate. These variables represent the

Next, TOBACCO INCOME equals tobacco production (lbs) per dollar of state income and comes from USDA (various years); it measures the relative importance of tobacco for the state. In addition, GAS measures gasoline production per dollar of state income. Tobacco producers may be expected to lobby for lower cigarette taxes, while gasoline producers should take the opposite stance (attempting to reduce the need to raise gas tax revenue). GRANTS is federal grants/capita, which reduces the need to raise state tax revenues. INCOME TAX is the federal income tax divided by adjusted gross income, which seeks to capture the ability of states to engage in further taxation effort. The daily gasoline production data comes from the US Department of Energy (various years) database, whereas federal grant and income tax data comes from the US Census Bureau (various years).

Empirical Results

Tables 2 through 4 present our fixed-effects models. As shown by Moulton (1986), ordinary least squares (OLS) estimations may give spurious results if the dependent variable is at the individual level and one or more of the independent variables are at the aggregate level. Thus, we utilize White (1980) robust standard errors and allow for within-year correlations. 14 We also report the joint significant tests for LAMEDUCK and its interactions with FEDTAX, SMOKER STATE, TOBAC STATE, and MANUF STATE, respectively. For all models in tables 2 through 4, R 2 fluctuates closely around .75 (not reported).

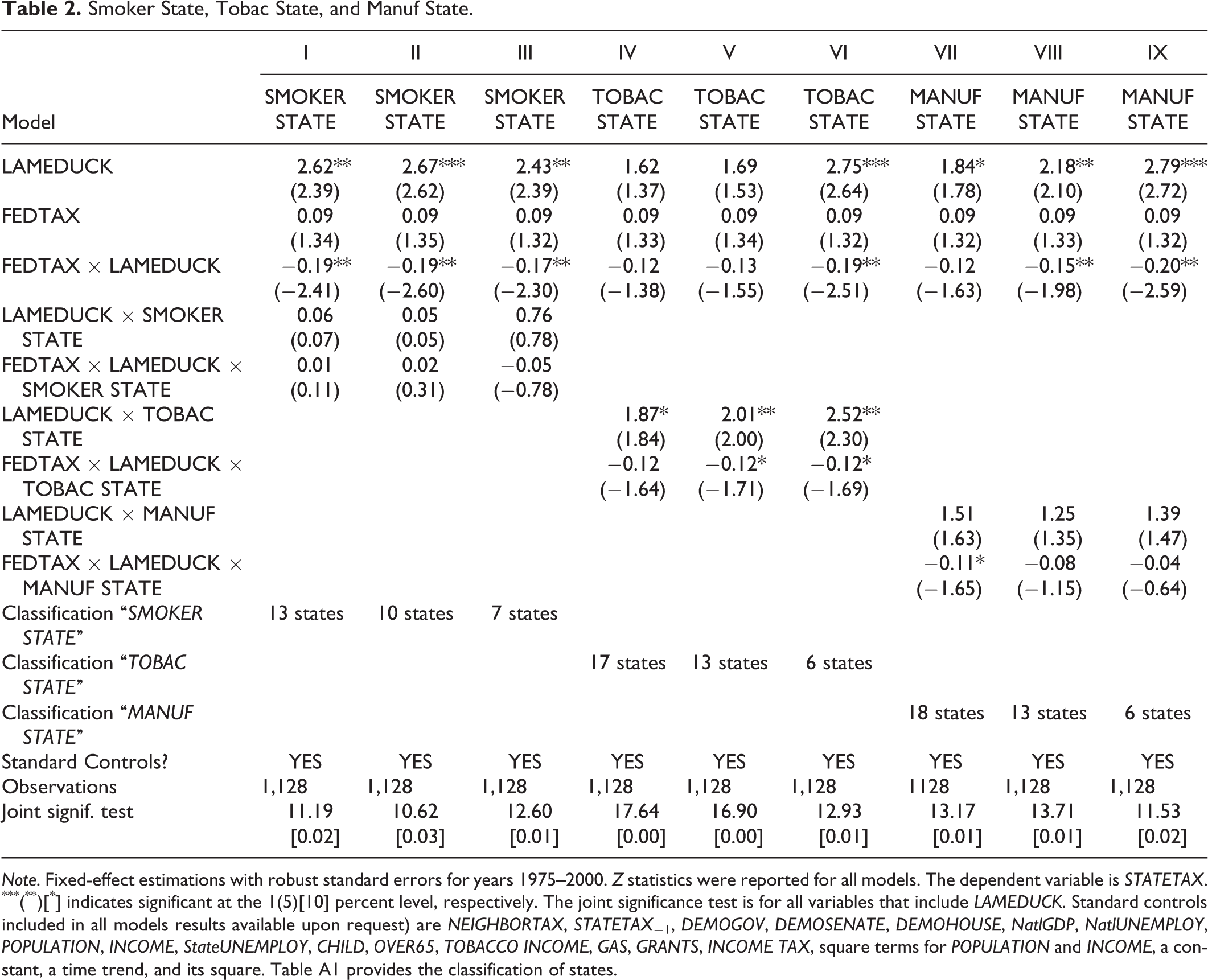

Smoker State, Tobac State, and Manuf State.

Note. Fixed-effect estimations with robust standard errors for years 1975–2000. Z statistics were reported for all models. The dependent variable is STATETAX. ***(**)[*] indicates significant at the 1(5)[10] percent level, respectively. The joint significance test is for all variables that include LAMEDUCK. Standard controls included in all models results available upon request) are NEIGHBORTAX, STATETAX −1, DEMOGOV, DEMOSENATE, DEMOHOUSE, NatlGDP, NatlUNEMPLOY, POPULATION, INCOME, StateUNEMPLOY, CHILD, OVER65, TOBACCO INCOME, GAS, GRANTS, INCOME TAX, square terms for POPULATION and INCOME, a constant, a time trend, and its square. Table A1 provides the classification of states.

Basic Model Results

Models I through III in table 2 present results for our measure of the share of voters most likely making a lower state cigarette tax a high priority (SMOKER STATE), with three classifications based on different cutoff levels (see table A1). Our classification of SMOKER STATE varies between cutoffs at seven states (at least 26.36 percent of the population are smokers) and thirteen states (at least 25 percent of the population are smokers). 15 Models IV through IX in table 2 report results using our two measures of interest group lobbying intensity; the classification of TOBAC STATE varies between cutoffs at six states (at least 500 lbs agricultural tobacco production per real GSP) and seventeen states (positive amount of agricultural tobacco production). The classification of MANUF STATE varies between cutoffs at six states (at least 0.1 percent of real GSP comes from tobacco manufacturing) and eighteen states (positive amount of tobacco manufacturing). See table A1 in appendix for further details.

Let us first turn to governor behavior in states not classified as SMOKER STATE, TOBAC STATE, or MANUF STATE. For example, model III indicates that, at the mean of FEDTAX, a lame duck located in such a state raises STATETAX by (2.43 − 0.17 × 13.94) = 0.06 cents. Moreover, she raises STATE TAX further (by 0.48 cents) if FEDTAX is 1 standard deviation (SD) below its mean (1 SD = 2.44). This is economically significant, particularly in states with low cigarette tax rates (see figure 1). The result is a first indication that under some circumstances reelectable governors build reputation by keeping state cigarette taxes low but raise the tax upon gaining lame duck status (when relieved of electoral accountability). However, model III suggests that at 1 SD above the mean of FEDTAX governors would lower STATETAX by 0.35 cents. Thus, lame duck behavior is conditional on the federal tax, and the federal tax may even reverse the direction of lame ducks’ tax changes. Models I through II and VI through IX yield similar results.

Why is lame duck behavior conditional on the federal tax? Lame ducks may encounter greater political resistance to tax hikes from lobby groups and (lobbied) state legislators, the higher the federal tax rate. If the drop in political contributions from tobacco-related lobby groups to lame duck politicians (as argued by Kroszner and Stratmann 1998) is less sharp when FEDTAX is high, lame ducks have a greater incentive to keep STATETAX low. Vertical yardstick competition (between the state and federal governments) may affect governors’ reputation building (see Salmon 1987; Bodenstein and Ursprung 2005). Moreover, Besley and Rosen (1998) argue that states raise tax rates in order to keep state revenues intact when the federal tax is high; Keen (1998) suggests that a higher federal tax raises the consumer price and reduces demand with the consequence that the welfare loss resulting from the state tax declines; and both Besley and Rosen (1998) and Keen (1998) argue that a higher federal tax increases the marginal value of state public goods, raising the attractiveness of the state tax. These effects cause reelectable governors to raise (lower) the state tax when the federal tax is high (low; for welfare reasons, in order to win reelection) above (below) their preferred level, ceteris paribus. Lame ducks are less guided by welfare considerations and set a tax in accordance with her preferences (as argued by Alesina 1988).

Next, we turn to the behavior of governors in states classified as SMOKER STATE, TOBAC STATE, and MANUF STATE, respectively. The results in table 2 indicate that reputation building among special interest groups by governors occurs primarily in TOBAC STATES. This behavior is most accentuated in the six states where agricultural tobacco production is relatively most important, as suggested by model VI (compare models IV–VI). Thus, agricultural tobacco lobbying interests are influential in the determination of state cigarette taxes in TOBAC STATES. Model VI suggests that at the mean of FEDTAX, a lame duck holding office in such a state raises STATETAX by 0.95 cents [(2.75 + 2.52 − (0.19 + 0.12) × 13.94) = 0.95]. However, if FEDTAX is 1 SD below the mean in a TOBAC STATE, a lame duck raises STATETAX by 1.70 cents. At 1 SD above the mean of FEDTAX, a lame duck raises STATETAX by only 0.19 cents. Table 2 indicates that the SMOKER STATE and MANUF STATE classifications yield no additional reputation-building effects (as evidenced by the mostly insignificant effects for the interactions with LAMEDUCK and FEDTAX × LAMEDUCK, respectively).

In sum, our results suggest that governors engage in reputation-building activities, and these activities are particularly aimed at agricultural tobacco producer lobby groups. Moreover, the degree to which voters and lobby groups hold governors accountable is conditional on federal tax policy. If the federal tax is relatively low, reputation building appears more accentuated. One reason may be that lame ducks face less resistance to tax hikes from the state legislature and other interests with sway over cigarette taxes when the federal tax is relatively low. On the other hand, if high federal taxes are in place, lame duck governors may be pressured not to raise (and even to lower) the state tax, as agricultural tobacco special interests continue to lobby to a greater extent when the federal tax takes more of a bite. Moreover, revenues, tax welfare losses, and the marginal value of public goods may play roles (Besley and Rosen 1998; Keen 1998).

Robustness Analysis

Tables 3 and 4 offer robustness analysis (no controls reported; available upon request). The three panels in table 3 present results using the middle-case cutoffs for the classifications as SMOKER STATE (10 states), TOBAC STATE (13 states), and MANUF STATE (13 states), respectively (remaining cases available upon request). In model I in table 3, both NEIGHBORTAX and STATETAXt −1 are dropped from the model, and in models II and III only one of these controls is included, respectively. Models I–III are included for completeness and serve to illustrate the roles of NEIGHBORTAX and STATETAXt −1. In all remaining models, NEIGHBORTAX and STATETAXt −1 are included. In model IV, FEDTAX is instrumented by the federal deficit as a percentage of national GDP and national unemployment, following Besley and Rosen (1998) and Devereux, Lockwood, and Redoano (2007). The state and federal cigarette tax rates may simultaneously be affected by some common factor that might motivate federal and state governments to act simultaneously. For example, new information may become available on the adverse health effects of smoking. Moreover, the federal government may also be influenced by state governments’ tax changes.

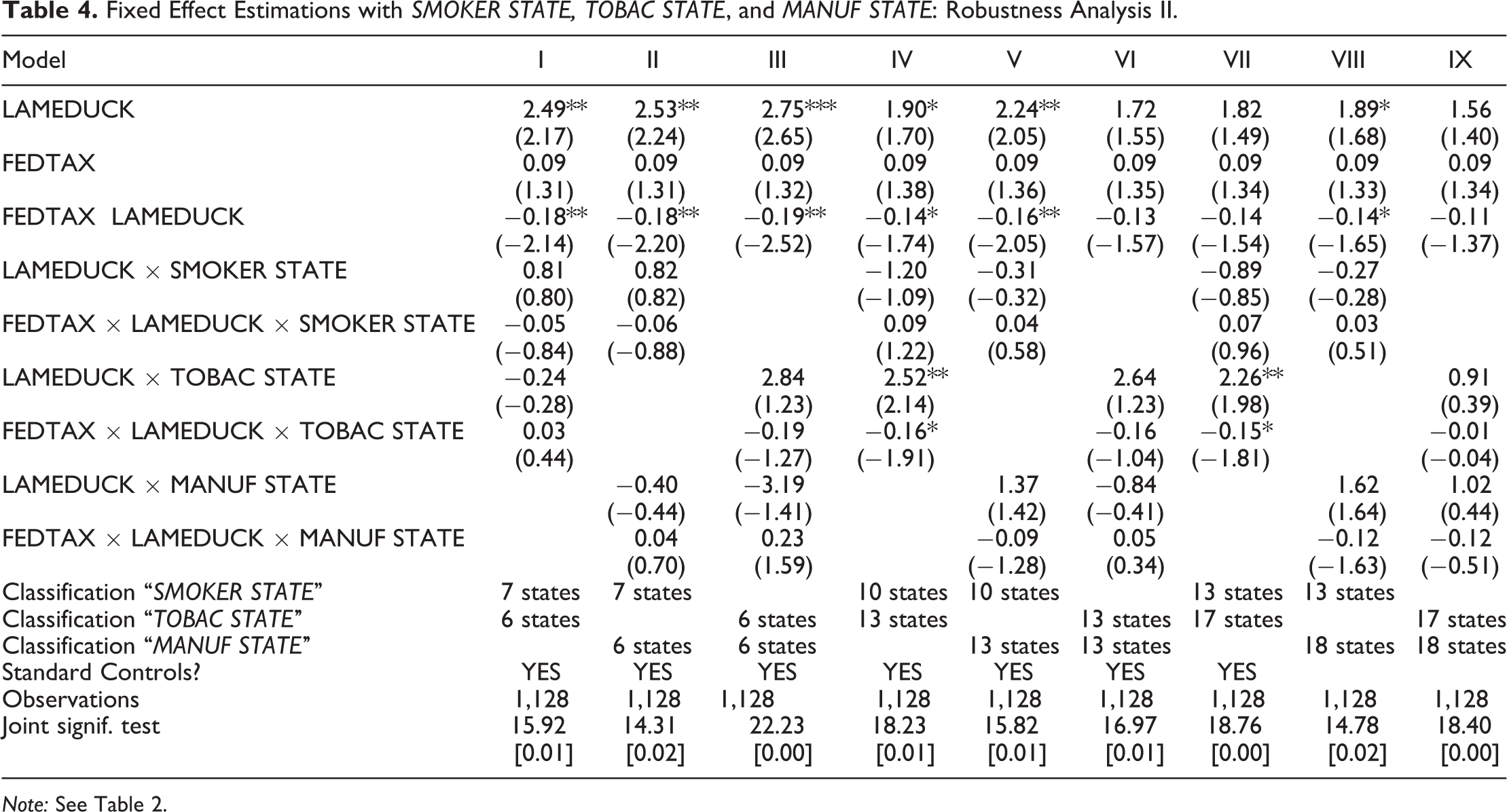

In model V, LAMEDUCK is allowed to affect STATETAX with a one-year lag. A lag may occur between the passing of tax legislation and the time at which it takes effect (Poterba 1994; Reed 2006). Model VI includes only states without any changes in the term limit legislation, as such changes may be simultaneously determined (Besley and Case 1995). Model VII includes only states having term-limit legislation at some point during the sample period (see List and Sturm 2006). This forces us to drop 11 states. Model VIII includes BEERTAX from the World Tax Data Base (2006); it adjusts for another sin tax. Model IX includes DEFICIT −1, which is the lagged (one year) state budget deficit as a percentage of real GSP. Model X uses nominal tax rates only. In model XI, we follow Esteller-Moré and Rizzo (2011) by deflating state and federal cigarette taxes and other financial variables by the house price index (HPI) computed by the Office of the Federal Housing Finance Agency (see http://www.fhfa.gov). This enables us to include time fixed effects in model XII. Table 4 provides a fixed-effects analysis using several different combinations of the state classifications used in table 2, using various cutoff levels. See the table notes for further details.

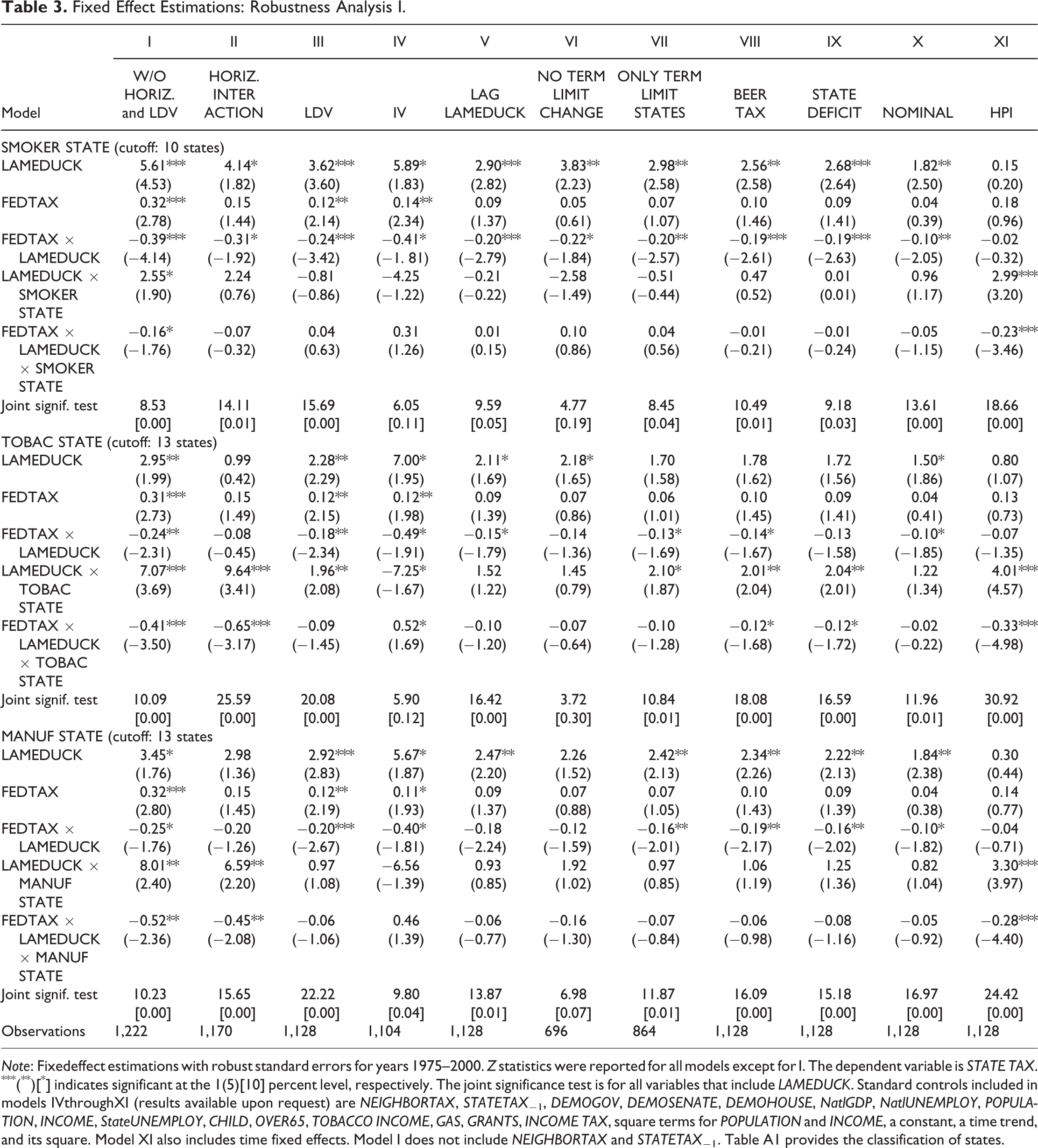

Fixed Effect Estimations: Robustness Analysis I.

Note: Fixedeffect estimations with robust standard errors for years 1975–2000. Z statistics were reported for all models except for I. The dependent variable is STATE TAX. ***(**)[*] indicates significant at the 1(5)[10] percent level, respectively. The joint significance test is for all variables that include LAMEDUCK. Standard controls included in models IVthroughXI (results available upon request) are NEIGHBORTAX, STATETAX −1, DEMOGOV, DEMOSENATE, DEMOHOUSE, NatlGDP, NatlUNEMPLOY, POPULATION, INCOME, StateUNEMPLOY, CHILD, OVER65, TOBACCO INCOME, GAS, GRANTS, INCOME TAX, square terms for POPULATION and INCOME, a constant, a time trend, and its square. Model XI also includes time fixed effects. Model I does not include NEIGHBORTAX and STATETAX −1. Table A1 provides the classification of states.

Results of Robustness Analysis

The results reported in the three panels in table 3 show a reasonable degree of robustness, in our view. LAMEDUCK and FEDTAX × LAMEDUCK are positive and significant in twenty-three and twenty-four out of the thirty-three models, respectively. Among the three state-classification variables, the two interactions with TOBAC STATE are significant (with consistent signs) most frequently (fourteen out of twenty-two coefficients). While the SMOKER STATE interactions are rarely significant, the MANUF STATE interactions are significant in six models. Models I through III in table 3 reveal the importance of simultaneously controlling for horizontal interactions and a lagged-dependent variable. 16 The IV estimations in model IV suggest that reputation building using state cigarette taxation is particularly prevalent in states with agricultural tobacco industry (TOBAC STATE states), and again that lame duck behavior is conditional on FEDTAX. Model IV suggests that in TOBAC STATE states, a lame duck raises STATETAX by 0.17 cents at the mean of FEDTAX. However, at 1 SD above (below) the mean of FEDTAX, STATETAX rises by 0.25 cents (0.1 cents) when a lame duck is in office. This result is consistent with earlier results in table 2; a relatively low FEDTAX facilitates lame ducks’ tax hikes.

Models V through XI confirm the picture that governors engage in reputation building, conditional on FEDTAX. The influence of special interests again appears particularly strong in the TOBAC STATE states. We note that model XI (which uses time fixed effects) produces insignificant LAMEDUCK and FEDTAX × LAMEDUCK coefficients, while the interactions of these variables with the three special interest indicators are consistently significant in the three panels. For example, model XI suggests that at the mean of FEDTAX, a lame duck governor reduces STATETAX by 0.59 cents in a TOBAC STATE (using only significant coefficients). However, at 1 SD below (above) the mean of FEDTAX, a lame duck raises (reduces) STATETAX by 0.38 (1.40) cents. One possible reason for the insignificant LAMEDUCK and FEDTAX × LAMEDUCK coefficients is that the HPI may not differ significantly from the CPI during our sample period. If the time fixed effects pick up most of the common variation in the HPI, the remaining variation in the real state tax may be close to zero in many states (see Esteller-Moré and Rizzo 2011). Our results indicate that this may be the case particularly where no tobacco-related special interest groups are active.

Turning now to table 4 (no controls reported; available upon request), the insights gained from the earlier estimations remain largely intact. These models suggest that reputation building occurs conditional on FEDTAX and is particularly intense in states earning a TOBAC STATE classification. 17 Again, lame duck behavior is consistently conditional on FEDTAX. For example, model IV implies that (at the mean of FEDTAX) a lame duck in a TOBAC STATE raises STATETAX by 0.24 cents, while at 1 SD below the mean the same lame duck hikes STATETAX by 0.97 cents.

Fixed Effect Estimations with SMOKER STATE, TOBAC STATE, and MANUF STATE: Robustness Analysis II.

Note: See Table 2.

Conclusion

This article provides evidence consistent with the hypothesis that state governors engage in reputation-building strategies in the area of cigarette taxation. As they gain lame duck status, governors tend to raise the cigarette tax rate. This strategy appears focused on winning the approval of agricultural tobacco producer lobby groups. Cigarette manufacturing lobby groups and smoking voters do not appear to strongly affect governors’ reputation-building strategies.

Moreover, the reputation building appears conditional on the federal cigarette tax. In particular, lame duck governors raise the state cigarette tax by a greater amount when the federal cigarette tax rate is relatively low and may even lower this state tax rate when the federal tax rate is relatively high.

Footnotes

Appendix

Cutoff Values for the Classification as SMOKER STATE, TOBAC STATE, and MANUF STATE

| SMOKER STATE | ||

|---|---|---|

| Smokers’ share of population | Number of states | States |

| 26.36% | 7 states | IN, KY, MO, NV, OH, TN, WV |

| 26% or greater | 10 states | AR, IN, KY, MI, MO, NV, NC, OH, TN, WV |

| 25% or greater | 13 states | AR, DE, IN, KY, MI, MO, NV, NC, OH, OK, SC, TN, WV |

| TOBAC STATE | ||

| Agric. tobacco prod. in Pounds/real GSP | Number of states | States |

| 500 lbs/RGSP ($Mn) | 6 states | GA, KY, NC, SC, TN, VA |

| 50lbs/RGSP ($Mn) | 13 states | FL, GA, IN, KY, MD, NC, OH, PA, SC, TN, VA, WV, WI |

| >0lbs/RGSP ($Mn) | 17 states | AL, CT, FL, GA, IN, KY, MD, MA, MO, NC, OH, PA, SC, TN, VA, WV, WI |

| MANUF STATE | ||

| Share of tobacco manuf. in real GSP | Number of states | States |

| 0.1% of RGSP | 6 states | GA, KY, NY, NC, TN, VA |

| 0.01% of RGSP | 13 states | AL, CT, FL, GA, IL, KY, NY, NC, PA, SC, TN, VA, WV |

| >0% of RGSP | 18 states | AL, CA, CT, FL, GA, IL, IN, KY, MO, NJ, NY, NC, PA, SC, TN, TX, VA, WV |

Note: RGSP = Real gross state product.

Acknowledgments

We would like to thank the helpful referees, Jim Alm, Rohan Christie-David, Paul Coomes, Elbert Dijkgraaf, Mark Frank, Don Freeman, Steve Gohmann, Darren Grant, Angeliki Kourelis, Niclas Hanes, Hiranya Nath, Eik Swee, Wally Thurman, Mark Tuttle, Pierre Vilain, and participants at presentations at Sam Houston State University, the University of Louisville, the Canadian Economics Association Meetings in Toronto, the NARSC Meetings in Brooklyn, New York, and the Southern Economic Association Meetings in Washington, D.C., for helpful comments and suggestions at various stages of this research program. Tim Besley, Alejandro Esteller-Moré, Leonzio Rizzo, and Daniel Sturm kindly provided various aspects of the data, and Lakeisha Mabry and Michael Weis performed valuable research assistance. The usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.