Abstract

Managing the increasing number and complexity of customer-initiated interactions across multiple channels consistently and effectively has become a key priority for marketing academics and practitioners. To achieve this, it is imperative that marketers understand how and why customers choose the available channels. In this study, we distinguish between two types of interactions, purchases and communications, and argue that the nature of these interactions influences the way customers behave in the presence of multiple channels. Drawing upon perceived risk research, this study develops an integrated conceptual framework that provides a theoretical understanding of customer channel choice for these interactions. The framework is tested empirically in financial services and the results reveal that channel choices significantly differ for purchases and communications. Channel choices for purchases are more inertial and more strongly affected by attitudes (i.e., relationship quality) than for communications. At the same time, preference for a personal touch in channel choice is more pronounced for purchases than for communications, and marketing activities are more effective at driving channel choice for communications. These results offer some recommendations for managing interactions across channels more effectively. For example, the use of personal channels is advised for managing high-risk interactions (i.e., purchases), while for low-risk interactions (i.e., communications), firms can use marketing activities to migrate customers to cheaper channels.

Keywords

Introduction

In an informal poll at the Customer Relationship Management Conference in Chicago, over 65% of loyalty leaders admitted they felt unable to deliver a consistent cross-channel experience to their members. Most organizations cite the complexity of managing customer interactions across expanding numbers of channels.

With the proliferation of marketing channels (e.g., the Internet, social media, call centers, physical stores, catalogs), customers increasingly use alternative channels to make purchases of products and services (Neslin and Shankar 2009), which we refer to as purchase behaviors (PBs). Notably, at the same time, customers have begun to use these channels to contact the firm for purposes other than purchases, including requesting information, soliciting technical advice, facilitating feedback about the products and services, and inquiring about a product’s use or availability (Neslin et al. 2006). According to a report by Econsultancy (2012), nearly 90% of customers make use of various channels to communicate with the firm. These interactions, which we refer to as customer-initiated communications (CICs), are conceptualized as “any communication with a manufacturer that is initiated by a customer” (Bowman and Narayandas 2001, p. 281). Because companies increasingly view each single touch point with the customer as a critical element that shapes the development of the relationship, it is not surprising that around 90% of firms openly manifest their desire to manage interactions across channels effectively (Econsultancy 2013). Yet, as the introductory quotation illustrates, they struggle to deliver consistent and coherent experiences to their customers, due in part to an inadequate understanding of cross-channel behavior. Thus, firms today face a new critical challenge: Managing an increasing number of customer-initiated interactions across multiple marketing channels consistently and effectively.

Resolving this challenge is also a key priority for service research. Ostrom et al. (2015) identify the management of customer relationships across touch points and channels as the third most important priority for service research in the coming years (in a list of 80 themes). Van Bruggen et al. (2010) also note the importance of understanding how to manage the customer experience throughout the purchase process satisfactorily, given the current proliferation of marketing channels (channel multiplicity). However, while research on channel choice and usage is abundant and has provided valuable insights into how customers behave across multiple marketing channels (Ackermann and von Wangenheim 2014; Ansari, Mela, and Neslin 2008; Bilgicer et al. 2015; Thomas and Sullivan 2005; Valentini, Montaguti, and Neslin 2011), the study of customer channel choice across different touch points (e.g., types of interactions—PBs and CICs) has received limited attention (Baxendale, Macdonalda, and Wilson 2015). This lack of research is noteworthy, given the different performance implications of these behaviors and the importance of managing them effectively and profitably across the available channels (Neslin et al. 2006).

Only a few studies have started to look at the differences in channel choices across types of interactions. Conceptually, Balasubramanian, Raghunathan, and Mahajan (2005) offer a theoretical framework to understand how customers behave across channels in different stages of the buying process: consideration set, product choice, and product purchase. Valentini, Montaguti, and Neslin (2011) distinguish between a trial phase and a posttrial phase and empirically investigate how marketing, experience, and channel preferences differently affect the way customers use the available channels. Gensler, Verhoef, and Böhm (2012) distinguish between search, purchase, and after-sales stages of the buying process and study how channel attributes and experience differentially affect channel choices. Our study complements prior findings on how customers choose among multiple marketing channels for different types of interactions by distinguishing between transactional (i.e., purchases, with an immediate impact on the bottom line) and nontransactional interactions (i.e., communications, with a deferred impact on profits). In addition, compared with previous studies that consider a subset of drivers of channel choice and use information on stated preferences and intentions, our work contributes to existing knowledge by simultaneously considering the different roles of marketing activities, customer attitudes, channel preferences, experience and channel spillover and by studying actual channel choices.

Drawing upon perceived risk research (Dowling and Staelin 1994), we develop a conceptual framework to understand the differences in channel choices between PBs and CICs that we validate in a service context. In doing so, this study contributes to existing knowledge in at least three ways. First, with the increasing number and complexity of interactions that occur over time in ongoing customer-firm relationships, we present a broader categorization of these interactions that distinguishes between PBs and CICs, depending on their temporal effects on performance (immediate vs. deferred). Second, we offer an integrative conceptual framework for the drivers of channel choice and provide a theoretical understanding of the differences in channel choice for PBs and CICs. This understanding is necessary, given the complex behavioral patterns that have emerged in the current “omni-channel” environment and the need to identify what drives “customers’ choice for touchpoints and channels” (Verhoef, Kannan, and Inman 2015, p. 6). Third, we provide an empirical test of our framework in financial services and demonstrate that channel choice differs significantly depending on the type of interaction (CICs vs. PBs). Specifically, we find that customers, when making purchases, have stronger preferences for off-line channels, are less influenced by marketing activities, are more affected by their attitudes toward the firm (i.e., relationship quality), and their channel choices are more inertial than for communicating with the firm. These findings call for the development of interrelated, but differentiated, channel strategies for PBs and CICs to provide customers with a consistent and seamless experience across the available channels.

Conceptual Framework

In this study, we propose a conceptual framework to manage different types of customer-initiated interactions across marketing channels differentially and effectively. To do so, we distinguish between two types of interactions: PBs and CICs. PBs refer to behaviors that involve the exchange of products and services and they include, for example, making purchases, cross-buying additional products and services, modifying the level of service usage, and upgrading to a superior offering. CICs are conceptualized as any communication with the company initiated by the customer. Examples include requesting and searching for information, soliciting technical advice, and facilitating feedback about the products and services. The distinction between PBs and CICs is different from other distinctions such as search versus purchase (Gensler, Verhoef, and Böhm 2012) because these refer to the purchase process of a specific product or situation, while our conceptualization is valid for a wide variety of behaviors and interactions that occur in an ongoing customer-firm relationship. This distinction is relevant from both an academic and a managerial perspective. Academically, it complements prior findings on the differences in customer channel choices across different stages of the purchase process (Balasubramanian, Raghunathan, and Mahajan 2005; Gensler, Verhoef, and Böhm 2012; Valentini, Montaguti, and Neslin 2011). From a managerial standpoint, the distinction between PBs and CICs with their differential impact on short- and long-term performance offers marketers an actionable approach to manage customer touch points across multiple channels differentially, effectively, and profitably.

In this section, we propose a conceptual framework that describes and analyzes how and why customers decide which channels they choose to interact with the firm for PBs and CICs (Figure 1). This research builds upon the main thesis that different types of interactions entail different motivational forces and psychological mechanisms and, thus, will lead to differences in the way customers behave in the presence of multiple marketing channels.

Conceptual framework: Channel choice for PBs and CICs. PBs = purchase behaviors; CICs = customer-initiated communications.

To offer a theoretical understanding of the differences in channel choice for PBs and CICs, we draw upon perceived risk research and argue that the nature of the interactions between the parties influences the amount of perceived risk (Cox and Rich 1964). As indicated by prior research, other factors such as convenience, accessibility, and enjoyment can also be important to understand customer channel choices (Dholakia et al. 2010). However, we argue that these factors will mainly determine customer channel preferences (we include them explicitly in our model, as we note below) and, thus, will affect channel usage irrespective of the nature of the interactions. In the presence of different types of interactions with the firm, perceived risk will be a central aspect to understand customer channel choices (Herhausen et al. 2015). Perceived risk is defined in terms of the uncertainty and adverse consequences that are associated with a behavior or course of action (Dowling and Staelin 1994), and it is frequently considered as one of the most crucial factors explaining consumer behavior (Bettman 1973). We argue that PBs and CICs entail different levels of risk perception. As suggested by perceived risk research, certain properties of any given situation, such as its complexity, level of involvement, and the importance attached to it (Dholakia 2001), determine the level of perceived risk. A purchase situation is usually perceived as complex, important, and with a strong personal meaning and involvement (Dowling and Staelin 1994). This leads customers to attach great value to achieving purchase goals and, as a result, to perceive high levels of uncertainty about potential adverse and unpleasant consequences. In contrast, communications, although not risk-free situations, entail less risk, given their lower complexity and level of involvement. Jacoby and Kaplan (1972) identify five different risk dimensions, including financial and performance risk, which are likely to be high for PBs but absent for CICs. As a result, we conclude that the nature of the interactions influences the amount of perceived risk in such a way that purchases (PBs) will entail a higher risk than communications (CICs).

These differences in perceived risk between PBs and CICs are important because different levels of perceived risk have been shown to activate different goals in consumer behavior. Hamilton and Biehal (2005) show that when perceived risk is high prevention goals are more salient and customers pay more attention to potential losses, but when perceived risk is low promotion goals are more salient and customers direct their attention toward potential gains. These differences in goals between PBs and CICs will result in differences in consumer decision-making. Specifically, customers pursuing prevention goals (high-risk condition: PBs) will focus on minimizing losses and negative outcomes, striving for security and safety, while customers pursuing promotion goals (low-risk condition: CICs) will focus on maximizing gains and positive outcomes, striving for growth and advancement (Gürhan-Canli and Batra 2004; Higgins 1997).

Building on the previous arguments, this research posits that, due to differences in perceived risk, the nature of the interactions (PBs vs. CICs) will influence consumers’ sensitivity to gains and losses in making choice decisions about marketing channels. For PBs, customers will be more sensitive to potential losses and, for CICs, they will be more sensitive to potential gains (Chernev 2004). Below, we discuss the implications of these differences in the sensitivity to gains and losses between PBs and CICs for channel choice and derive our research hypotheses.

Research Hypotheses

The aim of this section is to identify relevant factors that explain customer channel choice and provide a theoretical understanding of their (different) impact on choice for PBs and CICs. A customer’s choice decision depends on the perceived costs and benefits associated with each option considered (Gatignon and Robertson 1986). In a multichannel context, the options are the marketing channels available or any combination of them. According to Wendel and Dellaert (2005), different channels provide different perceived benefits and costs. The benefits are advantages that the customer enjoys from using a specific combination of channels to interact with the firm (e.g., convenience, bidirectional communication, familiarity, efficiency), while the costs refer to the sacrifices or lost opportunities, which the customer must incur from using that combination (e.g., time consumption, monetary investments, waiting time). When deciding how to choose among the available channels, a customer compares the benefits and costs of alternative combinations.

We build on prior research and identify five categories of relevant factors that can contribute to explaining the customer’s anticipation of gains and losses associated with the use of alternative channels (Neslin et al. 2006): (1) channel preferences, (2) prior experience, (3) marketing activities, (4) customer attitudes, and (5) channel spillover. These variables are theoretically grounded and can offer meaningful and actionable managerial insights for managing customer-initiated interactions across channels. While we believe that the set of factors that prior research has identified is central to the understanding of customer channel choice irrespective of the nature of the interactions (PBs and CICs), we expect that the nature of the interactions can indeed affect the direction and strength of the associations between these antecedents and channel choice.

Channel Preferences

Customers tend to have a natural preference for some channels to interact with the firm due to factors such as convenience, enjoyment, and accessibility, among others (Dholakia et al. 2010; Montoya-Weiss, Voss, and Grewal 2003). However, we argue that these preferences (or their strength) can differ depending on the type of interaction. As noted, when perceived risk is high (PBs), customers focus on minimizing losses. Avery et al. (2012) conclude that a number of capabilities of off-line channels (e.g., the physical store), including the opportunity to touch the merchandise, to talk to salespeople face-to-face and to get advice, help customers to reduce the risk of their channel choices and, thus, minimize the potential loss from this decision. In contrast, when perceived risk is low (CICs), customers focus on maximizing gains. Online channels, such as the Internet, by not having geographic or time restrictions, offer a higher degree of accessibility, convenience, and flexibility (Dholakia et al. 2010), helping customers increase the gains derived from their channel choices. These benefits, however, are frequently accompanied by higher potential losses, such as those related to privacy concerns, potential delays in the responses to the interactions or in the delivery of the merchandise, and lack of personal assistance to solve problems or conflictive situations. These costs typically discourage customers who are very sensitive to potential losses. Therefore, compared with CICs, for PBs we expect customers to have a stronger preference for channels that help them reduce the losses in decision-making (e.g., off-line channels) and a weaker preference for channels that help them increase the gains (e.g., online channels).

Prior Experience

Previous research has shown that having experience with a particular channel increases the likelihood of choosing that channel in the future (Ansari, Mela, and Neslin 2008; Melis et al. 2015). However, we argue that the extent to which prior experience determines current channel choices depends on the type of interaction (CICs vs. PBs). Individuals tend to disproportionately prefer the current state of affairs over situations that imply change (i.e., status quo bias; Samuelson and Zeckhauser 1988). This phenomenon is attributed to loss aversion, a psychological principle under which losses tend to be exaggerated relative to corresponding gains (Kahneman and Tversky 1979). The status quo bias, however, has been shown to be more pronounced for customers who focus on minimizing negative outcomes (prevention oriented) and less pronounced for those who focus on maximizing gains (promotion oriented; Chernev 2004). In support of this thesis, Campbell and Goodstein (2001) show that, when goals are associated with higher perceived risk, customers become more conservative and have a preference for the norm (familiar options) over the novel, and Erdem (1998) demonstrates that, when customers perceive a high risk, they are more likely to choose a known brand than an unknown one. However, when perceived risk is low, these studies reveal that customers enjoy the “positive stimulation” provided by novel situations (Campbell and Goodstein 2001, p. 440). Applying this reasoning to our multichannel context, we expect customers to show a stronger (weaker) tendency to choose the same channels that they have used previously for PBs (CICs), given their higher (lower) risk.

Marketing Activities

Prior research has demonstrated that the use of marketing activities influences channel choice (Li and Kannan 2014; Thomas and Sullivan 2005; Valentini, Montaguti, and Neslin 2011). In addition to other factors such as the content and type of the marketing intervention, we sustain that the extent to which marketing activities influence channel choices is contingent upon the type of interactions (PBs vs. CICs). Typically, marketing activities aim to “favorably impress” customers by emphasizing benefits and advantages (Wulf, Odekerken-Schröder, and Iacobucci 2001, p. 35). That is, these activities focus on the gains that will accrue to the customer and on growth and development. Thus, customers facing low-risk situations (e.g., CICs), by focusing on maximizing gains, will be expected to respond favorably to these marketing activities. In contrast, customers facing risky choices (e.g., PBs) tend to develop a greater confidence in their own ability to judge and evaluate choices (Dowling and Staelin 1994), and are less influenced by information that is provided by external sources. Therefore, these customers will respond less favorably to marketing activities. For example, all else being equal, if a customer receives an incentive to use a channel, she will probably be more willing to initiate a communication (which is less risky) rather than the direct purchase of a product (for which she may want to evaluate other sources and types of information).

Customer Attitudes (Relationship Quality)

In the presence of multiple channels, perceptions and attitudes toward the firm have been identified as important drivers of channel choice. In this study, we consider relationship quality, “an overall assessment of the strength of a relationship” between the customer and the service provider (Wulf, Odekerken-Schröder, and Iacobucci 2001, p. 36). We expect the extent to which relationship quality drives channel choices to vary between PBs and CICs. When confronted with decision processes, customers are known to frequently resort to simplifying heuristics (Tversky and Kahneman 1974). Attitudes, “high-order mental constructs [that] summarize consumers’ knowledge and experience with a particular firm” (Garbarino and Johnson 1999, p. 71), constitute an important heuristic (Lane and Jacobson 1995). They organize an individual’s knowledge, beliefs, and experiences about the relationship with the firm, helping customers simplify decision-making and process, organize, and respond to information stimuli more rapidly and efficiently. However, the extent to which relationship quality is used as a simplifying rule depends on the complexity and uncertainty of the decision process. As noted by Tversky and Kahneman (1974), heuristics are frequently resorted to when uncertainty or the chances of greater negative consequences are high (i.e., high-risk situations). Consistent with this reasoning, Sheth and Parvatiyar (1995) note that attitudes constitute a good risk reducer and that customers satisfied with prior experiences are less motivated to search for additional information to make further decisions. In addition, relationship marketing research has shown that, in strong relationships, customers are willing to engage in risk-taking behaviors (Dwyer, Shurr, and Oh 1987; Morgan and Hunt 1994). High-quality relationships provide a buffer against any potential loss or adverse consequence of an action, and, thus, customers become more willing to invest in the relationship and assume risk. Therefore, in our multichannel context, we expect customers to be more influenced by relationship quality in their channel choices when they perceive a higher risk (PBs) in such a way that their positive or negative accumulated experiences will be more easily recalled and more influential in subsequent decisions than when the perceived risk is lower (CICs).

Channel Spillover

Independent of the effects of the four categories of drivers discussed above, customer channel choices for PBs and CICs may also be influenced by channel spillover effects or the influence that channel choices for one particular type of interaction (e.g., PBs) may have on channel choices for the other type of interaction (e.g., CICs; Gensler, Verhoef, and Böhm 2012). Although we do not provide a formal hypothesis for these effects, we expect that choosing a channel in one type of interaction (e.g., PBs) will increase the likelihood of choosing the same channel in the other type of interaction (e.g., CICs).

Research Methodology

In this section, we develop a modeling strategy to empirically test the proposed conceptual framework and its associated hypotheses. We first indicate how we conceptualize customer channel behavior. Then, we present our modeling approach.

Customer Channel Behavior

To understand the way in which customers choose among the available channels and the drivers of their choices for PBs and CICs, we first conceptualize customer channel behavior. Prior research frequently uses a discrete and/or static perspective toward channel choices: Customers are operationalized as either single channel (use of one channel) or multichannel (use of more than one channel) at a specific point in time. In contexts in which there are multiple channels and interactions are frequent (e.g., services), it is important to consider the specific mix of channels that customers choose, instead of simply grouping individuals into single versus multichannel. For example, Internet-only and catalog-only customers would be grouped together as single-channel users, and customers using any mix of two (or more) channels (e.g., the catalog and the Internet, the call center and the physical store) would be treated as multichannel customers. However, the factors that explain why customers use different channels and their performance implications vary significantly across channels. This approach also prevents an understanding of the intensity with which each channel is used. For example, imagine two customers, Sophie and John, who contact the firm 6 times in a given month. Sophie approaches the firm 5 times through the physical store and once through the Internet. John approaches the firm using the Internet 4 times and the physical store twice. Using an aggregated and discrete approach, Sophie and John would be treated similarly (they would be considered as multichannel customers because both use the two channels). However, the degree to which the channels are used is different: Sophie uses the physical store more intensely (83%) than the Internet (16%), but John uses the digital channel more than the physical store (66% vs. 33%, respectively). In addition, the use of a static approach implies looking at cross-sectional, ex post measures of channel choices at the end of the observation period. However, the changing nature of customer channel choices recommends using measures that vary over time to explicitly consider its dynamics (Valentini, Montaguti, and Neslin 2011). In this research, we provide a continuous and dynamic conceptualization of customer channel behavior. We capture its continuous nature by identifying the position of the customer on a continuum of single to multichannel. We capture its dynamic nature by identifying changes in customer channel usage over time.

Modeling Approach

Customer channel choices are a combination of two processes: (1) the arrival of (purchase and communication) needs to interact with the firm and (2) the choice of channel for fulfilling those particular needs. Thus, we first identify the process by which customers arrive at the needs to interact with the firm: model for the arrival of the purchase (PBs) and communication (CICs) needs. Then, we derive a model to understand channel choice: model for the drivers of channel choice.

Model for the arrival of the purchase and communication needs

In this model, we investigate the process by which customers arrive at the needs to interact with the firm, either to make a purchase (PBs) or to make a communication (CICs). It is important to model this process first because individuals may differ substantially with respect to their motivations to interact with the firm, and these differences may translate ultimately into differences in channel choices.

Let PB jit and CIC jit be the number of purchases and communications of type j (for a total of J types, where J = 3 for PBs and J = 2 for CICs) initiated by customer i in time t. To identify the factors that motivate customers to interact with the firm, we specify a linear regression model as follows:

Model for the drivers of channel choice

To investigate the drivers of channel choice, we develop a modeling approach in which channel choice is explained by the five categories of variables identified in the conceptual framework. Given the discrete approach used in past research to understand channel choices on a given purchase occasion (mutually exclusive options), studies have frequently used multinomial logit, probit, or hazard models. However, the continuous and dynamic approach that we propose for the study of channel choice implies that channels are not mutually exclusive options. Rather, customers decide how to distribute the interactions across the available channels. This is in line with Gensler, Verhoef, and Böhm (2012) who explicitly consider the different propensities of customers to use different channels. As a result, in our study, the dependent variable is the time-varying, customer-specific channel shares (CSHikt): the percentage of all interactions that customer i allocates to each channel k (for K total channels) in period t, or

When dealing with fractional response variables, traditional linear regression models are inappropriate and would produce inconsistent estimates, as they fail to account for important nonlinearities in the effect of the independent variables. To produce consistent estimates with satisfactory efficiency properties, Papke and Wooldridge (1996) propose estimating a fractional response model using the quasi-maximum likelihood estimation (QMLE) method.

Formally, let CSHikt be channel k’s share for customer i in period t, where K is the total number of channels (K = 3). By definition, this variable is bounded between 0 and 1 (0 < CSHikt < 1). We consider the following model for the conditional expectation of the fractional response variable:

To derive the parameter vectors (γ and δ), we maximize the Bernoulli log-likelihood function where individual i’s contribution is given by Equation 3 as follows:

Papke and Wooldridge (1996) show that using the QMLE approach to obtain the coefficients gives consistent and asymptotically normal estimates. We estimate the two models (PBs and CICs) using fmlogit in Stata (Buis 2008).

Estimation procedure

As noted previously, customer channel choices are a combination of two sequential processes (i.e., arrival of needs and channel choice). To estimate the two models, we proceed recursively using a two-stage approach. In the first stage, the potential endogenous variables (i.e., number of interactions, PB jit and CIC jit) are modeled as a function of some pertinent covariates (Equation 1) and estimated using a linear regression approach. From this model, we derive the predicted values for the number of customer-initiated interactions (for the different types of PBs and CICs) and introduce them as explanatory variables into the second model (

Data

We empirically test the conceptual framework and its associated hypotheses in financial services. The data come from a major bank in a European country. This bank sells financial services in different categories (e.g., certificates of deposit, savings accounts, mortgages) to individual customers. In financial services, and for the bank studied, there are three main channels that customers can use to interact with the firm: the branch, the ATM, and the Internet. These three channels receive more than 95% of the total number of interactions. Other channels, such as the mobile phone, were only recently introduced by the bank at the time of the data collection and marginally used by customers. In this study, we focus on the three previously mentioned channels to conduct our analyses. While these three channels have been designed to offer customers the possibility of performing a wide variety of operations and activities, they do not support the same number and types of interactions. For example, there are interactions that are restricted to specific channels, such as the withdrawal of money (i.e., enabled by the branch and the ATM but not the Internet) or the subscription of mortgages (supported by the branch but not by the ATM or the Internet). Specifically, in the studied bank, there are a total of 514 possible operations, of which around 40% (more than 200 operations) can be performed using the three channels studied (this percentage increases if we consider only the operations that are more commonly performed by customers). Despite the high degree of overlap between the channels in the interactions they enable, our econometric model also controls for the possibility that channel choices are influenced by restrictions in the types of operations supported by each channel, as we have noted in the previous section.

The data requirements for our study are significant, as we need to combine different types of PBs and CICs, longitudinal and cross-sectional data, and objective and subjective information and merge them into a single data set. We proceeded as follows. First, the collaborating bank obtained a representative sample of 3,723 customers from the entire customer base. The sample was then restricted to (1) customers who showed some activity with the bank during the study period and (2) customers who made at least three PBs and three CICs during the study period (irrespective of the channels used to contact the firm), resulting in an effective sample size of 2,244 customers. For each of these customers, we had access to longitudinal (monthly) information from January 2008 to May 2009, which enabled us to identify the total number of interactions (a total of 498,459 interactions), their nature (grouped into five types of contacts: (1) purchases and subscriptions of products and services, (2) cancelations, (3) other economic operations, (4) information requests, and (5) service-related operations) as well as the specific channels used to contact the bank. Based on the indications provided by the bank’s managers, we categorized an interaction as a PB if it involved the purchase of products or services, cross-buying additional products and services, modifying the level of service usage, or upgrading to superior offerings (Types 1, 2, and 3 described before). Examples include subscribing to a product or service, getting money from the account, making a bank transfer, and ordering a tax payment. We categorized an interaction as a CIC when it involved any communication with the bank that is initiated by the customer (Types 4 and 5 described before). Examples include contacting the bank to modify personal information, checking the status of accounts, checking the status of credit or debit cards, and requesting information about movements in accounts or cards. In this way, we separated PBs and CICs and created the central variables of our study. Although we group together different types of interactions under PBs and CICs (Bowman and Narayandas 2001), we control empirically for potential differences in channel choices for the identified categories of PBs and CICs by introducing them explicitly into our model. As noted previously, this allows us to control for the fact that some channels may be more suitable than others to perform specific operations.

Second, we had access to longitudinal (monthly) information about the customer transaction history (e.g., crossbuy, relationship tenure). Third, we were also provided with monthly information about the number of direct marketing activities targeted by the bank at the individuals in the sample during the observation window. Fourth, we had access to demographic information for the sample, including gender and age. Fifth, during 2007, a third-party research firm collected cross-sectional information about customer attitudes toward the bank. Specifically, we were provided with information about customer satisfaction and commitment. Following prior research, which conceptualizes relationship quality as a higher order construct consisting of various distinct, although related, dimensions, we collapsed these two factors into a single indicator of the quality of the relationship (Wulf, Odekerken-Schröder, and Iacobucci 2001).

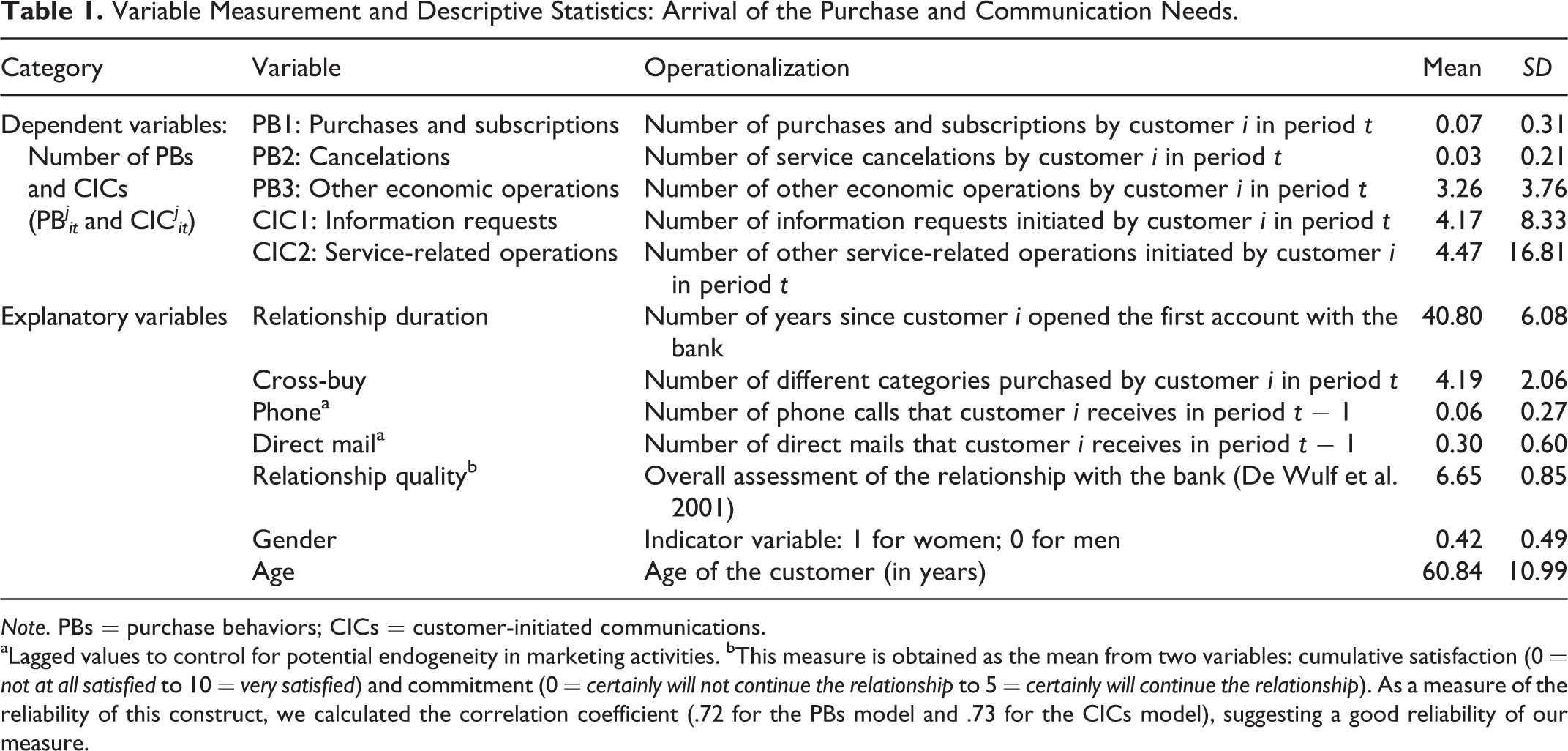

We merged these five data sources and created a unique and comprehensive data set describing customer channel choices over time and containing relevant information for the implementation of the models for the arrival of the purchase and communication needs and for the drivers of channel choice. In Tables 1 and 2, we present a description of the variables that we include in our models and their operationalization and provide a set of selected descriptive statistics (mean and standard deviation).

Variable Measurement and Descriptive Statistics: Arrival of the Purchase and Communication Needs.

Note. PBs = purchase behaviors; CICs = customer-initiated communications.

aLagged values to control for potential endogeneity in marketing activities. bThis measure is obtained as the mean from two variables: cumulative satisfaction (0 = not at all satisfied to 10 = very satisfied) and commitment (0 = certainly will not continue the relationship to 5 = certainly will continue the relationship). As a measure of the reliability of this construct, we calculated the correlation coefficient (.72 for the PBs model and .73 for the CICs model), suggesting a good reliability of our measure.

Variable Measurement and Descriptive Statistics: Drivers of Channel Choice.

Note. PBs = purchase behaviors; CICs = customer-initiated communications; CSH, customer-specific channel shares; ATM = automated teller machine.

aLagged values to control for potential endogeneity in marketing activities. bThis measure is obtained as the mean from two variables: cumulative satisfaction (0 = not at all satisfied to 10 = very satisfied) and commitment (0 = certainly will not continue the relationship to 5 = certainly will continue the relationship). As a measure of the reliability of this construct, we calculated the correlation coefficient (.72 for the PBs model and .73 for the CICs model), suggesting a good reliability of our measure. c Predicted.

Estimation Results

Model for the Arrival of the Purchase and Communication Needs

We report the coefficient estimates for the five models for the arrival of the purchase and communication needs in Table 3. The fit statistics indicate that our models fit better than a null model with no explanatory variables (p < .001). A positive (negative) sign for a coefficient indicates that an increase in the explanatory variable leads to an increase (decrease) in the number of interactions initiated by the customer in that specific type of contact. As Table 3 shows, in general, the results reveal reasonable effects for the variables considered. It is interesting to note the negative and significant effect of relationship quality on the number of information requests and service operations (β = −1.15; β = −.42, respectively), indicating that customers in high-quality relationships initiate a smaller number of interactions to request information or perform service operations. This result offers support to relationship marketing theories, suggesting that strong relationships involve exchange efficiencies and thus require lower resources to be maintained (Dwyer, Shurr, and Oh 1987; Morgan and Hunt 1994). In high-quality relationships, customers have a deeper knowledge about the firm and its products and services and, thus, do not need to contact the firm so frequently. In addition, the results show the positive association between the different types of interactions (bottom of Table 3): An increase in one type of interaction (e.g., subscriptions) leads to increases in other types of interactions (e.g., information requests).

Estimation Results for the Model for the Arrival of the Purchase and Communication Needs.

*p < .1. **p < .05. ***p < .01.

Model for the Drivers of Customer Channel Choice

We report the coefficient estimates for the models about the drivers of channel choice for PBs and CICs in Table 4. In the two models, we set the branch as the reference channel against which the coefficients are compared. For each model, we obtain two sets of parameter estimates: (1) ATM versus branch and (2) Internet banking versus branch. A positive (negative) sign for a coefficient in one of the two sets indicates that an increase in the explanatory variable leads to an increase (decrease) in the focal channel share (ATM in Set 1 and Internet in Set 2) and a decrease (increase) in the branch’s share (reference category). We performed Z tests to test the significance of the differences in coefficients across the two models for PBs and CICs. Unless otherwise stated, in all the reported results, the differences between the parameters are statistically significant.

Fractional Response Model Estimation Results: Drivers of Channel Choice.

Note. PBs = purchase behaviors; CICs = customer-initiated communications; ATM = automated teller machine.

*p < .1. **p < .05. ***p < .01.

The fit statistics appear in Table 4, and they indicate that our models fit better than a null model with no explanatory variables (p < .001). We also implemented a nested modeling strategy by sequentially introducing the five categories of drivers that we study into the models. Adding each set of variables produces a better fit to the data, according to the likelihood ratio test. This provides further support for the relevance of the categories of variables selected to explain customer channel choice. In addition, we evaluated the predictive accuracy of the proposed model against a rival model that investigates the drivers of the absolute number of times each channel is used (instead of our relative measure, channel shares) using the mean absolute percentage error (MAPE), which suggested a better predictive accuracy of our proposed model.

The results indicate that customers have a preference for the branch (i.e., off-line channel) over the Internet (i.e., online channel) to interact with the bank, as is revealed by the negative parameters for the intercepts in the Internet sets, and that this preference is stronger for PBs than for CICs (βPBsInternet = −28.21 vs. βCICsInternet = −13.28, p < .01), lending support to our Hypothesis 1a. The results also indicate that customers have a preference for the branch over the ATM for PBs (βPBsATM = −3.77, p < .01) but not for CICs (βCICsATM = −.32, p > .1), offering additional support to our contention that, for high-risk situations, customers prefer off-line channels. At the same time, these results indicate that, although the Internet is not the preferred channel for PBs and CICs, it reduces customer utility much less for CICs than for PBs (βPBsInternet = −28.21 vs. βCICsInternet = −13.28, p < .01), suggesting a stronger preference for this channel when conducting CICs and supporting Hypothesis 1b.

In our second hypothesis, we argued that customers would be influenced by their prior experience with the channels when making current channel choices but that this effect would be stronger for PBs. In support of our predictions, the results show that having a greater accumulated experience with a channel increases the probability of choosing this channel again in the present and that this effect is stronger for PBs than for CICs (βPBsATM = .07 vs. βCICsATM = .05; βPBsInternet = .08 vs. βCICsInternet = .01, p < .01).

In our framework, we hypothesized that marketing activities would have a stronger impact on channel choice for CICs than for PBs. The results show that all parameters except one (effect of direct mail on the probability of choosing the Internet for CICs) have a negative sign, suggesting that marketing activities mostly drive customers to go to the branch. In line with our prediction, we obtain a higher number of significant parameters for the effect of marketing on channel choice for CICs (all parameters are significant) than for PBs (three out of four are significant), which offers initial support to our hypothesis. However, the differences in the magnitude of the parameters are not statistically significant (phone: βPBsATM = −.16 vs. βCICsATM = −.15; βPBsInternet = −.29 vs. βCICsInternet = −.37; direct mail: βPBsATM = −.25, βCICsATM = −.28). So we can conclude that the effect of marketing is slightly more effective in conditioning channel choice for CICs than for PBs only in terms of the number of significant parameters (four vs. three), lending partial support to Hypothesis 3.

Our fourth hypothesis was concerned with the differential impact of relationship quality on channel choice for PBs and CICs. The results reveal that relationship quality is a significant driver of channel choice, as it increases the likelihood of choosing the ATM and the Internet to contact the firm. With regard to the strength with which relationship quality affects channel choice for PBs and CICs, the results show that the positive effect of relationship quality on the probability of using the Internet (over the branch) is stronger for PBs, as we hypothesized (βPBsInternet = 1.99 vs. βCICsInternet = 1.12, p < .01). Also, relationship quality increases the probability of using the ATM (over the branch) for PBs (βPBsATM = .23, p < .05) but not for CICs (βCICsATM = .09, p > .1). Thus, these results offer support for Hypothesis 4.

For channel spillover, the results indicate that these effects are significant, demonstrating the interdependent nature of channel choices for different types of interactions (PBs and CICs). Specifically, the results suggest that having a greater experience with the ATM for PBs increases the likelihood of choosing this channel for CICs as well (βCICsATM = 0.01, p < 0.1). However, having experience with the ATM for CICs decreases the likelihood of using it for PBs (βPBsATM = −.01, p < .01). While one might have expected a positive influence, this result is in line with our theoretical model in that the familiarity gained with a channel for PBs (high risk) makes the use of this channel more likely for lower risk operations but not the other way around. That is, customers will be more willing to extrapolate their experiences with a channel from higher to lower risk situations but not from low to high risk. These results also show that a higher accumulated experience with the ATM in CICs decreases the likelihood of choosing the Internet for PBs (βPBsInternet = −.01, p < .05) and that experience with the Internet for PBs reduces the likelihood of choosing the ATM for CICs (βCICsATM = −.05, p < .01).

Although they are not the main focus of the present research, the results show that some of the control variables are also important in explaining channel choices. For example, the (predicted) number of interactions initiated by customers in each of the five categories considered influences the channel mix chosen. These results reveal (and help control for) two important issues: (1) not all products are available through all channels and, thus, there are associations between specific types of interactions/operations and channels (e.g., economic operations, including money withdrawal, are mostly performed in the branch—βPBsInternet = −58.33, p < .01, and service subscriptions tend to be performed in the branch—βPBsInternet = −3.52, p < .01) and (2) customers have preferences for specific channels for conducting particular activities or operations (e.g., information requests are mostly performed in the branch –βCICsInternet = −.39, p < .05 and service-related operations over the Internet –βCICsInternet = 3.43, p < .01). Thus, by including these variables, we are controlling for the fact that different channels may fulfill different (purchase and communication) needs and, thus, be more suitable for performing specific operations.

Discussion

Theoretical Implications

Our study contributes to current knowledge on how customers make channel choices for different types of interactions and stages of the purchase process (Balasubramanian, Raghunathan, and Mahajan 2005; Gensler, Verhoef, and Böhm 2012; Valentini, Montaguti, and Neslin 2011). Due to the increasing number and complexity of customer-initiated interactions and their ongoing nature, our study presents a broader categorization that distinguishes between PBs, which comprise all interactions that have an immediate impact on profitability, and CICs, which include all communications with the firm that, while not having an immediate impact on the bottom line, help in building successful relationships. Importantly, given the nature of these interactions (dynamic, continuous), our study also advances a more comprehensive conceptualization of customer channel behavior. While most studies take a discrete and static approach, regarding customers as either single channel or multichannel at a specific moment in time, our study introduces a continuous and dynamic perspective to the study of customer channel choice (i.e., channel shares).

Drawing upon perceived risk research (Dowling and Staelin 1994), our study theoretically proposes and empirically demonstrates that the way customers choose among the available marketing channels differs significantly for PBs, which entail a higher risk, and CICs, which carry less risk. By simultaneously considering a wider set of drivers than previous research (we include channel preferences, prior experience, marketing activities, customer attitudes and spillover effects) and studying actual channel choices instead of choice intentions, our results offer a number of novel insights. While we find a solid preference for the off-line channel for both types of interactions (PBs and CICs), this preference is stronger for PBs. Face-to-face, high-touch interactions, allowing real-time synchronous communication between the customer and the firm, provide richer and more trustworthy information and are a good mechanism to reduce the risk and minimize potential losses (Dholakia, Bagozzi, and Pearo 2004). We also demonstrate that the extent to which accumulated channel experience influences future channel choices depends on the nature of the interactions, the effect being stronger for PBs than for CICs. This result seems to suggest that, when confronted with high-risk situations, and due to loss aversion, customers tend to favor well-known, familiar options over novel ones.

While previous research suggests that marketing influences channel choices (Ansari, Mela, and Neslin 2008; Li and Kannan 2014), our results show that customers are slightly more responsive to these activities in their channel choices for CICs. This may be due to the higher sensitivity of customers to potential gains in low-risk situations, which makes them more easily influenced by marketing activities that emphasize advantages and benefits, while, in high-risk situations (PBs), customers are more rational and calculative, and their judgments and evaluations about channels are less susceptible to marketing investments (Beatty, Kahle, and Homer 1988). However, we only obtained marginal support for this finding, and, thus, more research is required to validate it in this and other contexts. Interestingly, the study findings reveal that customers tend to rely more heavily on attitudes that summarize prior experiences with the firm (e.g., relationship quality) to make channel choices for PBs than for CICs, as attitudes convey important information to help customers reduce their uncertainty when they engage in purchases of products and services. This is in line with relationship marketing theories, which show that, in strong relationships, customers are more willing to invest in the relationship and engage in risk-taking behaviors (Dwyer, Shurr, and Oh 1987; Morgan and Hunt 1994). Furthermore, our results provide support for channel spillover effects, suggesting that channel decisions for different interactions or stages of the buying process are not independent (Gensler, Verhoef, and Böhm 2012).

Managerial Implications

Service research and practice have changed dramatically in the last two decades due to the increase in the number of interaction channels. As more and more customers use this multitude of marketing channels to interact with the firm, it becomes increasingly important to manage these interactions consistently and effectively (Verhoef, Kannan, and Inman 2015). Our framework and findings offer insights into how to achieve this. Because of the different profitability implications across interactions (PBs vs. CICs) and channels (branch vs. ATM vs. Internet), managers must ascertain which combinations of channel and type of interaction are most desirable to serve customers in a cost-efficient, yet satisfactory, way. For purchases, migrating customers to low-cost channels (e.g., the ATM and the Internet) and, thus, dehumanizing the interactions, while potentially reducing the cost of serving customers, is a risky strategy that may miss valuable opportunities to engage with them, better understand their needs, and cross-sell high-value products and services. Thus, firms are advised to elevate the human component (e.g., encourage the use of the physical store) in interactions that involve a high risk for the customer and that, at the same time, are more profitable for firms. In our application, two of every three purchases occurred in the branch, a figure that can even be increased by targeting customers with direct marketing campaigns, as shown in our research.

In contrast, for routine communications, such as checking account balances, firms may consider migrating customers to automated channels (e.g., online channel) in order to reduce the cost of serving the customer and, at the same time, improve the customer experience (through a more convenient service). This can be done in a number of ways. While our findings indicate that customers tend to prefer the branch for communicating with the firm, they also suggest that customers with more experience in automated channels have a higher likelihood of using them again. Thus, firms are advised to train their customers in how to use the ATM and the Internet, convincing them of their convenience for performing these types of operations. For example, leading international banks (e.g., BBVA) are introducing gamification strategies to encourage customers to use digital channels for routine operations (Burke 2014). Trying these channels and gaining usage experience will promote their future use, as our results demonstrate. At the same time, more experience in these channels for communications does not increase the likelihood of using them for purchases (as shown by the channel spillover effects), where the human contact is important, as we note previously. In our application, nearly 60% of all communications occurred in the branch, which suggests a good opportunity for improving the management of these interactions.

While migrating customers to low-cost channels for communications seems to be a good strategy for a more effective and profitable management of these interactions, managers should also carefully consider some potential negative consequences (Trampe, Konus, and Verhoef 2014). For example, some customers may hold strong preferences for human contact. Migrating them to automated channels may generate frustration and anger, weakening the relationship with the firm with potential negative implications for future purchase behavior. This strategy might also result in an overall increase in demand for the automated channels, for example, if customers find it very convenient to interact with the firm through them and increase the use of these channels. This would ultimately lead to an increase in the overall cost of serving the customer base through these channels and the need to devote additional resources to satisfy the high demand. This migration strategy might also lead to increased information monitoring and, in turn, more active account management resulting in less profitable customers (e.g., more switching to other banks offering better conditions). A careful analysis of individual reactions to migration strategies as well as their aggregated effect on channel demand would be pertinent before any migration strategy is implemented.

Limitations and Further Research

The limitations of our study can provide several opportunities for future research. First, for theory-testing purposes, we applied our conceptual framework and hypotheses to a particular context, financial services, and to a particular company. While the characteristics of this industry (large and strategic with a contractual nature that offers customers multiple opportunities to interact with the firm) make it a good candidate to test our theory, caution should be used in extrapolating the results to other contexts. In an effort to generalize our research, we derive a conceptual model that offers theoretical and managerial insights into the underlying forces that drive channel choice. However, future research should investigate whether our findings are consistent across different industries and geographical regions.

Second, given our focus on financial services, we have considered the three most prevalent channels: the branch, the ATM, and the Internet. Although these three channels are dominant in the industry and receive more than 95% of the total interactions, customers can use other (newer) channels to contact the firm. For example, with the proliferation of smartphones, the use of the mobile channel is growing very rapidly (Wang, Malthouse, and Krishnamurthi 2015). Social network platforms are also increasingly used by customers to interact with firms and with other customers. While we have provided a sound theoretical basis for understanding channel choice and its drivers, it would be valuable to extend our study and consider these relatively new channels.

Third, our study shows that marketing activities play a key role in influencing channel choice. While our study was concerned with the number of marketing actions, their content (e.g., economic incentives, information) may also be important for understanding customer channel choices. However, we did not have access to this information. Moreover customers are heterogeneous, and they may respond differently to marketing activities or have different preferences for certain channels. Future research should validate our findings using explicit information about customer channel preferences and testing the impact of different types of marketing messages on channel selection and usage at the individual customer level.

Footnotes

Acknowledgment

The authors appreciate the financial support received from the projects ECO2014-54760 (MINECO, FEDER), and S09-PM062 (Gobierno de Aragon and Fondo Social Europeo). F. Javier Sese acknowledges the financial aid received from the program “Ayudas a la Investigación en Ciencias Sociales, Fundación Ramón Areces.” Both the authors want to show their gratitude to the collaborating bank for providing the data for the analyses. They gratefully acknowledge comments and feedback by research seminar participants at the University of Muenster.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.