Abstract

Keywords

electrosawhq.com

The ownership of rental housing by private equity (PE) companies has been on the rise in the United States and abroad in recent decades. PE firms invest funds contributed by institutional and otherwise large investors, including pension and sovereign wealth funds. The typical PE playbook is to take controlling interest in a business, restructure it to increase the appearance of improved financial performance, and resell for a substantial profit. PE operates in a variety of sectors, including healthcare, media, and retail, often to the long-term detriment of these businesses and their services. PE firms frequently take aggressive asset-stripping and cost-cutting measures, leading to lower quality services, while also raising costs for customers. Since the expansion of PE buyouts in the 1990s, there has been widespread documentation of the damages wrought by PE takeovers, from the elimination of local news coverage to declining care in nursing homes. 1 Since the foreclosure crisis and the recession of the 2000s, these firms have begun taking a controlling interest in the ownership of rental housing, leading to widespread attention on the larger phenomena of corporate landlords.

While corporate ownership is sometimes conflated with PE ownership, not all corporate landlords are PE firms. Some, including the largest and most widely known, are publicly traded real estate investment trusts (REITs). Though PE funds and REITs differ in their specifics, both are conduits for investing in real estate, yoking the housing needs of millions of renters across the planet to investors’ expectations for competitive financial returns. Because of PEs’ and REITs’ aggressive expansion in rental markets, tenants have faced escalating rents and reduced services, exacerbating rent burden and displacement, and crowding out of opportunities for affordable homeownership. Here, we describe the factors contributing to the rise of PE and REIT ownership in housing, the impact of this trend on poor and working-class communities, and the current organizing that seeks to address it. We give particular attention to single-family rentals (SFR), a new frontier for PE and corporate investment and the subject of our ongoing research. We present an analysis of the spatial concentration of rental homes by PE and REIT firms in the Atlanta metropolitan area, which has become one of the principal sites of PE investment into SFRs across the country.

Seeing Opportunity in Crisis: PE Firms and the Rental Market

Historically, owners of both low-cost apartments and SFR homes were predominantly local independent landlords seeking long-term, stable rental income. Though corporate ownership of multifamily properties like apartment buildings is not new, PE has claimed a growing share of this market in recent decades. The burst of the dot-com bubble of the late 1990s and the stock market crash in the 2000s led to low interest rates and easy mortgage credit, making real estate an attractive investment. These conditions piqued PE interest in multifamily properties, particularly in New York City, where PE firms targeted rent-stabilized properties. The attractiveness of rental properties was enhanced by revisions to state laws governing rent regulation in the 1990s allowing units with already high rents and those that became vacant to exit the rent-stabilized inventory. 2 The rationale for these changes was that occupants of high-rent units do not require protection and that rent regulations made it financially infeasible for owners to renovate units upon vacancy. PE firms capitalized on these changes, purchasing rent-regulated properties in order to remove existing tenants and replace them with higher-paying occupants, exacerbating displacement and gentrification. Similar patterns occurred in San Francisco, following the thinning of rent regulation there in the 1990s. 3

PE firms have continued to acquire multifamily properties in desirable housing markets across the country since the housing crash and recession of 2008, which tightened mortgage lending and boosted demand for rental housing. Recently, PEs saw opportunity in yet another crisis, the Covid-19 pandemic. Even as tenants faced difficulties paying rent during the pandemic, PE firms bet big on the post-pandemic resurgence of rental apartments in destination markets like New York, targeting relatively lower-valued properties relative to what investors believe they could realize through restructuring. 4 Limited reporting requirements and the use of shell corporations to purchase real estate makes it difficult to precisely enumerate the number of units controlled by these firms. One source estimates the minimum number of apartment units owned by PE firms in 2022 at more than one million nationwide, though these are concentrated in high-demand markets like New York and San Francisco. 5

Growth of Private Equity in Single Family Rentals

Even with the precedent of corporate ownership of multifamily apartments, the incursion of PE into the SFR market, in particular, has represented a dramatic shift in housing ownership. Before the foreclosure crisis of 2008, large financial institutions avoided operating SFRs because they are scattered and have diverse characteristics, making them more difficult to manage. The foreclosure crisis, however, presented investors with the opportunity to buy discounted homes at scale during a period of surging demand for rentals. Blackstone was the largest PE investor in SFRs, buying and operating homes through its rental-home company Invitation Homes since 2012. American Homes 4 Rent was another early investor in single-family homes, leveraging a $600 million investment from the Alaska Permanent Fund. Other early investors included Front Yard Residential and Tricon American Homes. More recently, there has been a period of SFR industry consolidation through mergers and acquisitions, alongside shifts in their corporate structures. Invitation Homes—now the largest SFR landlord in the United States after a decade of acquiring other competing firms—initially started as a PE-controlled subsidiary of Blackstone, but was taken public in 2017 in order to raise additional capital for expansion. Pretium Partners, the PE parent firm of Progress Residential is the largest private owner of SFRs after their 2021 acquisition of previously publicly traded Front Yard Residential.

Estimates of PE ownership of SFRs indicate they own at least 240,000 homes across the United States. 6 A common industry talking point is that this is just a small fraction of SFRs, somewhere in the range of 1 to 3 percent, challenging suggestions they are monopolizing the market for rental homes. This talking point has been amplified in mainstream media, with some arguing PE funds play too small a role in the rental home market to cause concern. 7 However, this argument fails to recognize the fundamental importance of location in understanding housing markets. Certainly, 300,000 rental homes are a small fraction of the entire U.S. inventory, but they are highly concentrated in specific metropolitan areas. In other words, they are unevenly distributed, and national statistics obscure how local markets possess high concentrations. In the immediate aftermath of the foreclosure crisis, firms like Blackstone bought heavily in the Sunbelt, particularly in suburban neighborhoods with newer housing. Atlanta has by far the largest number of homes owned by these PE and REIT landlords, followed by places like Phoenix, Houston, Las Vegas, and Tampa.

Investors targeted these metropolitan areas for a number of reasons, among them low purchase prices, but also strong underlying fundamentals in terms of housing demand and a permissive regulatory environment, including a lack of tenant protections that might constrain their business models. Even within the metros in which these firms own SFRs, their holdings are often highly spatially concentrated in certain neighborhoods, 8 as we demonstrate below.

After the initial wave of SFR acquisition by the largest firms, another set of firms began buying lower-valued properties in different housing submarkets, often in working-class and relatively lower income neighborhoods compared to the more middle-class suburban Sunbelt neighborhoods where Blackstone and its peers concentrated investment. With reduced inventory and higher acquisition costs in the once-distressed neighborhoods where firms like Blackstone bought large portfolios of discounted properties, these second-wave SFR investors searched for other sources of lower-cost homes. These firms include FirstKey Homes, owned by Cerberus Capital Management, and Vinebrook Homes, controlled by a REIT created by NexPoint Advisors who also specialize in the Midwest, including in cities like Cincinnati, Indianapolis, Milwaukee, and St Louis.

Patterns of SFR Home Investment in Metro Atlanta

One of the principal challenges in studying institutional landlords is their use of corporate aliases to obscure the true scale of their holdings. Rather than finding the full scope of a given company’s holdings in tax assessor records under the parent company’s name, anyone who goes looking for these corporations will instead find an overlapping series of shell companies with obscure names like SFR 2014 GA LLC, SUNFIRE 3 LLC or 2018-4 IH BORROWER LLC. The proliferation of shell companies makes it incredibly difficult to identify the full scope of any company’s holdings. While some researchers have taken advantage of corporate filings for the largest publicly traded REITs, including Invitation Homes, American Homes 4 Rent, and Tricon American Homes, 9 PE firms are not required to disclose such information publicly because of a carve out in the Investment Company Act of 1940, and so their operations remain relatively opaque. This has in part contributed to a dearth of research into PE firms and other institutional investors relative to REITs.

We were, however, able to uncover the full scope and a more localized picture of the properties owned by these investors in the metro Atlanta area, by cross-referencing corporate LLC aliases and office addresses to tax assessor records. We identified over 32,028 single-family homes owned by the ten largest institutional SFR investors in just the five core counties, 10 representing 2.35 percent of all housing units, 3.47 percent of all single-family homes, 5.59 percent of all rental units, and 17.36 percent of all SFRs across these five counties.

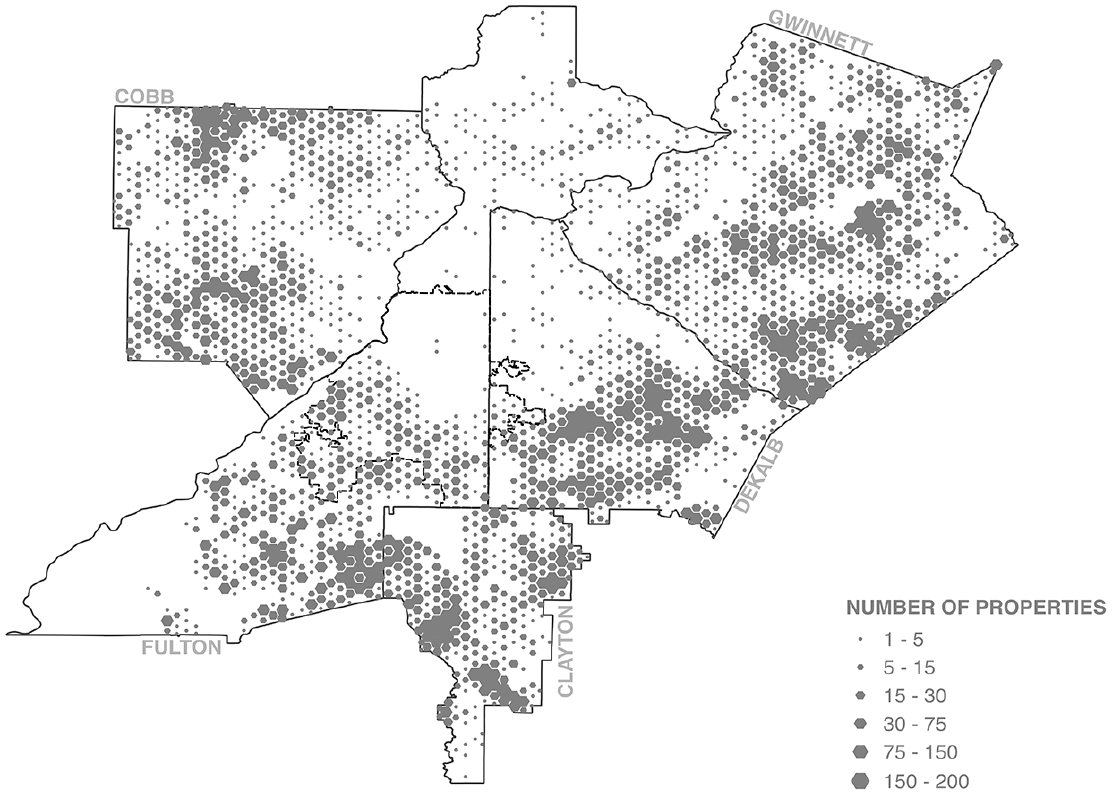

Just like the national-level statistics used by apologists for these corporate landlords, these metro-wide statistics similarly obscure the deep spatial concentration of ownership. The top 10 percent of census tracts account for over half of the total properties owned by these companies. So while these landlords own almost no single-family homes throughout the predominantly wealthy and white area that noted housing scholar Dan Immergluck calls the “favored northern quarter” of the Atlanta metro, 11 they own thousands in predominantly Black and working-class suburbs of south DeKalb, south Fulton and Clayton counties, along with the more racially diverse and middle-class suburbs of eastern Gwinnett County and northern Cobb County.

While Figure 1 shows the total concentration of properties owned by these ten landlords, and therefore, the areas where these firms generally have targeted their investments, it does not address the question of market power that is crucial for understanding the impact of these institutional investors. By comparing these concentrations of corporate-owned SFRs to the total number of SFRs in the same neighborhoods, we can identify twenty-four census tracts where these corporate-owned SFR properties account for more than 50 percent of all SFRs, and in some tracts these figures rise to as much as 80 percent. Even more so than the total number of properties, it is these shares of particular submarkets that point toward oligopolistic, if not outright monopolistic, control, allowing these firms to not only set rental prices, but also to more readily exploit tenants through substandard conditions, lack of maintenance, extraneous fees, and serial evictions due to the lack of alternative options available to them.

Geography of corporate-owned single-family rental properties across Atlanta. Single-family homes owned by the ten largest corporate landlords, Atlanta five-county area, 2022.

Our research further shows that different types of corporate landlords adopt different kinds of strategies when it comes to the neighborhoods they target, as seen in Figure 2. PE firms like Amherst and Vinebrook have concentrated their acquisitions almost entirely in the southern portions of the five-county metro, while publicly traded REITs were more active in the northern reaches of the metro. This pattern maps almost perfectly onto the geographies of race and income in Atlanta, where predominantly Black and poor to lower-middle-class communities are concentrated in a crescent shape across the southern suburbs, while whiter and more affluent neighborhoods sit to the north of the city itself. Indeed, the average property owned by a PE firm sits in a census tract that is 73 percent Black and has a median household income of $62,750, while the average property owned by public REITs is located in a tract that is only 45 percent Black and has a median income of nearly $79,000.

Comparison of investment strategies of publicly traded REITs and private equity firms. Single-family homes owned by the ten largest corporate landlords, Atlanta five-county area, broken down by publicly traded REIT or private equity, 2022.

While all corporate landlords follow a similar playbook, this map demonstrates clearly that different firms have distinct spatial strategies for investment that target different segments of the market. While it reveals clearly that PE firms in particular are most directly targeting working-class communities of color in cities and suburbs in Atlanta, this is a strategy these firms are using in communities across the country.

Impact on Residents and Communities

Investigative journalists and academics have repeatedly identified problems with rental housing companies owned by PE and REIT entities. There is ample documentation that these companies raise rents and otherwise increase revenues by adding and aggressively collecting numerous fees and charges. 12 Even as they charge ever-higher rents, several PE and REIT landlords have reduced services, leading to unsafe housing conditions. In January 2023, the city of Cincinnati filed a lawsuit against VineBrook Homes for failing to maintain its rental homes in accordance with municipal codes and landlord-tenant laws. VineBrook owns more than 3,000 homes in Hamilton County, which contains Cincinnati, and thousands more in nearby Dayton, making them by far the single largest SFR landlord in the region. Investigative journalists in Memphis similarly found that FirstKey Homes—controlled by PE firm Cerberus Capital Management—was linked to an outsized number of code violations. 13 Most, if not all, of the largest SFR landlords have been accused of cutting back on maintenance costs. The Washington Post recently reported that Invitation Homes failed to follow the permitting process for repairs, leading to faulty repairs including leaking pipes. 14

PE and REIT landlords are also associated with elevated eviction rates, reflecting these firms’ aggressive pursuit of revenues, even in the presence of code violations and habitability concerns. A study of eviction filings in Atlanta found that several corporate SFR landlords were significantly more likely to file for eviction compared to owners with fewer than fifteen properties. 15 Related research in metro Las Vegas has come to similar conclusions. 16

PE firms and REITs buying single-family homes are also crowding out homeownership opportunities for working-class households. 17 These entities, with their ability to pay cash and waive contingencies, have an unfair advantage competing for homes compared to prospective homebuyers, who typically require a mortgage to finance the purchase. The incursion of firms like Cerberus and VineBrook into moderately priced, working-class and minority neighborhoods that have historically served first-time homebuyers has been especially impactful. As a result, would-be homebuyers are consigned to renting from companies backed by institutional investors and paying more than they would have paid to a mom-and-pop landlord, and often more than they would have paid toward their mortgage and taxes had they been able to purchase the property themselves.

Organizing Resistance to Private Equity in Housing, and Its Challenges

Despite the considerable power these institutional investors hold in the markets in which they are active, tenants, housing justice activists, and even some politicians have begun standing up to these new corporate landlords, suggesting strategies for holding owners accountable and promoting housing security in Atlanta and beyond. In San Francisco, tenants formed the Veritas Tenants Association (VTA), now a statewide tenants union, to fight for important concessions from the large multifamily PE landlord Veritas. 18 Tenants demanded Veritas cancel rent debt accumulated during the pandemic, and they withheld applying for rental assistance until Veritas canceled debt not covered by the state and canceled scheduled rent increases. Coming out of this effort, San Francisco adopted a “Right to Organize” ordinance, requiring landlords to bargain with tenant associations. This campaign was successful in bringing Veritas to the table because of its need to collect state rental assistance to meet the substantial debt obligations these firms take on to expand their holdings. Rent and debt strikes, particularly large-scale multi-building campaigns, can force these firms to negotiate better terms with their tenants, though this capacity is contingent on tenant protections, which are far stronger in California than most of the other states where institutional investors, particularly single-family landlords, have targeted their investments.

Despite corporate landlords’ growing presence and the media attention paid to them, tenant organizing campaigns against these landlords are less common than those in multifamily buildings. One of the principal barriers to organizing against SFR landlords is the fact many of them targeted investments in states with limited tenant protections like Georgia, Florida, and Arizona. Similarly, it is considerably more difficult to organize SFR tenants given that each of them lives in a completely separate property that might be spread quite far across a metro area. Perhaps the most notable exception to this rule comes from the Twin Cities of Minneapolis and Saint Paul, Minnesota, where tenants of properties owned by SFR landlord Pretium Partners have been organizing with Inquilinxs Unidxs por Justicia (United Renters for Justice) to demand better housing conditions and treatment and bringing public attention to the problems associated with this company, which targeted its investment in Black working-class neighborhoods on the northside of Minneapolis. Since 2018, city inspectors have documented more than 1,500 code violations across the company’s roughly 200 homes. Tenant activism has brought this problem to the attention of Minnesota Attorney General Keith Ellison, who filed a lawsuit against HavenBrook, the property management arm of Pretium-subsidiary Front Yard Residential. The city of Minneapolis and Front Yard Residential recently agreed to a set of conditions the landlord must abide by to continue operation, including addressing code enforcement violations. The company is also subject to a temporary moratorium on acquiring additional properties pending the company meeting those conditions. 19

Pro-tenant activists have also applied pressure to the institutional investors contributing funds to corporate landlords. Some of the largest investors in PE funds are public pension funds and university endowments, whose investments pit their financial returns against the housing security of the workers and communities they represent. The California Public Employees’ Retirement Fund (CalPERS) and the New York State Teachers’ Retirement Fund (NYSTRS), two of the nation’s largest public pension funds, have invested substantial amounts with Blackstone, among other PE funds managed by firms active in real estate. Given increasing awareness of the effect of PE and REIT housing investments, activists have raised the possibility of conditioning pension fund investments on tenant protections. As noted in a 2019 Gothamist article, there is precedent for this type of conditional investment: in 2009, a coalition of housing advocates pressured the New York City comptroller to adopt a policy allowing pension funds to withhold investments in PE firms found to be engaged in predatory behavior. 20 More recently, tenants and union members have protested the University of California’s more than $4 billion investment in the Blackstone Real Estate Investment Trust (BREIT). 21 The Private Equity Stakeholder Project (PESP) has similarly brought attention to the North Carolina Retirement System’s (NCRS) investment with PE firms who are in turn investing in Progress Residential. 22

In addition to these various other challenges facing those seeking to rein in these corporate landlords, there is also the problem of information: tenants and organizers require the kind of property ownership information and corporate aliases employed by landlords in order to understand the scale of their holdings. Efforts by organizations like the PESP have been helpful on this front, using their research capacity to demonstrate the practices and ownership patterns of entities like Pretium Partners. The Action Center on Race & the Economy (ACRE), often in partnership with PESP and other organizations, has also elevated the issues raised by residents of working-class communities of color to the national stage, and they have been instrumental in recent action by Congress to investigate the practices of some of these PE and REIT landlords. 23 Together, these efforts point to the challenges of understanding and organizing against a newly emerging form of landlordism that is both intensely local in its effects and experiences, but also national or global in its structure. While tenants within a single building can gain leverage over their landlords when the conditions are right, organizing tenants of a shared corporate landlord dispersed across thousands of single-family homes in the sprawling suburbs of a major metro area represents a more daunting task, though one that also cuts to the heart of the changing nature of the landlord-tenant relationship today.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.