Abstract

Based on mechanism design theory on asymmetric information, this study devises a selectable menu of contracts with price discounts and trade credit rates and proposes strategies for mitigating the risk of payment default when a tourism service provider trades with unfamiliar tour operators. Tourism service providers are suggested to remain conservative under a positive economic condition and progressive under a moderate economic condition when engaging in a new business opportunity. However, a fringe level of progressivism may be maintained under a moderate economy and a low-risk environment. The net benefit of tourism service providers increases when the bank rate is high, and the profit of the entire tourism channel increases when the percentage or ability to pay reliable agents is high.

Keywords

Introduction

Trade credit is a common business practice that allows buyers to pay suppliers at a later date, particularly in a business-to-business context; this practice accounts for 17–18% of total account receivables and 35–40% of the total debts of small- and medium-sized enterprises (SMEs) in the United Kingdom and the United States, respectively (Cuñat, 2007).

In the tourism industry, tourism service providers (e.g. hotels, restaurants, amusement parks, and cruises) likely deal with third-party intermediaries to their products/services. No matter operating online or off-line, most tourism intermediaries either follow an agency model in which they receive commission from tourism service providers or a merchant model in which they purchase tourism products/services at a discount with trade credit and sell them to customers with markups (Ivanova, 2017; Lee et al., 2013). When dealing with intermediaries under a merchant model, such as tour operators, tourism service providers often offer trade credit to buyer intermediaries for facilitating business transactions. The buyer intermediaries often do not immediately transfer the collected fees to the sellers when offered trade credit. They keep the money in their escrow account until the payment due date. Although the accumulated cash of buyers can increase quickly, a few tour operators may delay the payment after tourists’ departures (Buhalis, 2000). Therefore, tourism service providers often bear a payment default risk, thereby possibly leading to tremendous income losses when buyers fail to satisfy their payment obligations before an agreed-upon deadline. The delayed payment could eventually become bad debt. In addition, tourism intermediaries using a merchant model, such as Orbitz.com, Cheaptickets.com, part of Expedia.com and Hotels.com (Lee et al., 2013), and traditional tour operators (Ivanova, 2017), account for a large portion of the tourism distribution channels. Thus, most interorganizational conflicts in tourism are related to tourism intermediaries’ opportunistic behavior of delayed payment (Buhalis, 2000; Ivanov et al., 2015; Mwesiumo and Halpern, 2016). Our study focused on tourism intermediaries adopting a merchant model.

To tackle such conflicts associated with delayed payment, a seller generally screens buyers carefully and opt to deal with those with established credit histories and favorable reputations or those who are willing to prepay 50–80% of the sales amount; however, trading risk continues to concern tourism and hospitality businesses. By contrast, being over prudent may not be the best strategy when businesses search for new business opportunities with enticing benefits. Therefore, an effective risk management framework, which can assist service providers to target and trade with credible partners that offer business opportunities, is important.

The majority of tourism service providers are SMEs (e.g. over 90% in Europe) (Bastakis et al., 2004); furthermore, in various countries, about 20–75% of their business opportunities come from trade intermediaries, such as tour operators (Buhalis, 2000; Mohammad and Ammar, 2015; Stangl et al., 2016), who play a prominent role in the integration of tourism products and services. When dealing with powerful intermediaries, small- and medium-sized suppliers likely have no choice but to offer trade credits to generate or secure business. However, tour operators often cannot earn adequate profit from regular business operations; thus, they may seek out risky financial investments to earn additional returns when possible (Buhalis, 2000). Even tour operators in Europe with good performance only earn approximately 4% profit margin from regular business annually (Roper, 2005), and up to 25% of tour operators’ profit is earned either from interest gained or from other businesses (Buhalis, 2000; Bywater, 1992). A medium-sized operator can easily accumulate billions of dollars in cash because of delayed payments (Buhalis, 2000); such cash accumulation is equivalent to tourism service providers’ granting trade credits to tour operators. Furthermore, offering extensive credit periods may assist in bringing in business opportunities for tourism service providers. However, delaying the receipt of payment could increase the risk of default.

Information asymmetry exists between a buyer and a seller because the buyer is certainly more aware of its ability to pay or tendency to default than the seller. Although credit risk can be partially estimated from historical records, a tour operator’s actual payment intention remains undetermined. Long-lasting whole sellers are considered to be financially healthy, whereas newly established agencies may possess a high default risk. Nevertheless, even large and famous tour operators can become bankrupt but are unlikely to reveal their updated financial conditions until the final moment. For example, XL Leisure, which was named the third largest tour operator in the United Kingdom, collapsed in 2008, thereby leaving 85,000 tourists stranded in the countries they were in and costing the Air Travel Trust over £27 million in refunds and repatriation costs; this incident caused severe damage to the development of the British tourism industry (Bowers, 2011; Wray, 2008). ShunDa Company, which previously claimed to be the largest tour operator in Anhui Province, China, declared bankruptcy in 2010, thereby leading to tremendous losses in the entire tourism business of the province (Li et al., 2013). The bankruptcy of tour operators is among the top three causes of conflict between hospitality suppliers and tour operators (Buhalis, 2000), thereby pushing many tourism suppliers into an empty-handed condition (Ivanov et al., 2015). After declaring bankruptcy, tour operators must pay consumers and other legal bodies. Tourism service providers are often the last to receive compensation among all creditors. Most tourism service providers lose a significant amount of money because of tour operators’ payment default (Buhalis, 2000).

Given that the said conflicts commonly exist in interorganizational relationships (Lumineau et al., 2015), surprisingly rare research has investigated such conflicts and feasible solutions in tourism (cf. Mwesiumo and Halpern, 2017, for a review). However, from the viewpoint of practitioners, when tourism service providers encounter uncertainty of delayed payment from tour intermediaries working on a merchant model and consequently the risk of payment default, they must exploit risk management tools and techniques to reduce or avoid such losses. Only few tourism studies contributed to this issue by using statistical models to assess or predict default risks of bankruptcy; however, other conflict management or risk management techniques, such as contract design, did not receive adequate attention. Therefore, the research question of this study is how tourism service providers can manage the risk of payment default when dealing with unfamiliar tourism intermediaries?

In answering the research question, based on mechanism design theory, the present study aims to devise a menu of contracts to facilitate self-selection of tour operators with low- and high-risk of payment default through acquiring their private information by offering commensurate financial compensation (i.e. “information rent”). Business contracts are prevalent in the tourism industry and govern the selling prices, shipping quantities, or interest rates of late payment. Contracts in this study exclusively concern price discounts and interest rates. A well-designed self-selection contract based on the principle of contract mechanism shall ensure that different types of agents will select a contract particularly designed for them. The selection process reveals private information on the financial condition of buyer agents by conceding a part of the income of suppliers to the buyers in the self-selection contracts. For example, a conservative buyer may prefer a price discount rather than a low credit rate.

Each tourism supply chain member strives to maximize its own profitability. During the course of a business transaction involving trading credits, the buyer agents often possess more reserved information on their intention or ability to pay than service providers do. The study results shall assist tourism service providers in protecting their own interests by proposing a framework to mitigate the buyer agent’s payment default risk when a seller deals with unfamiliar partners.

Literature review

Risk management studies in hospitality and tourism

The management of default risk has not received sufficient attention in the tourism literature. Most existing studies focus on maximizing various statistical models in assessing or predicting default risks of bankruptcy (cf. Li et al., 2013, for a review). Several studies apply regression and intelligent models in predicting the default risk of hospitality firms (e.g. Youn and Gu, 2010). Multivariate discriminant analysis has been applied in the works of Gu (2002) and Gu and Gao (2000) to analyze business failure and bankruptcy of tourism firms. Kim and Gu (2006) employed a logit model to forecast the default risks of hotel and restaurant firms. However, other risk management mechanisms, such as the use of contract approaches in distinguishing and selecting between low-risk and high-risk buyers, are rarely included in the tourism management literature.

Information asymmetry and mechanism design

Agency theory suggests that agents in a principal–agent context should act in the principal’s best interests; agency problems arise when the agent and principal have distinct objectives or the agent protects and advances his/her own interests at the expense of the principal (Song et al., 2012; Stabler et al., 2009; Tsai and Gu, 2007). The agent takes advantage of the principal because of the existence of information asymmetry, in which the agent is often more knowledgeable on the ins and outs of the context than the principal. A more knowledgeable agent can also benefit from delivering credible information to the principal with limited knowledge. Two types of problems could result from the principal–agent relationship. The first is adverse selection, when the agent holds private information that confuses the principal’s decision. The second is moral hazard, when the agent takes private action at the cost of the principal. This study mainly focuses on solving the adverse selection problem by developing a tool to reveal the agent’s private information. However, the moral hazard problem should be avoided once the adverse selection problem is solved.

An agent may deceive a principal for a reward. Hence, mechanism design theory (Mas-Colell et al., 1995) suggests that a mechanism or a contract for the principal should be created to encourage the agent to tell the truth for the benefit of both parties, as well as to address the problems resulting from information asymmetry between two parties. A favorable mechanism drives both parties to reveal their real private information while maximizing their own interests. For example, a mechanism that provides selection between low-stipend, high-bonus and high-stipend, low-bonus can reveal an employee’s working intention. The mechanism design problem can be solved using the revelation principle (Dasgupta et al., 1979; Myerson, 2008), which is explained in “Model and method” section and “Risk analysis” section.

Models incorporating mechanism design theory have been applied extensively in managerial studies related to various fields, such as the manufacturing supply chain. For example, Tomlin (2009) devised a model in which a manufacturer faces suppliers of unknown reliability and allows learning of the suppliers’ reliability through their repeated interactions. Corbett (2001) analyzed the contract design issue of procurement auctions under asymmetric information on the cost of suppliers. Yang et al. (2009) applied mechanism design theory in designing a menu of contracts that could assist manufacturers to obtain private information on the disruptions of suppliers. However, these concepts and methods have rarely been used in analyzing the behavior of firms or consumers in the tourism industry (Song et al., 2012; Yang et al., 2009). Guilding et al. (2005) adopted agency theory to discuss the condominium owner–manager relationship in the Australian tourism sector; Bastakis et al. (2004) proposed a framework describing a bargaining game with asymmetric information between tour operators and tourism suppliers. To the best of our knowledge, no tourism study has employed such concepts in analyzing risk management strategies for tourism service providers.

Trade credit and default risk management

Several studies on risk management have investigated the default risk in seller–buyer relationships. Several scholars advocate the development of risk prediction models in forecasting the default risk of buyers to assist sellers avoid doing business with high-risk buyers (e.g. Li et al., 2013; Youn and Gu, 2010). Ng et al. (1999) suggested that expanding the customer base can facilitate the prevention of default risk by extracting the possible default intention of other customers through a complex information interchange. Cuñat (2007) argued that sellers can increase the interest rate of trade credit for high-risk buyers, and the part exceeding the regular bank rate goes to an insurance premium. Smith (1987) showed that contracts with two-part payment terms that specify high effective interest rates for cash discounts can be used to effectively screen buyers’ creditworthiness.

Although Smith (1987) and Cuñat (2007) also investigated the contract design problem in trade credit, their focus differs from that of the present study. Cuñat (2007) designed contract terms in a symmetric information context in which the buyers’ default risk is known to the sellers. Smith (1987) was not concerned with risk issues and emphasized that trade credit is a source of revenue that substitutes the function of banks and provides a screening tool to discover unknown payment intention. The two studies jointly proposed a direction for risk management. Therefore, this study materializes the risk management idea in the revenue management context through the effective tool of trade credit.

The study considers the trade-off between default risk and financial income in contract design and integrates mechanism design theory with specific risk management strategies in the model design. It also proposes a framework that guides tourism suppliers to improve their risk management when dealing with unfamiliar tour operators or new business partners.

Model and method

In our stylized model, a tourism service provider, such as a hotel, sells hospitality products and services to tour operators who engage in speculative investment and short-term financial activities in managing their collected fees in escrow. Some operators may fail to pay their debts because of imprudent financial investment or insolvent condition. The proposed model advances a proper design of contracts that reveals the financial condition of these operators.

An operator’s tendency to pay, which reflects a company’s short-term liquidity and solvency on arbitrage assets and investment, is assumed to be unknown to the hotel. The model considers two types of tour operators, namely, θi and

The contract term

Parameters and decision variables used in this study.

Making a full payment is just a matter of time for high types. Therefore, the financial cost rate is φ + c with a generic bank rate φ if the high-type operators pay their debts immediately. If they pay late, then the financial cost rate becomes

The tendency-to-pay is low for low-type operators. For the convenience of analysis, we assume θl = 0 (i.e. low types would not pay from their pocket). Not paying without penalty is the ideal choice. To motivate the low types in selecting the paying option, we impose a business liability μ to operators for the loss of business goodwill in credit default. The choice for a suspicious operator is between φ and μ because of implicit penalty. The offered credit rate ξl is never paid by the low types but the issued credit rate represents a financial cost that the operator should pay but will not pay in the future. Thus, a low-type operator decides whether to pay by considering the choices between

Operators receive commensurate utility if they are given options among a set of properly designed contracts, which is specified in the next section. A high-type operator obtains a profit of

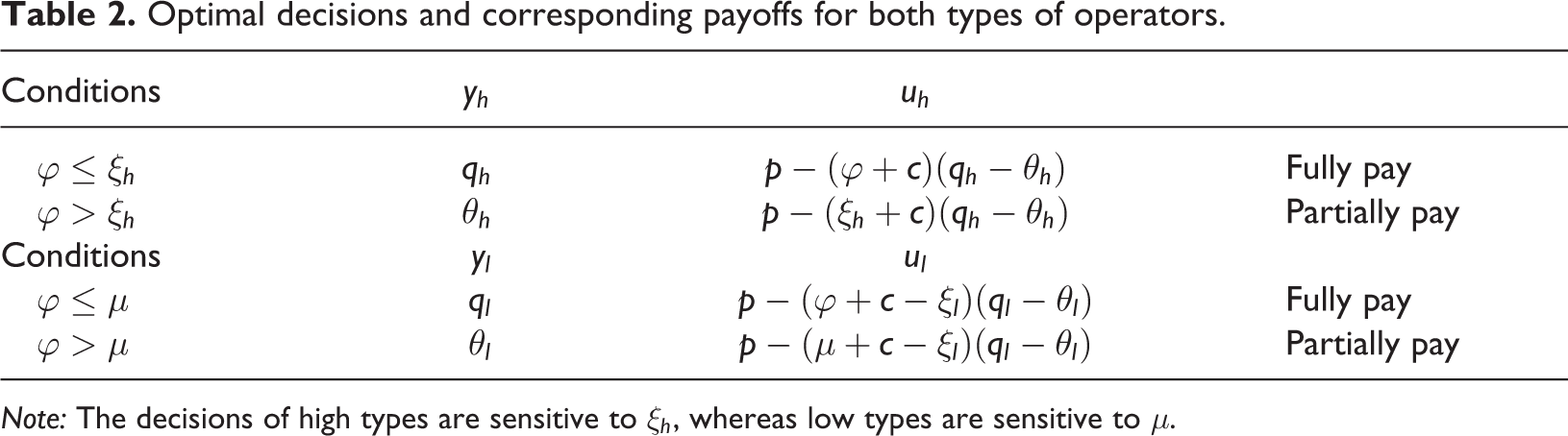

Operators’ decisions to trade on credit should be made according to the utility value (see Table 2). Table 2 lists all possible decisions yh and yl and the resulting utility uh and ul. Optimal decisions are shown separately for the two types of operators in the upper and lower part of Table 2.

Optimal decisions and corresponding payoffs for both types of operators.

Note: The decisions of high types are sensitive to ξh, whereas low types are sensitive to μ.

Definition 1

Given the fixed contract (q, ξ), the value

For the two contracts

To evaluate the optimal contract design, a truth-telling mechanism can be implemented by applying the revelation principle and envelope theorem (Dasgupta et al., 1979; Myerson, 1981, 2008). Two stages of games are involved in this mechanism, namely, contracting and executing. Operators hold private information on their payment ability at the beginning of the contracting stage and provide claimed information regarding their types. For an operator with a tendency-to-pay θi, the hotel expects an income of

The incentive compatibility (IC) constraints (equation (2)) make the contracts

Risk analysis

A satisfactory risk management strategy must minimize possible risks and maximize potential profits. The conventional methods of risk management disregard the possibility of concealment, and the practices of revenue management mostly overlook the influences of risks. Individuals make their decisions solely according to a risk value, which is the product of risk probability and loss value. This measure of risk value is rough and takes no account of asymmetric information. The sources of uncertainty may come from God’s dice or people’s deceits. The task of risk management is considerably easy if the factors that are known to someone but not to others can be revealed. This study’s analysis can assist tourism and hotel companies in reducing transaction losses because of information asymmetry, as well as increase their business income by seeking opportunities proactively.

Ideal world without disguise

This study determines the maximal profits that a hotel can earn under which no pretense is allowed to assess the cost and reveal the actual tendency-to-pay of operators.

Under information symmetry, the hotel principal and agent operators know each other well. Moreover, the business terms, such as prices, are offered to the operators according to their tendency-to-pay for maximizing the profitability of the hotel. The operators are not allowed to select the best deal to maximize their profitability. However, they can walk away from the deal if the offered contract is not profitable. Therefore, the contracts offered by the hotel must ensure positive profits for the operators. Problem (1) is simplified to

Proposition 1

The optimal contracts

Solutions of the optimal contracts for the hotel under information symmetry.

Table 3 shows the optimal contract design

Optimal business strategies under information symmetry.

An optimal contract in this ideal world suggests a lower price ql to low-type operators compared with qh offered to high-type operators. A hotel can unilaterally design an “optimal” contract that extracts all profits from operators without worrying about high-type operators selecting an l-type contract because high- and low-type operators can only accept h-type and l-type contracts, respectively. That is, the operators’ profits become

However, without an effective mechanism, self-selection would not be guaranteed under the contracts in Table 2 if operators were free to select the best contracts for improved profits. High-type operators will unexpectedly choose l-type contracts, under which the agents maximize their profits. In proposition 1, if the hotel knows the types of operators but cannot ensure self-selection from a contract mechanism, this model implies double marginalization: The total profit of the hotel and tour operators is less than the one under self-selection. The utility in situations where cross-selection is allowed, under which an h-type operator chooses an l-contract, becomes

Profits and utility when all operators pretend as low type.

The contract solutions in Tables 3 and 4 reveal a counterintuitive reaction: Untrustworthy operators tell the truth, whereas reliable ones deceive. This disguising phenomenon is generally attributed to the relatively high contract price for high-type operators in the first design of contract optimization. All operators appear to be low-type ones when they can select from the contracts in Table 3. In this case, low-type operators do not worry about exposing themselves because the hotels are unable to distinguish between the good and bad ones. Thus, the hotel performs risk management blindly or based on probability. The hotel has no reliable method of identifying operator types before a truth-revealing contract menu can be designed properly, and anyone is equally likely to incur bad debts or generate revenue streams. A rough idea in urging high-type operators to select the h-type contract is to reduce the price and increase credit rate. However, determining the extent of price reduction is not straightforward because a poorly designed contract may conversely enable low-type operators to disguise themselves as high-type ones. Therefore, the discovery of operators’ true types is the key in devising an effective set of risk management strategies.

Optimal contract in a disguised world with information asymmetry

The two optimizations in equation (1) are combined by applying the envelop theorem, in which operators’ optimizations are embedded into the hotel’s profit optimization (Myerson, 1981). Accordingly, the solution ensures self-selection in the informatics game. Given that

Proposition 2

The optimal contracts

Solution of the optimal contracts for the hotel under information asymmetry.

Table 5 shows the optimal contract design when operators hide their types from the hotel and where the optimization values are represented by the superscript (⋅)*. The contract allows the hotel to surrender the least share of benefits to the operators and effectively eliminate any disguise. Therefore, IC constraints are satisfied under the informatics game (5). Thus, high-type operators lose motivation to disguise themselves as low-type ones because the incentives received from the hotel are higher than those provided if they pretend to be low-type operators. In proposition 2, the hotel manager does not know the types of operators. As a result, self-selection surely will not be guaranteed without an effective mechanism. In this disguised world, the service provider makes the same contract with all types of operators without knowing their types.

Self-selected tour operators could benefit from either price discounts or delayed payments for an improved cash flow. The solutions in Table 5 achieve the goal of mechanism design and yield a menu of self-selection contracts, thereby effectively preventing both types of operators from disguising themselves. The contract

This study’s optimal contract design can also prevent certain unprofitable actions by hotels. Hotels that are unaware of the true financial condition of operators often act over-prudently on most business transactions, including asking for a high wholesale price q or a high credit rate ξ. This reaction may not be desirable in a speculative business world. Regimes (i) and (iii) of Table 5 show that a sufficiently low ql can induce immediate payment from less trustworthy operators. Therefore, the money that could otherwise disappear can be collected.

A guideline for risk mitigation strategies can be devised based on the contract design in Table 5. Because we are in a disguised world, the hotel manager cannot know the agent’s true payment intention (high or low) and the agents have motives to hide their types. With the use of a truth-telling tool, we summarize our strategies in Figure 2 by subdividing regime (I) in Figure 1 of a healthy business environment into regimes (i) and (iii), whereas the speculative business environment remains in regime (ii). The hotel manager is unaware of operator types; thus, a concession of profit between the hotel and the operators results in the latter’s confession of private information. Figure 2 explicitly shows the types of operators resulting from the revelation of the designed contract. To ensure self-selection, that is, the high types selecting a high-type contract and not pretending to be the low types to enjoy the benefit for inducing the truth, the hotel must pay extra incentives to the high types to let them stick to a high-type contract.

Optimal payment strategies under information asymmetry.

If the goodwill loss when defaulting is higher than that of borrowing from a bank to pay off debts, or μ > φ, as shown in regimes (i) and (iii) of Figure 2, then low-type operators borrow money to pay all debts. By contrast, high-type operators defer a portion of payment, that is,

The hotel should incur additional cost to compensate for the motivation of deception because operators tend to pretend to be of low type to enjoy discounted payment if paid immediately. Therefore, this additional cost paid to high-type operators is defined as information rent

Figure 3 suggests risk attitudes for the hotel manager facing business uncertainty α given the results of proposition 2. Figure 3 mirrors the regime setting of Figure 2 but changes the coordinates to bank rate φ and the percentage of high types α, respectively. Note that the high types have incentives to become low-types to enjoy better terms. Therefore, the higher the percentage of the high types exists in a market, the more the cost the hotel needs to bear. Therefore, the hotel becomes less profitable and it must conduct its business more conservatively. The extent of willingness to pay high information rent γ in exchange for the truth and certain returns is an attitude that accommodates risk. The value γ and

Risk attitudes toward business uncertainty.

However, low-type operators tend to defer payment at high credit rates. The hotel in regime (ii) should reject doing business with low-type operators because of their evident default intention. The risk attitude in regime (ii) is called differentiation.

Information-inductive risk mitigation

A risk management practice is developed when information is not transparent. Trade credit is reported to be cost-effective in revealing customers’ private information (Smith, 1987); thus, the current study’s analysis develops a risk management tool that is relative to an operator’s behavior toward the derived optimal contract menu in trade credit. Variable costs account for a small percentage of the total cost in hospitality operation. Therefore, the present study employs the trade credit tool to propose an effective coping strategy to minimize avoidable risks, costs, and losses.

The total tourism channel profit generated for the hotel, h-type, and l-type operators is defined as

The tendency of profit changes in each decision regime must be investigated to complete our risk mitigation strategies through a set of optimal contracts.

Proposition 3

The optimal profit π* earned by the hotel, information rent γ, and value of information δ to the hotel are listed in Table 6.

Optimal profits of the hotel for each contract under information asymmetry.

The various types of benefits that each type of operator brings to the hotel under information asymmetry are presented in Table 6, which shows that the hotel earns less as compared with Table 3 although the total channel profits increase. Part of the profit loss for the hotel is transferred to the operators, who are the information holders. Thus, the hotel should reduce the motivation of operators to disguise themselves while maintaining the maximum profitability of the hotel to uncover the types of the operators.

The targeted risk event is a payment default from the tour operators. Risk management refers to the implementation of actions in reducing the consequences of possible risk events. Most businesses do not simply walk away from all risk because doing so also precludes potential income. Most existing risk management practices are based solely on a risk value that is determined by the estimated likelihood of a risk occurrence and the financial consequence in a risk event. For risk assessment modeling, the percentage of less trustworthy operators and the selling price of hotel rooms are set as the likelihood and the consequence, respectively. However, this study’s risk assessment maximizes the use of hidden information in the decision-making process.

Proposition 4

Retail price p must be confined within the range of

Proposition 4 elaborates the key decision framework in this study. Figure 4 summarizes the resulting risk mitigation strategies. Decision-making is straightforward for a sufficiently high p. When the retail price p is high, the operators’ reward increases and business transactions tend to shift toward cooperation for all types of operators, regardless of risk. This situation is considered a high-reward event in risk assessment. When α is high, a high percentage of reliable operators are available in the market and the hotel anticipates a low probability of payment default. Therefore, a considerably high α results in a low risk of payment default. The situation is a low-risk event in risk assessment.

Risk mitigation strategies.

High-type operators lose the motivation to disguise themselves as low-type ones when p is high, such as

Four risk mitigation strategies are adopted in relation to the analytic results: avoidance, acceptance, transfer, and sharing (cf. Norrman and Jansson, 2004). Risk avoidance eliminates events that can trigger risks. Risk prediction and credit screening of customers are examples of risk avoidance strategies. Risk acceptance refers to the self-absorption of risks and its consequences. Preparing a reserve fund is an example of risk acceptance strategies. The ambiguous situations of low-reward, low-risk and high-reward, high-risk are considered in four detailed transfer and sharing strategies through information-inductive tools. Risk transfer often refers to the use of mechanisms to transfer risks to other parties or financial institutions, such as insurance companies, supply chain partners, and customers. Therefore, this study further distinguishes between the case of paying premium as risk transfer and the case of providing collateral as liability transfer. Finally, a general risk sharing strategy emphasizes the reduction of a risk impact by distributing risks to multiple parties or objects, such as business diversification. This study also views revenue sharing as risk sharing and business opportunity as liability sharing, because the former uses money and the latter uses the tool of making money to trade financial safety. Several hotels can perform risk sharing by sharing a credit loss collectively or performing liability sharing by collaboratively offering hotel rooms to complete a single transaction. The conditions in proposition 4 are further applied to concrete risk mitigation strategies through the following arguments. Proposition 4 shows that our focus is on the price range

The process of decision-making becomes ambiguous when business transactions are conducted in high-reward, high-risk or low-reward, low-risk situations because both situations are endowed with similar risk values in terms of quantitative steps of most-risk assessment processes. Determining a suitable mitigation strategy solely on the basis of the risk value is difficult without referring to other factors. The two boundary prices indicated in proposition 4 characterize an interesting region in Figure 4, which includes regimes (i) and (iii), and are divided by the discriminating α value in equation (5). High-reward, high-risk and low-reward, low-risk agents occupy the left and right wings of the region, respectively. In regime (i), the hotel is dealing with a low-reward, low-risk operator if

Low-type operators would prefer to borrow when the interest rate imposed on borrowing from a bank is lower than that imposed on delayed payment. Thus, the hotel encourages low-type operators to pay immediately by reducing prices that are lower than the h-type price and adapting transfer strategies by transferring risks to a third-party institution. The hotel’s accountability, responsibility, and authority under the transfer strategies are reassigned to another stakeholder (i.e. the bank) who is willing to accept the risks. Thus, the hotel earns high profits from transactions with reduced risks. Given that most agents are reliable in regime (i) and hotel profit is reduced slightly, the hotel exercises the risk transfer strategy by sharing a small amount of income, which is equivalent to an insurance premium. Conversely, if

Only a small percentage of operators in regime (iii) is reliable. Therefore, the hotel should focus on collecting revenues from low-type operators and pay information rent to high-type ones, that is,

Regime (ii) is excluded in Figure 4 because it does not involve α. Therefore, avoidance strategy is clearly associated with regime (ii). The hotel should exercise avoidance strategy when detecting profit loss tendency because of defaulting from low-type operators to prevent risky transactions in which rewards and well-being drop to unacceptable levels. The hotel can design a contract to enable the low-type operator to voluntarily terminate the cooperation. Contract terms or constraints are adjusted to eliminate or reduce risks. These adjustments can be accommodated by changing the funding, schedule, or technical requirements.

Discovering the truth behind operators’ minds is considered the most difficult component of risk management. This study’s trade credit tool can overcome this challenge. The operator types are manifested, and business operation strategies are determined. Thus, the hotel can engage effectively with agents who can bring additional profits. The hotel earns profits with mitigated financial risks by paying information rent to discourage operators with low tendency-to-pay from opting for payment default. Existing due diligence measures, such as enhancing the rating for quality, qualifications, or credit of an enterprise, can be applied as strategic supplements.

Strategic analysis

Our risk mitigation strategies are contingent on the business environment and enterprise characteristics and differ from ad hoc risk management practices. Members of the tourism channel can obtain the most profits by utilizing information through suggested tailored strategies.

International hotel chains often conduct businesses across various countries under heterogeneous business environments. Therefore, a single set of operational strategies may be unsuitable for application across all countries. Consequently, the influence of business conditions on the selection of strategies deserves further elaboration.

Proposition 5

A high bank rate results in high information rent, thereby diminishing the gap between the values of high- and low-type information to hotel profits. That is,

Proposition 5 implies that the cost of implementing an effective contract depends on the bank borrowing rate, which is generally a standard indicator in measuring economic prosperity. In terms of the changes in hotel profit, both loss in high-type operators and gain in low-type operators decrease in high bank rate cases. The value of high-type information to hotel profit is negative, whereas that of low-type information is positive. Therefore, the net effort of the hotel in extracting type information decreases when the bank rate is high. Our risk mitigation strategies require limited effort under good economic conditions. However, paying high costs in the case of low bank rates is suggested because the loss and gain of the hotel are not transferred completely to the operators. Low-type operators with a positive value of information to hotel profit should not be disregarded automatically. A good risk management strategy can ensure profitability, even in a risky environment, when information is revealed.

Proposition 6

A high tendency level of high-type operators (θh) leads to high values of information to tourism channel profit, that is,

Proposition 6 indicates that the profit of the entire tourism channel increases with a high tendency-to-pay (θh) when the proposed risk management strategies are implemented in a moderate business environment. Extreme pricing conditions, which are higher or lower than the two price boundaries, should be excluded because hotel losses are unlikely to be converted into channel profits. Therefore, engaging with operators with a high tendency-to-pay should be encouraged regardless of information rent losses. An increasing number of high-type operators may similarly lead everyone to have a positive risk attitude. Thus, a healthy business environment leads to profitability for all business participants.

Numerical illustration

This section demonstrates our recommended strategies for risk mitigation in the tourism industry. Our example is an international hotel chain that is about to enter an emerging market with an unregulated tourism industry. Most local tour operators in such a business environment are enthusiastic in developing business opportunities with this hotel chain. However, payment defaults may occur regardless of the operators’ claimed reputation. A credibility check on the local market can only provide a generic picture of the transaction history among existing operators or the estimated percentage of reliable operators, such as α = 0.7. That is, the estimated percentage of reliable operators is 70%.

The local credibility report covers all required information, which includes the average level of financial condition θh = USD80, average room price p = USD150, generalized capital cost rate c = 1.8%, bank rate φ = 1.7%, and goodwill penalty rate μ = 1.8%. Table 7 lists the numerical values of contracts based on the provided parameters and optimal contract solutions shown in Tables 3 and 5, respectively. For an ideal world where people only tell truth, the hotel offers high price and slightly low credit rate for the high types and low price/high rate for the low types. We assume the hotel prices USD133 per room on average. For a disguised world, the hotel scarifies its profit through offering a better deal to the high types, who are generally considered credible in paying back debts. The better deal will keep the high types sticking to an h-type contract and the low types away from such contract. When the wholesale price of an h-type contract is USD83, the profit then becomes USD97.

Numerical values of the optimal contracts.

Based on the situation of this hotel, its market resides only in regime (i) (i.e. when the bank rate is moderately related to financial costs) but not in regime (iii) (i.e. when the bank rate is low related to financial costs) because φ = 1.7%, and

The two retail price boundaries are USD264 and USD112 given the business environment provided in and based on Figure 4. The value of α that divides regimes (i) and (iii) is 0.37, and the minimum value of α to exercise the risk transfer strategy is 0.31. The lowest price to adopt the acceptance strategy in regime (i) is 206. For room price lower than USD206 and α > 0.37, the hotel should implement a risk transfer strategy that involves a third-party finance institution for this tourism company given the risk assessment in proposition 4 and the clearly known types of operators. Because the hotel shares part of its benefit to those agents who have incentive to disguise, the high information rent reduces the hotel’s profit and the high value of information increases the hotel’s profit. According to proposition 5, this hotel is in a situation, where

Discussion and conclusions

Tourism service providers rely heavily on intermediaries using a merchant model in selling their products and services to end customers. Because of the agency problems resulting from information asymmetry and conflict of interest, intermediaries tend to delay payment, thus leading to great risk of payment default for tourism service providers. Identifying and doing business with reliable intermediaries is critical for tourism service providers to obtain viable operating results.

Prior tourism research deals with the issue of payment default risk management mainly by predicting or accessing default risk through the use of various statistical models (Li et al., 2013); not much attention has been paid to other techniques, such as formal contracting. Although formal contracting is helpful in aligning the interests of both sides of the exchange partners (Gulati et al., 2005), rare research has noticed the importance of contracts in resolving tourism interfirm conflicts (Mwesiumo and Halpern, 2016). The current study contributes to the literature on default risk management in tourism by considering contract design as an effective approach enabling self-selection between low-risk and high-risk buyers, and consequently to deter the high-risk tour operators from doing business with hotels.

Through the lens of agency theory and mechanism design theory, this study extends the work of Yang et al. (2009) on supply disruption management in manufacturing to payment default management in tourism. In addition, agency problems are inherent in the relationships between tourism service providers and tour operators; however, this concept and associated approaches have not been adequately applied in tourism economics research (Song et al., 2012). The present study contributes to tourism economics by incorporating agency theory and information asymmetry in developing a useful tool for tourism service providers to manage the risk of payment default.

This study suggests that companies in the tourism industry should not persist in conducting business over-prudently, which may lead to unexpected losses because intermediaries may hide information from their creditors. Strategies are investigated for risk mitigation, thereby avoiding payment defaults when a tourism service provider trades with unfamiliar tour operators in tourism distribution channels. The key in performing effective risk mitigation is to induce tour operators to reveal the true intention to pay by offering a self-selection menu of contracts.

This study shows the effectiveness of a trade credit tool in managing the default risks in tourism research. We employ mechanism design theory and devise a contract menu to satisfy self-selection and thereby convince high- and low-type operators to opt to pay either immediately or later. Such contracts discourage tour operators from disguising themselves or opting to default on their payments for profitability. Thus, the hotel can evidently distinguish between the high- and low-type operators by observing their contract selection behaviors. Subsequently, the hotel can manage risks with acquired beneficial information on private financial conditions by following the risk mitigation strategies suggested in our study.

This study’s information-inductive risk mitigation strategies can effectively resolve equivocal risk values and complement conventional risk management. Risk sharing, liability transfer, liability sharing, and risk transfer strategies are recommended to tourism service providers when their businesses are situated in high-reward, high-risk toward low-reward, low-risk environments. The risk attitude to assume when engaging in business opportunities should be conservatism under a good economic condition and progressivism under a bad economic condition. However, the level of progressivism in a bad economy can be moderated if the business is situated in a low-risk environment. The net benefits surrendered by the hotel decrease when the bank rate is high. The profit of the entire tourism channel increases when the percentage or tendency-to-pay of reliable operators increases.

The current analysis can be extended from a single-period model to a multiple-period one, and the model can incorporate a reserve fund to cover unexpected financial incidents. Hotels can maintain business relationships with low-type operators until a first default occurs. Revenue losses are also partially compensated through the reserved fund. Other factors that may influence profitability, such as the economy and human behaviors, should be analyzed further in addition to the operators’ tendency-to-pay. The additional complexity in the uncertain returns of speculative investment can also be investigated. Lastly, risk management strategies associated with tourism intermediaries adopting an agency model could be explored in future research.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article:The authors acknowledge the funding support from Ministry of Science and Technology, Taiwan, ROC (Grant No. MOST 104-2410-H-327-018-MY3).