Abstract

The purpose of this study is to investigate the strategic value of advertising expenditures in the tourism and hospitality industry. Adopting a market-based valuation approach and longitudinal analysis, this study assesses the magnitude of advertising value by comparing the magnitude of the value with those from other expenses and book value. Results show that the economic benefits from advertising expenditures, unlike other expenses, don’t expire in the current period. Furthermore, advertising expenditures are significant strategic investments in intangible assets, providing greater future economic benefits than other assets. In addition, there is no significant heterogeneity regarding the effectiveness of advertising expenditures across subsectors in the tourism and hospitality industry.

Introduction

Marketing is under increasing pressure to demonstrate the value of its expenditures, especially advertising expenditures (Lodish and Mela, 2007). Chief Executive Officers and Chief Financial Officers know that marketing matters, but is skeptical of the magnitude of its influence and its contribution to corporate strategy from a long-term perspective (Stewart, 2009). Consequently, the marketing department is losing its strategic role within firms (Verhoef and Leeflang, 2009). Marketing is now perceived as tactical activities for which costs must be controlled, not strategic investments (Stewart, 2009). Under the current dominant accounting policy in the United States and all over the world, advertising expenditures are fully expensed in the same period incurred and cannot be capitalized. However, with the significant influence of social media and empowered consumers, the academic community in marketing calls for research attention to marketing as an integral part of the organization’s decision-making framework (Kumar, 2015). In 2015, the measured advertising expenditure of the tourism and hospitality industry in the United States was approximately $9.5 billion (Kantar Media, 2017). For example, Yum! Brands, McDonald’s Corporation, and The Walt Disney Company spent $792.8, $791.7, and $723.4 million dollars, respectively, on advertising in 2015 (RedBooks, 2017). Given the huge size, there is a need for the hospitality and tourism industry to demonstrate the contribution of advertising expenditures to firm value and the importance of marketing function to corporate strategy.

Mixed results about advertising value relevance have been reported, and a more detailed and industry-wise analysis of firms’ advertising value relevance has been suggested as an avenue for future research (Ali Shah and Akbar, 2008). Within the context of the tourism and hospitality research, most previous studies typically relate advertising expenditures to sales and accounting profitability (Assaf et al., 2015; Denizci and Li, 2009; Herrington and Bosworth, 2016; Kamal and Wilcox, 2014; Park and Jang, 2012). However, there has been mixed evidence in support of advertising effectiveness, which can be explained by several drawbacks of linking advertising to sales and accounting profitability (Grabowski and Mueller, 1978; Heflebower and Telser, 1969; Hirschey, 1982). Additionally, prior studies consistently support the link between advertising expenditures and firm market value for restaurant firms (Denizci and Li, 2009; Hsu and Jang, 2008; Park and Jang, 2012), and recent emerging research explores the impact of franchising on advertising effectiveness for restaurant and hotel firms (Park and Jang, 2016). However, systematic comparisons across firm investments and subsectors have been largely neglected. To further investigate the strategic value of advertising investment decisions in the tourism and hospitality industry, there is a need to answer two questions: How relevant is advertising investment for a company’s success compared with other investment alternatives in the tourism and hospitality industry? How does advertising relevance differ across subsectors within the tourism and hospitality industry?

Therefore, using financial data from Compustat, this study aims to compare the importance of advertising expenditures with other investment alternatives in tourism and hospitality and to explore the differences in advertising value relevance across subsectors within tourism and hospitality.

This study contributes to the literature in several ways. First, this study extends the understanding of advertising effectiveness and brand equity in tourism and hospitality, by investigating a prior neglected role of advertising expenditures, the strategic value of advertising in the broad picture of equity evaluation. This study proposes that tourism and hospitality advertising provides greater future economic benefits than the average return of other assets. Second, this study takes an initial attempt to test the subsector differences in advertising effectiveness within the tourism and hospitality industry. The tourism and hospitality industry consists of a diverse group of subsectors, which create substantial issues in discipline integrity. This study proposes that advertising relevance varies between the tourism and hospitality industry and other industries, but does not vary across the subsectors within the tourism and hospitality industry. Third, this study contributes to the deflator selection literature, by including the scale proxy as an independent variable.

In the following section, this research evaluated three different approaches of advertising effectiveness in general accounting, finance, and marketing literature, as well as in tourism and hospitality literature. After a comprehensive evaluation, the market-based approach was selected for this study. In addition, this research used advanced longitudinal techniques, which could account for correlations among repeated measures and reduce problems associated with omitted variable bias. The magnitude of advertising value within the context of equity valuation was investigated by comparisons with value of other expenses and value of net assets. The subsector differences were then tested by utilizing a larger panel data, which included yearly observations data from multiple firms of three different subsectors in the tourism and hospitality industry.

Literature review

There are generally three different approaches to investigating the effectiveness of advertising expenditures: advertising and sales approach, advertising and profitability approach, and advertising and market value approach.

Advertising and sales approach

Linking advertising expenditures with sales is a typical starting point to assess the effectiveness of advertising. Systematic relationship cannot be consistently found, and results of previous studies vary by industry or subindustry. Building on the Koyck distributed lag model, Abdel Khalik (1975) found significant distributed lag effects in the food, drugs, and cosmetics industry, but not in the tobacco or the soap and cleansers industry. Consequently, different accounting treatments are recommended in different industries, rather than a uniform accounting policy. Based on a cointegration analysis, Elliott (2001) found that there is a long-run equilibrium relationship between advertising expenditures and sales for the food industry, but not for the more specific soft drinks industry. The industry difference of advertising effects was explained by the fact that the cointegrating relationship between advertising and sales is more likely to exist when demand saturation in that industry has not been reached. Based on a marketing-persistence model, Zhou et al. (2003) suggested the long-lasting television advertising effects on sales existed for consumer durables, but not for consumer nondurables. The reason may be that purchasing consumer durables is a high-involvement decision, which contains more purchasing risks and needs more information search efforts. Based on the statement from Vaughn (1980) that the involvement level affects receptivity to advertising, Zhou et al. (2003) concluded that purchasing durables requires more thinking process, has long-term memory effects, and builds stronger brand preference.

In tourism and hospitality subsectors and related industries, mixed results have been reported using the advertising and sales approach. While some prior studies found no effects of advertising expenditures on sales, other studies reported short-term or long-term effects on sales. From the demand perspective, Duffy (1999) found no effect of advertising expenditures on inter-product distribution of food consumption over the period from 1969 to 1996 in the UK food sector. Herrington and Bosworth (2016) found that there was a lack of relationship between advertising and sales for restaurant chains from 1984 to 2008. However, Simon (1969) found a long-run effect of advertising on sales for 15 of the largest selling liquor brands in the United States from 1953 to 1962. Kamal and Wilcox (2014) found a positive relationship between advertising expenditures and sales of quick-service restaurants from 1986 to 2007 but the impacts small. Furthermore, Park and Jang (2012) found that advertising expenditures had a positive short-term effect on sales growth for the restaurant industry from 1995 to 2008. Finally, Assaf et al. (2015) found that advertising spending has a positive impact on sales performance measured by the dynamic stochastic frontier approach for a sample of Slovenian and Croatian hotels from 2007 to 2012.

However, the advertising and sales approach is plagued with several issues. The Koyck distributed lag model, measuring distributed lag effects of advertising on sales, is a popular way to investigate the magnitude of the advertising effectiveness (Abdel Khalik, 1975; Clarke, 1976; Koyck, 1954). However, the distributed lag approach is inappropriate in studying advertising effectiveness due to high multicollinearity between current and past advertising expenditures (Hirschey, 1982; Picconi, 1977). In addition, there is a potential omitted variable problem in previous studies. Landes and Rosenfield (1994) found that many existing economic models failed to control for other firm-specific factors, which could bias the results significantly. Furthermore, the directions of casual relationship are not clear, because the causality may run in both directions: advertising may affect sales because advertising influences consumers’ preference, and sales may also affect advertising because many firms set their advertising budget based on certain percentage of sales (Herrington and Bosworth, 2016; Lee et al., 1996).

Advertising and accounting profitability approach

Rather than just focusing on sales, Hirschey (1982) argues that a firm’s overall objective in advertising is profit, including increasing sales as well as reducing costs. Specifically, product advertising moves the potential customers through a hierarchy of stages towards a final purchase decision, which is directed toward sales. While institutional advertising deals with broader stakeholders, it is related to both increasing sales and reducing costs. As a result, the advertising and accounting profitability approach has been suggested as a more comprehensive method than the advertising and sales approach.

However, mixed results have been reported in terms of the relationship between advertising expenditures and accounting profitability. Erickson and Jacobson (1992) found no evidence that advertising expenditures can generate supernormal accounting profits, but Graham and Frankenberger (2000) found advertising expenditures contribute to earnings for more than 1 year. In the tourism and hospitality industry, Denizci and Li (2009) found no significant relationship between advertising expenditures and accounting profitability ratios including return on equity, return on assets, and profit margin for 17 large tourism and hospitality firms.

The mixed results can be explained by several drawbacks of this approach, including unadjusted accounting profitability measures and simultaneity causality problem. Before analyzing the determinants of profitability and especially the effect of advertising expenditures on profit rates, the profit rates as the dependent variable must be adjusted (Grabowski and Mueller, 1978). Corrected profit measures should be constructed because the profit measures under the current accounting treatment fail to incorporate the value of firm investments in intangible capitals such as advertising expenditures. The current accounting treatment tends to depreciate tangible assets, while expensing intangible assets, which leads to measurement error of the accounting profit measures, such as net profit, return on equity, return on assets, and profit margin. The problem of the accounting bias is particularly severe if the research objective is the role of intangible capitals such as advertising expenditures in explaining variation of profit rates. As a result, the problem of using unadjusted profits leads to systematic bias in regression analysis (Heflebower and Telser, 1969). Furthermore, there is the simultaneous problem of causation between advertising expenditures and profitability. Advertising expenditures can benefit a firm’s profitability by differentiating the firm’s products from competitors, while a firm’s internal funding such as profitability is crucial for determining and financing advertising expenditures (Erickson and Jacobson, 1992).

Advertising and market value approach

In order to avoid the problems in associating advertising expenditures with sales or profitability, a better alternative is the market-based valuation approach (Ali Shah and Akbar, 2008). Based on the efficient market hypothesis (Malkiel and Fama, 1970), the market-based valuation approach believes that firm’s market value is “the present value of all expected cash flows from a firm’s assets and, at any given time, reflects all the available information about a firm’s current and future profit potential” (Agrawal and Kamakura, 1995: 57). Both tangible and intangible factors that have systematic influences on profitability can be captured by a firm’s market value (Hirschey and Wichern, 1984). A firm’s market value can be considered as a firm’s economic profit based on market participants’ valuation of firm stock. Instead of the accounting profit, firm’s market value is a more accurate dependent variable that can minimize the measurement error due to accounting bias. Furthermore, there is potential for advertising expenditures to affect both current and future profitability, and firm market value as a future-oriented measure of profitability can capture both the current and future profitability effects of advertising (Ali Shah and Akbar, 2008).

A typical market-based valuation analysis uses the regression model to investigate the relationship between advertising expenditures and firm market value. While the independent variables in the model vary from study to study due to different theoretical frameworks, the dependent variable is often either the firm’s market value based on stock price or firm’s market value deflated by some scale variables. For example, firm’s sales data have been used as deflator to reduce heteroscedasticity (Han and Manry, 2004). In addition, book value was more often used as deflator in valuation studies (Hirschey, 1982; Hirschey and Weygandt, 1985). Tobin’s q, defined as the ratio of market value to replacement costs of its assets by Tobin (1969), is one typical example of using book value as deflator of firm’s market value and is often used in tourism and hospitality valuation studies (Denizci and Li, 2009; Hsu and Jang, 2008; Park and Jang, 2012). However, the choice of deflator is concluded to be one factor that contributes to the inconsistent results of previous studies (Ali Shah and Akbar, 2008; Agnes Cheng and Chen, 1997). The underlying reason is that selecting a different deflator means hypothesizing different linear relationship between variables. The advantage of the theoretical framework of this study is that it avoids the problem associated with deflator selection. Book value and sales are both included as independent variables based on this study’s theoretical framework, which is a more effective way than deflating regression variables by a scale proxy at mitigating coefficient bias (Barth and Kallapur, 1996). Based on a widely accepted valuation theory developed by Ohlson (1995) and the following market-based valuation model developed by Han and Manry (2004), this study developed three research hypotheses within the tourism and hospitality industry.

Using advertising and market value approach, Hirschey (1982) found that current advertising expenditures have significant and positive influences on the firm’s market value, suggesting significant future effects (intangible capital) of advertising. Following Hirschey (1982), the positive effect of advertising on the firm’s market value was confirmed, using a slightly different approach by regressing Tobin’s q on advertising intensity, research and development intensity, and control variables (Hirschey and Weygandt, 1985). Graham and Frankenberger (2000) also confirmed the positive association between advertising expenditures and firm’s market value, based on the equality of a firm’s marketing value and the market value of its net assets (Tobin, 1978). However, Han and Manry (2004) found a negative association between advertising expenditures and stock price, which may result from deflator choice or context difference. In the tourism and hospitality industry, Hsu and Jang (2008) found a positive relationship between current year’s advertising intensity and intangible value of restaurant firms measured by Tobin’s q. Following Hsu and Jang (2008), Park and Jang (2012) found that advertising intensity had both positive short-term and long-terms effects on Tobin’s q in the restaurant industry. Denizci and Li (2009) also found that advertising expenditures are significantly associated with Tobin’s q. Finally, Assaf et al. (2017) found that advertising has a positive impact on market value added for restaurant and hotel segments. In sum, previous studies support the asset value of advertising expenditures on firms’ market values in the tourism and hospitality industry (Assaf et al., 2017; Denizci and Li, 2009; Hsu and Jang, 2008; Park and Jang, 2012). From an accounting perspective, if the nature of advertising expenditures is short-lived expenses, advertising can only benefit the current accounting period and the effects quickly decline, and should be expensed when incurred. If the nature of advertising expenditures is long-lived assets, the advertising expenditures will benefit beyond the current accounting period in which the expenditure is incurred, and should be capitalized and amortized over time (Sorter and Horngren, 1962). Accordingly, research hypothesis 1 suggests that the influence of advertising expenditures on firm market value is higher than the influence of other expenses. This indicates that the advertising expenditures don’t expire totally in the current year like other expenses; instead, they may have future economic benefits for the firm’s market value, which is the core characteristic of assets.

In addition, recent literature empirically shows that the overall importance of brands for consumer decision-making differs substantially across types of goods due to the differences in risk reduction and social demonstrance (Fischer et al., 2010). Advertising expenditure is a key element of marketing spending and the major contributor of brand equity (McAlister et al., 2016). According to information economics theory, consumer’s ability to assess product quality prior to purchase varies fundamentally across types of goods, and the guidance they need is higher for experience goods than search goods (Nelson, 1970). Producers of experience goods advertise significantly more than producers of search goods, because advertising for experience goods increases sales by increasing the reputability of brands (Nelson, 1974).

Advertising expenditures are more important for nonmanufacturing firms than manufacturing firms that have tangible products or technologies that contribute to the firm value (Ho et al., 2005). Compared with goods products, services products rely more heavily on advertising to deliver tangible and differentiating information about the attributes and benefits of the services to the market and to build brand value (Pickett et al., 2001). Furthermore, as the tourism and hospitality industry provides hedonic services, it has significantly higher advertising effectiveness on consumer response than utilitarian services such as banking and insurance due to different cognitive processes and greater need to justify hedonic purchases (Décaudin and Lacoste, 2018; Kivetz and Zheng, 2017; Stafford and Day, 1995). At the aggregated firm level, firms with a strong marketing’s influence are more market oriented and have better performance (Verhoef and Leeflang, 2009). Specifically, advertising has a double positive impact on firm value, through increasing sales and profits and building brand assets (Joshi and Hanssens, 2010). Based on the information economics theory and previous findings, we propose the strategic value of advertising expenditures on firm market value in the tourism and hospitality industry. Accordingly, research hypothesis 2 suggests that the influence on firm market value of advertising expenditures is higher than the influence of book value. This indicates that advertising expenditures lead to higher firm market value than the average return of firm value from firm net assets.

Prior advertising effectiveness research mainly focuses on specific subsectors within the tourism and hospitality industry, yet the big picture of the umbrella industry is understudied. Tourism and hospitality is categorized as a service industry, providing consumers with an experience as their core product (e.g., a good night’s rest, safe transportation, a nice dining experience, etc.). The product offered by the tourism and hospitality industry, being intangible by nature, is typically abstract, perishable, mentally impalpable, non-searchable, inseparable, non-standard, and non-owned (Lovelock and Gummesson, 2004; Mittal and Baker, 2002). Based on the contingency theory, the effect of firm’s actions such as advertising on firm performance is moderated by characteristics of the firm and its marketplace (Srinivasan et al., 2011; Zeithaml et al., 1988). As a result, research hypothesis 3 is to test whether there is heterogeneity among subsectors in the tourism and hospitality industry regarding the effectiveness of advertising expenditures.

Methodology

Data

The purpose of this study was to examine the effect of advertising expenditures on firms’ market values in the tourism and hospitality industry. From a statistically representative perspective, airlines, hotels, and restaurants, identified using US Standard Industrial Classification (SIC) codes, were included in the tourism and hospitality industry. SIC 4512 represents airlines, SIC 5812 represents restaurants, and SIC 7011 represents hotels (see Table 1). Yearly financial data of public companies, from 2005 to 2014, in North America were retrieved from the Compustat database. As a result, 226 companies were identified. To make data comparable, December fiscal year-ends were used as a screening variable and 192 firms remained in the final sample. As a result, 10-year financial data of 192 firms were collected for the 2005–2014 period. All continuous variables were measured using millions of dollars. 1

Example of firms in the tourism and hospitality industry.

Proposed models and variables

The study employed longitudinal analysis to examine the value relevance of advertising expenditures on firms’ market values. The defining feature of longitudinal analysis is that the same individuals are measured repeatedly at different times. “With repeated measures on individuals, one can capture within-individual change. Indeed, the assessment of within-subject changes in the response over time can only be achieved within a longitudinal study design” (Fitzmaurice et al., 2011: 2). Longitudinal analysis is the direct study of change over time, which characterizes the change in response over time and the factors that influence change.

The distinguishing advantages of using longitudinal analysis are that it takes account of the correlation among repeated measures, thereby resulting in more accurate inferences (Fitzmaurice et al., 2011). The statistical models for cross-sectional data cannot be used directly in longitudinal data due to the violation of the assumption of independence. The longitudinal data are clustered, there is dependence among within individual measures, and repeated measures made on the same subject are correlated. Within the context of this study, observations from different firms are independent, while repeated measurements on the same firm are not independent. Yearly observations within firms tend to be more similar than yearly observations from different firms. Yearly observations closer in time tend to be more similar than yearly observations farther apart. Ignoring the correlation among yearly observations of firms will result in biased estimates.

In addition, longitudinal analysis can to a large extent reduce problems of omitted variable bias, thereby leading to more precise estimates. The beauty of a longitudinal study design is that any extraneous factors (regardless of whether they have been measured) that influence the response, and whose influence persists but remains relatively stable throughout the duration of the study (e.g., gender, socioeconomic status, and many genetic, environmental, social, and behavioral factors), are eliminated or blocked out when an individual’s responses are compared at two or more occasions. (Fitzmaurice et al., 2011: 21)

This study also adopted the market-based valuation approach by associating advertising expenditures with firms’ market values. Market-based valuation model was viewed as a better alternative than relating advertising expenditures to firm sales or accounting profitability for its several advantages discussed before. This study applied the Han and Manry (2004) framework into the context of tourism and hospitality and added subindustry as a new categorical independent variable in the marginal model. The underlying rationale was to investigate and control the influence of different subsectors within the tourism and hospitality industry. In addition, the measures of the Han and Manry’s (2004) model were improved to reduce problems associated with deflator selection bias. Furthermore, research and development expenditures are not included in the model as little research and development activity takes place in most consumer service industries (Howells, 2000). The basic marginal model is proposed below:

where ekit is correlated within firms, suggesting that repeated measurements from the same firm are not assumed to be independent. Pkit is in sub-sector k the firm i’s market value of common stock 3 months after the end of year t. Dkit is cash dividends in year t. YEAR t is the yearly intercept to vary yearly over the test period in order to capture the business cycle. BV kit is the book value of net assets before cash dividends at the end of year t. SALE kit is the net sales in year t. OEXP kit is other expenses in year t. ADEXP kit is advertising expenditures in year t. Pkit and Dkit were added together to form one dependent variable, which is continuous. BV kit , SALE kit , OEXP kit , and ADEXP kit are continuous independent variables, while YEAR t and SIC k are categorical independent variables.

In order to investigate the influence of subsector differences on the advertising effectiveness within the tourism and hospitality industry, the possible heterogeneous slopes of advertising expenditures were tested by adding the interaction of SIC k and ADEXP kit into the previous marginal model as a fixed effect. The marginal model with interaction was proposed below:

Furthermore, in order to account for the heterogeneity among firms in different subsectors, SIC was included as a random effect in a three-level model and a random slope of ADEXP kit was included to vary across the subindustries level. As a result, in addition to the marginal models, this study also proposed the following multilevel random effect model:

The proposed research hypotheses can also be expressed mathematically. Research hypotheses 1 and 2 were tested in the basic marginal model (model 1). H1 suggests that the coefficient of advertising expenditures is higher than the coefficient of other expenses in model 1. Furthermore, H2 suggests that the coefficient of advertising expenditures is higher than the coefficient of book value in model 1. Research hypothesis 3 was tested in the marginal model with interaction (model 2) and the multilevel random effect model (model 3). In model 2, research hypothesis 3 suggests that the coefficient of the interaction of advertising expenditures and SIC is different from 0. Furthermore, in model 3, H3 suggests that the variance of the random slope of advertising expenditures in the subsector level is different from 0.

In terms of the measures of the variables, BV kit , SALE kit , OEXP kit , ADEXP kit , and Dkit come from annual company data, while Pkit comes from quarterly company data (see Table 2). The 3-month delay of Pkit’s measure allowed the market to deal with the release of the information (Han and Manry, 2004). OEXP kit was measured by subtracting advertising expenditures from all the expenses in earnings before extraordinary items. The sum of Pkit and Dkit was used as the dependent variable Y in this study.

Measures of variables.

Data were screened before analyses. Both a marginal model and a three-level random effect model were used in this study. Specifically, three different marginal models with different correlation matrix assumptions were tried and compared. A three-level model with random effects was then employed.

Results

Screening data

Data were screened prior to parametric testing. In regard to missing data, list-wise deletion was used in this study, because the distribution of missing data in the sample suggested that the type of missing data was missing completely at random. As a result, 102 firms and 545 yearly observations remained in the sample. The normality assumption was violated based on quantile plot of residuals. Natural logarithmic transformation was applied to the dependent variable Y to reduce the kurtosis and skewness to acceptable levels.

Marginal model

With the cleaned data, a marginal model was employed. Based on the comparison of Akaike information criterion (AIC) and Bayesian information criterion (BIC) among different models with different correlation matrix assumptions, the model using an first-order autoregressive (AR [1]) correlation matrix assumption was preferred. This correlation matrix assumption also met the reality because when the yearly observations got closer, the correlation got larger. Based on type 3 tests of the AR (1) model, YEAR, BV, SALE, OEXP, ADEXP, and SIC were all statistically significant at the 0.05 significance level.

Table 3 shows the coefficient estimates obtained. YEAR was significant across all 10 years except for year 2006 (p = 0.1071). In terms of SIC, the influence of airline subsector on firm market value was not significantly different from the influence of hotel subsector (p = 0.6999), and restaurant didn’t have a significant difference on firm market value from hotel subsector (p = 0.0812). Book value and other expenses had a significantly positive influence on firm market value (for book value, β = 0.0002, p < 0.0001; for other expenses, β = 0.000116, p = 0.0006). Sales significantly affected firm value, but the magnitude of the influence was very small (β = −0.00008, p = 0.0416). Advertising expenditures had a positive influence on firm market value, and the magnitude of the influence was very large compared to other factors (β = 0.004189, p < 0.0013).

Coefficient estimates in AR (1) model.

Note: DF: degrees of freedom; SE: standard error.

F test was employed for the hypothesized comparisons of certain coefficient estimates. 2 The coefficient estimate of advertising expenditures was significantly larger than that of other expenses (p = 0.0018, see Table 4). Furthermore, the coefficient estimate of advertising expenditures was significantly larger than that of book value (p = 0.0023).

Contrast results.

Note: Num DF: degrees of freedom of the numerator; Den DF: degrees of freedom of the denominator.

In order to understand the subsector difference on the influence of advertising expenditures on firm market value, the interaction of SIC and ADEXP was added into the previous marginal model as a fixed effect to test heterogeneous slopes. Based on the p value of Type 3 tests of fixed effects, the interaction variable was not statistically significant (p = 0.5318). In addition, the model fit statistics AIC and BIC were increased by adding the interaction (AIC: from 1190.6 to 1207; BIC: from 1196.3 to 1212.6), suggesting model fit was not improved and there was no need to add the interaction. As a result, there was insufficient evidence that the slopes of advertising expenditures differed significantly among subsectors in the marginal model.

Three-level random effect model

An alternative approach to test possible heterogeneous slopes was to include the variable ADEXP as random slope at the subsector level in a three-level random effect model, which could account for the heterogeneity among firms in different subsectors. A three-level random effect model was used in the following study: level 1 was yearly observations, level 2 was firms, and level 3 was subsectors. A random slope of ADEXP was added into the subsector level, allowing the relationship between the predictor ADEXP and the outcome Y to vary across subsectors. The results of fixed effects section were similar to the previous marginal model.

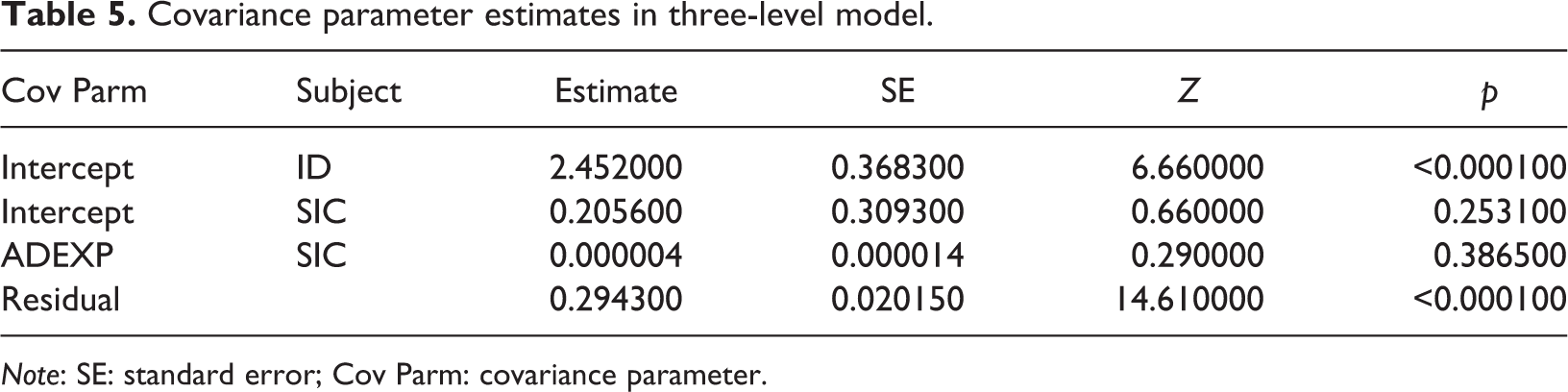

Examining the random effect section, there was significant variability in between-firm level and within-firm level, not in between subsector level. In terms of the three levels, 83% of the variation in firm value was significantly explained by between-firms’ variability (p < 0.0001, see Table 5). On the contrary, 7% of the variation in firm value was explained by subsector variability, but it was not significant (p = 0.2531). Approximately, 10% of the variation in firm value was significantly explained by within-firms’ variability (p < 0.0001). As a result, individual variability had a larger and more consistent contribution to the firm value variance than subsector variability. The random slope of ADEXP was not statistically significant based on the p value for the estimated variance components (p = 0.3865). In addition, the model fit AIC and BIC were not improved when the random slope was added to the three-level random effect model. Thus, the association between ADEXP and Y didn’t vary significantly among subsectors.

Covariance parameter estimates in three-level model.

Note: SE: standard error; Cov Parm: covariance parameter.

Discussion and conclusion

This study investigated the economic effects of advertising expenditures on firms’ market values in the tourism and hospitality industry. Market-based valuation approach and longitudinal analysis were selected as robust theoretical framework and methodological model. The findings of this study indicated that advertising expenditures in the tourism and hospitality industry have strategic asset value captured by the market participants. This suggests that tourism and hospitality advertising provides greater future economic benefits than the average return of net assets. In addition, there is no significant heterogeneity among different subsectors in the tourism and hospitality industry regarding the advertising’s effectiveness.

Within tourism and hospitality context, the economic benefits from advertising expenditures didn’t expire fully in the current period, unlike other expenses. Results showed that advertising expenditures had a larger positive impact on firm market value than other expenses. Controlling other variables as constant, a $1-million increase in advertising expenditures would lead to an approximate 0.4198% increase in firm market value. On the contrary, controlling other variables as constant, a $1-million increase in other expenses would lead to a 0.0116% increase in firm market value. This large difference in magnitude indicated that advertising expenditures should not be fully expensed and may have some future economic benefits, like assets. This finding is consistent with the previous results of advertising asset value using marketing-based valuation approach (Denizci and Li, 2009; Hsu and Jang, 2008; Park and Jang, 2012).

Furthermore, firm market value priced advertising expenditures significantly higher than other assets in the tourism and hospitality industry. Results showed that advertising expenditures had a larger positive impact on firm market value than book value. Keeping other variables constant, a $1-million increase in advertising expenditures would lead to an approximate 0.4198% increase in firm market value. On the contrary, controlling other variables as constant, a $1-million increase in book value would only lead to a 0.02% increase in firm market value. This magnitude comparison indicated that the future economic benefits from advertising expenditures were expected to be significantly higher than a normal return from ordinary net assets. This finding provides new insights regarding the magnitude of advertising value in the tourism and hospitality industry. Advertising expenditures brings significantly numerous benefits to firms in the tourism and hospitality industry and should be valued as strategic investments in intangible assets in this industry.

Interestingly, the findings are inconsistent with Han and Manry’s conclusion about short-lived nature of advertising expenditures, indicating that advertising effectiveness differs between tourism and hospitality industry and other industries. In addition, in terms of research hypothesis 3, there is insufficient evidence that there is heterogeneity regarding the effectiveness of advertising expenditures across subsectors in the tourism and hospitality industry. In sum, advertising effectiveness is sensitive to between-industry difference, but is not sensitive to subsectors difference within the tourism and hospitality industry.

This study contributes to the literature in several ways. First, this research extends previous findings on advertising effectiveness in the tourism and hospitality industry. Tourism and hospitality advertising expenditures not only positively contribute to firm market value but also have the strategic value compared with the average return of net assets. Inconsistent with the perception of marketing’s declining position in manufacturing industries (Auh and Merlo, 2012), our results suggest that marketing should be considered as board-level strategic investments in service firms. In addition, marketing department in service firms should be viewed as a strategic function relative to other business functions, rather than as a cost center with a declining functional position. Second, this study is one of the few exploratory studies, which empirically tests the sub-sectors’ differences in the tourism and hospitality industry. Advertising effectiveness in the tourism and hospitality is sensitive to between-industry difference, but is not sensitive to within-industry difference. Therefore, although the dichotomy between services and goods marketing is blurred under the emerging paradigm of service-dominant logic (Baron et al., 2014), this study suggests that services marketing is different from goods marketing in terms of marketing relevance, specifically marketing’s strategic dimensions. Third, this study contributes to the deflator selection literature by including sales and book value as independent variables in the model.

This study has financial management implications for firms in the tourism and hospitality industry. The strategic value of advertising significantly justifies the power of advertising expenditures and the role of marketing department within tourism and hospitality firms. Advertising managers in the tourism and hospitality industry receive empirical supports from this study to invest money in advertising media and promotional expenditures in order to deliver value to the market. Furthermore, this study indicates that advertising expenditures in the tourism and hospitality industry can bring considerable future benefits to firms, indicating that the effects of advertising are lasting and advertising of firms will not be forgotten by the market participants from a forward-looking perspective. Tourism and hospitality marketers should play a more strategic role within the firms instead of tactical decisions and focus on developing long-term customer relationships and brand equity rather than short-term transactions. Financial managers who temporarily face cash constraints can reduce advertising of the current year without any major impacts until the future.

In terms of practical accounting policy implication, this study provided empirical evidence in the tourism and hospitality industry as a whole to answer the accounting policy question of whether to capitalize or expense advertising expenditures from a market value perspective. The current simplified accounting policy implies that advertising expenditures are only value relevant to the financial performance in the current year, and they do not have long-term effects on firm market value. However, this research suggested that the accounting policy treat advertising expenditures in the tourism and hospitality industry as intangible assets to be amortized over their useful lives. Advertising expenditures in the tourism and hospitality industry should be treated as strategic investments and long-lived assets rather than current period expenditures and short-lived expenses. The findings from this study are expected to lead to improvements in the quality of financial statements and provide the impetus for making more informed strategic decisions within the tourism and hospitality industry.

Despite the theoretical and practical contributions, there are some limitations in this study which may provide directions for future research. The data were limited within accounting and financial context. Specifically, the sample was limited to publicly traded firms, and the advertising expenditures were only measured by accounting records, which may ignore other information. Future research could explore broader data sources beyond the accounting and financial system. In addition, this study is limited to the tourism and hospitality industry, and therefore the strategic value of advertising expenditures may not be generalized to other industries. Future research may apply this research design into other industry settings and explore more empirical findings. Furthermore, estimating an amortization rate of advertising assets for the tourism and hospitality industry will be another area of future research. From a statistical perspective, the negative relationship between sales and firm value may indicate multicollinearity problems, and more advanced statistics dealing with multicollinearity of panel data could be explored in future research. Last but not the least, this study only assumes multiplicative scale effect. Diagnosing other types of scale effect could also be explored in future research.

Supplemental material

Supplementary_File-AD-5-17-18 - The strategic value of advertising expenditures in the tourism and hospitality industry

Supplementary_File-AD-5-17-18 for The strategic value of advertising expenditures in the tourism and hospitality industry by Rui Qi, David A Cárdenas, Xichen Mou, and Simon Hudson in Tourism Economics

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.