Abstract

This article provides new evidence on the stability of the long-run income elasticity of tourism and travel demand by use of the recently developed smooth time-varying cointegration regression model. The estimations control for relative purchasing power parity of the source country and make use of a specific country dataset where domestic and foreign overnight stays are available over a longer period of time (Switzerland, 1934–2015). Results show that the income elasticity of foreign overnight stays peaks at approximately two in the early 1960s, drops to around one in the early 1980s and from then on remains stable until the end of the sample. Domestic income elasticity reaches its highest levels in the 1930s, then steadily falls towards one in the mid-1960s, and therefrom remains stable until 2015. Different phases in the tourism area life cycle might be a major explanatory factor for variation in income elasticities over time.

Keywords

Introduction

There is an ongoing discussion about the stability of the aggregate income elasticity in research on tourism and travel demand (Smeral, 2012, 2017b; Smeral and Song, 2015). These studies show that income elasticities vary considerably in the short and medium run and especially in terms of the business cycle. A recent meta-analysis documents that income elasticity exhibits a high degree of variation over the past 50 years (Peng et al., 2015), where also the point in time of the study seems to be an aspect of importance. The average income elasticity of tourism and travel demand is higher in more recent studies.

The aim of this article is to test the stability of the long-run income elasticity of tourism demand, measured as overnight stays, using the recently developed time-varying cointegration (TVC) model (Bierens and Martins, 2010; Neto, 2012). This model makes it possible to account for possible structural changes (Neto, 2014) and thus complements standard methods of time-varying models such as the recursive coefficient, subsample regressions or Kalman filter approaches. One advantage of the method is that it works without additional unit-root or cointegration tests for the different subsamples. Another benefit of the model is that the starting sample does not need a minimum number of observations, unlike the recursive method. Data at hand for the analysis include domestic and foreign overnight stays in Switzerland for the period 1934–2015. Switzerland is chosen for the application of the model because of its long experience of collecting accommodation data. Besides real GDP per capita of the visitor countries, the tourism and travel demand model also accounts for relative bilateral purchasing power parity (PPP). To account for different structures of tourism, the robustness of the results are controlled by separate treatment of the largest Swiss city (Zürich), with a high degree of business travellers and cultural tourists. The Swiss tourism and travel industry exhibits different phases of demand, from the strong period of growth after the 1950s until a stagnating phase from the 1990s.

The main contribution of this study is the use of the TVC model to investigate the long-run stability of both foreign and domestic income elasticities of tourism demand for a specific country, measured as the number of overnight stays. This is in contrast to previous studies, which focus on the behaviour of income elasticity during different stages of the business cycle or on the medium and short-run. The long-term approach also allows the investigation of how the income elasticity varies across different stages of the tourism area life cycle. To the best of the author’s knowledge, the smooth TVC model has so far not been utilized in tourism research.

The article is structured as follows. The second section introduces the conceptual background while the third section presents the empirical approach with the TVC model. The fourth section contains the data and descriptive statistics. The fifth section presents empirical results and the sixth section concludes.

Conceptual background

Analysing the time-varying relationships in tourism demand is becoming increasingly popular (Falk and Lin, 2018; Gunter and Smeral, 2016; Pérez-Rodríguez et al., 2015; Ramos et al., 2017; Smeral, 2012, 2017a, 2017b; Smeral and Song, 2015; Song and Wong, 2003). These studies commonly stretch over a period of 30–40 years and employ either the rolling regression technique (Tang and Abosedra, 2016) or the recursive regression analysis on annual data (Falk and Lin, 2018; Tang and Tan, 2013). However, a drawback with these approaches is the requirement of sufficiently large initial subsamples. Often, this means that the time span is not long enough to allow for testing of structural breaks in the cointegrating relationship. Because of this, several studies use the Kalman filter method applied to the error correction model or to a first difference specification (Li et al., 2006; Riddington, 1999; Smeral and Song, 2015; Song and Wong, 2003), but with contradicting results. Li et al. (2006) experience that the Kalman filte improves the accuracy of the forecast, while Smeral and Song (2015) discover that the same model has poor forecast precision. Presumably, this is because the Kalman filter only allows the short-run parameters to vary over time while the long-run parameters are fixed. Thus, the time-varying Kalman filter method is not expected to fully account for the possibility of a TVC relationship. Song et al. (2011) combine the time-varying parameter (TVP) regression model with structural time series model and show that this model outperforms other TVP models. However, it is not clear if the model can be applied to non-stationary variables. Koop et al. (2011) manage to deal with non-stationary variables by use of a Bayesian estimator and a state-space framework. There are also studies that use a first difference specification combined with dummy variables for different sub-periods in order to test for instability of coefficients (Gunter and Smeral, 2017; Smeral, 2017b), although this still only allows the short-run variation in the relationships to be tested.

In absence of data for longer periods of time, panel data models are possible alternatives. However, studies based on panel data models often neglect or cannot identify the time series properties of the data. As shown by Entorf (1997), standard panel data approaches such as the fixed effects model may lead to spurious results if non-stationary variables are not cointegrated. In addition, the risk of a spurious relationship in a panel data regression is likely to be higher than for the pure time series case (Entorf, 1997; Kao, 1999). In this study, the TVC model is used to test the long-run stability of income elasticity of tourism demand. This model is expected to manage better structural changes and non-stationary data than the approaches discussed above.

Just like the variation in approaches used, there is also a lack of consistency in results from the different studies on the income elasticity of tourism demand possibly implying that the choice of model drives the results. One strand of the literature investigates how income elasticities evolve across different phases of the business cycle (Gunter and Smeral, 2017; Smeral, 2012, 2017b; Smeral and Song, 2015). This literature finds an asymmetric pattern, which means that the income elasticity differs between phases of slow and fast GDP growth. For instance, Smeral and Song (2015) show for the EU-15 countries that the income elasticity is lower in slow growth than in high growth periods. Few studies investigate the stability of the income elasticity over a longer time period. An exception to this is Gunter and Smeral (2016), who demonstrate that the elasticities are falling during the period 1977–2013, starting at values of two and reaching values below one in the most recent period.

Previous studies for Switzerland show income elasticities of approximately two for both domestic and US visitors, while income is insignificant for travellers from European countries (Ferro-Luzzi and Flückiger, 2003). Marvel and Johnson (1997) suggest that the sensitivity of demand for Swiss hotel accommodations to real income is highest for domestic visitors and generally lower for foreign visitors. Other recent studies on Swiss inbound tourism and travel demand use panel data with a short time series, which makes it difficult to test the stability of the coefficients (Falk, 2013; Stettler, 2017).

The asymmetric behaviour of income elasticity in different stages of the business cycle might have several reasons, including variations in the consumer behaviour or in the macroeconomic conditions. However, the instability of the long-term income elasticity may be due to other factors, such as the phase of the life cycle of the tourist area, which characterizes the destination over time. Butler (1980) divides this life cycle into six phases: exploration, involvement, development, consolidation, stagnation and a final phase of decline or rejuvenation. Beritelli (2015) suggests that the Swiss tourism industry has experienced several different development phases, encompassing the discovery of alpine leisure activities in the 1850s. After this followed the first strong growth phase until the crisis period during the years 1918–1950. From the 1950s to the 1990s, tourism demand grew even stronger. This was caused by more leisure time and real income increases of the main source markets, growing motorization of the population and improvements of the transportation network. Since the 1990s, Swiss tourism is stagnating. There are several reasons for the stagnation, including falling flight prices and increased international competition from long-haul destinations. Thus, several factors external to the tourism industry itself may affect the long-term trend of the income elasticity of tourism demand.

Empirical approach: TVC model

The TVC model is developed to overcome the specification error caused by the instability of parameters in a traditional time-invariant cointegration model developed by Engle and Granger (1987). This instability may be caused by discrete regime shifts, leading to gradual changes in the long-run relationship. Chang et al. (2014) point out that in the case of time-varying long-run coefficients, the standard cointegrating regressions would be biased even in combination with a rolling approach.

If changes in the coefficients are gradual, time-varying coefficients can be generated by a corresponding smooth function. Park and Hahn (1999) assume trigonometric functions and focus on the single cointegration relation. The canonical cointegration model is employed because of possible endogeneity of the regressors. Further, Chang et al. (2014) show that this approach is robust if at least one I(1) regressor is cointegrated with the dependent variable in the time-varying framework even if additional stationary variables are included. On the other hand, Bierens and Martins (2010) adopt the Chebyshev time polynomials function and allow multiple cointegration relationships in line with the Johansen procedure. Given that many studies focus on single cointegration relationships, Neto (2012) simplifies the procedure of Bierens and Martins (2010), by focusing on one single cointegration relationship. Based on this approach, Neto (2014) develops an alternative, the cumulative sum (CUSUM) TVC test in case of presenting structural breaks using fully modified least squared (FMLS). This test coincides with the ordinary least squares-based CUSUM test developed in Xiao and Phillips (2002), which is designed for the fixed coefficient cointegration test.

The TVC model is often used for estimating demand functions. Park and Hahn (1999) analyse the time-varying US automobile demand function, while Park and Zhao (2010) focus on the US gasoline demand function. The Chinese money demand function based on quarterly data from 1996 to 2009 is examined by Zuo and Park (2011), and Neto (2012) estimates the Swiss gasoline demand function with quarterly data from 1973 to 2010. Chang et al. (2014) study the time-varying income elasticities of electricity demand in Korea. All these studies provide evidence for time-varying long-run elasticities.

In this article, we employ the procedure in line with Bierens and Martins (2010) and Neto (2012, 2014), since the FMLS-based CUSUM TVC test is more robust when there is a possibility of structural breaks. In more detail, the independent variables in the long-run relationship are decomposed into a small numbers of smooth components based on the Chebyshev time polynomials. The coefficients of these components are estimated using the FMLS estimator (Phillips and Hansen, 1990). The smooth TVC coefficients are the linear combinations of the coefficients of these components. The time-invariant test can be easily implemented by the Wald tests (Neto, 2012).

Tourism demand, based on Swiss data, is specified as a function of real GDP, relative prices and oil prices (Song et al., 2009). Cortés-Jiménez and Blake (2011) and Lim and Zhu (2017) suggest that the determinants of tourism demand differ markedly across country of residence (see also Ferro-Luzzi and Flückiger, 2003; Nordström, 2005). This means that tourism inflows from various visitor countries may respond differently to changes in relative prices and real income. In this study, national tourist overnight stays for foreign and domestic visitors are specified as a function of foreign or domestic real GDP, weighted by its relative PPP. The long-run cointegration relationship can be expressed as

where t = 1,…, T, j = domestic or foreign and

Overnight stays at the country level are a highly aggregated measure that does not allow the assessment of different types of destinations. For this reason, domestic and foreign overnight stays for the largest Swiss city of Zürich are also examined. The composition of tourists in Zürich is likely to be different from Switzerland due to the high proportion of business travellers and cultural and shopping tourists. Equation (1) can be adopted for modelling Zürich tourist demand. All variables are defined in the similar way. Due to the similarity, the following discussions are mainly based on national level. Furthermore, for simplicity, the index j is dropped from equation (1) in the following discussion.

The smooth components are characterized by Chebyshev time polynomials,

where

where ξ s are 2(m+1) coefficients of these smooth components to be estimated. This study follows Neto (2012), who adopts the FMLS approach to estimate the parameters of ξs in equation (3), as suggested by Phillips and Hansen (1990). The order of the Chebyshev polynomials, m, involved in equation (3) can be determined, by minimizing the Hannan–Quinn information criterion (HQC), in accordance with Neto (2012), where

Several tests may be carried out based on the FMLS estimates of equation (3). First, as noted by Neto (2014), the smooth components will appear non-stationary if the original InGDPCPt and lnRPPPt are I(1)-processes. Second, cointegration tests based on equation (3) can be carried out. Neto (2012) employs the residual-based non-cointegration test based on work by Engle and Granger (1987), Engle and Yoo (1987) and MacKinnon (2010). However, Neto (2014) concludes that there is a possibility for under-rejection of the null hypothesis of non-cointegration in the presence of structural breaks. Thus, a FMLS-based CUSUM TVC test developed by Xiao and Phillips (2002) is used. The statistic of FMLS-based CUSUM test, CS, is defined as

where

An additional test concerning the time-invariant coefficients can be formulated by testing a null hypothesis of

This reveals that when the null is true, equation (3) is reduced to equation (1), that is, a time-invariant cointegration relation with

The standard deviation is also time-varying

These standard errors can be used to calculate confidence intervals.

Concerning the short-run responses, we assume time-invariant short-run coefficients. These short-run coefficients may be estimated under the framework of the vector error correction mechanism (VECM) model. Note that short-run estimation is mainly necessary for Swiss domestic overnight stays because the foreign real GDP and PPP are truly exogenous variables in relation to overnight stays in Switzerland. Presence of weak exogeneities for Swiss real GDP and PPP can be tested under the framework of the VECM model.

Data and descriptive statistics

The application of the TVC model is based on Swiss data, because Switzerland is one of the first countries in the world to collect data on arrivals and overnight stays in accommodation establishments. This means that the long time series required by the model is available. Official statistics in Switzerland started in 1934, and the country also has a long tradition in tourism. British mountaineers discovered the Swiss Alps as tourists – already in the 19th century and Switzerland was also part of the ‘Grand tours’ (Beritelli, 2015).

The data set contains time series of overnight stays for the period 1934–2015, provided by Statistics Switzerland. The seven largest visitor countries amount to approximately 95% of the international tourists in Switzerland: Belgium, Germany, France, Italy, the Netherlands, the United Kingdom and the United States. These countries are aggregated to one group of foreign tourists.

For the year 2004, data on overnight stays are missing. There is also a lack of information on whether the overnight stay is private or related to a business trip. Because of this, domestic and foreign overnight stays for the largest Swiss city Zürich are investigated separately. Real income is measured as GDP per capita (in 1990 International Geary–Khamis dollars) provided by the Maddison Project (Bolt and van Zanden, 2014). Data on real GDP per capita are only available for the period 1945–2010, while more recent figures are based on data from the World Bank development indicator database (measured in constant international dollars). The break in the time series for Germany after 1990 is over-bridged by using the growth rate of GDP per capita for West Germany (which is 3.7% in 1990). From 1991 onward, GDP per capita is interpolated using the growth rate of GDP per capita for the whole of Germany. PPPs from 1950 onward originate from the Penn world tables. The relative PPPs, RPPPs, are defined as Swiss PPP over visiting countries’ PPPs. For the period 1934–1950, PPPs are interpolated using historical inflation rates and fixed nominal exchange rates. GDP per capita and the PPP for each country are aggregated to composite time series using the share of overnight stays of the midpoint sample values.

The time series of the logarithm of GDP per capita, relative PPPs and overnight stays are displayed in Online Supplemental Figure 3A. Foreign overnight stays increased until the middle of the 1960s, but then remained relatively stable. In contrast, overnight stays of Swiss residents continue to grow. As can be seen, the Swiss francs appreciated by more than 30% in real terms against the EURO countries from 2008 to 2015.

Results

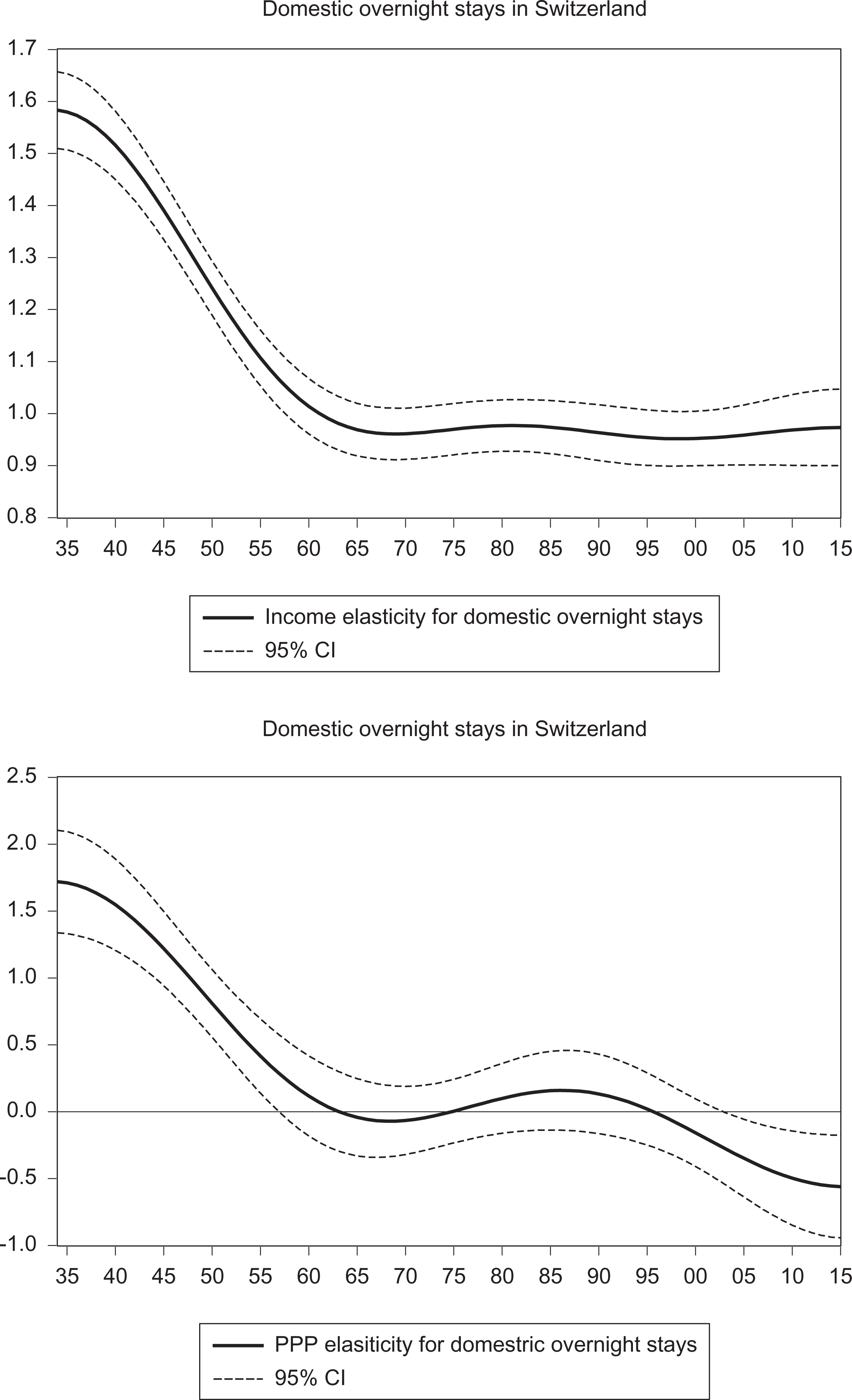

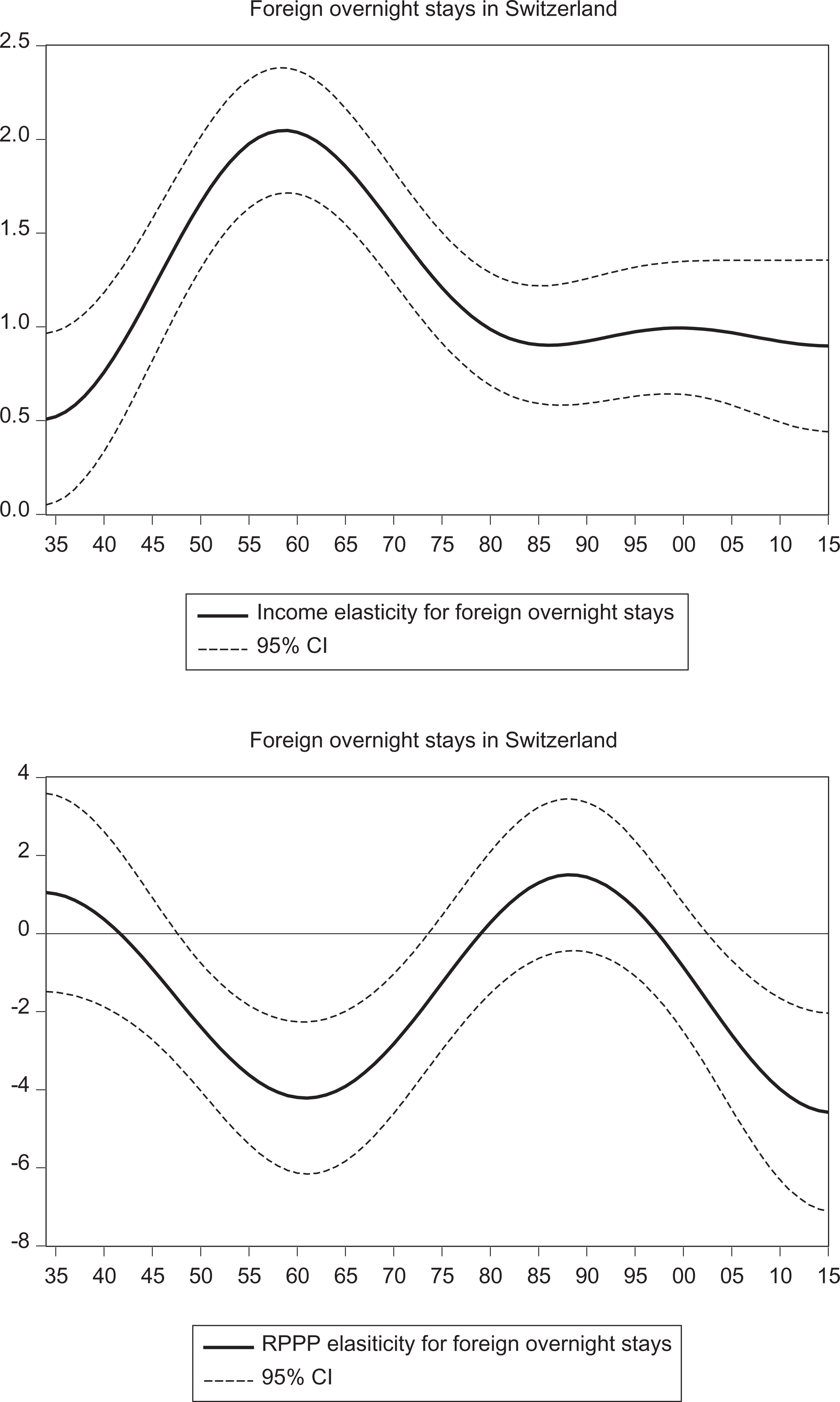

The estimations reveal that the long-run income elasticities vary considerably over time (Figures 1 and 2). The early phases of the time period studied experience higher elasticities, while they are at their lowest after the 1990s. Initial years also show higher elasticities for foreign tourists, although in recent years, this difference converges.

Income and price elasticities of domestic overnight stays in Switzerland.

Income and price elasticities of foreign overnight stays in Switzerland.

The first step is to check the stationarity of involved variables. Three unit-root tests are employed: the Augmented Dickey–Fuller (ADF) (Dickey and Fuller, 1979), the Phillips and Perron (PP) (Phillips and Perron, 1988) and the Kwiatkowski, Phillips, Schmidt and Shin (KPSS) (Kwiatkowski et al., 1992). In the first two tests (ADF and PP), the null hypothesis is the unit-root, while in the third one, KPSS, it is stationarity. The results are reported in the upper panel of Table 1. As a summary, all variables are I(1) processes.

Unit-root tests, TVC tests and VECM.

Note: TVC: time-varying cointegration; VECM: vector error correction mechanism; ADF: Augmented Dickey–Fuller; PP: Phillips and Perron; KPSS: Kwiatkowski, Phillips, Schmidt and Shin; ONS: overnight stays; GDPCP: GDP per capita measured in 1990 International Geary–Khamis dollars; RPPP: relative purchasing power parity; FMLS: fully modified least squared; AIC: Akaike information criterion; SIC: Schwarz information criterion. Parentheses show p-values. Squared brackets show t-values.

*** Significant at the 1% level.

** Significant at the 5% level.

* Significant at the 10% level.

a Unit-root tests with maximum lags of 11 and lag selection criterion according to AIC.

b The p-values are reported.

c For the foreign overnight stays, lnRPPP is used and the maximum lag is 20.

d Maximum m is set at 4.

e Critical values are according to Table 1 in Neto (2014).

f No VECM is applied to foreign overnight stays since foreign GDPPC is exogenous for foreign overnight stays in Switzerland.

g Lag selection criterion according to SIC.

The next step is to estimate the tourism demand equation (3) by FMLS separately for domestic and foreign overnight stays and carry out cointegration and time-invariant tests. The goodness of fit measured by the adjusted R 2 is quite high, 0.76 and 0.93, respectively.

The results of the FMLS-based CUSUM TVC tests are displayed in the middle panel of Table 1. Here, the 90% critical values from Neto (2014) are used. All the test statistics are smaller than these critical values. This means that the null hypothesis of TVC at 90% cannot be rejected. The Wald tests reported in the following panel confirm this.

The result of the VECM model for the relationship between domestic overnight stays, ONS, and Swiss GDP per capita, GDPPC, as well as Swiss PPP, referred as RPPP, is presented in the lowest panel of Table 1. The significant negative loading coefficient for overnight stays and positive loading coefficient for GDPPC illustrate that both variables are endogenous while the RPPP is exogenous.

The TVC parameters and associated confidence intervals can be easily calculated based on the estimation result from equation (3) and are reported in Figures 1 and 2. These calculations reveal that the long-run income elasticities vary considerably over time. The income elasticity for domestic overnight stays declines from 1.6 in the 1930s to approximately 1 in 1960 (Figure 1). From 1960 onward, this elasticity is stable around one. In contrast, the income elasticity of foreign overnight stays shows an inverted U-shaped relationship over time, with a peak of approximately two in the early 1960s that thereafter falls down to one in the early 1980s. From then onward, the elasticity is stable until the end of the period studied. Thus, it can be concluded that the foreign income elasticity is highest during the build-up phase of the Swiss tourism industry and lowest in the more recent stagnation phase. A tentative explanation of the evolution over time is the maturity of the destination and its position in the destination life cycle.

Furthermore, the Wald test shows that income elasticities are not significantly higher than 1 given the 95% confidence interval around 0.2. Table 1 shows the results of the Wald time-invariant test. The Wald test strongly rejects the null hypothesis that the income elasticity is time invariant at the 1% level in all cases. This indicates that the income elasticities are time-varying. However, the dependence of the long-run elasticity on time is mainly caused by an increase in income elasticities in the first half of the 1960s. Since the mid-1980s, income elasticities have not changed much.

A comparison with the meta-analysis of Peng et al. (2015) shows that the income elasticity of international tourism demand is relatively low. Again, this can be explained by the (Swiss) stage in the destination life cycle. The falling income elasticity over time is consistent with Gunter and Smeral (2016) for a shorter time period.

In order to account for different kinds of tourists (leisure or business), separate estimations for the largest Swiss city Zürich are performed as a robustness check. These results show a similar pattern as for the country as the whole, where the domestic income elasticity is at its highest in the 1930s, and then slowly recedes to the present level of 1.4. Since the early 1960s, this level is stable (Online Supplemental Figure 4A). The main deviation from the aggregate value, is the 0.4 higher elasticity from the 1990s onward. Income elasticity of international overnight stays peaks during the 1960s and then stabilizes at a level similar to that of domestic overnight stays. The higher income elasticity for overnight stays in Zürich indicates that the demand for trips to this international financial city is more responsive to economic growth of the source countries.

It also shows the evolution of price elasticities over time (see Online Supplemental Figure 5A for Zürich). A rise in a country’s PPP leads to a lower relative PPP and, in turn, to an increase in tourism inflows to Switzerland. The price elasticity of foreign overnight stays varies markedly over time, with the highest values (in absolute terms) at the end of the time period studied and in the 1960s. To the contrary, price elasticity of domestic overnight stays is not significant during a major part of the time period.

As a second robustness check, the TVC is estimated by source markets. The results confirm the general pattern of the evolution of income elasticities over time (results are available upon request).

Conclusions

This study adds new evidence to tourism research by introducing a model that examines the stability of the long-term income elasticity of tourism demand. For this purpose, the TVC model is applied to a Swiss data set on domestic and foreign overnight stays for the period 1934–2014. The results show that there is a time-varying long-run relationship between overnight stays and GDP per capita. This holds true not only for domestic, but also for foreign overnight stays. The domestic income elasticity is close to one and relatively stable from the mid-1960s onward, while the elasticity of foreign overnight stays is at its highest in the 1960s and then falls rapidly to one and has stayed at that level since the 1980s.

Since type of overnight stays (leisure or business) cannot be identified in the data set, separate estimations are performed for the largest city Zürich, expected to have a high proportion of business travellers. These estimations confirm the pattern of the declining income elasticity over time, but at a 0.4 higher level than for the average income elasticity which is around one. Different stages in the destination life cycle (attractiveness of the destination) are possible additional explanations for the variations in long-term income elasticities. Income elasticities are highest in the build-up phase of the tourism industry and lower in the stagnation phase.

This study shows that the TVC model is suitable to apply on tourism and travel demand. It can handle extreme events and political situations with travel restrictions and closed borders as well as the economic and financial crisis period. The structural stability test can easily be applied to other destinations with a sufficiently long time series of overnight stays or arrivals. A disadvantage of the method is that short-term or medium-term changes or fluctuations during the economic cycle cannot be analysed. It would also be preferable to distinguish between different types of destinations (beach and mountain destinations) and seasons (winter and summer). Weather conditions and transportation prices might also have an impact on tourism demand. Regrettably, the smooth TVC model does not allow for the inclusion of many covariates.

The variation of the income elasticity over the phases in the destination life cycle is a novel result. In the current phase of stagnation, long-term international tourism demand is reacting proportionally to changes in foreign real income, excluding economic fluctuations. Destination marketing organizations need to target source markets other than those already saturated.

Supplemental material

Supplemental Material, Appendix - Income elasticity of overnight stays over seven decades

Supplemental Material, Appendix for Income elasticity of overnight stays over seven decades by Martin Falk, and Xiang Lin in Tourism Economics

Footnotes

Acknowledgements

The authors would like to thank Eva Hagsten, Gang Li and Haiyan Song as well as the participants of the IATE 2017 conference in Rimini for helpful comments on an earlier version of the article. The authors would also like to thank Caroline Wigerstad for careful proofreading of the article.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.