Abstract

Recently, many firms that have caused direct pollution to the environment have begun to think about the necessity of environmental management. As buildings have played an important role in environmental issues, the real estate industry can no longer ignore demands for environmental management. Research on environmental management has mainly focused on its financial implications. However, there has been no consensus in the literature about the relationship between environmental management and firm performance. By comparing portfolios of environmentally certified properties of 19 lodging Real Estate Investment Trusts, this study explores the relationship between environmental management and firm performance, while taking into account the moderating role of outside board of directors. The relationship between environmental management and firm performance appeared to have mixed results, but this study found a positive moderating effect of outside board of directors. This study provides new insights into the hospitality and the real estate literature from a corporate governance perspective.

Keywords

Introduction

Society has now become more conscious about environmental issues and is now challenged with rapid environmental changes happening in places all across the world. With the concern about the environment, many executives in various industries that have caused direct pollution to the environment have begun to think about the necessity of environmental management, development, and shaping of environmental policy in business (Cramer, 1998).

Among the factors that influence the environmental issues, buildings have played an important role, since buildings account for nearly 40 percent of global energy consumption, they hold a pivotal role in effective climate policy (U.S. Energy Information Administration (EIA), 2018). About 39 percent of total U.S. energy consumption was consumed by the residential and commercial sector, which is mostly building-related (U.S. Energy Information Administration (EIA), 2018). Based on the increasing role of buildings, the environmental impact of buildings has attracted attention from practitioners, policymakers, and researchers (Khasreen et al., 2009). For example, leading property investors in the U.S., including Prologis or Hines, have actively supported green activities with the increased tenant demand (Parker, 2018), while government legislations require a certain level of energy disclosure to bring awareness of building energy efficiency (Newell & Lee, 2012). In the academic field, recent studies indicate that the demand for sustainable building facilities is increasing and there is recognition of the importance of their attributes (e.g., Simons et al., 2014).

The real estate industry sector is of particular interest in sustainable building facilities as buildings play a substantial role in affecting the environment. Among different types of firms, Real Estate Investment Trusts (REITs) have been interested in this issue because they own real estate assets that are mainly buildings. One of the significant accelerations for environmental management among REITs can be represented by environmental certifications on their properties. Energy Star label and Leadership in Energy and Environmental Design (LEED) certification are nationally recognized certifications highlighting a commitment to energy conservation in buildings. Accordingly, Energy Star and LEED have significantly contributed to sustainable building construction and management (Simons et al., 2014). Previous studies found that eco-certified buildings have higher asking rents, lower vacancy rates, sale price premiums, and lower operating expenses than non-certified buildings (Fuerst and McAllister, 2011; Wiley et al., 2010).

Therefore, stakeholders of REITs, especially managers, became interested in environmental certifications on their properties for mitigating the environmental impacts caused by business operations. However, due to some specific requirements for these certificates, the perceived additional costs associated with constructing eco-certified buildings are high, which is still a barrier for some building owners (Sah et al., 2013). In addition, due to the separation between ownership and control in the modern corporation, managers tend to pursue strategies to mitigate the environmental impacts that are aligned with their self-interest goals (i.e., reputation or image), not to maximize the shareholders’ wealth in what is termed in the literature as agency problem. The agency problem between shareholders and managers, and their impact on firm performance, has been an area of intensive research in the strategic management literature (Ghosh and Sirmans, 2003). From a corporate governance standpoint, the board of directors, a basic element of corporate governance, has gained importance in this matter given that directors perform vigorous monitoring of managers’ actions to make sure that decisions by managers come in line with shareholders’ interests. Their roles in REITs could be particularly important since managers have restricted investment opportunities to real estate assets by regulation (i.e., 90% of a REIT’s taxable income should be distributed annually to shareholders as dividends).

In this regard, the current study is to investigate whether environmentally certified REITs’ properties in the context of environmental management are beneficial to their financial performance, providing insights into the net benefits of certified properties in the lodging REITs context. The current study first hypothesizes that environmentally certified properties positively influence lodging REITs’ financial performance based on the resource-based perspective (Barney, 1991; Wernerfelt, 1984). Specifically, this study employs both an accounting-based and a market-based measure of firm performance to investigate the effect in a more comprehensive manner. After examining the main effect, this study further proposes that the proportion of outside directors in a corporate board positively moderates the effect of corporate environmental strategy (i.e., the increasing number of certified buildings) on firms’ performance based on agency theory (Eisenhardt, 1989) and resource dependence theory (Pfeffer and Salancik, 2003). Campbell et al. (2001) suggest that capital market is relatively ineffective for the real estate sector, and outside directors have special roles and responsibilities in this circumstance to protect shareholder interest in REITs. In addition, regarding the board’s provision of resources, outside directors who hold multiple channels for communicating information between firms have access to essential elements outside of their firm. Therefore, outside directors in REITs can provide profound advice and better directions to implement corporate environmental management strategy more effectively.

In the following sections, we review the relevant literature, develop our hypotheses using several theoretical lenses, describe our methodology, present results of data analysis, and finally conclude with implications and suggestions for future research.

Literature review

Environmental management and Firm performance

Environmental management denotes the organizational efforts and activities aimed at minimizing the negative environmental impact caused by a company’s operation (Cramer, 1998; Klassen and McLaughlin, 1996). The impact of environmental management in the context of sustainability on financial performance has been debated intensively for many years. In the academic field, researchers have been focused on whether or not a corporate investment in environmental management can improve firm performance. Some researchers pointing out the benefits of environmental management asserted that initial investments in environmental management could be a cost to a firm, but the investments usually pay off and thus enhance the firms’ bottom line (Cohen et al., 1995; Klassen and McLaughlin, 1996). On the other hand, other researchers (e.g., Schaltegger and Synnestvedt, 2002) argued that there is no mechanism directly linking environmental management to financial performance, assuming that the relationship holds only in specific cases. Researchers in this position argued that the firms, whose financial performance is weak, are less likely to implement environmental management strategy simply because they have fewer available resources to allocate as compared to those firms holding strong financial performance (Orlitzky et al., 2003). In this context, contrary to expectations, environmental management may cause an adverse effect on firm performance since a firm needs to use resources on environmental activities impeding the optimal resource allocation to maximize shareholder value.

Meanwhile, a resource-based perspective argues that competitive advantages are defined in terms of value and rarity rest on firm-specific resources and capabilities that are inimitable (Barney, 1991). Powell (1992) proposed a new expansion of the resource-based perspective, relating concerns for the natural environment to the resource-based view. In this context, Hart (1995) posited that sustainable development would increasingly be an important source of competitive advantage due to the growing awareness of constraints caused by the changes in the natural environment. Hart (1995) also stressed the need for an expanded scope of firm performance that includes environmental dimensions. In other words, natural resources are expected to become increasingly constrained over time, and those firms that respond adequately to uncertainty in the availability of natural resources will have a sustainable competitive advantage over their competitors. In this respect, studies have posited the importance of environmental management as a significant function to enhance the prospects of continued viability (Lim and McAleer, 2005) as well as a value creation channel through environmental certification (Chan and Hawkins, 2010).

REITs

Up to this day, companies have concentrated mainly on adjusting their business process to an environmental requirement imposed by the government (Cramer, 1998). Companies looking beyond what is necessary now seek environmental strategies that yield financial benefits. In the real estate industry, the investors and tenants are increasingly seeking energy efficiency, green buildings, and better disclosure of environmental performance (Zahid and Ghazali, 2015). At the same time, the increasing emphasis on “green rating” system for buildings, initiated by both government and industry, suggests that the behavior of the real estate sector is quite important in matters of environmental sustainability. Due to these stakeholders’ pressure, firms in this sector are encouraged to develop strategies for the satisfaction of stakeholders as well as legitimize their operations. For these reasons, environmental management practices have been one of the most burning issues in the real estate industry to improve a firm’s competitiveness (Reed and Willis, 2013). Among various environmental management practices, in the last decade or so, there has been a significant impetus for green buildings (Sah et al., 2013), and the studies on green buildings have been increasing in the last few several years. Previous studies found that commercial buildings with energy efficiency ratings generate significantly higher rents, occupancy rates, and prices than other comparable conventional buildings (Fuerst and McAllister, 2011; Wiley et al., 2010). These studies generally suggest that green buildings may be a valuable resource for the firm that likely helps create competitive advantage. Nevertheless, companies in the real estate sector wondered to what extent the environmental benefits of sustainability in real property can be led to an increase in financial performance.

While previous studies have examined the impact of environmental management in the traditional real estate sector (i.e., office, industrial, retail, and apartments), non-traditional REITs that do business in other sectors, such as self-storage, healthcare, timber, or hotels, have been rarely examined for financial implications of their environmental management (Harris, 2019). Specifically, although firms so-called lodging REITs that mainly own hotel properties play a significant part in the entire lodging sector, the impact of environmental management in these firms has been rarely examined in the hospitality literature. While traditional REITs operate business through residential type business, lodging REITs operate business with both residential and retail activities (e.g., food and beverage, accommodations, and recreational amenities) within a real estate investment. That is, lodging REITs also require investment in activities associated with hotel business, such as inventories, working capital, labor, specialized management expertise, and ongoing marketing that make them more akin to a retail type business, as well as investment in land and buildings (Manning et al., 2015).

A topic of environmentally sustainable hotel development has received recent attention in hospitality academia (Manning et al., 2015). While research has shown that commitment to environmental practices positively influences hotels’ various performance indicators, such as guest ratings (Peiró-Signes et al., 2014) or profitability (Segarra-Oña et al., 2012), hotels still struggle to develop the most effective way to promote their green status. One way of such promotion is formal certification from a third-party declaration, which is slowly becoming a common approach for hotels to demonstrate their commitment to environmental management (Rodríguez-Antón et al., 2012). In this respect, the Environmental Protection Agency (EPA) created Energy Star certification providing commercial building developers and owners with an overall energy efficiency score for benefiting both the environment and the building owners. In a similar vein, the United States Green Building Council (USGBC), a nonprofit organization, has taken large initiatives towards prosperous, cost-efficient, and energy-saving green buildings. This way, USGBC promulgated the LEED standards considering people, planet, and profit, not just energy use. Eichholtz et al. (2010) assessed the rents and transaction prices of buildings with environmental certificates (LEED and Energy Star), relative to non-certified comparable buildings in U.S. Findings from the study indicated that about three to five percent higher rents were generated from environmentally certified buildings and 11–19 percent increase in sales prices among these buildings. Further, Eichholtz et al. (2012) discussed that the premium from environmentally certified buildings includes not only the direct energy cost savings from green buildings but also collateral benefits (e.g., improved working environment, increased productivity, and corporate image enhancement) as a potential constituent for better firm performance.

Given that lodging REITs differ from traditional REITs as noted earlier, the current study is focusing on lodging REITs, differentiating itself from earlier studies on traditional REITs (e.g., Eichholtz et al., 2012; Sah et al., 2013). Since the main asset of lodging REITs is building, the current study operationalizes environmental management in terms of a company’s greenness of property portfolios and examines the effect of environmental management on financial performance. Based on a resource-based perspective that highlights sustainable competitive advantages over competitors and unique characteristics of the business (Hart, 1995), the current study proposes a positive relationship between environmental management and a firm’s financial performance for lodging REITs.

H1. Lodging REITs’ environmental management will positively influence a firm’s financial performance

Moderating effects of Board Independence

A corporate board typically plays an influential role in controlling and maintaining organizational operation and effectiveness. Scholars have discussed two distinct functions of corporate directors based on agency perspective and resource dependence perspective (Eisenhardt, 1989; Pfeffer and Salancik, 2003). First is the monitoring function of boards, also described as the “control role” (Boyd, 1990). The monitoring function denotes the responsibility of corporate directors to monitor executives on behalf of shareholders. Agency theorists assert this monitoring role as a crucial function of boards that monitors the actions of “agents”—managers—to protect the interest of “principals”—owners (Eisenhardt, 1989). As the shareholders’ formal representatives, the board of directors is eventually responsible for monitoring management’s performance and confirming that a firm’s strategic decision is well aligned with the maximization of shareholders’ profit and value of the firm (Rechner and Dalton, 1991). This monitoring role is important because of the potential costs (i.e., agency cost) incurred when managers pursue their own interest at the expense of shareholders’ interest (Hillman and Dalziel, 2003). In the case of REITs where a form of closed-end mutual fund is mainly used as an investment type, this agency problem may be particularly troublesome because shareholders find it difficult to evaluate and monitor transactions involving real estate properties (Alshimmiri, 2004). In this respect, the board of directors in REITs could play an important role in reducing agency costs that are likely to have a direct impact on corporate performance. Given that the board of directors is facing great pressure from shareholders regarding sustainability issues these days, the board of directors has been more likely to make a decision on corporate spending for a firm’s environmental management and create separate standing committees dealing with environmental-related matters (Walls et al., 2012).

Second is the provision of resources function of boards. This perspective has been perceived as resource dependence (Boyd, 1990; Daily and Dalton, 1994; Pfeffer and Salancik, 2003). The resource provision function denotes the ability of the board to provide the firm with resources (Wernerfelt, 1984). This function has its roots in several previous works on resource dependence. Pfeffer and Salancik (2003) noted that “when an organization appoints an individual to a board, it expects the individual will come to support the organization, will concern himself with its problems, will variably present it to others, and will try to aid it” (2003, p.163). The resource dependence perspective suggests that the resource provision function is directly related to firm performance (Hillman and Dalziel, 2003). Pfeffer and Salancik (2003) asserted that resources help reduce dependency between the firm and external contingencies and diminish uncertainty for the firm. Therefore, in the resource dependence perspective, directors are expected to provide resources to help build appropriate strategies by providing impartial, sound, and experienced advice. Zahra and Pearce (1989) depicted this role as directors’ active involvement in the strategic arena through advice and counsel to the Chief Executive Officer (CEO).

Associated with the function of boards on environmental issues, both perspectives point out the distinct role of outside directors. Based on the agency perspective, outside directors who do not have pecuniary relations with the company may be more responsive than inside directors to shareholder pressures around environmental issues. It is because outside directors can enhance their reputations by meeting their responsibility of promoting the shareholders’ interests, and therefore, it improves their chances of receiving additional board nominations (Daily et al., 2003). In this respect, shareholders are likely to rely on outside directors to protect their interest from insiders pursuing non-value-maximizing agendas, reducing agency problem (Friday and Sirmans, 1998). Consistent with shareholders’ growing interest in an environmentally responsible organization, it becomes more important to implement appropriate environmental management strategies (Darnall et al., 2008). Therefore, outside directors show greater motivations to align themselves with shareholders, rather than with managers, and to encourage the firm to implement sustainability strategies successfully.

Meanwhile, the resource dependence perspective predicts a relationship between the degree of uncertainty and the composition of the board as measured by the number or proportion of outside directors (Pfeffer and Salancik, 2003). Especially when a corporation deals with a capital investment in the context of environmental management, having an outsider board member who possesses more diverse expertise, knowledge, and experience may reduce uncertainty (Hillman et al., 2000). Therefore, outsider directors’ involvement in a decision on environmental management is important and particularly noticeable when it requires a significant amount of capital investment but has uncertain outcomes (Daily and Dalton, 1994). Outside directors can use their affluent backgrounds, experience, and direct or indirect network ties to help navigate strategic moves (Carpenter and Westphal, 2001). In order to successfully implement an environmental management strategy, it is important to nominate directors who have the ability to advise management and have preferential access to outside resources. Each director may bring unique attributes to the firm, and this uniqueness reflects the heterogeneity of resources such as expertise, skill, information, and linkages to other external constituencies (Hillman et al., 2000). Hillman et al. (2000) proposed that outside directors, classified as “business experts,” “support specialists,” and “community influential,” can contribute to a board with different types of resources. Hillman and Dalziel (2003) asserted that outside directors might be more effective at providing resources to the firm, which, in turn, are related to firm performance.

Pfeffer (1972) suggested that, for board composition, an optimal ratio exists for the outside directors that is related to superior financial performance, but that ratio differs among industries. Different from other industries, REITs belong to a regulated industry in respect to restricting their investments to real estate assets (Ghosh and Sirmans, 2003). This circumstance limits the investment option available to managers (Demsetz and Lehn, 1985). It encourages shareholders to appoint outside and unaffiliated directors who can play distinctive roles and responsibilities to protect shareholder interest in REITs (Ghosh and Sirmans, 2003). In REITs, compared to outside directors, insider directors tend to be more of a business expert in real estate who provide firm-specific information and resources that are internally focused (Friday and Sirmans, 1998). Inside directors, who are principally employed by REITs, are engaged in ongoing business relations with the REITs. Outside directors, on the other hand, are more of an expert in other fields and hold other positions outside of the company. Outside directors tend to have a keen understanding of external factors such as economic trends, financing information, environmental concerns, or other property-specific information (Friday and Sirmans, 1998). When it comes to dealing with environmental issues, inside directors in REITs may not be best suitable for advising and helping executives to implement a corporate strategy properly. This circumstance results in increasing demands for external linkage and more outside directors on the board who tend to have more knowledge regarding environmental issues and their impact (De Villiers et al., 2011). In addition, given that firm’s sustainable practices and environmental management often involve high initial investments, outside directors who are less subject to shareholder pressures are better positioned to provide oversight for management and support these kinds of strategies from a long-term point of view. Therefore, boards consisting of resource-rich outside directors are less subject to pressure to produce short-term accounting results and thereby are better placed to ensure that firms pursue positive environmental performance.

In this respect, the current study focuses on the role of outside directors and employs the ratio of outside to inside directors representing one dimension of formal structural independence (Westphal, 1998). Since outside directors in REITs are thought to be informative and knowledgeable about environmental issues as well as have more external linkages and resources, the current study argues that greater board independence will help implementing a firm’s environmental management and lead to an increase in firm performance, thus proposing a moderating role of outside directors as follows.

H2. Board independence will positively moderate the effect of lodging REITs’ environmental management on a firm’s financial performance

Methodology

Sample and Data

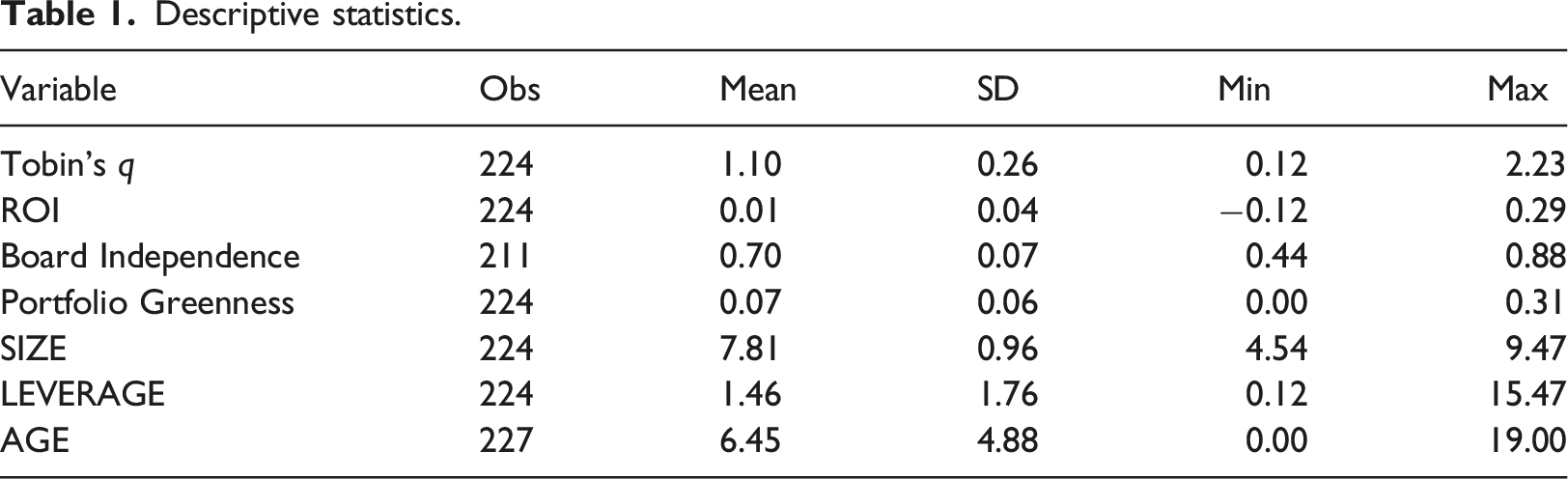

The current study uses the SNL Real Estate database and identifies 19 publicly traded lodging REITs that filed with the US Securities and Exchange Commission (SEC) and whose shares were traded on national stock exchanges as the sample panel for the current study. The study selects the sample period ranging from 2000 to 2019 to cover all economic conditions, obtain a sufficient number of sampled observations, and reflect more recent phenomena of the proposed relationships. To measure the greenness of REITs property portfolios, this study uses a dataset consisting of REITs green buildings that received either a LEED certification from the USGBC or an Energy Star certification from the EPA. Accounting data was retrieved from the COMPUSTAT database, while boards related data (e.g., the number of outside directors) was collected from firms’ annual reports (10-K) filed with the US SEC. After the deletion of missing data, the final sample consists of 19 firms, yielding 208 observations, which are further explained in the following sections.

Dependent variables

Two different measures, return on investment (ROI) and Tobin’s q, are used to represent firm performance: a firm’s profitability and the market’s evaluation of future profitability for a given firm. First, ROI is a performance measure used to evaluate the profitability of an investment and previous literature (e.g., ; Kudus and Sing, 2011; Seo and Sharma, 2012) employed ROI as a measurement for financial performance of REITs. The current study measured ROI as net income divided by the sum of long-term debt, minor interest, preferred stock, and common stock (Jung et al., 1996). Second, the current study employs Tobin’s q (Q) to measure the market evaluation of a firm’s future profitability. Q is chosen over some other market-based performance measures such as stock returns since Q accounts for risk adjustment or normalization required to make the comparison across different firms possible (Lang and Stulz, 1994). Following the Q estimation suggested by Chung and Pruitt (1994), the current study defines Tobin’s q (Q) as follows

Independent variables

The current study constructs a dataset on the greenness of REITs property portfolios by retrieving the year of certification data from the USGBC and EPA databases along with the year of acquisition and sale data from the SNL database. The current study refers to this data as “Portfolio Greenness,” representing a company's environmental management. This study counts the number of properties with environmental certifications (LEED or Energy Star) and divides the number by the total number of properties owned by each company in a given corresponding year. The formula is as follows

In addition, for testing Hypothesis 2, an interaction term between Portfolio Greenness and Board Independence is included in the model. Board Independence, a variable of particular interest, is the percentage of outside directors on a firm’s board. Following Mallette and Fowler (1992), this study calculates the percentage by multiplying a ratio of the number of outside directors on a board over the total number of board members by 100 as below

Control variables

This study considers three control variables in the model: firm size (SIZE), leverage (LEV), and age (AGE). Firm size (SIZE) controls for any systematic, size-related impact on a firm’s performance and a firm’s fundamental operational characteristics. Based on the argument regarding economies of scale (Riordan and Williamson, 1985), large firms are prone to perform better than small ones with the advantage of lower average operating costs, thereby proposing a positive relationship between firm size and financial. The current study uses a natural logarithm of total assets as a proxy of firm size, following previous literature (Pfeffer and Salancik, 2003). Leverage (LEV) is employed as another control variable since a higher leverage ratio can positively impact a firm’s performance (Dammon and Senbet, 1988). The current study operationalizes LEV in terms of a firm’s debt-to-asset ratio. Firm age (AGE) is included because previous literature found a significant relationship between a firm’s profitability and AGE (Das, 1995). The current study operationalizes AGE as years since a firm’s inception to going public and includes AGE as a control variable in the model.

Econometrics models

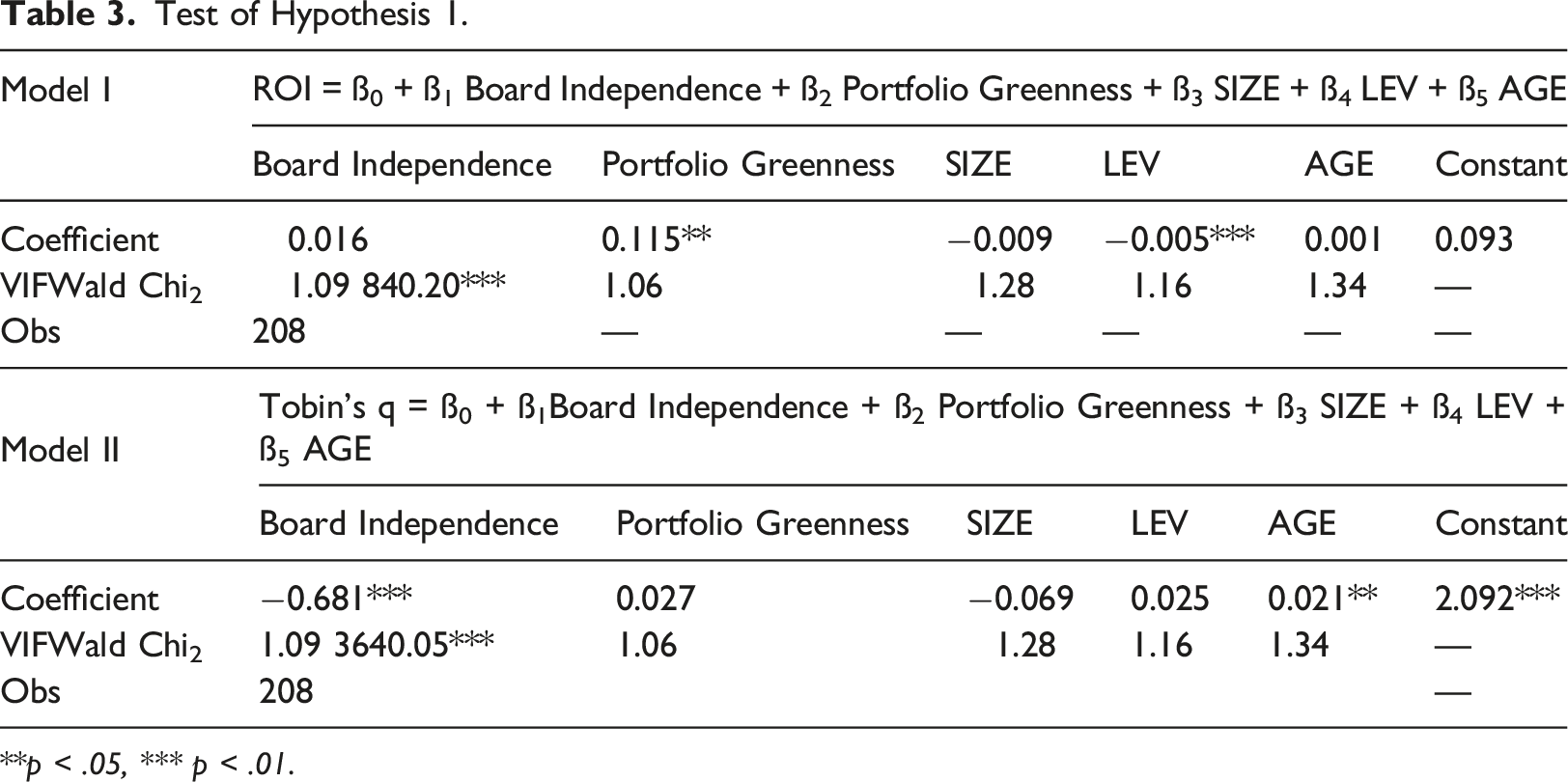

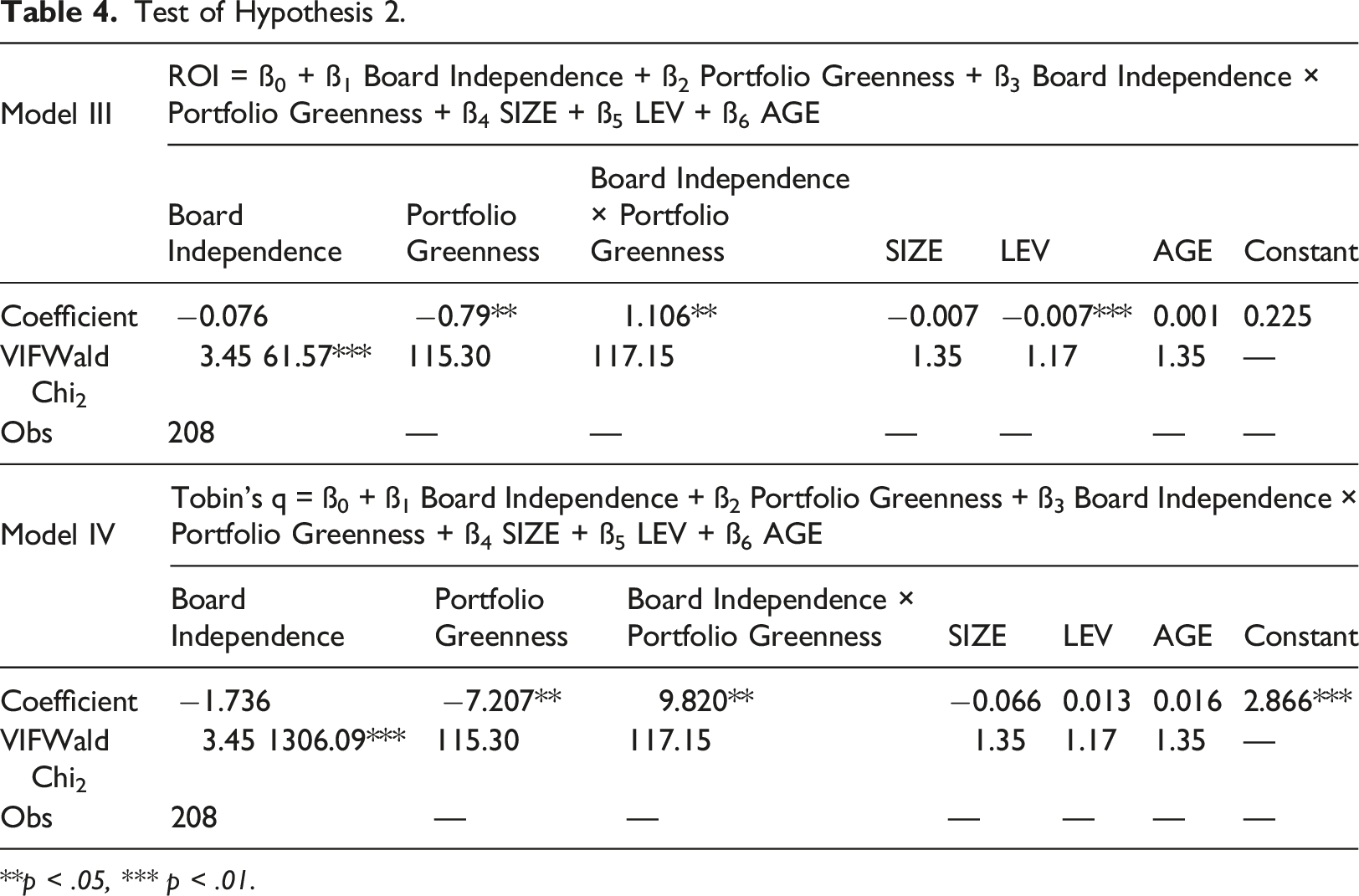

To examine the research hypotheses and accomplish the study purpose, the current study uses panel data. While the panel data provides several benefits such as controlling unobservable firm-specific attributes or reducing measurement errors, there are also some issues that need to be addressed when analyzing panel data, including unobserved heterogeneity (Wooldridge, 2002). To overcome these issues, the current study employs panel analysis and performs Hausman’s (1978) specification test to choose either a fixed- or random-effects estimator to estimate the proposed coefficients appropriately. For Model 1, based on the results of the Hausman test (χ2 = 6.18, p > .05), the current study employs a two-way random effects model by firm and year (Wooldridge, 2002) and performs the analysis to test the proposed hypothesis. For Model 2, based on the results of the Hausman test (χ2 = 14.63, p < .05), the current study employs a two-way fixed effects model by firm and year (Wooldridge, 2002) and performs the analysis to test the proposed hypothesis. The regression models are presented below. Model 1: ROI = Model 2: Tobin’s q = Model 3: ROI = Model 4: Tobin’s q =

Results

Descriptive statistics

Descriptive statistics.

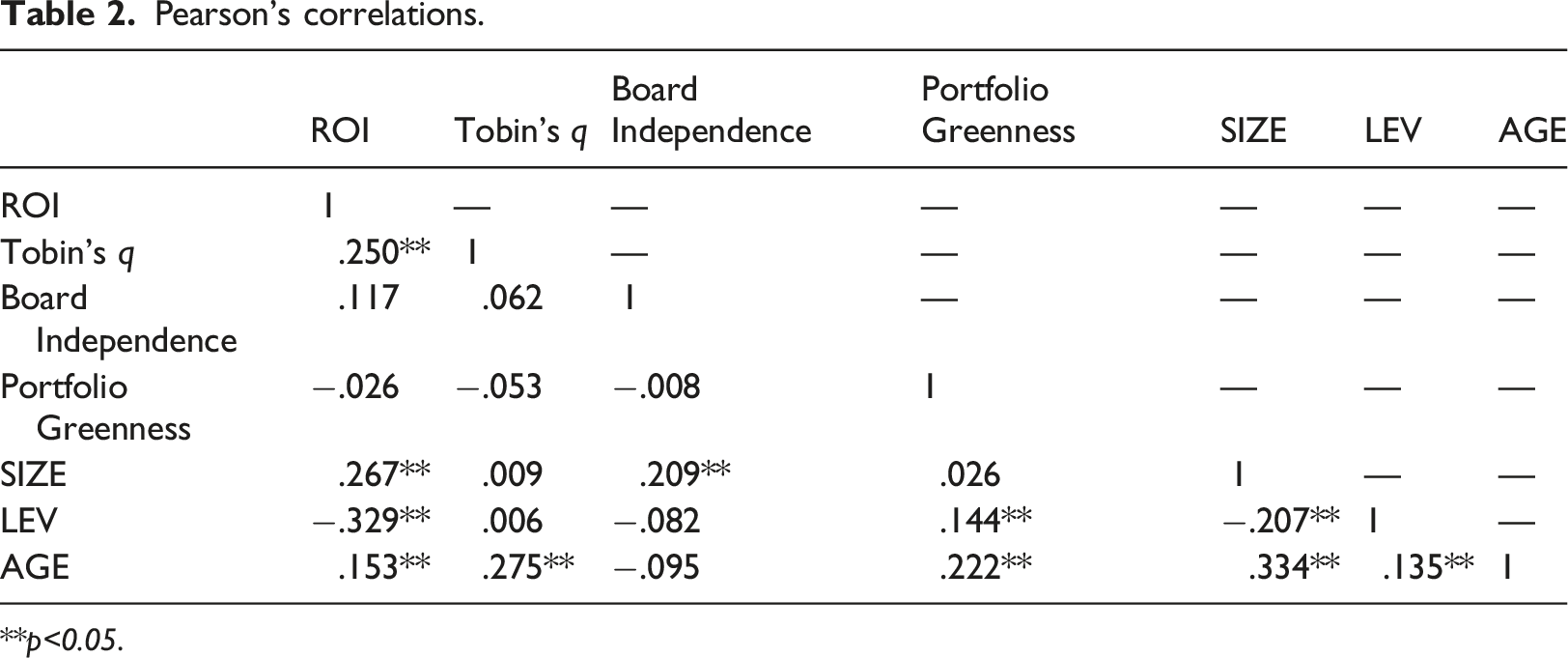

Pearson’s correlations.

**p<0.05.

Main findings

Test of Hypothesis 1.

**p < .05, *** p < .01.

Test of Hypothesis 2.

**p < .05, *** p < .01.

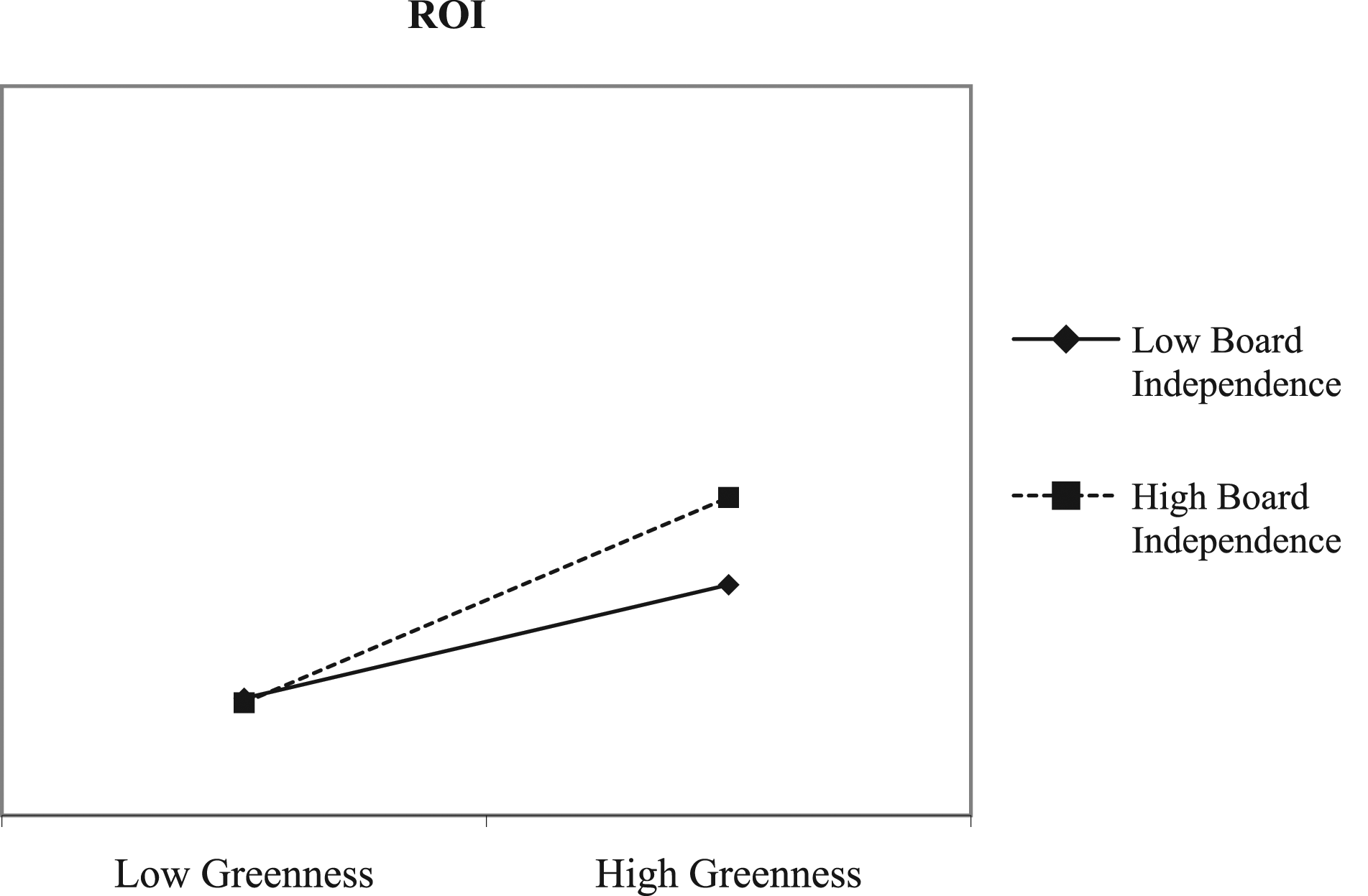

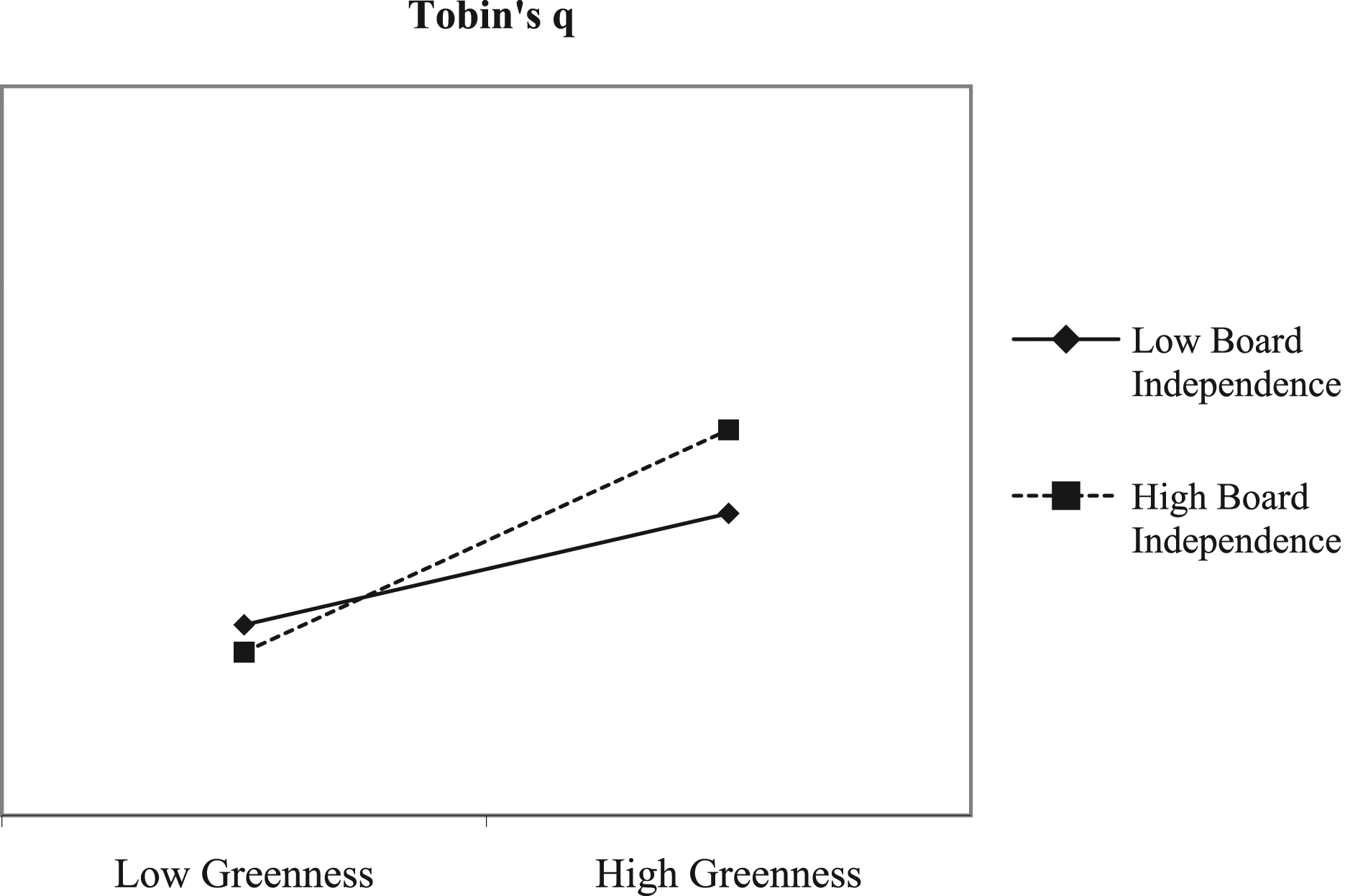

In addition, this study applies simple slope analysis to interpret the significant interaction effects on the relationship between Portfolio Greenness and firm performance, with interactions plotted using Dawson’s (2014) procedure. Figures 1 and 2 provide a graphical representation of the empirical result. Both figures suggest that when the value of Portfolio Greenness is high, Board Independence has a positive effect on the relationship between Portfolio Greenness and firm performance (i.e., ROI and Tobin’s q). The moderating effect of Board Independence on the relationship between Portfolio Greenness and ROI. The moderating effect of Board Independence on the relationship between Portfolio Greenness and Tobin’s q.

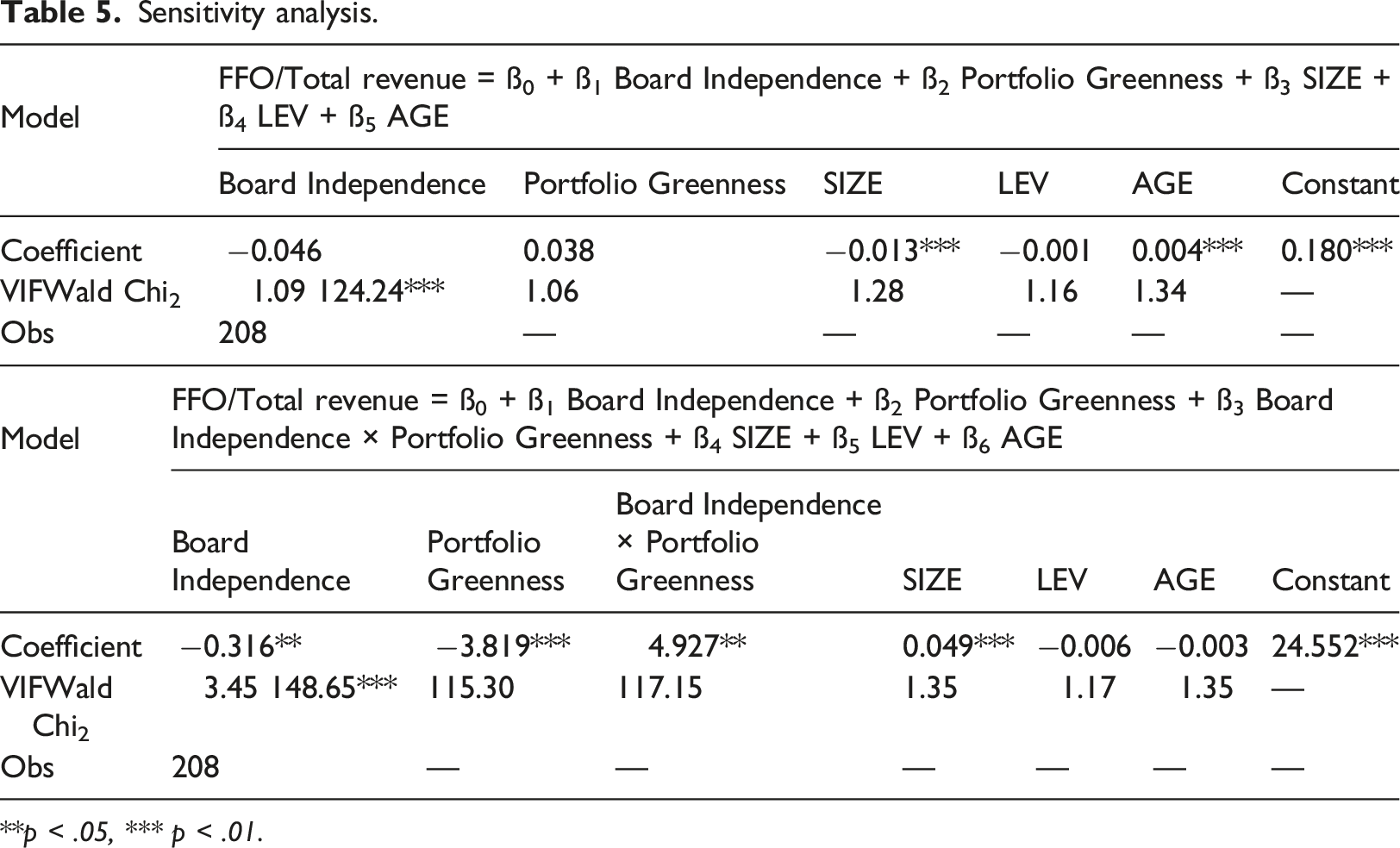

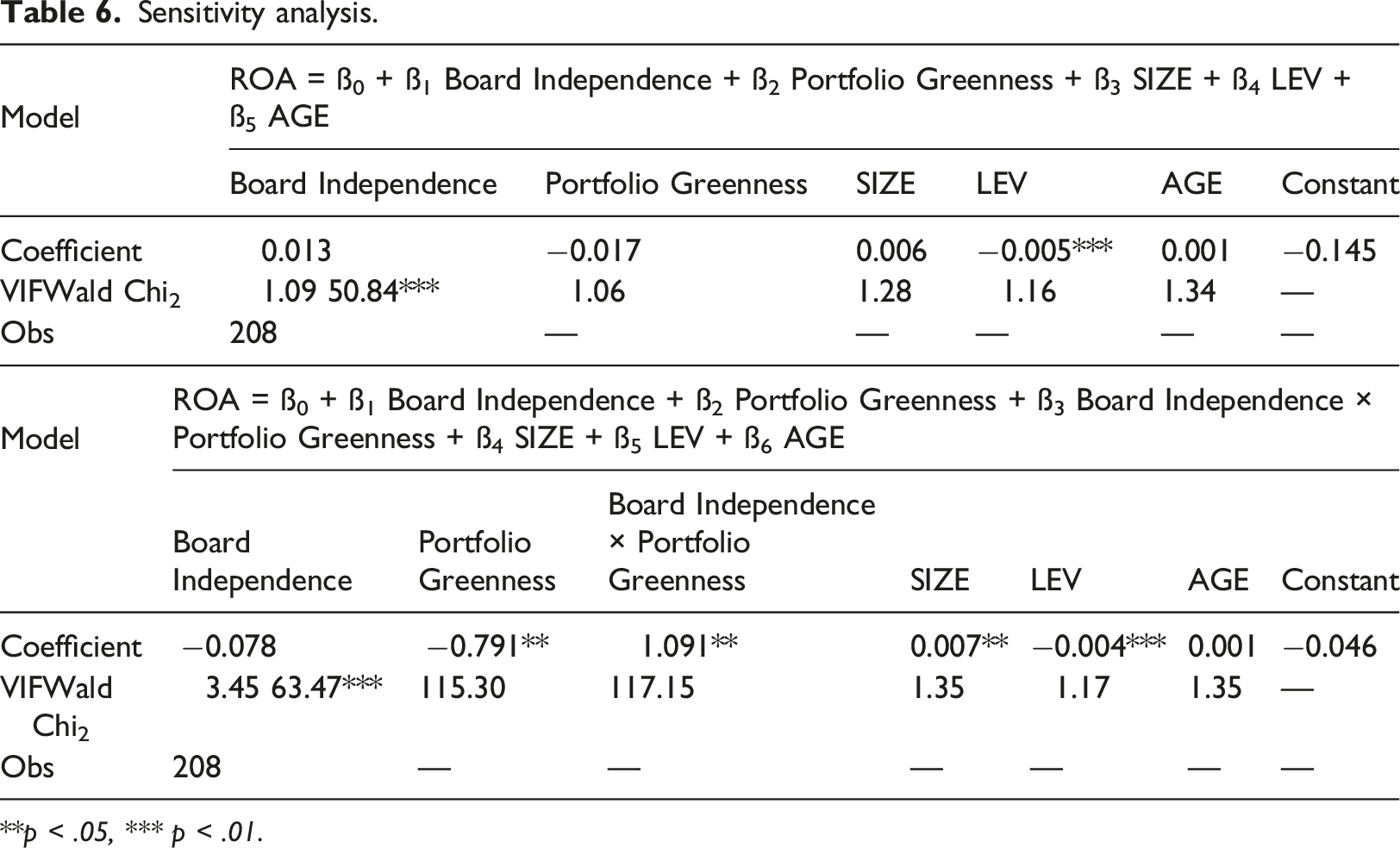

Sensitivity analysis

Sensitivity analysis.

**p < .05, *** p < .01.

Sensitivity analysis.

**p < .05, *** p < .01.

Discussion

While there is emerging literature that investigates the implication of environmental management on a firm’s financial performance (e.g., Eichholtz et al., 2012), there has been little empirical examination to test this link in the context of the lodging REITS from the perspective of green-certified properties. Based on Hart’s (1995) resource-based perspective, the current study proposed a positive impact of environmental management on a firm’s financial performance (H1) and found statistical support for the association in the case of ROI. However, our study does not find statistical support for the association in the case of Tobin’s q, FFO/total revenue, and ROA. A possible reason for the nonsignificant main effects may be explained by additional costs associated with obtaining eco-certification for buildings, specifically, payments to the certifying body for rating the building and/or the additional production costs associated with meeting the certification standards. Accordingly, additional costs may offset benefits of eco-certification, leading to the nonsignificant result for FFO/total revenue and ROA. Also, as Wang et al. (2016) suggested, eco-certified buildings may require high initial investments but a long payback period, and the markets may not be able to incorporate those perspectives in an efficient manner, thus again leading to the nonsignificant result for Tobin’s q.

Regarding another possibility of contingent factors, this study tested the moderating effect of Board Independence (H2) and found statistical support for H2 that the proportion of outside directors on the board (i.e., Board Independence) moderates the relationship between environmental management and lodging REITs’ profitability and market-based performance, measured by ROI and Tobin’s q. That is, as the proportion of outside directors increases, the positive effect of environmental management (the greenness of REITs property portfolios) on lodging REITs’ profitability and market-based performance becomes greater. The findings indicate that investment in green and sustainable buildings is a financially worthwhile strategy for lodging REITs companies with a high proportion of outside directors, possibly suggesting that stock investors perceive the value of sustainable investment. In the sensitivity analysis, this study found the same significant moderating role of Board Independence in the case of operating efficiency (i.e., FFO/total revenue) and short-term profitability (i.e., ROA), suggesting the robustness of this study’s findings.

The results of this study can align with an agency perspective that outside directors have greater motivation to be effective than inside directors with respect to monitoring managers and protecting shareholder interests. Also, the results correspond to a resource dependence perspective (Eisenhardt, 1989; Pfeffer and Salancik, 2003), suggesting that provision of external resources reduces uncertainty. As the implementation of environmental management may require a significant amount of capital investment with uncertain outcomes, lodging REITs may require board members who possess expertise or knowledge that reduces uncertainty. Therefore, having outside board members who have greater motivation and can provide more proper advice to the management with preferential access to outside resources may contribute to implementing an environmental management strategy successfully. In this context, the results of this study imply that the benefits of having more outside directors may increase strategy effectiveness and diminish uncertainty associated with a firm’s investment in environmental management. This finding is in line with the previous discussion of the role of outside directors associated with firm valuation (Cotter et al., 1997) and firm performance in the real estate industry (Friday & Sirmans, 1998; Ghosh and Sirmans, 2003).

The findings of this study provide theoretical implications. The results of this study imply a need for a new extension of the resource-based perspective (Barney, 1991; Hart, 1995), linking sustainable competitive advantage to a firm’s financial performance in the real estate industry. In specific, this study aggregated all eco-certified buildings (i.e., property level) to represent a collective effect of a firm’s environmental management, and examined how such collective efforts in the environmental management affect the firm’s performance. By revealing the relationship between the greenness of REITs property portfolios and firm’s financial performance, this study expands understandings of how environmental management influence firm performance. In addition, corporate governance structure in the real estate sector may play a crucial role in restricting the managers’ self-interest and incentive in continuing the project that is possibly failing. In that regard, external monitoring mechanisms including outside directors can provide additional benefits (Ghosh and Sirmans, 2003). Though outside directors do not have exposure to the day-to-day activities of the firm, their role in monitoring managers will ensure that the firm’s investment decision on continuing environmental certification of their properties after a set period can be taken in a way that is transparent, fair, effective, and efficient. The findings of this study that outside directors further improve the positive effect of environmental management on firm performance, therefore, are worthwhile. Given that the evidence on corporate governance in regulated industries (e.g., the real estate) is limited, the results of this study enrich the hospitality and the real estate literature.

The current study implies practical implications for the lodging REITs practitioners, suggesting that implementing environmental management (i.e., investing in sustainable buildings) is associated with positive firm performance. Based on the results of this study, lodging REITs companies with a high proportion of outside directors may more readily achieve a positive effect of environmental management than a firm with a low proportion of outside directors. When appointing new corporate directors, shareholders of lodging REITs companies may consider the fact that outside directors not only have more incentives to align themselves with shareholders but also encourage the firm to successfully implement environmental management strategies by providing various resources. Thus, to efficiently implement environmental management strategies, a corporate board is advised to have more outside directors in its pool. Furthermore, investors of the lodging REITs should use this information when they develop the lodging REITs investment portfolios to achieve the highest returns possible.

Limitations and Future research

Despite the importance of this study, there are limitations that future research might address. First, even though the current study collected panel data from 2000 to 2018, a limited sample size is still apparent, especially for lodging REITs. This results from the fact that only a few publicly traded REITs companies exist in the lodging industry. Future researchers are encouraged to collect a larger sample and replicate this study to enhance the external validity of our findings. However, it should also be noted that the data used in the current study is the most available to the public at the time of the study and further, even with the small sample size, the current study found results that support the proposed hypotheses. Second, while there are specific establishments for the lodging sector in the environmental certification system, LEED and Energy Star are not the only indicators representing the degree of greenness. Several regional hospitality-specific eco-certifications have been developed in recent years, such as BIO Hotels, Green Tourism, and Green Key. However, these eco-labels are not a property level label and future studies may incorporate a non-property level label to measure the degree of greenness in a more comprehensive manner. Third, the collected data is an unbalanced panel data, which potentially makes the pooled ordinary least squares specification biased due to overlooked time- and firm-specific heterogeneities as well as autocorrelation (Gujarati and Porter, 2003). In order to mitigate these issues, the current study performed a panel data analysis that controls the unobserved heterogeneity within both firms and years, and provides efficient estimates (Wooldridge, 2002). However, the unbalanced panel data could still be problematic when the attrition rate is high, and the results should be interpreted with a caution of this potential problem.

While the current study focuses on the moderating role of outside directors potentially reducing uncertainty in the context of environmental management, the examination does not mathematically measure the level of uncertainty associated with capital investment. Future research can specify the risk associated with the uncertainty and clarify the effect of outside directors to alleviate the risk. In addition, the current study does not observe board capital in a comprehensive manner. This capital, composed of both human capital (e.g., experience or expertise) and relational capital (a network of ties to other firms or external contingencies), explains much of the variations in resources that outside directors possess. In this regard, future studies are encouraged to examine more elaborate effects of outside directors on environmental management. In addition, even though the current study rules out the role of inside directors, inside directors may help the firm with their firm-specific knowledge about the firm’s operational activities to evaluate and ratify the firm’s strategies. This assertion may be particularly true in certain situations, such as financial crises or market crashes, that require a proper understanding of core business processes. In this respect, investigating the role of inside directors in different situations would be of great interest for a future study.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.