Abstract

The winery tourism literature has traditionally focused on how to increase tasting room sales or to understand visitors as wine buyers to better promote product sales. It has been found, however, that wine tourists desire more from the wine tourism experience than just the tasting and purchase of wine, resulting in wineries offering additional attractions and experiences to their visitors. This paper uses a case example located in South Africa to examine how one privately owned business has created a highly successful ‘micro-cluster’ of authentic, experiential, and holistically synergistic attractions spread across two of its adjacent wine farms. Using a novel business model combining wholly-owned businesses, partnerships, and tenants paying a percentage of gross revenue, this agritourism venture has become a major tourist destination, attracting more than 400,000 visitors annually. This study demonstrates how ‘micro-clustering’ on wine farms, previously unexplored in the literature, can become a major revenue stream for wineries and their related on-site businesses, while at the same time providing an excellent marketing opportunity for their products. The model may also be applicable to other businesses in rural areas where the creation of micro-clustered attractions can contribute to the economic development and prosperity of a community as a whole.

Introduction

Wine tourism has been part of both the wine and tourism industries for many years and has become a major source of revenue for both. However, it takes more than the physical presence of vineyards and wineries to create a wine tourism destination. While typical components of wine tourism include the places where people visit (e.g., vineyards, wineries, and wine festivals/events) and the intentions of the visitors (e.g., tasting wine and experiencing the unique characteristics of the wine-producing area or wine-related event) (Hall, 1996; Macionis, 1996), wine tourists have been shown to desire more from their winery experience than simply the tasting and purchasing of wine. They also desire options such as food, accommodation, recreational activities, cultural attractions, and enjoyable scenery and surroundings (Back et al., 2018; Brown et al., 2007; Bruwer and Alant, 2009; Cohen and Ben-Nun, 2009; Dawson et al., 2011; Getz and Brown, 2006; Getz et al., 2008; Park et al., 2019). As a result, activities found on wine farms continue to increase as wine tourism evolves. South Africa is one of the countries at the forefront of wine tourism development, with a number of its wineries becoming destinations with ‘clusters’ of offerings such as trails, restaurants, cafés, food stores, wildlife, and more (Carter, 2016).

Clusters are believed to generate innovation (Terstriep and Lüthje, 2018), and cluster theory (Porter, 1998) has been used to characterize the synergy of wine industry businesses that creates a competitive advantage as well as tourism development (Iordache et al., 2010; Michael, 2003). The current longitudinal case example builds on the foundational elements of wine tourism and extends the micro-cluster concept by examining the agritourism micro-cluster business model developed by one privately owned organization for the purpose of creating a wine farm destination. Three key aspects make this case unique: (1) the micro-cluster business model is real, rather than hypothetical; (2) multiple, complementary businesses with varying financial arrangements constitute the micro-cluster and contribute to both the physical development of a wine farm destination as well as the marketing efforts to attract visitors to the destination; and (3) the number of businesses in the micro-cluster, ownership variations, and visitation numbers is tracked over a 7-year time frame from March of 2011 through February of 2018 in order to demonstrate both the development of this micro cluster as well as the increased visitation to the wine farm destination that currently attracts more than 400,000 visitors annually.

This paper begins with a review of the literature and longitudinal overview of the example, followed by the business model for an agritourism micro-cluster and discussion of its characteristics. Lastly, this paper concludes with the importance of the model and its applicability to other wineries and agricultural businesses.

Literature review

Wine tourism and wine tourists

The first widely cited definition of wine tourism originated from the research of Hall (1996) and Macionis (1996). Hall (1996) also provided one of the earliest descriptions of wine tourist market segments (e.g., ‘wine lover’, ‘wine interested’ and ‘curious tourists’) and, with Macionis (Hall and Macionis, 1998; Macionis and Cambourne, 1994 cited in Hall and Macionis, 1998), outlined their characteristics, and stated that the market share for each of these three market segments is dependent on the following: ‘the individual characteristics of each winery and wine region in terms of its accessibility; the profile of its wine; the types of wine produced; marketing and promotion; attractiveness; and facilities’ (Hall and Macionis, 1998: 216). While there are a number of definitions of wine tourism, one of the most widely cited is ‘visitations to vineyards, wineries, wine festivals, and wine shows for which grape wine tasting and/or experiencing the attributes of a grape wine region are the prime motivating factors for visitors’ (Hall et al., 2000: 3).

Subsequent studies have expanded the description of wine tourists (Alebaki and Iakovidou, 2011; Bruwer et al., 2012; Charters and Ali-Knight, 2002), winery visitation (Alant and Bruwer, 2004; Dawson et al., 2011), visiting wine tourism destinations (Brown and Getz, 2005; Brown et al., 2007; Sparks, 2007), and the relationship between the experiential expectations/preferences of potential wine tourists and wine tourism (Asero and Patti, 2011; Back et al., 2018; Cohen and Ben-Nun, 2009; Galloway et al., 2008; Lee and Chang, 2012; Olsen et al., 2007; Quadri-Felitti and Fiore, 2012).

As previously stated, wine tourists have been shown to desire more from their winery experience than simply the tasting and purchasing of wine. It has been suggested that winery visits include a complex group of experiences (Mitchell and Hall, 2006), with Mitchell (2004) finding that only 23% of visitors to New Zealand wineries identified tasting and purchasing wine to be their main motivation for visiting. As wine tourism expands beyond just wine, a more fitting definition may be that wine tourism includes a particular destination, site, or event that is related to wine (Getz et al., 2008).

Tourists increasingly seek to engage in more authentic experiences, which has given rise to a growing interest in alternative forms of tourism. As most wineries are located in rural, agricultural areas, wine tourism often falls under the umbrellas of both rural tourism and agritourism, and frequently also falls into the trending categories of sustainable, green, eco, and slow tourism. Wine tourism has been increasing in popularity, paralleling the growth of rural tourism (Quadri-Felitti and Fiore, 2012), which has continued to develop in both North America and Europe (Gartner, 2004). It is also increasingly being linked to gastronomy or culinary tourism, with the United Nations World Tourism Organization (UNWTO) defining wine tourism as ‘a fundamental part of Gastronomy Tourism’ (UNWTO, 2016:1).

The experiential nature of wine tourism

Wine is considered to be a lifestyle product, a consumer choice rather than a necessity, with its consumption regarded as experiential (Bruwer and Alant, 2009). Wine tourists often enjoy beautiful rural landscapes and, besides the experiential nature of tasting or drinking wine, frequently get to see the vineyards and production process, and converse with winemakers. In their experience economy model, Pine and Gilmore (1998) state that experiences are distinct from both goods and services. The entertainment industry, theme parks, and attractions have always sold experiences, but the concept has been spreading to other industries including themed restaurants and retailing (Pine and Gilmore, 1998). Such experiential components are sought by consumers to differentiate otherwise similar choices (Oh et al., 2007).

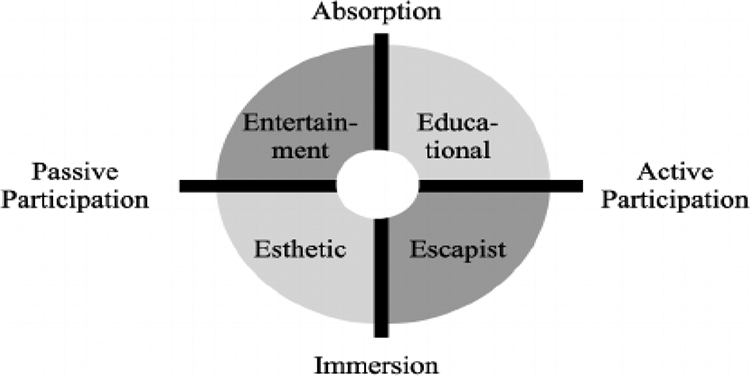

Pine and Gilmore’s (1998) Four Realms of an Experience delineated entertainment, educational, aesthetic, and escapist, known as ‘the 4Es’, into which experiences may be sorted, in their model (Figure 1). Experiences may fall into multiple quadrants, with their position on the horizontal axis representing the degree of consumer participation and their position on the vertical axis demonstrating the degree of immersion or absorption. Pine and Gilmore (1999) argued that service businesses should shift their offerings to staged experiences to make them more memorable. Quadri-Felitti and Fiore (2012) posited that the 4Es ‘are equally relevant and useful in conceptualizing the wine tourism experience’ (p. 7), and suggested, ‘a more encompassing view of the experiential nature of wine tourism’ (p. 7). What has become known as Consumer Experience Tourism (CET) is also increasingly used as a strategic tool to strengthen the bond between consumers and brands (Mitchell and Mitchell, 2000). CET represents a diverse group of experiences, including manufacturing plant tours, company visitor centers, tasting centers, and company themed theme parks and stores. A disproportionate number of the tourist activities included in CET are provided by producers of frequently purchased consumer staples such as food and beverages (Mitchell and Orwig, 2002), especially wineries, breweries, and distilleries.

The four realms of an experience.

Another key to the wine tourism experience is authenticity (Pine and Gilmore, 1999). Local food may enhance the authenticity of the visitor experience by connecting the consumer to the region, culture, and heritage (Sims, 2009). Chhabra (2010) showed that authenticity has become an important indicator for heritage tourism, by enriching both the tourist experience and satisfaction. These same arguments may hold for wine tourism.

In recent years there has been considerable consolidation within the wine distribution sector, reducing the number of distributors and making it more difficult for wineries to secure retail product placements (Thach and Olsen, 2006). This has put pressure particularly on small and medium-size wineries, which find it more difficult to obtain distribution and shelf space in increasingly corporate-controlled channels, thereby adding to the impetus of such wineries to form stronger and longer-lasting bonds with their consumers. Offering high quality, authentic, experiential, and memorable tourist experiences may be a key tool to assist smaller wineries and other agritourism businesses in achieving this.

Clustering

Cluster theory has been used to demonstrate the benefits of ‘geographic concentrations of interconnected companies and institutions in a particular field’ (Porter, 1998: 78). One of Porter’s (1998: 79) examples of cluster theory was its applicability to the California wine industry, stating that clusters can take various forms and may include producers of complementary products, specialized support providers, and trade associations. The key to the economic success of the cluster was the way in which companies compete. Specifically, clusters affect competition by increasing the output of area-based companies, driving the pace of innovation, and stimulating the development of new business, which in turn strengthens and increases the size of the cluster (Porter, 1998). Porter (1998: 78) also links his California Wine Cluster to other California clusters in tourism, food and restaurants, and agriculture, although these clusters are said to have weaker linkages than complementary industries such as barrel and equipment makers.

Although cluster theory was conceived by Porter (1998) as a way to consider the economic benefits and competitive advantage gained by clusters of co-located industrial firms in a particular field that are economically interdependent, additional ways to conceive of clusters have emerged (Donahue et al., 2018; Estevão and Ferreira, 2012; Jackson and Murphy, 2006). For example, Michael (2003, 2007) described three forms of clustering: (1) ‘horizontal clustering’—with firms as competitors, (2) ‘vertical clustering’—with firms co-located in the supply chain, and (3) ‘diagonal clustering’—with firms as complimentary, each adding value to the others in the cluster. Donahue et al. (2018: 5) offer three models of cluster organizational structure: (1) ‘cluster hub’—with one organization taking the lead, (2) ‘shared leadership’—with two or more organizations taking joint leadership, and (3) ‘holding company’—with one organization leading several cluster initiatives.

Although geographic proximity of firms is one of the required components of a cluster along with a critical mass of firms and economic interdependence (Donahue et al., 2018: 17), the structure of the cluster and the level of engaged interaction among its members influence how the cluster develops and how well it works (Donahue et al., 2018; Michael, 2003). In addition, Donahue et al. (2018) state that individual leaders are the key drivers of successful clusters and that clusters anchored by a physical center or cluster hub that ties the enterprises together in a visible way contribute to their success.

Cluster theory is perfectly suited to the evaluation of the performance of tourism clusters, which belong to the service class of clusters, and has more recently been used for research in this field (Čolović et al., 2016). For example, tourism-related studies have used cluster theory to explore regional tourism development and competitiveness (Estevão and Ferreira, 2012; Iordache et al., 2010; Jackson and Murphy, 2006; Lade, 2006, 2010; Malakauskaite and Navickas, 2010) and to explore both the competitive and collaborative strengths of tourism clusters (Michael, 2003, 2007; Murphy, 2002). However, less attention has been paid to the role of clusters in developing a region and many countries lack studies on tourism sector clusters (Estevão and Ferreira, 2012).

Much tourism takes place in what we refer to as ‘tourist destinations’, which are, in fact, tourism clusters, providing a variety of both competing and complementary tourist facilities as well as companies that supply and service these tourism providers. The wine industry is another area well suited to cluster analysis, with wineries and their related industries frequently grouped as a result of the requirements of both geological and climatic conditions. Much has changed in the wine industry in the 21st century as Direct to Consumer (DTC) sales make up 61 percent of the average U.S. family-owned winery’s revenue with 42 percent originating from tasting room sales and 36 percent from wine clubs, thereby demonstrating the importance of cellar door visitation (McMillian, 2019). Thus, it is not surprising that many wineries offer visitor experiences beyond traditional wine tasting and sales, with wine tourism important to the economic success of many wineries.

With the evolution of winery tourism and the desire by wine tourists for a more diverse range of experiences (Back et al., 2018; Brown et al., 2007; Bruwer and Alant, 2009; Cohen and Ben-Nun, 2009; Dawson et al., 2011; Getz and Brown, 2006; Getz et al., 2008; Park et al., 2019), many wineries have expanded their offering into a broader-based agritourism product with multiple activities and experiences for visitors on a single wine farm (Back, 2012). When such activities and experiences are owned by a single entity, it may be argued that they represent business diversification rather than a cluster. However, when there is diversified ownership of such experiences and attractions, the development may be termed a ‘micro-cluster’.

Micro-clustering

The term ‘Micro-clustering’ has been used in relation to the creation of economic and social opportunities in smaller communities. This may be accomplished by developing clusters of complementary businesses that ‘collectively deliver a bundle of attributes to make up a specialized regional product’ (Michael, 2003: 133), while also creating both economic and social opportunities, especially in smaller communities (Michael, 2003). Micro-clusters provide access to established infrastructure for smaller businesses (Peters et al., 2015), as well as opportunities for innovation and growth for the businesses comprising the cluster (UNIDO, 2010). Thus, the formation of micro-clusters may be particularly relevant to tourism in rural areas, where the concepts of networks and networking are used to explain cooperation between small tourism firms, thereby enhancing economic growth (Ewen, 2007). In this regard, wine tourism micro-clusters, whereby multiple wineries are clustered in a single geographic area, have been found to create a regional identity, while also allowing smaller wineries access to shared resources, specialists, and knowledge (Grimstad and Burgess, 2014).

Although several wineries offer other activities and experiences beyond those directly related to wine (Back, 2012; Back et al., 2019; Carter, 2016), few have achieved the success shown by the South African wine company presented in the following longitudinal case. Using micro-clustering of complementary, highly experiential businesses and a novel business model of diversified ownership, this privately-held company has created a highly successful wine farm tourist destination.

Case example—The Fairview Trust micro-cluster, South Africa: A longitudinal overview

The Fairview Trust (FT) in Paarl, South Africa is a farming business owned by a private family trust, with wine and cheese as its principal products. Two of its contiguous wine farms, Fairview and De Leeuwenjagt, have become home to a highly successful collection of authentic, experiential, and holistically synergistic businesses, and show how a micro-cluster of complementary enterprises located in a single location and using a novel business model can evolve into a major tourist destination.

History

The Fairview farm, located on the slopes of Paarl Mountain about 50 km from Cape Town, was founded in 1693 and comprises around 230 ha. Neighboring De Leeuwenjagt, comprising around 400 ha and established a year earlier, was acquired by FT in 2011 as the home for its Spice Route wine brand.

By the 1960s, Fairview had become a mixed-use farm, raising livestock, growing grapes, and producing milk, eggs, and wine. In 1980, Fairview started its cheese business, having imported a herd of Swiss Saanen goats. Today Fairview concentrates its core business on wine and cheese production. What sets FT apart from other agricultural firms, however, is the size of its tourism business, attracting more than 400,000 visitors annually since 2012. Putting this into perspective, California’s Napa Valley attracted 3.5 million visitors in 2016 (Visit Napa Valley, 2019). This single South African agritourism attraction, therefore, received more than 13.5% of the total number of visitors received by the entire Napa Valley in 2016.

Evolution

According to the owners, the growth in the tourism business at Fairview evolved to keep up with visitor numbers. In the 1970s tourists who happened to pass the farm’s entrance were enticed to visit by a hand-painted sign, with the wines poured at a table in a barn. With the addition of a range of exotic cheeses and the construction of an iconic ‘Goat Tower’ in the 1980s, visitor numbers began to grow and a wine and cheese tasting room was added and regularly expanded to accommodate growing visitor numbers. In 2004, an old barrel room was transformed into a restaurant and a bakery added.

Fairview continued to increase its tourist offering with the opening of a delicatessen showcasing its products together with a range of locally made artisanal food products in 2007. This was followed by the opening of a Master Tasting Room, providing seated, tutored tastings for wine aficionados who desired more than the standard counter tasting, thereby segmenting wine-tasting visitors into two groups, with differentiated offerings (the entrance to the Fairview tasting rooms is depicted in Figure 2). Fairview’s most recent addition to its visitor experiences is the Junior Cheese Masters, where children learn to milk goats and make their own cheese. The children also roll out their own pita bread dough and have it baked to enjoy with their cheese.

The Fairview farm tasting rooms.

Expansion

In 2011, neighboring farm De Leeuwenjagt, home to a winery, tasting room, restaurant, bed and breakfast, and a glass blowing studio, was purchased by FT. Renovations to existing farm buildings and new construction have resulted in the Spice Route Destination, currently comprising the following ventures (March 2019) (tabulated in Table 1):

Full ownership: Wine tasting room, offering indoor and outdoor seated wine tastings, also available paired with chocolate or charcuterie; brewery restaurant, adjoining the onsite brewery and serving craft beers, cured meats and sausages, and gourmet burgers and fries; gift shop, selling a variety of home, gift, and jewelry items, mainly from local artists. A children’s playground (non-revenue producing) has recently been added.

Partnership: A partnership was entered into with an established Swedish beer brewing company, thereby drawing on existing expertise and resulting in the establishment of a craft brewery. Visitors can observe the beer production and bottling processes, and taste and purchase the range of craft beers.

Independent businesses (paying turnover rental): Fine dining restaurant, with dishes created to pair with Spice Route wines; Chocolate factory located in the farm’s historic manor house where visitors can watch the cacao beans being roasted, view chocolate being made, participate in chocolate tastings and workshops, and purchase a wide range of chocolates; Café that roasts its own coffee beans and offers gourmet coffees, coffee beans, home baked cakes and home-made ice cream; Micro-distillery producing gin using indigenous botanicals, where visitors may view the production process and engage in tasting; Pizzeria adjoining the distillery, offering brick oven pizzas as well as pasta and tapas, paired with the farm’s wine and beer on tap; Deli, located in the old farm schoolhouse and producing jams, preserves, chutneys, glazes, and herb and spice blends, with visitors able to view production; Charcuterie, producing hand salted, hung and cured pasture-reared meats that may be tasted; Glass blowing studio, where visitors can watch unique pieces being created; Ceramics studio, showcasing handmade ceramics by leading local ceramic artists; Adventure trails, offering walking, running and mountain biking along the farm’s mountain trails; Pilates Studio, with full Pilates training facilities.

Ventures at spice route destination.

The destination

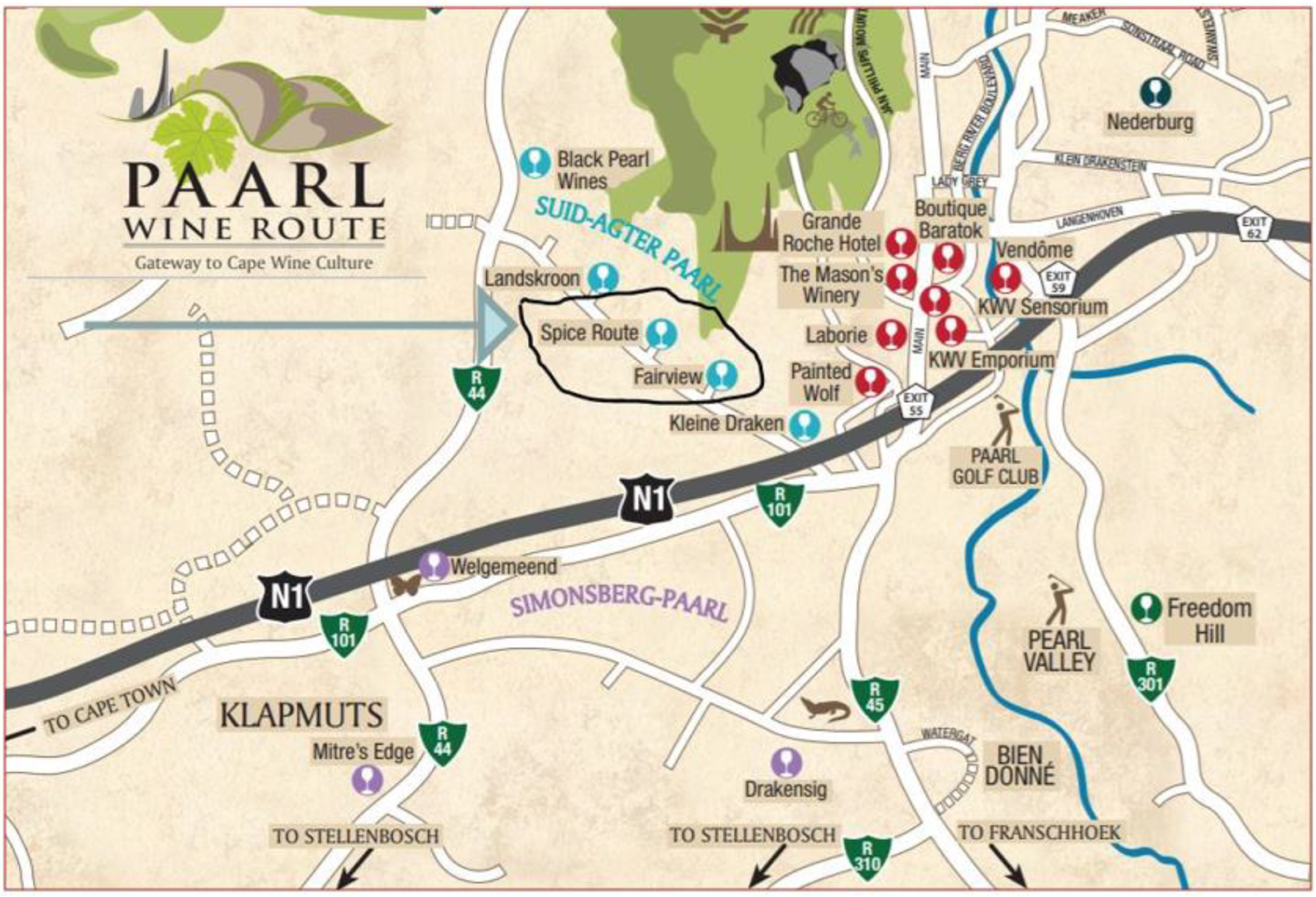

This micro-cluster of complementary businesses spread across two adjacent wine farms has created a self-contained destination. Although situated in the heart of the Western Cape’s Winelands and on the established Paarl wine route (see Figure 3), many visitors to this destination spend the entire day visiting, tasting, dining, and purchasing at the different FT venues. It is believed that a large part of their success is due to the authenticity and experiential nature of all these ventures (Back et al., 2019). Most of the products sold are grown and/or produced on these farms or other farms owned by FT, while ‘inauthentic’ items such as logo apparel, wine paraphernalia, and souvenirs, so often found in winery tasting rooms, are generally unavailable. Not only are most of the products sold produced on the farms but, other than the restaurants and the cheese factory, visitors may view the production processes. In the restaurants, many of the ingredients used are grown or produced on the properties. All of this adds to a profound sense of authenticity, found to be experienced by those seeking increasingly popular ‘farm-to-fork’ or ‘slow food’ experiences (Chung et al., 2018). Thus, even with so large a throughput of visitors, this micro-cluster is unlikely to be considered a ‘tourist trap’.

Map of wine region showing Fairview Trust’s destination location. Source: Adapted from ShowMe™SouthAfrica (n.d.).

All of the venues are highly experiential, with guests able not only to view production, but also able to wander through vineyards and along the farm trails, see where products are produced or grown, and enjoy the magnificent rural scenery. Additionally, at many of the venues, visitors can chat with and learn from passionate and experienced artisans, adding an educational dimension to the experience. Naturally, all products are also for sale to visitors.

Business model for an agritourism micro-cluster

One of the keys to the success of any business, but particularly to the types of smaller, artisanal businesses found in this micro-cluster, is that they require skilled, talented, passionate, and dedicated owners and/or managers and staff. Passionate owners can enhance their firm’s entrepreneurial culture as well as its financial performance through being more focused on innovation and entrepreneurship (Haar et al., 2009). FT recognizes that it cannot be expert at everything and this is reflected in its business model, as depicted in Figure 4. FT, therefore, has full ownership of its core businesses, albeit with a percentage of employee ownership. These include its vineyards, wineries, goat farm, and cheese factory, as well as the wine tasting rooms, two of the restaurants, and the gift shop. In other cases, FT has partnered with an expert in a particular field, e.g. the brewery is owned in partnership with a Swedish brewing company. The creation of such partnerships allows for a high level of expertise, while FT remains the landlord in addition to being a partner in the business. FT is also a landlord, supplying its independent tenants, who are experts in their fields, with infrastructure, including premises built or renovated to their specifications, in return for a percentage of gross revenue (turnover rental). This is the case with a number of the farms’ attractions, as previously detailed.

The FT micro-cluster business model.

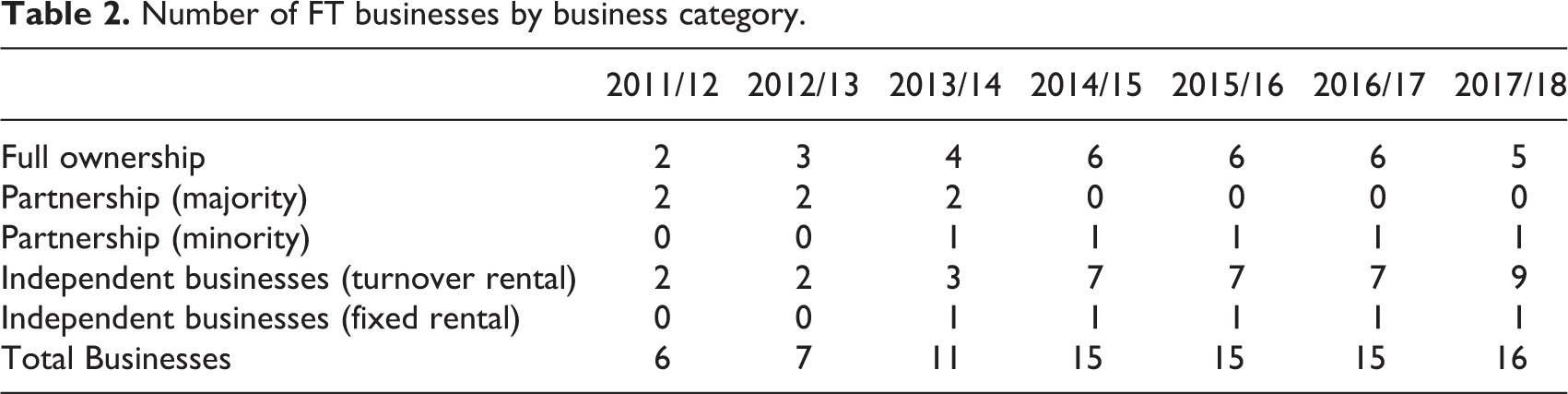

The evolution of the number of business units held by FT in each category is reflected in Table 2. FT went from just six business units in 2011/12 to 16 different units by 2017/18 with rapid diversification into additional full ownership businesses, a minority partnership, an increase in the number of independent businesses paying turnover rental, and introducing one fixed rental business (residential property rentals that are not part of the tourist offering). While the full ownership businesses have generated the majority of FT’s tourism-related revenue (non-tourism related revenues from the production of wine and cheese, as well as other farming operations, are not included) over the last 7 years, revenue from the full ownership businesses has dropped from 62.3% of total revenue in 2011/12 to closer to 50% of revenue since 2016, suggesting increased value of diversification (see Table 3). In terms of tourism-related revenues to FT in 2016/17, full ownership business contributed 51%, independent businesses 41%, and partnerships 8%, compared with 66%, 30%, and 4% respectively in 2013/14, reflecting the addition of two independent businesses and an increase in the partnership’s beer production during this interval. Turnover rental from independent businesses reflects the second largest source of revenues for FT, with more than 40% of income coming from turnover rentals in 2017/18.

Number of FT businesses by business category.

Percent of FT revenue by business category.

While an exact breakdown of each business’ share of the revenue contribution was not supplied, by dividing the percentage of FT revenue by category by the number of businesses per category, a better sense of the contribution by each business unit can be obtained. Although independent and full ownership businesses may be bringing in the most revenue overall, on a per business unit basis, the minority partnership is contributing more than the independent businesses. Using 2017 data, full ownership businesses contributed about 10% of the revenue each, while the minority partnership business brought in 8.6%, and independent business units 4.5% of the revenue each.

FT uses a portion of revenues collected to market the entire destination. Between the years 2011 and 2018, spending on marketing has stayed around the 2% of revenue level mark for tourism specific marketing (as opposed to product marketing), dipping down to a low of 1.65% of revenue during the 2015/16 marketing year (see Table 4). This is in line with many other businesses that allocate 2–3% of gross revenues to marketing (Beesley, 2013). Much of the marketing is through public relations, destination-wide events, and social media. This, in turn, drives visitor traffic to the destination as a whole, thereby benefitting all business units.

FT marketing spending and returns.

FT does not currently have an accurate way to measure number of the visitors to the sites, however, estimated visitor numbers were provided and are presented in Table 4. Visitor numbers were negatively affected by roadwork and road closures between 2015 and 2017, and severe drought in the Western Cape Province of South Africa is believed to have negatively influenced visitor numbers between 2017 and 2018 (Roelf, 2018). However, marketing spend has increased since 2011, and while there were initial increases in visitor numbers, more recently those numbers have declined (likely attributed to the aforementioned external factors).

In 2011, FT spent approximately 2.07 percent of gross revenue on tourism marketing, and by 2017 that marketing spend had increased to around 2.37 percent of gross revenue. While some might view this increase as a negative outcome, we must also consider that FT has become more of a tourism destination with more opportunities for visitors to spend their money on a variety of goods and experiences, increasing the revenue obtained by each visitor to the site and offsetting (and/or justifying) the increase in marketing money used to capture those visitors. FT’s investment in marketing has nearly doubled since 2011; however, if marketing expenses are considered by the number of businesses held, those expenses have declined by 28% as the expenses can be distributed out over a greater number of businesses.

Although actual destination revenue figures were not disclosed, FT tourism-related revenue increased each year from 2014 to 2017 (see Table 3). Recent downturns in revenue can likely be attributed to the environmental conditions in the region that have affected tourism as a whole. Most notably, however, is the increase in revenue between years 2012/13 and 2013/14 by more than 50%. This increase corresponds to the significant increase in the number of businesses held by FT with the addition of five new business units (art gallery, minority partnership in the brewery, turnover rental from the restaurant/distillery, deli, and residential property rentals as fixed rentals).

The data provided by FT lend some further insight into the structure of the FT business model, yet there are still many considerations that cannot be answered without additional data. Revenue sources only provide one side of the story and don’t capture the expenses, investments, and risks associated with each type of business added to the FT destination. Independent and full ownership businesses are generating the most revenue for FT; however, those two business structures are very different and present different challenges, risks, and potential rewards for the owners of FT.

FT Micro-cluster business model’s position within the clustering dialogue

The cluster-types discussed in the literature that are closest to the micro-cluster business model presented in this case include ‘Diagonal Clustering’ (Michael, 2003), whereby businesses within the cluster share a close symbiotic relationship, and both the ‘Cluster Hub’ and the ‘Cluster “Holding Company”’ (Donahue et al., 2018). In the Cluster Hub varietal, one organization takes the leading role and positions the cluster locally and in targeted markets. In the Cluster ‘Holding Company’ varietal, one organization leads multiple cluster initiatives. More importantly, Donahue et al. (2018) note that they are only aware of one example of this cluster approach—the Central Indiana Corporate Partnership described in their case study (Donahue et al., 2018: 30). The FT micro-cluster business model may well be a second example of this type of cluster and the first within the tourism industry.

Several factors contribute to the success of this business model: The buildout projects a cohesive whole that reflects the individual characteristics of each business while simultaneously blending the look and aesthetics into that of these historic wine farms. The group of businesses within the cluster were carefully selected to create the cohesive whole—not only for the experiential dimension but also in the more typical nature of complementary/symbiotic firms in the ‘Diagonal Clustering’ suggested by Michael (2003), or firms that have the ability to provide complimentary products to other members of the clusters suggested by Porter (1998). All of Pine and Gilmore’s (1998) Four Realms of an Experience (i.e., entertainment—being able to view the various production processes; educational—learning about the production processes; aesthetic—the aesthetic appeal of the buildings, interior designs, and landscape; and escapist—being in a tranquil, rural environment) are included within this micro-cluster. FT has passionate, entrepreneurial leaders guiding and developing the cluster and the relationships among the businesses within the cluster are both close and supportive. In addition, this cluster is anchored specifically to a single business entity and location. It has been suggested by Michael (2003) and Donahue et al. (2018) that such cluster attributes generate more successful clusters.

Discussion, implications, and conclusions

Discussion

This study shows how a single South African organization has created a novel business model, initially through natural evolution and then by design, by forming a micro-cluster of highly successful complementary businesses on its two adjacent wine farms. Further, it demonstrates how the micro-clustering of complementary, holistically synergistic businesses, within a single, rural location can be used to create a highly successful, major agritourism destination.

Using a business model where diverse forms of ownership allow for high levels of expertise creates synergistic relationships whereby the individual businesses benefit from being part of the cluster and from the marketing of the destination as a whole, while also being provided with infrastructure. Conversely, the farms’ owners benefit from the quality and diversity that these businesses add, thereby drawing additional visitors, benefiting their wholly-owned ventures and creating additional revenues. Additionally, by not owning all the businesses within the cluster, the farms’ owners limit their risk exposure—if a business within the cluster fails, the cluster still survives. The growth in tourism revenues is accompanied by an increase in the percentage of products sold directly to consumers. Besides DTC sales being more profitable, this has also lessened FT’s dependence on the increasingly competitive and expensive, corporately controlled distribution channels. While examples of similar winery and agritourism groupings of businesses in a single farm location do exist both in South Africa and elsewhere, they tend to be owned by a single person or entity and may, therefore, be viewed more as business diversification than a true micro-cluster. The authors are unaware of any other winery/agritourism farms having either the diversity of activities and experiences or the diverse forms of ownership seen in FT micro-cluster.

Theoretical implications

The current study extends Porter’s (1998) cluster theory and builds on the work of Donahue et al. (2018), Estevão and Ferreira (2012), Jackson and Murphy (2006), Michael (2003, 2007), and Murphy (2002). More specifically, a new application for diagonal clustering is shown, thereby extending the work of Michael (2003, 2007) while demonstrating the application of a ‘cluster hub’ in a wine tourism/agritourism context extends the work of Donahue et al. (2018). The study also identifies what is believed to be only the second business identified that fits Donahue et al.’s (2018) ‘cluster “holding company”’ type of cluster and the first in a tourism context. Furthermore, the study extends the work of Peters et al. (2015) by showing a further application of clustering providing infrastructure for smaller businesses.

No previous studies have been found using either cluster theory or the concept of micro-clustering to explore the creation of a tourist destination by a single business entity or at a single business location. Furthermore, this study extends the academic literature by showing a new business model encompassing a variety of forms of ownership used within a single business location and marketed as a cohesive whole, used to create a successful tourism destination.

This paper provides a solid basis for theory building. To test the benefits of different business partnerships/arrangements on the benefits identified in this example, the following propositions are suggested to be tested empirically in future research: (1) Turnover rental tenant arrangements are the most profitable means for agritourism farms to increase revenue without substantial capital investment; (2) Diagonal micro-clustering on agritourism farms will lead to an increase in visitors and profitability; (3) The ‘Cluster-hub’ model of clustering with centralized marketing will increase revenue for businesses within the cluster.

Practical implications

The business model shown also has interesting managerial implications for applied tourism development, and may be relevant not only to other wine farms but also to other agritourism locations and businesses in rural areas more generally. The creation of a micro-clustered destination may be beneficial not only to the businesses concerned but also to the economic development and prosperity of the community as a whole. It is therefore suggested that farm owners wishing to expand their tourism offerings consider using such a mixed-ownership type of business model to cluster synergistic businesses on their farms, thereby increasing the diversity of their offerings, adding skills and expertise, and potentially spreading capital investment and risk. Additionally, the model may also be applicable to the development of ‘cluster hub’ and ‘cluster “holding company”’ types of attractions in non-rural locations, such as seaside attractions and urban retail and food markets.

Limitations and future research

Although this study has provided significant insights into a new business model used in micro-clustering in a wine tourism/agritourism context, no study is devoid of limitations. This research, therefore, offers an avenue for future research to build on the findings of the study. First, this study investigated a single micro-cluster. The composition and finances of other micro-clusters may be different and should be investigated. Second, only one specific type of micro-cluster was investigated. Future research could delve into whether similar types of micro-cluster exist in other contexts, and how they may differ structurally. Third, a micro-cluster in a single geographic location, i.e. South Africa, was studied. It would be interesting to find out whether a similar model would be generalizable to other countries and locations. Fourth, a more in-depth investigation of the finances and financing of similar business models would be of interest, although obtaining such confidential information from privately held businesses remains a challenge.

Footnotes

Declaration of conflicting interests

The author(s) declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: One of the authors is a relative of the owners of the business in the case study, which allowed special access to data of the organization. The authors have no financial interest in the business.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.