Abstract

In the last few years the so-called ‘360 deal’, in which record labels receive a portion of income from revenue streams such as merchandising and publishing, have become increasingly common in the recording industry. However, the most publicised 360 deals have been made not by labels but by Live Nation, the world’s largest live music promoter, and some have argued that the emergence of the 360 deal reflects a shift in the balance of power within the music industry. This article provides an overview of 360 deals, discussing their emergence and overall structure as well as arguments for and against the 360 approach. It examines the broader implications of the 360 deal, concluding that the current situation of the major labels may not be quite as bad as is commonly perceived, and that the 360 approach may help them manage the challenges that they have faced in the last decade.

The recording industry has been in a well-documented state of upheaval since the start of the century. With income from the sales of recorded music falling by approximately 40 percent since 2000 (International Federation of the Phonographic Industry (IFPI), 2011), the four major record labels which dominate the sector (EMI, Sony, Warners and Universal) seem particularly vulnerable, and some commentators have questioned the long-term viability of selling recorded music (e.g. Wikstrom, 2009). The transformations in popular music production and consumption made possible by internet technology go beyond merely the selling and buying of records, however, with the nature of popular music stardom itself changing under the influence of advanced branding and marketing techniques. These broader transformations are affecting the ways in which record labels negotiate contracts with their artists. In particular, the last few years have seen the emergence of the ‘360’ or ‘multi-rights’ deal, in which the record label participates in and receives income from a range of musical activities beyond the sales of recordings. These new contracts are a clear reflection of the changing nature of the popular music economy but are also part of the wider discourse regarding these changes given that the most publicised 360 deals have been concluded not by labels but by Live Nation, the world’s largest concert promoter. In contrast with the fortunes of the recorded music industry, it is commonly argued that live music is experiencing an economic boom at the moment (e.g. Bintliff, 2010), and the 360 deals that Live Nation has struck with, for example, Madonna and Jay-Z, have been used as evidence of a shifting balance of power within the music industry.

However, this situation may not be so clear-cut. Considered in a broader historical perspective, the prevalence of the 360 deal demonstrates important historical continuities as well as change, and in this article I will outline and contextualise the significance of the 360 deal. The article begins by discussing the emergence of this new type of contract, before considering the relative positions of Live Nation and the major labels. It then offers more fine-grained detail on the nature of 360 contracts and the arguments for and against their use. Finally, the article examines the implications of these new contractual relationships, concluding that the major labels’ situation may not be quite as bad as is commonly perceived, and that the 360 approach may help them manage the challenges that they face.

The emergence of the 360 deal

Robbie Williams and EMI, 2002

Although the deal between Williams, one of the biggest stars in Europe, and EMI was not an actual 360 deal and occurred before the 360 had been conceptualised as such, it was an innovative deal that garnered much media attention and offers a significant precursor to deals later in the decade. In this instance ‘the deal’ was actually two separate deals, the first of which was a fairly standard recording contract, albeit one with an advance and royalty rate befitting Williams’ superstar status: Williams received £25m to £30m in advance for his next two albums (the already-recorded Escapology and a ‘Greatest Hits’ package), with another £25m to £30m advance for a further four albums (including one more greatest hits). It was the second part of the deal that makes the Williams deal an innovative precursor to the 360: unlike a conventional recording contract in which the record label receives a proportion of income generated by recordings only, Williams agreed to share some of the income generated by his activities outside of recordings. An independent company, In Good Company, was formed to manage these income streams, reported in the media as including TV specials, merchandising, publishing, touring, sponsorship and ‘other areas’. The company was part-owned by Williams and EMI on a 75/25 basis.

EMI received significant press criticism for this deal. Following in the wake of a number of high-profile contract buyouts, including paying Mariah Carey a reported $28m to never record for them again (Billboard, 2002), the Williams deal was portrayed as yet another example of recording industry extravagance and profligacy. The value of the deal was widely exaggerated, and it was incorrectly assumed that the deal relied on Williams breaking America to be profitable for the company. In reality, it was quite a sensible one for EMI and, according to Wadsworth, ‘went into profit for EMI pretty quickly’ (Forde, 2010: 66). It also showed a considerable amount of foresight in seeking revenue streams outside of record sales, the significance of which other major labels were slow to realise.

Korn and EMI, 2005; Korn and Live Nation, 2006

EMI were still leading the way when in 2005 they signed a deal with Korn that bears more resemblance to a 360 deal. The deal covered a two-album and touring cycle period, and provided Korn with a $25m advance for which EMI received 30 percent of all of Korn’s income until 2010. It is not clear that this deal was as successful for EMI as the Williams deal. Given that Korn received 70 percent of net profits from their record sales (far in excess of any conventional royalty rate achievable by even a superstar artist), profitability relied heavily on Korn’s touring schedule, and it was expected that Korn would perform roughly 100 shows per tour (Garrity, 2005).

However, the significance of Korn in the development of the 360 deal lies in a second deal that they signed a few months later with Live Nation. Live Nation paid Korn $3m, plus a share of concessions and parking fees at Live Nation venues, in return for a 6 percent share of Korn’s income from touring, licensing, publishing, merchandising and record sales. This deal received little media coverage at the time – certainly less than the deal with EMI – but with the benefit of hindsight, it seems significant, with Live Nation conceivably using the Korn deal as a pilot project to test its new strategy of moving beyond tour promotion. By acting as a ‘dry run’ for negotiating with artists on areas other than live concerts and for getting a sense of the practicalities of licensing, for example, Live Nation would have learned from this relatively small deal as it eyed bigger catches.

Madonna and Live Nation, 2007

The Madonna deal was a big deal in every sense. Most obviously, the amounts of money involved were very high. However, this deal was also symbolically significant. First, it brought the concept of the 360 deal into public discourse. Second, and more significantly, the fact that a star as influential as Madonna signed a deal with a tour promoter rather than with a record label was understood to reflect major changes in the music industry, demonstrating that the major labels were becoming much weaker. As Madonna noted, ‘the paradigm in the music business has shifted’ (BBC, 2007).

The deal was widely reported as being worth $120m, although the full financial details were not disclosed. Reportedly, Madonna received 1.2m Live Nation shares (worth approximately $24.5m), a $17.5m signing bonus and a $17m to $20m advance per album for at least three albums. According to Live Nation CEO Michael Rapino, in return for their investment, Live Nation would receive a portion of ‘everything that Madonna will do music-related over the next ten years, anywhere in the world, including touring, private events, studio albums, DVDs, film [and] TV’ (Ashton, 2007: 2).

However, given its outlay, the proportion of income that Live Nation will receive may not be as high as expected. Reportedly, Madonna will retain 70 percent of merchandising income, 50 percent of licensing income and up to 90 percent of touring income. 1 The economics of this deal seem risky for Live Nation, particularly as the deal does not obligate Madonna to tour. It is by no means certain that Live Nation will make a direct return on its investment, and it is notable that the value of Live Nation’s shares dropped sharply when the deal was announced (Karubian, 2009). However, it can be argued that for Live Nation this deal was not merely about the bottom line; rather, that it served broader symbolic purposes in establishing itself as a major player in the new music industry, in gaining a figurehead for demonstrating its new strategy, and in acquiring a prestige artist who would attract other artists to the company.

The rise of Live Nation

Live Nation’s new strategy involved the formation of a new division, Artist Nation, which, according to its press release, ‘redefines the music industry with [a] unified rights model’, its stated goal being to ‘partner with artists to manage their diverse rights, grow their fanbases and provide a direct connection to fans’ (Live Nation, 2007). Artist Nation consists of five major divisions: recorded music; merchandising; fan sites and ticketing; broadcast rights and digital rights management; and sponsorship and marketing. It is notable that music publishing is absent from the list. Publishing has been declared as not a priority area for Live Nation, which is interesting because music publishing is commonly perceived to be one of the most dependable forms of music revenue in the uncertain digital future. It is also worth noting that although Artist Nation has a recorded music division, it lacks the infrastructure of a major label, especially in relation to the distribution of recordings. One repercussion is that Live Nation will have to license records to one of the major labels for distribution. For example, Roc-Nation, the label established by Jay-Z and Live Nation, has signed a deal with Sony to distribute its releases. These distribution deals, likely to be completed on a case-by-case basis, will cost Live Nation roughly one-third of the wholesale income of the record. 2

To achieve its aim of becoming a ‘one-stop shop’ for artists in managing their touring, merchandising, fan sites and so on, Live Nation has been aggressively acquiring companies with expertise in relevant areas. The most notable acquisitions are listed in Table 1.

Notable Live Nation acquisitions 2006–2008 a

Live Nation’s acquisitions did not end in 2008. For example, in 2010 it acquired or took major stakes in 14 new companies (Peoples, 2011a).

Acquisitions have centred mainly on merchandising, online fan clubs and ticketing, and have occurred simultaneously with the more widely-publicised merger with Ticketmaster. It seems likely that Live Nation’s strategy involves bringing ticketing and online fan clubs together in more targeted ways (for example, in the promotion of VIP fan packages for concert attendance).

Alongside these company acquisitions, Live Nation also concluded a small number of 360 deals with other headline artists. Most notable among them was a $150m deal with the hip-hop star Jay-Z. This gained much media attention due to the value of the deal and, like the Madonna deal, the magnitude of the artist involved. However, the deal is interesting because alongside payment for Jay-Z’s own music (a $10m advance per album for a minimum of three albums, plus $20m for other rights such as licensing and publishing), the deal also involved the establishing of Roc-Nation, a joint venture which is effectively Jay-Z’s own record label. To finance Roc-Nation, Live Nation provided $25m to cover overheads for five years, and $25m for artist acquisitions.

Between March and July 2008, other major deals were signed with U2, Nickelback and Shakira, although the agreement with U2 was not technically a 360 deal as it did not cover recordings. However, it was a substantial agreement, with Live Nation agreeing to provide the band’s website management, tour promotion and merchandising for 12 years. The deal with Nickelback was comparable to the deal that EMI had signed with Korn three years earlier: Live Nation paid $50m to $70m for a share of 12 separate rights for a three-album and three touring cycle period. 3 The deal with Shakira was for a similar amount and for a 10-year period covering ‘tours, recordings, sponsorship and merchandise’. 4

This rash of signings in 2007 and 2008 meant that Live Nation had notable figureheads in pop, rock, hip-hop and Latin. The publicity surrounding these signings, contextualised by widespread commentary on the decline of the recording industry, meant that Live Nation was clearly presenting itself as the future of the music industry. The following slide, from a Live Nation investor presentation, shows its vision of how the music industry will develop. In it, rather than the record industry being at the centre of the music industry, live music (and thus Live Nation) will now be the core (Figure 1).

Slide from Live Nation investor presentation

The reaction of the major labels

EMI excepted, the major labels demonstrated an initial reluctance towards the 360 model. Shortly after taking over at Warner Music Group in 2004, Edgar Bronfman Jr said of deals such as Williams: ‘I’m not convinced it’s in my best interests. I’m presuming I have to give up something to get something’ (in Goodman, 2010: 256). Presumably, Bronfman felt that he was better off holding on to the most profitable part of the music industry: CDs. Conventionally, the production and especially the distribution of CDs have been the area of the music industry with the highest profit margins (with profit margins in the mid-twenties, compared with 5–7 percent in the live industry; Woods, 2009). The format was largely responsible for the recording industry’s boom during the 1990s, with major labels increasingly stripping away other facets of their companies in order to specialise in CD manufacture and distribution. Although CD sales had declined in the first few years of the 21st century, labels argued that this was caused primarily by piracy, and that the decline was a blip which could be rectified by improved intellectual property enforcement.

However, over the last few years it has become increasingly apparent that the decline of CD sales is not merely a blip and, furthermore, that sales of digital music are unlikely to make up for the fall in revenue since the CD peak. Labels are having to develop alternative revenue streams and generally have become persuaded as to the merits of the 360 approach. Ironically, Warners has been the label most aggressive in pursuing 360s, and by the end of 2007 had a policy that it would only sign new artists to such deals. As Bronfman Jr stated in that year, ‘we’re not going to continue to sign artists for recorded music revenue only’ (in Karubian, 2009: 423). To support its new strategy, Warners has acquired Artist Arena, a company specialising in online ticket sales and fan clubs, and launched Brand Asset Group to oversee artist branding.

Warners may be the most vocal supporter of the 360 model, but all of the majors are reorienting themselves towards this new approach, utilising various combinations of acquisition and internal reorganisation to support the model. For example, Universal has launched Twenty First Artists, an artist management agency, and Bravado, ‘the only global 360° full service merchandise company’, while Sony has collaborated with branding specialists Exposure to launch SBX, a ‘new communications and artists agency’ that, according to its website, ‘creates outstanding 360° solutions’. All of the majors are investing more in divisions that focus on licensing, synchronisation rights, merchandising and sponsorship.

However, the most significant change has been a rhetorical one: all of the majors have stopped calling themselves record labels and have started referring to themselves as ‘music companies’. When Roger Faxon was appointed head of EMI in 2010, he circulated a memo to staff in which he outlined his vision for the company, stating that the company would have a ‘more diversified revenue base’ in the future, becoming a service company in partnership with its artists which ‘we cannot continue to view … as being limited to selling records’ (this was the only use of the words ‘record’, ‘recording’ or ‘CD’ in the whole 3000-word memo). The goal, he stated, was to transform EMI into an ‘artist-focused global rights management business’, to become a ‘wholly different music company’ (Faxon, 2010). Similar sentiments can be found throughout what was once the recording industry. For example, Richard Story, the chief operating officer of Sony Music Continental Europe, described SBX as ‘a key pillar of our new business strategy. It delivers on our mission to transform Sony Music from a record label into a global music entertainment partner for our artists and brand clients’ (Exposure, 2008; emphasis added).

At least on the surface, the major labels have rethought their mission statements completely in the last few years. Indeed, while much has been written about the impending decline of the recording industry, the above statements enable us to assert confidently that the record industry already no longer exists; in its place stands the global music entertainment partner industry. 5

Characteristics of 360 deals

One thing that this means is that the 360 contract is now the normal contract that a recording artist will sign, described by Music Week as ‘standard for new acts at major labels and common among indies’ (Woods, 2010: 22). Initially they were more common in the USA than in the UK (Passman, 2011 suggests that this was the result of tougher restraint of trade laws), but are now becoming prevalent in the UK and other European countries: Warner has established 360 divisions in both France and Italy while, in Finland, despite legal challenges from the local Musicians’ Union, Universal is actively pursuing 360 deals. Clearly, the reach of the 360 deal is spreading.

So, what do 360 deals usually entail? In this section, I shall outline the broad conventions of 360 deals, but this data require two significant provisos. First, 360s remain relatively new and, as such, no clear standards have become institutionalised (although lawyers are reporting that things are now settling down and becoming more standardised; Woods, 2010). Second, contracts are private matters and many contain confidentiality clauses; therefore, getting the actual details of actual contracts is difficult. The figures outlined below are gathered from reports from managers, and especially lawyers with firsthand experience of 360 deals. There is enough consistency among their accounts to suggest some degree of reliability, although clearly this is not absolute.

A final point to make here is that the deals outlined earlier in this article, with superstars such as Madonna and Jay-Z, are irrelevant to any discussion of the conventions of the recording industry. Those blockbuster deals were important in establishing 360 as a concept but they are more like profit-sharing deals than recording contracts. These net profit deals will tend to be more generous to artists than royalty-based deals but are only available to the most powerful artists in the major label system, as their track record gives them a stronger bargaining position. 6 The majority of artists are in a weak bargaining position and will sign a contract with major record labels which pays the artist a royalty for each album sold. When the 360 was emerging it seems that labels sometimes would offer a bonus to the artist, such as a higher royalty rate or an unrecoupable advance, in exchange for the extra rights that they gave up. However, as the 360 has become more standard, these bonuses have vanished and ‘unless you’ve got enormous bargaining power, the record part of a 360 deal looks pretty much like a standalone record deal’ (Passman, 2011: 103).

The record deal is, however, only one part of the 360 package, the defining characteristic of which being that the label receives income from revenue streams outside of recordings. What other rights may be included? The most important ones are recordings, publishing, merchandising and touring (Passman, 2011 lists these as the four cumulative nineties of a 360, so that potentially one can make a ‘180 deal’ incorporating, for example, recordings plus publishing). There are also various subsidiary rights that could be discussed under these headings, such as secondary ticketing income. However, the breadth of rights that can be included leaves little outside of the contract: Nickelback’s deal with Live Nation included ‘literary rights’, while lawyer Bob Donnelly states that contracts can include things such as ‘the books that artists write [and] the Hollywood movies in which they act’ (2010: 4).

The non-recording parts of the 360 deal do tend to be more like profit-sharing agreements, with labels requiring a proportion of the artist’s net income. Passman (2011) suggests that most labels require 10–35 percent of non-recording sources, dependent upon the artist’s bargaining power, with most deals being in the 20–30 percent range. However, negotiations occur for each different kind of right, and so the percentage of income that a record label may request will vary across the different aspects of the deal. Using details from 360 contracts at Warners and an independent label, Day (2010) outlines the following percentage splits: ‘endorsements (15–20%), performance (10–30%), merchandising (20–50%) and film/TV money (15–40%)’.

An important distinction to make is between active and passive rights. In a passive deal, the label will request a percentage of the artist’s income from publishing, for example, but will not play a role in the management of those rights. So in this case, the artist can sign with a separate publisher but the record label will top-slice a percentage of the publishing revenue. By contrast, an active deal is when the label insists on having a role in rights management by, for example, demanding that the artist signs a deal with its in-house merchandising division. 7 Most deals are actually a mix of both active and passive rights: for example, by mid-2007 Warners’ policy was to insist on active rights in recordings, merchandising and fan clubs, with passive rights being negotiated for all other kinds of rights (Goodman, 2010).

The important thing to recognise is that these revenue streams can be cross-collaterised. Cross-collaterisation always has been a fundamental feature of recording industry contracts. In a conventional recording contract, the label pays the artist an advance for recording an album, which covers their subsistence while this happens. However, this advance is recoupable, which means that the artist must repay the advance from their subsequent income: that is, their record royalties. If the album sells less than expected and the artist does not earn enough royalties, they remain ‘unrecouped’. However, if any future album released under the contract is successful, royalties from the successful album can be used to recoup the advance of any previous albums. The technical term for this process is cross-collaterisation: all albums under the recording contract are cross-collaterised against each other. The same situation exists under a 360 deal, only now cross-collaterisation can occur from income sources other than recorded music. So, for example, the artist’s income from the sale of T-shirts can be used to offset the advance paid by the record label for recording an album. This does not necessarily mean that all of the different revenue sources will be cross-collaterised, as that is a matter for negotiation in each individual case, but this principle of cross-collaterisation from sources other than recordings is one of the fundamental characteristics of the 360 deal.

Justifications for the 360 deal

Given that the 360 deal is now the standard offered by major labels, it is important to consider how labels are justifying taking income from revenue streams other than recorded music. Broadly speaking, there are two different kinds of justification being provided: a ‘just desserts’ argument and an ‘active partnership’ argument. Before outlining these positions, it is important to recognise the context in which these justifications are being made. It is now obvious to the major labels that income from recorded music is not going to sustain them in the future; what is equally important is that labels are relying on everyone else recognising this as well. The major labels are extremely adept at using their business problems for rhetorical benefits. It seems unlikely that someone in the recording industry has not considered top-slicing alternative revenue streams in the past. However, this approach has not been pursued, partly because the profit margins from CDs meant that it was a low priority, but also because any such claims would have been unacceptable to other parties – it would have just looked too greedy. While by no means has the 360 deal has been accepted uncritically by others in the music industry, the public discourse concerning the ‘crisis of the music industry’ means that the shift to 360 seems more realistic at this moment.

In order to avoid accusations of outright greed, the labels need to justify taking income from areas which, in recent memory at least, have been deemed off-limits to them. The ‘just desserts’ position, in which labels emphasise the role that they play in building the artist’s career, which then positively impacts on a much wider range of income than records, is summarised neatly by Donald Passman: Of all the players in your [the artist’s] life, we [the label] are the only ones who spend substantial money to make you a household name. Then, thanks to our rocket launch, you make tons of money by touring, songwriting, selling your face to teenagers on T-shirts etc. This isn’t right. We should share in all the businesses we help build for you. (2011: 102)

In this instance, labels are emphasising the role that they already play in developing artists’ careers – not something that they claim they will do in the future, rather something they have always done but are now making explicit. As the former managing director of Parlophone, Miles Leonard, stated: [Labels] invest a lot of money in making an artist – the exposure to the public is huge. The knock-on effect is celebrity endorsements, which we don’t share the income from. Going forward, that is going to have to change. Income from record sales isn’t enough to sustain the artist. (in Cardew, 2007a: 4)

Of course, there are countless examples of artists complaining that their label failed to support their career, did not promote their albums adequately, did not support their artistic directions, financially exploited them and so forth. However, whatever dubious practices may exist in the recording industry, it is true that the majority of popular music stars have benefited from record company investment. Traditionally (and, as I will argue below, still), recording has been central to popular music careers, as even the most industrious of bands are limited in the number of people they can play to each year. By providing artists with funding for recording an album (and perhaps more importantly, for promoting it), by offering money to support bands going on tour (as touring is generally loss-making for all but the most successful artists) and by having considerable expertise in ‘breaking’ an artist, record labels have played a vital role in establishing pop careers, and it is the establishment of a career which generates financial opportunities for artists (endorsements, merchandising, playing bigger tours and so on). This is how the old system could work: on the one hand, because of advances and low royalty rates, most artists have never received money from their recordings, but the success of their recordings has helped to produce income from other sources; record labels, on the other hand, have been able to overlook these alternative sources of income because they receive the vast majority of profit generated by the records. However, as the income from recorded music has rapidly declined, labels are highlighting the role that they play in career-building and arguing that they should receive a return for it.

If the ‘just desserts’ argument claims that labels have always been the drivers of career development for pop musicians, then the second form of justification for the 360 deal – the ‘active partnership’ position – asserts that labels will do much more for artists in the future. Signing artists to 360 deals, the labels argue, gives them a greater incentive to participate actively in the artist’s career and to support artists for longer periods. Supporting the 360 approach, Franz Ferdinand’s manager, Cerne Canning, suggested that ‘it keeps the labels on the game longer. If you give them ancillary rights, labels have got a vested interest to go down the road with you’ (in Cardew, 2010). Importantly, it also means that labels can view an artist’s career holistically rather than focusing narrowly on record releases. As Mike Smith, former managing director of the Columbia Label Group, stated, 360 deals mean that ‘we are able to do things that go much further than record sales. It means we can work on an act’s career’ (in Cardew, 2007a: 5). Signing a 360 deal means that the labels’ strategy does not focus too strictly on the album cycle. Providing an example of how the deal with Korn liberated the artist–label working relationship, Jeff Kempler, then-chief operating officer of Capitol Music Group, discussed the release of two albums, Korn Unplugged and Chopped, Screwed, Live and Unglued (a remix/live album): We didn’t have to get into a whole big rugby scrum with the band over, ‘Does this count as an album?’, ‘How do we apply royalties since it is old songs?’ ‘What do we do about the publishing?’ … We didn’t have to try to manoeuvre our way through a touring agent who might not have wanted to have them in rehearsal for Unplugged when they could have been touring. I don’t think you would be able to get those additional pieces of product [so quickly] in a normal deal. (in Martens, 2007: 22)

While the two different kinds of justification risk being contradictory (with labels arguing that they will start doing something which they are claiming they have always done), both forms of justification are being put forward simultaneously. Indeed, these two kinds of arguments justify the different kinds of deals outlined previously in this article: whereas the ‘just desserts’ argument justifies the acquisition of passive rights (‘we should get a share because our investment significantly boosts your income’), the ‘active partnership’ defence justifies the acquisition of active rights (‘we will provide you with new services and you shall pay us for them’).

Criticisms of the 360 approach

Despite the rationales offered for the 360 approach, these deals have received more criticism than praise and, perhaps unsurprisingly, the loudest complaints have come from artist managers and lawyers. For a variety of reasons, major record labels do not have a huge amount of goodwill from many in the music industry. A certain amount of scepticism exists towards labels’ motives and intentions, as well as a certain schadenfreude regarding the difficulties that they have experienced in the last decade.

The most frequent criticism made is that the extra rights required in a 360 deal are little more than a ‘land grab’ being made by companies whose business model is failing. For example, artist manager John Glover stated that ‘a lot of people want 360 degrees because their business is going down the toilet’ (in Cardew, 2007b: 6), while lawyer Bob Donnelly argues: [N]ow that the record business economy is faltering, label honchos are complaining that they can’t make enough money from record sales alone. Perhaps not surprisingly, they expect their own recording artists to sign so-called ‘360’ deals to subsidise executive compensation packages worthy of Wall Street. (2010: 4)

Clearly, these criticisms are more appropriate for passive rights, in which the record label top-slices a proportion of income for no extra work. It is reasonable to expect that managers and lawyers may have a more positive attitude towards active rights, in which the label is at least offering services that they did not previously. However, many artists’ representatives are sceptical that labels have the appropriate expertise to bring value to artist development: Many of the labels don’t just want a participation – they want to have approvals over decisions traditionally made by the artist manager … In negotiations, we’re having to educate the business affairs folks on how the business runs in areas outside of records. That makes me worry about how prepared the majors are to get into these areas. (lawyer J. Reid Hunter in Butler, 2008a: 22) In a recent deal, the company proposed to be the merchandiser, but the business affairs guy didn’t understand merchandising. We couldn’t even get the deal done. The ivory tower sends an edict to start signing merchandising rights, but the poor business affairs guys haven’t been educated in those deals. (lawyer Gary Gilbert in Butler, 2008a: 22) If they want to be actively involved in your touring, that’s problematic because they really don’t understand the touring business. (lawyer Elliot Groffman in Butler, 2008a: 22)

The perceived lack of appropriate expertise means that some managers are sceptical that the labels have really changed. As one manager, Iain Watt, stated: ‘I was offered a 360 deal recently that I thought was classic major label thinking, with the worst parts of a record deal and loads of extra rights’ (in Barrett and Clarke, 2008: 9), with another, Graham Wench, commenting that ‘nothing much has changed. I think the rude awakening is yet to come because many record labels think they have changed’ (in Barrett and Clarke, 2008: 9).

The final criticism made of the labels’ 360 deals is that in focusing on ancillary rights, 360 deals may be distracting record labels from their core task of producing and distributing records. Some lawyers and managers have suggested that the label should have to achieve minimum levels of record sales before earning revenue from alternative sources: Labels having a piece of things like touring … makes no sense if they don’t sell [enough] records … Unless they sell a certain number of records in two [albums], there should just be a notice and an out … It is hard to meet, but if they only sell 100,000 units, I’m not sure that’s good enough to merit participation in other income streams. (Gary Gilbert, in Butler, 2008a: 22)

Given the manner in which the 360 has become established as the new standard recording contract, such mutual accountability seems unlikely to evolve any time soon. The balance of power between the record label and the new artist remains heavily skewed in the label’s favour, and thus it retains the ability to establish the terms of the deal. However, there are many commentators on the music industry who believe that this balance of power may be changing. To such commentators, ‘in the new music economy, the record label is no longer in the driver’s seat; it is the artist, or the artist/manager, who is’ (Wikstrom, 2009: 143). From such a perspective, the 360 deal is an important reflection of the changing dynamics of the music industry. In the final section of this article I intend to evaluate this argument and consider the ramifications of the emergence of the 360 deal.

Making sense of the 360 deal

The 360 deal has become a bit of a buzzword in discussions concerning the music industry, with the Madonna, U2 and Jay-Z deals in particular taking on a certain zeitgeist feel. Coupled with public discussions of rampant piracy and plummeting CD sales, there is a sense of radical reorientation within the music industry as the CD, the cornerstone of the music industry for almost three decades, rapidly declines in significance, while a supposed ‘live music boom’ occurs, featuring an increase both in the number of tickets sold and overall ticket prices (see Frith, 2007). The overall picture painted by some commentators is that having tied their fortunes to the CD format, record labels, for decades the biggest fish in the music industry pond, are in terminal decline (e.g. Knopper, 2009; McLeod, 2005). From one side they are being challenged by new major players, most notably Live Nation and Apple; from the other side artists are in a much stronger position than they were in the past, able to acquire financing from venture capitalists or fan-funding, and reach audiences through the internet without label support. Whichever way you look at it, the future seems bleak for the major record labels.

I wish to argue that this position, although quite widespread, is somewhat exaggerated. It is certainly true that the major labels’ stranglehold on the music industry has been loosened somewhat, and that they have lacked strategic direction over the last decade or so. However, this particular moment may be the darkest one for the labels and it is conceivable that, when considered in a broader historical perspective, their situation may not be as bad as it seems on the surface and, furthermore, that their current circumstances and responses demonstrate considerable historical continuities. In this section I shall outline four reasons for this view.

Recordings will remain at the centre of the popular music experience

Throughout the course of the 20th century, popular music has grown up alongside, and been dominated by, the record. Toynbee (2006), for example, discusses how the dissemination of records has structured the very sounds of popular music (what he refers to as ‘phonographic orality’) but, for the present article, the more significant factor is the impact that the record has had on the listeners of popular music. Put simply, the vast majority of people have heard the vast majority of popular music through recorded music. This creates what Bennett calls a ‘recording consciousness’ that ‘defines the social reality of popular music’ (in Middleton, 1990: 88). It is the record that defines the popular song: if asked to think of a particular song, it is the recorded version that one is likely to hear in one’s head. The record dominates our sense of popular music and this affects how we hear live music, with live performances generally heard as crude interpretations of the recorded experience, as variations from the record (Eisenberg, 1987).

Although the CD format may be in decline, there seems little reason for the significance of recorded music to decline soon. Indeed, the changing format of musical recordings has been one of the major features of the music industry over the last century, and the significance of the record has supposedly been threatened in the past by new inventions such as radio. The means that the media through which we access recorded music may change, but YouTube hits, Spotify streams and ringtones are still recorded music. Piracy levels indicate that records remain important. The physical limits of live performance and touring ensure that people will still hear the vast majority of the music through recorded music. This can be easily illustrated by comparing 2010 data: in the USA there were exactly 300 million more album purchases than concert ticket purchases (326.2m and 26.2m respectively; of the 326.2m albums sold, 225.8m were physical rather than digital purchases) (Branch Jr, 2011; Christman, 2011). 8 Worldwide, the most popular live act in 2010 was Bon Jovi, who sold just under 1.6m tickets (Waddell, 2010). The most popular album in 2010 was Eminem’s Recovery, with an estimated 6m combined physical and digital sales (IFPI, 2011) plus many more millions of unauthorised downloads. Recorded music remains significantly more important than live performance in popular music culture.

Labels remain in a relatively strong position

Recorded music, the thing that the major labels specialise in producing, is thus likely to remain in a central position for the foreseeable future. However, there are other companies and individuals capable of producing recorded music and, as mentioned previously, there are other kinds of companies interested in contracting artists to 360 deals. Nonetheless, in relation to these competitors, the major labels remain in a relatively strong position both financially and culturally.

Financially, their strength comes from the fact that the major labels own a lot of the most popular music recorded over the last 70 years or so. Catalogue ownership provides labels with a big advantage over many competitors, in that a reliable source of income is ensured from selling and licensing these works. Licensing is particularly significant in a cultural environment that samples heavily and is very nostalgic. In terms of residual income, it is also important to recognise that the CD is not dead yet. The rate of decline of CD sales has been dramatic, but it is unlikely to continue the same trajectory until it reaches zero. Instead, it is more likely that the pace of decline will stabilise: the pop mainstream has been most affected by the decline in CD sales but, for example, older music consumers, country music fans and Germans are still buying CDs (Peoples, 2011b; Ross, 2011; The Economist, 2011). CD sales may have declined by roughly half in the last 10 years, but they were still worth $12bn in 2010 (Peoples, 2011b), with the major labels accounting for the majority of that total. These sources of income provide some insulation for the major labels, giving them the opportunity to develop strategies more suited to contemporary circumstances.

Culturally, too, labels remain significant, not least because it is recognised that ‘there are still a lot of very good people in record companies with real expertise’ (Adele’s manager, Jonathon Dickens, in Barrett and Clarke, 2008: 9). As discussed previously, one of the labels’ core functions is developing artists’ careers in ways that facilitate income opportunities from merchandising and sponsorship, for example. Given that arguably, these non-record income streams are becoming more important in the music industry, and viewing the artist as a brand is becoming more common, it is recognised that the labels have expertise that remains relevant in the contemporary industry. It is, of course, reasonable to argue that this expertise has diminished given the dramatic cuts in staff at major labels since the start of the downturn. Overall, 29 rounds of job cuts were announced by the majors between 2004 and 2008 (Barthel, 2008) and Wikstrom (2009: 65) suggests that the record industry has seen a 25% reduction in its workforce since 2000. Further job losses will inevitably occur as a result of the sales of EMI and WMG in 2011. Even before the downturn, labels had been outsourcing the ‘creative’ elements of artist development in order to concentrate on distribution of physical product. As such, and as illustrated earlier in this paper, some critics argue that the major labels have little relevant expertise to offer artists.

There is definitely substance behind such a stance. However, it is also important to note that, as well as laying off large numbers of workers, the major labels have also been recruiting in areas related to artist brand development. Furthermore, where internal expertise was deemed lacking, labels have sought to acquire more specialised firms. For example, as early as 2000, Warners acquired Artist Arena, an online ticketing and fan club specialist (Christman, 2008) while, in 2007, Universal acquired Sanctuary, the management-company-turned-independent-label considered as one of the 360 pioneers (Hayward, 2007). The internal reorganisation of the labels and the extra emphasis being given to artist management, licensing and merchandising divisions, indicates that labels are taking seriously their promises to provide new services and this has been recognised in some quarters. Warners, in particular, has been praised for enhancing its merchandising expertise (Peoples, 2010).

This expertise helps explain why, culturally, labels still matter and most bands still want to sign with major labels. Getting a record deal remains a significant marker of status, a sign of having made it – perhaps even more so in an environment in which anyone can make recordings available to the public. The cachet of being a major label artist can be demonstrated by a survey of 1869 independent artists by Reverbnation (2011), in which three-quarters of artists wanted to sign a deal with a record label, with the major labels (and their subsidiaries) consistently being stated as preferred destinations. 9

The labels’ overall strategy is not fundamentally changing

The majors’ expertise in developing artists’ careers points to a further reason why their future may not be as bleak as commonly presented. While the 360 deal may reflect a refinement to their approach, their fundamental strategy is not changing. This may seem like a bad thing on the surface, given that their strategy has resulted in declining income; however, the benefits become clearer when it is recognised that the description ‘record industry’ was a misnomer, given that its profitability did not depend upon the production of records. Over the last 30 years or so, the fundamental functions of the major record industry have been twofold. The first is the generation and exploitation of intellectual property rights (Frith, 1987) and, despite the quite public challenges to the intellectual property regime prompted by the internet and widespread file-sharing, rights will remain an important source of revenue to the labels in the future through licensing songs to television, advertisements, websites and so on (the ‘business-to-business’ model). However, here I want to focus on the second basic function of record labels: the creation and maintenance of stars.

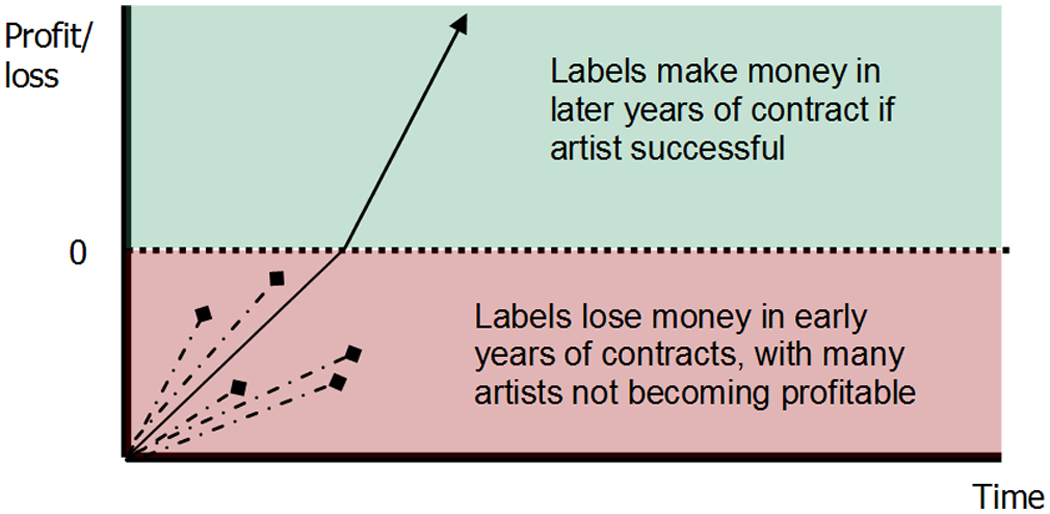

The development of pop stars is important to the recording industry because stars generate new markets and make existing markets reliable in an industry characterised by unpredictability and high failure rates (Marshall, forthcoming 2014). Recording contracts signed with the major labels are always long-term deals, more like seven albums rather than one or two, although later albums have to be ‘optioned’ by the label rather than being guaranteed by the contract itself. The length of such contracts reflects two characteristics of label strategy: first, that the majority of artists who sign with a major label are unsuccessful; and second, that early career pop stars are not very profitable, with artists often not becoming profitable until their second or third albums (but then becoming very profitable if succeeding – pop stars have a ‘high upside’ but a relatively low chance of success). Thus the labels utilise portfolio management, signing many artists and expecting the few that are successful to generate sufficient income to subsidise the costs of the unsuccessful ones and create profit (Negus, 1999). To effect this strategy, labels sign a number of new artists to long-term contracts, take a financial hit in the early years of the contract while the artist’s career is developing and, for the few that are successful, reap the benefits in the later years of the contract. Figure 2 offers a representation of this strategy.

Major record labels’ strategy for management of artist rosters

In the shift to the 360 approach, very little is changing in the overall shape of this figure. What is happening is that as income from CD sales becomes unsustainable, labels seek parts of other revenues generated by the star’s career. However, even this transformation has precedents, given that cross-media stardom, including the sponsorship and endorsements of non-music products, has been significant for earlier popular music stars such as Bing Crosby (Negus, 1992), country music stars from Jimmie Rodgers to Garth Brooks, and non-Western markets such as Japan, where the 360 model has long been a convention (McClure, 2008). There is little historical reason to suggest that the previously successful strategy of portfolio management and star-building will become unsuccessful.

Labels remain vital to artist development (and thus the future viability of the music industry)

Without wishing to present the major labels as self-effacing patrons of the arts, it is important to recognise the important structural role that they play in the ecosystem of the music industry, offering investment and expertise to new artists to help them become established. One thing this does mean is that the major live industry is to some extent parasitic on the recording industry. Despite talk of a live music boom, the majority of revenue is concentrated in a very few acts, mainly heritage acts such as The Rolling Stones and U2. Generally speaking, live music is only profitable for acts that are already successful, and virtually all of the acts that are able to make a profit from touring have reached their position as a result of record label investment. This is the case even for many bands held up as paradigms of modern, independent artists, such as OK Go: when asked the best way to make it as an independent artist, OK Go’s digital strategy manager, Mike Rosenthal, replied: ‘be on a major label for ten years first’ (in Lindvall, 2011).

If the major labels disappear, then new ways of supporting fledgling artists will need to develop. However, there do not appear to be any alternative sources of investment appearing. At the time of the Madonna deal Live Nation explicitly stated that it is not interested in developing new acts: We don’t want to be in the business of pouring tens of millions of dollars into unknown acts, throwing it against the wall and then hoping that enough sticks that we only lose some of our money and not all of our money … It’s not part of our business plan to be out there signing 50 or 60 young acts every year. (Michael Cohl, then chairperson of Live Nation, in Waddell, 2007: 25)

11

Figure 3, from a Live Nation investor presentation, graphically demonstrates its lack of interest in artist development. It presents a new and totally unrealistic model of the music industry in which an artist can go from posting a song online to selling out an arena in three months.

Slide from Live Nation investor presentation

The argument that major labels retain an important functional role in the music industry runs counter to many of the popular arguments that their significance is declining because artists have access to other sources of funding and other ways of reaching their fans through the internet. However, in an industry perhaps even more uncertain than in the past, the major labels remain the primary source of investment for developing artists. The sources of venture capital, such as Power Amp and Ingenious, are available only to artists with already established fan bases. As the Sugababes’ co-manager, Sarah Stennett, stated: ‘people talk about private investors, but people will not invest in new music outside of the major labels’ (in Cardew, 2010).

This is not to suggest that it is impossible for artists to be successful without major labels (and it may be that what counts as ‘being successful’ will change radically in the next few years). However, in an industry perhaps even more uncertain than in the past, the major labels thus remain the primary source of investment for developing artists. This explains why most bands still want to sign with record labels: very few artists have been successful without one. Tom Silverman, founder of Tommy Boy Records and the New Music Seminar, argues that ‘the premise of technology being the great democratizer and allowing more artists to break through than before — actually, we’ve seen the opposite effect. Fewer artists are breaking through than ever before, and fewer artists who are doing it themselves are breaking through than ever before’ (in Van Buskirk, 2010). Silverman points out that, in 2008, only 225 artists in the US sold 10,000 records for the first time and, of these, only ten artists did not have a record label while ‘79,000 releases sold less than 100 copies. Under a 100 copies is not a real release – it’s a noise, an aberration’. 10

Conclusion

Can the 360 deal save the record labels?

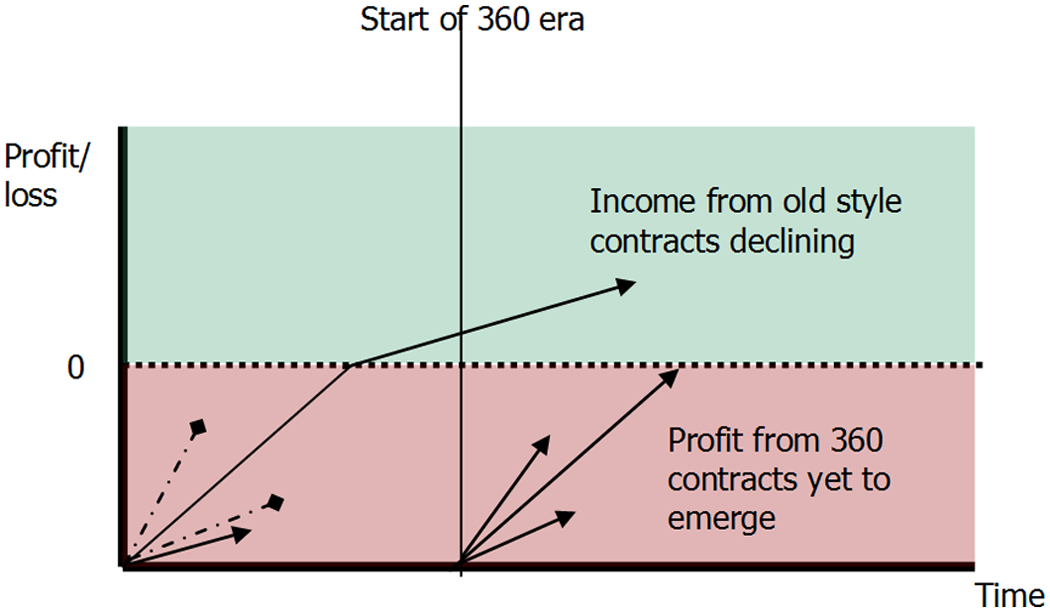

Just because an important functional role exists does not necessarily make it financially viable. Is it possible for labels to continue making enough money to continue to invest in new artists? I would argue that it is, and that the current crisis being experienced at the present time is deceptive. It is important to recognise that this may well be the worst possible moment for labels. First, income from old-style record deals (i.e. those that rely on income from recordings) is declining. Second, substantial income from new-style 360 deals has not yet begun to materialise, as they have been signed with new artists who are in the early part of their careers and thus unlikely to be profitable (as would have been the case with the standard recording contract). This is represented in Figure 4 below.

Schematic representation of major labels’ income from artist rosters before and after the emergence of 360 deals

Of course, one thing this means is that the 360 deal remains rather speculative, with few likely to have made any significant money thus far. Labels are taking 360s as a hunch and, as they do not exactly know how the music industry will develop, they are seeking to get their fingers into as many pies as possible. Yet the 360 approach does create some possibilities for weathering the labels’ current problems. There will be some changes, as the high profit margins of the CD, and thus the boom years of the late 1990s, are unlikely to return. It is also plausible that the high failure rates associated with the recording industry may become less sustainable; but on the whole, the record labels should be able to find a way of continuing their business model.

They will not be record labels any more, though, but global music entertainment partners with interests in a diverse array of popular music activities. In this sense, one of the interesting ramifications of current developments may be that labels begin to resemble what they were in the middle part of the 20th century. During the 1970s, for example, EMI had control of a major British cinema and theatre chain (one of the major live music circuits), a network of clubs, discos and dancehalls, a network of talent and artist agencies, concert promotion companies, ticket outlets and a ‘muzak’ library. It was Britain’s largest distributor of musical instruments and owned, among others, an American recording equipment producer, the record store HMV, an American rack-jobbing enterprise and a shopfitting service (Frith, 1983). The general approach of the major recording companies at this time was to seek income from all forms of musical activity and, in their new business models, labels may find themselves going back to the future, becoming more all-encompassing music empires once more.

Footnotes

Funding

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.

Notes

Biographical note

Lee Marshall is a senior lecturer in sociology at the University of Bristol. His research interests centre on issues concerning authorship, stardom and intellectual property. His first book, Bootlegging: Romanticism and Copyright in the Music Industry (Sage, 2005) won the Socio-Legal Study Association’s early career book prize. His second book, Bob Dylan: The Never Ending Star was published by Polity Press in 2007.