Abstract

In this contribution we give common guidelines on how unemployment schemes for the self-employed could be developed in practice. These guidelines have been derived from national descriptions contained in this special edition on unemployment protection for the self-employed, or in other recent comparative contributions on the matter. Our reference framework is the EU Council Recommendation (2019) on Access to Social Protection, and more in particular the overall objective that social protection should be designed in a labour status neutral manner and, where necessary, adapted to the specific work situation of the professional groups covered. Applied to unemployment, the design of the scheme should be as similar as possible to that of unemployment insurance for wage earners. However, it is crucial to adapt the rules as specifically as necessary to the nature of self-employed work, such as, for example, the fact that the self-employed do not work for an employer. Starting from this basis, we developed key rules with regard to unemployment schemes for the self-employed. We did so by addressing the essential components of unemployment schemes: the definition of the unemployment risk, financing, access and entitlement conditions, and re-eligibility in case of repeated claims for unemployment benefits. We also address recent evolutions in the labour market, such as coverage when multiple activities are performed (combining activities as an employee and as a self-employed person), and elaborate on situations involving temporary closure of the self-employed activity (e.g. due to Covid-19) and partial unemployment. In conclusion, we provide some reflections on the apparent ongoing evolution of the risk of unemployment towards a broader income protection scheme, which not only provides income replacement in case of a final loss of professional activity or self-employed business, but also gives structural income support if the person loses income partially due to external economic and/or social reasons.

Introduction

This paper discusses the setting up of an unemployment insurance scheme for the self-employed. The spread of Covid-19 placed economies, labour markets and social systems worldwide in a state of emergency. The disruption of supply chains, the slump in world trade and export demand, as well as the loss of working time would have been enough for a major recession. The drastic lockdown of domestic economic activity, particularly in the areas of public life, represented a completely new challenge.

The political reactions were correspondingly far-reaching. Governments around the world struggled to safeguard jobs and firms, so wage earners 1 in standard employment relationships benefited from short-time work subsidies or unemployment benefits in case of job loss. Short-time work, especially, surged in many countries. However, the lack of social protection for many of the self-employed became a serious gap in social security systems. The crisis particularly hit the self-employed in various sectors of personal and business services, only a minority of whom are usually covered by unemployment insurance. Therefore, many of the self-employed got into financial difficulties, and many governments were forced to introduce ad-hoc liquidity support packages. Due to restrictive conditions, complicated design or poor adaptation to the working situation of the self-employed, a lack of experience or uncertainty in how far operating expenses or costs of living could be addressed as ‘entrepreneurial salary’ meant that access to the schemes was problematic for the group of self-employed. In the end, these programmes were not appropriately used; access was not always effectively granted to those in need.

Indeed, the shock of Covid-19 strengthened existing policy efforts to reduce the gaps between self-employed persons and wage earners. In that way, the pandemic acted as a catalyst to extend social security coverage to self-employed persons, especially with regard to unemployment and work incapacity (Spasova et al., 2021; see also Macron's 2017 election programme). At the European level, this concern is mirrored by the 2019 EU Recommendation, adopted just before the Covid-19 crisis, on access to social protection for all workers and the self-employed. Similarly, a multitude of national legal reforms opened up unemployment protection to (groups of) self-employed (e.g. Ireland and Malta in 2019), while at the same time adapting the entitlements to the specific working situation of these groups (see below). The challenge of extending coverage to the group of self-employed persons thus preceded the pandemic; yet at the same time we acknowledge that Covid-19 sped up the development of these schemes. Still today, however, we face quite some challenges to make a fully-fledged protection for unemployment a reality for the self-employed. Whereas mandatory unemployment insurance is generally standard for wage earners, access to unemployment protection for the self-employed is usually restricted to voluntary schemes, regulated in differing ways in different countries. Effective coverage for the self-employed turns out to be weak (Spasova et al., 2017; Spasova et al., 2019), so that fundamental risks connected to the uncertainties of working life are regularly not insured. This should not come as a surprise. Social protection systems, and in particular work-related social insurances such as unemployment schemes, were primarily developed for standard workers, implying a long-term, full-time work relationship (Schoukens and Barrio, 2017). Hence, social security systems are not always tailored to the specific work situations of self-employed and other non-standard workers (Schoukens et al., 2018; OECD, 2018). This contribution therefore focusses on how comprehensive contribution-based unemployment insurance schemes for the self-employed can be developed, adequately compensating the loss of prior occupation.

Due to the nature of self-employed work, it is no straightforward task to redesign unemployment schemes to include this group adequately in unemployment insurance schemes. Therefore, in this contribution, we discuss key unemployment insurance rules and conditions for the self-employed. We make use of the numerous practices described in this special edition and enrich them further with other descriptions in recent comparative studies on unemployment for the group of self-employed (see bibliography). Starting from the underlying principles of labour status neutrality and adaptation, where necessary, to the specific working needs of the professional groups covered by the unemployment schemes, we try to discern some guidelines on how to design unemployment protection for the self-employed. We derive conclusions on such schemes and make suggestions for practicable steps forward.

The paper is structured as follows. The subsequent section maps the existing unemployment insurance schemes in general and for the self-employed in particular. We then make the case for a mandatory unemployment insurance for the self-employed. The subsequent sections cover financing issues, followed by access and entitlement conditions. The next two are devoted to unemployment insurance for combined activities and for temporary unemployment, respectively. In the last section we come to some concluding thoughts.

Mapping unemployment schemes

The social risk of unemployment

Social security schemes were traditionally organised based on conditions tailored to standard long-term and full-time work relationships (Schoukens and Barrio, 2017). Self-employed work can differ from this standard in several respects. There is, for example, a less steady flow of income and a far more flexible and self-determined working time. Logically, conventional systems are not always tailored to the specific work situations of the self-employed (Schoukens et al., 2018; OECD, 2018). It follows that, when providing social security coverage for the self-employed, such schemes need to respect their specificity. In order to accommodate this specificity, the social security system will need to be neutral in its design as regards labour status, yet sufficiently specific in its rules for application. The weakness of existing systems in this respect is often more related to effective rather than only formal coverage of social security. There is no need for ‘improved’, ideal types of schemes that cannot be applied, because these give no effective access to social protection. This means that, when designing social security systems, conditions should be, as far as possible, universal for all working groups. Insurance against social risks connected to the uncertainties of working life has some commonalities for all groups of workers, although its practical application might differ. Such underlying principles are the principles of equivalence, solidarity, financial sustainability as well as adequacy of benefits and contributions. Specifically for unemployment, insurance schemes should be sufficiently transversal across the various work statuses to guarantee protection in case of frequent labour market transitions or multiple jobholding.

In this contribution, our focus is on unemployment insurance addressing loss of income due to the loss of previous occupational activity. Unemployment as a social risk can in fact refer to different situations: either the emphasis is on covering the absence of (paid) work or it can be on the loss of previous paid employment (Pieters, 2018). In the first type of unemployment protection, the earlier work record will be less relevant. If, however, unemployment refers to the loss of previous paid work, the earlier work record becomes more prominent in the design of the scheme. This second type of protection is more likely to include part-time unemployment schemes, where the entitlement to an unemployment benefit (compensating the loss of work) can still be combined with income from work (within given limits). Such systems, specifically, may have schemes of partial unemployment where the beneficiary combines a benefit with income from the remaining work or where the beneficiary maintains a part of the unemployment benefit to compensate for the lower remuneration in a new job. The definition of unemployment as the loss of previous paid work is more often to be found in a social insurance based approach, whereas coverage of the more general absence of (paid) work is more the approach taken by general social assistance and/or by the category-based unemployment assistance schemes (Pieters, 2018).

Very often, countries have both unemployment insurance and social assistance schemes in place. The social assistance scheme, related to the risk of unemployment, is sometimes subdivided into a general social assistance and a specific (category-based) unemployment assistance; the latter (unemployment) assistance targets persons who have no work and hence are left without sufficient means; slightly different entitlement conditions may be applied and another form of means testing may be in place, more restricted to work income. The social insurance often covers the first period of unemployment; the social assistance scheme is reserved in a residual manner for the unemployed who have exhausted their entitlement to benefits under the social insurance scheme or for those who, in general, did not qualify from the outset for unemployment insurance (such as, for example, the self-employed). For this contribution we will focus on the unemployment insurance schemes only. 2

Unemployment insurance coverage for the self-employed

The self-employed were traditionally not targeted by unemployment insurance. It was considered not to be possible to cover the risk of unemployment for the self-employed. Two main reasons were invoked. First, self-employment is characterised by the taking of economic risks, one of these being that the business has to stop because of a lack of economic success. Secondly, one of the major conditions used to assess the risk of unemployment (for wage earners) is its involuntary character (Pieters, 2018). Unemployment benefits are not to be granted to persons who have chosen to stop working. In case of self-employment, it is difficult to assess whether closing down the business was involuntary or a choice. To what extent is a self-employed person to be blamed for the failure of his or her business (for instance because of mismanagement or a wrong assessment of the potential economic success)? What should be done with a self-employed person who deliberately closed down the business? (Schoukens, 2000 and 2019).

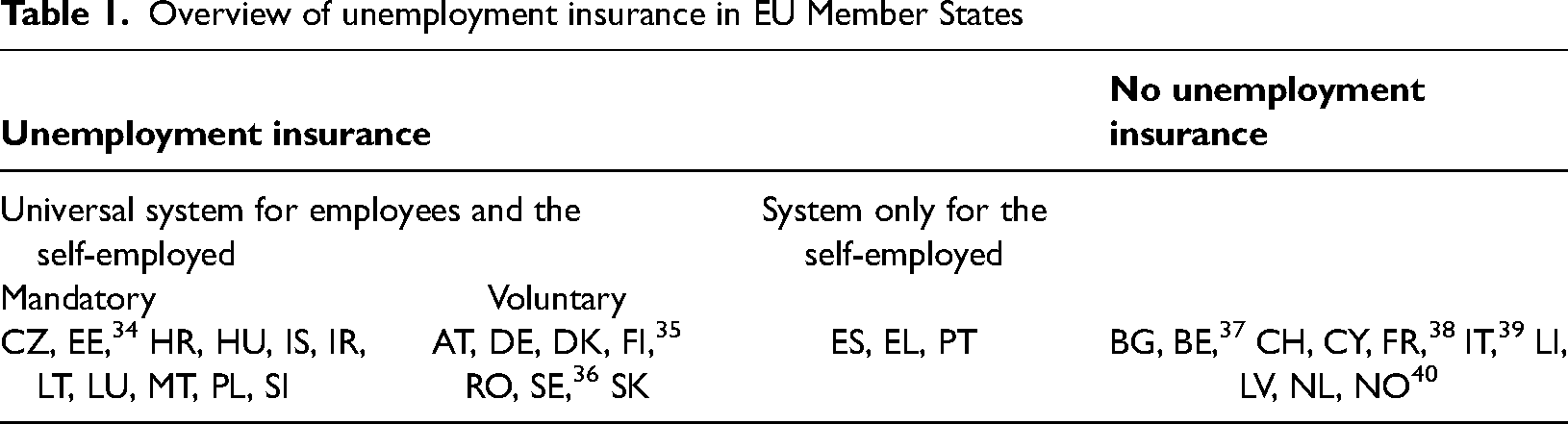

Nowadays, the situation is quite different. A majority of European countries have (some kind of) unemployment protection in place for the group of the self-employed (see Table 1). From the reports in this special issue and a recent consultation of the MISSOC comparative social security tables covering the EU (27 countries) and EFTA (four countries), we came to the following findings (MISSOC, 2024): 3

Overview of unemployment insurance in EU Member States

Only 10 countries reported having no unemployment insurance in place covering the self-employed (Belgium, Bulgaria, Cyprus, Estonia, Latvia, Liechtenstein, Malta, Norway, Switzerland and the Netherlands). However, of these countries, it was reported by the Netherlands that there is specific social assistance available for the self-employed, in particular for the self-employed who had to stop their business and/or where the business revenues, due to old age or invalidity, are below a defined minimum subsistence level. In Belgium, there is a specific social insurance scheme (i.e. the bridging benefit) in place, guaranteeing a flat-rate income replacement for the self-employed who had to close down their business. This scheme is formally not to be considered as genuine unemployment insurance due to the multi-tier coverage, which goes beyond mere income replacement (e.g. continued health care insurance is also provided for this group of the self-employed; it is considered to be more important than the income replacement covering the loss of revenues) and due to the absence of specific labour meditation services. Moreover, Estonia reported 4 that the self-employed who become unemployed are directed to the general unemployment assistance; furthermore, there is protection for solo entrepreneurs employed in their own private company, as they are formally considered as employees for the application of social security law (Vallistu, in this special issue). Finally, we should not underestimate the right granted to the self-employed in some countries (such as Belgium, Switzerland and Norway) to fall back on the unemployment insurance for employees if they had a prior insurance record built up as a wage earner (before they started up their self-employed activity) and if the start-up in self-employment fails within a certain defined time period. Strictly speaking, it is not to be considered as a formal unemployment insurance for the self-employed; yet this right, built up as an employee – which is preserved for a period (with the status of dormant participant) – is providing in reality an effective protection against the loss of income due to business closure.

In some circumstances, unemployment protection is limited to certain specific groups of self-employed (often economically dependent self-employed): for example, Italy (gestione separata for the new self-employed), Norway (self-employed fishermen), Germany (artists and farmers), and Lithuania (self-employed in individual companies and members of small and/or full partnerships). 5 The majority of countries which make unemployment insurance available to the self-employed cover them together with the other professional groups (i.e. wage earners) in the general unemployment insurance (Austria, Croatia, Czech Republic, Denmark, Finland, Germany, Hungary, Iceland, Ireland, Lithuania, Luxembourg, Malta, Poland, Romania, Slovak Republic, Slovenia and Sweden). Some countries report that they adapt the entitlement and financing conditions in these general schemes to the specific working situation of the self-employed. Denmark reported that it organises the unemployment scheme in a neutral manner regarding labour status. Instead of establishing the conditions in terms of wage earnership or self-employment, they are now defined in terms of professional activities. In that way, the scheme has moved from occupational insurance towards a more activity-based insurance, as this guarantees better unemployment protection to all professional categories and allows more effective protection for persons who combine two or more mixed activities (as a wage earner and as self-employed). Furthermore, it should be pointed out that in several countries, the unemployment insurance is only made available on a voluntary basis (Austria, 6 Germany, Finland and Sweden for the occupational (2nd) pillar, Denmark, Romania, Spain (for farmers) and Slovakia). With the exception of the Scandinavian states, it turns out that only a minority of the self-employed take out this voluntary insurance (Schoukens, 2022); hence the majority of the self-employed remain without any specific protection against unemployment. In all countries, the self-employed can always fall back upon the general social assistance schemes in place if their income is below the minimum subsistence threshold (e.g. due to closing down of the business).

The case for mandatory unemployment insurance

By default, social security schemes are organised on a mandatory basis (Pieters, 2006). The self-employed are an exception to this general rule. They are often allowed to join, on a voluntary basis, unemployment scheme(s) that are in place for employees or for all residents looking for a job. For this group of persons, voluntary schemes seem to be the standard, although the number of mandatory insurance schemes has grown (see annex I). While voluntary schemes give the self-employed the prospect of coverage against the risk of unemployment, in reality most self-employed do not take up the insurance (Codagnone et al., 2018), raising the question of why insurance should not be made mandatory. There are several reasons which support compulsory protection against unemployment.

First there is the work perspective: work-related social security is most effective when it is connected to the earning of an income rather than to a specific legal status such as a standard employment relationship. This would align with the objectives of social insurance, i.e. protecting against loss of income due to contingency. The separation between self-employment and dependent work is becoming increasingly blurred (Truman et al., 2019). Over the life-course, changes in labour status can become more and more significant (European Commission, 2018; Schoukens, 2019). Mandatory insurance can avoid both false incentives to shift from work as an employee to bogus self-employment for cost-saving reasons, and the risk of additional payments due to uncertainty as to whether specific activities may be classified as dependent work.

Then there is the welfare perspective: there is no natural difference between wage earners and the self-employed in the need for social security; unemployment is a significant phenomenon also for the self-employed (Codagnone et al., 2018). 7 In the absence of social security and in case of need, social (assistance) benefits kick in. But then, tax payers end up as de-facto insurers actually subsidising unsustainable developments in specific sectors (in some systems, this is the reason for having made social insurance mandatory for the self-employed; Schoukens, 2000). The plethora of emergency schemes established in the Covid-19 crisis could be taken as evidence that systems are able to adapt in critical situations. However, besides proving the failure of the protection systems in place, as argued above, ad-hoc adjustments typically have considerable shortcomings. Moreover, they are likely to tempt people into anticipating bailout measures, so that adequate precaution could be disincentivised. Such considerations and a focus on short-term earnings lead to an underprovision of social insurance.

The next is the market perspective: social security contributions represent additional costs. However, although formally the self-employed pay the contributions, in a market, the burden is shared between the two sides of the market. With mandatory insurance covering all individuals, higher market prices will reflect higher costs. In contrast, in the absence of social security coverage, there is the risk that remuneration can be pushed below a sustainable level. Affordability is a much-discussed point whenever contribution-based social protection is to be widened, especially in view of insufficient incomes that evidently represent a challenge going beyond social security. However, when it comes to alleviating affordability issues, mandatory schemes will improve the financial scope compared to individual, voluntary participation that does not affect market prices. Naturally, self-employed services become more expensive as compared to the work of employees. However, as argued in the ‘work perspective’, this does not put self-employed activities at a disadvantage, but rather eliminates short-term false incentives.

Then there is the participation perspective. Voluntary coverage implies that a certain share of the individuals will decide not to join (either deliberately or due to a lack of consideration) the available social security schemes. A study on the voluntary unemployment scheme in Austria showed a high risk of selectivity. ‘Good risks’ were not as likely to join the scheme as ‘bad risks’, as shown by the fact that the vast majority of the self-employed who joined the scheme claimed benefits within a certain period (for a more detailed discussion, see Pfalz, in this special issue). A mandatory scheme avoids such risk selection so that the mandatory social security schemes can be sustainably organised. It turns out that groups deciding not to join are mainly found at both the highest and lowest levels of income (Codagnone et al., 2018). For the lowest income level, this shows the intrinsic weakness of the voluntary approach. Losing high-income groups is equally problematic, not only with regard to guaranteeing the financial sustainability of the system, but also for maintaining the trust of the public. Hence, effective coverage in voluntary schemes turns out to be rather weak. The reasons for this can be asymmetric information, insufficient awareness of social rights and responsibilities, problems in reaching minimum thresholds, or adverse selection and moral hazard, as explained above. In this regard, experience with voluntary unemployment insurance schemes shows that they require substantial public subsidies to reach significant coverage rates (e.g. as in Denmark). Interestingly, the self-employed often consider unemployment insurance as a necessary element in their social security protection (Codagnone et al., 2018; Schoukens, 2019), and are inclined to accept mandatory insurance for this risk. 8

Finally, there is the dynamic perspective: Social protection can have important forward-looking effects that will remain subdued if effective coverage fails. In times of hardship, precarious situations are exacerbated without social protection, if, for example, time cannot be spent on training or if personal capital, goods have to be sold. Furthermore, individual investments in the future, for example in education and training and career development, will be thwarted for fear of calamities. Social protection strengthens sustainable productive development of personal capacities, including the willingness to invest and to take risks, and career development prospects. This is even more so if the mandatory insurance comprises continuing education services, to which many of the self-employed do not have organised access. Logically, this also has positive external effects on the whole economy. On the downside, excessive risk-taking and business failures due to moral hazard must be prevented by incentive-compatible regulation (as discussed below); in an evaluation of the Danish unemployment insurance, Ejrnæs and Hochguertel (2013) find no sizeable moral hazard effects in business failures. 9 In the dynamic sense, all those involved, including customers, would benefit from insurance against unemployment risks.

Traditionally, insuring the income risks of the self-employed is often seen as contradicting the nature of self-employed risk-taking. However, from several perspectives, extending unemployment insurance beyond standard wage earners has the potential to contribute to sustainable, productive and social labour market development. Nevertheless, besides these advantages, unemployment insurance for the self-employed can also involve some critical points. It is crucial to adapt rules appropriately, to address the specific needs of the self-employed (Schoukens and Barrio, 2017). Therefore, in the following sections we discuss key rules and conditions for the self-employed and derive conclusions on how unemployment insurance for this group should be designed.

While we can make the case for mandatory unemployment insurance, most aspects of insurance design are, however, equally relevant to voluntary schemes.

Financing

What is the ‘income’ of the self-employed?

Our focus is on the development of comprehensive mandatory contribution-based unemployment insurance. This would mean that income replacement in case of unemployment is (preferably) financed by (social security) contributions paid from one's current income. As is the case for social security financing overall, the notion of income (of the self-employed) is crucial here. Yet what is to be understood by ‘income’ in this case, and how is it to be determined? This is not an easy assessment in the case of the self-employed. For employees too, the concept of (professional) income has become more diverse; yet the basis for employees remains largely the wage, which overall is a rather stable income paid by the employer on a regular (weekly/monthly) basis. In the case of employees, the employer traditionally withholds the (employee) contributions directly and transfers them with the employer contributions to the social security system. Self-employed workers, on the other hand, declare their income themselves; moreover, they pay the required contributions themselves. So what is to be understood by income? And who determines it in the case of the self-employed?

In many of the systems, we traditionally fall back on the fiscal concept of ‘self-employed income’, which is understood as the profit made by the self-employed minus professionally related costs. Yet, this definition of income is increasingly being criticised, as the (professional) income which is determined for tax reasons does not always support the objectives underlying the idea of professional income in social security (creating solidarity though vertical redistribution; persons with high professional income supporting persons with low professional income). Some of the deducted costs become questionable for social security purposes. Should social security accept (all of) the tax-related deductions (see below)?

Furthermore self-employed people who organise their activities in (their own) private limited companies are often in a position to themselves determine, fictitiously, the level of their professional income (frequently established on the basis of a monthly income or wage); this professional income can then, for example, be kept low, keeping profits in the company (to be paid out at a later stage in case of partial or full liquidation of the company) and/or with the capital returns paid directly as company dividends. These capital returns are traditionally not subject to social security levies as they are not considered to be professional income. Work-related social security schemes focus on professional income and not on income from capital. Hence there is a discussion in a growing number of countries suggesting that self-employed income be defined more extensively, including at least also income gains, when they are the result of the activity of the company in which the self-employed have their professional activities.

Some examples show that countries are (still) struggling with the notion of income of the self-employed for social security purposes.

In Estonia, independent contractors and solo-entrepreneurs are taxed in a similar way to regular employees with regard to social tax, unemployment insurance contributions and income tax. Solo-entrepreneurs (employed in their own private limited company) have, however, the possibility of keeping the ‘wages’ at a minimum as they decide the level themselves; often the surplus income is added to dividends which are paid out from the profit (a similar practice is mentioned in the country reports in this special issue on Belgium and the Netherlands). In case of unemployment, the benefit will, however, be paid at the minimum level (reflecting the reported minimum wage), but not in relation to the other income sources from the company which may benefit the solo-entrepreneur, such as dividends (Vallistu, in this special issue).

In Denmark, income from self-employment and employment is to be taken into account to qualify for unemployment benefits. In connection with the unemployment reform, there were discussions on changing the definition of income in order to have it defined in a more labour status neutral manner. The legal condition for entitlement to the benefit is not tied to the legal status of the person as employee or self-employed, but to their professional activity. In the end, the criteria were aligned more closely with the income categories used by the tax authorities. In this, the social law authorities usually follow the position of the tax authorities. Income from both self-employment and wage earning is taken into account Yet, only income from professional activities counts, not income from capital or leisure (Jacqueson, in this special issue). In Ireland, on the other hand, the self-employed should contribute on the basis of reckonable income or reckonable emoluments. Reckonable income is to be regarded as the aggregate income from all income sources for the contribution year in question, as estimated in accordance with the Income Tax Act; this can extend to some capital income as well, as defined in the Taxes Consolidation Act (Cousins and Whyte, 2024).

As unemployment insurance aims at stabilising the loss of income connected to work, there is an argument for considering the full income related to the self-employed activity. This basis should be independent of the type of income, particularly if the activity is organised in a legal entity. Logically, if the relevant national system allows some shifting between remuneration, dividends etc., it would be advisable to take into account the full income from the legal entity related to the self-employed activity. The growing integration of self-employed activities into legal entities shows that it is very hard to maintain the distinction between income from professional activities and related income from capital (as discussed by Vallistu for Estonia; see above). In fact, the importance of capital gains, from which persons earn their living, is increasing. This is true also for the self-employed. While capital is in fact unequally distributed, it is often taxed to a lesser extent and excluded from social contribution payments. As a consequence, we may have to broaden the social contribution base to also include capital (at least capital gains related to the company in which the activity of the self-employed is organised). If this approach is to be applied, political will and administrative capabilities (e.g. registers) will be necessary. A reconsideration of the contribution base is considered among scholars to be much needed in order to broaden social security coverage, especially for non-standard and self-employed workers (see the more detailed discussion in De Becker, 2023).

Using the taxable income as a (provisional) basis?

As mentioned already, taxable income is traditionally used as the income basis for determining the social security levies. Two issues arise here. To what extent should social security accept all tax deductible expenses? And further, is the income declared for tax purposes to be used as a provisional or final income basis for social security?

Depending on the activity, the self-employed may have (substantial) business-related expenditure. Some of these deductible expenditures (investment costs, business car, etc.) may have a justification for tax reasons, yet may be less suitable for social security. Thus, some deductions should be modified, leading to a socially corrected income. This will be a policy that more than likely will be applied to all social security schemes, and not only to unemployment insurance.

A clear example of a contribution base independent of tax exemptions can be found in the Irish social security system. As mentioned before, in Ireland, the self-employed contribute on the basis of reckonable income or reckonable emoluments. Reckonable income is to be regarded as the aggregate income from all income sources for the contribution year in question, as estimated in accordance with the Income Tax Act, but without taking into account various tax exemptions. Deductions are possible insofar as allowed by the ‘capital allowance’ provisions in the Taxes Consolidation Act (Cousins and Whyte, 2024).

Apart from the deductibility of costs, there is also the question of how the tax basis should be used: as a fixed basis (meaning that it should already be finally determined by the tax authorities) or as a provisional basis (meaning that the final assessment and hence determination of income is still to be made in the future, justifying future additional levies or contribution returns). The first approach is more stable; the second creates issues in relation to legal certainty.

It will often be practically unfeasible to determine the income realised after deduction of costs on a current monthly basis. It can only work in relation to income that has already been formally approved in the past (most often by the tax authorities). When the income has already been formally established by the tax authorities, it can be considered as a fixed income basis for the collection of social security contributions, and hence no provisional payments have to be made. This method was traditionally applied in the Belgian system (until 2015). It has the advantage of providing certainty for the self-employed when paying contributions. The disadvantage, however, is that a time gap emerges between the year in which the income has been reported for tax purposes and the year when it is used in its consolidated form for contribution collection (two to three years depending upon the particular system in place). The economic circumstances in which the self-employed is working may by then be different, and the current income in the year of payment may deviate quite substantially from the income that once served as the basis for a tax declaration.

An alternative approach is to have the contributions calculated on the basis of a provisional defined income which, once the final income is established by the tax authorities, can be revised. Consequently, additional contributions will be levied if the income turns out to be higher than provisionally declared, or the social security fund will have to return contributions if the final established income turns out to be lower (the current system in Belgium). Also in Portugal, the self-employed must declare the income earned in the last quarter of the previous year, as well as confirming or stating the income earned for the previous calendar year (annual statement). The social security services review the annual earnings statement submitted in the previous year on the basis of the income information handed over by the tax administration. If there is a difference in income resulting from the annual review, the contribution base is taken into account for the contributions to be paid in January of the following year. The self-employed person is notified of the confirmed differences and has a right of response (ISS, 2023). Thus, by way of illustration, the Belgian and Portuguese approaches start from an estimated income, which needs to be assessed as realistically as possible.

Overall, for the estimate, one may refer to the already established tax income from the past. Adjustments can be made based on recent income developments and expected changes. Regular VAT information could also be used for this purpose, for example. Then, the estimation mainly refers to the costs. Relevant information can be provided by the tax authorities. When costs are low, a baseline lump-sum value can be used, which is individualised based on experience and in case of any major changes that have occurred. Alternatively, the basis could be an income estimate based on certain criteria, such as the average wage earned in the economic sector, which is adjusted by the current revenue of the individual. This idea underlies a recent reform in Finland (ISSA, 2024). As an option, at a later stage, once the actual income is known and established, corrections can be applied, leading to collection of further contributions (if the declared provisional earnings were too low) or to a refund (in cases of too high provisional payments). In order to reduce the amount of work involved, it might also be enough to draw on the past gaps between the individual’s estimated and realised income to form the expectations underlying future contribution payments. This could be established on the basis of fixed time periods (e.g. every five years). In any case, as unemployment is by nature a short-time risk (as opposed to, for example, pension schemes), financing based on a measurement of current income would have clear advantages.

Defining the income basis independently of the taxable income

In the previous chapters, we described the reliance (by many a system) on cooperation with the tax authorities, either by having the contribution organised by the tax authorities and/or by using relevant tax data (such as declared professional income or the income established by the tax authorities). As an alternative to this cooperation, the social security system may opt to determine the income levels, separate from the tax system. In this situation, the self-employed persons may be invited to choose their contribution level themselves; sometimes the level chosen will eventually determine a certain benefit level. The advantage is the practical simplicity and, if the benefit level depends on the income level, the underlying transparency of the scheme (low declared income will lead to low benefits and high(er) declared income will result in higher benefits). For voluntary schemes, such a solution may seem attractive. However, it may fall short of the requirements of comprehensive compulsory schemes. The issue of non-participation, known of from voluntary schemes, would probably reappear in the form of a person choosing to pay the lowest possible social security contributions. Evidently, this would trigger adverse selection and hamper important principles such as solidarity, financial sustainability and benefit adequacy.

The practice of choosing lower social security contributions has been documented in Austria. Austrian self-employed can choose between three income brackets, each with a corresponding lump-sum contribution (for the actual amounts, see Pfalz, in this special issue); thus the contribution is not calculated on the basis of their actual income. Estimates indicate that 75% of the self-employed have chosen the lowest contribution tier (Pfalz, in this special issue).

For this reason, several European countries already follow a broader approach. For example, the confirmed income for Finnish self-employed corresponds to what should reasonably be paid to a person hired as a wage earner to perform identical tasks or tasks that correspond to the work in question (Arajärvi, 2018). This is established for the purposes of the (income-related) pension scheme but is used as well for the other schemes, such as unemployment. Firstly, the pension providers make an estimate of the self-employed income, based on the median wage of the business field and the turnover of the company in question. Secondly, a certain leeway is allowed (30% of the recommended confirmed income) within which the confirmed income should fall. Additionally, if the value of the work input is not sufficiently considered in the recommended income level and the leeway, the self-employed person can submit work details justifying a deviation from the recommended estimate. Finally, the income of the self-employed individual will be reviewed and adjusted every three years if needed (ISSA, 2024).

In Slovenia, for the self-employed, the calculation base is considered to be an ‘insurance base’, i.e. the profit as determined by tax law, decreased by 25%. There is an upper and lower limit. The lower limit is 60% of the average salary in Slovenia, while the upper limit is 350% of the average salary (Kresal et al., 2020).

This shows that the income basis can be constituted in a manner separate from the tax system, either fully, by having the income basis defined by social security itself, or partially, by correcting the income basis derived from the tax data. We also refer to the above country examples, in which not all tax deductions are accepted when determining the income for social security purposes.

Contribution rate?

What should, in the end, be the contribution rate for the self-employed? Should it be equal to the contributions paid for wage earners? The self-employed are a diverse group. Differentiation of contributions by unemployment risks is rather uncommon in European social security systems built on solidarity principles. Indeed, a high unemployment risk often coincides with low income. If there is no wish to depart from the existing approach, we would suggest per se equal contribution rates for all individuals. At least in the current regulatory frameworks, the transition rates of the self-employed into unemployment are not worryingly above usual levels (Fondazione G. Brodolini et al., 2018). However, if potential financial imbalances play a key role in political decisions, the unemployment incidence of the self-employed compared to wage earners could be monitored, and the contribution rates set accordingly. If politically necessary, separate insurance budgets could be used. However, the principle of balance of risks works more efficiently, the larger the common pool of insured individuals. Moreover, from a social insurance logic, high income earners can be expected to contribute more to the scheme than low income earners (see the discussion above on the definition of income).

As to the contribution level, varying approaches can be seen in the States that have an unemployment scheme in place for the self-employed (applying the same level or a different level, as will be discussed below in this paragraph and further on in the text). In Denmark, for example, the insurance funds define the contribution, both for wage earners and for the self-employed. It is normally a flat rate contribution and mostly the same for all insurance funds. The level of benefits is also the same across all funds (see Jacqueson, further in this special edition). Yet, one should be aware that this system started from the idea of a voluntary insurance based on a collective labour agreement, which was then, later on, opened up to the group of the self-employed. Unlike other systems under discussion here, it did not start from the general social security system.

Letting the self-employed choose the level of their contribution (rate) is also an option, yet we should be aware of the inherent risk of this approach. As discussed before, in Austria, for example, the choice of financing level given to the self-employed is creating issues of unfair treatment between the groups covered. The self-employed can choose their contribution base for unemployment insurance. Concretely, they can choose between three income brackets, each with a corresponding lump-sum contribution (ranging from €51 to €307); 75% of the self-employed who are voluntarily insured for the risk of unemployment choose the lowest income bracket. However, both social security schemes, for employees and the self-employed, are financed from the same pool of contributions. On the one hand, Pfalz (in this special issue) commented that this policy is creating unfair treatment vis-à-vis employees, who pay income-related contributions respecting the vertical (income-related) redistribution principle behind traditional social security schemes; on the other hand the insurance for the self-employed justifies the approach of flat-rate contributions, as they can opt to join the system whose flat-rate contribution level seems to be more appropriate (see also Denmark in this regard).

Third party contributions?

If the contribution level is comparable to that in place for wage earners, should the self-employed pay the sum of both employee and employer contributions? The distinction between employee and employer contributions is a fictitious one (Pieters, 2006; Schoukens and Bruynseraede, 2021) and based on a historical rationale introduced by the Bismarckian approach, making both groups responsible for the financing of their scheme. The overall financing needs must be considered, meaning that the combined contribution (employer/employee) is to be used as a reference. Using the same contribution rate is thus to be preferred when both groups face a similar risk of becoming unemployed, and if the income basis from which the contribution is levied is comparable. In Slovenia, in case of unemployment, the self-employed pay the total of the employee and employer contributions (Kresal et al., 2020); a similar approach is applied in Serbia, where the self-employed pay the same contributions as other insured persons. They pay the entire amount of the contributions themselves since they do not have an employer (Jasarevic, 2020).

Meeting these preconditions will not always be straightforward. The question is whether the incidence of becoming unemployed is comparable in the groups of employees and self-employed. Moreover, employees can often fall back on temporary unemployment if the employer cannot provide work due to external situations of crisis (recently, for example, because of the global Covid-19 crisis). At the end of the day, it is more important to have contribution levels in place that make sustainable social protection possible. At the same time, this need can be an incentive to introduce ‘third party’ contributions (comparable to the employer contribution) which co-finance the social protection scheme for the self-employed. In Portugal, the contractor of a dependent self-employed person also pays a contribution. Persons are considered to be contractors of ‘dependent self-employed’ if they pay up to 50–80% of the total value of the worker's activity within one calendar year. These contractors must pay a 7% contribution in favour of the dependent workers to the competent authorities. If they pay more than 80% of the total value of the worker’s activity, they must pay a 10% contribution (ISSA, 2024). In Malta, the state co-finances the social insurance of the self-employed as a third payer: the self-employed pay 15% and the State 7.5% on the annual income of the self-employed. 10 The same ceiling applies to the self-employed (Seed Consultancy, 2022).

Third-party contributors could also be included in cases where the self-employed work though an interface such as a platform (as in the system introduced in France, at least to a certain degree, see Daugareilh, 2021). 11 Here it is suggested that where self-employed persons are contracted by a client through an interface institution, such as a digital platform, the contribution could be withheld directly at the source by the interface institution, on the basis of the fee paid by the client for the purchased service or good, and paid directly into the social protection scheme. Formally, the amount could be deducted from the remuneration, paid by the customer on top of the price, or could be withheld from payment. In line with the concept of digital social security (Weber, 2018 and 2022), this could even be organised in a transnational manner, as many of the platforms work at global level. A digital mechanism could be implemented in the platforms, which transfers a percentage of the agreed remuneration to a personal social security account of the platform worker (in the country where the worker is residing or organising his or her activity), each time a job is finished. Making use of digitalisation, this enables a pay-as-you-go system for platform work, thus extending the advantages of common systems for wage earners to all platform work, regardless of how the activity is organised (wage earnership or self-employment). The idea of deducting contributions directly at the platform could be mirrored when digital invoicing becomes standard. Then, provision of a universal digital interface to an electronic contributions system would allow efficient standardised handling of social security contributions from both the self-employed and the customer.

Thresholds and ceilings

In social insurance, upper and lower income bounds often apply for redistributive reasons. The former are assessment ceilings that define the maximum income to be insured. The latter are a condition for access (see also the discussion further on in the text). Upper and lower limits may conflict with the principle of equivalence, which underlies traditional (social) insurance schemes designed to safeguard income replacement reflecting prior earnings, yet they are often justified by the need to generate vertical redistribution (income solidarity). For the self-employed, a strong social security equivalence (between what one pays in and receives from the system) is sometimes advocated (Pieters, 2018; Schoukens and Bruynseraede, 2021). However, practically all social security schemes apply minimum and maximum bounds. For example in Slovenia, the calculation base for the self-employed is considered to be an ‘insurance base’ – the profit as determined by tax law, decreased by 25%. There is an upper and lower limit. The lower limit is 60% of the average salary in Slovenia, while the upper limit is 350% of the average salary in the country. The self-employed can freely choose their contribution base as long as they stay within the lower and upper limits (Kresal et al., 2020).

Austria too applies a minimum income threshold to social contributions for the self-employed with business licences. It also applies a maximum contribution base. Self-employed with an income above € 6825 per month (€81,900 per year) do not need to pay contributions on the surplus income exceeding the maximum contribution base (Pfalz, in this special issue). In Belgium, unlike for employees, an upper contribution cap is applied to the net professional income of the self-employed, and no benefits are due on the amount which exceeds the cap. A lower minimum contribution threshold is applied as well: every self-employed person is obliged to pay these minimum contributions even if their income falls below the minimum contribution threshold (De Becker and Bruynseraede, in this special issue). In the Czech Republic, lower and upper income limits apply and the self-employed determine the calculation base themselves. If the real tax base does not reach the minimum income threshold, the minimum is lowered to 50% of the tax base (Koldinská and Lang, 2019).

When second (or multiple) jobs are performed, it is advisable to combine the income for the purpose of financing social security, as discussed in section 6. If lower limits apply, they should apply to the total income, not to each job individually. Furthermore, the more volatile character of self-employed earnings should be taken into account. When applying absolute bounds, rather than evaluating income on a monthly basis, an average over a period such as a year should be considered. As an option, a certain period directly before applying for benefits may be excluded in order to avoid incentives for overhasty business closures once the earnings situation deteriorates. Access conditions are treated below.

More generally, we should consider whether minimum income thresholds and maximum ceilings that determine access to social protection are still advisable in a world where professional activities are becoming intensively digitalised (leading among other things to a growing platform economy), and where it is becoming difficult to distinguish between professional activities (work) and other activities, also generating income (sponsorship, rental income, return on capital investment). In reality, people may live on the return from both kinds of activities; it may even be that work-related income is marginal compared with the return from the other activities. But should that matter in the end for social protection, when the overall goal is to safeguard the loss of income from which people live?

One of the leading arguments for excluding marginal work from protection was (or still is) administrative in nature – that there is too little activity or income to justify the administrative costs involved. But is this argument still valid in the light of digitally driven administration? Taking into account the variety of activities (professional or not; subordinate or not) that may generate income, the approach should be that all earned income matters for social protection. The simple fact that an activity is marginal cannot by itself justify an exemption from the payment of contributions. Income from any activity – however marginal it may be – can be used to finance social protection, especially as a growing number of people combine a series of small-scale, marginal activities, as in platform work (Schoukens and Bruynseraede, 2021). This policy will of course not always result in decent minimum protection in terms of benefits. From an equivalence point of view, low incomes will more than likely result in low benefits; these benefits will eventually be corrected by minimum protection levels, means-tested or not.

Starting up the self-employed activity: contribution basis?

In contrast to employees, who earn a guaranteed wage from the first month onwards, income in the starting phase of self-employment is likely to be uncertain and to fall short of a later steady-state level. Moreover, young firms are more likely to channel saved means into business expansion (Benzarti et al., 2020). Therefore, one could consider setting a lower contribution rate in this phase. Realistically, however, the contributions would in many cases not be sufficient during this period to generate unemployment benefits above the social assistance level. This could be resolved if hypothetical contributions at a normal level are used for accessing benefits and calculating claims. Logically, for such a solution, one would have to accept a certain degree of cross-financing from other contributors or tax for the start phase. For example, in Germany a halved contribution is required in the start-up phase if the self-employed person takes up the voluntary insurance (to which they previously belonged as an employee). However, the amount does not depend on income, i.e. the absolute contribution is the same for all the self-employed, and the benefits increase with the qualification level (or the wage in a previous employment relationship), thus not in line with the current income of the self-employed person.

Contributions can either be reduced proportionally, or to a flat-rate contribution. For example, in Slovenia, persons starting off in self-employment only need to contribute a smaller proportion of their income to social security. During the first two years of self-employment, reductions are applied. During the first twelve months, the self-employed pay only 50% of the contributions due, while during the following twelve months, they pay 70% of the contributions due (Kresal et al., 2020). In a similar manner, Finland grants new entrepreneurs a 22% reduction in contribution payments for the first 48 months of self-employment (Arajärvi, 2018). In Spain, unlike in Slovenia, contributions are reduced to small flat-rate sums. New entrepreneurs can enjoy reduced, flat-rate contributions of €80/month in the first year of the business start-up. This rate can be extended for one additional year if the income falls below the interprofessional minimum wage, or for two or three years for certain sectors. Autonomous communities can allow further reductions, for example, zero-fees in Madrid, Murcia, etc. (ISSA, 2024; Seguridad Social, 2024). Similarly, in Belgium, income is set at a lower level for new self-employed during the first three years: they pay a flat-rate contribution calculated on a minimum income threshold. One reduction is possible in the first quarter. After three years, the contribution level is readjusted to the real net professional income. The difference in contribution rate needs to be offset. For first-time starters, a higher reduction is applied in the first four quarters. They can also benefit from the first quarter reduction (De Becker et al., 2024).

For the self-employed in particular, practical simplicity and low administrative burdens of insurance schemes are very important. Since the mere collection of contributions is unspecific with regard to the respective scheme, (mandatory) unemployment insurance contributions should be administered together with other social insurance such as health and pensions. This could be justified in light of the 2019 EU Recommendation, to enhance system transparency (Schoukens, 2022).

Access and entitlement conditions

Access conditions: minimum work or income?

Unemployment insurance, covering the loss of prior occupation, traditionally applies conditions on minimum insurance periods. Hence, before claims can be made, certain prior minimum work records, contribution payments and/or income prerequisites are required.

How to measure working hours? Assessing entitlement based on the number of working hours, as is often done for employees in unemployment benefit schemes, is difficult in the case of the self-employed. This group do not usually keep track of the number of working hours, nor would it be practicable to verify such a number. Therefore, access conditions for the self-employed are more usefully income-based. A fixed contribution rate will coincide with a contribution-based access condition. The minimum contributions reflect minimum financing needs. Certain minimum contributions should therefore be applied for accessing the scheme.

Systems can choose to have the minimum conditions defined differently across the professional groups (for employees, conditions regarding minimum working time; for the self-employed, minimum income/contribution conditions). The disadvantage is the loss of labour status neutrality: the conditions will have to be defined differently. Malta takes an interesting approach to conditions for formally accessing the unemployment scheme. Both employees and the self-employed are covered against the risk of unemployment. Yet, workers are covered only if they fall within the definition of ‘employee’, meaning that they work at least eight hours a week. For the self-employed, the condition is to have earnings exceeding a fixed amount (€910 in 2022) a year (Seed Consultancy, 2022). The entitlement conditions (see also further below), refer, for all professional groups, to the minimum insurance contributions paid into the system. A two-tiered contribution record is required to qualify for unemployment benefits: (a) the claimant has to prove that (s)he has paid at least 50 contributions (payable on each Monday) since being registered as insured under the Social Security Act; and (b) has to prove that (s)he has paid or credited at least 20 contributions during the last two calendar years prior to the application (Seed Consultancy, 2022). Alternatively, in Denmark, the self-employed can access the unemployment benefit scheme on a voluntary basis; for that purpose they document a minimum level of income (at least DK233.376) earned in the last three years. If this income comes solely from the company's profit, it should not be lower than the minimum level established within the last five years (Jacqueson, in this special edition). Here as well, the income level determines formal access to the unemployment insurance scheme, and not working days/hours, which are more difficult to measure. However, if activities are combined, all hours worked as both employee and self-employed can be accrued to reach the minimum threshold, including supplementary secondary work (Munckholm and Schjøler, 2020). The unemployed have then to prove a certain work record. Due to the volatile nature of self-employed activities, the income is retrospectively transformed into the required work record, on the basis of a fixed parameter. 12 By doing this, a labour status neutral measure – activity-based, regardless of whether as an employee or as self-employed – is applied, which helps the individual to reach the required minimum more easily if activities are combined simultaneously or consecutively.

Unlike Malta and Denmark, Slovenia does not distinguish between labour statuses in order to determine the insurance record requirements. The unemployed – regardless of whether they were employees or self-employed – have to prove that they have been insured for at least 10 months in a reference period of 24 months immediately prior to the unemployment. 13 An unemployed person younger than 30 years old has to prove that they have been covered for at least six months in the last 24 months (Kresal et al., 2020). 14 The insurance requirement is not further specified in numbers of working hours.

Minimum income? Lower bounds in social security systems are connected to the assumption that a certain minimum income is needed to earn a living. This minimum is often required to formally access the scheme; likewise it often serves as a minimum basis from which contributions are to be paid (see above). While such limits are the outcome of important social policy decisions, they are not specific to the group of the self-employed. Rather, a default solution would be to apply the regulations in place for wage earners in each country. This assumes that comparable legal concepts of income are taken as a basis, such as the minimum wage level for employees.

Naturally, self-employed income can fluctuate even if the activity itself is continuous. Applying a minimum contribution avoids a situation in which, for certain time periods, the self-employed person is no longer covered when failing to reach a required minimum income. This means that the self-employed are considered to pay contributions (minimum) from a virtual minimum income level, even if in reality their income may fall below the minimum. However, setting a minimum level can create other problems, such as consolidation of the self-employed income around the lower limit. This is reported as problematic in the Hungarian report (Jakab, in this special issue). Self-employed workers are required to pay at least contributions calculated on the minimum monthly wage. Most self-employed declare their income at the minimum level, thus limiting their participation to the minimum contribution floor (Jakab, in this special issue). Regardless of the predefined minimum threshold applied for formal access, the eligibility requirements are still based on the number of working days (see further below).

Some States do not necessarily impose a strict obligatory minimum for contributions to be paid in all circumstances, but limit formal access to certain insurance schemes when the self-employed (or employees) do not reach a minimum income threshold. For example, in Austria, the self-employed are, similarly to employees, subject to a minimum income threshold (calculated on an annual basis). For employees, failure to reach the minimum threshold means loss of mandatory coverage for all risks except work-related accidents. They can voluntarily opt into the health and pension insurance scheme. Self-employed workers with an income below the minimum income threshold are still insured if they hold a business licence and are members of the Chamber of Commerce. If so, contributions are calculated on the basis of this minimum threshold, as if their income amounts to the relevant threshold. If they do not have a business licence, they lose all mandatory insurance (also for work-related accidents). However, they can opt into health, work-related accidents and pension insurance. Voluntary access to unemployment insurance is not possible (Pfalz, in this special issue).

If the self-employed person is not able to pay the required minimum contributions (‘temporary low income’), an exemption from payment can be granted. By use of a temporary payment exemption, complete loss of social coverage can be avoided. This would, however, have an effect on the eventual protection (coverage): it can result in a longer waiting period for payment, as the first period of unemployment would not be covered (suspension of payment in a first period). Alternatively, the maximum duration may be shortened.

In Iceland, a minimum contribution is also required. The self-employed are fully insured against unemployment if they have paid the relevant taxes and social insurance tax on their calculated remuneration, equivalent to a reference sum for the last 12 months prior to the claim to the Directorate of Labour. According to the entitlement conditions, the self-employed must ‘have paid social security tax and tax deductions at source on calculated remuneration, in accordance with the decision of the tax authorities, when they ceased business operations’. 15 However, the Directorate of Labour may grant exemptions in cases where they have not paid (social) taxes at the time of cessation of business operations, if they pay these contributions later, retroactively. Only a maximum period of three months can be taken into account, in which the payment of these levies was in arrears. 16 However, benefits are reduced pro rata if: (a) the self-employed person contributed for less than 12 months but on their calculated remuneration equivalent to the reference sum; or (b) if they contributed for 12 months, immediately prior to the application, on their calculated remuneration lower than the reference sum. They are not insured if they have contributed less than 25% of the reference sum or for less than three months. 17

Minimum contributions in a given time frame? As an access condition, at least minimum contributions would be required in a minimum number of consecutive periods (months or quarters). What if a person, after a period of unemployment, starts up an activity but does not reach the minimum for renewed entitlement to unemployment benefit? We are of the opinion that non-employment gaps should not immediately lead to the loss of coverage, as maintenance of coverage may help ensure a smooth transition between professional activities (even if these are performed under different labour statuses: see in this respect the 2019 EU Recommendation on effective protection; Article 10). In such cases, it would make sense to use the regulations already applying to unemployment insurance for wage earners. For instance, a time frame of a few years could be established within which payments should be received in a minimum number of months.

For example, Finland applies a similar time frame to that for employees, but allows a longer reference period within which to demonstrate a longer work record. In order to be entitled to unemployment benefit, employees must have worked for 26 weeks in a period of 28 months. For the self-employed, the requirement is for 15 months activity out of a reference period of 48 months (Arajärvi, 2018).

In addition, Austria, when determining the reference period, differentiates by age and the presence of subsequent applications. For first time claims, in order to be entitled to unemployment benefits, one has to be insured against unemployment for at least 52 weeks in the 24 months immediately preceding the date of application. If the person is under 25 years of age, only 26 weeks in 12 months need to be proven. For each subsequent claim, one has to prove 28 weeks of insurance in 12 months or at least 52 weeks in the 24 months prior to the claim (Pfalz, in this special issue).

Moreover, Belgium allows the opening of additional rights in the bridging right (the specific unemployment scheme for the self-employed) subject to a sufficient contribution record. After the first period of the bridging right (one year) is exhausted, a new minimum period of insurance is applied, amounting to four quarters preceding the quarter in which the event which caused the business closure took place. Contributions must be paid, but these need only to be paid for at least four out of the 16 quarters preceding the quarter when the event that caused the business closure took place (De Becker and Bruynseraede, in this special issue).

Lastly, apart from the fulfilment of an insurance record during a predefined reference period, it is also possible to explicitly include insurance interruptions in the calculation of insurance records. In Serbia, for example, interruptions in the insurance period can be accepted. In principle, the unemployed person must have been covered by the mandatory insurance for at least 12 or 18 months; however, that period may include interruptions of up to 30 days (Jasarevic, 2020).

Labour status neutral approach. In general, as some national examples show for access conditions, it is possible to think of an overarching rule applicable to all groups. For wage earners, a minimum level of contributions within a certain time frame paid in a minimum number of months coincides, in practical terms, with a certain lower limit on the monthly salary. For employees, work is usually measured in hours, so income- or contribution- based approaches are applicable. The above-discussed regulation for the self-employed can be linked to the logic of many social security systems. Such an approach has the further advantage of including different activities in the same insurance scheme. Access would not have to depend on whether contributions were paid from a previous wage earner job, only from self-employed activity, or both. This is especially beneficial since income security is particularly important during transitions from one job or activity to another (ILO, 2016).

Here we refer again to the Danish system, where all hours worked as an employee and all hours worked as self-employed can be taken into account when determining eligibility for unemployment benefits (by using the income converter for the self-employed: see above). The focus is on the person’s activities rather than his or her labour status (Jacqueson, in this special issue). In a similar fashion, previous records built up in another status (e.g. as an employee) can be taken into account. For example, in Luxembourg, the self-employed need to prove they have been covered by the mandatory pension insurance for at least two years. Affiliation as an employee can be taken into account insofar as the self-employed activity started at least six months before the benefit claim. 18 In a comparable manner, the Icelandic Unemployment Insurance Act allows the cumulation of activities in determining insurance entitlements insofar as the self-employed person was employed as a wage earner in the 12 months before applying for unemployment benefits. 19 Similarly, in Austria, where access is based on voluntary insurance, we find rules reflecting this idea of using insurance periods accumulated under the other professional status. If the self-employed person opts into the unemployment scheme, a certain commitment period is required. If a person wishes to join the unemployment insurance, they must commit to contribute to the system for eight years. He or she can terminate the insurance by declaring his/her wish to terminate within six months of the end of each eight-year period. If the unemployed person has not done this, they will be bound for an additional eight years. The chosen contribution base cannot be changed during the commitment period, but only if the person rejoins the insurance scheme after an exit (Pfalz, in this special issue).

In practice, additional access conditions may be applied, making the combined application of minimum insurance records across the professional statuses more problematic. In Germany, for instance, the self-employed have access to the scheme only in the first three months of their activity and only if they were previously employed in a job subject to social security. Here, the challenge would be to provide access to all self-employed regardless of their employment history (Weber, 2022), as advocated in the 2019 EU Recommendation (see in particular Article 10 on effective access).

Entitlement conditions

Entitlement to unemployment benefits is dependent on several factors (Pieters, 2018). First and foremost, unemployment should be involuntary; the unemployed person must actively look for a new job or occupation and should thus be available to the labour market; formally (s)he should register with the labour market services so that they can provide help with the job search and can monitor the follow-up of the conditions. The unemployed person should be capable of working (otherwise they may claim a work incapacity benefit), not of pensionable age, have no labour income and no (professional) activity. We will focus mainly on the involuntary character of the unemployment (and the adapted provisions for self-employment, expressed as closure of business vs. temporary drop in income), availability to the labour market and active job search, as these elements often seem to be problematic for the self-employed.

Involuntary unemployment. One of the major conditions for wage earners is usually that unemployment should be involuntary; the worker must not be ‘responsible’ for the unemployment. If they are, no entitlement to the benefit is granted, or alternatively the worker is sanctioned during a first period of unemployment (suspension of the benefit). In the case of wage earners, the (in)voluntary nature depends strongly on the dismissal (how the worker was dismissed). Involuntary unemployment is the consequence of a dismissal for which the worker cannot be blamed (dismissal by the employer i.e. not grounded on serious misconduct by the employee).

By analogy, the involuntary closing down of the self-employed activity would be an essential element in the evaluation of unemployment. Yet, it can be difficult to check whether the self-employed stopped their business voluntarily, since there is no formal layoff and the information is asymmetrical. Closing down a business that is still profitable and generates at least a reasonable subsistence income may, for example, be seen as quitting voluntarily. Even closing down the business because of individual mismanagement by the self-employed person could also be considered as unemployment provoked by the person’s own misbehaviour (and thus voluntary). Assessing the involuntary character of unemployment is thus a challenging exercise when applied to the self-employed. Logically, this condition will have to be reconsidered for this group, due to the absence of an employer. Most countries link the involuntary character of the cessation of activity to an external situation.

A clear list of external situations which must have taken place to cause unemployment for the self-employed, can be found in the Luxembourg Labour Code. In Luxembourg, the cessation of activities can be accepted as involuntary on the basis of four situations: (a) economic and financial difficulties; (b) medical reasons; (c) actions by third parties; and (d) force majeure. Furthermore, the (former) self-employed have to sign up as jobseekers at the employment offices (see further below). 20

In a similar manner, but with different conditions, Spain also relates the involuntary business closure of the self-employed to external economic, technical, productive or organisational reasons: these should make it unfeasible to continue the activity and/or require the closure of (every) establishment open to the public, at least during the period of receipt of benefits (Salas Porras, in this special issue).

Exceptionally, the Belgian bridging right contains an element of ‘voluntary’ access. In Belgium, the bridging right is granted in situations in which the self-employed have been forced to cease or interrupt their activities due to circumstances beyond their control. The bridging right restricts entitlement to a limited list of causes (i.e. natural disasters, fires, impairments, allergies, bankruptcies and decisions of third economic actors or events that have an economic impact). Protection is also provided if the self-employed ‘voluntarily’ stop their activities due to economic difficulties (De Becker and Bruynseraede in this special issue). These difficulties are identified by the fact that the self-employed has an income below the minimum subsistence level for a certain period of time, has asked for an exemption from contribution payments and/or received social assistance benefits. 21 One could therefore say that the closure of the business is not completely left to the voluntary will of the self-employed. External economic elements accompany the person’s decision to finally close down the activity, which seems to be no longer economically viable.

Apart from difficulties assessing the (in)voluntary nature of unemployment, we also observe a trend regarding the legal consequences of voluntary unemployment: workers in many systems will in any rate become entitled to a benefit after a certain period of benefit suspension. Voluntary unemployment is only sanctioned with no entitlement at all in situations when the unemployment is intentional: i.e. if a person stops working with the intention of drawing benefit. In other words, wilful misconduct cannot be a basis for benefit entitlement.