Abstract

This study attempted to assess the impact of Amanah Ikhtiar Malaysia’s (AIM) microcredit programme on the level of economic vulnerability among hard core poor household clients in Peninsular Malaysia. To attain the objective, this research utilized economic vulnerability index. This study employed a cross-sectional design and stratified random sampling methods. Findings showed that participation in AIM’s microcredit programme decreases the level of economic vulnerability. The study suggests that AIM should, therefore, emphasize on designing flexible and diversified financial products and delivery methods together with skill development training to improve the socio-economic condition of the hard core poor households in Malaysia.

I Introduction

The challenges in effectively measuring the level of poverty have increased with our recent understanding as the literature on poverty emphasized on multidimensional aspects of poverty instead of focusing only on money-metric measurements. Moreover, existing studies on poverty also highlighted on measuring various dimensions and exposure to risks that effect household’s economic conditions. For example, vulnerability to income poverty was conceptualized as the probability of falling below the poverty line income (McCulloch and Calendrino, 2003). Microcredit, on the other hand, is considered as one of the leading mechanisms that help improving the socio-economic conditions of the poor. It’s an innovative method enabling poor households to reduce vulnerability during socio-economic crises (Gurses, 2009). Access to microcredit therefore is expected to lead to a decline in the level of economic vulnerability among clients’ households (see Bayulgen, 2008; Islam, 2007; Matin et al., 2002; Ray-Bennett, 2010; Schurmann and Johnston, 2009).

In fact, whether the access to microcredit has a significant impact in reducing poverty (Khandker, 1998) or it carries a negligible impact in reducing poverty (Morduch, 1998) is in question but, in the extant literature, there are clearer evidences that it became successful in declining the vulnerability. For example, the following studies (Hashemi et al., 1996; Husain and Mullick, 1998; Montgomery et al. 1996; Morduch, 1998) found that microcredit is effective in acquiring assets and empowering women, diversifying income generating sources and escalating disaster coping mechanisms. Vulnerability is now recognized as a key element of poverty alleviation dimensions while literatures on microcredit have already established the effective role of financial services on vulnerability.

The relationship between poverty and vulnerability is also acknowledged in the literature of Mareen (2008) as the accepted academic wisdom on these two concepts experienced a marked change in the near past. Most of the literatures on vulnerability (see Cutter, 1996; Fussel, 2005, 2007; Janssen et al., 2006; Kasperson et al., 2005; O’Brien and Leichenko, 2000; O’Brien et al., 2004; Turner et al., 2003) stressed on the measurement of peoples’ livelihood change. Microcredit generated the support for additional income sources which, in turn, could be used for education, health expenditure, and savings (Pearlman, 2006; Khandker, 2001); hence, it has emerged as a useful tool in enhancing income.

While literatures on microcredit based poverty and vulnerability are on the rise around the globe, there is lack of extensive study on this issue in the Malaysian context as a less disaster prone economy. Researchers also argued that participation in microcredit programme may not mostly benefit non-poor or better-of-poor and it can even harm hardcore poor (Parker and Pearce, 2005). Therefore, it is imperative to measure the impact of microcredit programme on economic vulnerability in Peninsular Malaysia. This study aims to minimize this literature gap by employing economic vulnerability index which is the unique contribution of this study. This study also proposes that the use of such index will also contribute in increasing our understanding on the influence of microcredit in reducing vulnerability in Peninsular Malaysia.

The most well known microcredit provider in Malaysia is Amanah Ikhtiar Malaysia (AIM). AIM was established in 1987 to provide small scale financial services to the poor. AIM selects their clients based on household income that falls below the poverty line income. AIM provides three economic loans: I-Mesra loan, I-Srikandi loan and I-Wibawa loan. Until August 2010, AIM had extended their outreach to a total of 254,116 clients with a 99.42 per cent repayment rate (AIM, 2010). AIM also provides skill development trainings including basic accounting, basic entrepreneurship, financial management, business communication and members’ development programme. Since AIM is the only microcredit organization that operates at the national level and serves more than 82 per cent of the poor households in Malaysia, this study, therefore, selected AIM in order to measure the impact of microcredit programme on economic vulnerability among the hardcore poor households in Peninsular Malaysia.

II Literature review

Commonly the borrowers utilize the loans they received from microcredit organizations to mitigate their economic and social needs. Microcredit enables them to cope with economic vulnerability and to seek better livelihood. A review of earlier studies conducted to measure the effectiveness of microcredit on reducing economic vulnerability of the poor borrowers and their households are presented in this section.

Béné (2009) conducted a study that aimed to observe the nature of poverty among fishers in two dimensions – chronic poverty and vulnerable to poverty. The chronic poverty exists due to inherent low-productivity of the sector while vulnerable to poverty arises because of the existence of high exposure to risks and shocks. The study attempted to examine whether the existence of poverty among fishers is created from chronic poverty or it is because they are vulnerable to poverty. The author developed an economic vulnerability index along with the utilization of conventional approach of estimating the income poverty in an attempt to examine the reasons for continual poorness of fishermen. The study addressed the concept of vulnerability as a two dimensional facts: (a) exposure to risk, and (b) susceptibility – both was considered as a composite factor. The development of quantifying and measuring the economic vulnerability had gained focus only in recent times among researchers which was ignored previously due to complex nature.

Naude, Santos-Paulino, and McGillivray (2009) attempted to measure household vulnerability to poverty along with country and regional level vulnerability due to external shocks. The main purpose of their study was to assert the recent advances in the concept and measurement of vulnerability on different levels. This article provides details on the concept of vulnerability giving definitions of several disciplines, such as International Strategy for Disaster Reduction (ISDR), as well as an economist’s view of vulnerability. The common element found about the vulnerability is that it evolves from an unexpected outcome. In such situation, vulnerability arises as a result of ‘exposure to hazards’ which is the source of trouble. The study stressed that such type of hazards could be stimulated from environmental, socio-economical, physical and political trouble that exhibit vulnerability at micro (household), meso (regional) and macro levels.

Mareen (2008) conducted a study with the aim of overcoming the limitations on contextual analysis of microcredits and vulnerability in terms of poverty alleviation or poverty traps in Bangladesh. This study addressed an in-depth investigation on the twofold impact of microcredit and flooding in Bangladesh using empirical data and accumulating literatures from a number of disciplines. It was cited that vulnerability is the root and indicator of poverty. The link between vulnerability and microcredit was addressed for further discussion on the concepts of vulnerability and poverty using extent literatures. The article attempted to recognize the historical change in the academic wisdom on these two concepts – poverty and vulnerability while it evaluated the context on which microcredit in Bangladesh are disbursed. It was found that the utilization of preventive mitigation and coping strategies appeared to be deteriorated in the last few years due to financial constraint because of a fall in rural income even though there were presence of many micro credit organizations operating in Bangladesh. Potential poverty trap resulted due to microcredit organizations’ policy of lowered debt capacity and restrictive terms for which indebtedness increases. In this instance, borrowing from other sources is creating more indebtedness and making the borrowers more vulnerable to poverty. The theoretical argument of microcredit policies is giving importance on protecting its clients away from poverty traps. The study suggested that microcredit organizations need to emphasize on the demand of their clients to prove their argument of alleviating poverty is the outcome of their programmes where environmental disaster is chronic and a threat to sustainable livelihood.

The study conducted by Fisher and Weber (2004) aimed to contribute in improved understanding on asset-poverty relationship by analyzing the influence of place of residence while available literature is full of experiments at individual-level. The authors employed random-effects logistic model of the probability while considering asset poor as dependent variable and household and place of residence are independent variables. This research translated that asset or wealth is an important indicator for measuring poverty. The study used Panel Study Income Dynamics data of 1989, 1994 and 1999 to attain the objective. It was found that place of residence is an important determinant of asset poverty whether there are existences of household characteristics or not. The results showed that when all else equal, there is a high risk of being asset poor either households place of residence is in a central metropolitan area or in a non-metropolitan area.

With the objective of exploring the relationship between microcredit and the reduction of poverty and vulnerability using data from Bangladesh Rural Advancement Committee (BRAC) as one of the pioneering microcredit organization in Bangladesh, the study conducted by Zaman (1999) argued that microcredit helps in mitigating a number of contributing factors that cause vulnerability. Among the issues, such as impact of microcredit on poverty, the role of microcredit in reducing vulnerability during crisis, reducing vulnerability through asset creation, reducing vulnerability of women and empowering women addressed in this study. This study employed univariate and multivariate data analysis using primary survey data of 1,072 households. The study had drawn several policy implications to reduce vulnerability, such as the usage of collected savings, and complementing microcredit with other offerings.

Gurses (2009) conducted a study on microcredit and poverty reduction in Turkey with the goal of examining the manifestation of poverty in contemporary Turkey. To date it was found that economic vulnerability is still the vital problem in Turkish economy. The study suggested conducting well designed poverty impact studies to decide on microcredit organizations success in reaching the core poor. To be more effective, microcredit organizations disbursement of microcredit should be supported with other complementary interventions.

The estimation of vulnerability was conducted using past information to know the probability of attaining or failing a specified level of welfare (McCulloch and Calendrino, 2003). While longitudinal (panel) data were used to measure the vulnerability in the literature of McCulloch and Calendrino (2003), Béné (2009) noted that the use of such index in the case of sub-Saharan Africa is not possible. This is due to the relative scarcity of household data in sub-Saharan Africa and because of the presence of highly seasonal and temporary mobile population among small-scale fishers. Therefore, Béné (2009) proposed a cross sectional vulnerability index which is composed from the original vulnerability definition that combines the notion at two levels of exposure and susceptibility. The proposed vulnerability index (Vig) is the function of coefficient of variation (CVg) of households’ incomes belonging to the same group g, and proportion of total cash-income (or cash dependence) of the household i derived from its main activity a which is noted as Depia. Using such cross sectional data it is only possible to estimate the variability of expenditure or income across household rather than over time (Béné, 2009).

Finally, acknowledging the conceptual differences of vulnerability and income poverty, Béné (2009) added a poverty gap component in the index which addresses that a household’s poverty vulnerability is less likely if its status is far above the poverty line than the one which is just above poverty line. To illustrate the empirical relevance of the index, the relevant data were collected from survey held in June and July, 2006 along the Luilaka River and Salonga River area. 104 fishing camps were considered and of that, 43 were surveyed randomly which is 41 per cent of the total number. The numbers of focus-groups were 17 selected based on standard rapid rural appraisal techniques covering the social, institutional and economical characteristics of the groups. The numbers of individual interviews among fishers were 74 and additional 14 interviews were conducted from women involved in collective fishing. The comprehensive information on household main activities, income and general characteristics was collected through questionnaire. The origin of households were divided into two – local (residents) and non-local (comers) and based on this four ‘geo-economic groups were categorized as (a) Resident fishers operating along the Salonga (Res-Sal); (b) Resident fishers along the Luilaka (Res-Lui); (c) Comers operating along the Salonga (Com-Sal), and (d) Comers operating along the Luilaka (Com-Lui). The findings of the study translated that a high vulnerability exists among full-time fisher folk and indicated that mobility was a major issue for increasing vulnerability. The results also illustrated that households could be essentially highly vulnerable even when their income status had lied well above the average local income. The findings of the study were found to be more consistent with the available small-scale fisheries specific literature. The evidences found from that the new vulnerability index was able to give a simplistically meaningful methodology in analysing vulnerability arising from economic poverty which could be utilized to other small, or marginalized, and socio-economic groups in the case of lacking of longitudinal data for a large sample size where data collection would not be accomplished (Béné, 2009).

III The economic vulnerability index

At individual or household level, vulnerability is commonly defined as risk of exposure to potentially harmful events. Studies conceptualized vulnerability as vulnerability to income poverty (McCulloch and Calendrino, 2003), to asset poverty (Fisher and Weber, 2004) or a more dynamic concept reflecting the risk of exposure of a combination of political, natural and economic disasters. Economic vulnerability index was designed to measure hardcore poor household’s current level of exposure to risk. The economic vulnerability index is presented below:

EV denotes the vulnerability index that measures the level of economic vulnerability of the hardcore poor client’s households. CVi is the coefficient of variation of average monthly household income (last twelve months) among the same group of households (new and old). A higher CVi indicates a higher variation in the distribution of household income, therefore members of that group are more likely to be highly income vulnerable than that of others (Béné, 2009).

IV Research methodology

The underlying assumption behind microcredit programme is that the borrowers will invest the credit they received in income generating activities, which commonly includes small scale production or farming or microenterprise activities and these new investments expected to improve their socio-economic wellbeing as well as deal with economic vulnerability (Montgomery and Weiss, 2011). As mentioned by Montgomery and Weiss (2011), impact assessment methodology addressed how participation of microcredit programme affect the selected variables with how those same selected variables would have in the absence of microcredit programme. The most appropriate method to address the question should be by employing an experimental design. In full experimental approach, researchers need to construct an experiment in which all other variables are controlled, so that the effect can be attributed to the causes (Hulme, 2000). However, it is just not possible to control all the factors while measuring the impact of microcredit (Hulme, 2000). Moreover, other limitations of randomized study design are that it fails to address the effect of programme placement and self-selection bias (Montgomery and Weiss, 2011).

Since the full experimental approach is not feasible for assessing the impact of microcredit programmes (see Khandker and Pitt, 1998; Montgomery and Weiss, 2011; and Swain and Varghese, 2009), this study therefore used a quasi-experimental approach to measure the impact of microcredit. In quasi-experimental approach control and treatment groups are used to measure the impact of AIM’s microcredit programmes on the hardcore poor borrowers’ household level of economic vulnerability in Peninsular Malaysia. In Malaysia, AIM provides financial services to more than 82 percent of the poor and hardcore poor households. The rest of the poor and hardcore poor households are more likely to receive financial aid from other government and non-government development agencies or projects. It is also highly likely that these poor households live in remote locations, and therefore are unable to form a five member group and participate in weekly centre meetings and/or they just do not want to participate in AIM’s microcredit programme. To minimize the difference between the control and the treatment group, this study therefore selects the control group from AIM’s client base. Selecting the control group from the clients’ base is expected to minimize the self-selection bias. Nevertheless, sampling only existing clients may bias the sample based on those who stayed, not dropped-out. Since the average dropout rate for in AIM is very low, therefore this research did not collect any data from dropouts.

This research employed a cross-sectional design to measure the impact of AIM’s microcredit schemes in Peninsular Malaysia. This study used a deductive reasoning approach to assess the impact of microcredit. It adopted the group statistics that has been most often used known as ‘average effect of treatment of treated’, which measures the impact on the outcome of one group compared to others. The average programme impact is estimated by comparing the average outcome of the members of treatment group (old respondents) with the same average outcome of the members of the control group (new respondents).

This research employed a stratified random sampling method, where samples were selected from three different geographic areas from three states namely Kedah, Kelantan and Terengganu in Peninsular Malaysia. These three states were randomly selected from the bottom six states (poverty rate were relatively higher in these six states) of Peninsular Malaysia. AIM offered financial services to the poor and hardcore poor households through a total of 28 branches in three selected states. Most of these branches are located in a very small town or rural areas, as the poverty rate in isolated rural areas are expected to be much higher than urban areas. Among these 28 branches, this study randomly selects three branches from each state. The selected three states were Baling from Kedah, PasirPuteh from Kelantan and Setiu from Terengganu. All data were collected from these three branches.

The sampling methodology was designed to compare two groups of clients, where both groups were selected from the client base of AIM. Therefore, instead of external control group, this study selects new clients (number of months as clients was less than 24 months) as control group and old clients (number of months as clients were between 48 months to 72 months) as treatment group based on the number of month they were participating with AIM. All the clients were first selected based on number of months as client and then selected again based on pre-AIM household income. Clients with pre-AIM household income below half of the joining years PLI were the hardcore poor clients. 2,779 clients participated in this programme in all three branches for the selected period. Among them, a total of 505 clients or around 18 per cent of the 2,779 clients were hardcore poor and among these 505 clients, 22 clients or around 4.36 per cent clients were dropped out from the programme. This study then collected data from AIM’s client’s record book. Data about 483 hardcore poor new and old clients’ current unpaid debt, pre-AIM household income, joining date, total amount clients saved in AIM, total amount of credit received from each scheme and the total amount of credit received, had been collected.

In the second stage of data collection, the researcher explained the purpose of this study and asked these 483 selected clients for their permission in interviewing them. Among the 483 clients, 386 clients agreed to participate in the interview after their weekly centre meeting, among them 184 were old clients and 202 were new clients. Among these 386 clients, 45 clients mentioned that they received credit from other sources after they joined AIM’s microcredit programme, and 8 clients did not answer all the questions because of their personal reasons. This study then excluded those clients who received credit from other sources and did not answered all the questions, and collected complete data from total 333 hardcore poor clients, among them 161 were old clients and 172 were new clients.

V Summary of findings

1 Demographic characteristics

The mean age of the old respondents is 37.40 with a standard deviation of 10.51, which is higher than the mean age of new respondents, 34.42 years with a standard deviation of 9.93, and it indicates that respondents who are participating AIM’s microcredit programme for a relatively longer period of time are also relatively older than that of others. As presented in Table 1, the mean number of years in school by old respondents and their household heads are also relatively higher than that of new respondents and their household heads. However, among these 333 household heads, 98 of them did not have any formal education.

Although all the respondents were women, findings showed that 168 out of 333 respondents’ household heads (principle economic decision maker) were male. The proportion of households reported to have male household heads among new and old respondents were 53.48 per cent and 47.21 per cent, respectively. The mean number of members among new and old respondents’ households was found to be 4.42 and 5.11 members, respectively.

Demographic characteristics

Source: Authors’ research.

Notes: *YIS: number of years in school; **GEM: number of gainfully employed members.

2 Participation status

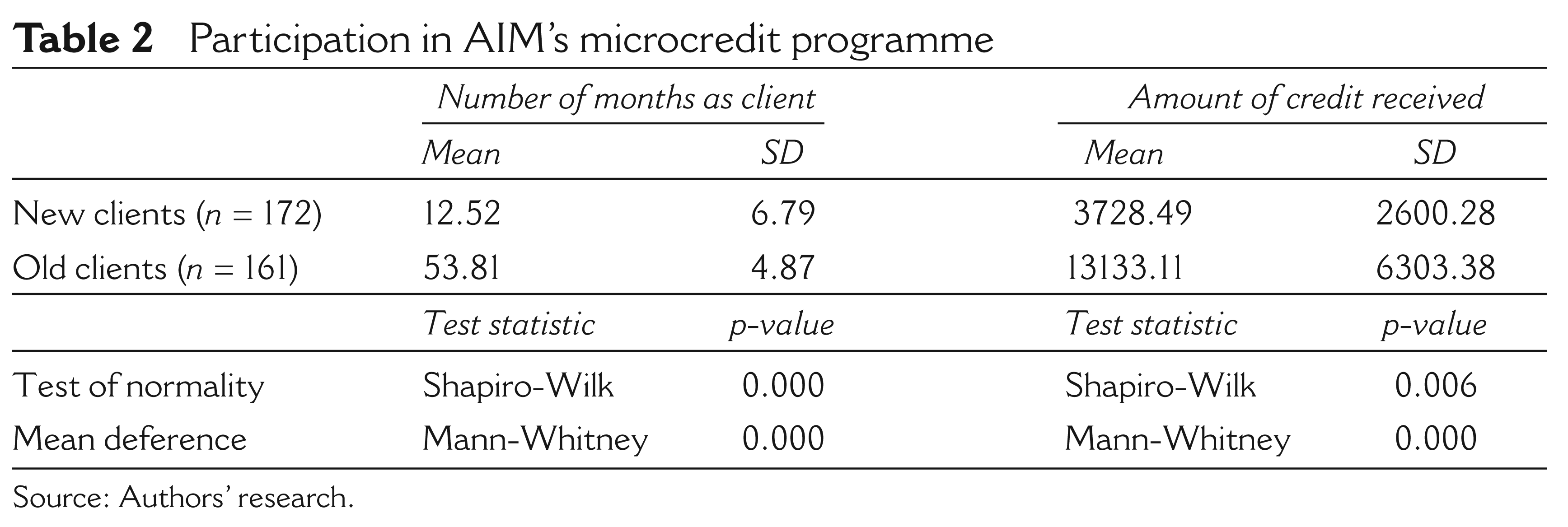

As presented in the Table 2 below, the mean number of months between new and old respondents participating in AIM’s microcredit programmes was 12.52 and 53.81, respectively. It is also important to note that the old respondents mean number of month is significantly higher than that of new respondents at 5 per cent level of significance (Shapiro-Wilk test, p-value = 0.000; Mann-Whitney test, p-value = 0.000). The mean amount of credit received by new and old respondents was RM2208.14 and RM4722.75, respectively. In fact, the total amount of credit received by old respondents was found to be significantly higher than that of new respondents (Shapiro-Wilk test, p-value = 0.000; Mann-Whitney test, p-value = 0.000).

Participation in AIM’s microcredit programme

Source: Authors’ research.

3 Indicators of economic vulnerability

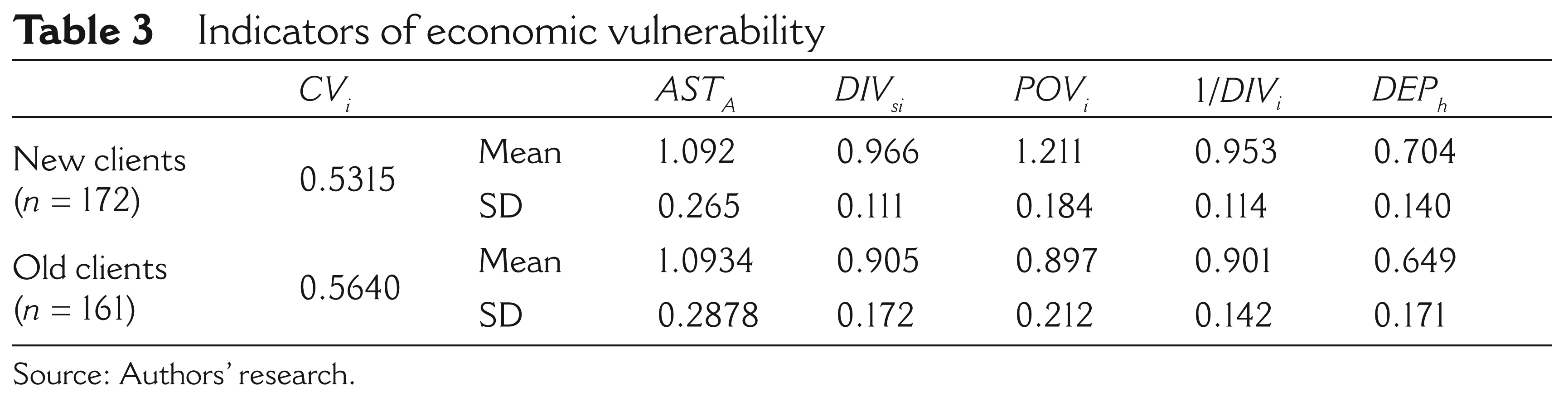

The coefficient of variation in the distribution of household income among old respondents was relatively higher (Table 3), indicating a relatively higher level of variation in the distribution of income among old respondents than that of new respondents. About 96.6 per cent of the total household income of new respondents comes from only one source. Among old respondents about 90 per cent of their total income generated from main economic activities. The mean POVi among the new respondents is relatively higher than that of old respondents, indicates that new respondents are in a higher level of ‘economically vulnerable to income poverty’ than that of old respondents. The mean number of sources of income among new and old respondents is 1.18 and 1.34, respectively. The mean effect of ‘diversification in the sources of income’ on economic vulnerability among new and old respondents are 0.953 and 0.901 respectively, indicates that old respondents are less economically vulnerable because of higher level of diversification in the sources of household income. The proportions of dependent members among new and old respondents’ households were 70.39 per cent and 64.94 per cent (see Table 3).

Indicators of economic vulnerability

Source: Authors’ research.

4 Participation and economic vulnerability

The impact of AIM’s microcredit programme on economic vulnerability was estimated by comparing the mean level of economic vulnerability between new and old respondents. It was hypothesized that participation of AIM’s microcredit programme leads to a decline in the level of economic vulnerability among respondent’s households over time. Since the mean values of participation indicators denoted that old respondents participated longer and received more credit, it was, therefore, expected that the mean level of economic vulnerability among old respondents will be significantly lower than that of new respondents. As presented in Table 4, the mean and standard deviation of current level of economic vulnerability among new respondents were 0.4680 and 0.1940, while the mean current level of economic vulnerability was 0.3279 with a standard deviation of 0.2320 among the old respondents. The p-value for Shapiro-Wilk test of normality for new and old respondents was 0.320 and 0.000, accordingly. Because of the violation of normality assumption, a non-parametric test was performed. The mean rank for economic vulnerability among new and old respondents appeared to be 199.37 and 132.42 respectively. The p-value for Munn-Whitney test was 0.000 which was less than the chosen 5 per cent level of significance, indicating that the mean economic vulnerability among old respondents were significantly lower than that of new respondents (see Table 4).

Participation and economic vulnerability

Source: Authors’ research.

VI Conclusion

The role of AIM’s microcredit programme on poor household’s socio-economic development was well documented in the literature of microcredit. However, there is lack of studies attempted to measure the impact of microcredit on economic vulnerability. Findings of this study, therefore, is increasing our understanding on the impact of AIM’s microcredit programme as it was found that microcredit decreases the level of economic vulnerability among hardcore poor clients’ households in Peninsular Malaysia. A concretely new and improved economic vulnerability index was designed and tested to measure economic vulnerability against microcredit, which contributes to the literature of multidimensional poverty measurement methods. As Malaysia aims to be a developed nation and to eradicate poverty, findings of this study will guide the policymakers to undertake appropriate steps and formulate policies in achieving the goal of vision 2020.

The government of Malaysia should, therefore, cater a favourable environment for the development and growth of various specialized small scale financial service providers. AIM and other non-governmental development organizations must focus on adopting a well designed need-based products and services which will enable the poor households to take maximum advantage from the income generating opportunities that they have. Since findings of this study revealed that participation in AIM’s microcredit programme decreases the level of economic vulnerability, therefore, we suggest AIM to emphasize on designing flexible and diversified financial products and delivery methods together with skill development training in order to improve the socio-economic condition of the poor households in Malaysia.