Abstract

Much research has identified the difficulties of promoting women’s empowerment using microcredit, but there has been little research on the potential for empowerment from promoting women’s savings. We address this gap through a qualitative study of three women’s savings programmes in the Highlands of Peru. The results reveal changes in several domains of women’s lives (economic, personal and relational), emphasizing that these programmes enable them to think about the future, expand their social support networks, and become entrepreneurs. We conclude that savings interventions have considerable advantage over microcredit programmes for facilitating female empowerment and that the merits of these interventions go far beyond financial inclusion with significant impacts on women’s psychosocial well-being and broader empowerment.

Introduction

There is currently little consensus as to the benefits of financial inclusion for moving out of poverty. Some authors assert that people who have greater access to the formal financial system have higher well-being levels (Rutherford, 2002). However, many families in poverty are often financially excluded (Krumer-Nevo et al., 2016). This is due to a lack of knowledge, mistrust, negative personal experiences, inappropriate financial products with high associated costs, social constraints, and uninterested financial institutions (Karlan et al., 2014; Trivelli and Yancari, 2008).

Financial inclusion can be achieved in several ways. Generally, the efforts of public and private institutions to promote financial inclusion of the poor have been mainly based on credit, modelled on the Grameen Bank or Bank for the Poor founded by Muhammad Yunus in 1998. Although some benefits associated with such initiatives have been identified (Banerjee et al., 2014), critical voices have warned of the problems and risks associated with credit: irresponsible consumption, indebtedness, and burdening families with loans that are unaffordable (Thomas and Sinha, 2009). Thus, people who are already at a disadvantage—in terms of their financial knowledge and resource management—may end up losing control over their limited domestic finances (Goetz and Sen Gupta, 1996).

In this context, the challenge of public policies is to support people move out of poverty via financial inclusion. Crucially, financial inclusion for poor people means being able to access and use financial services that are appropriate to their needs, which are responsibly delivered and which contribute meaningfully to improving their lives. It is in this context that savings offer an alternative path to credit. Saving allows people to enter the financial system, which entails greater participation, development of financial assets, a boost of their competences, and a general improvement in their well-being (Trivelli et al., 2011), but without taking on the liabilities and risks associated with a loan. Accordingly, this study focuses on the connections between saving and becoming an entrepreneur for women in vulnerable situations. Here, entrepreneurship is defined as ‘the process of using private initiative to transform a business concept into a new venture or to grow and diversify an existing venture or enterprise with high growth potential’ (Rikwentishe et al., 2015: 113).

As Minitti and Mardone (2007) suggest, women worldwide are much less likely to be involved in entrepreneurship than men (Gupta et al., 2009). However, the important role of women in entrepreneurship (considering entrepreneurial intentions, nascent and new business activity, and established business ownership) and how they ‘invest in their communities, educate their children, and pay back the benefits they receive by helping others’ (Kelley et al., 2015: 68) have been recognized worldwide. In this sense, some have argued that women entrepreneurs’ contribution to welfare is usually higher than that resulting from men’s entrepreneurial activity (Minniti, 2010). In this context, female entrepreneurs have been cited as the rising stars of the economies of developing countries, providing both well-being and prosperity (Vossenberg, 2013).

It has been observed that, in general, rich people save more money than the poor in amount and in terms of savings as a proportion of income (Balami, 2006). Kanjanapan (2004) has argued that the propensity to save increases with the perception of financial well-being. More recently, Rikwentishe et al. (2015) showed that having a low income topped the list of reasons for not saving in people in general.

However, lack of income is not the only reason poor people save less. As Bernal (2007) notes, poor people’s lack of access to social security networks (e.g., health, education, unemployment) and more limited access to formal savings institutions makes it difficult for them to increase their savings or save at all. In addition, for many low income populations, it is not easy to protect their savings, both owing to physical limitations (because they do not have safe places in their homes) and due to commitments to relatives or neighbours who also live in difficult economic situations or have urgent needs (Rutherford, 2002).

Gender differences in saving must also be considered. As shown by Nava et al. (2013), gender inequality is also expressed in saving capacity, since the average household savings show important and significant differences depending on the sex of the head of household, with women saving notably less than men. This factor must be considered alongside the incidence of objective factors, such as higher levels of unemployment and informal employment among women and wide gender wage gaps in Latin America (Lexartza et al., 2019).

Women’s capacity to save is diminished by factors associated with cultural norms and gender roles. For example, it has been found that raising children is an obstacle to saving for women, since many feel the need to stop working in order to care for their children (Jaramillo and Daher, 2015). The hours dedicated to domestic work also decrease the savings rate in households headed by women (Nava et al., 2013). At the same time, the greater responsibility of women for the care of children results in an increase in the resources allocated to children’s consumption, which makes it difficult for them to save (Seguino and Sagrario, 2003). Women’s capacity to save is also diminished by the expectation that women give all their income to their husbands, often having to save in secret and through informal mechanisms (Guerín, 2010).

Low-income rural women are particularly vulnerable, as they tend to have low levels of access to productive assets (which are needed for income generation) and financial services (due to poor financial infrastructure in more remote areas), issues compounded by difficulties associated with childbearing at very early ages (Paredes, 2013). Likewise, people from rural areas have limited saving capacity due to the scarcity of job opportunities (which in any case are seasonal) and because of gendered barriers to labour market entry (Jaramillo and Daher, 2015).

Notwithstanding the extent of these difficulties, low-income groups report the benefits of saving both through various informal strategies and in financial institutions (Rutherford, 2002). Agrawal et al. (2009) have demonstrated that people save more as their income increases, but this study does not include those who are outside the financial system and save informally, which is the case of many poor rural women. The use of informal savings mechanisms evidences how low-income women want to save and work hard to do so (Vonderlack and Schreiner, 2002). Low-income women who lack access to formal and secure savings, despite generating scarce and irregular income, spend an estimated 10% to 15% on savings (Women’s World Banking, 2015).

In this context, it has been shown that even rural women can save and that this effect is durable. For instance, a study by Villada et al. (2018) revealed that, two years after a social intervention, almost half of the participants continued to save (with lower or higher transaction costs, related to distance from financial services and the amount of money spent to get there, being the main factor explaining the tendency to continue or give up the habit of saving).

Based on this kind of positive evidence, social programmes oriented towards savings have spread globally. These programmes comprise multiple strategies, such as: (a) the delivery of subsidies or conditional cash transfers; (b) the opening and use of savings accounts; (c) financial training and awareness including knowledge about the functioning of the formal financial system, products and services, advantages in terms of security and trust; (d) the development of capacities aimed at the appropriate use of financial services, informed decision-making, protection against risks and identification of long-term projects, such us entrepreneurship; (e) learning guidelines to improve the management of income flows within the household including income management and planning of expenditures to allow for surpluses; (f) the provision of incentives to complement savings efforts such us raffles, prizes, or additional interest; (g) accompaniment or monitoring by professionals, local leaders and/or peer groups; (h) promoting good practices in financial education among key actors in the financial system; and (i) ensuring financial consumer protection (Campos, 2010; Caballero, 2017; Chiapa, 2012; De los Ríos and Trivelli, 2011; Kast et al., 2012; Paredes, 2013; Roa, 2013; Trivelli et al., 2011; Villada et al., 2018).

Regarding the results of these programmes, a study conducted in Peru with women belonging to the Social Protection System which measured variables such as deposits, withdrawals, amounts saved, and expenses covered by savings reported a monthly average of 30USD saved and signs of empowerment (Trivelli and Yancari, 2008), which participants defined as deriving satisfaction from being able to contribute to the home and make decisions regarding monetary resources. In Mexico, a similar study examined the financial effects of saving, which included higher incomes and entrepreneurship, as well as social effects such as greater access to services, changes in gender relations within the couple, improvements in children’s education, and enhanced ability to manage resources and make investment decisions (Zapata et al., 2003). Unfortunately, this study only details said effects without examining how the factors examined interact with one another. A broader perspective offered by Villada et al. (2018) highlight how empowerment associated with saving is often measured quite narrowly—in terms of financial decision making—in studies based on surveys and other standardized instruments.

However, when women gain control over more income—for instance, through credits, saving, or entrepreneurship—a much deeper and complex phenomenon is reported: female empowerment. Women’s empowerment can be understood as the process of increasing women’s power, conceptualizing it not as domination over others, but as women’s ability to increase their self-confidence and influence the direction of change by gaining control of material and non-material resources (Hidalgo, 2002). In this regard, it is important to note the processual emphasis of the definition. According to Eyben et al. (2008), empowerment involves three inter-connected and iterative dimensions—social, economic, and political—and must be understood as a path rather than a building or a final result. Following this thinking, our study goes beyond an outcome focus (asking if savings programmes lead to female empowerment) to explore how savings programmes facilitate or enable changes in different dimensions and what this means for constructing a path towards broader empowerment.

Considering the relevance of the processual nature of empowerment, it is important for the field of microfinance to use qualitative methods in the study of savings as a strategy for the overcoming of poverty, revealing the subjective and relational processes through which material changes in savings lead to empowerment and determining their contribution to programme effectiveness (Wright, 2003). In this regard, the qualitative study conducted by Chen and Mahmud (1995) is recognized as an initial contribution. In the context of aid programmes in rural Bangladesh, they detected four pathways to change in women’s lives: material (changes in access to and control over material resources), cognitive (changes in levels of knowledge, skills, and awareness of the wider environment), perceptual (changes in women’s self-perception plus changes in other people’s perceptions of women), and relational (changes in contractual agreements and bargaining power in various types of relationships). Our article seeks to update knowledge about how women’s savings foster lead to female empowerment and extend it for Latin American countries through a study in Peru.

In addition, one of the ways in which we seek to extend this knowledge, is by considering the relationship between women’s savings and their financial strategies through a focus on the link between women’s savings and women’s entrepreneurship and how this may contribute to women’s empowerment. One of the main problems encountered by individuals who wish to start a business venture is the lack of seed money: if it does not come from an external source—credit or investment—it must be acquired by the prospective entrepreneurs themselves (Vázquez et al., 2017). Most entrepreneurship programmes use credit, which puts a strain on families by forcing them to repay a loan that they often cannot afford during the set-up period of their small businesses and which tends to result in losses rather than profits (Reyes, 2011). In this context, it could be argued that savings might be a better and more sustainable way of starting small businesses. Studies on social interventions oriented to savings conducted in Bolivia, Peru, and Colombia show how families that manage to save whilst maintaining greater interaction with the credit system and institutions supporting economic initiatives tend to use these resources to start small businesses (Rincón et al., 2012; Zárate et al., 2012).

Efforts to use credit to promote women’s empowerment and ‘transformative’ change have often floundered on women’s lack of ability to control the loans that they are given, particularly where they are married and where those loans are sizeable (Hidalgo, 2002; Holloway et al., 2017). However, women’s lack of ability to control loans, contrasts with their capability of managing risk and limiting consumption in the face of a crisis or a loss of income (Holloway et al., 2017). The uneven financial capabilities demonstrated by poor women suggest that savings may offer them more room for empowerment than taking on loans. Nevertheless, it is not only women’s saving abilities that are relevant to how far they can use savings to advance their own empowerment, but also aspects related to wider gender relations. For instance, Johnson (2005) identifies aspects of gender relations, both within the household and beyond, which constrain the impact of microcredit. In this regard, there is a need to explore how far savings programmes facilitate or enable changes in gender relations that may contribute to broader female empowerment.

Thus, although connections between microfinance and empowerment have been reported in the studies mentioned, most attention has focused on credit programmes and few authors have conducted a thorough analysis of the association between saving and empowerment. Also, many studies operationalize the concept of empowerment narrowly as just financial competency, which comprises making financial decisions, contributing financially at home, and making individual investment choices (Ashraf et al., 2010). This article contributes to recognizing the psychosocial dimensions of social interventions around women’s savings through an in-depth study of a broader interpretation of empowerment. Considering its psychosocial nature, empowerment is related to the acquisition or enhancement of one’s capacity to control one’s life or the ability to handle matters or issues of interest to oneself (Rappaport, 1984). In this broader sense, empowerment is understood as the process of gaining personal competence (Zimmerman, 1995), achieving greater autonomy which involves independence and the capacity to make decisions in general (Tyler, 2004), having control over the circumstances of one’s life (Montero, 2003), connecting with and participating in the social opportunities network (Maton and Salem, 1995), and developing female leadership in communities so that other women are empowered to participate in social networks (Martínez, 2017).

In summary, savings incentive programmes not only influence the accumulation of savings but also have indirect impacts related to empowerment and entrepreneurship, which is consistent with their goal of contributing to the overcoming of poverty in all its complexity and multidimensionality (Hishigsuren, 2007). Our study explores the broader empowerment effects of social programmes that incentivize women’s savings in order to generate financial inclusion and overcome poverty, and we do this from the perspective of women themselves.

Context

Three programmes were considered in this study because their main objective was to encourage savings based on financial education. These programmes were implemented in rural areas of Peru, specifically in the Highlands, a mountainous and high plateau region characterised by Andean culture, which is mostly Quechua and Aymara (the two predominant indigenous populations of Peru).

In Peru, despite the urbanization processes of recent decades, 27.1% of the population still lives in rural areas. The income poverty rate is 16.2%, reaching 25-29% in certain regions (such as the Highlands regions considered in this study). Another relevant characteristic of Peru is its multi-ethnic, multiracial, and pluricultural make-up, with the State recognizing 72 ethno-linguistic groups of which the Quechua and Aymara populations are the most prominent (Instituto Nacional de Estadística e Informática [INEI], 2020).

As Dorival (2018) explains, in Peru, indigenous people are marginalized because their cultures are ‘different’ from the prevailing ones; furthermore, in the face of the predominance of Western culture, they are perceived as a hindrance to modernization. Thus, indigenous people, especially those residing in rural areas, still lack educational and employment opportunities, generate less income, and have a lower rate of access to public services than non-indigenous people (Dorival, 2018). Regarding the labour sphere, indigenous women living in rural areas constitute a particularly vulnerable group. They are mainly engaged in agriculture, livestock and forestry activities, and the retail trade, with this sphere being one where the intersectionality of inequalities is clearly visible (as their ethnic background, gender, and rurality incur multiple disadvantages; Del Águila, 2015). In addition, indigenous women, specifically Quechua and Aymara, experience high levels of domestic and sexual violence and recognize that chauvinism remains one of the main factors that prevent them from overcoming these situations (Zúñiga, 2014).

Three areas were selected due to their high levels of poverty and a rural development policy associated with public-private initiatives (Yancari, 2009) aimed at supporting those excluded from the formal financial system. These initiatives were: (a) Innovations for Scaling Up Financial Education; (b) the Puno-Cusco Corridor Development Project, and (c) Savings Promotion Pilot at JUNTOS Programme.

The first, Innovations for Scaling Up Financial Education, was implemented in the Northern Highlands. It consisted of financial education in terms of: (a) knowledge— managing relevant information about the financial system and its services; (b) skills—using the savings account and planning savings effectively; (c) attitudes—appreciation of savings in banks, trust in the bank, and willingness to save in the bank; and (d) savings behaviours—saving a certain amount of money and using the savings account. These elements were implemented through the utilization of new media: flip charts, radio soap operas, and Short Message Service (SMS) messages (Ramos, 2018).

The second, the Puno-Cusco Corridor Development Project, was implemented in the Southern Highlands and consisted of financial education programmes for female savers in general (organized in saving groups of around 20 people), and for women leaders of savings groups (two members of each savings group who facilitate the association between the participants’ families and the financial system). The first strategy mainly consists in providing information to the women about the link with the financial system, making guided visits to financial institutions, carrying out training modules, and generating opportunities for the exchange of experiences. The second intervention strategy aims to strengthen the skills and capacities of the leaders while helping them to establish a fluent line of communication with the participating financial institutions through three training modules about the following topics: consolidating savings, accessing new services, and building a plan for training other women in their group (Procasur and Fondo Internacional de Desarrollo Agrícola, 2007).

The third, the Savings Promotion Pilot, also was undertaken in the Southern Highlands and consisted of financial education programmes mainly implemented by an intervention agent: the so-called ‘promoter’. This initiative comprised: training in financial awareness including functioning of the formal financial system and its characteristics, products and services, and advantages in terms of security and trust; financial accompaniment through local leaders and visits from promoters; and incentive mechanisms including raffles and prizes. It is important to note that this third programme is related to the JUNTOS Programme, which is part of the Social Protection System of Peru. JUNTOS benefits the most at-risk and vulnerable people, who live in a situation of extreme poverty and exclusion, and was the first programme in Peru to grant conditional cash transfers to its participants. In this context, the Savings Promotion Pilot made it possible to offer poor rural families medium-term strategies allowing them to graduate from the JUNTOS Programme and ultimately move out of poverty (Trivelli et al., 2011).

Although certain differences in the implementation of these programmes affected their outcomes, as will be seen later, they did not appear to have a major impact on participants’ ability to save. Finally, it should also be noted that, despite being implemented in different geographical locations, there were no cultural variations among the programmes studied.

Method

The study was qualitative in nature. The choice of this approach was based on the fact that it favours the analysis of the particularities of the participants, their saving experiences, and their trajectories in the programmes upon the basis of their contextual emergence. The type of design was descriptive and relational, which led to the inductive generation of comprehensive models to account for the phenomena under study, anchored in participants’ reality.

Participants

The study included 36 women from the Northern Highlands and 47 from the Southern Highlands. Their age ranged from 20 to 68 years, with the average being 40 years. As the programmes were sponsored by the Social Development and Inclusion Ministry, all participants were low-income, as certified by the Household Targeting System (Gobierno del Perú, Contraloría General de la República 2008). All participants reported belonging to the Quechua ethnic group. Most of the women had completed their primary education. On average, their families comprised two parents and three children. In terms of occupation, all the women were engaged in housework and childcare and most did family-based subsistence work or had small business ventures. In Northern Highlands households, women’s work mostly involves field cultivation and weaving. In the Southern Highlands, women tend to farm and raise small animals (e.g., chickens, guinea pigs, rabbits). Four women reported having grocery stores in their homes.

Data production

Data production involved six different activities. Three focus groups and three in-depth interviews were conducted (Kvale and Brinkmann, 2009), as well as one group evaluative discussion and one community assembly (Montero, 2003). Simultaneously, five individual evaluative discussions were conducted with key informants, alongside five participant observations which included home visits and a training programme for women leaders who would later promote saving among their peers (Taylor and Bogdan, 1986). Evaluative discussions, both group and individual, are qualitative data production strategies based on the conversational approach (Canales, 2002) and Participatory Action Research (Durston and Miranda, 2002), as well as systematic discussions for evaluation (Montero, 2006). Combining different data production strategies made it possible to attain greater theoretical saturation and validate the interpretations generated (Denzin, 1970). The researchers were not Quechua, but they had access to their language and culture through Quechua women who participated in the programmes.

Semi-structured thematic scripts (Kvale and Brinkmann, 2009) were created for the data production activities conducted, which included questions about participation experiences regarding the programme, its possible effects, and relevant milestones and recommendations for improvement, as well as questions about the participants’ ideas about savings and poverty (which were recorded digitally). In all these parts of the project, the ethical standards set by the American Psychological Association and the National Commission for Scientific and Technological Research of Chile (Lira, 2008) were followed. The ethics committee of Pontificia Universidad Católica de Chile’s Psychology Department granted ethical approval for this project.

Data analysis

Following Grounded Theory, descriptive and relational analyses were conducted. Data were explored via detection of relevant events and were complemented by incorporating a holistic approach to the experiences and meanings of the participants, following the methodological considerations derived from the Analytical Device Context–Encounter–Themes (Daher et al., 2017).

Results

This section begins with a brief description of the women savers’ experiences with financial systems and saving before admission to these programmes, including the factors facilitating their involvement, before offering an analysis of obstacles that they experienced and the changes that they reported as a result of their participation in these programmes. We structure the impacts they attributed to the savings programmes around three themes: the ways in which savings made it possible to plan for their futures; how savings were a mechanism that helped expand their social support networks; and how savings fostered their entrepreneurship.

Experiences prior to participation in the programmes

Most women had little or no experience with financial institutions such as banks. When asked about their reasons for not using banks before joining the savings programmes, they cited distrust and fear of financial institutions based on bad experiences and/or fears that the bank would deceive them or keep their money. These fears were rooted in real experiences where many people lost savings or were unable to get their money back from the bank during the financial crises that had previously occurred in Peru or in neighbouring countries such as Argentina or Venezuela. Also, the women recounted being marginalized due to their physical appearance being associated with indigenous features, because they were beneficiaries of the Peruvian Social Protection System, or because they were living in poverty. There was also some insecurity based on a lack of knowledge about how financial institutions operate and how to manage them appropriately: ‘We were afraid to go to the bank, because we were hesitant, because we didn’t know how to go, or because we didn’t know how to use the cash machine, or because we could forget the password’ (Focus Group 2, Northern Highlands).

Most women said they had never saved before the programmes. Nevertheless, a closer look at how these women had previously managed their income, especially during months when their expenses were higher (such as the beginning of the school year and the rainy or planting season), revealed that they used informal saving strategies to cope. Although the participants mentioned that before the programme they recognized the benefits and the importance of having money for emergencies (such as ensuring personal safety and protection), they were not able to see the point of saving beyond dealing with contingencies. This changed when they accessed the programmes and linked saving to their own goals or projects.

The participants reported factors that facilitate or hinder saving that are important to take into account when implementing these types of programmes. Some factors were directly related to the person who saves (including degree of knowledge and trust in the financial system, determination to save, and willingness to participate in the programme). Others were linked to access to (or absence of) support from extended family as well as their own partners and children. Other factors included: occupation (having a job or a small business as a source of income); institutions (effective access to financial institutions and products); socioeconomic and cultural factors (including male chauvinism and the ‘confinement’ of rural women to the domestic sphere); and spatial context (including geographic isolation and climate). There were also factors directly related to the programmes, mainly the training provided and the staff member delivering the programme (‘promoter’). One respondent highlighted that one of the main difficulties for women to save in this context was cultural tolerance of patriarchy leading to violent behaviours against them both physical, psychological, or economic, leading to fear of their husbands:

Yes, there is violence, maybe not from beatings, but violence anyway. What happens is that here in Peru we are under a chauvinist culture. … So all the consultations and important decisions [like saving] are left to him [husband]. … Also, they [women] can decide to save, but they have to hide their money, because the man is very authoritarian and if he feels like drinking he will just grab it (Individual Evaluative Discussion 2, Southern Highlands).

Impacts of savings programmes

At the end of the intervention, the participants had become aware that saving was possible. Although the amounts and times of saving varied among them, most suggested that they would continue saving in banks even after their participation in the programmes ended. They appreciated saving not only due to the monetary accumulation that it enabled, but also because of the positive effects that it had on their lives in terms of enhancing their economic situation, their sense of self, and their relationships with other people and institutions.

With respect to improvements in their economic situation, the participants reported that the most important change was that they built their ability to save, switching from informal to formal savings. Before participating in the programmes, many of them did not save or did not realize that they were saving, as they did so informally and sporadically. Thanks to the programmes, the participants not only saved but also saw the benefits of formal savings, including the safeguards guaranteed by financial institutions.

Saving was made possible through the following strategies. First, by keeping the money physically safe in a bank account, compared to putting it under the mattress, hiding it in food jars, or in the house’s infrastructure (such as holes or between wall boards), which might cause the money to deteriorate due to dirt or humidity or because mice could gnaw at it. Second, by keeping the money safe from third parties, for example, not allowing spouses or sons to have easy access to the money. Third, by improving their administration of their income and expenses and by regulating themselves: ‘I didn’t know how to handle my money before. … Now I measure myself a little bit on the expenses to keep’ (Interview 2, Southern Highlands). Fourth, by restricting the consumption expenses of others, for example, limiting children’s requests of branded clothes or shoes, a problem expressed by some participants: ‘children make demands, they no longer want to dress as before, […] that’s why the money is running out. So, I can’t save if my son says “I want my branded clothes”’ (Focus Group 2, Northern Highlands). In this regard, the programmes encouraged them to identify more clearly that these expenses were secondary. Fifth, the programmes prompted savings to be associated with specific goals, which generates greater motivation and awareness of what has been saved and how much is left to reach the goal, helping participants plan for and project themselves into the future.

These strategies for achieving formal savings improve women’s economic status by increasing their economic capacity and by accruing interest from the bank, in contrast to the devaluation of money associated with informal savings. Also, the participants learned to manage their resources better, enjoying greater clarity about how much money they had saved, since all their funds were in one place and they could easily check the amount saved and monitor incomings and outgoings in their account balances.

Personal changes were mainly psychological, leading the participants to regard saving as a way to imagine new possibilities for the future. This enabled the participants to feel free, independent, sure of themselves, competent, and able to achieve what they set out to do, leading to a sense of accomplishment and greater happiness. They became validated as important people and recognised their own courage in accepting the challenge of imagining a better life. There were also physical changes to their appearance (clothing and hairstyle), as well to their knowledge of financial education. The participants reported feeling empowered, as they experienced greater self-reliance and felt capable of providing for their families.

Relational changes occurred within the family and in interactions with other people and institutions. Before the programme, the women’s partners had strongly opposed their participation, leading in some cases to domestic violence. After the women’s participation, however, their partners came to support them in their saving efforts. This was related to women becoming more empowered in their relationships with their husbands and overcoming their previously mentioned fear of opposing them:

Being able to understand and knowing how things work helped me, and even though my husband was against my decision, I understood the programme and managed to put all my energy into my goals. … I am no longer afraid, I am a person who has come out of the programme with no fears after attending the awareness training (Interview 1, Southern Highlands).

Sharing these experiences with other women in the group motivated them to talk with their husbands, explaining to them that they must look to the future, project themselves, and make plans, with savings being portrayed as a way to achieve these projects. For some women, domestic violence ceased to occur, because these conversations and negotiations allowed them to develop a new family dynamic. In this regard, one participant noted: ‘In the training I heard many things and then I explained to my husband that we should think about the future and about being good parents to our children. He doesn’t drink or hit me anymore’ (Interview 2, Southern Highlands).

The participants’ social environment also shifted as a result of the training, allowing them to meet and share their experiences. This caused them to become less shy, introverted, withdrawn, and reluctant to ‘come out’ and relate with other people and places outside the home, such as these programmes and other institutions. Some women were even inspired to take up important positions in the saving groups, as women leaders, or in their communities. This was possible because the programmes identified women leaders in each territory and empowered them in the training sessions. This was especially true for the Savings Promotion Pilot at JUNTOS Programme, where the promoters already knew the participants and leaders; however, if no obvious leaders were identified beforehand, they emerged over the course of the programme.

In their relationships with other financial institutions, particularly with the banks involved in these programmes, the participants overcame their initial fears, developing greater self-confidence and learning how to deposit and withdraw money, going to the customer service counter to ask questions, and losing the fear of being discriminated against by the bank staff. This greater connection with banks opened the door to inclusion in the financial system and increased the participants’ contact with other kinds of institutions (such as the Ministries of Health and Education and other local government agencies). Having become empowered to manage their interactions with banks, the participants learned to demand quality service and good treatment in all their dealings.

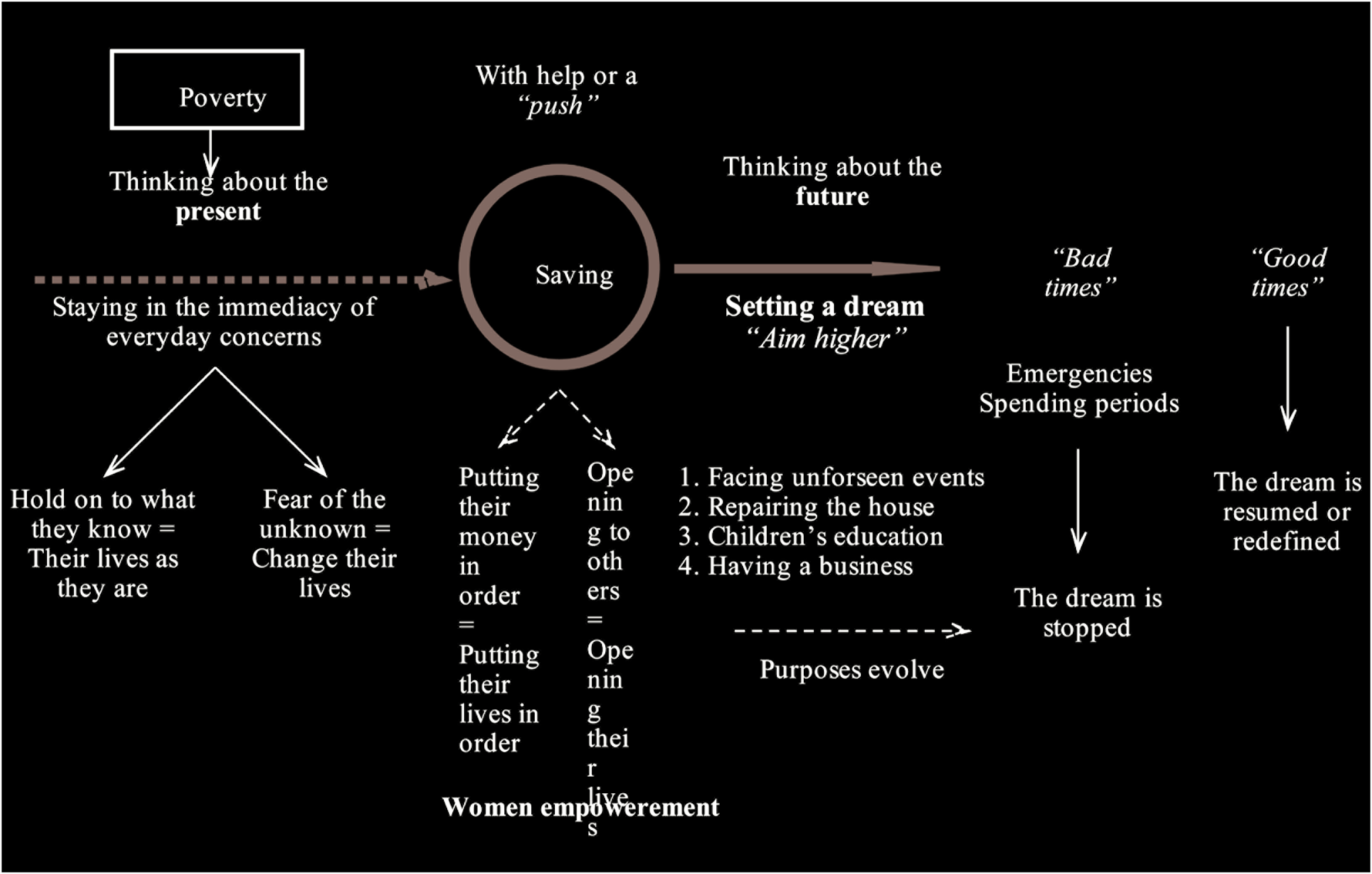

Savings make it possible to plan for the future

Participants viewed savings not only as a tool for managing revenue and achieving financial inclusion, but also as a powerful catalyst to radically transform how they lived their lives. This was possible because saving forces people to think about the future, their goals, and their desires, which included: a better education for their children, starting businesses, expanding their small homes, financing celebrations, having some support for their old age, and having peace of mind when dealing with an emergency. These thoughts about their lives and their projects pulled them out of a short-term mentality concerned with immediacy due to the structural conditions of poverty and enabled them to move beyond their daily concerns and dare to confront their future by considering other options and alternatives. This possibility of imagining and planning a better life was complemented by the acknowledgment that they deserved to live well, as one participant highlighted:

We have to understand that what we do is of our own free will, and understand that what we do is for our own good and for our future. And all this saving has not been appreciated by many, but once we encourage it, it has served us (Community Assembly, Southern Highlands).

Perceptual shifts had also been experienced by participants due to their participation in these programmes. It was very common to find a very negative initial view of banks, training, savings, and even money itself, which was gradually changing. As one woman said: ‘My mother told me that money is from the devil. Now I tell her it’s not, that it’s just a chance to get ahead’ (Community Assembly, Southern Highlands).

As was explained before, most participants had formerly displayed a fear associated with a lack of knowledge about saving, distrust of banks, and strong initial opposition from their husbands to their participation in the programmes:

At first, when the project monitor came here to talk of savings it was difficult because we didn’t know anything about the financial institutions and we were afraid, at the same time our husbands would not let us be savers, they thought that maybe we would lose the money. Then, little by little we have been trained to save. Until then we didn’t know what saving was or what a loan was, we didn’t know anything about that (Interview 1, Southern Highlands).

As a result of participating in the programmes or having indirectly witnessed the positive experiences of neighbouring villages, the women gradually became motivated to give saving a try. The programmes showed them that they could organize their funds by keeping a record of their monthly expenses, which allowed them to obtain a picture of their outgoings for the first time. In addition, they were able to define what their fixed and variable expenses were, realizing that they sometimes overspent (e.g., in the supermarket), as the programmes allowed them to determine how much they had to spend per month on food and thus revealed surpluses that they could use for savings.

Also, they opened themselves up to a wider world by leaving their homes to interact with other women and other institutions. Seeing specific achievements in their lives, such as improving their kitchens or starting small businesses, made them feel excited, dispelled their initial fears, and strengthened their will to save money. In this sense, savings did not merely represent an accumulation of money—they symbolized the ability to ‘aim higher’:

Interviewer: Before the project, how was your financial situation? Participant: Bad. It was so because we had no business, I didn’t know how to earn money. After the project, this has completely changed because I knew how to earn [money], I had an account, I could get a loan, buy machinery, save some money and so, little by little, I have moved forward. … I felt secure because I knew that if anything happened, I had the money to buy what I needed, so, I was relieved, and it made me happy to see the things I could achieve (Interview 1, Southern Highlands).

However, this was not a straightforward journey. Although the starting point was similarly marked by fear and apprehension for most women, the path was complicated by unforeseen events and by times of the year that required extra effort. At those times, women had to use their savings and give up, momentarily, what they had planned to do with those resources. But after overcoming these obstacles, they were able to resume these projects or think of something new. In this sense, as they progressed through the programme, their saving goals also changed. For example, the participants initially viewed saving simply as a way to face unforeseen events, but once they were able to capitalize, they had the possibility of setting a goal for that money, such as their children’s education. This purpose was essential, as it constitutes one of the main ways of overcoming the inter-generational transfers of poverty and inequality which they associated with ‘moving forward’. As one participant explained: ‘I have been able [thanks to the savings] to fulfil my dream of fixing up my house and thinking about the future of my children, their education and health’ (Community Assembly, Southern Highlands).

In other cases, the participants reported that there were other women who—because of these obstacles or other life circumstances had—been forced to suspend their participation in the programmes. However, most of the participating women dreamed of starting something of their own, like a small venture that they could feed with their savings, and typically eventually surpassed the amount of money that they had initially planned to raise.

This situation, which is illustrated in Figure 1, shows the association between savings and female empowerment. The participating women developed a stronger sense of self inasmuch as they dared to take these future desires and goals seriously, which speaks of personal competence, autonomy, control over their own life, and ability to connect with others:

Participant 1: To be willing and eager to work, that more than anything, to have the desire to succeed and not be marginalized anymore. Participant 2: Yes, it is to feel like doing something and wanting to improve ourselves, we must learn to value ourselves and make an effort to be able to move forward, so that our children can be better than us and so that we can fight poverty in Peru (Community Assembly, Southern Highlands).

The above makes it possible to counter the narrative—which two men had initially voiced and which was also observed in the opinions of bank managers and promoters—that it is impossible for people living in poverty to save money and that it is necessary to have additional income to do so. In fact, the participating women saved, and many did so even without receiving a subsidy. Although none of the three programmes provided subsidies for savings, in one of them the women did receive conditional cash transfers—since the programme was part of a broader Social Protection System. However, this additional income did not prove to be as influential on savings as financial education and the driving force that resulted from connecting saving with the desire for a better future. This was noted by some women during one of the observations: ‘Participant 1: Sure, when you set goals, you can do it! Sometimes you just need to restrict your spending a little and you can save. When you have the will, you can. Participant 2: If we have the will, we can do it [save]’ (Community Assembly, Southern Highlands).

In this context, psychological shifts such as increased self-esteem, female empowerment, or envisaging a better future were critical for the participants. These critical aspects refer to the importance of positive attitude and willpower for moving out of poverty. However, these aspects must also be accompanied by broader structural changes and anti-poverty measures.

Savings as a mechanism to expand social support networks

Another indirect impact of savings for women who had felt ‘locked-up’ in their homes prior to participation in these programmes was that new worlds and new possibilities for social interaction opened up for them:

Now we get together [referring to the training], but before women just complained in their homes with their children, their gardens, and their husbands. Not now, now we share our experiences. … It is important to leave the house, because at home you feel bored and locked-up, but now we have fun when we get together (Interview 2, Southern Highlands).

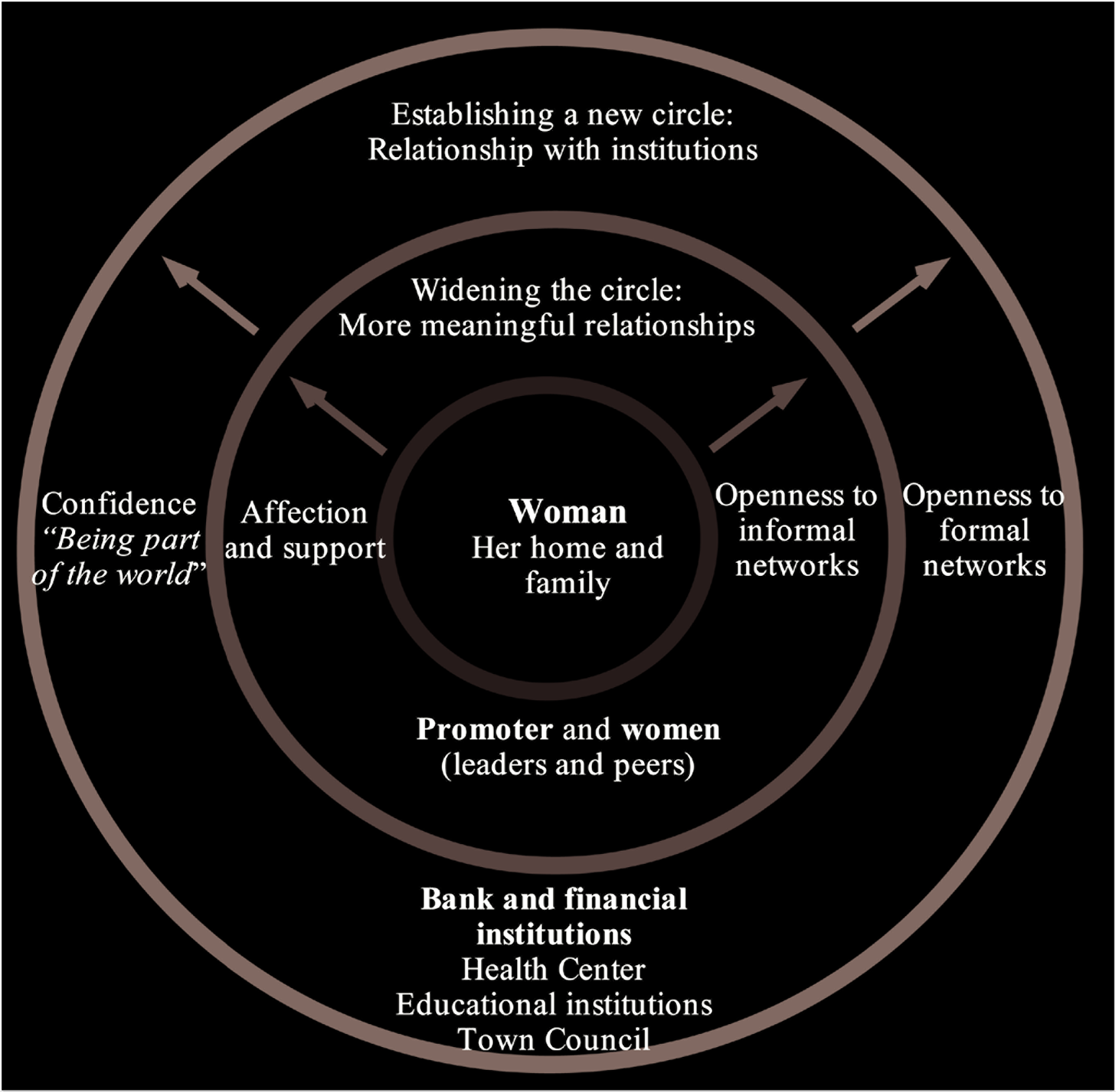

Opening up to new interactions was very important for women who rarely leave their villages, allowing them greater access to a range of benefits because of the new contacts that they had been able to establish. In that sense, the programmes enabled the participating women to ‘come out’ of their homes, meet other women in their same situation, and lean on a promoter or women leaders who helped and strengthened them. This greater connection extended the participants’ social networks from their homes and farms, generating networks of opportunities to create friendships, gain access to jobs, and benefit from basic services such as health and education, in addition to achieving greater financial inclusion.

This openness to new worlds can be represented in a network map where some points that connect different areas and have different functions become visible (see Figure 2). In the case of these women, it could not be said that these points or nodes were created, as they were already present in their contexts, but it does appear that they emerged in their daily lives as accessible people and places that they could count on.

In this context, affection and emotional support became fundamental parts of this network, particularly in association with promoters, women leaders, and partners with whom they received training. The women appreciated having a special time to express themselves and a space where they could enhance their skills whilst enjoying themselves.

The outermost circle in the figure is made up by the institutions with which participants begin to interact: first the bank and financial institutions, followed by health centres, educational institutions, and the city council or the local government. Regarding the participants’ interaction with banks, one participant suggested:

[Before the intervention] we were afraid to go to the bank and we did not know the it, we had doubts and mistrust, that the bank would leave with our money. With the training we lost that mistrust. … We now know how to get in and out of the financial system, because before they marginalized us, but now they respect us, they no longer treat us badly (Group Evaluative Discussion, Southern Highlands).

In addition, women recognized that being registered in the financial system allowed them not only to save, but also to take advantage of other opportunities it offered, such as applying for loans or credits in an informed manner, for example, with a knowledge of the costs and interest payable. This allowed them to ‘defend themselves’ by being active and attentive clients. One woman mentioned that being part of the financial system allowed her to have greater visibility as an entrepreneur, thus expanding her networks of opportunities: ‘We have more services available to us, because we are already registered in the system, so we can take out loans. If I didn’t exist in the financial system, how would they know about me, that I am a person who likes to do business? Things are much easier when you’re in the system’ (Interview 1, Southern Highlands).

Thus, in this case, informal networks formed by people who are important to these women—promoters, women leaders, and training partners—were crucial in the process of opening up to formal networks. Also, these informal contexts, especially that of training, were relevant to the extent that they allowed them to acquire new knowledge and learn to interact with formal institutions. Having knowledge proved crucial for women to feel confident and beat the initial fear to change their lifestyles.

These changes had unexpected transformative effects: ‘Before we were shy, now we are participative’ (Group Evaluative Discussion, Southern Highlands). Also, the participants learned to value themselves as part of a much larger world and even emerged as women leaders thanks to the training offered in the programmes. This enabled some women to raise their voices to fight for others in order to obtain the same well-being that they had experienced and allowed them to move forward: ‘I’m proud to be a leader and to be able to express many things and to manage to move forward. I changed my personality, I’m not shy, and with my knowledge I’m no longer uncultured’ (Interview 2, Southern Highlands).

It is noteworthy that the participants often spoke in the plural, referring explicitly to their community. They referred to themselves as a community of women, beyond the fact that they were formally participating in an organization. Hence, Figure 2 becomes more meaningful, not only because the programmes connect the participants to those networks, but also because they are geared towards community integration.

Savings and entrepreneurship

Finally, the connection that women established between savings and entrepreneurship, understood as small-scale productive activities, was noteworthy. This relationship was relevant because they regarded saving as a financial tool that allowed them to input resources into their new business without the risks associated with credit: ‘I would like to save so I can have a business later on and get out of poverty. When I get my business I can leave the JUNTOS Programme so other mothers who need this support can access it’ (Community Assembly, Southern Highlands).

This is how saving becomes an attractive strategy to promote micro-enterprises among women without the potentially negative effects of credit. Indeed, many of the participants spontaneously decided to start small businesses to make their money ‘grow’. As pointed out by the participants, saving was first encouraged by these programmes, and when they realized how much money they had accumulated, the idea of starting a business emerged, often linked to subsistence activities (e.g., raising small animals or poultry, growing vegetables, preparing food, or making handicrafts). These ventures developed through the accumulation of savings, enabling the participants to invest in them to achieve higher profits, further maximizing their savings.

Businesses earnings grow, for example, through the acquisition of more animals and increasing sales; however, losses can also occur, for example, when animals get sick and die in the rainy season. Savings accumulated in the ‘good times’ were crucial for facing the ‘bad times’ so the business could become sustainable. Credit was only used at a more advanced stage, when the participants were in a position to pay it back. Savings became a gateway to micro-enterprise development by helping the participants to access funding in a responsible manner, as illustrated in the accounts below:

If there is no interest, your money ‘goes to sleep’; like many people who do not have a steady job and are independent, we prefer to generate profits with our savings by investing them in our businesses (Participant Observation 3, Southern Highlands). In the programme I saved money that I have used for my business; I spend it on the business, but afterwards I save it again to obtain more growth (Community Assembly, Southern Highlands).

As seen in Figure 3, saving acted as a gateway to the ‘business world’ by safely injecting seed money as start-up capital to develop the participants’ small ventures. This was particularly beneficial—compared with credit—in the initial phase of the business, when sales were lower and set-up costs were high, making it difficult to repay a loan. In the growth phase of the business, although it was more likely for women to apply for credit as sales revenues were generally higher and therefore allowed them to repay, these revenues also allowed them to increase their saving capacity and reinvest in the business, thus supporting their growth on both fronts. In this way, saving provided access to credit. This occurred because savings are a protective device leading to gradual and informed entry into the financial system, preventing the risks associated with credit obtained without preparation or training.

In this manner, linking savings with micro-enterprises can generate a stable income and sustain the business over time, which does not always happen when credit and seed capital are provided by an external institution. This, in turn, helps to improve the lives of low-income groups by offering a sustainable path to planning a venture of their own.

Keeping their savings in the bank was insufficient for the participants who instead chose to invest them in small businesses. Once the business was formed, the participants explained it had an impact on their self-worth because it positioned them as people with increasing financial autonomy. As their plans progressed and their capacity for responsible consumption developed, the business became a mainstay of their families:

Change happens little by little. First, saving gets you out of trouble. Then you come up with ideas to start your small business, if you had five chickens now you have ten, which is a business and it’s not just for consumption. After you realize this, there are always obstacles ahead, because there are seasons when the animals can die, but the important thing is not to give up and, as we have our savings, we can use them to face these obstacles. Once we start our business and we do well, we value ourselves because we feel like independent women. If you do not know how to do business with your money, it is useless, you must make the most of the savings, you must invest them (Observation 3, Southern Highlands).

The women participating in this study offer important insights into saving and ideas that may enable us to extend its benefits to other fields, such as micro-enterprise development and responsible financing. In this regard, there are several advantages of using saving as a gateway to financial education and inclusion, and eventually to move out of poverty. In the economic sphere, saving allows people to manage their budgets more efficiently, accumulate assets for later consumption and investment, overcome negative impacts, and take advantage of market opportunities and the financial system, leading to enhanced financial competency. Hence, saving is a protective agent that leads to more mindful consumption and provides access to credit in a responsible manner.

In terms of personal development, saving and financial education tools have been proven to enhance the female empowerment and the knowledge needed to make informed decisions. Thus, saving appears to go beyond revenue management and financial inclusion by, at a psychological level, allowing low-income women to stop merely reacting to the precarious structural conditions that constrain their lives and offering them the possibility of envisaging and planning for a better future. In the relational domain, saving fosters shifts in family dynamics, strengthening relatedness with individuals and institutions so that participants can engage as citizens with entitlements and rights.

Thus, this study corroborates prior research that shows that saving is possible even among low-income women in rural areas who face multiple obstacles to save (Bernal 2007; Jaramillo and Daher 2015; Nava et al. 2013; Paredes 2013; Rikwentishe et al. 2015; Rutherford 2002; Seguino and Sagrario 2003). Moreover, this study shows the positive direct and indirect effects that saving has on women’s lives, which go beyond the mere accumulation of money and include expanding networks and planning for a better life. This represents both personal development and greater community integration (Montero, 2003), particularly among women. Whilst many studies looking at microfinance for women have operationalised empowerment as financial competence (for example, Ashraf et al., 2010), our study shows that this is a narrow approach and demonstrates the value added of distinguishing financial competence from broader female empowerment. Also, this study highlights that the subjective impacts of savings on women’s lives merit further attention. Quantitative studies that account for the monetary impact of saving (e.g., Trivelli and Yancari, 2008) are valuable and make it possible to ascertain the material or objective effects generated by savings programmes, with an emphasis on their final results. However, this study sheds light on the strategies behind savings behaviour, with an emphasis on processes, while also making it possible to recognize other subjective and relational effects involved in the experience of saving.

These findings call for public policies and programmes in the private sector to invest in these kinds of interventions, while also extending the field of micro-enterprise development in a way that connects it more explicitly with savings products. This would potentially reduce the costs associated with microfinance programmes. While low-income rural women constitute a significant percentage of the population, such opportunities might not only attract customers, but more broadly create a culture of financial responsibility and solidarity. This connects with the idea that including low-income groups such as women is a necessary step in any attempt to sustain growth, development, and welfare (Vossenberg, 2013), since countries that do not include them in their national policy frameworks run the risk of achieving growth without development (Hope, 2004), a common situation in Latin America and in countries pursuing neoliberal agendas such as Peru.

In this context, saving becomes not an end in itself, but a path to a better quality of life. The integration of women living in poverty to the financial system levels the playing field without exposing them to undue risks such as over-indebtedness. Therefore, it is important to highlight how saving acts as a mechanism for social protection by increasing the capacity of low-income groups to make informed financial decisions with awareness of their economic and social rights. Further, it promotes personal, family, and community well-being.

We conclude by highlighting six implications arising from our study for developing policy promoting women’s savings for women’s empowerment. First, this study points to the importance of providing financial training beyond financial incentives or subsidies, because this allows women to give meaning to the act of saving (which is consistent with the findings of Trivelli and Yancari, 2008). In this regard, the promoters and women leaders played a critical role not solely in terms of providing information or knowledge, but also in terms of female empowerment and in a relational sense by connecting women to informal and formal networks.

Second, it is essential that people approach financial institutions voluntarily and in person, which is a prelude to expanding their connections with other institutions. In this context, financial education and entrepreneurship need to be addressed considering the power-laden mechanisms that people living in poverty must deal with in their interactions with the incumbent constituencies of society, such as government, banks, or capital owners (De Clercq and Honig, 2011).

Third, this study points to the importance of public policies and Social Protection Systems and the willingness of financial institutions to collaborate in these initiatives, as well as the need for the geographical expansion of banking services. Also, it is necessary to educate financial institutions to dispel prejudices about low-income groups and thus encourage them to offer them credit on more favourable terms.

Fourth, it is relevant to improve the association between saving incentive programmes and agencies that promote entrepreneurship. In this regard, a virtuous circle could emerge, with savings injecting resources into micro-enterprises in a more sustainable manner and then reinforcing saving behaviour as these resources begin to generate higher revenues (Agrawal et al., 2009).

Fifth, it is necessary to recognize the obstacles which women confront in the saving process, but taking into account that resources such as tenacity, creativity, and social networks that existed to some degree even prior to these. Therefore, interventions do not need to recreate those resources, but should instead provide the impetus required to activate them (Bellò et al., 2018; Kast et al., 2012). This recognition of women’s resources and the strengths of their contexts is fundamental to avoid adopting the colonialist logic that women from the South—who are considered monolithic, backward, and incapable of generating knowledge—need to be ‘rescued’ (Mohanty, 2003).

Finally, women need to believe that they can save, plan, and progress. Increased knowledge of savings and entrepreneurship amongst low-income groups of women can contribute to reducing the gender gap (Swail and Marlow, 2017; Vossenberg, 2013). This is especially important given that other researchers associate low-income people with limitations in terms of personal abilities (Narayan et al., 2000) and consider that women have limited educational attainment opportunities and little control over their financial futures (Holloway et al., 2017).

In this context, the results of this study demonstrate how savings programmes can be a path to empowerment for rural women living in poverty. The effects of the programmes in multiple domains of women’s lives clearly illustrate the process whereby their power increases, leading to improved control over material (savings) and non-material resources (e.g., self-confidence, relationships). This is consistent with Hidalgo’s (2002) definition of female empowerment and represents a clear case of how female empowerment must be comprehended as a process (Eyben et al., 2008).

In line with the results reported by Chen and Mahmud (1995), this study also revealed that women experienced changes in several dimensions of their lives. However, the results presented in this article provide a more detailed picture of how these changes can reinforce themselves in each dimension. For example, they show how the relational change of getting out of the home to meet a promoter, women leaders, and other women in similar situations ultimately fosters relational changes in broader spheres, improving connections with financial institutions and even granting access to other basic services such as health and education. Moreover, the results show how these dimensions of change are closely interconnected and intertwined; for example, they reveal how a material change such as gaining control over money influences relational changes such as overcoming the fear of opposing their partners.

In relation to the above, the results highlight the potential benefits of saving, especially for women in relationships that hinder their decision-making power due to patriarchal structures (Hidalgo, 2002). As Johnson (2005: 1) indicates, ‘assessments of the impact of microcredit targeted towards women have tended to focus on evaluating whether women have become “more empowered”, rather than on the dynamics of gender relations in which they are embedded.’ In this regard, the present study paid close attention to how gender relations (specifically related to partners) were hindering women’s empowerment and how they can change in order to facilitate it, particularly through saving programmes in rural areas.

In this regard, saving allowed women at an individual level to achieve greater economic stability and more sustainable outcomes, offering greater social protection and safeguarding their rights. However, female empowerment not only acts at an individual level, but also has ripple effects in the community, manifested through closer relationships among women and more community integration. This is illustrated when the participants say ‘we are a community’: for them, empowerment is not individual but relational and the importance of membership and shared emotional ties (McMillan and Chavis, 1986) shows the importance of understanding the collective dimensions of empowerment.

Also, a community perspective of empowerment includes developing female leadership, which can empower other women as well (as noted by Martínez, 2017). This is the case in the programmes analysed, where some women raised their voices to encourage their peers to move forward. However, it remains as a challenge to study if the women’s leadership and activism that these interventions promote can be linked to systemic and structural changes.

To recap, Eyben et al. (2008) proposed three kinds of empowerment as paths out of poverty: social, economic, and political. According to these authors, political empowerment involves increasing a group’s equity of representation in political institutions and ‘enhancing the voice of the least vocal so that they can engage in making the decisions that affect the lives of others like them’ (p. 18). Although in the present study women leaders did not report being involved in local government or the political sphere in general, they stated that these programmes improved their ability to express themselves and be more confident, reflecting their pride in being leaders.

Considering that political empowerment involves enhancing people’s ability to speak about and for themselves (Eyben et al., 2008), it could be argued that saving programmes make it possible to establish this basic framework for future political empowerment. However, it remains a challenge for these programmes to facilitate the institutional or political aspects necessary for these incipient effects to translate into effective political empowerment for women. This should encourage researchers to consider women’s empowerment in microfinance programmes with respect to both their ‘practical needs’ (material and survival conditions) and their ‘strategic interests’ (social position), in terms of Molyneux (1985). This is relevant in the literature about gender empowerment, where the notion of empowerment is often devoid of its political meaning (Kabeer, 1998).

Finally, this study suggests that empowerment is as important as financial inclusion, hence an integrative and more holistic Model of Programme Evaluation is required for evaluating this type of social initiatives (Daher et al., 2020). It also highlights the necessity of analysing saving programmes aimed at rural women who live in poverty and belong to indigenous groups from an intersectional feminist perspective (Hill Collins, 1990). Our analysis of the subjective experiences of poor, rural, indigenous women in savings programmes reveals the importance of these intersections for understanding how three savings programmes facilitated a path towards female empowerment and entrepreneurship in the Highlands of Peru.

Footnotes

Acknowledgements

This article has been enriched by the comments and discussions held with Johanna Yancari, Jaime Ramos, María Cristina Gutiérrez and Ximena Montenegro from the Institute of Peruvian Studies, which is part of the Capital Project. Also, it has benefited from the observations made by Jean Paul Lacoste and the funding granted by the Ford Foundation and the Multiple Donors Research Platform for Social Protection, Financial Inclusion, Information Technologies and Communication (with the financial support of the International Research Center for Development).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the authorship, research, or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This article is part of the doctoral thesis ‘Facing the challenge of integrating objective and subjective dimensions in social programs evaluation’. This work was supported by the National Commission for Scientific and Technological Research CONICYT; and the Interdisciplinary Center for Intercultural and Indigenous Research CIIR [FONDAP 15110006].