Abstract

This paper investigates the impact of the Economic and Monetary Union on international tourism flows across a set of 37 developed countries. To do this, an augmented gravity model is estimated using a sample of 31 European countries plus six non-European OECD countries over the period 1995–2012. Results suggest a substantial impact of the euro on intra-Eurozone tourism of between 44 and 126% when proper estimation method, control group and definition of the Eurozone are used. Moreover, evidence of tourism creation is also found. Finally, the potential tourism gains for new members and possible entrants of adopting the euro are explored. This study provides a detailed analysis on the effect of the euro on tourism flows which might be of interest for policymakers of the Eurozone or future member states.

Introduction

According to Baldwin (2006), the euro must be the world's largest economic policy experiment. In 1999, 11 European nations found themselves using the same currency. Given the importance that monetary regimes have on economies, switching to the euro should have had effects all across the board. Since the inception of the euro, the bulk of the literature has focused on the analysis of its economic impact. Indeed, empirical research in International Economics views the euro effect as an area of significant interest, mainly trying to quantify its impact on international trade, FDI or economic growth. However, only few papers have explored the impact of sharing a common currency on international tourism. Tourism is closely linked to the economic activity in general and its development is inevitably marked by the introduction of the Euro. According to the Eurobarometer elaborated by the European Commission (2011), citizens of the New member States showed a weak support for the introduction of the euro, although an overwhelming majority agreed that joining the common currency would be more convenient for those who travel in other countries that use the euro and that the euro would make it easier to shop in other countries using the common currency. Therefore, the euro effect on tourism flows might have important policy implications since it not only affects tourism flows across European Union (EU) countries but also it might help to improve the attitude towards the euro. In this respect, a better understanding of the effect of the euro on tourism flows may add another argument to the debate on the benefits of joining the Economic and Monetary Union (EMU).

Traditionally, substantial effort has been put into estimating the impact of the euro on international trade and its role in macroeconomic performance (Frankel, 2010). Some papers have estimated an early effect of the euro on international trade. For instance, Micco et al. (2003) find an increase in trade which ranges between 5 and 20%; Faruquee (2004) estimates that the euro has boosted trade among member states by roughly 10%; Flam and Nordstrom (2006) report an estimate of 26%; Aristotelous (2006) estimates an overall effect of the euro of around 6%; Baldwin (2006) obtains a pro-trade effect of 9%; while Bun and Klaassen (2007) report an increase of 3% for the euro trade effect. Recent papers update the euro effect considering more years since the common currency was adopted. Camarero et al. (2013) estimate a euro effect of 18%, while Sadeh (2014) finds that exports between two participating member states are 92% higher than they would have been without the euro. These different estimates of the euro effects depend on the sample size, the countries considered in the analysis, the estimation techniques and the dependent variable used. Indeed, Sadeh (2014) provides an interesting review of previous papers on the euro impact on trade highlighting their studies' main empirical problems.

According to the World Tourism Organization (UN-WTO, 1998), the euro would bring positive impacts or benefits on tourism flows, since it affects the economic environment in which firms and consumers move. Adopting the euro enhances price transparency, since it makes it easier for tourists to compare prices in the various destinations of the Union, and hence competition is improved. Moreover, sharing a common currency eliminates exchange rate fluctuations, for travellers and firms, reducing the costs and time spent on currency exchange, leading to lower travel-operational costs and mitigating administrative problems and even possible cheating on the currency exchange. Additionally, within the currency union, the exchange rate is no longer a factor of relative price competition, since it is not possible through real exchange rate depreciation to take advantage of lowering the relative price of tourism products vis-a-vis competitors (Rudež and Bojnec, 2008). The UN-WTO also highlights some macroeconomic benefits of the euro when economic and political integration leads to lower interest rates, and thus less expensive investment in tourism, as well as providing long-run price stability, which both enhance tourism competitiveness. Finally, the birth of a new international reference currency allows stakeholders to denominate international contracts in euros and not only in dollars or yen. Consequently, EMU countries become more sheltered from the exchange rate fluctuations of strong currencies, which facilitate the internationalization of tourism enterprises. Belke and Gros (2001) provide an additional channel for the euro effect through the option value of waiting which shrinks when exchange rate volatility disappears. Webber (2001) found that variance of the exchange rate is a significant determinant of tourism demand holding that a risk averse tourist may decide to cancel, delay or even switch to another tourist destination if there is too much volatility of the exchange rate at the destination country of her initial choice. So an increase in the exchange rate volatility may induce tourists to wait to travel.

According to the UN-WTO data, tourist arrivals to the Eurozone represented 30% of overall world tourist arrivals in 2012, and half of these tourists arrived from other member states. However, in spite of the relevance of exploring the impact of the euro on inter-EU tourism flows, the only antecedent in the empirical literature is the article by Gil-Pareja et al. (2007). These authors estimate an effect of the euro on intra-Eurozone tourism flows of 6.5% by considering a sample of 21 OECD countries over the period 1995–2002. This moderate effect could be explained by the shortness of the euro period studied (1999–2002), as well as by the control group and the econometric technique used. For their part, Santana-Gallego et al. (2010) analyse the role of different exchange rate regimes on tourism flows including the currency union. However, the application of this result to the specific euro case is hard to accept because they consider different common currency experiences beyond the euro. This argument is also discussed by Frankel (2010) in the analysis of the discrepancy between the magnitude of the euro effect on trade and the impact of other monetary unions. Finally, De Vita (2014) explores the role of different exchange rate regimes on international tourism flows obtaining that sharing a common currency exerts the strongest positive impact on inbound tourism. In particular, by considering the case of the euro up to 2011, the effect of common currency on tourism is around 30%.

Baldwin (2006) holds that EU membership is an extremely complex process that involves thousands of laws, regulations and practices that affect trade (as well as tourism flows) within the EU and third-party nations, most of which are unobservable. Therefore, to properly analyse the impact of the euro on international flows, the control group must be limited to the EU countries. Nevertheless, Sadeh (2014) argues that an appropriate control group must include enough countries that have not joined the euro area but that would have responded similarly to the launch of the euro had they joined it. 1 The present study analyses tourism flows between the 28-EU countries plus three non-EU countries (Switzerland, Norway and Iceland) that participate in the European Free Trade Association (EFTA), which is part of the EU's internal market. Moreover, to have enough countries in the control group, six non-European OECD countries (Australia, Canada, Japan, New Zealand, Turkey and United States) are also included. 2

Another relevant aspect studied in this paper article is the path of the euro impact over time. For instance, the relevance of the dates of introduction of the irrevocable exchange rates in 1999 and that of circulation of coins and notes in 2002 can be compared. Since 2002, any calculus has been eliminated and the decisions of tourists, as consumers, could have been more affected by the introduction of euro coins and notes than by the inception of the irrevocable conversion rates for the euro in 1999. From a psychological point of view, Jonas et al. (2002) and Wakker et al. (2007) argue in favour of the year 2002, as from that date, consumers were physically confronted with the euro. Ranyard et al. (2005) find that consumers' attitudes with respect to the euro focus mainly on the economic and practical aspects of currency exchange. Moreover, the influence of the euro on the magnitude of tourism flows may take time to be registered, although its effect could have been felt in advance. In other words, the announcement and the last phases of the exchange rate mechanism prior to the inception of the euro could have influenced tourists' decisions about the destination country of their visits. So, the presence of leads and lags in the euro impact may be tested. What is more, this analysis may shed light on the euro effect during the current economic crisis.

Two more related issues are explored in this research. Firstly, the euro could lead to tourism diversion. Following Belke and Spies (2008), tourism creation implies that lower cost tourism suppliers inside the currency union substitute higher cost domestic producers as a result of diminished tourism costs. Tourism diversion takes place when low-cost tourism suppliers outside the currency union are replaced by higher cost Eurozone producers. So, trips to destinations outside the Eurozone are replaced by travels within the Eurozone countries. Therefore, the adoption of the euro may lead to new international tourism flows (tourism creation) as well as to geographical restructuring of tourism (tourism diversion). Secondly, the effect of the euro on tourism is compared among EMU members in order to study whether the positive impact that the euro has on tourism is widespread across members. This analysis would clarify the issue of whether all countries are taking advantage of joining the EMU in the same way or, on the contrary, whether the results are driven by the experience of just a few of them.

Finally, the tourism potential of adopting a common currency is explored. The EMU has experienced an enlargement process after the introduction of the euro in 1999, and there are still several countries planning to join the Eurozone. Although potential gains of the enlargement process have been explored in the international trade literature (Baldwin, 1994; Belke and Spies, 2008; Brouwer et al., 2008; De Benedictis and Vicarelli, 2005; Papazoglou et al., 2006 among others), no article has calculated the tourism potential of adopting the euro. Our paper aims at filling this gap by estimating tourism potential for a sample of European countries.

To sum up, this research contributes to the literature in several ways: (i) the impact of the euro on international tourism is properly estimated by using a sample that includes 37 developed countries; (ii) the ex-post euro effect on tourism is estimated for the period 1995–2012, which involves 11 years during which euros circulated and 14 years of irrevocable exchange rates, respectively; (iii) the existence of tourism diversion or tourism creation effects of the EMU is tested; (iv) the path of the impact of the euro over time is addressed; (v) the effect of the euro on bilateral tourism for each of EMU-11 members is explored and (vi) the tourism potential of adopting the euro is calculated for a set of candidates and hypothetical members. As far as we know, this article is the first attempt to explore tourism diversion and the time path of the effect of the euro on tourism, as well as calculating the potential gains for tourism in joining the EMU. Furthermore, this contribution addresses some empirical problems that have arisen in the extant literature on this issue by using a database with a longer time period, a proper control group with enough no EMU countries and by including both country-year and country-pair fixed effects (CPFEs) in the regression.

Econometric specification

The gravity model has been the workhorse for empirical analyses of the euro effect on trade flows. Rose (2008) surveys 26 studies and, taking together all these estimates, observes that EMU has increased trade by about 8–23% in its first years of existence. Under the assumption of tourism as a particular type of trade in services, a gravity equation can be used to study the main determinants of tourism volume (see for instance Durbarry, 2008; Eilat and Einav, 2004; Khadaroo and Seetanah, 2008; Neumayer, 2010). In fact, Kimura and Lee (2006) show that trade in services is better predicted by gravity equations than trade in goods, and Culiuc (2014) finds that the gravity model explains tourism flows better than trade in goods for equivalent specifications. Morley et al. (2014) show that gravity models for tourism can be derived from consumer choice theory providing theoretical underpinnings for the use of this model to explain bilateral tourism. These authors consider that individuals maximize their utility by consuming tourism trips and other goods and services subject to a budget constraint. By summing up all individual demands, total international trips between two countries can be obtained.

Anderson and van Wincoop (2003) show that the volume of trade between any two countries depends not only on their level of bilateral trade resistance, but also on how difficult it is for each of them to trade with the rest of the world. In other words, multilateral resistance need also be considered. Feenstra (2002) proposes the introduction of exporter and importer dummies as a way of controlling multilateral trade resistance (CFE), whereas Ruiz and Vilarrubia (2007) point out that, when using panel data to estimate a gravity equation, the omission of time-varying multilateral trade resistance biases the results. Thus, time-varying fixed effects, as an extension of the methodology proposed by Feenstra (2002) for cross-sectional data, are considered in this empirical analysis. 3 In particular, we include exporter (destination)-year (EYFE) and importer (origin)-year fixed (IYFE) effects. Furthermore, it is necessary to control for the endogeneity bias that arises when countries decide to adopt a common currency because it would increase their tourism flows with other member countries. Baier and Bergstrand (2007) and Flam and Nordstrom (2006) introduce both country-year and CPFEs to assess the impact of Free Trade Agreements on trade flows. Berger and Nitsch (2005) and Pakko and Wall (2001) also include both sets of fixed effects to explore the effect of currency unions on international trade. As argued by Pakko and Wall (2001), including country-pair fixed-effects avoids estimation bias that can arise because of misspecified or omitted time invariant factors that are correlated with bilateral trade and some right-hand side variables.

Here, it is important to note that the introduction of time-varying fixed effects makes it impossible to estimate the coefficient on time-variant country characteristics, such as GDP and population in origin and destination countries. Similarly, when CPFEs are included in the regression, time-invariant country-pair characteristics, such as distance between countries, common language or common colonial relationship, are absorbed by these fixed effects. Therefore, after controlling for EYFE, IYFE and CPFE, what remain to be explained are time-variant country-pair characteristics that influence tourism, such as sharing the euro. Our preferred specification is as follows

Secondly, there are time-variant bilateral factors affecting tourism such as EU ijt that is a binary variable which is unity if i and j are both members of the EU in year t. EU ijt controls for the different enlargement episodes of the EU. 5 Regarding the variables of interest, E ijt is a set of dummy variables measuring the effect of the euro on tourism. 6 Following Morley et al. (2014), sharing a common currency can be interpreted as part of the bilateral cost of travelling from an origin country to a destination one. Adopting the euro might in other words reduce not only variable but also fixed costs related to international travel, and hence it helps justify the absence of the tourism diversion effect of the euro.

Empirical results

The empirical analysis uses a sample of 37 developed economies (EU-28, three EFTA countries, i.e. Switzerland, Norway and Iceland and six non-European OECD economies, i.e. Australia, Canada, Japan, New Zealand, Turkey and United States) over the period 1995–2012. Equation (1) is estimated by defining different variables related to the euro effect on tourism.

The effect of the euro on tourism

Euro's effect on tourism.

Note: Significant at 1% (***), 5%(**) and at 10% (*) level.

Constant, EYFE, IYFE and CPFE are not reported.

Standard errors are reported in parentheses and p-values in brackets.

Robust standard errors clustered by pair are computed.

In Model A, a dummy variable that is unity when both countries in the pair belong to the EMU is defined (Euro both) This variable considers all the countries that belong to the EMU in a certain year. So, this variable jointly considers the initial countries that joined the EMU in 1999, as well as the new ones that joined during the various enlargements. Here is important to note that the variable Euro both takes the value zero for the period 1995–1998 for all country pairs. For instance, euro both takes the value zero for the pair Austria–Germany before 1999 and the value one since 1999. The coefficient of Euro both is positive and significant at 1% level suggesting that the euro promotes intra-Eurozone tourism by a factor of 44.63%. 7

Another relevant issue is to check whether adopting the euro has made the Eurozone more open to tourism (tourism creation) or, on the contrary, has led to more intense tourism flows within the Eurozone at expense of diversion of tourism with non-members (tourism diversion). The argument is direct if a change in relative bilateral resistances is recognized, i.e. the increase of relative costs with third-party countries could lead to tourism diversion. In the case of international tourism, the elimination of exchange rate volatility, transaction costs and any calculus since 2002 may lead to more intense tourism flows within the Eurozone but also to a reduction of international tourism between the Eurozone and other countries. So, a dummy variable that fully controls for tourism with third-party countries whatever the direction is included (Euro one). This variable takes the value of one when only one country in the pair belongs to the EMU. The estimated coefficient shows that the euro effect on trade with non-members is around 18.77%. Consequently, as for international trade (Cafiso, 2011; Faruquee, 2004; Micco et al., 2003), evidence of tourism creation is found. That is, adopting the euro makes country members more open and therefore boosts their trade and tourism flows with third-party nations.

Model B addresses the different enlargement episodes on the effect of the euro depending on the date of inception, i.e. differences in the impact of the euro depending on whether the country initially adopted the euro in 1999, Euro-11, or joined later, Euro-new. In 1999, 11 countries joined the EMU, and afterwards six more countries adopted the euro at different stages. 8 Euro-11 both takes the value 1 if both countries in the pair joined the EMU in 1999, e.g. for the pair Austria–Germany for years 1999–2012. Euro-new both takes the value of 1 when one of the countries in the pair is a new member and the other already belongs to the EMU. For instance, the pair Cyprus–Austria takes the value of 1 for years 2008–2012. Euro-11 one and Euro-new one are accordingly defined to consider only one Euro-11 or a Euro-new country in the pair.

The estimated coefficients of both variables suggest that the impact of the euro on international tourism flows is slightly higher for countries that initially joined the EMU rather than for those which incorporated it afterwards. In particular, the impact of the euro on EMU-11 countries is 146%, whereas the effect on new member states is around 112.5%. This estimated impact is larger than the euro effect estimated in Model A, but as will be shown latter, this result can be explained by the large heterogeneity in the estimated impact of the euro by country, mainly between Euro-11 and Euro-new countries. For the tourism diversion effect, the impact on tourism with third countries is 59.4 and 28.7% for the EMU-11 and the new euro members, respectively, suggesting again evidence of tourism creation. We address this through a counterfactual analysis below, where the potential tourism gains are calculated considering what would have happened if new entrants had adopted the euro in 1999.

As presented in Table 1, when individual hypothesis are tested for differences in the coefficient between the Euro-11 and the Euro-new group of countries (H1 and H2), coefficients are not significantly different for the euro effect (Euro both), while they are significantly different for the tourism creation effect (Euro one) at 5% significance level. Moreover, when both hypotheses are jointly tested, results suggest that the null hypothesis of equal coefficients for Euro-11 and Euro-new countries is rejected at 5% significant level, and so Model B is preferred to Model A.

Model C takes into account the initial stage of the EMU when irrevocable exchange rates were set in 1999, and the second stage when the euro started to circulate in 2002. Two dummy variables are defined, Euro-11 both (1999–2001) that takes the value one if both countries in the pair belonged to the EMU-11 during the period 1999–2001, and Euro-11 both (2002–2012) that takes the value of 1 when both countries are EMU-11 for the period 2002–2012. The former variable controls for the fixed irrevocable exchange rate between country members, although national currencies remained circulating, while the latter reflects the introduction of the euro as the national currency. Similarly, to control for tourism with third countries, Euro-11 one (1999–2001) and Euro-11 one (2002–2012) dummy variables are defined.

From Model C, it can be observed how the effects for the period 2002–2012 are higher than for the period when the irrevocable exchange rates were fixed. However, when individual test for differences in the coefficients in both periods is applied, only for the tourism creation effect (Euro-one) these coefficients are significantly different at the 10% significance level. Therefore, having a common physical currency circulating seems to be more relevant than just the elimination of exchange rate volatility. These results are confirmed in the next section where a significant effect of the changeover in 2002 is shown. Finally, when both hypotheses are jointly tested (H3 and H4), at 1% significance level we cannot reject that the coefficients are significantly different, suggesting that Model B is again the preferred one. To sum up, Table 1 presents joint test to discriminate which is the preferred model, and as can be observed, this is Model B. Consequently, this specification is the one to be used in further estimates.

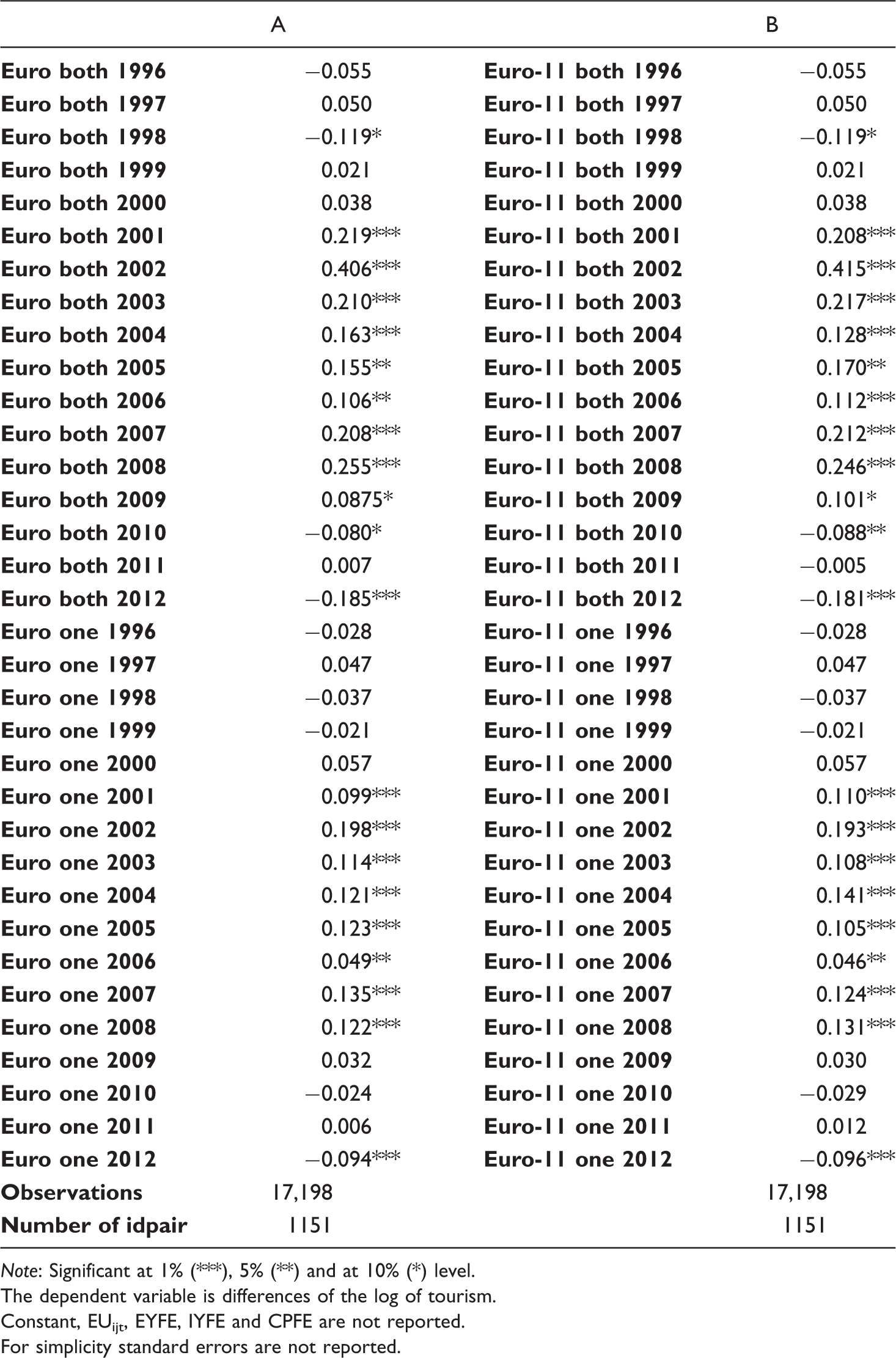

The effect of the euro by year

The second part of this research explores the dynamic of the impact of the euro on tourism flows. This exercise may shed light on the time path of the euro effect as well as exploring the euro performance during the current economic crisis. Indeed, the characterization of the impact path of the euro on tourism over time would be of interest for future common currency experiences and for prospective members of EMU. The influence of the euro on tourism flows might take time to be registered, but its effect could have been felt in advance. In other words, the announcement of the last phases of the exchange rate mechanism prior to the inception of the euro could have influenced tourists' decisions about the destination country of their visits. Therefore, the presence of an anticipated effect of the euro can be tested for by analysing the effect of the euro in tourism flows for the whole sample period even before the inception of the euro. As far as we know, this is the first attempt to measure the path of the euro impact on tourism over time.

Euro's effect over time.

Note: Significant at 1% (***), 5% (**) and at 10% (*) level.

The dependent variable is differences of the log of tourism.

Constant, EUijt, EYFE, IYFE and CPFE are not reported.

For simplicity standard errors are not reported.

To explore a possible advanced effect of the euro, the Euro year variables would take the value of 1 for a specific year if both (or one) countries had been members of the Euro since 1995. To that end, we include separate euro dummies for each year from 1995 to 2012 to follow the tourism performance of the countries that joined the euro over time and if an anticipated effect of the euro exists before it was created in 1999. Similar to Micco et al. (2003), we need to redefine the Euro Both and Euro One variables so that they take a value of 1 for two Euro-11 countries throughout the whole sample period, even before the formal creation of EMU. Euro-New countries are considered from the year the euro was introduced. As an example, Euro both 1995 would take the value of 1 for the pair Austria–Belgium in 1995 since both countries adopted the euro in 1999, but would take the value of 0 for the pair Austria–Greece since the latter adopted the euro in 2002. Similarly, Euro both 2002 would take the value of 1 for both pairs Austria–Belgium and Austria–Greece. To remove the effect of the enlargement process, the year-by-year estimate is also calculated for the variable EMU-11, including only the countries that initially joined the EMU in 1999.

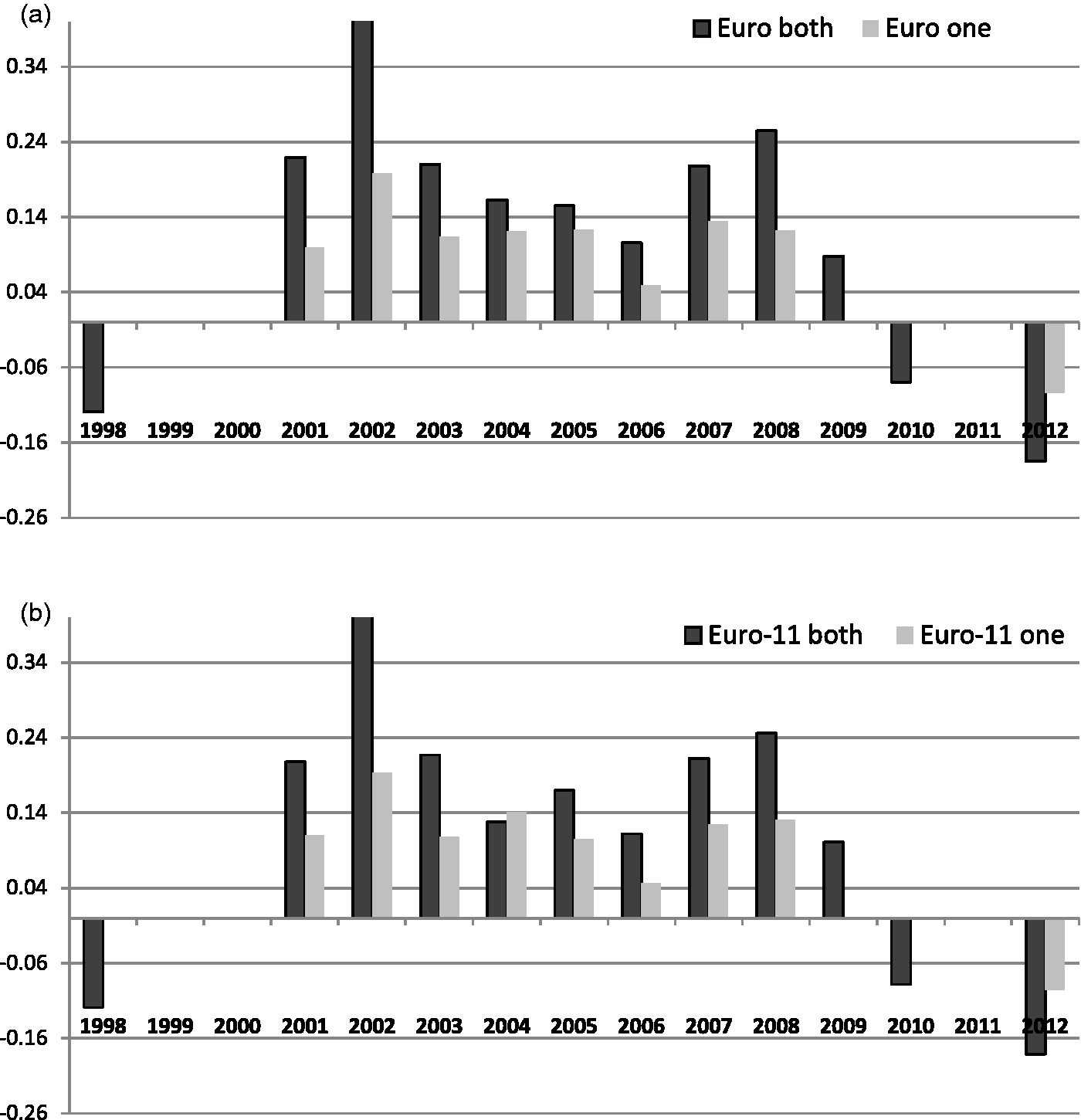

As we can observe in Table 2 and Figure 1, the time path of the Euro both and Euro one dummy variables is similar. There is not a positive and significant effect of the euro until 2001 and the largest impact on tourism differences is detected in 2002. This year is precisely when the euro coins and notes started to circulate. These results suggest that tourism flows responded strongly to the creation of the euro in 2002, but did not diminish steadily thereafter rather there was a varied pattern. From 2003 to 2006, the effect of the euro decreases but rises in 2007 and 2008. The fall since 2009 can be attributed to the global/euro crisis. The impact of the euro on tourism presents a significantly negative impact in 2010 and 2012, i.e. the advantage of sharing the euro in terms of promotion of tourism seems to vanish during the current crisis. Austerity measures implemented in several European countries as well as rising unemployment are expected to result in lower disposable, thus reducing intra-regional travel and spending. This pattern could suggest that tourism has large income elasticity, rising with the bubble in 2007–2008, and collapsing when times are hard. Coefficients of Euro-11 follow a quite similar time path, and so they confirm the main results already presented for the set of all countries belonging to the Eurozone.

(a) Effect of the Euro over time, (b) effect of the Euro-11 over time.

The euro effect across member states

Euro's effect by country excluded from the sample (Euro-11 countries).

Note: Significant at 1% (***), 5% (**) and at 10% (*) level.

Standard errors are reported in parentheses.

Constant, EYFE, IYFE and CPFE are not reported.

Euro's effect by country excluded from the sample (Euro-New countries).

Note: Significant at 1% (***), 5% (**) and at 10% (*) level.

Standard errors are reported in parentheses.

Constant, EYFE, IYFE and CPFE are not reported.

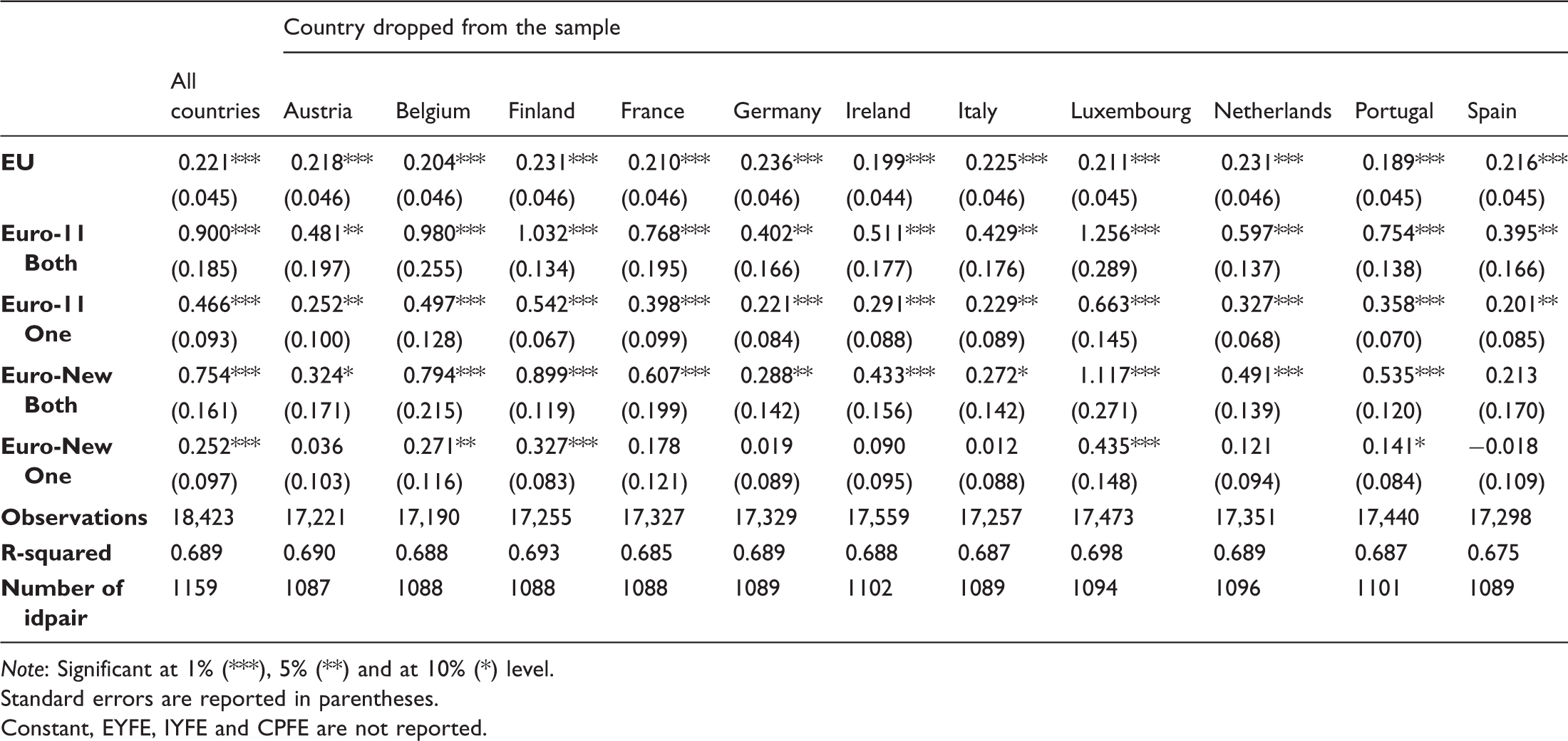

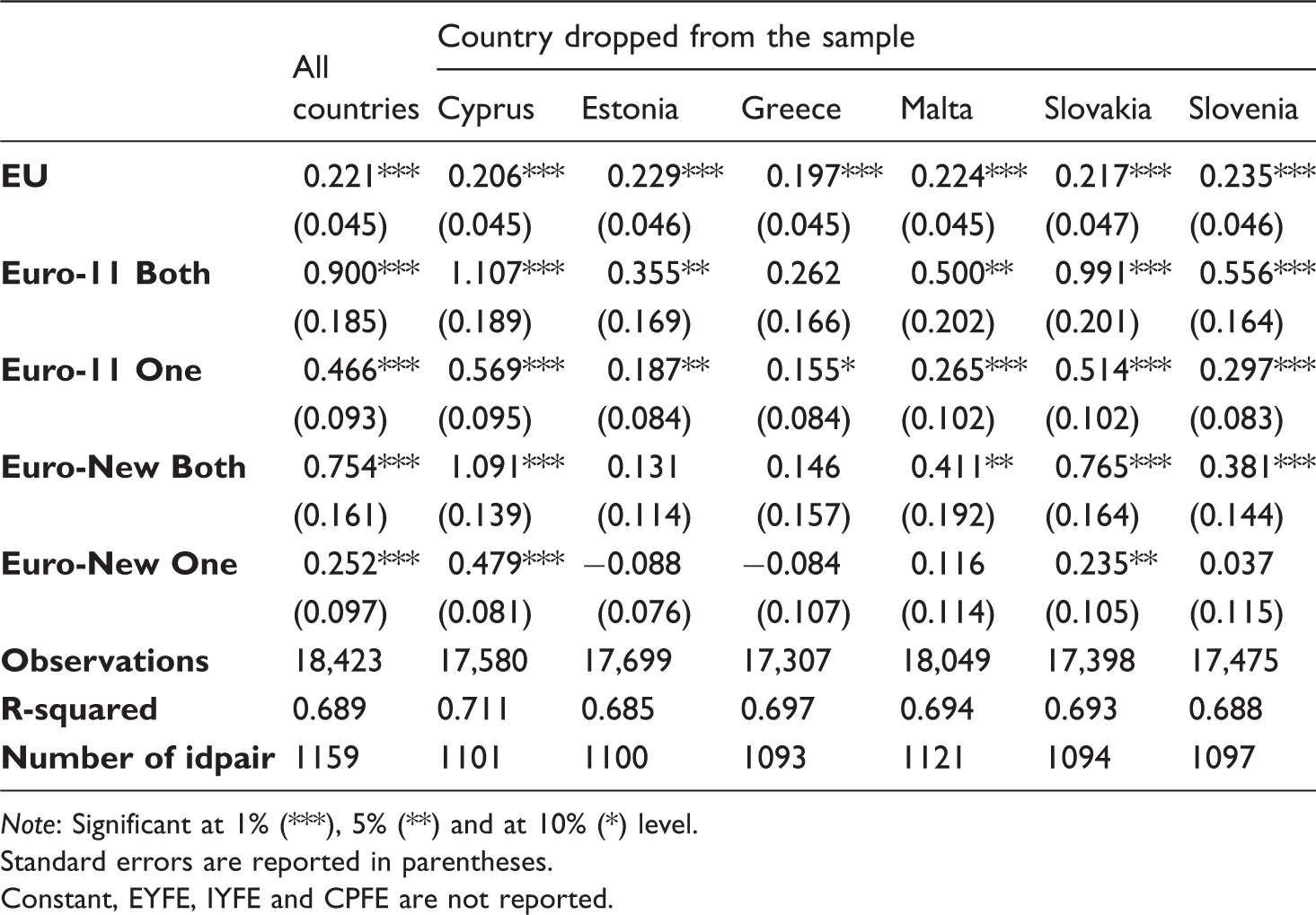

These results are robust for the exclusion of one country at a time, with the magnitude of the Euro Both and the Euro One dummy variables being significantly positive in almost all cases. However, the magnitude of the estimated impact of the euro effect varies depending on the excluded country, suggesting that tourism gains of adopting the euro present a wide dispersion at the country level. As presented in Table 3(a) for the Euro-11 group of countries, dropping Belgium, Finland or Luxembourg from the sample increases the estimated impact of the euro on tourism flows. This result might suggest that the euro effect on these countries is lower than for the rest of the Euro-11 countries. Moreover, there are some countries like Austria or Germany, which are important origin countries for tourists, or Italy and Spain, which are important tourist destinations, which decrease the magnitude of the euro effect on tourism when they are excluded from the sample. A large impact of the euro on their tourism flows has to be expected since they have a substantial weight on the estimated euro effect. Regarding new members states, when Cyprus or Slovakia is dropped from the sample the magnitude of the euro effect increases, while if Estonia or Slovenia is excluded from the sample, the euro impact on tourism flows decreases. Note that the dummy variable is not significant when Greece is dropped.

These heterogeneous results for the euro effects across countries are also found by Gil-Pareja et al. (2007) for international tourism and by Aristotelous (2006), Faruqee (2004) and Micco et al. (2003) for the case of international trade. These estimated effects of the euro suggest that tourism gains are high for some new entrants like Slovenia or Estonia. These countries benefit more from the elimination of tourism barriers that the adoption of the euro implies, since these countries were less integrated than the initial Eurozone members. For Euro-11 group of countries, the estimated impact of the euro is expected to be larger for the main origins of tourists, i.e. Germany, or for destination countries, i.e. Spain or Italy. Conversely, the euro effect seems to be less relevant in two expensive tourist destinations like Finland and Luxembourg. According to data from the World Development Indicators, those countries present the highest price level. These results agree with the ideas discussed by Jenkins (2001), who argues that there will be downward pressures on prices in the Eurozone, especially where prices are high, because tourists seek better value for money, which may easily be identified by improved possibilities to assess prices using a single currency. 9

Counterfactual analysis

As mentioned in ‘Introduction’ section, a very relevant issue when evaluating the effect of the euro on intra-EU tourism flows is analysing the potential tourism gains of joining the Eurozone. The EMU has experienced successive enlargement processes after the introduction of the euro in 1999, and there are still several countries planning to adopt the euro. Although the potential of the enlargement process has been explored in the international trade literature, no paper has calculated the ‘tourism potential’ of adopting the euro. This analysis may shed light on the gains of joining the Eurozone in terms of tourism. To do this, a counterfactual analysis is carried out.

Counterfactual analysis is a common methodology to evaluate the effect of joining the EU or adopting the euro. It can be used to explore whether the United Kingdom or Sweden would have been better off if they had joined the euro. An important caveat to counterfactual analysis is that it can be subject to the Lucas (1976) critique in the sense that the deep parameters underlying the baseline estimates are likely to be different under the counterfactual scenario. However, several authors have argued that the change in the deep parameters may be too small to have a major effect (Dubois et al., 2007; Rudebusch, 2005; Smith, 2009). Moreover, Belke and Spies (2008) find that the in-sample and out-of-sample results are in the same direction when they are analysing the impact of the euro enlargement process. In this section, a counterfactual analysis estimates the potential tourism gains considering what would have happened if new member states had adopted the euro in 1999. Furthermore, potential gains for candidate states and for possible entrants are also computed.

Following Belke and Spies (2008) and Brouwer et al. (2008), the effects of EMU enlargement, future and ‘hypothetical’ adoption of the euro for individual countries can be approximated using a counterfactual analysis that involves three different steps. (i) Firstly, the baseline scenario (real model) is estimated. In this case, equation (1) is calculated including the Euro-11 both and the Euro-11 one dummy variables, and then tourism flows between country pairs are predicted. (ii) Secondly, a counterfactual scenario is estimated by considering that a new country joined the EMU in 1999. Now this country is added to the Euro-11 both and Euro-11 one dummy variables. This scenario is replicated for each of the 20 European countries in the sample that did not join the EMU when it was created. Again, tourism flows under this counterfactual scenario are predicted. (iii) Finally, predicted tourism flows for the baseline and the counterfactual scenario are compared to calculate the potential gains of adopting the euro in terms of tourism. 10

The baseline model is always the same but the counterfactual scenarios are computed country by country considering that a new member joins the EMU in 1999 each time. Taking Cyprus as an example, under the baseline scenario the Euro-11 both variable takes the value of 1, when both countries in the pair belong to the Euro-11 group, while under the counterfactual scenario Euro-11 both also takes the value of 1 when Cyprus is in the pair with another Euro-11 country since 1999. Similarly, the dummy variable Euro-11 one is generated under the real and the counterfactual scenario.

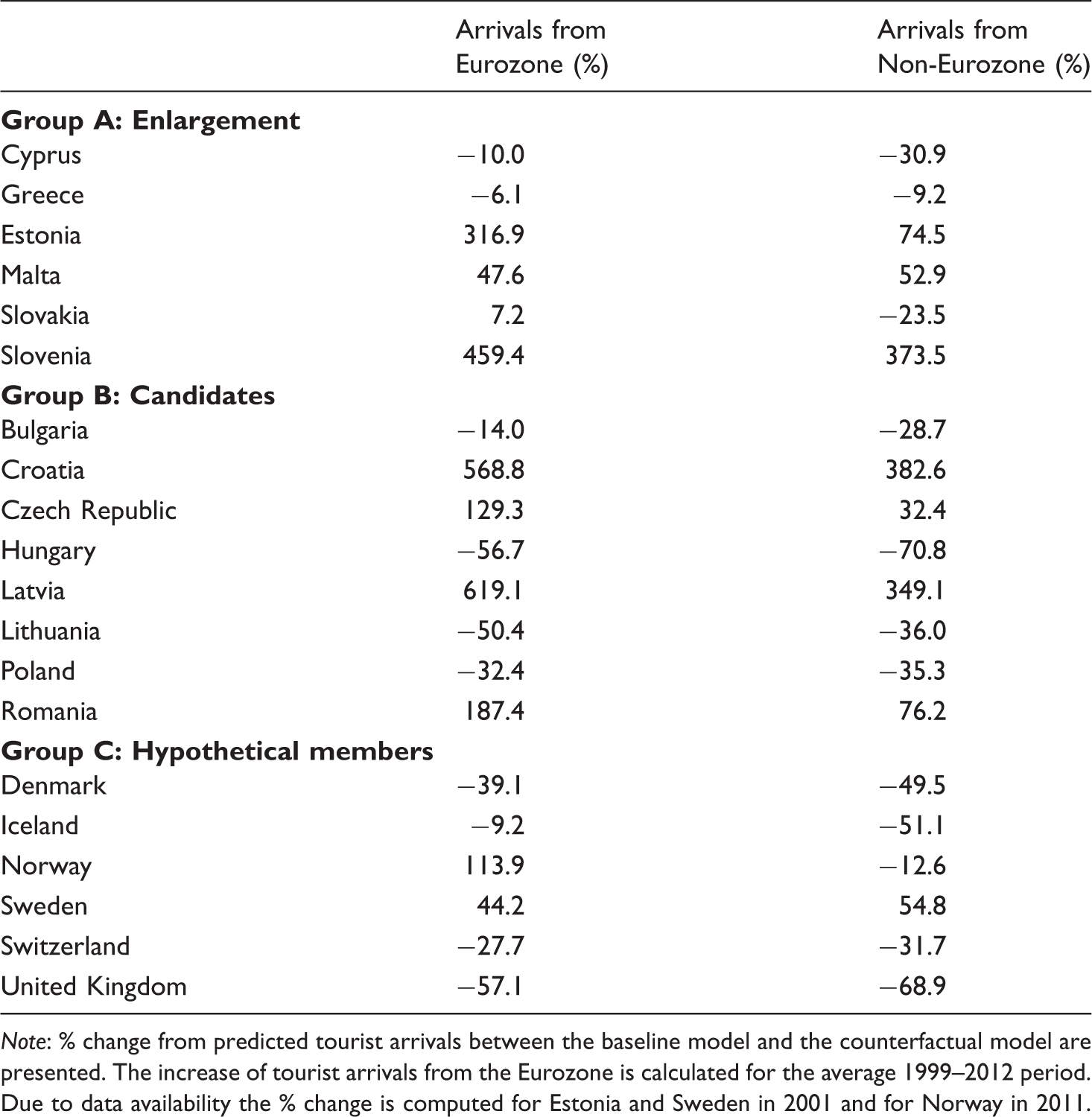

Counterfactual analysis.

Note: % change from predicted tourist arrivals between the baseline model and the counterfactual model are presented. The increase of tourist arrivals from the Eurozone is calculated for the average 1999–2012 period. Due to data availability the % change is computed for Estonia and Sweden in 2001 and for Norway in 2011.

In Group A, Slovenia (459.4–373.5%) and Estonia (316.9–74.5%) present the highest tourism gains from Euro-11 origins and third countries. This is a reasonable finding since these countries are relatively more open to the Eurozone countries than Cyprus or Slovakia, which present low or even a reduction in tourism arrivals. Note that the gains from tourism for Greece are very low since its real date of entry is close to 1999. For the candidate countries, Group B, Latvia (619.1–349.1%), Croatia (568.8–382.6%), Romania (187.4–76.2%) and Czech Republic (129.3–32.4%) present large gains in tourism of adopting the euro. In Group C, tourism gains are positive for countries like Norway (113.9%) and Sweden (44.2%), which receive large shares of tourists from EMU-11 countries. To sum up, the counterfactual analysis concludes that the potential tourism gains clearly vary across countries.

Belke and Spies (2008), Bussière et al. (2012) and Cieślik et al. (2005) also obtain some negative impacts of the euro on trade. This can be justified since there is evidence of tourism creation (Euro-11 one variable is significantly positive) in the baseline scenario. Therefore, benefits for non-member countries already exist because tourism is not diverted from third countries, so adopting the euro may have a negative effect on their tourist arrivals. This analysis might help policymakers to quantify the potential gains of adopting the euro.

Concluding remarks

This article provides an extensive and updated analysis of the euro effect on tourism flows. The empirical analysis not only uses a longer time period that allows a more thorough estimate of the ex-post effect of the euro, but also an appropriate control group is defined. Moreover, the updated sample period allows us to estimate the time path of the euro effect exploring the performance of the common currency on annual changes in tourism, and so exploring the impact of the changeover in 2002 and the 2008 economic crisis. These findings are relevant for demonstrating the effect of adopting the euro or for joining other currency union experiences. A better understanding of the euro effect on tourism flows contributes by adding another argument to the debate on the benefits of joining the Eurozone.

The estimated impact of the euro on tourism flows is 44.6%, although its magnitude increases to 146% when the analysis is limited to the initial Euro-11 initial members of the EMU. For tourism with third-party countries, evidence of tourism diversion is not found. Additionally, it seems that tourism gains from adopting the euro have not been evenly distributed among member states. The largest euro effect is estimated for new entrants and for Euro-11 countries with higher average price levels.

The time path of the euro effect is also estimated and results suggest that the highest impact is concentrated in the early stages (1999–2004), mainly during the changeover in 2002. Thereafter, the euro effect on tourism steadily falls until becoming not significant in 2009–2011 and significantly negative in 2012. These results suggest that the impact of the euro on tourism is lower during the current economic crisis.

Finally, the counterfactual analysis shows the potential gains in terms of tourism joining the EMU. These gains vary across countries, for some countries they are even negative. In this case, these countries would not further benefit from joining the Eurozone: benefits already exist even without adopting the euro. In any case, this is only one dimension of the effect of the euro. Other economic consequences of the political integration need to be evaluated. Overall, our research provides policymakers of future and potential entrants with an additional argument in favour of joining the EMU.

Footnotes

Acknowledgment

The authors wish to thank the UN-WTO for kindly providing us with tourism data and three anonymous referees for valuable comments on an earlier version of this paper.

Funding

Financial support from the Spanish Ministry of Economics and Competitiveness (ECO2011-23189) is gratefully acknowledged.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.