Abstract

To what extent did the European Monetary Union crisis alter the logic of European Union decision making? We analyze the relevance of asymmetric market pressures as compared to that of formal voting and agenda setting rules by applying three established bargaining models to the ‘EMU Positions’ data. Accounting for the interdependence between issues and agreements, we locate actors’ positions on three reform dimensions, namely the level of fiscal discipline, transfer payments and institutionalization. We find that market pressure during the height of the Eurozone crisis was particularly relevant, and that debtor countries were weakened by their difficulty in refinancing their public debt. Our finding shows that formal rules determining agenda setting and veto rights remain relevant even in times of crisis.

Introduction

Over the last few years, we have seen substantive reforms of the Economic and Monetary Union (EMU) aimed at preventing another Eurozone crisis. Starting with the first economic adjustment package for Greece in 2010, these reforms gradually institutionalized a financial assistance scheme in combination with reinforced fiscal austerity requirements to prevent a future sovereign debt crisis. Although they did so with different intensity, the same three fundamental reform dimensions kept resurfacing over the course of the negotiations. First, to what degree should Eurozone members assist each other financially (‘transfers’)? Second, how much should fiscal policy sovereignty be limited, especially the sovereigns’ right to borrow money and to accrue public debt (‘fiscal discipline’)? Third, cutting across both dimensions was the question of the ‘institutionalization’ of the new regime, meaning any mechanism that guarantees compliance with stricter fiscal discipline while ensuring mutual solidarity in the event of a crisis.

Despite the negotiations of these three reform dimensions having received a great amount of scholarly and public attention, opinions on whether formal, institutional or economic power affected the outcome of these reforms still differ. Some scholars have identified the significant impact of supranational actors, such as the Commission on the reform outcome (Bauer and Becker, 2014; Schimmelfennig, 2014), whereas other studies outline the newly strengthened power of the Franco-German alliance (Degner and Leuffen, 2019; Schild, 2013), or the leadership of a financially stable and economically strong Germany (Schoeller, 2017). Moreover, the EMU crisis hit member states asymmetrically. Whereas some states (e.g. Greece, Italy) faced acute challenges to refinancing their public debt, others (e.g. Germany, the Netherlands) were financially stable, but worried about the stability of the Euro. The key question that arises here is how far these acute and asymmetric market pressures offset the well-known effects of formal voting power and agenda rules on decision making in the European Union (EU).

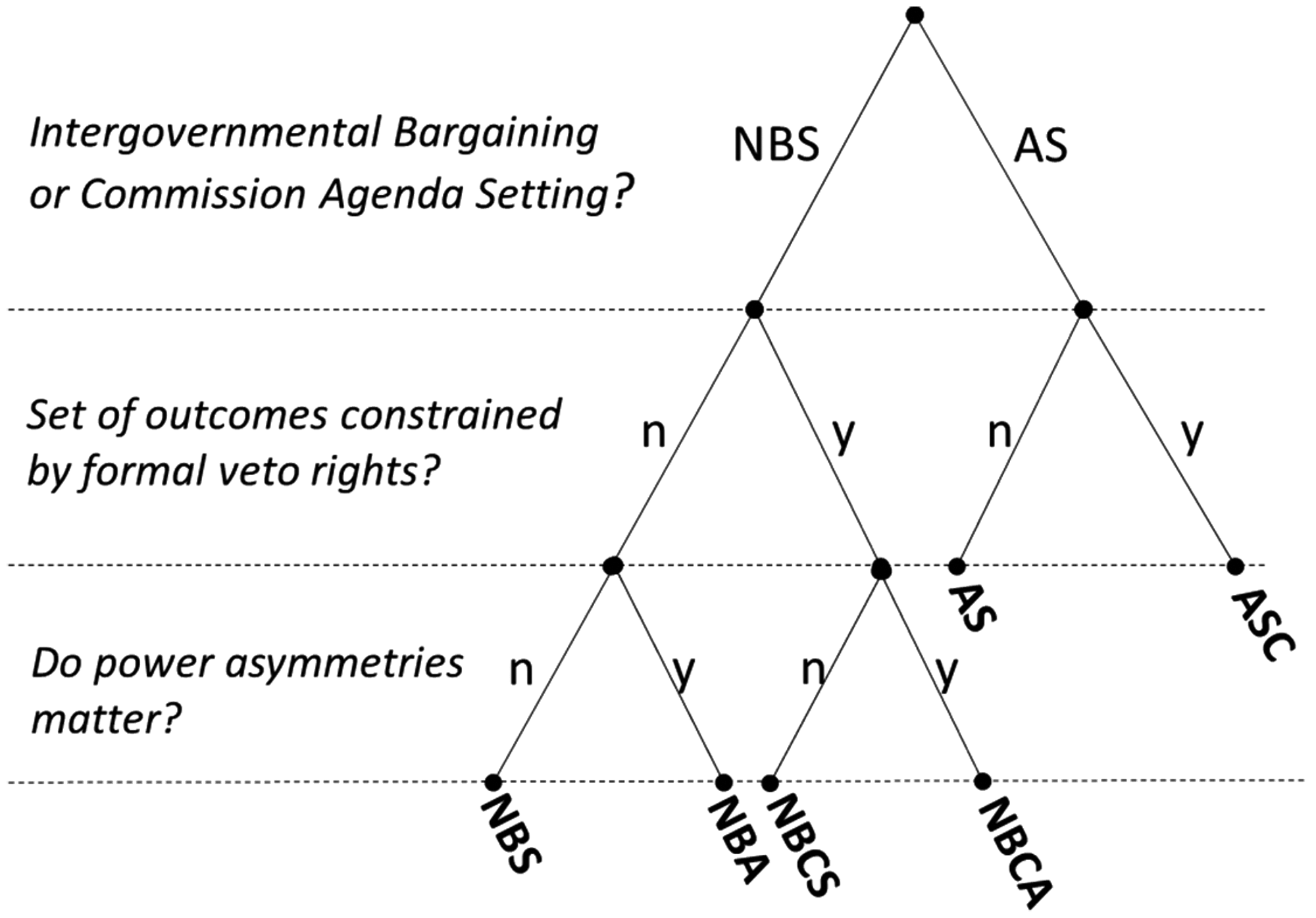

To analyze the relative importance of economic pressure as compared to that of voting and agenda power for understanding EU crisis politics, we use the ‘EMU Positions’ data to conceptualize and illustrate bargaining using three established models of EU decision making. The models differ in two important ways. First, they incorporate different assumptions about actors’ power in multilateral bargaining, i.e. how individual preferences are aggregated to a collective bargaining outcome. Second, they rely on different assumptions about the relevance of formal veto rights, resulting in different constraints defining the set of feasible bargaining outcomes (Finke and Fleig, 2013; Thomson et al., 2006). Thus, the combination of established models with unique data enables us to discuss the relevance of formal voting and agenda setting rules as compared to that of financial market pressures. Given the small number of truly independent cases, we cannot statistically test the predictive power of these competing models. Instead, this article offers a set of three case studies of EMU crisis bargaining, guided by a visualization of the different constraints, mechanisms for aggregating preferences and, ultimately, predictions offered by established models.

Which power resources are relevant to understanding the outcome of EMU crisis bargaining? First, we are interested in the relevance of economic power asymmetries that may have originated from member states’ different exposure to the crisis. While all states had an incentive to avoid a fully fledged currency crisis, only few were paying enormous risk premiums on refinancing their public debt. During the height of the crisis, these debtor countries were subject to particular market pressures and impatient to find a collective solution. In contrast to Schimmelfennig (2015), we find only limited support that asymmetric market pressures caused an EMU reform in favor of the German position.

Second, we evaluate the relevance of formal veto power. With regard to intergovernmental negotiations, we explore the extent to which every single Eurozone member had de facto veto power. With respect to legislative bargaining, we demonstrate that the qualified majority rules were crucial for opening a window for reforms. Third, we study the agenda setting role of the European Commission (EC), which has been described as a major winner in many of the reforms (Bauer and Becker, 2014).

In contrast to Lundgren et al.’s (2019) study of bargaining success, we find that asymmetric market pressures matter in times of crisis and that governments under less financial pressure are more likely to return successful from the international bargaining table. This confirms the importance of economic factors, as also found by Tarlea et al. (2019). In particular, during the height of the crisis, member states that considered refinancing their public debt increasingly costly were vulnerable at the bargaining table. We also found that market pressures did not perfectly correlate with governments’ reform positions. Specifically, France, which had relatively stable refinancing conditions throughout, shielded the group of crisis-ridden countries against more severe austerity measures. Moreover, we uncover that formal voting rules matter. Whereas the intergovernmental agreements left (almost) all Eurozone members better off, the legislative reform packages only satisfied a qualified majority of member states. Consequently, our analysis does not support the argument according to which intergovernmental bargaining was dominated by a Franco-German axis. Finally, we argue that the Commission’s agenda power depends on its formal rights and, consequently, only matters for reforming EU law.

After a brief review of the relevant literature, we introduce the bargaining models and their operationalization. In the empirical section, we offer three case studies on how the intergovernmental and legislative bargaining processes led to the EMU reforms. The empirical section starts by conceptualizing the three-dimensional reform space (the three dimensions being discipline, transfers and institutionalization). We then visualize, explore and discuss the different models for aggregating preferences, the sets of feasible outcomes and emergent predictions in that reform space. In addition, we offer a comparative evaluation of the models at the level of the individual reform acts: Greek Assistance Package, European Financial Stability Facility (EFSF), European Stability Mechanism (ESM), Fiscal Compact, Two Pack, Six Pack and Banking Union.

Bargaining during the Eurozone crisis

Studies of member states’ bargaining positions (Lundgren et al., 2019) or their ultimate

bargaining success (Tarlea et al., 2019) during the Eurozone crisis are static. They do not

consider the dynamics of multilateral crisis bargaining, such as agenda setting by the EC or

governments’ veto threats. Our comparison of different bargaining models allows for the

exploration of different sources of power, including asymmetric market pressures as well as

veto threats and supranational agenda setting. In the following, we contrast the existing

scholarly discussion of the EMU negotiations with three theoretical expectations derived

from established models of decision making in the EU. The Commission enjoys agenda setting power in legislative, but not in

intergovernmental bargaining.

Under the ordinary legislative procedure (OLP), the Commission’s unique right of initiative grants it gate-keeping, if not agenda setting powers (Tsebelis and Garrett, 2000). Empirical studies of EU legislative decision making find that the Commission is highly skilled in using its exclusive right of initiative (Boranbay-Akan et al., 2017; Crombez, 1996; Hartlapp et al., 2014; Kreppel and Oztas, 2017). By contrast, the Commission has no formal role in intergovernmental negotiations. However, this view has been challenged with respect to the Euro crisis negotiations from two sides:

First, the Commission has gained administrative powers under the intergovernmental treaties

reforming the EMU (Bauer and Becker, 2014; Lundgren et al., 2019; Tarlea et al., 2019). From

a supranationalist perspective, this result stems from how the Commission influences the

reform agenda by issuing a permanent flow of documents (Camisão, 2015). However, other

scholars refute this position, arguing that the Commission’s influence during the early

crisis management was limited (Camisão, 2015; Puetter, 2012: 282), not least because the EU

governments were eager to avoid agency slack in times of crisis (Menz and Smith, 2013: 198).

In legislative bargaining, the Commission’s impact was surprisingly limited (Chang, 2013)

and dependent on whether its preference coincided with the position of Germany and its

allies (Schimmelfennig, 2015: 188). Other scholars refute this intergovernmental turn in EU

legislation and argue that the Commission had great influence in setting the agenda for the

Six- and Two Pack legislation (Dinan, 2012; Menz and Smith, 2013), not least because it

tabled its legislative proposals a month before the intergovernmental task force (Bauer and

Becker, 2014; Camisão, 2015). 2. The formal voting rule constrains the winset for possible

reforms.

Essentially, the response to the Eurozone crisis has been adopted either in the form of

intergovernmental treaties among Eurozone members or as EU legislation. While the former

implies unanimity among Eurozone members, the latter requires a qualified majority in the

Council. Yet some studies question this formal unanimity-voting requirement, suggesting that

for small and crisis-ridden states, veto was not an option. Other analysts of the Eurozone

crisis have emphasized the reinforced Franco-German alliance (see for an analysis also

Degner and Leuffen, 2019), which was said to have had a crucial impact on the course of

negotiations (Dinan, 2012; Schild, 2013). While some claimed that it was the German

government that was proactive, dragging a weak and confused French leadership in its wake

(Menz and Smith, 2013: 203), others see the Franco-German relationship as more balanced

(Schild, 2013). A major compromise between the two leading governments – Germany embracing

the French demand for economic government and France agreeing to the automatic financial

sanctions desired by the Germans – is said to be at the core of the institutional solutions

found during the Eurozone crisis (Crespy and Schmidt, 2014). 3. The asymmetry of market pressures was decisive during the height of the

crisis.

During the crisis, countries such as Greece, Portugal, Spain, Italy and Ireland found it increasingly difficult to refinance their public debts and were facing an imminent threat of public default. Despite their fear of the spill-over effects of such defaults, other Eurozone economies faced no issues in borrowing money. Schimmelfennig (2015) analyzed EMU crisis bargaining as a chicken game, in which member states’ mixed motives resulted from their financial exposure to the crisis. He concludes that the breakdown of the Euro was averted by a cooperative solution, the terms of which ‘reflected German preferences predominantly’ (Schimmelfennig, 2015: 177). From the perspective of bargaining theory, the asymmetric market pressures resulted in different levels of patience (urgency) on the part of member states to strike a collective agreement. According to the Rubinstein model (1982), patience is an important source of bargaining power. Moreover, we expect market pressures to have had the greatest impact at the height of the EMU crisis (see Figure 1).

Overview of models and their relationship with the main research questions.

The relevance of asymmetric market pressures has been discussed from two perspectives. First, there are other sources of economic and financial bargaining power, most notable gross domestic product (GDP). Specifically, analysts emphasize that the unique resources of both Germany and France were their respective GDPs (Schoeller, 2017) and, correspondingly, their share of European Central Bank (ECB) capital: 27% for Germany and 21% for France (Schild, 2013). Second, other scholars argue that the power asymmetry was not actually that extreme, because the states that were not hit by public debt crises were eager to protect the unity of the Eurozone and, ultimately, the survival of the currency itself. Hence, Germany was relatively vulnerable, since it had greatly profited from the introduction of the Euro (Moravcsik, 1993), and since the German national banking system had a high level of exposure to at-risk countries (Howarth and Quaglia, 2016; Tarlea et al., 2019, Walter 2016).

Bargaining models

Individual utility function

In order to analyze the internal negotiation dynamics, we make use of decision making models that have been successfully applied to the empirical analysis of EU negotiations (Bueno de Mesquita and Stokman, 1994; Finke and Fleig, 2013; Schneider et al., 2008; Thomson et al., 2006).

All of these models assume the same spatial utility loss function:

Constraints

Some of the models explicitly account for the fact that individual or groups of member

states have the power to veto a reform proposal. Veto power depends on the formal voting

rule. In case of unanimity voting, every state has veto power. In the case of qualified

majority voting (QMV), a blocking minority of states has veto power. States will vote

against any reform proposal that is further away from their ideal position than the status

quo ante (SQ). In other words, they will reject all proposals x for which

Objective function

Finally, the models differ in how they aggregate individual utility functions to predict

the collective bargaining outcome,

Note that in the pure agenda setting model, other actors are only relevant to define the winset of the status quo Θ. Without any such constraints, this function would always lead us to predict the ideal position of the agenda setter.

In a similar vein, scholars modeling zero-sum bargaining games (‘divide the pie’) have studied different allocations of agenda setting rights (e.g. Eraslan, 2002; Merlo and Wilson, 1995; Rubinstein, 1982). Their overall conclusion is that actors who are more likely to be selected as agenda setters early on in the negotiations have an advantage in multilateral bargaining. As outlined above, the literature on the EMU crisis discusses whether the Commission has been able to set the agenda in international crisis bargaining.

Specifying the objective function is more complex in the absence of a unique agenda setter. The canonical Nash bargaining solution (NBS) (Nash, 1950) is a useful starting point for modelling multilateral bargaining. It is also firmly rooted in the literature on decision making in the EU. Achen (2006) shows that the unconstrained NBS is an approximation of the Compromise Model proposed by van den Bos (1994). The Compromise Model is simply the mean of all actors’ positions weighted by the salience they attach to the respective issue. The multidimensional extension of the Compromise Model has been termed the Position Exchange Model (Arregui et al., 2006). 2

Briefly summarized, the Nash Bargaining Model predicts that actors agree on the reform

proposal

If all actors have the same power, we can ignore

Figure 1 summarizes the six different models in the light of our three research questions. First, we distinguish between Agenda Setting (AS) models, minimizing the distance between the Commission and the outcome, and intergovernmental Nash Bargaining models (NBS), which maximize the Nash product. Second, we distinguish between those models that constrain the set of feasible outcomes to the winset to the SQ, and those without such constraints. Technically, this means that the optimization algorithm searches only within the winset (‘constrained optimization’). The unconstrained NBS minimizes the product of the utility loss functions (equation (1)). Note that the unconstrained agenda setting model always predicts the ideal position of the Commission. Third, some of the intergovernmental bargaining models assume that member states possess different levels of power. These models maximize the asymmetric Nash product.

Operationalization

Reform space

In a next step, we apply the above models to the ‘EMU Positions’ dataset (for a detailed description of the ‘EMU Positions’ data please see the introduction to this special issue) (Wasserfallen et al., 2019). Our conceptualization and operationalization of the EMU reform space is based on two insights.

First, the ‘EMU Positions’ data contains seven collective reform acts which feature 41 individual reform issues. Obviously, negotiations on issues belonging to the same package, and even negotiations concerning different reform packages, were interrelated. For example, treating negotiations over the ESM and the Fiscal Compact as independent would lead to potential logrolling over rules of fiscal discipline and the extent of transfers being missed by the study. Considering the timeline, we therefore decided to combine the data into two intergovernmental and one legislative reform package. We start with a first intergovernmental package early on in the crisis (Greek Bailout, EFSF), followed by a second intergovernmental package at the peak of the crisis (ESM, Fiscal Compact) and, finally, a legislative package that began at the height of the crisis, but persisted until the crisis was almost over (Six Pack and Two Pack).

Second, we aggregate reform issues to three theoretically defined reform dimensions. Please note that this is not a contradiction to Lehner and Wasserfallen (2019), who identify one latent conflict dimension. We also find that most member states’ positions can be ordered along a single dimension with the Netherlands and Germany at one end, and Italy and Greece at the other end. However, in order to understand multi-dimensional negotiations, it is crucial to focus on conflict and consensus (Tollison and Willett, 1979). Moreover, it is important to include the minority of states that do not align with the main dimension of conflict but may nevertheless be crucial for understanding the negotiation outcome. Specifically, we follow the literature on political economics that conceptualizes the reform space along: (a) the level of transfers as well as (b) the level of fiscal discipline (austerity) (e.g. Rodden, 2002). As a third dimension, we identify (c) the level of institutionalization. This institutional dimension is crucial for understanding the bargaining dynamics in reforming the EMU. For example, we show below that the governments’ decision to postpone institutionalization enabled high levels of transfer and austerity during the early reform packages. Yet governments were eager to establish trust in their reforms, and therefore, institutionalization became more important in the later stages of the reform process. As a result, bargaining over the extent of transfers and the degree of fiscal discipline cannot be understood without taking into account agreed institutional safeguards, monitoring and sanctioning mechanisms (Moravcsik, 1998).

Aggregating the ‘EMU Positions’ data to theoretically meaningful reform dimensions within the three reform packages bears two additional analytical advantages. As outlined above, some of our models are highly dependent on the correct specification of the winset of the status quo. Unfortunately, many individual issue dimensions deal with the specific design of a new institution (e.g. EFSF, ESM), once it has already been founded. For example, in one instance, governments negotiated the EFSF’s effective capacity. However, any outcome on that issue assumed that the EFSF would be founded in the first place; an issue captured separately in the ‘EMU Positions’ data. Consequently, identifying the location of the status quo on ‘effective capacity’ is impossible because it is dependent on the foundation of the EFSF. Finding the location of the status quo is much easier at the level of aggregated, theoretically meaningful dimensions, because we know the ex-ante degree of fiscal discipline, the ex-ante level of transfers and the ex-ante degree of overall institutionalization. 3 Moreover, the aggregation enables us to compare different reform packages over time.

We aggregate the positions in the following three steps. First, we assign individual issues to one of the three dimensions in each of the three reform packages. All dimensions (austerity, transfer, institutionalization) were negotiated in each of the three reform packages – albeit to a varying extent. We explain the assignment below, when discussing the three packages of crisis bargaining in chronological order (see the Online appendix). Second, we impute missing values by averaging the actor’s position over other issues assigned to the same dimension, as well as other actors’ positions on the same issue. This imputation does not artificially shrink the winset, nor does it systematically favor any of the models, although it will pull all bargaining models towards the center of the reform space (see König et al., 2005). Third, we average each actor’s position over all issues assigned to the same dimension. In an alternative specification, we weigh the average with the salience actors attached to each issue, yet the results remain unchanged. In order to aggregate actors’ salience to each of our three conceptual dimensions, we follow the same steps.

The resulting space is a valid operationalization of the reform dimensions discussed in the literature. However, we would like to emphasize that the following applications of the data to the bargaining models come with an unspecified error term. First, the data have a measurement error. Second, though theoretically guided, parts of our assignment of issues to reform dimensions may be disputed. We guard ourselves against these errors by (a) reporting only major patterns and (b) combining numbers with a qualitative analysis of the reform process.

Asymmetric market pressures

Following the Rubinstein (1982) model and its multilateral extensions (Chae and Yang,

1988; Merlo and Wilson, 1995; Torstensson, 2009), patience is a source of bargaining

power. The longer a negotiator can wait for an agreement, the more the counterparts have

to concede if they are more interested in a timely agreement. The argument is of intuitive

relevance to bargaining during the Eurozone crisis. Only some Euro economies experienced a

sovereign debt crisis, including Portugal, Spain, Ireland and, most severely, Greece. By

contrast, other Euro economies such as Austria, Germany and the Netherlands were primarily

concerned that the debt crisis could become a currency crisis if some of the states went

bankrupt and, consequently, defaulted on their loans. While the crisis-ridden countries

had to pay high-risk premiums to refinance their public debt, the stable Northern European

economies experienced no such costs. A valid indicator for operationalizing the severity

of a sovereign debt crisis is the interest rate on government bonds, which indicates the

governments’ costs of refinancing their debt (see Ioannou et al., 2015). Thus, we use the

interests on 10-year monthly averaged governmental bonds as recorded by the ECB (see Figure 2).

4

Specifically,

Interest of 10-year governmental bonds between 2010 and 2015.

Model implementation

All models were implemented in Matlab version 2017b using the Global Optimization Toolbox. In the following section, we present our empirical analysis in terms of the three reform packages introduced above. Each of the three sections starts with a short description of the reform space followed by a description and discussion of the model predictions. Finally, we discuss the robustness of our approach by comparing it to a case-wise application of the formal models at the level of the original issue dimensions of the ‘EMU Positions’ dataset.

Empirical analysis

Package 1: First bailout of Greece and the EFSF

Reform space

In May 2010, the Council agreed on the EFSF and governments adopted the First Economic Adjustment Programme for Greece. The previous months were characterized by intense negotiations among the governments of the Eurozone. Simultaneously, the interest rates on 10-year government bonds began to diverge (see Figure 2).

These early rounds of reform negotiations placed an emphasis on transfer payments. Specifically, the ‘EMU Positions’ dataset contains information on the governments’ initial willingness to bail out Greece (G1), 5 on their willingness to relieve the Greek debt (G4) and on governments’ readiness to participate in the loan guarantees for the EFSF (EFSF1). Moreover, the data contain information on actors’ positions with regard to the EFSF’s effective capacity (EFSF2), and whether or not it should obtain a banking license (EFSF4).

The negotiations at this stage referred to a lesser extent to the issue of institutionalization. However, the dataset contains information on whether governments favored the establishment of a systemic crisis management framework or leaned towards an ad hoc combination of existing instruments requiring limited legal changes and institution-building (G2). Finally, the data contain no direct question regarding fiscal discipline preferences. However, for both packages we asked experts to indicate actors’ positions on the involvement of the International Monetary Fund (IMF) (G3, EFSF3). From the outset, all parties were aware that involving the IMF would imply rigorous austerity measures. 6 Although there may have been other motivations for or against involving the IMF, we consider it a valid proxy for governments’ diverging preferences on fiscal discipline requirements.

Results

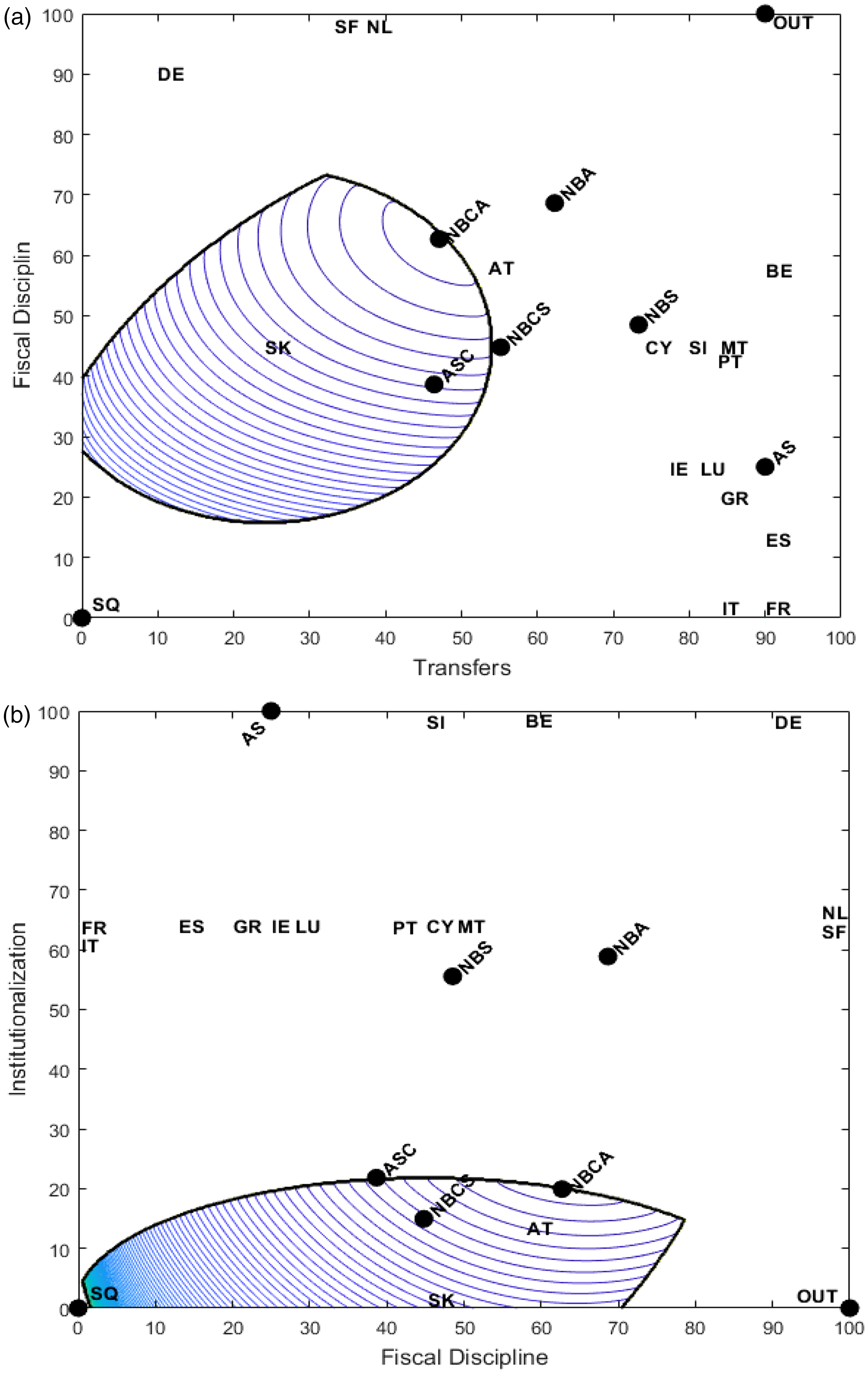

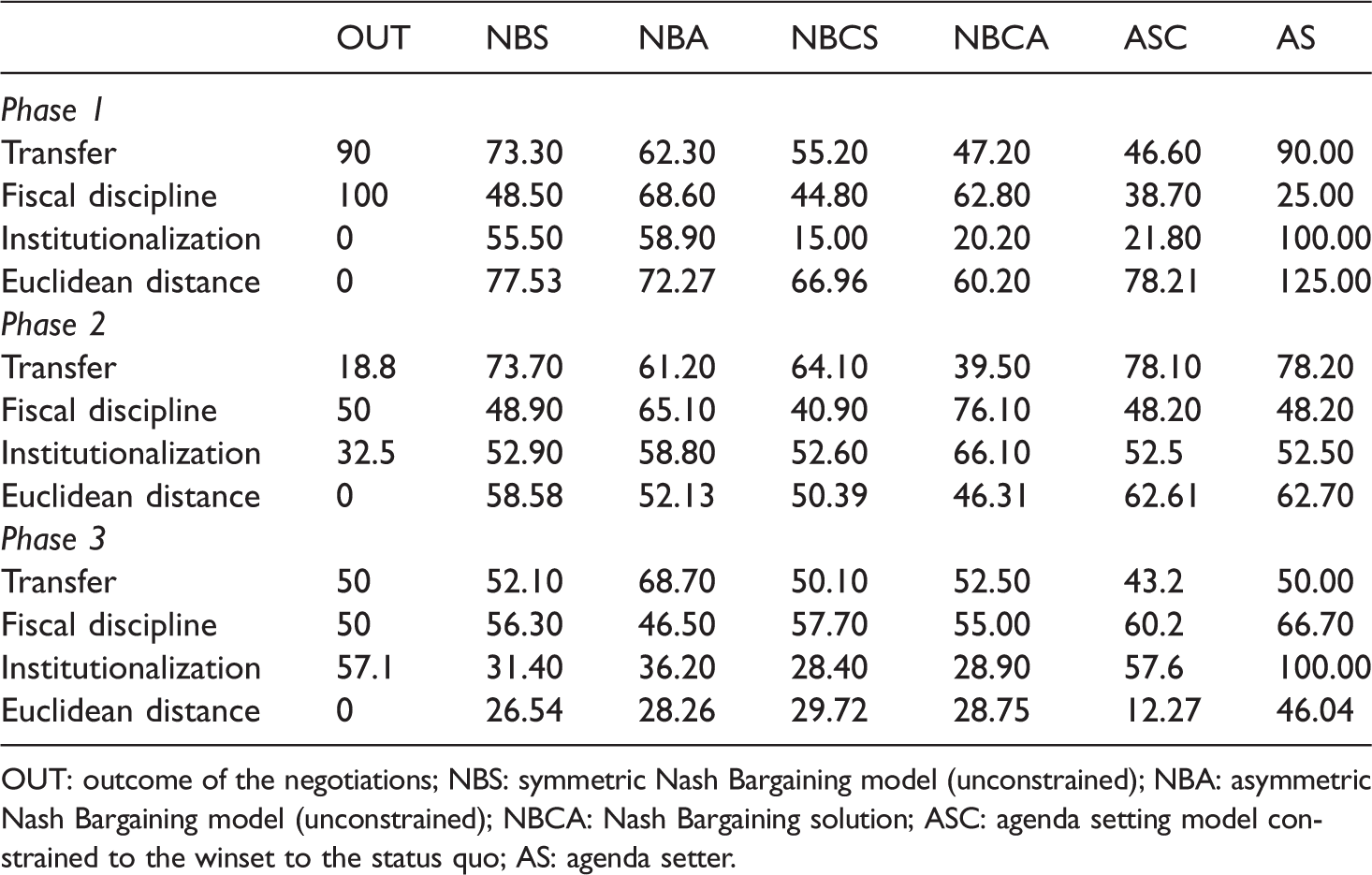

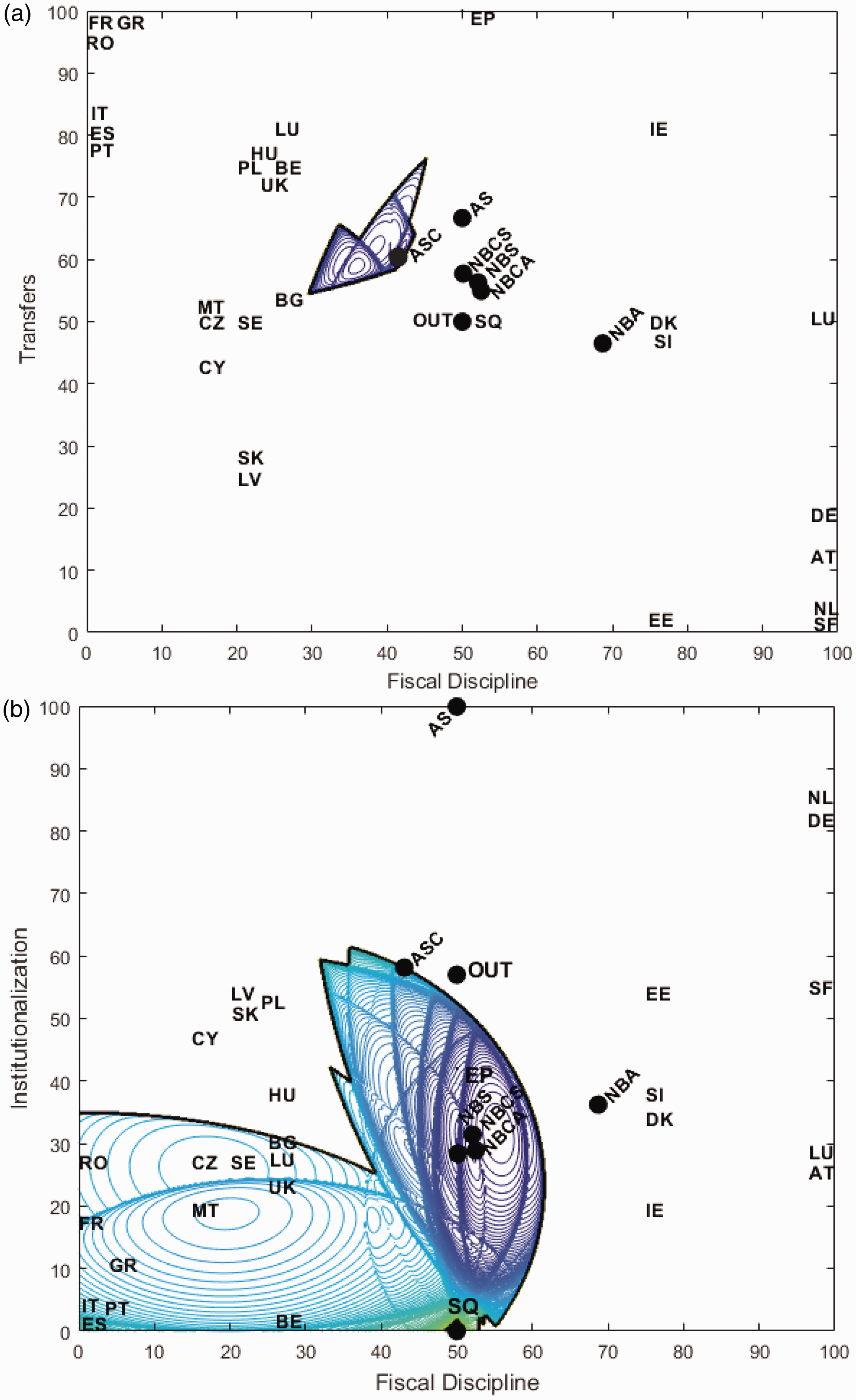

Table 1 lists the Euclidean distances from the predicted outcome to the actual outcome of the different bargaining models. This allows a comparison between the various models and an interpretation regarding which bargaining model provides the closest prediction of the bargaining outcome. Figure 3 represents two-dimensional projections of the negotiation space. These compact figures depict information contained in the ‘EMU Positions’ data, as well as information resulting from our application of the bargaining models. First, they locate member states’ ideal positions in the aggregated reform space. Second, they depict the status quo ante, as well as the outcome of the negotiations (OUT). Third, they show the point predictions of the six different models introduced above and summarized in Figure 1 (NBS, NBCA, ASC, etc.). Fourth, they depict the unanimity winset to the status quo, i.e. the set of positions all members of the Eurozone preferred to the status quo ante (the shape delimited by a black line). Finally, the contour lines within the winset illustrate the Nash Bargaining product. Please note that the reform space is three-dimensional and, therefore, the winset is also a three-dimensional object. In order to project it in two dimensions, we had to slice it at a chosen value on the third dimension. Figure 3 depicts the resulting cross-section. Here, we have chosen to ‘slice’ (or ‘evaluate’) the winset and the Nash product at the value predicted by the constrained, asymmetric Nash Bargaining solution (NBCA) on the third dimension. 7

Winset and model predictions for reform package 1 (two-dimensional projections evaluated at the prediction of the asymmetric, constrained Nash solution on dimension 3, NBCA).

Model predictions and Euclidean distances to the outcome.

OUT: outcome of the negotiations; NBS: symmetric Nash Bargaining model (unconstrained); NBA: asymmetric Nash Bargaining model (unconstrained); NBCA: Nash Bargaining solution; ASC: agenda setting model constrained to the winset to the status quo; AS: agenda setter.

Figure 3(a) depicts the Transfers-Fiscal discipline projection. The x-axis ‘Transfers’ contains all negotiation issues in the first bargaining round which dealt with transfer questions. Similarly, the y-axis displays all issues dealing with fiscal discipline questions in that first reform package. Governments’ positions cluster in two camps, with Germany (DE), the Netherlands (NL) and Finland (SF) demanding high discipline in combination with low transfers, and France (FR), Spain (ES) and Italy (IT) holding the diametrically opposite position, that is, low discipline in combination with high transfers. The position of these two groups of countries in the negotiation space corresponds to the single latent conflict dimensions identified by Lehner and Wasserfallen (2019). The third dimension, depicted in Figure 3(b), captures the level of institutionalization. Here, Germany (DE), Belgium (BE) and Slovenia (SI), as well as the Commission (AS), demanded the most far-reaching and systematic institutionalization. While a majority of the other governments also favored institutionalization, Austria (AT) and Slovakia (SK) (which refused to participate in the Greek bailout program) opposed any institutional reforms.

No single actor preferred high transfers in combination with rigorous fiscal discipline and very limited institutionalization. The bargaining outcome makes more sense when we link all three issues: both the austerity camp around Germany (DE), and the transfers camp around France (FR) preferred very high levels of institutionalization. Yet they soon discovered that far-reaching institutional reforms were not feasible – at least not at the swift pace the economic situation demanded. Consequently, France (FR), Germany (DE) and other states gave up on institutionalization, which made it possible to agree on transfers under the condition of strict fiscal discipline – yet only on an ad hoc, temporary basis.

What can we learn from the models?

First, given the temporary nature of the outcome regarding institutionalization, the Commission does not appear to have been successful at all (Hodson, 2013; Puetter, 2012). Thus, the two agenda setting models (AS, ASC) consistently feature the largest distance to the outcome. The different predictive accuracy of the remaining models is insightful. On the institutional dimension, the Slovakian (SK) and Austrian (AT) governments define the boundaries of the winset with their extreme positions. Both governments did not want to promote EU institutionalization further. As a result, we find that those models which consider the applicable voting rules (ASC, NBCS, NBCA) correctly predict low levels of institutionalization (Figure 3(b). By contrast, the two unconstrained Nash Bargaining models (NBA, NBS) provide better prediction of the actual high levels of transfer and fiscal discipline which were agreed upon in the negotiations. Overall, the constrained, asymmetric Nash Bargaining solution correctly highlights two factors of importance for understanding the negotiation outcomes. It respects the Austrian (AT) and Slovakian (SK) aversion to institutionalization, as well as the slightly higher bargaining power of the Northern European countries grouped around Germany (DE), which were not subject to financial market pressures.

In sum, the first phase of EMU reforms resulted in far-reaching transfers in return for IMF involvement as guarantor of fiscal discipline. The deal was the consequence of governments postponing any plans for institutionalization, a political compromise reached in the face of the economic urgency of the situation. The veto power of Austria and Slovakia, and the resulting unanimity winset was particularly relevant for understanding the lack of institutionalization. Asymmetric market pressures favoring financially stable Germany and the Netherlands on the one side, and France on the other, are particularly relevant for understanding the compromise outcome of high levels of transfer and fiscal discipline. Agenda setting power, i.e. the Commission, was irrelevant at this stage.

Package 2: ESM and fiscal compact

Reform space

At the next stage of the negotiations, the aim was to calm the markets and prevent a future debt crisis by reforming the EMU rules. The ESM established a permanent bailout regime that could rescue Eurozone members in the event of a future public debt crisis. The Fiscal Compact focused on ensuring fiscal discipline by all Eurozone members to prevent any public debt crisis. The two treaties were negotiated as one package with only member states that signed the Fiscal Compact being eligible to access ESM funds. Importantly, during negotiations over the ESM and the Fiscal Compact, the asymmetric market pressure among member states reached its peak (see Figure 2).

With regard to the ESM, some member governments preferred to match the effective lending capacity of the temporary EFSF, while others argued in favor of a substantively larger lending capacity (ESM2). Moreover, only some wanted to involve the private sector in future public debt-restructuring programs (ESM4). Finally, governments negotiated whether the ESM should be granted a bank license and be allowed to issue bonds (ESM6), as well as whether it should have access to additional financial resources such as fines collected under the Stability and Growth Pact (SGP) (ESM6).

With regard to fiscal discipline, the ESM negotiations centered on the crucial issue of conditionality. Ultimately, governments agreed on full conditionality, i.e. that the ‘granting of financial assistance under the mechanism [the ESM] will be made subject to strict conditionality’ (Art. 136.3) (ESM3). Some member governments, most notably France, argued for a broadening of the focus of the Fiscal Compact beyond fiscal stability and discipline, also including objectives such as the generation of growth and jobs (FC7).

At this stage, the negotiations focused especially on institutionalization. There was a debate about incorporating the ESM and the Fiscal Compact into the EU treaty framework (ESM1, FC1, FC2, FC9). Some opposed, whereas others favored some coordination between the ESM and the EU institutions responsible for SGP enforcement, and yet others were open to integrating the ESM into the supra-nationalized SGP enforcement (ESM7, FC4, FC5).

Results

Figure 4 provides the same kind of information as Figure 3. We start the analysis with the transfers-fiscal discipline projection (Figure 4(a)). As previously, we sliced the three-dimensional winset at the level of institutionalization predicted by the constrained asymmetric Nash Bargaining model (NBAC). With respect to the reform positions, we still observe a cleavage between Germany (DE), Austria (AT) and the Netherlands (NL) (high discipline, low transfers), and France (FR), Spain (ES) and Portugal (PT) (low discipline, high transfers). However, in the ‘French’ camp, crisis-ridden governments such as Italy (IT) and Greece (GR) were now more open to fiscal discipline – not least to reinstall market trust in their planned consolidation. The location of the outcome in Figure 4(a) shows a clear victory for Germany (DE), the Netherlands (NL), Austria (AT) and Sweden (SV) on the transfer dimension, while on the discipline dimension the outcome was a compromise between the two extreme positions.

Winset and model predictions for reform package 2 (two-dimensional projections evaluated at the prediction of the asymmetric, constrained Nash solution on dimension 3, NBCA).

With respect to institutionalization, Germany’s position to establish far-reaching, legally guaranteed monitoring and sanction mechanisms came closest to the extreme position. Interestingly, the Commission (AS), as well as France (FR), Belgium (BE) and Spain (ES) were less enthusiastic about institutionalization as a vehicle to enforce conditionality.

What can we learn from the models?

The outcome is a compromise at a low common denominator. The camp not subject to financial pressure situated around Germany (DE) was very successful in prohibiting high transfer payments and obtained some concessions with regard to institutionalization, in particular the conditionality guarantee in Art. 163 ESM. This is reflected in the superior performance of the asymmetric Nash Bargaining models (NBCA, NBA) which explicitly accounts for asymmetric market pressures (see also Table 1). Note that the constraints set by the unanimity winset are irrelevant in this case, and therefore the two asymmetric Nash Bargaining solutions are identical. Again, the agenda setting models (AS, ASC) deliver the worst predictions in terms of distance to the real-world outcome. This corresponds to the logic of intergovernmental treaty negotiations where there is no place for agenda setting by the Commission, such as in the OLP.

Overall, we correctly expected the success of the financially stable and unpressured Northern governments on the transfer dimension. By contrast, veto power played a limited role at this stage because the three-dimensional winset of the status quo was very large. As a result, the winset had no effect on the prediction of the asymmetric Nash Bargaining solution (NBCA = NBA). Thus, despite their higher financial stability and patience, the states in the ‘German’ camp did not obtain their desired institutional capacities to monitor and sanction fiscal indiscipline. Finally, our analysis of the second stage of intergovernmental reform negotiations does not point to any kind of supranational agenda setting power.

Package 3: Legislative bargaining

Reform space

In September 2010, the EC tabled a package of five regulations and one directive (aka ‘Six Pack’) to reform the SGP, and to introduce greater macro-economic surveillance. Simultaneously, the Commission proposed a package of two additional regulations (‘Two Pack’) to strengthen the coordination and surveillance of budgetary processes within the Eurozone. This package was not adopted until March 2013. The Two Pack was prepared during the negotiations over the Six Pack. All legislative proposals were negotiated and adopted under the OLP, which requires QMV in the Council of Ministers and co-decision by the EP.

Both packages had a distinct focus on institutionalizing future monitoring and sanctioning procedures. Nevertheless, some elements also touched on transfers and fiscal discipline. With regard to transfers (see Figure 5(a), the EP strove to secure a formal commitment to a redemption fund that would mutualize some member governments’ debts (TP1). However, all it obtained in the negotiations was an expert group evaluating the possibility of such a fund. Moreover, governments negotiated over the question whether EU funds should be withheld from deficit countries (SP2). Note that this proposal would have moved the outcome (OUT) towards lower levels of transfer. However, the status quo prevailed.

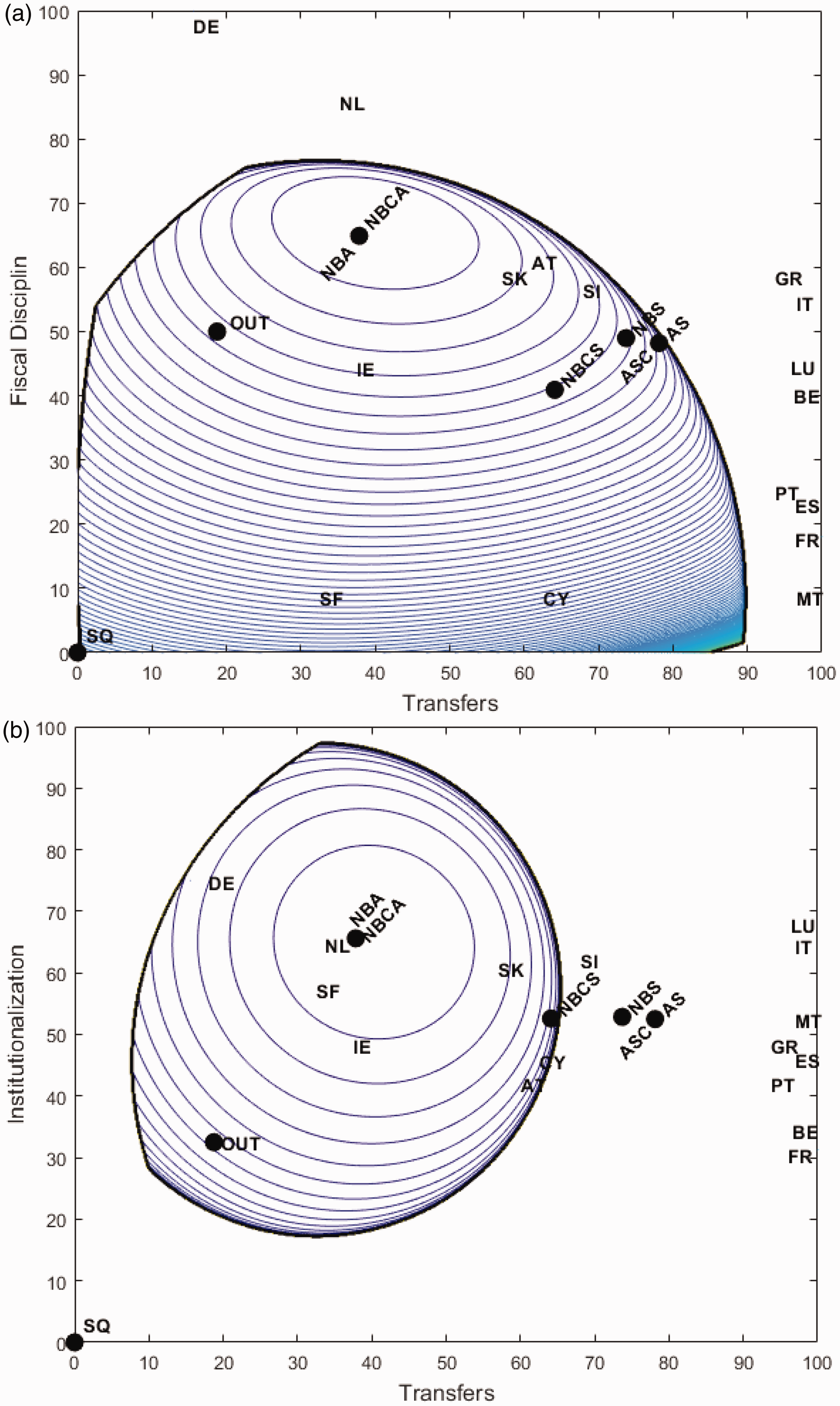

Winset and model predictions for reform package 3 (two-dimensional projections evaluated at the prediction of the constrained Agenda Model on level 3, ASC).

With regard to fiscal discipline, some governments pointed out that debt increases brought about by the implementation of structural reforms or investments in public goods should not be fully included in the macro-economic imbalance calculation, in order to provide fiscal space for desirable reforms (SP5). Note that this proposal would have moved the status quo towards less discipline. In a similar vein, there was a debate on whether the macro-economic imbalance procedure should be symmetrically applied to surpluses and deficits (SP6). None of these reform proposals were adopted however, hence, the status quo prevailed.

In terms of institutionalization, the member states and the EP negotiated whether sanctioning in the event of non-compliance with the SGP should include suspension of Council voting rights (SP1). Furthermore, they discussed whether sanctions should be at the discretion of the Commission unless blocked by a qualified majority in the Council (SP3). In the Two Pack, they deliberated on whether the Commission should be given a role in pre-approving national budgets (TP2), and whether national fiscal councils should be established to provide independent macro-economic forecasts as basis for monitoring (TP3).

Results

Figure 5 is adapted to match the formal rules governing legislative bargaining in the EU. The black line delimits the set of positions a qualified majority of member states and the EP would have preferred to the status quo ante. Within that space, the contour lines illustrate the asymmetric Nash product. Given the applicable qualified majority rule, legislative bargaining is characterized by a multitude of possible winning coalitions. Therefore, the shape of the winset and the Nash product become significantly more complex. Finally, the figures locate the point predictions of all six models introduced above (see Figure 1).

In legislative bargaining, the Commission should enjoy significant agenda setting power. In order to explore that power, we chose to slice the three-dimensional reform space at the level predicted by the constrained agenda setting model (ASC) on dimension 3.

As before, we start the analysis with the transfers-fiscal discipline projection (Figure 5(a)). In contrast to reform stages 1 and 2, the status quo is located in the center of the reform space. Around the status quo, we observe a similar pattern of conflict as before, albeit now including all 28 EU member states. In the ‘low transfer-high discipline’ corner, we find Austria (AT), Germany (DE), Sweden (SV) and the Netherlands (NL). At the other end of the continuum, we find France (FR), Greece (GR), Spain (ES) and Italy (IT). Yet some of the member states are also located outside this main conflict line, such as Ireland (IE), which demands fairly high discipline and transfers. The Commission, as agenda setter (AS), was close to the status quo, whereas the Parliament was unwilling to change the fiscal discipline rules, but preferred higher transfers.

The crucial dimension in the legislative bargaining game concerns the reform of monitoring and sanctioning procedures, that is, institutionalization (Figure 5(b)). On this dimension, the Commission (AS) now sought full-scale empowerment as the agent responsible for monitoring and sanctioning national budgets. By contrast, the Parliament was more skeptical with regard to institutionalization. Concerning the member states, Germany (DE) and the Netherlands (NL) were most in favor of institutionalization, while the majority of member states favored a limited increase in this. Notable exceptions were Belgium (BE), Spain (ES), Italy (IT) and Portugal (PT), who preferred the status quo, but did not command a blocking minority under the QMV voting rules.

What can we learn from the models?

Because of the centrally located SQ, the winset in the two-dimensional ‘transfer-fiscal discipline’ space would be empty. However, a qualified majority of member states preferred an increased level of institutionalization, thereby opening the winset for reforms on all three reform dimensions (Tollison and Willett, 1979). Nevertheless, the outcome neither contained substantive reforms of the level of transfers nor of the required fiscal discipline. Why?

The results in Figure 5 illustrate that the Commission (AS) acted as a powerful agenda setter, but it was satisfied with the level of transfers and fiscal discipline under the status quo. It’s primary concern was in increasing the level of institutionalization. The projection in Figure 5(a) depicts the transfers and fiscal discipline dimension at the level of institutionalization predicted by the constrained agenda setting model (ASC). Since the Commission preferred maximal institutionalization, the ASC predicts an outcome at the fringes of the winset. The opposite holds when slicing the winset lengthways, revealing that the Commission enjoyed significant discretion to push for a high level of institutionalization.

Our results confirm the Commission’ strong agenda setting role in EU legislative bargaining. Specifically, the constrained agenda setting model (ASC) perfectly predicts the outcome on the institutional dimension, where the outcome is located right at the fringes of the QMV winset. The ASC predictions are also very close to the outcome on the other two dimensions.

The constrained Nash Bargaining models (NBCS, NBCA) are clustered closely together in the center of the space. By contrast, the unconstrained, asymmetric Nash Bargaining model (NBA), predicts an edge for the northern states, despite the slow convergence in interest rates on governmental bonds since autumn 2012. This failure of the asymmetric Nash Bargaining model illustrates that asymmetric market pressures were not particularly relevant when it came to negotiating the Two Pack and Six Pack legislation. All of the three bargaining models underpredict the level of institutional reforms, because they fail to consider the agenda setting power of the EC.

In the Online appendix, we offer a more detailed model comparison and robustness tests.

Conclusion

The ‘EMU Positions’ data enable us to analyze the relevance of agenda setting, formal voting rights and economic power in EU crisis bargaining. Specifically, we apply the dataset to established bargaining models. In short, our case studies emphasize the importance of formal rules as well as the relevance of asymmetric market pressures during the Euro crisis.

More specifically, we find that the Commission was a very powerful agenda-setter in the legislative bargaining over the Six Pack, the Two Pack and the Banking Union. By contrast, we find the Commission to be irrelevant for explaining the outcome of international treaty negotiations such as the Greece Assistance Package, the EFSF, the ESM and the Fiscal Compact. This result not only confirms a major theoretical argument in the literature on EU politics, but also corroborates those qualitative studies that find a limited role of the Commission during the EMU reforms (Dinan, 2012; Menz and Smith, 2013). By contrast, our finding refutes accounts arguing either that the Commission was influential in intergovernmental negotiations, or that legislative crisis bargaining followed the logic of the Union Method rather than that of the Community Method (Chang, 2013).

Moreover, our results clearly emphasize the relevance of formal voting rules and the resulting veto power. This holds for the QMV rules as well as for the implied unanimity among Eurozone members when adopting international treaties. The latter is only ‘implied’, because not every small member state has to participate to make an international treaty effective. However, our results indicate that smaller member states were important: some of them, for example Austria and Slovakia in the first phase, effectively constrained the winset.

Finally, we find that modelling asymmetric market pressures is key to understanding the strict fiscal discipline agreed during the height of the crisis. This highlights how important package deals over different issue dimensions are for our understanding of the EMU reforms, especially with regard to the Franco-German axis (Degner and Leuffen, 2019). The two largest financially stable member states represent the two coalitions that span the main conflict dimension. France shielded many of the crisis-ridden countries against more severe austerity requirements. Hence, Germany, the Netherlands, and Austria had to overcome France (protecting Greece, Spain, Portugal and Italy) to strike a deal. In the end, what appeared to be an effective and dynamic Franco-German tandem is an almost inevitable result of asymmetric market pressures in combination with reform interests.

Supplemental Material

Replicationfiles FinkeBailer - Supplemental material for Crisis bargaining in the European Union: Formal rules or market pressure?

Supplemental material, Replicationfiles FinkeBailer for Crisis bargaining in the European Union: Formal rules or market pressure? by Daniel Finke and Stefanie Bailer in European Union Politics

Supplemental Material

Supplemental material for Crisis bargaining in the European Union: Formal rules or market pressure?

Supplemental Material for Crisis bargaining in the European Union: Formal rules or market pressure? by Daniel Finke and Stefanie Bailer in European Union Politics

Footnotes

Acknowledgement

We thank Piers Lawrence for his excellent work in implementing the models.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We gratefully acknowledge funding from the European Union’s Horizon 2020 research and innovation programme for the project EMU_Choices under grant agreement No. 649532.

Supplemental Material

The supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.