Abstract

To advance understanding of the reasons for informal sector entrepreneurship, this article evaluates the determinants of cross-country variations in the extent to which enterprises are unregistered when they start operating. Reporting the World Bank Enterprise Survey data on 67,515 enterprises across 142 countries, the finding is that one in five (19.9%) of the formal enterprises surveyed started-up unregistered, although this varies from all enterprises surveyed in some countries (e.g. Pakistan) to 1% of surveyed enterprises in Slovakia. To explain these cross-country variations, four competing theories are evaluated which variously assert that nonregistration is determined by either: economic under-development and poorer quality governance (modernization theory); too much state interference (neoliberal theory); too little state intervention (political economy theory); or an incongruence between the laws and rules of formal institutions and the beliefs, values, and norms of informal institutions (institutional theory). A multilevel probit regression analysis confirms the modernization, political economy, and institutional theories but not neoliberal theory. Beyond economic under-development, therefore, nonregistration is associated with too little state intervention and the rules of formal institutions being incongruent with the socially shared beliefs of entrepreneurs. The article concludes by discussing the theoretical and policy implications of these findings.

Keywords

Introduction

Over the past decade or so, a growing literature has begun to study entrepreneurs who start-up their business ventures on an unregistered basis (Perry and Maloney, 2007; Thai and Turkina, 2014; Williams et al., 2017). This scholarship has revealed that informal sector entrepreneurship, defined here as starting-up a venture on an unregistered basis, is not some minor feature existing in a few peripheral enclaves of the global economy. Rather, some two-thirds of all enterprises are estimated to start-up unregistered (Autio and Fu, 2015), and at least half of all enterprises globally are unregistered (Acs et al., 2013). The indications nevertheless are that significant cross-country variations exist in the extent to which enterprises start-up unregistered (Dau and Cuervo-Cazurra, 2014; Thai and Turkina, 2014; Williams, 2014b).

Why, therefore, are enterprises more likely to start-up unregistered in some countries than others? To answer this, the aim of this article is to evaluate determinants of cross-country variations in the extent of nonregistration at start-up. These determinants are derived from four competing theoretical perspectives. Firstly, modernization theory asserts that nonregistration is greater where there is economic under-development and a lack of modern governance (La Porta and Schleifer, 2008, 2014), Secondly, neoliberal theory argues that the level of nonregistration is greater where there is too much state interference (De Soto, 2001). Thirdly, and conversely, political economy theory views new venture nonregistration as higher when there is too little state intervention (Castells and Portes, 1989), and fourthly and finally, institutional theory views registration at start-up as lower the laws and regulations of formal institutions are incongruent with the norms, values, and beliefs of informal institutions (Webb et al., 2009, 2013, 2014; Williams, 2018).

The intention is to advance the understanding of informal sector entrepreneurship in three ways. Theoretically, by evaluating the determinants of cross-country variations in the extent to which enterprises start-up unregistered, the intention is to reveal that these are not mutually exclusive theories but, rather, are necessary but insufficient perspectives that can be synthesized to produce a more holistic explanation. Empirically, meanwhile, this article provides a first multilevel regression analysis of the firm- and country-level determinants of the varying extent to which enterprises start-up unregistered. Third and finally, and from a policy perspective, this article reveals the need for a different policy approach toward nonregistration at start-up than is currently used.

To commence, therefore, the next section provides a theoretical framing by reviewing what is known about cross-country variations in the level of nonregistration of business start-ups and the various competing theories that seek to explain these cross-country variations. The outcome will be a set of hypotheses that can be tested. The third section then reports the data, variables, and methods used to test these hypotheses, namely a multilevel probit regression analysis of the 67,515 enterprises interviewed in the World Bank Enterprise Survey (WBES) across 142 countries between 2006 and 2014. The fourth section then reports the findings regarding the validity of the various theorizations, followed in the fifth and final section by a discussion of the theoretical and policy implications along with the limitations of the study and the future research required.

Cross-country variations in business nonregistration at start-up: Competing theories

Recent years have seen the emergence of a burgeoning literature on informal sector entrepreneurship (Bureau and Fendt, 2011; Ram et al., 2017; Webb et al., 2009, 2013; Williams, 2008, 2018). Although informal sector entrepreneurship can be widely defined as starting-up and/or owning and managing a business venture which does not register with and/or declare some or all of its production and/or sales to the authorities for tax, benefit, and/or labour law purposes when it should do so (Williams et al., 2017), this article reflects much current scholarship by confining analysis to those starting-up a venture on an unregistered basis (Ketchen et al., 2014; Siqueira et al., 2016; Thai and Turkina, 2014). This scholarship has until now sought to understand not only the socioeconomic characteristics of the entrepreneurs and firm types that start-up unregistered (Thai and Turkina, 2014; Williams and Martinez-Perez, 2014) and whether their motives are necessity driven and/or opportunity driven (Maloney, 2004; Perry and Maloney, 2007) but also the extent to which enterprises start-up unregistered (Autio and Fu, 2015; Dau and Cuervo-Cazurra, 2014; Siqueira et al., 2016). Firstly, therefore, the literature is here reviewed on the level of nonregistration at start-up and, secondly, the previous literature seeking to explain the cross-country variations in the level of registration at start-up.

Prevalence of starting-up unregistered

Numerous studies have evaluated in individual countries the extent to which businesses are registered when they commence operations (e.g. Godfrey and Dyer, 2015; London et al., 2014; Williams and Martinez-Perez, 2014; Williams et al., 2016; Yu and Bruton, 2015). However, a more limited number have evaluated cross-country variations in the extent to which enterprises start-up unregistered.

Using the Global Entrepreneurship Monitor (GEM) data on 51 countries, Dau and Cuervo-Cazurra (2014) find that 3.37 informal enterprises are created annually for every 100 people, while Autio and Fu (2015), also using the GEM data and a similar measure, find that two-thirds of enterprises start-up unregistered. Moreover, this proportion is the same in Organization for Economic Cooperation and Development (OECD) countries (where 0.62 informal enterprises compared with 0.43 formal enterprises are annually created for every 100 people) as in emerging and transition economies (where 0.62 informal enterprises compared with 0.37 formal enterprises are created annually for every 100 people). To derive these GEM estimates, both studies subtract World Bank estimates of the number of registered businesses from the GEM estimates of the total number of new enterprises in each country to produce these figures on the proportion of unregistered start-ups. This, however, can be only a very tentative estimate.

One of the few other sources of cross-country data on this issue is the WBES, which collects data on whether formal businesses started-up unregistered and whether they compete with the informal sector. Although this WBES data set has been used to analyse the impacts of starting-up unregistered on future firm performance (Williams et al., 2017) and whether formal enterprises compete with the informal sector (e.g. Hudson et al., 2012), it has not been used until now to analyse cross-country variations in the extent to which formal enterprises start-up unregistered and/or the reasons for the cross-country variations. To begin to address this, therefore, the different explanations for the cross-country variations in the level of registration at start-up are reviewed in this study so that hypotheses can be formulated which can be tested.

Theorizing cross-country variations in the level of registration at start-up

To identify explanations for cross-country variations in the scale of business nonregistration at start-up, the wider literature explaining cross-country variations in the scale of the informal sector can be drawn upon (Williams, 2014a; Williams and Martinez-Perez, 2014). On this wider topic, four competing theoretical perspectives exist which argue that the level of informality is determined by economic under-development and poorer quality governance (modernization theory), too much state interference (neoliberal theory), too little state intervention (political economy theory), or an incongruence between the laws and rules of formal institutions and the beliefs, values, and norms of informal institutions (institutional theory).

Until now, most studies have adopted the singular logic of one or other of these theories. For example, La Porta and Shleifer (2008, 2014) use modernization theory, De Soto (1989) adopts neoliberal theory, Castells and Portes (1989) and Slavnic (2010) use the logic of political economy theory, and Webb et al. (2009) use institutional theory. However, recent studies have questioned whether these theories are mutually exclusive. Analysing bivariate correlations of the relationship between the scale of the informal sector and the determinants in each theory, across the European Union (Williams, 2014a), Central and Eastern Europe (Williams, 2015a), Latin America (Williams and Youssef, 2013), and the wider developing world (Williams, 2015b), the modernization, political economy, and institutional theories have been confirmed but not neoliberal theory. This is also the case in multivariate analyses of the scale of the informal sector across Central and Eastern Europe (Williams and Horodnic, 2015a) and Southeast Europe (Williams and Horodnic, 2015b).

When studies have tested these theories as explanations for cross-country variations in the prevalence of informal entrepreneurship using simple bivariate correlations, the same finding is identified (Williams, 2014b,c). However, there have been few multivariate regression analyses testing these theories as explanations for cross-country variations in informal entrepreneurship and those conducted are narrow in scope. One evaluation examines whether these theories explain cross-country variations in informal entrepreneurship by the extent to which small business owners under-report the wages of their employees in the 28 countries of the European Union (Williams and Horodnic, 2016) and another the extent to which the self-employed in European Union countries conduct some of their transactions off-the-books (Williams and Martinez-Perez, 2014). Both studies confirm the validity of the modernization, political economy, and institutional perspectives but not neoliberal theory.

Until now, however, there have been no evaluations of these theories for explaining cross-country variations in the extent to which businesses start-up unregistered. To fill this gap, each theoretical perspective is here reviewed in turn to formulate hypotheses which can be tested.

Modernization theory, which dominated the study of informality during the 20th century, asserts that the modern formal sector is extensive and growing, while the informal sector is disappearing. Informal entrepreneurs, such as street vendors, are thus portrayed as a residue of a premodern production system. Their presence in a country is a sign of the ‘under-development’ of its economy and a lack of modernization of its system of governance (Geertz, 1963; Lewis, 1959). When explaining the cross-country variations in the proportion of businesses unregistered at start-up, therefore, it can be suggested that this will be higher in less economically developed countries, measured in terms of gross domestic product (GDP) per capita, and in countries with less modern state bureaucracies, measured by the pervasiveness of public sector corruption (Tonoyan et al., 2010). The following hypothesis can be therefore tested:

For neoliberal theory, meanwhile, too much state interference in the free market leads entrepreneurs to make a rational economic decision to exit the formal sector due to time, costs, and efforts of conforming to the bureaucratic burdens imposed on enterprises (e.g. De Soto, 1989, 2001; London and Hart, 2004). For neoliberal theory, nonregistration is thus a rational economic decision of entrepreneurs who confront burdensome laws and regulations by a stifling state bureaucracy (Becker, 2004; Perry and Maloney, 2007). Nonregistration is a result of over-regulation, high taxes, and too much state interference, and the solutions are deregulation, tax reductions, and minimal state interference. The level of nonregistration at start-up will be more prevalent in countries with higher tax levels and greater state interference. To explore the validity of this neoliberal theory, the following hypothesis can be tested:

For political economy theory, conversely, nonregistration at start-up is an outcome of a deregulated open-world economy, where outsourcing and subcontracting to informal enterprises have become a principle means of reducing costs in contemporary capitalism (Aliyev, 2015; Meagher, 2010). From this perspective, enterprises operating unregistered reflect the shift towards unregulated production and the advent of precarious low-paid survival-driven endeavor for those excluded from the formal economy (Castells and Portes, 1989; Dibben et al., 2015). Unregistered enterprises and informal entrepreneurship are the outcome of too little state intervention in not only the economy but also social protection and social transfer systems. The level of nonregistration at start-up is viewed as more prevalent in countries with too little state intervention to protect workers and citizens (Davis, 2006; Gallin, 2001; Slavnic, 2010). To evaluate this, the following hypothesis can be tested:

For institutional theorists, a problem with all the above theories is that they do not explain why some entrepreneurs’ start-up unregistered in a country and others do not; they do not take agency into account. Institutional theory, however, has started to overcome this problem (Baumol and Blinder, 2008; Denzau and North, 1994; North, 1990). In this perspective, institutions are the rules of the game which govern and prescribe behavior, and all societies have both formal institutions (i.e. laws and regulations) that are the legal rules of the game and informal institutions which are socially shared norms, values, and beliefs about what is right and acceptable (Denzau and North, 1994; Helmke and Levitsky, 2004). Formal entrepreneurship is thus endeavor conforming to formal institutional prescriptions (i.e. the laws and regulations), informal entrepreneurship sits outside the formal rules of the game but within the norms, values, and beliefs of informal institutions (Kistruck et al., 2015; Siqueira et al., 2016; Webb et al., 2009; Welter et al., 2015; Williams and Vorley, 2015), while criminal entrepreneurship sits outside both formal and informal rules of the game (Bunei et al., 2016; McElwee and Smith, 2014; Smith and McElwee, 2015; Smith et al., 2017). Viewed through this institutionalist lens, cross-country variations in the level of nonregistration at start-up result from the incongruence between the laws and regulations of formal institutions and the values, beliefs and norms of informal institutions (Godfrey, 2015; Kistruck et al., 2015; Siqueira et al., 2016; Sutter et al., 2017; Vu, 2014; Webb and Ireland, 2015; Webb et al., 2013, 2014; Williams et al., 2017). The belief is that the greater the degree of incongruence, the higher is the level of nonregistration at start-up (Williams and Shahid, 2016). To evaluate this institutional theory, therefore, the following hypothesis can be tested:

Data, variables, and methods

Data

To test these determinants of cross-country variations in the extent to which enterprises start-up unregistered, the WBES data collected from 67,515 enterprises across 142 countries between 2006 and 2014 are analysed, including 15 developed countries and 127 developing countries (of which 41 are in Africa, 31 in Latin America and Caribbean, 29 in Europe and Central Asia, 13 in East Asia and the Pacific region, 7 in the Middle East and North Africa, and 6 in South Asia). Of the countries covered in this survey are 20 high-income, 4 upper middle-income, 36 middle-income, 42 lower middle-income and 25 low-income countries. All global regions and economic development levels are therefore covered.

To collect data in each country, the WBES uses a stratified random sample of non-agricultural formal private sector businesses with five or more employees. The sample is stratified by firm size, business sector, and geographic region. The WBES strata for firm size are 5–19 (small), 20–99 (medium) and 100+ employees (large-sized firms). The strata for sectors, meanwhile, are manufacturing, services, transportation, and construction. In larger countries with bigger samples, the strata for manufacturing is again subdivided based on number of jobs, value-added, and total number of establishments. Businesses involved in health care, public utilities, financial services, and government services are excluded from the WBES sample. Finally, the strata for geographical regions are based on cities and regions based on their level of economic activity. The sampling frame is derived from the universe of eligible firms which are usually obtained from either the country’s statistical office or some other government agency such as the tax or business licensing authorities. Since 2006, all national surveys explain the source of the sample frame.

A harmonized questionnaire is also used in all countries reported here, which is answered by 1200–1800 business owners and top managers in larger countries, 360 in medium-sized countries and 150 in smaller countries. Even though the WBES has been conducted since 2002, the country surveys reported here are restricted to the 142 countries who since 2006 have employed both the harmonized questionnaire and the above stratified sampling method. This assures that the data reported are comparable across countries and over time.

Dependent variable

To measure the proportion of non-agricultural formal private sector businesses with five or more employees that started-up unregistered in each country, the responses to the following WBES question are used, “Was this establishment formally registered when it began operations?”. This is a dummy variable which takes a value of 1 if the firms declare that they started operations in the country without formal registration and a value of 0 when the firm was formally registered at the outset of operations.

Key independent variables

To test the theories explaining cross-country variations in the level of registration at start-up, variables are used that capture the tenets of the modernization, neoliberal, political economy, and institutional perspectives. To evaluate the economic development tenet of the modernization hypothesis (H1a), the indicator used is: the current GDP per capita of each country expressed as the purchasing power parity in international dollars transformed into natural logs. This was retrieved from the IMF World Economic Outlook Database for the relevant years for each country surveyed.

To evaluate the modernization of governance hypothesis (H1b) meanwhile, a composite index is used which evaluates the corruption behaviors collected in the WBES, namely:

Corruption composite index: a dummy variable that indicates whether the entrepreneur has paid public officials bribes and other payments to ‘get things gone’ in relation to customs, taxes, licenses, permits, regulations, and services. This is a dummy variable, with a value 1 if a firm had paid officials in one or more of such cases and value 0 otherwise.

Meanwhile, to test both the tenets of the neoliberal thesis (H2) that state interference increases the level of nonregistration at start-up and the inverse political economy thesis that state intervention reduces the level of nonregistration at start-up (H3), two indicators of the level of state intervention are employed, namely:

Tax revenue to GDP ratio, from the IMF World Economic Outlook database.

Expense of government as a percentage of GDP, which is a measure of the size of government and, therefore, a loose proxy of the degree of intervention. The expense of government is the level of cash payments for the operating activities of the government in providing goods and services. It includes compensation of employees (such as wages and salaries), interest and subsidies, grants, social benefits, and other expenses such as rent and dividends (World Bank, 2017).

To test the institutional hypothesis (H4), meanwhile, the indicator used is:

Trust in the court system, measured by the percentage of firms believing that the court system is fair, impartial, and uncorrupted. This is based on the response to the following question: “I am going to read some statements that describe the courts system and how it could affect business. For each statement, please tell me if you strongly disagree, tend to disagree, tend to agree, or strongly agree.” This is a dummy variable with a value of 1 given to those firms who agree and strongly agree that “the court system is fair, impartial and uncorrupted” and a value of 0 for those who disagree or strongly disagree.

This variable of trust in the court system is here used a proxy indicator of the level of trust of entrepreneurs in the formal institutions and thus a measure of the degree of incongruence between the formal and informal institutions (i.e. the extent to which entrepreneurs have faith in the court system).

Other control variables

To control for other key explanatory variables that may also affect nonregistration at start-up, a series of individual-level variables are included that are revealed to influence the likelihood of informal entrepreneurship both in previous analyses of the WBES data (Hudson et al., 2012; Williams et al., 2017) and other studies of informal entrepreneurship (Dau and Cuervo-Cazzurra, 2014; Thai and Turkina, 2014; Vu, 2014). These firm-level control variables are:

Firm age: a continuous variable for the number of years since the firm was established.

Foreign-owned: a dummy variable with a value 1 indicating if the share of the firm’s ownership held by foreign individuals or enterprises is larger than 49%.

Export-orientation: a dummy variable with a value 1 indicating the proportion of firm’s sales which are for the export market and 0 for the share of sales for the domestic market.

Firm size: a categorical variable with value 1 for small firms with less than 20 employees, value 2 for medium-sized firms between 20 and 99 employees, and value 3 for large firms with more than 100 employees.

Legal status: a categorical variable indicating whether the legal form of the firm is an open shareholding, a closed shareholding, a sole proprietorship (i.e. ownership), a partnership, a limited partnership, or any other form.

Quality certification, a dummy variable with value 1 indicating the firm has an internationally recognized certification and 0 otherwise.

External auditor, a dummy variable with value 1 indicating the firm has its annual financial statement reviewed by an external auditor and value 0 otherwise.

Presence of a website, a dummy variable with value 1 when the firm uses a website for business-related activities and value 0 otherwise;

Use of e-mail, a dummy variable with value 1 when a firm uses e-mail to interact with clients and suppliers and value 0 otherwise.

Top manager’s experience, a continuous variable of the years of experience the top manager has in the sector.

Temporary workers, a variable measuring the average number of temporary workers in the firm.

Permanent full-time workers, a continuous variable of the average number of permanent full-time workers in the firm.

Female full-time workers, examining the share of permanent full-time workers who are female.

Female involvement in ownership, a dummy variable with value 1 indicating whether women are involved in the ownership of the firm and value 0 otherwise.

Methods

To evaluate the country-level determinants of whether formal firms are more likely to state that they started-up unregistered across the 142 countries, multilevel techniques are used. Given that the surveyed enterprises in the WBES are clustered across country–year subsamples, multilevel modelling is the optimal technique to elicit unbiased standard errors as well as reliable statistical comparisons. The estimating standard probit equation takes the following form:

where x1i denotes a vector of exogenous variables capturing firm-level characteristics and Ii represents whether formal firms are unregistered at start-up. The error term ∊1i is normally distributed with zero mean and constant variance.

Findings: Determinants of cross-country variations in nonregistration at start-up

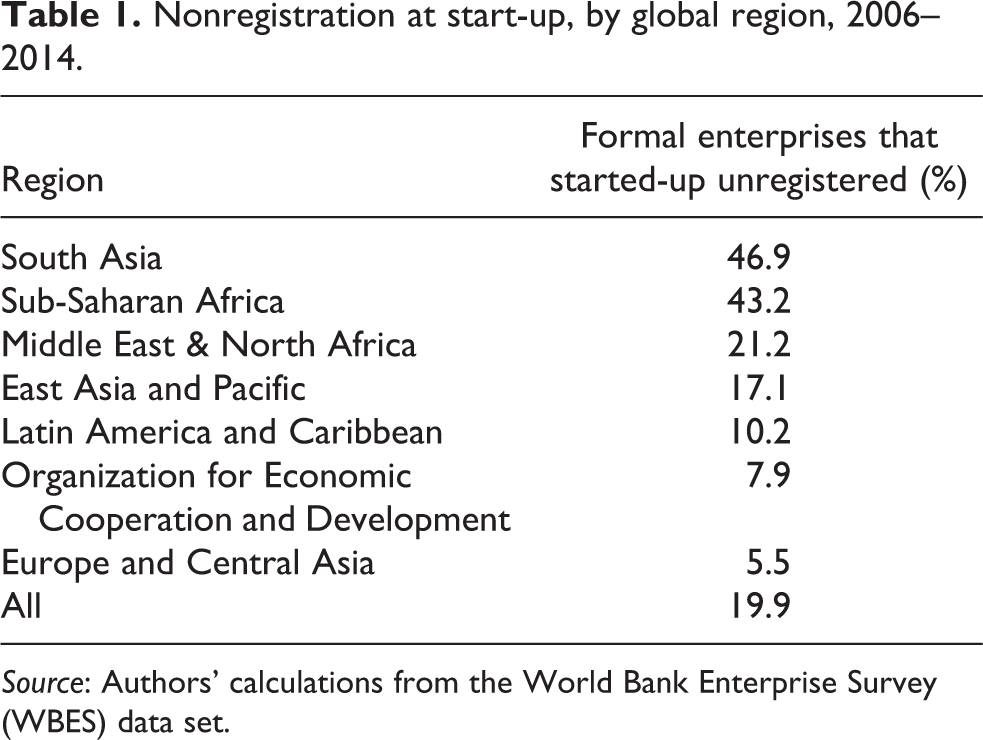

One in five (19.9%) formal enterprises surveyed in these 142 countries report that they started-up unregistered. A significant minority of the current formal business community worldwide, therefore, started unregistered and made a transition to legitimacy. Nevertheless, the proportion of formal enterprises that started-up unregistered varies across global regions. As Table 1 reveals, the share of formal enterprises that were unregistered at start-up ranges from 46.9% in South Asia and 43.2% in sub-Saharan Africa to 7.9% in OECD nations and 5.5% in Europe and Central Asia.

Nonregistration at start-up, by global region, 2006–2014.

Source: Authors’ calculations from the World Bank Enterprise Survey (WBES) data set.

There are also significant cross-country variations in the extent to which formal enterprises started-up unregistered ranging from all enterprises surveyed in Burundi, The Gambia, Guinea, Guinea Bissau, Namibia, Nigeria, Pakistan, and Swaziland, 74% in Angola, and 63% in Uganda, to only 3% in Djibouti, Dominica, Eritrea, Estonia, FYR Macedonia, Hungary, Jordan, Kazakhstan, Latvia, Moldova, Panama, Poland, St Lucia, Venezuela, to 2% in Armenia, Bhutan, Croatia, Romania, Suriname and Slovakia, and just 1% in Slovenia.

How, therefore, can such cross-country variations be explained? Are cross-country variations in nonregistration at start-up associated with the level of economic development and the modernization of governance as modernization states? Are they associated with too much or too little state intervention as the neoliberal and political economy theories state respectively? And are they associated with the level of incongruence between formal and informal institutions?

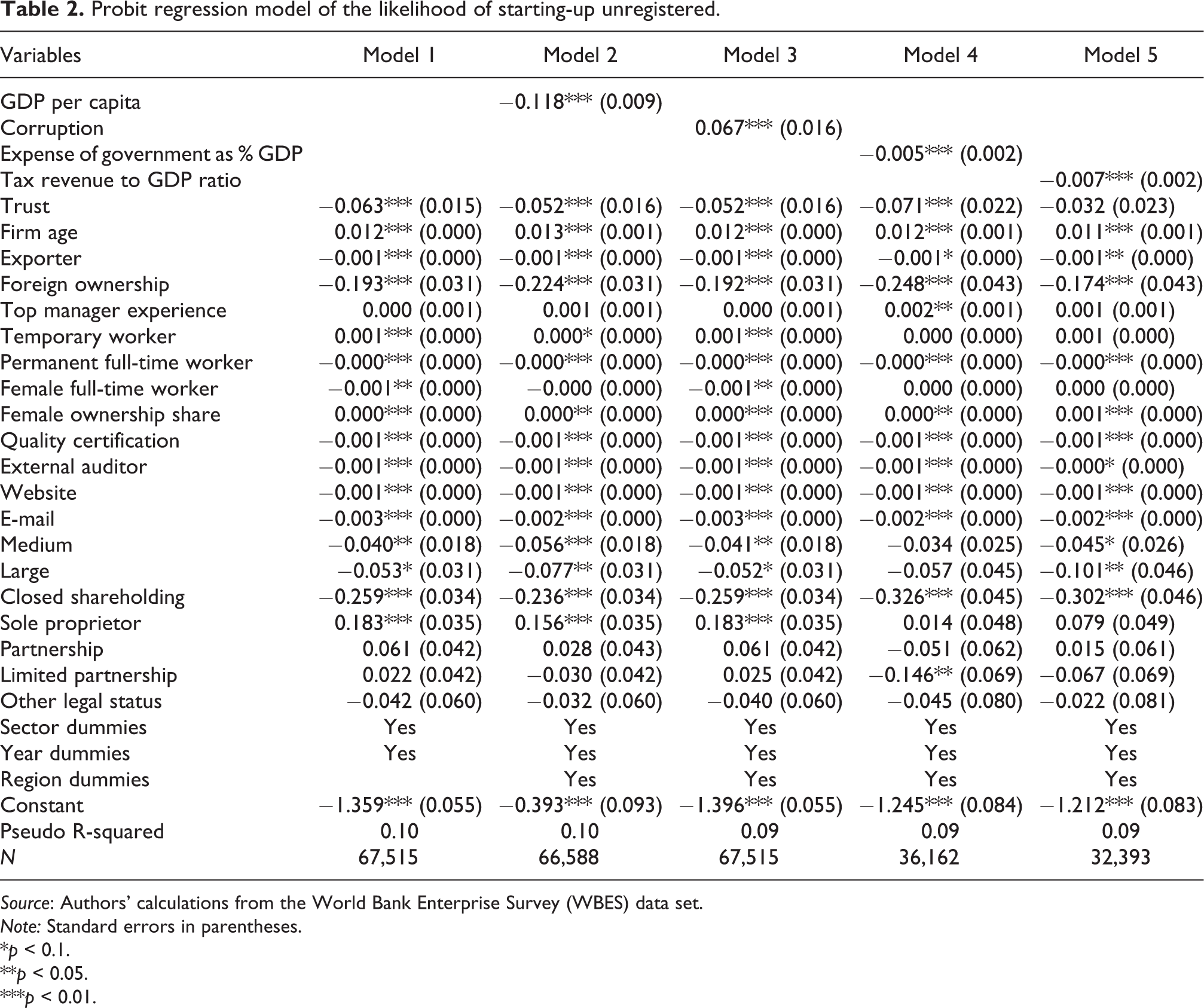

Table 2 reports the standard probit coefficient estimates of the likelihood of a formal business starting-up unregistered across the 142 countries. Model 1 reports the probability of an enterprise staring-up unregistered using only the firm-level variables. This reveals that older firms being more likely to have started-up unregistered. Meanwhile, firms that export and are foreign-owned are significantly less likely to have started-up unregistered than non-exporting and domestic-owned enterprises. Turning to workforce characteristics, top manager’s working experience in the sector is not significantly associated. Firms with full-time permanent and female workers, nevertheless, are significantly less likely to have started-up unregistered, as are firms where women are involved in the ownership of the enterprise. Examining innovation and technology, furthermore, formal firms with quality certification, a website, e-mail, and external auditor are less likely to have started-up unregistered. Akin to previous studies (Kanbur, 2015), small firms are significantly more likely to have started-up unregistered than medium-sized and larger enterprises. And finally, and with respect to the legal status of firms, sole proprietors are significantly more likely to have started-up unregistered, but closed partnerships are significantly less likely to have done so.

Probit regression model of the likelihood of starting-up unregistered.

Source: Authors’ calculations from the World Bank Enterprise Survey (WBES) data set.

Note: Standard errors in parentheses.

*p < 0.1.

**p < 0.05.

***p < 0.01.

To evaluate the different explanations for the cross-national variations in nonregistration at start-up, model 2 then adds the first country-level indicator of the log of GDP per capita and shows a significant negative association. This confirms the first tenet of the modernization thesis (H1a), namely that the higher the GDP per capita, the lower is the probability that formal enterprises started-up unregistered. Importantly, moreover, the significances and signs of nearly all the first-level variables in model 1 remain the same when this country-level variable is added in model 2. The remaining models then include each of the country-level variables associated with each tenet of the remaining theoretical explanations in a sequential manner to evaluate whether they are significantly associated with cross-country variations in nonregistration at start-up, while holding constant the firm-level variables.

To analyze the second tenet of the modernization thesis regarding whether the quality of governance, measured here in terms of the level of corruption, is significantly associated with the likelihood of formal enterprises starting-up unregistered, model 3 finds a positive association. The higher the level of corruption, the higher is the likelihood that formal enterprises started-up unregistered (confirming H1b).

Turning to the neoliberal thesis (H2), the first tenet to analyze is whether the level of nonregistration at start-up is greater in countries with higher taxation, measured by the tax revenue to GDP ratio. Contrary to neoliberal theory that higher taxation results in higher levels of non-registration at start-up, model 4 reveals the opposite. The higher the level of tax revenue to GDP ratio, the less likely are formal enterprises to be unregistered at start-up. This refutes H2a and is supportive of the political economy view that the greater the level of state intervention, measured here by the tax revenue to GDP ratio, the less likely are formal enterprises to be unregistered at the commencement of operations (confirming H3a).

It is similarly the case when hypothesis H2b is tested, namely that the level of nonregistration at start-up is greater in countries with higher levels of state interference in the free market, measured by the expense of government as a percentage of GDP. Model 5 reveals that there is a statistically significant association, but the sign is in the opposite direction to the neoliberal thesis. The greater the expense of government (as a percentage of GDP), the less likely are formal enterprises to start-up unregistered (refuting H2b). This, therefore, is supportive of political economy theory; the greater the expense of government as a percentage of GDP, the less likely are formal enterprises to be unregistered at start-up (confirming H3b).

Turning finally to whether there is a strong significant negative association between an incongruence between the formal and informal institutions (measured by whether the court system is viewed as fair, impartial, and uncorrupted) and the likelihood of formal enterprises starting-up unregistered, the finding is that the greater the level of incongruence, the greater is the probability that formal enterprises will start-up unregistered (confirming H4). This remains valid across all models.

Discussion and conclusions

Evaluating the WBES data from 142 countries collected between 2006 and 2014 on cross-country variations in the level of nonregistration at start-up, the finding is that one in five formal enterprises were unregistered at start-up, although there are marked cross-country variations in the proportion of formal enterprises that started-up unregistered. Evaluating the determinants of the cross-country variations in the level of nonregistration at start-up, a multivariate probit regression analysis has confirmed the modernization, political economy, and institutional theories but not neo-liberal theory. Here, therefore, the theoretical and policy implications are discussed.

Theoretically, this study reveals the importance of transcending singular logics when explaining cross-country variations in the level of nonregistration at start-up. Not all these theories are mutually exclusive. Understanding the cross-national variations in informal entrepreneurship requires the modernization, political economy, and institutional theories to be combined. They are each necessary but insufficient perspectives that need to be synthesized. This new theory that synthesizes these previous theoretical perspectives is here termed “neoinstitutionalist modernization” theory. Reflecting the above findings, this theory asserts that the level of nonregistration at start-up is higher in countries where there is a lower level of economic development, lower quality of governance, lower levels of state intervention, and higher levels of institutional incongruence.

These findings of this study not only have implications for theory, they also have implications for how starting-up unregistered is tackled. Conventionally, the dominant policy approach has been for tax and labour inspectorates to pursue the eradication of unregistered enterprises by changing the cost/benefit ratio confronting entrepreneurs at start-up to make registration a rational economic decision. This has been predominantly achieved by raising the perceived and/or actual risks of detection and the level of fines for nonregistration (Allingham and Sandmo, 1972). Recent years, nevertheless, has seen more emphasis on making it easier, beneficial, and less burdensome to register (Williams et al., 2017), due to a recognition that the policy objective should not be to shut unregistered enterprises but, rather, to formalize enterprise in the informal sector (ILO, 2014). The finding in this article that one in five formal enterprises started-up unregistered provides evidence that shutting unregistered enterprise is deleterious to economic development and that formalizing informal enterprise is a more progressive approach.

However, changing the cost/benefit ratio confronting entrepreneurs does not deal with the structural causes of the level of nonregistration at start-up. It simply seeks to cure the problem rather than prevent it from happening. To do this, governments need to tackle the structural causes. The likelihood of enterprises starting-up unregistered is significantly higher in countries where GDP per capita is lower; there are higher levels of corruption; the tax revenue to GDP ratio is lower; the expense of government as a percentage of GDP is lower; and the formal rules of the game are incongruent with the norms, values, and beliefs of entrepreneurs. Nonregistration at start-up will only reduce if these structural conditions are addressed.

Nevertheless, even though this article reveals that the level of nonregistration at start-up is significantly correlated with these structural conditions, there are limitations to the conclusions that can be drawn and caveats required. A first limitation of this study is that it examines only cross-country variations in the level of nonregistration at start-up of formal enterprises that employ five or more employees. It examines neither formal smaller enterprises and sole traders that started-up unregistered nor unregistered enterprises that have not formalized. Second, the WBES when measuring whether formal enterprises started-up unregistered does not define what is meant by nonregistration. Participants may thus interpret nonregistration in different ways (e.g. not having a local trading license, not being registered under commercial or factories’ acts, not being registered with relevant professional associations or regulatory acts). Third, this WBES survey does not provide any evaluation of their reasons for being unregistered at start-up (e.g. whether they were simply awaiting registration, test-trading to evaluate their venture’s viability before deciding to register or whether they had no intention initially of registering) or their reasons for registration (e.g. to access formal finance or markets, to win contracts with formal firms, to access public sector contracts). And fourth and finally, only a few structural determinants have been evaluated here, particularly in relation to state intervention and institutional incongruence. Future surveys should therefore not only examine smaller enterprises that are both registered and unregistered, and clarify to survey participants what is meant by being registered, but also more qualitative in-depth research is required of the reasons for being unregistered and for registering, and there is a need for evaluating in finer-grained detail the state interventions leading to reduced levels of nonregistration (e.g. active labour market policies, social protection expenditure, and educational provision). This would enable governments to better tailor the policy initiatives required to reduce nonregistration at start-up.

In sum, if this article thus stimulates further entrepreneurship research that further advances the finding that cross-national variations in nonregistration at start-up require a synthesis of the modernization, political economy, and institutionalist theories, by conducting further research as suggested above, then one of its intentions will have been fulfilled. If this then results in governments pursuing the prevention of nonregistration by tackling its structural determinants, rather than simply curing the problem once it has happened, then the wider intention of this article will have been fulfilled. What is certain, however, is that this article provides no support for the view that decreasing taxation and reducing state intervention will reduce the proportion of enterprises starting-up unregistered.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.