Abstract

What is the economic value of the UK hospitality industry and the wider tourism industry? How many people does each employ? Estimates from different sources provide wildly differing answers, leading to confusion and misunderstanding. Here, the authors, using information appearing in a new publication (Hospitality Digest 2014, 189 pages (PDF format only), is published by the Institute of Hospitality, (www.instituteofhospitality.org). It provides over 100 tables of information on the size and structure of the tourism, hotel, food service and conference industries, with a special section on employment and education with articles by leading educationists and commentators.), discuss the different values put on the size and value of UK tourism and UK hospitality, and suggest that only by improving productivity will creating 300,000 more jobs in the industry be justified.

The tourism industry is a difficult creature to capture. What does it comprise? Certainly, there are recognised sectors of the economy that are part of it – hotels and other serviced accommodation, restaurants and all things foodservice but not hospital and education catering nor food and service management – the sector that used to be called contract catering – which is certainly part of the hospitality industry but not necessarily of tourism (though, even here, contractors are catering in tourism and leisure outlets, such as museums).

We have other sectors of the tourism economy like retail (tourists do a great deal of shopping), attractions (where would Britain be without its culture and its history?), theatres, concert halls and other places of entertainment (few London theatres would survive without overseas visitors), travel (tourists hire cars and use air and rail services and, decreasingly, travel agents) while many watch sports or take part in them; some even gamble. And, of course, there is the £4bn a year earned from the corporate and conference sector. All of these sectors can legitimately claim to be part of the tourism industry, but how do we calculate their value?

So defining the tourism industry (including hospitality) presents challenges which Hospitality Digest 2014 acknowledges and illustrates with four separate estimates of its value.

Which should the industry believe? Clearly, these are different years; even more clearly, the definition of tourism is different in each calculation.

But with a 15% difference between the highest and lowest estimate it may not be surprising that confusion tends to reign. No surprise that many people combine hospitality and tourism into one ever-growing but amorphous industry – perhaps in an effort to magnify the size and importance of both hospitality and tourism. Trying to separate them may be a fool’s errand; on the other hand, it is important to recognise the role that each plays in the UK economy.

Growing? Of course, even these figures can be misleading. If we take Deloitte’s estimates, UK tourism was worth £84.7bn in 2005, rising to £101bn by 2013. When inflation (at 30.3%) is taken into account over this nine year period, the real value of UK tourism in 2013 should have been £109bn – no growth at all.

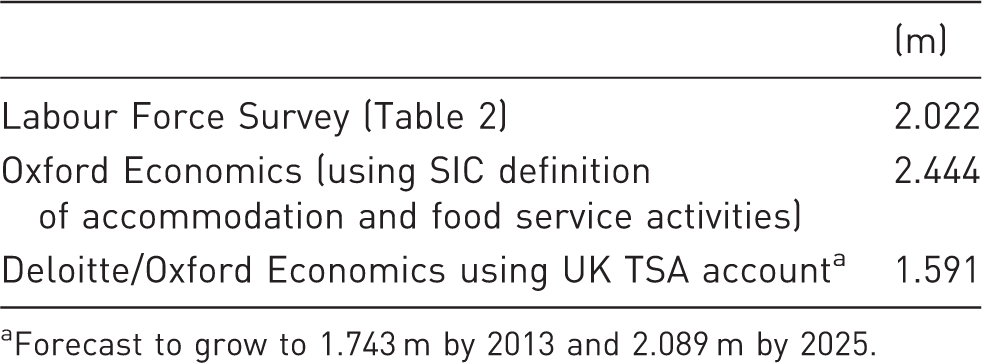

A similar picture emerges when we look at employment. Trying to estimate the number of people working in the tourism industry is as difficult as estimating its value. Deloitte/Oxford Economics suggest that by 2025 the wider tourism economy will be supporting 3.7 m jobs (630,000 more than in 2013) though, in the hospitality industry alone, we have a number of different estimates, all using the same SIC rating for accommodation and food service activities.

Estimated size of UK tourism industry.

Sources: Horizons market research consultancy for Hospitality Digest 2014; ONS UKTSA 2011 account; Deloitte for Visit Britain’s publication, Tourism, Jobs and Growth Tourism Alliance.

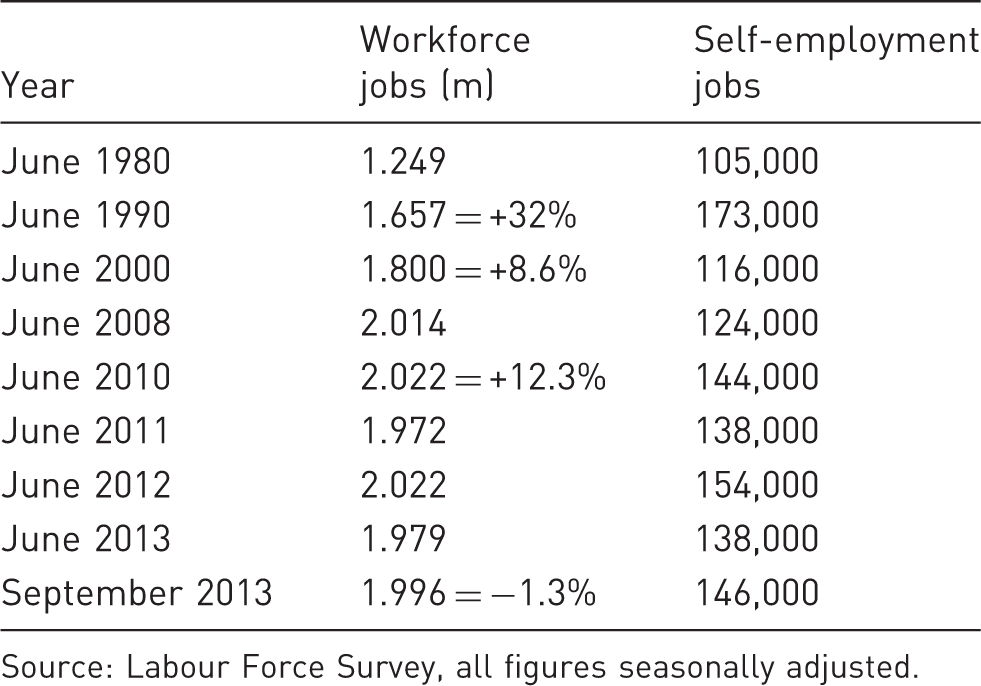

Employment in the accommodation and food service activities (SIC) – 1980, 1990, 2000–2013.

Source: Labour Force Survey, all figures seasonally adjusted.

Estimates of direct tourism industry employment, 2010.

Forecast to grow to 1.743 m by 2013 and 2.089 m by 2025.

Make what you will of these various estimates. Disraeli’s dictum of lies, damned lies and statistics seems ever more appropriate.

Without a detailed breakdown of employment by sector (which People 1st does provide), it is difficult to reconcile all these different figures.

It is here that we come to the hospitality industry’s Big Conversation programme, which aims to create 300,000 jobs by 2020. This is 43,000 new jobs every year for the next seven years or an increase (on Labour Force figures) of some 15%. How feasible is this?

If all those 300,000 jobs were to be created, economic activity in the industry would need to expand mightily – in fact, by far more than 15%; given the industry’s poor productivity record, an increase of some 20–25% would be needed to profitably justify such an increase in the workforce.

Labour Force figures show that it has taken some 30 years to create 747,000 jobs with employment expanding by 12% in the heady period of economic growth between 2000 and 2008. This is unlikely to be repeated in the next seven years because much hotel construction has been completed and the many restaurant openings tend to be partially off-set by the many restaurant closures.

Of course, the hospitality industry is in an expansionary mood and new outlets are opening (though many are closing – over 4000 hotels and some 8000 pubs since 2004), but the danger lies in creating new jobs when existing workers are insufficiently well trained to fulfill the jobs they already have.

So the industry might well be recruiting 30,000 + young people every year (particularly the politically important young and unemployed job seekers), but this does not necessarily mean that they move into new jobs. Employers are promising to recruit numbers of (cheaper?) young people, and even into apprenticeships, but no employer will create a job for the sake of creating a job. Current recruitment is primarily filling up an employment bucket which has a hole in the bottom caused by the high number of people quitting the industry, going abroad or retiring.

While the industry’s Big Conversation recruitment programme will undoubtedly help to attract more youngsters into a career in the industry, and has the support of major employers, it is difficult to escape the impression that its purpose is more to raise the profile of the industry as a major employer and thus encourage government to take a more favourable view of industry campaigns and issues. Not much luck so far.

People 1st appears to agree. It forecasts that, by 2020, 184,000 new workers are required to meet additional growth, which is just over half the industry’s stated aim of 300,000 new jobs, but that a staggering 1,613,000, will be needed to replace existing staff by 2020. The hole in the bucket is, indeed, very large.

The cost to the industry of this labour turnover is huge. According to Deloitte, creating one new job costs £54,000, so creating 300,000 new jobs would cost the industry £16.2bn. But that’s not the whole story. With labour turnover at 30% per year – and costing about £1,900 (People 1st) to replace each leaver – replacing 1.6 m workers will add a further £3.0bn to the industry’s wage bill by 2020.

Industry revenues will have to rise dramatically to meet such massive cost increases.

In the rush to be active in job creation; however, little mention is made of the industry’s productivity levels. Can so many new jobs be created when there is a question mark over how efficiently employers use their existing staff?

According to People 1st, there are some 400,000 hospitality staff (some 20% of the total workforce) who do not have the full range of skills required. This is a situation exacerbated by the industry’s high levels of labour turnover. Staff are not employed for long enough to develop the skills they need; nor are sufficient operational staff progressing to management roles. Even though there are claimed to be high levels of training in the industry, much of it is directed at training the very recruits (25% of them migrants) caused by industry’s high labour turnover rather than those skills and occupations that have the highest skill gaps.

If the existing workforce is working at only 80% capacity or less, as the evidence suggests, recruiting more and more workers will not make the industry more efficient (which must be the ultimate aim if profitability is to be maintained) but less productive.

The greater need is for the industry’s productivity to improve so that fewer workers are needed. Unfortunately, as the recession fades and the economy grows, employers will be tempted to recruit more people rather than take the trouble to train and organise existing staff to work more effectively. But it is economically illiterate to recruit increasing numbers of people into jobs that might not be needed if existing skill levels were higher and work procedures better planned and more systematic.

Unfortunately, for many employers, productivity remains something of a mystery, which perhaps explains why the latest Office for National Statistics (ONS) statistics on falling levels of productivity and competitiveness make for depressing reading. Productivity is back on the agenda.

The view, 15 years ago, was that employers in the UK tourism and hospitality industry had half the levels of productivity of those in the USA, France and Germany. It was against this background that the Best Practice Forum (BPF) – which included the British Hospitality Association, the Institute of Hospitality and the British Institute of Innkeeping – launched a major productivity drive.

The good news was that by 2007, the ONS was able to report that productivity growth in tourism and hospitality had outstripped that in the service sector, as well as the economy as a whole, averaging 2.3% compared with 1.8% in the service sector and 1.9% for the economy overall. Sadly, the latest 2014 ONS data show that there has been a 3% slump in output per worker in the UK – a fall greater than in any other G7 country, barring Italy.

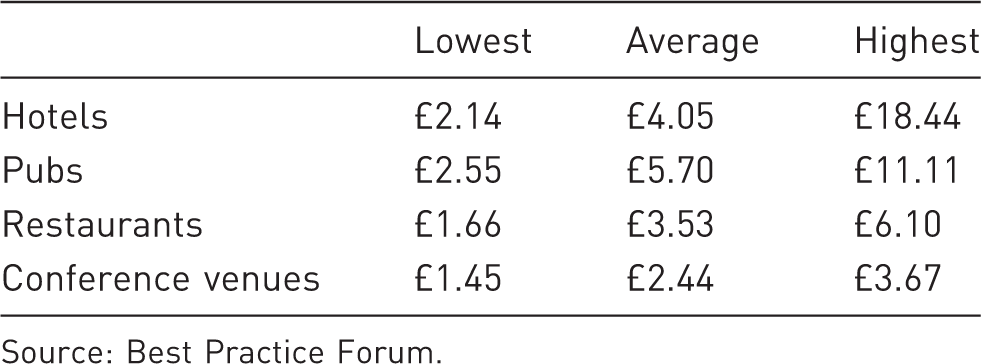

Sales revenue generated for every £1 spent on labour.

Source: Best Practice Forum.

Best Practice Forum studies concluded that more than a third (about 37%) of working time is wasted. This is mainly a result of:

Doing too much Waiting around Transporting Unnecessary actions Dealing with faults

Three-quarters of that wasted time within hospitality businesses is down to poor planning, a lack of work organisation and inadequate supervision.

Yet all too often government and industry have set their sights on the wrong targets when it comes to raising levels of productivity. Simply boosting the supply of skills alone will not necessarily improve performance and productivity. Research by Department for Education and Skills shows that only 7% of total output growth can be attributed to improvements in labour quality. Much more significant is the 93% of improvement in performance which comes from investment in innovation, rethinking the ways in which services are designed, work is organised, staff are rostered, technology is utilised and skills are deployed.

There can be no denying that world tourism is a proven growth industry, with tantalizingly tempting long-term prospects. If UK tourism can continue to ride on the back of this particular tiger, the hospitality industry will prosper, too; it will also employ ever more people.

But the industry depends on a skilled workforce and there is no overwhelming indication that employers are doing anything other than training people to fill gaps that are created by high levels of labour turnover that could, with improved supervision and better management, be avoided.

As ever, the challenges of staff recruitment, retention and development remain at the top of the industry’s agenda. Not a lot has changed.