Abstract

This paper examined nonfinancial disclosures by hospitality and tourism firms on corporate social responsibility (CSR)/sustainability dimensions. Specifically, the study utilized content analysis to assess and document CSR and sustainability reporting practices by firms in this economic sector. The study found that in general, firms utilized the Global Reporting Initiative as the standard guideline for reporting. Findings also suggested that there is a vast difference in the types of information reported by firms in the industry’s various sectors. Lodging firms disclosed the most information on the CSR/sustainability dimensions than firms operating in the food and beverage and cruise line sectors. These findings suggested that CSR/sustainability reporting in the hospitality and tourism industry is in its infancy. Overall, the most frequently disclosed information related to performance on indicators associated with water usage, energy conservation, and waste generation. Community involvement activities were also frequently disclosed by sampled firms. The least reported dimensions were information germane to compensation and work–life balance.

Keywords

Introduction

Today, academic and professional literature is replete with research and reports addressing the issue of corporate social responsibility (CSR) practices and reporting by firms. In fact, over the past two decades, organizations and researchers have sought to gain a better understanding of firm’s responsibilities to the communities in which they operate, and further, the importance of ensuring adherence to practices that are generally accepted as sustainable. This bourgeoning and sustained interest in CSR by firms has been driven in part by the societal trend of stakeholders holding firms responsible for their actions in the environments in which they operate (Jackson and Hua, 2009; Jackson and Parsa, 2009; Jackson and Singh, 2015). Consequently, several firms have implemented corporate policies and procedures aimed at ensuring that CSR becomes a central tenet of their corporate strategy. Although governments often extol the virtues and positive outcomes of such policies, it is important to note that CSR implementation and reporting for the most part, are typically unregulated, unilateral, and voluntary initiatives undertaken by firms. Furthermore, on a global scale, currently, there no clear methods for governments to fully incentivize or penalize firms for noncompliance with generally accepted CSR practices. As such, firms typically adopt and implement dimensions of CSR that are financially feasible and will generate incremental economic and social benefits for relevant stakeholders. In conjunction, firms have also developed strategies aimed at informing stakeholders about their CSR initiatives via voluntary disclosures.

Voluntary CSR disclosures have increased exponentially since the 1990s. Such disclosures have been driven largely by societal demand for information about firms’ deliberate contribution to society, the environment, and the economy. In addition, firms have voluntarily disclosed their CSR efforts to leverage actual or ostensible stakeholder benefits. Such demands and benefits have encouraged firms to not only implement dimensions of CSR germane to their corporate objectives, but to also convey performance-related information and outcomes of CSR initiatives (Romero et al., 2014). For a fact, CSR reporting via disclosures is not a new phenomenon. Instead, the concept has been around since the 1970s, when it was formally described as social accounting, or the process of evaluating firms “social performance” and reporting such performance outcomes to internal and external stakeholder groups (Ramanathan, 1976). However, in recent years, the concept has expanded to include environmental and economic performances in stakeholder-driven CSR reports (Ballou et al., 2006; Garz and Volk, 2007; Goel, 2010; Romero et al., 2014; Slater and Gilbert, 2004). In the context of this research, stakeholders refer to groups or individuals who can impact or is affected by the achievement of an organization’s objectives (Mitchell et al., 1997).

As CSR and sustainability reporting becomes the norm, especially among publicly traded firms, it is conceivable to posit that there will be increased stakeholders need for such reports, especially for investment decision purposes (Garz and Volk, 2007; Romero et al., 2014). However, in the absence of specific legislated or industry-specific CSR reporting guidelines, a persistent challenge faced by today’s firms is deciding what to report, specific formats, and measuring CSR performance (Smith, 2010). This is due in part to the fact that CSR is a broad construct that encompasses several dimensions. Currently, The Global Reporting Initiative (GRI) offers a standardized set of guidelines to assist firms with reporting and disclosing CSR performance (Global Reporting Initiative, 2014). Several firms have utilized these guidelines to aid in documenting and reporting CSR initiatives.

Like most of today’s economic sectors, the hospitality and tourism industry has dutifully incorporated CSR principles into all aspects of operations and strategic management, and several firms have started to disclose performance voluntarily via CSR or sustainability reports. Such adoptions are typically driven by hospitality firms attempting to: enhance their company’s image; gain competitive advantages; retain employees; attract new employees and customers; comply with government regulation; reduce risk exposure; and reduce operational costs (Bader, 2005; Graci and Dodds, 2008; Jackson, 2010). To date, hospitality and tourism research is replete with studies addressing CSR-related issues such as: sustainability practices within the industry’s various sectors; CSR practices and financial performance; and CSR applied to specific entities such as restaurants, hotels, and the industry as a whole (Peršić et al., 2013). Despite advances in hospitality and tourism research in this area, there is paucity of research on the subject of CSR and sustainability reporting practices within the industry (Peršić et al., 2013). Such research is important, given the growing relevance of CSR and sustainability in the decision-making process of both internal and external stakeholders (Jackson, 2010, 2013; Jackson and Singh, 2015). As such, the purpose of this research is to examine and document the CSR and sustainability reporting practices of hospitality and tourism firms. This is accomplished through content analysis of CSR and sustainability reports of publicly traded hospitality and tourism firms operating in the lodging, food and beverage, cruise line, and airline sectors of the industry. This research is important since it will add to our understanding of the dimensions of CSR and sustainability reported by such firms. It is hoped that the findings of this research will aid stakeholders, especially small hospitality firms in developing CSR practices, guidelines, and benchmarks.

Literature review

Social responsibility and sustainability reporting

The broad and related disciplines of sustainability and CSR have been the focus of studies in several economic sectors (Crittenden et al., 2011; Graci and Dodds, 2008; Vuontisjärvi, 2006; Waller and Lanis, 2009). In recent years, an area that has generated interest from researchers and the public as a whole is CSR reporting, which is often interrelated with terms such as sustainability reporting, corporate sustainability reporting, and triple bottom line reporting (Ballou et al., 2006; Garz and Volk, 2007; Goel, 2010; Slater and Gilbert, 2004). In fact, the need for sustainability reporting has forced firms to modify corporate practices, incorporate CSR and sustainability initiatives, and report outcomes. Consequently, sustainability reporting has progressed from general economic concepts to more specific determinants in the form of periodic reports and online reporting updates (Romero et al., 2014). These reports typically disclose a company’s performance on economic, social, and environmental initiatives that forces firms to be accountable for externalities associated with their operations (Goel, 2010).

The overarching goal of effective corporate social reporting is to address organization performance and make necessary changes to attain sustainable development (Hess, 2008). Hence, firms’ economic, social, and environmental changes, initiatives, and activities must be linked to core business strategies in order to enhance risk management in the three pillars of triple bottom line, increase company reputation, and attract and retain new stakeholders (MacLean and Rebernak, 2007). At its purest, CSR, generates a positive relationship between corporate social performance and financial performance (May and Khare, 2008). This perspective postulates that firms can simultaneously promote a social agenda while achieving superior financial performance achieved through efficiency gains, which ultimately positively impacts their bottom line (English and Schooley, 2014). However, sustainability reporting should not be perceived as a pursuit for a new bottom line metric but instead, should be a management and performance assessment philosophy that emphasizes the importance and interdependence of economic, environmental, and social performance relevant to firm’s core business strategies (Goel, 2010). In regard to process, sustainability reporting is a cycle that involves the release of information, communication with internal and external stakeholders, and moral development or an organization’s own self-reflection of its social behavior (Hess, 2008). The cycle starts with a dialogue with stakeholders to establish expectations of legitimate goals specific to sustainable development. This should be followed by the firm working to achieve established goals while simultaneously internalizing corporate values through moral development. The cycle is complete when the firm disclosures its performance, and restarts when dialogue continues (Hess, 2008).

For a fact, stakeholders, especially investors typically engage with a firm to maximize their value and return on investments, financially and otherwise, such as social returns. For several of today’s stakeholders, the concept of value not only includes financial returns but also social returns. This revolution in thinking has led to the performance-related concept of the triple bottom line, which relates to firms, performance on financial measures, as well as social and environmental measures. Hence, firms have come to the realization that in order to maximize shareholders’ value and profitability, it is essential that they to meet and exceed expectations of internal and external stakeholders and on financial, social, and environmental or sustainable measures of performance (MacLean and Rebernak, 2007).

Although there is growing interest from stakeholders in CSR and sustainability reporting, in most jurisdictions, including the U.S., sustainability reporting is not mandatory since it is not legislated (MacLean and Rebernak, 2007). Despite this fact, firms are increasingly electing to voluntarily disclose performance of CSR and sustainability initiatives (Goel, 2010). In fact, it is suggested that this type of reporting is now the norm for firms, especially those that are publicly traded (Garz and Volk, 2007). For publicly traded firms, this form of reporting is typically disclosed separately from their annual financial report (e.g., Form 10-K) since it contains information for all stakeholders and not only investors. In addition, currently, the data, facts, and figures reported are typically expressed in nonfinancial qualitative terms (Slater and Gilbert, 2004). However, in the future, it is anticipated that CSR and sustainability reporting will evolve and become a component of firms’ annual reports, which will include both financial and nonfinancial disclosures via a process known as integrated reporting (IR) (Dragu and Tudor-Tiron, 2013; Milne and Gray, 2013; Slater and Gilbert, 2004).

As CSR and sustainability reporting evolves, its format, content, and measurement are also progressing to include detailed information pertinent to specific industries (Smith, 2010). However, in general, sustainability reporting includes three main aspects related to CSR: existing strategies to improve performance; current issues and how to tackle them; and ongoing and future activities/initiatives by the firm (Waller and Lanis, 2009). In essence, CSR reports present a quantitative analysis of the company’s current social, economic, and environmental performance and future goals to improve firm value (MacLean and Rebernak, 2007). Examples of social indicators include: employee health and safety; equal opportunity and nondiscrimination plans; and volunteering activities. Economic indicators include disclosure of investments in human capital, wages and benefits packages, and local community economic development initiatives among others. Environmental performance typically addresses the consumption and preservation of energy, water, and waste management policies (Goel, 2010).

Nonfinancial disclosure reporting

Voluntarily nonfinancial disclosures by firms are grounded by at least three closely related theories—legitimacy, stakeholder theory, and institutional theory. Legitimacy theory (Suchman, 1995) is grounded in the idea that firms undertake specific actions that are congruent with prevailing social norms and values and communicate these actions to stakeholders. On the contrary, stakeholder theory (Freedman and Jaggi, 2010; Manetti, 2011; Manetti and Toccafondi, 2012) suggests that firms are motivated to initiate action to satisfy specific stakeholders (e.g., shareholders, customers, suppliers, and citizens). Finally, institutional theory (DiMaggio and Powell, 1983) postulates that firms are forced (typically by legal or shareholder pressures) to provide voluntary disclosure. For hospitality and tourism firms, it can be argued that direct and indirect shareholder pressures have helped to advance nonfinancial disclosures in the industry.

Sustainability reporting standards

Sustainability reporting is based on firms’ internal guiding principles or on standards and guidelines from external bodies such as the International Standards Organization (ISO), the World Business Council for Sustainable Development (WBCSD), and the GRI (Adams and Narayanan, 2007). The GRI is a private institution that works in partnership with the United Nations and has become increasingly popular among firms in international jurisdictions (Ballou et al., 2006; Sarfaty, 2013). The GRI is generally accepted as the standard for effective corporate sustainability reporting (Ballou et al., 2006; MacLean and Rebernak, 2007; Slater and Gilbert, 2004). The GRI labels sustainability reporting as an important element for managing change toward a sustainable global economy. This change synthesizes long-term profitability with ethical behavior, social justice, and concern and care for the environmental (Global Reporting Initiative, 2014). The GRI reporting standards are dynamic and evolve to incorporate the best practices. For example, in 2006, the GRI launched the third generation of reporting guidelines, the G3 Guidelines (Global Reporting Initiative, 2014). The G3 Guidelines offer a standard set of disclosures, performance measurements, and analysis, as well as different application levels, self-declared by each company, based on the extent to which the guidelines were adhered to (Legendre and Coderre, 2013; MacLean and Rebernak, 2007). Application levels are graded as A, B, C, or undeclared and can receive a plus sign (+), which indicates the highest level of coverage of the GRI standards (Legendre and Coderre, 2013; Sustainability Reporting Guidelines, 2011).

The G3 Guidelines call for greater transparency of reports, listing of issues, and stakeholder contribution (MacLean and Rebernak, 2007). Sustainability reports under the G3 Guidelines are mainly divided into three categories—economic, environment, and social. The latter is subcategorized into labor, human rights, society, and product responsibility (Global Reporting Initiative, 2014). In 2011, the G3 Guidelines were updated to G3.1 and in 2013, the GRI introduced the G4 Guidelines—Fourth Generation of Guidelines. The fourth generation guidelines will effectively replace the third-generation guidelines, which will not be utilize after 2015 (English and Schooley, 2014; Global Reporting Initiative, 2014). The G4 Guidelines allow reporting organizations to emphasize factors relevant to their operations in order to better evaluate how they influence stakeholders and impact the triple bottom line. Finally, the G4 Guidelines are generally regarded as a step in the process of combining nonfinancial and financial disclosures into one single report (IR) (English and Schooley, 2014).

Sustainability reporting and practices in the hospitality industry

Several studies have examined or suggest reasons why hospitality and tourism firms elect to choose to follow sustainable practices and implement CSR activities (Bader, 2005; Chan and Hawkins, 2010; Graci and Dodds, 2008; Jackson, 2010). However, there is paucity of hospitality-related research that specifically examines voluntarily nonfinancial disclosures. Existing research on the issue has generally been sector specific. For example: Bonilla-Priego et al. (2014) focused their study on corporate social reporting in the cruise line industry; Peršić et al. (2013) researched sustainability reporting of hotel companies in Croatia, and; Grosbois (2012) evaluated sustainability reporting practices among the largest lodging firms in the globe.

In general, hospitality firms tend to invest more in environmental initiatives relative to other economic sectors and generate fewer concerns on environmental issues, such as carbon footprint. As such, firms in the hospitality and tourism sector can leverage positive sustainability outcomes (Singal, 2014). Furthermore, the nature of the industry is conducive to the core principles of social responsibility and sustainability. For example, tourism-related activities, especially those in pristine environments, can improve a community’s social and economic profile and well-being, while generating few undesirable social, financial, and environmental impacts such as directly contributing to change in climate temperatures, air and noise pollution, and biodiversity loss among others. Consequently, issues related to not only the execution but also the reporting of sustainability practices, are of great importance to the development of the industry (Grosbois, 2012).

Methodology

Sampled firms.

Major corporate office. UK domiciled, has major office in Atlanta, USA.

Content analysis was conducted on each firm’s sustainability report and other relevant information found on their website. This methodology was deemed appropriate since content analysis was deemed appropriate since it allows the researchers to a examine documents for content and make replicable and valid inferences from information found in the texts of each document as well as the contexts in which the information was used (Krippendorff, 2013). Furthermore, content analysis was deemed appropriate since it enables researchers to gain greater understanding of a specific phenomenon (Krippendorff, 2013), such as CSR reporting. Prior to conducting the content analysis, a checklist of CSR and sustainability dimensions, or themes were identified. Each dimension was further divided into categories. The checklist was developed after a careful review of extant literature (Sobhani et al., 2012; Vuontisjärvi, 2006) germane to CSR and sustainability application and reporting. A total of 13 dimensions were identified. The 13 categories are: general CSR reporting; community involvement; social responsible products/services; education, training, and staff development; pays and benefits; participation and staff involvement; values and principles; employee health and well-being; measurement of policies; employment policy; security in employment; equal opportunities; and work–life balance. Each firm’s disclosure document was examined for instances of reporting on each dimension and recorded on the checklist under the appropriate category. For the purpose of this research, instance refers to each mention or reference of the dimensions in each firm’s sustainability report.

Results and discussion

Findings suggest that in general, hospitality and tourism firms utilized the GRI as the standard guideline for their reporting. In general, the level and detail of information reported by each firm varied greatly especially in regard to the number of issues covered in each report. Overall, firms in the lodging sector had the most complete reports that were centered on the three pillars of the triple bottom line, namely, economic, social, and environmental. These reports also included a greater number of indicators compared to those from the cruise and food and beverage sectors. The majority of the restaurant firms examined focused a significant portion of reporting on their supply and food chain, providing information about sustainable practices along their supply chain. The cruise industry had a higher focus on environmental initiatives than employment disclosure. This could be due to the fact that in recent years, the cruise industry has been heavily scrutinized for its negative environmental impacts (Klein, 2013) and hence, firms in this sector have taken steps to ameliorate environmental impacts.

As noted, this study identified 13 CSR and sustainability dimensions or reporting categories. As such, sampled firms’ were assessed to ascertain reporting on these dimensions. Findings of such reporting are highlighted and discussed below appropriately under each dimension heading.

General CSR and sustainability reporting

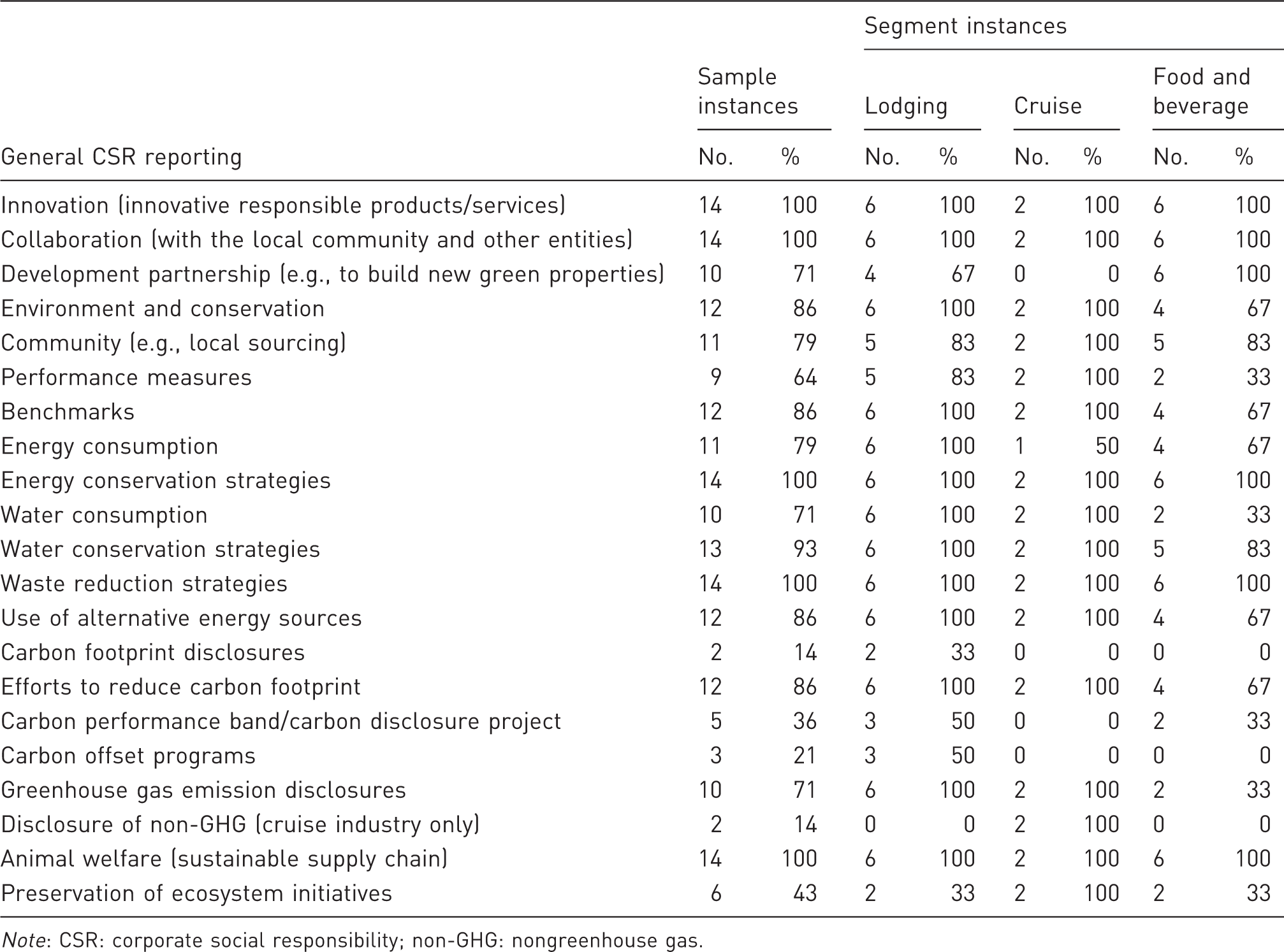

General CSR reporting.

Note: CSR: corporate social responsibility; non-GHG: nongreenhouse gas.

From a sustainability perspective, it is encouraging to note that a high majority (71%) of firms disclosed information about greenhouse gas emissions. However, only 14% disclosed information about nongreenhouse gas (non-GHG) emissions (0% lodging, 100% cruise, 0% food and beverage). This finding suggests that disclosure of emissions of non-GHG could be perceived as relevant and important for the cruise segment, but does not garner such importance in the other two sectors. Furthermore, all firms showed interest toward utilizing and encouraging a sustainable supply chain, including use of a supplier sustainability policy and making efforts to educate suppliers on the benefits of sustainability.

Community involvement

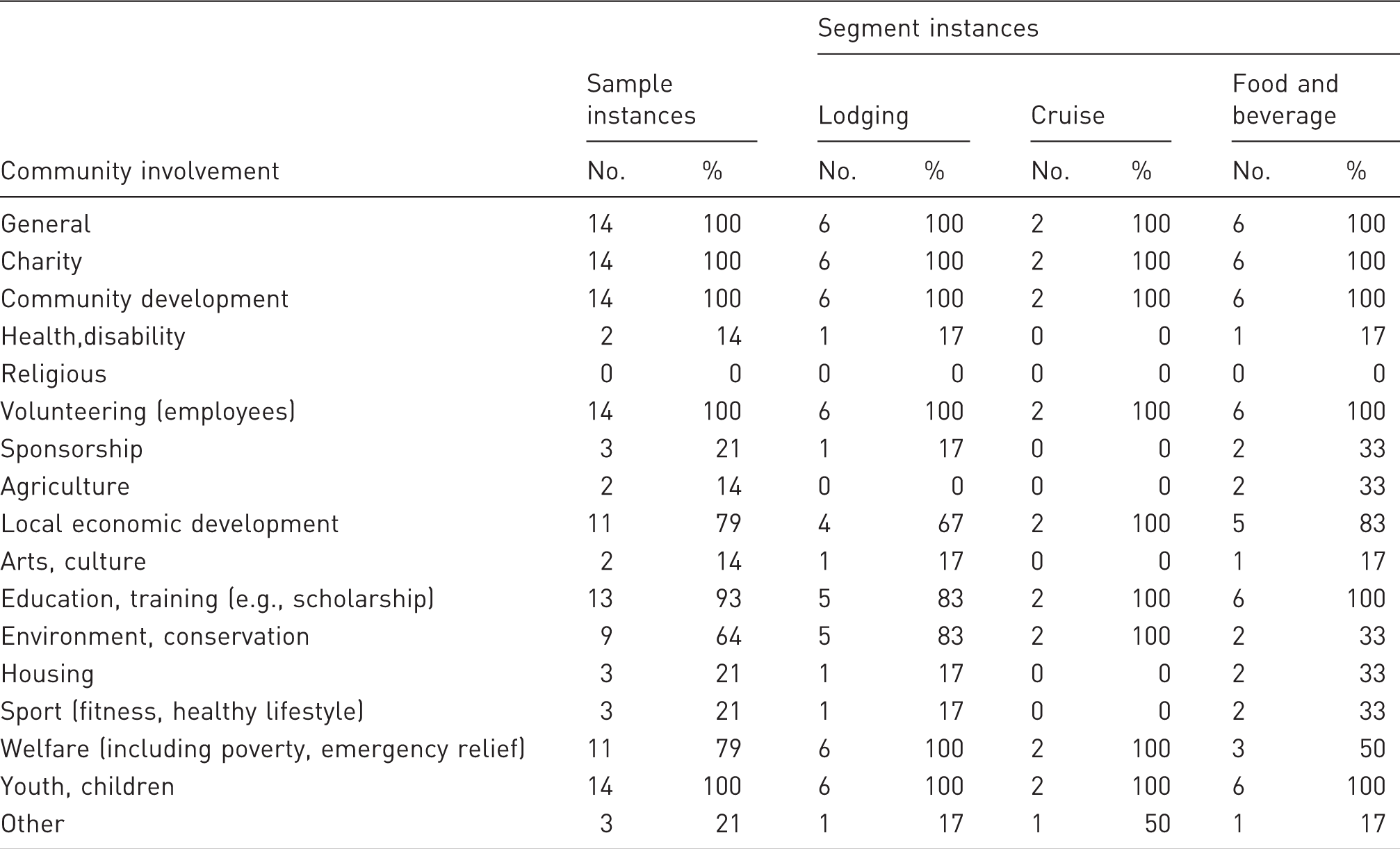

Community involvement.

Socially responsible products/services

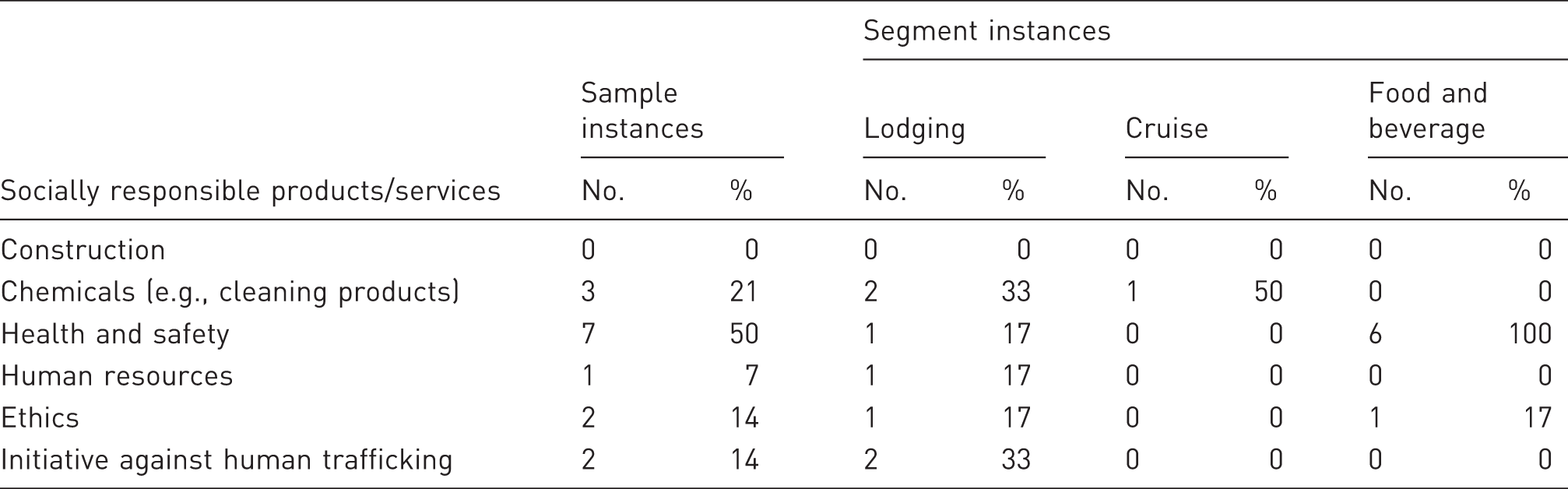

Socially responsible products and services.

Education, training, and staff development

Employee relations: education, training, and employee development.

Pays and benefits

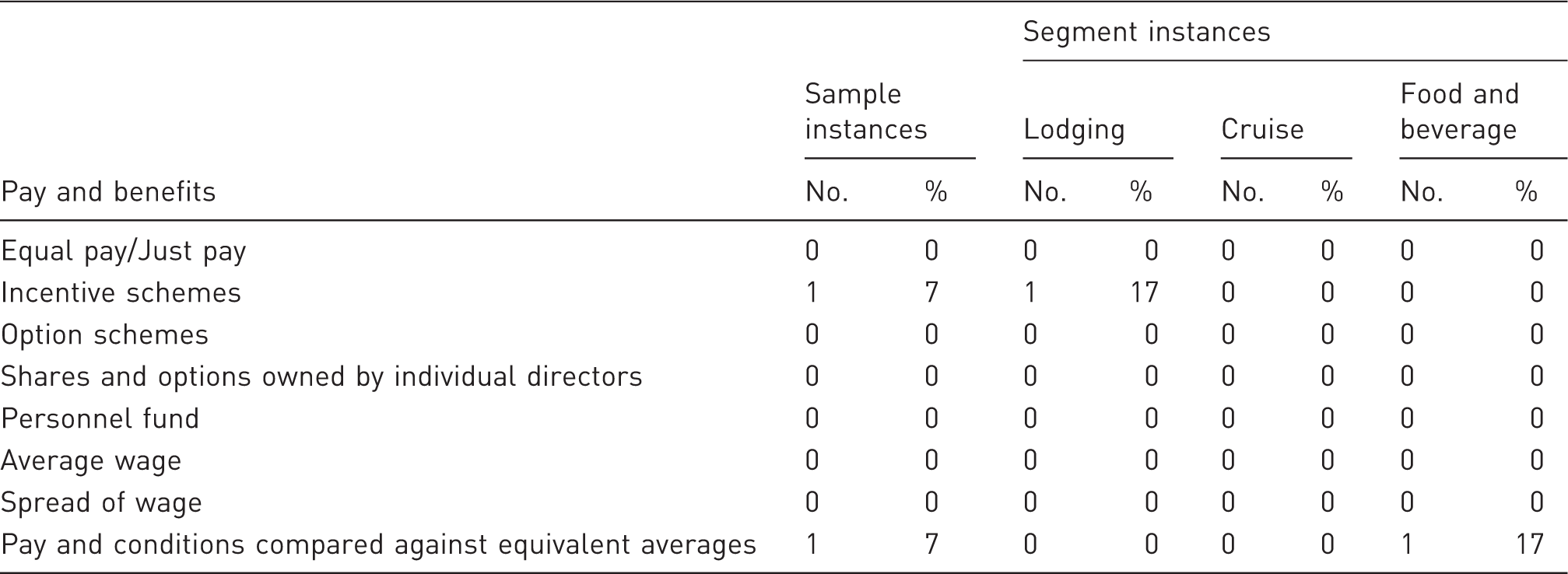

Employee relations—pay and benefit.

Participation and staff involvement

Employee relations—staff participation and involvement.

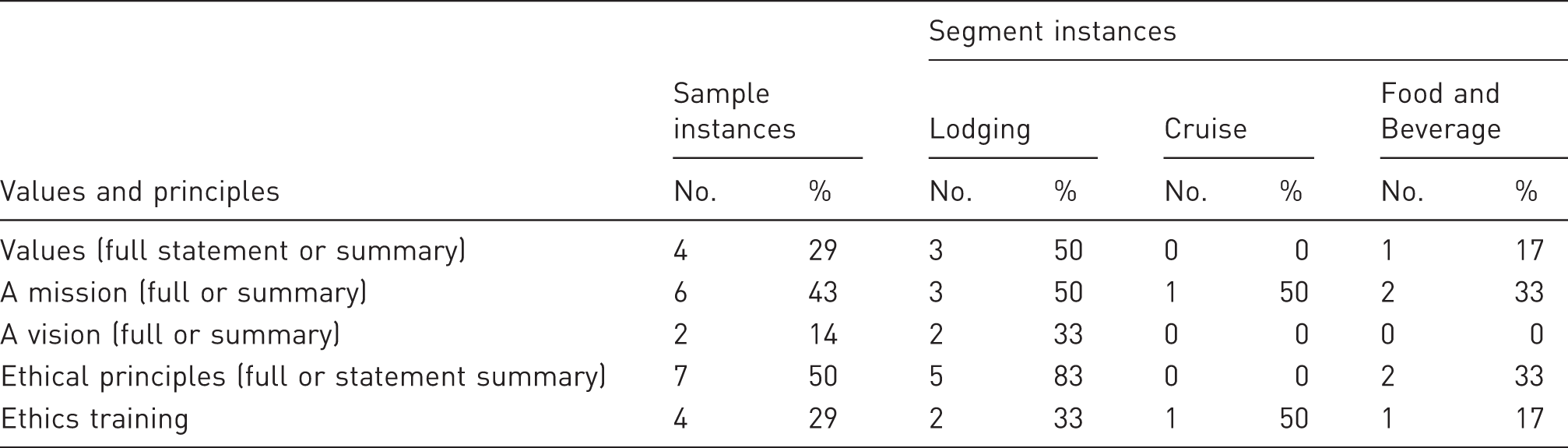

Values and principles

Values and principles.

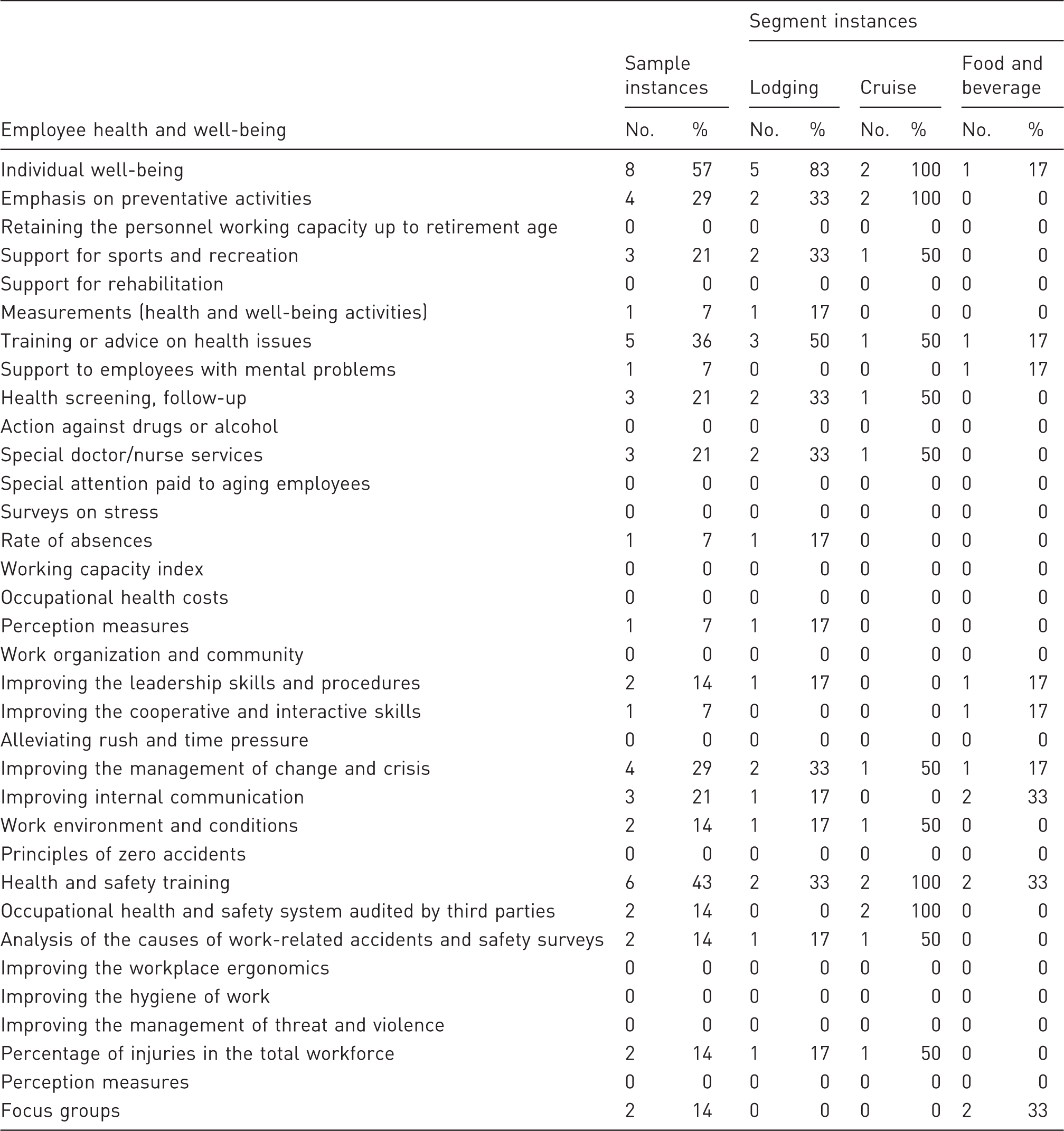

Employee health and well-being

Employee health and well-being.

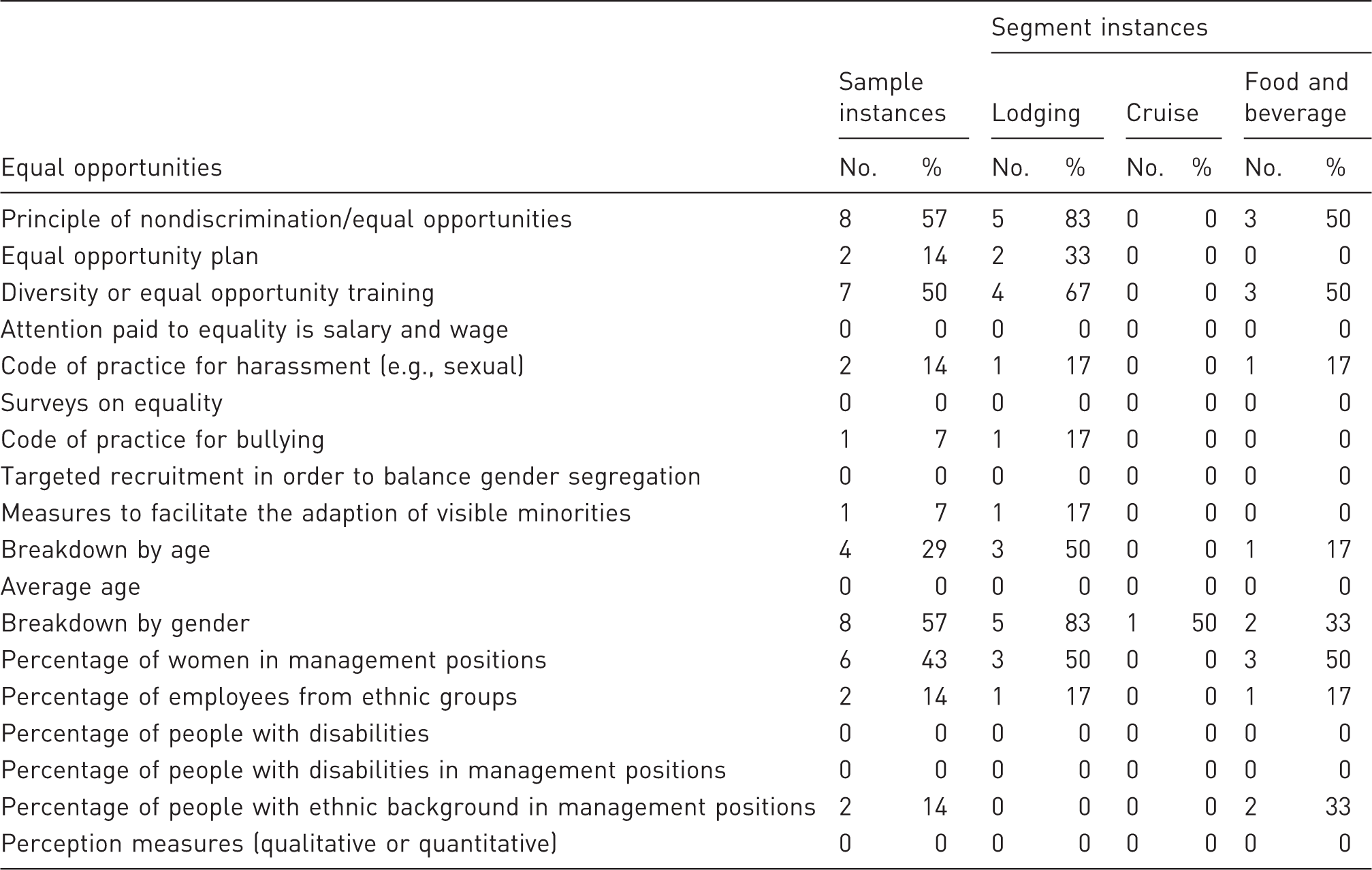

The data also suggest that firms are somewhat reluctant to disclose employee-related information since only two organizations openly disclosed the percentage of injuries in their workforce and while only one disclosed the rate of absences. Management of change and crisis was reported by only 28.6% of the firms. This finding was unexpected since management of change and crisis is often perceived as important factors in improving workplace working conditions. Additionally, only one firm (Starbucks Corporation) explicitly reported support for employees with mental problems, more specifically autism.

Measurement of policies

Measurement of policies.

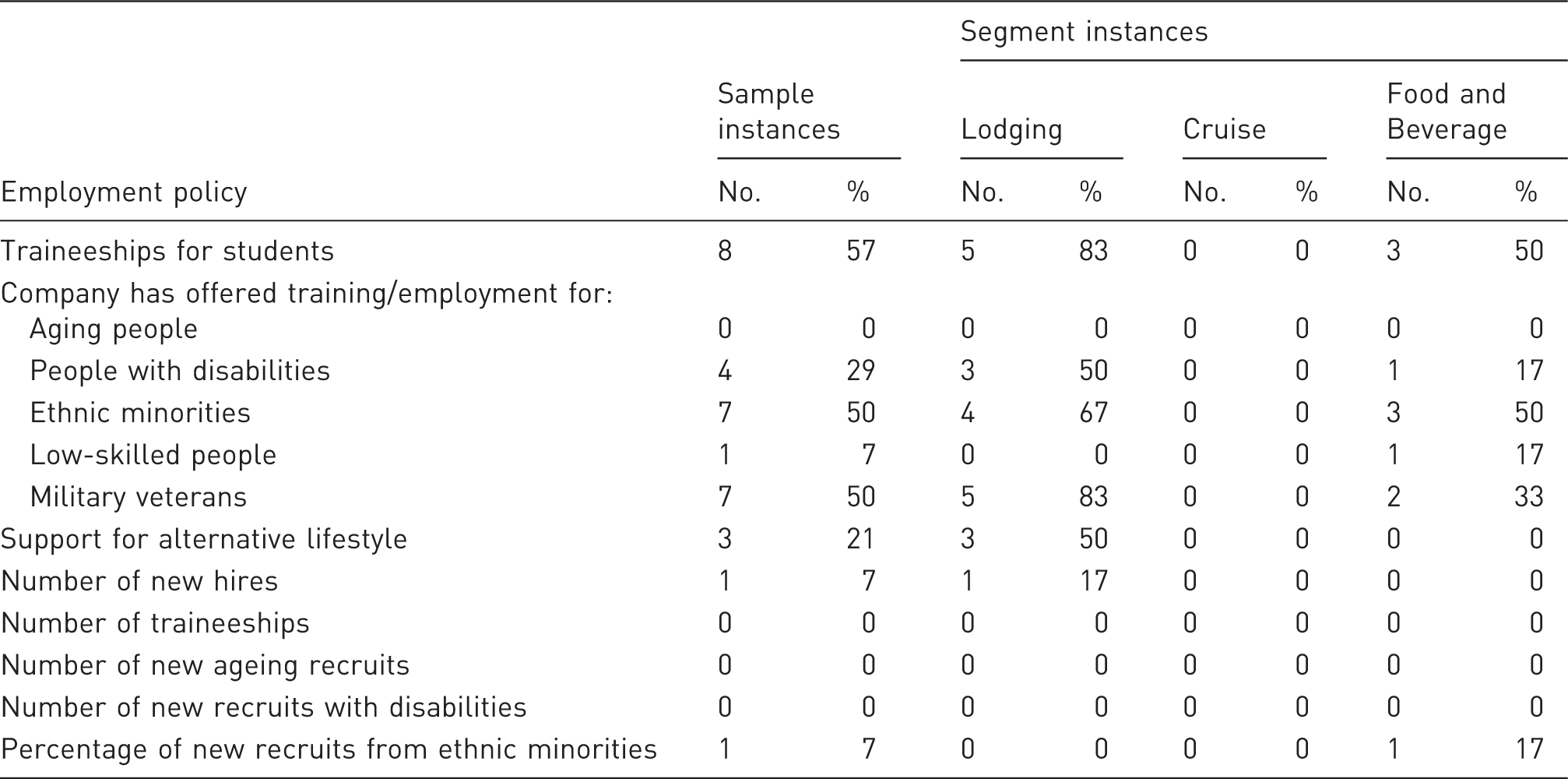

Employment policy

Employment policy.

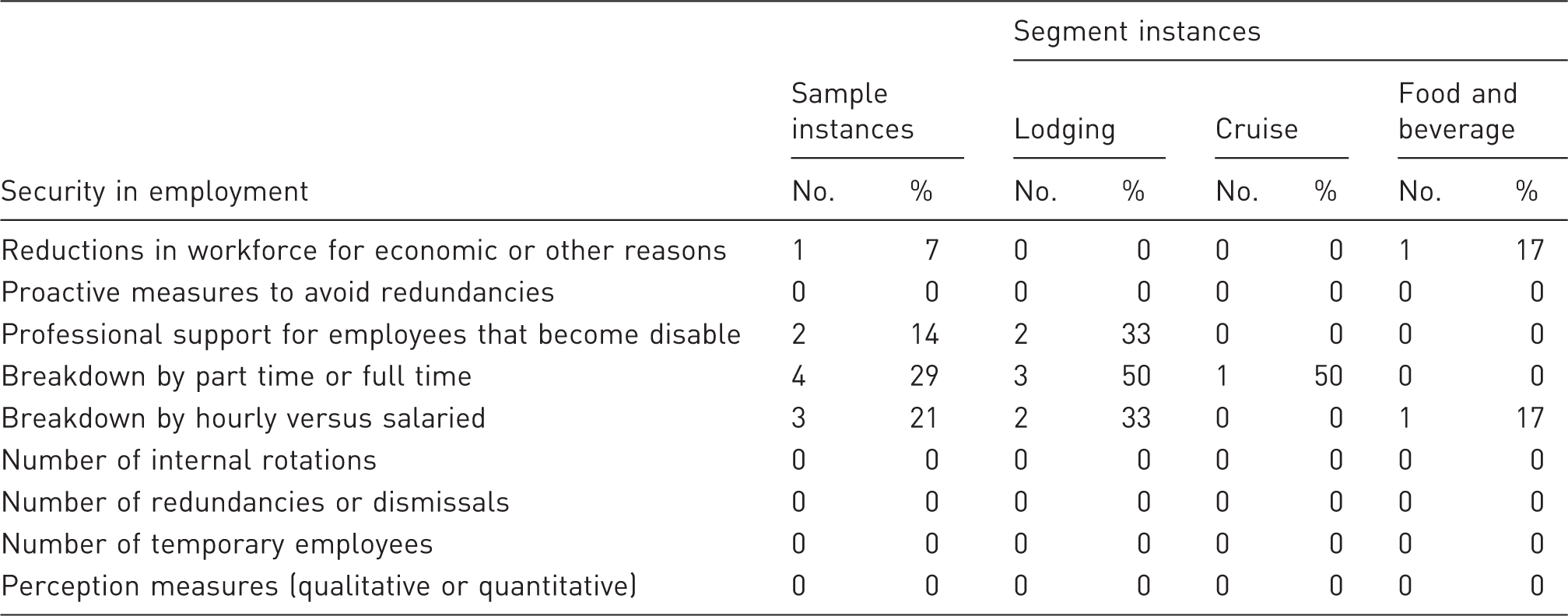

Security in employment

Security in employment.

Four organizations (28.6%) disclosed a breakdown by part-time or full-time employment and three firms (21.5%) disclosed a breakdown of hourly versus salaried employees. A small percentage of companies (14.3%) reported that they provided professional support for employees who become disabled. Only one firm, Dunkin’ Brands Group, disclosed information about initiatives aimed at addressing employees in the event of workforce reductions for economic or noneconomic reasons.

Equal opportunities

Equal opportunities.

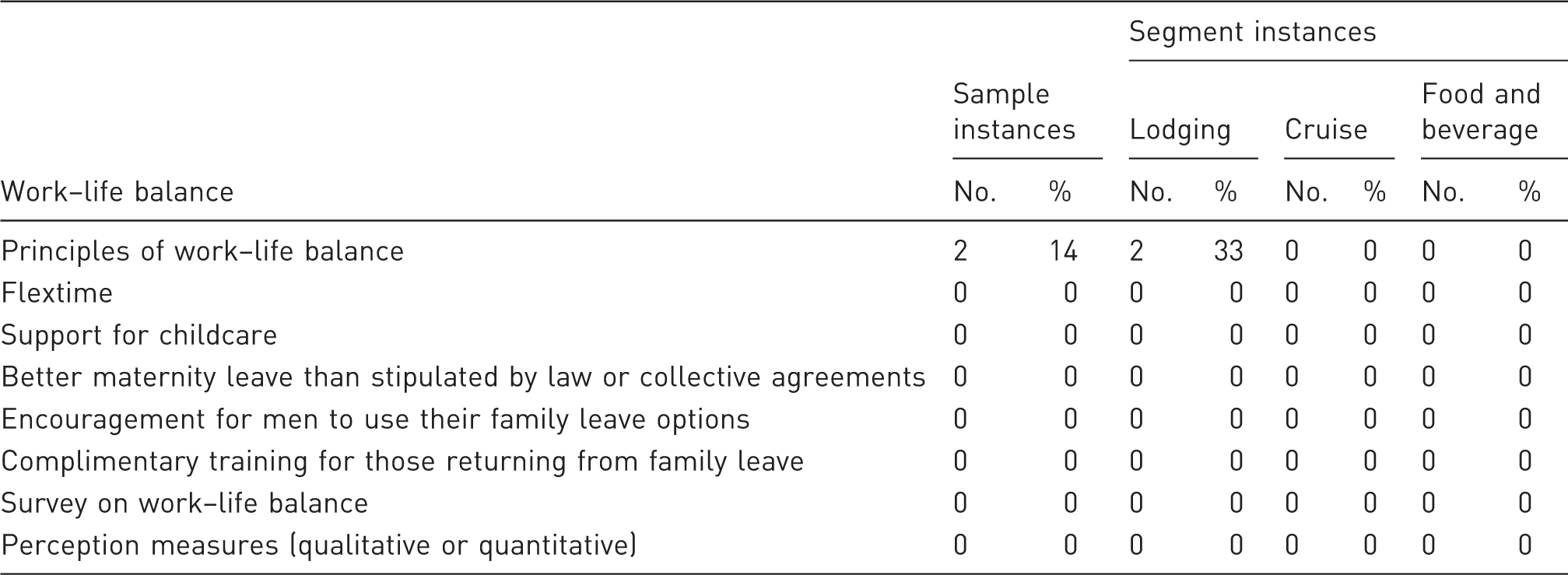

Work–life balance

Work–life balance.

Conclusion

CSR and sustainability implementation and disclosure are undergoing a rapid growth in the hospitality and tourism industry as stakeholders are demanding such actions from firms. In conjunction, hospitality and tourism firms are engaging in such practices to receive actual or ostensible benefits including: corporate reputation enhancement; increased employee and guest loyalty; attracting new investors; and increasing new market share and productivity. However, in recent years, stakeholders have become more concerned and interested not only in firms’ implementation of CSR and sustainability initiatives but also require more transparency via disclosure of information on such initiatives. Like most industries, firms in the hospitality and tourism industry have started to disclose information about their CSR and sustainability initiatives via CSR/sustainability reports. Given that such disclosures by hospitality and tourism firms are currently in their infancy, this research attempts to shed light on what aspects of CSR and sustainability firms within the sector are reporting.

General CSR/sustainability reporting was the dimension having the most instances of reporting. In fact the most reported categories included indicators that are often viewed as the foundation or the pillars of the triple bottom line, namely water, energy, and waste disclosures. This seems to suggest that firms often view sustainability and performance on CSR initiatives as intricately related issues. Community involvement, another pillar of the triple bottom line was the second most frequently reported component. This suggests that hospitality and tourism firms continue to strive to enhance their social reputation by highlighting their social activities in the communities in which they operate. The least reported dimensions were pays and benefits and work–life balance. As previously noted, it is plausible that firms did not perceive a need to disclose information about pays and benefits due to their dynamic and fluid nature. Other plausible reasons for nondisclosures could be: firm might not want to make this information publicly available to competitors; organizations might not see this subject as a potential competitive advantage; and firms might have chosen to focus on other areas of employee relations on their reports. However, given the importance of this dimension in today’s full disclosure and information relevant society, it could be beneficial for firms to disclose such information to inform relevant stakeholders about their fair compensation practices. Work–life balance information should also be disclosed by firms especially to improve their competitiveness for attracting the best and most talented job candidates. Thus, it is not sufficient for firms simple to have work–life policies and practices, instead, they should also disclose this information.

Like most empirical studies, this study had limitations that future studies are encouraged to overcome. First, the sample size utilized for this was small. This was not unexpected since CSR/sustainability reporting by hospitality and tourism limitations is a relatively new practice. It is hoped that future studies will replicate this study using a larger sample size. This study also utilized formal published CSR/sustainability reports and information found on firms’ websites. It is hoped that future studies will expend beyond these sources to include all relevant reports and other means by which companies can communicate with stakeholders such as press releases, publicity, and public relations reports. Moreover, future research could take a step further and investigate how a company can benefit from reporting on each specific indicator and construct a framework for best reporting practices in the industry. Additionally, the sample was drawn from US domiciled firms or those having a major corporate office in the United States. Future studies are encouraged to include firms domiciled in different countries since firms in these countries, such as those domiciled in Europe could have different or additional disclosure information.

Finally, the findings from content analysis of the CSR/sustainability reports of 14 hospitality and tourism firms, suggest that there is a vast difference between the levels of information reported by those firms in the industry’s sectors. Hotel or lodging firms report on a larger scale and on a greater number of issues than firms operating in the food and beverage and cruise line sectors. This suggests CSR/sustainability reporting in the hospitality and tourism industry is in its infancy, and as such, there is room for growth and improvement in the area CSR/sustainability reporting by hospitality and tourism firms.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.