Abstract

The present paper addresses the antecedents of cruise companies’ strategy implementation, focusing on mergers, acquisitions and alliances as potential alternative choices for managers. Specifically, a model for interpreting the drivers of such decisions is proposed, based on two dimensions: (1) the level of riskiness and complexity of the industry and (2) the importance of the acquired resources and capabilities for the competitive advantage of the acquiring firm. The theoretical model is then applied to the cruise industry, through a qualitative analysis on three case studies based on the major companies: Carnival, RCCL, and Star Cruise–Norwegian Cruise Line (Genting Group). Such industry represents an ideal set for studying the issues, as, in the last few years, the growing turbulent environment has increased the number of mergers and acquisitions and strategic alliances with other partners belonging to the same supply chain. The results show that in the cruise tourism industry, the two aforementioned dimensions seem to matter in firms’ choice between the different external growth strategies, highlighting the presence of homogeneous behavioral models among the cruise companies. This contribution presents some valuable research implications, useful for researchers and academics, but also professionals and policy makers may benefit from this knowledge.

Keywords

Introduction

The cruise industry has been considered as one of the fastest growing segments of the global travel and leisure business since the late 1980s (Cruise Line International Association, 2015; Cruise Market Watch, 2016; Dowling, 2006; Dowling and Weeden, 2017; Wild and Dearing, 2000) and is still rapidly growing. During the 1990–2007 time frame, the industry experienced a dramatic traffic expansion with an average annual growth rate of 7.4% (Brida et al., 2013), while since 2008, the cruise tourism industry has continued to increase but at a slower pace, falling down to around 3% annual growth rate in the last three years (2013–2015), and reaching 22.24 million passengers worldwide in 2015 (Dowling and Weeden, 2017).

Despite its continuous growth, cruise-related literature represents only a small portion of published tourism academic contributions (Papathanassis, 2017) and it has only recently attracted a rising interest from academics and practitioners. Papathanassis and Beckmann (2011) highlighted that cruise-related published research tends to be fragmented, descriptive, and focused on social science domain. From a managerial and economics perspective, most contributions dealing with the cruise industry belong to the tourism management and service management domains or to the maritime economic approach (Lekakou et al., 2009; Rodrigue and Notteboom, 2013) and are focused on several research themes, such as the evolution of the demand/supply of the industry (Cartwright and Baird, 1999; Dowling, 2006; Kester, 2003), the implications of cruise tourism on port destinations (Dwyer and Forsyth, 1998; Penco and Di Vaio, 2014; Satta et al., 2015) and the cruiser’s behavior (Hung and Petrick, 2011; Petrick et al., 2017; Satta et al., 2016).

Following the results of an in-depth systematic review of the cruise research literature, Papathanassis and Beckmann (2011) stated that extant literature is still limited with respect to the wide managerial and economic implications stemming out from cruise activities; in particular, only few academic contributions have addressed strategic management and business administration topics (corporate strategies, managerial accounting, human resource planning and development, supply chain management, and outsourcing) of the cruise companies (Penco et al., 2017; Vogel, 2009, 2017; Weaver, 2005; Wie, 2005), despite the increasing competition and concentration in the industry underline this research domain’s relevance and rationale.

In particular, cruise companies’ corporate strategies, together with their drivers and implementation paths, represent an underdeveloped research area (Vogel et al., 2012), with most of the studies focused on brand strategies (Hwang and Han, 2014; Vogel, 2009) or the impact of Mergers and Acquisitions (M&As) on brand image (Lee et al., 2011). In this vein, the present paper tries to extend tourism strategic management literature investigating, among the antecedents of cruise companies’ strategy implementation, M&As and alliances as potential alternative choices for managers. Since such corporate development initiatives are central to the growth and change of cruise companies, they are central to cruise management literature and their study could represent an important building block for the development of cruise management domain.

The industry represents an ideal set for studying such issues, as the increasing turbulent environment has forced cruise operators toward growing strategies that follow different paths. Since 1990, cruise tourism industry has known a staggering growth of the number of M&As that led to an high level of industry concentration (the three majors companies accounted for approximately 83% of the global passengers); moreover, cruise line companies have been involved in several strategic alliances with other partners belonging to the same supply chain.

In particular, our aim is to answer to the following research questions (RQ): RQ1: Which are the main strategy implementation paths followed by cruise line companies? RQ2: Which are the antecedents of firms’ choice between mergers and acquisitions (M&As) and alliances? RQ3: Is it possible to find homogeneous strategic behaviours adopted by cruise line companies?

The theoretical model is then applied to the cruise industry, through a qualitative analysis on three case studies, focused on the major companies and their M&As and alliances in the last 15 years.

The results show indeed that, in the cruise industry, the two aforementioned dimensions seem to matter in firms’ choice between M&As and alliances.

In seeking to answer to the aforementioned research questions, the present study contributes to extant academic literature in several ways. It firstly develops tourism management literature by exploring the strategic motivations of M&As and alliances implemented by cruise line companies. The study could, in fact, advance cruise management literature, which has not fully been investigated (Penco et al., 2017; Vogel et al., 2012). Moreover, the manuscript extends strategic management studies by developing an overall conceptual framework on the antecedents of the choice between M&As and alliances. While alliances and M&As are typically considered to be alternative choices for firms interested in combining their resources (Wang and Zajac, 2007), relatively little is known as to when firms should pursue one vs. the other (Dyer et al., 2004; Frehse, 2012; Profumo, 2017; Yin and Shanley, 2008). It is however important to identify what are the key factors in deciding which growth option a company should choose. The proposed model could also be applied to other industries, testing its validity.

The study has also several valuable implication for both managers and policy makers. It contributes to outline the relevance of certain resources/activities in the choice between different external growth strategies. Moreover, for policy makers, the study highlights a developing trend of cruise companies to control port terminals that could lead to an excessive raising of entry barriers for new cruise operators, thereby making the access to the port less convenient for cruise companies that are not “also” terminal owners.

The remainder of this paper is organized as follows. The first section, addressing the extant literature on the antecedents of strategy implementation, provides the theoretical background useful for the development of the interpretative theoretical model. The second section introduces the current trends and structure of the cruise industry. The third section proposes the research method and the followed procedure, while the fourth section discloses the main implementation paths followed by the three selected case studies (Carnival, RCCL, and Star Cruise). The fifth section, instead, presents the application of the conceptual model to the selected cruise line companies, together with an in-depth discussion of the results, as well as suggests implications for academics, managers, and policy makers. The last section concludes and explains the main study limitations and further research.

The drivers of external growth strategies

The choice among the different implementation paths of firms’ corporate strategies is a key decision for firms’ survival and value creation. That is why a wide international literature belonging to financial, legal, economic, and managerial backgrounds has already developed on the theme. A special attention has been dedicated to the determinants of the different external implementation paths, although the strategic management literature on this topic has not reached shared results yet, being rather fragmented and focused on single strategy implementing instruments (Frehse, 2012; Profumo, 2017).

As regards M&As, scholars can be essentially grouped into two broad categories (Seth, 1990): “value-maximizing” and “non-value-maximizing.” The “value-maximizing” determinants are related to the concept of synergy, i.e. the value of the businesses combination exceeds the sum of each individual business value (Jensen and Ruback, 1983), that may be prompted by economies of scale and scope (Williamson, 1968), by increased market power (Eckbo, 1983; Ellert, 1976; Fee and Thomas, 2004), by redeployment of assets and transfer of resources and competences (Capron et al., 1998; Haleblian et al., 2009), by learning processes that augment the knowledge base, resources, and capabilities of the acquirer firm (Collins et al., 2009; Ferreira, 2014) or by the coinsurance and risk effects (Galai and Masulis, 1976; Lewellen, 1971). The latter, instead, takes in all those who prefer reasons related to the management’s personal advantage at the expense of stockholders (Manne, 1965; Marris, 1964) that sometimes may destroy shareholders’ value. In this sense, following the “hubris hypothesis” (Roll, 1986), Malmendier and Tate (2008) found that often overconfident CEOs overestimate the generation of returns and as a result overpay for target companies.

As regards, instead, the literature on the determinants of alliances, it is possible to discern scholars related to the concept of value creation, to be achieved through transaction cost efficiency (Williamson, 1975), through the improvement of the competitive position (Cools and Roos, 2005; Hamel, 1991) or the attainment of a certain level of economies of scale (Dussauge et al., 2000), from those who, following the resource-based view of the firm, found other strategic motivating forces, such as the sharing of resources and expertise (Hamel et al., 1989) or the generation of new competences (Tjemkes et al., 2013).

Despite the aforementioned wide literature on the determinants of the external corporate strategies, it emerged a scarcity of comparative studies aiming at understanding the drivers inducing a company to choose among the different external growth modes and, specifically, between M&As on one side, and alliances on the other. Prior research has, in fact, specialized on one instrument but not the other, with very few studies considering the two implementation paths interchangeable (Wang and Zajac, 2007). The choice between acquisitions and alliances has been studied in the context of foreign market entry (Anderson and Gatignon, 1986; Hennart and Reddy, 1997), but only few studies (Garette and Dussauge, 2000; Profumo, 2017; Villalonga and McGahan, 2005; Wang and Zajac, 2007; Yin and Shanley, 2008) have investigated the issue in more general terms. Notwithstanding, the selection of the way to grow represents a core question for management teams (Capron and Mitchell, 2012) and scholars have argued that such choice is among the most important decisions a firm makes concerning its corporate development (Dyer et al., 2004; McCann et al., 2016).

A first attempt has been developed by Hennart and Reddy (1997), analyzing the investments of the Japanese firms in the United States. They found that joint ventures are preferred when the target assets are strictly linked to unneeded assets, thus making M&As less “digestible.” They also showed that the greater the enterprise knowledge of the new business market, the higher will be its proclivity to plan M&As rather than collaborative relationships.

According to the resource dependence theory and the transaction cost theory, Yin and Shanley (2008) identified in the trade-off between commitment and flexibility the choice ground between M&As and alliances. Hence, in the most unstable and risky businesses, it is likely to prevail the demand of flexibility, thus preferring collaborative forms of growth, while in businesses where large investments are required—e.g. to exploit economies of scale and of scope—the commitment requirement will be chosen thus favouring more stable forms of partnerships.

By focusing their attention on the resources and capabilities of the enterprises involved in the growth process and using the resource-based view of the firm, Wang and Zajac (2007) remarked that the more resource similarities and expertise between the companies are present, the more they will tend to choose M&As rather than alliances; on the contrary, high levels of resource complementarity of the two firms are more likely to trigger companies to choose alliances rather than M&As. McCann et al. (2016), instead, reported how a shared cluster location fosters lower levels of information asymmetry between partners, leading the firms to employ acquisitions rather than alliances. On the other hand, Profumo (2017) highlighted that the drivers of external corporate strategies, within the passenger air transport industry, are related to the importance of the efficiency for attaining competitive advantage, as well as to the business risk and complexity degree of the business environment.

According to the proposals of Yin and Shanley (2008) and Profumo (2017) concerning the creation of an interpretative model for the external drivers of corporate strategies, it is useful to start pointing out the differences between M&As and alliances. From the control viewpoint, these two modes differ sharply (Cools and Roos, 2005; Yin and Shanley, 2008): M&As imply a strong control with a majority or controlling ownership, whereas in collaboration forms the control is shared, thus involving more complex management issues—even if they seem to be more flexible and easier to exit if necessary.

This factor has strong cost implications: the control rights allow more thorough exploitation of the combined organizational resources, such as the production concentration in a single plant, the reduction of the production lines, or the use of common IT platforms, being able to back the utmost potentialities to achieving cost-savings (Garette and Dussauge, 2000). On the contrary, these choices are difficult to be implemented through control sharing, due to the need of mediation among conflicting interests.

On the other hand, the large disbursements required for takeovers are not tailored for high-risk situations and environmental uncertainty. Therefore, in these events, partnerships seem to be more useful, since they are more flexible and reversible (Cools and Roos, 2005; Dyer et al., 2004).

By examining the different dimensions, it therefore appears that the external growth modes present two key differences (Garette and Dussauge, 2000; Profumo, 2017; Yin and Shanley, 2008). Firstly, alliances allow partners to share the risk and are reversible processes—thus being more flexible and able to face both complexity and risk compared to M&As. Secondly, alliances give less control over resources than M&As. Therefore, when the appropriation of such resources, capabilities, and expertise becomes crucial for the achievement of the competitive advantage, M&As are to be preferred.

Thus, an interpretive model able to join the different implementing logics of the external growth strategies should be based on these two variables: (1) riskiness and complexity of the business in which the firm is operating, or would like to operate, (2) as well as the importance of the resources, capabilities, and expertise to be acquired for the competitive advantage of the acquiring firm.

The acquisition of control rights implies greater risks for companies compared to alliances, but it also enables the total control and the resources’ exploitation of the acquired entity—and this is even more important when these resources are critical for achieving a competitive advantage (Yin and Shanley, 2008). On the contrary, in case of severe unstable and dangerous environmental situations, it is better to pursue the growth through the share of control, which allows to invest less resources (even financial resources) and less expertise, as well as to distribute the risk among several parties and it appears to be a reversible process.

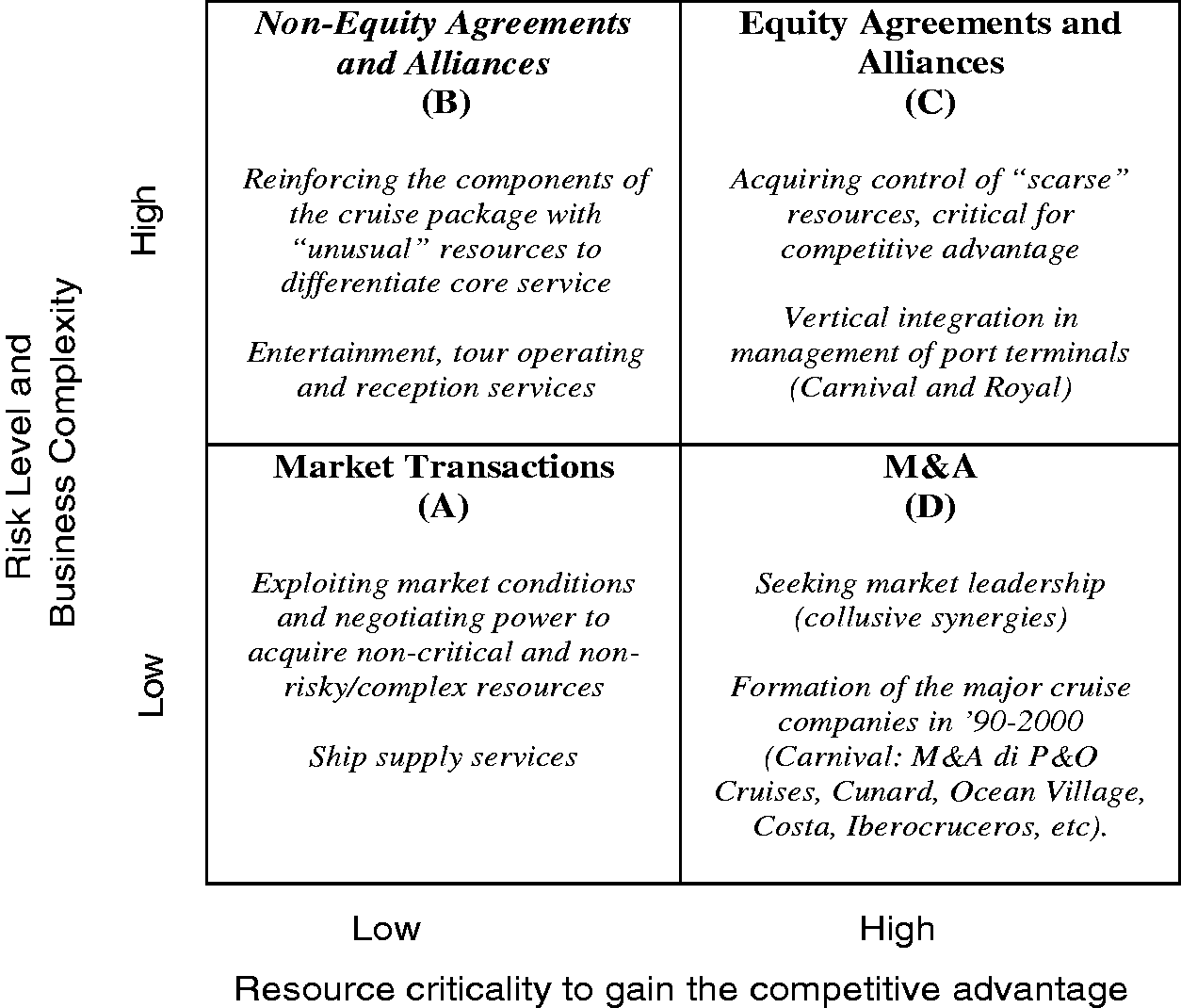

Building an interpretative scheme, these variables may be located on an ideal Cartesian coordinate system, where the four quadrants of the matrix correspond to four different modes to pursue external growth strategies (Figure 1).

The implementation of external growth strategies. Source: Our elaboration.

A first dimension is related to the level of riskiness and business complexity in which firms are operating or intend to operate. When the environmental complexity and the risk level of the industries in which a firm wants to invest are sharpening, the company will tend to seek collaborative forms of growth in order to share the incurred risk and to curb the resources, expertise, and competences. From this viewpoint, the risk level could also increase with the raise of the transaction costs, including those related to the lack of knowledge of the new market, as already pointed out by Balakrishnan and Koza (1993).

The second dimension shows, instead, the importance of the acquired resources and capabilities for the achievement of the competitive advantage of the acquiring firm. If these resources and capabilities are important, but not crucial for the competitive advantage of the acquiring firms, the likelihood that companies will pursue forms of collaborative development should increase: the full control over the resources is not essential. But, if the resources to be gained are crucial to win in the competitive arena, and if they are strongly firm specific, the total control will allow their appropriation and exploitation.

The quadrant (A) features low business complexity, low risk levels, and limited importance of the new resources to attain the competitive advantage.

When the target industry is not so risky and complex due to previous knowledge and similarity to the firm original business activity, less transaction costs from market imperfections are likely to emerge; if the assets are not mainly firm specific, no significant advantages will derive in adopting M&As or alliances, in comparison to mere market transactions that are less expensive. Furthermore, in such industries, the resources to be gained by the firm are not particularly critical for attaining the competitive advantage. Therefore, according to the proposal of Yin and Shanley (2008), it is possible to postulate that, in this quadrant, the growth is implemented through market transactions, which enable faster target achievements with little financial outlays.

In the quadrant (C), the business risk and complexity levels are high and the acquired resources and capabilities are critical to achieve the competitive advantage. This quadrant is, indeed, the most complex to interpret, since the two axes highlight opposite trends.

On the one hand, the high complexity and risk level of the business lead to engage collaborative arrangements aiming at limiting risks and invested resources—this is even more true when the new industries are more “distant” and complementary from the starting one (Wang and Zajac, 2007). But, on the other hand, the severe criticality of the resources to acquire seems to drive toward solutions with a higher degree of control.

Hence, this quadrant shows external growth modes based on collaborative arrangements with higher control levels, such as equity agreements and alliances. In industries very different from the original one, characterized by a strong dynamism and competitiveness and resulting from vertical integration strategies or diversification, such instruments allow to better face the risk and, at the same time, to exercise some control. The scale alliances, that represent an alternative to the concentration processes implemented through M&As (Hennart, 1988), fall within this definition when the external environment is particularly turbulent and complex.

The two dimensions shown in the quadrants (B) and (D) present opposite levels thus being easily understood. In the first case, the high risk and complexity of the industry are offset by the lower critical resource demand. Therefore, companies are dealing with high risk and uncertain markets characterized by high transaction costs, such as new industries or new geographically and culturally far markets, in which are seeking complementary resources and capabilities that are, anyway, not critical for their competitive advantage. In these cases, the non-equity alliances seem to be more suitable to the purpose, especially risk sharing alliances, since they do not require the full control on the created resources and capabilities.

On the contrary, the quadrant (D) features a low level of business risk and uncertainty against an high importance of the acquired resources and capabilities for the competitive advantage of the acquiring company. In this case, growth should be implemented through M&As since target industries seem “known” by the firms and characterized by low transaction costs, and also because the full control of the critical resources is crucial to achieve scale advantages and market power. Therefore, market transactions are not advantageous. For example, we can locate in this quadrant the M&A transactions aiming at expanding the firm market share in the same industry and achieving collusive synergies. The increase of the resources and capabilities becomes, indeed, critical to expand market power, thus improving firm profitability with the elimination of a real or potential competitor.

Market trends and structure of the cruise industry

The cruise industry is a “unique industry” (Clancy, 2017). It presents some structural features which make it a peculiar business both in the tourism and the shipping sectors (Wild and Dearing, 2000). Such industry is a “scale intensive” industry, characterized by significant economies of scale. Finding similarity with the airline industry, “cruise industry presents two main categories of such saving: economies of density and economies of fleet size” (Papatheodorou, 2006).

Moreover, the cruise industry leverages the efficiencies and the synergies emerging from the economies of scale and, hence, the entry barriers are high (Clancy, 2017). The sources of the entry barriers are related not only to the economies of scale but also to brand awareness and associated reputation effects, relationship with the distribution channels, i.e. agencies and tour operators, and with complementary players in the cruise value system, the access to ports and their associated facilities (cruise terminals).

Differently from other shipping markets in which the demand is derived from trade and is rather price inelastic, cruise lines companies have the opportunity to carry out a “supply push” strategy, creating new demand through pricing, brand/marketing, and the deployment of new cruise ships (Dowling, 2006). Recently, the advent of e-commerce and the use of social media in order to create dialogue with potential customers has created further challenges (Pantelidis, 2017).

Although the cruise industry has been increasingly characterized by standardization of services and by the importance of cost leadership, differentiation is becoming a relevant competitive weapon. Cruise companies are challenged to create differentiated cruise packages composed by a high-quality level of on-board services and shore-based activities (excursions) offering the chance of visiting new cultures and touristic attractions, together with integrated transfer to/from the ship (Brida et al., 2011; Lee and Ramdeen, 2013; Lekakou et al., 2009; Lois and Wang, 2005; Teye and Leclerc, 1998); in this way, cruise companies may create additional revenue streams through the provision of goods and services sold on board and through the sale of touristic excursions in the port of call (Biehn, 2006; Klein, 2006; Vogel, 2017; Weaver, 2005). Finally, compared to the other traditional segments of the entire tourism sector, cruise companies have the possibility to geographically reposition ships and to exploit the geographical complementarity between the different cruise destination areas connoted by opposite seasonality (Charlier and McCalla, 2006; Rodrigue and Notteboom, 2013).

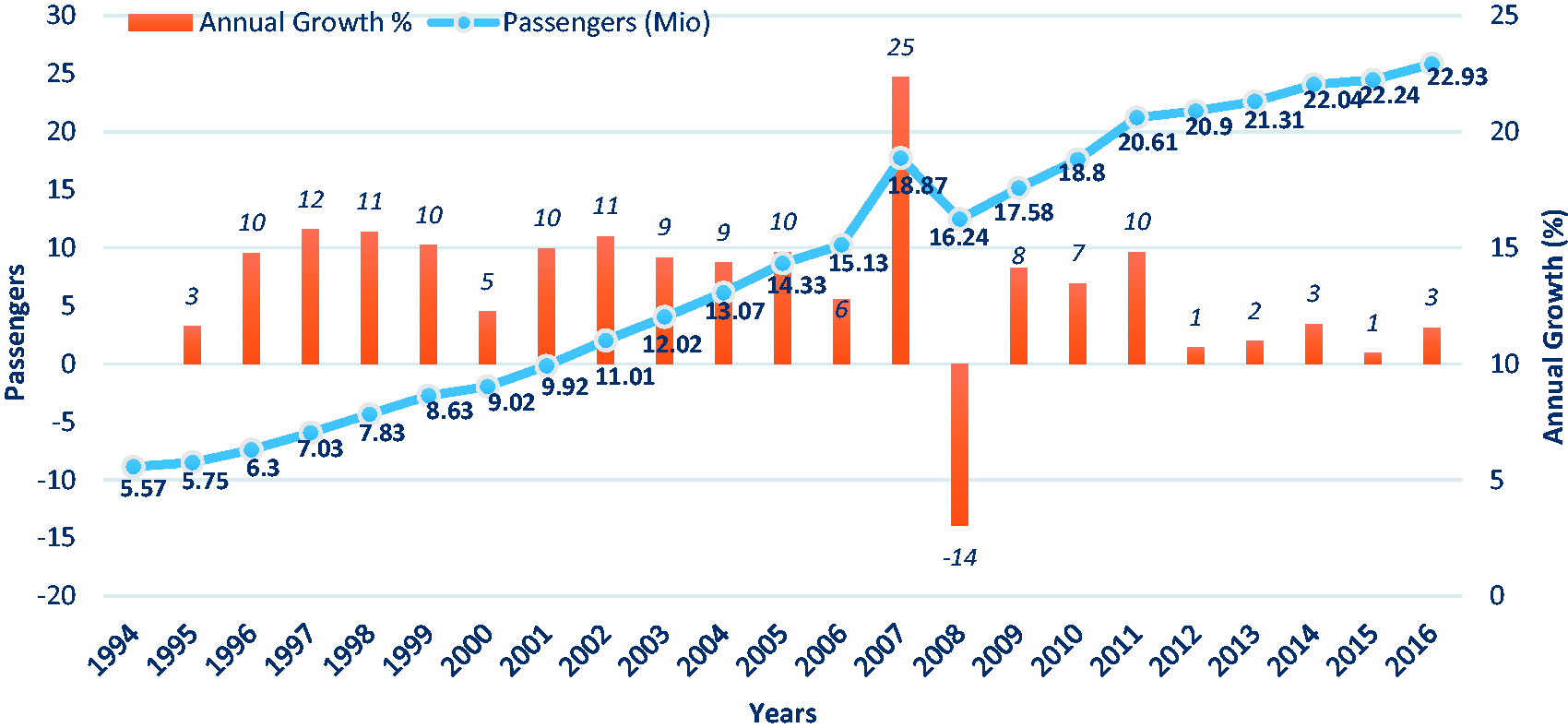

The global cruise industry has grown at a remarkable rate since 1980 (Wild and Dearing, 2000). From 500,000 cruise passengers in 1970, the global demand has reached 22.9 million passengers worldwide in 2016 (Figure 2). This industry is one of the most attractive of the of blue economy and tourism sector (Clancy, 2017; Dowling and Weeding, 2017; McKee and Chase, 2003; Penco and Di Vaio, 2014): the low market penetration and favorable demographics in the key markets and new areas (i.e., China) suggest that continued growth should be possible for the predictable future (Dickinson and Vladimir, 2008; Dowling, 2006; Petrick et al., 2017; Weaver, 2005). In particular, the global cruise industry has experimented a dramatic boom in China (Dowling and Mao, 2017; Petrick et al., 2017), since it is estimated that China will become the second largest market after USA by 2017.

Evolution of the world cruise industry. Source: Our elaboration on Cruise Market Watch (2016).

The deployed capacity has increased of 84.2% from 2003 to 2014, growing from 73 to 134.5 million of lower berths (Rodrigue and Notteboom, 2013). Taking into account the positive demand forecast, the order book of the major shipbuilders confirms the spectacular growth of the industry. The new ships are becoming larger (mega ships), in order to implement economies of scale (Clancy, 2017; Papatheodorou, 2006); the 30% of the new ships launched between 2004 and 2013 can, in fact, accommodate over 3000 passengers and, in the next years, the average size of cruise vessels will increase. The largest cruise vessels in the world are Royal Caribbean International’s three “Oasis of the Seas” with a size of above 225,000 Gross Registered Tonnage (GRT) (Dowling and Weeden, 2017): Harmony of the Seas weights 227,000 GRT and has capacity for 5496 passengers and 2300 crew.

The mega ships represent in themselves the destination, acting as a floating resort with a high variety of attributes and facilities (bar, swimming pools, spa, casino, theaters, restaurants, boutiques, etc.). This allows cruise companies to create a captive market within the vessel and for on-shore excursion services, hence providing additional opportunities of revenue sources (Klein, 2006; Toh et al., 2005). Vogel (2017) states that the onboard revenues of RCCL and Carnival account for 25% of overall revenues, exceeding the sum of their respective costs of onboard business and operating profit.

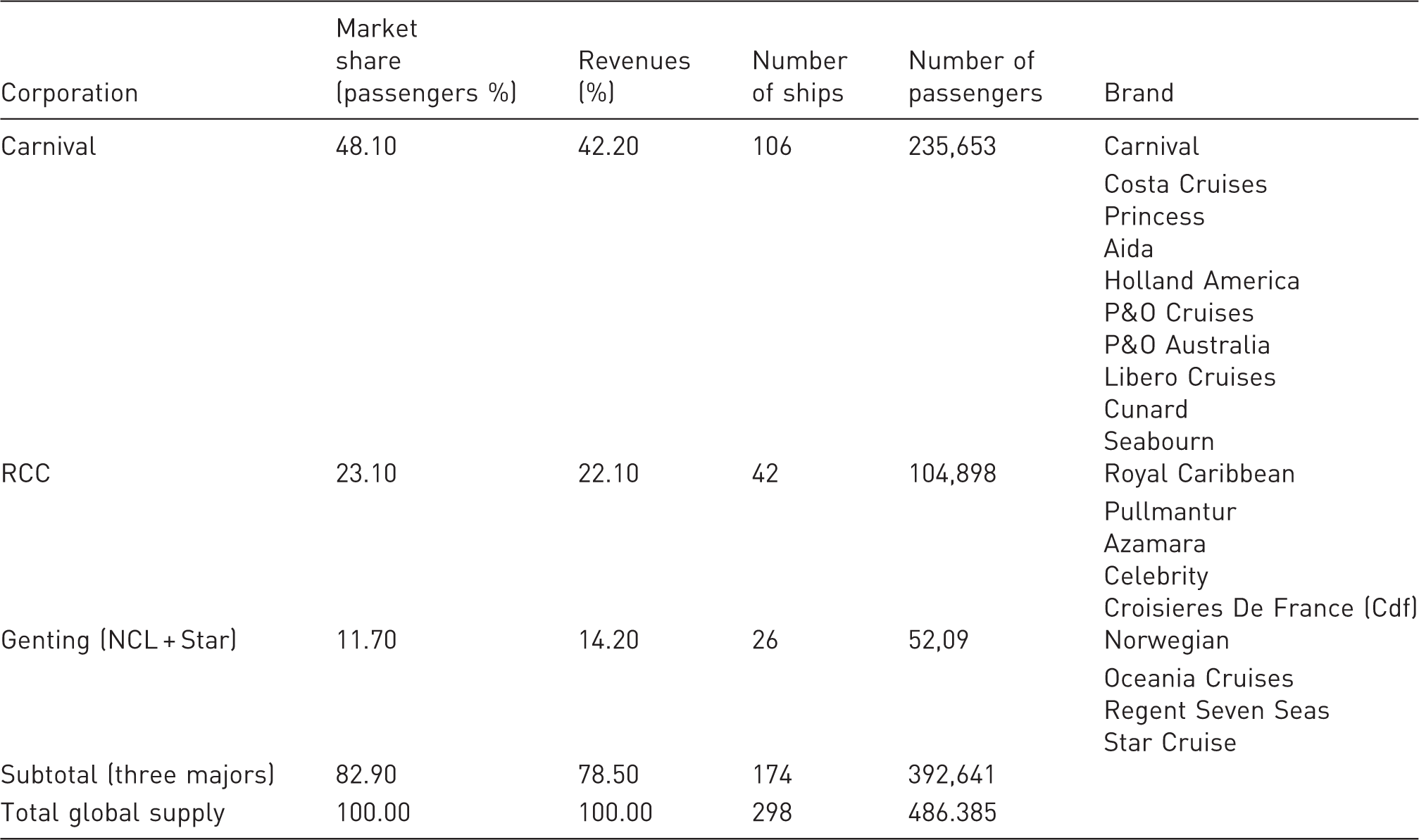

The cruise industry is characterised by a very high level of concentration, since the three largest cruise companies (Carnival Corporation & Plc., Royal Caribbean Cruises Ltd, and Star Cruises–NCL) account for 83% of the market in terms of number of cruise passengers (Clancy, 2017). This level of concentration is the consequence of the growing level of capital intensiveness of the industry due to the investments in new mega ships. Such concentration has been reached through an intense wave of M&As (Clancy, 2017; Cruise Line International Association, 2015; Cruise Market Watch, 2016; Lekakou et al., 2009), implemented by the leading cruise companies in the last decades. Cruise companies strategically have invested in M&As in order to block entries by potential competitors, to have a cost advantage in the post-entry competition due to the exploitation of economies of scale, to increase market share and to preempt subsequent expansions by incumbent competitors (Wie, 2005). Moreover, cruise line companies have been involved in several strategic alliances with other partners belonging to the same supply chain (e.g., tour operators, entertainment operators, catering suppliers, port terminals), in order to reinforce their competiveness.

Notwithstanding the increasing industry concentration and competition, there is little evidence of research in this area, with few studies focused on the impact of M&As on brand image (Lee et al., 2011). Therefore, this literature gap highlights the relevance and the rationale of the study of the antecedents of cruise companies’ strategy implementation.

Methodology

Case studies are particularly useful when the topic of the research is the understanding of complex phenomena (Yin, 1994). The case study design adopted in this work may be described as a multiple case study (Eisenhardt, 1989; Yin, 1994). Multiple case designs are, in fact, appropriate when a researcher wants to achieve a deep understanding of a specific multidimensional complex phenomenon, such as corporate strategies, going beneath the surface of a situation and using a replication strategy. If all or most of the cases provide similar results, there can be substantial support for the development of a preliminary theory that describes the phenomena (Eisenhardt, 1989).

Key numbers of the three major cruise companies.

Source: Our elaboration on CLIA (2015) and Cruise Market Watch (2016).

In order to develop the cases, we collected heterogeneous data exploring different topics:

‐ the principal features of the cruise groups and their business segments; ‐ the evolution of their corporate strategies; ‐ the number, typologies, and characteristics of M&As and alliances that each cruise group implemented in the last years; ‐ the motivations behind the different strategy implementation instruments (M&As and alliances) used by the companies.

For analyzing all the previous topics, the authors have collected different data, in the period December 2015–March 2016, using multiple data collection techniques:

‐ use of the Capital IQ Standard and Poor's database for gathering information on M&As, alliances (equity and non equity) and partnerships developed by the three cruise companies until the end of 2015. The attention has been focused on the principal operations made by the “ultimate parent company” or other subsidiaries whose “primary activity” belongs to the cruise industry. All the buyback and intragroup operations have been excluded, together with the buying and selling procedures of ships. The database contains information on all the transactions in which a company has been involved (M&As, private placement, buyback) and all the implemented strategic alliances. In particular, as regards M&As, we gathered data on announcement and closing date, the target of the transaction, the buyer and the seller, the size of the operation, the primary industry and business description of the target, together with the link to the original documents; as regards, instead, the strategic alliances, we collected information on the companies involved, together their primary industry and business description, date and name of the alliance (if applicable). ‐ analysis of several secondary sources for each operation (M&As and alliances) identified from the database. In particular: company’s press releases, company’s websites, company’s investor presentations, Annual Reports, articles from magazines and newspapers; ‐ personal semi-structured interviews with experts of the cruise industry, such as a Cruise Line International Association (CLIA) officer and maritime agents operating in different Italian and international ports, which took place in April 2016.

Each case study is therefore based upon a mix of descriptive analysis and semi-structured interviews to elicit the growth implementation paths followed by the cruise operators and the antecedents of the choice between M&As and alliances.

The collection, analysis, and interpretation of data followed the principles recommended by Spiggle (1994), moving back and forth between the stages, as an iterative process, until we reached a high level of confidence with the data and their interpretation. In particular, the mixed methods approach presented the ability to cross validate information obtained from different sources. The case studies were in fact built from data gathered from primary and secondary sources and were written independently of each other, to maintain the independence of the replication logic. Furthermore, this methodological approach provided a higher level of credibility to the findings since the findings were able to be triangulated. Guided by our theoretical framework, we then built the insights emerging from the case studies.

M&As and alliances in the cruise industry: The results of three case studies

The analysis of M&As and of the partnerships and alliances implemented by the three major players will help to answer the first research question, related to the main strategy implementation paths followed by the cruise companies.

Carnival Group

Carnival Group is the world largest cruise line, operating with ten different brands and 100 ships with more than 212,000 cruise berths (Clancy, 2017). Its aggressive expansion policy has been forced by two main drivers: market penetration via new ship orders and marketing policies and internationalization through brand takeover. After consolidating its leadership in the American market (mature market), Carnival Group has extended its strategies to other geographical markets through M&As of leading brands/companies: P&O Cruises, Cunard and Ocean Village for the UK market; Costa for Italy, France, Spain, and Germany; Iberocruceros for the Spanish market. Carnival has maintained the brands of the target companies and their operational autonomy, especially with regard to marketing and sales (Rodrigue and Notteboom, 2013; Vogel, 2009).

Its strategic expansion is mostly based on M&As, acquiring brands/companies operating in geographic markets where there is a high brand loyalty and awareness (i.e., the brand “Costa” in the Mediterranean Sea and in Europe). Such acquisitions of existing cruise companies may be positioned in the quadrant (D) of the proposed model; the antecedents of the external growth, in fact, are linked to the direct control of critical resources for reaching a sustainable competitive advantage and achieving collusive synergies, in the same industry (thus the level of risk/complexity appears to be modest). The wave of horizontal acquisitions appears to have stopped; the industry, in fact, is now quite consolidated and is characterized by an oligopolistic configuration.

More recently, Carnival has implemented few vertical alliances with different actors belonging to the same cruise supply chain. In order to increase the quality of its services on board/a-shore and in order to globally promote its cruise products, Carnival has entered into alliances with partners belonging to the entertainment system (e.g., the collaboration with the New York Times is aimed to create the Exploration Cafe on Holland America; the collaboration with Discovery Channel has launched the “Discovery channel at the Sea,” while together with Dr. Seuss has created the program for children “Seuss at Sea”). Two relevant partnerships have also been implemented with Microsoft in order to increase the quality level of some services (i.e., the digitization of photos and videos). These operations can be located in the quadrant (B) of the model, because Carnival has tried to control activities far away from its core business (high risk and uncertain markets), which contribute to enrich the cruise package in terms of value created for the cruisers, but are not critical for its competitive advantage.

Carnival has also implemented equity collaborations with firms operating in other activities considered strategic for the achievement of competitive advantage (quadrant C). During the period 2014–2015, Carnival has signed two important agreements with shipbuilders: Fincantieri and China CSSC, in order to develop Chinese shipbuilding capacity in the cruise tourism segment. This alliance is consistent with the strategy of penetration of the Chinese market (in terms of origin and destination area) by building new “dedicated” ships.

The company has also entrusted in an equity partnership with few port terminals in order to improve the services in the port-related phases (Penco and Di Vaio, 2014). The vertical integration in the port services is aimed at enhancing the services to the cruisers, that contribute to the creation (or disruption) of value and satisfaction (or dissatisfaction) of the customers. Consistent with the service management literature, these phases are crucial for the moments of truth, as in such situations, the first customer’s experience plays a critical role in contributing to the perception of the total service quality (Penco and Di Vaio, 2014; Satta et al., 2015); the ports, in fact, represent the first experience of the overall vacation experience, especially in the case of home port. Carnival participates actively in the construction and management of cruise terminals (Puerta Maya in Cozumel, Mexico; Grand Turk Cruise Centre in the Turks and Caicos Islands; Mahogany Bay in Roatan, Honduras; Long Beach, California). Recently, Costa has also signed a partnership with the Shanghai Port Authority with the aim to control the cruise terminal. In Barcelona, Carnival already operates as private cruise terminal (Terminal D, named Palacruceros) and it has received approval to build and operate a second terminal. The new Terminal E on the port’s Adossat Wharf will be one of the largest in Europe. Carnival has started its construction in 2016, with the opening scheduled for 2018. Moreover, Carnival is currently collaborating with the Port Authority to build and open the first public parking facility located on the wharf, providing cruise passengers access to over 300 parking spaces.

Royal Caribbean Cruises Group

Royal Caribbean is the second largest cruise group in the world. The company was founded in 1997, as result of a merger between Royal Caribbean and Celebrity Cruise Lines. While Carnival has predominantly pursued the horizontal growth through M&As, on the contrary Royal Caribbean has principally implemented internal growth strategies or joint ventures with tourist operators aimed at creating new brands for new markets. The acquisition of Pullmantur has been the only significant horizontal M&A implemented by Royal Caribbean, whose strategic goal was to penetrate the European and Latin America markets.

Following an internal growth path, Royal Caribbean created Azamara Club Cruises (as a subsidiary of Celebrity Cruises in 2007) and CDF Croisieres de France in 2008. The joint venture with the German tour operator TUI was, instead, followed to create the “TUI Cruise” brand committed to the German domestic market. Considering the strategic role of Chinese market in the global scenario, in 2014 a JV was implemented with Ctrip International for the development of a new brand for the Chinese market (Sky SEA Cruises); in this case, Royal Caribbean has repeated the same “business model” used for the partnership with TUI. In all the descripted joint ventures, the company has followed implementation paths consistent with the quadrant (C); as new geographic markets are assessed as highly “risky markets” (as “distant” in terms of sociodemographic and cultural characteristics) and the development of new brands in the new markets is crucial for the achievement of competitive advantage, the company’ choice is to use equity partnerships. In the same direction, it is possible to assess the vertical integration strategy in the port-related phase that Royal Caribbean entrusted in 2013, by an equity partnership with the port of Barcelona. The recent focus of the company is to expand its presence in the Chinese port terminals. In 2012, in fact, Royal Caribbean entered into a partnership with Shun Tak Group and Worldwide Flight Service Holding for the management contract of Kai Tak Cruise Terminal in Hong Kong.

Royal Caribbean has used non-equity partnerships in order to control activities related to the cruise package (quadrant B). The recent tendency is to involve Chinese operators, in order to penetrate the most attractive origin market of the world. In 2011, in fact, Royal Caribbean launched a partnership with SATS Ltd Singapore, a company focused on the airport gate management and catering services. In particular, the partnership is aimed at controlling the organization of the check-in phase and of the luggage transfer to/from the Royal Caribbean and Azamara ships. This implementation mode has been followed also by Carnival: the oligopolistic structure, in fact, highly encourages imitative behaviors.

Genting (Star Cruises–NCL)

The Star Cruises–Norwegian Cruise Line (NCL) is the third largest cruise operator in the world. The cruise activity carried out by the two companies is now controlled by the holding company Genting Hong Kong Ltd. Star Cruises operates in the East and South East Asian region. NCL operates, instead, in Europe and North America and it is one of the oldest players in the industry, since the company was founded in 1966. The acquisition of NCL, in 2004, may be placed in the quadrant (D) of the model, as a M&A aiming at expanding the market share in the same industry. After this acquisition, however, the group has strengthened its market share mostly via internal mode, investing in new ships and marketing. Only recently, in March 2015, Genting Group has acquired Crystal Cruises, a luxury cruise line belonging to the Japanese group Nippon Yusens Kaisha.

The group has also pursued partnerships with firms operating at different stages of the cruise value system, in order to foster synergies with the core service: catering and food and beverage suppliers in the Philippines (Alliance Global Group Inc.); tour operating and agency services for China (China Cyts Tours Holding Co. Ltd); wireless technical services (Wireless Maritime Services, LLC—WMS); transport and terminal services (SATS Ltd). Consistent with Carnival and Royal Caribbean, these implementation modes are placed in the quadrant (B) of the model, as these activities, far from the core business, help to enrich the cruise package in terms of value created for cruisers, but are modestly significant for the firm’s competitiveness.

Discussion of the case studies

The cruise industry constitutes an ideal context for applying the previously proposed interpretative model on the implementation logic of external growth. The model appears useful to respond to the research questions 2 and 3, related to the drivers of the choice among different implementation modes and to the possibility of identifying homogenous strategic behaviors. In this industry, companies typically implement internal growth paths by investing in ships, branch offices, and foreign commercial companies, in order to expand geographic markets and market share, but cruise companies also make extensive use of external growth paths based on both M&As and alliances. In a thorough analysis of the three case studies, some paths emerge that seem to fit with the previously proposed model. Figure 3 shows the original interpretative model in which the principal strategic motivations of the cruise companies are highlighted.

Cruise company implementation of external growth strategies. Source: Our elaboration.

In line with the evolution of the external environment, companies have followed different growth paths over time. In the period from the 1990s to the subsequent decade, all the three major cruise lines used an implementation model based on M&As in order to grow horizontally, increasing their market share and thus acquiring increasing leadership. M&A operations have shaped the current structure of the industry, which is oligopolistic. Carnival is the group that has made most use of this kind of growth mode. These growth paths may be placed in the (D) quadrant of the model and respond to the general motivation “Seeking market leadership.” The activities into which the major cruise lines have expanded are “well-known” because they belong to the same business and therefore the levels of risk or complexity are low. M&A processes have also been crucial to obtaining competitive advantage: these companies had in fact the objective of attaining global leadership, eliminating current competitors. The control and appropriation of resources have been, in this sense, fundamental for attaining the aim of reaching collusive synergies (Dyer et al., 2004; Garette and Dussauge, 2000). As a result, the majors have consolidated the market and created their own brand portfolios; in this vein, cruise companies have been able to capture separate market niches of passengers and to create entry barriers for potential competitors (Clancy, 2017).

The wave of mergers and horizontal acquisitions slowed down once a fairly high level of industry concentration was attained, as Yin and Shanley highlighted: “in more concentrated industries, acquisition options are scarcer and more costly” (2008, p. 480). In fact, the presence of independent and strategically relevant cruise companies that could be potential targets has become increasingly contained. In the cruise industry, by contrast—due to the characteristics of the product and the market—it is difficult to apply horizontal scale alliances among existing players like in other contexts, such as airline passenger transport (Profumo, 2017).

Since 2000, cruise lines have increasingly used growth modes based on equity agreements with other “non cruise” actors that can be placed in the (C) quadrant of the model (“Acquiring control of “scarce” resources critical for competitive advantage”). Equity collaborative forms have been used to create new brands focused on single national/regional markets in partnership with tour operators that were strongly geographically rooted. The choice of this instrument is coherent with what Wang and Zajac (2007) demonstrated: the more the resources and expertise between companies are complementary, the more probability there is for alliances; in this case, tour operator competencies integrate and reinforce those of cruise companies, allowing them to enter new risky geographical areas.

When activities that companies want to control are both complex and critical for competitive advantage, cruise companies have opted for equity alliances (C quadrant), that sometimes led to vertical M&As (D quadrant). This occurs for operations implemented by cruise companies in order to manage port terminals. Integration strategies in the port phase are functional for ensuring an excellent level of passenger service which is critical as it constitutes the first moment of truth (Penco and Di Vaio, 2014; Pino and Peluso, 2015; Satta et al., 2015), and for raising entry barriers. Among recent operations, Carnival has undertaken an equity participation and direct investments in building terminal structures. In 2013, Royal Caribbean also undertook a strategy of investment based on an equity partnership in Barcelona port and it owns a terminal which it manages directly.

When the resources to be acquired are not particularly crucial for competitive advantage, and businesses are fairly unknown and “distant” from the cruise core business, cruise companies have used collaborative forms of non-equity growth, as the full control on the resources seems not necessary (Cools and Roos, 2005; Profumo, 2017) (B quadrant “Reinforcing the components of the cruise package with “unusual” resources to differentiate core service”). For example, tour operating and agency services, entertainment services that improve life on board and transport services. In this instance, it is possible to find Royal Caribbean’s partnership with a company that manages airport gate services, or Genting’s alliance with a technical wireless service company. Thanks to alliances within the same cruise supply chain, cruise lines are able to extract additional revenues from passengers both onboard (casino, restaurant, entertainment, sport services) and onshore (private islands, traditional events, excursion packages) (Vogel, 2017).

In relation to the (A) quadrant, considering the articulation of the cruise package and the strong presence of goods and services provision (e.g., all ship supply services and provision of food products), companies make abundant use of market transactions. Mere contractual relations are used when cruise companies are dealing with low market complexity (because, e.g., they have strong bargaining power and transaction costs are low), and resources held by partners are not critical for company competitiveness. In these cases, no significant advantages emerge from adopting M&As or alliances, in comparison to mere market transactions, which are less expensive and enable faster target achievements, following the proposal of Yin and Shanley (2008).

Conclusions

On the basis of an original interpretative theoretical model built on an in-depth literature review on the different strategy implementation paths, the present paper has analyzed the antecedents of the different external growth strategies (M&As vs. alliances) implemented by the three major cruise companies (Carnival, Royal Caribbean, and Star Cruise–NCL). The analysis has highlighted how companies have followed common behaviors over time: the oligopolistic structure has in fact led to copycat behaviors (Coleman et al., 2003; Wie, 2005). Moreover, the three case studies have shown that, in the choice between M&As and alliances, cruise companies seem to consider the two variables of the proposed model (Dyer et al., 2004; Garette and Dussauge, 2000; Profumo, 2017; Yin and Shanley, 2008): the level of riskiness and complexity of the business in which the firm is operating, or would like to operate, as well as the importance of the resources and competences to be acquired for the competitive advantage.

In the first phase, all companies—more or less intensely—carried out M&As operations. The need to control resources that are critical for the development of competitive positioning, together with the industry knowledge, drove companies to acquire smaller companies, often with excellent local/regional positioning, or in specific market segments. By now, the industry seems to have settled as an oligopoly dominated by three major companies, despite the fact that MSC, by taking totally different paths based on internal growth, has been increasing its market share. Consequently, cruise companies have halted the wave of acquisitions and, in order to reinforce competitive advantage in relation to service quality and differentiation, they have begun to implement vertical integration strategies through equity collaborations with key actors in the cruise value system: for example, public/private companies created to manage port terminals, which are crucial nodes for the creation of the cruise service. When the importance of the acquired resources for reaching the competitive advantage is crucial and the complexity and risk level of the new business are high, companies seem to prefer collaborative arrangements with high level of control. When, instead, the activities that cruise companies want to control are less critical for the competitive advantage, a logic of non-equity partnership has prevalently been used, such as collaborations with tourist–entertainment actors in order to enrich the cruise package.

The analysis of these case studies has on one hand contributed to the development of strategic managerial studies focused on the cruise industry, which are still rather scant. With few studies having examined the growth strategies of cruise companies, the results of this study make indeed a positive contribution to the tourism research literature. On the other hand, this contribution has filled a knowledge gap in relation to comparative analyses on the drivers of external growth implementation strategies, thus supplying a useful interpretative model for future studies. Since such corporate development initiatives are central to management literature, their study could represent an important building block for this domain.

From a managerial point of view, the paper has contributed to outlining the relevance that certain resources/activities (similar or complementary) present for the competitiveness of cruise companies (Wang and Zajac, 2007). In particular, the importance of some noncruise activities (complementary) in the current competitive structure emerges. Moreover, for policy makers, it is necessary to note that the trend of cruise companies to control port terminals could lead to an excessive raising of entry barriers for new cruise operators, thereby making the access to the port (and the city) less competitive for cruise companies that are not “also” terminal owners. This could also has an economic impact on cruise destinations (Penco and Di Vaio, 2014). On the other hand, cruise company investments ensure continuity of traffic, thus making cruise traffic less unpredictable. Lastly, as regards passengers, both M&As and alliances enlarge the possibilities to capture revenues streams, due to an increase in market power and in cruisers spending opportunities (Clancy, 2017; Vogel, 2017).

The paper presents some limitations that may be ironed out in future studies. One limitation is related to data collection and, in particular, to the interview method: the interviewed people may have choose to disclose what they want or can at the moment of the interview (Mishler, 1986). In order to avoid the risk of bias, we have however followed the recommendations of Qu and Dumay (2011). Moreover, the main limitation is related to the use of the case-study methodology (Yin, 1994), which may present the bias of the researcher’s subjectivity and the criticism of external validity and results’ generalizability. Further research should therefore have the aim to extend the number of cases, in order to verify the applicability of the model to smaller cruise companies or other industries. It could also be interesting to focus the attention on the motivations that led cruise partners to entrust alliances with cruise operators.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.