Abstract

In contrast to prior reviews, this study provides a review of research contexts, research designs, and theories used in restaurants’ business performance research. It also identifies measures and antecedents of restaurants’ business performance. Additionally, this systematic review highlights gaps for future research on restaurants’ business performance. A total of 148 articles were obtained from the Web of Science (WoS) database (1997 till February 2021) and then 33 articles were identified as eligible for the final analysis. Based on reviewing findings, this article proposes some intriguing research questions and contributes actionable results for practice. This research ends with a framework that draws the findings concurrently to apprise future theoretical and empirical advances in the area.

Keywords

Introduction

The restaurant sector has a profound importance for economic growth and employment (Gheribi, 2015; Lin et al., 2014; Salem et al., 2021b; Tibon, 2014). The first step of the improvement process in restaurants is to measure their business performance (Heo, 2017). Business performance is much known in organizational research (Fernandes Sampaio et al., 2020; Miller et al., 2013; Zeglat and Zigan, 2013). Further, Rao et al. (2009) highlighted that business performance management can assist firms including restaurants to achieve a better competitiveness level in the market.

Indeed, there is a numerous number of business performance definitions. For instance, Lebas (1995) defined business performance as the ability of a firm to reach its objectives or targets by implementing a number of actions. Business performance is to plan and manage a business by using a multi-dimensional set of performance measures (Bourne et al., 2003). Business performance is the ability of a firm to meet customers’ needs and achieve its goals and objectives (Garg et al., 2020).

According to the OCDE’s report 1 about business and vulnerability, small and medium-sized enterprises (SMEs) are significant for economies. In addition, SMEs are more vulnerable. It is clear that SMEs have a profound importance in the scientific research (Kozubíková et al., 2015). The restaurant industry is dominated by small and medium-sized restaurants (SMRs). For example, in the USA, 9 of 10 restaurants have less than 50 employees 2 .

There are previous studies highlighted business performance of SMEs including restaurants that have a profound importance for tourist image-building (Fuentes-Luque, 2017). For instance, Ma and Lin (2010) showed that SMEs have faced several difficulties. More precisely, small enterprises have encountered huge obstacles in their growth and acquiring external finance. Therefore, financial and institutional development are significant to solve their problems (Beck and Demirguc-Kunt, 2006). More, SMRs are vulnerable to failure. 60% of small independent restaurant businesses cannot survive for more than 3 years, whereas 25% of them fail during their first year of operations (Nizam, 2017). This is a call to deepen research on restaurants’ business performance.

In spite of the increasing academic interest in restaurants’ business performance (e.g. Abbas and Hussien, 2021) and the significance of creating a comprehensive picture of where the restaurants’ business performance literature has been and where it must go, up to now, there is no systematic and critical review for restaurants’ business performance research. Prior systematic reviews focused on the association between business performance and big data (Maroufkhani et al., 2019), employee engagement (Motyka, 2018), corporate social responsibility (Saha et al., 2020), psychological safety (Abror and Patrisia, 2020), and the complexity of products (Trattner et al., 2019). Moreover, these studies did not focus specifically on the restaurant industry.

A surprising lack of systematic literature reviews for restaurants’ business performance highlighted the need to conduct the current review to demonstrate research outlets that publish restaurants’ business performance research, indicate research contexts and designs utilized in restaurants’ business performance research, illustrate theories and measures used in restaurants’ business performance research, and map antecedents of restaurants’ business performance. Based on reviewing findings, the current research presents several avenues for expanding future research through theoretical and empirical development. The analysis part was organized with taking four questions into consideration: 1. What types of restaurants are analyzed in restaurants’ business performance research? And what are the research designs utilized in research? 2. What are the theories and measures used in research? 3. What are the antecedents of restaurants’ business performance? 4. What is the future path of research on restaurants’ business performance?

To answer these questions, a systematic review was conducted on restaurants’ business performance. To include an article in the current systematic review, it must concentrate on the business performance in the restaurant industry.

Methodology

The main aim of this systematic review is to provide an inclusive review of the recent state of restaurants’ business performance research and highlight gaps for expanding future research in the area. To ensure comprehensiveness and capture studies related to restaurants’ business performance, the keywords of “business performance and restaurant” were used to search by “topic” for published studies about restaurants’ business performance in the disciplines of “hospitality, leisure, sport, tourism or business” in the Web of Science (WoS) database.

According to Singh et al. (2021), the WoS is a more selective database than Scopus and Dimensions. Due to the ability of the WoS to provide several options for filtering content, it is significant in conducting systematic reviews (Elkhwesky et al., 2022a; Gusenbauer and Haddaway 2020). The WoS is a well-established and well-known database to conduct systematic and major reviews in hospitality and tourism (Elkhwesky, 2022; Elkhwesky et al., 2022a, 2022b). The overlap between the WoS and Scopus databases is high (59%) in hospitality and tourism (Sánchez et al., 2017; Álvarez-García et al., 2020). The WoS was accessed via the Egyptian Knowledge bank (https://www.ekb.eg/) that gave us the permission to access studies for free. We searched restaurants’ business performance from 1997 till February 2021.

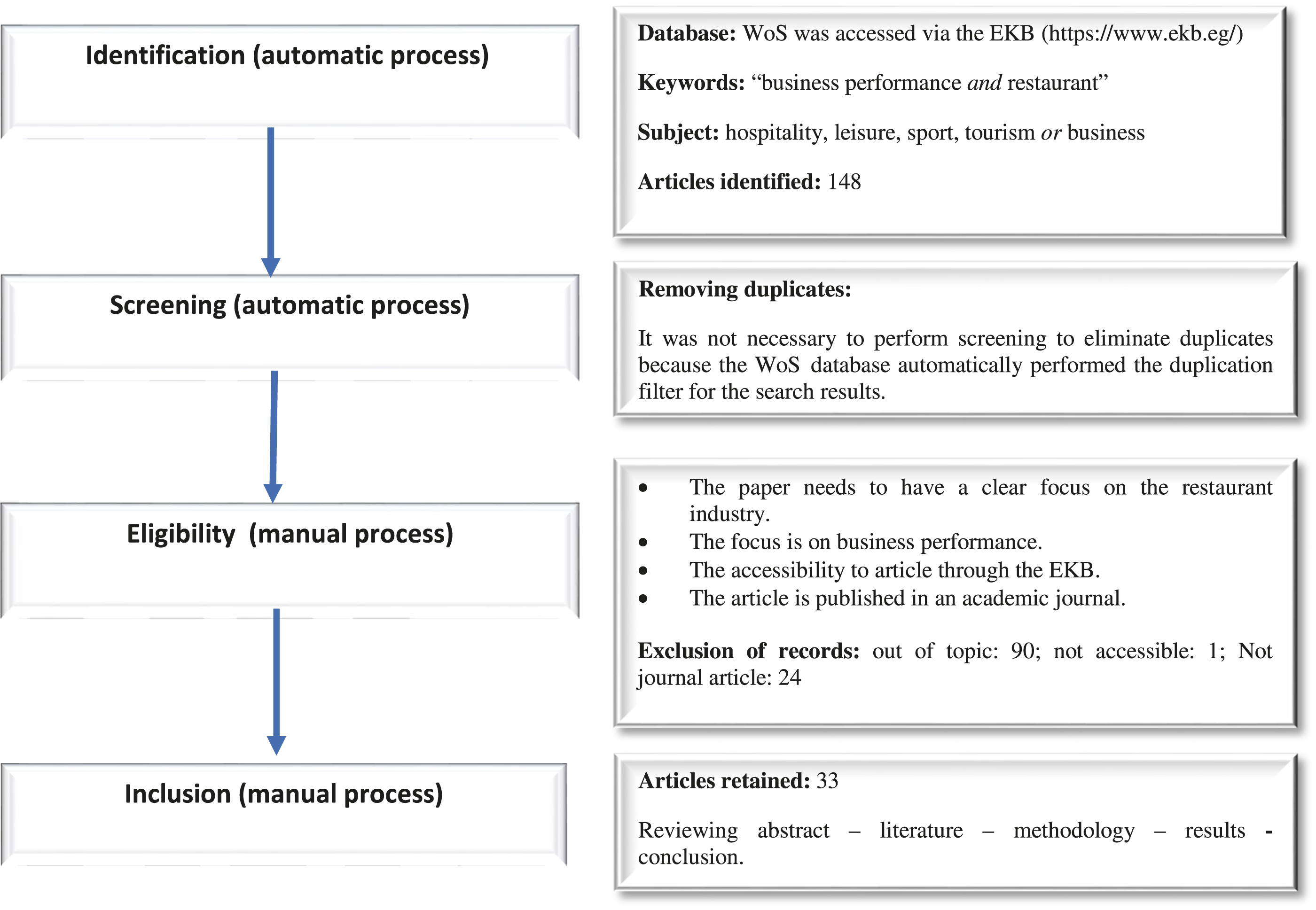

Figure 1 demonstrates the current systematic review process undertaken in this research through different phases, which was derived from Chon and Zoltan (2019), Elkhwesky (2022), Elkhwesky et al. (2022a; 2022b), and Yang et al. (2017). Firstly, 148 articles were identified from the WoS database. It was not necessary to be screened to eliminate duplicates because the WoS database automatically performed the duplication filter for the search results. Thereafter, a manual screening was performed over all papers reading the abstract and the conclusion sections. The eligibility criteria applied was based on the following principles: - The paper needs to have a clear focus on the restaurant industry. - The focus is on business performance. - The accessibility to article through the Egyptian Knowledge Bank (EKB). - The article is published in an academic journal. Literature search process was adopted from Chon and Zoltan (2019), Elkhwesky (2022), Elkhwesky et al. (2022a; 2022b), and Yang et al. (2017).

Ultimately, 33 articles published between 2000 and 2020 were proper for the final analysis. The analysis of all 33 articles was based on reviewing the abstract, literature, research methodology, in addition to results/findings and conclusion.

Review findings

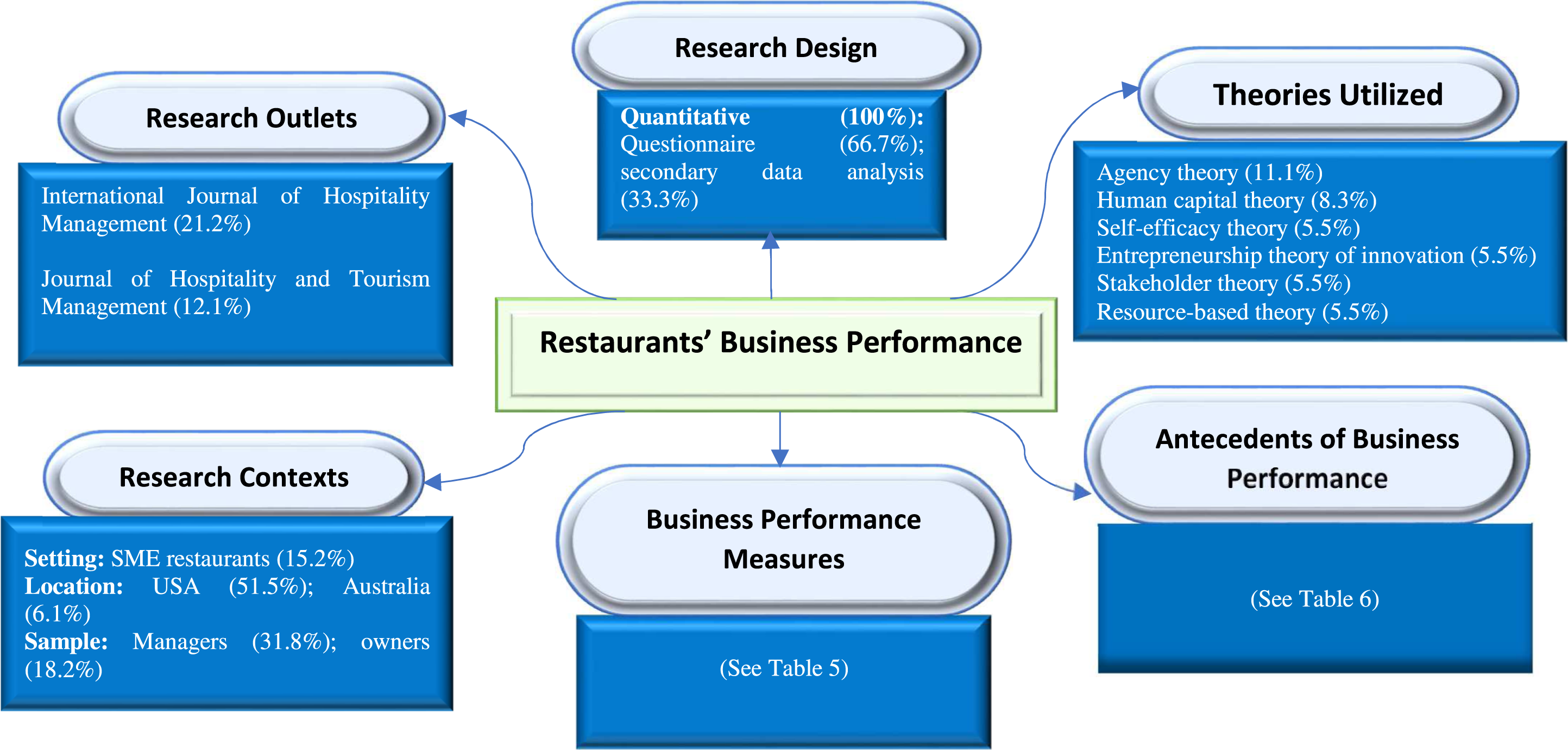

Based on the current study questions, the analysis part has been structured into five main sections. Specifically, this part (I) demonstrates research outlets publishing restaurants’ business performance research; (II) indicates research contexts and designs utilized in restaurants’ business performance research; (III) illustrates theories utilized in restaurants’ business performance research; (IV) indicates measures of restaurants’ business performance research; and (V) maps antecedents of restaurants’ business performance. Drawing on reviewing results, the current study presents several avenues for expanding upcoming research in the area.

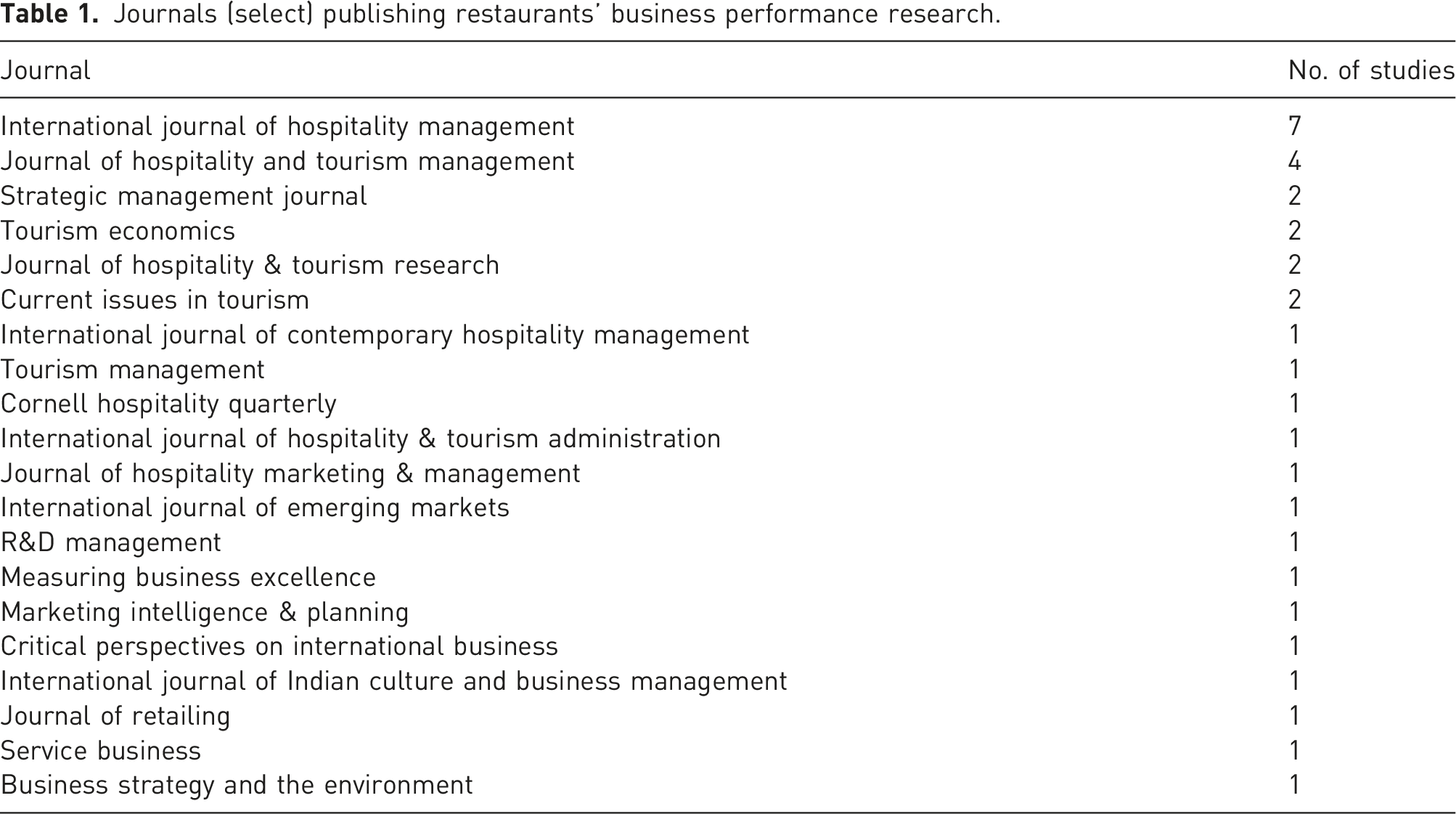

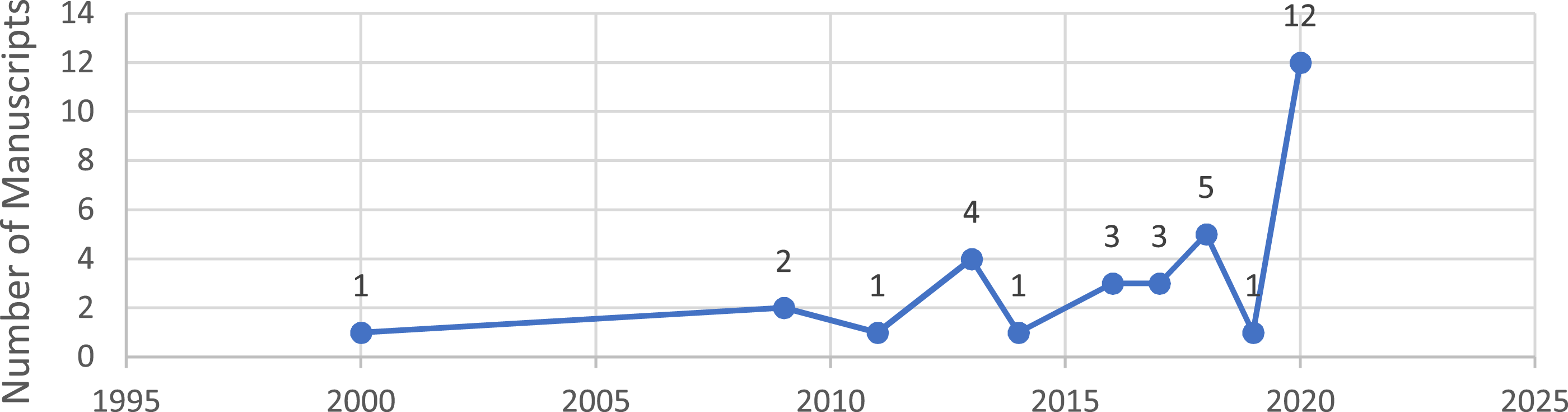

Research outlets publishing restaurants’ business performance research

Journals (select) publishing restaurants’ business performance research.

Restaurants’ business performance publications per year (n = 33).

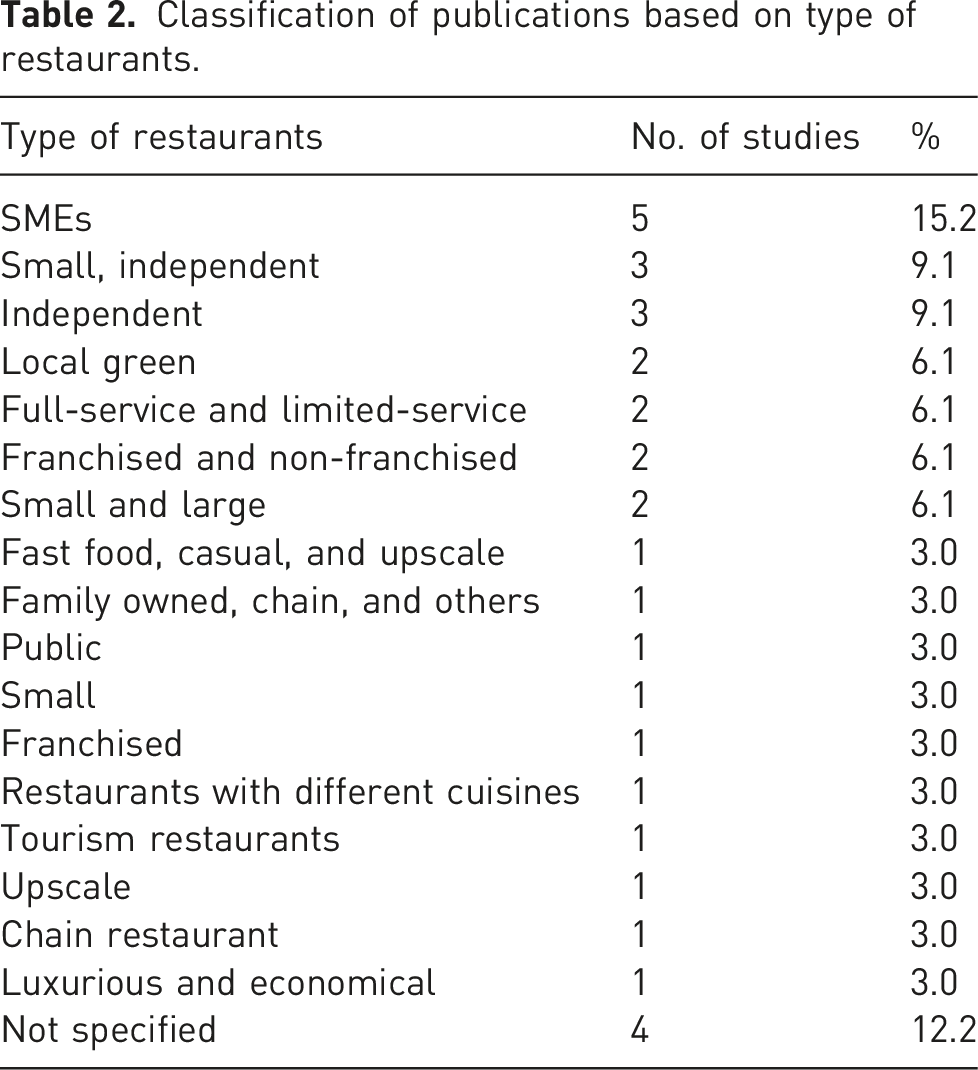

Research contexts and design utilized in restaurants’ business performance research

Classification of publications based on type of restaurants.

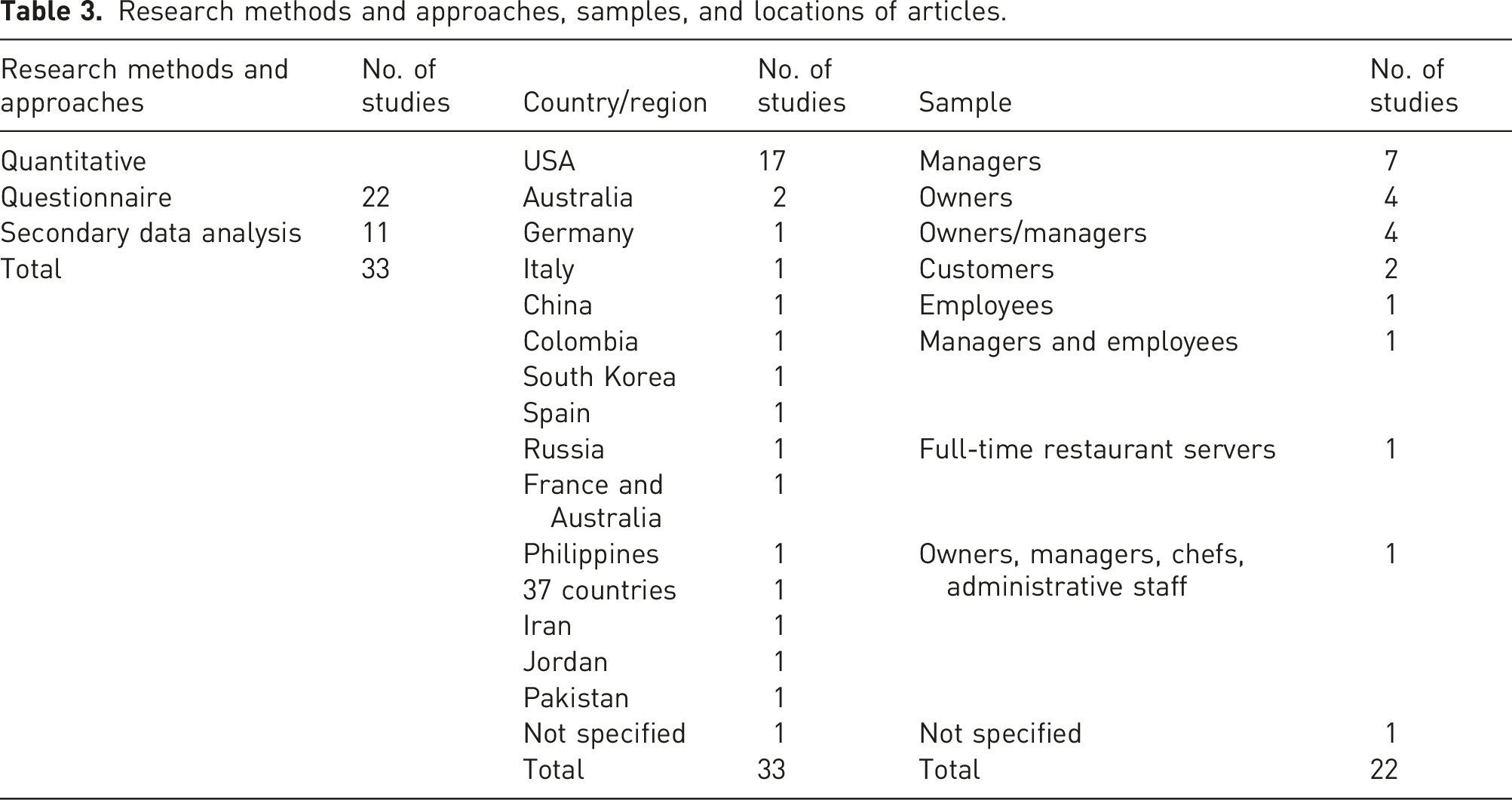

Research methods and approaches, samples, and locations of articles.

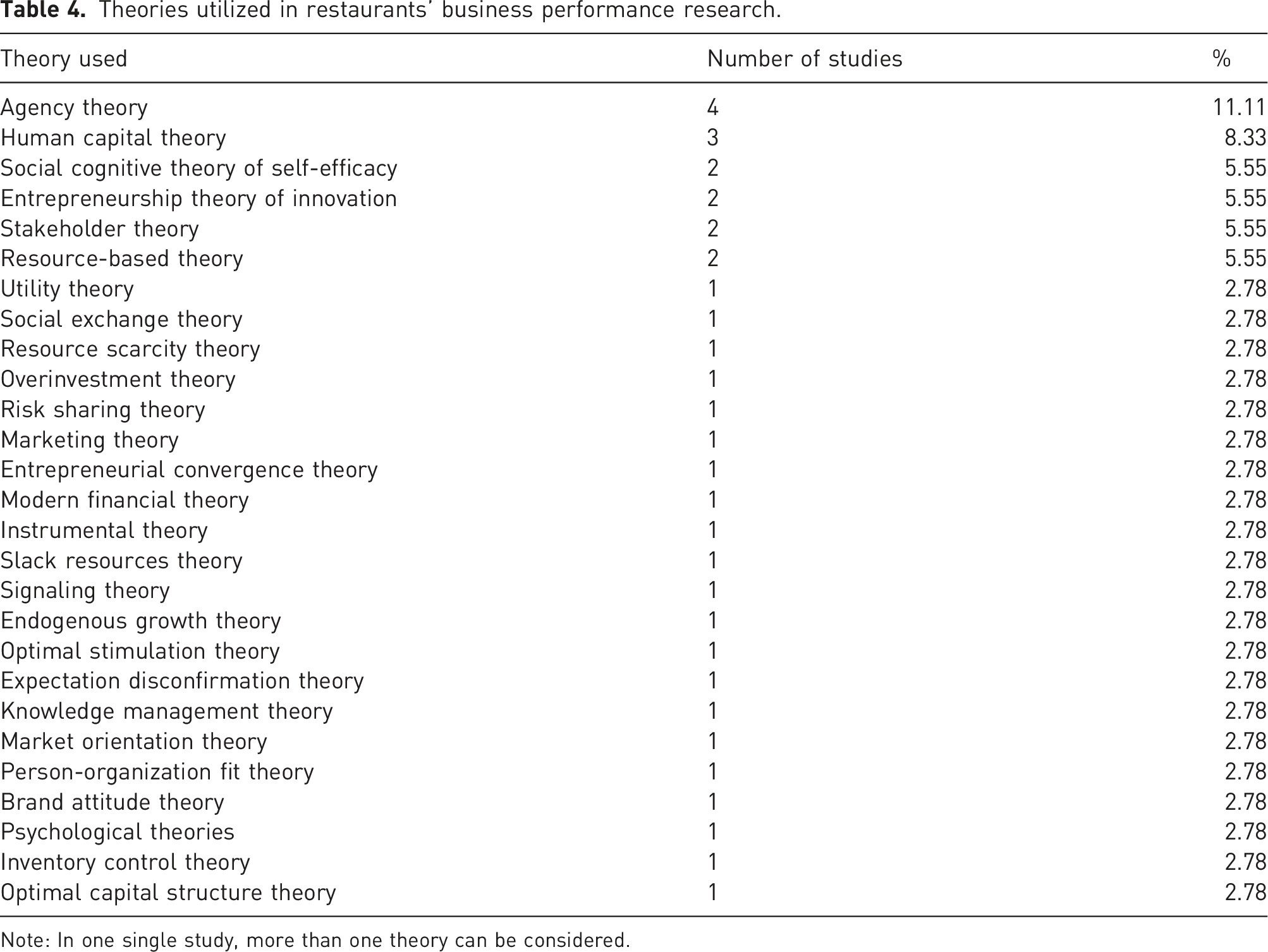

Theories utilized in restaurants’ business performance research

Theories utilized in restaurants’ business performance research.

Note: In one single study, more than one theory can be considered.

Agency theory (AT)

AT is an important part of economics literature. Drawing on AT (Jensen, 1986; Rozeff, 1982), firm managers are considered the agents of shareholders and their relationship charged with conflicting interests because payouts to shareholders could minimize their control over resources and their power. When an enterprise generates huge free cash flow, conflicts could be appeared between shareholders and managers regarding policies of payout. The problem is how to make managers disgorge the cash rather than investing it at below the cost of capital or wasting it on firm inefficiencies. AT claimed that firms growth is important for maximizing managers' power by raising the resources under their control. Further, the growth in sales is positively correlated with compensation of managers.

A study of Madanoglu et al. (2011) was built on AT to investigate whether franchising restaurant enterprises show improved financial performance (performance measures include the Sharpe Ratio, the Treynor Ratio, the Jensen Index, the Sortino Ratio, and the Upside Potential Ratio) than non-franchising restaurant enterprises. Mun and Jang (2020) studied the phenomenon of the asset growth anomaly to examine restaurant firms’ financial performance, using overinvestment theory and agency theory.

Regarding AT (Hsu and Jang, 2009), franchising can achieve the interests of both franchisees and franchisors. Rubin (1978) affirmed that franchising can minimize franchisors’ costs for monitoring managers. AT (Hsu and Jang, 2009) demonstrates that enterprises select franchising due to the lack of their ability to efficiently supervise their managers as they grow. In addition, AT indicates that managers minimize their tasks when there is no growth in compensation, therefore enterprises bear huge monitoring expenses to make sure that managers work for the firm’s interest.

Human capital theory (HCT)

HCT is one of leading theories in restaurants’ business performance research. Lucas (1988, 1990) exhibited that the main principle of HCT is that individuals' learning capabilities have a profound value as other resources in products and services production. Further, human capital can enhance productivity.

Based on Nafukho et al. (2004), HCT perceived that investment in people could be useful to increase productivity and profitability of firms. In accordance with HCT, experiences, education, qualifications, and skills of restaurants' owners, managers, or entrepreneurs can influence organizational outcomes (Jogaratnam, 2017b, 2018; Pennings et al., 1998).

On the basis of HCT, Assaker, Hallak, and O’Connor (2020) analyzed the impact of human capital factors (e.g. past managerial experience, education, and entrepreneurship qualification) on restaurant performance. In addition, HCT has been used by Jogaratnam (2018) to investigate the association between HC (education and experience) and restaurant performance (market performance and financial performance). HCT was also adopted by Lee, Hallak, and Sardeshmukh (2016b) to develop the link between human capital (such as entrepreneurship and hospitality education), innovation, entrepreneurial self-efficacy, and restaurant performance.

Social cognitive theory of self-efficacy (SCT)

Regarding SCT, perceived self-efficacy affects actions directly and through its impact on other elements. Individuals actions and behaviors are influenced by their beliefs in their abilities (also known as self-efficacy) (Bandura, 2001; Ng and Lucianetti, 2016). Bass and Stogdill (1990, p.153) argued that “self-efficacy is closely allied with self confidence and self-esteem”. According to Maddux (1995), self-efficacy theory has guided several researches in social, personality, and psychology. This theory is an aspect of a more general social cognitive theory and it argues that skills, capabilities, and abilities are the motivators for behaviors and actions (Maddux, 1995).

Entrepreneurial self-efficacy originated from SCT (Lee et al., 2016b). Chen, Greene, and Crick (1998) highlighted that entrepreneurial self-efficacy has a profound importance for increasing entrepreneurial intention of people to launch their new ventures. On the basis of SCT, Lee, Hallak, and Sardeshmukh (2016a) and Lee et al. (2016b) investigated the correlation between entrepreneurial self-efficacy and restaurant performance (e.g. profitability, sales, and growth).

Entrepreneurship theory of innovation (ETI)

Entrepreneurship theory of innovation is also called the Schumpeter’s entrepreneurship theory of innovation. Schumpeter is the prophet of innovation (McCraw, 2009). Schumpeter is one of the greatest economies who focused on business strategy, innovation (new combinations), entrepreneurship, and creative destruction (McCraw, 2009; Śledzik, 2013). Schumpeter (1939) defined entrepreneurs as individuals who can carry out innovations.

In this regard, the personality of entrepreneurs is the driving force for innovations that is a part of entrepreneurship (Schumpeter and Backhaus 2003). Śledzik (2013) affirmed that Schumpeter’s theory perceived that the central innovator is the entrepreneur. Besides, innovation is the “creative destruction” that is essential for economic growth. Drawing on ETI, Lee et al. (2016a, 2016b) assessed the relationship between innovation activities and restaurant performance (e.g. profitability, sales, and growth).

Stakeholder theory (ST)

According to Friedman and Miles (2002), and Salem et al. (2021a), ST indicates that all enterprises have stakeholders (e.g. managers, shareholders, suppliers, employees, and customers) who have a legal interest in different aspects of the enterprise’s activities. More importantly, ST argues that the interests of all stakeholders should be a priority when setting organizational policies, structures, and decisions. In order to enhance sustainability and financial performance, taking care of stakeholders' demands is important (Berman et al., 1999).

To ensure support and participation of stakeholders, enterprises need to provide their stakeholders with more utility and benefits. Stakeholders could satisfy their own interests through enterprises and other stakeholders (Harrison and Wicks, 2013). Interactions and collaboration of enterprises with their stakeholders constitute the corporate social performance record (Brower and Mahajan, 2013; Waddock and Graves, 1997).

Measures of restaurants’ business performance

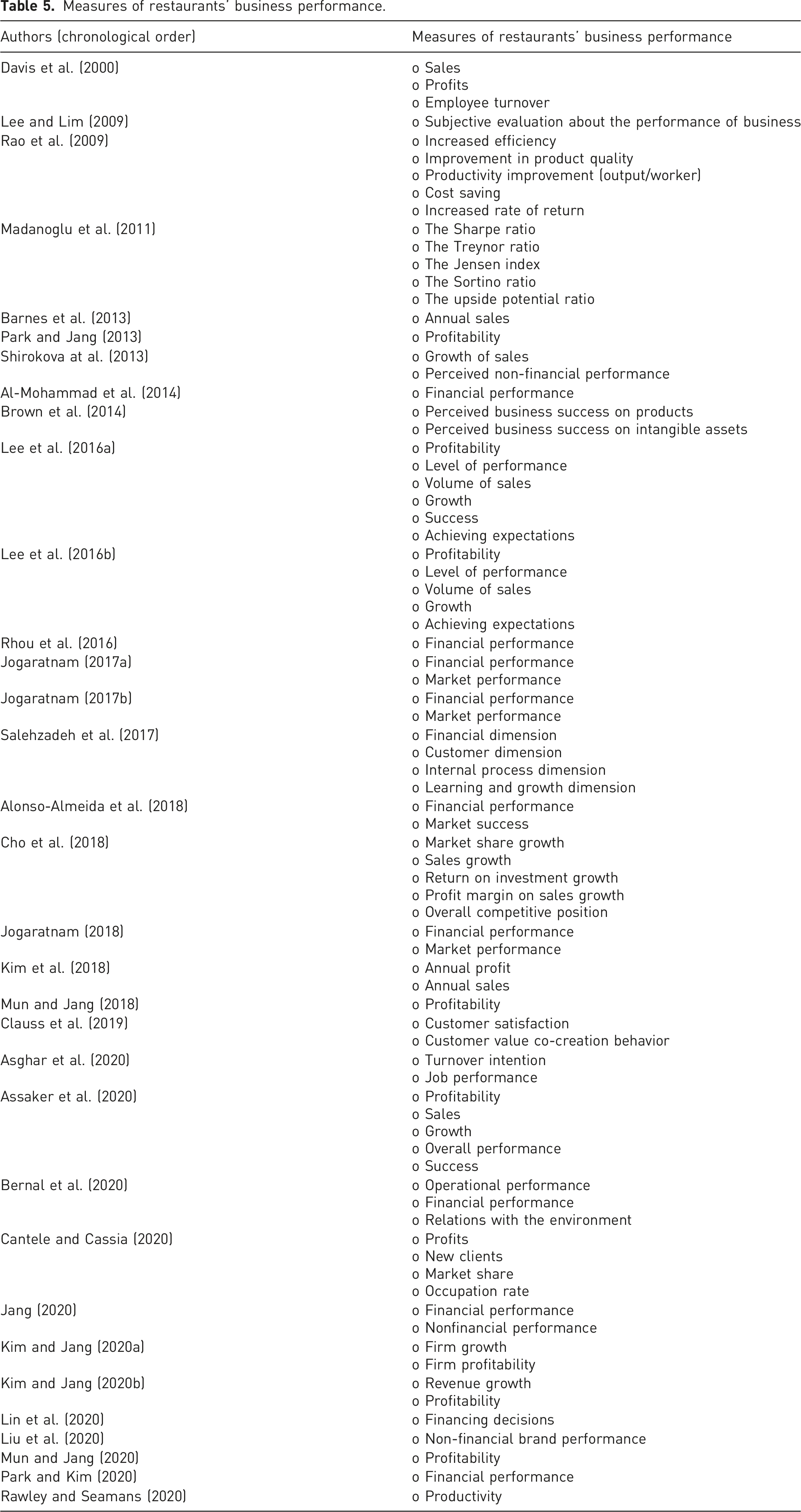

Measures of restaurants’ business performance.

Jang (2020) measured business performance by depending on financial and non-financial performance. Financial performance items focused on sales, profit, return on investment, and cost advantages, while non-financial performance items concentrated on employee and customer satisfaction, and customer retention.

A study by Bernal et al. (2020) used financial, operational, and environmental performance to measure business performance. Based on this study, financial performance refers to minimizing costs and increasing sales and profits, while relations with the environment performance refers to improved relations with customers, suppliers and competitors, and operational performance refers to improved organization climate, customer service, control procedures, and personnel autonomy in the workplace.

Business performance was also measured based on four subscales which included financial, customer, internal process, and learning and growth (Salehzadeh et al., 2017). For clarification, financial performance measures were productivity, returns, costs and wastage, and efficient and effective use of investment. Customer dimension of business performance was measured by four items which involved achieving customer satisfaction, identifying customers’ demands, providing customer service, and addressing customer complaints.

Internal process dimension was measured by using items such as improving quantity and quality of services, research and development, and working methods. Learning and growth dimension of business performance was measured by focusing on items involving skills and knowledge of staff, employee satisfaction, developing creative ideas, and identifying the staff development needs (Salehzadeh et al., 2017).

However, three studies (9.09%) measured business performance by concentrating only on financial performance. For instance, Al-Mohammad et al. (2014) measured financial performance by using items such as sales volume and profitability. Secondary data analysis was also used for measuring financial performance (e.g. Park and Kim 2020; Rhou et al., 2016).

Three researchers (Mun & Jang, 2018, 2020; Park and Jang, 2013) measured business performance by concentrating on profitability through secondary data analysis. Other five studies (15.15%) focused on profitability with other factors to measure business performance. For instance, Kim and Jang (2020a, 2020b) used two variables to measure business performance including revenue or firm growth and profitability through secondary data analysis. To measure firm growth, Kim and Jang (2020a) used total assets, while as for firm profitability, return on equity was used. Besides, Lee et al. (2016a, 2016b) used items involving profitability, level of performance, volume of sales, growth, success, and achieving expectations. In this regard, Assaker et al. (2020) measured business performance of restaurants by using items such as profitability and sales.

Five studies used profit with other factors to measure business performance. For example, items of profits, new clients, market share, and occupation rate were used by Cantele and Cassia (2020). Besides, Kim et al. (2018) based on annual profits and annual sales to measure business performance through secondary data analysis. In addition, restaurant performance measures were profits, sales, and employee turnover (e.g. Davis et al., 2000). Profit margin on sales growth was also used with other items involving market share and sales growth, ROI growth, and overall competitive position (e.g. Cho et al., 2018).

Antecedents of restaurants’ business performance

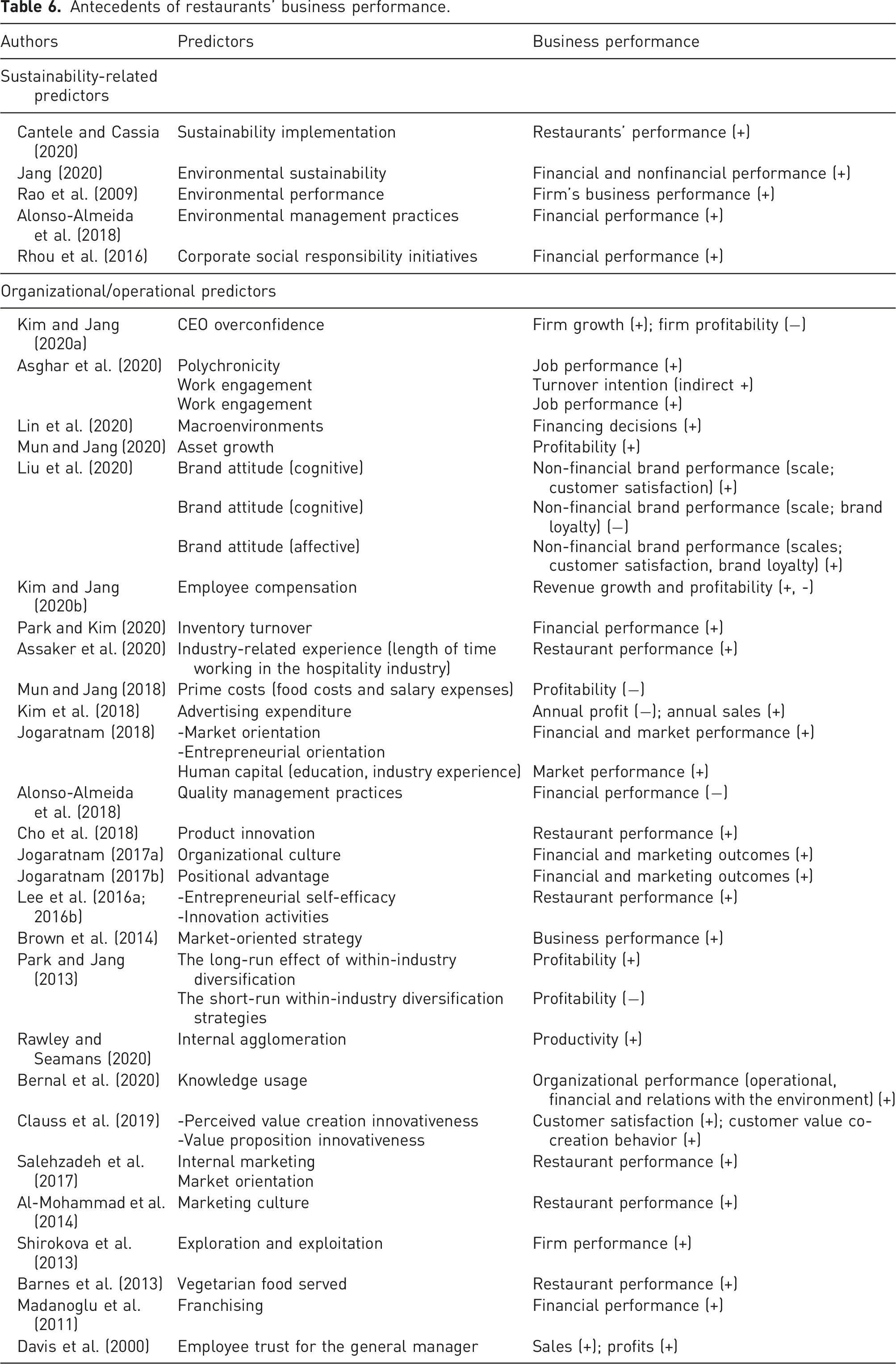

Antecedents of restaurants’ business performance.

Sustainability-related antecedents

Five studies (15.15%) focused on investigating the influence of sustainability issues on business performance of restaurants. For instance, financial and non-financial performance could be enhanced through environmental sustainability (Jang, 2020). In this vein, restaurants’ performance is positively influenced by sustainability implementation (Cantele and Cassia, 2020) and performance related to the environment (Rao et al., 2009). Besides, environmental management practices (Alonso-Almeida et al., 2018) and CSR initiatives (Rhou et al., 2016) have a positive effect on financial performance.

Organizational/operational antecedents

A number of articles focused on organizational/operational factors and their influence on restaurants’ business performance. For example, it was found that business performance is positively influenced by internal marketing and market orientation (Brown et al., 2014; Salehzadeh et al., 2017), marketing culture (Al-Mohammad et al., 2014), innovation activities (Lee et al., 2016a; 2016b), product innovation (Cho et al., 2018), organizational culture (Jogaratnam, 2017a), asset growth (Mun and Jang 2020), inventory turnover (Park and Kim 2020), and franchising (Madanoglu et al., 2011).

Kim and Jang (2020a) indicated that CEO overconfidence affected firm growth positively and firm profitability negatively. Entrepreneurial self-efficacy is important for improving restaurant performance (Lee et al., 2016a; 2016b). Jogaratnam (2018) resulted that entrepreneurial orientation is critical for financial and market performance. In this regard, Lee and Lim (2009) concluded that restaurant performance could be improved by entrepreneurial orientation. This study measured the performance by requesting the owner’s subjective evaluation about the performance of their business. Restaurants’ business performance is positively influenced by experiences related to industry (Assaker et al., 2020) and human capital (education, industry experience) (Jogaratnam, 2018).

Agenda and call for future research

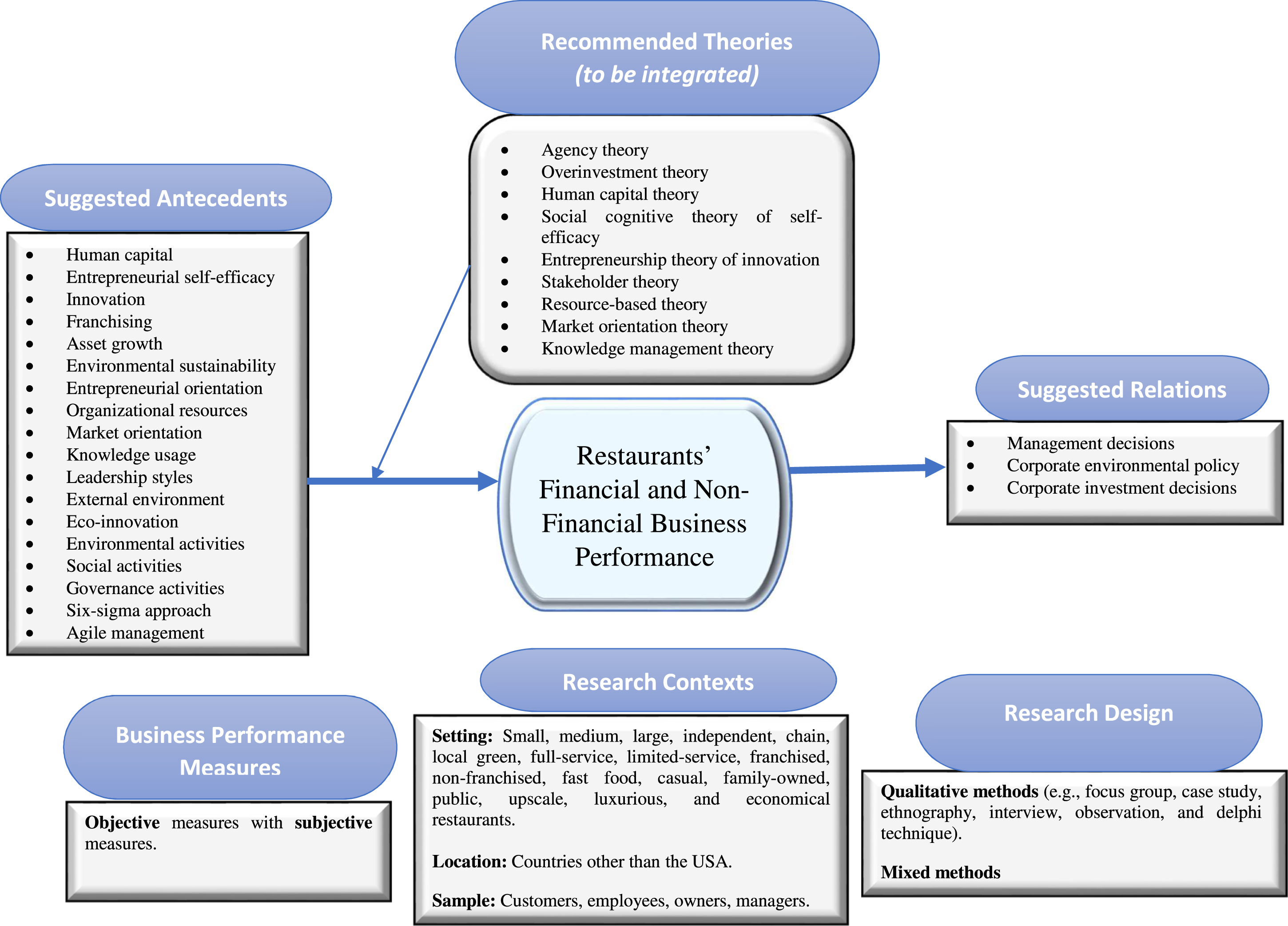

Figure 3 maps the key findings obtained from the current systematic review. This section presents recommendations and suggestions for forthcoming studies. It also provides a comprehensive synopsis of future research potentials of restaurants’ business performance, thereby providing significant clues for researchers who want to further investigate restaurants’ business performance (see Figure 4). Summary of key review findings. Suggestions for future research on restaurants’ business performance.

Novel research line 1: Advancing research contexts and designs in restaurants’ business performance research

It is acknowledged that there are several shortcomings in research contexts of restaurants’ business performance research. Based on our results, it is obvious that there is a critical need for conducting more research on restaurants’ business performance including small, medium, large, independent, chain, local green, full-service, limited-service, franchised, non-franchised, fast food, casual, family-owned, public, upscale, luxurious, and economical restaurants. A huge percentage of researches examined have been performed in the USA. There has been an obvious shortage of research on restaurants’ business performance from other countries, such as Australia, South Korea, China, Egypt, Italy, Germany, Spain, Russia, Jordan, and Pakistan.

The majority of questionnaires used in restaurants’ business performance research was directed to managers or/and owners because they are responsible for restaurants’ management including accounting, human resources, marketing, and maintenance (Mealey, 2018). In addition, O'Cass and Sok (2012) affirmed that managers have a good knowledge with business capabilities and performance. Hutchinson, Quinn, and Alexander (2006) asserted that managers of SMEs are responsible for planning and improving their enterprises’ capabilities.

Besides, owners and managers of SMEs are responsible for implementing innovative strategies (Aksoy, 2017). Future research should also consider other parties including customers and employees in restaurants’ business performance research. Employees are the cornerstone of all enterprises (Elkhwesky et al., 2018, 2019, 2021).

The current review recommends future scholars to merge quantitative methods (e.g. questionnaire, secondary data analysis, and experimental design) with qualitative methods (e.g. focus group and interview). This integration is important in obtaining more data related to restaurants’ business performance. Concerning the link between sustainability implementation and restaurants’ performance, Cantele and Cassia (2020) suggested conducting qualitative studies to deepen results.

Novel research line 2: Theoretical advancement

With the importance of investigating factors affecting restaurants’ business performance, it is critical to consider outcomes of business performance to affirm the significance of its improvement. Future research could investigate the impact of restaurants’ business performance on their intention to expand or reduce their external activities, and on management decisions. In addition, investigating the effect of business performance on corporate investment decisions (Agyei-Mensah, 2021) and corporate environmental policy (Elsayed and Paton, 2009) could be a vital area for further analysis.

Even though the significance of integrating theories for adding more theoretical contributions, it is clear that almost scholars focused only on one theory as the basis for conducting their studies related to restaurants’ business performance (e.g. Assaker et al., 2020; Bernal et al., 2020; Jang, 2020; Liu et al., 2020). Therefore, we recommend merging theories in future research. This integration could be between agency theory, human capital theory, social cognitive theory of self-efficacy, entrepreneurship theory of innovation, stakeholder theory, overinvestment theory, resource-based theory, market orientation theory, contingency theory, and knowledge management theory.

AT (Jensen, 1986; Rozeff, 1982) claimed that firms growth is significant in maximizing managers' power by increasing the resources under their control. Further, the growth in sales is positively associated with compensation of managers. According to Nafukho et al. (2004), HCT argued that investment in people could be useful to enhance productivity and profitability of enterprises.

Concerning SCT, actions and behaviors are influenced by individuals' beliefs in their abilities (self-efficacy) (Bandura, 2001; Ng and Lucianetti, 2016). Based on Śledzik (2013), ETI claimed that innovation is the “creative destruction” that is vital for economic growth. ST indicated that the interests of all stakeholders should be a priority when setting organizational policies and decisions. This is important for enhancing sustainability and improving financial performance (Berman et al., 1999; Friedman and Miles, 2002; Salem et al., 2021a).

Novel research line 3: Advancing measures of restaurants’ business performance

Due to there are several different measures for restaurants’ business performance, it is critical for further research to develop a unified set of measurement tools by using a projective tool for data collection with an expert panel. Although many studies adopted subjective measures of business performance (e.g. Lee et al., 2016a; Jogaratnam, 2017a; Assaker et al., 2020) that correspond closely to objective measures, it is suggested for upcoming research to use objective and subjective measures to improve findings (Jogaratnam, 2018).

Assaker et al. (2020) recommended that obtaining several sources of data on business performance would enhance the models validity (measurement and structural). To measure business performance, our review suggests for further studies integrating financial performance, market performance, environmental performance, and operational performance that refers to improved organization climate, customer service, competitive differentiation, human capital, control procedures, and personnel autonomy in the workplace.

Novel research line 4: Variables in relation to contemporary and future issues in restaurant context

Given the importance of environmental and sustainability issues (Elkhwesky, 2022; Elkhwesky et al., 2022b), it is advisable for upcoming scholars to investigate the effect of environmental sustainability (Jang, 2020), sustainability implementation (Cantele and Cassia, 2020), environmental performance (Rao et al., 2009), environmental management practices (Alonso-Almeida et al., 2018), CSR initiatives (Rhou et al., 2016), and environmental leadership (Elkhwesky et al., 2022a; Jang et al., 2017) on both restaurants’ financial and non-financial business performance.

Our review also suggests investigating the association between different leadership styles and restaurants’ business performance. These leadership styles could include spiritual, Pygmalion, safety, bureaucratic, humor, Machiavellian, environmental transformational, paternalistic, and responsible leadership. Based on a recent systematic review by Elkhwesky et al. (2022a) on leadership styles in hospitality, Pygmalion leadership means motivating subordinates through high expectations of their supervisors, whereas humor leadership is to use humor in dealing with followers.

Besides, paternalistic leadership is to spread atmosphere that merges fatherly benevolence with authority, while responsible leadership focuses on creating constructive dialogues with all stakeholders. The opposite of bureaucratic, directive or Machiavellian leadership is democratic, supportive or spiritual leadership (Elkhwesky et al., 2022a). Given that leadership styles could reduce the impact of the biggest problems in hospitality, such as employees’ rotation and poor performance, as well business management in an uncertain context, we strongly suggest that further research could be extended. This is in line with Elkhwesky et al. (2022a).

The influence of environmental, social, and governance activities on business performance should be examined (Ruan and Liu, 2021). Ch’ng, Cheah, and Amran (2021) suggest examining the influence of agile management, eco-innovation practices (e.g. marketing, management, and business model innovation), and six-sigma approach on business performance.

Conclusion

The impetus for this study has been formed as a result of the academic interest in restaurants’ business performance, the importance of indicating where restaurants’ business performance in literature has been and where it should go, and the lack of systematic and critical review for restaurants’ business performance research. Thus, our systematic review aimed at: demonstrating research contexts and designs utilized in restaurants’ research, indicating theories and measures utilized in restaurants’ business performance research, and mapping antecedents of restaurants’ business performance. Finally, we presented and discussed a roadmap for advancing future research in the area.

To accomplish these objectives, our research reviewed 33 articles that concentrated on restaurants’ business performance. Our study revealed that restaurants’ business performance research has advanced in the last 20 years, however, there are conceptual and empirical overlaps. Additionally, restaurants’ business performance research is restricted in research designs and research contexts. There is a lack of research on consequences and merging theories in publications. We expect by following our systematic review to move restaurants’ business performance research ahead and maintain to present substantial visions to restaurants’ business performance context over the next years.

Limitations of the study

Even though the WoS is one of the most well-known databases (Elkhwesky, 2022; Elkhwesky et al., 2022a), we recommend forthcoming research to include Science Direct. According to the knowledge of the researchers, the current study is the first to systematically and critically review restaurants’ business performance.

Footnotes

Acknowledgements

We would like to thank Prof. Islam Elbayoumi Salem for his constructive suggestions during the first stage of conducting our systematic review.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.