Abstract

This article analyses pension reforms in Central and East European countries in the aftermath of the 2008 financial crisis. The crisis revealed unresolved problems in the implementation of previous reforms, namely the financing of the transition costs. In their attempts to solve the funding-gap issue, the reforms needed to address legacies of past choices as well as the exceptional circumstances of the crisis. The interaction of fiscal constraints and political conditions shaped the variety of these reform outcomes.

Introduction

The 2008 crisis marked a turning point in the evolution of pension systems in Eastern Europe. Before 2008, a majority of countries in the region had reformed their pension systems along the model laid out by the World Bank (WB) in its influential 1994 report, Averting the Old Age Crisis. In contrast, pension reforms following the financial crisis were far more diverse. Some countries de facto nationalized their private pension funds, while others temporarily diverted contributions from private accounts into the public pillar and/or downsized the second pillar. This article analyses pension reforms in Central and Eastern European countries (CEECs). 1 It assesses the impact of the financial crisis on the political economy of pension reform and its transformation. In particular, it focuses on a key aspect of post-2008 reforms: the solutions to financing the transition costs of pension privatization.

Two claims are made on the politics and the political economy of reforms. First, pension privatization is still on the agenda in Eastern Europe, but the politics of reforms have changed. One of the countries that had not privatized before 2008 implemented pension privatization according to the standard WB model. There were also attempts at further liberalization of privatized pensions and moving closer towards the old WB model. However, as the WB and other international actors had stopped promoting pension privatization, it became an issue of domestic politics and an agenda of liberal right-wing parties. Second, the political economy of reforms also changed after 2008. The funding gap in covering the transition costs became the key issue. Unresolved problems in the implementation of earlier reforms became apparent and had to be addressed. The reforms were therefore a reaction both to the legacies of past choices, and to the exceptional fiscal circumstances brought by the crisis.

The outcome of pension reform policies in CEECs is discussed in the next section, followed by an analysis of the different solutions to the funding-gap problem, showing that financing through debt was a key implicit option. The remainder focuses on the politics of pension reforms after 2008. The diversity of reform outcomes in CEECs is explained by the combination of economic constraints and political factors. The need to pursue fiscal stabilization set the parameters for manoeuvre. However, the reaction was also conditioned by ruling party ideology and cabinet composition.

Reform outcomes

In the first wave of reforms in the late 1990s and mid-2000s, the majority of CEECs pursued pension privatization by implementing a three-pillar pension system (Table 1 provides an overview of pension reform trajectories in all Eastern new member states of the European Union). These pillars comprised: a publicly financed pillar, based on the pay-as-you-go (PAYG) principle; a compulsory fully funded second pillar; and a voluntary fully funded third pillar. 2 The Czech Republic and Slovenia were the only countries that did not implement this WB-style pension reform. They pursued only parametric reforms in their state-run PAYG schemes. 3

Pension reforms in Eastern EU member states.

System characteristics (total contributions as percentage of wage, contributions to second pillar); m/w: men/women.

Includes contributions for permanent disability and/or survivors’ pensions.

State of pension scheme as of 1 Jan 2008.

The second wave of reforms after 2008 saw a wide range of outcomes. Slovakia retained its second pillar and further attempted to decrease the redistributive nature of its pension system as well as the involvement of the state. The 2010–2012 right-wing coalition proposed an overhaul of the pension system that allowed for automatic and continuous adjustments of pensions awarded to new retirees. However, this reform was not implemented following a no-confidence vote in the government in October 2011. Poland also remained committed to the three-pillar system, but substantially reduced the size of the programme. The reform in Poland was implemented by a government led by the liberal right-wing party Citizens’ Platform (PO), historically a champion of pension privatization. The Czech Republic eventually implemented pension privatization as well, albeit at a more modest level than was common in the first wave of reforms among the CEECs. The reform breakthrough came after right-wing parties gained a strong majority in 2010. However, the second pillar (which is to be created in 2013) remains voluntary, with the requirement that those who opt for membership in the plan contribute an additional 2% of their gross salary. Of the group, only Slovenia remains a non-reformer. In 2010, the social-democratic-led government attempted to stabilize the pension system by gradually increasing retirement age, however the results of a trade union-initiated referendum rejected the measure. Hungary de facto nationalized its second pillar following the 2010 election of the right-wing Fidesz. The savings accumulated in the private funds were automatically transferred to the state by June 2011. While savers had the option to stay in the private system, the conditions set by the new law were so unfavourable that only 3% chose to remain (Simonovits, 2011: 93). As of January 2012, all pension contributions, including those paid by savers that remained in the second pillar, flow into the public PAYG system.

These second-wave pension reforms — despite their diversity — have one thing in common: they all reacted to the problem of financing the transition costs of pension privatization. As discussed in the following section, this problem remained unresolved in the first wave of reforms.

The funding gap

Pension privatizations in CEECs were legislated in states that already had mature PAYG systems. Active-age population and present pensioners had already accumulated pension rights, representing future liabilities on state budgets. PAYG systems cover pensions from present revenues. Pension privatization simply diverted part of these contributions to fund the second pillar. However, the subsequent funding gap in the first pillar was a result of the loss of resources previously designated to finance the pensions of those with accumulated pension rights. Diverting contributions also leads to reduction in contributors’ pension rights (i.e. claims on the budget after they retire). The funding gap that resulted from the first-wave reforms thus represents the transition costs of pension privatization.

As described, the transition costs are the result of pension contributions lost from the PAYG system due to the introduction of the second pillar and the subsequent claims on the PAYG system that the state avoided through the same mechanism. A stylized depiction of the development of this funding gap is shown in Figure 1. After introducing the second pillar, the number of people in the non-contributing workforce increases, while those who could in theory reduce the burden on the state – by receiving part of their pension from the second pillar – will in fact end up retiring decades after the reform has been introduced. 4 For instance, the transition costs of the Slovak pension reform adopted in 2005 were expected to peak around 2030, when costs would have reached approximately 2.9% of GDP. After this point, the number of retired workers who rely on the second pillar would have started to grow, thus reducing annual transition costs. Contributions lost and benefits spared due to the introduction of the second pillar would have evened out around 2052 (Ódor and Novysedlák, 2005).

The development of the funding gap.

Some proponents of pension privatization question the relevance of transition costs, claiming they merely amount to the implicit debt of the PAYG system being transformed into explicit debt. 5 While the latter statement is factually correct, it indicates a misunderstanding of the difference between implicit and explicit (real) debt. On the one hand, it conflates implicit debt and real deficits that can be generated by the PAYG system; on the other hand, the misunderstanding can lead to the perception that the funding gap and transition costs would be faced by governments in the future anyway in the form of a PAYG deficit. As this is incorrect, a short clarification is warranted.

Implicit debt is a theoretical construct that refers to expected liabilities in the form of payments to pensioners due in the future (see Cheikh and Palacios, 1996; Holzmann et al., 2004). In a PAYG system, these liabilities are financed by current revenues. The expected revenue streams could thus be understood as implicit financing. Real deficits can occur if current revenues do not match current liabilities. Over the long term, a PAYG system can therefore generate real deficits, or surpluses, if implicit debt and financing do not balance.

It is important to note that both implicit debt and implicit financing are mere theoretical concepts based on predictions about an uncertain future. Both of them depend to a large extent on pension legislation, which provides the necessary tools for balancing state-run PAYG schemes. Furthermore, future legislation-based liabilities of the state towards its citizens are of a very different nature from current accumulated debt, which is often held by non-residents (foreign investors). Implicit debt is a future liability that is theoretical and partly dependent on the creditor’s own legislation. By contrast, transition costs constitute a current and real liability that is often accumulated against foreign entities.

Finally, transition costs should not be understood as the funding of potential future deficits resulting from demographic ageing in a PAYG system. The introduction of a fully funded second pillar was seen as a solution to this problem during the first wave of reforms. However, from a macroeconomic perspective, a shift to funding is at best secondary since the only real measure to effectively counter demographic ageing is the retention of the level of economic output (Barr and Diamond, 2008: 94–104).

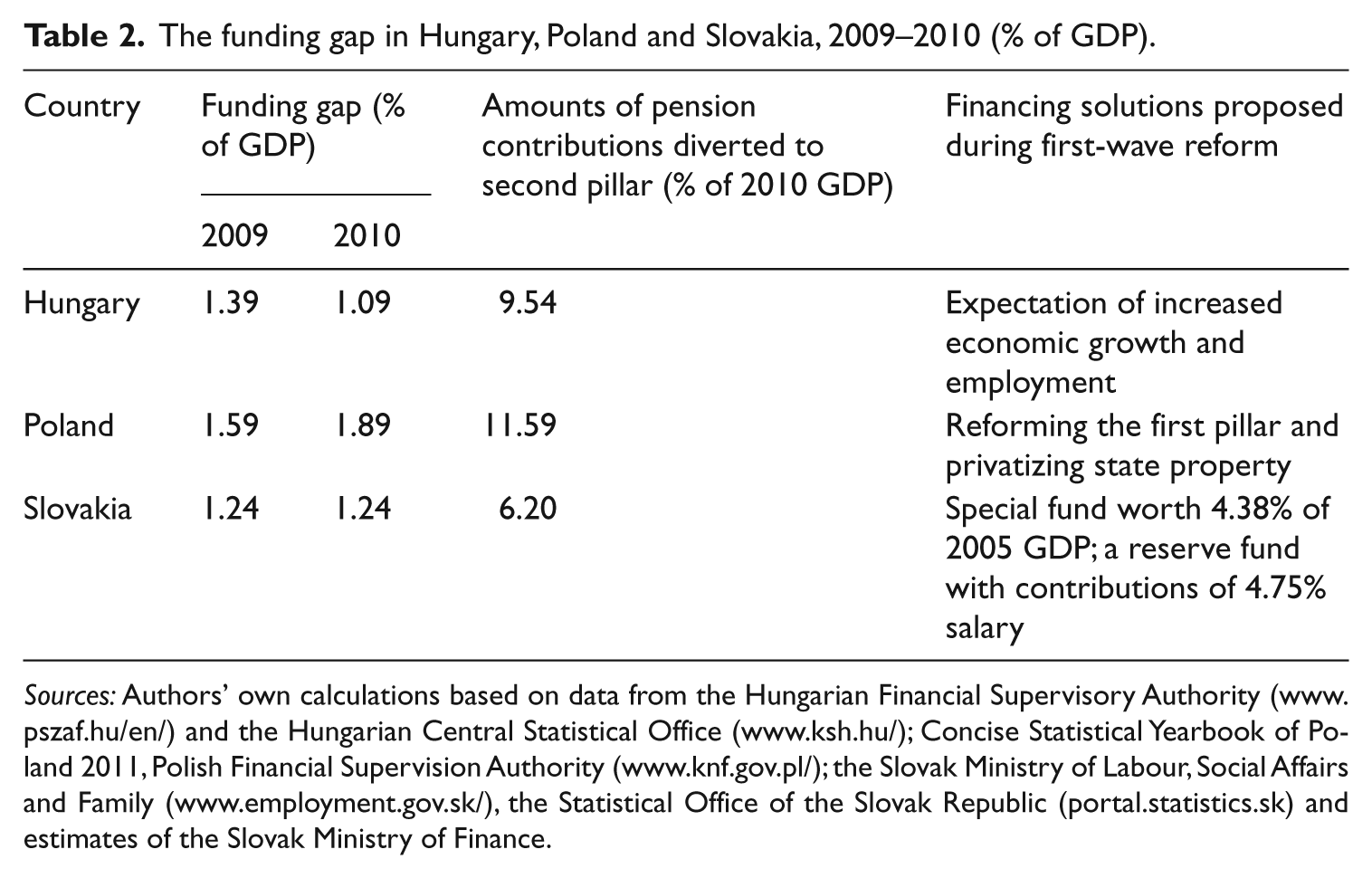

The funding gap created by pension privatization therefore represented a real liability that states needed to face in addition to the costs of demographic ageing (see Table 2 for data on reformers in CEECs). Transition costs could have potentially been covered through several means: increasing taxes, cutting spending in the general budget and/or the PAYG scheme, or by using the exceptional revenues from privatization. In addition, it was argued during the first wave of reforms that pension privatization could be (partly) self-funded and even generate additional revenues by increasing output and formal employment. Private pillars were therefore expected to motivate workers in the shadow economy to formalize their status since contributions paid would not be redistributed, but rather paid into workers’ private accounts. Privatization was also expected to increase output by channelling savings into more productive segments of the economy. However, such an effect is far from automatic as it requires several demanding conditions to be fulfilled. 6

The funding gap in Hungary, Poland and Slovakia, 2009–2010 (% of GDP).

Sources: Authors’ own calculations based on data from the Hungarian Financial Supervisory Authority (www.pszaf.hu/en/) and the Hungarian Central Statistical Office (www.ksh.hu/); Concise Statistical Yearbook of Poland 2011, Polish Financial Supervision Authority (www.knf.gov.pl/); the Slovak Ministry of Labour, Social Affairs and Family (www.employment.gov.sk/), the Statistical Office of the Slovak Republic (portal.statistics.sk) and estimates of the Slovak Ministry of Finance.

In Slovenia, the funding-gap problem was a major reason the country did not pursue a three-pillar reform. 7 Among the reforming countries, recognition of the funding-gap problem increased only gradually, as reflected in the financing plans. In Hungary, little attention was given to the funding-gap problem at the time of reform. Polish reforms did include plans to mitigate the problem, although they have gone largely unfulfilled. A late reformer, Slovakia, allocated actual privatization receipts and created additional revenue streams to fund transition costs. However, none of the funding plans proved sufficient to meet actual needs.

In Hungary, the funding-gap problem did not seem to have entered public discussion in the reform of the mid-1990s. Given how the advantages of fully funded systems were understood in debates at the time, the social democratic government assumed that introducing the three-pillar system would help increase employment and economic growth that would enable future governments to fill in the gap created in the first pillar. There was no intention to cut first-pillar contributions to fund transition costs, nor was there political will to balance the first pillar until 2010. To function properly, the state-run PAYG pension scheme required a subsidy of 2.3% and 2.0% of GDP in 2009 and 2010, respectively.

In Poland, the pension reform funding gap was to be financed by rationalizing the first pillar with new price-based indexation and by withdrawing early retirement options after 2006. Revenue from privatization was expected to cover initial costs before the rationalization of the first pillar became effective in financial terms. The reformers therefore expected that the PAYG system caused by the diversion of funds to the second pillar would initially generate an annual deficit of under 1% of GDP (Epstein and Velculescu, 2011) and that it would generate a surplus after 2012. 8

However, reality showed the transition to a three-pillar system to be more difficult than expected. In 2000, the increase in the annual deficit of the PAYG system due to the second pillar was approaching 1.5% of Polish GDP, and was constantly growing (see Table 2). The number of people joining the new system at this time was also considerably higher than expected: 10.5 million enrolled in the second pillar in 1999 as opposed to the expected 6–7 million (Hausner, 2002). Compounding the problem, privatization of state companies moved too slowly to cover the costs (Golinowska and Zukowski, 2011) and, most importantly, savings in the first pillar proved to be politically unfeasible due to electoral constraints. Pension indexation did not survive the debate in parliament on the original reform package and the ratio of the average pension to the average wage increased between 2000 and 2004. Although a centre-left government introduced price indexation in 2005, pensions soon returned to the mixed price-wage principle introduced by the pre-2007 conservative-right government. Moreover, the initial plan was not followed in cases of early retirement, nor was the retirement age for men and women equalized. Finally, a number of preferential treatments were introduced: judges, miners and army and police officers were excluded from the general defined-contribution system in 2003 and 2005. The disability insurance contribution rate was cut in 2007 (Bielecki, 2011; Égert, 2012). As a result, the total level of pension expenditure in Poland increased annually by around 0.5% of GDP between 1999 and 2009 (Chłoń-Domińczak and Stańko, 2011).

In Slovakia, the financing of transition costs was given more prominence than in Poland. In the debate preceding the reforms a two-prong solution was proposed. First, receipts from the privatization of the national gas company – 4.4% of GDP (2005) – were put aside to finance the new system and cover the first five years (2005–2010). Second, the government established a so-called ‘Reserve Fund of Solidarity’ in 2003 that currently collects contributions at a level of 4.75% of average salary. Although the fund was intended to cover deficits in social security in general, rather than to finance pension privatization, at present it has only been used to cover the PAYG deficits. Following a left-wing victory in 2006, no Slovak government seriously attempted to raise money through privatization, and thus the Social Insurance Agency relies entirely on state coverage of its mounting deficit.

For a number of reasons, the plans to finance the transition costs proved unrealistic among these first-wave reformers. Primarily, reformers underestimated the numbers of individuals entering the second pillar, leading to a higher funding gap than expected. In addition to this miscalculation, the expectations that pension reforms would lead to higher formal labour market participation or increased economic growth proved to be excessively optimistic. Finally, the policies laid out to fund the transition costs were either politically unfeasible (i.e. cutting pensions from the PAYG system in Poland) or insufficient for covering the expenses of the several decades long transition (i.e. privatization in Slovakia).

Debt financing proved a major implicit option among all reform efforts. In fact, a large part of the pension contributions towards individual accounts were invested into government bonds that had been issued to finance the costs of pension privatization in the first place. This mechanism – that circuitously returned funds to the government while still meeting its obligations – was most extreme in Poland, where approximately 70% of pension fund assets were invested into either state bonds or formerly state-owned companies (Bielecki, 2011). Relying on debt financing became more problematic after the financial crisis.

The financial crisis catalysed the funding-gap problem. This was evident in the 2011 Czech pension privatization reform. In contrast to previous efforts, this legislation was specifically designed to avoid a funding-gap crisis. The reform includes a smaller second pillar, however it is voluntary and subscribers must pay an additional contribution. The 2011 Czech reform plan intended to cover transition costs by raising VAT, but simultaneously spending cuts (including first-pillar pensions) were pursued. It is thus impossible to distinguish between financing through higher VAT and austerity measures.

The political economy of post-2008 reforms

The financial crisis in Eastern Europe after 2008 reduced the fiscal space for CEECs (see Myant and Drahokoupil, 2012). Public deficits and demands on state spending increased as revenues fell. However, the change in pension privatization cannot be fully attributed to this ‘exceptional fiscal circumstance’ (Beblavý, 2011). The economic crisis was one of several factors that contributed to the transformation of the political and economic context surrounding these reforms.

Even before the financial crisis hit the region, it was obvious that pension reform was an unprecedented burden on public finances. The fiscal freedom to manoeuvre had been significantly limited before the crisis due to the Maastricht Criteria. This limitation was particularly stinging after the European Union (EU) rejected CEE member states’ attempts to exempt pension privatization transition costs from the criteria. Maastricht obliged new member states to keep their public deficit and public debt under 3% and 60% of GDP, respectively. As of 2007 debt stemming from the funding gap must be counted as a part of public debt according to Eurostat (2004), although the European Council ruled in 2005 that transition costs will be partially exempted from the Maastricht debt-criteria for a short transitory period (EC, 2005: Art. 3.4).

Moreover, the WB changed its view on pension privatization. The Bank’s active promotion of pension privatization had a major influence on the first wave of reforms and constituted an important base of political support for reformers (Müller, 2001; Orenstein, 2008). However, consensus on the issue within the WB had already begun to unravel before the crisis. By 2008, WB’s pension privatization advocacy campaign had effectively ended (Orenstein, 2011). This was similarly echoed at the International Monetary Fund (IMF), which also stopped promoting pension privatization after 2008, providing even tacit support to scale down and even close second-pillar systems in countries relying on the Fund’s financial assistance.

These moves signified a broader shift in the overall discipline following the first wave of pension privatization encouraged by the WB, which stimulated a learning process in both international policy-making networks and among experts in CEECs. The propositions of the WB’s Averting the Old Age Crisis were subjected to a wide range of criticism (e.g. Barr, 2000; Fultz and Ruck, 2000; Orszag and Stiglitz, 2001). Therefore it became less common among experts to make assumptions about growth-stimulating effects of funding. No longer was pension privatization seen as a solution to demographic ageing or assumed to automatically stimulate growth. In CEECs, first-pillar stabilization became a significant part of the debate, which had not been the case in the first wave of reforms.

Finally, the maturation of the first wave of CEE reforms contributed significantly to the learning process. New data made it possible to evaluate the performance of pension funds in terms of their return rates, charged fees and investment strategies. This maturation also exposed the unresolved problem of transition costs, a problem that could no longer be ignored, as sizeable austerity measures seemed to require continued financing of these reforms. 9

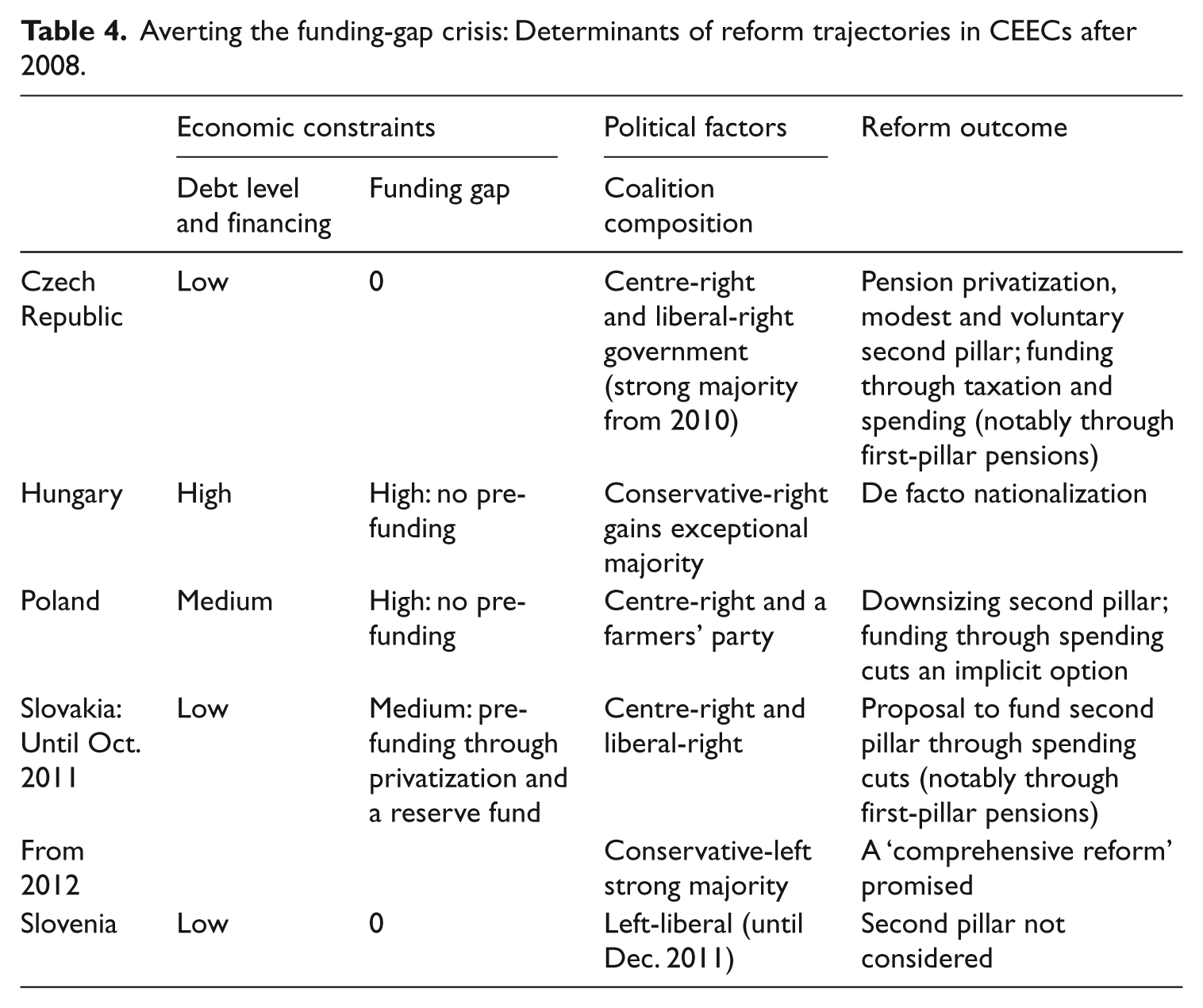

The new circumstances, such as the WB’s withdrawal from the privatization agenda, changed the politics of pension reform, making it essentially a domestic affair. However, the reforms in CEECs reacted to the legacies of earlier choices, namely the unresolved financing of transition costs. The combination of the tougher fiscal environment and the growing transition costs prevented further deferral of these debts. Dealing with the funding gap thus became a matter of distributing the costs in the short term. The actual solutions to this dilemma were the result of both fiscal constraints and political conditions. Countries with high constraints had little choice other than to (temporarily) scale down the second pillar. The policy towards the pillar, however, also reflected political factors that came into play when fiscal constraints allowed more room to manoeuvre.

Economic constraints

The fiscal constraints on the second pillar resulted from a combination of economic and political factors. These included the ratio of the funding gap to the budget deficit and whether governments had the ability – or willingness – to cover the latter through new debt or immediate spending cuts. The issue became vitally important in the aftermath of the 2008 financial crisis that created a noticeable drop in revenues, which in turn led to increasing budget and pension account deficits. The fiscal strain eventually pushed second-pillar reforms onto the agenda as these contributions amounted to a substantial revenue loss. The increasing pressure on national budgets only compounded the growth in indebtedness. Given these circumstances, it is hardly surprising that the CEECs came to see the funds accumulated in the second pillar as a large source of potential revenue that could help balance the budgets, or repay the debt.

With Hungary’s exception, levels of indebtedness in CEECs were modest. Although there were no problems with financing public borrowing, these governments still faced growing deficits. Following a Europe-wide trend, the Czech Republic, Slovakia (2010) and Poland (2011) all chose to address the problem with austerity policies (Myant et al., forthcoming).

Hungary dealt with the funding problem differently. The country was particularly vulnerable to the crisis due to its dependence on credit from abroad. As a result, after October 2008 the government experienced significant problems in financing its debt and was forced to request funding from the IMF and the EU. These economic constraints were crucial for the decisions to de facto nationalize the second pillar in 2010. The one-off transfer of accumulated assets amounted to 10% of GDP and allowed the government to balance the budget through revenue increases at a delicate time when it had decided to terminate its stand-by agreement with the IMF.

The decision to de facto nationalize the second pillar could be interpreted as a consequence of political change: Fidesz – a long-term opponent of pension privatization – took power with an overwhelming majority in the May 2010 elections. However, fiscal conditions had made pension nationalization popular on both sides of the Hungarian political spectrum. The first proposal of this kind came in 2009 from an eminent former central banker, György Surányi, who was then a potential prime ministerial candidate for the Socialist Party. Moreover, the idea had already been contemplated in the Ministry of Finance during the socialist government of 2006–2009.

The need to balance the budget was also pressing in Poland, which – along with a somewhat higher level of indebtedness – faced regulatory constraints on increasing public debt. The government agreed with the EU to reduce its budget deficit to approximately 2% of GDP by 2012. Moreover, self-imposed restrictions triggered penalties if public debt crossed the 55% level. The decision of the ruling party PO to scale down the second pillar was primarily motivated by immediate budget constraints (cf. Naczyk, 2010; Rae, 2011).

Slovakia’s transition costs also contributed significantly to increasing indebtedness, but, as its debt-to-GDP ratio was a healthy 40%, the country did not need to balance the budget immediately. Moreover, after a 4.9% contraction in 2009, Slovakia’s economy appeared to have quickly returned to a growth of 4.4% in 2010.

New politics of pension reforms

The end of the WB’s privatization campaign, coupled with the learning processes following the maturation of the first wave of reform, changed the politics of pension reform in CEE. Economic and regulatory constraints limited the funding of transition costs through debt. However, these setbacks did not represent the ‘death’ of the privatization agenda. The WB’s withdrawal from the pension privatization agenda made pension privatization a domestic political issue. The respective decisions made by national governments regarding the second pillar were thus determined by the ideology of the ruling party. As coalition governments were typical in CEECs, the coalition composition shaped the policy output.

Party positions on pension privatization became structured by the left/right divide and the conservative/liberal dimensions (see Table 3): while left-wing parties preferred policies that allowed for decommodification and redistribution, liberal parties pursued limiting the role of the state in favour of market processes. Pension privatization thus became an agenda of the liberal right. The post-2008 reforms were therefore a result of both economic constraints and cabinet ideology. (An overview of the conditions and outcomes is provided in Table 4.)

Party ideology and expected preferences towards pension privatization.

Political parties characterized by respective ideological positions in italics, Slovenian parties not displayed as the three-pillar model is not on the agenda in the country.

Averting the funding-gap crisis: Determinants of reform trajectories in CEECs after 2008.

Although party ideology and coalition politics had also been important determinants in the first wave of pension privatization reform, the left/right dimension was far less prominent (see Armeanu, 2010; Guardiancich, 2011). This can largely be attributed to the facts that in the first wave of reforms most CEECs deferred finding solutions to financing the funding gap to the future, and that information about the actual costs and benefits of these programmes was poorly distributed due to the numerous reform ‘myths’ (Barr, 2000; Barr and Diamond, 2008). These myths, such as that funding resolves adverse demographics, also contributed to the conflation of the problems of pension privatization and stabilization of PAYG systems. As financing through debt became more difficult – and the actual costs of pension privatization became less obfuscated – the funding of transition costs became an immediate distributional issue.

Liberal right-wing parties continued to support pension privatization after 2008. Funding transition costs through spending cuts also fitted with the ideology of reducing the size of the state. These parties tended to support reforms that individualized insurance against old-age risks; increased the scope for markets in old-age insurance; and dismantled redistribution through the pension system. 10 Increasing VAT thus seemed to be the tax increase of choice for right-wing parties. However, liberal-right ideology is ambiguous on the desirability of a compulsory second pillar as the obligation to take insurance infringes upon individual choice. A compulsory system can also imply an implicit state guarantee for the second-pillar pensions. Given this ambiguity, the considerable reform costs were likely to split the right, as funding obtained through spending cuts and tax increases also threatened re-election prospects. The more pragmatic centre-right parties eventually accepted a more modest second pillar than had been common in the first wave of reforms.

Coalitions of centre-right and liberal-right parties shaped reform outcomes in Slovakia and the Czech Republic. The Slovak government reacted to the need to confront the funding gap by proposing to finance the second pillar through spending cuts – in particular by reducing first-pillar pensions. In the Czech Republic, an exceptional majority won the 2010 elections, allowing right-wing parties a reform breakthrough. Their concern with the ability to finance the funding gap led to reform that involved a more modest and voluntary second pillar, funded through VAT increases and spending cuts – also in the first pillar.

Conservative-right parties, in contrast, were more likely to oppose a second pillar, particularly if confronted with the financing of transition costs. They saw little value in expanding the scope for the market since it reduced the power of the state in directly influencing distributional outcomes. Conservative-right ideology at the time did not favour redistribution from higher-income groups, but preferred to influence the degree of decommodification directly as allowed by the parametric reforms of the first pillar.

As discussed earlier, the conservative right-wing Fidesz came to power in Hungary after its landslide victory in 2010 and implemented a de facto pension nationalization. The Polish Law and Justice Party (PiS) was in opposition, but it too put forward a proposal for making the second pillar voluntary with similar implications (see Rae, 2011).

Left-wing parties, both liberal and conservative, should have opposed privatization, as it commodifies pension insurance and dismantles redistribution through the first pillar. The position of left-wing parties on pension reform was ambiguous in the first wave (cf. Armeanu, 2010), with the left actually pursuing privatization in Hungary and Poland. Left-wing ideology also tended to oppose any pension cuts in the first pillar despite the fact that these cuts had provided a major source of revenue to fund transition costs. This can be attributed to poor information about the actual implications of pension privatization models and transition costs. As the first-wave reform matured and the information about its costs and benefits became more widespread, it became more apparent that privatization could neither solve first-pillar imbalances, nor deliver higher pensions.

The strong power of the left and the unions caused the three-pillar model to disappear from the Slovenian political agenda after the failed reform of 1998. In Slovakia, the Smer government of 2012 scrapped the reforms of the 2010–2012 right-wing government and planned a downsizing of the second pillar. Finally, in the Czech Republic, social democrats have mobilized against pension privatization promising to reverse such reforms if they take power.

Conclusion: What future for pension privatization?

In the diversity of post-2008 pension reforms, three broad categories of common features defining a new privatization agenda can be identified.

First, the new political economy surrounding these reforms does not allow the deferral of costs to the future. A much more modest second pillar, financed by about 3 percentage points diverted from the first pillar, seems to be the politically feasible maximum in CEECs. Liberal right-wing parties have thus faced electoral constraints regarding spending cuts and tax increases implied in financing second pillars. In the Czech Republic and Poland, proponents of reform have apparently accepted this point of view. The political feasibility of Slovak right-wing reform proposal was never tested. The cuts were anyway scheduled for later periods.

Second, the reforms that followed the 2008 financial crisis exposed the political risks of pre-funded schemes. The Hungarian example demonstrates that accumulated funds can be effectively nationalized. The risk of such nationalization can be correlated with the volume of funds accumulated on pension accounts on the one hand, and the narrowness of fiscal space on the other. The latter will certainly grow in coming decades and the likelihood of the former increasing is similarly high. The evidence shows that a formalized cross-party consensus on pension privatization during the first wave of reforms could have potentially counterbalanced future political risks, but such consensus was lacking in CEECs.

Third, although pension privatization has clearly lost much of its initial appeal in the region, this should not be taken as its final defeat. As Orenstein (2011) discusses, a rebirth of privatization in a different form is possible. This is evidenced by a shift among privatization proponents who are now less likely to extol the virtues of the second pillar as a solution to demographic ageing. Instead, ideological and social justice arguments have become more prominent (e.g. reducing the role of the state, creating property rights, reducing redistribution). Risk diversification appears to be the main macroeconomic argument proposed in favour of the multi-pillar system. 11 Several opponents of the second pillar are thus still in favour of the third pillar. This suggests that the reform reversals of the past few years may yet lead to the strengthening of the private component in the pension-policy mix via the third pillar.

Footnotes

Funding

This paper was partly funded by the German Science Foundation (DFG) project DR 827/2-1 ‘Weathering the crisis?’ (PI Jan Drahokoupil) and the EU-FP7 project GUSTO, based at the University of Warwick (PI Colin Crouch).