Abstract

Today’s regime of financialized capitalism requires individuals to engage with financial products and services to ensure their financial security and welfare. Within this regime, institutional actors formulate and communicate imaginaries of the future that prompt individuals to embrace particular financial logics, understandings, and practices in managing their personal finance. Financial literacy and education is an important institutional field where such imaginaries are formulated and communicated to the public. This article examines the notions and themes articulated in programs of financial education currently conducted by state and non-state organizations in Israel, considering the ways in which proper conduct in key financial activities (debt and credit, saving and investment, and insurance) is defined, explained, and justified. We argue that, replete with explicit and implicit references to emotions and emotional states associated with practices of everyday finance, these programs mobilize them to govern individuals’ imaginaries of the future and financial conduct according to the model of the desired responsible financial subject. This emotional dimension represents a significant component in the cultural political economy of the constitution of financial subjectivities and the culture of financialization, that naturalizes the behavioral and dispositional requirements and demands that everyday finance poses to the general public.

Introduction

In the current era of financialized capitalism, social and economic risks have shifted from the state and other public organizations to individuals and households, resulting in the individualization, privatization, and marketization of risk management. This regime requires individuals to engage with financial products and services to ensure their present and future financial security and wellbeing (Amable, 2014; O'Malley, 2015). We thus witness a process of financialization of everyday life, whereby the general public’s productive engagement with financial logics and instruments of risk management is regarded as critical to secure socio-economic life, both at the individual and societal level (Langley, 2020). Supporting and promoting this socio-economic order, in which facing risks and uncertainties is largely a private, individual matter, organizational actors populating varied institutional fields formulate and communicate imaginaries and projections of the future (Beckert and Bronk, 2018; Zaloom, 2018) geared to prompt individuals to make particular decisions and undertake actions concerning their personal finance.

An important institutional field in which these imaginaries are formulated and communicated to the general public is the field of financial literacy and education. Reflecting and boosting broad ideological, institutional and structural changes by which neoliberal logics of action and organization become entrenched in different spheres of life, international organizations such as the OECD and the World Bank, as well as local state and non-state actors, promote the notion that the provision of financial education is crucial for individuals to attain the information, knowledge and skills considered necessary for participating as proper actors in the financial sphere. The basic idea underpinning this political endeavor is that equipping individuals with these resources is essential for enabling them to take responsibility for their current and future financial wellbeing. As neoliberalism renders engagement with financial markets a central means for assuring individuals’ economic security and wellbeing, they are required to be inclined and capable of dealing with various technical and substantive aspects of everyday financial practices in accordance to established rules and conventions (Langley, 2008, 2020). However, financial education programs do not solely aim to raise individual’s awareness of financial uncertainties and risks and impart technical instrumental knowledge. It rather operates as a technology of governance, formulating and communicating a model of the proper financial subject, and specifying the dispositions and understandings considered necessary for engaging effectively and responsibly with financial practices (Arthur, 2012; Marron, 2014).

Specifying desired attributes and their behavioral manifestations, financial education programs define the desired financial subject as not only possessing certain cognitive abilities and technical knowledge, but also particular moral and emotional dispositions (Maman and Rosenhek, 2019) . In this article, we attend to the emotional dimension of financial education, examining how such programs construe and mobilize emotions to communicate and promote a model of the proper financial subject. Our analysis shows that this is accomplished by assigning emotional meanings to imaginaries of desired and undesired futures attached to individuals’ financial conduct, thereby motivating the public to adopt particular financial practices and develop certain financial subjectivities.

Our empirical case study follows financial education programs currently conducted by state and non-state actors in Israel. We examine the diverse themes and notions communicated in textual and audiovisual materials, analyzing how they define and explain proper and improper conduct in key everyday financial practices—debt and credit, saving and investment, and insurance—especially attending to how modes of financial conduct are portrayed as connected to emotionally charged imaginaries of the future.

The analysis suggests that although financial education programs present themselves as essentially informative, they are actually replete with explicit and implicit references to emotions and emotional states. The programs present imaginaries of the future that connect practices of personal finance and their consequences to positive and negative emotional states, aiming to affect individuals’ expectations and projections concerning possible futures and to prompt them to take particular financial decisions and actions. By detailing imaginaries of desired futures and promises of “the good life,” and mobilizing positive emotions, such as desire, hope, and optimism, they work to establish the notion that individuals can affect positively their financial future by adopting proper financial conduct today. Equally important, detailing threatening futures that elicit negative emotions, such as worry and fear, the programs aim to goad individuals into managing their personal finance responsibly, communicating the idea that accepted rules of financial caution and rational planning are essential means to effectively face risks and uncertainties.

We next introduce our conceptual framework, addressing analytical connections among emotions, imaginaries of the future, and financial dispositions and conduct. We focus mainly on the mobilization of emotions by institutional actors aiming to affect individuals’ expectations and imaginaries as a means to promote particular understandings of personal finance and motivate them to take particular financial actions. Then we address the character and functioning of financial education as an important technology of governance within a context of neoliberal financialization. In the following sections we present the research setting and methods, and our empirical analysis of financial education programs’ mobilization of emotions to formulate and communicate imaginaries of the future as connected to individuals’ modes of financial conduct. We conclude by discussing the significance of our analysis for the study of the political-cultural foundations of the financialization of everyday life, addressing the role of emotion mobilization in the functioning of technologies of governance implicated in the structuring and regulation of individuals’ understandings of, and engagement with financial logics and instruments.

Emotions, imaginaries of the future, and everyday finance

The last couple decades have seen a growing interest in the key role that emotions play in social life, and particularly in economic action (e.g., Berezin, 2009; Illouz, 2018; Loewenstein, 2000; Pixley et al., 2014). Bericat (2016), who summarized four decades of research in the sociology of emotions, defines emotions as mental states that manifest the importance and meaning that events in the natural or social world have for the subject (p. 493). As suggested by Stets and Turner (2014), the sociology of emotions addresses emotions as an outcome of social factors and conditions that affect how subjects experience reality as well as the modes in which they communicate these experiences. Thus, individuals’ emotional states are considered as embedded in social life, regarding both their sources and their effects on social action.

In the field of economic sociology most studies address the ways in which emotions and emotional states affect individuals’ preferences and behavior in diverse fields of economic action (e.g., Bandelj, 2009; Pixley, 2012; Zaloom, 2012). In the financial field, some studies consider emotions in traders’ conduct, critically examining the common sense notion that successful traders must neutralize their emotions (Ailon, 2015; Borch and Lange, 2016), while others consider the role emotions play in individuals’ investment and credit decisions (Gambetti and Giusberti, 2012; Marston et al., 2018). Building on Keynes’s classic notion of animal spirits (1936), studies also examine the emotional dimension of financial panics, which are considered as resulting from strong negative emotions that motivate protective action when individuals realize they can no longer control financial events and outcomes (Ackert et al., 2003; Bracha and Weber, 2012). Focusing on emotions’ influence on financial decisions and actions, these studies consider emotions as given and operating primarily at the individual level, thus providing a limited account of the emotional dimension of the functioning of the financial sphere, particularly concerning the political character of the connection between emotional states and everyday practices of personal finance.

Concerned with shedding light on the emotional facets of the financialization of everyday life, in this article we focus on the ways in which various institutional actors construe and mobilize emotions in order to produce desired individuals’ understandings and financial subjectivities, thereby goading them into adopting particular modes of financial conduct. We posit that a key mechanism connecting emotions to financial conduct is the formulation and communication of imaginaries and projections of the future. Financial conduct is essentially future-oriented, based on particular imaginaries of possible future economic states. As Jens Beckert (2016) notes, since future developments are unknown and fundamentally uncertain, actors making consumption, credit, and investment decisions draw on fictional imaginaries of how the future will look, how and by what it is affected, and how their own decisions might lead to wanted or unwanted outcomes. Given the essential uncertainty of the future, the images and specific expectations that affect actors’ conduct arise largely through imagination, rather than rational calculation (Appadurai, 2013; Zaloom, 2009). While evaluating possible courses of action and financial planning, subjects formulate “projective fictions” of economic futures that help them to define feasible goals and means (Zaloom, 2018). Addressing fundamental uncertainty, imaginaries of future economic opportunities and risks tend to carry a strong emotional charge, both responding to and generating powerful emotions, such as fear, anxiety, desire, and hope (Beckert and Bronk, 2018; Emirbayer and Mische, 1998).

As indicated by Zaloom’s concept of “regimes of foresight” (2018), though individuals are those that imagine economic futures, these imaginaries are essentially social, founded upon established cultural codes and categories, and connected to broad political and institutional conditions and configurations. Influential institutional actors—state agencies, firms, experts, and the media—generally formulate, frame, and communicate these imaginaries, defining future economic states as probable or improbable, desirable or undesirable. The more powerful the actors, the more effectively they will shape individuals’ expectations by bestowing legitimacy and credibility on particular imaginaries and discrediting others (Beckert, 2016). In their deliberate efforts to shape expectations and imaginaries of the future, institutional actors employ not only technical calculative methodologies and devices, such as business plans, discounted cash-flow analysis, and firms’ and countries’ credit ratings, but they also utilize less formal discursive instruments: stories about the past, individuals’ personal experiences, and causal narratives about the economic world (Beckert and Bronk, 2018). These discursive instruments frequently include a salient emotional dimension, that impart them with special weight as a means to influence individuals’ imaginaries and projections.

Formulated and communicated in particular institutional contexts, imaginaries loaded with emotions, like fear and hope, aim at motivating individuals to make decisions, particularly under conditions of uncertainty (Bandelj, 2009; Beckert and Bronk, 2018; Swedberg, 2017). For instance, Pixley (2012) identifies financial sector actors’ mobilization of emotions such as confidence, optimism, pessimism, fear, and trust as they attempt to shape the public’s expectations concerning future economic developments, thereby affecting actions and decisions. Furthermore, emotion mobilization is prominent in the formulation and communication of desired financial subjectivities. In his study of practices of credit reporting, Langley (2014) describes how firms offering credit scores products construe the neoliberal subject as animated by fear and anxiety about potentially failing to make credit repayments, and by optimism and hope of being able to properly manage her personal finances. Similarly attending to the emergence of neoliberal subjectivities, Fridman (2017) discusses how emotional work, particularly the mobilization of hope for a future of financial freedom, plays a key role in efforts to transform the self promoted in the field of financial self-help. These studies suggest that imaginaries of the future charged with emotional meanings are particularly important in the formation of undestandings and modes of conduct in the financial sphere, including the general public’s modes of engagement with practices of personal finance. Furthermore, they indicate that influential institutional actors are often involved in the formulation and communication of these imaginaries as a means to influence the ways in which individuals act as financial consumers. These two insights, which point to the essential role of institutional actors in the crafting of social imaginaries, will serve us to examine how financial education operates as a technology of governance aimed at constituting a particular type of financial actor in accordance to the logic of neoliberal financialization.

Financial education as a technology of governance

In the last two decades, the institutional field of financial literacy and education has gained momentum, especially since the 2008 global financial crisis. One among a wide range of new technologies of governance resonant with financialized capitalism, its introduction and development have accompanied and supported the expansion and deepening of the financialization of economic and social life (Langley, 2014). Studies drawing on the Foucauldian concept of governmentality consider notions of financial literacy and practices of financial education as key institutional devices for structuring and regulating individuals’ engagement with financial institutions and practices (Arthur, 2012). In this vein, Marron (2014) describes notions of financial literacy and practices of financial education as “a form of advanced liberal governmentality” (p. 491), a tool that enables to govern individuals “at a distance” (p. 501). As an instrument of discipline and responsibilization, this technology of governance involves regulating the mindset, understandings, and conduct of individuals mainly by communicating and promoting particular moral motifs, modes of knowledge, and conventions (Maman and Rosenhek, 2019, 2020).

Both global and local state and non-state actors promote financial literacy as a set of knowledge, skills, and attitudes defined as underpinning individuals’ proper and responsible financial conduct (Aprea et al., 2016; Lazarus, 2020; Ribeiro and Soares, 2017). Thus, financial education programs not only aim to disseminate information, but also, and primarily, to induce basic changes in individuals’ understandings and behavior in the financial sphere, making them able and disposed to manage risks and assume personal responsibility for their current and future economic situations (OECD and Russia’s G20 Presidency, 2013). Promoting individual responsibilization in financial matters through the formulation and communication of a particular model of the proper financial actor, financial education operates as an important political instrument of moralization that contributes to the naturalization of the financialization of everyday life and its inequalities and power relations (Maman and Rosenhek, 2019).

In this article we draw on the analytical insights provided by economic sociology concerning the key role of emotionally charged imaginaries of the future in the formation of subjectivities and action related to the financial sphere, to probe the operation of financial education as an important technology of governance supporting the financialization of everyday life. We elaborate on, and extend that scholarship by showing how institutional actors involved in financial education mobilize emotions to affect individuals’ imaginaries of their financial future, thereby attempting to govern their understandings and conduct concerning personal finance in accordance to the ideological and institutional foundations of a regime of neoliberal financialization of everyday life.

Research on the emotional dimension of financial education in some countries, such as Sweden (Pettersson and Wettergren, 2021) and South Korea (Kim, 2017), indicates that the mobilization of emotions is an important and widely used strategy in financial education programs. In the Korean case, private initiatives to educate individuals to become rich refer to feelings of hurt and memories of suffering, whereas in the Swedish case, programs of financial education jointly conducted by state and non-state organizations aimed at promoting citizens’ financial literacy appeal to emotions of boredom, fear, trust, fun, and hope. In both cases, financial education programs mobilize emotions as an instrument to raise individuals’ awareness of issues of personal finance. In this regard, financial education operates similarly to social and commercial campaigns in other domains, which appeal to emotions as a tool to produce people’s identification and commitment to certain messages and to affect their attitudes (e.g., Weber, 2012). In our following analysis, we suggest a broader perspective, which focuses on how emotions are mobilized to structure and regulate individuals’ engagement with financial institutions and practices at a deeper level. We show how institutional actors involved in the field formulate and communicate emotionally charged imaginaries of the future, that are geared to propel individuals to adopt understandings and develop dispositions and modes of conduct appropriate to the desired responsible and productive financial subject.

Research setting and methods

As in many other countries, financial education emerged in Israel as an institutional field with numerous actors conducting educational programs and activities to impart knowledge, develop dispositions, and promote particular modes of financial conduct among the general population (for a detailed account of the emergence of financial education in Israel, see (Maman and Rosenhek, 2019). The most salient actors active in the field include several state agencies, NGOs, and private financial firms. Their diverse educational activities comprise special programs for schools, courses of varying length and workshops targeting diverse population groups, publication of brochures, booklets and dedicated websites, and dissemination of instructional material through social media. Many organizations also produce videos, mostly animated, which they publish on dedicated websites, broadcast on television, and post on social media (Facebook and YouTube).

In this study, we focus on textual and audiovisual contents produced and published in social media and websites dedicated to promote financial literacy among the general young and adult population. We collected and analyzed the texts, videos and illustrations produced by the main state agencies involved in the field (the Ministry of Education, the Ministry of Finance, the Israel Securities Authority, and the Bank of Israel), and by several prominent non-state organizations, including one financial firm (Bank Hapoalim) and two NGOs (Paamonim and Adva Center). 1 All data were analyzed using critical discourse analysis (Wodak and Meyer, 2016), examining the notions, principles, and norms of conduct that the programs formulate and promote, particularly the ways in which they portray and explain three main areas of personal finance: debt and credit, saving and investment, and insurance. We examined also how these actors define and describe proper and improper conduct and their consequences for the economic and social life of individuals and families. We interrogated which emotions are explicitly and implicitly conveyed in the texts, videos, and illustrations, and how they connect emotional states to individuals’ and families’ financial conduct and conditions.

We complement this data with open, semi-structured interviews that we conducted in 2018–2019 with 12 senior officials who have played key roles in promoting notions and practices of financial education in the aforementioned organizations, and developing and implementing specific programs: five of them from state agencies, three in Bank Hapoalim, and four in the NGO Paamonim. The interviews focused on how the organizations define the character and functions of financial literacy and education, and on the ideational and institutional settings within which the programs were developed. More specifically, the interviews provided us with information on how the organizations specify the goals of financial education and the appropriate means to reach them, how they characterize the contents, methods and tools of their programs, and the strategies and resources they use to advance their ends, including the mobilization of emotions through the formulation and communication of emotionally charged imaginaries. 2

Emotions in financial education programs: Affecting imaginaries and motivating action

Offering emotionally charged imaginaries

Financial education programs articulate narratives of possible futures, specifying to their audiences what they must do in order to actualize desired financial futures and avoid worrisome ones. Seeking to attract attention and generate receptivity among their target audiences, these programs communicate imaginaries of the future that explicitly refer to particular emotional states. Furthermore, in interviews, officials involved in the field noted that stories with a high potential to arouse emotions are a crucial tool for shaping individuals’ understandings and expectations regarding personal financial conditions and practices. For example, officials in Paamonim explained that in their workshops for families in financial distress they evoke stories of families who have succeeded in attaining financial balance. They employ these narratives to arouse hope for a better future and a sense of control, using arguments such as “I saw other people in a worse economic situation than yours and they reached financial freedom” (Interview, 22 February 2019). Similarly, the Head of the Investor Education Unit of the Israel Securities Authority noted how its financial education campaign uses emotionally loaded stories to influence public understanding of finance: “If I present a story of a holocaust survivor who suffered a lot in his life, and in 3 weeks lost more than one million shekels…this is meaningful” (Interview, 12 April 2018).

To assist individuals in imagining personal financial futures in familiar and meaningful ways, the programs refer to different life stages—childhood, adolescence, adulthood, and retirement—specifying the financial needs and tasks characterizing each stage and clarifying what one could expect and how to prepare for each stage. Presenting images of the future that weave into the fabric of our daily lives connects it to the present, making the future appear more manageable and expectations more certain (Mische, 2014; Pixley, 2002). Associating specific opportunities and risks to different stages in the life cycle, the programs mobilize negative emotions, particularly the anxiety that an uncertain future elicits, while also offering imaginaries of a controllable and desired future that can be reached through proper financial conduct. For example, the following excerpt from the Ministry of Finance’s financial education website notes the essential uncertainty of the future, but also explains that engaging with financial instruments is the appropriate way to handle it: Why it is important to worry about your future? If there is one thing we can be certain about, it is that the future will come... Along the way we will encounter many surprises, not all of them pleasant… In order to be prepared for any event, expected or unexpected, and to be able to fulfill goals and dreams, think about what you will need for this, plan for the future, save, buy insurance, consider taking out loans. This is the way to build a brighter future for you and your loved ones… It is important to be concerned about your future... Proper financial conduct today will help you to build a better tomorrow.

3

Aspiring for “the good life” and its emotional connotations form a central imaginary in financial education, linking it to two constitutive principles of what it defines as proper financial conduct: setting of goals and planning. The Director of Group Activities at Paamonim told us: “A clear and achievable plan of action instills hope… Participants in the workshops define an economic goal, which they aspire to achieve…, it could be to close their overdraft, to fly abroad, it could be anything, which encourages them and motivates them to action” (Interview, 22 February 2019).

As the two quotations above indicate, hope is a key emotion that financial education programs seek to mobilize, formulating and communicating the basic maxim that individuals can make their desires and dreams come true by adopting proper financial conduct. The Bank of Israel’s educational program targeting the youth, in expressing the desires typical of young people, similarly stresses systematic planning as the way to fulfill them: “Ask yourself what you want. A smartphone? A new computer? Are you thinking of studying after your military service? Check how much it costs. Set short and long-term goals.” 4 Planning is presented here as the fundamental practice through which individuals’ should craft “projective fictions,” that is, these visions of the future that serve to guide their financial conduct in the present (Zaloom, 2018). In this way, rational planning, as the means to fulfill desires and hopes, is loaded with emotional meaning.

Likewise, the Finance Ministry’s website targeting adults refers to aspirations typical of this life stage, using terms and images aimed at instigating imaginaries of a bright future charged with positive emotions. Communicating a morality of individual responsibility and a connected emotionality of future-looking hope, its central message is that each individual is solely responsible for realizing her dreams: “Your dreams are your future—don’t you want to determine how it will look?”

5

The webpage identifies several typical dreams and details ways to accomplish them, accompanying the text with visual images that vividly communicate the sense of pleasure and self-satisfaction that one achieves when realizing one’s dreams (see Figure 1): All of us have dreams. Some people dream of buying a new apartment, others of buying a car or having a luxurious vacation. To achieve your dream, you need to define what you want—and then the sky’s the limit. Even though it seems far away, step-by-step you can realize your dream.

6

Ministry of Finance, “My Treasure: My Situation, How to Finance Dreams?” http://haotzarsheli.mof.gov.il/LifeState/Pages/Dreams-Come-True.aspx

As we can see, financial education formulates a model of the desired rational and calculative financial subject, communicating the message that individuals should set goals, clearly define and prioritize them, weigh alternative actions, and, finally, select the most effective means to achieve those goals. Interestingly, the guidelines for performing rational and calculative conduct are communicated tapping a trope of emotionally charged terms like “dreams”: When we dream, everything looks enchanting and wonderful, but to fulfill your dreams you need to define focused targets. The first step is to define what you want… (1) Define your dreams…. (2) Differentiate between short-term and long-term dreams… (3) Evaluate how much it will cost to achieve your dream…. (4) Try to prioritize your dreams...

7

Intertwining rationality and emotion (Bericat, 2016), financial education programs revert to emotionally charged imaginaries of the future to formulate general principles of proper financial conduct and communicate a model of the desired responsible and rational financial subject. As we show in the next section, financial education also evokes emotions to explain and promote specific rules of conduct in different spheres of personal finance.

Explaining and promoting proper financial conduct through emotions

In offering imaginaries of the future aligned with charged emotions like hope and fear, financial education attempts to motivate individuals to undertake the financial decisions and actions that it defines as appropriate and necessary. Emotions are ever-present in the ways programs define, explain, and promote proper conduct in key everyday financial activities: debt and credit, saving and investment, and insurance.

Debt and credit

Influential state and non-state actors in advanced capitalist countries define their populations’ over-indebtedness as a major economic and social problem (Lazzarato, 2015; Montgomerie, 2020). Furthermore, over-indebtedness is construed not only as a social hazard but also as a significant risk for individuals (Marron, 2012), which should be mitigated through practices of financial education aimed at inducing appropriate financial conduct (OECD, 2016a). In Israel, households’ total indebtedness is low compared to other advanced economies, yet state agencies and non-state organizations warn about its dangers and urge individuals to manage their debt appropriately and with caution. 8

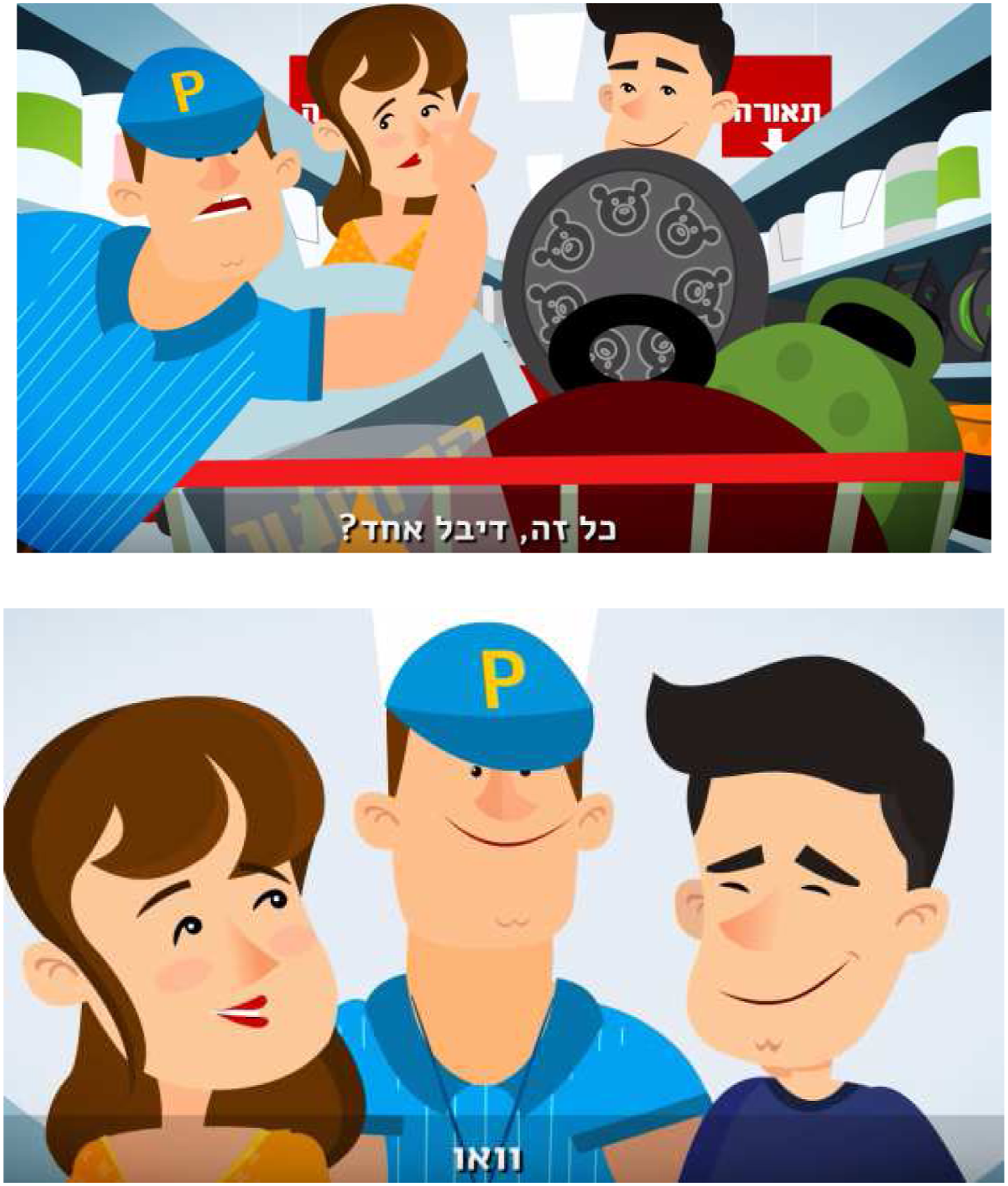

Financial education programs do not condemn consumption or credit per se, nor do they depict debt as intrinsically morally corruptive. Rather, they stress the importance of managing debt responsibly, categorizing situations as worth taking a loan and others for which a loan is unnecessary or too risky. The programs mobilize emotions such as despair, worry, happiness, and satisfaction to stress these messages, connect them to individuals’ lives and experiences, and motivate them to manage debt and credit in a rational and responsible manner. This is illustrated by an animated video produced by Paamonim that presents uncontrolled consumption as the primary cause of families’ over-indebtedness. Titled “Smart Purchase: Need or Want?”, this video mobilizes anger to condemn impulse buying and depicts relief and true happiness as resulting from self-control. Featuring a couple in a store with a shopping cart full of items, a character of a coach says angrily, “Stop! What is this mountain? Why did you enter this shop?… These are not things you need. They are things you just want.” Then he instructs the couple to prepare a list of things they really need. The couple prepares the list and looks at every item in the cart, asking, “Do we need it or not?” Eventually, nothing is left in the cart. The coach asks, “So how do you feel now?” The couple answers happily: “Wow, what a relief!”

9

(see Figure 2). Paamonim, “Smart Purchase: Need or Want?” https://www.youtube.com/watch?v=pufkiEAx3zk

Similarly, a Ministry of Finance animated video titled, “Take Preventive Measures,” contrasts emotional states of despair and relief to convey the message that individuals should be aware of the consequences of their financial actions and manage their debts responsibly. The video presents a middle-class looking man who receives a letter from a bank on his failure to meet a monthly debt repayment. He is in despair and decides to ignore the letter. The narrator says, “You cannot ignore the letter.” The person responds gloomily, “I do not have the money this month. I will pay it as soon as I have the money.” The narrator replies, “Even if you ignore it, the problem will not disappear… If you cannot manage the repayments, you must make some financial arrangement.” Following a meeting with a banker, the person declares with satisfaction and relief, “You were right. They rescheduled my debt and postponed the payment.” 10

These examples illustrate how financial education programs rely simultaneously on positive and negative emotions, contrasting between them and portraying them as resulting from proper or improper financial conduct, respectively (see Tuckett, 2018). Connecting financial practices and their consequences to individuals’ emotional experiences, this strategy is intended to motivate them to behave according to a morality of responsible and rational financial conduct that resonates with the individualization and privatization of risk management.

Saving and investment

The low level of savings among the Israeli population is a major concern for state agencies, an issue common to many advanced economies. People’s reluctance to save has led policymakers in many countries, including Israel, to use a range of tools to encourage savings, including financial education campaigns (Langley, 2007; Pinto, 2013; Ribeiro and Soares, 2017). To promote saving, these campaigns mobilize various arguments, evoking both negative and positive emotional states, especially despair, frustration, and hope. Specifically, financial education programs demand that individuals become keen savers to allow them to weather economic crises, rely less on credit for unexpected expenses, and realize their desires. 11

Neoliberal reforms to the pension system implemented in the mid-1990s connoting the individualization and marketization of risk management, particularly contribution-defined pensions replacing benefit-defined pensions, led to several campaigns aimed at increasing the public’s awareness of pension plan savings’ crucial importance to their future economic security. 12 The campaigns mobilized emotionally charged messages to goad individuals into opening pension savings accounts as early as possible. For example, a video produced by the Adva Center uses the emotion of frustration to convey the complexity of issues underlying pension saving that individuals must face, while hope for a good future is mobilized to encourage the public to start a pension plan at an early age. The main character is a young woman who gleefully declares, “The twenties is a great age to think about pensions!” She goes on to explain that savers who start saving young will enjoy a higher living standard when they retire. 13

The massive public’s involvement in financial markets in Israel is a relatively new phenomenon that developed as a result of the state-led process of liberalization of the political economy. While financial industry efforts deserve credit for the American public’s involvement in financial investment (Aitken, 2007; Ott, 2011), in Israel state agencies have taken the lead, launching several financial educational campaigns with the explicit goals of “reducing anxiety which results from lack of knowledge, and increasing the public’s involvement in capital markets.” 14

To prompt individuals to become investing entrepreneurial financial subjects (Aitken, 2020; O'Malley, 2000), state agencies have conducted TV campaigns, launched educational YouTube videos, published written texts, and provided online guides. Far more than merely providing information, and in addition to morally legitimizing the engagement with financial markets (see Kim, 2017), these initiatives invoke emotions, especially hope founded on optimist imaginaries of attractive financial futures, to emphasize the personal benefits that financial investment offers. A Ministry of Education video targeting high school students explains financial investment as a hope-based action: “Investment is giving up spending money today in the hope that the sum of money will increase in the future. Instead of wasting the money today, we invest it in various assets and hope their value will increase and we make a profit.”

15

Visuals accompanying this explanation include wide smiles, plenty of coins and bills, and the metaphor of watering a growing plant to clearly communicate the notion that investment yields optimism and joy (see Figure 3). Ministry of Education, “Video No. 15: Different Kinds of Investments” https://www.youtube.com/watch?v=7IZXQ9ccr18&list=PL1290554BD87250FE&index=5

The Israeli Securities Authority has also appealed to hope for a bright future, not only for the individual, but also for the society, stressing that investment in capital markets is crucial for the future wellbeing of individuals, firms, and the economy and society as a whole. In an animated video titled, “Buying or Selling?” a woman asks her friend who invests in the Tel Aviv Stock Exchange, “With all due respect to the companies that raise money, why should you care?” The investor replies enthusiastically, “With the help of stocks, large projects can raise money from the public and that is really good for economic growth. And what is good for the economy is good for all investors and is good for me.” 16 The economic interests of individuals, firms, and society thus intertwine in a promising future of economic growth and welfare for all.

Insurance

Deepening financialization involves the increase in the reliance on commercial insurance for facing uncertainty in diverse personal matters (McFall, 2011; O'Malley, 2015). Financial education programs thus stress insurance as an essential financial instrument providing protection from an uncertain and threatening future, warning against holding overly optimistic imaginaries of the future: "

We tend to be optimistic regarding the future, yet unexpected and unfortunate events often take place. One way to deal with such occurrences, and to protect the important things, is to purchase insurance. With insurance, you pay in the present so that if anything happens in the future, the insurance company pays the damage." 17

In contrast to their depictions of other key everyday financial activities that mobilize combinations of positive and negative emotions, financial education programs tend to emphasize the avoidance of undesired futures and negative emotional states when promoting insurance. Portraying threatening scenarios geared at provoking fear and anxiety, they assert that these negative emotions can be avoided or mitigated by the sense of protection that insurance offers. For example, emphasizing the importance of home insurance, the Ministry of Finance website presents a vivid picture of a wide array of catastrophes that can threaten homes: thieves, fire, tsunamis, avalanches, and airplane crashes (see Figure 4).

18

They thus convey the key message that insurance is the proper answer to tragic, or at least unwanted, events, providing peace of mind in the face of the essential unpredictability of the future: All of us want to protect the things dear to us, our health and our property. One way to do this is to purchase insurance, enabling us to cope with catastrophes such as illness and accidents. An appropriate insurance to your needs will enable you to deal with dramatic events of this kind. The insurance will liberate you from the financial burden and give you peace of mind over time.

19

Ministry of Finance, “My Treasure: Home Insurance: An Answer for Every Question,” https://haotzarsheli.mof.gov.il/Subject/Pages/Apartment-Insurance.aspx

The programs stress that individuals cannot control the unknown future but they can prepare themselves for it. By purchasing insurance, they “transfer the risk to the insurance company.” 20 Thus, buying insurance liberates them from the threat of uncertainty and its heavy emotional toll. In this way, financial education communicates and reaffirms the idea that private financial instruments, in this case insurance, offer the ultimate solution to the problem of essential uncertainty of the future.

Conclusions

As a technology of governance supporting and promoting the financialization of everyday life, financial education is part and parcel of the organized efforts to diffuse and institutionalize a culture of financialization, which involves “a habit of the imagination that reorients individuals, institutions and society at large toward the conscription of the future itself…” (Haiven, 2020, p. 349). Thus, financial education operates as a political-cultural project in which influential state and non-state actors mobilize a wide array of discursive resources and instruments with the purpose of governing individuals’ imaginaries of the future, understandings and conduct in the field of personal finance. This is aimed at constituting them as proper financial subjects disposed and able to engage with practices of everyday finance as a primal means to assure their economic security and welfare. The meanings, narratives, and imaginaries formulated and communicated by financial education therefore represent a significant component in the cultural political economy of the constitution of financial subjectivities, as they reflect and reaffirm the fundamental cultural and institutional principles of financialization (see Aitken, 2020).

In this article, we have argued that financial education mobilizes emotions as a central tool to formulate and communicate to the general public a model of the desired financial subject: an active, responsible and calculative actor able to effectively navigate the world of everyday finance. Our analysis of the Israeli case suggests that although presented as essentially informative, aiming at enhancing individuals’ knowledge, cognitive skills, and capacities, financial education programs prominently mobilize emotions to define and explain proper and improper financial habits and conduct. Research on financial education in other countries (Kim, 2017; Pettersson and Wettergren, 2021) indicates that invoking emotions is a common tool used in programs aimed at improving the level of the population financial literacy and promoting positive attitudes toward practices of personal finance. Our analysis demonstrates how emotions are mobilized mainly to govern individuals’ imaginaries of possible financial futures and their assumed causes. Offering imaginaries of the future loaded with negative and positive emotions and linking different financial behaviors and their desired or undesired results to familiar emotional experiences, financial education programs seek to instigate individuals to understand and conduct personal financial matters in accordance with the principles and dispositions that constitute the desired financially literate subject. Hence, a significant specific characteristic of financial education is its intertwining of emotions and rational calculability.

Financial education programs aim to inspire individuals with hope and motivate them to imagine and forge bright economic futures in which their dreams come true. However, they also warn about potential threats foreshadowed by uncertain futures. They mobilize positive emotions, such as hope and optimism, to substantiate and reaffirm the claim that individuals can realize their desires and dreams by adopting proper financial conduct. Negative emotions, such as worry and fear are mobilized to urge individuals to adopt responsible financial conduct that can protect them from future threats and insecurity. In this way, proper financial conduct is presented as necessary not only to assure individuals’ financial security, but also as necessary to assure their emotional wellbeing.

Reflecting dominant definitions of what constitutes the proper financial subject under a regime of neoliberal financialization of everyday life, financial education formulates and communicates notions of calculability and rational planning, presenting them as the most important foundation of proper everyday financial conduct. Notably, they accomplish this task by invoking emotions and emotionally charged situations. The engagement with financial instruments based on rational calculability is presented as the means to prevent, or at least to reduce, anxiety elicited by an uncertain future, as well as to realize dreams and hopes, and attain self-satisfaction. Rather than operating according to the dominant common sense view of emotions and rational calculability as separate and hostile worlds (Zelizer, 2005), programs of financial education actually interwine the two. Thus, proper financial conduct based on responsibility and rationality is presented as the way to achieve desired emotional states and avoid unwanted ones. This reaffirms the basic logic underpinning the culture of financialization, that is, the notion that the future and its risks can be managed through the use of financial products and services.

Our analysis contributes to the study of the financialization of everyday life revealing the key role of the mobilization of emotions and emotionally charged imaginaries in the operation of technologies of governance directly implicated in the constitution of desired financial subjects. Institutional actors mobilize emotions to connect individuals’ imaginaries, subjectivities and life experiences to the individualization and marketization of risk management that underlie the financialization of everyday life. In this way, they posit the proper understanding and engagement with financial practices and instruments as essential components of desired personhood, naturalizing the culture of financialization and the behavioral and dispositional requirements and demands that everyday finance poses to the general public. The ways by which the naturalization of financialization is promoted are particularly significant for the study of the cultural political economy of consumption within the current setting of expanding and deepening financialization of everyday life. In such a setting, the processes and technologies through which the proper financial consumer is constituted are a prominent factor in the formation of individuals’ understandings, actions, and experiences as consumers in general.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Research Authority of the Open University of Israel and by the Israel Science Foundation (Grant no. 597/17).