Abstract

Under corporate crises, the formation of credit relationships based on group-level credit reciprocity strategies is a multi-factorial phenomenon. From the perspective of a fully mixed corporate group, the research explores the inadequacy of traditional snowdrift game models in adapting to the structural elements of credit relationship formation. Firstly, it improves the model by introducing inter-temporal costs, benefits, and crisis randomness of credit reciprocity as decision parameters. Secondly, it introduces inter-temporal credit reciprocity as a condition to allow the snowdrift game model to express the evolution between corporate groups. Finally, based on credit reciprocity, the mechanism of credit relationship formation is verified through numerical simulations. The results show that under the crisis probability, the formation of credit relationships exhibits a “threshold trigger,” and the inter-firm assistance and crisis probability play an important role in establishing credit relationships between enterprises.

Introduction

A corporate crisis assistance is essential to activate micro market players, prevent systemic risks, and maintain financial and social stability. 1 In China, crisis relief mainly relies on non-performing asset management institutions, forming a market pattern dominated by “five major (China Huarong, China Orient, China Great Wall, China Cinda, and China Galaxy) + local + banking system + foreign investment + N (non-licensed institutions).” However, the coverage of market assistance is limited, especially because small and micro enterprises often rely on credit support from cooperative enterprises. Crisis relief for small and micro enterprises is not only the basic institutional arrangement for maintaining social stability but also the key to enhancing the resilience and anti-risk ability of enterprises. 1 At present, the academic research on corporate crisis assistance mainly focuses on corporate crisis management strategies, bank assistance, and other external assistance methods.2,3 For example, Martin Belmonte et al. proposed an assistance method that supported local commercial economy through direct cash transfers from the government. 4 Sheth analyzed the enterprise crisis assistance from the perspective of bank assistance and proposed the concept of interdependence between enterprises and society. 5 However, the existing research has not paid enough attention to the value of credit relationship and its risk absorption capacity within the corporate relationship network. In fact, enterprise relationship management is not only an important business strategy but also a key way to enhance enterprise resilience.

The research focuses on the mutual credit behavior between enterprises and discusses whether it is due to the lack of external credit channels and the credit constraint environment during the corporate crisis. During the crisis, although credit market innovation and credit creation can promote investment and consumption, insufficient credit evaluation capacity and high evaluation cost lead to insufficient credit supply for crisis relief. Banks tend to choose large projects and enterprises, while small and micro enterprises and crisis enterprises face liquidity difficulties. Despite legislation prohibiting inter-bank lending in the 1970s, borrowing through fictitious contracts remains widespread. In 2020 and 2021, the number of civil disputes in private lending ranks first in civil cases, which reflects the real demand for private credit. Judicial precedent actually supports the validity of inter-bank lending contracts, which reflects the social system’s tolerance for private credit. 6 According to the “2017-2019 China Private Enterprise Development Report,” internal accumulation is the largest source of funds for private enterprises, while formal credit only accounts for the second, which indicates that internal accumulation implicitly involves the internal credit activities of inter-bank lending. 7

Credit reciprocity mainly occurs in the “relationship alliance” of enterprise groups, and enterprises realize cooperation through “complementary advantages.” In enterprise groups, the credit reciprocity network of crisis enterprises is embedded in the enterprise basic relationship network, which makes the enterprise rescue behavior has systematic economic value.8,9 Enterprises form alliances based on common interests, achieve economies of scale through cooperation, reduce transaction costs, and quickly respond to resource imbalance caused by technological development. Such cooperation is not only based on the principle of trust and reciprocity between enterprises but also influenced by internal norms, supervision mechanisms, and external environment. 10 The intra-group credit relationship is a form of credit cooperation, which depends on intra-group cooperation and consensus, and is also restricted by external conditions such as social trust environment, regulatory system, and social credit system. By recording the credit information of market participants, evaluating and publishing their credit ratings, the social credit system constrains their behavior and increases the cost of credit failure. Therefore, it is of great practical significance and research value to analyze the formation of credit relationship between enterprises in crisis situation.

While existing research has explored the formation mechanisms of corporate credit relationships, there remains a research gap regarding the evolutionary process and dynamic mechanisms of inter-firm group credit mutual assistance behavior under crisis conditions. Therefore, this study improves the snowball game model by introducing intertemporal credit reciprocity and crisis randomness, proposing a novel evolutionary game model based on group credit reciprocity. The aim is to systematically reveal how enterprises form stable credit relationship networks through internal credit mutual assistance behavior under crisis conditions. The research objectives include the following: Introducing parameters such as crisis probability, mutual assistance costs, and benefits to improve the standard snowball game model; depicting the dynamic behavioral evolution paths of enterprise groups under asymmetric information and credit constraints; analyzing the influence of assistance intensity, enterprise scale, and liquidity costs on the steady state of credit relationships through numerical simulation analysis.

The main innovations of this research are as follows: Introducing intertemporal credit mutual assistance mechanisms into corporate crisis game analysis to reveal the temporal evolution characteristics of credit behavior for the first time; improving the snowdrift game model by incorporating real-world corporate crisis elements such as credit withdrawal and assistance success probability to enhance the model’s explanatory power; proposing a threshold-triggered mechanism for forming corporate group credit relationships, while revealing its nonlinear relationship with corporate scale and risk preference.

Literature review

The formation of credit relationships within groups is essentially a form of credit cooperation. However, the external conditions for these relationships are more stringent. Group cooperative games may result in non-cooperative outcomes for various complex reasons. These reasons mainly stem from the dynamic interactions between groups and within groups, the game structure, and behavioral psychological factors. Particularly in large-scale group games, the evolution of cooperation is complex. It is influenced by factors such as group size, game structure, and mechanisms supporting cooperative behavior. 11 In addition, factors such as group salience, shared destiny, group formation methods, communication, and procedural fairness can also affect cooperation. 12

The “conflict-cohesion hypothesis” suggests that introducing inter-group competition in defection games can lead to cooperation within groups. This highlights the impact of strategic incentives beyond material rewards. External threats or competition can prompt group cooperation to avoid group extinction.13,14 In particular, group size significantly influences the cooperation. Smaller groups often exhibit greater cooperation because they are easier to manage socially and can maintain closer relationships between members. 15 Research by Wang et al. 16 found that group strategies with unbiased preferences can effectively enhance cooperation levels, even in significant group divisions. Through appropriate strategy selection and adjustment, cooperation behavior in public goods games can be promoted. Therefore, credit cooperation and relationship formation within enterprise groups can be analyzed through group cooperation mechanisms. Factors such as group size, internal structure, and enterprise behavioral decision-making also lead to different outcomes in credit formation.

Credit reciprocity is not a prerequisite for the accumulation of basic relationships within groups. On the contrary, it is a form of credit behavior derived from basic relationships under indirect reciprocity norms. When there is less interaction among individuals within the group, indirect reciprocity has a particularly significant effect on promoting cooperative behavior. Reputation becomes an effective external signal of trust under this mechanism. It stimulates the willingness of other individuals to provide assistance. From a broader perspective, large-scale social cooperation can be understood as resulting from network effects originating from indirect reciprocity. Even if there is no direct reciprocity between individual A and individual B, A’s assistance to B may ultimately be returned to A through indirect chains such as C and D. However, this process is limited by the size of the interaction group.17,18 It is worth noting that different social norms have profound effects on the cooperation within groups. For example, the Bushido norm emphasizes intra-group cooperation and views cooperation with external groups as betrayal. In contrast, the merchant norm attaches greater importance to cooperation with external groups. When these two drastically different social norms coexist within the same group, it may lead to a complete collapse of cooperation. 19 Therefore, the formation of credit relationships requires interaction norms under indirect reciprocity.

Indirect reciprocity helps to form and maintain cooperative relationships in large-scale groups, which is applicable to the mechanism research of credit relationship formation. The core of the indirect reciprocity mechanism is the reputation system and social evaluation norms, which together promote cooperation within the group. This mechanism not only involves direct interaction between individuals but also includes the circulation and transmission of reputation information throughout the entire social network. Credit reciprocity behavior and indirect reciprocity norms are important forces driving the formation of credit relationships, but their ways and effects are influenced by various factors such as social norms, group size, and reputation systems.

The formation of inter-enterprise relationships is driven by knowledge sharing and innovation under uncertainty, as well as collaboration advantages. The formation of inter-enterprise credit relationships stems from both external institutional environment defects and basic relationships between enterprises. From the perspective of the external institutional environment, a low financial marketization and imperfect legal systems increase enterprises’ motivation to join guarantee relationships, ultimately leading to the interconnected risks of guarantee networks.

20

From the perspective of basic relationships, credit relationships originate from business relationships arising from industry associations, ownership relationships under the same group control, and personal relationships among executives and shareholders.

21

However, due to phenomena such as “lemon market” effects, moral risks, and market failures, guarantee relationships are essentially ineffective.

22

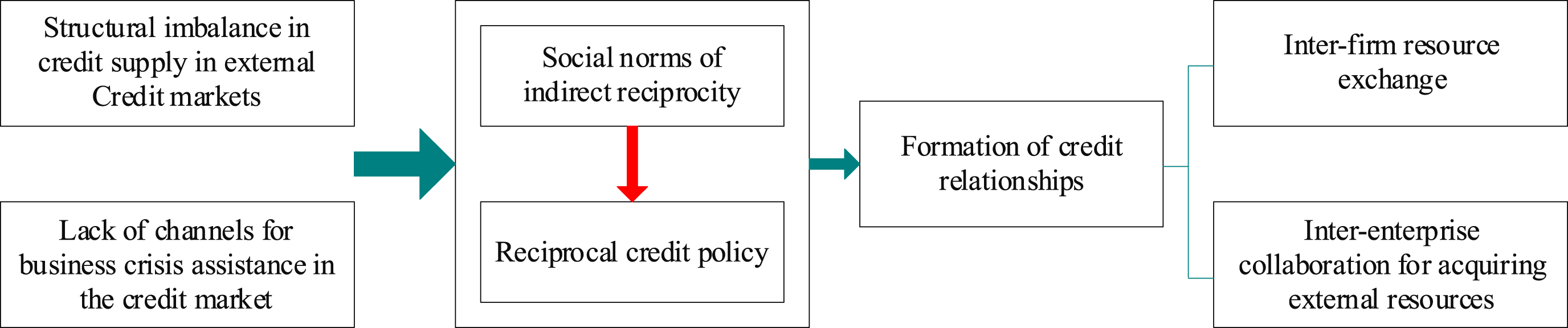

Both the “lemon market” effect and moral risk stem from a tendency towards betrayal in bank enterprise relationships, and guarantee relationships with unstable trust foundations are more prone to risk under crises. The specific path of credit relationship formation is illustrated in Figure 1. Formation of credit relationships.

In the context of enterprises facing crises, the dynamic construction of credit reciprocity and credit relationships brings substantial logical improvements to the snowdrift game model as cooperative conditions. Based on the principle of indirect reciprocity, the model highlights the characteristics of intertemporal credit exchange, combining key elements such as time dimension, crisis randomness, and corporate strategic decision-making, thereby significantly improving the adaptability and practicality of the model. When enterprises encounter crises, the mechanism of credit reciprocity becomes an important cooperative strategy, which is not only reflected in immediate transactional behaviors but also permeates long-term business relationships. Guided by indirect reciprocity norms, enterprises are more inclined to choose cooperation over betrayal when facing risks because long-term reputation accumulation and expected credit reciprocity promise greater benefits. Therefore, combining the above can be seen that the current research on the value of the credit relationship within the corporate relationship and its implied risk-absorbing capacity is relatively shallow, and ignores the positive value of corporate relationship management in corporate crisis assistance. The simulation of the related model on the corporate group cooperation game is one-sided. It is urgent to analyze and explore the group cooperation game in a comprehensive way.

In summary, although existing research has revealed some mechanisms for the formation of credit relationships between enterprises, there is still a lack of in-depth theoretical analysis and dynamic simulation on how to improve the resilience of enterprise groups through credit reciprocity between enterprises in crisis situations. To fill this research gap, this study will adopt a perspective of internal credit reciprocity within corporate groups. Based on insights from the literature, it will construct a dynamic model based on evolutionary game theory to systematically analyze the formation process and stability of credit relationships between enterprises, thereby depicting the evolutionary path of credit mutual assistance behavior among corporate groups during crises.

Enterprise crisis and the formation of credit relationships—Credit reciprocity game model

To thoroughly examine the dynamic evolution of credit relationships among enterprises in crisis situations, this section draws on evolutionary game theory to improve the traditional snowball game model by incorporating key elements such as crisis probability, assistance costs, and assistance success rates, thereby constructing a credit mutual assistance behavior model among enterprise groups. First, the research briefly reviews the snowdrift game model and its limitations, then proposes an improved model and set parameters and payoff functions, and finally derives its evolutionary steady state, laying the foundation for subsequent simulation analysis.

Multiplayer evolutionary snowdrift game model and limitations

The theoretical basis of the snowdrift game model

In this study, the rational agent model was chosen to analyze group credit reciprocity in corporate crisis mainly because the analysis was conducted at the group level. Whereas Kahneman’s outlook theory is more applicable at the level of the leader in the group. Since this study starts from the perspective of a fully hybrid corporate group, the evolution between corporate groups is modeled based on several parameters. The Snowdrift Game model is able to satisfy different stakeholder laws in corporate crisis at the group level and is more applicable to the proposed research technique. After comprehensive consideration, this study does not perform a relevant analysis based on Kahnemann’s Prospect Theory. The Snowdrift Game embodies the behavioral processes of economic agents in cooperation, collaboration, or conflicting interests.

23

The focus of its standard model lies in how to reflect the cost-sharing and benefit-sharing among collaborators. Global cooperation is achieved through the cost-sharing effect of reciprocal cooperation, reducing the difficulty of individual execution and thereby facilitating cooperation.

24

Furthermore, benefits and costs are realized in the current cooperation. That is, while costs are shared among collaborators, the benefits generated by cooperation can be equally realized among the group. The standard payment function of the multiplayer snowdrift game corresponding to the above rules is as follows:

Analysis of the limitations of the standard snowdrift game model

According to the calculations based on equations (1) and (2), in the standard Snowdrift Game, the optimal strategy is for the group not to cooperate. This is because the free riders inhibit the emergence of cooperation, which indicates an endogenous deficiency in the model. Additionally, when all individuals do not cooperate (n = 0), the payoff for all individuals is zero (

In addition, in a real scenario, situations where

Construction of credit reciprocity game model for enterprise groups during crises

Background and assumptions of model construction

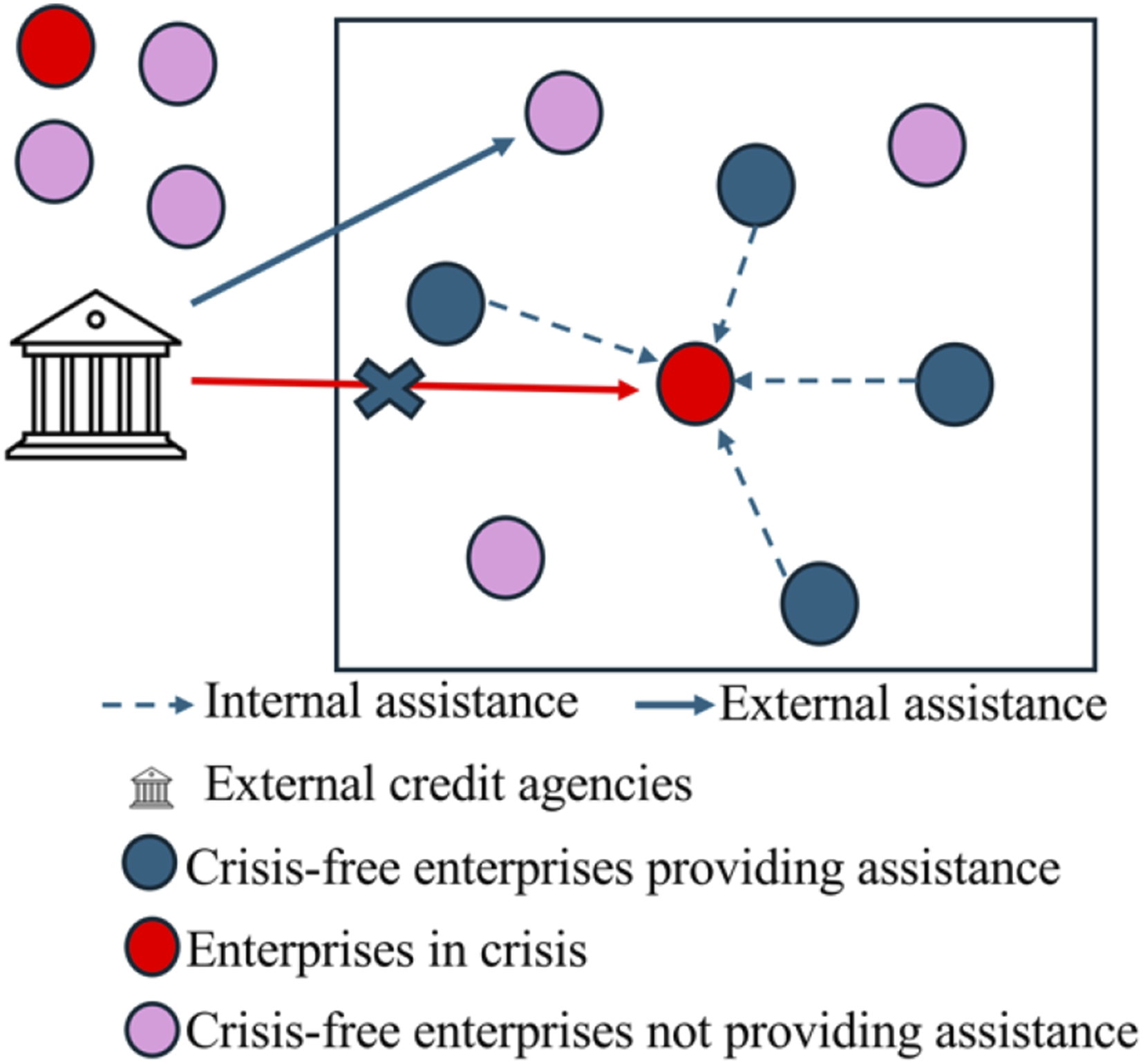

In response to the complexity of practical scenarios and the limitations of the basic standard model, this paper proposes enhancements to the model constraints and suggests appropriate scenarios, as illustrated in Figure 2. The diagram divides the space into the external and internal environments of the group of enterprises, where inside the box belongs to the internal environment of the firm and outside the box is the external environment. It is assumed that there are underlying conditions for forming credit relationships within the corporate group. Credit reciprocity during crises serves as the criterion for identifying credit relationships. Through the gradual hierarchical structure of relationships within and outside the enterprise in Figure 2, hierarchical differentiation can be achieved on relationships, and the evolution from the basic relationships of enterprise groups to credit relationships can be deeply transitioned. Mutual credit cooperation among enterprises amid crisis.

Initially, the players in the game include individual enterprises within the enterprise cluster, without considering the participation of external formal credit institutions such as banks. This is because there is no pre-existing trust relationship between external credit institutions like banks and enterprises. However, during enterprise crises, there often arises credit withdrawal from banks. Based on the three principles of credit institution operation, profitability, liquidity, and security, the credit supply decision-making mechanism of banks is established primarily on the basis of security. Therefore, the paper excludes the assistance provided by banks during corporate crises.

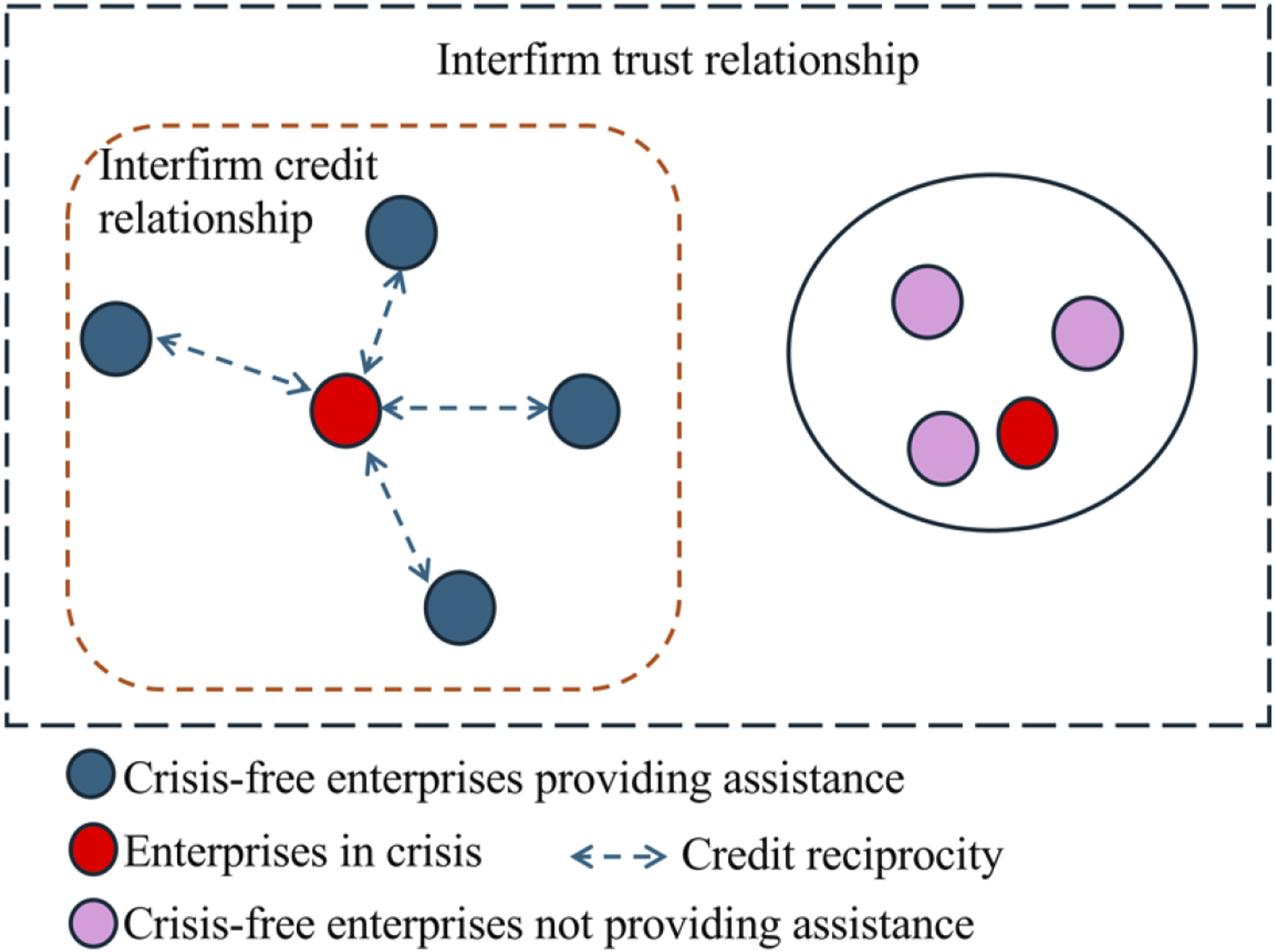

Internal relationship stratification of enterprise groups and credit reciprocity norms

In Figure 3, individual enterprises can be categorized into three types over a time horizon based on whether a crisis occurs and whether they adhere to the rules of credit reciprocity: crisis focal enterprises, non-crisis but rescued enterprises, and non-crisis but refused-to-rescue enterprises. Layered through the relationship dimensions shown in Figure 3, the clusters of enterprises transition from a basic trust relationship to a credit relationship. When the group adopts norms of credit reciprocity to regulate relational behavior, credit relationships arise from reciprocal credit actions. An enterprise cluster consists of N stable enterprises, where each enterprise chooses to provide assistance to others during crises, as depicted in Figure 3 with N = 9 and n = 5, such assistance forms soft contracts and norms between two or more enterprises, termed credit reciprocity, thereby establishing credit relationships within the enterprise cluster. Enterprise group relationship stratification.

Setting of cooperation benefits and costs and construction of the payoff matrix

Next, the analysis focuses on the cooperation benefits and costs among different individuals within the enterprise cluster. When the enterprise cluster adopts the aforementioned norms of credit reciprocity, several scenarios emerge. Enterprises experiencing crises for the first time receive credit support. This helps them overcome difficulties and avoid bankruptcy losses. Meanwhile, non-crisis but rescued enterprises may gain potential credit support opportunities during future enterprise crises.

Refused-to-rescue enterprises, having been rescued after the first crisis occurrence (free-riding), are considered potential subjects for forming credit relationships according to the “attention rule.” However, if they fail to meet the reciprocal expectations of other enterprises, they will be refused assistance in subsequent crises.

Crisis focal enterprises, having previously provided assistance to other enterprises or experiencing their first crisis, receive unconditional assistance. This explains the development of relationship information under indirect reciprocity norms. The symbol settings corresponding to the implementation rules of inter-temporal benefits and costs as follows. (1) Setting the probability of enterprise crises and liquidity management costs: The objective probability of enterprise crises is (2) Setting the enterprise assistance level and the probability of successful assistance: Assuming that homogeneous assets among enterprises, with a total asset amount of

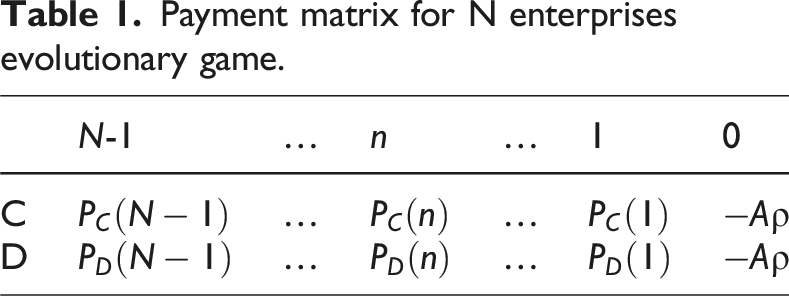

The payment matrix is as follows.

Payment matrix for N enterprises evolutionary game.

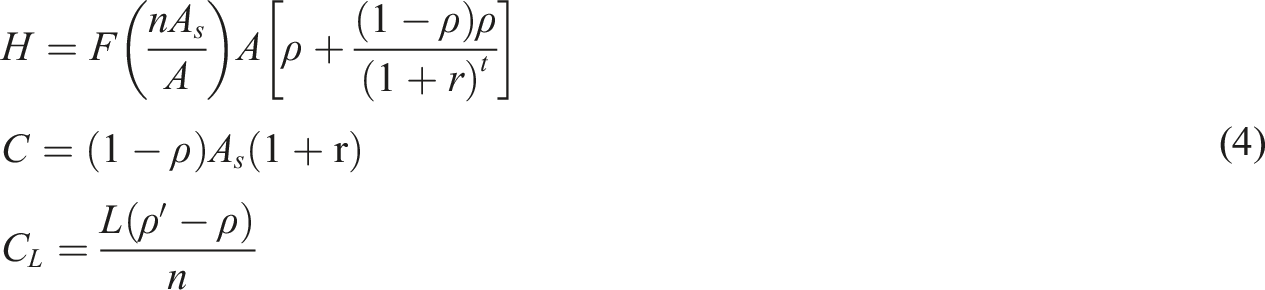

Based on the payment matrix in Table 1 and the parameters of the game model, the inter-temporal payoff function for the enterprise group’s credit reciprocity game can be formulated as follows:

For both parties involved in the credit relationship, the benefit equals the inter-temporal reciprocal benefit of a long-term relationship, while the benefit for “free riders” is a one-time gain. In the function

Steady-state solution of credit relationships based on credit reciprocity game model

The concept and significance of evolutionary stable solutions

Multiplayer evolutionary games can be used to characterize the credit reciprocity behavior among enterprises, leading to the evolution process of credit relationships in enterprise groups. The evolutionary stable solution represents the stable state of relationship stratification. The driving force behind the credit relationships depends on the belief in reciprocity between enterprises, which is strengthened through the transmission and manifestation of reciprocal behavior. Reciprocity beliefs are usually based on interpersonal relationships and strategic business relationships, and different foundational relationships lead to different attributes and micro-structures of credit relationships. Based on theories of bounded rationality, cooperation among agents is established based on the dynamic learning of the intensity of credit reciprocity norms within the group and the interaction process.

Evolutionary dynamics analysis of credit reciprocity behavior

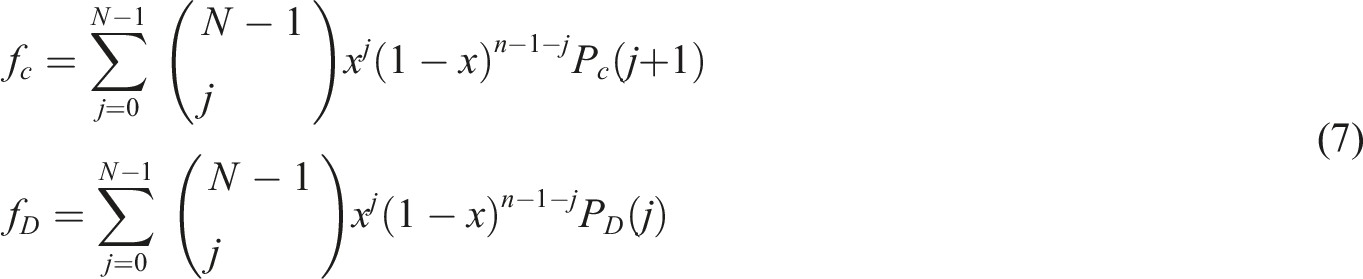

Therefore, it is assumed that credit reciprocity behavior is achieved under well-mixed population, and the evolutionary process of credit reciprocity behavior in enterprise groups based on the snowdrift game theory is a selection process of rescue behavior. This paper adopts the principles of evolutionary dynamics for expression. The number of enterprises engaging in credit reciprocity at time t is represented by x, that is,

Solution and analysis of the steady-state equilibrium equation of credit relationships

Individuals adopting credit reciprocity strategies provide benefits to all members of the group at a certain cost. The profits of a single credit reciprocator and a single refuser of reciprocity are denoted by Equilibrium point stability analysis.

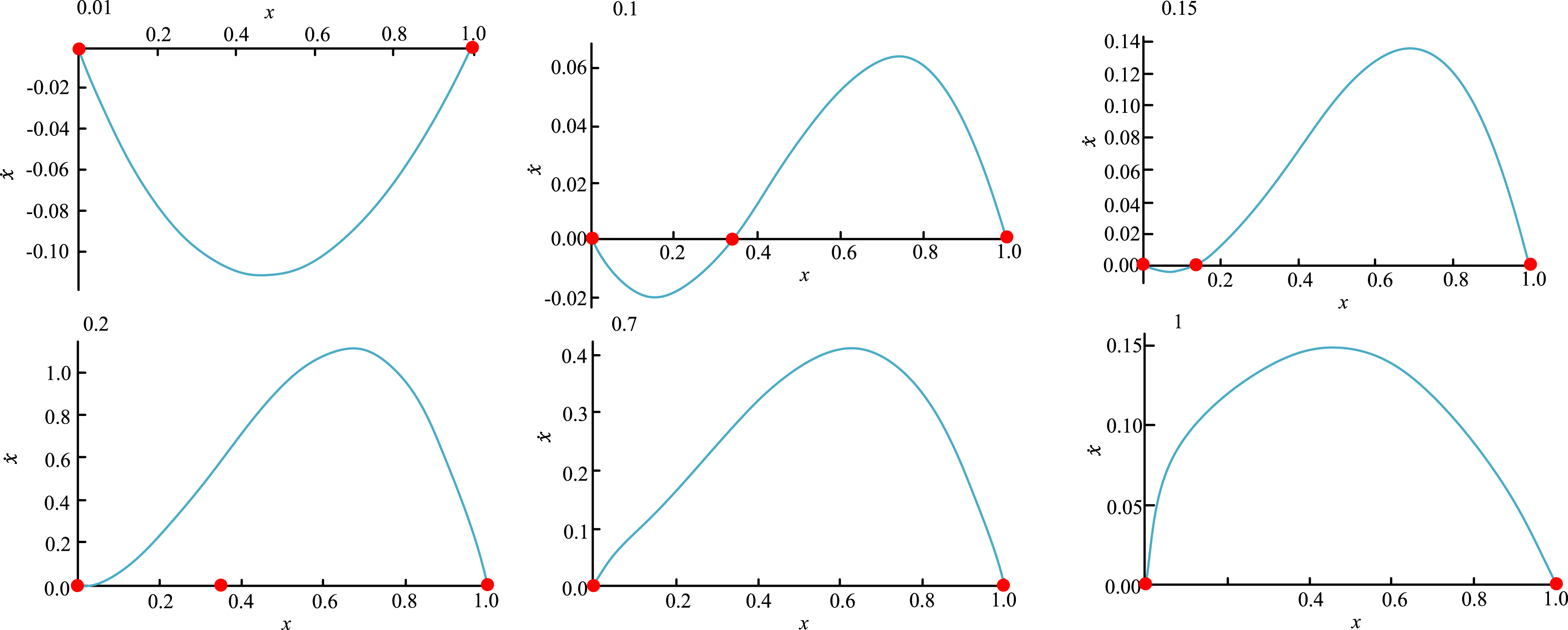

In Figure 4, the stability of the equilibrium point for different probabilities of crises leads to significantly different results. The stability of the equilibrium point can be further inferred by examining and calculating the curve shape and the equilibrium point location on the graph for different crisis probabilities. If the curve crosses the x-axis downwards at the equilibrium point, it means that the derivative at that point is negative, indicating a stable equilibrium point. If the curve crosses the x-axis upwards at the equilibrium point, it means that the derivative at that point is positive, indicating an unstable equilibrium point. It can also be observed from the graph that stable equilibrium points exist with nonzero values, particularly when

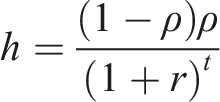

To simplify the solution and reduce the complexity of the distribution assumption, this paper assumes that the probability distribution function

The equilibrium equation for the steady state of credit relationships in the credit reciprocity game model under crisis conditions is as follows:

Simulation analysis of credit relationship evolution in steady state

According to the steady-state equation (7) and parameter equation (8), assuming that the parameters of the probability distribution function are

After calculating the parameter equation (8), equation (10) is obtained:

Global parameter settings: The risk-free interest rate is

Based on the previous model construction, the study establishes a theoretical framework that can describe the evolution of credit—reciprocity behaviors among enterprises in crisis situations. However, although the derivation of the theoretical model can provide some basic conclusions, its dynamic behavior and stable-state characteristics may exhibit complex properties under different parameter conditions. To further investigate the behavior of the model and verify its effectiveness, the study will further analyze the model in this section through numerical simulation methods. The simulation results are as follows.

Impact of rescue level on the stability of credit relationships

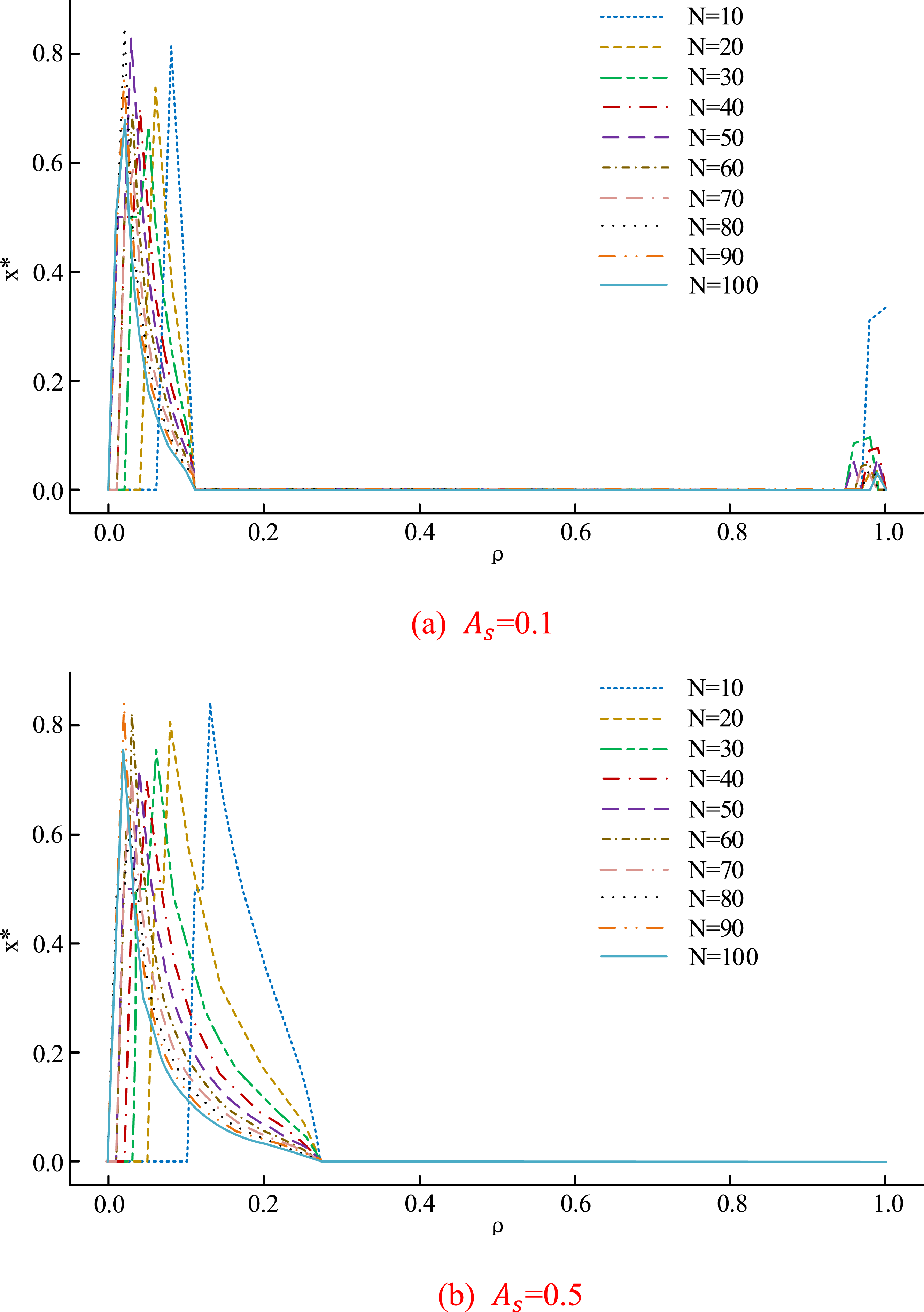

Firstly, the formation conditions of credit relationships and the pattern of relationship hierarchy under different rescue levels were analyzed. The rescue level, as an important constituent factor in the formation of social capital under the theory of resource exchange, may have potential influences on the credit relationship. Therefore, this paper takes Steady-state results of credit relationships (

In Figure 5, the simulation is based on an assistance success probability function set to

From a holistic perspective, it is found that the relationships within the enterprise group cannot fully form credit relationships (

Regarding the impact of the assistance, the parameter

From the above simulation results, it can be concluded that trust within enterprise groups cannot fully form credit relationships, and the formation of credit relationships exhibits a threshold-trigger characteristic. The assistance under the credit reciprocity strategy among enterprises shifts the probability interval of credit reciprocity in the crisis scenario to the right, thereby increasing the proportion of more prevalent credit relationships formed by enterprise groups of different sizes.

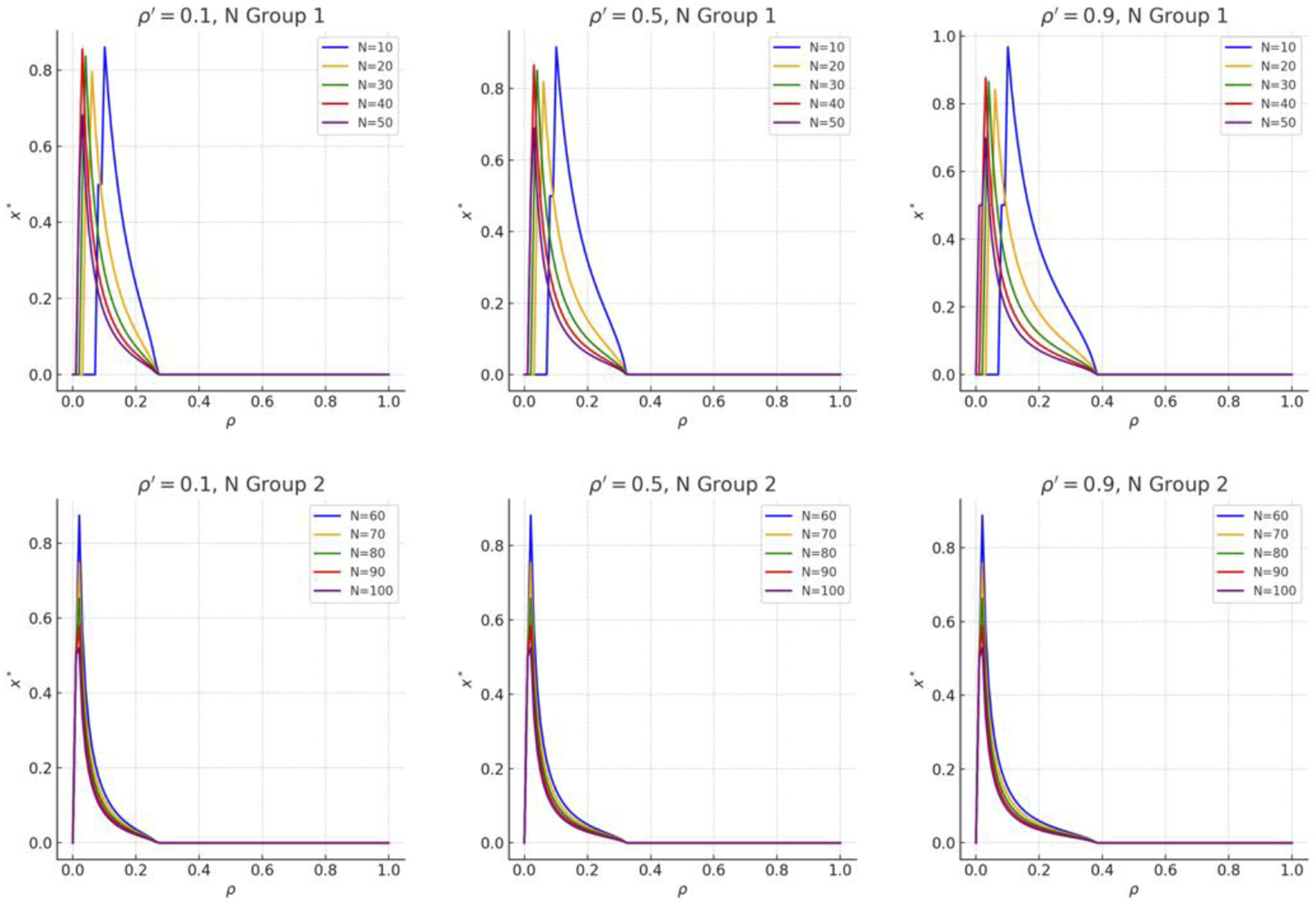

Impact of enterprise group size on the steady state of credit relationships

From Figure 5, it is evident that the size of the enterprise group significantly influences the steady-state results of credit reciprocity games. The group size can modify the contribution of individual enterprise behavior to the overall benefits of the group. Individual decisions can propagate and influence other individuals within the group, further demonstrating the impact of enterprise size N on the stability of credit relationships, denoted by

From Figure 6, with the change in the probability of enterprise crises, the size of the enterprise group N has a significant nonlinear impact on the steady-state of credit relationships. Overall, the larger the enterprise scale, the more inclined the enterprises are to adopt credit reciprocity strategies under low crisis probabilities. This is because in large-scale enterprise groups, the steady-state extremum of credit relationships is inversely proportional to the size of the enterprise group and is achieved at the same level of enterprise crisis. In contrast, in small-scale enterprise groups, the steady-state extremum of credit relationships exhibits a U-shaped relationship with the size of the enterprise group and corresponds to different crisis probabilities Steady-state results of credit relationships (N,

The parameter of liquidity management costs (

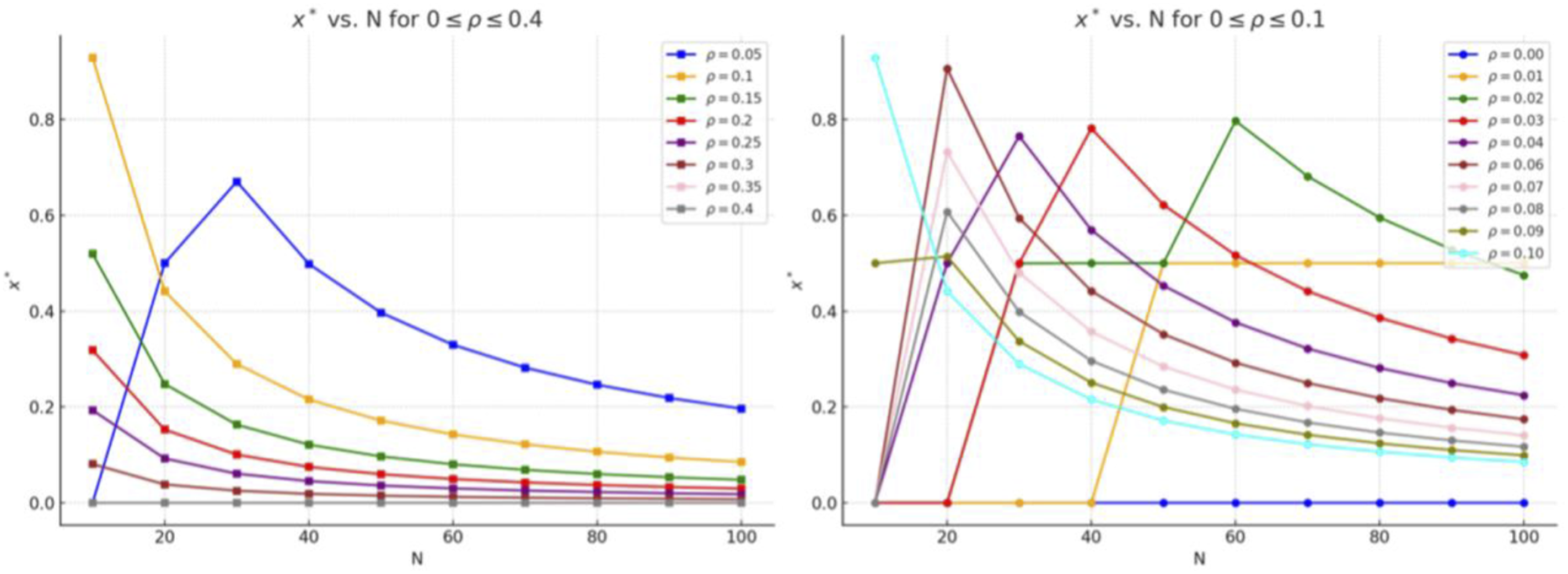

To better illustrate the nonlinear phenomenon of credit relationship formation among enterprises of different sizes under different risks, cross-sectional analysis with Influence of enterprise group size on steady-state solutions (

Conclusion: When the probability of enterprise crises is greater than zero, credit relationships initially form locally within large-scale enterprise groups. However, subsequent frequent credit reciprocity behaviors among enterprises within small-scale enterprise groups strengthen trust relationships, leading to a higher proportion of credit relationships. The enterprise group size influences evolutionary stability through its impact on the assistance success probability. In large-scale enterprise groups, where direct interactions between enterprises become sparse, the formation of credit relationships requires stronger additional mechanisms.

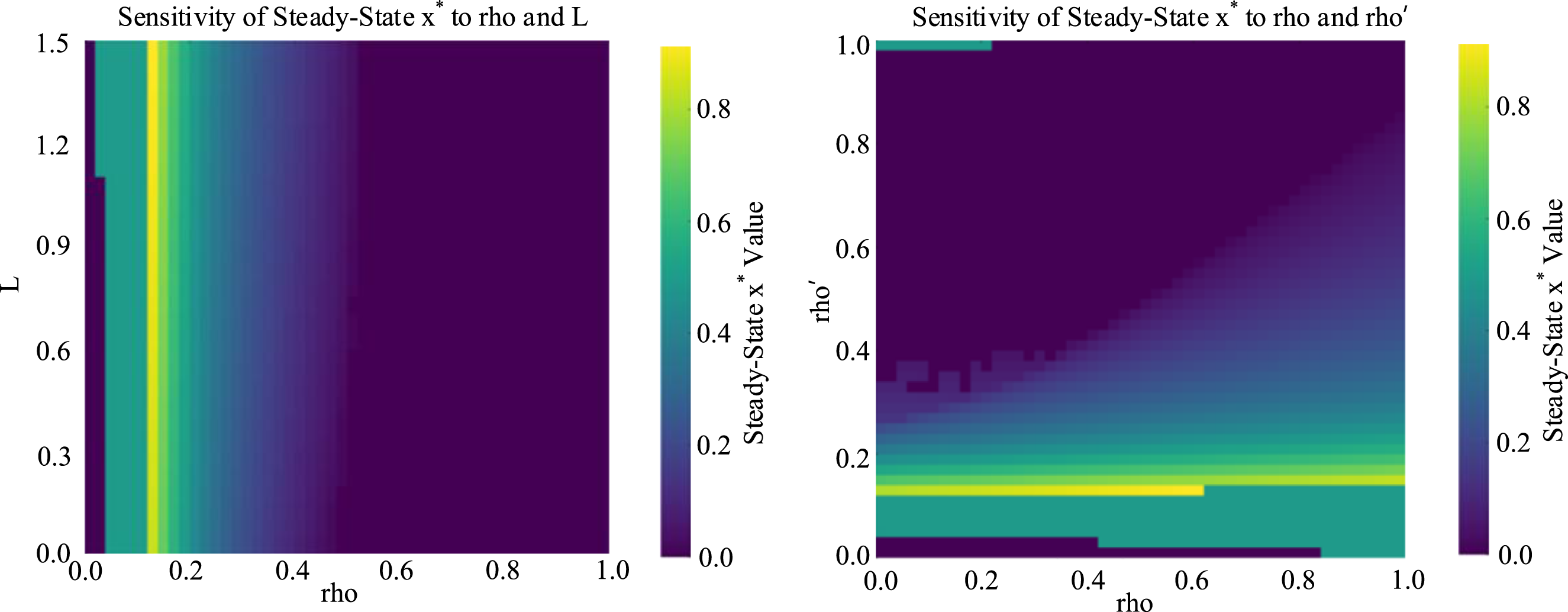

Impact of liquidity management costs on the steady state of credit relationships

In Figure 8, darker areas represent lower steady-state cooperation, while brighter areas represent higher steady-state cooperation. The combined effects of Sensitivity analysis of liquidity management costs on enterprise credit relationships.

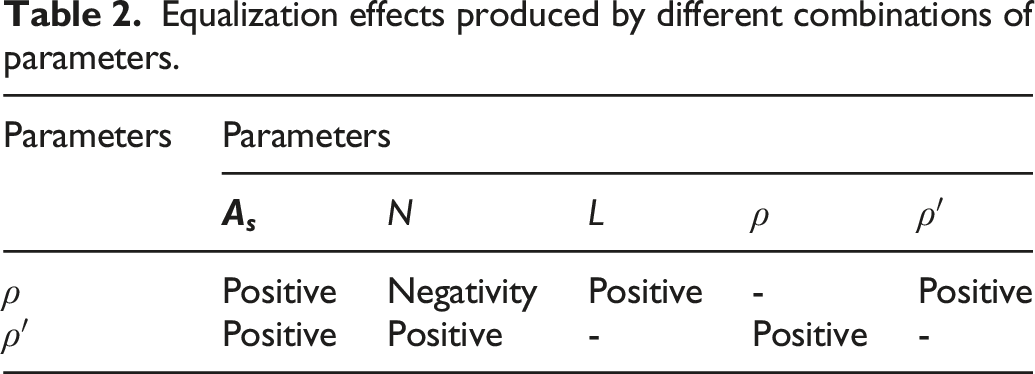

Equalization effects produced by different combinations of parameters.

From Table 2, the combination of the bailout level parameter

An example verification of corporate credit relationship homeostasis based on credit reciprocity game modeling

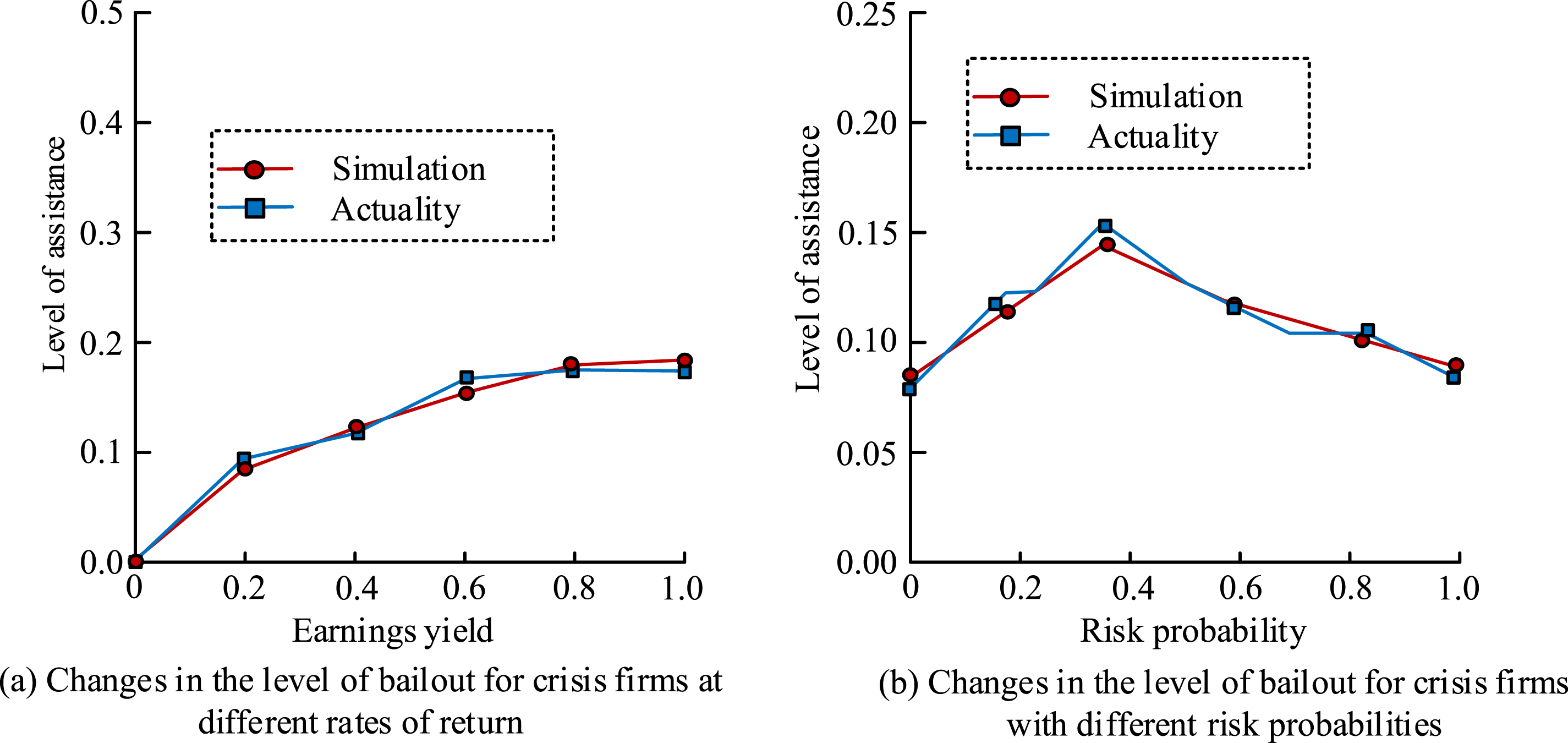

To further illustrate the effectiveness of the credit reciprocity game model proposed by the study in corporate credit relationships, the study conducted a simulation analysis on corporate crisis and credit mutual assistance, taking an SME as an example. To enhance the realism of the simulation, external objective factors such as local policy changes and industry prosperity were introduced as disturbance variables during the simulation process. Under policy support, the weight of historical mutual assistance returns increases, reflecting the strengthened corporate reputation incentives advocated by the government. In the industry downturn, the probability of crisis and liquidity costs increases accordingly. The actual bailout obtained by the crisis enterprise under different rates of return and risk probabilities are shown in Figure 9. Comparison of simulated and actual results on the level of bailout received by crisis enterprises. (a) Changes in the level of bailout for crisis firms at different rates of return. (b) Changes in the level of bailout for crisis firms with different risk probabilities.

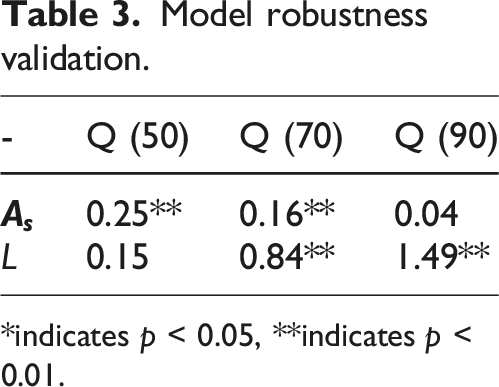

Model robustness validation.

*indicates p < 0.05, **indicates p < 0.01.

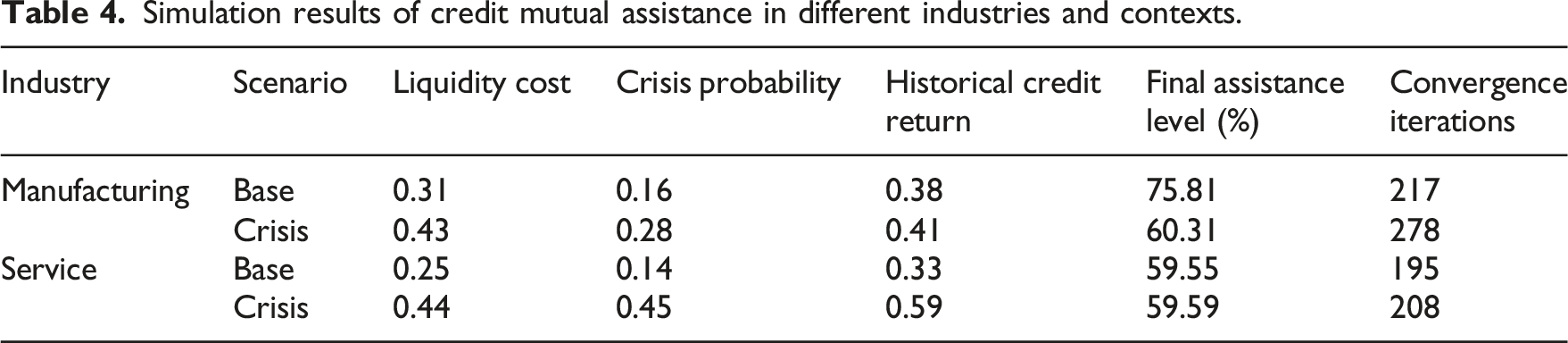

Simulation results of credit mutual assistance in different industries and contexts.

In Table 4, under baseline conditions (with liquidity costs of 0.31 and a crisis probability of 0.16), the manufacturing sector has high mutual assistance level, with convergence occurring after 217 rounds. In a crisis scenario, although the assistance level drops to 60.31%, it remains at a relatively stable level, indicating that the model retains strong stability even under increased financial pressure. However, the service sector exhibits some differences. In the baseline scenario, the assistance level is 59.55%, slightly lower than that of the manufacturing sector. In the crisis scenario (with the crisis probability increased to 0.45), the assistance level remains at 59.59%, and the convergence speed is also maintained within 208 rounds. This indicates that the increased weight of reputation in the service sector plays a buffering role under shock scenarios, helping to maintain stable mutual assistance relationships. Under different industrial backgrounds and external crisis intervention conditions, the model demonstrates stable evolutionary trends and good convergence, indicating that it possesses good industry-wide applicability and real-world adaptability.

Discussion

Inter-firm credit reciprocity involves intertemporal resource allocation. 26 This behavior is reinforced by the universal motivation for reciprocity, increased expectations of reciprocity, and urgent needs of companies facing survival crises. The results show that the existing relationships within the group have limited influence on the formation of credit relationships, and there seems to be a specific trigger threshold for credit reciprocity. In particular, large enterprise groups have relatively low credit reciprocity ratios, while small enterprises with high risk levels exhibit higher credit reciprocity ratios. This phenomenon further reveals the steady-state correlation between enterprise group size and credit reciprocity game, indicating that the change in group size has a significant positive impact on the overall interests of individual enterprises.

According to self-organization theory, credit reciprocity behavior can be regarded as the foundation of an orderly behavioral framework within a system, achieved through mutual reflection and mutual benefit. The evolution and development of the community of shared interests mainly come from the reachability of the goal after resource integration and the practical improvement of the assistance effect. First, resource integration enables enterprises or common interests to achieve goals more efficiently, and enhances the cooperation motivation among members. In addition, resource integration improves the effectiveness of assistance, enabling enterprises to solve problems more effectively and reduce the impact of crises when providing assistance, thus enhancing trust and cooperation among members. In the process of providing crisis assistance to relationship partners, a balance between benefit distribution and internal trust constraints can effectively solve corporate crises. 27 In corporate credit reciprocity, social ties have a positive impact on corporate credit reciprocity. Enterprises with embedded ties with banks are more able to obtain credit transaction opportunities and reduce the probability of crisis.28–30 In addition, the personal behavior of business owners as well as corporate culture also affects the homeostasis of corporate credit reciprocity. The trust relationship between members of enterprise groups and the psychological tendencies of individual members also have a complex impact on the credit reciprocity of crisis enterprises.

The credit reciprocity strategy during a corporate crisis is beneficial in reducing the probability of corporate risk and increasing the survival rate of enterprises in crises. However, the conflicts of interest or individual behavior among policy makers, managers, and other stakeholders determine the outcome of implementing a corporate credit reciprocity strategy. Similarly, through the credit reciprocity strategy of crisis enterprises, policy makers have received some policy recognition, while managers have the opportunity to ensure the survival of the enterprise. When the credit reciprocity strategy is successfully implemented, it will reduce the number of corporate bankruptcies, ensure the interests of the majority of the population, alleviate financial pressure, and reduce unemployment. Therefore, it can be considered positive and meaningful to carry out corporate credit reciprocity strategy during the crisis. In turn, theoretical research drawn by Borzaga et al. has shown that cooperation among all types of enterprises is more effective in protecting employment than investors using useful enterprises, indicating that credit reciprocity strategies are effective in reducing the probability of corporate crises. 31 Cornée et al. have proposed a theoretical model to analyze the repayment performance of enterprises generated by reciprocity. The results show that enterprises with favorable credit conditions are more likely to obtain social bank loans. Cornée et al. have argued that credit markets are reciprocal and have a weakening effect on the probability of enterprise crises. 32 This is consistent with the results obtained in the study.

Kremp and Sevestre analyzed the credit changes of independent small and medium-sized enterprises in France to obtain bank loans. However, this study only analyzes the changes from the perspective of sample observation and does not deeply explore the relevant factors of credit changes. 33 Their research mainly focuses on obtaining credit for individual enterprises, lacking in-depth analysis of the dynamic changes in credit relationships between enterprises. In contrast, Graafland explored the restriction formation process from government and banks in the corporate credit crisis, but the research did not analyze at the group level either. 34 Although Graafland provides a macro perspective, it lacks in-depth discussion on the interaction between enterprises and credit reciprocity behavior at the micro level.

Different from these research studies, this study is based on the traditional snowdrift game model, from the perspective of the mixed enterprise group, facing the group credit reciprocity model in the enterprise crisis. This change in perspective can provide a more comprehensive understanding of the dynamic characteristics of credit reciprocity behavior between enterprises and its impact on the overall stability of enterprise groups. By introducing intertemporal credit reciprocity and crisis randomness, the proposed model not only considers the immediate interaction between enterprises but also analyzes the long-term credit relationship. This is in sharp contrast to Kremp and Sevestre’s sample observation method and Graafland’s macro-analysis. This study focuses more on the dynamic changes and underlying mechanisms of credit relationships between enterprises.

In addition, it is worth noting that the stability of credit relationships may differ in different contexts. For example, in the high crisis probability and low liquidity management cost, inter-firm credit reciprocity is easier to form and maintain. This is because the high crisis probability makes enterprises more inclined to seek external support, while the low liquidity management cost reduces the burden of enterprises to provide help, thus promoting the stability of credit relations. On the contrary, in the low crisis probability and high liquidity management cost, the stability of credit relationship is relatively weak. In this case, enterprises may pay more attention to their own liquidity management and be less willing to provide credit support, leading to greater challenges in the formation and maintenance of credit relationships. Through these scenario analyses, the subsequent research can better understand the dynamic changes of inter-firm credit reciprocity in complex and changeable environments, and provide more specific guidance for enterprises in crisis management.

The decision-making process of inter-firm credit reciprocity may be affected by many irrational factors. For example, when a company faces major decisions, overconfidence among decision-makers may overestimate their own company’s credit status, leading to excessive optimism in providing credit support and overlooking potential risks. Conversely, when businesses are in a highly uncertain market environment, policy makers’ risk aversion may lead to being overly cautious about credit reciprocity opportunities, even if these opportunities may generate long-term returns. This behavioral deviation contradicts the assumption of rational economic agents in traditional economics, but it is widely present in reality. By introducing the principles of behavioral economics, subsequent studies can more accurately simulate the decision-making process of enterprises and consider the influence of factors such as cognitive bias, emotional influence, and social norms on reciprocal credit decision-making, so as to provide more realistic theoretical support for enterprises to formulate more effective credit management strategies in complex and changeable economic environments.

Conclusion

Based on the improved snowdrift game model, the formation mechanism of the credit relationship between enterprises under the enterprise crisis situation is deeply discussed. It is found that the credit relationship is initially partially generated within large enterprise groups and then strengthened within small enterprise groups. However, due to the scarcity of direct interaction between enterprises within large enterprise groups, the formation of credit relations needs more and stronger mechanisms to support. In addition, trust relationships within enterprise groups cannot be completely transformed into credit relationships, and the formation of credit relationships presents the characteristics of “threshold triggering” under certain crisis probabilities. Finally, the mutual assistance level and crisis probability between enterprises interact with the scale of enterprise groups and jointly affect the credit relation within enterprise groups. These findings not only reveal the complex dynamic process of credit relationship formation between enterprises but also provide a new perspective for enterprise risk management in crisis situations. By understanding these mechanisms, companies can better design and implement credit reciprocity strategies to enhance their own resilience and the overall stability.

Limitations and future research directions

The study has yielded certain results, but limitations remain. Firstly, it did not employ machine learning algorithms to predict the probability of crises and simulate inter-firm credit reciprocity, which may have restricted the precise prediction of the dynamic changes in credit relationships under crisis situations. Future research can introduce algorithms such as XGBoost and support vector machines to train crisis early warning models based on historical credit data and simulate the evolutionary trends of mutual assistance behavior among enterprises, thereby improving prediction accuracy and dynamic adaptability. Secondly, it did not fully integrate big data resources, such as social media sentiment, economic indicators, and industry-specific news, which may have resulted in a less comprehensive research perspective. In the future, it will combine emotional analysis technology and feature fusion models to incorporate heterogeneous data into the corporate behavior assessment system, thereby constructing a credit game framework with greater timeliness and multidimensional perception capabilities. Thirdly, it did not adopt dynamic network analysis to study the formation and evolution of credit relationships, which may make it difficult to capture the dynamic changes and key nodes of credit relationships within corporate groups. Future research can introduce time-slice networks and node centrality evolution analysis to identify and track the dynamic evolution paths and key nodes of the credit structure within corporate groups. Fourthly, it did not utilize agent-based modeling to simulate the behavior of individual enterprises within corporate groups, which may have led to a lack of in-depth understanding of the impact of individual firm decision-making processes and inter-firm assistance on credit relationships. Future research can combine agent-based modeling to construct multi-agent heterogeneous behavior models and conduct in-depth analysis of credit interaction mechanisms between corporate levels. Fifthly, it did not introduce optimization algorithms to identify the most efficient credit reciprocity strategies under different crisis conditions, which may have made it difficult for enterprises to quickly develop optimal credit management strategies during crises. In the future, heuristic optimization algorithms such as genetic algorithms and simulated annealing can be introduced to explore the optimal strategy combination under multiple constraints, thereby enhancing the model’s strategy recommendation capabilities and practicality. Sixthly, it did not conduct sensitivity analysis, making it difficult to assess the impact of variations in key parameters (such as crisis probability and inter-firm assistance) on the formation of credit relationships. Future research should carry out sensitivity analysis to evaluate the impact of changes in key parameters on the formation of credit relationships, thereby providing a basis for formulating more stable credit reciprocity strategies. Lastly, the intertemporal game theory model was relatively simplified in terms of strategy and payoff settings, failing to fully consider the complex long-term interactions and dynamic strategy adjustments between enterprises. This may have limited the in-depth understanding of long-term credit reciprocity dynamics. Future research can further develop the model by introducing more complex strategies and payoff structures to more accurately simulate the long-term credit reciprocity behaviors between enterprises.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The research is supported by Hebei Province Key R&D Plan Project: Development and application demonstration of an atmospheric environment monitoring, warning and source tracing evaluation system based on comprehensive analysis of big data (No.20313701D); Science and technology projects of Xiong’an New Area: Application and demonstration of communication, navigation and perception fusion technology for emergency scenarios in the underground space of Xiong'an New Area, as well as the emergency robot control platform (0104008); Hebei Province Major Science and Technology Support Program Project: “Beidou + In-Building Wireless Network” Positioning and Navigation Application Demonstration for the Ultra-Large-scale Underground Space of Xiong'an New Area (242Q0401Z).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Appendix

Proof: (1) when

Let

The following equation can be obtained: (2) Solving

Considering

Let

The following equation can be obtained: (3) Simplification of the above formulas:

A. Consider simplification of

Given that

Integrate both sides:

After derivation, it can be derived that:

B. Consider simplification of

Given that

Integrate both sides

After derivation

Now, back to the original expression, the following can be obtained:

Then we have:

Arranging the final equilibrium result, the proof is complete.