Abstract

In this article, we explore the differential effects of a firm’s reputation and status on its interorganizational network. We hypothesize that due to its stable, unitary, and relational characteristics, status has a stronger influence on partner selection than reputation, which is less stable, multidimensional, and based more on perceptions of product quality and financial performance. Results from our analyses of the director networks of the 300 largest US firms from 1985 to 1993 confirm that across multiple measures of network characteristics, it is status that is the stronger predictor. In particular, high-status firms have networks that are higher in partner quality but are less diverse and contain fewer opportunities to bridge structural holes than the networks of high-reputation firms. These results contribute to our understanding of the different effects of reputation and status on firm behavior by emphasizing the importance of studying both together in order to understand the effects of either. They also contribute to work on interorganizational networks by demonstrating how structure emerges primarily as a function of focal firm status.

The tension between economic and sociological drivers of firm action is reflected in the research on reputation and status. While reputation is a multidimensional construct that is more commonly associated with dynamic expectations of future economic performance based on changing perceptions of prior quality, status is a unitary construct that is more stable and linked to position or rank within the social structure (Jensen and Roy, 2008; Podolny, 2005; Washington and Zajac, 2005). Due to these different foundations, both constructs have been associated with important firm outcomes. Reputation, for example, has been shown to deliver higher sales (Shapiro, 1983), easier access to capital (Stuart et al., 1999), and greater survival rates (Rao, 1994), while status brings increased opportunities (Washington and Zajac, 2005), greater product quality and valuation (Benjamin and Podolny, 1999), and lower levels of uncertainty (Podolny, 1994). While the literatures on reputation and status are sizable, however, studies that embrace both reputation and status are rare (cf. Dimov et al., 2007; Jensen and Roy, 2008). As a result, while we know that reputation and status are important drivers of firm behavior, we know little about their differential effects in direct comparison to each other.

An area of the management literature that speaks directly to understanding both economic and sociological drivers of firm action is the study of networks. Networks are important to firms because interorganizational ties both enable and constrain economic activity. Such ties are valuable because they act as conduits for trust (Granovetter, 2005), nonredundant information (Burt, 1992), and other valuable resources (Pfeffer and Salancik, 1978) but can also limit the range of actions due to the embedded networks that form around firms (Uzzi, 1996). A particular area of interest is interlocking directorships, which have been identified as an important tie between firms along which ideas and practices diffuse (Davis, 1991; Haunschild, 1993; Pennings, 1980; Strang and Sine, 2002).

In spite of the large body of work that has grown around understanding the consequences of networks in general and interlocking directorships in particular, we know much less about the antecedents of this kind of interfirm ties and, at the intersection of these three broad literatures, how a firm’s reputation and status may enable or constrain the firm in its partner selection. One notable exception to this is the important work by Jensen and Roy (2008) who demonstrate empirical support for a staged model of firm behavior in which firms form resource exchange partnerships with other firms by, first, using status to identify the band of firms with whom they wish to partner and, second, using reputation to make a more fine-grained selection. As indicated by the relative lack of work encompassing reputation, status, and network theory, however, this research stream is in the early stages of development and, to our knowledge, has not addressed interlocking director networks. As such, there is still much to learn about when reputation matters, when status matters, and when they both matter in terms of a firm’s ties to other firms.

Theoretically, it is intuitive that reputation and status have different effects on network structure due to their fundamental differences. Previously, these differences have been difficult to capture empirically (Washington and Zajac, 2005), although recent progress has been made in this respect (Dimov et al., 2007; Jensen and Roy, 2008). In this article, we build on this emerging body of research and contribute to theory by exploring how a firm’s reputation and status differentially influence the characteristics of its partners and resulting network structure. In particular, we seek to determine the effects of reputation and status on partner selection in the context of the important ties formed among firms via their boards of directors. We contend that due to its more stable, unitary, and relational characteristics, status has a stronger influence on partner selection than reputation, which is more dynamic, multidimensional, and based more on perceptions of product quality and financial performance (Jensen and Roy, 2008; Podolny, 2005; Washington and Zajac, 2005). As a result, we predict that high-status firms have networks that are higher in partner quality but are less diverse and contain fewer brokerage opportunities than the networks of high-reputation firms.

If true, we anticipate this study making the following contributions to research on reputation, status, and interfirm networks. Our primary contribution is to the literature working to tease apart the effects of reputation and status. By demonstrating a stronger relationship between status and network structure, we are helping to understand the differential effects of status and reputation on firm behavior (in this case, network partner selection). This is particularly valuable because studies at the intersection of the reputation, status, and network literatures are rare (cf. Jensen and Roy, 2008), and because much prior work has focused on market, rather than behavioral, implications of status and reputation (Podolny, 1993, 2005; Rindova et al., 2005; Shapiro, 1983).

Second, we contribute to the organizational network literature by theorizing the effects of two independent determinants of partner characteristics and network structure—the status and reputation of the focal firm. While we understand the consequences of network ties for a firm’s status (e.g. Podolny and Phillips, 1996; Stuart et al., 1999) and its reputation (e.g. Raub and Weesie, 1990), the reverse relationships (status or reputation as antecedents of network ties) are rarely tested (cf. Zaheer and Soda, 2009) and, as noted above, are even more rarely studied in combination (cf. Jensen and Roy, 2008).

These contributions emerge from our analysis of a longitudinal dataset of the interlocking director network ties of the largest 300 firms in the United States.

Reputation and status

Although related and often confounded, reputation and status are now considered independent constructs (Washington and Zajac, 2005). While reputation is defined more in terms of economic performance—a signal of observable quality (dynamic and continuous), status draws on a sociological foundation and is defined more as an actor’s position within the social structure—a signal of less observable quality (stable and categorical; Dimov et al., 2007; Jensen and Roy, 2008). High levels of status and good reputation carry many important benefits for firms and their effects have been well studied.

The literature on reputation is extensive (for a comprehensive review of recent work, see Lange et al., 2010). In short, reputation is a multidimensional construct (Fombrun and Shanley, 1990; Rindova et al., 2005) that largely revolves around a firm “being known for something” (Lange et al., 2010: 156). The idea of reputation as “perceived quality” (Rindova et al., 2005: 1035) refers to the firm’s ability to create value consistently in a way that is evaluated positively by stakeholders. This external perception, based on past economic performance and product quality, acts as a proxy for full information about the firm’s operations that informs stakeholder expectations regarding future performance (Shapiro, 1983). As such, reputation is considered an asset and an important component of a firm’s strategic competitive advantage (Fombrun, 1996).

Organizational status, in contrast, is based largely on sociological concepts of markets (for recent reviews, see Bitektine, 2011; Jensen et al., 2010; Podolny, 2005); it is generally thought of in network terms and is allocated to firms according to their location in the social structure (Podolny, 1993). As such, status can be observed from firm affiliations with prominent network partners. Such ties are particularly valuable in the absence of other sources of information as stakeholders infer specific qualities about the focal firm due to its connections to high-status others (Podolny, 1994, 2001; Stuart et al., 1999).

In spite of the important work that has been done in identifying the antecedents and consequences of reputation and status independently, much less work has attempted to test the differential effects of these two constructs within the same study. On the contrary, with a few notable exceptions (Dimov et al., 2007; Jensen and Roy, 2008; Washington and Zajac, 2005), researchers are more likely to treat reputation and status as interchangeable constructs (Porac et al., 2002; Rindova et al., 2005, 2006).

1

Scholars tend to study one or the other, but not both, “considering status at least a strong correlate of reputation or a dimension that stabilizes reputation ordering” (Rhee and Valdez, 2009: 153). Yet, there are fundamental differences between these two constructs that are likely to result in differential effects on firm behavior. As Washington and Zajac (2005: 283) note, Studies of organizational status do not control for real or perceived differences in quality or merit, which in turn makes it impossible to determine whether one is capturing differences in social status or simply reputational differences based on an organization’s ability to generate higher versus lower product quality.

Without studying both constructs together, it is difficult to understand fully the underlying drivers of the measured outcomes and the relative importance of status and reputation as predictors of firm behavior.

In terms of network structure, the status and reputation of a firm’s partners have independently been shown to be consequential—affecting outcomes in situations related to resource acquisition (Stuart et al., 1999) and alliance formation (Ebbers and Wijnberg, 2010). Some work has also been done on the effects to network structure following a negative change in focal firm reputation (Sullivan et al., 2007), and network structure has been shown to be a vehicle by which reputation penalties are transferred among firms (Kang, 2008). In addition, recent work has begun to investigate drivers of firms’ willingness to enter into heterophilous status relationships (e.g. Castellucci and Ertug, 2010; Shipilov et al., 2011). It is much rarer, however, for scholars to address the differential effects of both firm reputation and status in the context of interfirm networks (cf. Jensen and Roy, 2008). We seek to advance this important work by adding to our understanding of how a focal firm’s reputation and status influence tie formation and network structure.

Social networks and interlocking director ties

Social networks are important because they both enable and constrain action. Due to the prevalence of networks among firms, there has been a great deal of research devoted to documenting the consequences of various network structures and partner characteristics. In particular, network structure has been associated with important outcomes that include practice adoption (Palmer et al., 1993), learning and innovation (Powell et al., 1996), and firm survival (Podolny et al., 1996). While there has been much debate and work on the consequences of various types of network structures, there has, however, been much less research on the causes of these structures, with a few exceptions (e.g. Gulati, 1995; Gulati and Gargiulo, 1999; Zaheer and Soda, 2009).

Where such research has been done, it has focused on firm motivations to network with certain types of partners in order to alleviate uncertainty (Beckman et al., 2004) as a result of performance feedback (Baum et al., 2005; Shipilov et al., 2011) or to provide learning opportunities (Kogut, 1988). We build on this work to understand why some firms have networks with particular structural characteristics. Specifically, we theorize why some firms have networks that are higher in partner quality, lower in diversity, and contain fewer brokerage opportunities. Importantly, therefore, contrary to prior work that has looked independently at the effects of network structure on either reputation (Raub and Weesie, 1990) or status (Podolny and Phillips, 1996), we study the reverse relationships by looking at the simultaneous effects of both reputation and status on partner characteristics and network structure.

We develop and test our theory in the context of one particular network form—interlocking directorates, which are consequential for firms and central to prior research that has investigated interorganizational network ties (e.g. Davis, 1991; Haunschild, 1993; Pennings, 1980; Strang and Soule, 1998). We selected this form of network tie because it is particularly appropriate to the organizational-level arguments on which we draw to motivate our hypotheses. One of the key roles of directors is to act in an information advisory capacity, and directors are selected, in part, for their access to relevant experience and knowledge that is gained from working for firms with which the focal firm wishes to partner (Haunschild and Beckman, 1998; Lorsch and MacIver, 1989). As a result, while directors serve officially in an individual capacity, we argue that their value to the focal firm is drawn primarily from their organizational affiliation (Beckman and Haunschild, 2002). Nevertheless, it is also intuitive that the characteristics of an individual that predict selection as a director (e.g. personal reputation, ability, and trustworthiness) are correlated with the organizational-level characteristics that make the firm that person works for attractive as a potential partner, primarily because it was those characteristics that allowed the individual to rise to prominence within that firm. While recognizing that board interlocks bridge individual- and firm-level networks and that in addition to macro-level predictors, the formation of these ties can be driven by personal self-interest (Useem, 1984; Zajac, 1988) or social relations among firm leaders (Westphal, 1999; Zajac and Westphal, 1996), therefore, we argue that the primary motivation for an invitation issued by a firm to a specific director can be discerned from the firm-to-firm tie, particularly in the case of the large, public firms that we study. Thus, while our theory extends to all network ties where information is sought from the partner firm, it is particularly appropriate in the director interlock context.

In the following sections, we first theorize why firm status is likely to be a more important predictor of partner selection than reputation. We then hypothesize why it is that these specific characteristics, which give high-status firms the opportunity to select from the widest range of potential partners, instead result in networks that are higher in partner quality but are less diverse and contain fewer opportunities to bridge structural holes than the networks of high-reputation firms.

Network partner quality

Given the different economic and sociological foundations of reputation and status (Washington and Zajac, 2005), together with our emerging understanding of their different effects on firms’ network partner decisions (Jensen and Roy, 2008), analyzing the effects of both constructs simultaneously is essential to provide a more comprehensive understanding of the underlying relationships among reputation, status, and network structure. A measure of particular interest to high-reputation and high-status firms, we suspect, is the quality of their network partners, a proxy for which is partner reputation.

Although reputation and status are clearly related and, we believe, will both predict the reputations of a firm’s network partners, they are also conceptually different (Washington and Zajac, 2005). As such, we do not anticipate that reputation and status will be equally important predictors of which network partners’ firms choose. Specifically, we contend that focal firm status will be a more important predictor of partner selection than focal firm reputation. This argument is grounded in prior research that has identified status as the primary determinant in tie formation (Jensen and Roy, 2008), which enables high-status firms to have their first choice of partners (Podolny, 2001). Central to the theory we build to support these effects is the conceptualization of status as a more stable construct than reputation. It is this stability that elevates status as a more permanent fixture in external perceptions of the firm, which makes it a more salient determinant of tie formation and allows high-status firms first choice among potential partners.

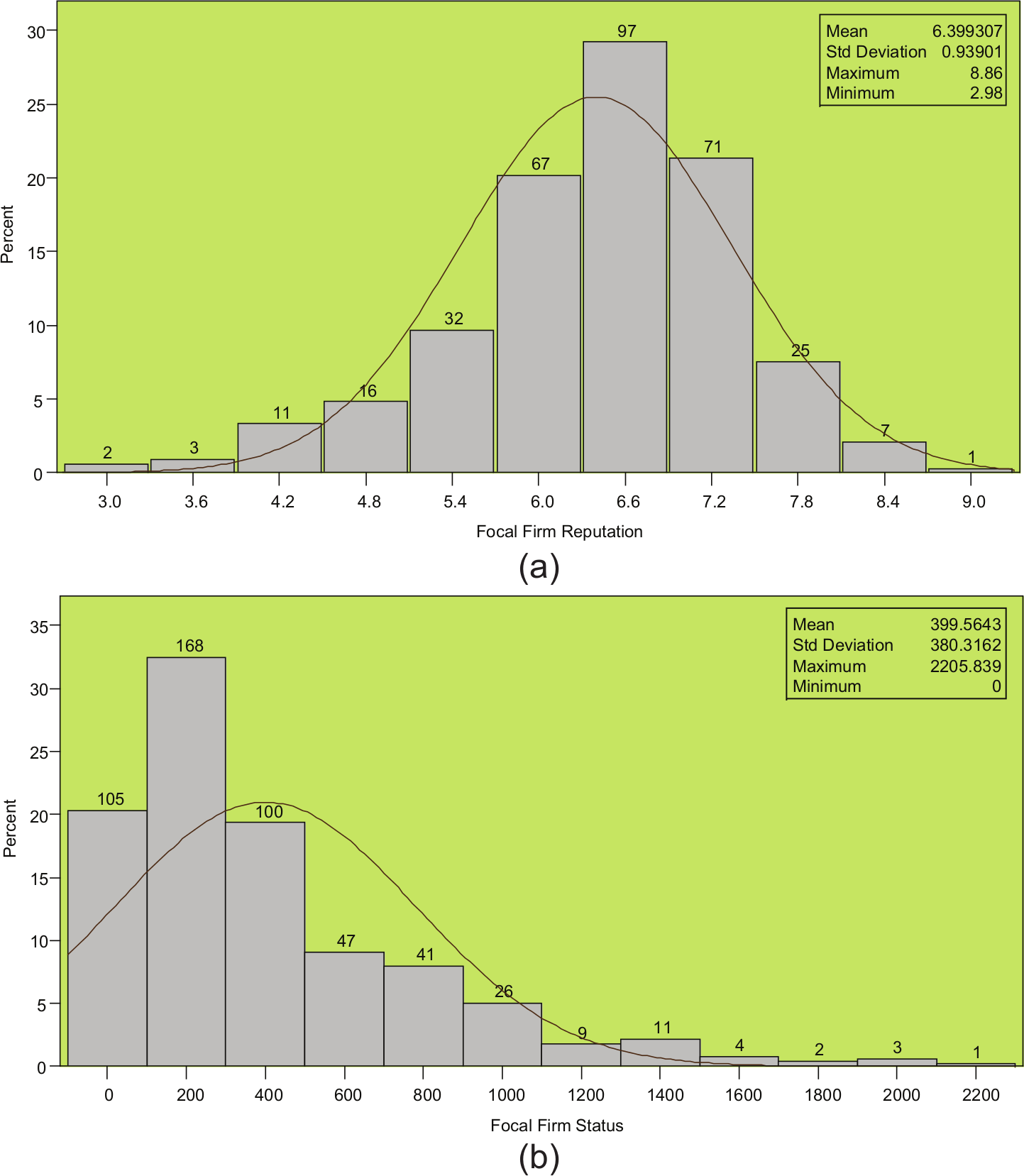

This conceptual distinction is demonstrated empirically by viewing the different distributions of reputation and status in Figure 1(a) and (b). While status is more skewed, reputation scores are more normally distributed. This has important theoretical implications because the skewed distribution of status increases the visibility of high-status firms. When you consider the quality (reputation) and prestige (status) of car brands, for example, high-status cars are more prominent than high-reputation cars partially due to this distribution effect (Rhee and Haunschild, 2006). In a sense, our cognitive map distinguishes among different status levels on a binary basis (high/low), whereas reputation is used to refine partner choices based on relative quality within specific status bands (Jensen and Roy, 2008). It is status that is more stable (there is less likely to be movement among bands), while reputation is more susceptible to fluctuation in changing perceptions of product quality or some other dynamic measure of firm performance. As such, we anticipate that firm status will be a more important and consistent determinant of tie formation than reputation.

Distribution of focal firm (a) reputation and (b) status.

Reinforcing this notion of status as a more dominant determinant of partner selection is the idea of status as a unitary, all-encompassing assessment of the firm. As Jensen and colleagues argue (Jensen and Roy, 2008; Jensen et al., 2010), while status is unitary (evaluated for the firm as a whole), reputation is multifaceted (tied to different firm characteristics in different areas of performance). In other words, while firms tend to have one social status within a social system (good or bad), they can have multiple reputations within that system based on different attributes (some good, some bad). As such, “status provides an assessment of the quality of the organization as a whole, whereas reputation provides an assessment of the quality of individual organization attributes” (Jensen et al., 2010: 90–1). We argue that these different characteristics imply different opportunities for high-status firms (they are better placed to select the high-reputation partners they seek), even while those choices form structural constraints (high-reputation partners are selected from a narrow range of similar “quality” firms), and result in a stronger predictive power for status in tie formation.

Finally, in addition to being more stable and unitary than reputation, a further distinguishing characteristic of status is that it is more relation based. In particular, while “reputation captures differences in quality that generate earned, performance-based rewards … status captures differences in social rank that generate unearned, non-performance-based privilege” (Jensen et al., 2010: 90). In other words, because status is socially embedded (and includes quality, but is not limited to quality), while reputation is grounded in economic performance (focusing primarily on product quality), status is likely to be a stronger predictor of board interlock tie formation than reputation due, in part, to the social nature by which such ties are formed (Westphal, 1999; Westphal and Stern, 2007; Zajac and Westphal, 1996).

These three points of distinction suggest that the more stable, unitary, and relation-based characteristics of high status will generate different firm-level network outcomes than the more dynamic, multifaceted, and performance-based characteristics of reputation. In particular, they suggest that status will be a stronger predictor of partner selection than reputation because, given the preferential ability to choose, firms will likely seek to maximize this advantage. We predict that high-status firms will choose partners with high reputations because reputation is a salient signal of perceived quality in firm products and economic performance. Thus, high-reputation firms will be thought more likely to have good information about such operational matters, and high-status firms will select these firms as partners in an attempt to access that information.

Hypothesis 1 (H1): Focal firm status will be a stronger positive predictor of partner reputation than focal firm reputation.

As suggested above, in addition to high-status (rather than high-reputation) presenting firms with greater opportunity to select the partners with which they choose to network, high status can also constrain decision making. Although such firms have the freedom to select partners from across the reputation spectrum, for example, they are more likely to select high-reputation partners (H1). While justifiable in any isolated decision, once this tendency is generalized across all partner decisions, it carries the potential to produce networks that contain less diversity and greater density as high-status firms select among the narrow group of acceptable higher reputation partners. Low-status firms, in contrast, faced with selecting among firms below the upper reputation echelon, have a less restricted range of partner choice and, as a result, end up with more diverse and less dense networks. If true, this relationship is of interest given that homogeneous, dense networks tend to present fewer opportunities to the focal firm to bridge structural holes and, therefore, tend to be less beneficial in terms of information gathering (Burt, 1992) and decision-making quality (Beckman and Haunschild, 2002).

We test this proposition, grounded in our theory that focal firm status will generate different network outcomes than focal firm reputation, by studying the effects of status on two network attributes (network partner diversity and network brokerage), while controlling for focal firm reputation. If true, we anticipate that the dense networks of high-status firms will be less diverse and contain fewer opportunities to bridge structural holes than the networks of low-status firms, and that high reputation will have a much weaker effect on network structure (or no effect at all).

Network diversity

In contrast to pressures that push firms toward homophily in tie formation (Beckman and Phillips, 2005; Seidel and Westphal, 2004), firms also tend toward self-enhancement. In other words, all else equal, firms will aspire to network with others that have higher reputations than their own (Ebbers and Wijnberg, 2010). This is likely because of the referred benefits a high-reputation partner confers. Acting as a constraint on this ambition, however, is a countervailing force—a firm’s ability to network with others (i.e. the focal firm’s attractiveness to potential partners). While lower status firms might aspire to partner with higher reputation firms, for example, their ability to do so is constrained because higher reputation firms have little incentive (in terms of their own enhancement) to reciprocate and partner with them (Kang, 2008; Podolny, 1994). High-status firms, however, have both the aspiration and ability to form ties with high-reputation partners. If true, this should result in high-status firms partnering with high-reputation firms, but lower status firms unable to connect with higher reputation firms.

In practice, the consequence of the combined effects of both the aspiration and ability to partner is that the higher the status of the focal firm, the narrower the range of desirable partner choices. Any firm that is situated at the upper echelons of the status hierarchy, for example, faces a relatively small pool of attractive reputation partners. In contrast, a firm lower in the status hierarchy, with less ability to connect with the very highest reputation firms, but with the same desire toward self-enhancement, faces a much larger pool of firms with which they are willing to partner. This effect should produce a concentration in the network partner characteristics of higher status firms, while resulting in greater diversity among the network partners of lower status firms.

This mechanism is central to our argument. We agree with Podolny and Phillips (1996) that the issue of status mobility is an empirical question that is yet to be determined in the literature, especially in terms of how the status distribution evolves over time and whether the rate of mobility is constant across status levels. Our study helps address this question by arguing that status has differential effects on firm actions at different points along the status hierarchy (Bothner et al., 2011; Phillips and Zuckerman, 2001). In particular, we test the hypothesis that there are mobility barriers at the higher echelons of the status hierarchy that constrain the choices of network partners made by firms.

Rather than having a smaller choice set per se, we argue that high-status firms choose to limit their range of network partners to those they consider most desirable, while those at the bottom place fewer restrictions on their potential partners. High-status firms could, in theory, select a diverse set of partners because of the advantages of diversity for decision making (Beckman and Haunschild, 2002). In fact, it would be easier for them to do so because, due to their location at the higher echelons of the status hierarchy, they are at the front of the queue for partner selection—they are sought out as potential partners and, therefore, have more choice about who they can select (Podolny, 2001). Similar to Seidel and Westphal (2004), however, we argue that these firms generally do not take advantage of the breadth of possible choices because of the salient attractiveness of high reputation. Thus, the larger pool of firms available as acceptable partners for lower status firms suggests that the reputation variance among these firms’ network partners is likely to be higher than the partner reputation variance for firms at the higher end of the status hierarchy.

We do not anticipate that this relationship will hold equally, however, for high-reputation firms. As noted above, due to the conceptual differences between reputation and status, we theorize that status will be the dominant predictor of partner selection. In particular, we argue that due to its more stable, unitary, and relational characteristics, status will be a stronger predictor of tie formation than reputation, which is more dynamic, multifaceted, and based more on firm performance. Drawing on the same theory used to predict the average reputations of a firm’s network partners (H1), therefore, we hypothesize that these differences will also generate different outcomes in terms of partner reputation variance as high-status firms are more able to select their high-reputation partners of choice.

Hypothesis 2 (H2): Focal firm status will be a stronger negative predictor of network partner reputation variance than focal firm reputation.

Network brokerage opportunities

Brokerage is defined in the network literature as “a relation in which one actor mediates the flow of resources or information between two other actors who are not directly linked” (Fernandez and Gould, 1994: 1457). Brokerage is a well-studied phenomenon by social network scholars that contains both advantages and disadvantages for the focal firm (e.g. Hansen, 1999). As a result of this research, for example, we know that network brokers occupy a structural position that confers specific advantages, such as access to nonredundant information (Burt, 1992), greater influence among partners (Fernandez and Gould, 1994), and higher performance (Soda et al., 2004). These advantages, however, are often contingent on specific factors, such as the type of bridging tie (Tortoriello and Krackhardt, 2010), the complexity of the knowledge being transferred (Hansen, 1999), and the degrees of separation over which the brokered tie occurs (Burt, 2007).

As this large body of work attests, brokerage is an important network structural characteristic that, for network scholars, exists “not only as an explanatory variable but also as a phenomenon to be studied and explained in its own right” (Gould and Fernandez, 1989: 124). While work has been done separately on status as an antecedent of structural holes (Zaheer and Soda, 2009) and the effects of structural holes on organizational status (Shipilov and Li, 2008), however, we are not aware of any attempts to tease apart the competing effects of reputation and status on the opportunity for brokerage within the focal firm’s social network. As such, demonstrating the relationships between status, reputation, and brokerage should be of interest to network scholars. This measure is also an important additional test of our theory that denser networks, composed of similar actors, constrain the focal actor due to redundant interconnectivity among ego’s alters (Granovetter, 1973, 1983).

Assuming that the desire to partner with high-reputation others is relatively stable across firms, but that the ability to partner varies, high-status firms should be better placed to select the small subset of high-reputation firms as partners (H1). This argument suggests that the higher a firm’s status, the smaller the pool of attractive potential partners. As the pool of actors at the top of the status and reputation hierarchies concentrates, the variance within a high-status firm’s network should decrease (H2). The combination of these two hypotheses, if true, suggests that a firm’s network density will increase the further it is along the status continuum, which also suggests that high-status firms will have fewer structural holes in their networks (Burt, 1992). In other words, in contrast to others who have looked at the relationship between status and structural holes (Zaheer and Soda, 2009), we expect greater embeddedness in the networks of high-status firms as the focal firm and partner networks increasingly overlap.

Consistent with our hypotheses above, we also anticipate that focal firm status will be a stronger predictor of this outcome than focal firm reputation. Due to their conceptual differences, high-status firms are better able to form ties with their target partners than high-reputation firms and, therefore, will likely have networks that are more efficient as they compete more effectively for the narrow range of the most attractive partner firms.

Hypothesis 3 (H3): Focal firm status will be a stronger negative predictor of network brokerage opportunities than focal firm reputation.

To summarize, we have theorized that due to its stable, unitary, and relational characteristics, focal firm status will be a more important predictor of network structure than focal firm reputation. In practice, this means that high-status firms will have networks that are higher in partner quality but are less diverse and contain fewer opportunities to bridge structural holes than the networks of high-reputation firms. We have theorized that the mechanism that leads to these results is self-constraint in the partner selection process. Paradoxically, while high status affords greater freedom for firms to select from the widest range of partners, they instead limit themselves to selecting partners among the narrow set of high-reputation firms, which leads directly to the outcomes we hypothesize.

Methods

The data for this study were obtained from the 300 largest publicly held service and manufacturing firms listed in the United States in 1990. We collected data on each of these firms and their network partners in the years 1985, 1990, and 1993. These years were selected in order to capture a sufficiently long period of time in which to study changes in the firms’ director networks, while the intermittent periods between data collection points allowed us to test for different lag effects. In order to gather our network data, the proxy statements of each of the focal firms were obtained and coded to identify the direct interlock ties of that firm in each year. As such, we constructed the complete ego networks for each focal firm, including all of their partners. Some of these partners are among the 300 largest firms, but many are not.

A focal firm’s network consists of a combination of both sent and received ties. Sent ties occur when an officer of the focal firm sits on the board of another firm. Received ties occur when an officer of another firm sits on the board of the focal firm. We used both sent and received ties in our analyses because both contribute to the position of the focal firm in the larger network and the firm’s status within that network. We also included indirect ties among firms, which occur when two firms have directors who sit on the board of a third firm but have no direct tie between them because these ties are similarly critical to the comprehensive picture of the overall network needed for our measures (e.g. Bonacich centrality and brokerage). For example, if Google (focal firm) forms a tie with Apple because of Apple’s high status and Apple has a tie with Starbucks for a similar reason, the status of Google is enhanced when its direct partner, Apple, is tied to other high-status firms, such as Starbucks (Podolny, 1994, 2001; Stuart et al., 1999). Essentially, the indirect tie opens an avenue for linking Google and Starbucks, even though there is no direct link between the two. As such, we use both direct and indirect ties to construct our measures in line with other interlock research (Beckman and Haunschild, 2002; Palmer et al., 1995), while controlling for the proportion of sent and received direct ties in each network.

Of the 300 firms in our dataset, complete network data were available for a total of 290 focal firms over the 3 years of our study—256 firms in 1985, 285 firms in 1990, and 265 firms in 1993. Our total dataset, therefore, comprises the ego networks of interlocking director ties for each of these focal firms in 1985 (3381 unique partners and 8471 network ties), 1990 (3406 unique partners and 8796 network ties), and 1993 (3184 unique partners and 7898 network ties).

Independent variables

There are two independent variables of interest in this study—focal firm reputation and focal firm status. In order to measure a firm’s reputation (stakeholder perceptions of firm performance and product quality), we use the America’s Most Admired Companies data published annually in Fortune magazine. The Fortune data have been produced annually since 1982. They are a compilation of eight separate measures (Innovation, People management, Use of corporate assets, Social responsibility, Quality of management, Financial soundness, Long-term investment, and Quality of products/services) that have been widely used by researchers as an indicator of firm reputation, with firms being scored on a scale from 0 to 10 (Deephouse, 2000). Figure 1(a) reveals that the reputation scores of the focal firms in our dataset have a normal distribution that ranges from 2.98 to 8.86. 2

Despite its widespread use as a proxy for firm reputation (e.g. Fombrun and Shanley, 1990; Staw and Epstein, 2000), researchers have identified serious limitations with the Fortune data that include the compilation methodology, narrow stakeholder focus, and large US firm bias (Deephouse, 2000). Other concerns include construct validity due to the fact that the ratings are largely determined by managers’ perceptions of financial performance (Brown and Perry, 1994; Fryxell and Jia, 1994). As such, rather than use the overall Fortune score, we operationalized reputation in line with other researchers who study reputation but who share our concern with the raw data. In particular, we use the within-industry rankings that are published in Fortune magazine for both the focal firms and their network partners (Love and Kraatz, 2009). Fortune publishes the top 10 firms in a wide range of industries. As such, these data range from 1 to 10, with 1 being the highest ranking reputation firm in a particular industry. Similar to Love and Kraatz (2009: 322), we inverted these rankings to ensure that a higher positive coefficient represents the effects of a better reputation.

In additional analyses not reported here, we also operationalized reputation in line with other researchers who focus predominantly on high reputation (Pfarrer et al., 2010). These researchers argue that while appearing on the Fortune list represents “prominence” (Mishina et al., 2010: 708), only those firms that are awarded a high Fortune score can safely be considered to have a good reputation (Pfarrer et al., 2010). In line with this research, we created a dummy variable to represent high reputation, coding the Fortune data available for both the focal firms and their network partners as 1 if the firm scored at or above the 75th percentile for all available data (7.00 for focal firms and 6.72 for network partners) and 0 otherwise. This alternative coding of the Fortune data generated results that are consistent with those reported below.

For our measure of focal firm status (a firm’s location in the social structure, as indicated by its affiliations with others), we used the network data to calculate each focal firm’s Bonacich (1987) centrality. This measure of centrality captures the extent to which each actor is partnered with well-connected others in the total network and has been widely used as a measure of status. In line with prior work, we weighted the beta value at 100% of the reciprocal of the largest eigenvalue (Benjamin and Podolny, 1999). When we use a beta value that is 75% of the reciprocal (Podolny, 1993), the results are unchanged. The UCINET output generates two measures (normalized and nonnormalized power); the nonnormalized variable is included in the models because we already control for network size, but results remain essentially the same to the ones reported below when we use the normalized value. Figure 1(b) reveals that the status scores of the focal firms in our dataset have a skewed distribution that ranges from 0 to 2205.84. For our regression models, we divided the overall score by 100 to create comparability among the variable coefficients.

Dependent variables

We created three dependent variables to capture the focal firm’s ego network structure. We used the Fortune data to calculate the measures of reputation among a firm’s network partners that form the first two dependent variables in this study—average partner reputation and partner reputation diversity. We use the coefficient of variation, the standard deviation divided by the mean, to calculate reputation diversity. The coefficient of variation is a commonly used measure for information-based arguments about diversity as a source of variety (Harrison and Klein, 2007; Sorensen, 2002).

The network that we used to calculate the brokerage dependent variable was formed by building a nonsymmetrical, nondirectional square matrix, which was read into UCINET 6.0 (Borgatti et al., 2002) to create the matrices that represent the aggregate ego networks for each of the focal firms in our sample. We then used UCINET’s Networks/EgoNetworks analysis to calculate the brokerage score for each firm in each network. Specifically, this measure was developed by Gould and Fernandez (1989) and captures the effects of five different types of brokerage (Coordinator, Consultant, Gatekeeper, Representative, and Liaison), all of which reflect the focal firm’s ability to access unique sources of information. In particular, an individual i is a broker between individuals j and k if and only if ioj, iok, jōk, where o denotes some flow or tie from the first to second actor, and ō denotes no flow from the first to second actor. (Friedman and Podolny, 1992: 34)

Gould and Fernandez’s brokerage measures have been used by other researchers publishing in top management and sociology journals as a measure of the extent to which the focal firm bridges structural holes within its ego network (e.g. Fernandez and Gould, 1994; Friedman and Podolny, 1992). For our regression models, we divided the overall score by 100 to create comparability among the variable coefficients.

Control variables

To rule out alternative explanations for our findings, we controlled for several factors.

Focal firm industry

The uncertainty associated with a specific industry is expected to influence both the kinds of partners a firm seeks (Beckman et al., 2004) and the value of reputation as a signal of quality or location in the social structure (Podolny, 1994). As such, we use a measure of uncertainty related to the focal firm’s industry as our industry control (Beckman et al., 2004). This variable is operationalized as the mean monthly stock price volatility of all sampled firms in the focal firm’s industry grouping in the year in which the firm’s network was constructed. The monthly volatility is calculated as the coefficient of variation for a firm’s monthly stock closing price (the standard deviation of the monthly closing price divided by the mean price). The greater the variation in the stock prices of firms throughout the industry, the greater the uncertainty facing the focal firm. As such, this uncertainty variable offers a control that is more proximate to the mechanism by which industry should matter. In addition, given that 41 different two-digit standard industrial classification (SIC) industries are represented in our data, this variable also serves to retain statistical power in our analyses.

Focal firm network size

The size of the focal firm’s network (measured as the total number of partners) was included in each model as a control. It may be that the networks of higher or lower reputation/status firms tend to be either larger or smaller and, as a result, have specific structural characteristics. Controlling for a firm’s network size removes these possible alternative explanations from our analyses and provides a more accurate comparison of measures across networks. This variable was logged due to its skewed distribution.

Proportion of sent and received ties

In order to control for the possible different effects of the direct and indirect network ties in our data, we included both the number of sent ties and the number of received ties as proportions of the total ties in each focal firm’s network. To the extent that direct ties are more influential than indirect ties in explaining our results, these two controls account for this influence. These variables were logged.

Focal firm profitability

It is important to account for a firm’s profitability because prior work has demonstrated that along with firm size, it predicts inclusion in the Fortune dataset. In addition, Washington and Zajac (2005) note the importance of controlling for performance in order to better isolate the social effects of reputation and status. Following prior work, we operationalized this variable using a firm’s return on assets.

Focal firm size

Firm size is an important predictor of firm attributes and behavior. Prior work has also demonstrated that the larger the organization, the more likely it is to be included in the Fortune reputation rankings (Deephouse, 2000; Fombrun et al., 2000). In line with past studies, we used the log of assets as a proxy for firm size.

Endogeneity and unobserved heterogeneity

Finally, there are multiple possible alternative determinants of the dependent variables in our regressions that we are not able to capture in our models. To control for this potential bias, we included a year dummy in our models to capture any broad, unobserved heterogeneity that varies by time period and that might act as an alternative explanation of our hypothesized effects. We also included lagged dependent variables as controls in all our models. Running these models more clearly represents a measure of change in network structure as a function of prior firm reputation and status, and also creates a conservative test of our hypothesized relationships.

Statistical analyses and results

Our repeated observations on firms across time rule out the use of ordinary least squares (OLS) estimation—the multiple observations per firm compromise the assumption of independence that is a necessary condition for OLS. 3 Given the continuous nature of our dependent variables, we used generalized estimating equations (GEEs) with robust standard errors to analyze our data, with repeat statements by firm to account for the nonindependent observations (Liang and Zeger, 1986). GEE models with a specified log link function (due to the distributions of the dependent variables) and a Gaussian (i.e. normal) distribution provide an appropriate analysis of these longitudinal data (Rhee and Haunschild, 2006). All regressions were run using a first-order autoregressive correlation structure, although, due to the limited number of time lags in our data, alternative correlation structures (unstructured, independent, and exchangeable) produced the same results.

Focal firm reputation is one of the independent variables of theoretical interest in our analyses. By definition, however, Fortune reputation scores are not available for all firms. In order to account for any potential selection bias among our reputation data, therefore, we conducted all analyses using a two-stage Heckman (1979) Selection model, which corrects for potential bias by controlling for those factors that predict inclusion in the Fortune data (Deephouse, 2000). In constructing our selection parameter, which we used as a control variable in our main regression models, we regressed a dummy variable indicating the presence of a reputation score for a given firm onto three variables—industry uncertainty, the log of network size, and the log of the firm’s employees (which was excluded from our second-stage regression models).

Table 1 presents the simple statistics and pairwise correlation coefficients for all the dependent, predictor, and control variables tested in our models. In order to be sure that multicollinearity is not an issue in our analyses, we calculated condition indices for all models and found no cause for concern. In none of the main effects models did the reported condition indices rise above 6.44, well below the recommended level of concern of condition indices greater than 30 (Belsley et al., 1980: 112). Variance inflation factors also did not suggest any cause for concern, with neither of our independent variables of interest higher than 2.22, well below the level of concern of 10 (O’Brien, 2007).

Descriptive statistics and Pearson correlation coefficients.

SD: standard deviation; DV: dependent variable.

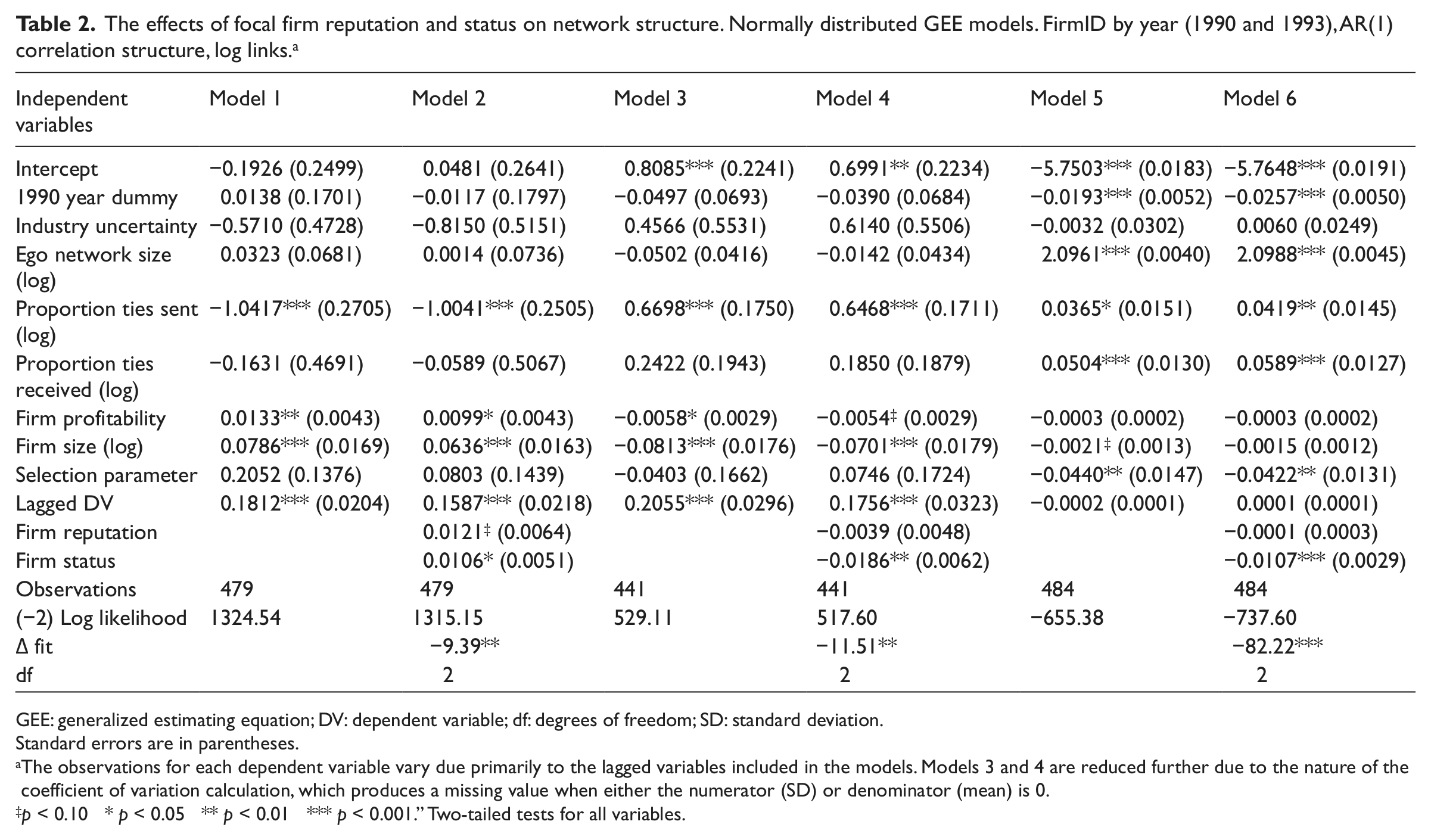

We regressed each of the three dependent variables onto our lagged reputation and status measures (1985 predicting 1990 and 1990 predicting 1993). We ran two models for each dependent variable. The first model includes the control variables only, as a baseline point of comparison, while the second model adds our independent variables, focal firm reputation and status. We draw our conclusions about our hypotheses, therefore, from the second, full model for each dependent variable. The GEE method invoked by the REPEAT statement is not a likelihood-based method, which means that QIC is the only fit statistic available for these models. As such, we conducted separate likelihood ratio tests to compare log likelihoods across nested models and calculate the value added by our variables of interest. Table 2 reports the regression results and fit statistics for all models. Two-tailed significance tests were conducted for all variables.

The effects of focal firm reputation and status on network structure. Normally distributed GEE models. FirmID by year (1990 and 1993), AR(1) correlation structure, log links. a

GEE: generalized estimating equation; DV: dependent variable; df: degrees of freedom; SD: standard deviation.

Standard errors are in parentheses.

The observations for each dependent variable vary due primarily to the lagged variables included in the models. Models 3 and 4 are reduced further due to the nature of the coefficient of variation calculation, which produces a missing value when either the numerator (SD) or denominator (mean) is 0.

p < 0.10 * p < 0.05 ** p < 0.01 *** p < 0.001.” Two-tailed tests for all variables.

In Model 2, the dependent variable is average partner reputation. In this model, the coefficients for both focal firm reputation (marginal, p < 0.1) and status (p < 0.05) are positive and significant. While not independently hypothesized, these results support the concept of homophily, the “observed tendencies for similarity between the group affiliation of friends or between their positions within a group” (Lazarsfeld and Merton, 1954: 24). While status homophily has been shown to occur in various contexts such as investment banking (Podolny, 1994) and the California wine industry (Benjamin and Podolny, 1999), and has also been shown to extend to the similarity of structural location in a network (McPherson et al., 2001), however, the phenomenon of reputation homophily has not been directly tested. The results presented in Table 2 suggest support for this concept.

In order to test H1, which predicted that a firm’s status, rather than its reputation, is a stronger predictor of the average reputation of its network partners, we first compared significance levels and t values from the regression output, both of which demonstrate a stronger effect for status as a predictor of partner reputation. In addition, we reran Model 2 using standardized reputation and status variables and compared the coefficients to see whether status (0.1789) or reputation (0.1185) had a larger effect size. The combination of the results presented in Table 2, together with our additional robustness checks, and the statistical test of the relative predictive power of both variables (reported with our seemingly unrelated regression (SUR) analyses below) suggest strong support for H1 that focal firm status is a more important predictor of the average reputation of the firm’s network partners than focal firm reputation.

H2 predicted that the higher the status of the focal firm, the lower the variance among its network partners, and that focal firm status would predict this negative relationship more strongly than focal firm reputation. In Model 4, where partner reputation diversity is the dependent variable, the coefficient for focal firm status is negative and significant, while the coefficient for focal firm reputation is nonsignificant. These results demonstrate support for H2—while focal firm status predicts a lower level of diversity among the firm’s ego network, reputation has no effect. As an additional test of H2, we reran Model 4 using standardized variables to compare the coefficients of status (−0.498) and reputation (−0.191) in order to measure their relative effects. This result, combined with the significant status coefficient and nonsignificant reputation coefficient in Model 4, provides strong support for H2.

Next, we tested the effects of focal firm status on its ego network brokerage, while controlling for the firm’s reputation. In particular, H3 predicted that higher status firms will have networks that contain fewer opportunities to bridge structural holes than the networks of high-reputation firms. In Model 6 in Table 2, the coefficient for firm status is negative and highly significant, while the coefficient for reputation again is nonsignificant. These results demonstrate strong support for H3 and were replicated when we reran Model 6 using the standardized status and reputation variables. Again, using the standardized variables, the coefficient for focal firm status (−22.50) indicated that it had a significantly stronger effect on network efficiency than the coefficient for focal firm reputation (−5.94).

Overall, these results provide strong support for our theory and hypotheses. Regressing multiple dependent variables on the same set of independent and control variables in separate regressions, however, raises the potential for endogeneity. The extent to which these dependent variables are related conceptually suggests that, at least in part, they are derived from the same processes and likely have correlated error terms. A SUR analysis corrects for the possibility of correlation among the error terms across regressions by analyzing all variables in the models simultaneously (Greene, 1997; Zellner, 1962) and is increasingly being used by management researchers to correct for this potential bias (e.g. Kennedy and Fiss, 2009; McDonald and Westphal, 2003).

We conducted our SUR analysis using PROC SYSLIN in the SAS statistical program, which is a command used to analyze cross-sectional data. At present, SUR models do not accommodate longitudinal estimation with multiple dependent variables in an efficient way. These SUR analyses replicated the results of our initial regressions. Although results gained from running longitudinal data through cross-sectional estimation methods should be treated with some caution, the fact that they replicate our initial analyses gives us confidence that our reported results are robust and that we have adequately accounted for endogeneity across our different dependent variables. In particular, we are encouraged that the test that the status β coefficient is statistically different from zero across models is highly significant (p < 0.001, two-tailed test) with a system weighted R2 of 0.635, while the same test for the reputation variable was nonsignificant (p = 0.5336). In addition, we ran a statistical test of the different predictive powers of status and reputation across all models, with results providing conclusive support for our hypotheses that it is focal firm status that predicts network ties and not reputation (p < 0.001, 0.05, and 0.05, respectively).

One final concern that we wanted to dispel in our analyses concerned the relative complexity of the different measures of reputation and status that we used in this study. In particular, as noted above, several researchers have raised concerns about using the Fortune data to measure the firms’ reputation (e.g. Brown and Perry, 1994; Deephouse, 2000; Fryxell and Jia, 1994). Due to the complex measure of status that we use, Bonacich (1987) centrality, compared to the relatively blunt rankings measure of reputation, we were concerned that this difference was driving our results. In order to address this concern, we conducted a number of robustness checks on our measure of reputation. Specifically, we tested our hypotheses using multiple forms of the Fortune data. In addition to the measure that we report (intraindustry rankings), we also tested our hypotheses using the raw Fortune scores as well as using a dichotomous high-reputation score (Pfarrer et al., 2010). All three measures are used widely in the literature and, while all have associated problems, the fact that our results were consistent across all three measures gives us confidence that our results are robust.

In addition, an important assumption of our statistical analyses is that the Fortune rankings are correlated with the raw continuous data on which the rankings are based (0.811 across our observations) and that the ordinal nature of our reputation measure is not driving the results (e.g. Safón, 2007; Trieschmann et al., 2000). In order to test this assumption, we conducted additional robustness checks with different manipulations of the Fortune data to ensure the validity of our final results. To this end, in addition to the checks reported above (testing the raw Fortune scores as well as the dichotomous measure of high reputation, which suggest strongly that the varied distances between the different ranking levels are not determining the results), we also entered the ranking data as a categorical variable in the regression model (essentially creating dummy variables for each of the 10 levels of the rankings and omitting one category) with unchanged results (see Love and Kraatz, 2009). We also tested our hypotheses by logging the ranked Fortune data. If variance in the distances between ranking levels is driving our results, logging this variable would minimize these distances and, therefore, remove our results (Booth and Chua, 1996). Finally, we tested the linearity of the ordinal data by regressing the reputation rankings (1–10) onto the raw Fortune scores—first, using only observations below 5; then using observations 5 and above; and, finally, using all observations. The magnitudes of the regression coefficients are similar across all three regressions, providing good evidence that the rank scale approximates the behavior of a linear variable. All robustness checks confirmed the underlying results reported above and, as such, give us great confidence that none of the measurement issues related to the Fortune data (in any form) are driving the results of our statistical analyses.

Discussion and contributions

The results presented above constitute a robust test of the theory that status and reputation are independent predictors of interorganizational network ties. Status and reputation, however, are differentially important in key aspects. Primarily, the effects of status are consistently stronger than the effects of reputation in predicting partner characteristics and network structure. In other words, having high status makes good reputation less important as a determinant of tie formation. In particular, high-status firms have networks that are higher in partner quality but are less diverse and contain fewer opportunities to bridge structural holes than the networks of high-reputation firms. These results are important because much of our existing knowledge of the effects of status and reputation has either assumed that these constructs are essentially interchangeable, or has not tested one while controlling for the other. We show that at least in the context of interlock partner selection and resulting network attributes, status and reputation have differential effects that need to be accounted for independently, both theoretically and empirically.

We have presented two arguments in support of these findings. First, due to its more stable, unitary, and relationally based characteristics, status has a stronger influence on network partner selection than reputation, which is less stable, multidimensional, and based more on perceptions of product quality and financial performance. Second, in spite of being at the front of the queue for selection, a position that theoretically enables them to have the widest choice of partners, high-status firms in fact confine themselves to selecting among a narrower range of perceived high-quality firms. Results provide compelling support for our theory, demonstrating that status is a more important predictor of tie formation and that these high-status effects generate networks that are qualitatively different from the networks of high-reputation firms. That this support for our hypotheses is replicated using SUR analyses and multiple robustness checks attests to our confidence in the findings.

These results contribute to the work on reputation and status because, although there is a sizable body of research that has increased our understanding of the separate causes and consequences of reputation and status, work that has helped understand their competing influences is rare (cf. Dimov et al., 2007; Jensen and Roy, 2008). Our results complement those of Jensen and Roy (2008), in particular, by adding to our understanding of the different roles played by status and reputation in the partner selection process. These results also extend our knowledge of the consequences of reputation and status beyond the market focus of much of the prior research in this area (Podolny, 1993, 2005; Rindova et al., 2005; Shapiro, 1983).

These results also make a valuable contribution to the networks literature because, while much work has focused on the outcomes of social networks, we know relatively little about the antecedents of these structures, especially at the firm level of analysis (Brass et al., 2004; Zaheer and Soda, 2009). We tested a theory that high status constitutes a constraint on behavior that results in firms selecting partners from a narrower range than either low-status firms or other high-reputation firms, even though their high status privileges them to select from a wider range of possibilities. We find specific evidence that this is occurring and that network structure emerges from multiple partner choices by firms that aggregate to determine the composition of the entire network.

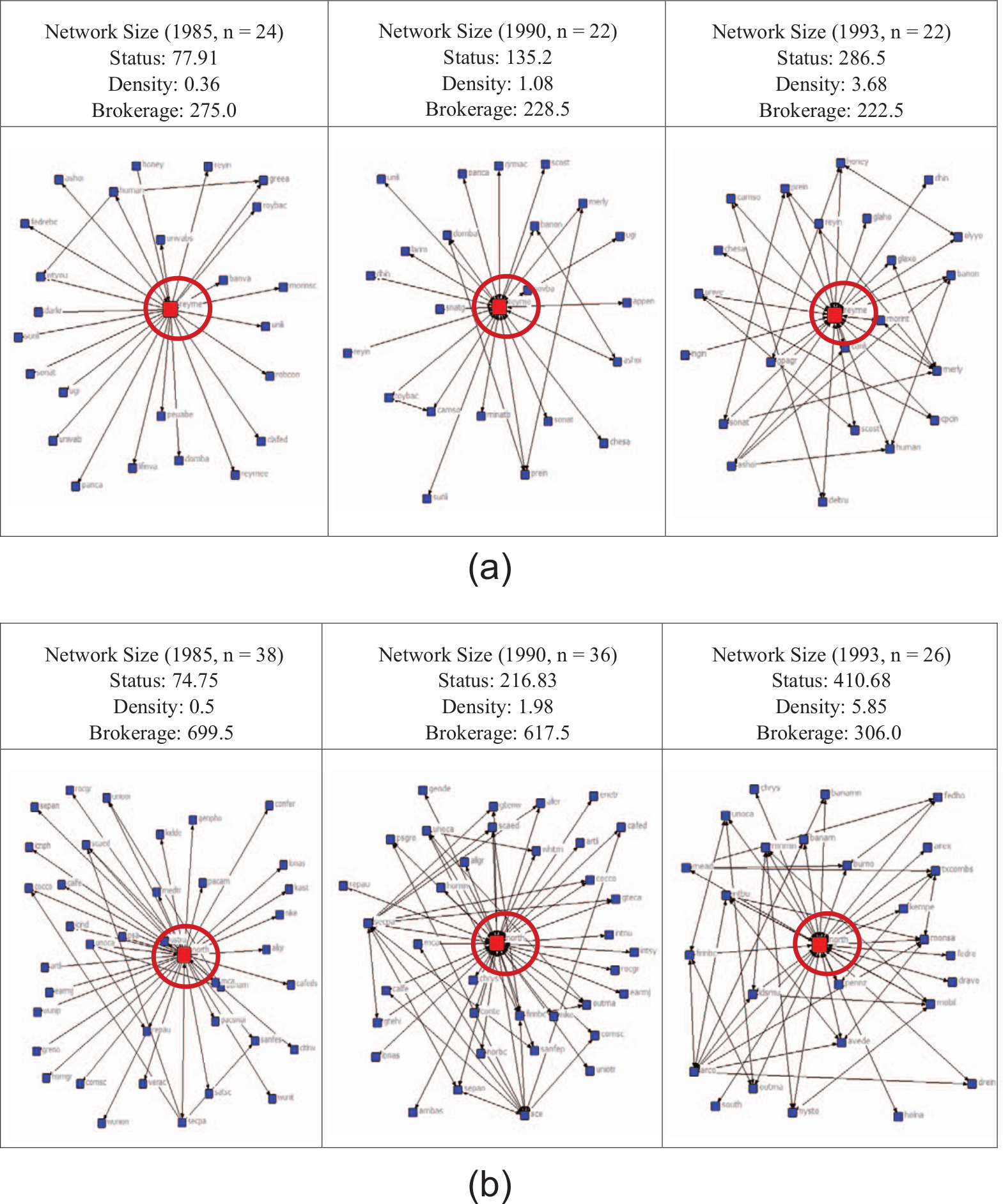

In interpreting these results, it is important to note the dynamic nature of our data—firm status at time t − 1 predicts the change in partner characteristics and network structure from time t − 1 to time t (as we control for prior characteristics and structure using lagged dependent variables). Figure 2(a) and (b) shows the effects of such changes in terms of the relationship between firm status, network density, and brokerage for two firms from our dataset over the period of our study. As can be seen in Figure 2(a) for Reynolds Metals and in Figure 2(b) for Northrop Grumman, as each firm’s status increases from 1985 to 1993, network density increases while the opportunity to bridge structural holes in the network decreases. It is noticeable that the larger the increase in status, the greater the increase in density and the greater the decrease in brokerage opportunities.

The relationship between focal firm status, network density, and brokerage: (a) Reynolds Metalsa and (b) Northrop Grumman.a

The dynamics inherent in our study respond to a call from Zaheer and Soda (2009) for greater understanding in this area of network research. Interestingly, Zaheer and Soda (2009) also examine the relationship between status and network structure and find that status is positively related to the number of structural holes in a network. While, initially, this finding seems to contradict our results that status is associated with dense networks and, thus, reduces brokerage opportunities, we believe that our study complements Zaheer and Soda’s valuable work due to the different kinds of networks studied. Zaheer and Soda studied the temporary networks of the Italian TV industry, where networks are formed and dissolved on a project-by-project basis. In this situation, high-status actors are likely to retain ties that quickly develop into sparse networks as colleagues leave one project and join another. In our situation, the interlocking director ties of the largest 300 US firms, the networks are more stable, with lower turnover and, therefore, different characteristics and structural dynamics.

The differences these two studies identify suggest opportunities for further, much-needed research into how structure emerges, how it varies across networks, and what consequences it contains for firms. Prior research, for example, indicates that the effects of status on tie formation that we identify are detrimental as having fewer diverse partners and fewer structural holes in a network results in reduced information benefits for the focal firm (Burt, 1992). In particular, Beckman and Haunschild (2002) demonstrate the link between partner diversity and decision making by showing that firms with more diverse partners (on various dimensions) make better acquisition decisions than firms with less diverse partners. They argue that this effect occurs because of the learning opportunities afforded to the focal firm by the broader range of information and experience contained within a diverse network.

Our findings that partner reputation diversity is lower for high-status firms and that these firms have denser networks that contain fewer opportunities to bridge structural holes, therefore, suggest that these firms might receive lower levels of unique information from the redundant ties among their partners, which could, in turn, affect performance. It is likely that similar firms with similar characteristics (e.g. status, reputation, profitability, size) find themselves in similar circumstances and, as a result, have similar experiences. As such, high-status firms might be disadvantaged by having a disproportionate number of higher reputation firms in their networks. Thus, in situations where firms turn to their network partners for information and advice, such as when developing strategy (Westphal et al., 2001) or under conditions of uncertainty (Haunschild, 1994), the lower levels of diversity that are likely in the networks of high-status firms suggest that these networks are poorer sources of information than the networks of lower status firms (Beckman and Haunschild, 2002). These findings add to the research that has begun to examine when a good reputation (e.g. Rhee and Haunschild, 2006) and high status (e.g. Bothner et al., 2011) might constitute a liability for the focal firm by identifying the structural implications of high status in terms of the firm’s network. Different network structures serve different purposes in different contexts. It would be useful, therefore, for future research to explore the various contexts in which the network structures we identify in this study are useful to firms and when they are not, and by extension, when a firm’s status or reputation serves as a potential liability.

In addition to our contributions to theory, our study also has practical implications for managers. While we would not advocate managers doing anything other than building the best profiles for their firm in the eyes of external stakeholders, it is important to be aware of the potential negative consequences of certain actions in terms of information diversity. Castellucci and Ertug (2010), for example, demonstrate that there are performance advantages for higher status firms to enter into exchange relationships with lower status firms, but it is not clear that firms are aware of these benefits. Or, at least, it is not clear that they act on this knowledge when selecting partners. On the contrary, our results demonstrate that high-status firms select partners in patterns that form denser networks with less diversity. Firms that are aware of this potential outcome can develop other sources of information to make informed decisions. Alternatively, as high-status firms are in the most advantageous position to select network partners, overcoming the tendency to have dense, homogeneous networks and partner with firms that possess different profiles is another way of bringing information diversity back into the boardroom. These actions, taken with the full knowledge of the consequences of a firm’s network partner decisions, can help managers align their firm’s network structure with its strategic goals.

This discussion leads to one potential limitation of this study—we used the interlock network context. This has advantages in that we know a lot about what goes on in these networks because they are well studied and interlock data can be reliably obtained for publicly traded firms. We recognize the possibility, however, that the interlock network may function differently than other interfirm networks. Alliance networks, for example, could be more functional and designed with specific goals in mind, and thus the relative importance of status and reputation in tie formation may differ from the relationships we found (cf. Jensen and Roy, 2008). We feel that our decision to motivate our hypotheses at a more general network level is valid, however, because the implications of the network structures that result from high status (low levels of information diversity) likely extend to all firms that draw on different kinds of network partners for information in making decisions. Of course, in each case, there may be alternate sources of information that can be consulted and the status of the firm relative to the status of the individual director in the network may not completely correspond and may vary across network forms. It is also possible that there are different kinds of liabilities at different points along the status continuum—lower status firms may benefit from the network structures in the scenario we outline, but perform less well in other board activities such as alliance formation, which is aided by a history of prior network relations and established trust (Gulati, 1995). Exploring these alternative types of networks and how status and reputation affect their structure and information outcomes would be a useful direction for future research.

Related to our use of interlock networks, a second limitation of this study is our reliance on macro-level predictors of tie formation. Prior work demonstrates that individual director characteristics also predict an invitation to join a board (e.g. Westphal, 1999; Zajac and Westphal, 1996). An important assumption of our theory, therefore, is that the characteristics of the individual that are likely to predict selection as a director (e.g. personal reputation, trustworthiness, and ability) are correlated with the organizational-level characteristics that we include in our regression models. We think it is intuitive, for example, that if IBM’s CEO is invited to join the board of another firm, the primary reason for the invitation is that the individual is the CEO of IBM. Of course, this individual would also have many personal characteristics that make him or her attractive as a board member, but these characteristics are likely related to the attractiveness of IBM as a potential network partner. The reason for this is that in order for this person to rise to become CEO of a firm such as IBM, it is intuitive that he or she would necessarily need to have a good reputation, be trustworthy, highly capable, and so on. If true, many of the individual characteristics that make this CEO an attractive director are captured, at least indirectly, in the organizational-level variables we include in our statistical analyses.

A third limitation, arises due to the empirical constraints associated with our measure of status, Bonacich (1987) centrality, which meant we were unable to measure the status of each focal firm’s network partners without engaging in a prohibitively exhaustive data collection effort to construct the complete networks of all the 3400+ partners of our 300 focal firms. As such, we limit our analyses in this article to the relationship between the reputation and status of each focal firm and the reputations of their partners. Of obvious interest would be to look at the status of our focal firm’s network partners and future work that can illuminate this issue would be a welcome complement to the results we present here.

Conclusion

This article contributes to the growing body of work that seeks to understand when status matters, when reputation matters, and when they both matter. By looking at an under-theorized area of the networks literature (structural antecedents) and by drawing on the respective economic and sociological roots of reputation and status to theorize why they cause different network outcomes, we extend research on reputation, status, and interorganizational networks. Outside the partner selection context, we anticipate that other important firm decisions and outcomes are differentially affected by status and reputation. These and similar questions are clearly important and deserving of further study.

Footnotes

Acknowledgements

The authors would like to thank their editor, Tim Rowley, and two anonymous Strategic Organization reviewers for their insightful and constructive guidance throughout the review process. In addition, we would like to thank Gautam Ahuja, Joel Baum, Steve Bovie, Don Lange, Dovev Lavie, Martin Kilduff, and Tim Pollock for their valuable assistance in developing our ideas. Finally, we would like to express our gratitude to the participants of the May 2009 conference on “The Genesis and Dynamics of Networks” at Bocconi University, the participants at the October 2008 conference on “Network Evolution” at INSEAD, and the participants at the University of Michigan and the University of Texas at Austin colloquia, who all contributed helpful comments at various stages in the evolution of this article.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.