Abstract

While the diversification–performance link is well covered in strategy research, we know much less about the link between firm diversification and risk. This article draws from modern portfolio theory and corporate diversification theory to derive a comprehensive set of hypotheses on the impact of related and unrelated diversification on the systematic risk, total risk, and bankruptcy risk of a firm. Based on a large international sample, we find the portfolio effect to be more important than previously thought, while synergy effects appear to be largely counterbalanced by the direct and indirect costs of diversification. Specifically, we find that systematic risk is not reduced by corporate diversification, while bankruptcy risk is significantly lower in diversified firms, possibly leading to conflicts between shareholders and other stakeholder groups.

Keywords

Introduction

The impact of diversification on firm performance is one of the best studied fields within strategic management research (for a summary, see Palich et al., 2000). In contrast, the link between firm diversification and risk has received much less scholarly attention. This lack of interest is surprising, given that diversification might be more about “risk management than returns [or valuation]” (Lubatkin et al., 1993: 447). A deeper understanding of the diversification-risk (DR) link might explain why diversified firms still exist, despite public criticism of the conglomerate model and empirical evidence for diversification discounts in their valuation (Nippa et al., 2011).

In spite of the essentially sound theoretical basis for the relationship between diversification and risk (Hill and Hansen, 1991; Lubatkin and Chatterjee, 1994), several key issues remain unsolved. First, whether diversification yields risk benefits to shareholders is unclear. Theoretical arguments have been advanced both for and against the view that firm diversification reduces risk beyond what shareholders can achieve on their own. Correspondingly, the empirical evidence on the relationship between diversification and shareholder risk is mixed (Barton, 1988; D’Aveni and Ilinitch, 1992; Hann et al., 2013; Hill and Hansen, 1991). Second, diversification’s benefits for other stakeholders have been largely neglected in the literature. To fully comprehend the risk implications of diversification, the research focus needs to be broadened to include more than shareholders and their risk perspective (Ruefli et al., 1999). Similarly, Chatterjee et al. (1999) argue for the use of multiple risk measures to test empirical results for robustness. And third, while both the strategic management and finance literature have contributed important findings on the DR link, these disciplines use distinct concepts of risk and different definitions of diversification, hindering progress toward a more complete understanding of the DR relationship.

In order to address these issues, we develop and test a comprehensive theoretical model of the link between firm diversification and risk. We draw from modern portfolio theory (the finance perspective) and corporate diversification theory (the strategic management perspective) to identify three effects with an impact on the DR link: (1) the portfolio effect from combining not perfectly correlated cash flows, (2) advantages from synergies between the different businesses in the portfolio, and (3) costs of diversification from internal transactions and complexity. By applying these effects to related and unrelated diversified firms, we argue that systematic risk is not reduced by diversification, while total risk and bankruptcy risk can be lowered by corporate diversification. Extensive testing based on a large international sample provides robust empirical support for our hypotheses. Since fully diversified shareholders are mainly concerned with systematic risk whereas managers (and debt holders) also care about total risk and bankruptcy risk, our findings provide an explanation why companies pursue diversification strategies, and indicate that this risk diversification may happen at the expense of shareholders, supporting an assumed agency conflict (Amihud and Lev, 1981; Lane et al., 1998).

Our study yields several contributions to the DR literature. First, we draw from the finance and strategic management literature by combining modern portfolio theory and corporate diversification theory into an overall model of the DR link. Second, we consider different risk types (systematic, total, and bankruptcy risk) that reflect the risk perspectives of different stakeholders to the firm and yield a more differentiated picture of the DR link. And third, we make distinct methodological contributions to the empirical DR literature by employing a broad international sample to test our hypotheses, introducing credit default swap (CDS) spreads as a market-based measure of bankruptcy risk, and applying a number of advanced econometric techniques to account for endogeneity biases in the DR link.

The rest of this article is structured as follows. In section “The DR relationship in the literature,” we briefly discuss what we know about the DR relationship from the extant literature. In section “Risk types and stakeholder perspectives,” we introduce different risk definitions and the corresponding stakeholder perspectives. We derive our hypotheses in section “Derivation of hypotheses.” Section “Data and method” describes our data sample and research methodology. In section “Results,” we present our empirical results, and we conclude our article in section “Discussion and conclusion” with a discussion of our findings, their limitations, and avenues for further research.

The DR relationship in the literature

Diversification research has strongly focused on the relationship between diversification and performance (Nippa et al., 2011; Palich et al., 2000). The DR link has received much less scholarly attention, although diversification is generally hypothesized to have a significant influence on a firm’s risk profile (Lubatkin and O’Neill, 1987; Montgomery and Singh, 1984). Moreover, the field suffers from conflicting theoretical predictions and empirical findings both across and within the finance and strategic management literature streams.

Finance theory traditionally assumes perfect capital markets (e.g. fully rational agents, full information transparency, no transaction costs) and considers corporate diversification as the simple pooling of uncertain cash flows of firms operating in multiple product markets (e.g. Langetieg et al., 1980). A negative link between diversification and risk is predicted due to the “portfolio effect”: the risk of a portfolio of businesses is lower than the sum of the risks of individual businesses because the latter’s cash flows are not perfectly correlated. However, no benefits are assumed to materialize that shareholders could not replicate on their own (Levy and Sarnat, 1970).

By contrast, strategic management research allows for the possibility of (capital) market imperfections such as shareholder-manager conflicts, taxes, bankruptcy costs, and information asymmetries (Aron, 1988; Higgins and Schall, 1975; Jensen and Meckling, 1976). Accordingly, diversified firms can internalize market transactions and force market pressure onto competitors (e.g. through “market power” and “multi-point competition”). This should lead to risk reduction from corporate diversification beyond what can be achieved by shareholders themselves (Beattie, 1980; Helfat and Teece, 1987). By introducing the notion of resource immobility and heterogeneity, strategic management scholars further relax market assumptions and distinguish between “related” and “unrelated” diversification (Barney, 1991; Chatterjee and Wernerfelt, 1988; Rumelt, 1974). They expect a curvilinear relationship between diversification and risk: Related diversifiers should have lower risk than unrelated diversifiers (and focused firms) because they provide more synergy potential (Lubatkin and Chatterjee, 1994). These synergies not only can increase returns but can also extend to risk advantages of related diversified firms (the underlying mechanisms are explained below when we derive our hypotheses).

Empirical findings on the DR link are ambiguous. Some studies have found a negative relationship between the degree of diversification and risk (Amit and Livnat, 1988b; Hann et al., 2013), some have found a curvilinear relationship (Bettis and Mahajan, 1985; Lubatkin and Chatterjee, 1991, 1994), and others have found risk to be invariant to diversification (Bettis and Hall, 1982; Chang and Thomas, 1989).

We believe that these divergent results are mainly due to differences in the underlying risk and diversification constructs and to corresponding measurement problems (Boyd et al., 2005). Furthermore, we maintain that the diverse views of stakeholder groups have received too little attention. The extant DR literature has primarily employed variability risk measures, although stakeholders differ in their risk perceptions, requiring different risk metrics (Jemison, 1987).

Risk types and stakeholder perspectives

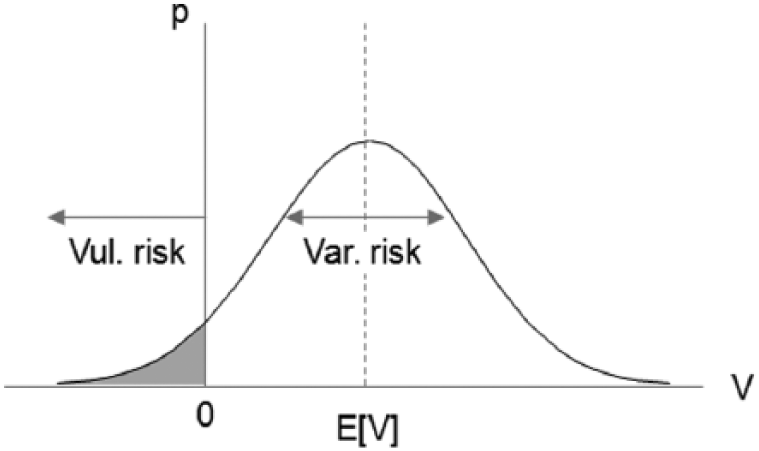

We differentiate between two fundamental risk perspectives: variability risk and vulnerability risk (see Figure 1). The variability perspective focuses on the volatility of firm value within a given time period. It emphasizes the deviation from the expected outcome and does not consider the direction of change. The notion of variability reflects the concept of risk initially employed in Markowitz’s (1959) seminal work on portfolio selection and has become the standard risk definition in finance. By contrast, vulnerability risk is a function of the probability of occurrence and the severity of adverse outcomes (e.g. March and Shapira, 1987) and is a one-sided risk construct. In a corporate context, it can be interpreted as the probability of bankruptcy.

Graphical illustration of variability risk and vulnerability risk.

According to modern portfolio theory and the framework of the Capital Asset Pricing Model (CAPM) (Lintner, 1965a, 1965b; Sharpe, 1964), variability risk has two components: market (systematic) and firm-specific (unsystematic) risk. Systematic risk (or “beta”) is defined as the standardized co-movement of a firm’s returns with the market and thus measures firm sensitivity to general market factors such as changes in interest rates, the regulatory environment, and the activity level in the economy. By comparison, unsystematic risk considers firm-specific risk factors only (e.g. the loss of a major patent, the outcome of a research or investment project, or the default of a key supplier). Unsystematic risk is estimated as the standard deviation of the residuals in the single-factor market model. Total risk is the sum of systematic and unsystematic risk; it assesses the firm’s overall riskiness, measured as the volatility of firm performance.

By contrast, vulnerability risk can be estimated in the corporate context as the probability of firm bankruptcy, often thought of as a “distance-to-default” measure (e.g. March and Shapira, 1987). Bankruptcy is a legal finding that imposes court supervision over the financial affairs of a firm that defaults or is unable to serve its debt. Standard bankruptcy risk measures include Altman’s (1983) z-score in the management literature and interest rate spreads or ratings in finance research (e.g. Blanco et al., 2005).

There is consensus in the literature that the three types of risk are not fully independent. For example, prior studies have found that beta and unsystematic risk, as estimated from the market model, are correlated at 0.43, 0.32, and 0.31, respectively (p ≤ 0.001) (Cannella and Lubatkin, 1993; Lubatkin and Chatterjee, 1994; Miller and Bromiley, 1990; see also Chatterjee et al., 1999). Similarly, Shapiro and Titman (1986) found that an increase in total volatility heightens default probability, and D’Aveni and Ilinitch (1992) could show that systematic and bankruptcy risk are positively correlated because they have common drivers such as a chosen corporate strategy. Despite this correlation, Miller and Bromiley (1990) confirmed by factor analysis that these risks fall onto different factors and should thus be considered as different constructs.

How do these three risk types relate to the risk perceptions of different stakeholders of the firm? Shareholders have residual claims on all excess cash flows of the firm (Merton, 1974) and are directly affected by the volatility of firm value, both positively and negatively. Their risk perspective is thus related to variability. According to modern financial theory, systematic risk is the only relevant risk measure for shareholders because they can diversify all unsystematic risk components and will not be rewarded with higher return for holding any additional other risk (Montgomery and Singh, 1984).

However, this model rests on two main assumptions: (1) perfect capital markets (i.e. fully rational agents, full information transparency, no transaction costs) and (2) well-diversified and rational investors who maximize their expected utility. Both assumptions have been questioned repeatedly throughout the literature. First, transaction costs and taxes challenge the notion of perfect capital markets (Grossman and Stiglitz, 1980; Levy, 1978; Zajac and Westphal, 2004). Second, the assumption of well-diversified and rational investors holds true only for a limited number of investors. Although free in their decision making, investors tend to disproportionately invest in their home markets, not exploiting potential risk diversification from a more international portfolio (French and Poterba, 1991). Some investor groups, such as family owners and firm managers, typically invest a considerable portion of their wealth in a single company and are thus not fully diversified (May, 1995; Miller et al., 2010). Moreover, traits of irrationality and cognitive biases such as overconfidence and overreaction undermine the notion of rational investors and cause investors to hold non-diversified portfolios (De Bondt and Thaler, 1985; Kent et al., 1998). For such shareholders who do not conform to the assumptions of modern financial theory, total risk and bankruptcy risk may also be important reference points (Amit and Livnat, 1989).

Debt holders have a very different perspective on company risk. Creditors assume the risk of default on the loans they made to the firm. This risk can be considered bankruptcy risk because loan default triggers bankruptcy (Altman, 1983). The primary reference for debt holders is thus vulnerability risk. They are less concerned with volatility risk because their claims are predominantly contractually guaranteed; they don’t directly benefit from better-than-expected performance (positive variability) and will depend on negative performance variability only to the extent that it leads to corporate default.

The exact nature of risk that managers should care about is less clear. Bettis (1983) summarized this confusion in his “Conundrum #1: Unsystematic Risk Management” by asking, if “the continuous management of unsystematic risk lies at the heart of strategic management” (p. 408) but “the equity markets will not reward such managerial behavior” (p. 409), then does strategy really make a meaningful difference (Chatterjee et al., 1999)? It seems that managers have a more complex risk perception and should be concerned with all three types of risk. Intuitively, many managers refer to risk primarily as negative outcomes or failure to reach aspired-to performance levels (e.g. Baird and Thomas, 1990; March and Shapira, 1987; Miller and Leiblein, 1996; Ruefli et al., 1999). Their risk perception is asymmetric and focuses on the downside. Managers’ claims against the firm are usually guaranteed by contract and will depend on negative performance variability only to the extent that it leads to corporate default (Merton, 1974). The vulnerability risk perspective is thus much more relevant for managers than for shareholders.

At the same time, managerial interests might be aligned with those of shareholders for several reasons: (1) managers often have a considerable amount of their wealth invested in the firm, (2) well-designed governance mechanisms have been implemented (e.g. incentivizing managers to increase stock prices), and (3) managers perceive themselves as stewards of the shareholders and put the shareholders’ interests first (Donaldson, 1990; Donaldson and Davis, 1991). If one or several of these conditions are met, managers’ reference point for risk will not only be vulnerability risk but also variability risk as reflected in systematic and total risk of the firm.

To summarize, all risk types have some relevance for all stakeholders, but there are certain priorities. Fully diversified shareholders will mainly be concerned with systematic risk because they can diversify away all other risk components. However, less diversified shareholders (e.g. family owners) also care about total and bankruptcy risk because they have a high relative share of their wealth invested in the firm. Debt holders are mainly concerned with bankruptcy risk because default is the only instance when they lose their contractually guaranteed claims against the firm. And finally, managers will be concerned not only with systematic risk but also with total risk and bankruptcy risk. The relative importance of the different risk types depends on their self-perception, incentive schemes, and personal wealth invested in the firm. We conclude from this discussion that it is important to carefully distinguish these different risk perspectives to understand whether diversification actually reduces risk or merely shifts risk between different stakeholders (D’Aveni and Ilinitch, 1992).

Derivation of hypotheses

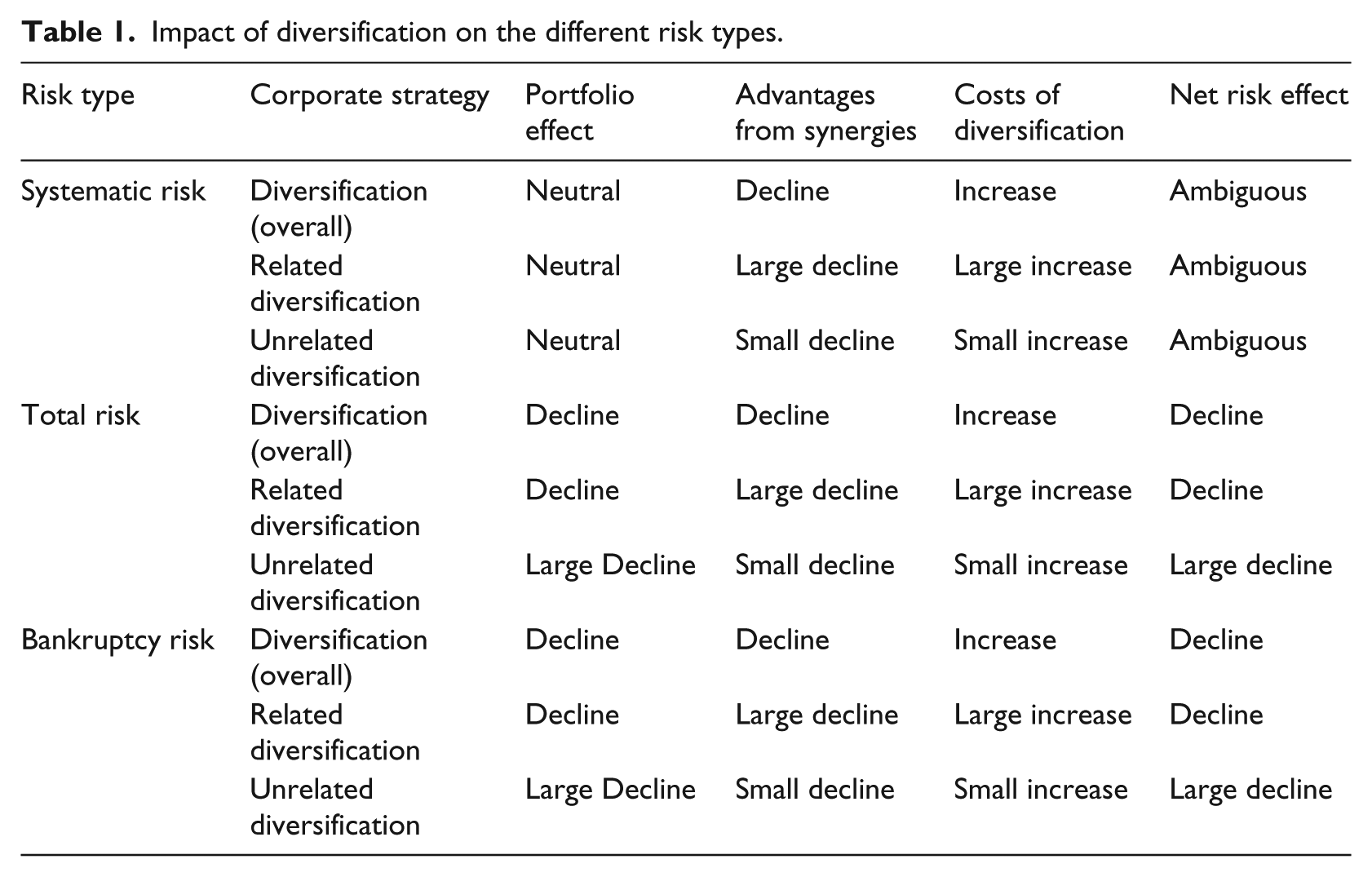

We draw from modern portfolio theory (the finance perspective) and corporate diversification theory (the strategic management perspective) to identify three effects with an impact on the relationship between diversification and risk: (1) the portfolio effect from combining not perfectly correlated cash flows, (2) advantages from synergies between the different businesses in the portfolio, and (3) costs of diversification from internal transactions and complexity. We will discuss each effect in turn before summarizing our hypotheses for the individual risk types (Table 1).

Impact of diversification on the different risk types.

Portfolio effect

From a modern portfolio theory perspective, corporate diversification is similar to financial diversification: A corporate portfolio consists of various business units, not much different from a portfolio of securities (Markowitz, 1959). The business units are exposed to industry-specific market dynamics, resulting in non-perfectly correlated cash flows. Thus, the risk of the entire portfolio is lower than the sum of the risks of the individual businesses.

This argument does not apply to systematic risk, however. According to the assumptions of the CAPM, diversification is a simple pooling of cash flows with no involvement in business management, and the systematic risk of a diversified portfolio is the value-weighted average of the systematic risks of the individual businesses (Levy and Sarnat, 1970). This risk-pooling is also available to shareholders (via securities portfolio diversification) and thus does not yield an additional risk effect (Haugen and Langetieg, 1975; Langetieg et al., 1980). Consequently, diversification neither increases nor decreases systematic risk. The more diversified a firm’s business-unit portfolio, the more the firm’s systematic risk reflects the risk of the market; thus, beta converges toward the “grand mean” of one (Blume, 1971, 1975). 1

However, the portfolio effect of corporate diversification from pooling not perfectly correlated cash flows reduces the unsystematic risk of a diversified company, and thus also its total risk (Lubatkin and O’Neill, 1987). Similarly, this coinsurance effect from corporate diversification will also reduce bankruptcy risk (Lewellen, 1971).

The portfolio effect is largest for firms with the least correlated cash flows. It is therefore more pronounced for unrelated diversifiers because they operate in distinct markets (Kim et al., 1993). On average, unrelated diversification allows firms to better balance adverse firm-specific events, reducing unsystematic risk and thus total risk. Bankruptcy risk will also be lower, on average, in unrelated diversified firms given the lower correlation of cash flows. The effect on systematic risk remains neutral irrespective of the type of diversification.

Advantages from synergies

While modern portfolio theory is based on the premise that cash flows in diversified firms are merely combined but not altered, corporate diversification theory assumes that managers can actively intervene to lower corporate risk, beyond what is possible for shareholders. In particular, diversified firms have more opportunities than focused firms to utilize excess resources internally, thus creating synergies (Penrose, 1959; Porter, 1985). Synergies provide higher cash flows and thus allow firms to better cope with adverse events, lowering their overall risk (Porter, 1985). 2 Beyond this indirect effect, there are also direct risk benefits from synergies because managers of diversified firms can leverage tacit knowledge and past experience across business units. All these factors should reduce firm-specific risks and help the diversified firm to become less dependent on and better react to adverse market fluctuations. Thus, one can expect diversification to have a risk-reducing effect on systematic, total, and bankruptcy risk.

To differentiate the risk impact for related and unrelated diversifiers within the context of corporate diversification theory, a careful analysis of different types of synergies is required. We distinguish between operational, strategic, managerial, and financial synergies.

Operational synergies are based on tangible and intangible interrelations between the businesses, such as common production facilities, shared sales forces, centralized back office functions, and joint brand utilization (Panzar and Willig, 1981; Teece, 1980). These synergies require a certain similarity or relatedness of the operations of the different businesses and are thus more relevant for related than for unrelated diversifiers.

Strategic synergies can be market related and include market power and multi-point competition (Amit and Livnat, 1988c; Montgomery, 1994). But they can also be based on sharing experience and capabilities between businesses with similar strategic challenges and risks. Related diversified firms can thus be expected to be better able to realize these capability-based strategic synergies than unrelated diversifiers.

In contrast to strategic synergies, managerial synergies aim to improve firm performance by financial steering and control through superior corporate processes, organizational structures, and monitoring systems (Hoskisson et al., 1991). They also include risk management capabilities such as early-warning systems, risk reporting processes and policies, and dedicated risk management functions. Managerial synergies are less specific to the underlying businesses and are thus equally available to related and unrelated diversifiers.

Finally, financial synergies provide diversified firms with better or cheaper access to capital, particularly during economic downturns (Kuppuswamy and Villalonga, 2016). Businesses can benefit from lower external financing cost, lower deadweight costs (e.g. by avoiding adverse selection, stakeholder defection, forgone business, or investment distortions when the firm is in financial distress), the tax shield of higher debt levels, and internal capital markets (Hadlock et al., 2001; Hann et al., 2013; Higgins and Schall, 1975). These opportunities are greatest if the businesses in the portfolio have only weakly correlated cash flows. Hence, unrelated diversifiers should be better able to realize financial synergies than related diversifiers.

To summarize, according to corporate diversification theory, related diversified companies should benefit more strongly from risk diversification than unrelated diversified companies. Managerial synergies can be used by both types of firms, and unrelated diversifiers may have some advantages when it comes to financial synergies. However, the exploitation of operational and strategic synergies for risk reduction is more effective if the businesses in the corporate portfolio have a certain relatedness, which puts related diversified firms at a clear advantage.

Costs of diversification

In the diversification-performance literature, costs of diversification are frequently cited to counterbalance the positive performance effects from diversification (Palich et al., 2000). Interestingly, they are rarely discussed in studies that investigate the link between diversification and risk, although some authors used them to explain unexpected empirical results. For example, Chatterjee and Lubatkin (1990) argue that “the weak findings may be attributed to the fact that operational economies are more difficult to implement, since they involve considerable interaction among business units” (p. 265).

Direct costs of diversification are all expenses directly related to the firm’s diversification. They include corporate headquarters costs (Goold et al., 1994) as well as additional personnel and other business-unit expenses for corporate processes, such as corporate planning, budgeting, and reporting (Chandler, 1991). Diversified firms’ greater need for internal coordination might also lead to indirect costs like higher complexity and slower decision making (Jones and Hill, 1988; St John and Harrison, 1999) as well as inefficiencies from inadequate processes and organizational set-ups (Jensen, 1986; Lubatkin, 1983; Markides, 1992).

These direct and indirect costs of diversification will affect not only the value of the diversified firm but also its risk profile. They will reduce the firm’s cash flow and thus decrease its ability to cope with adverse events. More importantly, the expected inefficiencies, complexity costs, and adverse corporate influence will reduce the firm’s ability to manage risk effectively. Thus, we posit that the costs of diversification will exert a risk-increasing influence on all three risk types: systematic, total, and bankruptcy risk.

As discussed above, related diversifiers tend to focus more on operational and strategic synergies (Chatterjee and Lubatkin, 1990) because these require similar operations and strategic challenges, which are not given in an unrelated diversified firm. However, operational and strategic synergies are more difficult to implement since they require closer collaboration between the businesses and a more active corporate parent (Palich et al., 2000). Realizing these synergies will exacerbate the predicted inefficiencies, complexity costs, and adverse corporate influence from diversification. We thus assume that related diversified firms will suffer more from the costs of diversification and their negative effect on the ability to manage risk than unrelated diversified firms.

Summary of hypotheses

Table 1 summarizes the three effects of corporate diversification on systematic, total, and bankruptcy risk. We use it to derive our hypotheses.

Diversification and systematic risk

Modern portfolio theory predicts that the portfolio effect will have no impact on the systematic risk of the diversified firm. Corporate diversification theory claims that synergies should reduce the risk of a diversified company, particularly for related diversifiers. However, this effect will be largely counterbalanced by the costs of diversification, which are also higher for related diversifiers. We assume that synergies and costs from diversification balance to the extent that no significant net effect can be observed, and therefore hypothesize,

Hypothesis 1a: Systematic risk in diversified firms is equal to systematic risk in focused firms.

Hypothesis 1b: Systematic risk in related diversified firms is equal to systematic risk in unrelated diversified firms.

Diversification and total risk

Modern portfolio theory predicts a total risk reduction from diversification through the portfolio effect, which should be particularly large for unrelated diversifiers because they have less correlated cash flows. Corporate diversification theory predicts an additional total risk reduction through synergies; this effect should be largest for related diversifiers because they can better exploit operational and strategic synergies. However, these benefits are largely counterbalanced by the higher costs of diversification for related diversifiers to the extent that the portfolio effect dominates. We therefore hypothesize,

Hypothesis 2a: Total risk is lower in diversified firms than in focused firms.

Hypothesis 2b: Unrelated diversifiers have lower total risk than related diversifiers.

Diversification and bankruptcy risk

Conclusions for bankruptcy risk are similar to those for total risk. The portfolio effect should lead to lower bankruptcy risk for all diversified firms, with higher coinsurance for unrelated than for related diversifiers. Corporate diversification theory predicts an additional bankruptcy risk reduction from synergies that should be larger for related diversifiers, but this effect is again largely counterbalanced by higher costs of diversification to the extent that the portfolio effect dominates. We therefore hypothesize,

Hypothesis 3a: Bankruptcy risk is lower in diversified firms than in focused firms.

Hypothesis 3b: Unrelated diversifiers have lower bankruptcy risk than related diversifiers.

Note that our hypotheses (as summarized in Table 1) suggest that modern portfolio theory dominates corporate diversification theory. However, we do not imply that the advantages from synergies cannot dominate their costs (as it might be the case for related diversification) or vice versa (as it might be the case for unrelated diversification). We only suggest a counterbalancing effect to a degree that modern portfolio theory emerges as the theory with the highest explanatory power for the relationship between diversification and risk.

Data and method

Data sample

We derived our sample by initially selecting the largest 1500 global companies (based on market capitalization), covering the period of 2005–2011. This selection ensures a sufficiently large, international sample from a recent time period. Employing an international sample is very important given the general critique that applying US-based empirical findings to other institutional settings has no theoretical justification (Hoskisson et al., 1999). We collected our firm financials and capital market data from Thomson Reuters and Capital IQ.

We restricted our sample as follows. Financial institutions were excluded given their differences in business model, success metrics, and regulatory environment (Amit and Livnat, 1988c). For double-listed firms, only one data point was included to avoid double-counting. We also eliminated firms for which the sum of their segment sales deviated by more than 5% from their total reported sales as well as firms with invalid Standard Industrial Classification (SIC) codes. Given data availability limitations, the final sample consists of 7306 firm-year observations across 1132 firms. Of these, 2819 were from diversified firms and 4487 from focused firms. Half of the firms are manufacturers, followed by transport and public utility (20%) and trade (16%). One-third is incorporated in the United States, followed by Europe (28%) and developed Asia (22%), mainly Japan.

Variables

The dependent variables in our research represent various types of risk. Diversification is the independent variable. We include a number of control variables to clarify the DR relationship. Each variable employed in our analysis is discussed below.

Variability risk measures

We use two different variability risk measures: systematic risk and total risk. We estimate systematic risk via the standard market model

Vulnerability risk measure

Our measure of bankruptcy risk is the cost of a firm’s CDS. 3 We believe that the use of CDS spreads as a measure of bankruptcy risk yields several advantages, particularly over Altman’s (1983) z-score and corporate bond ratings. First, CDS spreads provide a relatively pure and direct measure of default risk (Zhang et al., 2009), as opposed to commonly used indirect proxies such as financial leverage, cash flow correlations, and excess debt (Berger and Ofek, 1995; Hann et al., 2013; Kuppuswamy and Villalonga, 2016). Second, CDS spreads are market derived and therefore free of managerial manipulations (Palich et al., 2000). Third, they incorporate all changes in market or firm conditions that may have an impact on a firm’s bankruptcy risk (Blanco et al., 2005; Zhu, 2006) and are thus more effective in unraveling the impact of general economic trends than the multi-year averages of risk measures often used in strategic management research (e.g. Lubatkin and Chatterjee, 1991). Fourth, in contrast to Miller and Leiblein’s (1996) downside risk measure based on behavioral theory, CDS spreads also include “unintentional” risks—“risks that can occur that are environmentally determined and result in deviations from managers’ risk preferences” (p. 116). Based on available monthly data, we averaged the CDS spreads across a year to match our annual firm financials data. We performed a logarithmic transformation to account for kurtosis and skewness (Russell and Dean, 2000).

Diversification measures

To incorporate multiple perspectives on diversification, we use a binary as well as a continuous measure of diversification. For the binary measure, we classify firms as either “focused” (those with more than 90% of their sales in their largest Fama-French (1992) segment) or “diversified” (all others).

4

As a continuous diversification measure, we employ Total Entropy DT that quantifies diversification based on the distribution of the firm’s business volume across different product categories and output markets (Jacquemin and Berry, 1979). Specifically, DT is calculated as

Control variables

We include control variables for size, cash flow ratio, leverage, market-to-book ratio, industry, region, and year. Based on the natural logarithm of a firm’s total assets, we control for size to account for size-related effects on risk, such as the greater “safety buffers” of large firms. An operating cash flow ratio (i.e. operating cash flow to total assets) is included because higher cash flows make firms less vulnerable and reduce adverse external effects on them. 6 Merton (1974) predicts that leverage has a positive impact on a firm’s risk profile, particularly default risk. We employ net leverage (i.e. interest-bearing debt minus cash, divided by total assets) to exclude any effects a firm’s liquidity management policy might have on unadjusted leverage (Kuppuswamy and Villalonga, 2016). The market-to-book ratio (based on equity) controls for differences in companies’ valuation levels. Industry dummies are included on a 1-digit SIC code level. To control for differences in the institutional environment of the firms, we follow Hitt et al. (1997) and Wiersema and Bowen (2008) by assigning the firms to one of four regional clusters—Europe, North America, developed Asia, and the “rest of world”—based on where the firm is incorporated. 7 All ordinary least squares (OLS) models contain year dummies to account for year fixed-effects (FE) and contemporaneous correlation (Certo and Semadeni, 2006).

Analysis

We applied a hierarchical multiple OLS regression design using a pooled sample to test our hypotheses. We tested for differences in the coefficients of related and unrelated diversification by introducing an auxiliary variable

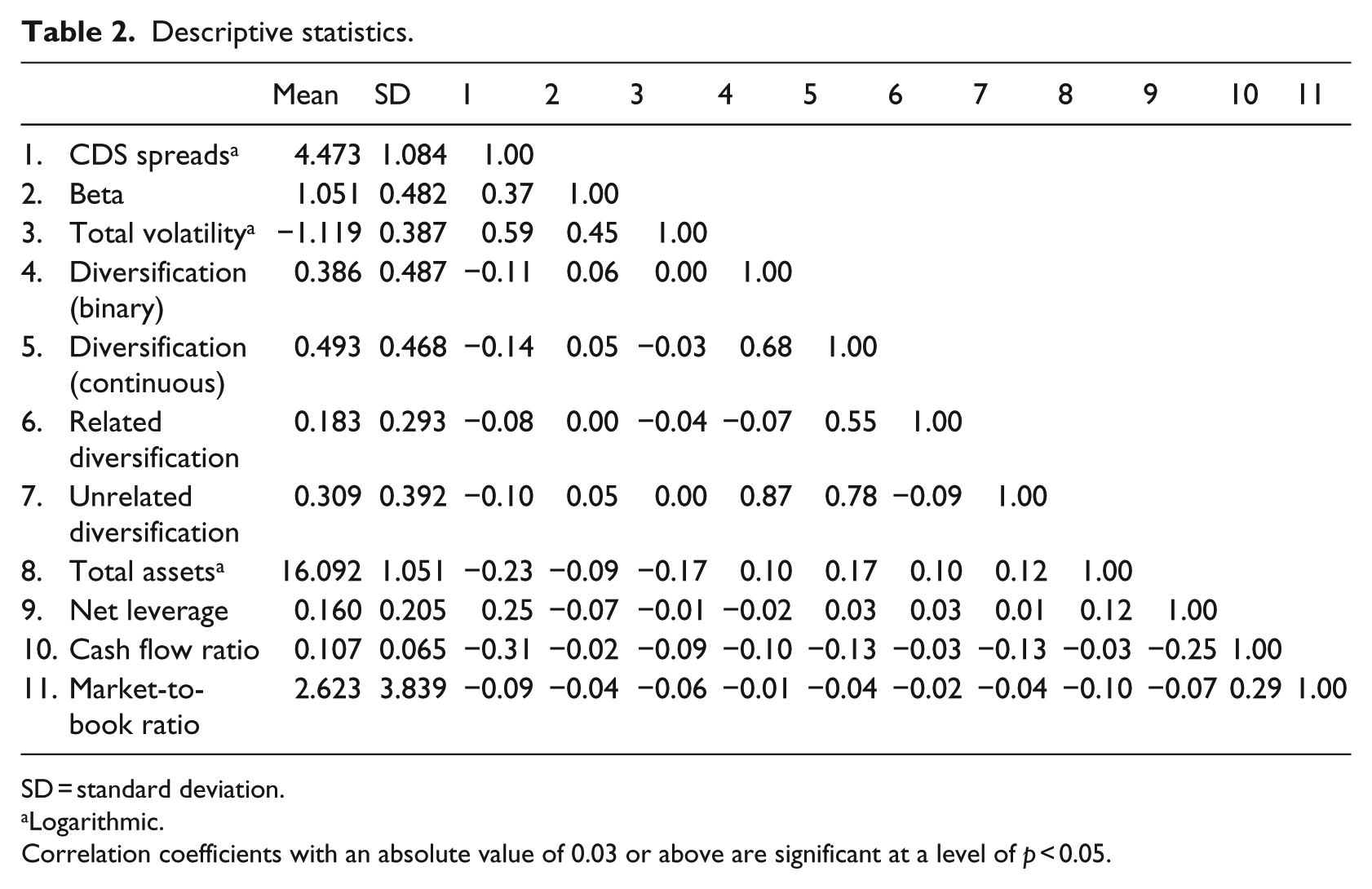

Table 2 provides descriptive statistics of our data set. All variables show adequate dispersion and all correlations between the control variables are as expected.

Descriptive statistics.

SD = standard deviation.

Logarithmic.

Correlation coefficients with an absolute value of 0.03 or above are significant at a level of p < 0.05.

We conducted comprehensive robustness tests of the OLS assumptions. By calculating variance inflation factors, we verified that multicollinearity is not an issue in our sample (Wooldridge, 2009). The vast majority of variance inflation factors was below 2.5 (the highest being 3.41), considerably below the commonly accepted threshold of 10 (Greene, 2011). We further tested for autocorrelation, applying Durbin and Watson’s d (1950), and found no evidence of autocorrelated error terms (d between 1.868 and 1.966 for all models). Finally, we conducted White’s test (1980) and the Breusch-Pagan (1979) test of heteroskedasticity. We found heteroskedasticity to be present across all models. Thus, we calculated Huber-White-corrected robust standard errors.

We estimated FE models to account for unobserved inter-firm heterogeneity and potentially omitted variables, particularly firm-specific effects (Greene, 2011). 8 We verified our approach by conducting a Hausman test and found FE models preferable to random-effect models (p < 0.01 across all models). Within the FE models, we found a strong indication for groupwise heteroskedasticity, using a modified Wald statistic (Greene, 2011). Furthermore, Wooldridge’s (2009) test for autocorrelation in panel data detected autocorrelation. To correct for both issues, we followed Certo and Semadeni (2006) and used an OLS FE method with Huber-White-corrected standard errors.

Finally, we controlled for a potential endogeneity bias. Research on diversification and performance (e.g. Campa and Kedia, 2002; Villalonga, 2004b) found that factors affecting a firm’s decision to diversify also affect firm value. We extend this argument to risk. For example, risk-averse managers might seek to diversify in order to reduce their employment risk. These managers are also more likely to choose low-risk projects in general. Thus, the lower risk found among diversified firms might be attributable to managerial decision making rather than to diversification per se. We employed two econometric techniques to correct for a potential endogeneity bias (propensity score matching (PSM) models with Abadie and Imbens’ (2011) matching algorithm, and instrumental variables (IVs)), as well as Heckman’s two-stage estimators to account for a potential self-selection bias. 9 By definition, all endogeneity bias models rely on a binary definition of diversification. Thus, only Hypotheses 1a, 2a, and 3a can be tested for endogeneity.

Results

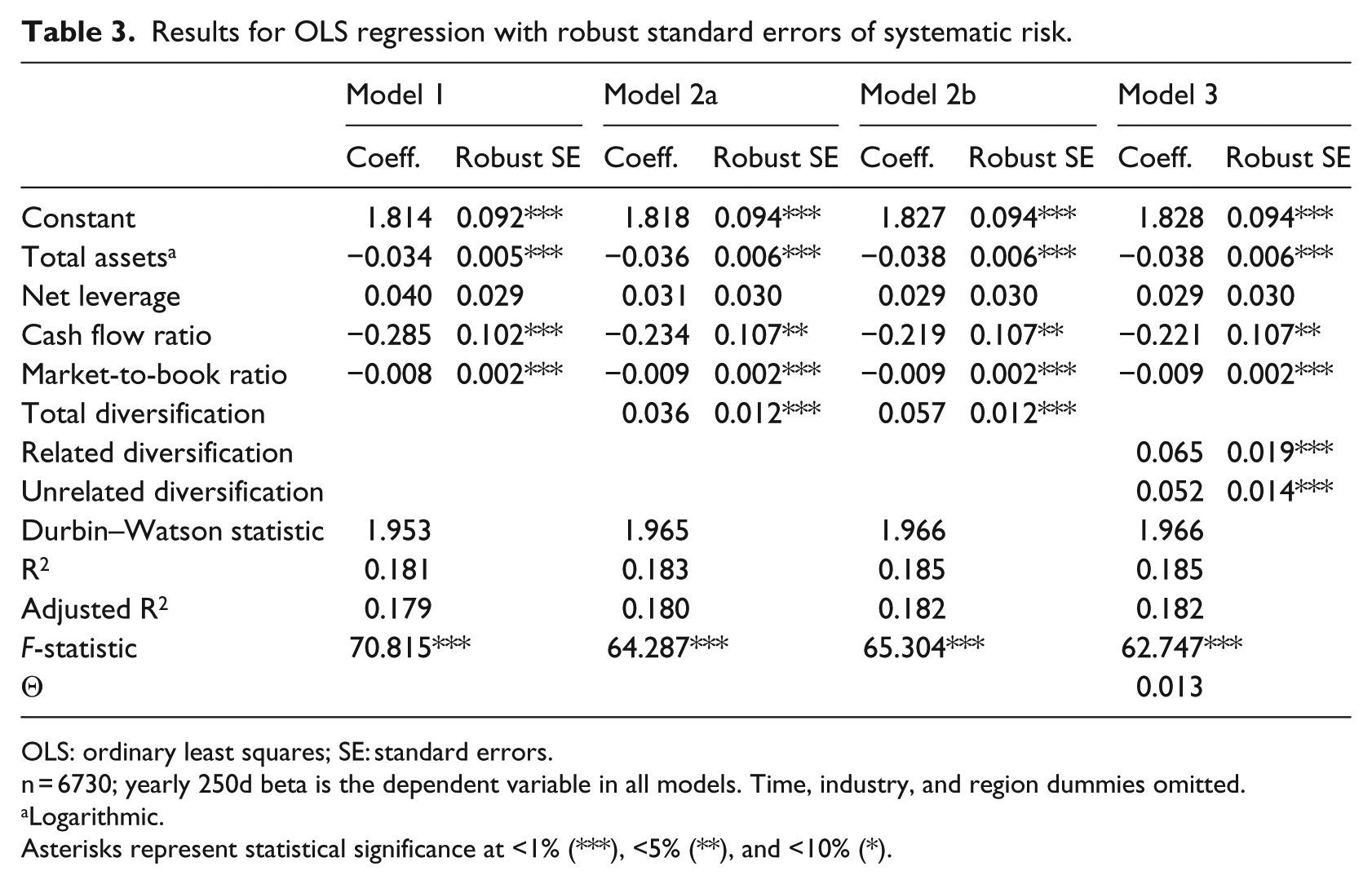

Tables 3 to 5 show the results of the pooled OLS regressions. The dependent variables are systematic risk, total risk, and bankruptcy risk in Tables 3, 4, and 5, respectively. Within each table, we use Model 1 as a control model. In Models 2a and 2b, we add binary and continuous measures of total diversification, respectively, to illustrate diversification’s effect on risk. Model 3 differentiates between related and unrelated diversification. Generally, all control variables yield the expected impact. All models have significant explanatory power.

Results for OLS regression with robust standard errors of systematic risk.

OLS: ordinary least squares; SE: standard errors.

n = 6730; yearly 250d beta is the dependent variable in all models. Time, industry, and region dummies omitted.

Logarithmic.

Asterisks represent statistical significance at <1% (***), <5% (**), and <10% (*).

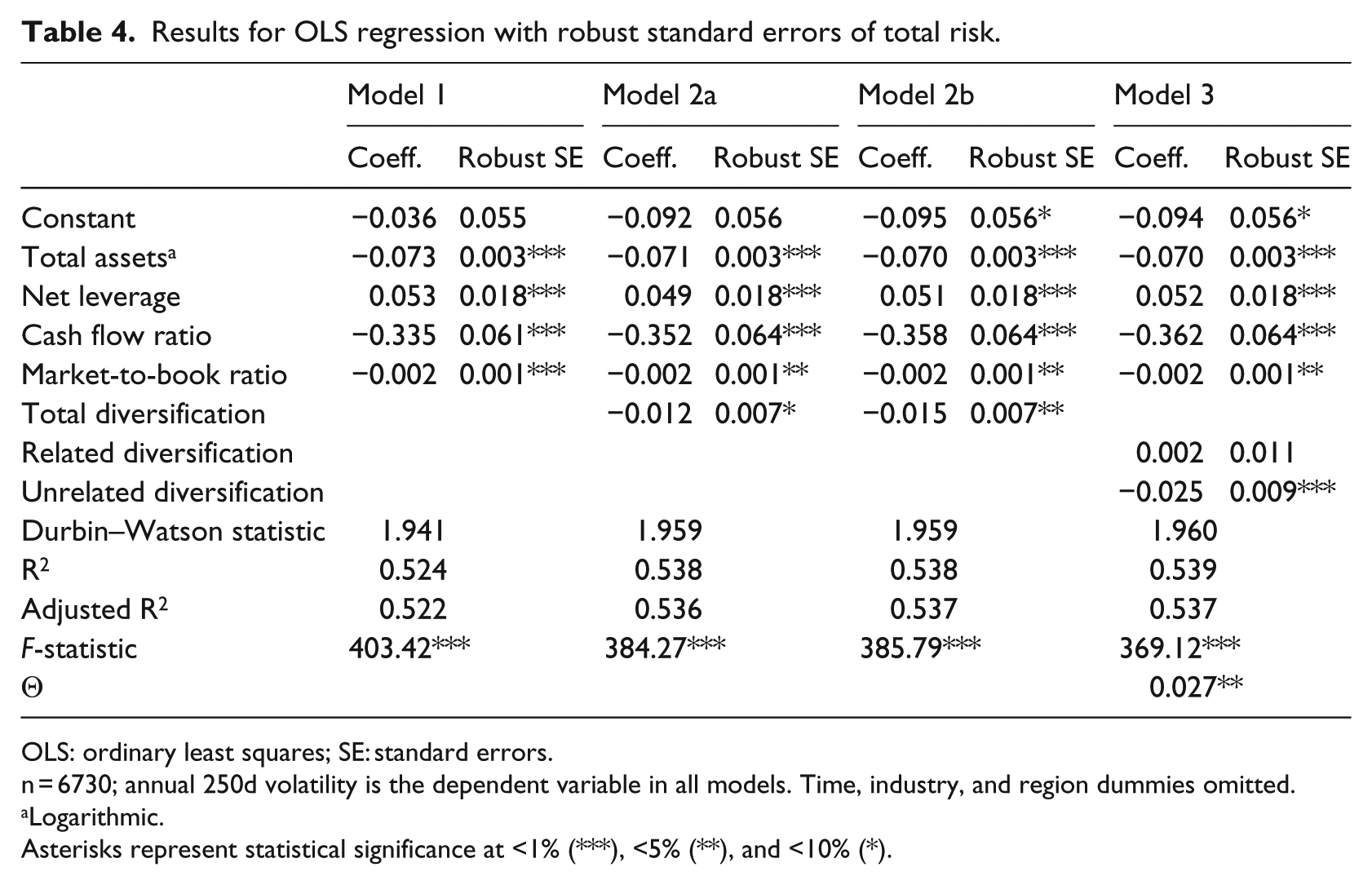

Results for OLS regression with robust standard errors of total risk.

OLS: ordinary least squares; SE: standard errors.

n = 6730; annual 250d volatility is the dependent variable in all models. Time, industry, and region dummies omitted.

Logarithmic.

Asterisks represent statistical significance at <1% (***), <5% (**), and <10% (*).

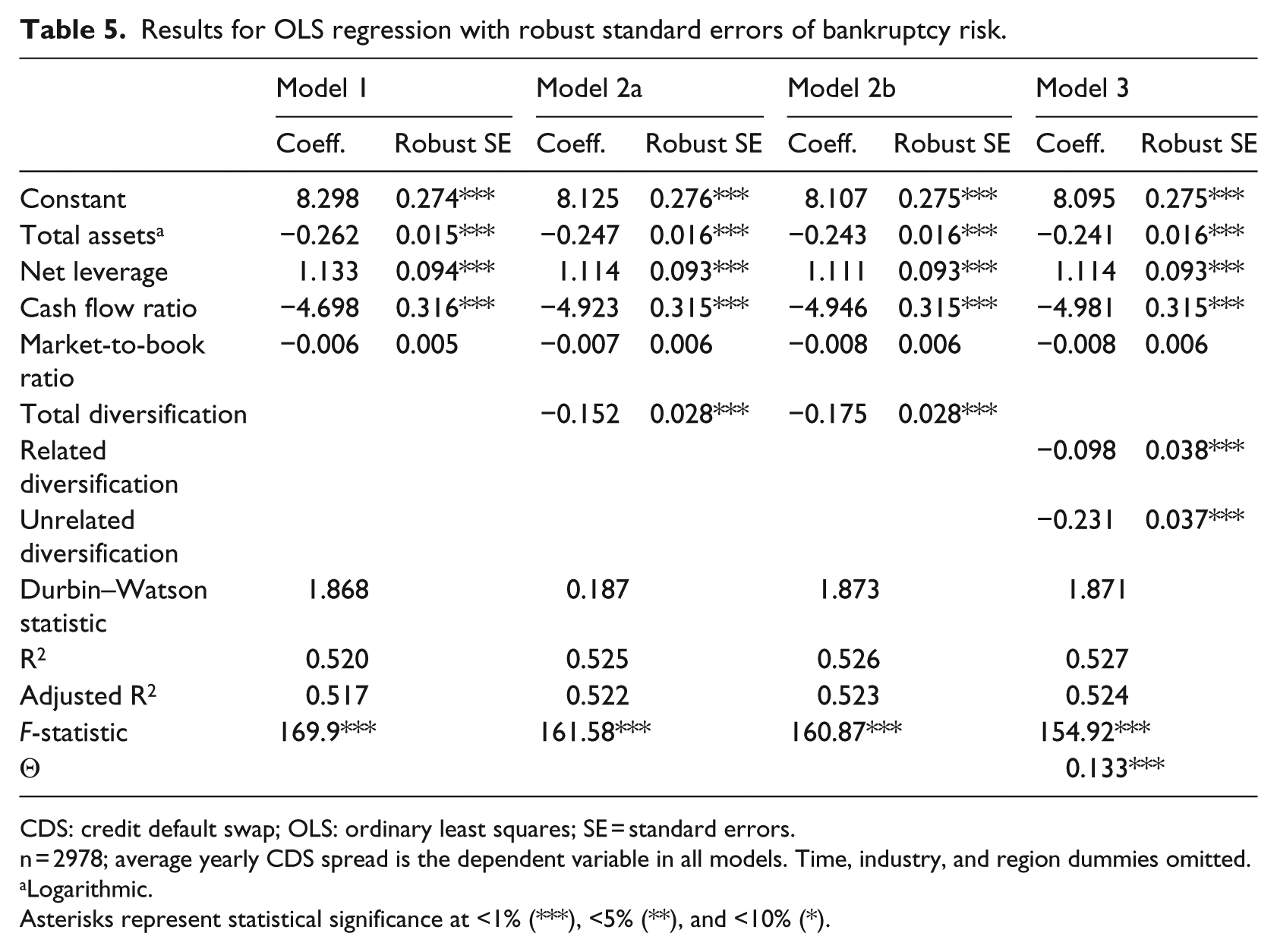

Results for OLS regression with robust standard errors of bankruptcy risk.

CDS: credit default swap; OLS: ordinary least squares; SE = standard errors.

n = 2978; average yearly CDS spread is the dependent variable in all models. Time, industry, and region dummies omitted.

Logarithmic.

Asterisks represent statistical significance at <1% (***), <5% (**), and <10% (*).

Our hypotheses for systematic risk (H1a and H1b) posit that there is no impact of diversification on systematic risk. Hypothesis 1a is rejected in the OLS models since the coefficients are positive and significant for both diversification measures (0.036, p < 0.01 and 0.057, p < 0.01 in Models 2a and 2b, respectively). Model 3 provides support for Hypothesis 1b that there is no difference between related and unrelated diversification because we cannot reject the null hypothesis (a formal test yielded θ to be insignificant) and the statistical power of the model (the probability that it will reject a false null hypothesis) is larger than 0.99.

Table 4 shows that diversification has a negative impact on total risk, supporting Hypothesis 2a (the coefficients of total diversification are negative and significant: −0.012, p < 0.1 and −0.015, p < 0.05 in Models 2a and 2b, respectively). The coefficient for unrelated diversification is negative and significant (−0.025, p < 0.01), while positive and insignificant for related diversification (0.002, p > 0.1). We validate this observation with a formal test (θ positive and significant at p < 0.05). This yields support for Hypothesis 2b.

Table 5 shows the empirical support for the predicted negative relationship between diversification and bankruptcy risk, consistent with Hypothesis 3a (the coefficients of total diversification are negative and significant: −0.152, p < 0.01 and −0.175, p < 0.01 in Models 2a and 2b, respectively). In line with Hypothesis 3b, we find that unrelated diversification yields a greater reduction in bankruptcy risk than does related diversification (θ = 0.133, p < 0.01).

We employed a three-fold robustness check: (1) replacing variables with substitutes, (2) employing FE models, and (3) using advanced econometric techniques to correct for a potential endogeneity bias. First, we replaced the entropy diversification measures with the Herfindahl index and the Concentric index (Montgomery, 1982; Montgomery and Hariharan, 1991). Using multiple measures has been considered sound, following the face validity debate regarding diversification measures (Robins and Wiersema, 2003). Moreover, we replaced CDS spreads with corporate bond ratings. We also used alternative control variables, replacing total assets with revenues and cash flow ratio with earnings before interest, tax, depreciation, and amortization (EBITDA) margin. Across all tests, we found results (not reported here) consistent with those from pooled OLS, confirming our conclusions.

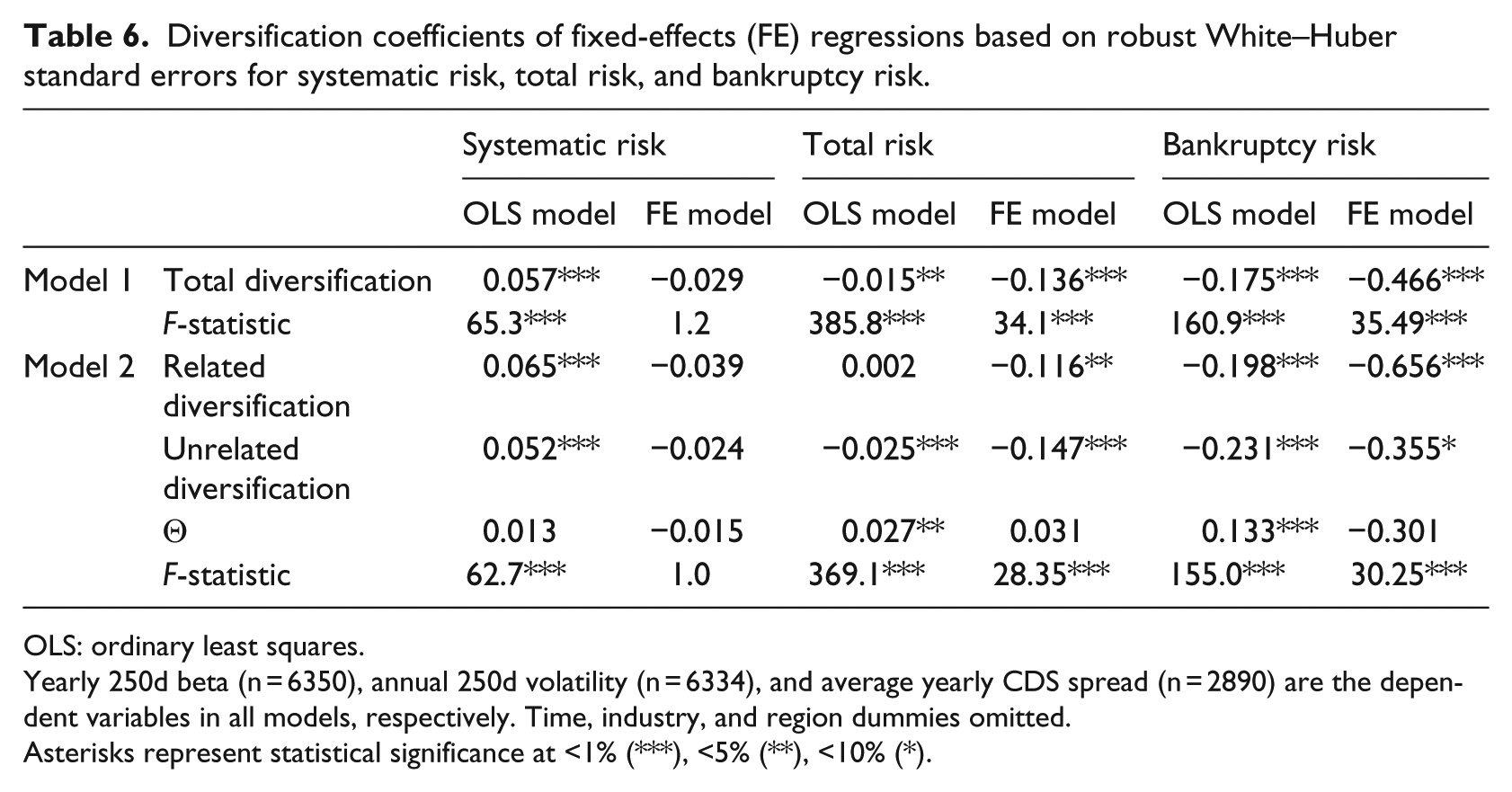

The results of the FE models also largely confirmed the findings of the pooled OLS regressions (see Table 6). However, the FE models no longer reject Hypothesis 1a; we find no significant impact of diversification on systematic risk. The observed increase in systematic risk found in the pooled OLS research design appears to be caused by firm heterogeneity. The high statistical power of the model (the probability that it will reject a false null hypothesis is larger than 0.99) provides support for Hypothesis 1a. Hypothesis 1b is also supported by the FE model; there is no significant difference in the impact of related and unrelated diversification on systematic risk (a formal test yielded θ to be insignificant and the statistical power of the model is larger than 0.99). The OLS finding that total risk is negatively correlated to diversification is corroborated by the FE models. The effect appears to be even stronger than in the pooled OLS model. Both related and unrelated diversification have a significant and negative relationship to total risk. The difference found in the OLS model cannot be confirmed with a formal test, undermining the original support for Hypothesis 2b. The FE results for bankruptcy risk are consistent with the OLS results: The negative link can be confirmed and appears to be stronger than in the pooled OLS model. The differences initially found between related and unrelated diversification cannot be confirmed.

Diversification coefficients of fixed-effects (FE) regressions based on robust White–Huber standard errors for systematic risk, total risk, and bankruptcy risk.

OLS: ordinary least squares.

Yearly 250d beta (n = 6350), annual 250d volatility (n = 6334), and average yearly CDS spread (n = 2890) are the dependent variables in all models, respectively. Time, industry, and region dummies omitted.

Asterisks represent statistical significance at <1% (***), <5% (**), <10% (*).

Based on the tests described above (i.e. PSM, IVs, and Heckman’s two-stage estimators), endogeneity as well as self-selection appear to be present within our sample (not reported here). While we could only test this for hypotheses H1a, H2a, and H3a, similar issues may be present in the corresponding hypotheses Hxb. However, these effects do not generally invalidate our findings. Systematic risk is significantly higher in diversified firms across all tests. The findings on diversification and total risk are more ambiguous. The negative effect found in the OLS model dissolves in all tests of self-selection. We thus fail to derive robust empirical evidence for Hypothesis 2a. However, the negative relationship between diversification and bankruptcy risk holds across models and econometric techniques, supporting Hypothesis 3a. Our findings highlight the need to explicitly account for endogeneity and self-selection biases in the DR context.

Discussion and conclusion

This article draws from the finance perspective (modern portfolio theory) and the strategic management perspective (corporate diversification theory) to identify three effects with an impact on the relationship between diversification and risk: (1) the portfolio effect from combining not perfectly correlated cash flows, (2) advantages from synergies between the different businesses in the portfolio, and (3) costs of diversification from internal transactions and complexity. We apply these effects to derive a comprehensive set of hypotheses on the impact of related and unrelated diversification on the systematic, total, and bankruptcy risk of a firm. Based on a large international sample, we find robust empirical support for several of our hypotheses. Specifically, we find that systematic risk is not reduced by corporate diversification, while bankruptcy risk is significantly lower in diversified firms. We could not confirm a negative effect of diversification on total risk, after controlling for unobserved inter-firm heterogeneity and potential endogeneity and self-selection bias.

Our empirical findings are in line with earlier studies that investigated individual risk types, for example, Barton (1988), Langetieg et al. (1980), and Chang and Thomas (1989) for systematic risk; Amit and Livnat (1988a, 1988c) and McDougall and Round (1984) for total risk; and Borghesi et al. (2007) and Singh et al. (2003) for bankruptcy risk. However, rather than studying the different risk types in isolation, our research integrates these various perspectives and provides a comprehensive and consistent view of the relationship between diversification and risk.

Our results are in contrast to the seminal work of Lubatkin and Chatterjee (1994) on the extension of modern portfolio theory into the domain of corporate diversification. In contrast to these authors, we find that the portfolio effect dominates the DR link, which we interpret as existing synergies being, on average, largely counterbalanced by the corresponding costs of diversification. In this way, our findings add to corporate diversification theory that has largely neglected the risk impact of the costs of diversification. Our results also confirm the importance of methodological diligence (large international sample, FE models, tests for endogeneity, and self-selection biases) that was previously called for in strategic management and particularly in diversification research (Boyd et al., 2005; Lane et al., 1998; Villalonga, 2004b).

This article underlines the importance of distinguishing different risk types, as postulated in prior studies of the DR link. Systematic risk, total risk, and bankruptcy risk are not fully independent, but should be treated as distinct constructs. Our results confirm that these three risk types are influenced in different ways by corporate diversification. This is important because different stakeholders will put different weights on the individual risk types. We conclude that fully diversified shareholders with their focus on systematic risk don’t benefit from risk diversification, while they may suffer from negative value effects from (unrelated) diversification. This can lead to an agency conflict with managers and a wealth shift to debt holders who seek diversification to reduce bankruptcy risk. Moreover, less diversified shareholders, for example, family owners with a high share of personal wealth invested in the firm, might also support diversification to reduce bankruptcy risk, which points to an additional type II agency (or principal-principal) conflict (Gomez-Mejia et al., 2001) that was not addressed in the prior DR literature.

These findings have substantial practical implications. They demonstrate that risk management can be a valid motive for corporate diversification, at least to the extent that bankruptcy risk is concerned. At the same time, they indicate the need to protect fully diversified shareholders from managers who might seek private benefits from risk diversification (Amihud and Lev, 1981; Lane et al., 1998). Interestingly, traditional incentive instruments for aligning manager and shareholder interests, for example, stock-based compensation, may not be sufficient because the higher the equity share of a CEO in his or her firm, the larger his or her interest in risk diversification at the expense of (fully diversified) shareholders. For example, May (1995) could show that CEOs tend to pursue risk-reducing acquisitions when they have higher levels of personal wealth vested in firm equity. In addition, our results also call for sound governance mechanisms to address conflicts between diversified and less diversified shareholders when it comes to corporate diversification.

We must acknowledge some limitations, which we tried to address. To cover the most recent possible time period, our sample includes data from the 2008–2009 financial crisis. This may lead to distortions, which we tried to minimize by including year dummies as control variables as well as by re-running our analyses without the crisis data (with results consistent with the reported ones). Our sample might also suffer from self-selection bias because companies need to have bonds outstanding to have CDS contracts. Being active in capital markets might require a certain level of management sophistication and skill. Consequently, firms with a CDS might systematically be better managed and thus less risky. As a robustness check, we re-ran the regression for systematic and bankruptcy risk with a CDS dummy (not reported here). Although the dummy variable is significant, the reported effects could all be confirmed. Furthermore, diversification as such might be endogenous (Villalonga, 2004a, 2004b). As described above, we use treatment effect models and FE models to account for self-selection biases and adjust our conclusions accordingly.

Other limitations of our study could be addressed by future research. We suggest four avenues. First, our assumptions about the advantages of synergies and the costs of diversification for managing corporate risk were not explicitly tested and remain somewhat speculative. Similarly, while we draw conclusions about the impact of diversification on the different stakeholders of the firm based on their different risk perspectives, we could not provide direct empirical evidence for their specific risk preferences. Both could be the focus of future research. Second, the stability of the DR relationships that we found should be tested over time, especially during economic upturns and downturns. If corporate diversification is considered as an instrument to “insure” the company against bankruptcy risk, this risk advantage should be best observable in times of economic crisis. The financial crisis of 2008–2009 may serve as a “natural experiment” to study the benefits of diversification in such an out-of-equilibrium situation (Kuppuswamy and Villalonga, 2016). Third, Khanna and Palepu (1997) and Chakrabarti et al. (2007) emphasize the importance of cross-country differences in the context of diversification and performance. We suggest that institutional differences, such as the sophistication and utilization of capital markets and shareholder protection rights, will also impact the DR link and require closer investigation. And fourth, the role of governance practices should be analyzed in more detail. Our findings indicate that the risk benefits from synergies in the average diversified firm are largely counterbalanced by the corresponding costs of diversification, particularly for related diversifiers. It would be valuable for boards and managers to better understand which governance practices (e.g. board involvement in portfolio decisions, outside board directors, information transparency to shareholders) are most effective in reducing the costs of diversification in order to increase its net risk benefit.

In the strategic management literature, studies on the link between diversification and risk always stood in the shadow of research on diversification and performance. We hope that our study has demonstrated that the risk perspective can help explain the prevalence and benefits of corporate diversification and understand the different stakeholder conflicts that are related to its implementation.

Footnotes

Acknowledgements

We thank Kulwant Singh for constructive comments to an earlier version of our article. An earlier version of this article was part of the first author’s dissertation project (with Ulrich Pidun und Dodo zu Knyphausen-Aufseß as co-authors also of this earlier version of the article). We did not receive specific grants for this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.