Abstract

By bridging literature on resource partitioning and markets for technology, this article proposes that companies that pursue a broad (focused) product strategy buy more (less) technology in the market but sign fewer (more) deals as technology suppliers. Furthermore, an alignment between product and technology market strategies increases firms’ survival chances: Companies that pursue a broad (focused) product strategy are more likely to prosper when they buy (sell) technology in the market. To test these contentions, the authors consider a population of 736 firms that entered the security software industry between 1989 and 2002.

Introduction

Robust evidence documents increasing levels of concentration coupled with rising organizational density in various industries (Carroll and Swaminathan, 2000; Dobrev et al., 2002; Hannan and Freeman, 1989; Klepper and Thompson, 2006; Mezias and Mezias, 2000; Sutton, 1991). To explain this empirical regularity, researchers have turned to dual market structures (Boone and van Witteloostuijn, 2004) and proposed that large, generalist firms occupy a concentrated, competitive center by making products or services with broad appeal whereas specialist organizations thrive on the industry’s periphery by focusing on a small range of specific customer tastes (Swaminathan, 2001). Resource partitioning theory assumes that, within a population, competition affects both the degree of specialization and the survival chances of organizations (Soule and King, 2008), such that it creates indirect interdependences between generalists and specialists. For example, market concentration among generalists increases the rate at which new specialist firms are founded and lowers their mortality rate (Carroll and Swaminathan, 2000; Freeman and Lomi, 1994). However, to date, researchers have paid relatively little attention to the empirical and theoretical nature of direct relationships between generalists and specialists (Freeman and Audia, 2006; Negro et al., 2014). This gap might not seem surprising, as generalists and specialists tend to develop heterogeneous codes and routines that govern their behaviors in different strategic domains, resulting in different identities that do not combine easily (Giarratana and Fosfuri, 2007; Sorenson et al., 2006).

This article posits that a company’s position in the industry resource space, which is the outcome of the underlying partitioning process, also provides incentives to trade some firm proprietary resources, thereby creating a direct, market-mediated link between horizontal subpopulations. Adding such a link allows us to make a more thorough assessment of how competition and resource partitioning affect industry evolution and firm survival (Audia et al., 2006). Specifically, we analyze an industry in which key firm inputs/resources embedded in final products could be traded separately. One such input is disembodied technology, which is usually considered a key driver of competitive advantage (De Figueiredo and Silverman, 2012). Moreover, technologies can be productively employed in noncompeting applications and/or contexts (Arora and Gambardella, 2010; Gans and Stern, 2010), which relaxes constraints on their trade.

We draw on a population of 736 firms that entered the security software industry (SSI) between its inception in 1989 and 2002. As a relatively recent segment of the software industry, SSI offers a sound study context for several reasons. First, while the majority of SSI customers are medium- to low-tech firms that demand comprehensive security packages, there are buyers that seek state-of-the-art security solutions. This distribution of security software users (a relevant resource space in this industry) facilitates the emergence of two types of industry players: specialists and generalists. Generalists address the bulk of industry demand by offering one-stop-shop software packages, while specialists focus on (niche) customers that require technological solutions to specific problems. Second, SSI encompasses an active technology market: approximately 15% of revenues come from licensing, according to Hoover data (www.hoovers.com). Our analyses show that there is a positive association between being specialists (generalists) and selling (acquiring) disembodied technology. We also find that a fit between a firm’s product strategy and its technology market strategy is associated with a lower mortality hazard.

This study proposes two contributions to current literature. First, although canonical ecology researches have investigated how the fates of generalists and specialists are linked through indirect competitive processes (Dobrev et al., 2001, 2002; Lomi, 1995; Soule and King, 2008), studies to date have put little emphasis on direct ties (Negro et al., 2014) between organizational populations (see Freeman and Audia, 2006), except when they span vertically related industries (Audia et al., 2006; De Figueiredo and Silverman, 2012). In this article, we develop a theory that links the process of resource partitioning to the exchange of firm resources between different types of organizations. Specifically, we are able to investigate how a firm’s position in the product space, which is the outcome of resource partitioning, is related to its strategy about the trade of disembodied technological resources.

Second, current literature (Arora and Gambardella, 2010) indicates as antecedents of firms’ decisions to participate in markets for technology the lack of complementary assets (Teece, 1986), the establishment of technology standards (Garud and Kumaraswamy, 1993), the competition among licensors (Arora and Fosfuri, 2003), and patents and market fragmentation (Cockburn et al., 2010; Gambardella and Giarratana, 2013). We contribute to this literature, by studying the linkage between a firm’s position in the product space and its decision about participation in the market for technology. Specifically, product-market choices, that is, whether a firm is a generalist or a specialist, generate unique routines, behaviors, and market identities, which constrain how a firm can make use of technologies. Interestingly, our empirical evidence suggests that firms that do not account for these trade-offs might suffer from reduced performance.

Theoretical background

Assumptions

Our theory rests on three industry-specific assumptions. First, we make the standard assumption in resource partitioning literature of a unimodal resource environment with a clear market center, in which the bulk of the demand falls, and a periphery, characterized by greater segmentation (Boone and van Witteloostuijn, 2004; Carroll, 1985). Second, we assume high demand for standard products and fringe demand for specialized products, for which the perceived value also depends on identity considerations. Finally, we restrict our study context to sectors in which some resources embedded in final products (e.g. the underlying technology) could be disembodied and traded. Research on markets for technology (Arora et al., 2001) has shown that technology transactions are more widespread in industries with a codified underlying knowledge base, few interdependencies across different production stages, and effective patents for protecting innovations (Arora and Ceccagnoli, 2006)—such as biotechnology, chemicals, software, and semiconductors. Therefore, entry into a downstream product market does not necessitate that technological capabilities are internally developed; rather, they can be accessed through arm’s-length arrangements.

Dual market structures: generalists versus specialists

Resource partitioning theory (e.g. Carroll and Swaminathan, 2000) asserts that in the presence of unimodal heterogeneous resource distribution with a clear market center, organizations secure positions in dense, central resource spaces by creating products or services with broad appeal. These firms, called generalists, establish their identities and compete on the basis of scale and scope economies and overall efficiency (Boone and van Witteloostuijn, 2004; Carroll and Swaminathan, 2000). Competition and concentration among generalists increase the viability of other organizations (i.e. specialists) on the periphery (Hannan and Freeman, 1977; Negro et al., 2014), because they establish opportunities to create and occupy viable niches that generalists cannot reach (Kim et al., 2003). Specialist organizations rely on a narrow resource space and appeal to a small range of specific customer tastes; the underlying selection process thus separates the organizational population (Boone et al., 2000; Carroll, 1985), which leads to a dual market structure. The two subpopulations develop different identities and experience, which attenuates direct competition. For example, organizational identity features influence consumers’ decisions to buy specialty beer rather than large, mass-market beer (Carroll and Swaminathan, 2000).

Scholars formally distinguish generalists from specialists according to the breadth of the markets in which they participate. For instance, Freeman and Hannan (1983) coded restaurants as being generalists if they offered a relatively broad menu, Baum and Singh (1994) defined day-care facilities as being generalists if they served a broad range of children ages, Dobrev et al. (2001) used instead the range of engine sizes to identify generalists in the automobile industry. A firm’s product strategy thus offers a tangible reflection of its underlying organization type. In addition, specialists and generalists are governed by different codes, routines, and organizational capabilities (Sorenson et al., 2006). Specialists develop routines, identities, and reputations that are idiosyncratic to a particular market, which creates barriers that prevent them from migrating to other, potentially attractive product markets. By contrast, generalists use resources to cope with a broader spectrum of customer demand, so they must develop and rely on heterogeneous routines and capabilities. They tend to be governed by routines that make expansion and diversification easier (Boone and van Witteloostuijn, 2004).

We acknowledge that some scholars have operationalized generalists with large firm size (see Carroll, 1985). For instance, Swaminathan (2001) identified specialist wineries as those producing small quantities, but high quality, while he labeled the large, mass producers, generalists. In this article, we prefer to follow Sorenson et al.’s (2006) approach to employ a product-range definition of niche width because it fits better the specific features of our study context, the SSI.

Interorganizational relationships

Traditionally, resource partitioning research has focused on the level of the industry and the corresponding indirect interdependencies between generalists and specialists that derive from competitive processes (Freeman and Audia, 2006). Several scholars have found positive relationships between the extent of competition among generalists and the entry rates and survival chances of specialists (Lomi, 1995; Negro et al., 2014; Soule and King, 2008). Research at the crossroads of ecology and network theory (e.g. Audia et al., 2006; Freeman and Audia, 2006) also analyzes symbiotic and commensalistic linkages. Symbiosis occurs when complementarity in organizational actions is present, such as in vertical relationships between a focal industry population and its buyers or suppliers. De Figueiredo and Silverman (2012) show that the viability of laser printing firms increases if the density of their supplier population increases as well. By contrast, commensalism arises when two subpopulations deal with the same customers or suppliers, so they can voluntarily or involuntarily share important information related to taking advantage of business opportunities (Audia et al., 2006).

Less attention has been placed on the more direct collaborative relationships among subpopulations. We focus on the market exchange of technological assets; in industrial settings characterized by the assumptions we outline, these assets are necessary to achieve successful products, but they can also be disembodied from the products themselves. It is worth noting here the two levels of analysis: the partitioning of industry resources is linked to the trading of firm proprietary resources. Therefore, we first show how positions in the product space (generalists vs specialists) drive firms’ behaviors in the technology space (selling vs buying disembodied technology) and then focus on how the consideration of technology trade affects their respective survival chances.

Hypotheses

Supply side of the market for technology

To sell technology on the market, a focal firm must possess technological assets and have the proper incentives to trade them. We explore both conditions for specialists and generalists. Specialists tap the niche demand for customized and technologically sophisticated products that generalists leave unsatisfied, and they often serve the high end of the market, as witnessed for example in the microprocessors industry (Wade, 1996). Thus, they gain legitimacy, establish an identity, and increase their survival chances (Carroll and Swaminathan, 2000) by building technological expertise and maintaining products highly customized to the needs of their niche customers. For instance, in SSI, a firm that specializes on antivirus software is unlikely to attract any interest by potential customers unless its products offer superior performance on some dimensions vis-à-vis the standard packages available from generalist vendors. The boundaries that confine specialists in the downstream product market do not extend to the technological space, however. Creating technologies incurs significant sunk costs and entails broad and deep search processes (Ahuja and Katila, 2001). In most cases, these technologies display economies of scope by supporting applications in multiple, distant domains (Gambardella and Giarratana, 2013). However, specialists cannot pursue expansion and diversification because these activities generate identity conflicts that deprive specialists of their legitimacy (Carroll and Swaminathan, 2000; Dobrev et al., 2002). Most importantly, entry into other product domains demand different routines and capabilities (i.e. integration and architectural competences) that are not easy to develop quickly because of learning dynamics and path dependence. Summarizing, while specialists are likely to possess valuable technological assets suitable of applications in other product domains, they are constrained in their ability to expand across product categories.

Technology licensing offers a possible way out: it generates financial returns from research-and-development sunk costs and avoids investments in downstream markets that could undermine the specialist’s identity and its ability to provide customized solutions to its niche customers. Technology licensing also helps strengthen a specialist’s legitimacy and its identity in the market segment as a provider of technologically sophisticated, niche products by emphasizing its role as a source of reliable, state-of-the-art technological competences (Wade, 1996).

Selling technology also can augment competition in the product market by encouraging other firms to enter or improving current rivals’ efficiency (Fosfuri, 2006). Specialists thus aim to sell technologies to firms that do not pose threats to their niche—that is, generalists.

Generalists compete at the market center, rely on a broad resource space by offering products in multiple niches, and benefit from both scale and scope economies (Carroll and Swaminathan, 2000). Consequently, a generalist’s success depends on its ability to design product architectures that integrate differentiated knowledge to serve customers with broad needs, which makes them more willing to buy and integrate technologies already developed by specialists. This view aligns with Henderson and Clark’s (1990) categorization of innovation between architectural, that is, “the way in which the components […] are linked together” (p. 10), and modular, that is, “innovation that changes only the core design concepts [of components]” (p. 12). We argue here that while specialists are focused on innovating in the modules, generalists are better in integrating modules inside a proprietary architecture. Thus, differently from specialists, generalists are less likely to possess state-of-the-art disembodied technological assets that could be sold separately from the products.

Regardless of their ability to generate technological resources that can be traded, generalists have also fewer incentives to sell their technology, all else being equal. Because generalist organizations compete to occupy the lucrative market center (Carroll, 1985), licensing could lead to saturation and higher competition (Dobrev et al., 2001), which could be detrimental to their survival. That is, generalists might suffer greater profit dissipation from licensing than the revenues they could earn (Arora and Fosfuri, 2003). Insofar as generalists have larger market shares, this prediction is consistent with Fosfuri’s (2006) evidence from the chemical industry. In addition, if their technological expertise can extend to distant product domains, generalists, differently from specialists, have the ability and the resources to diversify and grow without necessarily resorting to licensing (Teece, 1986). These arguments suggest the following:

Hypothesis 1. Specialists sell more disembodied technologies in the market for technology than generalists.

Demand side of the market for technology

We turn now to the other side of the market for technology and investigate which firms are more likely to buy disembodied technology. First, as we argued above, specialists focus on a single market segment, in which, to address the needs of their sophisticated customers, they have to stay at the technology frontier. Because of this product focus, specialists are exposed to a relatively narrow set of technological needs and thus lack interest in extramural technology. Their potential demand for disembodied technology is therefore bounded by the limited breadth of their product portfolio. Second, purchasing disembodied technology from generalists or other specialists might detract from the organization’s reputation and legitimacy, thereby reducing specialists’ ability to adapt to niche needs (Carroll and Swaminathan, 2000). Indeed, their customers might perceive the acquisition of extramural technology as a sign of technological backwardness and stop trusting their ability to address sophisticated technological demands (Wade, 1996).

By contrast, generalists display a broad product scope and require technological competences in multiple, diverse technological domains (Dobrev et al., 2001). Considering their intense competition with other generalists to secure core positions at the market center, they focus on investments that help them serve the bulk of their demand; that is, they seek to leverage scale and scope economies. Thus, beyond marketing capabilities or production efficiency, generalists have incentives to develop technological capabilities that can maximize the integration of different technologies within a complex portfolio of product offerings (Eggers, 2012). Because generalists serve a wider and more heterogeneous set of customers with a larger portfolio of products, if they want to nurture stand-alone technologies, they must move resources away from integration and architectural knowledge, which is where they achieve their economies of scale and scope. Differently from specialists, purchasing off-the-shelf technologies does not detract from their reputation as providers of efficient solutions (Wade, 1996); rather, it enables them to exploit their integration capabilities and absorptive capacity. Thus, we posit the following:

Hypothesis 2. Generalists buy more disembodied technologies in the market for technology than specialists.

Technology trading and survival

A main implication of our theory above is that positioning in the product space drives positioning in the technology space. Here, we close the circle in our attempt to bridge resource partitioning theory and markets for technology research by examining the impact of technology trading on organization viability for various organizational subpopulations. An underlying consequence of our theoretical model is that a firm enhances its legitimacy and thereby its survival chances by building consistency and coherence across its product and technology strategies. The role of legitimacy in innovation dates back to the seminal study of Wade (1996) who highlights how technology success and diffusion depend also on the reputation and social ties of organizations. He explains the success of IBM in the personal computer not with IBM’s technological superiority but with IBM’s legitimacy “with corporate clients who had previously invested in IBM’s mainframe computers” (p. 1221). In an industry like security software, Broekhuizen et al. (2017) have shown the importance of firm names as anchors of company reputation and legitimacy, especially in terms of resilience and soundness. As we mentioned, by resorting to arms’ length contracts, a specialist can focus on customization, obtain financial resources, and maintain its identity while leveraging the applicability of its technology to other product domains. Likewise, generalists can obtain off-the-shelf technology, while keeping their efforts focused on developing integration and architectural knowledge. Taken together, these arguments suggest that specialists that are more active technology sellers should experience lower exit rates because of the benefits created by the fit between their product and technology strategies. Similarly, generalists that buy technology should have reduced mortality rates. Therefore,

Hypothesis 3a. The benefit of a narrow product strategy (specialist) for organizational viability increases if the focal firm sells more disembodied technologies in the market for technology.

Hypothesis 3b. The benefit of a broad product strategy (generalist) for organizational viability increases if the focal firm buys more disembodied technologies in the market for technology.

Data and methodology

SSI

The inception of SSI coincided with the growing market for personal computers and the development of the Internet in the late 1980s (Giarratana, 2004). Worldwide sales increased from US$2.2 billion in 1997 to US$6.9 billion in 2002 (International Data Corporation, 2003). North America and Europe accounted for 50% and 30%, respectively, of worldwide market share in 2002 (International Data Corporation, 2003). The industry featured an active market for technology; 15% of its revenues in 2002 came from licensing software algorithms. Crypto-algorithms, which specify the mathematical transformations performed on data, are the main technology of SSI. The crypto-algorithm is responsible for the quality of the security software product, in terms of both its security level and the speed of mathematical calculations (Giarratana, 2004).

From 1989 to 2002, SSI firms undertook more than 400 technology transactions (www.gale.cengage.com). Our data do not suggest that specialized technology suppliers—which only sell technology but do not compete in the product market—are relevant for SSI, as they are in industries such as chemicals, biotechnology, and semiconductors (Arora et al., 2001). Most technology trades occur horizontally among firms that have a product-market presence and thus compete in the same downstream industry.

Customers of SSI fall into two broad categories: (1) medium- to low-tech users who demand comprehensive security packages, prefer one-stop-shop solutions, and ask for a high level of technological service and assistance and (2) sophisticated buyers who seek the best product quality and demand state-of-the-art technology. Similar to other industries (e.g. beer industry: Carroll and Swaminathan, 2000; wine industry: Swaminathan, 2001; US feature film industry: Mezias and Mezias, 2000), this customer partitioning makes both generalists and specialists viable despite strong competitive intensity in the industry. Generalists offer a broad product portfolio that covers several SSI niches and satisfies the needs of the majority of customers; specialists thrive by offering continuous updates and improved versions in their established niche, which addresses the requests of high-tech, sophisticated customers.

Check Point is a good example of a specialist that functions in the firewall niche: its FireWall-1 product won a prestigious industry award for several consecutive years, offering “best overall performance, management and logging features, which are three key parts to a security solution” (Network Computing, 1998). By contrast, Network Associates provides a good example of a generalist organization that competes in several market niches. The firm has built a large, flexible portfolio of software products to offer its customers (Fortune, 1998).

An important clarification is warranted: although the canonical approach of resource partitioning focuses on scale and scope advantages of generalists in terms of production, the software industry traditionally lacks these types of scale and scope economies. However, the same logic could be safely extended to distribution channels, sales forces, and brand reputation. To further prove this point and show that the SSI is indeed resource-partitioned, we perform some robustness tests in the section “Resource partitioning in SSI.”

Sample construction

Our study population consists of firms that introduced at least one off-the-shelf security software product before December 2002. Thus, all firms in our sample competed in the downstream market. We gathered product introduction data from Infotrac’s General Business File ASAP and PROMT database (formerly Predicast), which reports events in several industrial sectors, as publicized in various trade journals, magazines, and specialized press vehicles (e.g. eWeek, PC Magazine, PR Newswire, Telecomworldwire). We searched for all press articles that reported a “product announcement,” “new software release,” or “software evaluation” in SSI (standard industrial classification (SIC) code 73726) between 1980 and 2002. 1 We carefully cleaned these data to avoid product double counting. The first product was introduced in 1989, and from 1989 to the end of 2002, we registered 736 different firms that introduced 2589 products. According to their SIC codes, we classified these products into six niches: authentication digital signature, antivirus, data and hardware protection, firewalls, utility software, and network security and management.

From the Infotrac database, we downloaded all articles that reported a licensing event in SIC 73726 (encryption software sector). After carefully reading the abstracts, we kept only the articles that referred to technology licensing contracts and removed articles unrelated to a technology transaction (e.g. marketing, franchising agreements). Finally, using the article texts, we assigned buyer (licensee) and seller (licensor) roles to the firms engaged in each transaction. We assume that the date of the article is the date of the event.

Dependent variables

We used two dependent variables to test the first two hypotheses. The variable technology sales is time variant and corresponds to the annual number of contracts signed by a firm as a technology seller in SSI. The variable technology acquisitions is also time variant and equals the number of contracts signed by a company as a buyer of technology in SSI. For example, Entercept Security Inc. licensed its intrusion prevention technology to iPlanet, and iPlanet embedded it into its core product. The deal enabled iPlanet’s users to gain protection against intrusions, website defacement, data theft, and misuse (Telecomworldwire, 2001). In an example involving NeoPlanet and Compaq, the former supplied its Viassary security technology to the latter, which enabled Compaq to include the technology in its Advisor product, a tool for effective communication through multiple digital touch points (PR Newswire, 2001).

For the remaining hypotheses, we estimated a hazard model to predict survival. Our dependent variable is thus a time-variant dummy, equal to 1 if the firm exits the market at time t and 0 if it continues until the next period. We used several sources to identify exits from the market: the US Patent and Trademark Office, Hoover’s, Mergent Online, Bureau Van Djik’s Icarus, Jade, and Amadeus. In addition, we searched Infotrac Company Resource Data Center and Infotrac’s PROMT for any press articles that included news related to a firm’s exit (e.g. acquisition, bankruptcy, shutdowns).

Independent variables: generalists and specialists

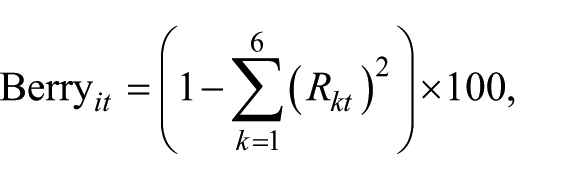

Organizational niche width provides a commonly used proxy for defining generalist versus specialist organizations. For example, Dobrev et al. (2001, 2002) measure the niche width of an automobile producer in terms of the min-max spread of engine capacity across all models manufactured by a firm at a given time. 2 Variations across this single dimension capture the differences across organizations along the specialist–generalist dimension. In line with prior research (Giarratana and Fosfuri, 2007), we computed a Berry index of the dispersion of a firm’s product portfolio:

where Rkt is the ratio of the cumulative number of firm i’s products in the kth niche of SSI to the total number of firm i’s products in all niches of SSI in year t. Because SSI consists of six major niches, k varies between 1 and 6. By construction, the Berry index can vary between 0 and 100 (maximum niche width).

The standard interpretation of this measure indicates that organizations with high values on the Berry index are more likely to be generalists than specialists, implying that a single measure captures both population groups. However, this standard interpretation of the Berry index (niche width) might be too coarse in our context, because a low Berry index does not necessarily correspond to a specialist firm. As our theory proposes and data from SSI confirm, product versioning is a standard practice in the software industry by organizations that specialize in a particular niche and rely on customization and innovation (Shapiro and Varian, 1999). A low Berry index cannot capture the high degree of product versioning or the constant releases that characterize this industry. We therefore complement it with a second product strategy measure to increase the chances of depicting our study phenomena accurately.

Specifically, we calculate a versioning index that is time variant and equal to the cumulative number of new versions in the product niche that spurred the firm’s entry into SSI. Thus, if firm i entered SSI in period t with a product in niche k, the versioning index counts the cumulative number of products by firm i in niche k. This entry product niche is crucial because it enables new ventures to establish their reputation and first-mover advantages, which provide substantial benefits in the fierce market competition that occurs in the periods immediately following entry (Kazanjian and Rao, 1999). Indeed, research shows that firms are more likely to specialize in the same niche they entered in the first place (Debruyne et al., 2002). Therefore, firms that score high on the versioning index should be more likely to follow a specialist product strategy. 3 Suppose that a firm enters SSI by developing a product in niche z in 1997 and, by 2000, it has updated this product three times, releasing a new version every year. The value of its versioning index would be 2, 3, and 4 in 1998, 1999, and 2000, respectively. If this firm also released products in another niche, it would affect only the Berry index, not the versioning index. In sum, the versioning index represents a good proxy for specialism for two reasons. First, it fully captures the case an SSI firm that remains specialized, and separate firms (false specialists) that just release one product and disappear from firms (real specialists) that consistently innovate. Second, using simultaneously the versioning index and the Berry index, we can capture the full movement of a specialist toward generalism, that is, when it diversifies and abandons the first niche (scoring low in versioning).

As a robustness check (available on request), our empirical results hold when we construct two dummies by combining the indexes: a specialist dummy, equal to 1 when a firm attains high values on the versioning index (top quartile) and lower-than-average values on the Berry index, and a symmetric generalist dummy.

To test Hypothesis 3a (3b), we built a variable, tech_acquisition (tech_sale), which counts, for firm i, the number of purchased (sold) technologies in each period t. It thus proxies for the extent to which a firm actively participates as a technology buyer (technology seller) in the technology market. We next interacted tech_acquisition (tech_sale) with our indicator of generalist (specialist) organizations to capture the notion that being a generalist (specialist) and an active buyer (seller) of disembodied technology increases survival chances.

Controls

We introduced several time-variant and time-invariant control variables. According to ecology research, population density can have a U-shaped relationship to firm exit rates (Carroll et al., 1996; Dobrev et al., 2002; Sorenson, 2000). Density (i.e. the number of firms operating in each SSI niche) and density squared (density2) with a 1-year lagged value (Carroll et al., 1996) appear in our models because they are canonical controls in survival analyses (Hypotheses 3a and 3b). We suspect that they might equally affect strategies in the market for technology (Hypotheses 1 and 2), such as through increased competition or improved chances to find suitable alternative buyers or suppliers. Another important environmental variable to control for is the extent of development of the technology market, which we proxy with market thickness. Gans and Stern (2010) refer to the thickness of the market for technology as the “degree to which a large number of buyers and sellers participate within a market, and hence the degree to which each buyer and seller has an opportunity to engage in an effective match” (p. 812). Market thickness is a necessary condition for effective matching because it implies that for each technology on sale, several potential buyers exist, and for each demanded technology, several potential sellers exist. We measure the thickness of the market for technology, thickness_mft, as the ratio of the annual number of seller and buyer organizations to the cumulative number of patents in SSI, which captures the realized (licensing parties) versus potential market for technologies (patent availability). 4

At the firm level, we introduced experience in the market, measured as the number of years a firm has competed in SSI (age in market), or the difference between year t and the year the firm entered the market. Although our sample contains some large information and communication technology firms, it mostly comprises small to medium-sized, young firms, which means that traditional, time-varying measures of firm size (e.g. sales, number of employees) are difficult to obtain. Instead, we used a measure of firm size that counts the raw number of products a firm sells in each year (total products). Dobrev and Carroll (2003) suggest a proxy for size: the scale of operations, calculated as the annual number of units produced. In line with this research, we controlled for the firm’s technological capital in SSI as well. Following Dushnitsky and Lenox (2005), we measured the cumulative number of firm patents granted by the US Patent Office (www.uspto.gov), applying a discount rate of 15% (other discount rates lead to similar results). We considered all patents granted in US technological classes 380 (“Cryptology”) and 705, subclasses 50–79 (“Business Processing Using Cryptography”) (Gambardella and Giarratana, 2013). We labeled this variable patents.

To temper any significant omitted variable problems of firm unobserved heterogeneity in technology abilities, we also introduced pat_forward citations and pat_generality. The former is the cumulative number of forward citations divided by the cumulative number of patents, which provides a proxy of patent quality (Fleming, 2001). The latter derives from the generality index introduced by Hall et al. (2001); the measure reflects the annual firm value of the index weighted by the number of firm patents. This generality index offers a proxy of the firm’s capability to produce general-purpose technology, which correlates with the ability to license (Palomeras, 2007). To be aligned with resource partitioning, we inserted the concentration index, a Herfindahl measure based on generalists’ sales data (a higher value implies a more concentrated market).

Time-invariant control variables capture the effects of several pre-entry conditions. We employed a measure of organizational population density at the time the firm entered the market (density delay), a standard control in entry and survival literature (Carroll et al., 1996; Sorenson, 2000). The firm’s age at market entry proxied for scale and experience effects. Age (entry age) is the difference between the entry year and the year of a firm’s founding. We also included a dummy variable that takes the value of 1 if the organization is a US firm and 0 otherwise (US dummy). The purpose of this control was to smooth out the possible distortion effect for non-US firms, because the United States is the largest and most important market for SSI. We also introduced the industry background dummy to control for companies whose main business is outside the software domain.

Following Ahuja and Katila (2001), we created control variables that correspond to the presample value of the dependent variable for each firm (i.e. entryseller and entryacquirer). These measures control for unobserved differences in capabilities and strategic postures in markets for technology. Failing to account for such unobserved heterogeneity in the empirical test of Hypotheses 1 and 2 can cause estimation problems, overdispersion, and serial correlation.

Finally, in testing Hypotheses 1 and 2, we inserted year dummies. We provide descriptive statistics in Table 1 and a partial correlation matrix for the variables in Table 2.

Descriptive statistics.

Source: These elaborations stem from various data sources, including Infotrac’s General Business File ASAP and PROMT, the US Patent and Trademark Office, and Compustat.

Bivariate correlation matrix.

Correlations with an absolute value of 0.04 or more are significant at p < 0.05.

Estimation method

The dependent variables for Hypotheses 1 and 2—that is, the annual number of sold/purchased technologies—are count variables and thus take only nonnegative integer values. Applying conventional linear regression models that assume homoskedasticity and normally distributed error terms would lead to biased estimates; a Poisson regression approach is more appropriate (Hausman et al., 1984). Thus, we estimate the following regression model:

where Yit is the number of technology licenses sold or purchased in year t, Xit refers to the set of measures of a firm’s product-market strategy that capture its generalist versus specialist orientation, and Cit is a vector of control variables. The results remain unchanged when we lag all independent and control variables by 1 year. The specification does not account for unobserved heterogeneity; therefore, we followed Ahuja and Katila (2001) and Ahuja and Lampert (2001), who estimate Poisson regression models using the general estimating equation (GEE) approach, which models the longitudinal Poisson data with serial correlation (Liang and Zeger, 1986). A clear advantage of the GEE methodology is that it provides a better treatment for overdispersion and serial correlation, which are often present in panel data sets (Liang and Zeger, 1986). For limited-range dependent variables and longitudinal research designs, GEE produces efficient and unbiased parameter estimates when the dependent variable is highly correlated within subjects (Ballinger, 2004). 5

To test Hypotheses 3a and 3b, we employed a hazard model to estimate the hazard rate, namely, the probability of exit from the market at time t, conditional on being in the market at time t – 1. Hazard rates capture those spells that are completed at duration t, if they have endured until t. The term f(t) = dF(t) / dt represents the quantity of firms departing the market at time t, while S(t) = 1 – F(t) = Pr(T ⩾ t) represents the quantity of firms still at risk at time t (Blossfeld and Rohwer, 2002). The ratio is the hazard rate, λ(t) = f(t) / S(t).

As other works suggest, we opted for the piecewise exponential model (e.g. Dobrev et al., 2002; Giarratana and Fosfuri, 2007; Sorenson, 2000), because it assumes an exponential time dependence, which better approximates industry life cycle. Intuitively, an exponential model allows acceleration or deceleration of time frames, a desirable feature to better fit an industry evolution. The exponential model can be expressed as Λjt = exp(α t + Xjtβ j ), where X is the covariate vector, β is the vector of coefficients, and α is a constant coefficient associated with the time period t (see Blossfeld and Rohwer, 2002). In our regression, we control for both left and right truncation, and the time period is the year. Furthermore, within each year, the base exit rate remains constant, but the effects vary across the years.

Resource partitioning in SSI

In order to verify that the partitioning process takes place in our empirical context, we performed additional analyses. As specialism in SSI is related to the versioning strategy, we interacted the versioning and the concentration indexes in the piecewise exponential model of market exit. Results in Model 1 of Table 5 confirm that core variables (Berry and versioning) are negatively associated with a firm’s probability of market exit and the interaction between the versioning index and the concentration index also displays a negative coefficient. These results show that, in SSI, the more concentrated the industry (i.e. larger generalists), the higher the survival chances of specialists, one of the main tenets of resource partitioning theory. In addition and available on request, we examined the correlation between the annual entry number of specialists and the concentration index in SSI: this correlation is positive and significant and displays a value of 0.29. We also ran a negative binomial regression predicting market entry of specialist organizations into SSI (294 entries). The result confirms a positive and significant association between the entry of specialists and concentration of SSI.

Results

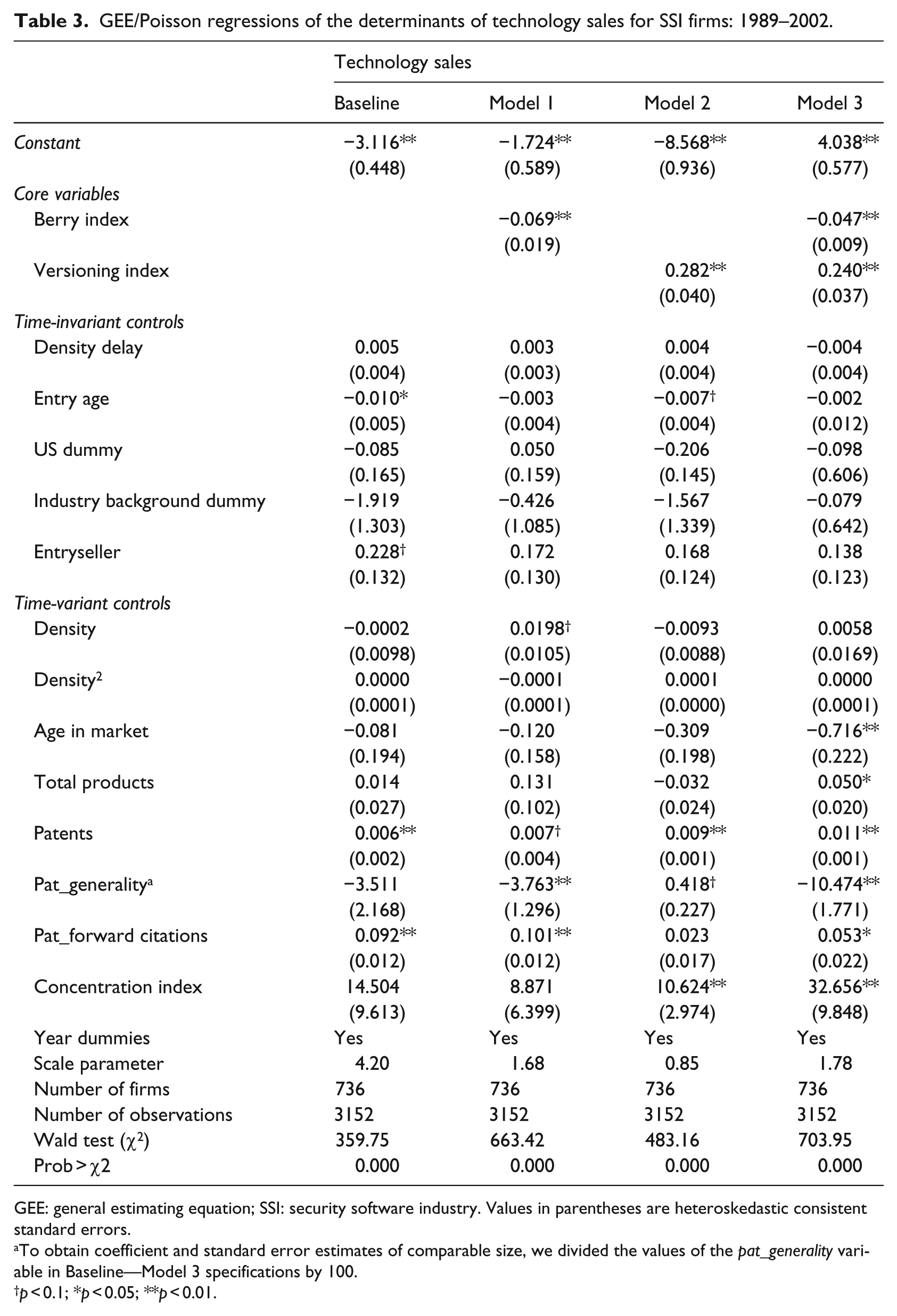

In Tables 3 and 4, we present the results for all models using the GEE Poisson estimators, with robust standard errors. The baseline models include only firm- and industry-level control variables. Then, Model 1 incorporates the Berry index, and Model 2 includes the versioning index. In Model 3, we introduce both indexes simultaneously.

GEE/Poisson regressions of the determinants of technology sales for SSI firms: 1989–2002.

GEE: general estimating equation; SSI: security software industry. Values in parentheses are heteroskedastic consistent standard errors.

To obtain coefficient and standard error estimates of comparable size, we divided the values of the pat_generality variable in Baseline—Model 3 specifications by 100.

p < 0.1; *p < 0.05; **p < 0.01.

GEE/Poisson regressions of the determinants of technology acquisitions for SSI firms: 1989–2002.

GEE: general estimating equation; SSI: security software industry. Values in parentheses are heteroskedastic consistent standard errors.

To obtain coefficient and standard error estimates of comparable size, we divided the values of the pat_generality variable in Baseline—Model 3 specifications by 100.

p < 0.1; *p < 0.05; **p < 0.01.

The findings in Table 3 confirm Hypothesis 1. The estimate of the Berry index is negative and highly significant when it appears separately and when it coexists with the versioning index. Therefore, the larger the niche breadth of a company, the fewer deals it makes as a supplier in the market for technology. In both Models 2 and 3, the parameter estimates of the versioning index are positive and statistically significant, such that firms that release more versions and updates of their core products sell more disembodied technologies. These findings receive further confirmation from an unreported regression, in which the specialist dummy is positive and statistically significant, whereas the generalist dummy is negative and statistically significant (see previous section for the construction of these dummies).

With regard to the control variables in Model 3 of Table 3, more experience in the market discourages the sale of technology, given the negative and significant coefficient of age in market. Size of firms, as captured by the raw number of products, positively correlates with licensing out. The variable patents is positive and significant, suggesting that technological capital is positively associated with the sale of disembodied technology. The negative and significant sign of pat_generality implies that firms with more general patent portfolios display fewer technology sales. The proxy for patent stock quality, pat_forward citations, is positively and significantly associated with the sale of technology. The positive and significant concentration index implies that industries with larger generalists license out more. The coefficients of the rest of the control variables are not statistically different from zero.

Table 4 displays the estimation results of the GEE Poisson models with the number of a firm’s technology acquisitions in a given year as the dependent variable. These results provide support for Hypothesis 2, in that the estimated coefficient of the Berry index is positive and significant. Organizations with broader niche width tend to buy more technology in the market. The coefficient for the versioning index in Model 3, though negative, is not statistically different from 0. However, our specialist and generalist dummy variables are both significant and display the expected signs, which suggest that generalists are more active than specialists as buyers in the market for technology (results are available on request from the authors).

Regarding our control variables, the positive and significant coefficient of density and the negative and significant coefficient of density2 jointly suggest an inverted U-shaped relationship between the extent of technology acquisition and the degree of product-market competition. Size, as measured by the raw number of products, enhances the number of technology purchases, perhaps through the provision of greater financial latitude or simply because of greater scale, which implies more demand for disembodied technologies. Firms with general-purpose technologies acquire more disembodied technologies, as evidenced by the positive and significant coefficient of pat_generality. An industry with few large generalists displays more licensing in of externally developed technologies. Harsher competitive conditions at entry push firms toward more technology acquisitions, as indicated by the positive and significant coefficient of density delay. Firms whose main business lies outside the software domain tend to purchase more disembodied technologies, as indicated by the positive and significant coefficient of industry background dummy. Pre-entry purchase of technology is associated with more technology acquisitions, as evidenced by the positive and significant coefficient of entryacquirer. The other controls do not exhibit statistical significance. Finally, the estimated scale parameters do not indicate that overdispersion in the data is a serious concern.

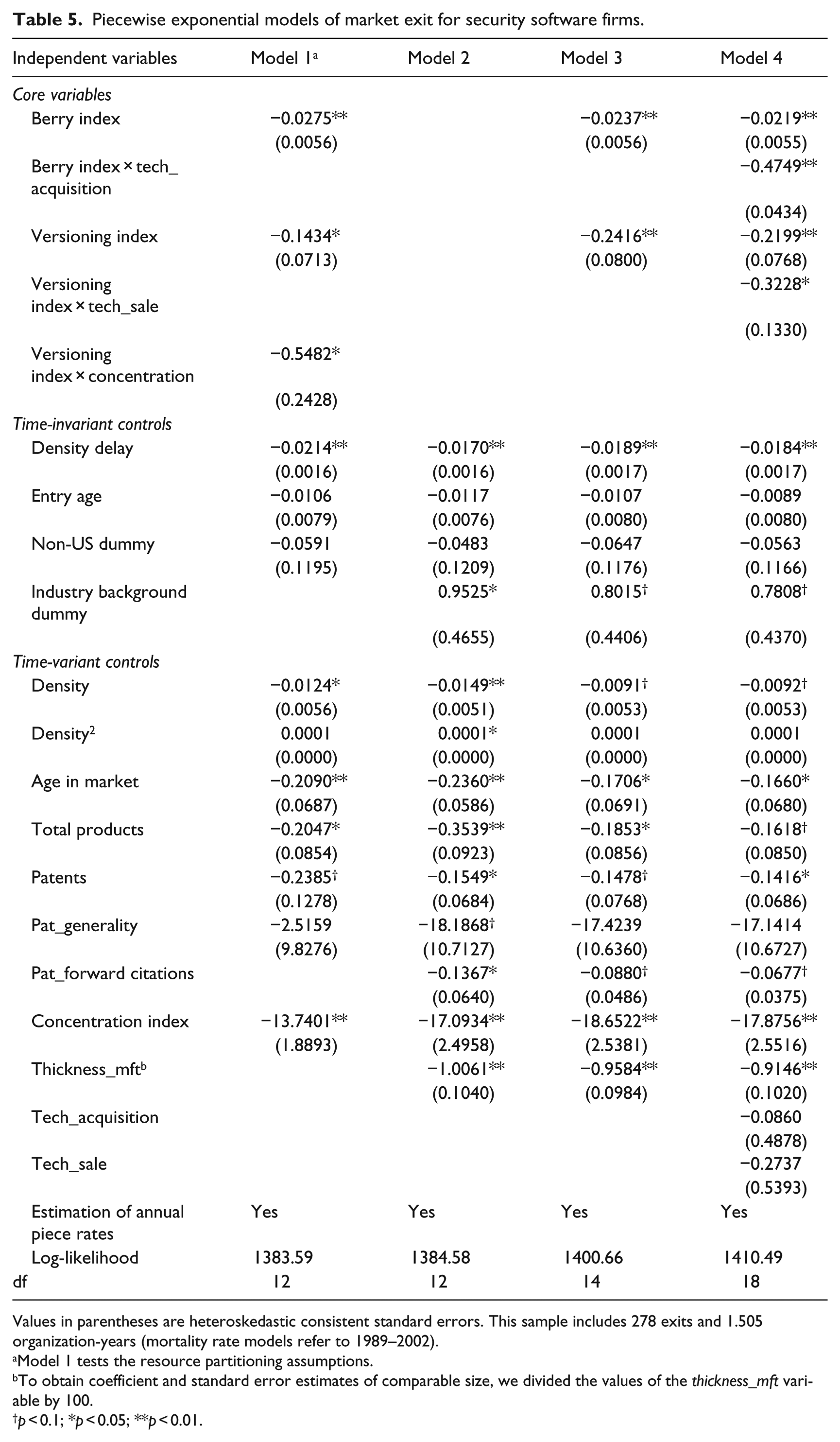

Table 5 provides the results for the hazard estimation. 6 Model 2 is the baseline model that excludes our core covariates, Model 3 encompasses the Berry and versioning indexes, and Model 4 is the full model that includes the interaction between tech_acquisition (tech_sale) and the corresponding product strategy index. Adding the variables in each model increases the level of fit, as implied by the chi-square test of significance.

Piecewise exponential models of market exit for security software firms.

Values in parentheses are heteroskedastic consistent standard errors. This sample includes 278 exits and 1.505 organization-years (mortality rate models refer to 1989–2002).

Model 1 tests the resource partitioning assumptions.

To obtain coefficient and standard error estimates of comparable size, we divided the values of the thickness_mft variable by 100.

p < 0.1; *p < 0.05; **p < 0.01.

The interaction between tech_sale and the versioning index is negative and significant, in support of Hypothesis 3a. In addition, the interaction between tech_acquisition and the Berry index is negative and significant, in support of Hypothesis 3b.

Taken together, these findings are consistent with our theoretical model, which suggests that by partitioning the resource space, firms increase their survival chances. Both product strategies decrease an organization’s likelihood of exiting the market. A firm’s position in the product market also interacts with its position in the technology market: the organizational viability of specialists (generalists) increases when they actively engage in technology sales (purchases). Results also reveal that survivors in SSI are either more aggressive in the adoption of versioning (specialism) or in portfolio broadening (generalism) strategies (Giarratana and Fosfuri, 2007). Therefore, unique product strategic orientation helps organizations to increase their probability of survival and leads to a bimodal resource distribution. The emergence of these two different groups within the population in the focal industry is consistent with resource partitioning theory (Dobrev et al., 2001; Kim et al., 2003; Negro et al., 2014) and recent studies on intra-industry diversification, which find a U-shaped relationship between diversification and performance (Barroso and Giarratana, 2013; Zahavi and Lavie, 2013).

Among the control variables, we emphasize the negative and significant coefficient of Thickness_mft, which implies that a thicker market for technology augments the survival chances of all competitors in SSI. In other words, thicker markets for technology allow for collaborative interactions among organizations and increase survival chances.

Discussion and conclusion

Although industry evolution and competitive dynamics have been subjects of academic debate for several decades, the relationship between positioning in the product market and that in the technology market has received scant attention (De Figueiredo and Silverman, 2012). Thus, investigating this relationship can shed new light on how industries evolve and firms compete for scarce resources.

Implications for researchers

Combining the resource partitioning tradition (Carroll, 1985; Dobrev et al., 2001; Swaminathan, 2001) and research on the market for technology (Arora et al., 2001; Gans and Stern, 2003)—domains that generally coexist as silos—enables us to understand better why some firms engage, as buyers or sellers, in more technology transactions than others and how the direction of technology trade affects their survival chances. Our work thus highlights some understudied facets of these two literature streams, which can only be appreciated by combining them.

First, our joint consideration of resource partitioning and markets for technology extends the literature. Most prior research has investigated the intensity and type of competition in different resource spaces (Carroll and Swaminathan, 2000; Hannan and Freeman, 1989). According to ecology research, partitioning resources creates two groups of organizations (Carroll, 1985; Dobrev et al., 2001; Swaminathan, 2001); we show that it does not follow that these two groups are completely isolated in impermeable spaces. Not all resources are partitioned, because specialists’ strategies and routines generate nonrival or abundant resources (e.g. technologies) that can be exchanged for another set of resources produced by generalists (e.g. liquidity, distribution channels). In short, an important contribution of our work is to underscore that the relationships between generalists and specialists are more complex than suspected; these two organizational populations might compete in one resource space and be complementary in another, with a significant impact on survival rates. Although extant ecology literature has emphasized that the lack of coherence creates a liability of “middleness” (Zuckerman et al., 2003), our study is one of the first to highlight the presence of this liability at a new level of analysis, between niche positioning and roles in technology trade.

Second, our framework offers novel insights for research into the market for technology. Current literature focuses on the determinants of out- and in-licensing, such as transaction costs, fear of competition, technology characteristics, and risk sharing (Anand and Khanna, 2000; Arora and Ceccagnoli, 2006; Arora et al., 2001; Fosfuri, 2006; Gans and Stern, 2003). We show that product strategy influences a firm’s strategies in the market for technology, thereby identifying another source of heterogeneity that can explain firms’ varying technology strategies. In so doing, we link technology diffusion and the emergence of a market for technology to a legitimacy argument, an embryonic idea so far (see Wade, 1995, 1996) Specialist organizations, which occupy the periphery (Swaminathan, 2001), can augment their legitimacy by remaining focused in the product space and simultaneously engage in licensing their technology to generalists. For generalists, the opposite holds. They can increase their appeal to their customers by acquiring technology through arms’ length contracts and remain focused on developing integration and architectural capabilities.

Limitations and future research

The empirical model that we present provides a general correlation structure among variables inside an industry time span, which is consistent with our theoretical predictions; however, we are cautious in claiming any sound causal relationships among these variables. We focused on technology trade through arm’s-length agreements, but extending our theoretical logic to trading or sharing resources other than technology (i.e. human resources) might provide novel insights while also confirming the generalizability of our framework. Especially important is the introduction of a monetary evaluation of the resources traded, given that this study is confined by data availability to using the number of transactions, not the value. Finally, our results have important applications in industries in which the resource partitioning assumptions hold and in which some of the resources embedded in products could be disembodied. These features make SSI an ideal setting for testing our hypotheses, but they also necessitate additional evidence to support the generalization of our findings. Industries such as lasers, biotechnology, conversion coating, and battery chemistry would be suitable candidates for such confirmatory studies.

Implications for practitioners and industrial policy

Our results can be useful to managers and executives functioning in different circumstances. First, we show different paths for survival, depending on the organization type. For specialists, the best process entails continuous research-and-development investments to update technological competences, sustain launches of new versions of products within a niche, and sell technological expertise to buyers in distant product niches. By contrast, generalists should focus on production and marketing investments that increase efficiency, augment the breadth of their product portfolio, and facilitate the penetration of new niches, which then implies the prompt acquisition of necessary technologies on the market. In sum, for specialists, our results call for actions that make their technology more easily accessible and visible on the market; for generalists, they imply the creation of business intelligence that constantly scans and monitors the technology landscape.

Second, we showed that mismatches between product and technology strategies can be detrimental to a firm’s survival. Successful organizations must guarantee coherence in their product and technology strategies, meaning an efficient coordination across the firm’s product, marketing, and research divisions. A stand-alone licensing unit could help both types of organizations and might strengthen bridges across divisions, avoiding mismatch among strategy timing, steps, and decision order. This proposition is consistent with recent research that shows that firms with centralized licensing units tend to be more active in markets for technology (Arora et al., 2013).

Footnotes

Acknowledgements

The authors are grateful to Robert David (coeditor) and three anonymous reviewers for their excellent guidance and feedback.

Authors’ Note

From 2015, August 7, PROMT, European Business ASAP, Business Index ASAP, Business & Company ASAP, General Business File, and Business International & Company Profiles will be automatically upgraded and replaced with Business Collection, a comprehensive, innovative new resource that incorporates their content.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.