Abstract

The commercial public service broadcasters (PSBs) in the United Kingdom (UK) make a significant contribution to the country’s public service television system, alongside the BBC. Operating under the UK communications regulator Ofcom, the commercial PSB channels ITV, Channel 4, and Channel 5 are required to broadcast varying levels of public service content. This places these channels in a different category to all other market broadcasters in the UK. By taking a critical political economy of communication approach, this article examines how the regulatory system functions to secure public service provision in television. A particular focus is placed on the first-run originations quotas, which govern the levels of programming that are originally produced or commissioned by a commercial PSB, and broadcast for the first time in the UK. It is argued that while fulfilling the public service remit, the commercial PSBs gain significant benefits that contribute to the underpinning of their business models.

Keywords

Introduction

While the BBC is the United Kingdom’s main public service broadcaster (PSB), the United Kingdom’s commercial PSBs make an important contribution to the overall framework of the public service television system. In return, they receive considerable benefits that they gain from being part of the PSB framework and that contribute directly to underpinning their business models. A critical political economy of communication approach is taken in this article to the United Kingdom’s commercial PSBs, a group made up of the television channels ITV, Channel 4, and Channel 5. Resulting from the analysis, it is argued that the framework that the commercial PSBs operate within ought to be conceptualized in a way that highlights the distinction between it and that framework which their non-PSB counterparts operate within. In other words, the shorthand distinction (commonly used journalistically) between the BBC and the other “market-based” broadcasters that posits them, respectively, “public” or “private” is a clumsy one, and means that the importance of the current governance system and its maintenance can be missed. It is argued in this article that there is a dearth of attention given to the contribution made by the commercial PSBs to a plural and democratic media system; this is shown to be in stark contrast to the limited contribution made by the non-PSB organizations, a group that broadcasts all other UK television channels.

A focus is placed in this article on the quotas in relation to “first-run originations” that the commercial PSBs are required to fulfill, that is, programming that is originally produced or commissioned by a UK broadcaster and shown for the first time within the country. This regulatory framework, which delivers high spending on originations outside of sports programming, is compared with that of the non-PSB television sector, where a very large proportion of money spent in this category is on sport. The first-run originations category is one key area where the PSB regulatory framework functions to ensure a form of broadcasting that meets the PSB requirements discussed below. The framework also helps demarcate a PSB system that remains normatively important within the wider broadcasting market. It is argued that the public service television system that is administered by the UK communications regulator Ofcom may come under political pressure to be further liberalized.

Applying Critical Political Economy of Communication to Public Service Broadcasting

Critical political economy of communication is a well-developed field within media and communication research, strongly influenced by the British tradition, shaped by the work of Murdock and Golding (see Golding and Murdock 2000; Murdock and Golding 1997) and Garnham (1979, 2010), among others. If the approach is less popular within media and communication studies than the more dominant cultural studies approaches, it does have strong communities of scholars working in North America (e.g., McChesney 2013; Mosco 2009), Western Europe (e.g., Hardy 2014), and, for example, Australasia (e.g., Thompson 2011). Mosco (2009, 2) defines political economy as “the study of the social relations, particularly the power relations, that mutually constitute the production, distribution, and consumption of resources, including communication resources.” Here, a focus is placed on flows of capital and labor, and on ownership and power in the media and communications industries. In addition, critical political economy of media and communication often encompasses a critical historical approach, as shown in the propensity of its proponents to illustrate the historical context of contemporary research subjects, and for the way in which the flexibility of the methods and disciplines it draws upon allows for this (e.g., sociology). Moreover, the history of communication itself is one area subject to critical political economy accounts (see Mosco 2009, 109–13).

For Hardy (2014, 7), the critical political economy of communication approach “rests on a central claim: different ways of organizing and financing communications have implications for the range and nature of media content, and the ways in which this is consumed and used.” According to Potschka (2012, 26), this form of analysis

provides an appropriate framework to investigate the shift from state control to market hegemony . . . it incorporates the relationship between transitions in the media and macroeconomics as well as socio-cultural paradigm changes and recognizes the special nature of the media and its societal and democratic function.

Potschka’s argument here is directly applicable to the present study, as the commercial PSBs are required to contribute to broadcasting that conforms to such a special nature in the United Kingdom’s television system, despite operating under market conditions. Here, the critical political economy of communication approach provides a frame whereby the role of the commercial PSBs can be assessed and judged for their normative value.

A critical political economy approach to PSB can encompass both publicly funded and commercial public broadcasting, an approach exemplified in some of the research carried out in this area. Golding and Murdock (2000, 75) use the BBC as an example of an “institutional counter to the commodification of communicative activity”. Later, Murdock (2010, 35) notes that in relation to the BBC’s commercial activities, “By introducing calculations around the potential for commodification into institutional strategies . . . they compromise the moral economy of public goods.” Addressing ITV, which is the main commercial PSB in the United Kingdom, Hardy (2012, 106) notes that the broadcaster has “lobbied, with success, for its PSB obligations to be reduced as it managed declining advertising revenues and audiences, and the diminishing value of its analogue spectrum.” (Later, we return to ITV as a company that reaps significant benefits from its role as the main commercial PSB.) Finally, Born (2003, 792) finds in her analysis of Channel 4 that the “assumption seems to be that C4’s commercial activities can have no detrimental effect on its PSB commitments; but even in purely economic terms such a view cannot be sustained.”

The BBC as a Methodological Case Study

While the BBC is not intended as the main focus of this article, we can use the Corporation as an example for this form of political economy analysis. As is the case throughout this article, qualitative document analysis (Atkinson and Coffey 2004; Forster 1994; Mason 2002) is used as a means of generating a range of data, such as information on legislation and regulation, and on the finances of the broadcasters considered here. A range of reports, documentation, and resources accessed through institutional and company websites has been considered from institutions including the BBC, the BBC Trust, Ofcom, ITV plc, Channel Four Television Corporation (C4C), and Channel 5. In each case, where the article discusses contemporary conditions, the most relevant and recent documents are used, which in some cases means drawing on data that might not have been updated for two or three years. 1

While the BBC’s income comes predominantly from the television license fee, a form of public funding, its income is supplemented by activities within the private sector, both in the United Kingdom and globally. As the Corporation’s license fee income continues to shrink—in the context of government imposed freezes to the license fee and additional funding responsibilities placed upon the BBC—the impetus for the BBC to raise its revenues from these sources makes pertinent the importance of analysis, and of greater transparency in relation to the BBC’s commercial activities (see Hewlett 2015). Drawing our attention now to these activities, BBC Worldwide (the commercial arm of the BBC) had sales of more than £1.002bn in 2014–2015, earned nationally and globally in the marketplace (BBC 2015, 134). This entailed a large market-based return to the license fee–funded BBC television channels of £226.5m in 2014–2015 (BBC 2015, 131). Such a return means that critical analysis of the BBC must take account of market activities that fall outside of the license fee, where there has been a dearth of analysis up to this point (with some exceptions; for example, Donders and Van den Bulck 2016). Indeed, as BBC Worldwide is now itself a significant commissioner of content—£94m in 2014–2015 (BBC 2015, 135)—the performance of it directly impinges on that content that is carried on the license fee–funded channels. Rather than the BBC’s commercial activities being conceptualized and analyzed separately from that research that focuses on the license fee–funded Corporation, BBC Worldwide should, instead, be considered alongside the rest of the Corporation.

In addition to addressing the structural conditions of the BBC, it follows that attention to individual remuneration of directors at the Corporation should also come under scrutiny: for example, Tim Davie, the CEO of BBC Worldwide and Director, Global, was due to receive a salary of £400,000 in 2015–2016, not including a bonus option. This salary “is funded entirely by the BBC’s commercial operations and is not paid for or subsidised by the licence fee” (BBC 2015, 112), and the suggestion is thus that it should be uncontroversial to the critics of high pay at the BBC (in the way that, say, the salaries of the CEOs of ITV plc and C4C are). And yet, as a member of the executive board of the BBC (and as of July 2015, the Corporation’s second highest paid employee after the Director-General Tony Hall, who earns £450,000), Davie ought not to escape scrutiny. Rather, his role and his performance are both directly affected by and in turn effect the license fee–funded part of the BBC.

The UK Television Market

The UK television industry had a revenue of £13.2bn in 2014, 21 percent of which originated from public funding (Ofcom 2015a, 145). By far the largest share of revenue is from subscription services, contributing £5.9bn, far ahead of the £3.8bn that came from advertising (Ofcom 2015a, 165). Of this, the share of advertising is mainly dominated by ITV/STV/UTV and ITV Breakfast, which gained 35 percent, and the multichannel sector, which gained 27 percent (other channel shares: Channel 4: 12%; Channel 5: 7%; PSB portfolio channels: 17%; Ofcom 2015a, 148). These significant revenue shares are driven largely by the high audience shares that the five main PSB channels command in the multichannel era. In 2014, 51.2 percent of all viewing was to BBC One, BBC Two, ITV, Channel 4, and Channel 5. Although this has been in overall and steep decline since the early 1990s, Ofcom (2015a, 192) has noted that it stabilized for the first time between 2013 and 2014. Whether that is a harbinger of future stability remains to be seen. However, it is these five main PSB channels (of which three are commercial PSBs) that remain overwhelmingly popular with the audience. For example, when sport is excluded, Ofcom found that the twenty television programs in the United Kingdom with the highest audiences in 2014 were all shown on either BBC One (thirteen) or ITV (seven) (Ofcom 2015a, 161).

The Role of Ofcom

As the United Kingdom’s communications regulator, Ofcom has a range of regulatory functions that mostly stem from the Communications Act 2003, which has been called “a sweeping programme of regulatory change . . . the most comprehensive legislation of its kind in British history” (Doyle and Vick 2005, 76). Under the terms of the Act, Ofcom was charged with carrying periodical reviews of the PSB system, the most recent of which was published as “Public Service Broadcasting in the Internet Age” (Ofcom 2015b), and is charged with conducting ongoing reviews of PSB in the United Kingdom (Ofcom 2015c). Ofcom has its own set of “PSB purposes and characteristics” (Ofcom 2015c, 4–5), with Ofcom summarizing the purposes of PSB as being “to deal with a wide range of subjects; to cater for the widest possible range of audiences—across different times of day and through different types of programme; and to maintain high standards of programme-making” (Ofcom 2015c, 4). One of the PSB characteristics is that content should be “Original,” with the principle being that the PSB channels in part broadcast “New UK content rather than repeats or acquisitions” (Ofcom 2015c, 5), which directly pertains to the discussion below about the role of the first-run originations quotas. These quotas do not relate to the content of programming, but rather ensure that it is original, and, thus, all forms of programming may be encompassed within them. That said, the PSB’s purposes and characteristics do ensure that across the board the commercial PSBs are contributing to the delivery of a public television system that stands apart from the non-PSB sector.

The United Kingdom’s Commercial PSBs

The UK’s commercial PSB channels are ITV (previously known as “ITV 1”), Channel 4, Channel 5, and S4C, channels that, along with the BBC’s television channels, form the United Kingdom’s public service television system. The category of non-PSB channels is comprised of every other channel broadcast on UK television lying outside of this group. 2 The funding models and ownership structures of the broadcasters who run these channels differ. ITV is a UK PLC and thus shareholder owned. Channel 5 is owned by the U.S. global–national Viacom, Inc., which bought the company from Northern & Shell in September 2014 for £450m (Viacom 2014). Channel 4 is broadcast by C4C, a publicly owned, statutory corporation, which is mainly commercially funded through advertising. Although C4C is alike to the BBC in the sense that it is publicly rather than privately owned, it does not receive any license fee income. Its main broadcast operation Channel 4 does, however, have a more stringent public service remit than ITV and Channel 5 (discussed below).

S4C, the Welsh-language broadcaster, is mostly funded from the license fee and direct grant, though some 2 percent of its income comes through commercial sources, including advertising (S4C 2015). Given this small proportion, S4C is not generally considered alongside the other commercial PSBs in the data that stem from Ofcom, and is, accordingly, not considered in this article on a full footing with the other commercial PSBs. In the case of ITV, Channel 4, and Channel 5, these channels are part of larger media organizations, with additional television channels and online provision. 3 These channels are augmented by time-shifted reruns on other channels.

To achieve the characteristics of public service television that it seeks, the Communications Act 2003 allows for separate public service remits for ITV (i.e., the ITV licenses and STV), Channel 4, and Channel 5. In the case of ITV and Channel 5, “The public service remit . . . is the provision of a range of high quality and diverse programming” (Communications Act 2003). Channel 4, distinct from Channels 3 and 5 in its ownership status as previously discussed, is set a more detailed and precise remit. Like Channels 3 and 5, it must produce high-quality and diverse programming, but in addition, it must produce programming that, for example, “demonstrates innovation, experiment and creativity in the form and content of programmes” (Communications Act 2003). The Digital Economy Act 2010 later made additional provisions for Channel 4’s remit. Finally, while the PSBs are governed by the regulations discussed, among others, the non-PSB channels are not free from all regulation: for example, they are required to adhere to Ofcom’s Broadcasting Code (Ofcom 2013a), which governs areas such as harm and offense and applies to all television channels broadcast in the United Kingdom.

The UK First-Run Originations Quotas

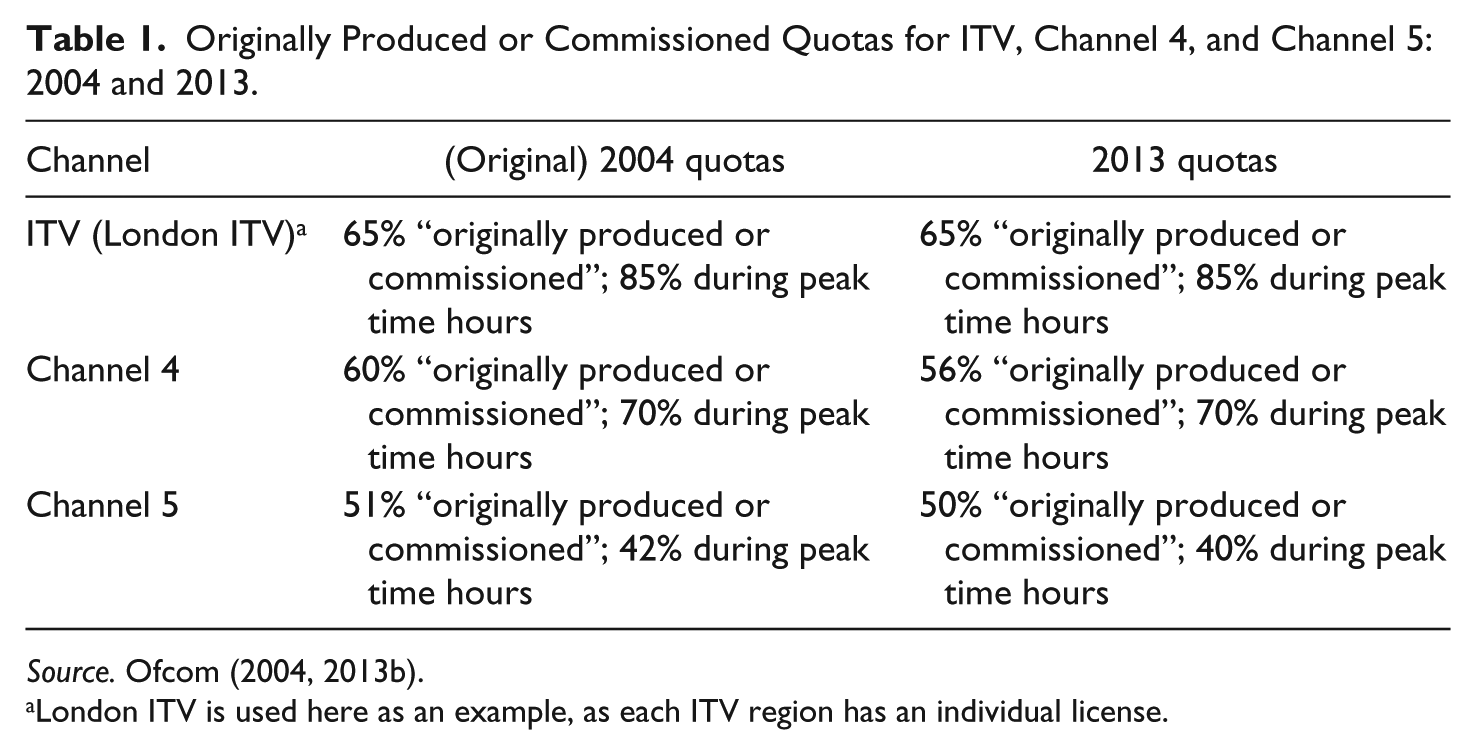

Ofcom (2015a, 413) has the power under the Communications Act 2003 to regulate the commercial PSBs on programming quotas for first-run originations, which are “Programmes commissioned by or for a licensed public service channel with a view to their first showing on television in the United Kingdom in the reference year.” These are distinct in the Ofcom terminology from first-run acquisitions, those programs that are bought by a broadcaster and shown on UK television for the first time. These quotas are one way in which the programming of the commercial PSBs is demarcated from programming from the non-PSBs (see Table 1), and which allow Ofcom to regulate for the PSB characteristic of “original” programming discussed above (Ofcom 2015c, 5).

Originally Produced or Commissioned Quotas for ITV, Channel 4, and Channel 5: 2004 and 2013.

Source. Ofcom (2004, 2013b).

London ITV is used here as an example, as each ITV region has an individual license.

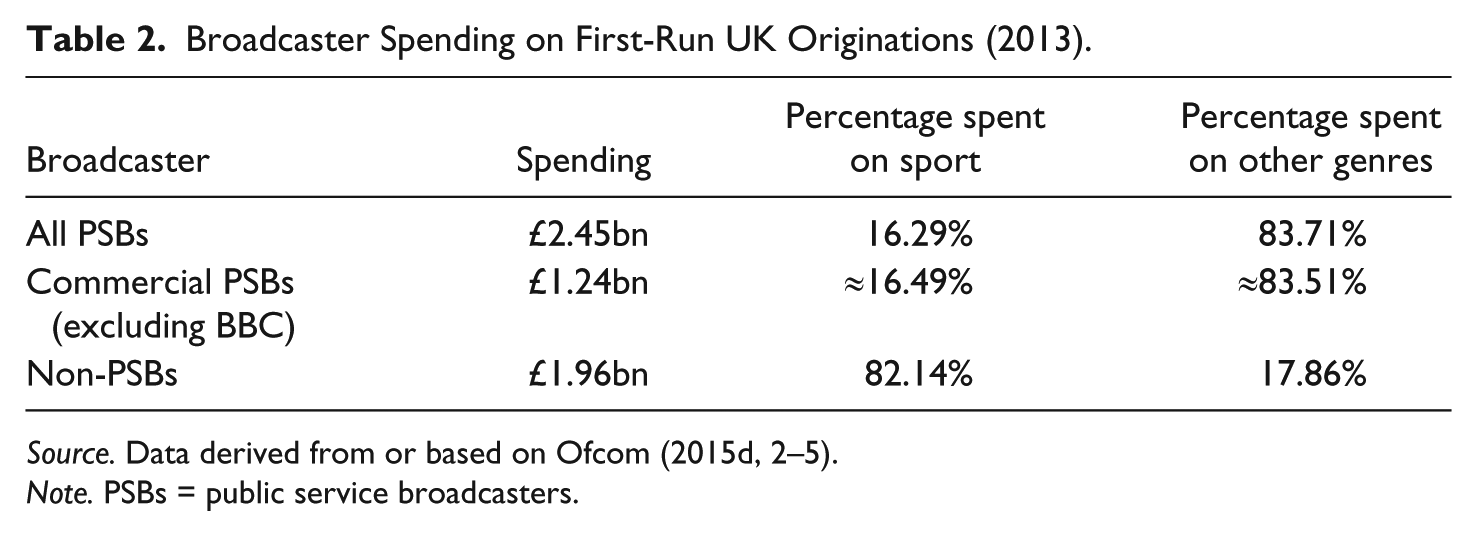

From the Ofcom data considered in this study, there are two main points to be made (given the time-lag in the release of statistics, the data considered here were the most current when this research was being conducted). First, the BBC channels and the other main commercial PSBs spent £2.45bn on first-run UK originations in 2013 (see Table 2); the non-PSB channels spent £1.96bn on first-run UK originations in the same year. However, spending by the PSBs in this category was only at 1998 levels, with spending reaching a peak in 2004 at £3.3bn (Ofcom 2015d, 2). By contrast, the non-PSB channel’s spending has been steadily rising, from £1.38bn in 2008 to £1.96bn in 2013 (Ofcom 2015d, 3). When sport is examined within the figures, the contrast between the PSB and non-PSB channels is stark. While sport dominates this figure for the non-PSBs, only 16.29 percent of PSB spending in this category is on sport (see Table 2).

Broadcaster Spending on First-Run UK Originations (2013).

Source. Data derived from or based on Ofcom (2015d, 2–5).

Note. PSBs = public service broadcasters.

The figure for the commercial PSBs (excluding the BBC) cannot be ascertained precisely, as it is not known exactly what percentage of the BBC’s spend goes on sport (due to, among other reasons, spending on sport being divided across multiple services). The projected figure for the money spent on sport by the commercial PSBs of 16.49 percent has been calculated by taking into consideration that they spend 50.6 percent of the total spend on first-run originations of £2.45bn (the BBC spending 49.4%; Ofcom 2015d, 2). This is then reassigned to the percentage of the approximate figure spent on sport by the all the PSBs (share of £399m; Ofcom 2015d, 5). Although this calculation may be considered something of a crude tool, consideration of various factors tends to suggest that it could be a workable approximation. Contained in a report (BBC Trust, MTM London 2011, 7) is the rare publication of the figure of £261m that the BBC spent on sports rights in the year 2009 to 2010 (such figures are not normally released). Given that the BBC’s sports rights budget was cut by 15 percent under the “Delivering Quality First” cuts of 2011 (BBC Trust 2011, 9), this would mean that the BBC’s spend on sport has become more modest than it was previously. 4

Second, when comparing the non-PSBs to the commercial PSBs, the 17.86 percent that the non-PSBs spend on first-run originations in program genres other than sport is paltry in comparison with the projected 83.51 percent spent by the commercial PSBs on other program genres. Given that the non-PSBs are collectively comprised of hundreds of channels, the some £350m that the non-PSBs spend is dwarfed by the ≈£1.03bn for the commercial PSBs (83.51% of £1.24bn; Table 2). That said, spending in this category is “up 43% in real terms from £245m in 2008” (Ofcom 2015d, 3). Spending on sport by the non-PSBs has been fueled mainly by the (English) Premier League soccer rights acquisitions, with the traditional subscription TV provider Sky facing massive competition from the comparatively new-entrant BT. The latest deal that involved BT and Sky paying £5.1bn runs for three seasons from 2016 to 2019 (Ofcom 2015a, 183). When BT’s additional purchase of rights for the UEFA (Union of European Football Associations) Champions League and Europa League are added in, this amounts to £2.01bn “a year on the rights to live coverage from these competitions alone” (Ofcom 2015a, 183).

Original Programming and the Public Service Imperative

The first-run UK originations quotas ensure that the market makes a significant contribution to delivering the public service remit within the UK media system. Harnessing such public service provision of the commercial PSBs contributes to a much greater plurality in public service provision than would be the case if only the BBC had a public service remit. As has been outlined, the commercial PSBs make up more than half of the spending on first-run originations by the PSBs overall. Without the commercial PSBs being held to these regulations, the public service television system would be greatly diminished. But what, in essence, is the “public service” value of original programming, or in other words, should the PSB characteristic of originality (in the Ofcom sense) be considered something that serves the public interest?

Ensuring that the audience has access to original programming, intended for first broadcast in the United Kingdom, ensures that it stands apart from programming laden with imported content (often mainly sourced from the United States), or repeats of previously broadcast content. As has been evidenced here, there is a substantial difference in the extent to which the commercial PSBs deliver original programming as compared with the non-PSBs, which are not required to meet quotas in this category. While the characteristic that the first-run originations quotas are designed to deliver on is not on its own enough to solely demarcate public service television from the rest of the market, it does make a substantial contribution to doing so. However, harnessing the market to make its contribution to the public service television system can also be mutually beneficial to the commercial PSBs. We now turn to a consideration of these benefits and of how they contribute directly to underpinning the business models of the commercial PSBs.

Benefits from the Public Service Remit

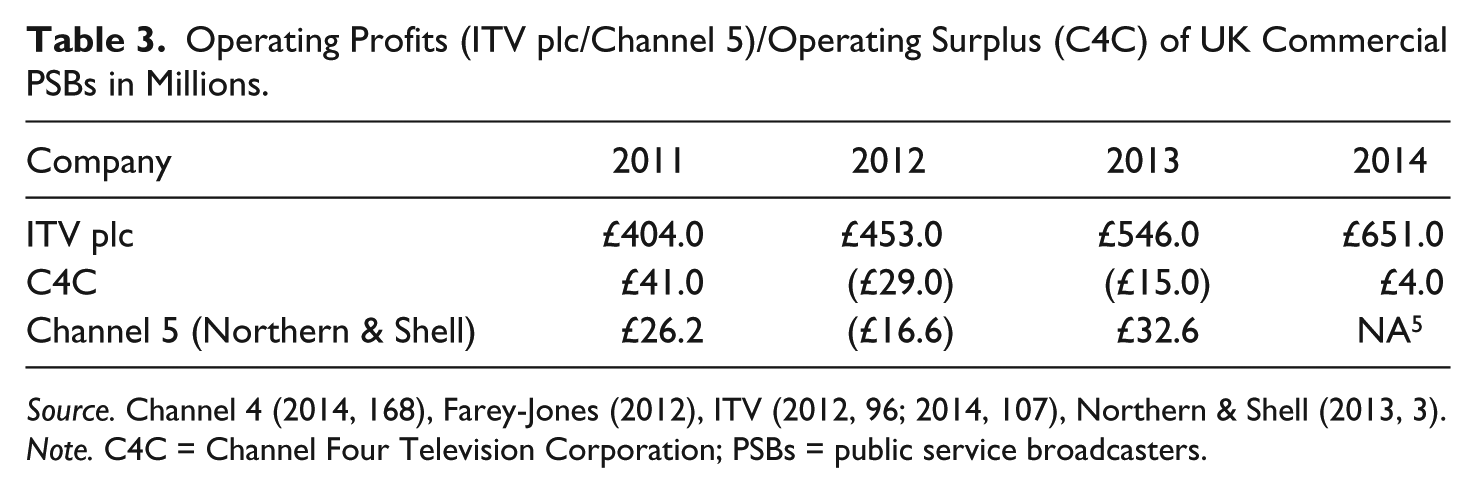

Although we have discussed up to this point how Ofcom regulation requires the commercial PSBs to comply with particular quotas, the critical political economy approach to the commercial PSBs also allows for greater attention to be paid to the benefits that the public service remit can bring to these broadcasters. Here, the main benefits are described as “predominantly access to spectrum (the valuable radiowaves that support wireless communication) to broadcast their services; prominence on electronic programme guides on television” (EPG) (Ofcom 2015b, 1). Ofcom (2015b, 28) notes, “Appropriate prominence continues to be one of the few key sources of regulatory benefit to PSB providers. We believe that in an increasingly complicated and fragmented digital world, the importance of these principles grows.” However, this statement appears to play down the importance of EPG prominence—especially the phrase “one of the few”—a benefit that when the financial positions of the broadcasters are considered (see Table 3) seems to be extremely important, especially in the case of ITV.

Operating Profits (ITV plc/Channel 5)/Operating Surplus (C4C) of UK Commercial PSBs in Millions.

Source. Channel 4 (2014, 168), Farey-Jones (2012), ITV (2012, 96; 2014, 107), Northern & Shell (2013, 3).

Note. C4C = Channel Four Television Corporation; PSBs = public service broadcasters.

Prominence is both historically and contemporaneously what the business model of a broadcasting company such as ITV is built upon. For example, during its financial year in 2014, ITV plc reported revenue of £2.6bn, and adjusted profit before tax of £712m (a 559 percent increase since 2009; ITV 2014, 5). At the cornerstone of these earnings are the company’s broadcast and online operations, which contributed more than £2.02bn to revenue (ITV 2014, 6). As the main ITV channel is a major contributor to this, we can posit that the company’s sole channel with a public service remit is the anchor of its earnings. While this is somewhat speculative—the profitability of the individual channels is not reported—there is evidence reported by Ofcom that tends to back up this assertion. In 2014, the advertising share of the total television market gained by ITV/STV/UTV/ITV Breakfast was £1.37bn, which dwarfs the £0.65bn gained by the PSB portfolio channels collectively (Ofcom 2015a, 148).

Indeed, implicit in ITV’s business model is that the investment in the ITV “brand” stems from the main ITV channel: this is described by the company as a form of progression, with one step leading to the next: “Building our ITV television and main channel brand; Extending that brand to our portfolio of channels and digital assets to reach all demographics; Growing our portfolio of programme brands and extending those brands beyond the television set” (ITV 2014, 8). Indeed, while only the main ITV channel has PSB regulatory responsibilities to fulfill, it is this channel that drives brand recognition in its portfolio of channels, gives it a prominent role as a provider of news, and gives maximum exposure to major television shows (such as The X Factor), from which its spin-off shows can be broadcast on its other channels.

The three commercially funded PSBs were mostly profit making in the years 2011–2014—or in the case of ITV plc, very profitable (Table 3)—while delivering their first-run originations quotas. As we have seen, the impact of the first-run originations quotas ensures that these broadcasters generate a large amount of original programming, which can be rerun or developed through spin-off programs through the portfolio channels of these broadcasters. As UK audience demand is still largely for UK-originated television, the quotas ensure that these commercial PSBs are replete with content—content that must compete on quality with the BBC in the PSB system—which can then be sold to international markets, often attracting high returns (e.g., as in the case of Downton Abbey).

Despite the mass proliferation of television channels in the multichannel era, none of these come close to matching the audience share of the three commercial PSBs. For example, the entire Sky portfolio of channels only had an 8.2 percent audience share in 2014, a decline from 10.6 percent in 2004 (Ofcom 2015a, 202). Thus, EPG prominence, alongside the demand for UK-originated content, consolidates the place of the commercial PSBs in the multichannel media system. If it can be described as “one of the few key sources of regulatory benefit to PSB providers” (Ofcom 2015b, 28), it is at the very least an exceptionally important one.

Even if the importance of EPG prominence becomes eroded over time, through the growing importance of online streaming, for example, the commercial PSBs have had their place historically secured at the center of the media system. In terms of “brand recognition,” their place at the forefront of television before the multichannel era on satellite and cable (and in the case of Channel 5 before mass proliferation of multichannel choice through digital terrestrial television) has been secured. While these benefits can be relatively hard to quantify in some areas, the legacies of these businesses in terms of capital accumulation and profitability are central to their current positions (e.g., Viacom’s purchase of Channel 5 led to a large windfall for Northern & Shell, stemming from a business built on PSB prominence).

Future Policy Challenges for Public Service Television

The events leading up to the publication of the White Paper on the BBC (Department for Culture, Media & Sport 2016)—the government paper that sets out the basis of what the BBC’s next Royal Charter will include—rightly placed the BBC at the center of public and political debate regarding public service television. However, the debate is too often divorced from a wider conversation on how the public service television system should be planned and implemented, and often discounts the vital role played by the commercial PSBs. Although Ofcom suggests that the BBC is “the cornerstone of the PSB system and is the key driver of investment across the system” (Ofcom 2015b, 3), it is a system that depends greatly on ITV, Channel 4, and Channel 5. The current PSB regulatory system ought not be taken for granted by scholars and policy analysts, especially given that a new Communications Bill may be introduced at some point in the near term in the UK political cycle. With a majority Conservative government elected in May 2015, the next Communications Act could revise this current system.

Under the previous Coalition government, Jeremy Hunt, then Secretary of State for Culture, Media and Sport, set out in September 2011 his priorities for what would have been a Communications Bill in that Parliament, a bill that still has not materialized by August 2016. Acknowledging that prominence in the EPG was still an important “lever”, Hunt (2011) states, “We will need a lighter-touch model which, in particular, means that ministers and regulators will have to move away from micromanaging programme outcomes.” Although it is unclear precisely what Hunt was referring to at this point, the originations quotas could easily be encompassed within this approach. If such thinking was applied by the current Secretary of State for Culture, Media and Sport and the wider government, quotas for first-run UK originations that apply to the commercial PSBs could come under pressure for liberalization or removal. The critical political economy approach draws an imperative here for considering the politics of the media system in the United Kingdom. In this sense, a focus is required on and there is a need for analysis of the politics of media policy of the current Conservative government. It is one that has been shown to be deeply entwined with the interests of the press (Freedman 2014, 1), and strongly antipathetic to the BBC (especially seen during the tenure of the former Secretary of State for Culture, Media and Sport, John Whittingdale). While speculation may offer little at this point, we might confidently state that were the public service television system to be liberalized in a future Communications Act, it would not come as a great surprise. The first throes of this can be seen in the manner in which the future of C4C has been handled by the government in recent years.

As well as the wider public service television system being up for debate and having the potential to be rearranged, it is also important to note the government had been considering various options for the future of C4C (and with it the broadcast entity Channel 4 itself), with the option that it might be fully privatized by the government. This would mean that its ownership as well as its funding model would be sourced from solely within the private sector, and its status as a statutory corporation would end. It was in the context of this the House of Lords (UK Parliament) Select Committee on Communications released a report on the matter. The committee recommended the continuation of the current ownership model, ruling out both full- and part-privatization, or the alternative option of mutualization (House of Lords, Select Committee on Communications 2016, 7). That said, John Whittingdale argued in evidence to the Committee for at least a part role for the private sector in C4C, through commercial partnership or investment (House of Lords, Select Committee on Communications 2016, 17–18).

Later in May 2016, reports suggested that the privatization of C4C had been ruled out by the government, under a prime minister who was two months later replaced by Theresa May (Sweney 2016). However, until the present government or its successor gives full and unconditional support for C4C to remain on its present statutory footing, it will remain as a potential target both for commercial investors and for the proponents of a UK broadcasting system that is nothing less than fully liberalized. It is possible that a privatized Channel 4 could fully retain its PSB remit, a point that Whittingdale considered in his evidence to be plausible, suggesting that for a buyer of C4C “the last thing they would want to do was to undermine it by moving downmarket or changing the nature of the programming” (House of Lords, Select Committee on Communications 2016, 17). That said, there is no particular reason why that would be the case, with the possibility that the government would receive a much higher sale price if it were freed from its public service obligations.

Conclusion

It has been argued in this article that the current public service television system functions both for the benefit of the audience and for the commercial PSBs: the audience has access to significant levels of original material other than sports programming, while the broadcasters have in place the basis of their financial models. A cutting back of the system would be in essence ideological given the successful financial functioning of the system as it currently stands, underpinned by the audience demand for the five main PSB channels. Moves to dismantle or diminish this system may have the unintended consequences of diminishing the financial success of the commercial PSBs, while weakening the overall size of the television market (with probable declines in investment). Specifically on the first-run originations, a weakening of those regulations could diminish quality in the sector, lead to additional acquisitions and reruns on the most watched channels, while inadvertently reducing advertising revenues. The point being, the regulated broadcasting system that includes both more-regulated PSBs and less-regulated non-PSBs can be economically as well as culturally valuable.

The use of the critical political economy approach allows the testing of the benefits and drawbacks of market-based broadcasters delivering a PSB remit. Such analysis draws attention to the strength of the current system, allowing for a strong evidence-based position from which to argue for a public service system based on mixed-funding models, which provides the audience with programming that is distinct from what the market would provide if it were left solely to its own devices. However, the current system is one that could yet be subject to change under the current Conservative government, as ideologically driven detractors continue to exert pressure on the very concept of public service television.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.