Abstract

This article explores the rise in foreign television production company ownership at the beginning of the twenty-first century as a new mechanism of internationalization. It joins mechanisms such as foreign program sales and transnational satellite channels in shifting television further from its domestic origins. To date, examination of television’s internationalization has focused on programs and programming. Foreign ownership may be a less obvious “cultural” form of business internationalization, but it nevertheless affects the television culture made available in many places and poses consequences for cultures of consumption. Foreign ownership also opens up new avenues of inquiry for global television scholars to question the shifting geographies of power in the field of television production.

It is widely known that media industries have steadily consolidated and conglomerated over the last half century (Herman and McChesney 1998). This process of narrowed ownership has eroded national boundaries so that the dominant players are multinational corporations that transcend particular media industries to encompass ownership of media across video, aural, and written forms. These conglomerates also achieve vertical integration across the production and circulation of media within particular media industries. Such growth was especially the case in television industries—the focus here.

This pattern of conglomeration has resulted in the steady internationalization of television businesses, with increasing pace in recent decades. Such organization contrasts with the origins of television industries in resolutely national broadcast systems, an orientation that historically shaped the medium’s relationship to culture, government regulation, and market dynamics in both subtle and direct ways. As the reach of television traversed national borders, media studies scholarship turned its attention to the different mechanisms that have contributed to the international scale of the industry’s operations. Cross-national program trade developed as soon as a suitable recording mechanism emerged (Havens 2006) and the sale of programs to foreign markets is arguably the first mechanism by which television and its businesses were internationalized. A second mechanism emerged in the 1990s as satellite distribution technologies made it feasible to expand channel offerings and circumvent national monopolies and oligopolies of broadcast service (Chalaby 2005, 2009). Satellite distribution, and the coinciding privatization of television in many countries with public broadcasting origins, significantly increased the reach of foreign television providers and expanded the internationalization from that of mere program trade.

Other mechanisms of internationalization include the foreign ownership of television infrastructure and the foreign acquisition of broadcasters. Both play important roles in internationalizing this sector, though have not received as extensive scholarly attention (Curtin 2007; O’Regan and Potter 2013; Thussu 2007; Torre 2012). Most recently, the emergence of multinational SVOD services has further challenged the national foundation upon which social constructions of television were commonly based.

Another mechanism of internationalization occurs through foreign acquisition of production companies. A massive wave of such acquisitions began near the turn of the century, and continues, though at a slower pace. Many of these acquisitions were spurred by the prominence of format sales and local format production that made it valuable for the owners of intellectual property to produce the format in several markets. A more nuanced understanding of this mechanism and its implications for the dynamics of cultural production and circulation is needed. This phenomenon has primarily been studied in terms of its ramifications for business and industry, including a recent and well-evidenced account of the UK context by Doyle et al. (2021), and in Doyle and Barr (2019). This article is interested in business dynamics, but foremost investigates the cultural implications of foreign production company ownership, and specifically with a focus on scripted programming.

The consolidation of production companies into corporations with massive, multinational holdings has received the most extended attention from Chalaby (2009, 2012) and Esser (2007) as a European phenomenon. In the first section, we build on this earlier work to chart a more expansive and accelerated pattern of ownership adjustment within the field of television production beyond Europe. We understand these developments as part of a longer trajectory of internationalization in the television industries. This enables us to more clearly establish a pattern of overlapping and iterative change with significant implications for understandings of the shifting economic imperatives and cultural consequences of contemporary global television.

We then examine the implications of these global developments in Australia, a country that benefits from its English-language production, but with far more limited scale than the US and UK. We first provide macro-level evidence of the consolidation of production companies and of their increased multinational ownership. Our analysis establishes the acquisition of production companies as a mechanism of internationalization that further erodes television’s domestic origins, but we maintain it is difficult to assert that the operational norms of any single company are “typical” of the overall trend. Rather, our goal is to expand the primary sites for investigating internationalization beyond macro-level structural change and draw attention to the potential complications and complexities this mechanism raises. By linking questions about culture, cultural policy, and foreign ownership with research that prioritizes the economic and business operations of media firms, we highlight how the international consolidation of production companies might produce variable cultural and industrial dynamics at odds with the domestic orientation of national television industries. 1

Establishing Foreign Acquisition of Production Companies as a Mechanism of Internationalization

Rarely are production companies recognizable to viewers beyond a brief screen credit that precedes their favorite program. Most viewers know even less about who these companies are or what they actually do. In the “field” (Thompson 2010, 4) of television, a production company typically sells an idea to a commissioning agent and organizes the production of the program—from hiring crew and casting, to filming episodes, to completing post-production mixing and editing—in exchange for a fee. Depending on the terms of their initial agreement with the commissioning agent, production companies often sell the completed program or format to a distributor to earn additional revenue from secondary buyers in other markets. 2

Part of the conceptual fuzziness around what production companies do results from the variable organizational structures that constitute a “production company.” Outside the US, they are commonly small- to medium-sized firms with no more than one or two employees that “staff up” once they receive a commission. Sometimes a producer forms a production company for a single production and dissolves it shortly after filming wraps as a means to mitigate individual financial liability and taxes. Other production companies, like many considered here, are part of much larger corporate structures that expand into multiple markets and often consolidate other functions, like distribution, within the same company. In the US, entities housed within giant media conglomerates such as Disney or Comcast, and commonly identified as “studios,” dominate this sector.

Because production companies can be everything from a multinational such as FremantleMedia to sole proprietors that number in the thousands if not tens of thousands globally, there is no systematic way to quantify the scale of production company acquisition that occurred throughout the early 2000s. Quantifying the number of production companies once in the market around the world in comparison with a post-consolidation figure is uncertain evidence: much of the production company sector—like the content they make—is transitory and consequently precarious. Nor is it easy to identify precisely when the first transnational acquisitions that compose this trend occurred such that it became a phenomenon with a scale distinct from typical business practices. Nevertheless, this process certainly transpired. One way to see it is by charting the acquisitions of what are now major production companies. Chalaby’s (2012) first publication recognizing this phenomenon of production company acquisition to build a multinational network in Europe appears in 2009. He notes that Grundy (an Australian company purchased by British Pearson in the 1990s) was a pioneer of this strategy in the 1980s. Grundy owned a number of game shows and would set up production companies in countries that licensed a local version of these series. Endemol and Pearson TV (which purchased Grundy) became the “first global TV production houses in the 1990s” (Chalaby 2012, 27). But Chalaby (2012) argues the 2000s as the decade in which the “super groups” emerged (p. 27).

One impressive indicator derives from revisiting Chalaby’s (2012) research in which he constructed a table of major international “super groups” that included thirteen companies. Those companies had acquired many other production companies in the preceding decade to increase their size and status and indicate significant consolidation in the sector. Yet just eight years later, this already highly-consolidated list had been reduced further to eight, as the remaining companies had subsumed the other five. Throughout the early century, production companies of all scale were steadily gobbled up, so that the food chain of acquisitions extended from medium companies acquiring smaller ones and then being acquired by large companies, so that with one acquisition, a company might consolidate what had been ten to twenty companies a decade earlier.

Also consider that one of the most substantial production companies in 2020 did not even exist before 2008. In just twelve years, the French company Banijay acquired Air Productions (France), Cuarzo Producciones (Spain), Brainpool TV (Germany), Nordisk Film & TV (Denmark), Bunim/Murray Productions (US), Screentime (Australia and New Zealand), Non Stop People (France), H2O Productions (France), Ambra Multimedia (Italy), DLO Producciones (Spain), Stephen David Entertainment (US), Castaway Television Productions (UK), 7Wonder (UK), Terence Films (France), Portocabo (Spain), and Good Times (Germany). In addition to largely allowing these companies to operate under their own names, Banijay launched Studios North America in 2014 and three new units in 2018: Banijay Studios Italy, Banijay Asia, and Banijay Productions Germany, as well as four companies focused on scripted series in the UK: BlackLight Television, Fearless Minds, Yellow Bird UK, and Neon Ink, and an unscripted producer Natural Studios with Bear Grylls and Delbert Shoopman. Among its biggest acquisitions were Zodiak Media in July 2015 and Endemol Shine Group in 2019 (Zodiak, Endemol, and Shine had all been separate companies on Chalaby’s 2012 “super groups” list).

The names of these eighteen-some acquired production companies (plus the nine others Banijay launched) are likely meaningful to few. Similar lists can be offered for many of the major production companies. The point isn’t the details but the pattern of multinational consolidation in production company ownership it illustrates.

Of course, these companies also competed with the US-owned content conglomerates—Disney, NBCUniversal, Viacom, Twenieth Century Fox—that came to dominate US production in the mid 1990s following the elimination of the Financial Interest and Syndication Rules and the broader conglomeration of that period (Holt 2011). The dominance of these companies was aided by their vertical integration with commissioners: many of the US broadcast networks and major cable channels were co-owned with the studios. With the US market reconfigured by consolidation and conglomeration, and in many ways at saturation by the end of the 1990s, these companies started aggressively internationalizing their businesses in the 2000s, as they too acquired production companies outside the US. For example, News Corp. purchased Shine (UK) in 2011, which had grown to include twenty-seven production companies in eleven countries and then, in a joint acquisition with Apollo Global Management, acquired Endemol and Core Media Group to make Endemol Shine. This was the largest acquisition at the time, and Endemol Shine became the world’s largest production group with an estimated valuation exceeding $2B and a network of more than one hundred twenty companies across six continents (Esser 2017). Banijay then acquired Endemol Shine in 2019 following Disney’s purchase of Twenty-first Century Fox.

The other Hollywood conglomerates made comparatively minor acquisitions, but also internationalized their operations beyond merely launching and operating global satellite channels. NBCUniversal International Studio bought Chocolate Media (UK), Carnival (UK), Monkey Kingdom (UK), Lark Productions (Canada), Matchbox (Australia), and Lucky Giant (UK), with a strategy apparently aimed at English language production. Warner Bros. International Television, established just in 2009, purchased Shed Media (UK) and Eyeworks (Netherlands), which was Europe’s sixth largest production company at the time, and were two companies on Chalaby’s 2012 list. The acquisition gave Warner Bros. television production units in fifteen additional territories (Tartaglione 2014). (To further illustrate the food chain of acquisitions, Eyeworks acquired the New Zealand company Touchdown Television, the Argentinian company Cuatro Cabezas, as well as a Dutch production company and a 50% stake in the US 3 Ball Productions in the years before Warner Bros. acquired it).

The business motivation for these acquisitions derives from different reasons for different companies but generally from the desire for diversification and to increase cash flow. Esser (2017) points to the value of expanding intellectual property libraries, basic diversification that comes from being a player in a multiplicity of markets, and the advantages of vertical integration in companies that grow to encompass multinational production and distribution. Narrowing from macro structural advantages, she identifies implications for production such as the ability to bundle programs for sales and to advance considerable budgets on development.

In relation to motivations for acquisitions tied to format production in particular, Chalaby (2011), Moran (2009), and Esser (2016) identify how formats quickly became central to the business as commissioning services used formats as a cost-effective way to manage risk, develop popular programming, and maintain local relevance to audiences. Formats came pre-tested, and the explosion in their popularity in the early 2000s ignited this sector of the business and led to industrial reconfiguration that involved the acquisition of “local” production companies. As Esser (2016) explains: The extraordinary financial success of the above, small, independent producers spurred other European producers to create and sell such formats. Emulating Endemol and FremantleMedia, which had expanded internationally by setting up and acquiring TV production companies during the 1990s, a new business model gradually emerged that increased both revenues and profits: Rather than sell franchise rights internationally, format owners now aimed to produce their shows themselves in as many markets as were viable (3590).

Once format sales were established, the ability to sell both the intellectual property of a format and produce local versions of the series allowed format owners to “double their money” according to Fremantle Asia Pacific CEO Christopher Oliver-Taylor. In short, companies owning the intellectual property for major formats recognized that there was greater success and revenue available if they did not merely sell a format for production in a national market, but if they could produce the series as well. Moreover, purchase of local companies gave them local market knowledge, contacts, and access to creative labor that facilitated this process. The desire to be able to produce formats in major markets resulted in the significant consolidation of production companies so that only a few companies dominated the production sector across dozens of countries.

The strategic development of format sales and the related acquisitions of production companies to support their production was mostly a phenomenon of unscripted programming. Scripted format sales lagged significantly due to the greater complexity and costs of localization but did occur (The Slap; Broen/The Bridge; The Nanny) (Chalaby 2016). Nevertheless, many of the acquired production companies were strategically diversified across scripted and unscripted production, and the implications of this ownership structure extend beyond format sales. This consolidated, multinational ownership structure quickly disrupted the established competitive field within nations as production companies with extensive multinational distribution relationships became a norm of the business rather than the exception. The competitive advantage these companies possess—considered in depth in the following section—alters the market dynamics within national ecosystems.

The concern with maintaining a particular type of ownership—local, or for Doyle and Barr (2018), independent—overlooks other adjustments in the field that have altered conditions and obscure the changing agency of local firms and how they exercise power within national production cultures. In many countries, the number of scripted hours that commissioners can afford is quite limited and dropping as a result of audience fragmentation, a budget arms’ race for high-profile titles, declines in advertising revenue, and proliferating competition. Although maintaining a multiplicity of producers is a noble goal, many features of the contemporary marketplace conspire against its feasibility. The expansion of multinational production companies into national ecosystems once domestically-owned increases the operational challenges and barriers to entry for small and medium sized enterprises that lack the increasingly normalized advantages of being part of a larger and multinational conglomerate. There are considerable advantages to scale in television production. Such ownership likely increases the creative and financial capacities for those local firms with access to a multinational firm’s deep resources, professional networks, and expert knowledge, allowing “local” content greater access to international finance and global audiences. The corresponding implications are difficult to assess and highly dependent upon the economic and cultural priorities at play within distinct production cultures around the world. To gain some perspective, we conducted a quantitative, macro level investigation of changes in production ownership and scripted series commissions in Australia and then assessed what the quantifiable data does and does not tell us about the changes taking place in the country’s television industry.

The Case in Australia

We do not make the argument that Australia is either particularly ordinary or unusual. Merely that it provides a place and case through which to develop a more grounded understanding of how the presence of multinational production companies affects a specific ecosystem. Given our particular interest in scripted production, our research team constructed an original database of Australian scripted production that spans from 2009 to 2019 and includes data such as production company, number of episodes, episode duration, commissioning entity, and distinguishes adult and children’s titles. 3 During that time, Screen Australia reported two hundred ninety-eight scripted titles produced in Australia by one hundred twenty different production companies. This count includes scripted drama and comedy series for adult and children audiences, but not made-for-television movies. We’ll refer to these forms simply as “drama.” Sixty-three percent of the titles are adult programs, and 37% children’s. 4

To better appreciate the production marketplace, we focused analysis on hours produced, which offers a better gauge of production activity than number of titles given the significant variation in production company sustainability provided by titles lasting only a single series and others running for multiple years (“returners”). We also removed the two long-running soap titles, Neighbours and Home and Away, from the hours-produced analysis because the exceptional number of hours skews results so significantly. 5

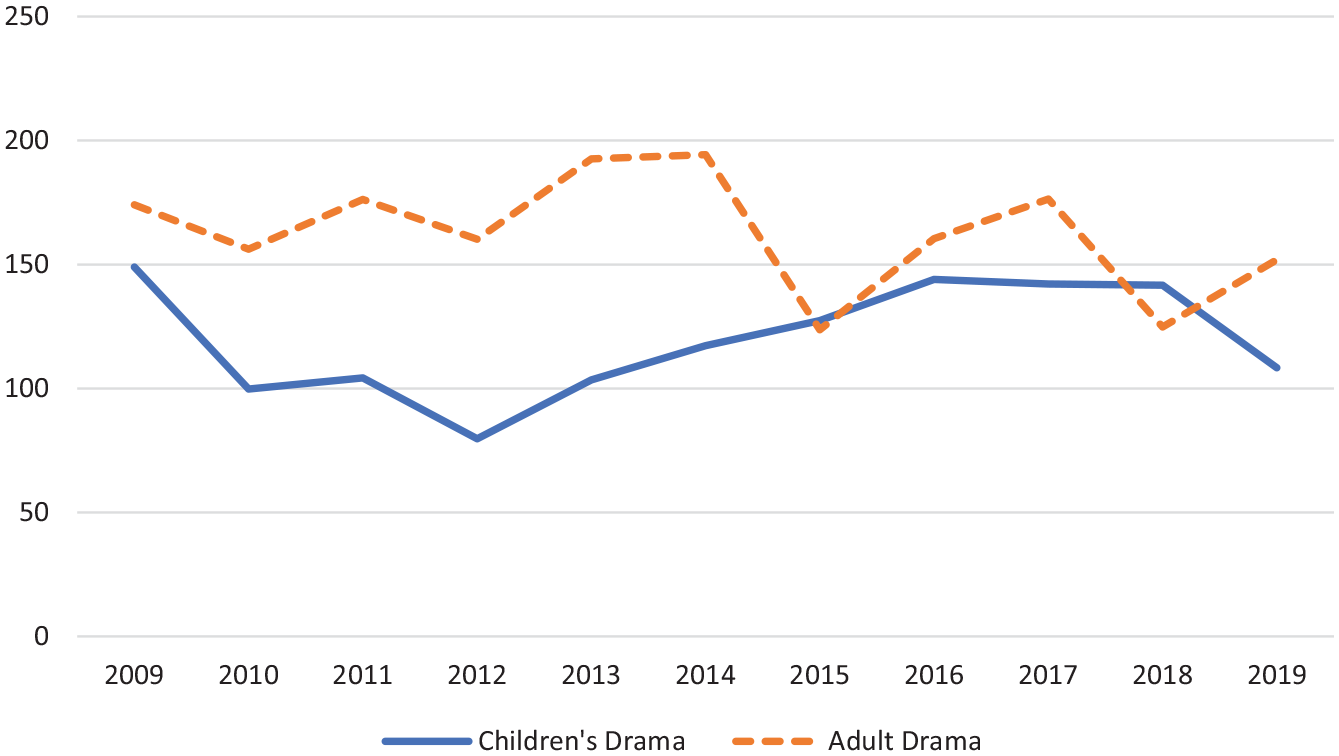

From 2009 to 2019, 3,108 hours of Australian drama were produced. General trends are evident in Figure 1, which charts the number of non-soap hours of adult and children’s programs produced by year. On average, children’s programs accounted for 42.4% of the hours produced. The total number of adult hours is nearly the same in 2019 as it was in 2009, though the decade is marked by fluctuation from a high of one hundred ninety-four hours to a low of one hundred twenty-four hours. Children’s programs faced strong decline until 2012 with only eighty hours, and then rebounded to hold steadily at one hundred forty hours until another decline in 2019. 6 Analysis of the underlying data shows that over the full period, adult drama hours produced by public service broadcasters (PSBs) the ABC and SBS increased 27% while commercial broadcasters showed a steady decline with adult drama hours dropping 41.8% over the period. Only one commercial broadcaster consistently uses an in-house production unit (Seven, discussed below). Otherwise, commissions of both PSBs and commercial networks were spread across non-aligned production companies, although no regulation requires this.

Hours of adult and children’s drama each year (2009–2019).

We then considered a series of questions related to who produced this content. Like in many countries, Australia’s television production sector is wide-ranging. Australia’s Screen Producers Australia (SPA) reported five hundred two member organizations in 2019 (Annual Report), although most of these are small firms engaged in limited and irregular work. Data from SPA characterizes the membership as including seventy-seven companies described as “sole traders” (38%), ninety-nine “small businesses” (2–4 FTE, 49%), nineteen “medium” companies (5–19 FTE, 9%), and seven large companies (20+FTE, 3%). 7 Good data that demarcates the percentage of the sector engaged in different types of production is not available, though the majority of the sector is engaged with unscripted production.

Despite the suggestion of a multifaceted production ecosystem, scripted production is dominated by a few companies, by large companies, and, increasingly, by large companies that have been acquired in the last decade by foreign conglomerates. Of the one hundred twenty production companies, seventy-two different companies make the adult dramas and fifty-six companies make the children’s titles. Eight production companies are credited with both adult and children’s titles. If the number of adult or children’s titles were distributed evenly across these seventy-two or fifty-six production companies, the adult production companies would be slightly more productive with 2.63 series per company and only 1.95 among children’s producers. But of course, this work is not spread evenly. Forty-five of the companies (38%) produced ten or fewer hours over the eleven-year period. Several of these producers also engage in unscripted production and others in feature film, but this data quickly dispels the sense of abundance suggested by SPA’s membership or the significance of having one hundred twenty different companies producing Australian drama.

There isn’t an obvious trend in the amount of production over the last decade despite the significant changes to the Australian ecosystem by digital technologies and the acquisition of many production companies by foreign conglomerates. By focusing on adult and children’s drama, what we see is the steadiness of an artificial market created by local content subquotas that have required particular levels of commissioning of Australian adult and children’s drama among commercial channels (these requirements do not apply to the ABC and SBS). 8 Those subquotas were altered in 2020, which, along with COVID-19 related production stoppages, are likely to produce profound changes going forward.

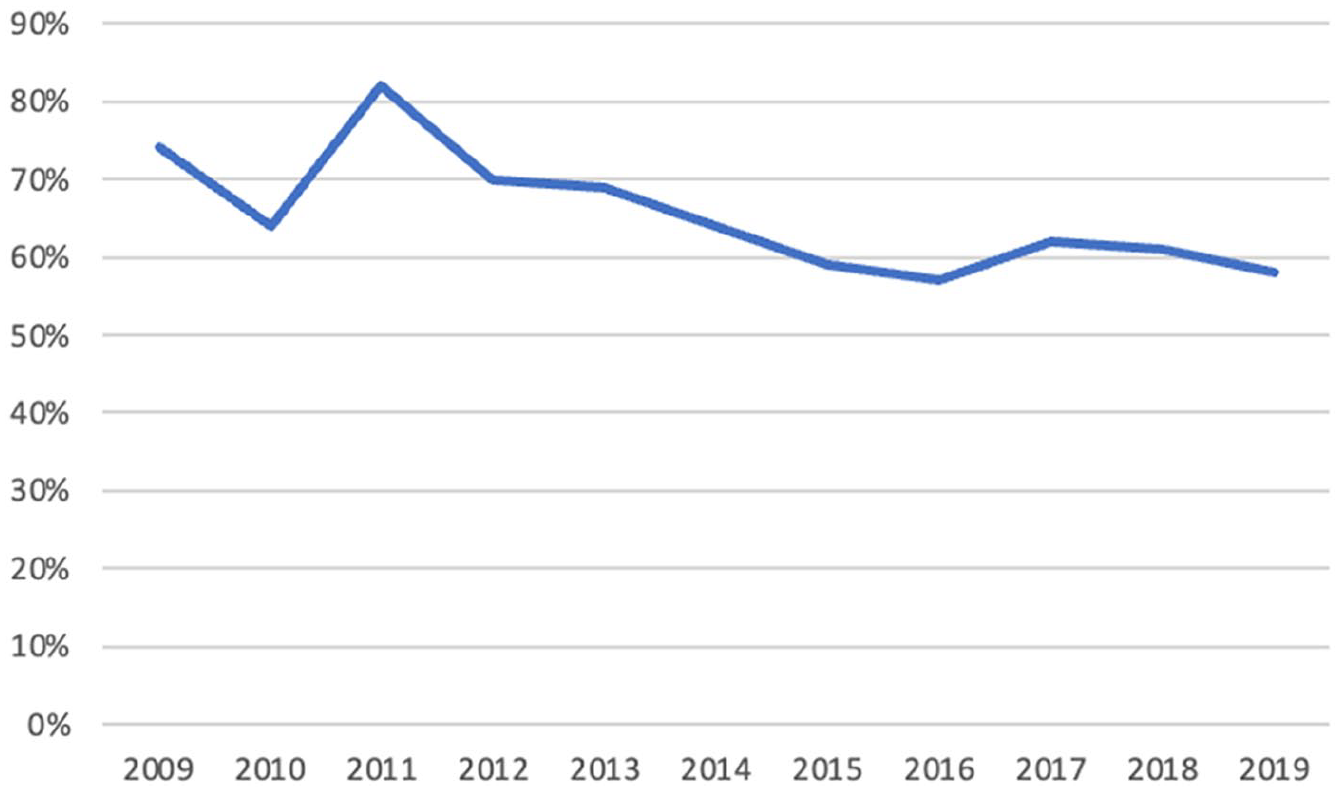

To investigate the question of how concentrated Australian drama production is—given so many firms produced fewer than ten hours across the eleven years—Figure 2 plots the percentage of hours produced by the ten companies with the greatest production output in each year. Although there is considerable fluctuation within the scope of study, the percentage of hours produced by these companies stays above 57% and peaks at 82%. This data reveals the extent to which a few firms steadily account for most of the drama production, while a significant number produced very few.

Percentage of total hours produced by top ten production companies each year (2009–2019).

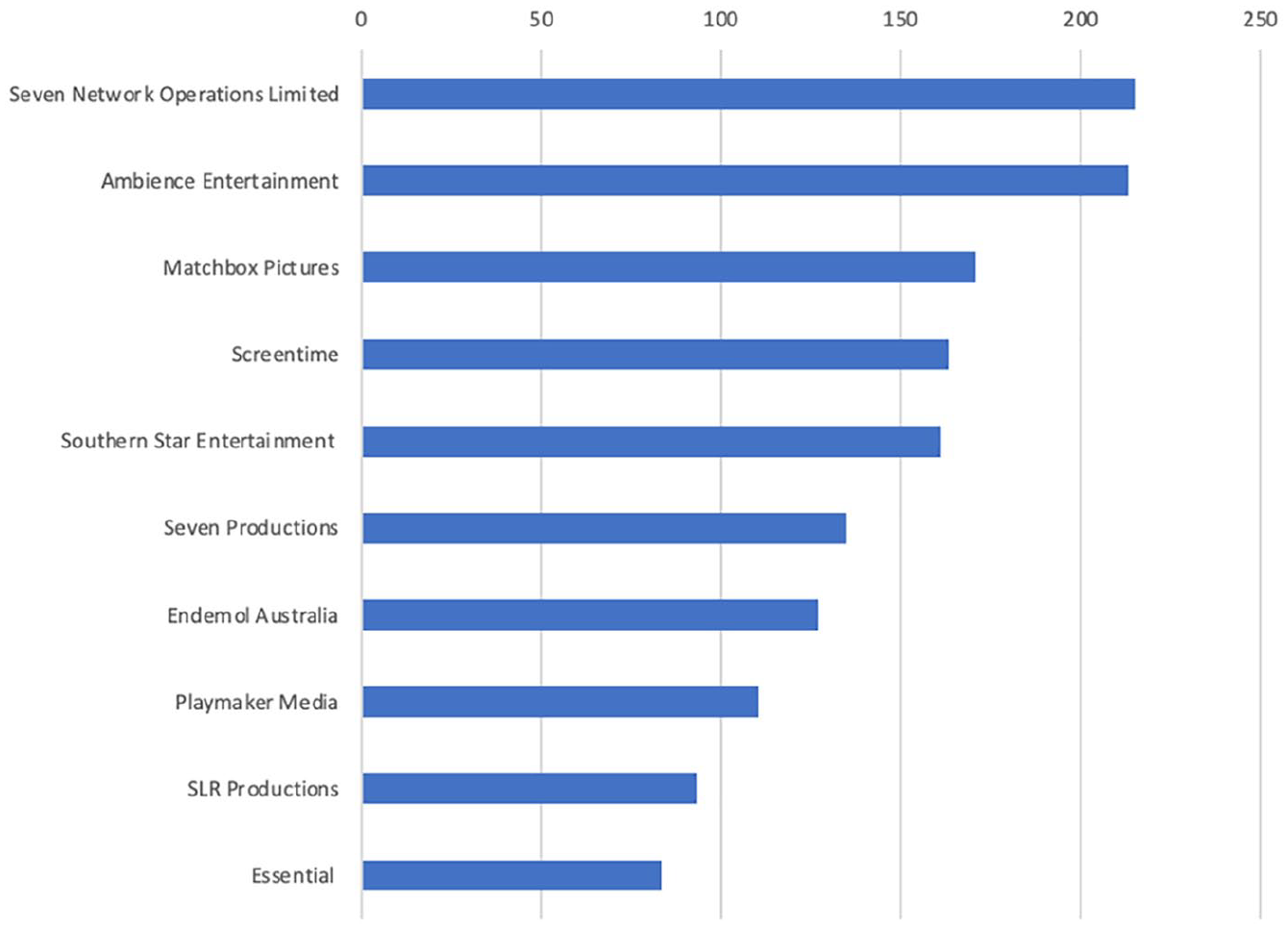

Figure 3 then lists the ten companies with the most productions across the full reference period. Two of these companies exclusively produce children’s titles (Ambiance Entertainment; SLR Productions). Some produce a few children’s titles amidst a slate skewing heavily toward adults (Matchbox, Endemol, Southern Star), while others only produce adult drama (Screentime, Seven Network Operations, Seven Productions). 9 A closer look at the underlying data reveals significant changes within the decade. Several of the top producing companies made far more drama in the first half of the reference period than the second, for example. Yet, while there may have been a decline in their activity in recent years, they remain top producers. So far, few other companies have achieved enough sustained production activity to disrupt earlier patterns of concentration.

Top ten production companies by total hours (2009–2019).

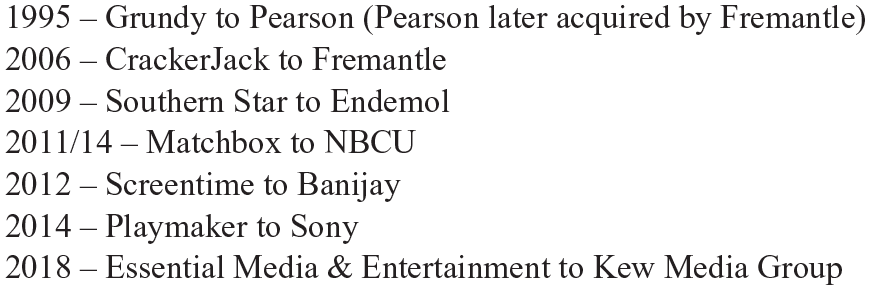

Notably, several of these companies have been acquired by foreign companies in the last decade (see Figure 4). All of the companies producing adult drama have been acquired in the last decade except Seven, which is currently up for sale. The peak years of Australian production company acquisitions span 2006 through 2018.

Major acquisitions of Australian production companies.

Most of these acquisitions align with the logics described in the first section and are tied to deals valuable because of the capability to not only license, but also self-produce unscripted formats in many countries. Fremantle, Endemol, and Banijay are predominantly producers of unscripted television but, as evident, occupy a significant place in the ecosystem of Australian drama production as well.

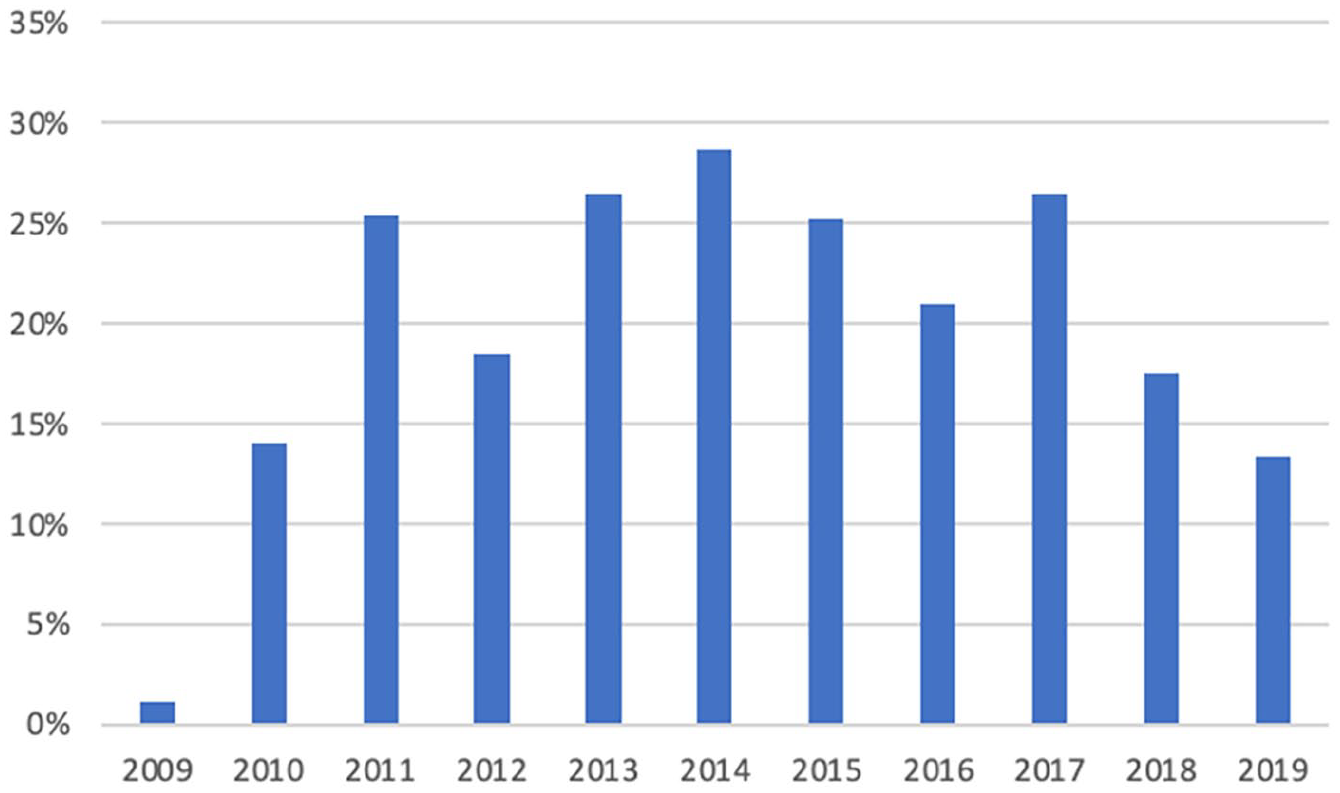

As Figure 5 indicates, the percentage of hours produced by foreign-owned production companies has increased significantly, from barely any to a high of 28% in 2014. 10 Based on a cursory review of titles and production companies before 2009, it does not seem 2009 was an anomaly in its low foreign production, but typical of market dynamics before foreign acquisitions accelerated over the last decade. Notably, the analysis is aimed at assessing the extent to which large multinational production conglomerates have come to influence the production ecosystem. A few other “foreign” production companies (such as New Zealand’s South Pacific Productions) occasionally appear in the data in the context of international co-productions, but the impact of the large conglomerates raises more concern here than a handful of smaller foreign production companies engaged in joint ventures.

Percentage of non-soap drama hours produced by multinational conglomerate owned production companies, each year 2009 to 2019.

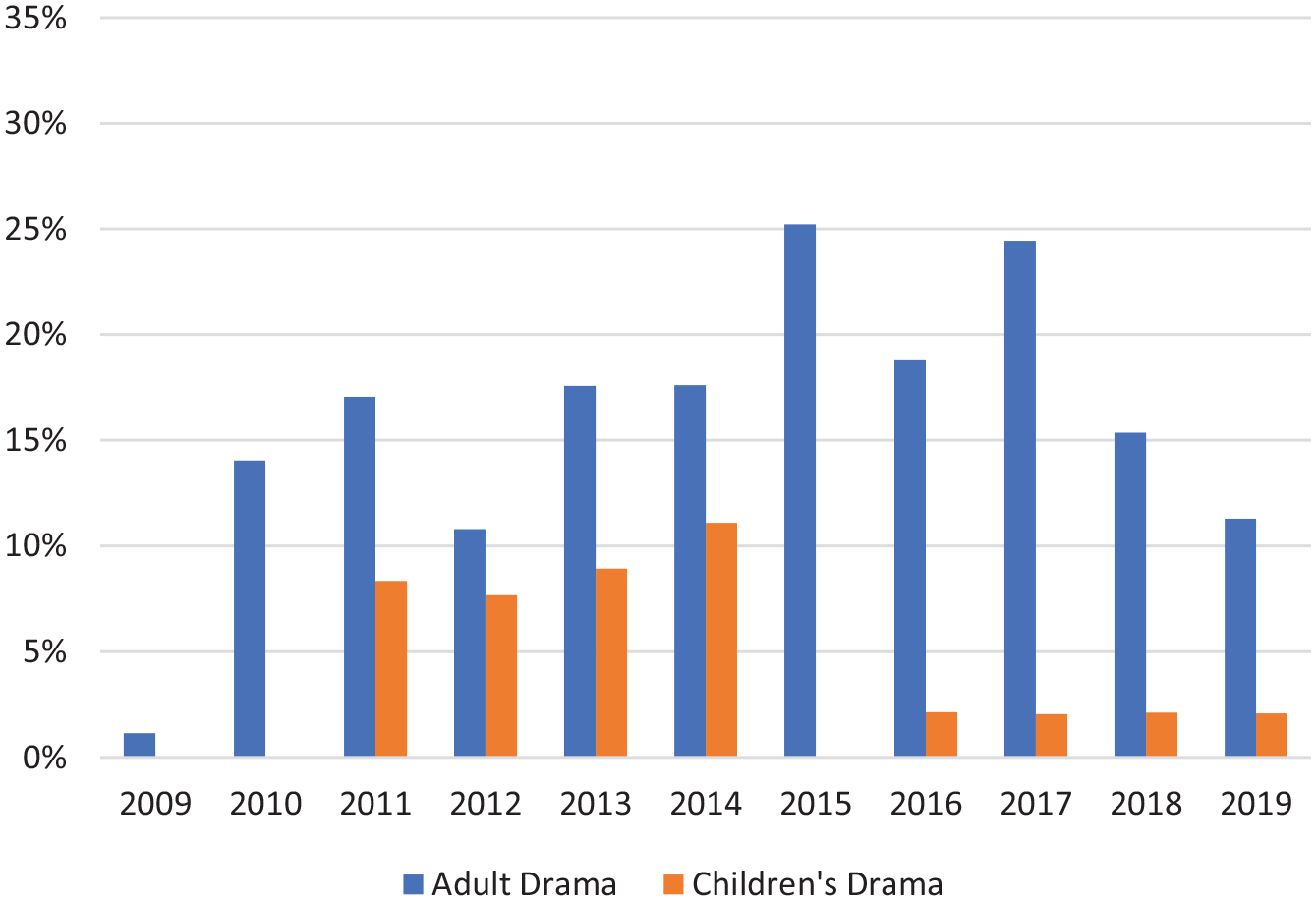

There are clear differences in the dynamics of adult and children’s drama (Figure 6). The level of children’s foreign-owned production is consistently much lower. We speculate this relates to broader industry dynamics that have led conglomerates to focus on adult drama producers. It may also relate to the extent of supports that exist for children’s television production in Australia. Broadly, the data indicate a significant increase in the percentage of hours produced by foreign-owned companies since 2009, particularly of adult drama. The cause of the decrease in 2018 and 2019 is unclear. 11 It is also unclear how foreign ownership matters.

Percentage of non-soap drama hours produced by multinational conglomerate owned production companies each year—adult versus children’s.

A Research Agenda for Drama Production Amidst Foreign Ownership

The data gathered in the previous section clearly document macro-level structural change in which a handful of multinational companies have come to play an expanded role in the local television marketplace in Australia. The impact of this expansion, both cultural and otherwise, is more difficult to discern. Historically, media scholarship has been concerned about foreign control—of trade, channels, or infrastructure—as a potential conduit for economic and cultural hegemony. Debates about media concentration and consolidation have worried the international reach of conglomerates threaten the cultural, political, and economic plurality of a global media market. Following a similar logic, several countries maintain regulatory defenses against foreign ownership of their broadcast channels, for example, to prevent “outside” influence over their citizenry and markets. Meanwhile, a robust tradition within cultural and media studies has focused on the cultural complexities to emerge in global contexts, largely by examining the dynamic and heterogenous patterns within regional program trade, programming strategies, and audience reception practices.

This intellectual history is well-worn territory within global television studies and is covered in detail elsewhere (cf. Morley and Robins 1995; Parks and Kumar 2003; Straubhaar 2007). Concerns related to the foreign ownership of television production companies have drawn less attention, but the growing empirical evidence of the phenomenon from Australia, the UK, Europe, and elsewhere signals the need to engage with this more recent internationalizing mechanism and its potential consequences. In what remains, then, we establish some of the core questions that are driving our research into Australian drama production. These concerns underscore the value of evidence drawn from varied registers and highlight what macro-level data alone cannot tell us about the incursion of multinational conglomerates into national production ecosystems.

As recounted earlier, there are many reasons why foreign acquisition may prove valuable for a production company. Being part of a large production conglomerate provides greater access to risk capital, a worldwide distribution infrastructure, and bargaining power that comes with scale (Doyle et al. 2021). Similarly, scale inspires confidence amongst commissioners and program buyers that the necessary expertise and resources are there to complete projects on time and under budget (Esser 2017). Scale also engenders a form of symbolic capital that can attract major creative talent, which is crucial to maintaining the machinery that consolidation puts in place. Multinational production firms can outbid competitors for highly coveted individuals or program ideas, often making first-look deals that effectively remove such “commodities” from the market (Esser 2017).

While our data shows evidence of a significant expansion in the market share of multinational production companies in Australia, it’s less clear if that expansion is a direct effect of structural advantage or a more diffuse correlation. The data does not tell us exactly how these acquired firms leverage the advantages of distant corporate resources nor does it reveal the potential “costs” associated with those benefits in terms of their professional autonomy, creative license, or the myriad other, more subtle workplace pressures they are likely to face. This point is especially pertinent in the context of small television markets like Australia that already lack the inherent structural advantages associated with larger, capital-intensive (and more studied) television industries as in the UK and US. For example, one of our informants recounted the transformations of workplace cultures that can upend local operations after acquisition, citing the need to reconcile divergent accounting practices and revenue calculations, adjust to elevated performance expectations and productivity pressures, and cope with what often feels like a loss of creative and financial control. “Suddenly, you must develop, finance, produce, and deliver five shows at a profit within the year. Producers in Australia aren’t accustomed to that pace,” they explained. “You can earn a lot of money from selling your company, but then comes the loss of control. If things get bad, you simply get [told what to do]. If things get worse, you get fired.”

It’s also important to remember that production companies have never possessed full autonomy in choosing what they produce, regardless of their resources. Commissioners read the audience market in light of corporate priorities and decide what programs are made and thus occupy a strategic position of power in the field of production. How much their decisions are influenced by the dynamics resulting from foreign acquisition of production companies or how impactful such ownership is as a bargaining tool is difficult, if not impossible, to isolate. Moreover, it’s hard to prove a negative—that is, it is difficult to identify program ideas that have failed to gain commission because the production company did not have access to the largess of its corporate parent. This was nearly the case with Mustangs F.C., a young adult drama that struggled to gain a commission until Matchbox Pictures, buoyed by its NBCUniversal ownership, financed the cost of pilot development and the first half dozen scripts on its own (Potter 2020). Development funds in Australia are limited, and most support mechanisms are available to a series only after it receives a commission. Drawing on the financial resources of its multinational owner, however, Matchbox was able to finance the pilot as proof of concept, which then secured a commission from the ABC. Other research has shown production of a pilot to aid series commissioning (Lotz 2018).

A more pressing query shifts the focus from the acquired companies to consider the affects upon the rest of the ecosystem, especially the survival strategies local production companies develop to compete in both global and domestic marketplaces. While local firms have been diminished in the Australian production landscape in comparison to conglomerates, they have not yet disappeared from the ecosystem. According to our conversations with SPA, the vast majority of its membership—nearly 90%—are sole traders and small businesses engaged in irregular work. Some of these small firms such as Jonathan M. Shiff Productions or slightly larger companies such as Hoodlum Entertainment have managed to maintain a sustainable development slate over time with notable international successes but without the benefits afforded by foreign acquisition. Notably, both of the examples here have had to forge their own global partnerships (Shiff with German broadcaster ZDF and Hoodlum with (now defunct) ABC Studios International) as strategic countermeasures to secure production financing and international distribution. A closer look at these firms and others, both successful and less so, will untangle the tactics they deploy to navigate a field characterized by increasingly stark power imbalances and varying forms of international connectedness. The dynamic of having a few companies with multinational scale, deep pockets, and interests not always aligned with the majority of small, domestic firms also challenges the ability of an organization such as SPA to advocate equitably for entities with different pressures and priorities.

Of course, the field of television production was never equitable, but the structural developments discussed in the previous section point to a much more profound reconfiguration of national ecosystems. Further, a number of other adjustments must be considered with respect to an individual firm’s strategies for success. As the television business has grown more international, the market for high-end drama has become more competitive, raising production costs that are increasingly too expensive even for many in the wealthiest markets. In Australia, these circumstances are exacerbated by lack of commissioning power by commercial broadcasters that have access to limited and diminishing advertising revenue. A low adopter of pay-TV, the Australian channel marketplace didn’t significantly fragment until the 2009 arrival of “multichannels” enabled by the transition to digital transmission. As a result, over the last decade commercial broadcasters have funded programming for three or four additional channels without an increase in the share of advertiser spending allocated to television. Commercial broadcasters have consequently reduced budgets, making it more difficult for production companies to fund content without significant advanced foreign rights sales. Production companies owned by foreign companies have ready access to distribution in other markets.

The dire straits of local drama producers in small markets raise difficult questions for cultural and media studies scholars. A plurality of production company voices that are non-aligned with commissioning conglomerates making local drama is a noble goal, for instance, but what if the economic realities of the current marketplace make maintaining such plurality an unfeasible objective? Conventional criticism remains rightfully suspicious of foreign ownership as a threat to economic and cultural sovereignty, but what if multinational capital is what domestic producers need to survive in a global television industry? How do these transformations confound notions of “independence” or even “local,” or obscure the entrepreneurial spirit of local producers who establish domestic firms as intentional acquisition targets?

There are likely additional concerns related to how foreign ownership might diminish the financial value of production as economic activity within a country—a question of how profits generated from local production activity are moved offshore rather than retained in Australia to sustain recurring development cycles in the domestic marketplace. But in the case of publicly held companies, wealth creation for investors and executives (who likely reside out of Australia) are, to some extent, conditions of any global business and not particular to television. Making television, however, is a cultural activity as much as it is a business, and historically has been a central lever within the Australian government’s broader “nationing” agenda (Turner 2018). Accordingly, its industrial and cultural functions are lifted by various support mechanisms, many of which are funded by taxpayers and designed to generate content of public value to audiences, but increasingly, also to maintain creative sector jobs and grow businesses.

As the domestic sector cedes control to multinational production firms, how many of these support mechanisms remain fit for purpose? As one executive of a foreign production conglomerate explained to us, foreign ownership encourages these companies to spend more money in Australia, which helps sustain local production activities, create well-paying jobs, and generate intellectual property that engages key creative talent. The support mechanisms are attractive enticements but essentially support economic activity the multinational companies are prepared to undertake anyway. Furthermore, in Australia and elsewhere, it is unclear how “public value” (Moore 1995) is secured for citizens when supports flow to multinational conglomerates. If these producers create content that achieves cultural goals—such as strengthening a sense of national identity, promoting social cohesion, and representing Australia’s cultural diversity—public value may be achieved, but these expectations have increasingly fallen aside in favor of economic metrics (Goldsmith and Thomas 2012). Advocates for robust creative sectors indiscriminately conflate economic activity with cultural dividends, latching onto the passports of key creative talent or domestic filming locations as evidence of the value of content to the citizenry and as justification for government support. But these criteria often do little to explicitly facilitate stories about Australians and Australian experiences, even if they generate financial metrics (e.g., jobs, revenue) that bureaucrats and lobbyists can use to paint a picture of a robust creative sector.

This paradox creates a significant quandary for policymakers in both economic and cultural terms. Do multinational firms with domestic outposts warrant government subsidy and investment for local activities they are able to fund themselves, especially given the limited availability of capital in the market? More to the point: does the inability of existing support structures to distinguish between multinational outposts and local production firms actually contribute to the sector’s instability and aggravate solvency issues for smaller production companies? At the very least, the quick expansion of foreign ownership in Australia calls into question the extent to which existing support mechanisms serve their intended purpose (especially those such as the Enterprise Program that pumped millions of dollars into some of the companies that were acquired) or generate unintended consequences for the competitive field. What forms of government support and investment are most effective if foreign activity comes to constitute the bulk of local drama production?

The evidence in Australia further suggests a closer look at the textual output of production companies acquired by foreign owners is necessary to disentangle questions of industrial activity and economic impact from a concern with public value for domestic audiences. Of course, tying textual outputs with industry formations, like ownership structures, is difficult to do with scale and most likely a matter of correlation rather than causation. Nevertheless, it currently remains unclear what role public value plays in the creative decisions of foreign-owned production companies, and how much it factors into the competitive dynamics of the field more broadly. For instance, what sort of cultural output emerges from foreign-owned production firms? Do they tell Australian stories? Does systematic analysis reveal differences? Do these dramas represent identities and narratives without meaningful connection to their place of origin, or construe stories that capture more culturally resonant images and histories? How do these choices impact on other industrial processes, like international distribution? How do domestic firms approach these decisions, and with what impact on their sustainability? What can domestic “public value” even look like in our current global moment? And perhaps most critically, how might policymakers reassess the ways in which cultural goals are currently defined and reconsider what sort of production activity deserves their protection?

Conclusion

By grounding the phenomenon of foreign acquisition of production companies in a particular national market, this article reveals some different dynamics than those that trace this trend at a more macro level. This article provides evidence of the extent to which foreign companies that accrue considerable market advantages as a result of their access to foreign capital, market intelligence, and in-house multinational distribution have become a significant sector of Australian scripted production and also can access Australian supports and offsets. Systematic and deep analysis of the consequences of foreign acquisition of Australian scripted television producers is too expansive for a single article, but we’ve suggested routes by which the cultural implications of this mechanism of internationalization can be investigated. Further analysis involves tracing what titles are produced and attending not only to “passport” determinants of Australian content, but also conducting analysis of how these series contribute public value to the domestic audiences that underwrite their support. Likewise, continued longitudinal data is needed for tracing the prospects of non-foreign owned production companies and their ability to earn commissions for scripted series. Finally, more detailed evaluation is needed of the portfolio of titles foreign-owned production companies produce to assess the extent they evidence design for the domestic market or suggest a strategy of using Australian production supports for content meant to be monetized globally.

There is no “going back” to industrial norms in place before widespread multinational ownership of production companies, and the point of this analysis is not to call for a halt to such acquisitions, rather to identify and acknowledge the consequences. Australian regulators can do little to manage the multinational sector, but they may want to consider limiting how much funding support foreign-owned production companies can access, create higher bars of achieving cultural goals that produce public value to access the funds, or develop specific supports for domestically owned companies. To be clear, we are not arguing there are strong negative consequences to these acquisitions, but there are consequences, and they are most pronounced for the competitive dynamics of the national sector. In a country with more capital than Australia there may still be abundant opportunity for small proprietors to develop production companies that can access commissions, but the Australian sector should be on guard for the extent to which this may quickly become infeasible. Importantly, this is a two-pronged issue of production company size and foreign ownership. It will be crucial to continue to follow mid-size, Australian-owned companies such as Hoodlum, Ambiance, and SLR, and the sale of Seven Productions over the next decade to more fully understand implications.

This analysis is not meant to dispute the strong and rigorous recent work of Doyle et al. (2021) that finds ownership to have minimal impact on production company operation. Rather, this research illustrates that there are other related questions that might be asked and different implications for small nations, at least for Australia. In focusing on drama here—a minor, but culturally-important sector of the business—our questions acknowledge the business dynamics driving these acquisitions but consider whether the internationalization that results from foreign acquisition creates a situation in which foreign ownership may impede domestic storytelling in subtler ways. For example, are stories made less Australian in casting and other strategies to better attract non-Australian viewers when these series circulate abroad? Evidence for definitive answers is likely to always be partial and complicated by the many peculiarities of producing different types of content (e.g., unscripted formats vs. drama), for services with different business models, and in countries with varied regulatory and competitive frameworks.

Footnotes

Acknowledgements

The authors relied on research assistance from Oliver Eklund in constructing the original database used in this research and Godwin Simon in mapping major international acquisitions and thank Anna Potter for advice and guidance. Our thanks as well to the reviewers who challenged us with substantive feedback that led to signficant improvement.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was conducted as part of the Australian Research Council Discovery program (DP210100849), a collaboration with Anna Potter. Early work utilized seed funding from the Digital Media Research Centre at Queensland University of Technology.