Abstract

We examine the impact of the Citizens United decision on firm value. While the value of U.S. firms do not respond significantly to the Citizens United decision on average, we find evidence that firms in industries subject to more extensive regulation react significantly and positively to the announcement. We also find evidence consistent with Justice John Paul Stevens’ argument that the Court decision will affect state laws. Specifically, our results indicate that firms that are headquartered in states with more stringent limits on political spending by corporations respond positively to the announcement.

Introduction

In 2002, the Bipartisan Campaign Reform Act (BCRA) prohibited unlimited contributions that firms and unions can make to the national political party committees, and prohibited them from using general treasury funds to finance electioneering communications. Subsequently, on January 21, 2010, the U.S. Supreme Court overturned BCRA’s provision banning the funding of electioneering communications. Following the ruling, firms, unions, and other interested parties are allowed to engage in unlimited spending on electioneering communication as long as such communication is not coordinated with the candidates. This ruling offers a unique opportunity to assess the effect of a form of corporate political spending on firm value.

We study the impact of political spending on firm value by examining the stock price reaction of firms to the announcement of the Citizens United decision. First, there is vast evidence that new, unexpected, and value-relevant information affects prices immediately upon an announcement. We use a well-established event study methodology that allows us to measure the market’s assessment of the ruling on value of firms net of other marketwide, industry-specific, and firm-specific effects. Second, the Citizens United ruling represents an exogenous change in the environment for firms to engage in political spending and thus does not suffer from endogeneity concerns (i.e., that firms perform well because they engage in political spending vs. well-performing firms do more political spending). We hypothesize that if spending influences the political process or outcomes, this ruling will have a more pronounced effect on firms that are more closely scrutinized by the government. For instance, the impact of the Citizens United ruling is potentially greater for firms in regulated industries because these industries have more interaction with the government. Similarly, firms for which legislation is pending around the time of the ruling likely stand to benefit because such firms have more to gain if the Citizens United ruling increases their ability to influence the pending regulations through independent spending.

Some states impose limits on political spending by corporations. The Citizens United ruling potentially places some of these laws in jeopardy, as suggested by the Supreme Court Justice John Paul Stevens. Cooper, Gulen, and Ovtchinnikov (2010) show a positive association between firm performance and political contributions when the firm is headquartered in the state of the politician receiving the contributions, arguing that politicians in the headquarter state are most able to affect the firm. Hence, we hypothesize that the Citizens United ruling affects firms headquartered in states that have more regulation of political spending by corporations.

Using a large sample of U.S. publicly traded firms, we find that the Citizens United decision had a measurable impact on many firms. Specifically, firms in a majority of regulated industries have a significant and positive reaction to the decision. Of the regulated industries, for example, firms in the oil industry react positively—around the announcement of the ruling shareholders of such firms experience a 2.97% increase in the value of their shares in excess of the overall market. Firms in other regulated industries react positively and significantly to the ruling as well. Furthermore, we find that firms headquartered in states that have more political spending restrictions have a significantly higher stock price reaction to the announcement than firms headquartered in states with less stringent political spending rules.

This research contributes to the literature on the role of political spending on firm value by examining the impact of the repeal of a key provision of BCRA that governs electioneering spending by corporations. It is closest to Ansolabehere, Snyder, and Ueda (2004) who study the impact of the passage of BCRA on Fortune 500 firms, and to Werner (2011) who studies whether the impact of the Citizens United decision is related to the level of political spending. Each article studies firms that are part of S&P 500 and finds no evidence that firms characterized by more political spending experience different valuation effects from firms that spend no money on political issues. In contrast to Ansolabehere et al. and Werner, we use a broad sample of all publicly traded firms with available accounting data as opposed to restricting study to the S&P 500, and, second, we use a model of expected returns that controls not only for the market factor but also for size and market-to-book (M/B) factors. Consistent with Werner, we find that on average the cross-section of firms does not react significantly to the Citizens United decision. However, we find significant and varied reaction to the Citizens United decision for firms in regulated industries, as well as for firms headquartered in states with restrictions on campaign spending.

Since the Citizens United decision and subsequent to this research, on June 25, 2012, the Supreme Court held that the Montana’s 100-year old law banning corporate political spending was unconstitutional. This ruling, while only directly affecting the state of Montana, is likely to put other states with restrictive election laws on notice and affect additional state election law changes. Our result that firms headquartered in states with more stringent election laws reacted more positively to the Citizens United ruling is consistent with an expected subsequent change in the state election laws that will allow corporations to avail themselves of increased political spending.

The following section provides background information on the Citizens United ruling, reviews the literature on politics and firm value, and proposes the hypotheses. The third section presents data and method. The fourth section presents the results and the final section concludes.

Background and Hypotheses

Under the BCRA of 2002, also known as the McCain-Feingold Act, corporations and unions are prohibited from using treasury funds to finance electioneering communications (referred to as election spending) and are also prohibited from unlimited direct contributions to candidates (referred to as election contributions). The Citizens United decision overturned the provision in BCRA’s ban on election spending, holding that under the First Amendment, corporate or union funding of independent election spending cannot be limited. Independent election spending is political speech that is not coordinated with the candidate. The renewed ability of firms to engage in election spending is likely to have implications on the amount of political spending by firms. For instance, Bebchuk and Jackson (2010) argue that if managers are willing to spend their own money to support candidates and issues, then they are likely willing to spend money for which they do not bear the full costs as is the case with their firm’s treasury funds. Furthermore, to the extent that the marginal benefit of political spending does not equal the marginal costs of such spending, the newly expanded ability to engage in political spending should affect firm value.

Existing literature studying the relationship between politics and firm value focuses on either how political connections affect firm value, or how contributions by firms, or individuals affiliated with the firm, affect firm value. For instance, in a study of 47 countries, Faccio (2006) examines the impact on firm value of board members becoming involved in politics and finds that such involvement is associated with a significant increase in firm value; however, no significant effects of politicians joining boards are identified. Faccio and Parsley (2009) find that when a politician from the hometown of a firm’s headquarters dies, that firm experiences a decrease in firm value of 1.7%. Faccio, Masulis, and McConnell (2006) find that government bailouts are more likely for politically connected firms.

While the political connectedness literature has been able to show a more solid relationship between political connections and firm value, the results on the relation between political contributions and firm value are mixed. Ansolabehere, de Figueiredo, and Snyder (2003) summarize existing literature and report that few studies find a significant benefit to firms making political contributions. More recently, Goldman, Rocholl, and So (2009) study S&P 500 firms and do not find a significant relation between political contributions and firm value. In contrast, other studies show a significant relation between firm value and political contributions. For instance, Roberts (1990) and Jayachandran (2006) show a negative impact on firm value when the political individuals to whom the firm contributed leave their political positions, suggesting that political spending is beneficial to firms. In a study of Brazilian firms, Claessens, Feijen, and Laeven (2008) find that firms that contribute to political campaigns increase their bank leverage after elections, suggesting that the political contributions increase access to bank financing. More recently, Cooper et al. (2010) study the relation between the number of candidates to which a firm contributes in U.S. political campaigns and firm value. They find that among firms that donate, those that donate to a greater number of candidates experience higher future stock returns. However, Aggarwal, Meschke, and Wang (2010) examine the corporate contributions of firms to U.S. candidates and find a significant negative relation between firm contributions and future stock returns. Furthermore, they show that firms making political contributions have worse corporate governance than noncontributing firms, indicating that political contributions may be a symptom of agency problems within a firm.

In contrast to previous research, we assess the impact of political spending on firm value by examining the market’s reaction to the announcement of the Citizens United ruling by the U.S. Supreme Court on January 21, 2010. In an efficient market, unexpected, new, and value-relevant information is immediately impounded into the stock price (Fama, 1971). This allows us to focus on a narrow window around the announcement of Citizens United ruling to measure the market’s assessment of the impact of the new information on the stock prices of firms. We posit that if political spending is a form of investment for firms, then the contributions should positively affect firm value provided such investment represents a value-increasing investment. However, if Citizens United simply allows more wasteful (and value-decreasing) investment in the political process then the repeal of BCRA should be associated with negative valuation effects for firms more likely to engage in such wasteful spending.

One potential concern with all event studies is that the announcement may be anticipated. In the context of our study, previous rulings by the Supreme Court on campaign finance laws may have caused the market to anticipate the Citizens United ruling. Specifically, Hasen (2010) provides a summary of the Court’s rulings on campaign finance leading up to and including Citizens. To the extent that the announcement was not a surprise, the market reaction should be insignificant as market prices only adjust upon the arrival of new and unexpected information (Fama, 1971).

We propose that the repeal of the election spending provision of BCRA will have a differential impact on firms contingent on the extent of their interactions with government as well as the extent of existing state political spending regulation. Aggarwal et al. (2010) find that the five industries that make the largest political contributions are Financial Trading, Banking, Telecommunication, Utilities, and Transportation. These industries have substantial interaction with the government because they are regulated. We therefore hypothesize that the impact of the Citizens United ruling announcement will be more significant for firms in regulated industries as these firms have more interaction with the government and more to gain from election spending. That is, we posit that if election spending enables firms to affect legislative process and outcomes, the valuation change should be more pronounced for firms that are subject to more regulation.

Some states impose strict limits on political spending by corporations. While the Citizens United ruling does not directly address such state laws, it may place some of these laws in jeopardy.

1

As Justice John Paul Stevens states, The Court operates with a sledgehammer rather than a scalpel when it strikes down one of Congress’s most significant efforts to regulate the role that corporations and unions play in electoral politics. It compounds the offense by implicitly striking down a great many state laws as well.

2

We hypothesize that the Citizens United decision will have a more pronounced effect on firms subject to more stringent political spending regulation, as the decision could lead to weakening of the effect of that state’s regulation. Cooper et al. (2010) argue that candidates in a firm’s headquarters state can do more to affect the firm and that therefore political contributions in the headquarters state are most relevant to firm value. Consistent with this, Cooper et al. show a positive association between firm performance and political contributions to a politician in the state in which the firm is headquartered. Therefore, we posit that firms with headquarters in states with more stringent regulation of political spending may have more favorable reaction to the Citizens United ruling.

Data and Method

We obtain daily stock price data from Center for Research in Securities Pricing (CRSP) database and require that a company has at least 200 return observations between January 1, 2009, and January 31, 2010. Accounting information for fiscal year end 2009 is from Compustat. We also collect information on corporate governance from Investor Responsibility Research Center (IRRC). Bebchuk, Cohen, and Ferrell (2009) develop an entrenchment index (E-index) based on six provisions followed by IRRC and show that six governance provisions are negatively correlated with firm performance. 3 Following Bebchuk et al., we calculate E-index for firms in the IRRC universe. The final sample consists of 4,848 publicly traded firms with sufficient stock price and accounting data.

We examine the stock price reaction of firms at the announcement of the Citizens United ruling using an event study methodology. The event study is a standard methodology that allows researchers to (a) assess the impact of new and unexpected firm-specific information on the value of a stock as well as (b) measure whether such impact is statistically significant. The past 30 years of research in financial economics show that stock prices respond to variety of marketwide, industrywide, and firm-specific information in efficient manner. Using an event study allows researchers to separate the impact of marketwide and industrywide information on the stock price and to isolate the impact of particular firm-specific information of interest to the researchers on the stock price. Hence, event study methodology allows researchers to measure the effect of particular firm-specific information on a firm’s stock price, above and beyond the effect of marketwide and industrywide factors. The impact of such firm-specific information on the stock price is measured as the abnormal (or “residual”) return, that is, the difference between the actual return minus the expected return for a particular stock.

To estimate the expected return, we use a standard Fama-French three-factor model. Specifically, we estimate the following model:

where Rt is the firm’s return, Rf t is the risk free rate, Rm t is the market return, SMB t is the size factor, and HML t is the book-to-market factor on date t. The dummy variables D_Event t,i are defined as in Salinger (1992) such that the coefficient β4,3 is the cumulative abnormal return starting 1 day before and ending 1 day after the announcement date. 4 The cumulative abnormal return is the sum of the abnormal returns over a 3-day period centered on the announcement of the Citizens United ruling on January 21, 2010. We denote this cumulative abnormal return as (CAR(−1, +1)) and it is also referred to as the announcement return.

As stock prices change every day, it is important to identify whether the impact of particular firm-specific information is sufficiently large, that is, statistically significant, or whether it is within a bound of normal daily variation for the stock. Event study takes into account the historical variation of the stock price and informs the researchers whether the observed stock price movement is statistically unusual. In terms of our Regression Model (1), the p value of the β4,3 coefficient reports the test of statistical significance. If the coefficient is positive and its p value is less than 5%, the researchers can conclude that the impact of the information studied is positive and statistically different from zero, even after controlling for market and industry factors.

Because the firms in our sample all share the same event (the announcement of the Citizens United ruling) their abnormal returns are correlated. Therefore, we use an event study methodology as in Schwert (1981) and Campbell, Lo, and MacKinlay (1997) that adjusts for this correlation.

Table 1 shows the distribution of characteristics of firms in our sample. There are 4,848 firms in our sample with average market value of equity as of December 31, 2009 of US$3.2 billion. We proxy for growth options using the industry adjusted M/B ratio that we calculate as the market value of common equity plus book value of total liabilities all divided by the book value of total assets; from this we subtract the industry average M/B. Firms with high (low) M/B are firms with high (low) growth options. We identify industries based on Fama-French 49 industry classification. The mean and median industry adjusted M/B is 0 and −0.175, respectively. 5 Firms that are less financially constrained (i.e., have high free cash flow or low leverage) may be more likely to make political contributions. Industry adjusted Free cash flow is defined as earnings before interest and taxes plus depreciation scaled by total assets, minus the industry average free cash flow. The firms in our sample have average industry adjusted Free cash flow of 0.40%. The mean unadjusted Free cash flow is 2.90%. Industry adjusted Leverage, calculated as total liabilities divided by total assets minus the industry average leverage, is −0.30%. 6

Sample Characteristics.

Note. Sample contains all publicly traded firms with sufficient stock price data during 2010 and 2011 on CRSP and data available on Compustat. MV = market value; Ind. = industry; M/B = market-to-book; CRSP = Center for Research in Securities Pricing; HQ = headquarters; CU = Citizens United.

We next identify which firms belong to regulated industries. We treat the following industries as regulated: alcohol, tobacco, drugs, aircraft, guns, gold, oil, utilities, telecom, transportation, banks, insurance, and finance. Approximately 43% of the firms are from regulated industries. The lower half of the table shows the distribution in particular regulated industries. The highest proportion of firms falls into the banking industry (12.3%), followed by drugs industry (6.3%) while the fewest firms are in alcohol, guns, and tobacco industries.

Finally, the National Conference of State Legislatures (NCSL) identifies states that limit direct corporate spending on candidate elections. 7 We identify each of these states because their laws are in conflict with Citizens United and therefore likely to be affected by the decision. We recognize other laws might exist that are common to all of these states. Identifying every such law is not feasible; therefore, we focus on the one law that these states have in common that is in conflict with Citizens United and the one to which Justice John Paul Stevens draws attention. The NCSL identifies these states as follows: Alabama, Alaska, Arizona, Colorado, Connecticut, Iowa, Kentucky, Massachusetts, Michigan, Minnesota, Montana, New Hampshire, North Carolina, North Dakota, Ohio, Oklahoma, Pennsylvania, Rhode Island, South Dakota, Tennessee, Texas, West Virginia, Wisconsin, and Wyoming. We obtain a firm’s state of headquarters from Compustat. Approximately 35.9% of our sample firms are headquartered in one of these states.

Results

We first present our univariate results for portfolios of firms based on various characteristics. We then study the firms’ stock price reaction to the Citizens United ruling in a multivariate setting.

Univariate Results

We first analyze the effect of the Citizens United U.S. Supreme Court ruling in a univariate setting. We report the average announcement return (CAR(−1, +1)) for portfolios based on industry membership and based on firms that are headquartered in states with laws that conflict with Citizens United.

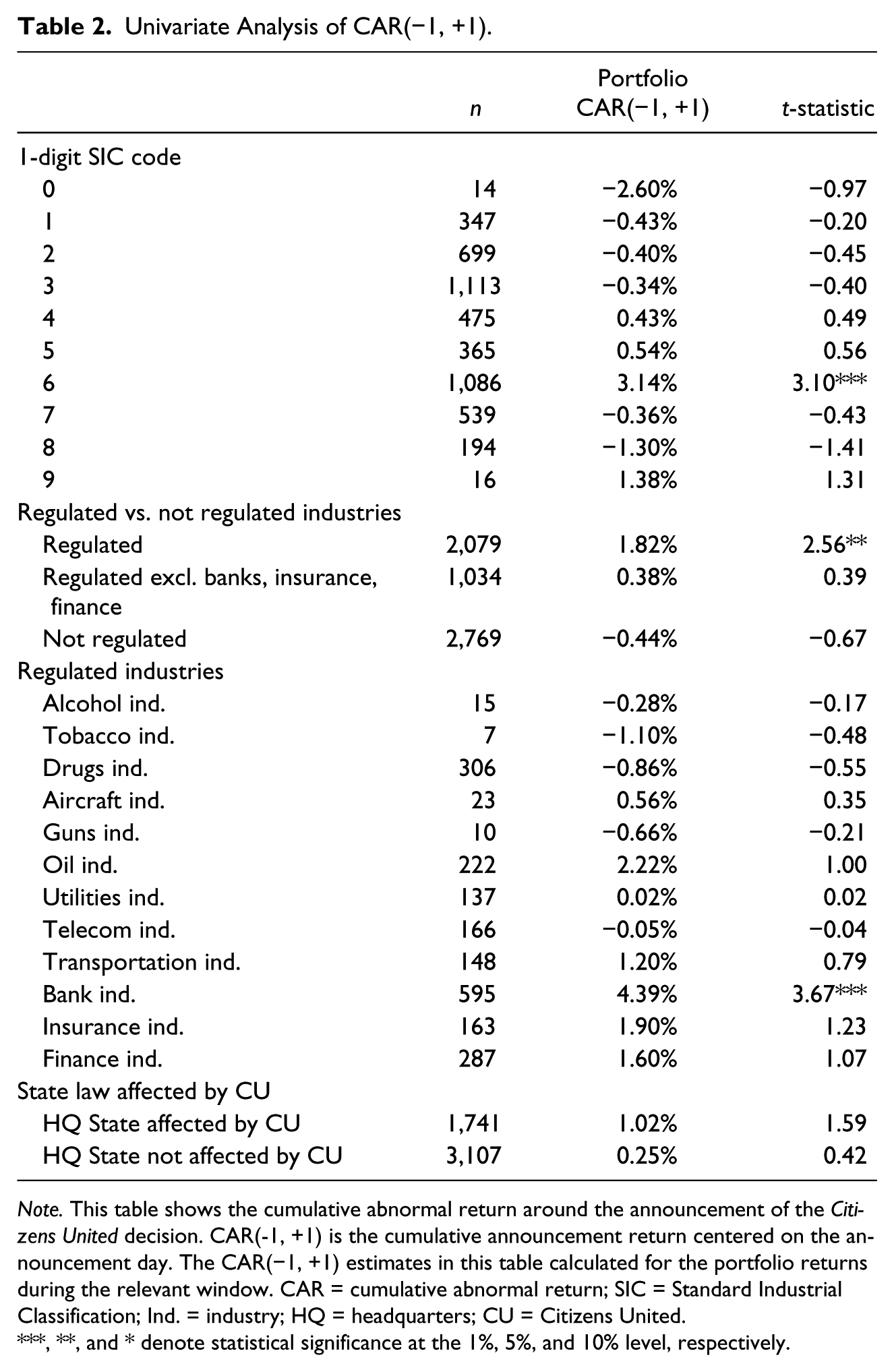

Table 2 presents the results based on broad groupings of firms by industry using one-digit Standard Industrial Classification (SIC) codes. SIC codes have been developed and updated by the Federal government to classify all economic activity into standard industry groups since late 1930s. For each industry, we report the CAR(−1, +1) in the 3-day event window centered on the announcement day of the ruling. We find little evidence of a significant reaction to the Citizens United based on the industry grouping. However, there is evidence that financial institutions benefit from the ruling, as the CAR(−1, +1) for firms with SIC code between 6,000 and 6,999 is 3.14%, significant at the 5% level. Industries in this group include, for example, banks, savings institutions, credit agencies, loan brokers, finance services, brokers, insurance, and real estate.

Univariate Analysis of CAR(−1, +1).

Note. This table shows the cumulative abnormal return around the announcement of the Citizens United decision. CAR(-1, +1) is the cumulative announcement return centered on the announcement day. The CAR(−1, +1) estimates in this table calculated for the portfolio returns during the relevant window. CAR = cumulative abnormal return; SIC = Standard Industrial Classification; Ind. = industry; HQ = headquarters; CU = Citizens United.

,**, and * denote statistical significance at the 1%, 5%, and 10% level, respectively.

Besides anticipation or lack of surprise, another concern about event studies is confounding information. If information unrelated to the Citizens United ruling is announced during the event window, some or all of the effect measured by the event study may be attributable to the confounding information. Based on a public press search via Lexis/Nexis, we identify a significant news announcement by president Obama of a proposal to increase bank regulation, the so-called Volcker rule. 8 Therefore, it is possible that the announcement effect includes the announcement of the Volcker rule. However, the Volcker rule, in increasing bank regulations to limit the way banks can invest, and more specifically, in reducing their ability to engage in proprietary trading for their own account, should have a negative impact on banks and financial firms. This argument is consistent with studies of the 1999 repeal of these Glass-Steagall-like restrictions on banks by the Financial Services Modernization Act. The findings related to the Financial Services Modernization Act show that the repeal benefited financial institutions (Akhigbe & Whyte, 2001; Carow & Heron, 2002; Carow, Kane, & Narayanan, 2011). Thus, imposing the restrictions again should imply a detrimental effect on financial institutions. This negative sentiment regarding the Volcker rule is echoed in the financial press. 9 Therefore, any positive effects to banks and financial firms due to the Citizens announcement are likely to be attenuated by the Volcker rule announcement, not enhanced. However, while unlikely, it is feasible that the announced version of the Volcker rule was less onerous than expected by the market participants, potentially enhancing the announcement returns on the event date. As we are unable to separate these market expectations, this argument remains a possibility that cannot be ruled out. However, we address this concern by examining firm reactions when excluding financial firms. To make sure that our results are not in some way driven by the confounding information that disproportionately affects financial firms, we report our regression results with and without financial firms in the sample. Nevertheless, it is important for us to point out that while the confounding information may affect the level of announcement returns on the event date, it is unlikely that the announcement of the Volcker rule biases our cross-sectional results related to the extent of regulation and the effect of state laws that we later explain.

In Table 2, we analyze regulated industries as defined in Section 3. Overall, regulated industries experience a significant CAR(−1, +1) of 1.82%. Excluding financial companies from other regulated firms, the CAR(−1, +1) is an insignificant 0.38%. Finally, industries that are not regulated also do not react significantly to the announcement, with a CAR(−1, +1) of −0.44%. Table 2 further separates the broad category of all regulated industries into individual industry groups and presents the market reaction for each industry portfolio. Results are similar to the one-digit SIC code industry separations previously discussed, with banks experiencing a positive 4.39% CAR(−1, +1), significant at the 1% level. Table 2 analyzes the reaction based on the location of the firm’s headquarters. As discussed earlier, the Citizens United ruling is expected to affect the state laws that currently regulate political spending. For the sample of 1,741 firms headquartered in states that limit political spending, the CAR(−1, +1) is 1.02%; however, it is statistically insignificant with a t-statistic of 1.59.

Based on the univariate results, we find a significant effect of the Citizens United ruling on financial firms, and an insignificant impact for nonfinancial, regulated industries. The evidence on the importance of the stringency of the state political spending regulation suggests that the market expects the ruling to affect firms’ political spending under the state laws; however, the result is not statistically significant. We note that univariate results have to be interpreted with caution, as many factors affecting the announcement returns are ignored in such analysis. We therefore next analyze the stock price reaction in a regression setting.

Regression Results

We next analyze the market reaction to the Citizens United ruling in a multivariate context. We present regressions analyzing how the firm’s industry classification affects the announcement return (CAR(−1, +1)). The standard errors are clustered at the industry level and are adjusted for heteroskedasticity. In all regressions, we control for firm-specific attributes that have been shown in prior research to be related to firm political donation activity. These firm-specific characteristics include industry adjusted Free cash flow, M/B, and Leverage, as well as size (measured as the natural logarithm of market value of equity on December 31, 2009; log(Equity MV)). Higher free cash flow may provide managers with more prospects to behave opportunistically. For example, Aggarwal et al. (2010) find that donating firms tend to have high free cash flow. However, Cooper et al. (2010), using the number of candidates a firm donates to, find that donating firms have low free cash flow. M/B has an inverse relation to donations according to Aggarwal et al., while leverage does not have a robust association. Firm size may matter because larger firms tend to have higher political contributions (Aggarwal et al., 2010). At the same time, larger well-known firms may shy away from high political contributions for fear of alienating investors and customers.

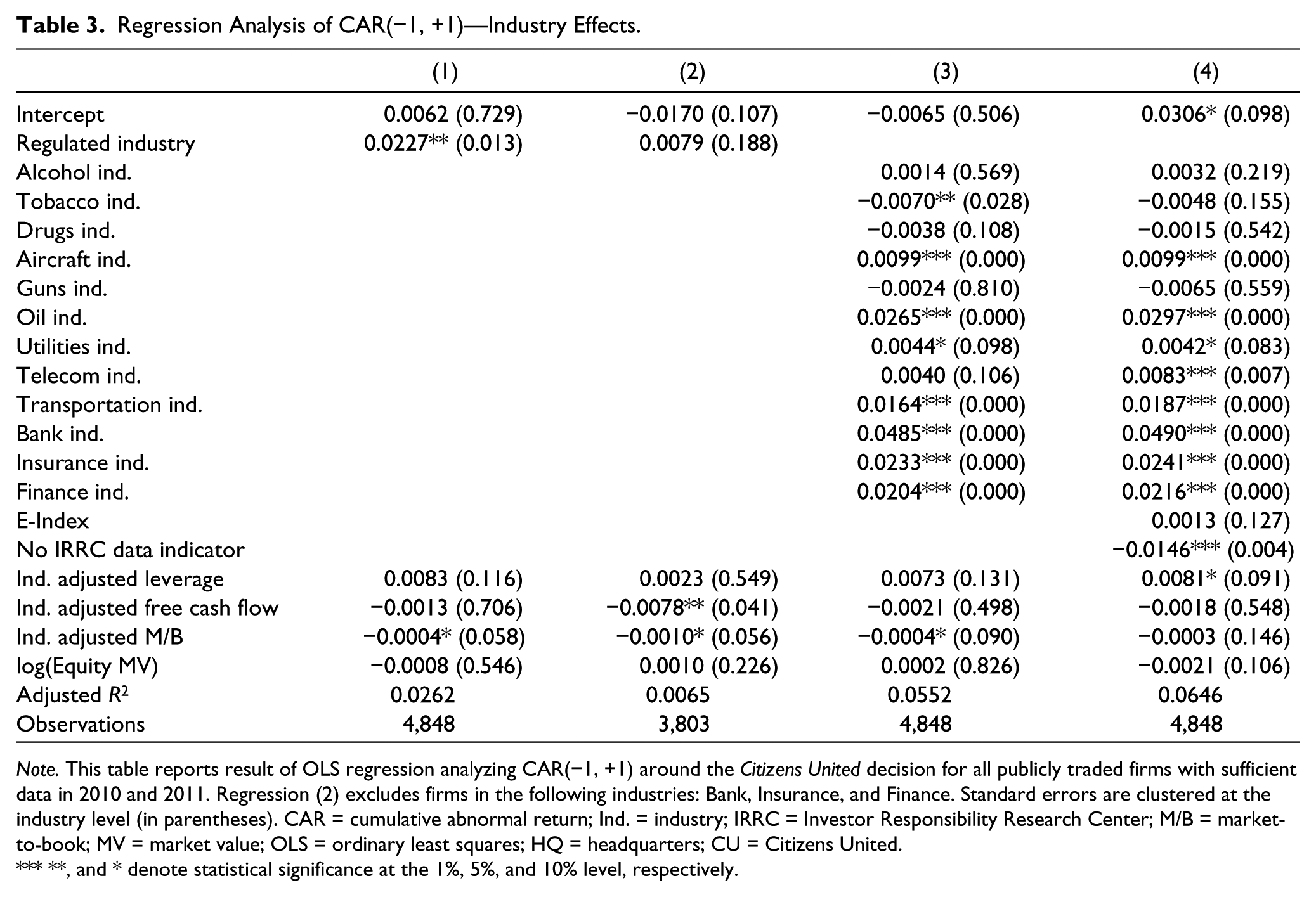

Regression results related to regulated industries are presented in Table 3. We begin by including an indicator variable for regulated industries in Regression (1). After controlling for firm-specific characteristics, regulated industry is positive and significant at the 5% level, indicating the market expects the ruling to be on average beneficial to regulated industries. The coefficient implies a 2.27% higher cumulative abnormal return for firms in regulated industries around the Citizens United ruling when compared with nonregulated firms. In Regression (2) we exclude bank, insurance, and finance industries from the sample. The coefficient on the regulated industries indicator remains positive; however, the p value increases to 18.8%. Regression (3) reports results for individual regulated industries. Financial industries including banks, insurance, and finance, all have positive and significant coefficients, ranging from 0.020 to 0.048. Therefore, despite the negative effect of Volcker rule announcement, financial firms experience positive abnormal return. Furthermore, coefficients on the indicator variables for other regulated industries, namely, aircraft, oil, transportation, utilities, and tobacco, become significant in the multivariate results, and with the exception of tobacco, all are positive. The range of the significant positive industry announcement effects when compared with nonregulated firms is from 0.44% for utilities to 2.65% for oil industry. The tobacco industry coefficient implies a negative announcement effect of 0.70%, indicating that the political spending by tobacco firms is expected to be wasteful, relative to the control group of nonregulated firms. We add the E-index to assess the effect of corporate governance on our results in Regression (4). As for more than 60% of the sample the IRRC data do not exist, we include an indicator variable No IRRC Data following Cohen, Cohen, West, and Aiken (2003). 10 We expect that firms with better governance (i.e., lower E-index) exhibit less wasteful political spending. Regression (4) presents the results. The coefficient on E-index is indeed positive; however, it is not significant (p value of 12.7%). The inclusion of E-index causes the tobacco indicator to become insignificant. Thus, after controlling for the effects of corporate governance, most regulated industries experience a positive or insignificant effect upon the announcement of the Citizens ruling.

Regression Analysis of CAR(−1, +1)—Industry Effects.

Note. This table reports result of OLS regression analyzing CAR(−1, +1) around the Citizens United decision for all publicly traded firms with sufficient data in 2010 and 2011. Regression (2) excludes firms in the following industries: Bank, Insurance, and Finance. Standard errors are clustered at the industry level (in parentheses). CAR = cumulative abnormal return; Ind. = industry; IRRC = Investor Responsibility Research Center; M/B = market-to-book; MV = market value; OLS = ordinary least squares; HQ = headquarters; CU = Citizens United.

**, and * denote statistical significance at the 1%, 5%, and 10% level, respectively.

Of the control variables, size is surprisingly insignificant. Leverage has a consistently positive coefficient; however, the significance is mixed. Free cash flow has a consistently negative coefficient, implying that firms with higher free cash flows experience stock price decline on the announcement of Citizens United ruling. However, only in Regression (2) is the coefficient on free cash flow significant. Finally, the coefficient on M/B implies that firms with higher M/B experienced a more negative price change upon the announcement of the Citizens United ruling.

We next analyze the extent of industry regulation and the effect it has on firm valuation on the announcement date of the Citizens United ruling. We use two measures of the intensity of industry regulation. The first measure uses data from Compustat that report the sum of all pre-tax settlement special items and includes insurance proceeds and provisions to boost or reverse reserves for litigation settlements. We sum the pre-tax settlement special items scaled by total assets for all firms in a particular industry—This approach mitigates the effects on intraindustry litigation and captures government, private litigation, and enforcement actions by entities outside of the particular industry. This measure is consistent with some of the measures used by Jackson (2007) who compares intensity of financial regulation across several countries. As our work focuses only on the United States, we adopt the measure to industries in our sample. Second, we use a simple measure of industry total market capitalization as a proxy for intensity of regulation (Industry market value). If large industries attract more government oversight, the total industry size should capture the variation in the extent of the current government regulation. Clearly, neither of these two measures is perfect and likely contains substantial noise.

We report the results in Table 4. In both regressions, we exclude financial firms. In Regression (1) we include Industry legal settlement expense as well as an interaction term with regulated industry. If the extent of government regulation affects the value of firms on the Citizens United announcement, we expect that the interaction term will have a positive and significant coefficient. We find that the coefficient on the interaction term is positive and significant at the 5% level suggesting that the relation between announcement returns and extent of regulation is stronger than for nonregulated firms. In Regression (2) we add Industry market value and an interaction term with the regulated industry indicator. The interaction term has a positive coefficient, significant at the 5% level. The interaction term of industry settlement expense and regulated industry remains positive and is now significant at the 1% level. These results are consistent with firms in industries subject to more regulatory scrutiny experiencing significantly higher increases in valuation on the announcement date of the Citizens United ruling.

Regression Analysis of CAR(−1, +1)—Extent of Regulation, Nonfinancials.

Note. This table reports result of OLS regression analyzing CAR(−1, +1) around the Citizens United decision, for all publicly traded firms with sufficient data in 2010 and 2011, excluding firms in the following industries: Bank, Insurance, and Finance. Standard errors are clustered at the industry level (in parentheses). CAR = cumulative abnormal return; IRRC = Investor Responsibility Research Center; Ind. = industry; M/B = market-to-book; MV = market value; OLS = ordinary least squares; HQ = headquarters; CU = Citizens United.

,**, and * denote statistical significance at the 1%, 5%, and 10% level, respectively.

Table 5 analyzes the effect of state laws regulating political spending. Regressions (1), (3), and (5) include all firms while Regressions (2), (4), and (6) exclude financial firms. In addition to firm-specific control variables, in Regression (1), the basic specification, we include an indicator for whether the firm is headquartered in a state with stringent regulation on corporate political spending. The coefficient of 0.006 on the indicator is significant at better than the 1% level and implies that firms headquartered in a state with stringent corporate political spending regulation experience a 0.6% higher return than firms in states without such regulation. In Regression (2), we drop finance firms from the sample and reestimate the regression. The coefficient on the stringent state election regulation indicator remains positive and is significant at the 5% level. These results are consistent with Justice John Paul Stevens assertion that state laws will be affected, with subsequent ruling on Montana’s state election law, and with findings of Cooper et al. (2010) that firms’ political activity in the headquarters’ state matters. In Regressions (3) and (4), we confirm that results continue to hold when including the regulated industry indicator—the significance of the coefficients on the state indicator is not affected by inclusion of the regulated industry indicator. In Regression (5) which once again includes financials, we examine whether firms in regulated industries that are headquartered in states with stringent corporate political spending regulation experience differential announcement effects by including an interaction term between the regulated industry and the headquarter state affected by Citizens indicator. The interaction term is insignificant while the significance of the coefficient on the state indicator is not affected. Hence, regulated firms headquartered in states with stringent political spending regulation do not experience any additional affects. Finally, in Regression (6), we exclude firms in banking, insurance, and finance industries to verify that the effect of the headquarter state is not driven by the confounding announcement of the Volcker rule affecting these industries. The coefficient of the state indicator is significant at better than the 1% level and implies that firms headquartered in a state with stringent corporate political spending regulation experience a 0.7% higher return than firms in states without such regulation. Therefore, we conclude that the confounding announcement of the Volcker rule affecting financial institutions does not drive the result related to state political spending regulation. We also note that the regulated industry indicator is significant at the 5% level. Overall, the results are consistent with the proposition that the Citizens United ruling is expected to subsequently affect the state law and that this effect is reflected in the market’s assessment of firm value at the time of the announcement.

Regression Analysis of CAR(−1, +1)—State Effects.

Note. This table reports result of OLS regression analyzing CAR(−1, +1) around the Citizens United decision, for all publicly traded firms with sufficient data in 2010 and 2011. Regressions (2), (4), and (6) exclude firms in the following industries: Bank, Insurance, and Finance. Standard errors are clustered at the industry level (in parentheses). CAR = cumulative abnormal return; IRRC = Investor Responsibility Research Center; Ind. = industry; M/B = market-to-book; MV = market value; OLS = ordinary least squares; HQ = headquarters; CU = Citizens United.

**, and * denote statistical significance at the 1%, 5%, and 10% level, respectively.

Conclusion

We study the impact of U.S. Supreme Court ruling, which expanded corporations’ political spending opportunities, on firm value. Using a large sample of U.S. publicly traded firms, we find evidence that the Citizens United ruling had an impact on many firms. The valuation effect of political spending is more pronounced for firms in regulated industries, especially for firms subject to more extensive regulation. Specifically, out of the regulated industries, banks react most strongly when compared with other firms. While financials are potentially affected by the Volcker rule announcement, even nonfinancial industries, specifically aircraft, oil, utility, telecommunications, and transportation industries, experience statistically significant positive CARs at the announcement of the Citizens United ruling.

Our results also point to the importance of the U.S. Supreme Court ruling on state election laws. We find that firms’ reactions differ based on the state laws affecting them. Firms headquartered in states with more stringent corporate political contribution regulation experience positive and significant reactions to the Citizens United ruling.

This study contributes to an emerging literature on the impact of corporate political spending. As corporate political spending grows, opportunities for further research will help to solidify our understanding of its impact.

Footnotes

Acknowledgements

We thank two anonymous referees, Brian Gaines (the editor), Dima Leshchinskii, Melissa Michelson, and John Wald for helpful comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.