Abstract

Investing in cryptocurrency has become more popular among Americans. Despite this, politicians and social scientists know almost nothing about the politics of cryptocurrency in the American public. By analyzing an original, nationally representative survey of 2500 American respondents, we create the first robust profile of the personalities, demographics, and political attitudes of cryptocurrency owners. We show that Americans who report hardship from inflation are more likely to own cryptocurrency, suggesting that when inflation is high, Americans may be more likely to use cryptocurrency as a medium of exchange and store of value. Americans who favor lower government spending and are more inclined toward conspiratorial thinking are also more likely to own cryptocurrency. Finally, there is a personality to cryptocurrency owners, with those open to new experiences more likely to own it and the conscientious less likely to own it. Our results have implications for how the American public may use cryptocurrency going forward.

Introduction

In the last several years, investing in cryptocurrency has become more popular among Americans. Everyday Americans use it to purchase goods and services, professional athletes earn portions of their salaries in it, and celebrities receive lots of media attention for backing new forms of cryptocurrency. Cryptocurrency is an increasingly normalized part of American society. Estimates vary, but data from the Pew Research Center suggest that about one in every six or seven Americans currently owns cryptocurrency or has owned it in the past. 1 Owning cryptocurrency has become such a common form of investment for Americans that in 2021, legislators in Congress introduced almost three dozen bills about cryptocurrency. Cryptocurrency is a potential rival to government-controlled fiat currencies like the dollar, and Congress has paid an increasing amount of attention to how to incorporate it into American law, markets, and taxation. There is a bipartisan, 32-member Congressional Blockchain Caucus that is in part focused on its promotion.

Despite the prominence of cryptocurrency in American society and government, social scientists know almost nothing about the personality or politics of cryptocurrency owners in the American public. This is remarkable because a central idea of Bitcoin, the world’s first and most valuable cryptocurrency, is limiting government’s monopoly control over currency due to lack of trust in government’s management of economic and monetary policy (Ammous, 2018). Popular discourse on cryptocurrency owners notes their distinctiveness in personality, demographics (young men especially), and issue preferences, but provides little hard evidence for these claims. On the other hand, the increasingly common ownership of cryptocurrency today suggests that cryptocurrency owners might be no different than the average member of society.

We remedy this lack of scholarly knowledge by examining the personalities, demographics, and political attitudes and perceptions of cryptocurrency owners. Using a nationally representative survey of 2500 Americans, we address hypotheses about cryptocurrency owners that have not been tested or have been tested only in small convenience samples. We find that Americans who own cryptocurrency are a large group, have distinct personalities, and do not reflect existing ideological coalitions. Our results provide some insight into the effects of inflation and the distinctiveness of the one in seven people in American society who own cryptocurrency.

Literature Review

The existing work on the profile of cryptocurrency owners is sparse. An informal survey of Bitcoin users from 2014 found that Bitcoin users were overwhelmingly male, about 33 years old, largely libertarian in political preferences with many left-wing owners as well, with a slight tendency to purchase illicit goods (Bohr & Bashir, 2014). Bohr and Bashir (2014) also found that freedom, weakening the power of a centralized state, avoiding government control of the money supply, and government surveillance of transactions were all reasons that Bitcoin users gave for why they used Bitcoin. More left-wing Bitcoin users liked it because it insulated them from the influence of banks on savings and investment and transactions. However, this informal survey is from 2014, and the number of cryptocurrency owners has grown dramatically since then. We are uncertain, at best, if that description still holds.

Auer and Tercero-Lucas (2022) use 2019 data from the Survey of Consumer Payment Choice to analyze the demographics of American cryptocurrency owners. Their results show that cryptocurrency owners are younger and more likely to be male, but not any more or less wealthy than those who do not own cryptocurrency. No particular ethnic or racial group was more likely to own cryptocurrency, but more educated individuals were more likely to own it. Marital status did not affect cryptocurrency ownership. The authors find that cryptocurrency owners are not concerned about the security of their money in cash, and state that they “can disprove the hypothesis that cryptocurrencies are sought as an alternative to fiat currencies or regulated banking” (Auer & Tercero-Lucas, 2022, p. 21). However, only 1.4% of their sample actually owned cryptocurrency, which is quite different from current estimates (14%–16%) and suggests their analysis might not be a good measure of who owns cryptocurrency going forward.

Bonaparte (2022) analyzes cryptocurrency ownership using Survey of Consumer Finance data from 2018 and presents evidence showing that cryptocurrency households view cryptocurrencies as a long-term asset to hold. In his sample, men, college-educated individuals, those who identify as white, and those who own stocks are significantly more likely to own cryptocurrency. However, only .35% of American households own cryptocurrency in his sample. Similar to Auer and Tercero-Lucas (2022), this is different enough from contemporary estimates that the representativeness and relevance of these findings for the future is uncertain.

Overall, there is little research on the personalities, demographics, and politics of cryptocurrency owners. There is strong reason to believe, though, that a certain type of person could be attracted to owning this asset. With respect to personality, two broad clusters of traits are well established in the discipline: The Big Five and the Dark Triad. Big Five traits, or Openness to Experience, Conscientiousness, Extraversion, Agreeableness, and Emotional Stability, are a powerful representation of an individual’s personality and have been shown to affect everything from likelihood of voting (Weinschenk, 2013), culture (Wilmot & Ones, 2022), and uncertainty avoidance (Varas et al., 2010) to investment in different types of financial assets (Aren and Hamamci, 2020), including risky ones (De Bortoli et al., 2019).

The Big Five broadly affect Americans’ political behavior (Mondak, 2010; Mondak et al., 2010; Weinschenk, 2014; Weinschenk & Panagopoulos, 2014). These traits cover how excited (or not) an individual is by new opportunities (Openness to Experience), how much an individual is prone to organization and self-control versus spur of the moment activity (Conscientiousness), the pleasure derived from social interactions with friends and strangers (Extraversion), how much an individual desires positive relations with others (Agreeableness), and how much an individual desires managing their environment and their willingness to exert impulse control to achieve it (Emotional Stability). Some work explores the relationship between these traits and cryptocurrency ownership with evidence for Agreeableness and Extraversion (Sudzina et al., 2021), but the work is descriptive, leaving the picture far from complete.

More infamous is the Dark Triad: Narcissism, Machiavellianism, and Psychopathy (Paulhus & Williams, 2002). Narcissistic individuals seek to bring attention to themselves, even at the expense of others. Machiavellian individuals do not mind manipulating or even lying to others out of self-interest. Psychopathic individuals tend to act out of impulse, even at the expense of others, lacking remorse or even being callous towards the feelings of others. Again, initial descriptive work finds a relationship between all three of these traits and cryptocurrency ownership (Martin et al., 2022), but that work relies on a convenience sample.

The Big Five and the Dark Triad might predict cryptocurrency ownership alongside other classic Personality Traits: Need for Cognition (Cacioppo & Petty, 1982, Arceneaux & Vander Wielen, 2013) and Need to Evaluate (Bizer et al., 2000; Federico, 2004; Jarvis & Petty, 1996). Need for Cognition is a trait that captures the tendency of individuals to enjoy the process of thinking itself and desire to know the true state of the world. Arceneaux and Vander Wielen (2013, 24) note that high Need for Cognition individuals “are motivated to reason through their evaluations.” Lin et al. (2006) find that Need for Cognition “determines the magnitude of the effect of emotion on risk-taking behavior.” Therefore, Need for Cognition might affect the likelihood that someone owns cryptocurrency, which is a risky asset.

Need to Evaluate measures how likely someone is to quickly form opinions about whether things are good or bad. Americans high in Need to Evaluate have more opinions than others, tend to take sides in a conflict, and are more likely to have a dualistic worldview. Since purchasing cryptocurrency, in some sense, requires rejecting the idea that the dollar is the only necessary medium of exchange and good store of value, and embracing that something else is, we might expect cryptocurrency owners to be higher in Need to Evaluate. Furthermore, the foundational ideas behind the creation of Bitcoin and its adoption are strongly ideological, with government and public/private management of the money supply viewed as not just bad, but evil.

Overall, a survey of the sparse existing research on cryptocurrency ownership shows that cryptocurrency owners are different from the average American, though there is considerable debate over their distinctive characteristics. The personality of cryptocurrency owners is supposedly distinct, with those low in Agreeableness and high in Extraversion and the Dark Triad traits of Narcissism, Machiavellianism, and Psychopathy more likely to own cryptocurrency. Cryptocurrency owners are often thought to be more likely to be young, male, educated, higher-income, and stock owners. They are more likely to identify as white. Politically, cryptocurrency owners are expected to be strongly motivated by freedom and conspiracy beliefs, distrustful of government, banks, and central management and surveillance of currency and markets, and libertarian to left-leaning (perhaps economically conservative and socially liberal). If this description applies to the one in every seven Americans that reliable estimates believe hold cryptocurrency, then cryptocurrency owners are a distinct and consequential group for American society and government.

What social scientists don’t know, however, is how accurate this description is. Virtually all existing research on who owns cryptocurrency suffers from a significant drawback, including being a convenience sample (Bohr & Bashir, 2014), college-student-only sample (Sudzina et al., 2021), small sample (Auer & Tercero-Lucas, 2022), a sample not representative of American adults (Bonaparte, 2022; Martin et al., 2022), or outdated data (Bohr & Bashir, 2014; Bonaparte, 2022). Social science, therefore, needs a rigorous understanding of the personality, politics, and demographics of cryptocurrency owners to understand how the American public is likely to react to the increasingly prominence of cryptocurrency in society and government. In the next section, we describe the theory behind the survey that we use to give us such an understanding.

Theory and Hypotheses

The Philosophical Origins of Bitcoin

To understand cryptocurrency ownership, it’s important to consider the motivation behind Bitcoin, which is by far the most valuable and popular cryptocurrency. 2 Bitcoin is sometimes referred to as “digital gold” because while it is not a tangible asset, like a dollar bill you can touch, like gold it has a limited world supply that only very slowly expands. 3 Unlike the dollar, no one can make more of it, and new Bitcoin can only be earned via lots of computing power. Bitcoin can’t be devalued via excessive printing like a dollar or bolivar. Some of the theory behind Bitcoin was laid out in an original paper by the still-anonymous creator of Bitcoin, Satoshi Nakamoto, on October 31st, 2008. 4

The basic premise of Bitcoin is that its creation allows for online transactions between individuals and groups without the need for any kind of trusted third party to guarantee the security of the transaction itself or the medium of exchange. Individuals can trade with each other, potentially anonymously, with all transactions automatically recorded on a public blockchain. A lack of trust in the public and private institutions 5 that guarantee trade was fundamental to the creation of Bitcoin, which was created and initially adopted during and after the Financial Crisis of 2008. While Nakamoto, (2008) did not specifically refer to “government” in his essay, he did refer to “financial institutions,” which are both government-controlled and private.

This lack of confidence was and is a critique of government monetary policy and attempts to manage the money supply and banking. It is an argument against government-managed fiat currency (that is not backed by a commodity, like gold) and how well it satisfies two of the three classic functions of money: as a medium of exchange and a store of value (Ammous, 2018). Bitcoin’s critique of fiat money as a medium of exchange is that transactions, online and in the real world, are guaranteed by third parties which are not trustworthy (banks and government). The fact that these institutions determine the conditions under which transactions can be performed and serve as middlemen was odious to the original adopters of Bitcoin because in their view, these actors are not transparent, set arbritary rules that benefit themselves, and are corrupt and can’t be trusted with an individual’s money. 6

The philosophical origins of cryptocurrencies, then, might attract a particular kind of person: someone who is distrustful of traditional systems, skeptical of traditional stores of value, and dismissive of opaque policy they cannot control. They might also be less willing to acquiesce to consensus and more willing to try alternatives to the status quo. Finally, they might be attracted to thinking about complex problems, like banking and currency, and be interested in evaluating those problems for themselves. We return to each of these with respect to personality.

The Economic Arguments of Bitcoin Proponents

The original adopters of Bitcoin lacked trust in government fiat money as a store of value. 7 They specifically argued that individuals could not have confidence in the long-term value of the dollar because of the American government printing too much money and causing inflation, as well as government ability to influence how private banks manage an individual’s money. They viewed the potential for high inflation, and the devaluation of the dollar, as persuasive arguments for owning Bitcoin.

Many of these ideas are similar to and inspired by those of the Austrian School of Economics, a particularly libertarian branch of economics that is critical of government’s attempt to control the money supply. 8 From this foundation, it is not surprising an early informal survey of Bitcoin users found them to be deeply distrustful of both government and banks (Bohr & Bashir, 2014).

The contemporary American macroeconomic environment offers an ideal opportunity to test these ideas. Both inflation and the national debt have increased considerably over the last several years. With brief exceptions, Americans’ trust in government and large financial institutions like banks has remained low for the last decade. In published research, scholars from the International Monetary Fund debate whether the dollar will remain the world’s reserve currency (Arslanalp et al., 2022). From a certain perspective, therefore, some of the concerns that inspired the creation and adoption of Bitcoin have become more prominent. It may be the case that cryptocurrency owners broadly, including those who own Bitcoin 9 or other cryptocurrencies, are still influenced by the economic ideas originally behind Bitcoin.

If more Americans use cryptocurrency at a time of high inflation, and many of the concerns behind the creation of cryptocurrency have at the very least become more visible, it seems likely that these two phenomena should be related. In other words, the ideas behind cryptocurrency should be related to who owns it. Using a new survey data set collected during period of high inflation, as well as an expansion of government spending and the national debt, we explore whether the economic arguments underlying cryptocurrency as an asset class have encouraged a wider adoption of that asset class, as more of the public feels the effects of inflation.

Theoretical Expectations

We therefore test the hypotheses below about politics, personality, and cryptocurrency ownership that have never been tested on a nationally representative sample of Americans. Our hypotheses broadly mirror the two lines of argument on who might be a cryptocurrency supporter: one based on personality, the other rooted in economics.

First, we describe our economic expectations. Since concerns about government spending and inflation were central to the ideas behind the creation and adoption of Bitcoin, and these problems are much more visible today than they were in 2009, we propose Hypotheses

Lack of trust in the government’s ability to regulate currency, especially in a time of high inflation, is also a foundational idea behind cryptocurrency. Therefore, we expect support for H2: H2: Respondents with lower trust in government are more likely to own cryptocurrency.

Our other line of inquiry concerns the personality of cryptocurrency ownership, based on its philosophic origins. We examine the relationship between cryptocurrency ownership and Personality Traits and demographics indicated by preliminary research to determine if there is a “cryptocurrency personality” among a distinct group of Americans. Previous research (described above) implies that there is, and we subject this idea to a rigorous analysis with a large, nationally representative sample of Americans. Our first expectation is for conspiratorial thinking, as those who are fundamentally distrustful of government in any capacity might seek alternative stores of values. Thus, H3: Respondents higher in conspiratorial thinking are more likely to own cryptocurrency.

More generally, we provide theoretical expectations motivated by our discussion of personality in the previous section with respect to the Big Five and the Dark Triad. In brief, cryptocurrency is designed to be a novel store of value for those who do not trust traditional systems and prefer to engage with other individuals directly. Individuals higher in several of the Big Five Personality Traits might be more sympathetic to this ideal, based on their personality. Specifically, individuals who are Open to Experience should be more likely to invest, as cryptocurrency is a novel form of investing. Those high in Conscientiousness should reject cryptocurrency, as its volatile nature contradicts their innate predisposition to control and orderliness. Those who are Extraverted might like cryptocurrency through engaging with its robust community of followers, though this effect should be weaker, as it is less related to the philosophical origins of cryptocurrencies. Disagreeable individuals might see an opportunity to invest in an asset class that is outside of the norm and contrarian. Finally, Emotionally Stable individuals should avoid cryptocurrency, as it would upset their ability to manage their surroundings. Each of these is additionally motivated by linkages between the Big Five (especially Agreeableness and Emotional Stability) and individual risk tolerance (De Bortoli et al., 2019, p. 4). Thus, we offer H4 - H8: H4: Respondents who are more Open to Experience are more likely to own cryptocurrency. H5: Respondents who are less Conscientious are more likely to own cryptocurrency. H6: Respondents who are more Extraverted are more likely to own cryptocurrency. H7: Respondents who are less Agreeable are more likely to own cryptocurrency. H8: Respondents who are less Emotionally Stable are more likely to own cryptocurrency.

These effects should parallel those for other enduring features of an individual’s personality. Those who are high in Need to Evaluate might use their dualistic worldview and tendency to take sides to see the alternative value in cryptocurrency as well as reject a homogeneous approach to investing. Those high in Need for Cognition might simply enjoy cryptocurrency (and investing in it) as an opportunity to think generally about the potential value of a novel investment strategy as well as considering flaws in traditional financial institutions. Thus we offer: H9: Respondents who are higher in Need to Evaluate are more likely to own cryptocurrency. H10: Respondents who are higher in Need for Cognition are more likely to own cryptocurrency.

The Dark Triad might also engage users in cryptocurrency, as they are predisposed to thrill-seeking behavior, an eye for exploitative opportunity, or a self-assessed superior ability to engage with currency. Relative to others, Narcissists are more sensitive to gains than losses, and are more likely to invest in volatile assets (Foster et al., 2011). Thus, Narcissists should be more likely to own cryptocurrency, known for its remarkable volatility. Further, personality research has found that those high in Machiavellianism are less likely to trust others, and that this distrust extends to government (Kay, 2021). Individuals high in Psychopathy may have a higher likelihood of being cryptocurrency owners due to a desire for the huge, rapid reward that investing in cryptocurrency can be. Thus, we expect the following: H11: Respondents who are more Narcissistic are more likely to own cryptocurrency. H12: Respondents who are more Machiavellian are more likely to own cryptocurrency. H13: Respondents who are more Psychopathic are more likely to own cryptocurrency.

Finally, we will control for a variety of demographic and political factors likely to influence an individual’s investing habits beyond their personality. Specifically, we account for individual age, gender, race, education, marital status, their place of residence, their religion, income, stock ownership, government spending preferences, symbolic self-placed ideology, and libertarian values. Each of these variables is outlined in the Supplemental Appendix.

The Profile of American Cryptocurrency Owners

To test these hypotheses, we use what has been previously lacking in research on cryptocurrency owners: a large, nationally representative sample of American adults. We commissioned a YouGov survey in May 2022 of 2500 American adults, and asked them questions about demographics, personality, political attitudes, and perceptions about national conditions. At the time, the U.S. inflation rate was 8.6%, the highest it had been in 40 years. Also at that time, the most popular cryptocurrency, Bitcoin, had halved in value from $65,000 in November 2021 to $30,000 in May 2022. While we cannot test this, we believe this decline in value makes it more likely crpytocurrency speculators and bettors left the market, leaving investors whose long-term antecedents, like personality, are philosophically aligned with the cryptocurrency model. This benefits our sample, as it enhances our understanding of the cryptocurrency investor that is likely in line with its philosophic or economic justifications, outlined above. 10

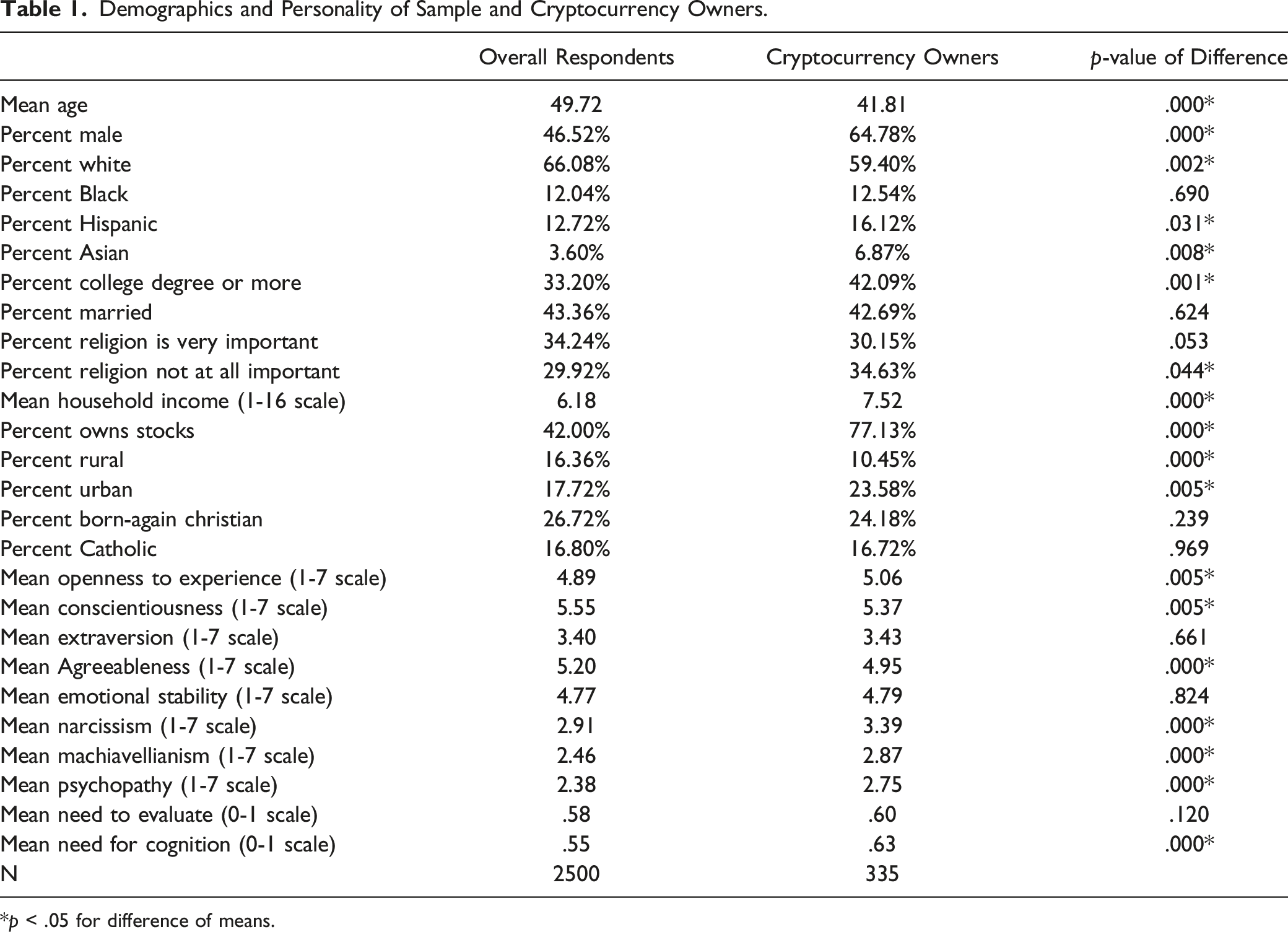

The Demographics of Cryptocurrency Owners

Demographics and Personality of Sample and Cryptocurrency Owners.

*p < .05 for difference of means.

The vast majority (77.13%) of cryptocurrency owners also own traditional stocks, which is far more than the 42% of all Americans in our sample. In line with Bonaparte (2022), cryptocurrency owners are investors and hold other liquid assets as investments. Cryptocurrency owners are also more likely to be educated, confirming Bonaparte (2022), with a higher percentage (42.09%) holding college degrees or post-graduate degrees than the sample average (33.20%).

Our analysis of a nationally representative sample of Americans, however, rejects previous notions about the demographics of cryptocurrency owners in a number of politically relevant ways. First, contradicting Bonaparte’s (2022) initial findings, cryptocurrency owners are significantly less white, but are significantly more likely to be Asian and Hispanic. Cryptocurrency owners are somewhat more wealthy on average. Table 1 also shows that cryptocurrency owners place significantly less importance on religion in their daily lives and are more likely to live in urban environments.

The Personality of Cryptocurrency Owners

An examination of the profile demographics of cryptocurrency owners shows that despite comprising about one in seven Americans, they are distinct from the overall population in many interesting and politically important ways. Their personalities are also distinct. With respect to the Big Five, Table 1 shows Americans who own cryptocurrency are significantly higher in Openness to Experience than average American in our sample, in line with H4. Previous research on the Big Five that conceptualizes Openness to Experience as having a greater tolerance for risk (Ramey et al., 2017) may be something that affects asset trading (Kleine 2016), since cryptocurrency is a volatile and risky asset to own in the short term. Our data also show that cryptocurrency owners are significantly lower in Conscientiousness than the average American, which supports H5. Since Conscientiousness affects ideology, partisanship, and political participation (Mondak, 2010), this is a noteworthy finding. Table 1 also shows that cryptocurrency owners are significantly less Agreeable than the average American, providing some support for H7. They are not, however, significantly different in Extraversion, in contrast to H6.

Table 1 also indicates cryptocurrency owners are significantly higher in all three Dark Triad traits than the average American. This supports our hypotheses H11, H12, and H13, along with some tentative initial research by Martin et al. (2022). However, our finding is based on a larger, nationally representative sample and shows a direct correlation between the Dark Triad and cryptocurrency, absent an intervening variable. In particular, the results for Machiavellianism are in line with previous research (Kay, 2021). The lack of trust in the dollar required to view cryptocurrency as a competitive medium of exchange and store of value, and the foundational lack of trust in banks and government at the heart of Bitcoin, should be more common among those high in Machiavellianism. 11

The high-Dark-Triad nature of Americans who hold cryptocurrency may simply be an artifact of the gender imbalance in cryptocurrency ownership. Men are much more likely to own cryptocurrency than women, and research has found that men score higher on all three Dark Triad traits than women (Chiorri et al., 2019). To account for these differences in demographics, and find what factors seem to cause cryptocurrency ownership and which are merely correlates, we turn to logistic regression analysis. First, however, we look at the profile of cryptocurrency owners on political attitudes and perceptions.

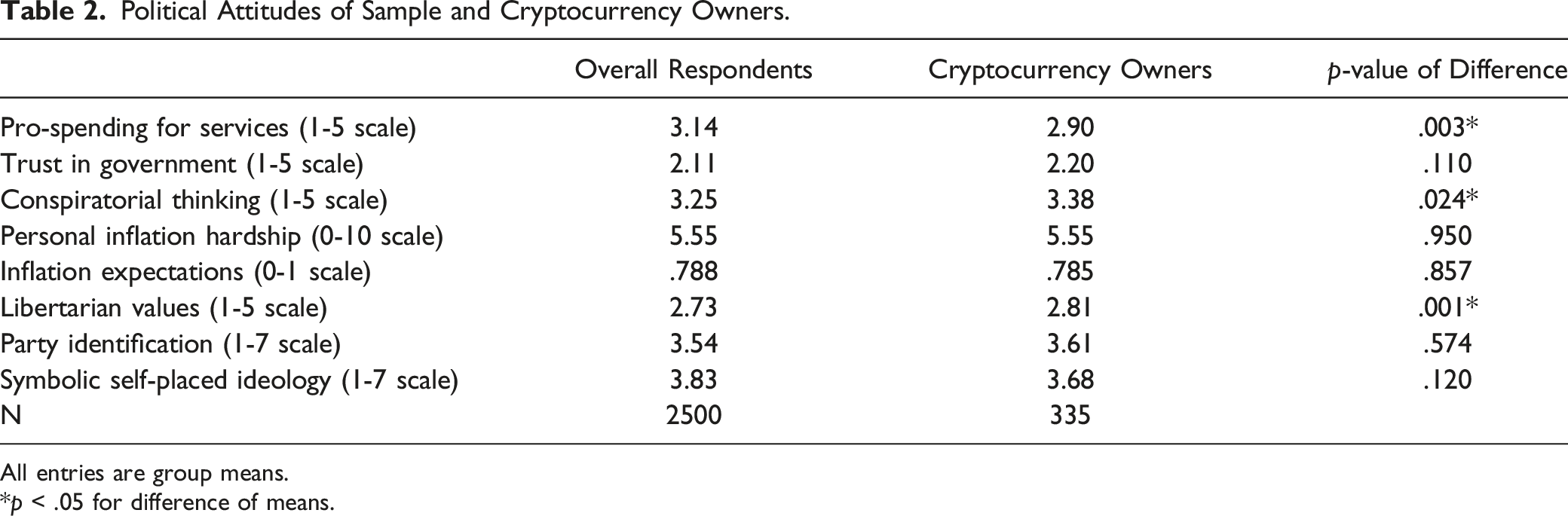

The Politics of Cryptocurrency Owners

A person’s Personality Traits and demographics are relatively fixed. They change little over time, if at all. On the other hand, political attitudes and perceptions are more fluid. Having begun our analysis of cryptocurrency owners by looking fixed characteristics, we now turn to examine their profile on more variable political considerations.

Political Attitudes of Sample and Cryptocurrency Owners.

All entries are group means.

*p < .05 for difference of means.

We also asked our respondents two questions designed to tap their economic pain and expectations about inflation. The first question asked respondents to rate their own experienced hardship because of inflation: “On a scale of 0 to 10, where 0 is no financial hardship whatsoever, and 10 is extreme financial hardship, how would you rate the financial hardship inflation has caused for you and your family over the last six months?” The second question gathered Americans’ perceptions about inflation in the near future: “During the next 12 months, do you think that prices in general will go up, or go down, or stay where they are now?” We expected that cryptocurrency owners would have experienced more hardship due to inflation, since we theorized that some Americans are purchasing cryptocurrency as a way of ameliorating some of the economic pain of inflation.

Table 2 shows that the expectations of

We next examine trust in government. Trust in government is very low among all adults, with the average response (2.11) effectively indicating that the government in Washington can only be trusted some of the time. Trust in government among cryptocurrency owners, while very low, is not significantly different (2.20 vs. 2.11) from the average. Cryptocurrency owners do not trust the national government, but not any less than the average American in our survey. This finding provides some evidence rejecting H2.

We also analyzed the relationship between owning cryptocurrency and average conspiratorial thinking (Uscinski et al.’s (2016) “underlying conspiratorial predispositions”). Three of the four questions whose responses comprise this measure are political in nature, tapping ideas about democracy, elections, and government control. 12 Compared to the average, cryptocurrency owners are marginally more likely to exhibit conspiratorial thinking. This finding provides some support for H3.

Next, we look at libertarian values. We construct this scale from two values core to American ideologies: egalitarianism and moral traditionalism (Enders & Lupton, 2021). Egalitarianism is “the need for the government to ameliorate social and economic inequality” while moral traditionalism “measures individuals’ preference for traditional social and family arrangements and aversion to change” (Lupton et al., 2017). Since one of these captures the values behind liberal economic policy and the other the values behind conservative social policy, opposition to both of them effectively represents libertarian values. Thus, we combine the scales such that higher values on our scale represent respondents who are both anti-egalitarian and anti-traditionalism. We expect cryptocurrency owners to be higher in libertarian values, and Table 2 shows our intuition to be correct. Cryptocurrency owners are higher in mean libertarian values (2.81) than the typical respondent (2.73), and this difference is statistically significant.

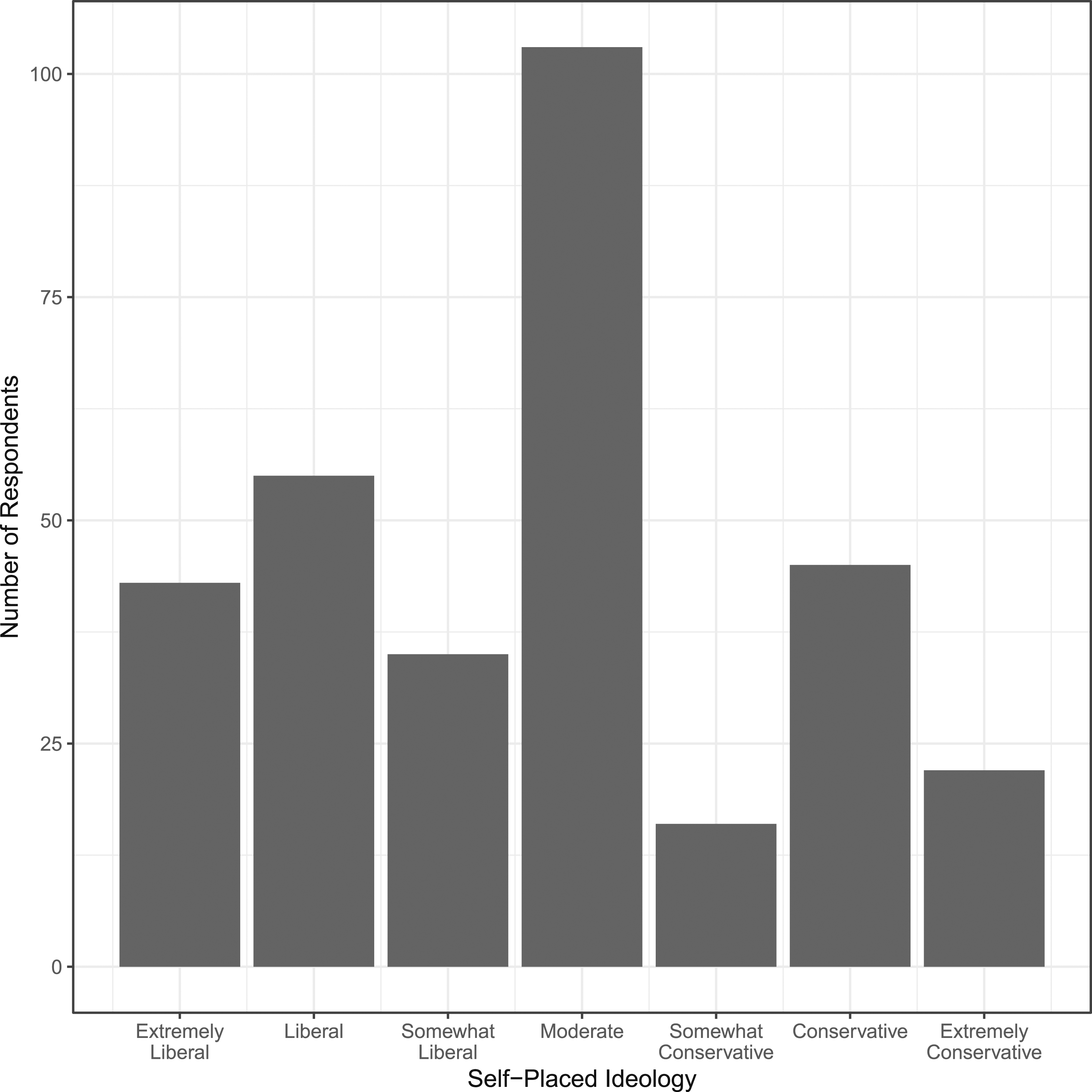

If cryptocurrency owners are somewhat more libertarian than average, they should be caught in the middle between the two parties and ideologies, since a unidimensional seven-point symbolic ideology self-placed scale between liberal and conservative does not capture their orthogonal preferences. Table 2 shows that, as expected, the mean ideological and partisanship preferences of cryptocurrency owners are not significantly different from those of the average American in our sample. Their generally moderate symbolic self-placed ideology is depicted in Figure 1. It is largely similar to those of all respondents but with lower variance and more centrality around “moderate.” Distribution of symbolic ideology of cryptocurrency owners.

To summarize, a descriptive examination of the political attitudes and perceptions of cryptocurrency owners in the American public, therefore, shows them to be similar to the average American. Cryptocurrency owners look a lot like they might vote for either party, with a couple exceptions. They are somewhat more in favor of reducing government spending, even at the cost of fewer services. They are also slightly more likely to have conspiratorial thinking. Cryptocurrency owners, however, are not less trusting of government than the average American. Americans who own cryptocurrency are no more concerned about inflation than the average American. This may be because cryptocurrency owners earn more money than the average American, or because they are less reactive to threats via a personality higher in Psychopathy. This claim, however, can’t be assessed with descriptive statistics alone. To determine what demographics, Personality Traits, and political attitudes and perceptions predict cryptocurrency ownership in the American public, and how cryptocurrency relates to perceptions of inflation, we now turn to logistic regression analysis.

Modeling Cryptocurrency Ownership in the American Public

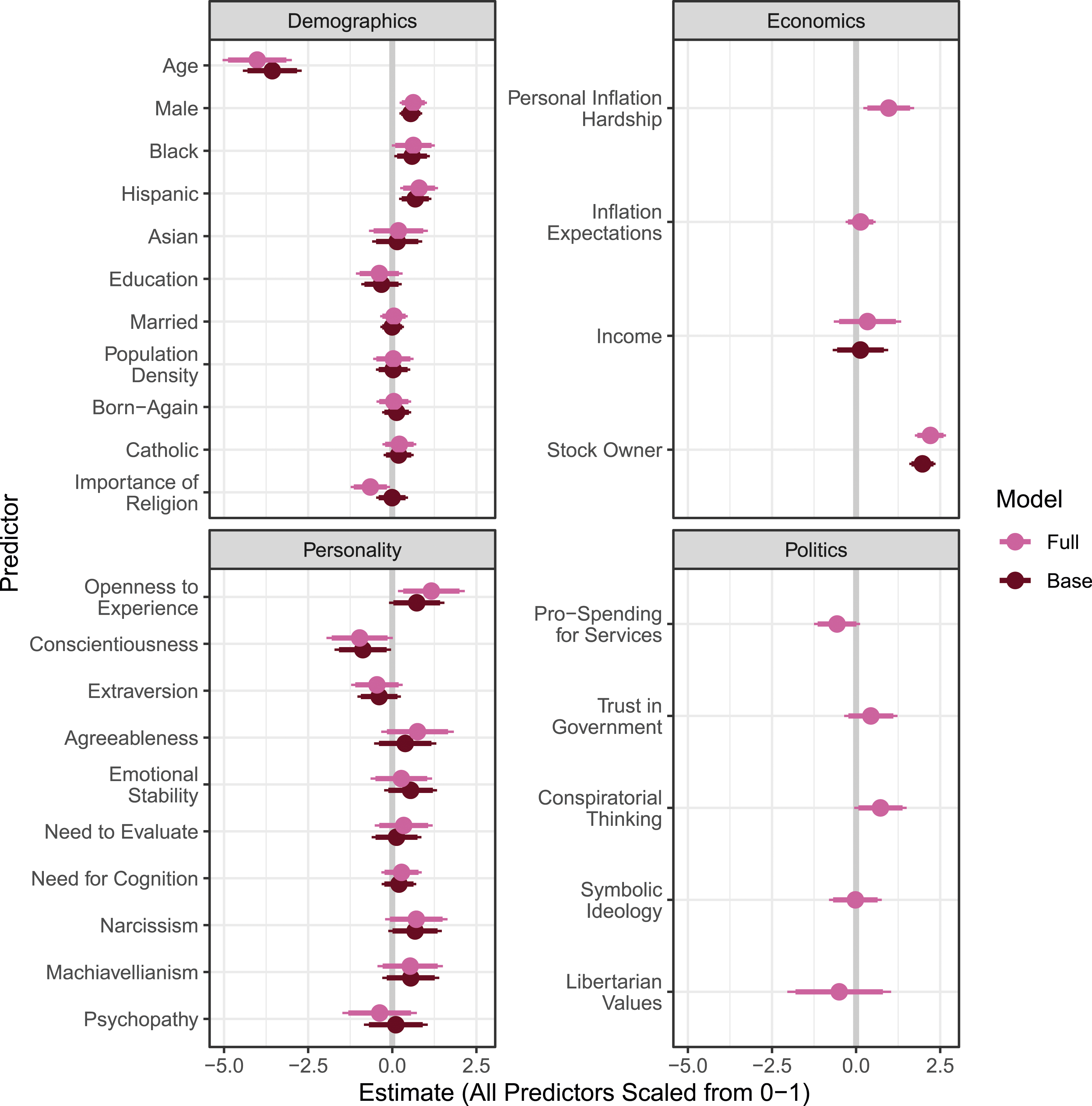

To assess what explains cryptocurrency ownership in the American public, all else equal, we ran a series of logistic regressions of cryptocurrency ownership on Personality Traits, demographics, and political attitudes and perceptions. In Figure 2, we present a coefficient plot of two models: a base model comprising demographics and personality, and a full model which additionally controls for political considerations (including two economic considerations: personal inflation hardship and inflation expectations).

13

Our objective is to question whether these personality results are simply an artifact of other political considerations or whether they persist after controlling for relevant political attitudes. Given the paucity of cryptocurrency ownership, we provide levels of significance for both p < .05 and p < .10. Logistic regression estimates of cryptocurrency ownership, with 95% and 90% error bars.

We start by interpreting the base model (the darker set of estimates). It is immediately apparent that even controlling for other factors, the demographics of cryptocurrency owners are distinct. Black Americans, younger Americans, men, and Hispanics are more likely to own cryptocurrency, as are the less religious and stock owners. These findings about age, men, and stock owners confirm prior research in a much larger, nationally representative sample.

Of course, our theoretical expectations chiefly concern the personality characteristics in the lower left corner. Personality Traits strongly predict cryptocurrency ownership among Americans. Americans who are higher in Openness to Experience and lower in Conscientiousness are more likely to own some cryptocurrency, though the effect for Openness to Experience is not significant in the base model. These findings hold even after accounting for a wide variety of demographics and Personality Traits. All else equal, cryptocurrency owners have a more risk-friendly, less diligent personality than other Americans. Other Personality Traits do not seem to exert an effect; the only other variable significant in the base model is whether an individual owns stocks (as stock owners are much more likely than non-owners to also own cryptocurrency).

We next test whether these effects persist after accounting for political considerations: are personality characteristics really the exogenous force we believe? We turn to interpreting the lighter set of estimates. For demographics, an almost identical pattern of results emerges, except for that Black individuals are now only significantly more likely to own crptocurrency at p = .055. Additionally, individuals to who religion is important are now also significantly less likely to own cryptocurrency.

With respect to our personality predictors, the pattern of effects is also the same as estimated in the base model. Individuals higher in Openness to Experience are now significantly more likely to own cryptocurrency. The effect for Conscientiousness is a little stronger, though significant at p = .053. This gives us confidence that personality effects are not simply a representation of omitted political considerations.

With respect to the newly included political considerations, individuals who have experienced more hardship due to inflation are more likely to own cryptocurrency. Individuals higher in conspiratorial thinking are also more likely to own cryptocurrency at p = .069, echoing a potential preference for alternative investment vehicles among those distrustful of traditional societal systems. Interestingly, neither measure of ideology—symbolic ideology or libertarian values—exert any influence on cryptocurrency ownership.

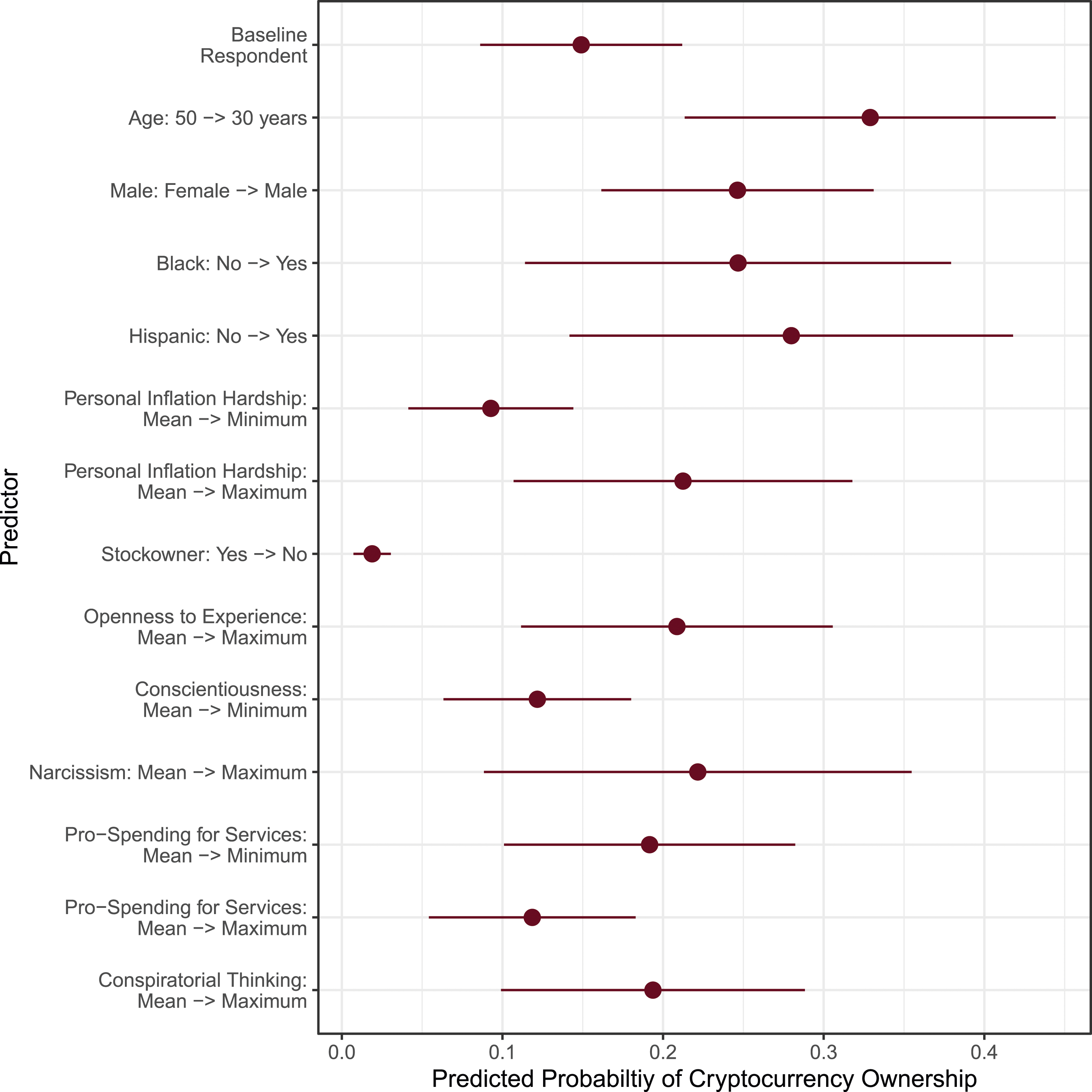

The effects of these significant Personality Traits and demographics on the probability of cryptocurrency ownership by a profile respondent are large. Figure 3 shows how the probability of a profile respondent owning cryptocurrency changes as these significant demographics, Personality Traits, and opinions vary (using estimates from the full model). Readers should compare the estimated probability of ownership as a covariate changes to the Baseline Respondent at the top of Figure 3. This profile respondent is in some sense typical of the sample, with her profile characteristics set at the mode or mean of the sample, or near them. She is 50 years old, single, not an ethnic minority, has a two-year associate’s degree, says religion is somewhat important in her life, earns about $80,000 - $99,999 a year, owns stocks, lives in a suburb, is neither a born-again Christian nor a Catholic, and has all personality and political variables set at their means. Our model predicts her probability of owning cryptocurrency is 14.33%, or roughly the overall sample probability (13.85%). Each other point estimate is the new predicted probability, changing one feature from the baseline. Predicted probabilities of cryptocurrency ownership.

If our profile respondent is 30 years old instead of 50, just 20 years younger, her probability of owning cryptocurrency increases by more than 15 percentage points. Tentative research on cryptocurrency ownership (Auer & Tercero-Lucas, 2022) is confirmed by our large, nationally representative sample. Even accounting for other factors, younger Americans are more likely to own cryptocurrency, and that is still true today. Our analysis also confirms the idea that cryptocurrency owners are more likely to be male than female. If our profile respondent were a man instead of a woman, he would be almost 10 percentage points more likely to own cryptocurrency.

Other factors that have a statistically significant impact on the likelihood that an American owns cryptocurrency also have a large substantive impact. Owning stock makes our respondent almost 13 percentage points more likely to own cryptocurrency than if she did not, all else equal. If she were Hispanic instead of white/Native American/Other (the excluded categories in the model), she would be more than 12.5 percentage points more likely to own cryptocurrency, even accounting for other factors. Black respondents are also considerably more likely to be cryptocurrency owners, though the relatively low number of Black and Hispanic respondents in our sample makes these effects difficult to estimate precisely.

More important to our argument, though, are personality characteristics. Americans who are higher in Openness to Experience are more likely to own cryptocurrency, and this distinction is large, supporting H4. If our profile respondent goes from having sample average Openness to Experience (4.89) to having the maximum (7), she is 6 percentage points more likely to own cryptocurrency. Conscientiousness also has an impact on the probability that someone owns cryptocurrency, evidence for H5. If our respondent had the minimum amount of Conscientiousness (1) instead of the sample average (5.55), she would be about 4 percentage points more likely to own cryptocurrency.

What is particularly noteworthy is how strong the effects of these Personality Traits are on the probability that someone owns cryptocurrency. They are comparable to the effects of influential demographics like gender, ethnic identity, and religiosity, along with stock ownership, which some research has found to be an important predictor (Bonaparte, 2022).

Interestingly, none of the three Dark Triad traits has a statistically significant impact on the probability that an American owns cryptocurrency once other factors are controlled for in the model. Narcissism, however, does have a sizable substantive impact on cryptocurrency ownership (p = .131). If our profile respondent had the maximum Narcissism (7) instead of the sample average (2.91), she would be about 7 percentage points more likely to own cryptocurrency.

The political factors in our model also significantly predict how likely an American is to own cryptocurrency. How much profile respondents says that inflation has created a hardship for their families has a strong effect on their likelihood of owning cryptocurrency. If our female profile respondent in Figure 3 went from having the average reported financial hardship caused by inflation (5.55) to the maximum (10), she would be about 5 percentage points more likely to own cryptocurrency. If she went from no reported hardship to maximum hardship, she would be almost 12 percentage points more likely to own cryptocurrency.

This result provides strong confirmation for

Americans who are concerned about government spending are also more likely to own cryptocurrency. As is shown in Figure 3, if our profile respondent went from having the average preference for government spending (a 3.14, or about “government spends about the right amount and provides about the right number of services”) to the maximum preference for decreasing spending (a 1, or “government should strongly decrease overall spending, even if it means fewer services”), she would be about 4 percentage points more likely to own cryptocurrency. If she changed from preferring that government strongly increase spending to preferring that it strongly decrease spending, she would be about 7 percentage points more likely to be a cryptocurrency owner.

This finding suggests that anti-government-spending philosophy behind the creation of Bitcoin may still play a role in the adoption of cryptocurrency. While views on government spending do not have as large of an impact on cryptocurrency ownership as inflation hardship, they have a maximum effect comparable to about a 10-year shift in an American’s age. This finding fits with some prior research (e.g., Bohr & Bashir, 2014) and provides tentative confirmation of

As Martin et al. (2022) suggest, those who have greater belief in conspiracies are also somewhat more likely to own cryptocurrency. If our profile respondent had the maximum tendency for conspiratorial thinking (5) rather than the average (3.25), she would be more than 4 percentage points more likely to be a cryptocurrency owner. The size of this effect is comparable to that of views on government spending. There is a relationship between how open someone is to ideas like “national currencies are affected by forces which are beyond your knowledge or control,” 14 and how likely that person is to own cryptocurrency. This finding provides some additional evidence supporting H3.

Does Anyone Own Just Cryptocurrency?

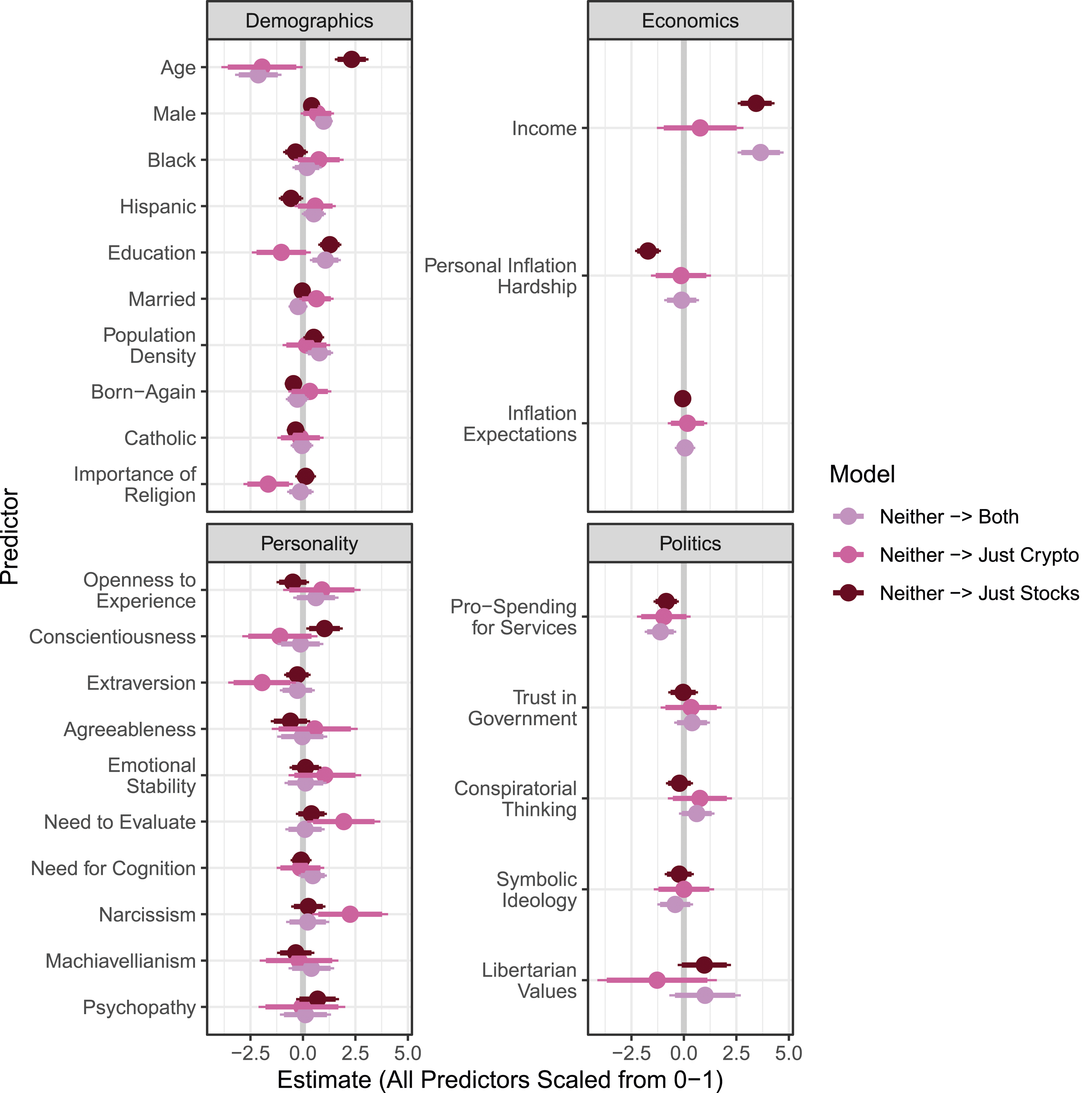

Finally, we assess whether cryptocurrency ownership is fundamentally different from ownership of other investment vehicles. To that end, we estimate multinomial logistic regression, where the baseline category is the ownership of no investments. We estimate the effect of owning just cryptocurrency, owning just stocks, or owning both cryptocurrency and stocks against this baseline. The estimates are shown in Figure 4.

15

The most interesting set of estimates is the middle shade: which factors uniquely predict owning just cryptocurrency? Given that the number of respondents in each category are limited (recall that only 13% of the sample owns cryptocurrency, let alone just cryptocurrency), we again interpret effects significant at both p < .05 and p < .10. Multinomial logistic regression estimates of owning cryptocurrency, owning stocks, or owning both, versus neither (baseline), with 95% and 90% error bars.

Begin with demographics in the top left. Age now looks somewhat asymmetric: older individuals are more likely to own just stocks, while younger individuals are likely to own just cryptocurrency or both, compared to owning nothing. Men are more likely than women to own any of the three options, compared to owning nothing. Individuals with higher education are more likely to own either both or just stocks; individuals with less education are marginally less likely to own just cryptocurrency. In contrast to Figure 4, individuals who identify as born-again are more likely to own either both or just stocks; there is no independent effect for owning just cryptocurrency. However, individuals to whom religion is important are uniquely less likely to own just cryptocurrency. This effect is not present for owning stocks or both stocks and cryptocurrency.

We remain chiefly interested in the effect of the personality and politics variables. Individuals higher in Openness to Experience are more likely to own just cryptocurrency, though not significantly so. Individuals higher in Conscientiousness are significantly more likely to own just stocks; individuals lower in Conscientiousness are less likely to own just cryptocurrency, though not significantly so. Individuals higher in Extraversion are significantly less likely to own just cryptocurrency compared to owning just stocks or to owning both. Those higher in Need to Evaluate are also significantly more likely to own just cryptocurrency. Finally individuals higher in Narcissism are significantly likely to own just cryptocurrency.

Most of the economic and political characteristics are either uniformly insignificant or estimated in the same direction. The exceptions are twofold. First, those with higher personal inflation hardship are no more or less likely to own either just cryptocurrency or just stocks. However, they are uniquely less likely to own just stocks. This finding may indicate that individuals who own just stocks are more likely liquidate their portfolio to cover the increased personal costs of high inflation, while those who own just cryptocurrency or own stocks and cryptocurrency hold their assets. Individuals with higher income are more likely to own either both or just stocks, but no such effect exists for just cryptocurrency. This suggests that individuals with low incomes might see this volatile asset class as an opportunity to gain a faster or greater (though riskier) return to capital than traditional assets.

Discussion and Conclusion

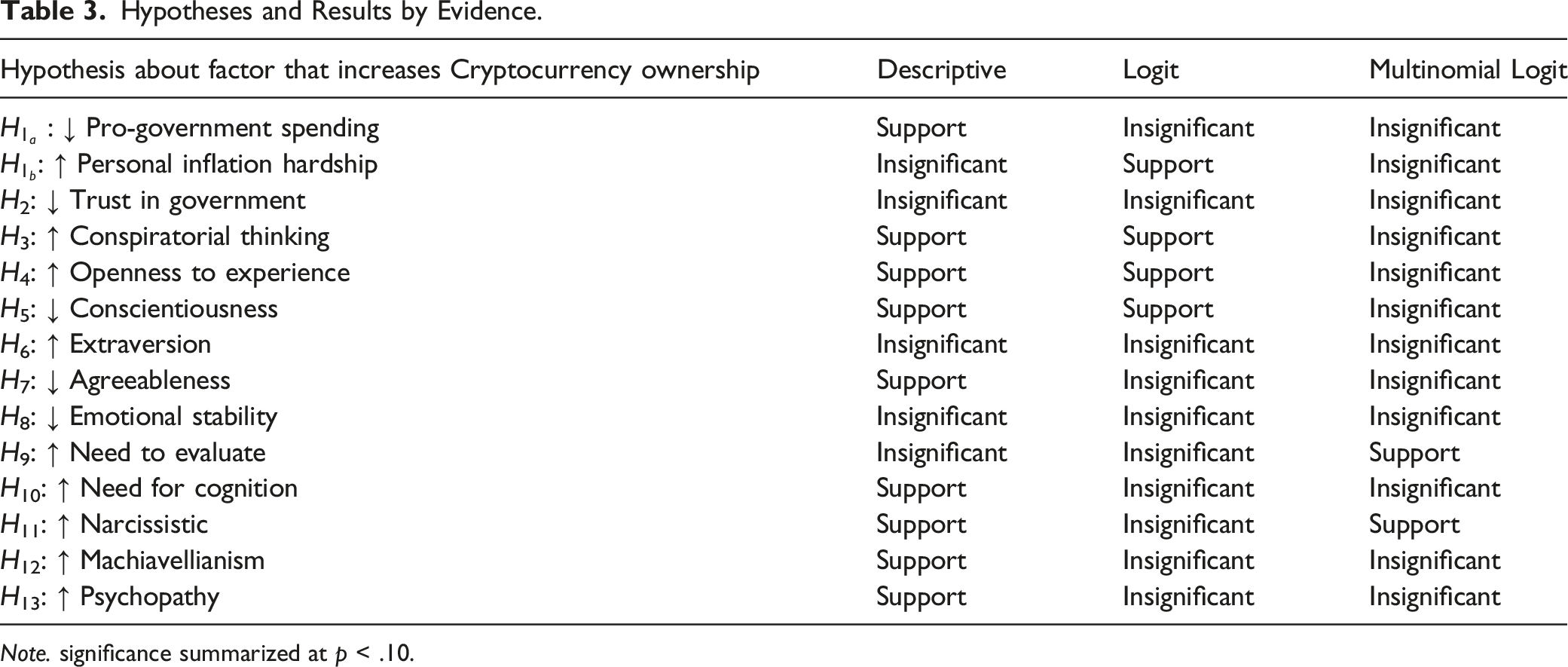

Hypotheses and Results by Evidence.

Note. significance summarized at p < .10.

Using a large, nationally representative sample of Americans, we confirm some aspects of prior research. Younger Americans, men, and those who own stocks are much more likely to hold cryptocurrency than other Americans. We also confirm that marital status and income do not explain cryptocurrency ownership when other factors are taken into account, though the typical cryptocurrency holder earns a slightly higher income than the average American.

The typical American who holds cryptocurrency is also somewhat more likely to believe in conspiracy theories about a lack of government transparency and democratic accountability, though this effect dissipates in multivariate models. Folk wisdom is correct in this regard. Importantly, cryptocurrency owners are not any less likely to trust the American government in Washington than the average American. While their trust in the American government is low, it is not distinct from the average American’s. This is a surprising finding, and one we encourage future research to test with other large, representative samples of Americans. On this basis, we reject H2.

The profile American who holds cryptocurrency is higher in all three Dark Triad Personality Traits of Narcissism, Machiavellianism, and Psychopathy. However, these traits usually do not explain why someone owns cryptocurrency, once other factors are accounted for in a multivariate analysis. Narcissism does not significantly affect an American’s likelihood of owning cryptocurrency among all respondents; however, it does exert a significant effect on owning just cryptocurrency versus no investments or cryptocurrency in conjunction with other assets. We see tentative support for H11. Machiavellianism and Psychopathy do not explain cryptocurrency ownership once other factors are taken into account; we do not have strong support for H12 or H13. Therefore, our findings mostly reject the importance of the Dark Triad traits for the probability that Americans hold cryptocurrency.

We reject a few findings about cryptocurrency owners from prior research in addition to confirming some of our own theoretical expectations. We reject the idea that cryptocurrency owners are more likely to be white or that identifying as white makes someone more likely to own cryptocurrency. Instead, the average, profile cryptocurrency holder in our sample is Hispanic or Asian. Once other factors are controlled for, identifying as Hispanic often makes someone significantly more likely to own cryptocurrency. Black Americans are more likely to hold cryptocurrency than white Americans among all respondents, all else equal. Furthermore, although cryptocurrency owners appear to be significantly more educated than the average American, as Bonaparte (2022) suggests, being more educated is not a significant predictor of cryptocurrency ownership when controlling for other factors.

We also find no evidence of Sudzina et al.’s (2021) conclusion that cryptocurrency owners are higher in Extraversion. Our profile American cryptocurrency holder is no different than the average American in our sample in Extraversion. Extraversion does not significantly predict cryptocurrency ownership among our whole sample in any evidence: descriptive or multivariate. On this basis we strongly reject H6. Furthermore, while Sudzina et al. (2021) appear correct that the average cryptocurrency owner has lower Agreeableness than the average person, lower Agreeableness does not predict cryptocurrency ownership once other factors are taken into account. This finding provides some evidence against H7, and may be due to the overall gender gap in cryptocurrency ownership. Men are much more likely to own cryptocurrency than women, and men are consistently lower, on average, in Agreeableness. Once gender is controlled for, the apparent lower Agreeableness of cryptocurrency owners disappears.

This is not to say that personality exerts no effect on cryptocurrency ownership. The most persistent effects are for Openness to Experience and Conscientiousness. For many, investing in cryptocurrency is literally a new experience, especially compared to traditional investment vehicles. People more amenable to this novelty are more likely to own the asset, providing support for H4. Highly organized individuals prone to caution and impulse control are seemingly put off by the wild swings in the value of cryptocurrency and avoid investing, demonstrating support for H5. This reflects a general disposition towards risk tolerance in investment among individuals high in Openness to Experience as well as low in Conscientiousness (De Bortoli, Da Costa, Goulart, and Campara 2019). However, we find no support for a relationship between Emotional Stability and cryptocurrency ownership, rejecting H8. We uncover mixed evidence for the relationship between cryptocurrency ownership and individuals who are prone to having opinions about many things (Need to Evaluate: H9) or solving complex problems (Need for Cognition: H10). More evidence is needed on these points.

Our other noteworthy contribution is our finding about political attitudes, perceptions, and cryptocurrency. In spite of our theoretical expectations, after controlling for other factors, trust in government is not a significant predictor of cryptocurrency ownership, rejecting H2. However, how much financial hardship someone perceives from inflation is a strong predictor of how likely an American is to own cryptocurrency after accounting for other factors. We find support for

Protection from inflation was an inspiration for the creation of the first cryptocurrency, Bitcoin, and even after controlling for income, stock ownership, and a host of other relevant factors, it is still a reason that Americans own cryptocurrency today. This should not surprise us, since it is easy to buy, hold, and sell cryptocurrency in America. Cryptocurrency seems to have begun functioning, to a limited degree, as a substitutable good for the dollar, in the same way that rival currencies do in a common market as their value varies. A large number of Americans, sensing their commerce and savings threatened by high prices and a dollar whose value seems to be declining over time, seem to be choosing to put some of their wealth in cryptocurrency as a medium of exchange and a store of value. 16 In that respect, Americans are becoming more like Turks 17 and Argentines, who have sought to ameliorate the pain of inflation by engaging in commerce and storing their wealth in another currency.

Inflation affects how likely Americans are to invest in cryptocurrency as a medium of exchange and a store of value. When Americans perceive more financial hardship from inflation, they are significantly more likely to own cryptocurrency. Americans who want to reduce government spending are also more likely to be cryptocurrency owners. These findings suggest that as the U.S. Congress and executive branch consider what to do about high inflation and the government actions that affect it, such as spending and interest rates, they ought to consider the impact of high prices on Americans’ willingness to trade and hold the world’s reserve currency. Our analysis shows that Americans, like Argentines, Venezuelans, Turks, and many others before them, are willing to exchange their national currency for something else that they can easily use as a medium of exchange and store of value in times of economic pain. Our analysis suggests that until high inflation no longer creates hardship for Americans, cryptocurrency may remain somewhat popular, and not just among young, paranoid men who believe in conspiracy theories, as folk wisdom would describe. In fact, this group cuts across traditional ideological and partisan lines: a rarity in contemporary American politics.

Supplemental Material

Supplemental Material - The Personality and Politics of Cryptocurrency Investors

Supplemental Material for The Personality and Politics of Cryptocurrency Investors by Grant Ferguson, Kathryn Haglin, and Soren Jordan in American Politics Research.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the internal Grant-in-Aid from the University of Minnesota.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.