Abstract

Previous research suggests that large firms are more committed to corporate social performance (CSP), because the society exerts heavier pressure on large firms for socially responsible activities, and firms correspondingly conform to the pressure. This seemingly plausible argument, however, ignores the internal process how the response occurs in firms. In this study, the authors propose that the relationship between firm size and CSP is mediated by outside director representation in the board. The authors tested the mediating effect using a data set of 180 Korean firms and found empirical support for the argument. The result indicates that a firm’s social performance is more directly influenced by internal responses, such as appointing more outside directors in this study, rather than firm size. This study advances the institutional theory perspective in the size–CSP linkage by introducing the mediation internal mechanism.

Keywords

Introduction

Corporate social performance (CSP) is defined as a “business organization’s configuration of principles of social responsibility, processes of social responsiveness, and policies, programs, and observable outcomes as they relate to the firm’s societal relationships” (Wood, 1991, p. 693). The interest in CSP has been heightened in the modern society, and firms have responded to the interest by actively participating in socially responsible activities (Freeman, 1984; O’Shaughnessy, Gedajlovic, & Reinmoeller, 2007). Among others, firms’ active participation can be explained by their pursuit of legitimacy (DiMaggio & Powell, 1983; Meyer & Rowan, 1977). Stakeholders in the society often use social performance as a criterion to judge firms (Fombrun & Shanley, 1990; Lewis, 2003), and firms regard the social demands for CSP as normative guidelines (Maignan & Ferrell, 2004; Shepard, Betz, & O’Connell, 1997). By supporting socially responsible activities, firms can gain legitimacy as a reward.

Previous research suggests that firm size has positive effect on CSP (Johnson & Greening, 1999; Muller & Kolk, 2010). Since the society tends to pay more attention to large firms, interpreting the attention as institutional demands or pressures, large firms are more willing to orient their activities toward stakeholders’ calls than small firms (Fombrun & Shanley, 1990; Stanwick & Stanwick, 1998; Udayasankar, 2008). However, such an institutional theory argument omits the role of internal process of firms. Neo-institutional theorists argue that institutional pressures are not just given to firms, but firms internalize and respond them strategically, within the context of external constraint (Oliver, 1991; Suchman, 1995).

This study aims to fill the research void by exploring one of the possible paths between firm size and CSP. Specifically, we suggest that firm size–CSP relationship is mediated by outside directors. Although several variants of definitions are used in previous studies, the corporate governance literature (e.g., Hillman, Cannella, & Paetzold, 2000; Walsh & Seward, 1990) defines outside directors as board members who are not managers or employees of the firm. For example, political leaders, university faculty members, senior officers of other firms, and leaders of community organizations are often recruited as outside directors. Prior studies (e.g., Wang & Dewhirst, 1992) suggest that because of their background and experience outside the focal firm, outside directors have greater knowledge and relationship with diverse stakeholders. Thus, we argue that as a response to stronger institutional pressures, large firms seek more outside directors who tend to have strong orientation toward stakeholders (Pfeffer & Salancik, 1978). Subsequently, outside directors would support and initiate socially responsible activities, making positive impact on firms’ CSP. In sum, this research proposes that CSP should be understood as an outcome of outside directors rather than firm size.

Theoretical Background

An Institutional Perspective on CSP

The early CSP literature paid substantially more attention to the consequences over antecedents of CSP. One reason might be that CSP was a relatively young field that sought acceptance by discipline-based scholars (see Borgatti & Foster, 2003). Another reason could be the prevailing cynicism that firms seldom reap financial benefits from engaging in CSP activities. Consequently, the determinants of CSP have been relatively underexplored compared with the outcome of CSP (Orlitzky, Schmidt, & Rynes, 2003).

More recent CSP research, however, has developed several arguments that explain why firms engage in CSP from a motivation standpoint (Aguilera, Rupp, Williams, & Ganapathi, 2007). First, firms seek CSP with instrumental motives to achieve greater profitability (Bansal & Clelland, 2004; McWilliams & Siegel, 2001). This approach is in accordance with the neo-classical economic framework, which proposes that firms can generate goodwill as a by-product of pursuing greater profits. Second, the moral motive argument suggests that firms engage in CSP when organizational key decision makers, such as top managers, are highly committed to moral/prosocial values. Stewardship theory supports this moral motive argument (Davis, Schoorman, & Donaldson, 1997).

A third stream of research emphasizes the relational or institutional motives viewing CSP as firms’ conformity or reaction to institutional forces (e.g., O’Shaughnessy et al., 2007). Institutions are defined as regulatory structures, governmental agencies, laws, courts, professions, interest groups, and public opinions (Scott, 1987a, 1987b). Their pressures are so influential—through constraining, constructing, or empowering the organizational actors—that institutions have tremendous influence on any strategic decisions of firms (Parsons, 1960; Weber, 1978). This view suggests that strategic decisions pertaining to CSP may reflect firms’ intentions and efforts to conform to institutional pressures (Kagan, Gunningham, & Thornton, 2003).

The institution–legitimacy thesis supports the positive effect of firm size on CSP. In essence, CSP should be understood as the result of firms’ legitimacy pursuits. Societies tend to impose more stringent standards, such as stricter tax imposition and governmental regulations, on large firms because of their visibility and scale of activities. As a response, large firms seek to align their activities with institutional calls in order to achieve legitimacy (Fombrun & Shanley, 1990; Stanwick & Stanwick, 1998; Udayasankar, 2008). Furthermore, since stakeholders often use CSP as a criterion to evaluate firms (Fombrun & Shanley, 1990; Lewis, 2003), firms consider demands for CSP as normative guidelines to conformity (Maignan & Ferrell, 2004; Shepard et al., 1997). By actively engaging in CSP, large firms can gain legitimacy as a reward.

However, the institution–legitimacy perspective has overlooked firms’ internal mechanisms in responding to institutional demands and pressures. Scholars have criticized the institutional theory for its lack of attention to organizations’ active responses to institutional pressures and expectations (Covaleski & Dirsmith, 1988; DiMaggio, 1988; Meyer & Rowan, 1983; Oliver, 1991; Suchman, 1995). For instance, since legitimacy could be considered an operational resource, it is important to recognize firms’ strategic process through which they seek legitimacy (Ashforth & Gibbs, 1990; Dowling & Pfeffer, 1975). Likewise, Oliver (1991) suggests that a widespread establishment, such as the Environmental Protection Agency or relevant departments, is clear evidence that firms make a strategic attempt to seek legitimacy or reputations by avoiding public criticisms of noncompliance. Taken together, it is valuable to incorporate firms’ response processes into the relationship between firm size and CSP.

Firms’ Strategic Responses to Institutional Pressure for CSP

As mentioned earlier, large firms are more susceptible to institutional pressures. As such, they are more likely to seek an effective strategic response, which may satisfy the high levels of institutional demands. The response might bring legitimacy to large firms. Institutional pressure for CSP is not an exception. Since large firms tend to receive more intense pressures for CSP implementation, they are likely to choose an effective strategic response to signal their high commitment to CSP.

One of the effective ways to satisfy the institutional demands is to build a board structure committed to CSP. When firms are confronting with external pressures for CSP, they may aim to reconfigure board resources and shape its structure to signal their commitment to CSP since a board structure can be seen as a corporate window reflecting value and worth of the organization (Certo, 2003; Pfeffer & Salancik, 1978). Firms’ commitment to CSP could be assessed by the extent to which their board is structured to be highly attentive and responsive to multiple stakeholders’ interests and demands and by the degree to which their board is committed to establishing positive relationships with stakeholders. In this article, we propose that outside director representation is one of the key elements of CSP-committed board structure (e.g., Johnson & Greening, 1999), and it mediates the relationship between firm size and CSP. To explain the mediating mechanism, we develop three hypotheses: ones for the relationship between (a) firm size and CSP, (b) firm size and outside director representation, and (c) outside director representation and CSP.

Hypotheses Development

Firm Size and CSP

Firms seek to gain legitimacy by conforming to the institutional expectations. Since CSP often has been viewed as a criterion for stakeholders to judge firms (Lewis, 2003), firms perceive the institutional pressures for CSP as normative guidelines to conformity (Maignan & Ferrell, 2004; Shepard et al., 1997). These pressures are often stronger on large firms because of their visibility (Stanwick & Stanwick, 1998; Udayasankar, 2008). In response, large firms have to devise effective responses to institutional pressures, hoping for obtaining legitimacy.

Several studies have suggested and found support for the positive relationship between firm size and CSP. Cowen, Ferreri, and Parker (1987), for example, argue that since large firms tend to have a stronger social impact because of their scale of activities, they are more likely to actively engage in socially responsible practices than are small firms. Udayasankar (2008) similarly argues that because of their visibility, large firms are highly motivated to align their business activities with what constituents would expect them to do, including firms’ social engagements. In addition, Fombrun and Shanley (1990) suggest that intense public scrutiny may place direct pressure on large firms, so that they actively engage in respectful activities. Empirical studies have also found support for the positive relationship between firm size and CSP (e.g., Johnson & Greening, 1999; Muller & Kolk, 2010; Stanwick & Stanwick, 1998). Therefore, we propose that a firm’s size will be positively associated with its social performance:

Hypothesis 1: A firm’s size is positively associated with its corporate social performance.

Firm Size and Outside Director Representation

It is seemingly plausible that large firms are likely to be more committed to CSP because of intense public attention and scrutiny. Yet it is still unclear how large firms achieve high CSP. One of the possible paths linking firm size and CSP can be found in the resource dependence theory that highlights the role of board structure in responding to institutional pressures.

Pfeffer (1973) claims, “[B]oard size and composition are not random or independent factors, but are rational organizational responses to the conditions of the external environment.” Meyer and Rowan (1977) also suggest that by incorporating socially rationalized elements in their formal structures, such as board structure, organizations maximize legitimacy and increase resources and survival capabilities. Certo, Daily, and Dalton (2001) similarly suggest that board structure, including size and composition, is closely associated with firms’ legitimacy gain because board structure can function as a window reflecting organizations’ value and worth. It is consistent with the resource dependence framework that firms would try to reconfigure board resources and shape their board structure to signal commitment to CSP when they face external pressures for social participation.

Accordingly, in this article, we suggest that outside director representation is critical in developing firms’ commitment to CSP. Outside director representation can signal to the public that firms have great willingness to monitor top managers’ agency behaviors and to promote stakeholders’ benefits. Since the selection of outside members can be viewed as a strategic decision to manage the relationships with their business environment, outside directors can enhance organizations’ reputations and credibility by helping firms establish and maintain legitimacy (Pfeffer & Salancik, 1978). Given that CSP is characterized by organizational efforts to build a positive relationship with environmental constituents (Wood, 1991), enhancing outside director representation can be viewed as organizations’ strong commitment to CSP. Therefore, firms under the high pressure for CSP are likely to appoint more outside directors.

Existing evidence confirms the above argument. For example, Boone, Field, Karpoff, and Raheja (2007) found a positive relationship between firm size and the proportion of outside directors in a sample of 1,019 U.S. firms. Chizema and Kim (2010) also found a similar result that firm size is positively associated with outside director representation in 2,233 firm-year observations of Korean data.

In sum, as size increases, a firm is likely to face more intense institutional pressures for CSP. In turn, it can strategically recruit more outside directors in order to gain legitimacy. Therefore, we propose the following hypothesis:

Hypothesis 2: A firm’s size is positively associated with its outside director representation in the board of directors.

Outside Director Representation and CSP

Stakeholder theory views stakeholders as any groups or individuals who can affect, or be affected, by achievement of the organization’s objectives, and it consider business a set of relationship among stakeholder groups and/or individuals (Freeman, 1984). Although recent CSP scholars suggest a moral basis for stakeholder management, the initial intent of stakeholder theory is directed toward a strategic approach in that organizations justify broader social policies and actions for strategic purposes (Freeman, 1984; Laplume, Sonpar, & Litz, 2008). In this vein, managers’ task is to manage those relationships for creating and distributing value for stakeholders (Parmar et al., 2010). Outside directors’ strong knowledge and relationship with diverse stakeholders beyond a firm’s boundary can facilitate bringing more stakeholders’ voice into the company’s boardroom and ultimately help satisfy stakeholders.

The above stakeholder theory argument is closely aligned with the resource dependence theory, which suggests that organizations are considered to be composed of external and internal coalitions; to survive in an environment with scare but valuable resources, organizations have to minimize their dependence on others but to gain external resources (Pfeffer & Salancik, 1978). One potential solution for obtaining external resources is to use outside directors. One of the valuable resources that outside directors provide to extant internal managers is knowledge and relationship with diverse stakeholders, which make them more conscious about the needs and expectations of various stakeholders (Wang & Dewhirst, 1992). Outside directors help top managers respond appropriately to external constituencies in participating in a wide variety of stakeholder-oriented activities (Pfeffer, 1973; Pfeffer & Salancik, 1978). Such activities can include compliances with environmental standards to avoid penalties, fines, and negative media exposure, and ultimately loss of reputation (Johnson & Greening, 1999). Similarly, Ibrahim, Howard, and Angelidis (2003) claim that the proportion of outside directors is positively related to the philanthropic component of CSP since outside directors tend to have strong social orientations.

Furthermore, outside directors’ monitoring role in the board supports the positive relationship between outside directors and strong CSP. Strategic decisions in a firm can be viewed as outcomes of the interactions among board members (Zajac & Westphal, 1996). Prior CSP studies suggest that different types of board members (e.g., internal vs. external boards) may have different orientations and preferences over firms’ social investments (Ibrahim & Angelidis, 1995; Ibrahim et al., 2003). Although CSP research has extensively investigated the effect of firm’s social actions on financial performance, past studies often found mixed results leaving ambiguities in the relationship (Margolis & Walsh, 2003). Considering that top managers’ incentives are largely aligned with the stockholders’ interest (or firm’s financial performance), it is more likely that managers are reluctant to support their firm’s active pursuit of stakeholders’ value above and beyond stockholders’ value. In this regard, agency theorists suggest that one of the primary functions of the boards is to monitor managers’ decisions and actions on behalf of stockholders (Fama & Jensen, 1983; Jensen & Meckling, 1976). Yet, from the perspective of stakeholder theory, the beneficiaries of the board’s service should include not only stockholders but also other stakeholders (Tirole, 2001). In safeguarding diverse stakeholders’ interests, it is expected that outside directors are more effective than inside directors since outside directors’ incentives are less likely affected by dependence on top managers. In contrast, insiders’ main function is often viewed as legitimizing top management’s decisions (Ibrahim et al., 2003). When there are a large number of outside directors in the boardroom, they can exercise substantial influence over the board’s strategic decisions for social investments. Therefore, a greater number of outside directors can have strong discretionary powers and ultimately elicit the firm’s CSP. All things considered, we predict that greater representation of outside directors on the board positively affects CSP.

Hypothesis 3: Outside director representation is positively associated with a firm’s corporate social performance.

Method

Institutional Context

Our main proposition is that CSP is the outcome of firms’ strategic responses to institutional pressures on corporate social contribution. To test the proposition, we use a sample of large Korean firms. Prior studies on CSP in the Korean context are rare (for exceptions, see Chapple & Moon, 2005; Oh, Chang, & Martynov, 2011), and those studies did not clearly consider the contextualized meaning of CSP. In this regard, Matten and Moon (2008) can offer a useful insight for the meaning of CSP in the country-institutional context, although they focused on the United States and Europe. Matten and Moon (2008) characterize the U.S.-style CSP as explicit, which is generally composed of voluntary programs and strategies that combine social and business value and address issues perceived as being part of social responsibility of the company. In comparison, they describe the European CSP as implicit, which normally consists of values, norms, and culture that result in customary requirements for corporations to address stakeholder issues; and in this system, individual firms tend not to commonly articulate their own versions of such responsibilities.

We believe that CSP in the Koreas context is closely aligned with the U.S. style. It has been acknowledged that Korean firms increasingly accept the U.S. management practices (Cho & Kim, 2007). The Asian financial crisis in the late 1990s spurred structural reforms in Korean firms and the economy (Arogyaswamy, 2001). For example, since the Asian financial crisis, Korean firms have adopted Western-based corporate governance systems, including appointment of foreign outside directors mostly from the United States (Chizema & Kim, 2010; Cho & Kim, 2007; Kim, 2007). Furthermore, Korean firms have been paying escalating attention to stakeholder-oriented practices, such as CSP. Evidence shows that Korea is one of the few Asian countries promoting firms’ social responsibility (e.g., Chapple & Moon, 2005); specifically, CSP from many Korean firms have been qualified by the U. S.-based assessments; and Korean firms have appeared in the Dow Jones Sustainability Indexes (see http://www.sustainability-index.com). It is noteworthy that, among many Asian countries, only Korea and Japan have successfully launched their individual social indices, such as the Dow Jones Sustainability Index Korea (DJSI Korea) and DJSI Korea 20. Taken together, CSP in Korea seems to be interpreted and assessed in a similar way in the United States. Korean firms’ increasing effort for adopting the U.S.-style management and CSP standards may endorse our overall theoretical approaches and hypotheses development on the basis of previous U.S.-based research.

Sample

All sample firms are large firms listed on the Korean Stock Exchanges (KSE) as of 2005. We initially selected target firms that appeared in the list of 2006 top-200 best corporate citizens, assessed by a leading Korean CSP evaluating institution, Korea Economic Justice Institute (KEJI). The CSP ratings are officially labeled as the KEJI Index. The trustworthiness of the KEJI Index is manifested by a 20-year-long history of publication as well as its extensive usage (e.g., Oh et al., 2011). The 2006 KEJI Index was based on firms’ CSP in year 2005 (i.e., 2006 is the year of publication).

Firm-level data were drawn from archival sources using Korea Listed Companies Association’s Directory of Corporate Management (for details, see Kim, 2005, 2007) and KISVALUE, a Korean electronic database equivalent to COMPUSTAT in the U. S. context. To ensure the sufficient time lag, we matched each firm’s CSP ratings (KEJI Index) in 2005 with a 3-year average of financial records between 2002 and 2004. Our final sample size decreased to 180 firms because of the full data availability.

Variables

Firm size

We used the natural logarithm of total asset as a proxy of firm size. Total asset has been one of the most commonly used proxies for firm size in previous studies (e.g., Morrow, Sirmon, Hitt, & Holcomb, 2007; Waddock & Graves, 1997).

Outside director representation

We calculated the Outside Director Representation by dividing the number of outside directors on a board by the total number of board members, following previous literatures (e.g., Mallette & Fowler, 1992). In measuring the outside director representation, we did not include gray or affiliated directors who are not managers or employees but have direct ties to the firm (e.g., relatives of founding family and business dealings with the company). The value is the average between 2002 and 2004.

CSP (KEJI Index)

The KEJI Index relies on multiple data sources. KEJI collected information in a disciplined process from a wide variety of companies, the Korean government, nongovernment organizations, and media sources. Firms are rated with standardized values based on original interval scales (i.e., A, B, C, D, and E) in seven major subdomains, including Environment, Community, Corporate Governance, Corporate Integrity, Customer Satisfaction with Product Quality and Safety, Employee Relations, and Long-term Orientation. These domain-specifics are comparable to Kinder, Lydenberg, Domini Research, and Analytics (KLD) ratings in the United States, in that KLD ratings consist of the following subdomains: Environment, Community, Diversity, Employee Relations, Human Rights, Product Quality and Safety, and Corporate Governance. Seventeen analysts—6 KEJI’s senior analysts and 11 independent university faculty with doctoral degrees in economics and business—were involved in developing the KEJI Index. For quality assurance, the KEJI auditing committee, composed of multiple public accountants, performed a quality review of every company profile. Because of the reliability of KEJI Index, previous researches used this Index as a valid measure for CSP (e.g., Oh et al., 2011). The highest possible score of KEJI Index is 75. We used 2006 KEJI Index, which represents the CSP ratings of 2005. It should be noted that KEJI Index contains the information of outside director independence in the domain of Corporate Governance, so the overlap might create a spurious relationship between predictor variable (the proportion of outside directors) and criterion variable (CSP ratings) in our empirical models. Therefore, we adjusted the total score of KEJI Index by removing the outside director information from the KEJI Index using the formula used to calculate the original score. To check the robustness of our analysis, we also conducted analyses using unadjusted scores of KEJI Index and the results were virtually same.

Control variables

We included industry dummies and firm characteristics as control variables in the analysis. First, we controlled for firms’ financial performance effect. Waddock and Graves (1997) argue that large firms’ strong commitment to CSP might be because they have more slack resources than small firms. To separate slack effect from the firm size effect, we included return on assets (ROA) as a proxy of slack resources. We also included debt ratio in our analysis, calculated by long-term debt divided by total equity. A high level of debt might discourage managers from being committed to CSP in order to satisfy multiple stakeholders’ claims.

We included board size as another control. Small boards might have stronger interpersonal ties, which may lead to greater loyalty to top management (Faleye, 2003; Hatfield, Worrell, Davidson, & Bland, 1999). In turn, they possibly become in favor of top managers’ decisions. In contrast, large boards are likely to be independent and exercise more power over top management, and they may affect top managers’ strategic decisions more objectively. Similarly, Zahra and Pearce (1989) argue that firms with large boards are more likely to contain expertise that protects the boards from dominance of top management. Board size is measured by the total number of directors on the firm’s board.

Firm age was also controlled. Previous studies found that firm age can positively (Moore, 2001; Roberts, 1992) or negatively (Cochran & Wood, 1984) affect firms’ CSP. Firm age was calculated by the number of years since a firm’s foundation. We controlled for change of CEO since it can influence firms’ strategic decisions (e.g., Beatty & Zajac, 1987; Pitcher, Chreim, & Kisfalvi, 2000). We created a dummy variable that we coded as 1 if there was change of CEO from 2002 to 2004, or 0 otherwise.

Furthermore, we included industry dummies based on the information reported in the KEJI data, to control for industry effect. Historically, the Korean Stock Exchange (KSE) has classified industries into 70 to 80 categories. However, considering the relatively small sample size of this study (N = 180), using 70 to 80 dummy variables to control for industry effect may mislead any statistical tests and interpretation of findings. Therefore, we adopted the industry categorization in the KEJI data, where industries are classified into four categories: the Metal/steel/chemistry, Service/nonmanufacturing, Food/textile/papers, and Electronics/IT industries. All control variables, except industry dummies, are average for 3 years in 2002, 2003, and 2004. Finally, we included an inverse Mills ratio as a control variable to correct nonrandomness of our sample, as discussed below.

Analysis

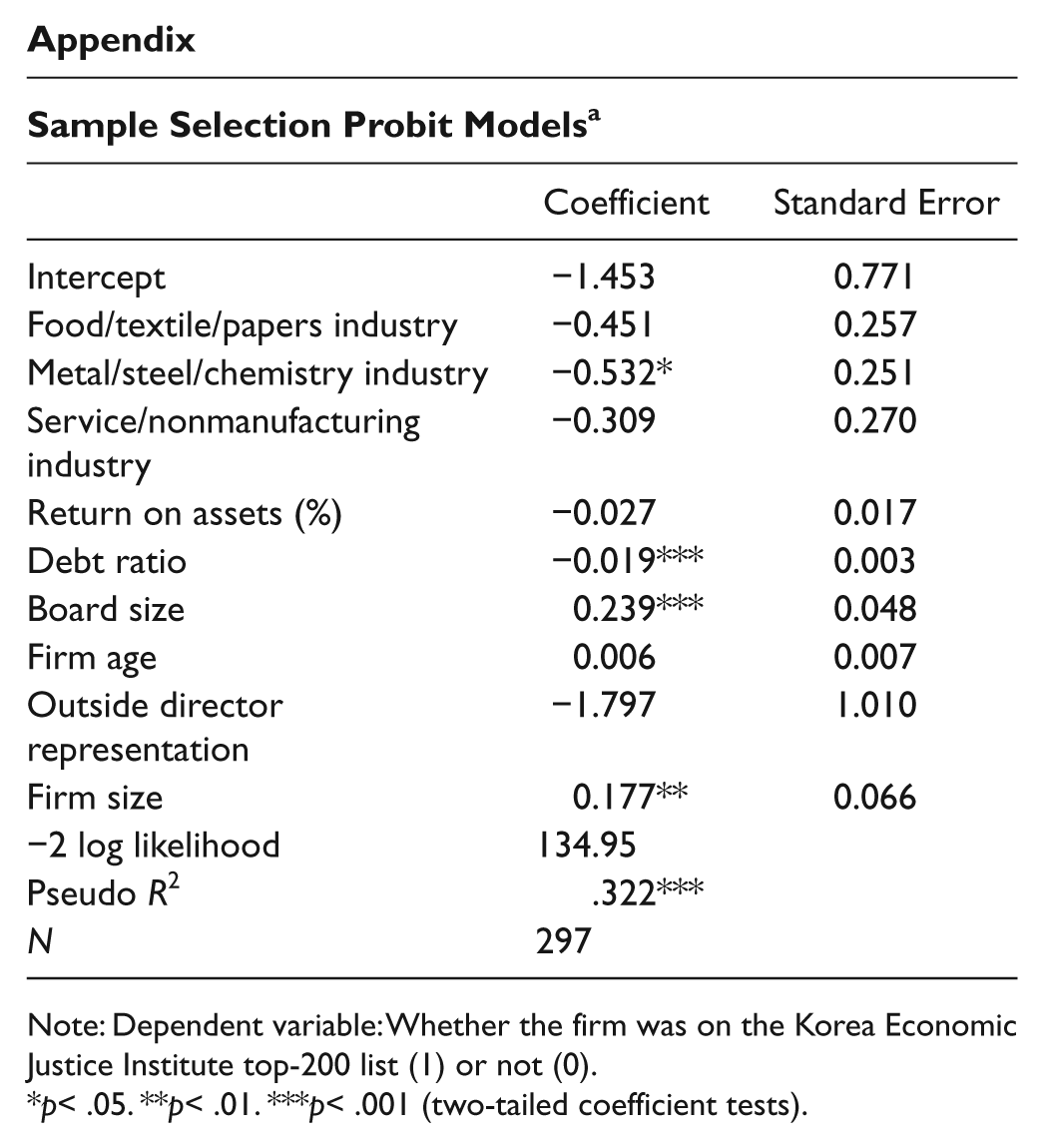

Our sample included “2006 top-200 best corporate citizens” in the KEJI Index. Since only top performers in CSP are included, our sample potentially represents more socially responsible firms than average Korean firms. To effectively address this nonrandomness, we used a Heckman selection model (see Heckman, 1979), a two-staged procedure that corrects sample selection biases. As a first step, we estimate the likelihood that a firm was on the list of top-200 best corporate citizens using probit regression model (N = 297). In our data year, KEJI evaluates roughly 350 firms and announced top-200 best corporate citizens. Data availability reduced the sample size of the probit regression to 297. Multiple variables were used to predict the likelihood (Y) that the firm was nominated as a best corporate citizen; the model took the following form:

The results of the first-stage probit regression are reported in the appendix. The selection model generated an inverse Mills ratio, which is included as an additional explanatory variable in our second-stage ordinary least squares (OLS) regression analysis predicting CSP. Since the probability of being included in the KEJI Index is reflected in the inverse Mills ratio, this approach helps to correct selection bias from nonrandomness of our data.

Results

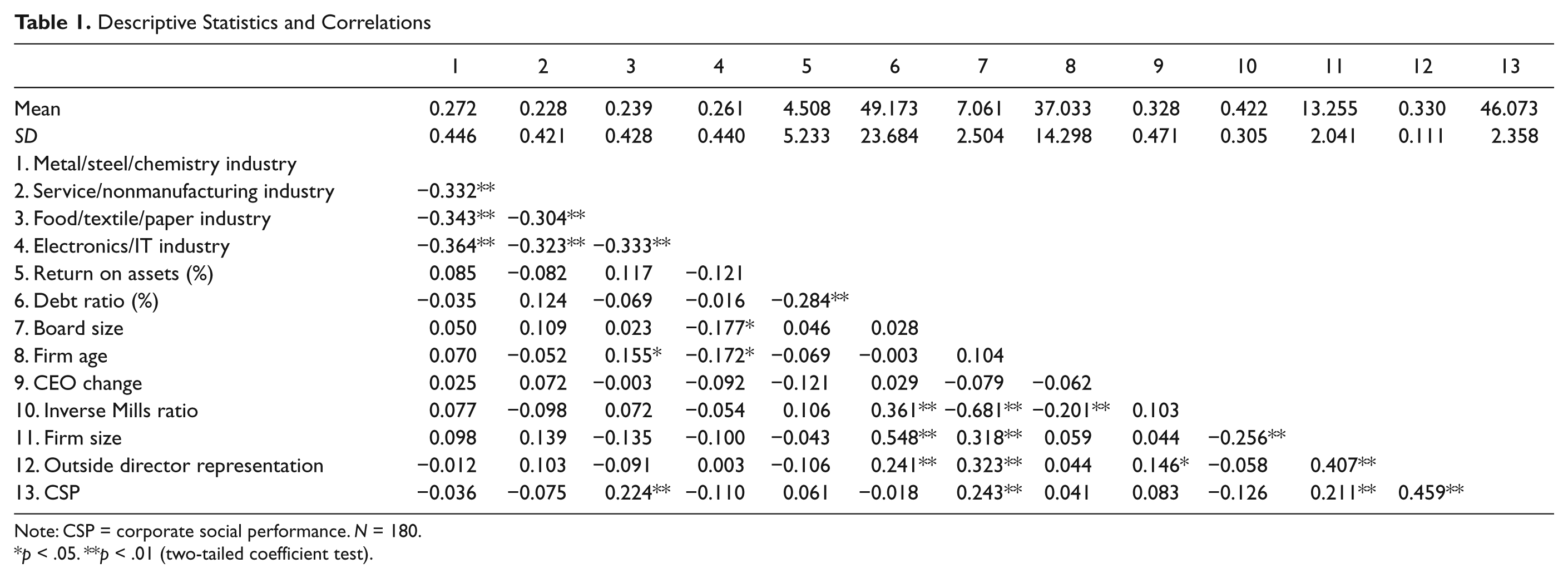

The means, standard deviations, and correlations for sample firms are presented in Table 1. The average proportion of outside directors in Korean sample firms is 0.33 with standard deviation of 0.11. Notably, the mean indicates that the outside directors are relatively underrepresented in Korean firms as compared with U. S. counterparts (e.g., 0.62 for 127 firms in Zahra, 1996 and 0.68 for 252 firms in Johnson & Greening, 1999). The average KEJI Index is approximately 46.07 with standard deviation of 2.36.

Descriptive Statistics and Correlations

Note: CSP = corporate social performance. N = 180.

p < .05. **p < .01 (two-tailed coefficient test).

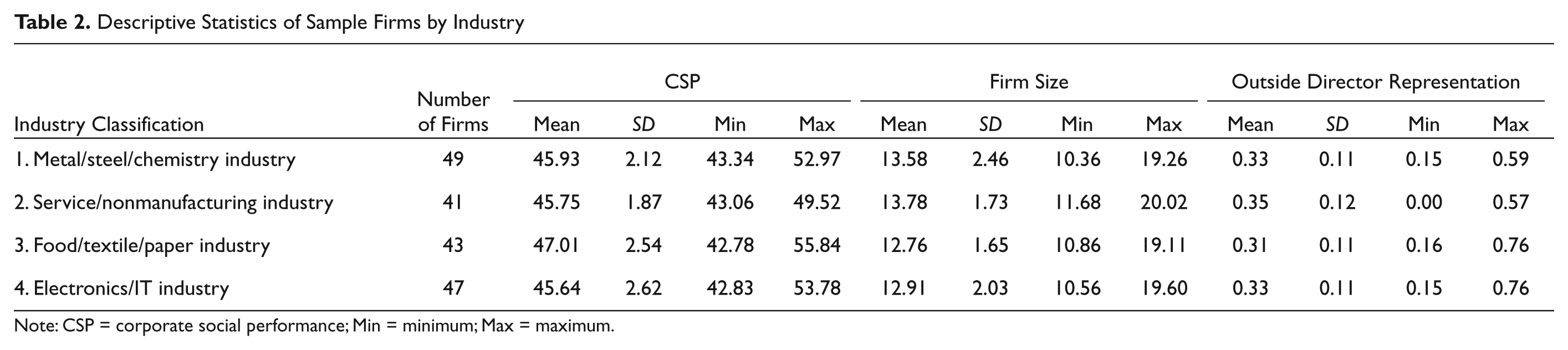

Among our samples, 47 firms fall into the electronics/IT industry, 49 firms in the metal-steel/chemistry industry, 41 firms in the service/nonmanufacturing industry, and 43 firms in the food/textile/papers industry. We included three industry dummies in our analysis, using the electronics/IT industry as a reference group. Descriptive statistics of our sample firms by industry is presented in Table 2.

Descriptive Statistics of Sample Firms by Industry

Note: CSP = corporate social performance; Min = minimum; Max = maximum.

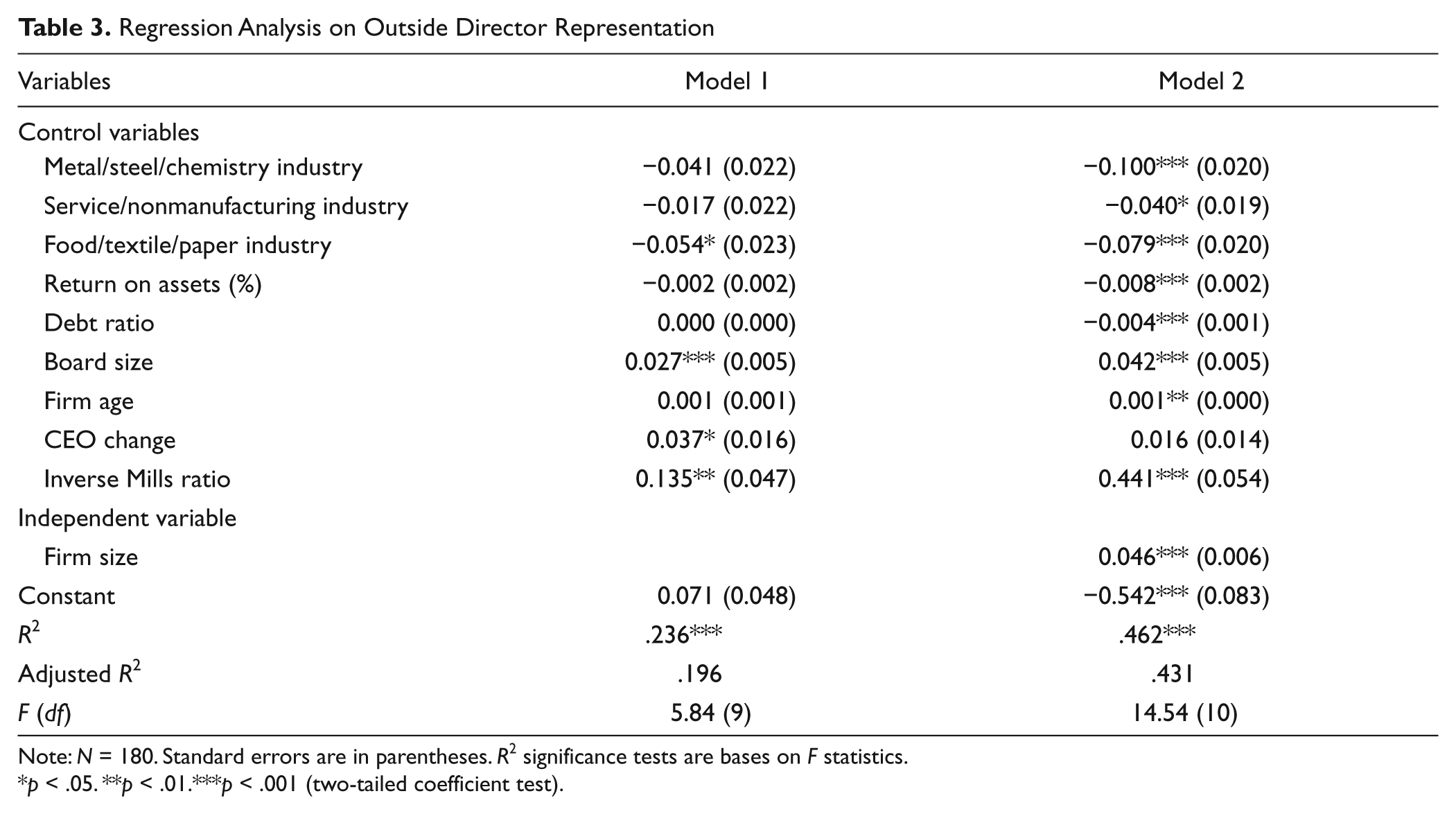

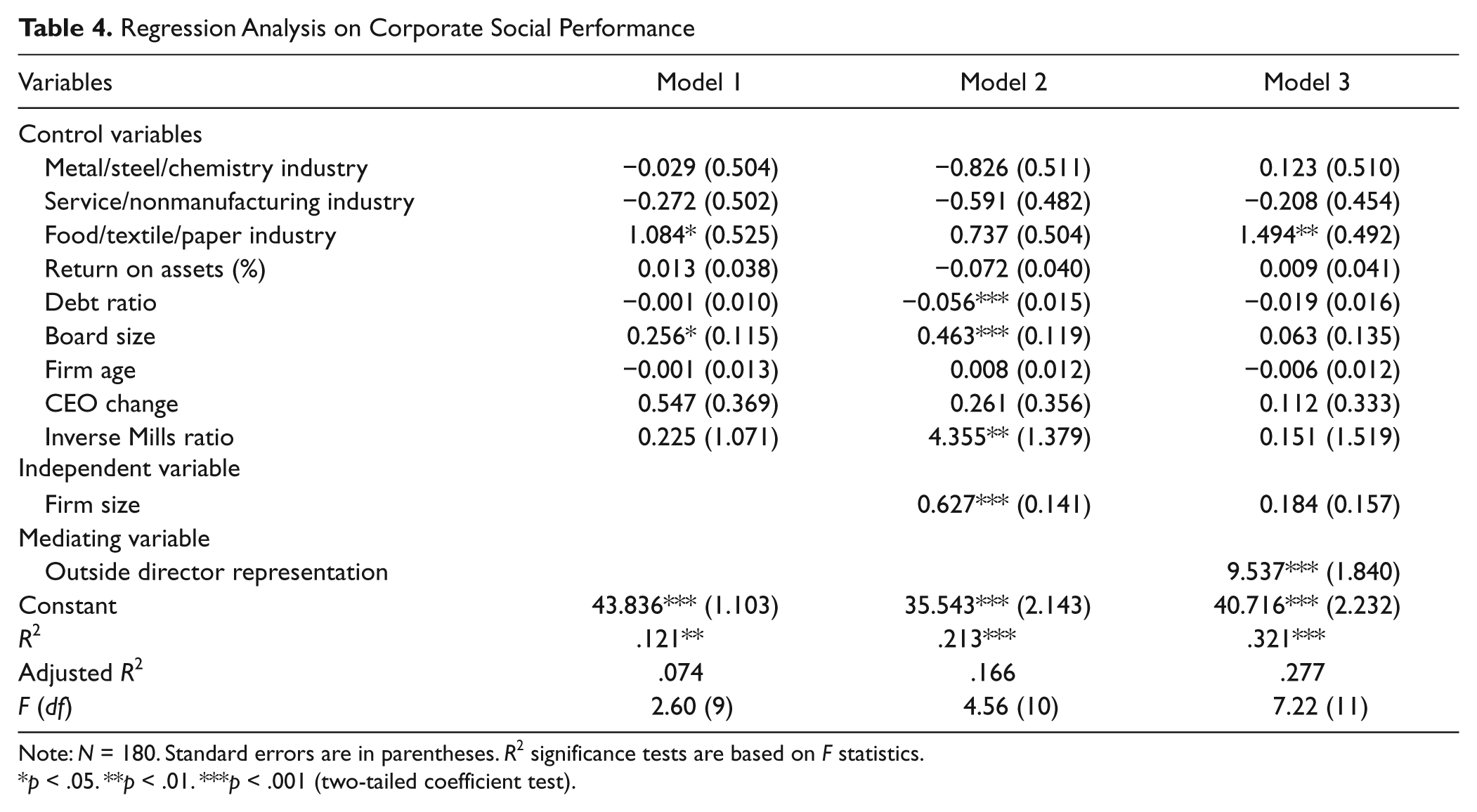

We tested the hypotheses OLS regression models. The results are reported in Tables 3 and 4. In Table 3, we included only control variables in Model 1. Model 2 tested the effect of firm size on outside director representation (independent variable → mediating variable). We found that firm size is positively associated with outside director representation (p < .001). This result indicates that larger firms are more likely to appoint more outside directors than smaller firms. In Table 4, we tested the mediating effect of outside direction representation. We first included the control variables in Model 1. Model 2 tested the main effect of firm size on CSP. The result shows that firm size is positively associated with CSP (p < .001), indicating that larger firms are more likely to actively engage in CSP. Finally, to test for the mediating effect of outside director representation in the relationship between firm size and CSP, we added outside director representation to Model 3, as Baron and Kenny (1986) suggested. The results of Model 3 demonstrate that outside director representation is positively associated with CSP (p < .001), while the significance of firm size effect became nonsignificant. Thus, this finding indicates that outside director representation fully mediates the relationship between firm size and CSP.

Regression Analysis on Outside Director Representation

Note: N = 180. Standard errors are in parentheses. R2 significance tests are bases on F statistics.

p < .05. **p < .01.***p < .001 (two-tailed coefficient test).

Regression Analysis on Corporate Social Performance

Note: N = 180. Standard errors are in parentheses. R2 significance tests are based on F statistics.

p < .05. **p < .01. ***p < .001 (two-tailed coefficient test).

For methodological rigor, we conducted two additional conservative tests to confirm the mediating effect of outside director representation. First, we executed the Sobel–Goodman test. According to Preacher and Hayes (2004), “the Sobel-Goodman test describes a procedure that more directly tests an indirect effect [mediation]” (p. 718). It detects a mediation effect by assessing the indirect effect of a predictor on a dependent variable via a mediator. The results of Sobel (z = 4.415, p < .01), Goodman I (z =4.392, p < .01), and Goodman II (z =4.438, p < .01) tests indicate that outside director representation significantly mediates the relationship between firm size and CSP.

Second, given the relatively small sample size (N = 180), we conducted the bootstrapping method, which is a resampling approach taking the sample as the population and the estimates of the sample as true values. The result of bootstrapping test confirmed the meditating effect of outside director representation, with a 95% bias-corrected confidence interval (CI) of 0.250 to 0.724. We found that effect size was 0.184 for the direct effect and 0.442 for the indirect effect; the proportion of the mediating effect over total effect was around 70.6%. To summarize, we found strong evidence that firm size is positively related to CSP; and outside director representation mediates the relationship. Thus, the results confirm our argument that the relationship between firm size and CSP is better understood when outside director representation, as an internal response mechanism in firms, is incorporated into the relationship.

Discussion

This study posits that larger firms tend to receive strong institutional pressures for CSP. As one of the possible reactions that lead to higher CSP, firms can strategically reconfigure their board of directors (Certo, 2003). As part of the reconfiguration, firms are likely to appoint more outside directors, and, in turn, the increased outside directors develop or support stakeholder-oriented strategic activities, such as CSP initiatives (Wang & Dewhirst, 1992). Accordingly, this article proposes that outside director representation would serve as a mediator in the relationship between firm size and CSP. We found strong empirical support for this argument. Our findings can complement the growing literature on firm size and CSP in several aspects.

First, this study puts forward the crucial role of firms’ strategic response to institutional pressures for CSP. The CSP literature relying on the institution–legitimacy approach has overlooked firms’ strategic response mechanisms for the institutional demands and pressures. However, guided by the suggestion that firms should strategically interpret, internalize, and respond to external pressures (Oliver, 1991), this study empirically confirmed that larger firms formulate a strategic response mechanism by increasing the proportion of outside directors. Thus, our findings complement the conventional institutional theory by underscoring organizational strategic responses to institutional pressures (Zhou & Delios, 2010).

To this end, we empirically examined whether outside director representation is an actual underlying mechanism through which larger firms closely engage in social contributions. In fact, past research propose the positive relationship between firm size and CSP, postulating different underlying mechanisms, such as firm affordability by slack resources (Udayasankar, 2008) or administrative advantages by the scale of business (Donaldson, 2001; Miles, 1987). Yet empirical evidence was limited. This study empirically investigated the actual underlying mechanism through a valid mediation test.

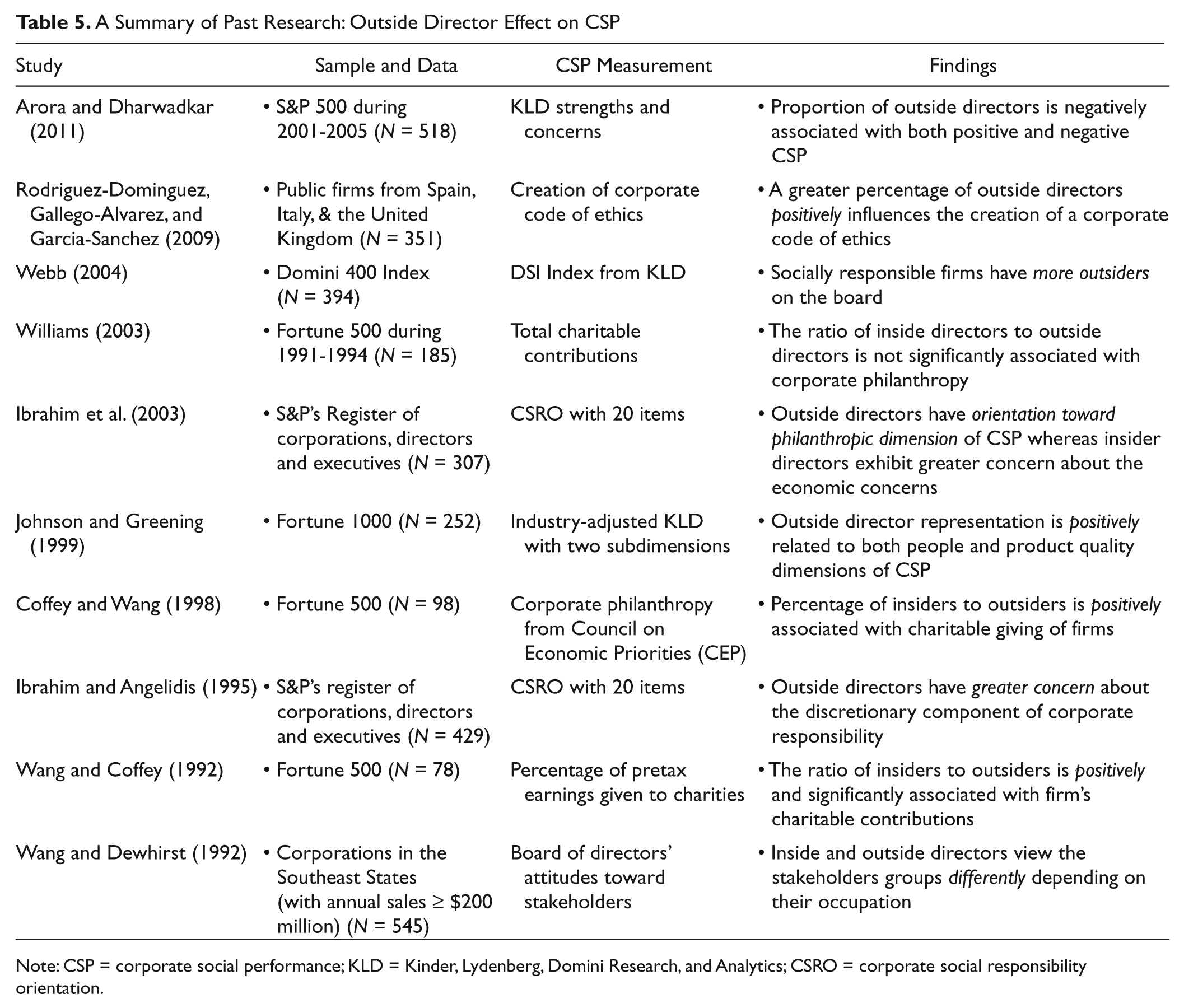

Second, this study confirmed the positive role of outside directors in enhancing CSP. As summarized in Table 5, our literature review indicates that the vast majority of previous studies found the “positive” relationship between the outside director representation and CSP (for exceptions, see Arora & Dharwadkar, 2011; Williams, 2003). Given the relatively minor inconsistency, which could be caused by different measurements, sample, and/or research design, it is reasonable to assume that our finding confirmed the positive effects of outside director representation on CSP.

A Summary of Past Research: Outside Director Effect on CSP

Note: CSP = corporate social performance; KLD = Kinder, Lydenberg, Domini Research, and Analytics; CSRO = corporate social responsibility orientation.

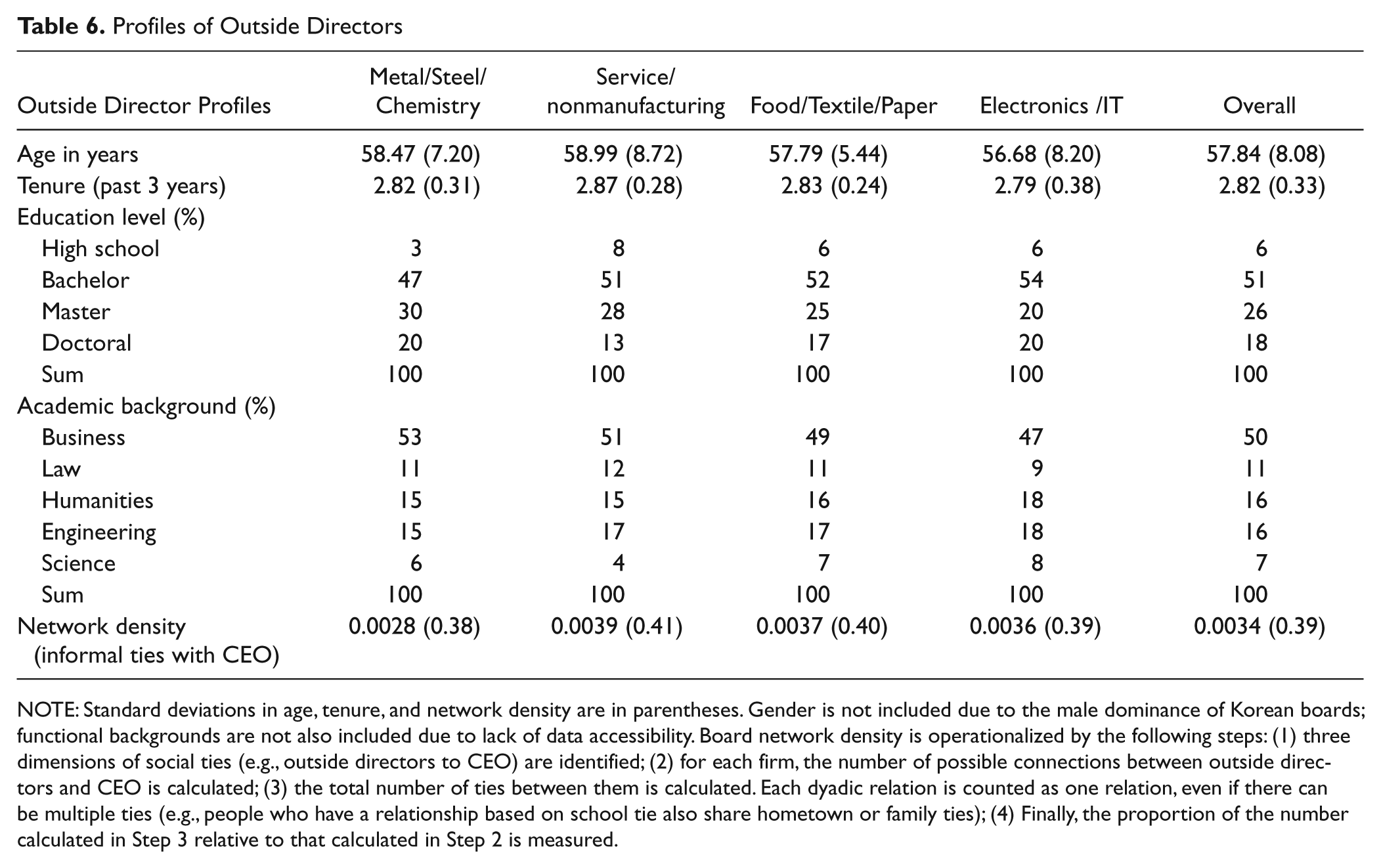

Nonetheless, findings in this study should be interpreted with caution. Since outside directors have divergent backgrounds, status, and demographics that may affect the degree of commitment to CSP (Hillman et al., 2000), it is meaningful to delve into the profiles of outside directors sampled in our specific study. Table 6 illustrates the profiles of outside directors in our study. The average age of outside directors is 57.8 years (8 year of standard deviation) and tenure is 2.82 years (0.33 year of standard deviation) during past 3 years of appointment time period. As expected, firms in electronic and IT industries have relatively younger outside directors with frequent turnovers than those in other industry clusters, presumably because firms in these industries should be responsive to fast-changing environments.

Profiles of Outside Directors

NOTE: Standard deviations in age, tenure, and network density are in parentheses. Gender is not included due to the male dominance of Korean boards; functional backgrounds are not also included due to lack of data accessibility. Board network density is operationalized by the following steps: (1) three dimensions of social ties (e.g., outside directors to CEO) are identified; (2) for each firm, the number of possible connections between outside directors and CEO is calculated; (3) the total number of ties between them is calculated. Each dyadic relation is counted as one relation, even if there can be multiple ties (e.g., people who have a relationship based on school tie also share hometown or family ties); (4) Finally, the proportion of the number calculated in Step 3 relative to that calculated in Step 2 is measured.

Regarding educational backgrounds, roughly half of outside directors (44%) hold graduate-level degrees with diverse academic backgrounds. Previous studies indicated that education levels may contribute to developing moral reasoning that should be responsible for an individual’s moral/prosocial attitudes (Kohlberg, 1984; Rest, 1986). If we follow this logic, outside directors sampled in this study can be seen as having high levels of prosocial orientation that positively influences CSP activities. Diverse academic backgrounds also indicate that outside directors sampled in this study seem to be supportive of CSP, since their different backgrounds enable them to be efficacious in suggesting innovative ideas or solutions for high-quality CSP initiatives. Experts on diversity argue that, since diversity can reduce the redundancy of knowledge being shared, the outcomes of knowledge creation and transfer should be more productive (Cohen & Levinthal, 1990; Cox & Blake, 1991; Tjosvold, 1988). For example, Cohen and Levinthal (1990) suggest that the team problem-solving abilities are likely to increase with the variety in knowledge structures reflected in diverse educational majors. Tjosvold (1988) reported that open discussions through diverse views in marketing teams were associated with completing tasks, using resources more effectively, and delivering better services to customers.

Most important, outside directors in this study have little social connections with top managers. We calculated network density by comparing the total number of social ties with the potential number that would occur if everyone in the network were connected to everyone else (Marsden, 1990). Typical types of social ties in Korea are family ties, school ties, and regional ties (Lee, 1994). As presented in Table 6, the average network density in our sample is virtually zero, which implies that outside directors are able to monitor top manager’s self-serving behaviors effectively. It has been frequently proposed that boards are less effective to monitor managers when they lack social independence from executives (Carpenter & Westphal, 2001). A number of studies have suggested that outside directors exert less control over a firm’s strategic decisions when they share close social ties with top managers (Fredrickson, Hambrick, & Baumrin, 1988; Walsh & Seward, 1990). In regard to CSP, if outside directors are socially tied to top managers, they may feel obligated to support a manager’s decisions without objective questioning; in turn, these informal ties may mitigate a board’s vigilant monitoring function in protecting a firm’s long-term interests and end up being less supportive of social investment. Taken together, outside directors in this study can be seen as having a strong orientation to social responsibility, which confirmed the positive role of outside directors in enhancing CSP.

Last, this study examines the relationship between outside director representation and CSP in one of emerging countries, Korea. Previous studies on the role of outside director in social performances were conducted mostly in the Western context (e.g., Ibrahim & Angelidis, 1995; Ibrahim et al., 2003; Johnson & Greening, 1999). In doing so, past studies have unconsciously assumed existence of “developed” corporate governance system in their theory development and empirical tests. Findings of this study inform that the role of outside directors in CSP is also crucial in the “developing” corporate governance context.

In fact, there have been reservations on the role of outside directors in emerging economies because firms often involuntarily adopt the outside directorate system only to avoid subsequent legal or financial sanctions. In fact, some scholars view outside directors in Korea, especially those who were appointed during the institutional transition following the Asian Financial Crisis, as an indicator of “coercive isomorphism” driven by institutional pressures (Chizema & Kim, 2010; Kim, 2007). They argue that large Korean firms have appointed a minimal (or just socially acceptable) scale of outside directors, so that such a passive reaction might not be translated to serious commitment to CSP. Nonetheless, this study found evidence that outside directors play a significant role in board decisions for CSP even in an emerging country environment.

Furthermore, starting from 2000, large Korean firms (defined as firms whose asset size is greater than 1.7 billion dollars) have been encouraged to nominate 25% of outside directors in board rooms or at least three outside directors. Therefore, the proportion of outside directors beyond the “recommendation” level (>25%) may be an indication that firms recruit, invite, and nominate outside directors proactively rather than passively. In this case, outside directors should be able to play a significant role in crafting social performance goals. As Table 1 shows, the average proportion of outside director in our sample (33%) is clearly beyond the required level. Thus, this evidence suggests that whether outside directors can play a significant role in board decisions for CSP does not necessarily depend on the country per se, but rather on whether outside directors are sufficiently represented or not.

Despite the contributions, this study is not without limitations. First, although we analyzed the attributes of outside directors in Table 6, our study used a traditional method of classifying directors (i.e. insiders vs. outsiders). However, as prior studies (e.g., Hillman et al., 2000) noted, the common insider and outsider definitions may not be always valid in understanding the roles of directors on organizational outcomes. Second, our study may have limited generalizability. Considering our exclusive focus on Korean firms, it would be meaningful to investigate generalizability of our findings in other country contexts, where corporate governance systems and practices are still developing. East Asian and Latin American countries would be the potential target countries (Ayra & Zhang, 2009; Muller & Kolk, 2010; Visser, 2008). Third, this study depends on cross-sectional data. Therefore, future research employing more sophisticated longitudinal research designs and analytic methods can explore dynamics of relationships and avoid causal ambiguities. Last, we proposed only one of the possible paths between firm size and CSP, focusing on the board characteristics. Future research may benefit from examining other mechanisms (e.g., managers’ attention toward CSP and changes in ownership structure) in the firm size–CSP relationship. Such extensions will shed additional light on how firm size has an impact on the organization’s social performance.

Conclusion

This study suggests that the relationship between firm size and CSP is mediated by outside director representation. It provides meaningful implications for the organizations and institutions. From an organizational perspective, our finding emphasizes the importance of corporate governance in CSP as one of possible response mechanisms. In order to promote social performance, firms can consider reconfiguring an appropriate governance structure, such as inviting more outside directors to the board. From an institutional perspective, our findings suggest that outside director representation is a more proximal cause of CSP than firm size. Accordingly, to elicit firms’ strong engagements in socially responsible activities, stakeholders can direct their attention to firms’ corporate governance structure, especially outside director representation. Rather than simply putting pressures on large firms for CSP, stakeholders should add influence on firms’ governance system. One potential direction might be raising the proportion of outside director beyond the level required legally or institutionally.

Footnotes

Appendix

Sample Selection Probit Modelsa

| Coefficient | Standard Error | |

|---|---|---|

| Intercept | −1.453 | 0.771 |

| Food/textile/papers industry | −0.451 | 0.257 |

| Metal/steel/chemistry industry | −0.532* | 0.251 |

| Service/nonmanufacturing industry | −0.309 | 0.270 |

| Return on assets (%) | −0.027 | 0.017 |

| Debt ratio | −0.019*** | 0.003 |

| Board size | 0.239*** | 0.048 |

| Firm age | 0.006 | 0.007 |

| Outside director representation | −1.797 | 1.010 |

| Firm size | 0.177** | 0.066 |

| −2 log likelihood | 134.95 | |

| Pseudo R2 | .322*** | |

| N | 297 | |

Note: Dependent variable: Whether the firm was on the Korea Economic Justice Institute top-200 list (1) or not (0).

p< .05. **p< .01. ***p< .001 (two-tailed coefficient tests).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.